17-1 Similarities and Differences Between Job Order Cost and Process Cost Systems Job Order Cost ...

43

17-1 Similarities and Differences Between Job Order Cost and Process Cost Systems Job Order Cost Costs assigned to each job. Products have unique characteristics. Process Cost Costs tracked through a series of connected mfg processes or departments … (mixing, baking, packaging etc). Products are uniform or identical (homogenous) and produced in a large volume. Nature of Process Cost Systems Nature of Process Cost Systems

-

Upload

wilfred-perkins -

Category

Documents

-

view

225 -

download

3

Transcript of 17-1 Similarities and Differences Between Job Order Cost and Process Cost Systems Job Order Cost ...

17-1

Similarities and Differences Between Job Order Cost and Process Cost Systems

Job Order Cost

Costs assigned to each job.

Products have unique characteristics.

Process Cost

Costs tracked through a series of connected mfg processes or departments … (mixing, baking, packaging etc).

Products are uniform or identical (homogenous) and produced in a large volume.

Nature of Process Cost SystemsNature of Process Cost Systems

17-2

Illustration 17-2

Process and Job Cost Comparison

Nature of Process Cost SystemsNature of Process Cost Systems

17-3

Nature of Process Cost SystemsNature of Process Cost Systems

Every production department has it’s own Work-In-Process account.

If you have 5 departments you have 5 “Work-In-Process” accounts

One Work In Process Account

17-4

Process Cost Flow

Illustration 17-5

TCorp makes skateboard wheels. Manufacturing consists of two

processes: machining and assembly. Machining Dept shapes &

drills materials. Assembly Dept assembles & packages the parts.

Nature of Process Cost SystemsNature of Process Cost Systems

17-5

Assigning Manufacturing Costs

Handling materials, labor, and overhead same as in Ch 16.

► Debit Raw Materials Inv for purchases of raw materials

CREDIT W-I-P to assign direct materials costs.

► Debit Factory Labor for factory labor incurred.

CREDIT W-I-P to assign direct labor costs.

► Debit Factory (Mfg) Overhead for actual cost incurred

CREDIT W-I-P to apply (estimated) Mfg Overhead costs.

Use of more than one W-I-P (Work-In-Process) is different

in “process cost” (ch 17) versus “job order cost” (Ch 16)

17-6

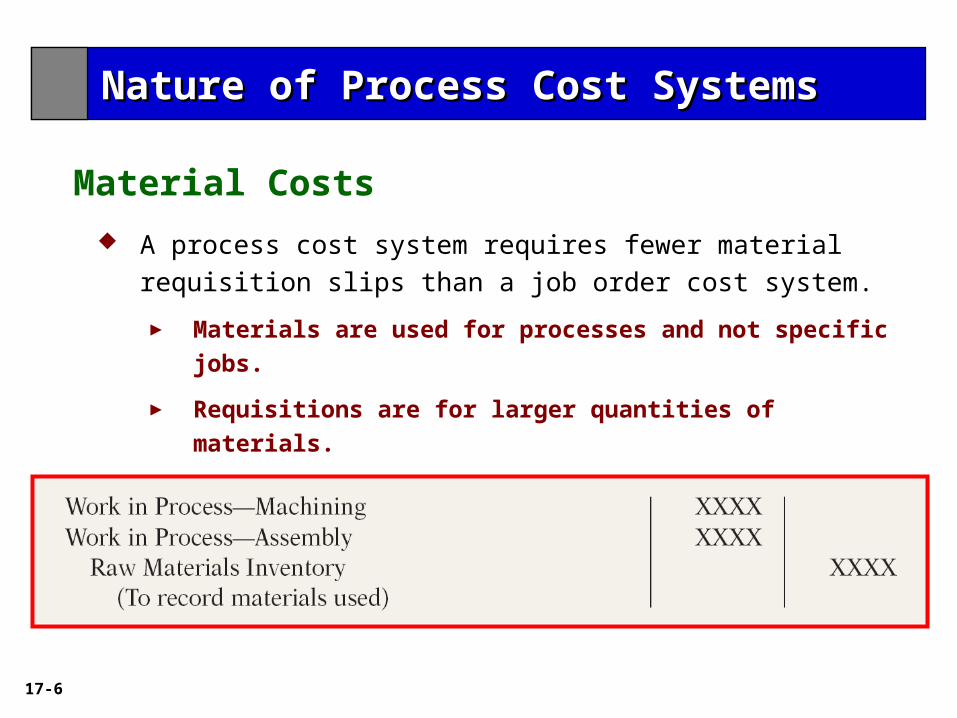

A process cost system requires fewer material requisition

slips than a job order cost system.

► Materials are used for processes and not specific jobs.

► Requisitions are for larger quantities of materials.

