1H 2015 Strategy & Results Presentation -...

25

1 1H 2015 Strategy & Results Presentation August 31, 2015

Transcript of 1H 2015 Strategy & Results Presentation -...

1

1H 2015 Strategy & Results Presentation

August 31, 2015

2

This document has been prepared by Iliad S.A. (the "Company”) and is being furnished to you solely for your information and personal use.

This presentation includes only summary information and does not purport to be comprehensive.

The information contained in this presentation has not been subject to independent verification. No representation, warranty or undertaking, express or implied, is made as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or opinions contained herein.

None of Iliad S.A., its affiliates or its advisors, nor any representatives of such persons, shall have any liability whatsoever (in negligence or otherwise) for any loss arising from any use of this document or its contents or otherwise arising in connection with this document or any other information or material discussed.

This presentation contains forward-looking statements relating to the business, financial performance and results of Iliad S.A. These statements are based on current beliefs, expectations or assumptions and involve unknown risks and uncertainties that could cause actual results, performance or events to differ materially from those described in such statements. Factors that could cause such differences in actual results, performance or events include changes in demand

and technology, as well as the ability of Iliad S.A. to effectively implement its strategy.

Any forward-looking statements contained in this presentation speak only as of the date of this presentation. Iliad S.A. expressly disclaims any obligation or undertaking to update or revise any forward-looking statements contained in this presentation to reflect any change in events, conditions, assumptions or circumstances on which any such statements are based unless so required by applicable law.

Disclaimer

3

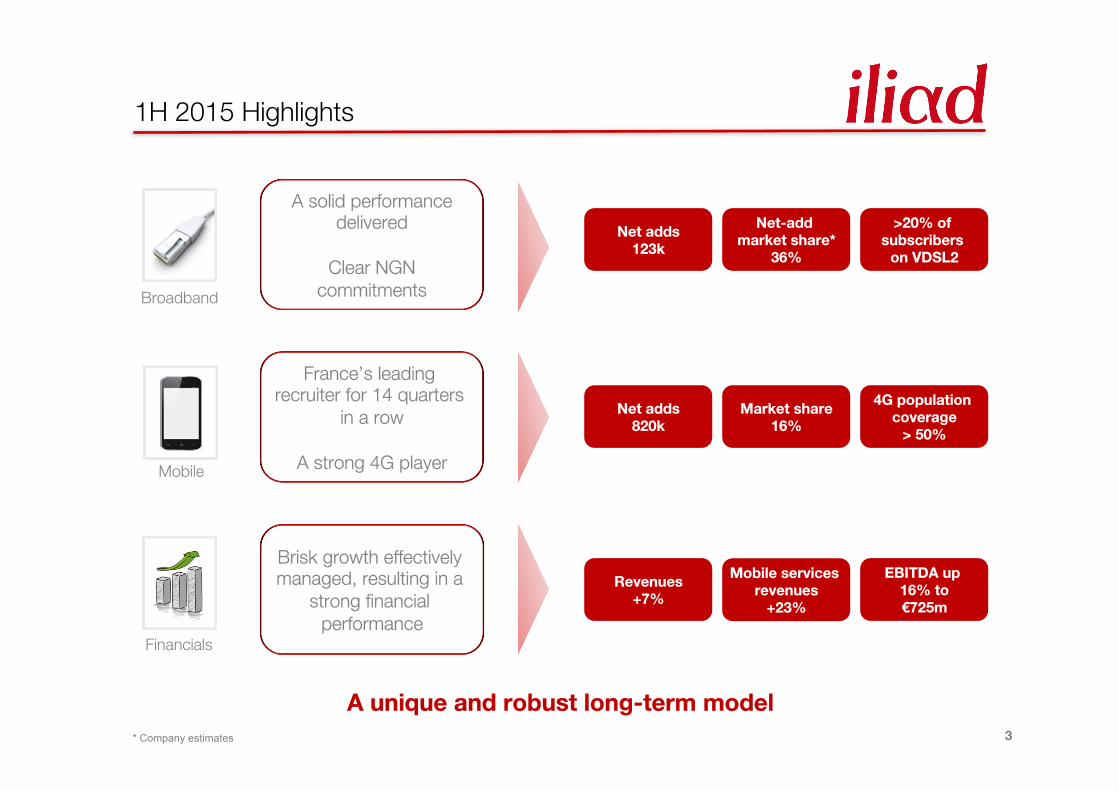

1H 2015 Highlights

A unique and robust long-term model

Broadband

Mobile

Financials

A solid performance delivered

Clear NGN

commitments

France’s leading recruiter for 14 quarters

in a row

A strong 4G player

Brisk growth effectively managed, resulting in a

strong financial performance

Net adds 123k

Net-add market share*

36%

Net adds 820k

Market share 16%

4G population coverage

> 50%

Revenues +7%

EBITDA up 16% to €725m

Mobile services revenues

+23%

>20% of subscribers

on VDSL2

* Company estimates

4

June 2014

Subscriber KPIs

- Broadband 5,735,000 5,868,000 5,991,000

- Mobile 9,095,000 10,105,000 10,925,000

Total number of subscribers 14,830,000 15,973,000 16,916,000

Other Broadband KPIs (end of period)

