2012 Q1 Report

15

QUARTERLY ECONOMIC UPDATE | Q1 2012

-

Upload

columbus-2020 -

Category

Career

-

view

578 -

download

1

description

Our Q1 report, with statistics on new business attraction and expansion, employment rates, industry growth, and much more.

Transcript of 2012 Q1 Report

QUARTERLY ECONOMIC UPDATE | Q1 2012

Th

e

TOTAL PAYROLL EMPLOYMENT

Source: Current Employment Statistics, U.S. Bureau of Labor Statistics. Source: Local Area Unemployment Statistics, Bureau of Labor Stats.

Seasonal adjustment of MSA employment by Regionomics LLC. Seasonal adjustment of regional rate by Regionomics LLC.

COLUMBUS REGION LABOR FORCE

Source: Local Area Unemployment Statistics, Bureau of Labor Stats.

Seasonal adjustment of regional rate by Regionomics LLC.

1

COLUMBUS REGION UNEMPLOYMENT

RATE

QUARTERLY ECONOMIC UPDATE | Q1 2012

EMPLOYMENT, LABOR FORCE, UNEMPLOYMENT RATES

88.0

90.0

92.0

94.0

96.0

98.0

100.0

102.0

1/0

8

4/0

8

7/0

8

10/0

8

1/0

9

4/0

9

7/0

9

10/0

9

1/10

4/1

0

7/1

0

10/1

0

1/11

4/1

1

7/1

1

10/1

1

1/12

Ind

ex: 1/

08

= 1

00

.0

Columbus MSA Ohio US

920

970

1,020

1,070

1,120

1/0

8

4/0

8

7/0

8

10/0

8

1/0

9

4/0

9

7/0

9

10/0

9

1/10

4/1

0

7/1

0

10/1

0

1/11

4/11

7/1

1

10/1

1

1/12

Th

ou

san

ds

Labor force

Labor force, normal growth

Resident employment

0%

2%

4%

6%

8%

10%

12%

1/0

8

4/0

8

7/0

8

10/0

8

1/0

9

4/0

9

7/0

9

10/0

9

1/10

4/1

0

7/1

0

10/1

0

1/11

4/1

1

7/1

1

10/1

1

1/12

Columbus Region Ohio U.S.

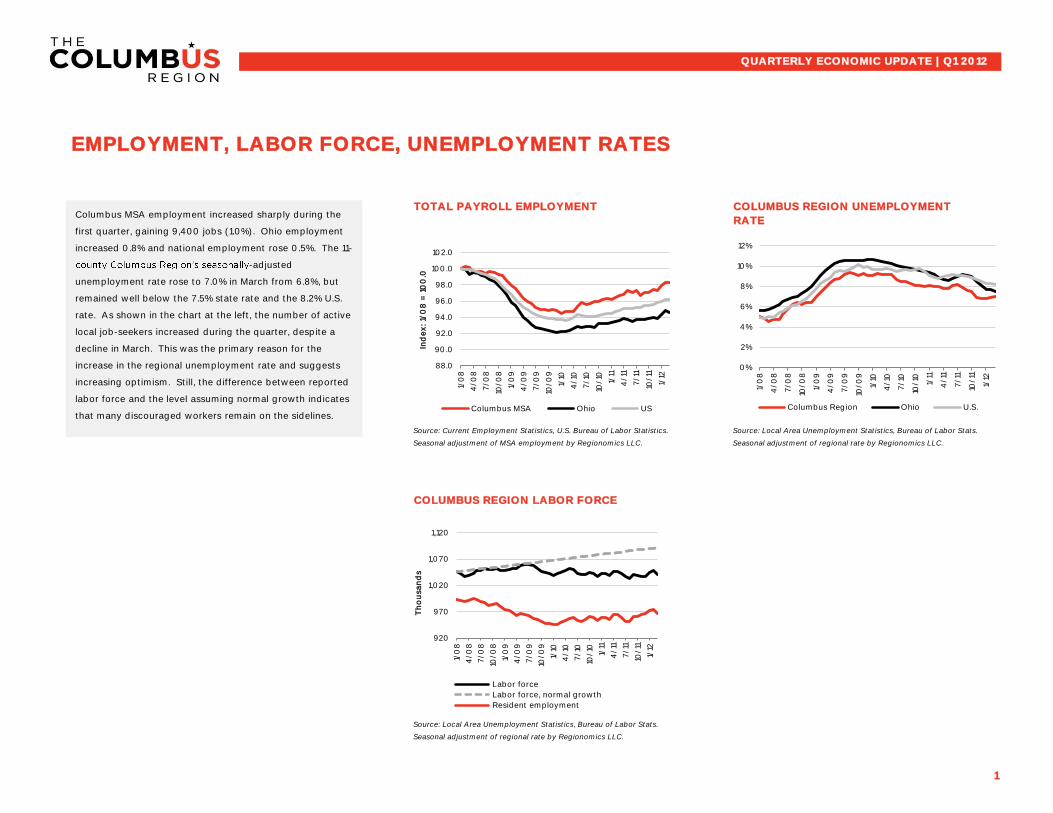

Columbus MSA employment increased sharply during the

first quarter, gaining 9,400 jobs (1.0%). Ohio employment

increased 0.8% and national employment rose 0.5%. The 11-

-adjusted

unemployment rate rose to 7.0% in March from 6.8%, but

remained well below the 7.5% state rate and the 8.2% U.S.

rate. As shown in the chart at the left, the number of active

local job-seekers increased during the quarter, despite a

decline in March. This was the primary reason for the

increase in the regional unemployment rate and suggests

increasing optimism. Still, the difference between reported

labor force and the level assuming normal growth indicates

that many discouraged workers remain on the sidelines.

MANUFACTURING

PROFESSIONAL & BUSINESS SERVICES FINANCE & INSURANCE

Source: Current Employment Statistics, U.S. Bureau of Labor Statistics.

Seasonal adjustment of MSA employment by Regionomics LLC.

