2013 Fourth Quarter Treasury Bulletin-1

44

TREASUR Octo Ministry of Fin RY QUARTERLY BULLETIN: ober - December 2013 nance & Economic Developme ent

-

Upload

kristi-duran -

Category

Documents

-

view

214 -

download

0

Transcript of 2013 Fourth Quarter Treasury Bulletin-1

TREASURY QUARTERLY

October

Ministry of Finance

TREASURY QUARTERLY BULLETIN:

ober - December 2013

Ministry of Finance & Economic Development

& Economic Development

1

Table of Contents

INTRODUCTION .................................................................................................................................................. 3

REAL SECTOR ...................................................................................................................................................... 4

Agriculture ..................................................................................................................................................... 4

Progress on the Basic Input Package Scheme ............................................................................................ 5

The 2014 Tobacco Marketing Season ........................................................................................................ 6

Cotton Production 2013/2014 Season ...................................................................................................... 6

Quarterly Milk Production ......................................................................................................................... 7

Grain Deliveries .......................................................................................................................................... 8

Agriculture Commodity Prices ................................................................................................................... 9

Mining .......................................................................................................................................................... 11

Gold Production ....................................................................................................................................... 13

Nickel ....................................................................................................................................................... 14

Platinum ................................................................................................................................................... 14

Chrome .................................................................................................................................................... 15

International Mineral Prices .................................................................................................................... 15

Value Addition and Beneficiation ............................................................................................................ 15

Manufacturing ............................................................................................................................................. 16

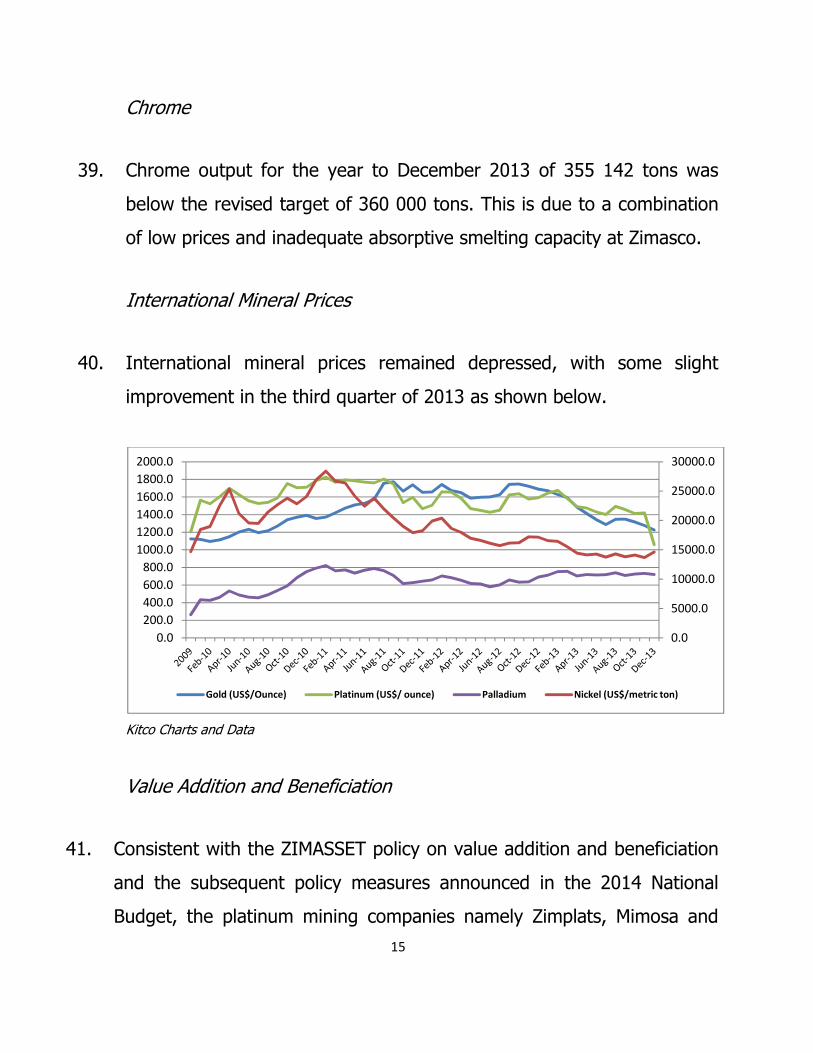

Electricity ..................................................................................................................................................... 18

PRICES .............................................................................................................................................................. 19

BUDGET PERFORMANCE .................................................................................................................................. 20

Revenue Performance ................................................................................................................................. 20

Performance of Revenue Heads .................................................................................................................. 22

Expenditures ................................................................................................................................................ 26

2

Recurrent Expenditure ............................................................................................................................. 26

Capital Expenditure .................................................................................................................................. 27

Financing .................................................................................................................................................. 28

FINANCIAL SECTOR .......................................................................................................................................... 29

Money Supply .............................................................................................................................................. 29

Domestic Credit ....................................................................................................................................... 31

Zimbabwe Stock Exchange........................................................................................................................... 32

EXTERNAL SECTOR ........................................................................................................................................... 34

Exports ......................................................................................................................................................... 34

Imports ......................................................................................................................................................... 35

Trade Gap ..................................................................................................................................................... 37

CONCLUSION .................................................................................................................................................... 37

STATISTICAL TABLES ......................................................................................................................................... 38

3

INTRODUCTION

1. The Fourth Quarter Treasury Bulletin provides an update on fiscal and

economic developments for the period October - December 2013 as

well as an overview of economic performance for 2013.

2. The last quarter of the year also coincided with the introduction of

Government’s Economic Blue Print, “Zimbabwe Agenda for Sustainable

Socio Economic Transformation (ZIM-ASSET) 2013 – 2018”.

3. ZIM-ASSET focuses on five priority areas namely;

• Food Security and Nutrition

• Social Services and Poverty Eradication;

• Infrastructure and Utilities;

• Value Addition & Beneficiation; and

• Fiscal Reforms

4. The fourth quarter also saw the announcement of the 2014 National

Budget to Parliament on the 19th of December 2013. The formulation of

the budget was guided by the ZIMASSET policy document.

5. Consequently, key parameters for the 2014 budget are indicated below:

4

2014 Projections

National Accounts (Real Sector)