Broadband ARPU (incl. promos) €35.80 €35.10 €34.50

Freebox Revolution ARPU (excl. promos) > €38.00 > €38.00 > €38.00

Another Strong Commercial Performance

Dec. 2014 June 2015

5

Broadband Business

6

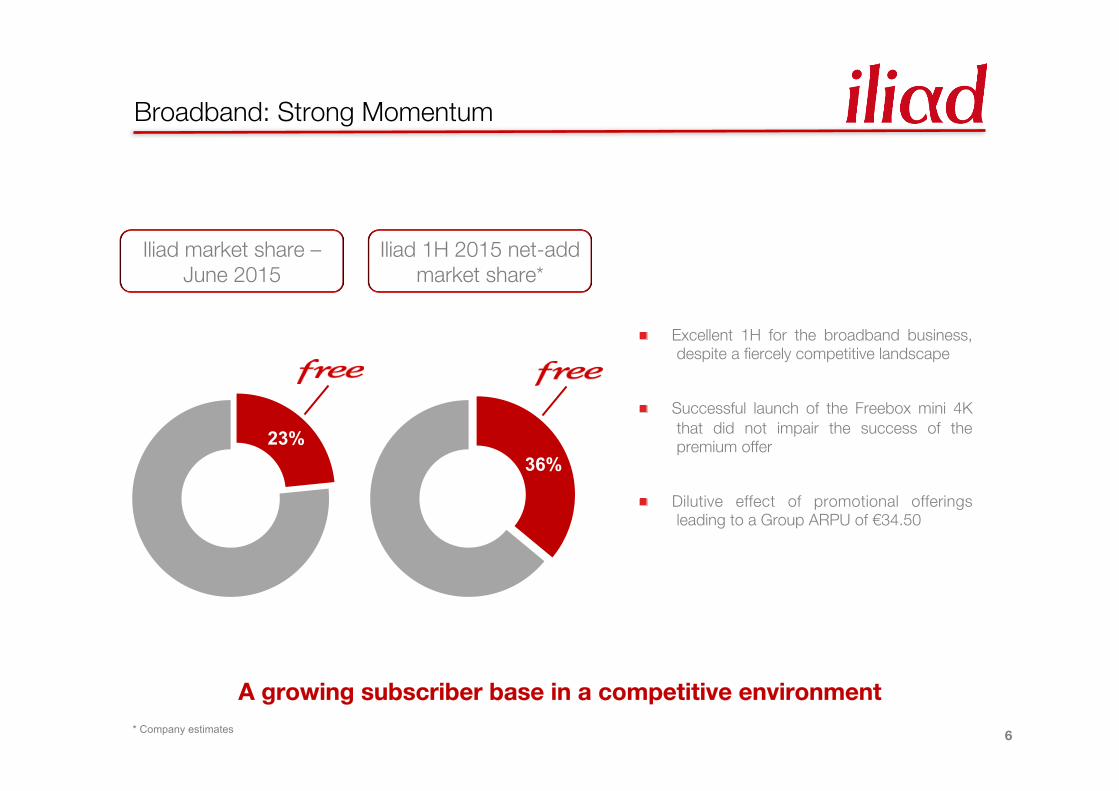

Excellent 1H for the broadband business, despite a fiercely competitive landscape

Successful launch of the Freebox mini 4K that did not impair the success of the premium offer

