19147914 Canara Bank Assignment

45

A BANKING MANAGEMENT REPORT ON CANARA BANK Submitted To: Mr. Ujjal Mehta Faculty: BM Submitted by: Chaudhary Mukesh J. Roll No: 46 Div: A V.M. Patel Institute of Management Ganpat University Kherva. 2009 1

-

Upload

keerthanasubramani -

Category

Documents

-

view

228 -

download

0

Transcript of 19147914 Canara Bank Assignment

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 1/45

A

BANKING MANAGEMENT

REPORT

ON

CANARA BANK

Submitted To:

Mr. Ujjal Mehta

Faculty: BM

Submitted by:

Chaudhary Mukesh J.

Roll No: 46

Div: A

V.M. Patel Institute of Management

Ganpat University

Kherva.

2009

1

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 2/45

History of Banking

The first banks were probably the religious temples of the ancient world, and were probably established sometime during the third millennium B.C. Banks probably predated the invention of money. Deposits initially consisted of grain and later other

goods including cattle, agricultural implements, and eventually precious metals such asgold, in the form of easy-to-carry compressed plates. Temples and palaces were the safest places to store gold as they were constantly attended and well built. As sacred places,temples presented an extra deterrent to would-be thieves. There are extant records of loans from the 18th century BC in Babylon that were made by temple priests/monks tomerchants. By the time of Hammurabi's Code, banking was well enough developed to justify the promulgation of laws governing banking operations.

Ancient Greece holds further evidence of banking. Greek temples, as well as private andcivic entities, conducted financial transactions such as loans, deposits, currencyexchange, and validation of coinage. There is evidence too of credit, whereby in return

for a payment from a client, a moneylender in one Greek port would write a credit notefor the client who could "cash" the note in another city, saving the client the danger of carting coinage with him on his journey. Pythius, who operated as a merchant banker throughout Asia Minor at the beginning of the 5th century B.C., is the first individual banker of whom we have records. Many of the early bankers in Greek city-states were“metics” or foreign residents. Around 371 B.C., Pasion, a slave, became the wealthiestand most famous Greek banker, gaining his freedom and Athenian citizenship in the process.

The fourth century B.C. saw increased use of credit-based banking in the Mediterraneanworld. In Egypt, from early times, grain had been used as a form of money in addition to

precious metals, and state granaries functioned as banks. When Egypt fell under the ruleof a Greek dynasty, the Ptolemies (332-30 B.C.), the numerous scattered governmentgranaries were transformed into a network of grain banks, centralized in Alexandriawhere the main accounts from all the state granary banks were recorded. This bankingnetwork functioned as a trade credit system in which payments were affected by transfer from one account to another without money passing.

In the late third century B.C., the barren Aegean island of Delos, known for itsmagnificent harbor and famous temple of Apollo, became a prominent banking center. Asin Egypt, cash transactions were replaced by real credit receipts and payments were made based on simple instructions with accounts kept for each client. With the defeat of its

main rivals, Carthage and Corinth, by the Romans, the importance of Delos increased.Consequently it was natural that the bank of Delos should become the model most closelyimitated by the banks of Rome.

Ancient Rome perfected the administrative aspect of banking and saw greater regulationof financial institutions and financial practices. Charging interest on loans and payinginterest on deposits became more highly developed and competitive. The development of Roman banks was limited, however, by the Roman preference for cash transactions.

2

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 3/45

During the reign of the Roman emperor Gallienus (260-268 AD), there was a temporary breakdown of the Roman banking system after the banks rejected the flakes of copper produced by his mints. With the ascent of Christianity, banking became subject toadditional restrictions, as the charging of interest was seen as immoral. After the fall of Rome, banking was abandoned in Western Europe and did not revive until the time of the

crusades.

Religious restrictions on interest

Most early religious systems in the ancient Near East, and the secular codes arising fromthem, did not forbid usury. These societies regarded inanimate matter as alive, like plants,animals and people, and capable of reproducing itself. Hence if you lent 'food money', or monetary tokens of any kind, it was legitimate to charge interest. [3] Food money in theshape of olives, dates, seeds or animals was lent out as early as c. 5000 BC, if not earlier.

Among the Mesopotamians, Hittites, Phoenicians and Egyptians, interest was legal andoften fixed by the state. But the Jews took a different view of the matter.

The Torah and later sections of the Hebrew Bible criticize interest-taking, butinterpretations of the Biblical prohibition vary. One common understanding is that Jewsare forbidden to charge interest upon loans made to other Jews, but allowed to chargeinterest on transactions with non-Jews, or Gentiles. However, the Hebrew Bible itself gives numerous examples where this provision was evaded.

During Late Antiquity and Middle Ages

Jews were ostracized from most professions by local rulers, the Church and the guilds and so were pushed into marginal occupations considered socially inferior, such as tax and rent collecting and moneylending, while the provision of financial services wasincreasingly demanded by the expansion of European trade and commerce.

Medieval trade fairs, such as the one in Hamburg, contributed to the growth of banking ina curious way: moneychangers issued documents redeemable at other fairs, in exchangefor hard currency. These documents could be cashed at another fair in a different countryor at a future fair in the same location. If redeemable at a future date, they would often be

discounted by an amount comparable to a rate of interest. Eventually, these documentsevolved into bills of exchange, which could be redeemed at any office of the issuing banker. These bills made it possible to transfer large sums of money without thecomplications of hauling large chests of gold and hiring armed guards to protect the goldfrom thieves.

Beginning around 1100s, the need to transfer large sums of money to finance theCrusades stimulated the re-emergence of banking in Western Europe. In 1156, in Genoa,

3

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 4/45

occurred the earliest known foreign exchange contract. Two brothers borrowed 115Genoese pounds and agreed to reimburse the bank's agents in Constantinople the sum of 460 bezants one month after their arrival in that city. In the following century the use of such contracts grew rapidly, particularly since profits from time differences were seen asnot infringing canon laws against usury. In 1162, King Henry the II levied a tax to

support the crusades -- the first of a series of taxes levied by Henry over the years withthe same objective. The Templars and Hospitallers acted as Henry's bankers in the HolyLand. The Templars' wide flung, large land holdings across Europe also emerged in the1100-1300 time frame as the beginning of Europe-wide banking, as their practice was totake in local currency, for which a demand note would be given that would be good atany of their castles across Europe, allowing movement of money without the usual risk of robbery while traveling.

By 1200 there was a large and growing volume of long-distance and international trade ina number of agricultural commodities and manufactured goods in western Europe; someof the goods traded during that period included wool, finished cloth, wine, salt, wax and

tallow, leather and leather goods, and weapons and armour. Individual trading concernsand combines often specialized in one or more of these, as did individual producers; because a large amount of capital was required to establish, e.g., a cloth manufacturing business, only the largest firms could diversify. As a result, businesses and clusters of businesses tended to market fairly narrow product lines. Big firms like the Medici bank could and did specialize; the Medici’s manufacturing division had a number of manufacturing facilities producing many different types of cloth. Perhaps the bestexample of product policy comes from the Cistercian monastic order, where individualmonasteries and granges tended to specialize in particular agricultural products or typesof industrial production, usually with an eye to meeting particular local or regionalmarket needs.

Ironically, the Papal bankers were the most successful of the Western world, though oftengoods taken in pawn were substituted for interest in the institution termed the Monte di Pietà. When Pope John XXII (born Jacques d'Euse (1249 - 1334) was crowned in Lyon in1316, he set up residency in Avignon. Civil war in Florence between the rival Guelph andGhibelline factions resulted in victory for a group of Guelph merchant families in thecity. They took over papal banking monopolies from rivals in nearby Siena and becametax collectors for the Pope throughout Europe. In 1306, Philip IV expelled Jews fromFrance. In 1307 Philip had the Knights Templar arrested and had gotten hold of their wealth, which had become to serve as the unofficial treasury of France. In 1311 heexpelled Italian bankers and collected their outstanding credit. In 1327, Avignon had 43 branches of Italian banking houses. In 1347, Edward III of England defaulted on loans.Later there was the bankruptcy of the Peruzzi (1374) and Bardi (1353). Theaccompanying growth of Italian banking in France was the start of the Lombard moneychangers in Europe, who moved from city to city along the busy pilgrim routesimportant for trade. Key cities in this period were Cahors, the birthplace of Pope JohnXXII, and Figeac. Perhaps it was because of these origins that the term Lombard issynonymous with Cahorsin in medieval Europe, and means 'pawnbroker'. Banca Monte dei Paschi di Siena SPA (MPS) Italy is the oldest surviving bank in the world.

4

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 5/45

After 1400, political forces turned against the methods of the Italian free enterprise bankers. In 1401, King Martin I of Aragon expelled them. In 1403, Henry IV of England prohibited them from taking profits in any way in his kingdom. In 1409, Flandersimprisoned and then expelled Genoese bankers. In 1410, all Italian merchants wereexpelled from Paris. In 1401, the Bank of Barcelona was founded. In 1407, the Bank of

Saint George was founded in Genoa. This bank dominated business in the Mediterranean.In 1403 charging interest on loans was ruled legal in Florence despite the traditionalChristian prohibition of usury. Italian banks such as the Lombards, who had agents in themain economic centres of Europe, had been making charges for loans. The lawyer andtheologian Lorenzo di Antonio Ridolfi won a case which legalised interest payments bythe Florentine government. In 1413, Giovanni di Bicci de’Medici appointed banker to the pope. In 1440, Gutenberg invents the modern printing press although Europe alreadyknew of the use of paper money in China. The printing press design was subsequentlymodified, by Leonardo da Vinci among others, for use in minting coins nearly twocenturies before printed banknotes were produced in the West.

By the 1390s silver was short all over Europe, except in Venice. The silver mines atKutná Hora had begun to decline in the 1370s, and finally closed down after being sacked by King Sigismund in 1422. By 1450 almost all of the mints of northwest Europe hadclosed down for lack of silver. The last money-changer in the major French port of Dieppe went out of business in 1446. In 1455 the Turks overran the Serbian silver mines,and in 1460 captured the last Bosnian mine. The last Venetian silver grosso was mintedin 1462. Several Venetian banks failed, and so did the Strozzi bank of Florence, thesecond largest in the city. Even the smallest of small change became scarce.

Western banking history

Modern Western economic and financial history is usually traced back to the coffeehouses of London. The London Royal Exchange was established in 1565. At that timemoneychangers were already called bankers, though the term " bank " usually referred totheir offices, and did not carry the meaning it does today. There was also a hierarchicalorder among professionals; at the top were the bankers who did business with heads of state, next were the city exchanges, and at the bottom were the pawn shops or "Lombard"'s. Some European cities today have a Lombard street where the pawn shopwas located.

After the siege of Antwerp, trade moved to Amsterdam. In 1609 the Amsterdamsche Wisselbank (Amsterdam Exchange Bank) was founded which made Amsterdam thefinancial centre of the world until the Industrial Revolution.

Banking offices were usually located near centers of trade, and in the late 17th century,the largest centers for commerce were the ports of Amsterdam, London, and Hamburg.Individuals could participate in the lucrative East India trade by purchasing bills of creditfrom these banks, but the price they received for commodities was dependent on the ships

5

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 6/45

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 7/45

History of Banking in India Without a sound and effective banking system in India it cannot have a healthy economy.The banking system of India should not only be hassle free but it should be able to meetnew challenges posed by the technology and any other external and internal factors.

For the past three decades India's banking system has several outstanding achievementsto its credit. The most striking is its extensive reach. It is no longer confined to onlymetropolitans or cosmopolitans in India. In fact, Indian banking system has reached evento the remote corners of the country. This is one of the main reason of India's growth process.

The government's regular policy for Indian bank since 1969 has paid rich dividends withthe nationalisation of 14 major private banks of India.

Not long ago, an account holder had to wait for hours at the bank counters for getting a

draft or for withdrawing his own money. Today, he has a choice. Gone are days when themost efficient bank transferred money from one branch to other in two days. Now it issimple as instant messaging or dial a pizza. Money have become the order of the day.

The first bank in India, though conservative, was established in 1786. From 1786 tilltoday, the journey of Indian Banking System can be segregated into three distinct phases.They are as mentioned below:

Early phase from 1786 to 1969 of Indian Banks Nationalisation of Indian Banks and up to 1991 prior to Indian banking sector Reforms.

New phase of Indian Banking System with the advent of Indian Financial & BankingSector Reforms after 1991.To make this write-up more explanatory, I prefix the scenario as Phase I, Phase II andPhase III.

Phase I

The General Bank of India was set up in the year 1786. Next came Bank of Hindustanand Bengal Bank. The East India Company established Bank of Bengal (1809), Bank of Bombay (1840) and Bank of Madras (1843) as independent units and called it PresidencyBanks. These three banks were amalgamated in 1920 and Imperial Bank of India was

established which started as private shareholders banks, mostly Europeans shareholders.

In 1865 Allahabad Bank was established and first time exclusively by Indians, Punjab National Bank Ltd. was set up in 1894 with headquarters at Lahore. Between 1906 and1913, Bank of India, Central Bank of India, Bank of Baroda, Canara Bank, Indian Bank,and Bank of Mysore were set up. Reserve Bank of India came in 1935.

7

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 8/45

During the first phase the growth was very slow and banks also experienced periodicfailures between 1913 and 1948. There were approximately 1100 banks, mostly small. Tostreamline the functioning and activities of commercial banks, the Government of Indiacame up with The Banking Companies Act, 1949 which was later changed to BankingRegulation Act 1949 as per amending Act of 1965 (Act No. 23 of 1965). Reserve Bank of

India was vested with extensive powers for the supervision of banking in india as theCentral Banking Authority.

During those days public has lesser confidence in the banks. As an aftermath depositmobilisation was slow. Abreast of it the savings bank facility provided by the Postaldepartment was comparatively safer. Moreover, funds were largely given to traders.

Phase II

Government took major steps in this Indian Banking Sector Reform after independence.In 1955, it nationalised Imperial Bank of India with extensive banking facilities on a

large scale specially in rural and semi-urban areas. It formed State Bank of india to act asthe principal agent of RBI and to handle banking transactions of the Union and StateGovernments all over the country.

Seven banks forming subsidiary of State Bank of India was nationalised in 1960 on 19thJuly, 1969, major process of nationalisation was carried out. It was the effort of the thenPrime Minister of India, Mrs. Indira Gandhi. 14 major commercial banks in the countrywas nationalised.

Second phase of nationalisation Indian Banking Sector Reform was carried out in 1980with seven more banks. This step brought 80% of the banking segment in India under Government ownership.

The following are the steps taken by the Government of India to Regulate BankingInstitutions in the Country:

1949 : Enactment of Banking Regulation Act.1955 : Nationalisation of State Bank of India.1959 : Nationalisation of SBI subsidiaries.1961 : Insurance cover extended to deposits.1969 : Nationalisation of 14 major banks.1971 : Creation of credit guarantee corporation.1975 : Creation of regional rural banks.1980 : Nationalisation of seven banks with deposits over 200 crore.After the nationalisation of banks, the branches of the public sector bank India rose toapproximately 800% in deposits and advances took a huge jump by 11,000%.

Banking in the sunshine of Government ownership gave the public implicit faith andimmense confidence about the sustainability of these institutions.

8

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 9/45

Phase III

This phase has introduced many more products and facilities in the banking sector in itsreforms measure. In 1991, under the chairmanship of M Narasimham, a committee wasset up by his name which worked for the liberalisation of banking practices.

The country is flooded with foreign banks and their ATM stations. Efforts are being putto give a satisfactory service to customers. Phone banking and net banking is introduced.The entire system became more convenient and swift. Time is given more importancethan money.

The financial system of India has shown a great deal of resilience. It is sheltered from anycrisis triggered by any external macroeconomics shock as other East Asian Countriessuffered. This is all due to a flexible exchange rate regime, the foreign reserves are high,the capital account is not yet fully convertible, and banks and their customers havelimited foreign exchange exposure.