2

TRANSPORTATION, WAREHOUSING &

WHOLESALE

QUARTERLY ECONOMIC UPDATE | Q1 2012

EMPLOYMENT BY INDUSTRY

The charts on this and the next page highlight employment

Distribution industries (including transportation,

warehousing, and wholesale trade) added 1,000 jobs (1.3%)

during the first quarter versus statewide growth of 1.9% and

0.6% nationwide. Manufacturing lost 3,300 jobs (5.0%)

while Ohio employment increased 1.3% and U.S.

employment rose 1.0%. The weakness in local

manufacturing employment growth seems to be due to

improving efficiency rather than weakness in the sector

itself. However, Columbus Region manufacturers are likely

to reach the limit of their productivity growth and will need

to increase employment, as their counterparts have

elsewhere. Business service employment increased 2,300

(1.6%), better than the statewide gain of 0.5% and the U.S.

gain of 1.1%. Finance and insurance lost 400 jobs (0.6%),

compared to gains of 0.5% in Ohio and 0.2% nationwide.

70.0

75.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

1/0

8

4/0

8

7/0

8

10/0

8

1/0

9

4/0

9

7/0

9

10/0

9

1/10

4/1

0

7/1

0

10/1

0

1/11

4/1

1

7/1

1

10/1

1

1/12

Ind

ex: 1/

08

= 1

00

.0

Columbus MSA Ohio US

70.0

75.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

1/0

8

4/0

8

7/0

8

10/0

8

1/0

9

4/0

9

7/0

9

10/0

9

1/10

4/1

0

7/1

0

10/1

0

1/11

4/1

1

7/1

1

10/1

1

1/12

Ind

ex: 1/

08

= 1

00

.0

Columbus MSA Ohio US

70.0

75.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

1/0

8

4/0

8

7/0

8

10/0

8

1/0

9

4/0

9

7/0

9

10/0

9

1/10

4/1

0

7/1

0

10/1

0

1/11

4/1

1

7/1

1

10/11

1/12

Ind

ex: 1/

08

= 1

00

.0

Columbus MSA Ohio US

70.0

75.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

1/0

8

4/0

8

7/0

8

10/0

8

1/0

9

4/0

9

7/0

9

10/0

9

1/10

4/1

0

7/1

0

10/1

0

1/11

4/1

1

7/1

1

10/11

1/12

Ind

ex: 1/

08

= 1

00

.0

Columbus MSA Ohio US

LEISURE & HOSPITALITY

GOVERNMENT RETAIL

Source: Current Employment Statistics, U.S. Bureau of Labor Statistics.

Seasonal adjustment of MSA employment by Regionomics LLC.

3

HEALTHCARE & SOCIAL ASSISTANCE

QUARTERLY ECONOMIC UPDATE | Q1 2012

EMPLOYMENT BY INDUSTRY (continued)

Columbus MSA healthcare employment enjoyed

particularly strong growth, gaining 2,700 jobs (2.4%) versus

Ohio and U.S growth of 1.4% and 0.7%, respectively. While

it is possible that the Bureau of Labor Statistics may revise

these estimates downward later , the latest increase in

healthcare employment is part of a longer-term trend.

Leisure and hospitality lost 500 jobs (0.5%), compared to

statewide growth of 0.1% and U.S. growth of 0.9%.

Government employment was essentially unchanged in the

Columbus MSA after a sustained decline in 2011.

Nationwide government employment was also unchanged

but the sector gained 0.2% in Ohio. Columbus MSA retail

added a massive 3,400 jobs (3.5%) while Ohio gained 1.6%

and the U.S. lost 0.3%. The $28.4 billion in taxable sales in

the Region during 2011 represented an after-inflation

increase of 2.8% from the 2010 level.

85.0

90.0

95.0

100.0

105.0

110.0

115.0

120.0

125.0

1/0

8

4/0

8

7/0

8

10/0

8

1/0

9

4/0

9

7/0

9

10/0

9

1/10

4/1

0

7/1

0

10/1

0

1/11

4/1

1

7/1

1

10/1

1

1/12

Ind

ex: 1/

08

= 1

00

.0

Columbus MSA Ohio US

70.0

75.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

1/0

8

4/0

8

7/0

8

10/0

8

1/0

9

4/0

9

7/0

9

10/0

9

1/10

4/1

0

7/1

0

10/10

1/11

4/1

1

7/1

1

10/1

1

1/12

Ind

ex: 1/

08

= 1

00

.0

Columbus MSA Ohio US

70.0

75.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

1/0

8

4/0

8

7/0

8

10/0

8

1/0

9

4/0

9

7/0

9

10/0

9

1/10

4/1

0

7/1

0

10/10

1/11

4/1

1

7/1

1

10/1

1

1/12

Ind

ex: 1/

08

= 1

00

.0

Columbus MSA Ohio US

70.0

75.0

80.0

85.0

90.0

95.0

100.0

105.0

110.0

1/0

8

4/0

8

7/0

8

10/0

8

1/0

9

4/0

9

7/0

9

10/0

9

1/10

4/10

7/1

0

10/10

1/11

4/1

1

7/11

10/1

1

1/12

Ind

ex: 1/

08

= 1

00

.0

Columbus MSA Ohio US

CONSTRUCTION

MANUFACTURING WHOLESALE TRADE

Source: Current Employment Statistics, U.S. Bureau of Labor Statistics. Source: Current Employment Statistics, U.S. Bureau of Labor Statistics.

Seasonal adjustment of MSA employment by Regionomics LLC.