Dilutive effect of promotional offerings leading to a Group ARPU of €34.50

Iliad market share – June 2015

Iliad 1H 2015 net-add market share*

23% 36%

Broadband: Strong Momentum

A growing subscriber base in a competitive environment

* Company estimates

7

Quality/Customer Experience

Ever more attentive to our subscribers

Ongoing investment in customer care

400 jobs created in 1H 2015 in France

Some 6,500 people dedicated to assistance services

A streamlined nationwide distribution network

48 Free Centers – covering major French cities

Some 1,600 SIM card dispensers set up in stores across France –

available in the Maison de la Presse and Mag Presse store networks

and Free Centers

Innovative services

Face-to-Free service: a customized assistance service via webcam

enhancing the customer experience and simplifying communication

with the Freehelper

Special assistance available for the hard of hearing

8

Freebox mini 4K – The Best Entry-price Product

An original offer to replace the Freebox Crystal for €29.99/month

ADSL2+/VDSL2/FTTH – WiFi up to 450 Mbps

Compact format: 11 x 15 x 3.5 cm

4K – Ultra High Definition Player

Powered by Android TVTM - GoogleTM Cast ready

Calls to landlines in 106 countries

More than 200 TV channels included, o/w 50 HD channels

Freebox Replay

Voice search remote control

Hotline & Home technical assistance

Multi TV offer

Option of receiving TV services on a second TV from

a Freebox Revolution for €1.99/month

A successful replacement of the entry-price product

9

Straightforward Offers and a Rational Market Approach

2 straightforward offers available in c.90% of France – compatible with all technologies

ADSL2+, VDSL2 and FTTH up to 1Gbps*.

Differentiating through innovation & simplicity:

Freebox mini 4K – The most innovative entry-price product

Ø First triple-play box in the world with 4K and Android TVTM

Ø Only €29.99/month

A well-established maverick positioning in a highly competitive market

Freebox Revolution - Leading innovation almost 5 years after its launch

Ø Most advanced triple-play box including Blu-rayTM, NAS server

with a hard drive, FreePlugs, gamepad, calls to mobiles, etc.

A selective and profitable promotion policy to attract price-sensitive subscribers

* Available only on bridge mode.

10

ADSL 2+: Leading operator in terms of unbundling footprint

More than 7,500 unbundled Central Offices

Unbundling footprint covering of 87% of the French population

More than 1,500 new unbundled Central Offices over the last 12 months

Pushing the Next-Generation Network Experience

* Available for subscribers who have a Freebox Revolution or a Freebox mini 4K and an eligible telephone line

Providing better bandwidth for subscribers

Ø More than 20% of our subscribers now have access to higher Internet speeds

through VDSL2

Ø Higher Internet speeds: 100Mbps* download and 40Mbps* upload

Ø All of subscriber connection nodes now have VDSL2 equipment

Increasing our FTTH commitments

Ø Dense areas: 230 optical nodes with a potential coverage of more than 3.4m FTTH plugs –

migration path improving

Ø Non-dense areas: Stepping up co-financing arrangements with Orange – agreement to