Real GDP at market prices ( million US$) 12 337

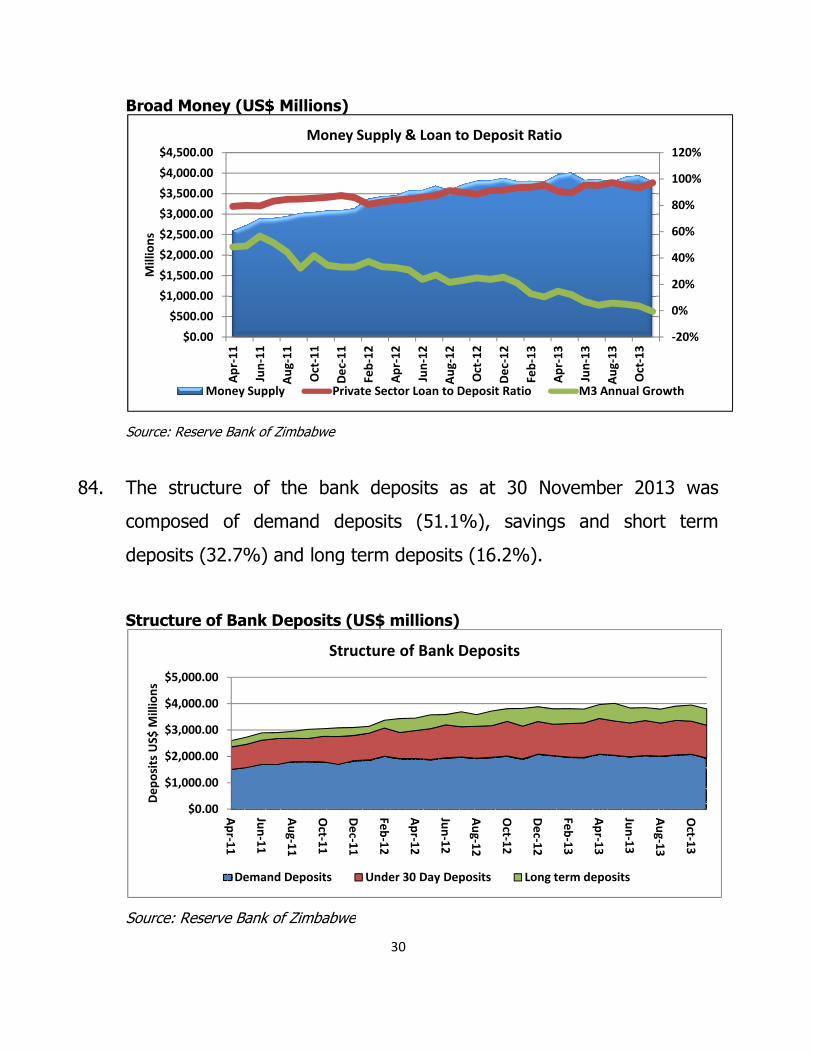

Nominal GDP at market prices (million us$) 14 065

Real GDP Growth (%) 6.1

Inflation (annual average) % 1.5

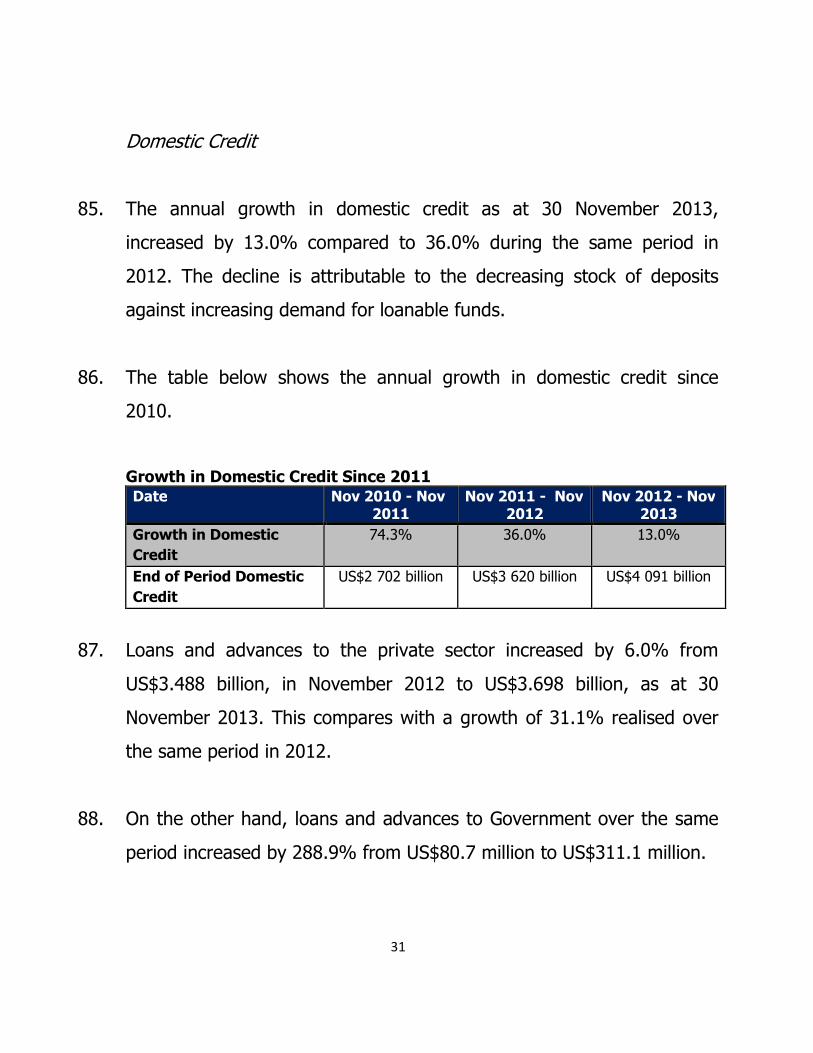

Government Accounts

Revenues & Grants (Millions US$) 4 120

% of GDP 29.3

Expenditures & Net Lending (million US$) 4 120

% of GDP 29.3

Balance of Payments Accounts

Exports (million US$) 5 024

Imports (million US$) 8 321

Current Account Balance (million US$) -2 471

Source: Ministry of Finance and Economic Development

REAL SECTOR

Agriculture

6. The 2013/14 agricultural summer cropping season experienced a late

start to the season, with rains received from late November.

7. However, the quality of the season has since improved significantly

following incessant rains received throughout the country. The wet

spell is expected to continue into the first quarter of 2014.

5

Progress on the Basic Input Package Scheme

8. In support of the 2013/14 agriculture season, Government provided

support to farmers under the Basic Input Package Scheme valued at

US$161 million.

9. Distribution under the Input Pack Scheme as at 31 December 2013

stood as follows:

• 16 548 tons of maize seed and small grains valued at US$39.4

million;

• 36 923 tons of compound D fertilizer valued at US$22.89 million;

• 24 353 tons of ammonium nitrate fertilizer valued at US$17.05

million; and

• 5 765 tons of lime valued at US$795 862.

Distribution of Inputs Contracted Deliveries by Suppliers Balance Based on

as at 31 December 2013 Contracted Tonnage

Company Quantity Value Quantity Value Quantity Value

(tons) (US$) (tons) (US$) (tons) (US$)

Maize seed 16,285 39,084,000 16181 38,744,688 104 339,312

Small Grains 665 1,000,000 367 676,325 298 323,675

Subtotal 16,950 40,084,000 16,548 39,421,013 402 662,987

Compound D 81,000 50,220,000 36,923 22,892,415 44,077 27,327,585

Ammonium Nitrate 80,000 56,000,000 24,353 17,046,925 55,647 44,327,605

LIME 30,000 4,150,000 5,765 795,862 24,235 3,354,138

Sub total 191,000 110,370,000 67,041 40,735,202 123,959 75,009,328

Grand total 150,454,000 80,156,215 75,672,315

Source: Ministry of Agriculture, Mechanisation & Irrigation Development

6

The 2014 Tobacco Marketing Season

10. The Tobacco Auction Floors are expected to be opened on 19 February

2014, with three auction floors, namely, Tobacco Sales Floor (TSF),

Boka Auction floors, and Premier Tobacco Floor having applied to

participate in the marketing of the crop.

11. Furthermore, TIMB advised that other companies have applied to

operate auction floors under a decentralised framework targeting Karoi,

Rusape, Mvurwi, Marondera and Mutare.

12. A total of 171 million kgs of tobacco expected to be delivered during

the 2014 marketing season. This will represent a 2.6% increase from

the 2013 deliveries of 166 million kgs.

13. According to Tobacco Industry Marketing Board (TIMB), 91 278 farmers

registered to grow flue-cured tobacco in the 2013/14 summer cropping

season, 28.7% up from the 70 904 registered in the 2012/13 season.

Cotton Production 2013/2014 Season

14. Registration of cotton growers closed on the 15th of December 2013.

The total number of growers is estimated at 171,303 farmers and an

estimated total area of 310 429 hectares.

7

15. The 1st tranche of inputs comprising of basal fertilizer compound L,

cotton seeds and chemicals have already been distributed to farmers

under contract farming arrangements.

16. There are 12 contractors in the 2013/2014 cotton production season,

namely; Cottco, China Africa, Cargill, SinoZim, Romsdal, Sinotex,

Grafax, Olam, Parrogate, Insing and Jinmac.

Quarterly Milk Production

17. Milk production for the period October to December 2013 stood at 14.2

million litres, 4.2% lower than the 14.8 million litres realised during the

same period in 2012. About 54.7 million litres of milk was produced in

2013, which is marginaly lower than 55.9 million litres produced in

2012 as indicated in the Table below.

Milk Production in litres

2010 2011 2012 2013

QI 10,731,820.0 11,925,314.0 12,809,452.0 13,320,384.0

QII 11,005,382.0 12,269,132.0 13,561,975.0 13,170,235.0

QIII 12,759,226.0 13,117,285.0 14,724,455.0 13,959,069.0

QIV 12,691,665.0 13,291,614.0 14,833,812.0 14,217,407.0

Total 47,188,093.0 50,603,345.0 55,929,694.0 54,667,095.0

Source: Dairy Association of Zimbabwe

8

Grain Deliveries

18. Cumulative deliveries to the Grain Marketing Board (GMB) under the

Strategic Grain Reserve (SGR), stood at 36,592 metric tons as at 31

December 2013.

2013 Grain Deliveries Price/Ton US$378.82 US$466 US$378.82

Commodities Maize Wheat Small Grains

Tons Value (US$) Tons Value (US$) Tons Value (US$)

April

May

June

July 7,312 2,770,042

August 12,897 4,886,256

September 1,818 688,936

October 5,959 2,257,795 1,981 923,180 169 49,855

November 3,145 1,191,602 4,038 1,881,546 16

December

Total 36,592. 13,863, 206 6,019 2,804,726 185.0 49,855

Source: Grain Marketing Board

19. Of this amount, about 9,104 metric tons were delivered during the

three months to December. The low deliveries are attributed to low

harvests due to the erratic rainfall pattern during the 2012/2013

agricultural season, as well as the delays in payments by GMB, forcing

farmers to sell to other dealers and millers.

20. The annual national requirement under the SGR is 500 000 metric tons.

9

Agriculture Commodity Prices

21. International agriculture commodity prices increased by 2.3% in

December. Major notable drivers of the increase relate to soyabean

which jumped from US$476.7 per ton in November to US$488.7 in

December on strong Chinese feed demand.

22. Cotton prices on the other hand increased to 87.5 cents per pound in

December from 84.6 cents per pound in November benefiting from

lower than anticipated production in the United States.

23. On the other hand, cereal prices, declined by 3% in 2013, owing to

recovery of production. Maize prices declined to US$197.5 per tons in

December from US$199.1 per ton in November. Wheat prices declined

by 5%, recording US$291.6 per ton in December from US$306.8 in

November.

24. Groundnuts prices fell by 8% to US$2 207.5 per ton in December, from

US$2 392.2 per ton in November, mainly as a result of favorable

harvests.

25. Sugar prices fell by 7% to 16.4 cents per pound in December, from

17.7 cents per pound in November, also on the back of abundant

supply.

10

26. The Table below indicates some selected international agricultural

prices for the period under review.

Selected International Agriculture Commodity Prices

Commodities Annual 2013 Quarterly 2013 Monthly

Units 2011 2012 2013 QI QII QIII QIV Oct Nov Dec

Wheat $/MT 223.7 316.2 313.3 355.7 321.4 313.8 305.9 325.1 306.8 291.6

Maize $/MT 186 291.8 298.4 317.3 305.1 290.9 240.4 201.7 199.1 197.5

Rice $/MT 520.6 551.7 580.2 580.3 570.7 550.7 504 453.3 448.8 447.5

Soybeans $/MT 384.9 484.2 537.8 544.4 532.8 540 516.5 479.4 476.7 488.7

Groundnuts $/MT 1239.4 1724 2318.2 2091.8 2521.0 2347.1 2312.7 2056 2392.2 2207.5

Sugar cts/lb 20.9 26.2 21.4 19.6 18.5 17.3 17.3 17.7 17.7 16.4

Cotton cts/lb 103.5 154.6 89.2 82.1 89.9 92.7 91.8 87.2 84.6 87.5

Source: IMF Commodity Prices

27. On the domestic market, agriculture commodity prices have remained

relatively unchanged for the three months under review. The table

below summarises the prices of some selected domestic commodities:

Selected Domestic Agriculture Commodity Prices

Commodity Price (US$/ton) Buyer

Groundnuts 1100 Breckabury

Soya beans 690 Kurima Gold

Wheat 470 Kurima Gold/National Foods

Maize 379 GMB

Barley 450 Delta

Source: AMA, GMB, Delta

11

Mining

28. Mineral output in 2013 indicates strong performance in respect of gold,

nickel and coal, whose perfomance surpassed the 2013 revised targets.