4

QUARTERLY ECONOMIC UPDATE | Q1 2012

CURRENT EMPLOYMENT STATISTICS REVISIONS

TOTAL PAYROLL EMPLOYMENT

TOTAL SEASONALLY ADJUSTED PAYROLL

EMPLOYMENT, MONTHLY

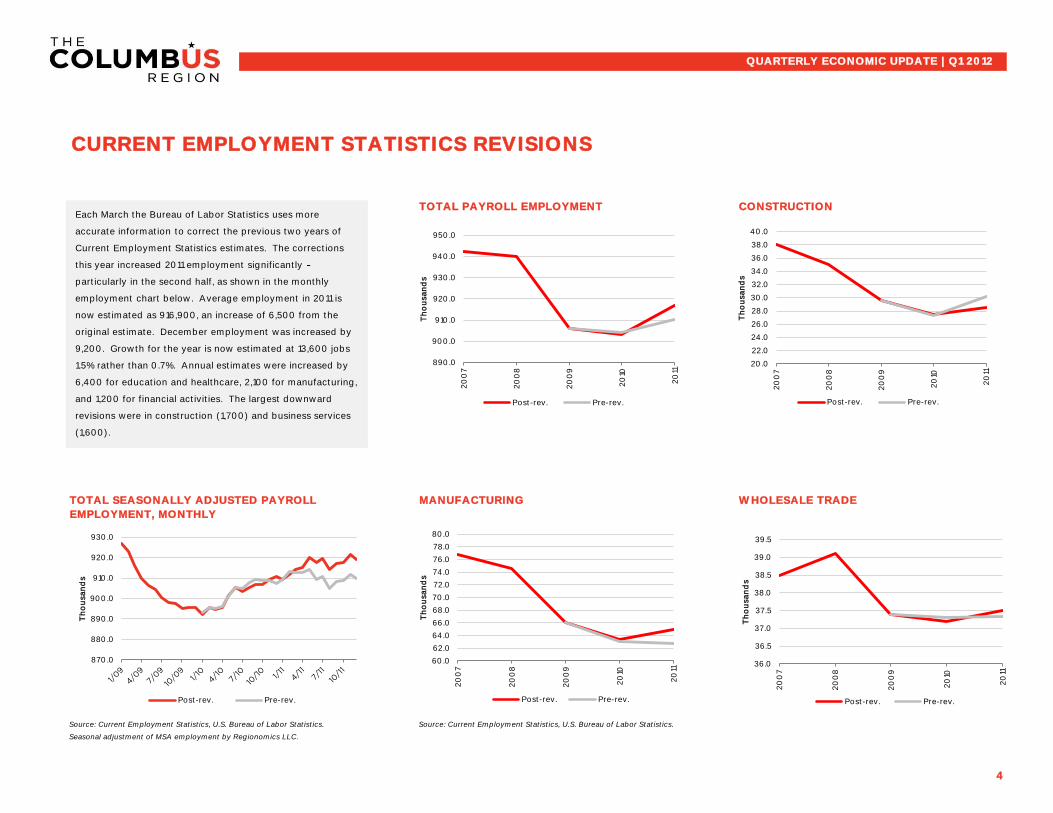

Each March the Bureau of Labor Statistics uses more

accurate information to correct the previous two years of

Current Employment Statistics estimates. The corrections

this year increased 2011 employment significantly

particularly in the second half, as shown in the monthly

employment chart below. Average employment in 2011 is

now estimated as 916,900, an increase of 6,500 from the

original estimate. December employment was increased by

9,200. Growth for the year is now estimated at 13,600 jobs

1.5% rather than 0.7%. Annual estimates were increased by

6,400 for education and healthcare, 2,100 for manufacturing,

and 1,200 for financial activities. The largest downward

revisions were in construction (1,700) and business services

(1,600).

870.0

880.0

890.0

900.0

910.0

920.0

930.0

Th

ou

san

ds

Post-rev. Pre-rev.

890.0

900.0

910.0

920.0

930.0

940.0

950.0

20

07

20

08

20

09

20

10

20

11

Th

ou

san

ds

Post-rev. Pre-rev.

20.0

22.0

24.0

26.0

28.0

30.0

32.0

34.0

36.0

38.0

40.0

20

07

20

08

20

09

20

10

20

11

Th

ou

san

ds

Post-rev. Pre-rev.

60.0

62.0

64.0

66.0

68.0

70.0

72.0

74.0

76.0

78.0

80.0

20

07

20

08

20

09

20

10

20

11

Th

ou

san

ds

Post-rev. Pre-rev.

36.0

36.5

37.0

37.5

38.0

38.5

39.0

39.5

20

07

20

08

20

09

20

10

20

11

Th

ou

san

ds

Post-rev. Pre-rev.

Source: Current Employment Statistics, U.S. Bureau of Labor Statistics.

5

QUARTERLY ECONOMIC UPDATE | Q1 2012

TRANSPORTATION & WAREHOUSING

CURRENT EMPLOYMENT STATISTICS REVISIONS (continued)

RETAIL TRADE FINANCIAL ACTIVITIES PROFESSIONAL & BUSINESS

SERVICES

EDUCATION & HEALTH SERVICES OTHER SERVICES GOVERNMENTLEISURE & HOSPITALITY

94.0

95.0

96.0

97.0

98.0

99.0

100.0

101.0

102.0

103.0

104.0

20

07

20

08

20

09

20

10

20

11

Th

ou

san

ds

Post-rev. Pre-rev.

40.0

42.0

44.0

46.0

48.0

50.0

52.0

20

07

20

08

20

09

20

10

20

11

Th

ou

san

ds

Post-rev. Pre-rev.

66.0

67.0

68.0

69.0

70.0

71.0

72.0

73.0

74.0

20

07

20

08

20

09

20

10

20

11

Th

ou

san

ds

Post-rev. Pre-rev.

144.0

146.0

148.0

150.0

152.0

154.0

156.0

20

07

20

08

20

09

20

10

20

11

Th

ou

san

ds

Post-rev. Pre-rev.

105.0

110.0

115.0

120.0

125.0

130.0

135.0

20

07

20

08

20

09

20

10

20

11

Th

ou

san

ds

Post-rev. Pre-rev.

84.0

85.0

86.0

87.0

88.0

89.0

90.0

20

07

20

08

20

09

20

10

20

11

Th

ou

san

ds

Post-rev. Pre-rev.