cover 4.5m homes – 700k plugs available as of June 2015

Ø Ready to accelerate subscriber migrations

Ultra Fast Broadband

11

Mobile Business

12

3,600

5,205

6,795

8,040

9,095

10,10510,925

1H 2012 2H 2012 1H 2013 2H 2013 1H 2014 2H 2014 1H 2015

16%

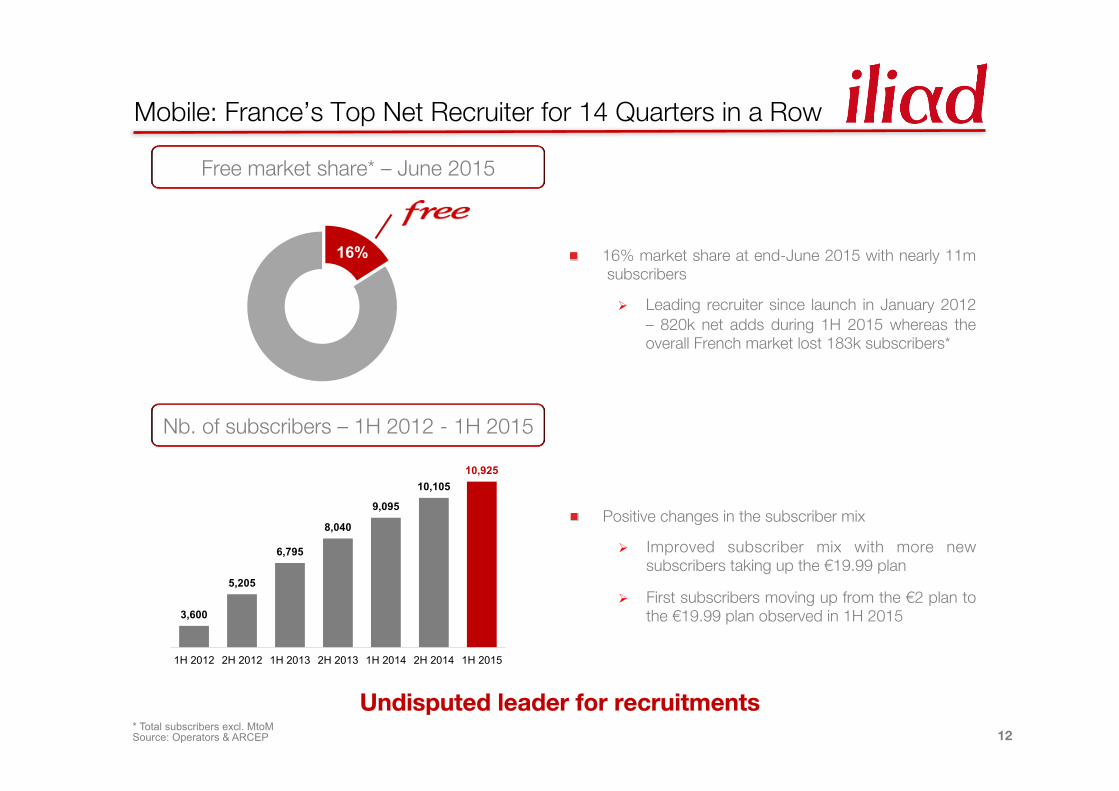

Mobile: France’s Top Net Recruiter for 14 Quarters in a Row

Undisputed leader for recruitments * Total subscribers excl. MtoM Source: Operators & ARCEP

Free market share* – June 2015

16% market share at end-June 2015 with nearly 11m subscribers

Ø Leading recruiter since launch in January 2012 – 820k net adds during 1H 2015 whereas the overall French market lost 183k subscribers*

Nb. of subscribers – 1H 2012 - 1H 2015

Positive changes in the subscriber mix

Ø Improved subscriber mix with more new subscribers taking up the €19.99 plan

Ø First subscribers moving up from the €2 plan to the €19.99 plan observed in 1H 2015

13

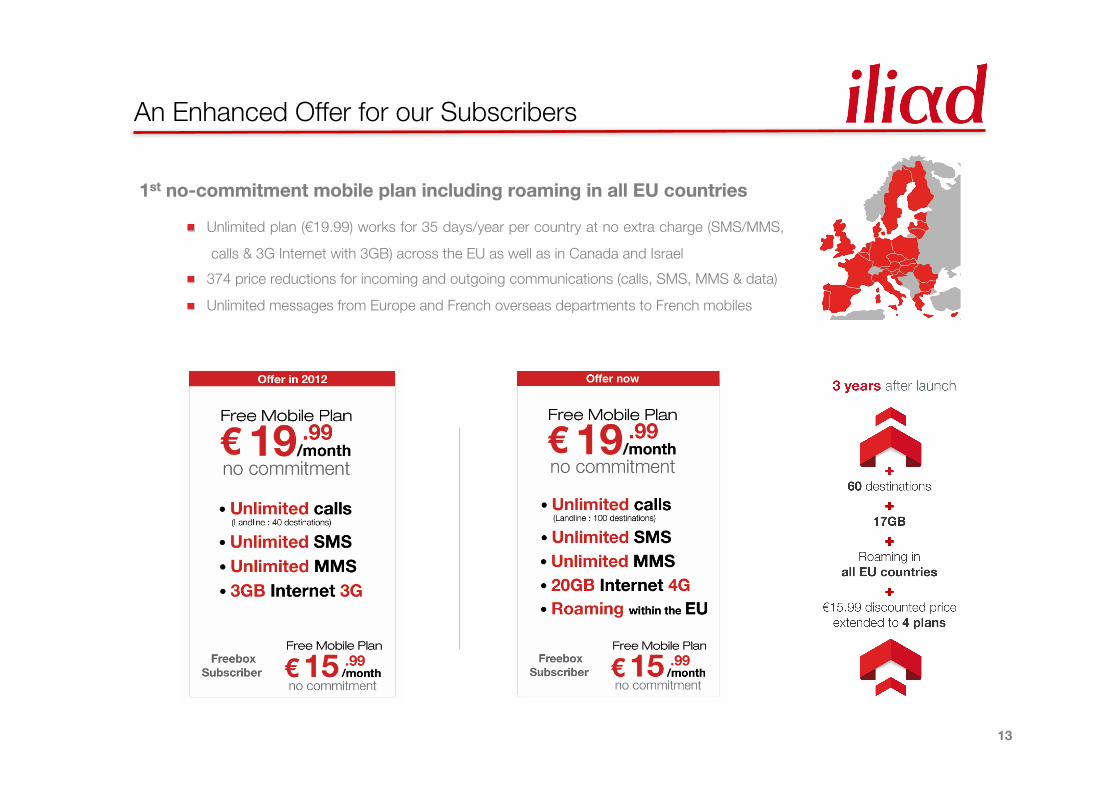

An Enhanced Offer for our Subscribers

1st no-commitment mobile plan including roaming in all EU countries

Unlimited plan (€19.99) works for 35 days/year per country at no extra charge (SMS/MMS,

calls & 3G Internet with 3GB) across the EU as well as in Canada and Israel

374 price reductions for incoming and outgoing communications (calls, SMS, MMS & data)