However, platinum group of metals and chrome output were marginally

below target.

29. Declining international mineral prices were the biggest factor weighing

down on improved mineral production, as most mineral prices were on

a downward trend since the beginning of the year.

30. Below is a summary of individual mineral outputs in 2013.

12

Monthly Mineral Production — January-December 2013 MINERAL Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec

2013 Total

Volume projection

Gold \kg 1,088.44 1,066.38 1,111.39 1,168.23 1,238.28 1,146.59 1,292.60 1,203.02 1,153.50 1,281.59 1,155.76 1,151.00 14,056.78 14,000.00

Nickel \t 739.37 882.88 775.1 947.54 1,238.28 1,145.67 1,238.29 1,127.31 1,816.51 1,572.47 1,494.29 1,235.00 14,057.86 12,000.00

Chrome \t 9,223.00 11,142.00 11,609.00 10,520.00 21,654.00 27,925.00 27,336.00 43,096.00 55,850.00 48,170.00 45,760.00 42,857.00 355,142.00 360,000.00

Platinum\kg 1,007.59 1,219.61 1,069.03 976.45 1,093.55 1,233.25 1,064.54 1,062.10 1,112.49 994.75 1,131.26 1,001.00 12,965.62 13,000.00

Palladium \kg 767.75 422.63 802.01 736.91 853.95 975.22 832.55 823.73 851.8 775.99 907.95 892 9,642.49 9,800.00

Coal 349044.14 328346.3 392655.9 328591.67 330150.35 491094.37 415913.69 418493.81 403038.44 359649.5 359649.5 359649.5 4536277 3300000

Source: Chamber of Mines and Fidelity Printers

13

2013 Quarterly Mineral Production QI QII QIII QIV Total Projection

Gold \kg

3,266.22 3,553.13 3,649.12 3,588.35 14,056.82 14000

Nickel \t

2397.35 3,177.01 4,182.11 4,301.76 14,057.86 12000

Coal \t

1,070,046.34 1,149,836.39 1,237,445.94 1,078,948.50 4,536,277.17 3 300

Chrome \t

31,974.00 60,099.00 126,282.00 136,787.00 355,142.00 360 000

Platinum \kg

3,296.23 3,303.25 3,239.13 3,127.01 12,965.62 13000

Palladium \kg

1,992.39 2,566.08 2,508.08 2,575.94 9,642.49 9800

Source: Chamber of Mines

Gold Production

31. Cumulative gold production for the year to December 2013 was 14

056.82 kgs against a revised target of 14 000 kgs. However, output for

the fourth quarter of 2013 declined to 3 588.35 kgs compared to 3

649.12 kgs produced in the third quarter of the same year.

32. The decline in the performance of gold, especially in the fourth quarter,

is partly explained by the continued deceleration of international gold

prices from the peak of US$1 670.95 in January to US$1272.47 in the

last quarter of 2013.

33. In addition, Mwana Africa, one of the biggest gold producers,

temporarly shut down its operations in December 2013 to undertake

some modifications at one of its mills. While this affected gold output,

the move is expected to boost gold throughput in 2014.

14

34. Furthermore, the introduction of a lower rate of royalty at 3% from 7%

for small scale miners will have a positive impact on guaranteeing

improved sales to the formal system and hence, reduce leakages.

Nickel

35. Cumulative nickel output for the year to December 2013 amounted to

14 057.86 tons against the revised target of 12 000 tons. The improved

performance is on account of successful recapitalisation of BNC which

facilitated enhanced production during the second half of the year.

36. Subsequently, output in the fourth quarter increased to 4 301.76 tons

from 4 182.11 tons produced in the previous quarter.

Platinum

37. Annual platinum output for 2013 at 12 965.62 kgs slightly failed to

meet the set target of 13 000 kgs by 34kgs, due to declining platinum

prices on the international market.

38. The underperformance of platinum also implies subdued pereformance

in the related platinum group of metals such as palladium, rhodium,

lithium, iridium and rhuthenium.

15

Chrome

39. Chrome output for the year to December 2013 of 355 142 tons was

below the revised target of 360 000 tons. This is due to a combination

of low prices and inadequate absorptive smelting capacity at Zimasco.

International Mineral Prices

40. International mineral prices remained depressed, with some slight

improvement in the third quarter of 2013 as shown below.

Kitco Charts and Data

Value Addition and Beneficiation

41. Consistent with the ZIMASSET policy on value addition and beneficiation

and the subsequent policy measures announced in the 2014 National

Budget, the platinum mining companies namely Zimplats, Mimosa and

0.0

5000.0

10000.0

15000.0

20000.0

25000.0

30000.0

0.0

200.0

400.0

600.0

800.0

1000.0

1200.0

1400.0

1600.0

1800.0

2000.0

Gold (US$/Ounce) Platinum (US$/ ounce) Palladium Nickel (US$/metric ton)

16

Unki have already submitted plans to set up a platinum refinery plant in

the country.

Manufacturing

42. In 2013, the manufacturing sector faced a number of challenges,

resulting in average capacity utilisation declining to 39.6%, compared

to 44.9% recorded in 2012.

43. According to the Confederation of Zimbabwe Industries (CZI)

Manufacturing Survey of August 2013, the obtaining capacity utilisation

across sub sectors are indicated below.

Manufacturing sector Average Capacity Utilisation (%) in 2012

Average Capacity Utilisation (%) in 2013

Bakers 40.0 82.5

Battery 76.5 71.5

Building (construction and related)

59.5 44.1

Car Assemblers 30.3 13.1

Electric Appliances Manufacturers

43.8 37.5

Engineering Iron and Steel 36.7 27.7

Food, Dairy and Beverages 58.2 42.0

Grain Millers 30.0 50.0

Chemical 41.6 30.0

Leather and Allied 27.5 11.3

Pharmaceuticals 58.0 20.0

Plastic, Packaging and Rubber 46.1 38.0

Paper, Printing and Publishing 58.3 55.0

Textiles and Clothing 34.4 35.3

Timber Processors 53.8 58.0

Source: CZI

44. The low capacity utilisation levels have been mirrored by company

closures and/or scaling down of operations. The most affected

17

subsectors included textiles and ginning, clothing and footwear, paper,

printing and publishing, chemicals and petroleum products as well as

pharmaceuticals.

45. Most company closures have been recorded in Bulawayo and Mutare,

resulting in de-industrialisation and job losses.

46. The major factor behind company closures is the difficult operating

environment, partly emanating from the influx of cheap imports,

thereby negatively affecting the competitiveness of the local industry.

47. The 2014 National Budget, therefore, proposed a number of measures

aimed at levelling the playing field through some tariff adjustments on

a number of domestically manufactured products. These include,

among others:

• Steel and Plastic;

• Dairy Products;

• Biscuit;

• Paint;

• Metal and Electrical;

• Rubber Industries; and

• Oil Expressers.

48. These supportive measures should augment the recovery of the

manufacturing sector, which is estimated to grow by 3.2% in 2014.

Electricity

49. The electricity generation capacity deteriorated significantly during the

last quarter of the year. After reaching a peak of over 1200 MW/h in

July and August, electricity generation declined to below 1000 MW/h

during the months of October and November. Th

intermittent breakdowns at Hwange and Kariba

thermal power stations

50. However, power generation

2012, as generating plants managed to run consistently in the first ten

months of the year as indicated in the table below.

Source: Ministry of Energy and Power Development

0

200

400

600

800

1000

1200

1400

Jan Feb

MW/h

Monthly Electricity Generation Capacities: 2012 VS 2013

18

The electricity generation capacity deteriorated significantly during the

last quarter of the year. After reaching a peak of over 1200 MW/h in

July and August, electricity generation declined to below 1000 MW/h

the months of October and November. This

intermittent breakdowns at Hwange and Kariba, as well as other small

thermal power stations.

However, power generation in 2013 was slightly higher

generating plants managed to run consistently in the first ten

months of the year as indicated in the table below.

Source: Ministry of Energy and Power Development

Feb Mar Apr May Jun Jul Aug Sep

Monthly Electricity Generation Capacities: 2012 VS 2013

2012 2013

The electricity generation capacity deteriorated significantly during the

last quarter of the year. After reaching a peak of over 1200 MW/h in

July and August, electricity generation declined to below 1000 MW/h

is was due to

as well as other small

higher compared to

generating plants managed to run consistently in the first ten

Oct Nov

Monthly Electricity Generation Capacities: 2012 VS 2013

19

51. In 2014, electricity sector is expected to grow by 4.5%, benefiting from

the on-going rehabilitation works at Hwange and small thermal power

stations.

PRICES

52. The general price level in the economy has been on a downward trend,

with year on year inflation opening the year at 2.5% and declining to

0.33% in December 2013.

Source: ZIMSTAT, Reserve Bank of South Africa

53. Annual inflation in October, recorded 0.59%, slightly dropping to 0.54%

in November, and 0.33% in December.