9

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 10/45

A Brief Profile of the Bank

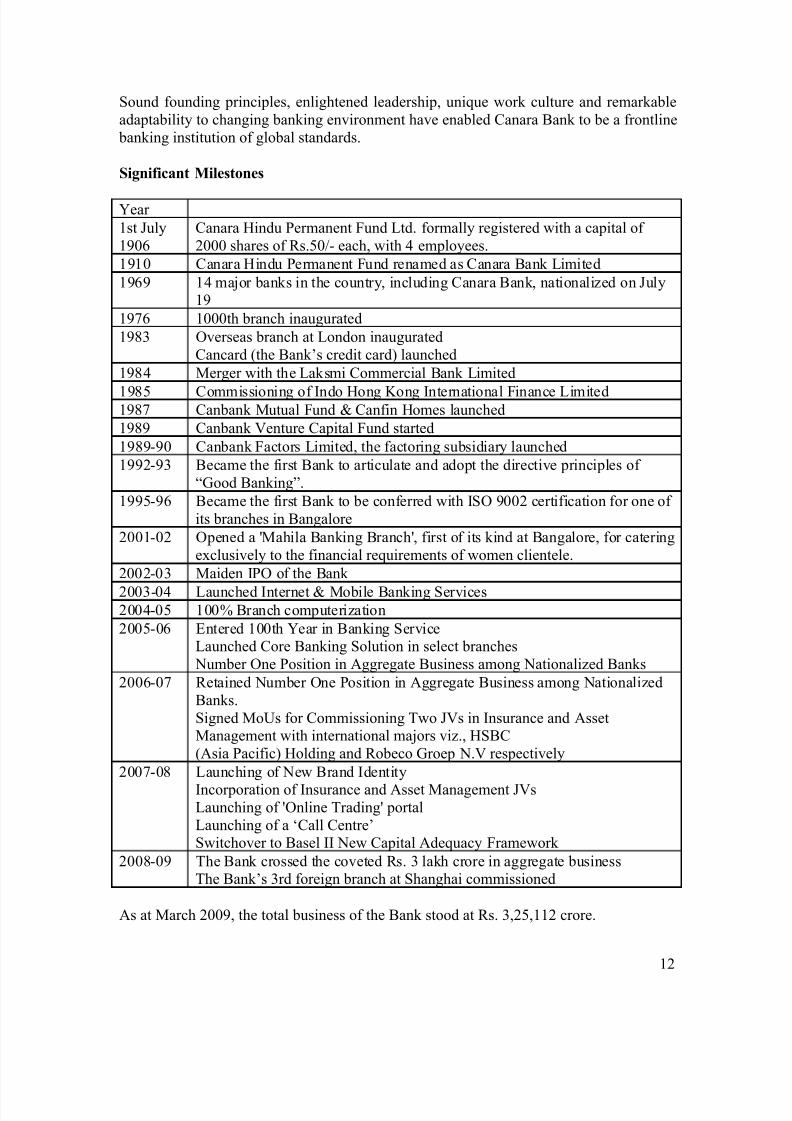

Widely known for customer centricity, Canara Bank was founded by Shri AmmembalSubba Rao Pai, a great visionary and philanthropist, in July 1906, at Mangalore, then asmall port in Karnataka. The Bank has gone through the various phases of its growthtrajectory over hundred years of its existence. Growth of Canara Bank was phenomenal,especially after nationalization in the year 1969, attaining the status of a national level player in terms of geographical reach and clientele segments. Eighties was characterized by business diversification for the Bank. In June 2006, the Bank completed a century of operation in the Indian banking industry. The eventful journey of the Bank has beencharacterized by several memorable milestones. Today, Canara Bank occupies a premier position in the comity of Indian banks. With an unbroken record of profits since its

inception, Canara Bank has several firsts to its credit.

These include:

• Launching of Inter-City ATM Network

• Obtaining ISO Certification for a Branch

• Articulation of ‘Good Banking’ – Bank’s Citizen Charter

• Commissioning of Exclusive Mahila Banking Branch

• Launching of Exclusive Subsidiary for IT Consultancy

• Issuing credit card for farmers

• Providing Agricultural Consultancy Services

Over the years, the Bank has been scaling up its market position to emerge as a major 'Financial Conglomerate' with as many as nine subsidiaries/sponsored institutions/jointventures in India and abroad. As at March 2009, the Bank has further expanded itsdomestic presence, with 2729 branches spread across all geographical segments. Keeping

customer convenience at the forefront, the Bank provides a wide array of alternativedelivery channels that include over 2000 ATMs- one of the highest among nationalized banks- covering 705 centres, 1362 branches providing Internet and Mobile Banking(IMB) services and 2062 branches offering 'Anywhere Banking' services. Under advanced payment and settlement system, all branches of the Bank have been enabled tooffer Real Time Gross Settlement (RTGS) and National Electronic Funds Transfer (NEFT) facilities.

10

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 11/45

Not just in commercial banking, the Bank has also carved a distinctive mark, in variouscorporate social responsibilities, namely, serving national priorities, promoting ruraldevelopment, enhancing rural self-employment through several training institutes andspearheading financial inclusion objective. Promoting an inclusive growth strategy,which has been formed as the basic plank of national policy agenda today, is in fact

deeply rooted in the Bank's founding principles. "A good bank is not only the financialheart of the community, but also one with an obligation of helping in every possiblemanner to improve the economic conditions of the common people". These insightfulwords of our founder continue to resonate even today in serving the society with a purpose. The growth story of Canara Bank in its first century was due, among others, tothe continued patronage of its valued customers, stakeholders, committed staff anduncanny leadership ability demonstrated by its leaders at the helm of affairs. We strongly believe that the next century is going to be equally rewarding and eventful not only inservice of the nation but also in helping the Bank emerge as a "Global Bank with BestPractices". This justifiable belief is founded on strong fundamentals, customer centricity,enlightened leadership and a family like work culture.

Late Sri Ammembal Subbarao Pai

Founded as 'Canara Bank Hindu Permanent Fund' in 1906, by late Sri.Ammembal Subba Rao Pai, a philanthropist, this small seed blossomed into a limited company as 'Canara Bank Ltd.' in 1910 and became Canara Bank in 1969 after nationalization.

"A good bank is not only the financial heart of the community, but also one with an obligation of helping in every possible manner to improve the economic

conditions of the common people" - A. Subba Rao Pai.

Founding Principles

1. To remove Superstition and ignorance.2. To spread education among all to sub-serve the first principle.3. To inculcate the habit of thrift and savings.4. To transform the financial institution not only as the financial heart of the

community but the social heart as well.5. To assist the needy.6. To work with sense of service and dedication.7. To develop a concern for fellow human being and sensitivity to the surroundings

with a view to make changes/remove hardships and sufferings.

11

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 12/45

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 13/45

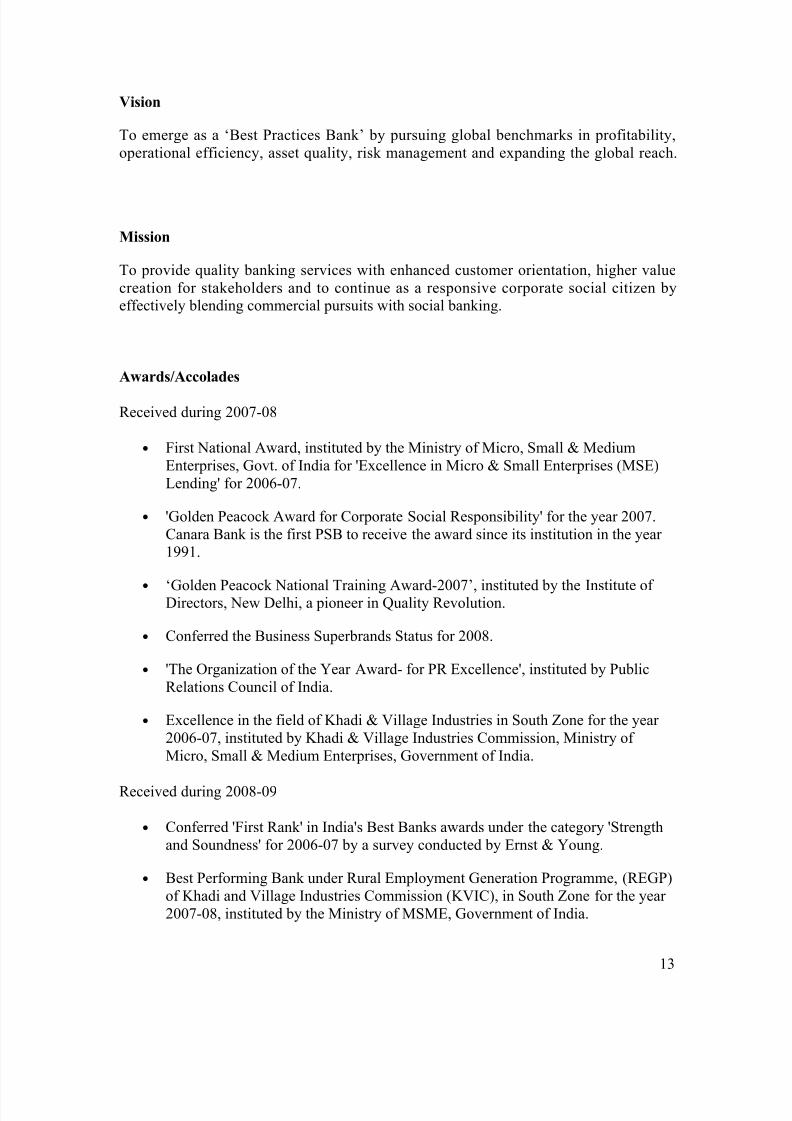

Vision

To emerge as a ‘Best Practices Bank’ by pursuing global benchmarks in profitability,operational efficiency, asset quality, risk management and expanding the global reach.

Mission

To provide quality banking services with enhanced customer orientation, higher valuecreation for stakeholders and to continue as a responsive corporate social citizen byeffectively blending commercial pursuits with social banking.

Awards/Accolades

Received during 2007-08

• First National Award, instituted by the Ministry of Micro, Small & MediumEnterprises, Govt. of India for 'Excellence in Micro & Small Enterprises (MSE)Lending' for 2006-07.

• 'Golden Peacock Award for Corporate Social Responsibility' for the year 2007.Canara Bank is the first PSB to receive the award since its institution in the year 1991.

•

‘Golden Peacock National Training Award-2007’, instituted by the Institute of Directors, New Delhi, a pioneer in Quality Revolution.

• Conferred the Business Superbrands Status for 2008.

• 'The Organization of the Year Award- for PR Excellence', instituted by PublicRelations Council of India.

• Excellence in the field of Khadi & Village Industries in South Zone for the year 2006-07, instituted by Khadi & Village Industries Commission, Ministry of Micro, Small & Medium Enterprises, Government of India.

Received during 2008-09

• Conferred 'First Rank' in India's Best Banks awards under the category 'Strengthand Soundness' for 2006-07 by a survey conducted by Ernst & Young.

• Best Performing Bank under Rural Employment Generation Programme, (REGP)of Khadi and Village Industries Commission (KVIC), in South Zone for the year 2007-08, instituted by the Ministry of MSME, Government of India.

13

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 14/45

• Golden Peacock National Training Award 2008 for excellence in training.

• Global HR excellence in Training, an award conferred by the Asia Pacific HR Congress, the largest rendezvous of HR Professionals, at its Employer BrandingTalent Management Congress held on 22nd and 23rd August 2008, Delhi.

• Best Corporate Social Responsibility Practice Award, instituted by BSE, NASSCOM and Times Foundation.

The Bank won two Silver Corporate Collateral Awards for Best Corporate Ad in the PrintMedia and Best Corporate Film on Corporate Social Responsibility at the PublicRelations Council of India Awards 2009.

Canara bank helps you in planning to own a home by buying a flat or building a house.The bank offers you loan for constructing a new house or for doing additions or renovation in the existing house. Anyone from salaried individual to self-employed persons can take the home loan by fulfilling certain criteria and documentation for theentitlement of the loan. Even NRIs can apply for home loan offered by Canara Bank.

Canara bank has a wide array of network opened in the country to help people in banking. As at December 2007 bank has network of 2641 branches spread all over India.Bank has over 1900 ATMs, covering 680 centers, over 1100 branches providing Internetand Mobile Banking (IMB) services and more than 1833 branches offering 'AnywhereBanking' services. Now more than 1693 branches of the Bank offer advanced paymentand settlement system under Real Time Gross Settlement (RTGS) and NationalElectronic Funds Transfer (NEFT).

Institution Information

Head Office

Canara Bank 112, J C RoadBANGALOREBangalore - 560 002KarnatakaIndia

Website http://canarabank.com/No. of branches

2641No. of ATMs

1900Customer Care Numbers

14

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 15/45

BANGALORE: 080-25586087, CHENNAI: 044 - 24344638, DELHI: 011- 26415331, KOLKATA: 033-22807899

Products / Services

Credit Cards

Canara Bank offers a credit card named CANCARD that provides both convenience andquality services to the cardholders. It is a widely accepted card under the principalmembership of Visa International and Master card International. The bank offers freeinsurance cover under the card.

The bank has set a liberal credit limit of minimum gross income of Rs 60,000 per annumto avail the card. There is no maximum amount for accumulation and you earn bonus points on using the card.

CANCARD VISA CLASSIC

• Liberal Card limit• Get 30% of your gross annual income with a maximum of Rs.3.00 lakhs. Fixing

up of the limit is at the sole discretion of Canara Bank.• Cash withdrawal facility at designated 450 branches all over India• Cash withdrawal at Canara Bank ATMs.• No Interest on cash withdrawal if paid by the due date. If not paid by the DUE

DATE, interest is charged from DUE DATE only and not from the DATE OFCASH WITHDRAWAL.

• Opt for Revolving Payment system and pay only 5% of the billed amount anddefer the payment.

• No financial charges! i.e., interest on other transactions subsequent to cashwithdrawal till the cash withdrawal is repaid.

CANCARD VISA CORPORATE

• Liberal Card limit• Get 30% of your gross annual income with a maximum of Rs.3.00 lakhs. Fixing

up of the limit is at the sole discretion of Canara Bank.• Cash withdrawal facility at designated 450 branches all over India• Cash withdrawal at Canara Bank ATMs.

15

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 16/45

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 17/45

Saving Accounts

Canara Bank savings account can be opened singly / jointly, as minor account, by non-corporate bodies, societies, associations, etc. The minimum balance required to open anaccount is Rs 500/- without cheque book and Rs 1000/- with cheque book in

Metro/Urban whereas in Semi-urban/Rural Branches the account can be opened with Rs100/- without cheque book and Rs 500/- with cheque book. You have to fulfilldocumentation criteria laid down by the bank for opening an account. Bank gives aninterest which is compounded half-yearly on the minimum balance in the account between the10th and the last day of the month.

SAVINGS BANK ACCOUNT

• NATURE OF DEPOSIT: Running (Operating) account.• PERIODICITY OF INTEREST PAYMENT: Interest is payable half-yearly,

every February and August on the minimum balance in the account, between the

10th and last day of the month.• SPECIAL RATE FOR SENIOR CITIZEN-Not applicable• SPECIAL RATE FOR BULK DEPOSITS- Not applicable• TDS- Not applicable

Highlights

Bank Canara Bank

Category Regular

Minimum AQB

(Average QuarterlyBalance)

Metro/Urban - Rs.500/- without cheque book & Rs.1000/-

with cheque book Semi-urban/Rural Branches - Rs.100/- without cheque book

& Rs.500/- with cheque book

Interest Rate 3.5%

Card Offered ATM cum Debit Card

CANSARAL SAVINGS ACCOUNT

• An SB product designed for the common man to provide a basic banking facilityas part of the financial inclusion objective of RBI.

• MINIMUM DEPOSIT The account can be maintained even with zero balance.• WITHDRAWAL/ DEPOSIT:

o Permitted through withdrawal order form, cheque and ATM cum Debit

Cardo Maximum 6 withdrawals per month including drawings through ATM free

of charge. For withdrawals exceeding 6 per month would be levied aservice charge at the rate not exceeding Rs.5/- per withdrawal at thediscretion of the branch.

17

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 18/45

o The minimum amount that may be deposited/ withdrawn “IN CASH” in

an account is as prescribed by the bank from time to time. Currentlyminimum deposit or withdrawal “IN CASH” is Rs.10/-. In case of withdrawal through ATM, the minimum amount is Rs.100/- (Currently).

• TDS- Exempted

Highlights

Bank Canara Bank

Category Regular

Minimum AQB(AverageQuarterly Balance)

An account can be opened with an initial deposit of Rs. 25/-. The

account can be maintained even with zero balance.

Metro/Urban - Rs.500/- without cheque book & Rs.1000/- with

cheque book

Semi-urban/Rural Branches - Rs.100/- without cheque book &

Rs.500/- with cheque book

Interest Rate 3.5%

Card Offered None

SB GOLD SCHEME (CBS branches only)

• NATURE OF DEPOSIT Running (Operating)account• PERIODICITY OF INTEREST PAYMENT Interest is payable half yearly, every

February and August on the minimum balance in the account, between the 10thand last day of the month.

• SPECIAL RATE FOR SENIOR CITIZEN Not applicable•

• SPECIAL RATE FOR BULK DEPOSITS Not applicable• TDS Not applicable• LOAN AGAINST DEPOSIT Not permitted• VALUE ADDED FACILITIES:

o DD facility at 50% concession i.e. Re.1/- per Rs.1000/- or part thereof

o Funds transfer under NEFT and RTGS(Canspeed) at 50% concession

o Free Debit Card (as per Bank's rules for issue of Debit Cards)

o Issue of free Credit Card to the 1st account holder (for others as per

existing rules of the Bank)o Waiver of demat account opening charges.

o Free Anywhere Banking (AWB) facility.o Sweep-in Sweep-out facility: Sweep-in into term deposit of amounts

beyond Rs.1,00,000/- at the request(one time) of the customer mentioningthe tenor of the term deposit.

o Name printed cheque book.

o Free funds transfer facility through our Internet Banking

o Free Telebanking facility.