Unlimited messages from Europe and French overseas departments to French mobiles

14

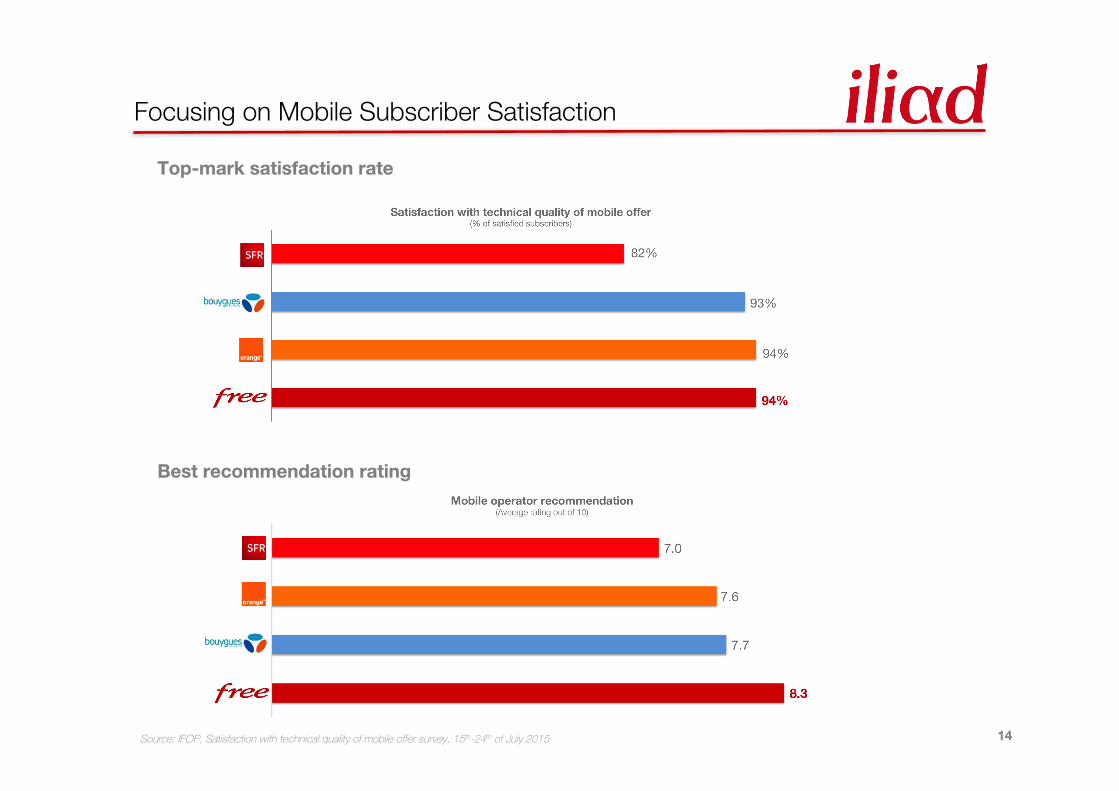

Focusing on Mobile Subscriber Satisfaction

Top-mark satisfaction rate

Best recommendation rating

Source: IFOP, Satisfaction with technical quality of mobile offer survey, 15th-24th of July 2015