8.0

8.5

9.0

9.5

10.0

10.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov DecR

an

d/U

S$

%

2013 Inflation & Rand/US$ exchange rate Profile

Rand/US$ exchange rate Month on Month inflation Year on Year inflation

20

54. On a monthly basis, deflation of -0.01% and -0.1% were recorded for

the month of October and December, respectively. In November,

overall prices gained 0.20% to record a monthly inflation of 0.09%.

55. This deceleration reflects weak aggregate demand induced by tight

liquidity, low disposable incomes, steady international oil and food

prices as well as stable inflation expectations.

56. Furthermore, given that 70% of our imports are from South Africa, the

depreciation of the rand against the United States dollar was also a

contributing factor.

BUDGET PERFORMANCE

Revenue Performance

57. Total revenue collections during the fiscal year 2013, amounted to

US$3.74 billion against a target of US$3.86 billion, resulting in a

negative variance of US$118.96 million.

58. Tax revenue contributed US$3.41 billion or 91% of total revenue

against a target of US$3.65 billion, giving a negative variance of

US$232.34 million.

59. Benefiting from telecommunication licence fees, non

collections were US$327.0 million

target of US$213.6 million. This gives a positive variance of US$113.10

million.

60. Telecommunication licence fees

61. Revenue performance reflects severe underperformance in the last

quarter of the year, as indicated in the

Source: Ministry of Finance and Economic Development

62. Historically, bulky of the revenues are collected in the last quarter of

the year. However, a complete reversal of this trend was noted

economy experienced liquidity constraint, which worsened during

last quarter of 2013.

Jan Feb

Actuals 254.50 269.47 314.00

Target 273.66 249.82 301.86

US

$M

illi

on

s

21

Benefiting from telecommunication licence fees, non-

US$327.0 million, or 9% of total revenue

rget of US$213.6 million. This gives a positive variance of US$113.10

icence fees alone amounted to US$151.5 million.

evenue performance reflects severe underperformance in the last

as indicated in the table below.

Source: Ministry of Finance and Economic Development

Historically, bulky of the revenues are collected in the last quarter of

However, a complete reversal of this trend was noted

economy experienced liquidity constraint, which worsened during

Mar Apr May Jun Jul Aug Sep Oct

314.00 271.04 363.59 354.41 323.03 319.54 353.43 278.15

301.86 282.83 293.2 360.21 292.66 293.6 367.15 328.83

Revenues:Jan-Dec 2013

-tax revenue

or 9% of total revenues, against a

rget of US$213.6 million. This gives a positive variance of US$113.10

US$151.5 million.

evenue performance reflects severe underperformance in the last

Historically, bulky of the revenues are collected in the last quarter of

However, a complete reversal of this trend was noted as the

economy experienced liquidity constraint, which worsened during the

Oct Nov Dec

278.15 259.10 380.89

328.83 351.71 464.48

Performance of Revenue Heads

63. Revenue heads that contributed significantly to total revenue include,

Value added Tax (28%), individuals (20%), Excise Duty (14%),

Corporate Tax (11%) and Customs Duty (10%).

64. Other taxes which include domestic dividends and interests and

royalties among others, contributed 9% to total revenue.

65. The breakdown of revenue performance is indicated in the chart below.

Source: Ministry of Finance and Economic Development

Value Added Tax

(VAT)

28%

Other indirect taxes

2%

2013 Revenue Composition

22

Performance of Revenue Heads

Revenue heads that contributed significantly to total revenue include,

Value added Tax (28%), individuals (20%), Excise Duty (14%),

Corporate Tax (11%) and Customs Duty (10%).

Other taxes which include domestic dividends and interests and

others, contributed 9% to total revenue.

The breakdown of revenue performance is indicated in the chart below.

Source: Ministry of Finance and Economic Development

PAYE

20%

Corporate Tax

11%

Customs duties

10%Excise duties

14%

Non-tax Revenue

9%

2013 Revenue Composition

Revenue heads that contributed significantly to total revenue include,

Value added Tax (28%), individuals (20%), Excise Duty (14%),

Other taxes which include domestic dividends and interests and

The breakdown of revenue performance is indicated in the chart below.

Corporate Tax

11%

Other Profit

and Income

Taxes

6%

66. Although VAT, Corporate tax, customs duty contributed significantly to

tax revenue, they however performed below

below.

Source: Ministry of Finance and Economic Development

67. This underperformance is attributed to general economic slowdown,

with the liquidity situation worsening during the last quarter.

-

200.0

400.0

600.0

800.0

1,000.0

1,200.0

2013 Revenue Performance (Actuals vs Targets)

23

Although VAT, Corporate tax, customs duty contributed significantly to

they however performed below the 2013 targets as shown

Source: Ministry of Finance and Economic Development

This underperformance is attributed to general economic slowdown,

with the liquidity situation worsening during the last quarter.

2013 Revenue Performance (Actuals vs Targets)

Although VAT, Corporate tax, customs duty contributed significantly to

the 2013 targets as shown

This underperformance is attributed to general economic slowdown,

with the liquidity situation worsening during the last quarter.

2013 Revenue Performance (Actuals vs Targets)

Actual

Target

Source: Ministry of Finance and Economic Development

68. Total revenue collections for the last quarter of 2013 amounted to

US$918.14 million, against a quarterly target of US$1.145 billion

a negative variance of about US$226 million.

Summary of Quarterly Revenue Heads Performance for

Revenue and Grants

Revenue

Tax revenue

Personal income tax

Corporate income tax

Other direct taxes

Customs

Excise

Value added Tax

Other indirect taxes

Non Tax revenue

Grants

Source: Ministry of Finance and Economic Development

0.00

200.00

400.00

600.00

800.00

1000.00

1200.00

Q1

Actual 837.97

Target 825.336

US

$ M

illi

on

s

2013 Quarterly Revenue Performance

24

Source: Ministry of Finance and Economic Development

Total revenue collections for the last quarter of 2013 amounted to

against a quarterly target of US$1.145 billion

a negative variance of about US$226 million.

Summary of Quarterly Revenue Heads Performance for (Millions Us$)2012 2013

QI QII QIII QIV QI QII

771.1 825.9 902.3 1027.3 838.0 989.0

771.1 825.9 902.3 1027.3 838.0 989.0

709.6 787.5 825.8 907.6 804.1 842.7

145.3 156.3 163.0 187.9 174.3 174.3

75.2 104.1 117.2 109.4 86.0 99.5

55.3 85.8 75.5 76.3 65.3 68.4

87.9 81.1 89.3 107.3 89.2 90.3

88.9 86.6 101.8 110.9 111.8 130.6

242.7 257.2 270.1 308.1 269.3 255.1

14.3 16.4 8.9 7.9 8.2 24.5

61.5 38.4 76.6 119.8 33.9 146.4

0.0 0.0 0.0 0.0 0.0 0.0

Source: Ministry of Finance and Economic Development

Q1 Q2 Q3 Q4

837.97 989.03 996.00 918.14

825.336 936.243 953.403 1145.02

2013 Quarterly Revenue Performance

Total revenue collections for the last quarter of 2013 amounted to

against a quarterly target of US$1.145 billion, giving

(Millions Us$) 2013

QIII QIV

989.0 996.0 918.14

989.0 996.0 918.14

842.7 891.8 875.47

174.3 211.3 184.47

102.4 116.45

44.4 49.09

91.5 90.28

130.6 129.9 138.16

255.1 284.0 259.68

28.3 37.41

146.4 104.2 42.67

0.0 0

Q4

918.14

1145.02

69. The Table below shows the nominal growth in revenues per quarter

from 2011 to 2013.

Source: Ministry of Finance and Economic Development

70. The ratio of revenue to GDP has been increasing since 2009

there are signs of stagnating between 2012 and 2013

below.

Source: Ministry of Finance and

0

200

400

600

800

1000

Q1

US

$ M

illi

on

s

Quarterly Revenues: 2011

25

The Table below shows the nominal growth in revenues per quarter

Source: Ministry of Finance and Economic Development

The ratio of revenue to GDP has been increasing since 2009

there are signs of stagnating between 2012 and 2013, as indicated

Source: Ministry of Finance and Economic Development

Q2 Q3 Q4

Quarterly Revenues: 2011-2013

The Table below shows the nominal growth in revenues per quarter

The ratio of revenue to GDP has been increasing since 2009, although

, as indicated

2011

2012

2013

Expenditures

71. Cumulative expenditure

billion, against targeted expenditure

expenditures, US$3.52 billion went towards recurrent expenditure,

while capital expenditure

US$396.1 million and US$71.65 million, respectively.

Source: Ministry of Finance and Economic Development

Recurrent Expenditure

72. Of the total, recurrent expenditures took up 88% of total expenditures.

Employment costs alone

48% of the total budget

0.00

50.00

100.00

150.00

200.00

250.00

300.00

350.00

400.00

450.00

500.00

Jan Feb

Revenues 254.5 269.4

Expenditures 225.5 324.5

US

$ M

illi

on

s

2013 Revenues vs Expenditures

26

Cumulative expenditures to December 2013 amounted to

against targeted expenditures of US$3.86 billion. Of these

expenditures, US$3.52 billion went towards recurrent expenditure,

while capital expenditure and net lending absorbed the remaining

US$396.1 million and US$71.65 million, respectively.

Source: Ministry of Finance and Economic Development

Recurrent Expenditure

recurrent expenditures took up 88% of total expenditures.

alone amounted to US$1.9 billion, constituting about

of the total budget and 55% of total recurrent expenditure

Feb Mar Apr May Jun Jul Aug Sep Oct

269.4 314.0 271.0 363.5 354.4 323.0 319.5 353.4 278.1

324.5 322.7 248.2 307.8 310.7 397.7 336.3 302.0 388.7

2013 Revenues vs Expenditures

amounted to US$3.99

of US$3.86 billion. Of these

expenditures, US$3.52 billion went towards recurrent expenditure,

and net lending absorbed the remaining

recurrent expenditures took up 88% of total expenditures.

amounted to US$1.9 billion, constituting about

recurrent expenditures.