34.0

34.5

35.0

35.5

36.0

36.5

37.0

37.5

38.0

20

07

20

08

20

09

20

10

20

11

Th

ou

san

ds

Post-rev. Pre-rev.

154.0

155.0

156.0

157.0

158.0

159.0

160.0

20

07

20

08

20

09

20

10

20

11

Th

ou

san

ds

Post-rev. Pre-rev.

INDUSTRIAL REAL ESTATE VACANCY RATES PORT COLUMBUS INTL. AIRPORT PASSENGERS

Source: CB Richard Ellis. Source: Columbus Regional Airport Authority.

OFFICE VACANCY RATES RICKENBACKER INTL. AIRPORT CARGO HANDLED

Source: CB Richard Ellis. Source: Columbus Regional Airport Authority.

6

QUARTERLY ECONOMIC UPDATE | Q1 2012

AIRPORT PASSENGERS & CARGOCOMMERCIAL REAL ESTATE

0.0

5.0

10.0

15.0

20.0

25.0

20

07-Q

1

20

07-Q

2

20

07-Q

3

20

07-Q

4

20

08

-Q1

20

08

-Q2

20

08

-Q3

20

08

-Q4

20

09

-Q1

20

09

-Q2

20

09

-Q3

20

09

-Q4

20

10-Q

1

20

10-Q

2

20

10-Q

3

20

10-Q

4

20

11-Q

1

20

11-Q

2

20

11-Q

3

20

11-Q

4

20

12-Q

1

Pe

rce

nt

Columbus U.S.

0.0

5.0

10.0

15.0

20.0

25.0

20

07-Q

1

20

07-Q

2

20

07-Q

3

20

07-Q

4

20

08

-Q1

20

08

-Q2

20

08

-Q3

20

08

-Q4

20

09

-Q1

20

09

-Q2

20

09

-Q3

20

09

-Q4

20

10-Q

1

20

10-Q

2

20

10-Q

3

20

10-Q

4

20

11-Q

1

20

11-Q

2

20

11-Q

3

20

11-Q

4

20

12-Q

1

Pe

rce

nt

Columbus U.S.

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

Q1 Q2 Q3 Q4

Th

ou

san

ds o

f p

asse

ng

ers

2008 2009 2010 2011 2012

0

10,000

20,000

30,000

40,000

50,000

60,000

Q1 Q2 Q3 Q4

Th

ou

san

ds o

f p

ou

nd

s

2008 2009 2010 2011 2012

Source: U.S. Census Bureau. Source: Columbus Board of Realtors.

CHANGE IN RESIDENTIAL SALES FROM SAME QUARTER PREVIOUS YEAR

Source: Columbus Board of Realtors, National Association of Realtors.

7

QUARTERLY ECONOMIC UPDATE | Q1 2012

HOUSING

RESIDENTIAL SALES, COLUMBUS MLS

AREA

RESIDENTIAL BUILDING PERMITS,

COLUMBUS MSAA total of 1,301 residential building permits were issued in

the Columbus MSA during the first quarter of 2012, 25.5%

more than were issued during the first quarter of 2011. The

multi-unit category continued to represent an unusually

large share of total activity (58.6%); single-unit permits

were down 10.5% from last year. The corresponding U.S.

changes were a 30.5% increase in total permits and an

18.7% increase in single-unit. Quarterly home sales in the

Columbus Multiple Listing Service area (larger than and

somewhat different from the Region) totaled 3,993, up

9.4% from the first quarter of 2011. Total dollar volume of

sales increased 13.7% to nearly $600 million. Nationally,

home sales during the quarter were up 7.2% from last year,

but were 14.4% higher in the Midwest.

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Q1 Q2 Q3 Q4

Nu

mb

ne

r o

f P

erm

its

2008 2009 2010 2011 2012

0

1,600

3,200

4,800

6,400

8,000

Q1 Q2 Q3 Q4

Nu

mb

ne

r o

f S

ale

s

2008 2009 2010 2011 2012

-30%

-20%

-10%

0%

10%

20%

30%

40%

20

08

-Q1

20

08

-Q2

20

08

-Q3

20

08

-Q4

20

09

-Q1

20

09

-Q2

20

09

-Q3

20

09

-Q4

20

10-Q

1

20

10-Q

2

20

10-Q

3

20

10-Q

4

20

11-Q

1

20

11-Q

2

20

11-Q

3

20

11-Q

4

20

12-Q

1

Pe

rce

nt

Ch

an

ge

Columbus MLS

U.S.

MSA HOUSE PRICE CHANGE, 2ND QUARTER 2007 TO 4TH QUARTER 2011

Source: Federal Housing Finance Agency House Price Index.

Source: Federal Housing Finance Agency House Price Index.

8

QUARTERLY ECONOMIC UPDATE | Q1 2012

HOUSING (continued)