► Journal entry to record materials used:

Material Costs

Nature of Process Cost SystemsNature of Process Cost Systems

17-7

Handling materials, labor, and overhead same as in Ch 16.

► Debit Raw Materials Inv for purchases of raw materials

CREDIT W-I-P to assign direct materials costs.

► Debit Factory Labor for factory labor incurred.

CREDIT W-I-P to assign direct labor costs.

► Debit Factory (Mfg) Overhead for actual cost incurred

CREDIT W-I-P to apply (estimated) Mfg Overhead costs.

Use of more than one W-I-P (Work-In-Process) is different

in “process cost” (ch 17) versus “job order cost” (Ch 16)

Assigning Manufacturing Costs

17-8

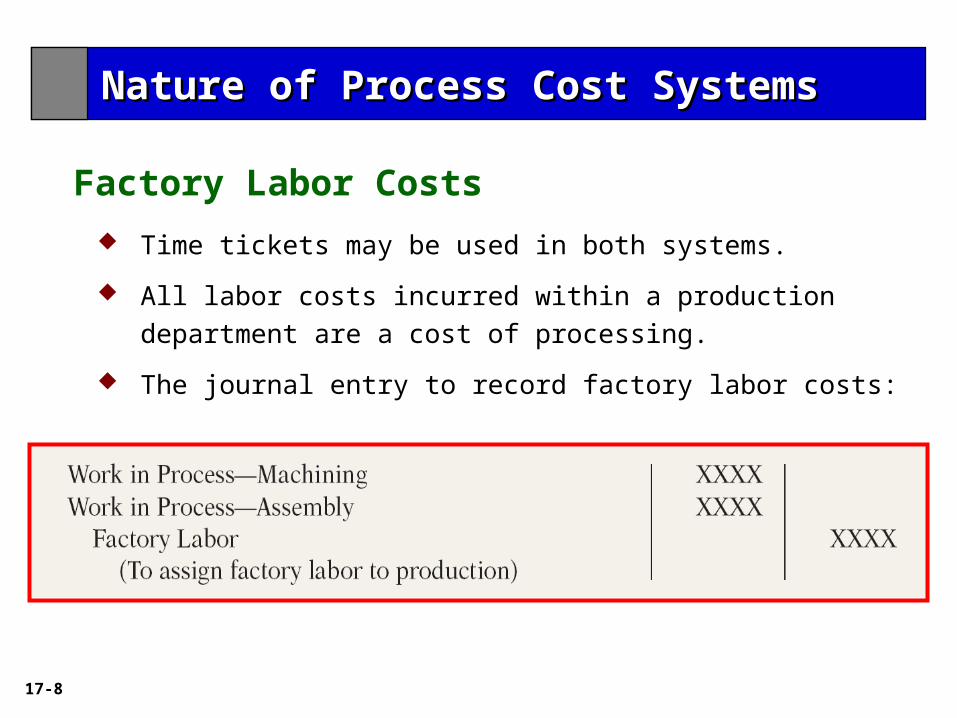

Time tickets may be used in both systems.

All labor costs incurred within a production department are

a cost of processing.

The journal entry to record factory labor costs:

Nature of Process Cost SystemsNature of Process Cost Systems

Factory Labor Costs

17-9

Handling materials, labor, and overhead same as in Ch 16.

► Debit Raw Materials Inv for purchases of raw materials

CREDIT W-I-P to assign direct materials costs.

► Debit Factory Labor for factory labor incurred.

CREDIT W-I-P to assign direct labor costs.

► Debit Factory (Mfg) Overhead for actual cost incurred

CREDIT W-I-P to apply (estimated) Mfg Overhead costs.

Use of more than one W-I-P (Work-In-Process) is different

in “process cost” (ch 17) versus “job order cost” (Ch 16)