Nov Dec

259.1 380.7

317.3 483.0

73. Accordingly, US$1.59 billion was left for other recurrent exp

as goods and services, interest payments and current transfers.

74. The graph below shows

Source: Ministry of Finance and Economic Development

Capital Expenditure

75. A total of US$386.5 million

benefitting mainly key

education, water and sanitation.

Interest on Debt

1%

Current Transfers

28%

Capital Expenditure

10%

27

US$1.59 billion was left for other recurrent exp

as goods and services, interest payments and current transfers.

The graph below shows the structure of expenditures for the year

Source: Ministry of Finance and Economic Development

US$386.5 million was expended on capital projects

key ongoing projects in sectors of transport, health,

water and sanitation.

Employment Costs

48%

Other Goods &

Services

11%

Current Transfers

Capital ExpenditureNet Lending

2%

Expenditures for Jan-Dec 2013

US$1.59 billion was left for other recurrent expenses such

as goods and services, interest payments and current transfers.

of expenditures for the year.

was expended on capital projects,

transport, health,

28

76. Some of the key interventions in water and sanitation included dam

construction, water conveyance infrastructure, rehabilitation and

upgrading of water and sewer infrastructure in urban settlements and

the rural water and sanitation programmes with disbursements

amounting to US$97.9 million, as at 30 November 2013.

77. The Table below shows disbursements for major water and sanitation

projects:-

PROJECT DISBURSEMENTS TO NOVEMBER 2013

Tokwe Murkosi Dam 65,962,300

Mutange Dam 1,088,392

Gwayi-Shangani Dam 9,370,000

Osborne Dam 322,000

Mtshabezi Pipeline 4,200,000

Wenimbi Pipeline 1,617,000

Local Authorities 8,964,300

Water Supplies 3,116,200

Rural Water and Sanitation 3,300,000

Grand Total 97,940,192

Source: Ministry of Finance and Economic Development

Financing

78. Given total expenditures of US$3.99 billion, and total revenues of

US$3.74 billion, a budget overrun of US$246.36 million for the year was

realised.

79. The deficit was financed mainly through the issuance of Treasury Bills.

29

FINANCIAL SECTOR

80. The 2013 fourth quarter was characterised by some turbulence in the

financial sector, with cash shortages being experienced in some

banking institutions.

81. Trust Banking Corporation succumbed to poor asset quality,

mismanagement, under-capitalisation and unsoundness resulting in the

cancellation of their banking licence by the Reserve Bank of Zimbabwe

on 6 December 2013.

Money Supply

82. As at 30 November 2013, total banking sector deposits stood at

US$3.807 billion, representing an annual decrease of -0.46% compared

to an annual growth of 23.8% during the same period in 2012. The

stagnation in money supply is being reflected by the current low annual

inflation level of 0.33% in December 2013.

83. The Chart below shows the growth rate in broad money since 2011 and

the loan to deposit ratio.

Broad Money (US$ Millions)

Source: Reserve Bank of Zimbabwe

84. The structure of the bank deposits

composed of demand deposits (51.1%), savings and short term

deposits (32.7%) and long term deposits (16.2%).

Structure of Bank Deposits (US$ millions)

Source: Reserve Bank of Zimbabwe

$0.00

$500.00

$1,000.00

$1,500.00

$2,000.00

$2,500.00

$3,000.00

$3,500.00

$4,000.00

$4,500.00

Ap

r-1

1

Jun

-11

Au

g-1

1

Mil

lio

ns

Money Supply

$0.00

$1,000.00

$2,000.00

$3,000.00

$4,000.00

$5,000.00

Ap

r-11

Jun

-11

Au

g-1

1

De

po

sits

US

$ M

illi

on

s

Demand Deposits

30

Broad Money (US$ Millions)

: Reserve Bank of Zimbabwe

The structure of the bank deposits as at 30 November 2013 was

composed of demand deposits (51.1%), savings and short term

deposits (32.7%) and long term deposits (16.2%).

Structure of Bank Deposits (US$ millions)

Source: Reserve Bank of Zimbabwe

Oct

-11

De

c-1

1

Feb

-12

Ap

r-1

2

Jun

-12

Au

g-1

2

Oct

-12

De

c-1

2

Feb

-13

Ap

r-1

3

Jun

-13

Au

g-1

3

Money Supply & Loan to Deposit Ratio

Private Sector Loan to Deposit Ratio M3 Annual Growth

Oct-1

1

De

c-11

Feb

-12

Ap

r-12

Jun

-12

Au

g-1

2

Oct-1

2

De

c-12

Feb

-13

Ap

r-13

Structure of Bank Deposits

Demand Deposits Under 30 Day Deposits Long term deposits

November 2013 was

composed of demand deposits (51.1%), savings and short term

-20%

0%

20%

40%

60%

80%

100%

120%

Au

g-1

3

Oct

-13

M3 Annual Growth

Jun

-13

Au

g-1

3

Oct-1

3

Long term deposits

31

Domestic Credit

85. The annual growth in domestic credit as at 30 November 2013,

increased by 13.0% compared to 36.0% during the same period in

2012. The decline is attributable to the decreasing stock of deposits

against increasing demand for loanable funds.

86. The table below shows the annual growth in domestic credit since

2010.

Growth in Domestic Credit Since 2011 Date Nov 2010 - Nov

2011 Nov 2011 - Nov

2012 Nov 2012 - Nov

2013

Growth in Domestic

Credit

74.3% 36.0% 13.0%

End of Period Domestic

Credit

US$2 702 billion US$3 620 billion US$4 091 billion

87. Loans and advances to the private sector increased by 6.0% from

US$3.488 billion, in November 2012 to US$3.698 billion, as at 30

November 2013. This compares with a growth of 31.1% realised over

the same period in 2012.

88. On the other hand, loans and advances to Government over the same

period increased by 288.9% from US$80.7 million to US$311.1 million.

89. The sectoral analysis of banking sector loans and advances showed

that cumulative funding to agricul

manufacturing got the lion’s share at 18%, 17%, 17% and 16%

respectively, as shown in the graph below

Distribution of Loans and Advances

Zimbabwe Stock Exchange

90. The industrial index grew by 32.6% during the year 2013

annual growth of 4.5% in 2012. The index

152.4 points and reached an all

2013, before closing the year

91. The mining index continued with contrary market sentiments

declined by 29.4%, compared to a growth of 51.3% in 2012.

Transport

2%

Distribution

17%

32

The sectoral analysis of banking sector loans and advances showed

that cumulative funding to agriculture, distribution, services and

manufacturing got the lion’s share at 18%, 17%, 17% and 16%

as shown in the graph below:

Distribution of Loans and Advances

Zimbabwe Stock Exchange

The industrial index grew by 32.6% during the year 2013

annual growth of 4.5% in 2012. The index opened the year 2013 at

reached an all-time high of 232.87 points in July

before closing the year at 202.12 points.

The mining index continued with contrary market sentiments

compared to a growth of 51.3% in 2012.

Agriculture

18%Construction

2%

Manufacturing

16%

Mining

7%

Services

17%

Individuals

16%

Transport

Distribution

Others

5%

The sectoral analysis of banking sector loans and advances showed

ture, distribution, services and

manufacturing got the lion’s share at 18%, 17%, 17% and 16%,

The industrial index grew by 32.6% during the year 2013, from an

opened the year 2013 at

time high of 232.87 points in July

The mining index continued with contrary market sentiments, as it

compared to a growth of 51.3% in 2012. The index

Construction

Manufacturing

was 65.12 points at the beginning of the year

45.79 points.

Source: Reserve Bank of Zimbabwe

92. The total market capitalisation

of the year, and grew by 31.3% to US$5.203 billion

2013. This is shown in the graph below.

Zimbabwe Stock Exchange Performance: 2009

Source: Reserve Bank of Zimbabwe

-

2,000

4,000

6,000

8,000

De

c-1

2

Jan

-13

US

$ M

illi

on

s

-

50.00

100.00

150.00

200.00

250.00

Jan-12 Apr-12

Po

ints

33

was 65.12 points at the beginning of the year, and closed the year at

Source: Reserve Bank of Zimbabwe

The total market capitalisation was US$3.963 billion, at the beginning

and grew by 31.3% to US$5.203 billion, as at

. This is shown in the graph below.

Zimbabwe Stock Exchange Performance: 2009 – 2013

Source: Reserve Bank of Zimbabwe

Jan

-13

Feb

-13

Ma

r-1

3

Ap

r-1

3

Ma

y-1

3

Jun

-13

Jul-

13

Au

g-1

3

Se

p-1

3

Oct

-13

Market Capitalisation

Mkt Cap

Jul-12 Oct-12 Jan-13 Apr-13 Jul-13

ZSE Indices

Industrial Index Mining Index

closed the year at

at the beginning

31 December

No

v-1

3

De

c-1

3

Oct-13

34

EXTERNAL SECTOR

Exports

93. Total exports for the period January to December 2013 amounted to

US$3.5 billion, compared to US$3.8 billion, realised during the same

period in 2012. Minerals contributed the bulk of the exports for the

period under review. The major exports destination remains South

Africa.

94. The table below shows monthly exports for the period January to

December 2012 and 2013, respectively.

Exports: 2012 &2013 Comparisons Month 2012 2013

January 258,124,310 279,555,180

February 255,206,355 279,047,033

March 309,946,785 253,927,213

April 227,035,793 209,914,487

May 278,145,876 278,314,632

June 232,719,132 244,883,722

July 338,011,302 287,436,037

August 449,726,798 282,668,224

September 324,018,806 308,664,377

October 479,772,803 363,714,307

November 414,848,477 467,471,012

December 314,872,655 251,838,635

Total 3,882,429,092 3,507,434,859

Source: ZIMSTAT

95. In the month of December,

from US$467.5 million

representing a 46% de

Source: ZIMSTAT: 2013

Imports

96. Cumulatively, imports to

Foodstuffs, motor vehicles and fuel contributed the bulk of the imports.