18

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 19/45

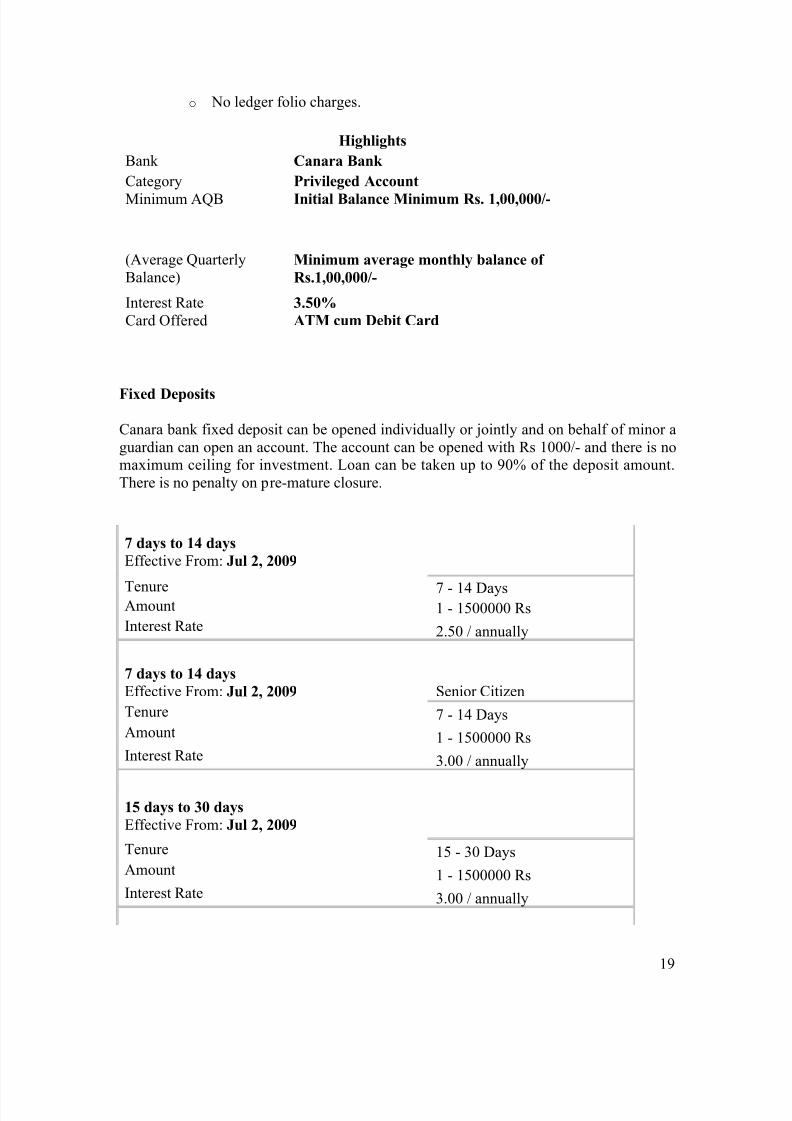

o No ledger folio charges.

Highlights

Bank Canara Bank

Category Privileged Account

Minimum AQB Initial Balance Minimum Rs. 1,00,000/-

(Average QuarterlyBalance)

Minimum average monthly balance of

Rs.1,00,000/-

Interest Rate 3.50%

Card Offered ATM cum Debit Card

Fixed Deposits

Canara bank fixed deposit can be opened individually or jointly and on behalf of minor aguardian can open an account. The account can be opened with Rs 1000/- and there is nomaximum ceiling for investment. Loan can be taken up to 90% of the deposit amount.There is no penalty on pre-mature closure.

7 days to 14 days

Effective From: Jul 2, 2009

Tenure 7 - 14 DaysAmount 1 - 1500000 RsInterest Rate 2.50 / annually

7 days to 14 days

Effective From: Jul 2, 2009 Senior Citizen

Tenure 7 - 14 DaysAmount 1 - 1500000 RsInterest Rate 3.00 / annually

15 days to 30 days

Effective From: Jul 2, 2009

Tenure 15 - 30 DaysAmount 1 - 1500000 RsInterest Rate 3.00 / annually

19

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 20/45

15 days to 30 days

Effective From: Jul 2, 2009 Senior Citizen

Tenure 15 - 30 DaysAmount 1 - 1500000 Rs

Interest Rate 3.50 / annually

31 days to 45 days

Effective From: Jul 2, 2009

Tenure 31 - 45 DaysAmount 1 - 1500000 RsInterest Rate 3.50 / annually

31 days to 45 days

Effective From: Jul 2, 2009 Senior Citizen

Tenure 31 - 45 DaysAmount 1 - 1500000 RsInterest Rate 4.00 / annually

46 days to 90 days

Effective From: Jul 2, 2009

Tenure 46 - 90 DaysAmount 1 - 1500000 Rs

Interest Rate 4.50 / annually

46 days to 90 days

Effective From: Jul 2, 2009 Senior Citizen

Tenure 46 - 90 DaysAmount 1 - 1500000 RsInterest Rate 5.00 / annually

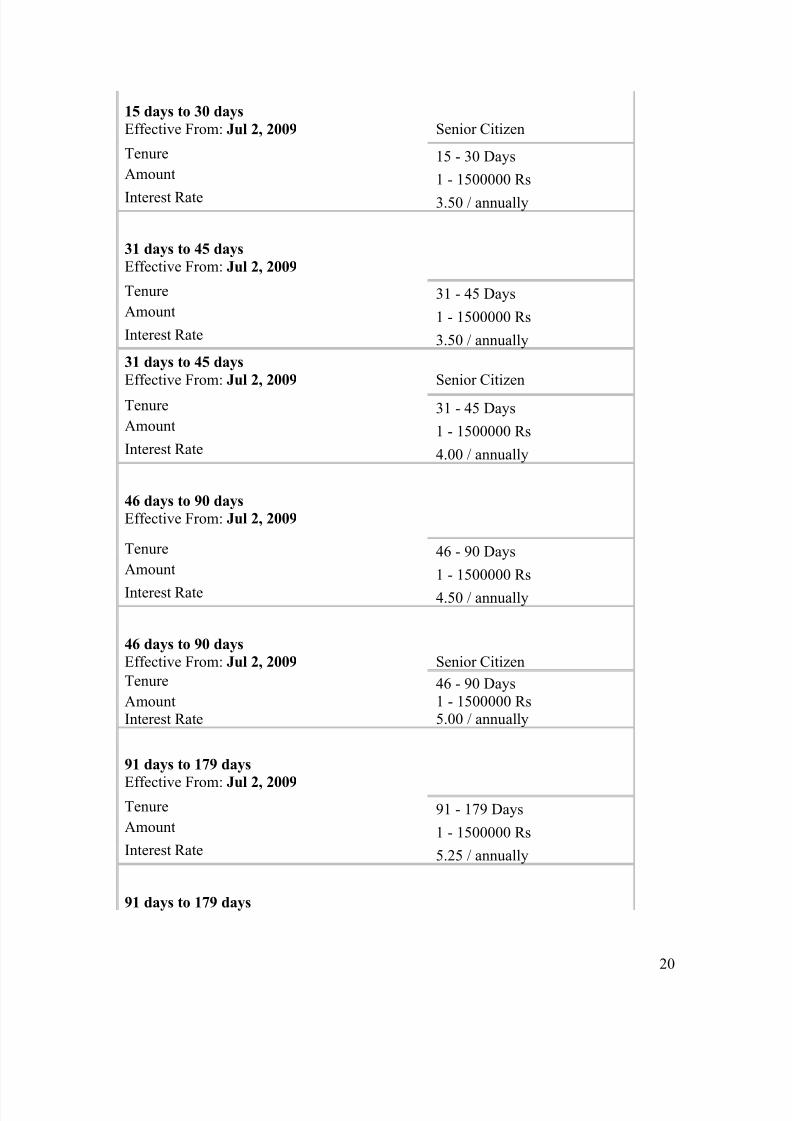

91 days to 179 days

Effective From: Jul 2, 2009 Tenure 91 - 179 DaysAmount 1 - 1500000 RsInterest Rate 5.25 / annually

91 days to 179 days

20

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 21/45

Effective From: Jul 2, 2009 Senior Citizen

Tenure 91 - 179 DaysAmount 1 - 1500000 RsInterest Rate 5.75 / annually

180 days to 269 days

Effective From: Jul 2, 2009

Tenure 180 - 269 DaysAmount 1 - 1500000 RsInterest Rate

6.25 / annually

180 days to 269 days

Effective From: Jul 2, 2009 Senior Citizen

Tenure 180 - 269 DaysAmount 1 - 1500000 RsInterest Rate 6.75 / annually

270 days to less than 1 year

Effective From: Jul 2, 2009

Tenure 270 - 365 DaysAmount 1 - 1500000 RsInterest Rate

6.50 / annually

270 days to less than 1 year

Effective From: Jul 2, 2009 Senior Citizen

Tenure 270 - 365 DaysAmount 1 - 1500000 RsInterest Rate 7.00 / annually

1 year & above to less than 2 years

Effective From: Jul 2, 2009 Tenure 365 - 730 DaysAmount 1 - 1500000 RsInterest Rate 7.00 / annually

1 year & above to less than 2 years

Effective From: Jul 2, 2009 Senior Citizen

Tenure 365 - 730 Days

21

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 22/45

Amount 1 - 1500000 RsInterest Rate 7.50 / annually

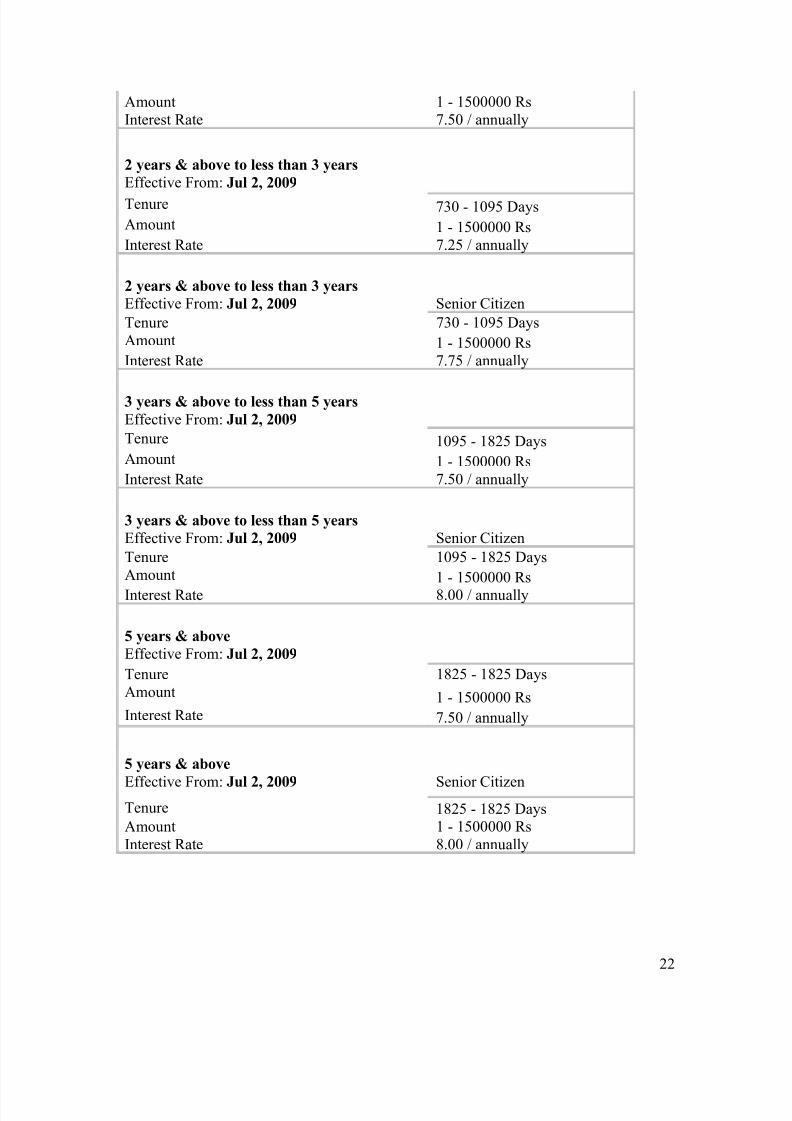

2 years & above to less than 3 years

Effective From: Jul 2, 2009

Tenure 730 - 1095 DaysAmount 1 - 1500000 RsInterest Rate 7.25 / annually

2 years & above to less than 3 years

Effective From: Jul 2, 2009 Senior Citizen

Tenure 730 - 1095 DaysAmount 1 - 1500000 RsInterest Rate 7.75 / annually

3 years & above to less than 5 years

Effective From: Jul 2, 2009

Tenure 1095 - 1825 DaysAmount 1 - 1500000 RsInterest Rate 7.50 / annually

3 years & above to less than 5 years

Effective From: Jul 2, 2009 Senior Citizen

Tenure 1095 - 1825 DaysAmount 1 - 1500000 Rs

Interest Rate 8.00 / annually

5 years & above

Effective From: Jul 2, 2009

Tenure 1825 - 1825 DaysAmount 1 - 1500000 RsInterest Rate 7.50 / annually

5 years & above

Effective From: Jul 2, 2009 Senior CitizenTenure 1825 - 1825 DaysAmount 1 - 1500000 RsInterest Rate 8.00 / annually

22

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 23/45

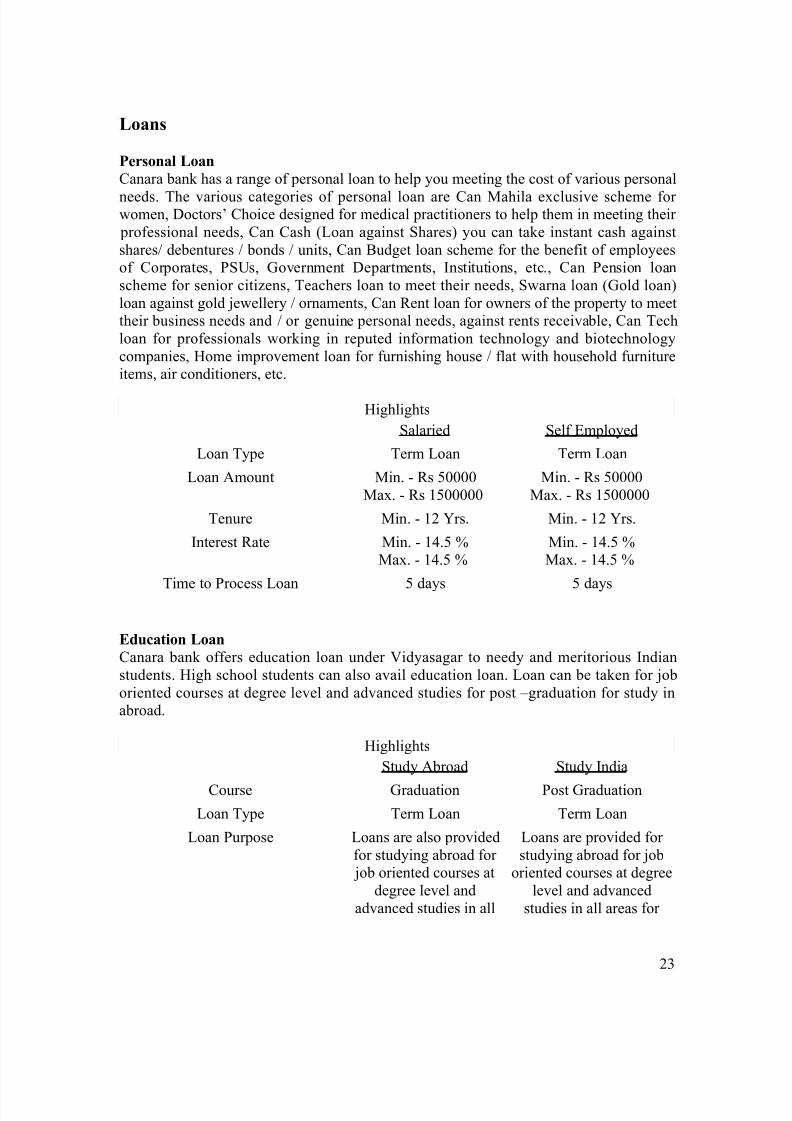

Loans

Personal Loan

Canara bank has a range of personal loan to help you meeting the cost of various personal

needs. The various categories of personal loan are Can Mahila exclusive scheme for women, Doctors’ Choice designed for medical practitioners to help them in meeting their professional needs, Can Cash (Loan against Shares) you can take instant cash againstshares/ debentures / bonds / units, Can Budget loan scheme for the benefit of employeesof Corporates, PSUs, Government Departments, Institutions, etc., Can Pension loanscheme for senior citizens, Teachers loan to meet their needs, Swarna loan (Gold loan)loan against gold jewellery / ornaments, Can Rent loan for owners of the property to meettheir business needs and / or genuine personal needs, against rents receivable, Can Techloan for professionals working in reputed information technology and biotechnologycompanies, Home improvement loan for furnishing house / flat with household furnitureitems, air conditioners, etc.

Highlights

Salaried Self Employed

Loan Type Term Loan Term Loan

Loan Amount Min. - Rs 50000Max. - Rs 1500000

Min. - Rs 50000Max. - Rs 1500000

Tenure Min. - 12 Yrs. Min. - 12 Yrs.

Interest Rate Min. - 14.5 %Max. - 14.5 %

Min. - 14.5 %Max. - 14.5 %

Time to Process Loan 5 days 5 days

Education Loan

Canara bank offers education loan under Vidyasagar to needy and meritorious Indianstudents. High school students can also avail education loan. Loan can be taken for joboriented courses at degree level and advanced studies for post –graduation for study inabroad.

Highlights

Study Abroad Study India

Course Graduation Post Graduation

Loan Type Term Loan Term Loan

Loan Purpose Loans are also providedfor studying abroad for job oriented courses at

degree level andadvanced studies in all

Loans are provided for studying abroad for job

oriented courses at degreelevel and advanced

studies in all areas for

23

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 24/45

areas for post-graduation.For payment of fees toschool/college and for

purchase of books, hostelfees, examination fees,

etc.

post-graduation.

Loan Amount Min. - Rs 50000Max. - Rs 400000

Min. - Rs 50000Max. - Rs 400000

Margin Money 15 % 5 %

Tenure Min. - 1 Yrs. Min. - 1 Yrs.