FHFA HOUSE PRICE INDEX

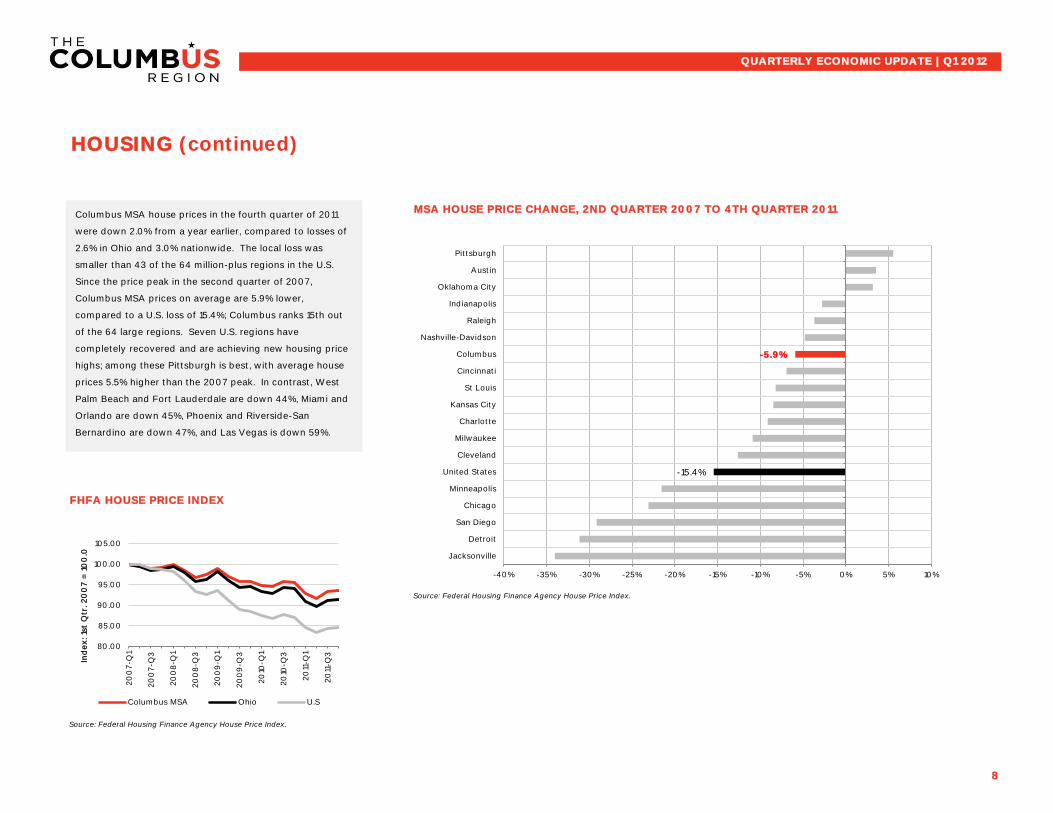

Columbus MSA house prices in the fourth quarter of 2011

were down 2.0% from a year earlier, compared to losses of

2.6% in Ohio and 3.0% nationwide. The local loss was

smaller than 43 of the 64 million-plus regions in the U.S.

Since the price peak in the second quarter of 2007,

Columbus MSA prices on average are 5.9% lower,

compared to a U.S. loss of 15.4%; Columbus ranks 15th out

of the 64 large regions. Seven U.S. regions have

completely recovered and are achieving new housing price

highs; among these Pittsburgh is best, with average house

prices 5.5% higher than the 2007 peak. In contrast, West

Palm Beach and Fort Lauderdale are down 44%, Miami and

Orlando are down 45%, Phoenix and Riverside-San

Bernardino are down 47%, and Las Vegas is down 59%.

-15.4%

-5.9%

-40% -35% -30% -25% -20% -15% -10% -5% 0% 5% 10%

Jacksonville

Detroit

San Diego

Chicago

Minneapolis

United States

Cleveland

Milwaukee

Charlotte

Kansas City

St Louis

Cincinnati

Columbus

Nashville-Davidson

Raleigh

Indianapolis

Oklahoma City

Austin

Pittsburgh

80.00

85.00

90.00

95.00

100.00

105.00

20

07

-Q1

20

07-Q

3

20

08

-Q1

20

08

-Q3

20

09

-Q1

20

09

-Q3

20

10-Q

1

20

10-Q

3

20

11-Q

1

20

11-Q

3

Ind

ex: 1s

t Q

tr. 2

00

7 =

10

0.0

Columbus MSA Ohio U.S

HISTORIC AND FORECAST U.S. GDP; HISTORIC PERSONAL CONSUMPTION

Source: U.S. Bureau of Economic Analysis, Wall Street Journal Economic Forecasting Survey.

CPI INFLATION, LARGE MIDWEST CITIES

Source: Consumer Price Index (CPI-U), U.S Bureau of Labor Statistics

9

QUARTERLY ECONOMIC UPDATE | Q1 2012

GDP AND INFLATION

U.S. Gross Domestic Product (GDP) increased at an annual

rate of 2.2% in the first quarter, less than the previous

was equal to the expectation of economists in the Wall

Street Journal forecasting survey, although less than

forecast in the Bloomberg survey. One positive sign was

the strongest growth in personal consumption in more than

a year (an annual rate of 2.9%) as consumer confidence

continued to improve from its lows of last summer.

Business investment growth slowed, however. The April

Wall Street Journal survey expected GDP growth to rise to

2.7% by the fourth quarter. Economists in the survey put

the risk of a recession at less than 20% the lowest level in

months although they remain concerned about oil prices

and the European economy.

-3%

-2%

-1%

0%

1%

2%

3%

4%

5%

6%

20

07-1

20

07-2

20

07-3

20

07-4

20

08

-1

20

08

-2

20

08

-3

20

08

-4

20

09

-1

20

09

-2

20

09

-3

20

09

-4

20

10-1

20

10-2

20

10-3

20

10-4

20

11-1

20

11-2

20

11-3

20

11-4

20

12-1

An

nu

alize

d C

han

ge

(P

erc

en

t)

All items

Excl.Food &Energy (core)

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

20

07-1

20

07-2

20

07-3

20

07-4

20

08

-1

20

08

-2

20

08

-3

20

08

-4

20

09

-1

20

09

-2

20

09

-3

20

09

-4

20

10-1

20

10-2

20

10-3

20

10-4

20

11-1

20

11-2

20

11-3

20

11-4

20

12-1

20

12-2

20

12-3

20

12-4

An

nu

alize

d C

han

ge

(P

erc

en

t)

GDP

Personal Cons.Exp.

PROJECTS ACTIVE AT END OF EACH MONTH

10

NUMBER OF PROJECTS (2012 v. 2011) FIRST-TIME VISITS (2012 v. 2011)

PROJECTS ACTIVE AT END OF EACH MONTH

BY INDUSTRY

QUARTERLY ECONOMIC UPDATE | Q1 2012

COLUMBUS 2020 PERFORMANCE | PROJECTS JAN-APR 2012

As of April 2012, Columbus 2020 had 78 projects started

year to date, more than 40 percent higher than the 2011

pace. There were also 30 first-time visits to the Columbus

Region by companies year to date through April, more than

double the 2011 pace.