97. The table below shows monthly

December 2013 and 2013

-

200

400

600

800

1,000

1,200

Q1

35

December, exports decreased to US$251.8 million

US$467.5 million, realised in the month of November

decline.

Cumulatively, imports to December 2013, amounted to US$

Foodstuffs, motor vehicles and fuel contributed the bulk of the imports.

The table below shows monthly imports for the period January to

2013, respectively.

Q2 Q3 Q4

2013 Quarterly Exports (US$M)

US$251.8 million,

of November,

amounted to US$7.7 billion.

Foodstuffs, motor vehicles and fuel contributed the bulk of the imports.

ports for the period January to

Exports

Imports: 2012 &2013 Comparisons Month

January

February

March

April

May

June

July

August

September

October

November

December

Total

Source: ZIMSTAT, 2013

98. In the month of December

from US$594.3 million

a 3% decrease.

Source: ZIMSTAT: 2013

-

500

1,000

1,500

2,000

2,500

Q1

2013 Quarterly Imports (US$M)

36

Comparisons 2012 2013

604,942,503 606,712,339

470,517,060 499,162,650

512,150,918 532,812,989

490,167,867 963,636,659

523,853,496 580,022,084

500,698,805 714,119,959

673,099,276 572,670,193

798,780,788 704,166,464

628,045,550 750,242,892

887,243,186 609,822,386

708,791,048 594,277,521

665,251,758 576,576,958

7,463,542,255 7,704,223,094

December, imports decreased to US$576.6

US$594.3 million, recorded in the previous month. This represents

Q2 Q3 Q4

2013 Quarterly Imports (US$M)

013

606,712,339

499,162,650

532,812,989

963,636,659

580,022,084

714,119,959

572,670,193

704,166,464

750,242,892

609,822,386

594,277,521

576,576,958

7,704,223,094

576.6 million,

recorded in the previous month. This represents

Imports

37

Trade Gap

99. Cumulatively, overall trade gap to December 2013, amounted US$4.2

billion.

100. The trade gap for the month of December worsened to US$324.7

million from US$126.8 million, realised in the month of November 2013.

CONCLUSION

101. The overall economic performance for 2013 was not impressive. Most

economic indicators performed well below their targets. The economic

growth targets for the year were revised downwards, while revenue

collections also were well below targets.

102. However, prospects remain positive in the future, anchored by full

implementation of ZIMASSET and the supportive measures as

contained in the 2014 National Budget.

38

STATISTICAL TABLES

Budget Outturn: Jan – December 2013

ZIMBABWE BUDGET CUMULATIVE DATA: 2013

ACTUALS (US$)

CUM ACTUAL to DEC 2013

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Dec-13

Total Revenue Including Retained Revenue,Transfers & Prepayments

263,322,595.4

277,624,816.2

324,114,157.0

281,118,395.4

373,338,288.5

364,949,954.3

332,838,987.8

329,917,199.1

364,432,332.4 286,915,734.6

266,321,441.0 391,590,668.2 3,856,484,569.8

-

Total Revenue Including Zimra Grant 254,502,364.

7 269,468,315.

4 313,999,640.

0 271,037,925.

9 363,588,165

.8 354,406,650.

6 323,032,992.

5 319,539,891.

2 353,430,354.

3 278,154,664.5 259,103,119.

7 380,777,335.7 3,741,041,420.2

-

Total Government Revenue (Net) 254,502,364.

7 269,468,315.

4 313,999,640.

0 271,037,925.

9 363,588,165

.8 354,406,650.

6 323,032,992.

5 319,539,891.

2 353,430,354.

3 278,154,664.5 259,103,119.

7 380,777,335.7 3,741,041,420.2

-

Tax Revenue 245,291,304.

7 258,828,013.

1 299,951,221.

4 251,986,599.

6 268,800,925

.7 321,893,080.

0 266,941,568.

6 286,147,936.

5 338,740,994.

8 263,013,004.3 247,610,090.

6 364,851,625.5 3,414,056,364.6

-

Tax on Income and profits 92,159,226.3 97,734,752.7 135,598,254.

9 95,260,008.8 97,348,120.

5 149,534,341.

7 92,714,707.9 105,973,358.

5 159,388,135.

7 93,311,598.4 83,596,740.5 173,103,339.2 1,375,722,585.1

Individuals 62,761,331.9 55,575,917.6 55,929,755.2 52,952,796.6 61,401,994.7 59,932,757.0 61,174,231.4 73,900,288.5 76,255,733.8 57,500,694.9 52,069,978.6 74,898,947.2 744,354,427.4

Companies 16,418,982.6 11,747,265.8 57,796,936.4 19,947,795.8 15,461,969.2 64,073,904.4 17,238,897.4 16,161,504.5 68,958,046.7 18,542,353.7 15,058,391.9 82,850,001.6 404,256,049.9

Domestic dividend and interest 3,081,626.0 70,137.8 4,172,065.9 846,586.3 3,170,748.3 4,266,725.4 834,086.6 1,646,346.5 2,807,443.0 1,302,314.4 1,121,750.1 1,560,678.1 24,880,508.3

Tobacco Levy

301,483.9 1,839,560.2 3,182,836.3 2,998,115.1 963,848.6 442,564.4 106,786.3 18,503.6 - 21,544.0

9,875,242.3

Royalties 6,259,119.5 26,001,779.8 10,853,017.3 13,457,817.9 9,828,109.7 14,708,976.8 8,020,432.3 9,584,567.7 7,364,712.8 9,978,943.6 10,276,884.5 8,044,184.4 134,378,546.4

Other income taxes 868,115.5 1,336,827.8 1,901,535.9 1,670,225.1 1,582,106.1 2,557,632.0 1,489,395.9 1,369,342.0 1,058,162.9 2,549,615.2 2,157,252.1 2,117,524.4 20,657,734.8

Vehicle Carbon Tax 2,770,050.7 2,701,340.0 3,105,384.0 3,201,950.8 2,905,077.6 3,030,497.5 3,515,100.1 3,204,522.9 2,925,533.1 3,437,676.7 2,890,939.3 3,632,003.4 37,320,076.1

TAX ON GOODS & SERVICES

-

Customs duties 24,376,463.1 27,200,299.4 37,638,021.8 28,494,165.5 31,386,994.

4 30,390,589.5 32,501,640.3 29,260,598.7 29,755,654.6 29,355,775.2 30,507,829.6 30,413,742.1 361,281,774.2

Oil products - -

-

16,921,092.0 -

16,921,092.0

Other(Prime &Surtax) 24,376,463.1 27,200,299.4 37,638,021.8 28,494,165.5 31,386,994.4 30,390,589.5 32,501,640.3 29,260,598.7 12,834,562.6 29,355,775.2 30,507,829.6 30,413,742.1 344,360,682.2

39

ZIMBABWE BUDGET CUMULATIVE DATA: 2013

ACTUALS (US$)

CUM ACTUAL to DEC 2013

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Dec-13

Excise duties 30,599,735.4 34,752,231.0 46,464,443.7 43,547,125.0 44,355,672.

1 42,730,501.0 42,657,329.5 43,286,287.0 43,961,230.1 49,184,876.2 41,245,760.0 47,666,157.0 510,451,347.9

Beer 10,117,668.1 8,218,369.5 13,994,398.2 7,623,017.1 8,717,830.9 7,690,496.0 5,966,440.8 6,948,343.2 7,553,206.9 8,087,089.0 7,120,225.5 7,419,722.2 99,456,807.5

Wines and Spirits 1,071,508.1 702,577.9 979,185.7 1,044,745.4 907,314.5 1,143,097.0 1,002,702.9 1,042,122.8 3,254,932.5 1,126,722.2 1,206,271.8 1,233,878.2 14,715,059.1

Tobacco 2,517,539.5 1,624,680.0 2,099,032.9 1,554,623.4 2,619,125.7 2,554,029.3 1,649,341.2 1,606,590.0 1,171,808.8 1,686,660.0 2,169,968.5 2,338,300.0 23,591,699.3

Second Hand Motors Vehicles 387,671.0 556,073.0 453,879.3 425,738.0 614,637.2 851,552.1 640,878.6 489,629.5 558,684.5 661,054.0 580,272.5 497,027.9 6,717,097.5

Fuels 16,505,348.6 23,650,530.6 28,937,947.5 32,899,001.1 31,490,944.3 30,491,326.6 33,387,231.1 33,198,482.8 31,421,117.7 37,620,838.1 30,165,604.1 36,173,425.9 365,941,798.4

Electric lamp

5,819.6

10,734.9 1,118.7 1,479.8 2,512.9 3,417.5 3,802.9 28,886.2

Value Added Tax (VAT) 97,041,720.4 96,604,456.4 75,668,628.2 78,167,686.0 89,914,536.