Assigning Manufacturing Costs

17-10

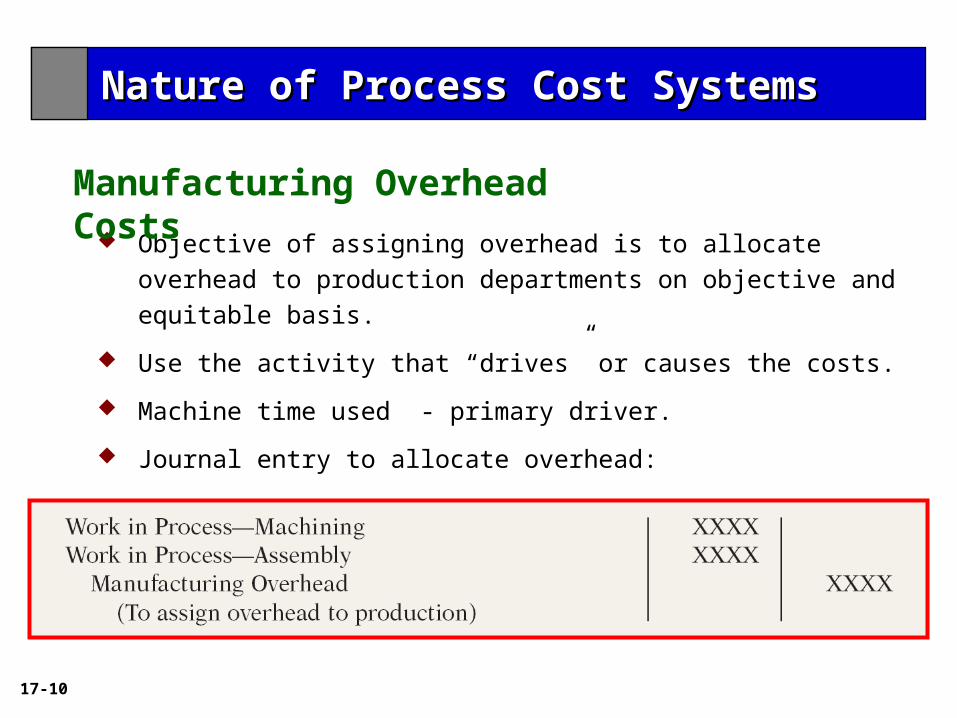

Objective of assigning overhead is to allocate overhead to

production departments on objective and equitable basis.

Use the activity that “drives” or causes the costs.

Machine time used - primary driver.

Journal entry to allocate overhead:

Manufacturing Overhead Costs

Nature of Process Cost SystemsNature of Process Cost Systems

17-11

Nature of Process Cost SystemsNature of Process Cost Systems

17-12

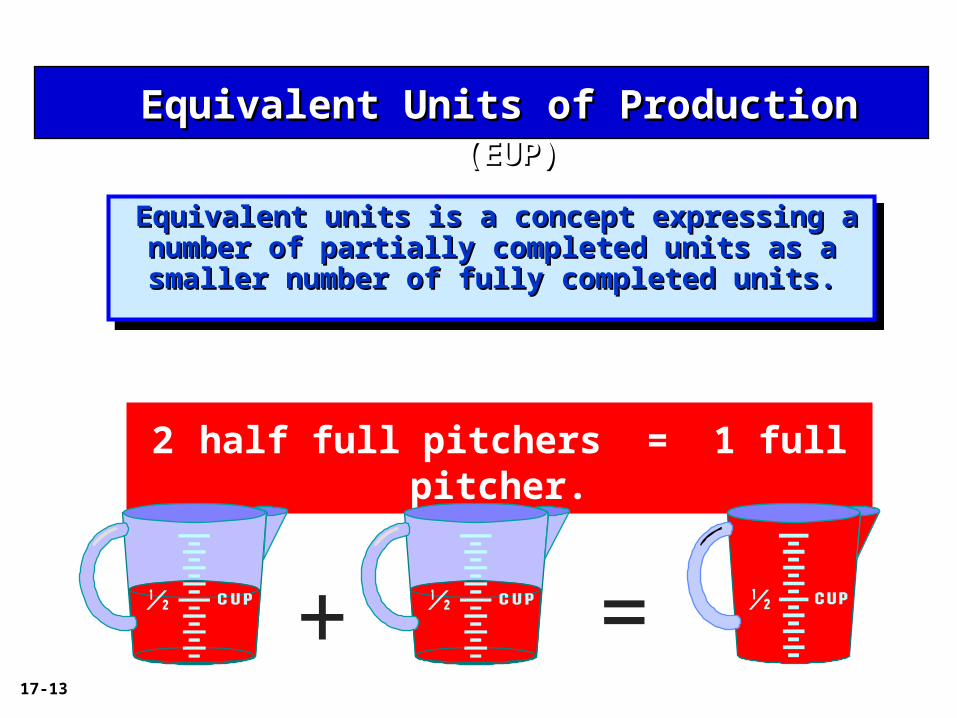

Equivalent Units of Production Equivalent Units of Production (EUP)(EUP)

A term used in cost accounting to arrive at the cost per unit.

* associated with the units that are not completed at the end of an accounting period (work-in-process).

* indicates how much work was done on the work units that are still in-process units at the end of a designated period.

* basically, all of the work-in-process inventory at the end of a period is expressed as fully-completed units which gives us the equivalent units of production.

17-13

Equivalent units is a concept expressing a Equivalent units is a concept expressing a number of partially completed units as a number of partially completed units as a smaller number of fully completed units.smaller number of fully completed units.