9 11

17 18

11 12

9 9

16

19

13

10

27

12

25

14

0

5

10

15

20

25

30

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2011 2012

0

7

4

2 2

9 8

3 2

4

8

2

12

6 7

5

0

3

6

9

12

15

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2011 2012

The composition of projects in the pipeline has changed in

2012 compared to 2011. Existing business projects now

make up 30-40 percent of projects active at any given

time, compared to 10-15 percent in 2011. Establishment of

Columbus 2020's Business Retention and Expansion team

has been a major factor. Industry composition has also

shifted. Office projects represent a greater share now: up

from 11 percent in July 2011 to 34 percent in April 2012. The

number of manufacturing projects has remained steady,

but the percent share fell from 59 to 41 percent.

8 7 6 6 5 7 10 8

17

44 34 34

39

54

61 58

64 61

70 73 65 66

57

66

53 59

0

10

20

30

40

50

60

70

80

Apr2011

May Jun Jul Aug Sep Oct Nov Dec Jan2012

Feb Mar Apr

Existing New

59%

11%

17%

13%

Jul 2011

52%

19%

17%

12%

Oct 2011

49%

19%

17%

15%

Jan 2012

41%

34%

17%

8%

Apr 2012

Manufacturing Office Logistics Tech/R&D

2012 Q2 PLANNED ACTIVITIES

11

COLUMBUS 2020 PERFORMANCE | DEVELOPMENT ACTIVITIES JAN-APR 2012

QUARTERLY ECONOMIC UPDATE | Q1 2012

2012 Q1 COMPLETED ACTIVITIES

EXISTING BUSINESS VISITS CONDUCTED BY

INDUSTRY

EXISTING BUSINESS VISITS CONDUCTED BY

PLACE

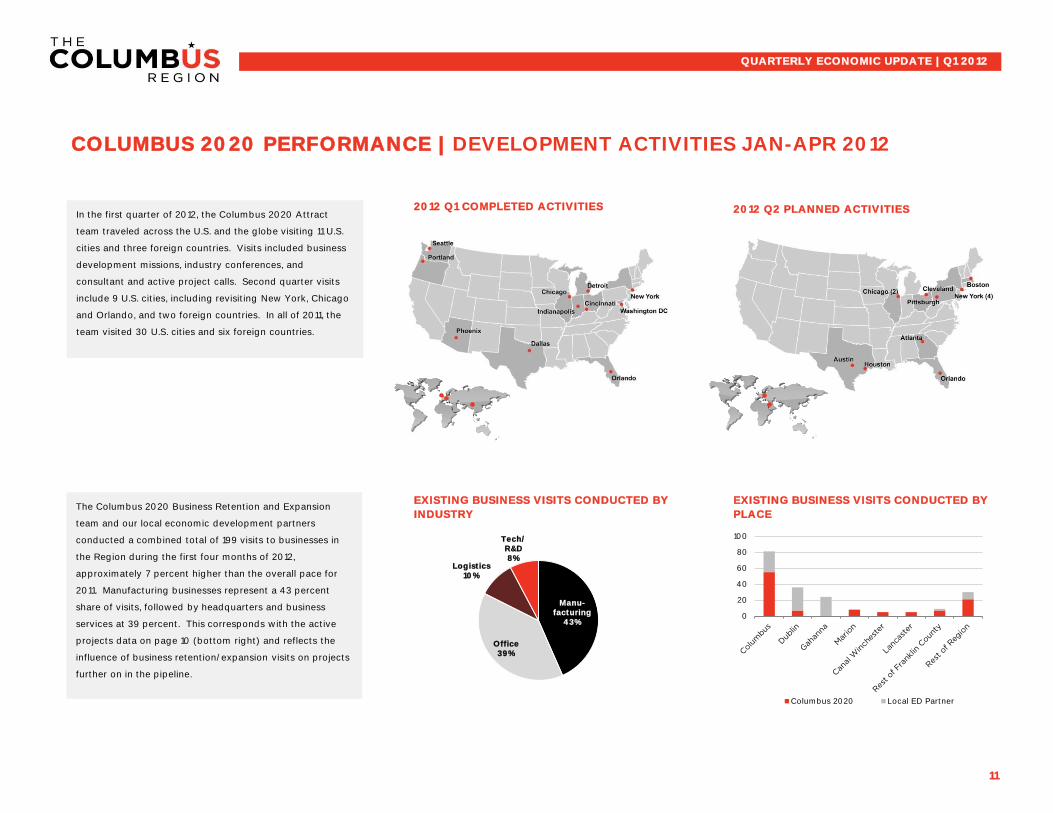

In the first quarter of 2012, the Columbus 2020 Attract

team traveled across the U.S. and the globe visiting 11 U.S.

cities and three foreign countries. Visits included business

development missions, industry conferences, and

consultant and active project calls. Second quarter visits

include 9 U.S. cities, including revisiting New York, Chicago

and Orlando, and two foreign countries. In all of 2011, the

team visited 30 U.S. cities and six foreign countries.

The Columbus 2020 Business Retention and Expansion

team and our local economic development partners

conducted a combined total of 199 visits to businesses in

the Region during the first four months of 2012,

approximately 7 percent higher than the overall pace for

2011. Manufacturing businesses represent a 43 percent

share of visits, followed by headquarters and business

services at 39 percent. This corresponds with the active

projects data on page 10 (bottom right) and reflects the

influence of business retention/expansion visits on projects

further on in the pipeline.