Interest Rate - Upto Rs.4 lakhs -12.50%

- Upto Rs.4 lakhs -12.50%

Time to Process Loan 7 days 7 days

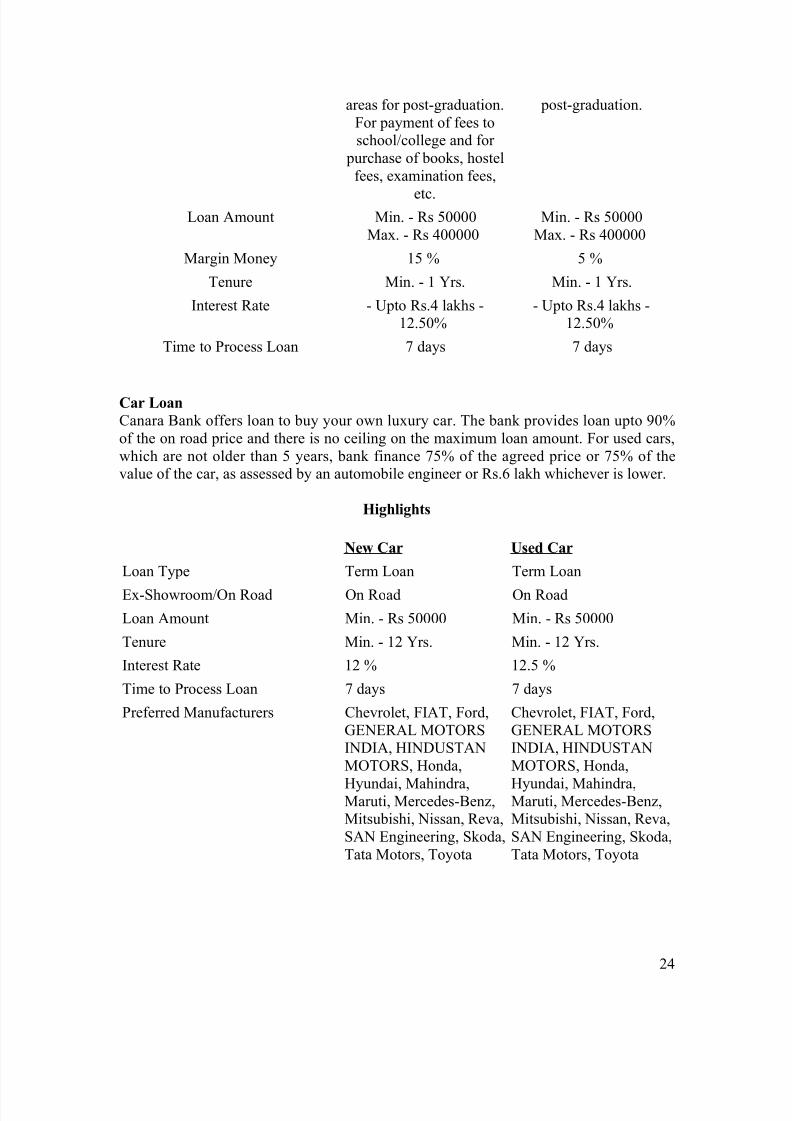

Car Loan

Canara Bank offers loan to buy your own luxury car. The bank provides loan upto 90%of the on road price and there is no ceiling on the maximum loan amount. For used cars,which are not older than 5 years, bank finance 75% of the agreed price or 75% of thevalue of the car, as assessed by an automobile engineer or Rs.6 lakh whichever is lower.

Highlights

New Car Used Car

Loan Type Term Loan Term Loan

Ex-Showroom/On Road On Road On Road

Loan Amount Min. - Rs 50000 Min. - Rs 50000

Tenure Min. - 12 Yrs. Min. - 12 Yrs.

Interest Rate 12 % 12.5 %

Time to Process Loan 7 days 7 days

Preferred Manufacturers Chevrolet, FIAT, Ford,GENERAL MOTORSINDIA, HINDUSTANMOTORS, Honda,

Hyundai, Mahindra,Maruti, Mercedes-Benz,Mitsubishi, Nissan, Reva,SAN Engineering, Skoda,Tata Motors, Toyota

Chevrolet, FIAT, Ford,GENERAL MOTORSINDIA, HINDUSTANMOTORS, Honda,

Hyundai, Mahindra,Maruti, Mercedes-Benz,Mitsubishi, Nissan, Reva,SAN Engineering, Skoda,Tata Motors, Toyota

24

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 25/45

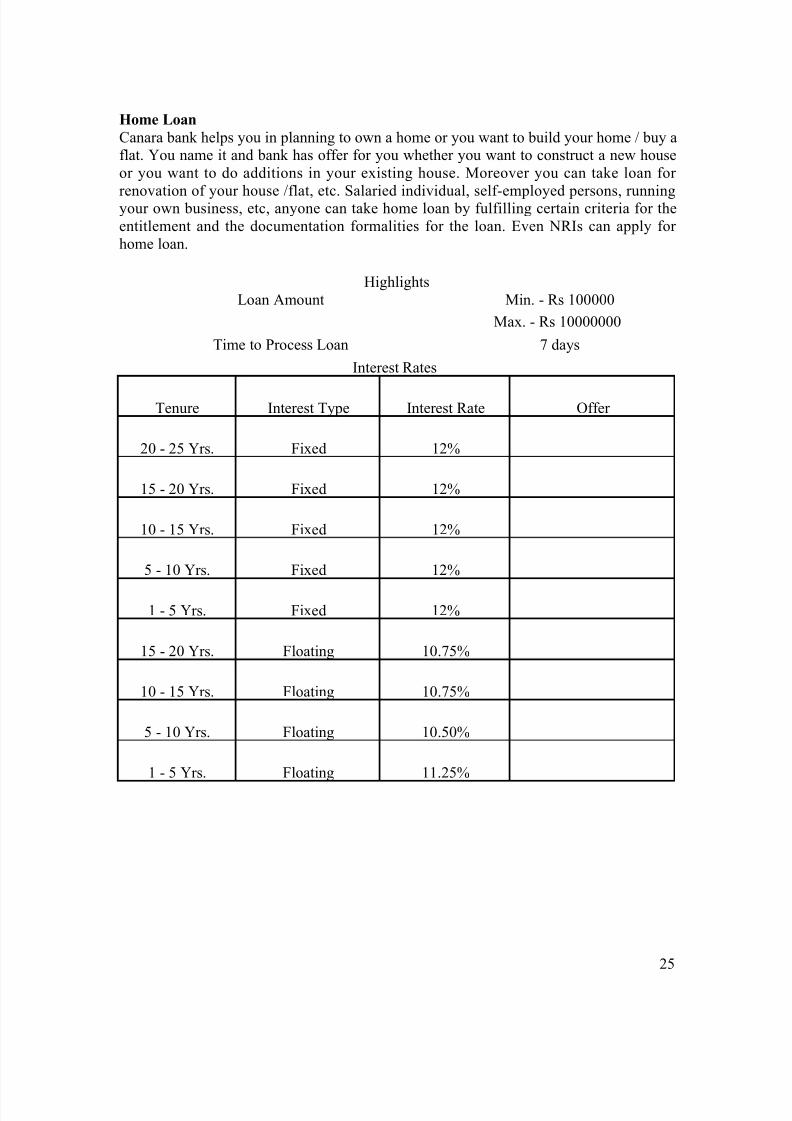

Home Loan

Canara bank helps you in planning to own a home or you want to build your home / buy aflat. You name it and bank has offer for you whether you want to construct a new houseor you want to do additions in your existing house. Moreover you can take loan for

renovation of your house /flat, etc. Salaried individual, self-employed persons, runningyour own business, etc, anyone can take home loan by fulfilling certain criteria for theentitlement and the documentation formalities for the loan. Even NRIs can apply for home loan.

HighlightsLoan Amount Min. - Rs 100000

Max. - Rs 10000000

Time to Process Loan 7 days

Interest Rates

Tenure Interest Type Interest Rate Offer

20 - 25 Yrs. Fixed 12%

15 - 20 Yrs. Fixed 12%

10 - 15 Yrs. Fixed 12%

5 - 10 Yrs. Fixed 12%

1 - 5 Yrs. Fixed 12%

15 - 20 Yrs. Floating 10.75%

10 - 15 Yrs. Floating 10.75%

5 - 10 Yrs. Floating 10.50%

1 - 5 Yrs. Floating 11.25%

25

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 26/45

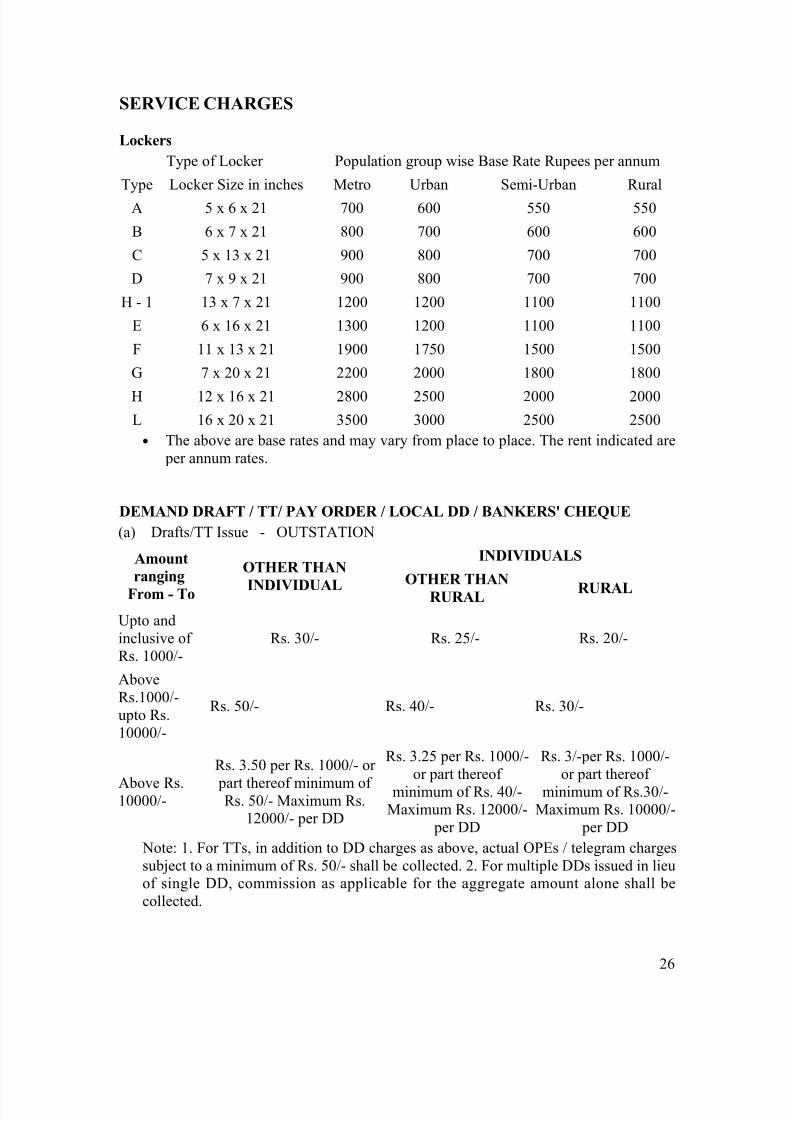

SERVICE CHARGES

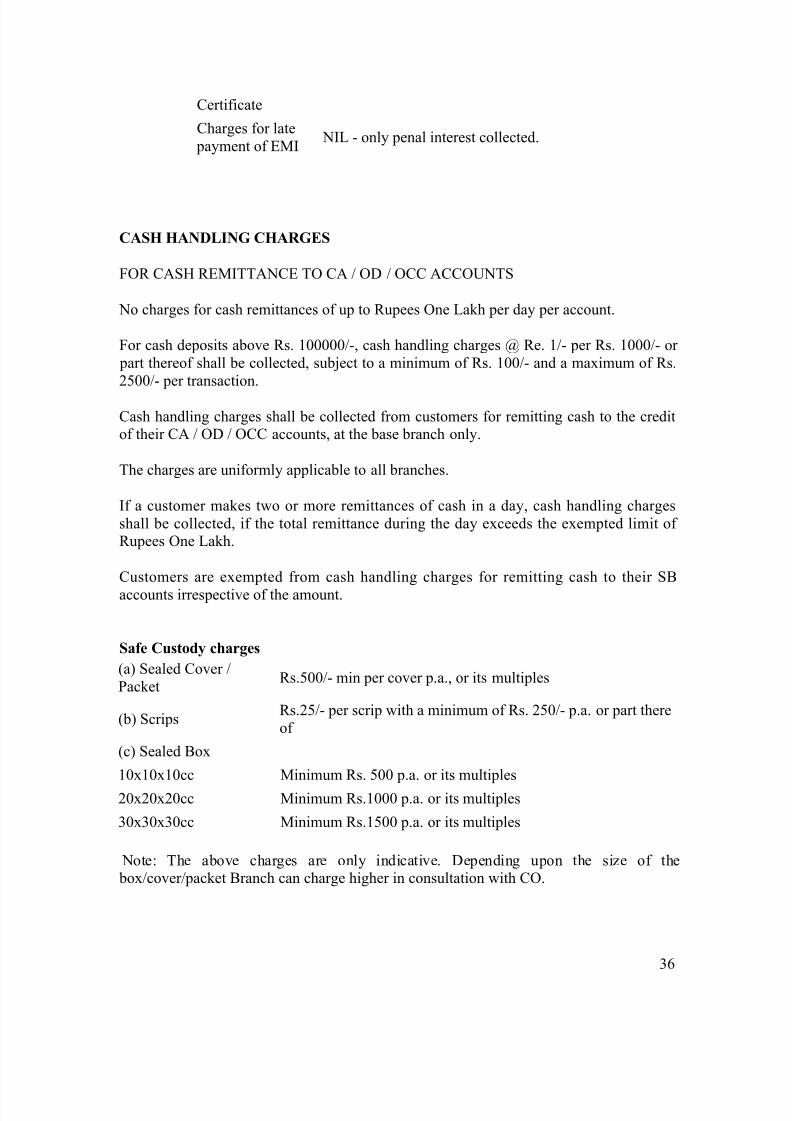

Lockers

Type of Locker Population group wise Base Rate Rupees per annum

Type Locker Size in inches Metro Urban Semi-Urban Rural

A 5 x 6 x 21 700 600 550 550

B 6 x 7 x 21 800 700 600 600

C 5 x 13 x 21 900 800 700 700

D 7 x 9 x 21 900 800 700 700

H - 1 13 x 7 x 21 1200 1200 1100 1100

E 6 x 16 x 21 1300 1200 1100 1100

F 11 x 13 x 21 1900 1750 1500 1500

G 7 x 20 x 21 2200 2000 1800 1800

H 12 x 16 x 21 2800 2500 2000 2000

L 16 x 20 x 21 3500 3000 2500 2500

• The above are base rates and may vary from place to place. The rent indicated are per annum rates.

DEMAND DRAFT / TT/ PAY ORDER / LOCAL DD / BANKERS' CHEQUE

(a) Drafts/TT Issue - OUTSTATION

Amount

ranging

From - To

OTHER THAN

INDIVIDUAL

INDIVIDUALS

OTHER THAN

RURAL RURAL

Upto andinclusive of Rs. 1000/-

Rs. 30/- Rs. 25/- Rs. 20/-

AboveRs.1000/-upto Rs.10000/-

Rs. 50/- Rs. 40/- Rs. 30/-

Above Rs.10000/-

Rs. 3.50 per Rs. 1000/- or

part thereof minimum of Rs. 50/- Maximum Rs.

12000/- per DD

Rs. 3.25 per Rs. 1000/-or part thereof

minimum of Rs. 40/-Maximum Rs. 12000/-

per DD

Rs. 3/-per Rs. 1000/-or part thereof

minimum of Rs.30/-Maximum Rs. 10000/-

per DD

Note: 1. For TTs, in addition to DD charges as above, actual OPEs / telegram chargessubject to a minimum of Rs. 50/- shall be collected. 2. For multiple DDs issued in lieuof single DD, commission as applicable for the aggregate amount alone shall becollected.

26

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 27/45

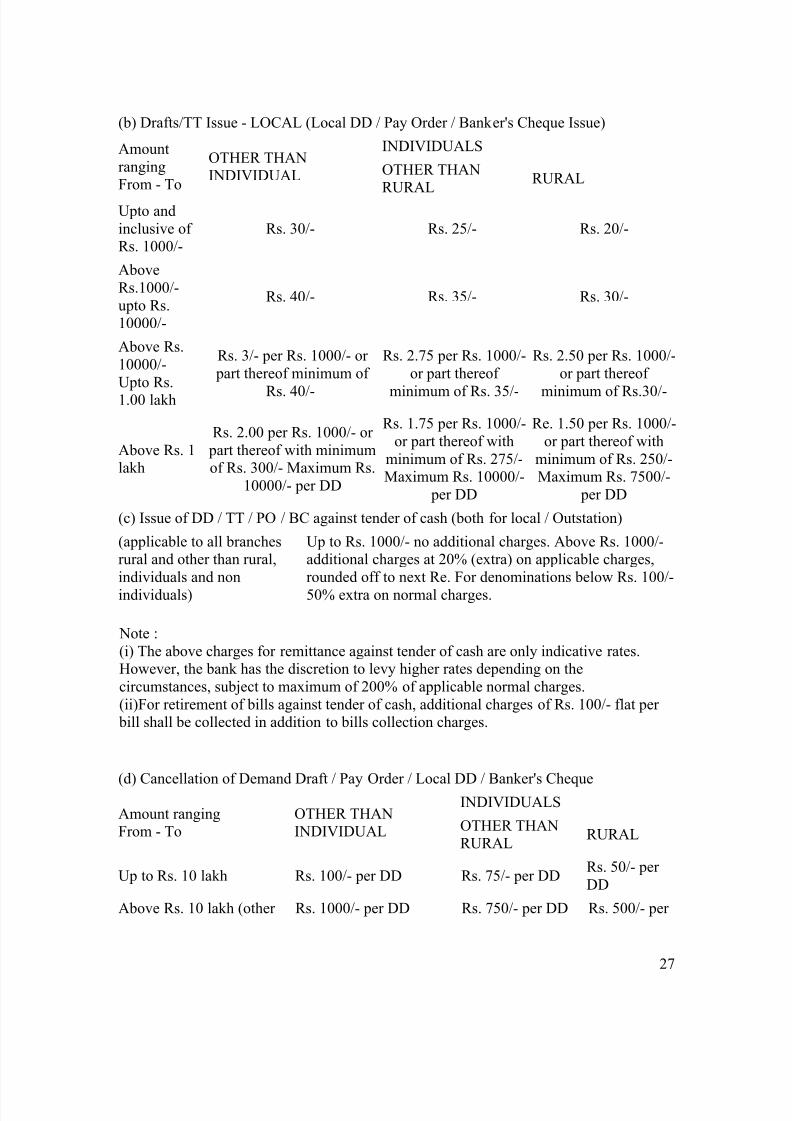

(b) Drafts/TT Issue - LOCAL (Local DD / Pay Order / Banker's Cheque Issue)

AmountrangingFrom - To

OTHER THANINDIVIDUAL

INDIVIDUALS

OTHER THANRURAL

RURAL

Upto andinclusive of Rs. 1000/-

Rs. 30/- Rs. 25/- Rs. 20/-

AboveRs.1000/-upto Rs.10000/-

Rs. 40/- Rs. 35/- Rs. 30/-

Above Rs.10000/-Upto Rs.1.00 lakh

Rs. 3/- per Rs. 1000/- or part thereof minimum of

Rs. 40/-

Rs. 2.75 per Rs. 1000/-or part thereof

minimum of Rs. 35/-

Rs. 2.50 per Rs. 1000/-or part thereof

minimum of Rs.30/-

Above Rs. 1lakh

Rs. 2.00 per Rs. 1000/- or part thereof with minimumof Rs. 300/- Maximum Rs.