15

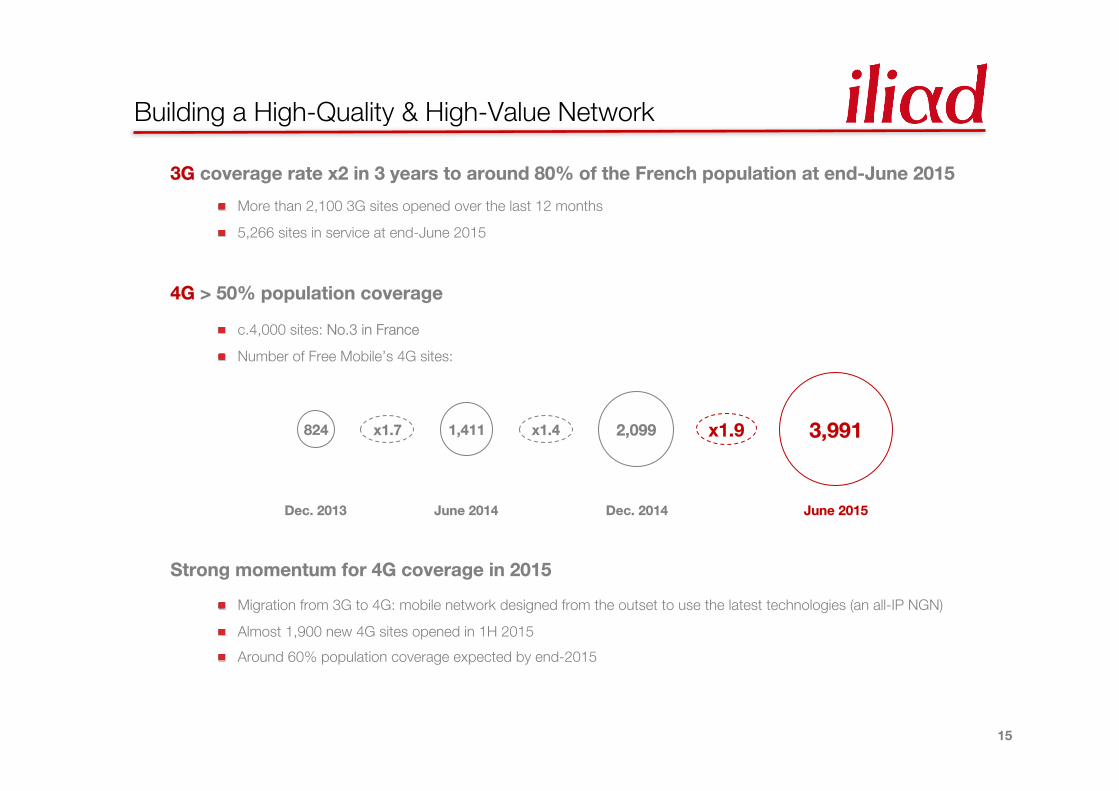

3G coverage rate x2 in 3 years to around 80% of the French population at end-June 2015

More than 2,100 3G sites opened over the last 12 months

5,266 sites in service at end-June 2015

4G > 50% population coverage

c.4,000 sites: No.3 in France

Number of Free Mobile’s 4G sites:

Strong momentum for 4G coverage in 2015

Migration from 3G to 4G: mobile network designed from the outset to use the latest technologies (an all-IP NGN)