5 87,035,265.9 88,483,199.0 99,329,600.6 96,182,635.4 83,933,550.1 86,479,912.3 89,265,108.2 1,068,106,299.2

VAT on Domestic Goods 67,872,356.4 68,682,535.2 46,395,926.2 50,094,733.3 60,406,379.9 60,637,134.7 56,074,363.6 72,079,192.4 57,167,899.0 58,605,666.7 54,405,362.7 56,702,762.6 709,124,312.5

Imported Goods & Services 37,572,399.9 39,220,806.1 46,878,179.3 38,396,550.4 42,376,336.1 39,358,182.2 43,008,755.0 40,562,705.1 45,746,663.4 43,008,874.3 45,034,600.6 42,038,794.7 503,202,846.9

Refunds (8,403,035.8) (11,298,884.8) (17,605,477.3) (10,323,597.6) (12,868,179.4

) (12,960,051.0) (10,599,919.5) (13,312,297.0) (6,731,926.9) (17,680,990.9) (12,960,051.0) (9,476,449.1) (144,220,860.3)

Other indirect taxes 1,114,159.4 2,536,273.6 4,581,872.8 6,517,614.2 5,795,602.1 12,202,382.0 10,584,691.9 8,298,091.8 9,453,339.0 7,227,204.5 5,779,848.3 24,403,278.8 98,494,358.2

-

Non-tax Revenue 9,211,060.0 10,640,302.4 14,048,418.6 19,051,326.3 94,787,240.

2 32,513,570.6 56,091,423.8 33,391,954.7 14,689,359.5 15,141,660.2 11,493,029.1 15,925,710.2 326,985,055.6

-

Revenue from Investments & Property 562,896.4 563,756.2 1,382,442.6 9,724,324.0 505,289.8 891,200.2 7,635,900.0 4,459,867.5 5,600,926.8 1,777,833.4 410,729.2 7,096,426.0 40,611,592.1

RBZ remittances

-

Govt Property rent, interest and dividends etc. 562,896.4 563,756.2 1,382,442.6 9,724,324.0 505,289.8 891,200.2 7,635,900.0 4,459,867.5 5,600,926.8 1,777,833.4 410,729.2 7,096,426.0 40,611,592.1

Fees: Govt./Dept facilities & services 6,750,729.15 7,629,799.7 10,761,380.8 7,429,429.5 92,642,765.8 22,418,599.7 47,241,051.7 27,883,320.0 7,329,404.5 11,745,510.1 8,054,154.2 7,523,458.6 257,409,603.8

Pension Contribution 69,599.5 227,211.9 44,595.3 71,552.3 97,467.8 7,933,817.0

45,812.7 223,507.8 26,881.8 1,444,118.4 81,369.4 10,265,933.9

Other

-

Gvt sales,licences,fines etc 812,727.7 1,266,884.3 580,966.7 733,669.0 621,011.0 597,577.5 435,207.9 376,195.3 563,348.2 1,033,852.1 401,345.1 598,128.9 8,020,913.7

Judicial Fines 561,437.3 450,349.3 383,753.4 434,212.3 468,161.9 448,880.4 466,119.9 427,718.1 460,956.0 453,122.8 571,115.9 473,136.1 5,598,963.3

Refunds of Miscellaneous Payments from Votes 6,484.99 382,834.2 463,355.9 594,319.3 281,216.8 122,199.7 41,357.8 78,189.8 416,362.8 31,416.7

4,301.8 2,422,039.8

Miscellaneous 398,427.3 94,080.3 412,665.5 37,069.4 27,379.1 50,669.3 208,263.9 49,662.6 23,715.7 17,419.4 31,625.1 22,891.9 1,373,869.4

40

ZIMBABWE BUDGET CUMULATIVE DATA: 2013

ACTUALS (US$)

CUM ACTUAL to DEC 2013

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Dec-13

Banking Levy 30,826.0 10,909.8 4,186.4 8,471.1 125,713.2 32,141.8 42,266.4 48,247.4 46,153.4

125,997.4 474,912.9

-

Retained & Prepaid Revenue(Others) 8,820,230.7 8,156,500.8 10,114,517.1 10,080,469.6 9,750,122.7 10,543,303.7 9,805,995.3 10,377,307.9 11,001,978.1 8,761,070.1 7,218,321.3 10,813,332.5 115,443,149.7

Aids Levy 2,306,222.8 1,679,344.3 3,328,487.3 2,187,008.2 2,238,756.2 3,611,844.5 2,347,037.4 2,702,058.3 4,229,527.6 2,287,633.5 2,017,291.4 4,594,629.6 33,529,841.1

Noczim Levy 5,139,396.4 5,286,291.8 5,462,936.7 6,061,761.4 5,382,832.0 5,510,430.7 5,863,920.2 5,877,763.0 5,415,456.9 6,473,436.6 5,197,509.8 6,214,667.94 67,886,403.3

Toll fees 1,374,611.6 1,190,864.8 1,323,093.1 1,831,699.9 2,128,534.5 1,421,028.4 1,595,037.7 1,797,486.7 1,356,993.6

3,520.0 4,035.0 14,026,905.3

Prepayment Account 7,774,048.7 3,011,832.0 (9,060,372.6) 3,427,176.7 (7,104,161.7) (5,996,319.3) (2,867,141.6) 3,223,919.9 437,479.9 383,161.6 6,904,075.3 (4,356,980.5) (4,223,281.6)

EXPENDITURES ACTUALS (US$)

CUM ACTUAL to DEC

2013

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Dec-13

Total Exp including Retained Grants(ZIMRA,AIDS&NOCZIM) 225,497,981.

8 331,998,622.

6 329,719,995.

6 256,984,255.

7 316,186,584

.5 340,871,273.

2 406,856,857.

9 344,590,146.

5 313,345,821.

2 398,373,304.2 326,147,536.

7 490,245,695.3 4,080,818,075.0

-

Total expenditure and net lending including ZIMRA Grant 225,497,981.

8 324,553,003.

4 322,754,359.

6 248,192,831.

7 307,828,984

.0 333,249,685.

0 397,734,582.

7 336,378,288.

9 302,063,941.

6 388,728,319.7 317,386,466.

6 483,030,894.0 3,987,399,339.0

-

Total expenditure and net lending (Net) 225,497,981.

8 324,553,003.

4 322,754,359.

6 248,192,831.

7 307,828,984

.0 333,249,685.

0 397,734,582.

7 336,378,288.

9 302,063,941.

6 388,728,319.7 317,386,466.

6 483,030,894.0 3,987,399,339.0

-

Current Expenditure 220,352,337.

8 288,088,222.

4 302,276,427.

5 239,521,648.

7 244,803,466

.0 310,765,177.

0 372,264,763.

7 302,142,009.

6 281,884,759.

9 275,737,095.1 296,554,061.

6 385,304,913.0 3,519,694,882.2

-

Goods and services 134,132,091.

0 206,797,040.

0 184,389,362.

0 158,992,982.

0 186,753,029

.0 219,832,212.

0 186,571,214.

0 221,065,774.

5 189,211,925.

0 174,094,042.0 217,215,451.

0 286,124,957.0 2,365,180,079.5

Employment Costs 123,071,218.0 167,980,111.0 156,201,781.0 135,279,161.0 155,703,674.0 154,451,735.0 153,276,674.0 148,427,534.0 147,944,336.0 143,123,588.0 190,861,315.0 249,424,560.0 1,925,745,687.0

Domestic Travel Expenses 501,411.0 757,012.0 11,527,073.0 1,190,152.0 1,008,222.0 664,598.0 1,842,373.0 931,904.0 374,924.0 1,468,737.0 476,900.0 889,649.0 21,632,955.0

Foreign Travel Expenses 3,553,812.0 4,743,852.0 5,077,053.0 3,896,036.0 6,349,391.0 5,142,123.0 1,867,470.0 3,982,015.0 4,024,435.0 3,288,300.0 4,559,517.0 5,684,913.0 52,168,917.0

Communication, Supplies and Services 130,733.0 7,927,341.0 315,104.0 1,427,870.0 3,287,003.0 39,296,689.0 7,462,244.0 29,879,982.5 772,373.0 827,306.0 11,919,456.0

103,246,101.5

Education supplies and Services 1,500.0 4,300.0 4,052.0 18,771.0 50,082.0 640,002.0 24,324.0 - 60,448.0 11,704.0 318,011.0 11,331.0 1,144,525.0

41

ZIMBABWE BUDGET CUMULATIVE DATA: 2013

ACTUALS (US$)

CUM ACTUAL to DEC 2013

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Dec-13

Medical Supplies and services 94,700.0 935,212.0 337,335.0 196,705.0 248,562.0 104,829.0 1,353,211.0 199,087.0 379,506.0 2,526,263.0 331,339.0 406,825.0 7,113,574.0

Office supplies and services 86,085.0 205,198.0 236,773.0 202,099.0 250,367.0 223,044.0 248,171.0 121,739.0 174,495.0 188,129.0 57,018.0 265,141.0 2,258,259.0

Training expenses 136,461.0 277,541.0 68,849.0 169,735.0 248,661.0 185,554.0 311,094.0 100,639.0 144,264.0 203,403.0 71,637.0 165,779.0 2,083,617.0

Rental and other service charges 2,318,587.0 15,920,119.0 3,293,741.0 5,551,287.0 5,198,969.0 5,727,713.0 6,797,729.0 24,233,610.0 19,837,194.0 3,881,474.0 1,422,742.0 11,462,741.0 105,645,906.0

Institutional provisions 590,626.0 1,763,982.0 1,299,337.0 1,585,266.0 2,046,178.0 1,896,898.0 1,979,827.0 1,804,707.0 806,250.0 2,868,553.0 2,732,065.0 2,904,734.0 22,278,423.0

Other 99,442.0 1,189,732.0 474,841.0 673,550.0 1,215,724.0 1,059,650.0 482,053.0 583,058.0 4,795,030.0 254,936.0 264,209.0 1,157,773.0 12,249,998.0

Maintenance of capital works 1,650,197.0 2,248,178.0 1,594,510.0 2,436,765.0 3,869,231.0 2,136,914.0 3,270,668.0 1,570,884.0 1,805,005.0 2,442,642.0 1,525,196.0 7,268,518.0 31,818,708.0

Programmes 1,897,319.0 2,844,462.0 3,958,913.0 6,365,585.0 7,276,965.0 8,302,463.0 7,655,376.0 9,230,615.0 8,093,665.0 13,009,007.0 2,676,046.0 6,482,993.0 77,793,409.0

Interest on debt 536,206.8 264,444.4 8,076,624.5 166,666.7 787,437.0 1,817,617.0 98,412.7 78,730.2 8,517,379.9 362,888.1 224,383.6 2,201,220.0 23,132,010.7

Foreign

7,835,513.3

649,659.0 437,993.0

7,046,827.9 324,792.1

602,343.6 16,897,128.9

Domestic 536,206.8 264,444.4 241,111.1 166,666.7 137,778.0 1,379,624.0 98,412.7 78,730.2 1,470,552.0 38,096.0 224,383.6 1,598,876.4 6,234,881.8

Current transfers 85,684,040.0 81,026,738.0 109,810,441.

