2005 full year results roadshow - Home | Nestlé Global · 5 2005 full year roadshow –...

41

2005 full year results roadshow 2005 full year roadshow – February/March 2006

Transcript of 2005 full year results roadshow - Home | Nestlé Global · 5 2005 full year roadshow –...

Name of chairman

2005 full year results roadshow

2005 full year roadshow – February/March 2006

Name of chairman2005 full year roadshow – February/March 20062

Disclaimer

This presentation contains forward looking statements which reflect Management’s current views and estimates. The forward looking statements involve certain risks and uncertainties that could cause actual results to differ materially from those contained in the forward looking statements. Potential risks and uncertainties include such factors as general economic conditions, foreign exchange fluctuations, competitive product and pricing pressures and regulatory developments.

Name of chairman2005 full year roadshow – February/March 20063

Restatement of 2004 results

• 2004 results have been restated following the first application of IFRS 2 share-based payment and the discontinued operation resulting from the announcement in December 2005 for the chilled dairy activities in Europe, where applicable.

• 2005 Full Year Organic Growth restated for chilled dairy: impact about 30 bps.

Name of chairman2005 full year roadshow – February/March 20064

Agenda

2005 key messages

EBITA evolution

A portfolio of strong brands

Nutrition, Health & Wellness –driving growth & profitability

Benefits of scale

Strategic review 2005/6

Corporate governance

Outlook

Name of chairman2005 full year roadshow – February/March 20065

2005: Delivering The Nestle Model:Improvement in key performance measures

Strong organic growth both F&B and Pharma: 6.2%

EBITA margin up 20bps to 12.9%; up CHF 1 Billion

Improvement in Return on Invested Capital: +50bps

Underlying EPS up 12.9%; dividend CHF 9, up 12.5%

Strong cash flow – 1st buy-back complete; 2nd begun

CHF 4.5 Billion returned to shareholders: up 59% vs 04

Group transformation on track – Nutrition, Health, Wellness, GLOBE, European Chilled Dairy

Name of chairman2005 full year roadshow – February/March 20066

MarketMix+ 30

Positive evolution of EBITA margin

2004

Operationalactivities

- 20

12.7

12.8Currencies

+ 10

12.8

13.1

12.9

Share-basedpayments

12.7

Portfoliooptimisation

+ 10- 10

2005

Name of chairman2005 full year roadshow – February/March 20067

EBITA influencers: 12.7% to 12.9% = + 20 bps

Positive• Efficiencies & growth +160• Mkt mix, inc Alcon +30• Portfolio

optimisation +10• Currencies +10

Total positive +210

Negative• Input costs, net of

pricing -155• One-offs: China,

Russian & UK confectionery -25

• Share-based payments -10

Total negative -190

Improvement +20bps

Name of chairman2005 full year roadshow – February/March 20068

Brands

A portfolio of strong brands:The foundation for value creation

Name of chairman2005 full year roadshow – February/March 20069

21 brands with sales over 1 billion Swiss Franc

Beverages Chocolate, confectionery and

biscuits

PetCare

Water

Prepared dishes and cooking aids

Name of chairman2005 full year roadshow – February/March 200610

21 brands with sales over 1 billion Swiss Franc

Milk products BABs

Ice cream

Pharma

Nutrition In Nutrition, Nestlé qualifies as a CHF 1 billion brand in both the Infant Nutrition and Baby Food categories. Branded Active Benefits are added to products to address a specific need state. The sales of products incorporating Prebio1 exceed CHF 1 billion.

Name of chairman2005 full year roadshow – February/March 200611

Bigger brands grow faster (Organic growth)

EUROPE AMERICAS AOA

n/a

+ 52.8

+ 5.0

+ 5.4

+ 0.2

+26.0

n/a

n/a

+ 6.3

+ 12.2

+ 6.6

+ 51.9

+ 7.8

+ 7.8

+ 11.3

n/a + 10.6 n/a

Name of chairman2005 full year roadshow – February/March 200612

Share gains in key categories

3.55.6

8.6

11.7

2.0

16.0

1.83.1

PetCareCAGR

Value (%)02-05

Ice CreamCAGR

Value (%)01-05

Soluble CoffeeCAGR (%)

95-05

WatersCAGR

Volume (%)98-05

Market

Nestlé

Name of chairman2005 full year roadshow – February/March 200613

The Transformation toNutrition, Health & Wellness

Driving growth & profitability

Name of chairman2005 full year roadshow – February/March 200614

BAB's: adding relevant nutrition, health & wellness to strong brands in a proprietary way