10000/- per DD

Rs. 1.75 per Rs. 1000/-or part thereof with

minimum of Rs. 275/-Maximum Rs. 10000/-

per DD

Re. 1.50 per Rs. 1000/-or part thereof with

minimum of Rs. 250/-Maximum Rs. 7500/-

per DD

(c) Issue of DD / TT / PO / BC against tender of cash (both for local / Outstation)

(applicable to all branchesrural and other than rural,individuals and non

individuals)

Up to Rs. 1000/- no additional charges. Above Rs. 1000/-additional charges at 20% (extra) on applicable charges,rounded off to next Re. For denominations below Rs. 100/-

50% extra on normal charges.

Note :(i) The above charges for remittance against tender of cash are only indicative rates.However, the bank has the discretion to levy higher rates depending on thecircumstances, subject to maximum of 200% of applicable normal charges.(ii)For retirement of bills against tender of cash, additional charges of Rs. 100/- flat per bill shall be collected in addition to bills collection charges.

(d) Cancellation of Demand Draft / Pay Order / Local DD / Banker's Cheque

Amount rangingFrom - To

OTHER THANINDIVIDUAL

INDIVIDUALS

OTHER THANRURAL

RURAL

Up to Rs. 10 lakh Rs. 100/- per DD Rs. 75/- per DDRs. 50/- per DD

Above Rs. 10 lakh (other Rs. 1000/- per DD Rs. 750/- per DD Rs. 500/- per

27

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 28/45

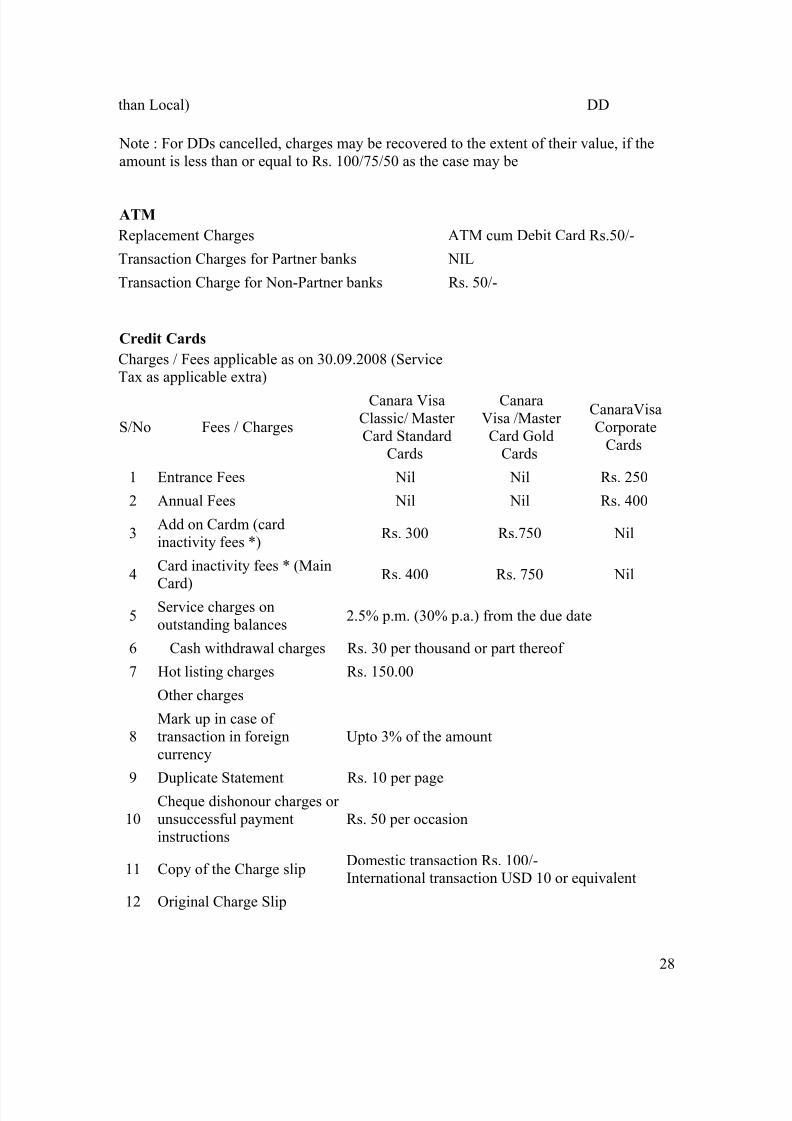

than Local) DD

Note : For DDs cancelled, charges may be recovered to the extent of their value, if theamount is less than or equal to Rs. 100/75/50 as the case may be

ATM

Replacement Charges ATM cum Debit Card Rs.50/-

Transaction Charges for Partner banks NIL

Transaction Charge for Non-Partner banks Rs. 50/-

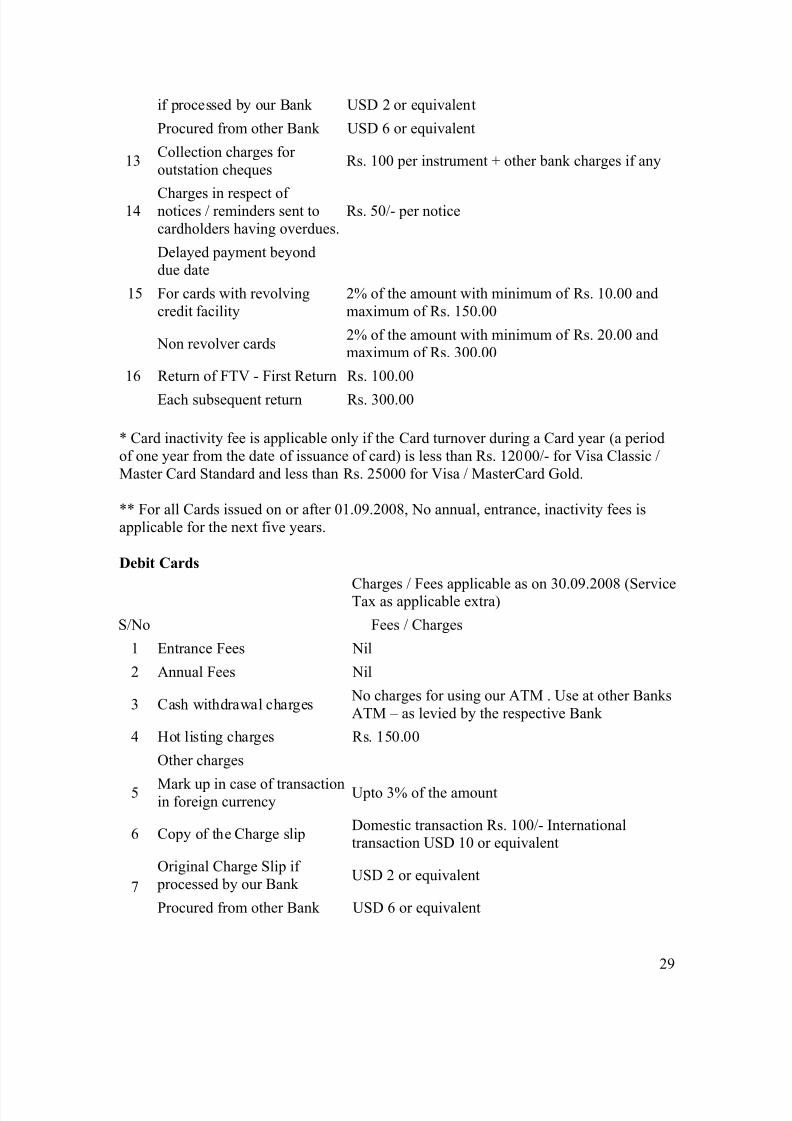

Credit Cards

Charges / Fees applicable as on 30.09.2008 (ServiceTax as applicable extra)

S/No Fees / Charges

Canara VisaClassic/ Master Card Standard

Cards

CanaraVisa /Master Card Gold

Cards

CanaraVisaCorporate

Cards

1 Entrance Fees Nil Nil Rs. 250

2 Annual Fees Nil Nil Rs. 400

3Add on Cardm (cardinactivity fees *)

Rs. 300 Rs.750 Nil

4Card inactivity fees * (Main

Card)

Rs. 400 Rs. 750 Nil

5Service charges onoutstanding balances

2.5% p.m. (30% p.a.) from the due date

6 Cash withdrawal charges Rs. 30 per thousand or part thereof

7 Hot listing charges Rs. 150.00

Other charges

8Mark up in case of transaction in foreigncurrency

Upto 3% of the amount

9 Duplicate Statement Rs. 10 per page

10Cheque dishonour charges or unsuccessful paymentinstructions

Rs. 50 per occasion

11 Copy of the Charge slipDomestic transaction Rs. 100/-International transaction USD 10 or equivalent

12 Original Charge Slip

28

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 29/45

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 30/45

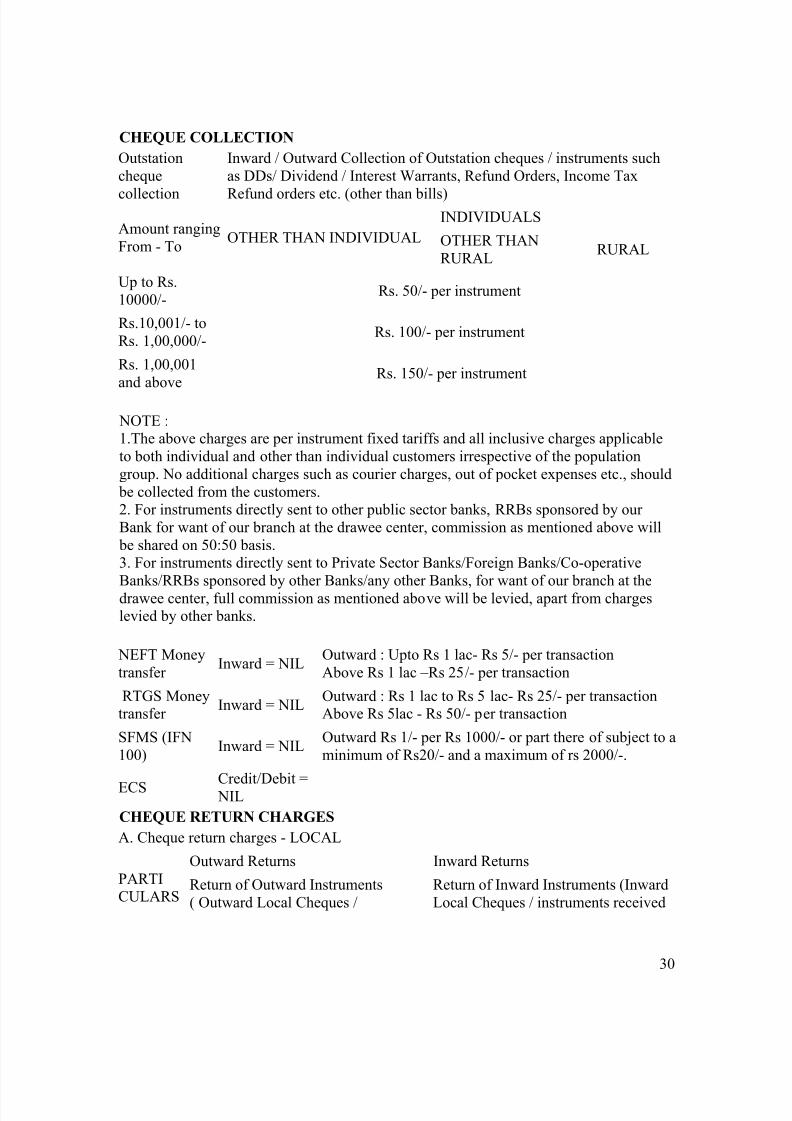

CHEQUE COLLECTION

Outstationcheque

collection

Inward / Outward Collection of Outstation cheques / instruments suchas DDs/ Dividend / Interest Warrants, Refund Orders, Income Tax

Refund orders etc. (other than bills)

Amount rangingFrom - To

OTHER THAN INDIVIDUAL

INDIVIDUALS

OTHER THANRURAL

RURAL

Up to Rs.10000/-

Rs. 50/- per instrument

Rs.10,001/- toRs. 1,00,000/-

Rs. 100/- per instrument

Rs. 1,00,001and above

Rs. 150/- per instrument

NOTE :1.The above charges are per instrument fixed tariffs and all inclusive charges applicableto both individual and other than individual customers irrespective of the populationgroup. No additional charges such as courier charges, out of pocket expenses etc., should be collected from the customers.2. For instruments directly sent to other public sector banks, RRBs sponsored by our Bank for want of our branch at the drawee center, commission as mentioned above will be shared on 50:50 basis.3. For instruments directly sent to Private Sector Banks/Foreign Banks/Co-operativeBanks/RRBs sponsored by other Banks/any other Banks, for want of our branch at thedrawee center, full commission as mentioned above will be levied, apart from chargeslevied by other banks.

NEFT Moneytransfer

Inward = NILOutward : Upto Rs 1 lac- Rs 5/- per transactionAbove Rs 1 lac –Rs 25/- per transaction

RTGS Moneytransfer

Inward = NILOutward : Rs 1 lac to Rs 5 lac- Rs 25/- per transactionAbove Rs 5lac - Rs 50/- per transaction

SFMS (IFN100)

Inward = NILOutward Rs 1/- per Rs 1000/- or part there of subject to aminimum of Rs20/- and a maximum of rs 2000/-.