0 80,362,000.0 57,263,000.

0 89,115,348.0 185,595,137.

0 80,997,505.0 84,155,455.0 101,280,165.0 79,114,227.0 96,978,736.0 1,131,382,792.0

Pensions 34,853,900.0 37,304,000.0 33,729,300.0 33,691,000.0 34,885,000.0 34,900,000.0 34,900,000.0 34,900,000.0 34,311,000.0 34,776,000.0 34,985,000.0 34,900,000.0 418,135,200.0

Other grants and transfers 50,830,140.0 43,722,738.0 76,081,141.0 46,671,000.0 22,378,000.0 54,215,348.0 150,695,137.0 46,097,505.0 49,844,455.0 66,504,165.0 44,129,227.0 62,078,736.0 713,247,592.0

Capital expenditure 5,145,644.0 36,064,781.0 7,878,800.0 10,831,183.0 38,411,274.

0 21,984,508.0 22,399,819.0 31,183,904.0 13,724,908.0 101,872,557.0 20,332,405.0 86,225,981.0 396,055,764.0

Breeding stock

-

-

-

Furniture and Equipment

4,400.0 564,697.0 205,059.0 837,337.0 4,964,789.0 195,419.0 238,209.0 1,933,935.0 1,413,821.0 388,501.0 72,173,557.0 82,919,724.0

Vehicles, Plant and Mobile equipment

485,000.0

- 41,350.0 148,050.0

37,795.0 - 721,513.0 - 4,500.0 1,438,208.0

Acquisition of buildings 1,850,644.0 5,449,877.0 481,803.0 503,085.0 8,463,151.0 2,932,958.0 3,316,790.0 2,648,900.0 2,975,129.0 9,826,654.0 2,454,904.0 2,115,145.0 43,019,040.0

Intangible assets

500,000.0

668,344.0 35,447.0

880,000.0 105,000.0 1,000,000.0 - 700,000.0 3,888,791.0

Feasibility studies

100.0

12,361.0 42,799.0 15,725.0 -

37,334.0

108,319.0

Capital transfers 3,295,000.0 29,625,404.0 2,368,300.0 10,123,039.0 28,388,731.0 11,348,465.0 18,871,885.0 27,379,000.0 8,710,844.0 88,325,235.0 17,489,000.0 11,232,779.0 257,157,682.0

Equity participation

4,464,000.0

2,512,000.0

- 548,000.0

7,524,000.0

Repayments

-

Net Lending - 400,000.0 12,599,132.2 (2,160,000.0

) 24,614,244.

0 500,000.0 3,070,000.0 3,052,375.3 6,454,273.8 11,118,667.6 500,000.0 11,500,000.0 71,648,692.9

42

ZIMBABWE BUDGET CUMULATIVE DATA: 2013

ACTUALS (US$)

CUM ACTUAL to DEC 2013

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Dec-13

Long-term loans (net) - 400,000.0 12,599,132.2 (2,160,000.0

) 24,614,244.

0 500,000.0 3,070,000.0 3,052,375.3 6,454,273.8 11,118,667.6 500,000.0 11,500,000.0 71,648,692.9

Loan and debt

400,000.0 12,599,132.2

24,614,244.0 500,000.0 3,070,000.0 3,052,375.3 6,454,273.8 11,118,667.6 500,000.0 11,500,000.0 73,808,692.9

Recoveries

(2,160,000.0)

(2,160,000.0)

Investments -

-

Short-term loans (net) - - - -

-

Lending

-

Other Grants - 7,445,619.1 6,965,636.0 8,791,424.0 8,357,600.5 7,621,588.2 9,122,275.2 8,211,857.6 11,281,879.5 9,644,984.5 8,761,070.1 7,214,801.3 93,418,736.0

Noczim Grant

5,139,396.4 5,286,291.8 5,462,936.7 6,170,592.3 5,382,832.0 5,510,430.7 5,863,920.2 8,579,821.2 5,415,456.9 6,473,436.6 5,197,509.8 64,482,624.5

Aids Grant

2,306,222.8 1,679,344.3 3,328,487.3 2,187,008.2 2,238,756.2 3,611,844.5 2,347,937.4 2,702,058.3 4,229,527.6 2,287,633.5 2,017,291.4 28,936,111.5

FINANCING (20,000,000.

0) (15,150,000.

0) (2,414,381.7

) (5,150,000.0

) 39,135,714.

0 (21,783,390.

1) 41,135,714.0 (5,864,286.0

) 59,106,008.0 (20,084,508.8

) 47,350,000.0 36,322,770.7 132,603,640.1

-

Foreign Financing (net) (150,000.0) (150,000.0) (22,414,381.

7) 4,850,000.0 (150,000.0) (16,069,104.

1) (150,000.0) (150,000.0) (23,751,134.

0) (792,236.0) (150,000.0) 78,926,347.0 19,849,491.1

Borrowings-SDR

5,000,000.0

5,000,000.0

Loan(Medical Equipment)

83,406,336.0 83,406,336.0

Repayments (150,000.0) (150,000.0) (22,414,381.7) (150,000.0) (150,000.0) (16,069,104.1) (150,000.0) (150,000.0) (23,751,134.0) (792,236.0) (150,000.0) (4,479,989.0) (68,556,844.9)

-

Total Domestic Financing (19,850,000.

0) (15,000,000.

0) 20,000,000.0 (10,000,000.

0) 39,285,714.

0 (5,714,286.0

) 41,285,714.0 (5,714,286.0

) 82,857,142.0 (19,292,272.8

) 47,500,000.0 (42,603,576.3

) 112,754,148.9

Treasury Bills

40,000,000.0

45,000,000.0

37,000,000.0

47,500,000.0

169,500,000.0

Loans

100,000,000.0

100,000,000.0

Repayments (19,850,000.0) (15,000,000.0) (20,000,000.0) (10,000,000.0) (5,714,286.0) (5,714,286.0) (5,714,286.0) (5,714,286.0

) (17,142,858.0) (19,292,272.8)

(42,603,576.3) (166,745,851.1)

SDF

10,000,000.0

10,000,000.0

DEFICIT

-

Surplus (Deficit) excluding grants 29,004,382.9 (55,084,688.

0) (8,754,719.7

) 22,845,094.2 55,759,181.

8 21,156,965.6 (74,701,590.

2) (16,838,397.

7) 51,366,412.7 (110,573,655.

2) (58,283,346.

8) (102,253,558.

4) (246,357,918.8)

-

43

ZIMBABWE BUDGET CUMULATIVE DATA: 2013

ACTUALS (US$)

CUM ACTUAL to DEC 2013

Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Dec-13

Surplus (Deficit) including grants 37,824,613.6 (54,373,806.

4) (5,605,838.6

) 24,134,139.8 57,151,704.

0 24,078,681.1 (74,017,870.

2) (14,672,947.

4) 51,086,511.2 (111,457,569.

6) (59,826,095.

6) (98,655,027.1

) (224,333,505.2)

-

TOTAL FINANCING 9,004,382.9 (70,234,688.

0) (11,169,101.

4) 17,695,094.2 94,894,895.

8 (626,424.5) (33,565,876.

2) (22,702,683.

7) 110,472,420.

7 (130,658,164.

0) (10,933,346.

8) (65,930,787.6

) (113,754,278.8)

BREAKDOWN OF DOMESTIC FINANCING

-

-

Non-bank Domestic Financing (net) 9,004,382.9 (70,234,688.

0) (11,169,101.

4) 17,695,094.2 94,894,895.

8 (626,424.5) (33,565,876.

2) (22,702,683.

7) 110,472,420.

7 (130,658,164.

0) (10,933,346.

8) (65,930,787.6

) (113,754,278.8)

Surplus

-

Tax Reserve Certificates/Prepayments 7,774,048.7 3,011,832.0 (9,060,372.6) 3,427,176.7 (7,104,161.7) (5,996,319.3) (2,867,141.6) 3,223,919.9 437,479.9 383,161.6 6,904,075.3 (4,356,980.5) (4,223,281.6)

Opening bank balances 176,418,398.

4 168,163,641.

8 129,930,538.

2 142,087,259.

9 107,282,555

.6 100,852,822.

5 132,421,751.

8 74,688,639.2 77,851,196.2 140,271,307.1 72,965,373.4 50,036,623.0 1,372,970,107.0

Payments in transit (25,033,188.1) 28,989,752.4 32,386,195.6 (55,926,975.2) (94,220,467.3

) 38,191,673.1 (21,300,094.8) 22,641,320.9 (48,489,789.6) 62,969,068.7 (18,899,478.9) 39,108,290.8 (39,583,692.4)

Closing bank balances 168,163,641.8 129,930,538.2 142,087,259.9 107,282,555.6 100,852,822.5 132,421,751.8 74,688,639.2 77,851,196.2 140,271,307.1 72,965,373.4 50,036,623.0 19,357,145.7

Source: Ministry of Finance and Economic Development