Vitality / Protection Immunity & Protection

Intestinal Health

Heart Health

Building StrongerBones

Long-Lasting Energy

Growth &Development

Feeling Good,& It Shows

Long-LastingAlertness

"Refuelling"Growth

Active CholesterolControl

Helps Keep Calciumin your Bones

R

EasyDigestion

Energy Release

Name of chairman2005 full year roadshow – February/March 200615

BAB's on increasing number of products

Name of chairman2005 full year roadshow – February/March 200616

0.5

1.0

1.5

2.0

2.5

3.0

98 99 00 01 02 03 04

Sal

es (

CH

F B

illion

s )

05

Accelerating sales of Branded Active Benefits

1.2

1.8

GLO

BE

GLO

BE

2.5

2.9

0.60.5

0.4

Branded Active Ingredients Branded Active Benefits

0.2

Name of chairman2005 full year roadshow – February/March 200617

Driving growth and margin through BAB's

Nesvita "Pro-Heart" with Acticol• With BAB to reduce cholesterol • 17% price premium to average

Nesvita "Pro-Digestion" with Actifibras• With BAB to smoothen digestion• 19% price premium to average

• Nestlé share in '05 grew from 33% to 37%• Roll out in 6 more markets in 2006

Adult milk segment achieved 23% Organic Growth

Name of chairman2005 full year roadshow – February/March 200618

Nutrition driving growth

• Nutrition sales* increased by 7.6%• Products with 60/40+ grow 15% faster than

Group• Sales of products with branded active benefits

increased by 20%

*Excluding 2005 product exchange. All numbers 2005

Name of chairman2005 full year roadshow – February/March 200619

F&B average

Portfolio mix improving

-3.0

0.0

3.0

6.0

9.0

12.0

15.0

-3.0 0.0 3.0 6.0 9.0 12.0

Organic Growth

RIG

Germany

France

GB Region

NPPE

Brazil

USA

NPP NA

Mexico

Waters

Dreyer's

% China

%

Name of chairman2005 full year roadshow – February/March 200620

Scale becoming a competitive advantage

• GLOBE roll-out accelerating75,000+ system users; 300+ factories; 300+ distribution centres; 200+ sales offices

• 80% of F&B using GLOBE systems by end 2006• Shared service centres operational in all Zones• Selective outsourcing started• Efficiency programmes deliver CHF 1.2 billion in 2005• Innovation Acceleration Teams & Clusters

Name of chairman2005 full year roadshow – February/March 200621

51.8% 51.2% 50.1%48.1%

44.5%43.2% 42.7% 41.7%

0%

5%

40%

45%

50%

55%

COGS in % of NPS CHF

0.6 bio Cumulative cost improvements

46.8%

CHF 1.3 bio CHF

2.2 bio CHF 3.1 bio CHF

4.0 bio CHF 5.2 bio CHF

6.4 bio CHF 7.6 bio

41.7%

CHF 8.7 bio

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Short term cost pressure; longer term efficiencies

Efficient operations driving down COGS

Name of chairman2005 full year roadshow – February/March 200622

Bigger innovations, rolled out faster

• NAN HA going global in Infant nutrition• Beneful going pan-European• Nescafé mixes launches going global• Nestlé Ideal rolling out across emerging markets

Name of chairman2005 full year roadshow – February/March 200623

Going global in Infant Nutrition

Premium Infant Formula

• Marketed under premium brands Nan, Nidina, Nidal or Beba

• Clinically proven allergy and/or diarrhoea preventive

• The roll-out is global & will be in most markets during H1/2006

Generating double digit growth in most markets

Name of chairman2005 full year roadshow – February/March 200624

Going pan-European with Beneful

Beneful – launched 2001 in US• Developed to various need states in US:

Healthy Radiance, Healthy Growth, etc• US sales grew over 35%; market share increased• Roll-out in Europe started in 2004

Brand sales over CHF 400 million

Name of chairman2005 full year roadshow – February/March 200625

Turkey: launch of Nescafé 3-in-1• Purchasable individually – affordable• Soluble coffee growth of 32%, Mixes 79%

Australia: launch of Nescafé Café Inspired• From 15% to over 50% share in 2.5 yrs• Total Nescafé growth of 6.3%, Mixes 85%

Nescafé global growth +6.7%; mixes +17.6%

Nescafé mixes go global: increasing coffee consumption among younger consumers

Name of chairman2005 full year roadshow – February/March 200626

Nestlé Ideal rolling-out across emerging markets: responding to milk cost crisis for low income families