ECS Credit/Debit = NIL

CHEQUE RETURN CHARGES

A. Cheque return charges - LOCAL

PARTICULARS

Outward Returns Inward Returns

Return of Outward Instruments( Outward Local Cheques /

Return of Inward Instruments (InwardLocal Cheques / instruments received

30

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 31/45

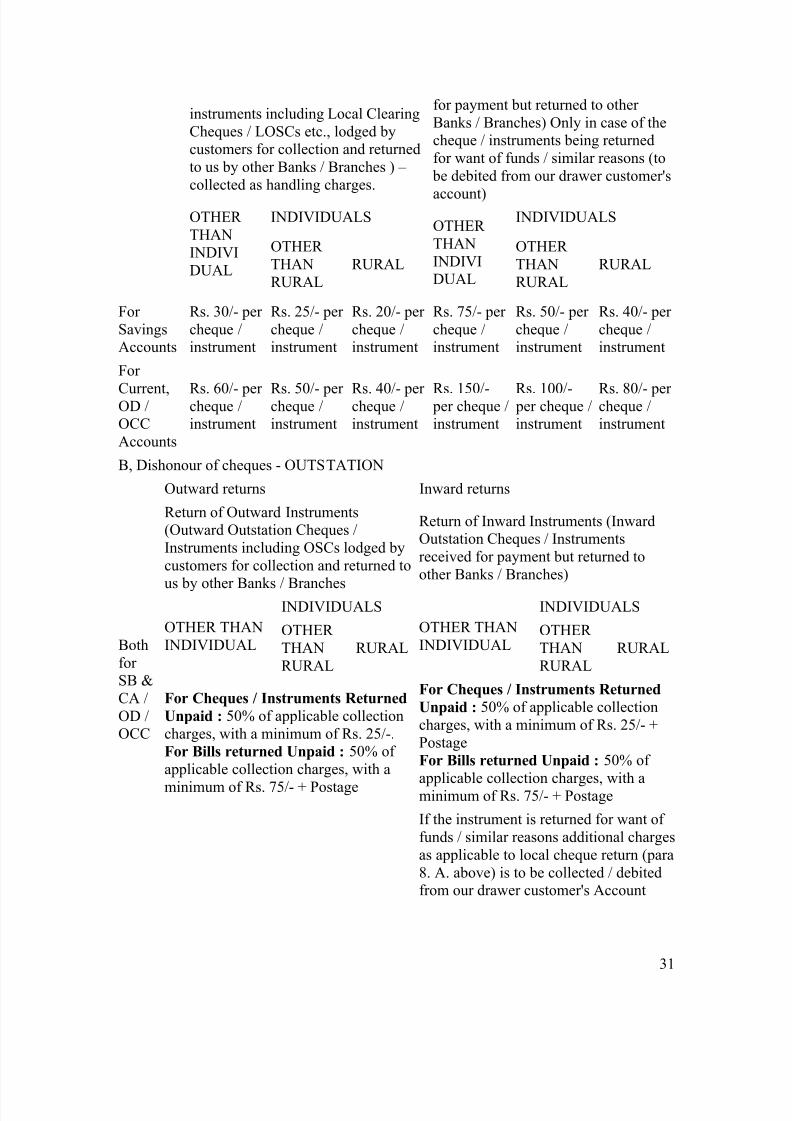

instruments including Local ClearingCheques / LOSCs etc., lodged bycustomers for collection and returnedto us by other Banks / Branches ) – collected as handling charges.

for payment but returned to other Banks / Branches) Only in case of thecheque / instruments being returnedfor want of funds / similar reasons (to be debited from our drawer customer's

account)OTHER THANINDIVIDUAL

INDIVIDUALSOTHER THANINDIVIDUAL

INDIVIDUALS

OTHER THANRURAL

RURALOTHER THANRURAL

RURAL

For SavingsAccounts

Rs. 30/- per cheque /instrument

Rs. 25/- per cheque /instrument

Rs. 20/- per cheque /instrument

Rs. 75/- per cheque /instrument

Rs. 50/- per cheque /instrument

Rs. 40/- per cheque /instrument

For

Current,OD /OCCAccounts

Rs. 60/- per cheque /instrument

Rs. 50/- per cheque /instrument

Rs. 40/- per cheque /instrument

Rs. 150/- per cheque /instrument

Rs. 100/- per cheque /instrument

Rs. 80/- per cheque /instrument

B, Dishonour of cheques - OUTSTATION

Bothfor SB &CA /OD /OCC

Outward returns Inward returns

Return of Outward Instruments(Outward Outstation Cheques /Instruments including OSCs lodged bycustomers for collection and returned to

us by other Banks / Branches

Return of Inward Instruments (InwardOutstation Cheques / Instrumentsreceived for payment but returned toother Banks / Branches)

OTHER THANINDIVIDUAL

INDIVIDUALS

OTHER THANINDIVIDUAL

INDIVIDUALS

OTHER THANRURAL

RURALOTHER THANRURAL

RURAL

For Cheques / Instruments Returned

Unpaid : 50% of applicable collectioncharges, with a minimum of Rs. 25/-.For Bills returned Unpaid : 50% of applicable collection charges, with a

minimum of Rs. 75/- + Postage

For Cheques / Instruments Returned

Unpaid : 50% of applicable collectioncharges, with a minimum of Rs. 25/- +PostageFor Bills returned Unpaid : 50% of

applicable collection charges, with aminimum of Rs. 75/- + Postage

If the instrument is returned for want of funds / similar reasons additional chargesas applicable to local cheque return (para8. A. above) is to be collected / debitedfrom our drawer customer's Account

31

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 32/45

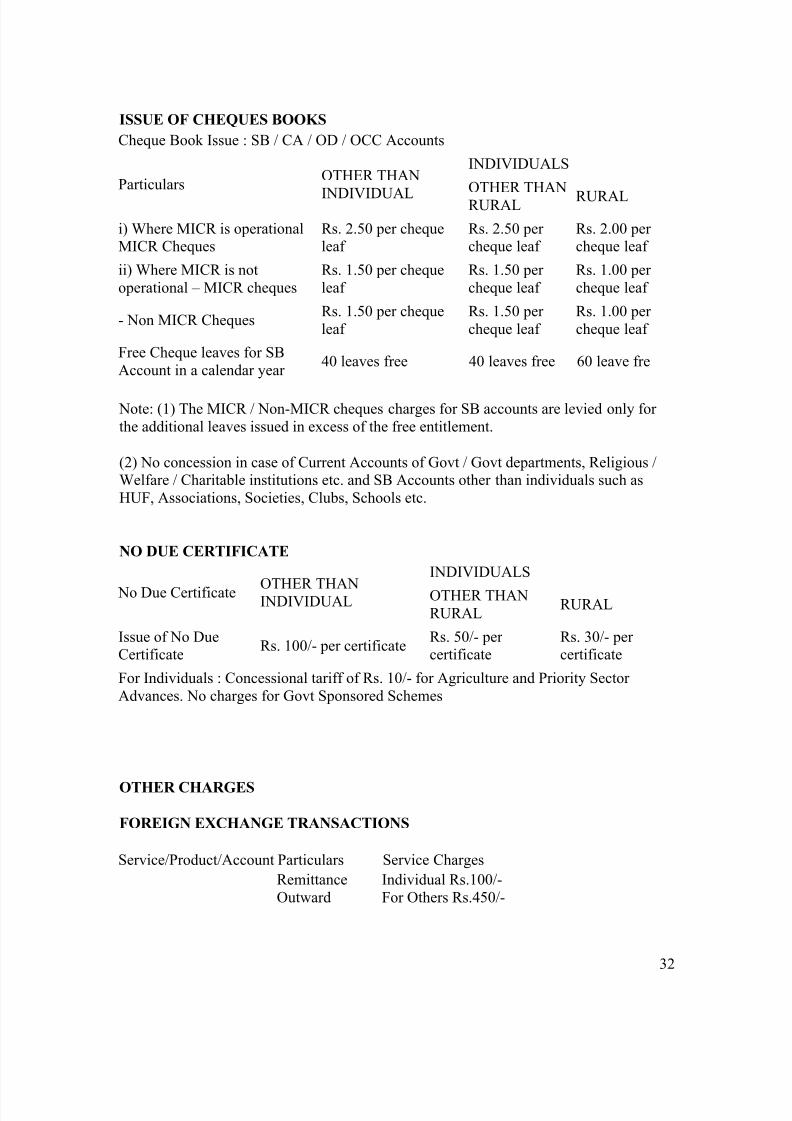

ISSUE OF CHEQUES BOOKS

Cheque Book Issue : SB / CA / OD / OCC Accounts

ParticularsOTHER THAN

INDIVIDUAL

INDIVIDUALS

OTHER THANRURAL RURAL

i) Where MICR is operationalMICR Cheques

Rs. 2.50 per chequeleaf

Rs. 2.50 per cheque leaf

Rs. 2.00 per cheque leaf

ii) Where MICR is notoperational – MICR cheques

Rs. 1.50 per chequeleaf

Rs. 1.50 per cheque leaf

Rs. 1.00 per cheque leaf

- Non MICR ChequesRs. 1.50 per chequeleaf

Rs. 1.50 per cheque leaf

Rs. 1.00 per cheque leaf

Free Cheque leaves for SBAccount in a calendar year

40 leaves free 40 leaves free 60 leave fre

Note: (1) The MICR / Non-MICR cheques charges for SB accounts are levied only for the additional leaves issued in excess of the free entitlement.

(2) No concession in case of Current Accounts of Govt / Govt departments, Religious /Welfare / Charitable institutions etc. and SB Accounts other than individuals such asHUF, Associations, Societies, Clubs, Schools etc.

NO DUE CERTIFICATE

No Due Certificate OTHER THANINDIVIDUAL

INDIVIDUALS

OTHER THANRURAL

RURAL

Issue of No DueCertificate

Rs. 100/- per certificateRs. 50/- per certificate

Rs. 30/- per certificate

For Individuals : Concessional tariff of Rs. 10/- for Agriculture and Priority Sector Advances. No charges for Govt Sponsored Schemes

OTHER CHARGES

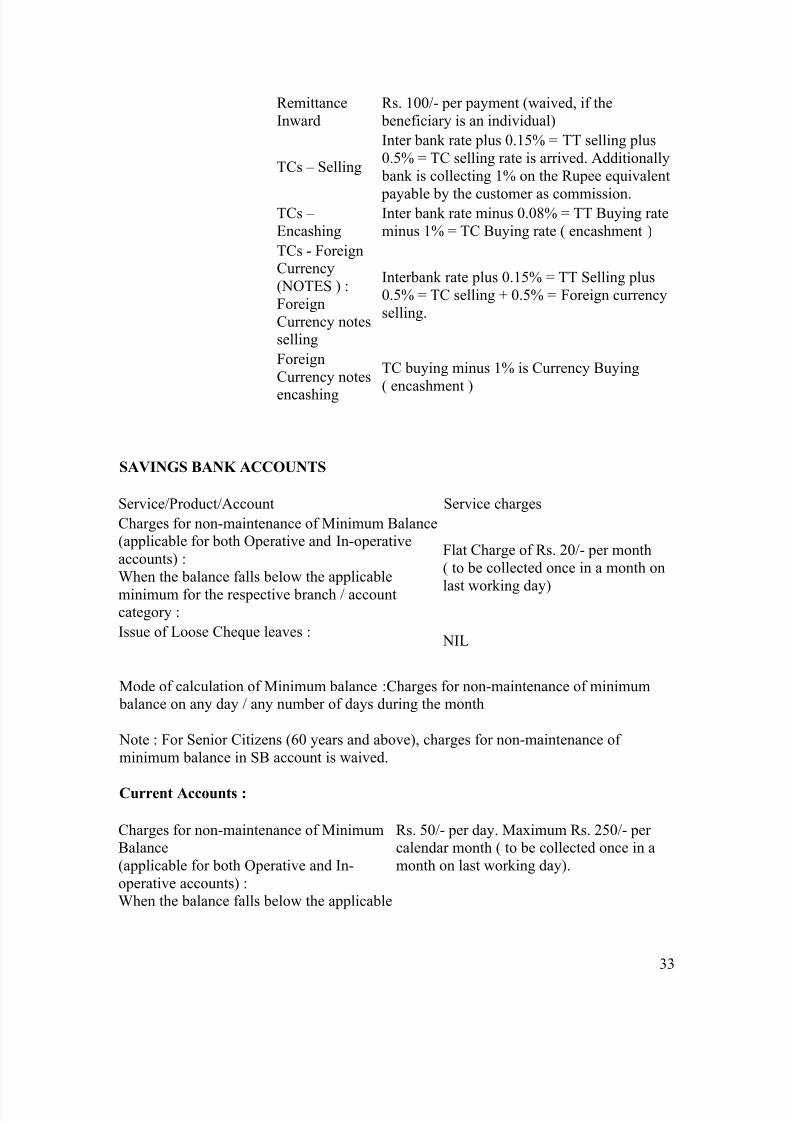

FOREIGN EXCHANGE TRANSACTIONS

Service/Product/Account Particulars Service Charges

RemittanceOutward

Individual Rs.100/-For Others Rs.450/-

32

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 33/45

RemittanceInward

Rs. 100/- per payment (waived, if the beneficiary is an individual)

TCs – Selling

Inter bank rate plus 0.15% = TT selling plus0.5% = TC selling rate is arrived. Additionally bank is collecting 1% on the Rupee equivalent

payable by the customer as commission.TCs – Encashing

Inter bank rate minus 0.08% = TT Buying rateminus 1% = TC Buying rate ( encashment )

TCs - ForeignCurrency(NOTES ) :ForeignCurrency notesselling

Interbank rate plus 0.15% = TT Selling plus0.5% = TC selling + 0.5% = Foreign currencyselling.

ForeignCurrency notes

encashing

TC buying minus 1% is Currency Buying

( encashment )

SAVINGS BANK ACCOUNTS

Service/Product/Account Service charges

Charges for non-maintenance of Minimum Balance(applicable for both Operative and In-operativeaccounts) :When the balance falls below the applicable

minimum for the respective branch / accountcategory :

Flat Charge of Rs. 20/- per month( to be collected once in a month on

last working day)

Issue of Loose Cheque leaves :

NIL

Mode of calculation of Minimum balance :Charges for non-maintenance of minimum balance on any day / any number of days during the month

Note : For Senior Citizens (60 years and above), charges for non-maintenance of minimum balance in SB account is waived.

Current Accounts :

Charges for non-maintenance of MinimumBalance(applicable for both Operative and In-operative accounts) :When the balance falls below the applicable

Rs. 50/- per day. Maximum Rs. 250/- per calendar month ( to be collected once in amonth on last working day).

33

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 34/45

minimum for the respective branch /account category :

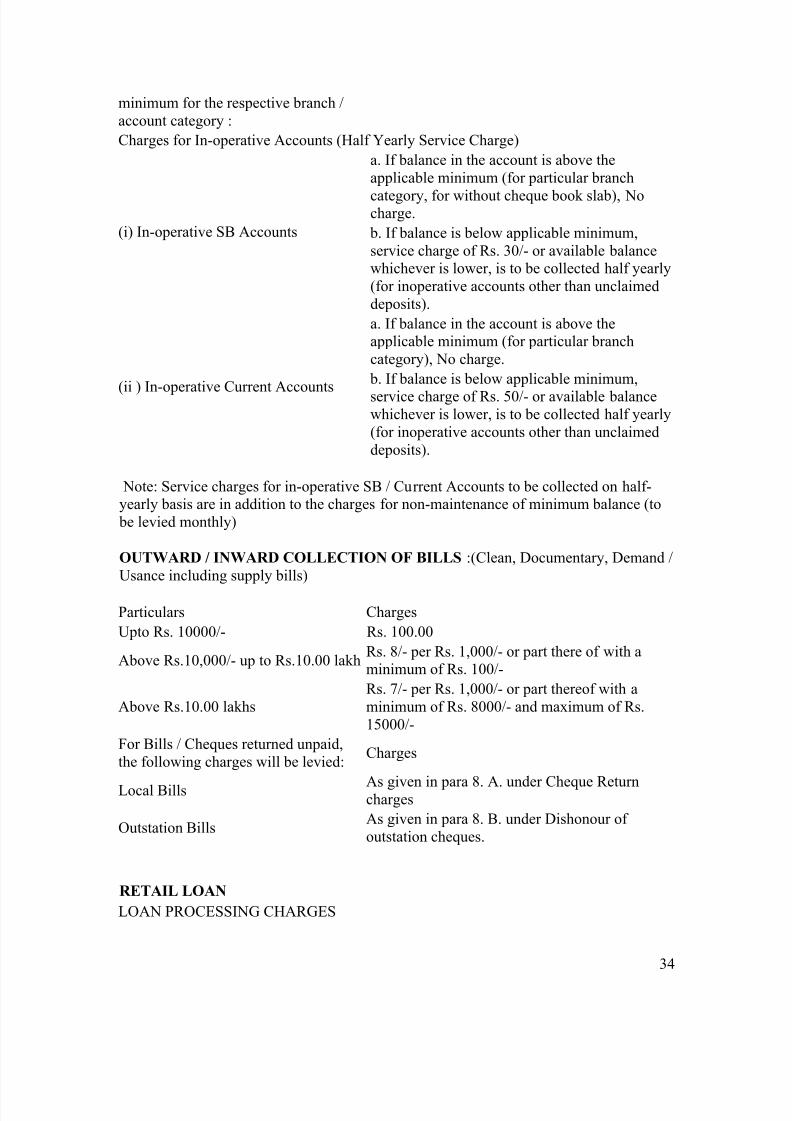

Charges for In-operative Accounts (Half Yearly Service Charge)

(i) In-operative SB Accounts

a. If balance in the account is above theapplicable minimum (for particular branch

category, for without cheque book slab), Nocharge.

b. If balance is below applicable minimum,service charge of Rs. 30/- or available balancewhichever is lower, is to be collected half yearly(for inoperative accounts other than unclaimeddeposits).

(ii ) In-operative Current Accounts

a. If balance in the account is above theapplicable minimum (for particular branchcategory), No charge.

b. If balance is below applicable minimum,

service charge of Rs. 50/- or available balancewhichever is lower, is to be collected half yearly(for inoperative accounts other than unclaimeddeposits).

Note: Service charges for in-operative SB / Current Accounts to be collected on half-yearly basis are in addition to the charges for non-maintenance of minimum balance (to be levied monthly)

OUTWARD / INWARD COLLECTION OF BILLS :(Clean, Documentary, Demand /Usance including supply bills)

Particulars Charges

Upto Rs. 10000/- Rs. 100.00

Above Rs.10,000/- up to Rs.10.00 lakhRs. 8/- per Rs. 1,000/- or part there of with aminimum of Rs. 100/-

Above Rs.10.00 lakhsRs. 7/- per Rs. 1,000/- or part thereof with aminimum of Rs. 8000/- and maximum of Rs.15000/-

For Bills / Cheques returned unpaid,the following charges will be levied:

Charges

Local Bills As given in para 8. A. under Cheque Returncharges

Outstation BillsAs given in para 8. B. under Dishonour of outstation cheques.