Almost 1,900 new 4G sites opened in 1H 2015

Around 60% population coverage expected by end-2015

Building a High-Quality & High-Value Network

824 2,099 3,991

Dec. 2013 Dec. 2014 June 2015

x1.7 x1.9 1,411

June 2014

x1.4

16

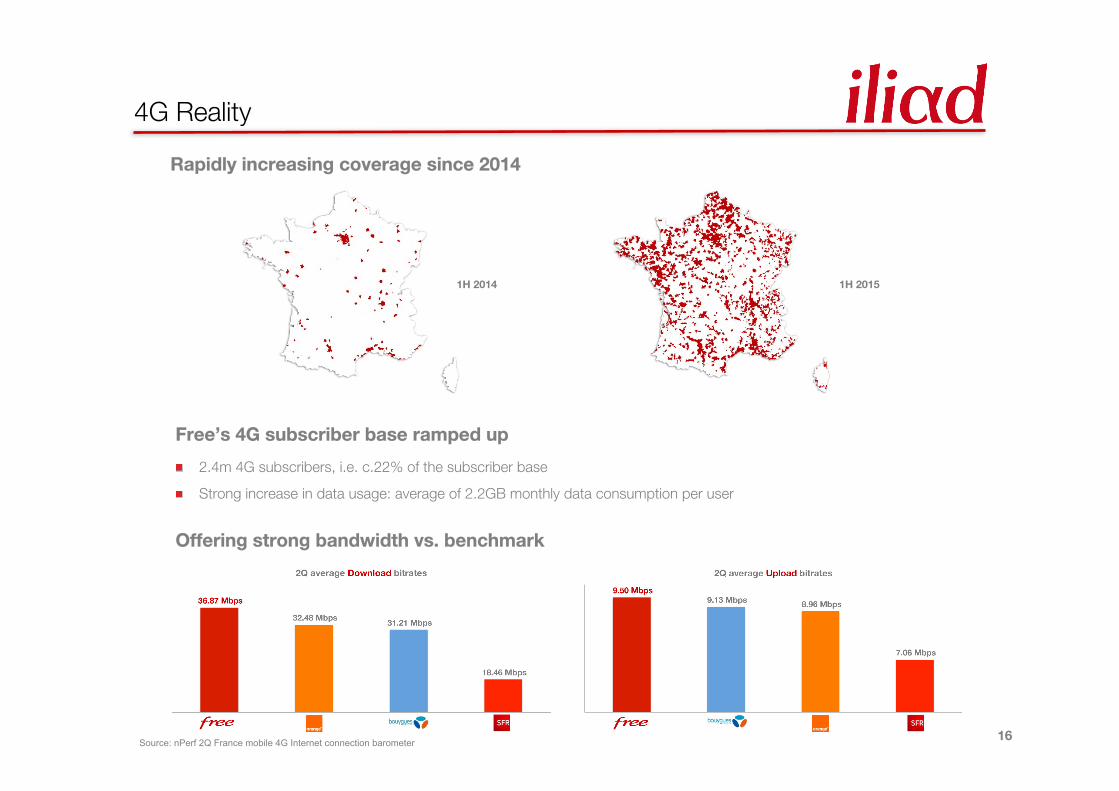

Rapidly increasing coverage since 2014

4G Reality

Free’s 4G subscriber base ramped up

2.4m 4G subscribers, i.e. c.22% of the subscriber base

Strong increase in data usage: average of 2.2GB monthly data consumption per user

Offering strong bandwidth vs. benchmark

Source: nPerf 2Q France mobile 4G Internet connection barometer

1H 2014 1H 2015

17

A balanced and improving portfolio of frequencies

In December 2014 Iliad was granted 5MHz in the 1,800MHz frequency band

From May 2016 the 1,800MHz frequency portfolio should further increase to 15MHz (following the ARCEP decision

on the refarming process on July 30, 2015)

A confirmed interest in the upcoming 700MHz auction

A clear path towards independency

A 3G network covering c.80% of the French population as of end-June and on-track to reach 90% population

coverage by end-2017 – in accordance with the terms of the Group’s license

Discussions under way with Orange (overseen by the regulator) on the gradual phase out of national 3G roaming

A topic that needs to be discussed and assessed in light of:

Ø The RAN-Sharing agreement in force between NC-SFR and Bouygues Telecom

Ø The 4G roaming provided by Bouygues Telecom to NC-SFR

Towards Network Independency

18

Financial Performance

19

Strong Financial Performance

* Excl. Other operating income and expense

Double-digit growth in profitability

Group revenues

€2,160m

+7%

EBITDA

€725m

+16%

EBIT*

€330m

+17%

Profit for the period

€163m

+16%

Cash from operations before tax & WCR

€721m

+17%

20

Group revenues

(€ millions)

Broadband revenues

Revenue Growth on the Back of Solid Fundamentals

Mobile revenues

Another sharp rise in Mobile

revenues, up by 18%

+ 820k new subscribers

+ Higher-value subscriber mix

driving services revenue up

by 23%

7% growth in Group revenues

during 1H 2015 (8% excl.

handsets)

+ High market share gains

+ Mobile: more than 40% of

Group revenues

1H 2014 1H 2015

1,279 1,285

+0.5%

1H 2014 1H 2015

746

880

+18.1%

1H 2014 1H 2015

2,020

2,160

+6.9%

Strong top line growth, with revenues reaching a record high of c.€2.2bn

Ongoing growth for Broadband

activities

+ 123k new subscribers attracted

by the Group’s offers

- Dilutive effect of promotional

offerings & pricing environment

21

Group Profit

(€ millions)

Group EBITDA

Significant Improvement in Profitability

Group EBIT

Robust Group EBITDA and a

wider EBITDA margin (+270 bps)

+ Fast-growing Mobile business

leading to better coverage and a

significant improvement in the

Mobile EBITDA margin

+ FTTH network rollout & scale

effect on fixed costs base for both

Broadband and Mobile

- Dilutive impact of enhanced

commercial offerings

A 17% year-on-year

increase in Group EBIT

+ Driven by EBITDA growth

- Dilutive contribution of Mobile

- Higher D&A due to new assets

(network, 4G license)

A 16% increase

in Group profit

+ In line with Group EBIT

- Negative impact of

increase in corporate

tax rate

1H 2014 1H 2015

624

725

+16.2%

1H 2014 1H 2015

281 330

+17.2%

1H 2014 1H 2015

140 163

-1

30.9%

33.6%

+16.4%

22

Strong Investments Backed by Robust FCF

(€ millions)

Group cash from ops before tax & WCR

Total CAPEX FCF

721

(613)

(80)

Group WCR

Other (interest, non-

rec.)