Manu- facturing

43%

Office 39%

Logistics 10%

Tech/ R&D 8%

0

20

40

60

80

100

Columbus 2020 Local ED Partner

12

NOTABLE EXPANSIONS & LOCATIONS | JAN-APR 2012

ED PROJECT ANNOUNCEMENTS - JOB

CREATION

ED PROJECT ANNOUNCEMENTS, COUNT

BY MUNICIPALITY

ED PROJECT ANNOUNCEMENTS, COUNT

BY PLACE

QUARTERLY ECONOMIC UPDATE | Q1 2012

ED PROJECT ANNOUNCEMENTS BY

INDUSTRYColumbus 2020 tracks economic development project

announcements in the Columbus Region. Our database contains 47

projects for the first four months of 2012, about the same pace as the

139 projects for all of 2011 . Of the 47 projects, 45% have been in

manufacturing and 27% in headquarters/office functions, roughly

similar to 2011 numbers. Projects year to date in 2012 represent a

combined total of more than 5,000 jobs anticipated to be created or

retained.

44%

25%

12%

19%

2011

45%

27%

13%

15%

Jan-Apr 2012

Manufacturing Office Logistics Tech/R&D

4,132

5,840

7,839

1,083

2,423

1,504

0

2,000

4,000

6,000

8,000

10,000

Attract Expand Retain

2011 Jan-Apr 2012

12

5 5

9

16

0

4

8

12

16

20

Columbus Dublin MountVernon

Rest ofFranklinCounty

Rest ofRegion

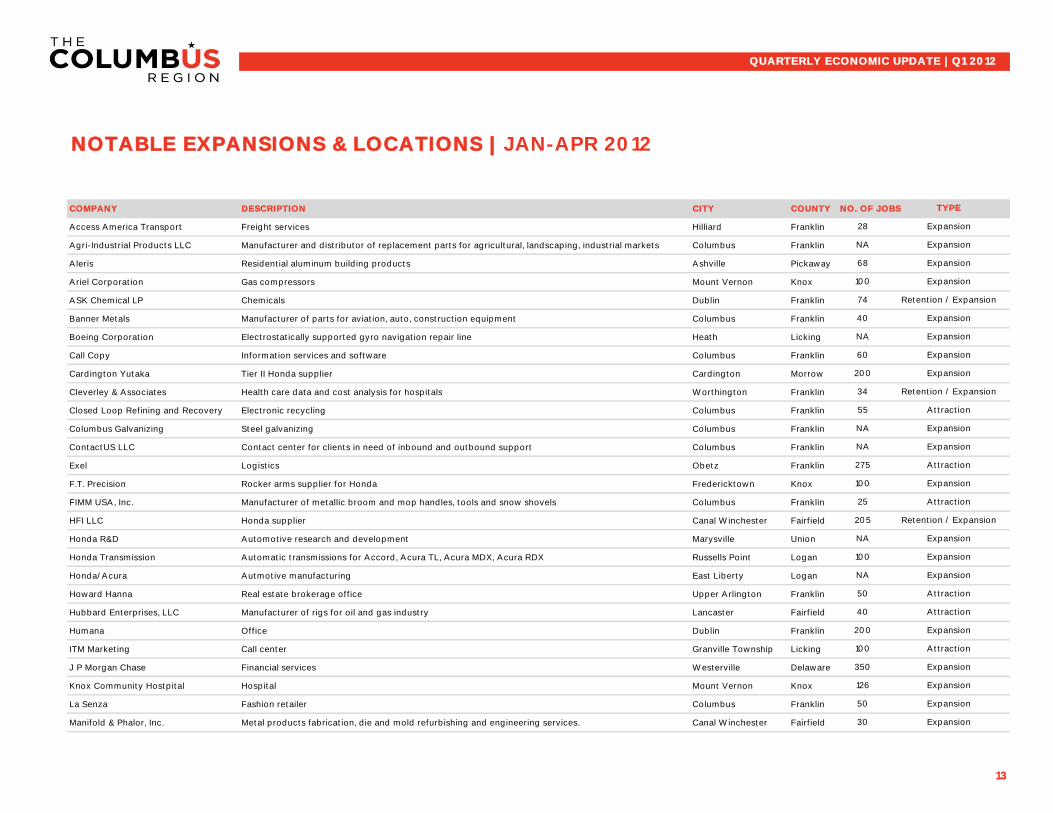

COMPANY DESCRIPTION CITY COUNTY NO. OF JOBS

Access America Transport Freight services Hilliard Franklin

Agri-Industrial Products LLC Manufacturer and distributor of replacement parts for agricultural, landscaping, industrial markets Columbus Franklin

Aleris Residential aluminum building products Ashville Pickaway

Ariel Corporation Gas compressors Mount Vernon Knox

ASK Chemical LP Chemicals Dublin Franklin

Banner Metals Manufacturer of parts for aviation, auto, construction equipment Columbus Franklin

Boeing Corporation Electrostatically supported gyro navigation repair line Heath Licking

Call Copy Information services and software Columbus Franklin

Cardington Yutaka Tier II Honda supplier Cardington Morrow

Cleverley & Associates Health care data and cost analysis for hospitals Worthington Franklin

Closed Loop Refining and Recovery Electronic recycling Columbus Franklin

Columbus Galvanizing Steel galvanizing Columbus Franklin

ContactUS LLC Contact center for clients in need of inbound and outbound support Columbus Franklin

Exel Logistics Obetz Franklin

F.T. Precision Rocker arms supplier for Honda Fredericktown Knox

FIMM USA, Inc. Manufacturer of metallic broom and mop handles, tools and snow shovels Columbus Franklin

HFI LLC Honda supplier Canal Winchester Fairfield

Honda R&D Automotive research and development Marysville Union

Honda Transmission Automatic transmissions for Accord, Acura TL, Acura MDX, Acura RDX Russells Point Logan

Honda/Acura Autmotive manufacturing East Liberty Logan

Howard Hanna Real estate brokerage office Upper Arlington Franklin

Hubbard Enterprises, LLC Manufacturer of rigs for oil and gas industry Lancaster Fairfield