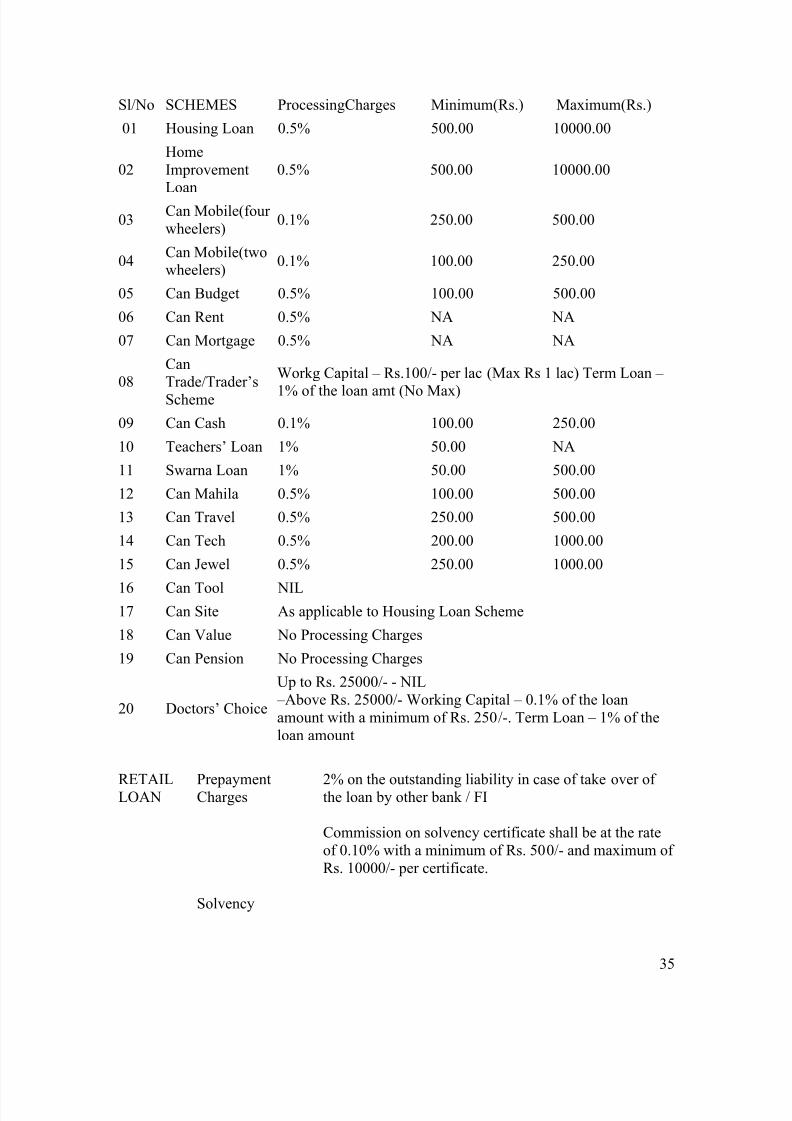

RETAIL LOAN

LOAN PROCESSING CHARGES

34

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 35/45

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 36/45

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 37/45

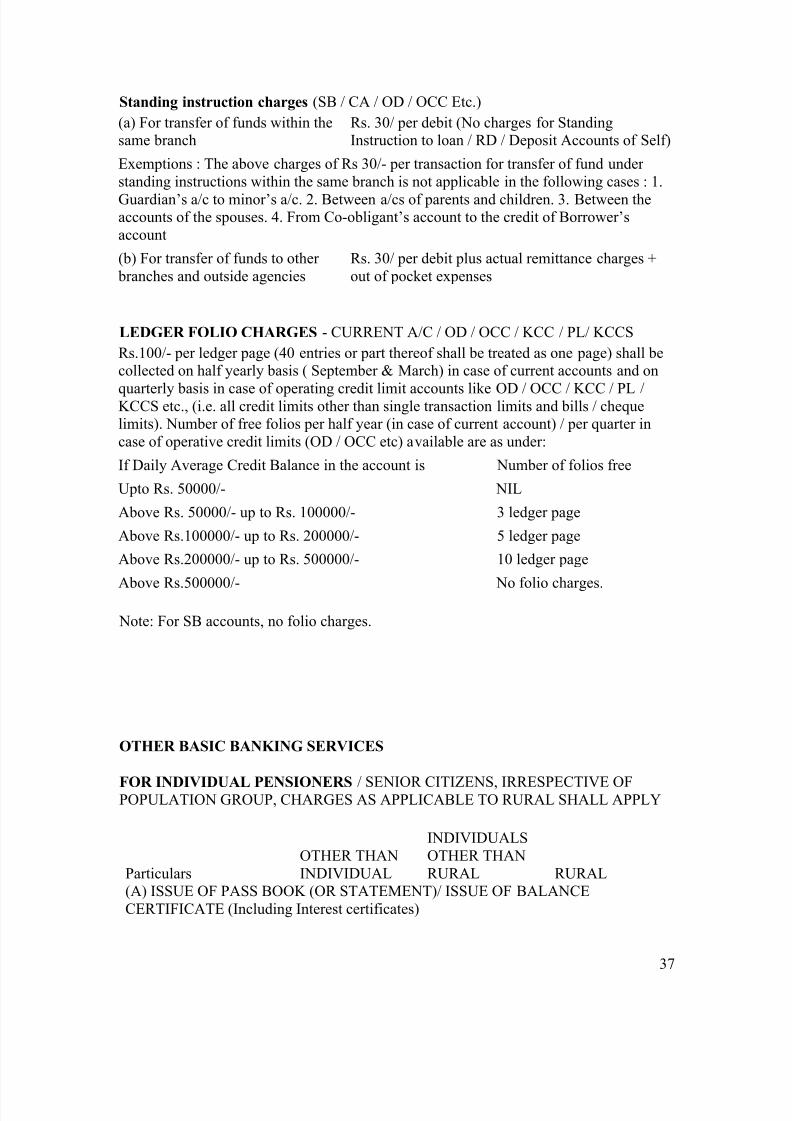

Standing instruction charges (SB / CA / OD / OCC Etc.)

(a) For transfer of funds within thesame branch

Rs. 30/ per debit (No charges for StandingInstruction to loan / RD / Deposit Accounts of Self)

Exemptions : The above charges of Rs 30/- per transaction for transfer of fund under standing instructions within the same branch is not applicable in the following cases : 1.

Guardian’s a/c to minor’s a/c. 2. Between a/cs of parents and children. 3. Between theaccounts of the spouses. 4. From Co-obligant’s account to the credit of Borrower’saccount

(b) For transfer of funds to other branches and outside agencies

Rs. 30/ per debit plus actual remittance charges +out of pocket expenses

LEDGER FOLIO CHARGES - CURRENT A/C / OD / OCC / KCC / PL/ KCCS

Rs.100/- per ledger page (40 entries or part thereof shall be treated as one page) shall becollected on half yearly basis ( September & March) in case of current accounts and on

quarterly basis in case of operating credit limit accounts like OD / OCC / KCC / PL /KCCS etc., (i.e. all credit limits other than single transaction limits and bills / chequelimits). Number of free folios per half year (in case of current account) / per quarter incase of operative credit limits (OD / OCC etc) available are as under:

If Daily Average Credit Balance in the account is Number of folios free

Upto Rs. 50000/- NIL

Above Rs. 50000/- up to Rs. 100000/- 3 ledger page

Above Rs.100000/- up to Rs. 200000/- 5 ledger page

Above Rs.200000/- up to Rs. 500000/- 10 ledger page

Above Rs.500000/- No folio charges.

Note: For SB accounts, no folio charges.

OTHER BASIC BANKING SERVICES

FOR INDIVIDUAL PENSIONERS / SENIOR CITIZENS, IRRESPECTIVE OFPOPULATION GROUP, CHARGES AS APPLICABLE TO RURAL SHALL APPLY

ParticularsOTHER THANINDIVIDUAL

INDIVIDUALSOTHER THANRURAL RURAL

(A) ISSUE OF PASS BOOK (OR STATEMENT)/ ISSUE OF BALANCECERTIFICATE (Including Interest certificates)

37

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 38/45

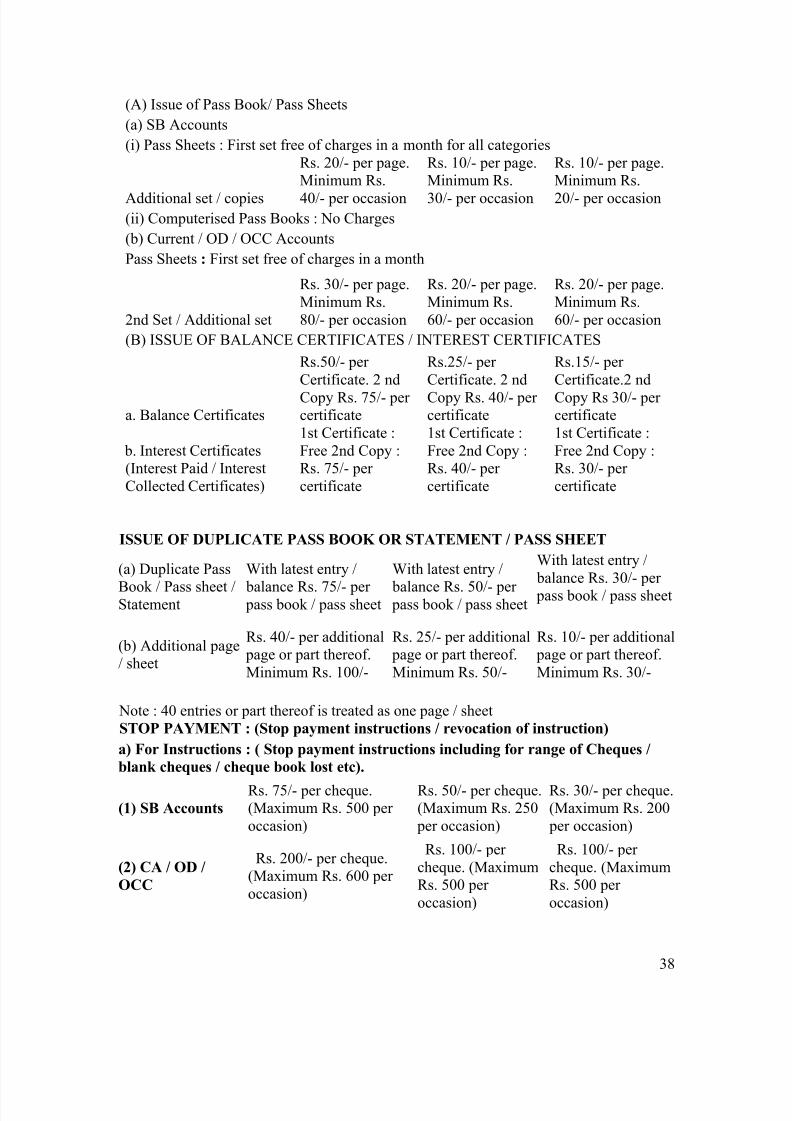

(A) Issue of Pass Book/ Pass Sheets

(a) SB Accounts

(i) Pass Sheets : First set free of charges in a month for all categories

Additional set / copies

Rs. 20/- per page.Minimum Rs.

40/- per occasion

Rs. 10/- per page.Minimum Rs.

30/- per occasion

Rs. 10/- per page.Minimum Rs.

20/- per occasion(ii) Computerised Pass Books : No Charges

(b) Current / OD / OCC Accounts

Pass Sheets : First set free of charges in a month

2nd Set / Additional set

Rs. 30/- per page.Minimum Rs.80/- per occasion

Rs. 20/- per page.Minimum Rs.60/- per occasion

Rs. 20/- per page.Minimum Rs.60/- per occasion

(B) ISSUE OF BALANCE CERTIFICATES / INTEREST CERTIFICATES

a. Balance Certificates

Rs.50/- per Certificate. 2 nd

Copy Rs. 75/- per certificate

Rs.25/- per Certificate. 2 nd

Copy Rs. 40/- per certificate

Rs.15/- per Certificate.2 nd

Copy Rs 30/- per certificate

b. Interest Certificates(Interest Paid / InterestCollected Certificates)

1st Certificate :Free 2nd Copy :Rs. 75/- per certificate

1st Certificate :Free 2nd Copy :Rs. 40/- per certificate

1st Certificate :Free 2nd Copy :Rs. 30/- per certificate

ISSUE OF DUPLICATE PASS BOOK OR STATEMENT / PASS SHEET

(a) Duplicate Pass

Book / Pass sheet /Statement

With latest entry /

balance Rs. 75/- per pass book / pass sheet

With latest entry /

balance Rs. 50/- per pass book / pass sheet

With latest entry / balance Rs. 30/- per pass book / pass sheet

(b) Additional page/ sheet

Rs. 40/- per additional page or part thereof.Minimum Rs. 100/-

Rs. 25/- per additional page or part thereof.Minimum Rs. 50/-

Rs. 10/- per additional page or part thereof.Minimum Rs. 30/-

Note : 40 entries or part thereof is treated as one page / sheetSTOP PAYMENT : (Stop payment instructions / revocation of instruction)

a) For Instructions : ( Stop payment instructions including for range of Cheques /

blank cheques / cheque book lost etc).

(1) SB AccountsRs. 75/- per cheque.(Maximum Rs. 500 per occasion)

Rs. 50/- per cheque.(Maximum Rs. 250 per occasion)

Rs. 30/- per cheque.(Maximum Rs. 200 per occasion)

(2) CA / OD /

OCC

Rs. 200/- per cheque.(Maximum Rs. 600 per occasion)

Rs. 100/- per cheque. (MaximumRs. 500 per occasion)

Rs. 100/- per cheque. (MaximumRs. 500 per occasion)

38

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 39/45

b) Cancellation /

Revocation of

Instruction

Rs. 30/- flat (SB / CA)Rs. 20/- flat (SB /CA)

Rs. 10/- flat (SB /CA)

BALANCE ENQUIRY ( Including Inquiries for old records)a) Inquiries up to six months :

SB / CA / OD (All type of

Accounts)Free of Charge Free of Charge Free of Charge

b) Entries above 6 months up to 1 yr old :

(i) Savings Bank

Accounts :Rs. 75/- per entry. Rs. 50/- per entry. Rs. 25/- per entry.

(ii) Current Account / OD

/ OCC A/csRs. 150/- per entry. Rs. 100/- per entry. Rs. 50/- per entry.

(iii) Other type of accounts : Same as applicableto SB Same as applicableto SB Same as applicableto SB

Note: For entries above one year old, Branch manger has discretion to levy extra chargesto (b) above, based on time spent / work involved. Copies of documents / cheques etc atcustomer's cost.

ACCOUNT CLOSURE : (Closure of SB / CA before one year)

a) SB Accounts -

(i) With Cheque Book

facility

Rs. 150/- per

account

Rs. 100/- per

account

Rs. 50/- per

account

(ii) Without Cheque Book

facility

Rs. 100/- per

account

Rs. 50/- per

account

Rs. 25/- per

account

b) Current AccountsRs. 750/- per

account

Rs. 500/- per

account

Rs. 150/- per

account

Exemptions: (1) Transfer from branch to branch. (2) Opening another account in joint names. (3)

Death of the account holder

SIGNATURE VERIFICATION

Signature Verification includingattestation of customer's signature/ photos

Rs. 100/- per attestation / case.

Rs. 50/- per attestation / case.

Rs. 30/- per attestation /case..

DEMAND DRAFT

A DEMAND DRAFT REVALIDATION : (both for local and outstation)

39

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 40/45

Revalidation of DD / Local DDRs. 75/- flat per DD

Rs. 50/- flat per DD

Rs. 25/- flat per DD

B DEMAND DRAFT DUPLICATE ISSUANCE (both for local and outstation)

Issue of Duplicate DDRs. 100/- per DD, upto Rs.10000/-

Rs. 75/- per DD,

upto Rs. 10000/-

Rs. 50/- per DD, upto

Rs. 10000/-

- For DDs above Rs. 10000/-

50% of applicablecommissionsubject tominimum of Rs.100/- per DD

50% of applicablecommissionsubject tominimum of Rs.75/- per DD

50% of applicablecommission subjectto minimum of Rs.50/- per DD

Collection of Dividend / Interest Warrants / Refund Orders for Individuals –

Concession

Concession to individualcustomers

No concession

If value of instrument is upto Rs. 500/-, Nocharges. OnlyOPE + Postage

If value of instrument is up toRs. 500/-, Nocharges. Only OPE+ Postage

For instruments above Rs. 500/- Normal Collection charges

TARIFF STRUCTURE FOR AWB / CBS CHARGES.

i) INTRACITY TRANSACTIONS (Branches located in the same centre)

Type of Transaction Revised charges for AWB / CBS branches

a) Remittance of Cash

SB Accounts Free

CA / OD / OCC AccountsUp to Rs. 25000/- perday

No Charges

Above Rs. 25000/-

Re. 1/- per Rs. 1000/- or partthereof Minimum Rs. 25/-

Maximum Rs. 5000/- b) Cash withdrawal Free

c) Funds transfer Free

d) Clearing Free

e) Issue of DDs Normal DD charges

ii) INTERCITY TRANSACTIONS : (Outstation Branches)