(48)

(67)

(47)

Operating FCF

675

Taxes

1H 2014 1H 2015

615

721

1H 2013

599 +3%

1H 2012

422 +42%

+17%

Strong growth in Group cash from operations before tax & WCR

23

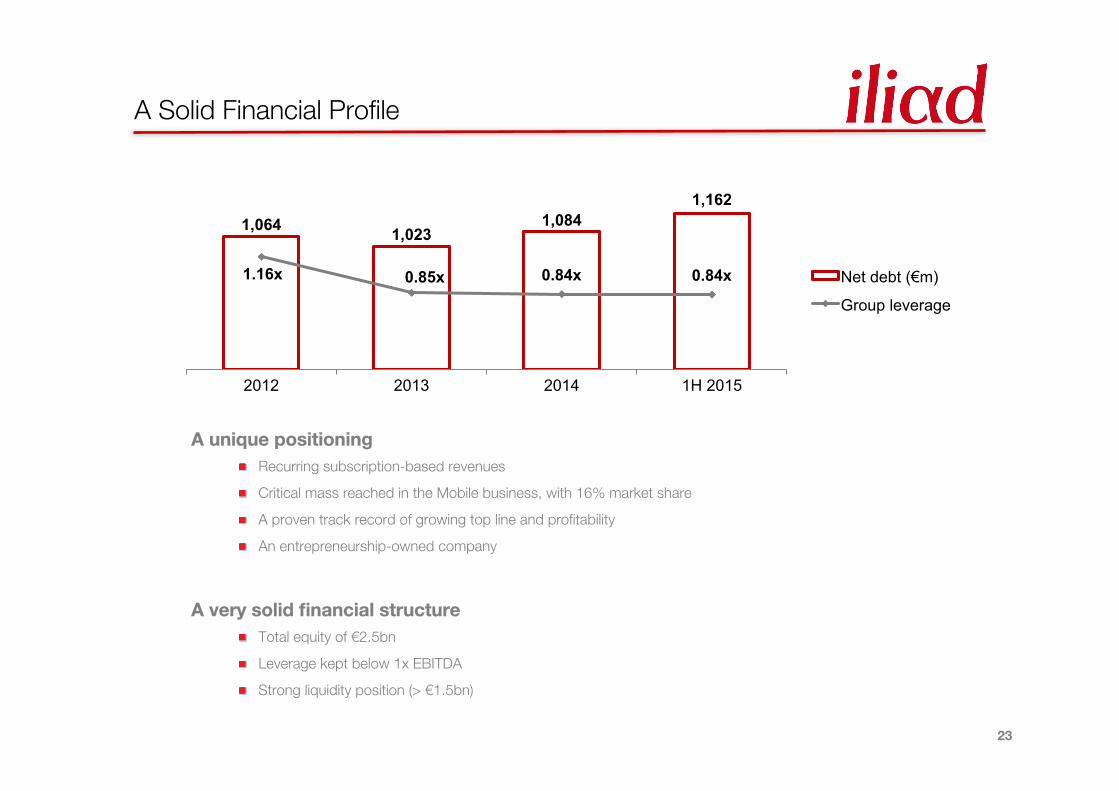

1,064 1,023 1,084

1,162

1.16x 0.85x 0.84x 0.84x

2012 2013 2014 1H 2015

Net debt (€m)

Group leverage

A Solid Financial Profile

A unique positioning

Recurring subscription-based revenues

Critical mass reached in the Mobile business, with 16% market share

A proven track record of growing top line and profitability

An entrepreneurship-owned company

A very solid financial structure

Total equity of €2.5bn

Leverage kept below 1x EBITDA

Strong liquidity position (> €1.5bn)

24

1,2502,519

3,122

5,266

40%

50%

67%

80%

1H 2012 1H 2013 1H 2014 1H 2015

Nb. of 3G sites Mobile coverage (% of population)

3,6006,795

9,09510,9255,147

5,518

5,7355,991

8,747

12,313

14,83016,916

1H 2012 1H 2013 1H 2014 1H 2015

Mobile Broadband

Nb. of Subscribers (‘000s)

417586 624

725

28.9%

32.0%30.9%

33.6%

1H 2012 1H 2013 1H 2014 1H 2015

EBITDA (€m) Margin (%)

Revenues (€m)

320601 746 880

1,130

1,2351,279

1,2851,444

1,8292,020

2,160

1H 2012 1H 2013 1H 2014 1H 2015

Mobile Broadband

Delivering Profitable Growth

CAGR: +24.6% CAGR: +14.4%

* Incl. intersegment revenues

*

* *

*

25

Operational and Financial Outlook

Broadband

Achieve a 25% share of the landline broadband market in the long term

Step up the pace of FTTH rollouts

Mobile

Deploy more than 1,500 sites in 2015

Reach a 4G coverage rate of around 60% of the French population by end-2015, 4 years before our coverage

commitment deadline

Achieve a 25% market share in the long term

Group

Achieve more than 10% growth in consolidated EBITDA in 2015

2H 2015 CAPEX in line with 1H 2015

Achieve consolidated EBITDA margin of over 40% by the end of the decade