Milk costs rise significantly – pricing it out of reach of low income families in Latin America – risk of malnutrition in children

25% growth in affordable milks in Latin America – rolling out in AOA as well

Solution: Nestlé Ideal, engineered to a low price but with enhanced nutritional benefits: iron, calcium, vitamins A, C & D

Name of chairman2005 full year roadshow – February/March 200627

1. Long-Term Organic Growth Target 5 - 6%

Resulting in an industry outperforming, long-term total shareholder return

1998 2000 2002 2004 2006 2008 2010

EBITA Margin

1998 2000 2002 2004 2006 2008 20101998 2000 2002 2004 2006 2008 2010

2. Continued year after year improvement of EBITA margin

3. Capital efficiency / Business ROIC

The Nestlé Model

Name of chairman2005 full year roadshow – February/March 200628

• Nestlé Nutrition & steps towards a wellness future• European Chilled Dairy• Nestlé FoodServices• Corporate governance• Outlook

Strategic overview

Name of chairman2005 full year roadshow – February/March 200629

The transformational opportunity

Strategic• From transforming

commodities to added value food products

• From added value to Health, Nutrition & Wellness

Operational• Creating an agile fleet of

businesses/markets• With increased focus on

demand generation • And an efficient support

structure• Resolving under-performers

Name of chairman2005 full year roadshow – February/March 200630

Nestlé Nutrition & steps towards a wellness future

Nestlé Nutrition• Now stand alone & reporting separately• Infant, Healthcare and Performance Nutrition

•

• Targets raised for growth and profitability

Name of chairman2005 full year roadshow – February/March 200631

European Chilled Dairy

• To grow Nestlé's brand presence in Chilled Dairy Müller in Germany, Emmi in Switzerland, Lactalis in Europe

• To make Chilled Dairy as good a business for our shareholders as it is for our consumers

The objective – a creative solution

The challenge• Private label eroding branded

volumes and NCDE market shares

• Chilled Dairy production overcapacity eroding margins

Name of chairman2005 full year roadshow – February/March 200632

JV can leverage

expertise of EUR 6.0 Bio, multi-category

Chilled Business

A base for renewed growth and profitability

Brands & R&D

Brands & R&D

Marketing Expertise

Marketing Expertise

Sales EUR 1.2 Bio

Sales EUR 1.2 Bio

Lactalis Nestlé Venture

Nestlé Lactalis

Supply Chain expertise

Supply Chain expertise

Sales EUR 0.3 Bio

Sales EUR 0.3 Bio

Growth & ProfitabilityGrowth & Profitability

A healthy base for renewed growth and profitability

Immediate low risk, stable income stream for Nestlé without capital allocations

Name of chairman2005 full year roadshow – February/March 200633

The attractiveness of Food ServiceEstimated Global

Sales (CHF bio. 2004)

4.0

3.7

1.9

3.7

6.5

≅3% of OOH Global

Manufacturer Market

• Big and growing opportunity

• Relevant market CHF 400 bio

• Consumer trends drive growth

• Customer consolidation

CHF 2 trillion global consumer spend5-7% growth in major operator segments

80% in Food, 20% in Beverages

50% of US consumer F&B spend is out of home

Common menus and processes drive manufacturer relevant customised solutions

Total = 19.8

Name of chairman2005 full year roadshow – February/March 200634

Five Strategic Business Pillars

• Improve and grow the standard ingredient business

Global Beverage Regional Food

Standard

• CHF 230 bn• 0-3% growth• Average EBITA

StandardReady-to-Serve

• CHF 30 bn• 0-3% growth• High EBITA

Proprietary Solutions

Customized

• CHF 25 bn• 5-10% growth• High EBITA

• Further develop the value added solutions business

• CHF 80 bn• High growth (5-7%)• High EBITA

• ~CHF 15 bn• 4-6% growth• High EBITA

Name of chairman2005 full year roadshow – February/March 200635

iStandard: Build on existing ingredient businesses; Nescafé, Chef, Maggi, etc.

iSolutions: Roll-out of beverages & customized food solutions to major customers

iRoute to Market a critical service component, to be rolled-out market by market

iMust win markets – North America, France, Germany, UK, Japan, Oceania; growth markets e.g. China, ASEAN, India, Brazil, Mexico

iStrategic Business Division reporting to CEO

Strategy

Name of chairman2005 full year roadshow – February/March 200636

Corporate governance

Mandate to facilitate modernisation of articles

• Existing articles relate to out-dated legal context

• "Dispos" currently render major change impossible

• Shareholder survey confirmed desire for change

• Shareholder mandate will lay foundation for future modernisation with shareholder approval, despite "dispos"