Humana Office Dublin Franklin

ITM Marketing Call center Granville Township Licking

J P Morgan Chase Financial services Westerville Delaware

Knox Community Hostpital Hospital Mount Vernon Knox

La Senza Fashion retailer Columbus Franklin

Manifold & Phalor, Inc. Metal products fabrication, die and mold refurbishing and engineering services. Canal Winchester Fairfield

13

NA Expansion

TYPE

126 Expansion

50 Expansion

30 Expansion

NA Expansion

100 Attraction

100 Expansion

350 Expansion

200 Expansion

100 Expansion

40 Attraction

205 Retention / Expansion

NA Expansion

275 Attraction

NA Expansion

Expansion

55 Attraction

60 Expansion

50 Attraction

25 Attraction

100 Expansion

74 Retention / Expansion

Expansion28

NA Expansion

QUARTERLY ECONOMIC UPDATE | Q1 2012

NOTABLE EXPANSIONS & LOCATIONS | JAN-APR 2012

68 Expansion

200 Expansion

40 Expansion

34 Retention / Expansion

NA

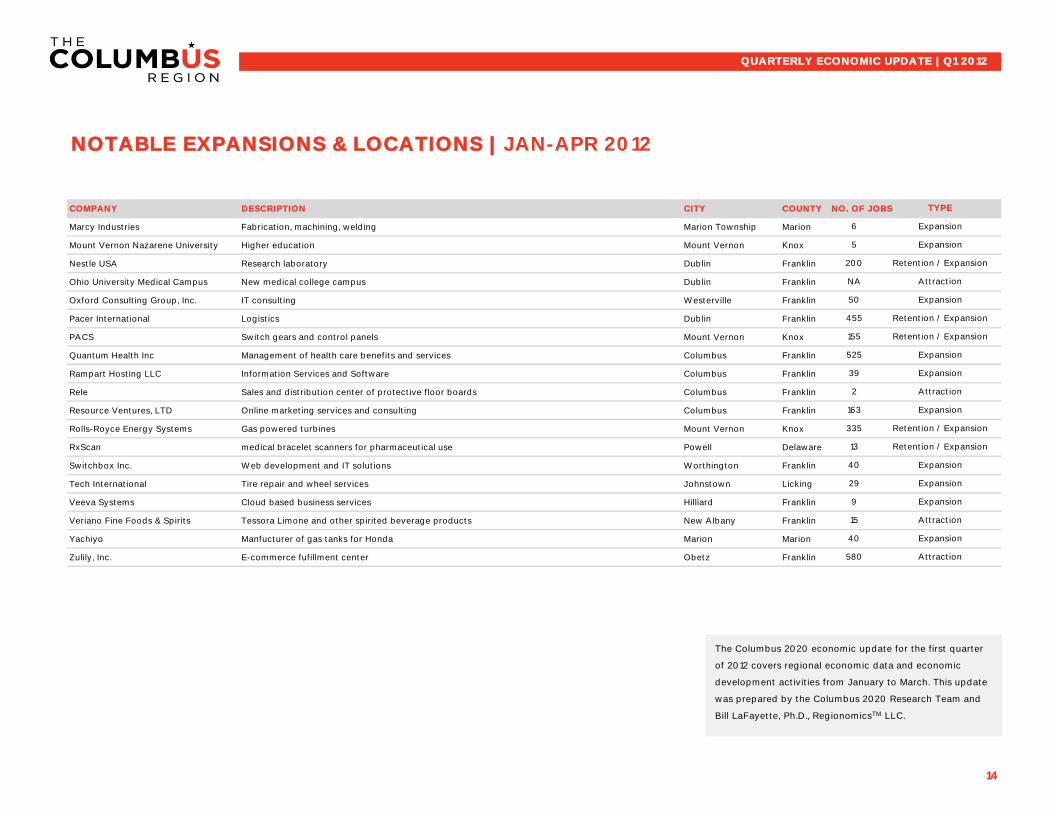

COMPANY DESCRIPTION CITY COUNTY NO. OF JOBS

Marcy Industries Fabrication, machining, welding Marion Township Marion

Mount Vernon Nazarene University Higher education Mount Vernon Knox

Nestle USA Research laboratory Dublin Franklin

Ohio University Medical Campus New medical college campus Dublin Franklin

Oxford Consulting Group, Inc. IT consulting Westerville Franklin

Pacer International Logistics Dublin Franklin

PACS Switch gears and control panels Mount Vernon Knox

Quantum Health Inc Management of health care benefits and services Columbus Franklin

Rampart Hosting LLC Information Services and Software Columbus Franklin

Rele Sales and distribution center of protective floor boards Columbus Franklin

Resource Ventures, LTD Online marketing services and consulting Columbus Franklin

Rolls-Royce Energy Systems Gas powered turbines Mount Vernon Knox

RxScan medical bracelet scanners for pharmaceutical use Powell Delaware

Switchbox Inc. Web development and IT solutions Worthington Franklin

Tech International Tire repair and wheel services Johnstown Licking

Veeva Systems Cloud based business services Hilliard Franklin

Veriano Fine Foods & Spirits Tessora Limone and other spirited beverage products New Albany Franklin

Yachiyo Manfucturer of gas tanks for Honda Marion Marion

Zulily, Inc. E-commerce fufillment center Obetz Franklin

14

2

455 Retention / Expansion

29 Expansion

40 Expansion

Attraction

580 Attraction

39 Expansion

9 Expansion

Attraction

163

TYPE

5 Expansion

NA

200 Retention / Expansion

Attraction

525

50 Expansion

40 Expansion

335 Retention / Expansion

13 Retention / Expansion

15

Expansion

155 Retention / Expansion

Expansion

6 Expansion

QUARTERLY ECONOMIC UPDATE | Q1 2012

NOTABLE EXPANSIONS & LOCATIONS | JAN-APR 2012

The Columbus 2020 economic update for the first quarter

of 2012 covers regional economic data and economic

development activities from January to March. This update

was prepared by the Columbus 2020 Research Team and

Bill LaFayette, Ph.D., RegionomicsTM LLC.