40

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 41/45

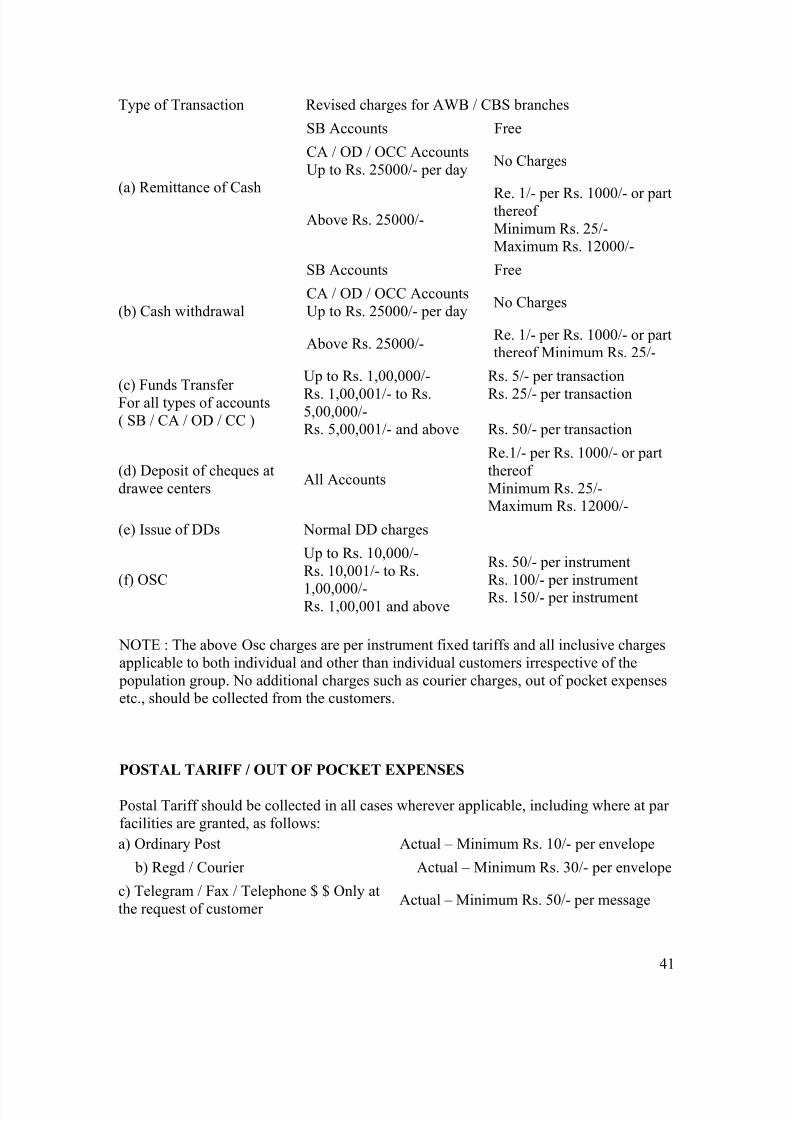

Type of Transaction Revised charges for AWB / CBS branches

(a) Remittance of Cash

SB Accounts Free

CA / OD / OCC AccountsUp to Rs. 25000/- per day

No Charges

Above Rs. 25000/-Re. 1/- per Rs. 1000/- or partthereof Minimum Rs. 25/-Maximum Rs. 12000/-

(b) Cash withdrawal

SB Accounts Free

CA / OD / OCC AccountsUp to Rs. 25000/- per day

No Charges

Above Rs. 25000/-Re. 1/- per Rs. 1000/- or partthereof Minimum Rs. 25/-

(c) Funds Transfer For all types of accounts( SB / CA / OD / CC )

Up to Rs. 1,00,000/-

Rs. 1,00,001/- to Rs.5,00,000/-Rs. 5,00,001/- and above

Rs. 5/- per transaction

Rs. 25/- per transaction

Rs. 50/- per transaction

(d) Deposit of cheques atdrawee centers

All Accounts

Re.1/- per Rs. 1000/- or partthereof Minimum Rs. 25/-Maximum Rs. 12000/-

(e) Issue of DDs Normal DD charges

(f) OSC

Up to Rs. 10,000/-Rs. 10,001/- to Rs.

1,00,000/-Rs. 1,00,001 and above

Rs. 50/- per instrumentRs. 100/- per instrumentRs. 150/- per instrument

NOTE : The above Osc charges are per instrument fixed tariffs and all inclusive chargesapplicable to both individual and other than individual customers irrespective of the population group. No additional charges such as courier charges, out of pocket expensesetc., should be collected from the customers.

POSTAL TARIFF / OUT OF POCKET EXPENSES

Postal Tariff should be collected in all cases wherever applicable, including where at par facilities are granted, as follows:

a) Ordinary Post Actual – Minimum Rs. 10/- per envelope

b) Regd / Courier Actual – Minimum Rs. 30/- per envelope

c) Telegram / Fax / Telephone $ $ Only atthe request of customer

Actual – Minimum Rs. 50/- per message

41

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 42/45

Note :: 1) Postages / Out of Pocket expenses are in addition to service charges applicable.2) If two or more instruments favouring a single party are sent to the same branch / officeof a bank together, in common single cover by post, in such cases postal tariff mentionedabove as applicable to single cover / instrument may be collected. 3) If a singleinstrument is collected and credited to number of accounts actual / minimum postage may

be shared amongst beneficiaries subject to minimum of Re.1/- per credit / customer.

Ratio Analysis

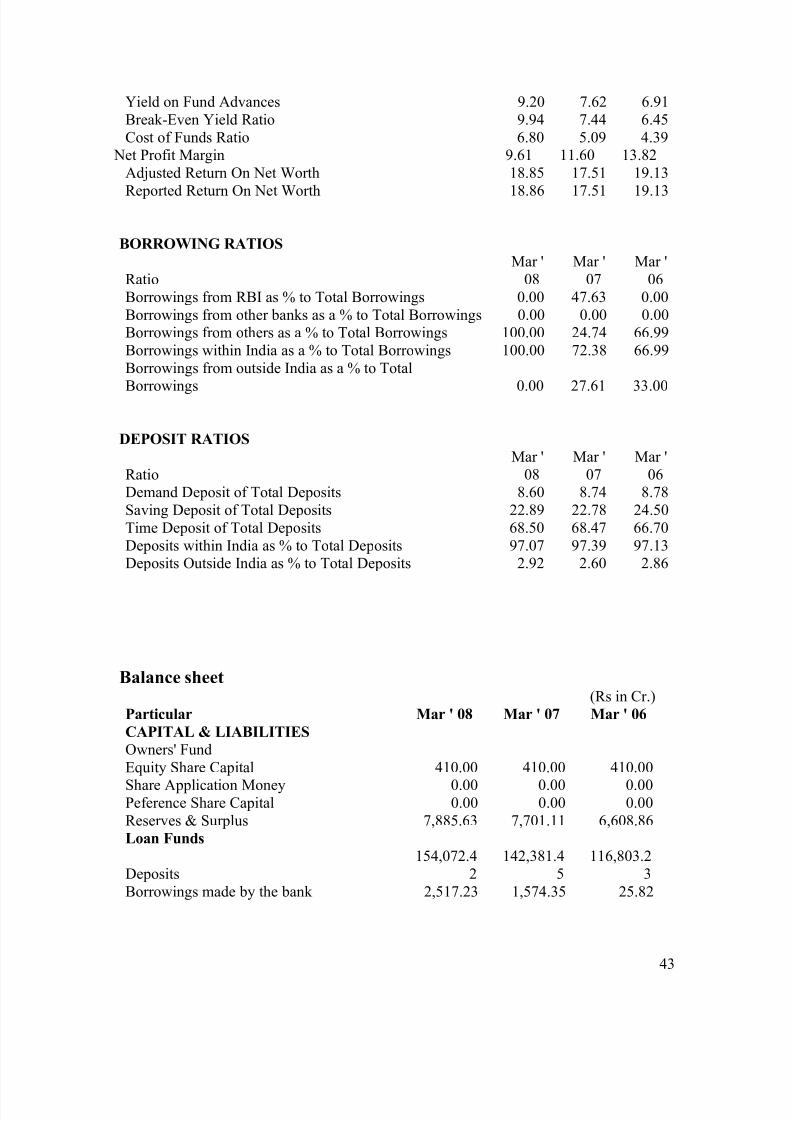

EARNINGS RATIOS

RatioMar '

08Mar '

07Mar '

06Income from Fund Advances as a % of Op Income 63.61 64.87 60.31

Operating Income as a % of Working Funds 14.47 11.74 11.45Fund based income as a % of Op Income 95.22 96.05 95.37Fee based income as a % of Op Income 4.77 3.94 4.62

PROFITABLITY RATIOS

RatioMar '

08Mar '

07Mar '

06

42

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 43/45

Yield on Fund Advances 9.20 7.62 6.91Break-Even Yield Ratio 9.94 7.44 6.45Cost of Funds Ratio 6.80 5.09 4.39 Net Profit Margin 9.61 11.60 13.82Adjusted Return On Net Worth 18.85 17.51 19.13

Reported Return On Net Worth 18.86 17.51 19.13

BORROWING RATIOS

RatioMar '

08Mar '

07Mar '

06Borrowings from RBI as % to Total Borrowings 0.00 47.63 0.00Borrowings from other banks as a % to Total Borrowings 0.00 0.00 0.00Borrowings from others as a % to Total Borrowings 100.00 24.74 66.99Borrowings within India as a % to Total Borrowings 100.00 72.38 66.99Borrowings from outside India as a % to Total

Borrowings 0.00 27.61 33.00

DEPOSIT RATIOS

RatioMar '

08Mar '

07Mar '

06Demand Deposit of Total Deposits 8.60 8.74 8.78Saving Deposit of Total Deposits 22.89 22.78 24.50Time Deposit of Total Deposits 68.50 68.47 66.70Deposits within India as % to Total Deposits 97.07 97.39 97.13Deposits Outside India as % to Total Deposits 2.92 2.60 2.86

Balance sheet(Rs in Cr.)

Particular Mar ' 08 Mar ' 07 Mar ' 06

CAPITAL & LIABILITIES

Owners' FundEquity Share Capital 410.00 410.00 410.00

Share Application Money 0.00 0.00 0.00Peference Share Capital 0.00 0.00 0.00Reserves & Surplus 7,885.63 7,701.11 6,608.86Loan Funds

Deposits154,072.4

2142,381.4

5116,803.2

3Borrowings made by the bank 2,517.23 1,574.35 25.82

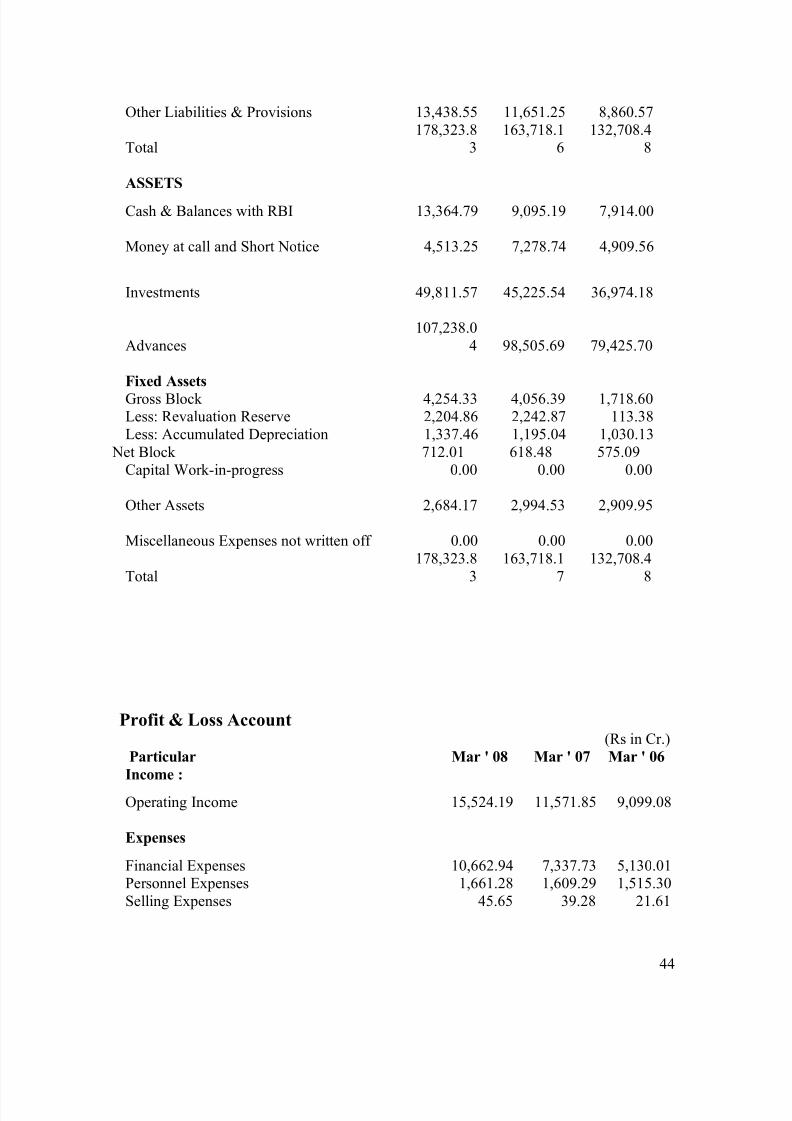

43

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 44/45

Other Liabilities & Provisions 13,438.55 11,651.25 8,860.57

Total178,323.8

3163,718.1

6132,708.4

8 ASSETS

Cash & Balances with RBI 13,364.79 9,095.19 7,914.00 Money at call and Short Notice 4,513.25 7,278.74 4,909.56

Investments 49,811.57 45,225.54 36,974.18

Advances107,238.0

4 98,505.69 79,425.70 Fixed Assets Gross Block 4,254.33 4,056.39 1,718.60Less: Revaluation Reserve 2,204.86 2,242.87 113.38Less: Accumulated Depreciation 1,337.46 1,195.04 1,030.13 Net Block 712.01 618.48 575.09Capital Work-in-progress 0.00 0.00 0.00 Other Assets 2,684.17 2,994.53 2,909.95 Miscellaneous Expenses not written off 0.00 0.00 0.00

Total178,323.8

3163,718.1

7132,708.4

8

Profit & Loss Account (Rs in Cr.)

Particular Mar ' 08 Mar ' 07 Mar ' 06

Income :

Operating Income 15,524.19 11,571.85 9,099.08 Expenses

Financial Expenses 10,662.94 7,337.73 5,130.01Personnel Expenses 1,661.28 1,609.29 1,515.30Selling Expenses 45.65 39.28 21.61

44

8/6/2019 19147914 Canara Bank Assignment

http://slidepdf.com/reader/full/19147914-canara-bank-assignment 45/45

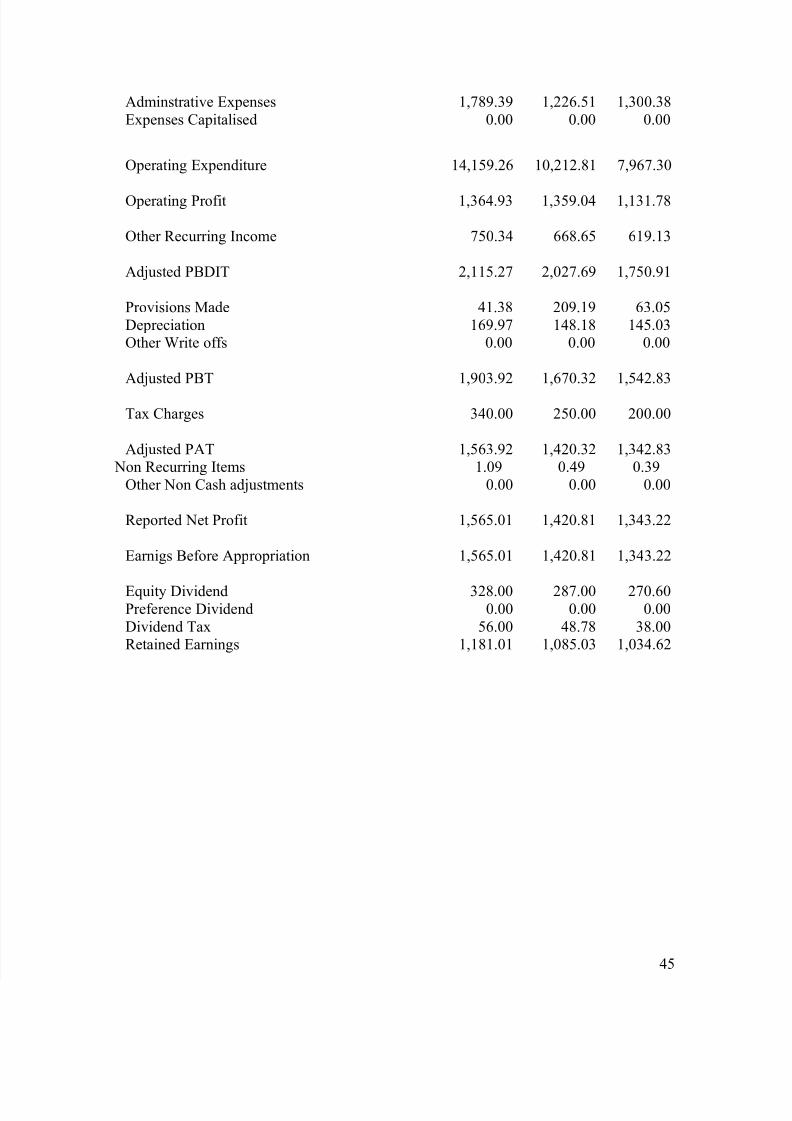

Adminstrative Expenses 1,789.39 1,226.51 1,300.38Expenses Capitalised 0.00 0.00 0.00

Operating Expenditure 14,159.26 10,212.81 7,967.30

Operating Profit 1,364.93 1,359.04 1,131.78 Other Recurring Income 750.34 668.65 619.13 Adjusted PBDIT 2,115.27 2,027.69 1,750.91 Provisions Made 41.38 209.19 63.05Depreciation 169.97 148.18 145.03Other Write offs 0.00 0.00 0.00 Adjusted PBT 1,903.92 1,670.32 1,542.83

Tax Charges 340.00 250.00 200.00 Adjusted PAT 1,563.92 1,420.32 1,342.83 Non Recurring Items 1.09 0.49 0.39Other Non Cash adjustments 0.00 0.00 0.00 Reported Net Profit 1,565.01 1,420.81 1,343.22 Earnigs Before Appropriation 1,565.01 1,420.81 1,343.22

Equity Dividend 328.00 287.00 270.60Preference Dividend 0.00 0.00 0.00Dividend Tax 56.00 48.78 38.00Retained Earnings 1,181.01 1,085.03 1,034.62