• The Board believes this initiative is in shareholders' best interests

AGM 2005: a commitment to shareholdersAGM 2006: a call for action to shareholders

Name of chairman2005 full year roadshow – February/March 200637

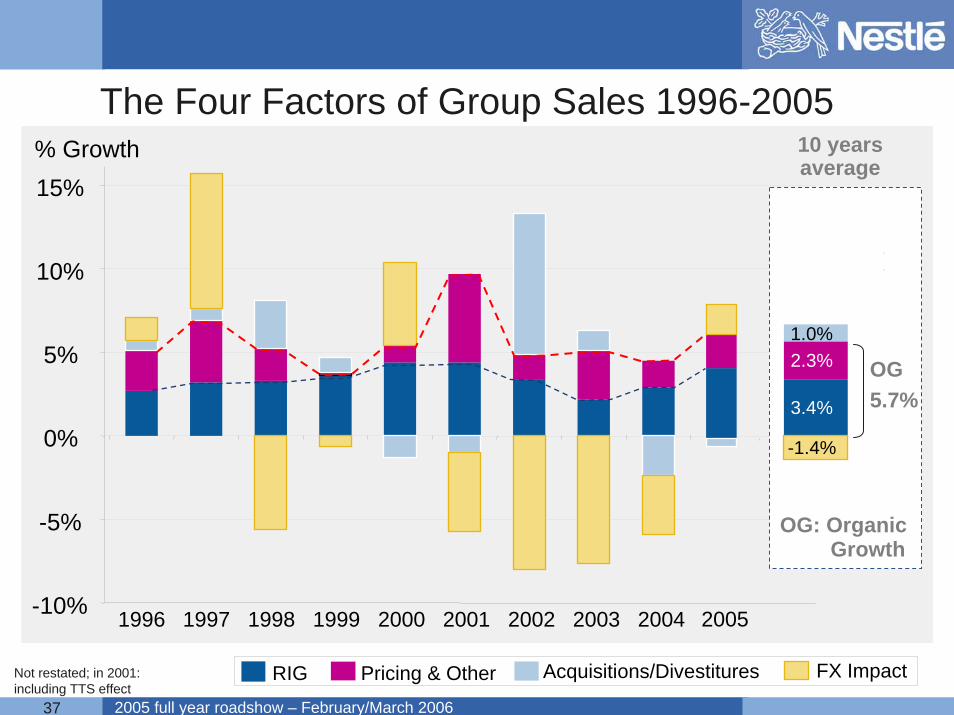

-10%

-5%

0%

5%

10%

15%% Growth

20051996 1997 1998 1999 2000 2001 2002 2003 2004

RIG Pricing & Other Acquisitions/Divestitures FX ImpactNot restated; in 2001: including TTS effect

10 yearsaverage

OG5.7%

OG: OrganicGrowth

3.4%

2.3%

-1.4%

1.0%

The Four Factors of Group Sales 1996-2005

Name of chairman2005 full year roadshow – February/March 200638

Group EBITA Margin over last 10 years

10.2% 10.3% 10.3%

11.8% 11.8%12.3% 12.5%

12.6%12.9%

11.1%

01'0002'0003'0004'0005'0006'0007'0008'0009'000

10'00011'00012'00013'00014'000

mn

CH

F

9.0%

9.5%

10.0%

10.5%

11.0%

11.5%

12.0%

12.5%

13.0%

13.5%

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005

Nestlé Group EBITA and EBITA Margin from 1996 to 2005 % of Sales

EBITA(mn CHF)

Not restated; New NPS definition in 2001

Name of chairman2005 full year roadshow – February/March 200639

Actively managed capital structure benefits shareholders: cash returns

* 2006 assumes completion of 2nd buy-back programme and payment of proposed CHF 9 dividend

2.8

4.5

6.2

0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2004 2005 2006*

1.4

3.1

2.6

3.6

Dividend

Share buy-back

+59%

+39%

CHFbn

Name of chairman2005 full year roadshow – February/March 200640

Outlook

The Nestlé Model reconfirmed for 2006:5-6% organic growth, plus

consistent margin improvement

Name of chairman

2005 full year results roadshow

2005 full year roadshow – February/March 2006