Equivalent units is a concept expressing a Equivalent units is a concept expressing a number of partially completed units as a number of partially completed units as a smaller number of fully completed units.smaller number of fully completed units.

2 half full pitchers = 1 full pitcher.

+ =

Equivalent Units of Production Equivalent Units of Production (EUP)(EUP)

17-14

Illustration: Suppose a professor is asked to compute the cost of instruction per full-time equivalent student at your college. The college’s finance dept. provides the following information.

Costs:

Total cost of instruction $9,000,000

Student population:

Full-time students 900

Part-time students 1,000

Illustration 17-6

Equivalent UnitsEquivalent Units

17-15

Total cost of instruction $9,000,000

Number of full-time equivalent students / 1,500

$ 6,000

Illustration 17-7

Illustration: Part-time students take 60% of the classes of a full-time student during the year. To compute the number of full-time equivalent students per year, you would make the following computation.

Cost of instruction per full-time equivalent student =

Equivalent UnitsEquivalent Units

17-16

Considers the degree of completion (weighting) of

units completed and transferred out and units in ending

work in process.

Most widely used method.

Beginning work in process not part of computation of

equivalent units.Illustration 17-8

Equivalent UnitsEquivalent Units

Weighted Average Method

17-17

Illustration: Output of the Packaging Dept consists of:

•10,000 units completed and transferred out,

•5,000 units in ending W-I-P which are 70% completed.

Calculate the equivalent units of production.

Completed units …………………...... __________

Work in process equivalent units …. __________

Equivalent UnitsEquivalent Units

Weighted Average Method

17-18

Illustration: Output of the Packaging Dept consists of:

•10,000 units completed and transferred out,

•5,000 units in ending W-I-P which are 70% completed.

Calculate the equivalent units of production.

Equivalent UnitsEquivalent Units

Weighted Average Method

Completed units ………………………… 10,000Work in process EU (5,000 x 70%) ……. 3,500

13,500

17-19

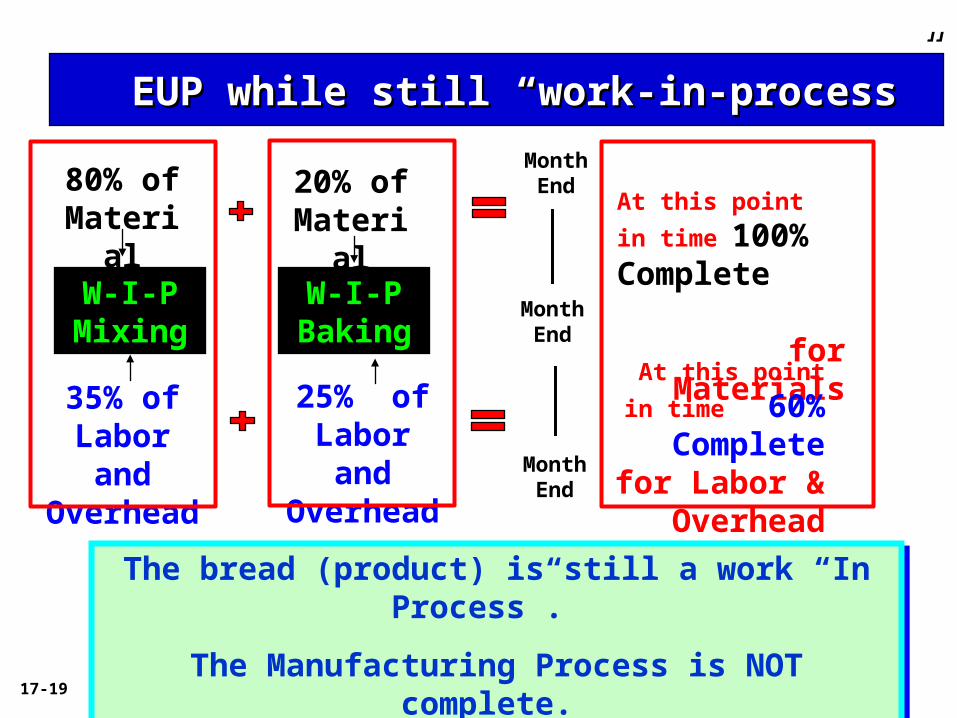

The bread (product) is still a work “In Process”.

The Manufacturing Process is NOT complete.

The bread (product) is still a work “In Process”.

The Manufacturing Process is NOT complete.

W-I-P Baking

25% ofLabor andOverhead

20% ofMaterial

W-I-P Mixing

80% ofMaterial

35% ofLabor andOverhead

EUP while still “work-in-process”EUP while still “work-in-process”

At this point in time

100% Complete

for Materials

At this point in time

60% Complete for Labor &

Overhead

Month End

Month End

Month End

17-20

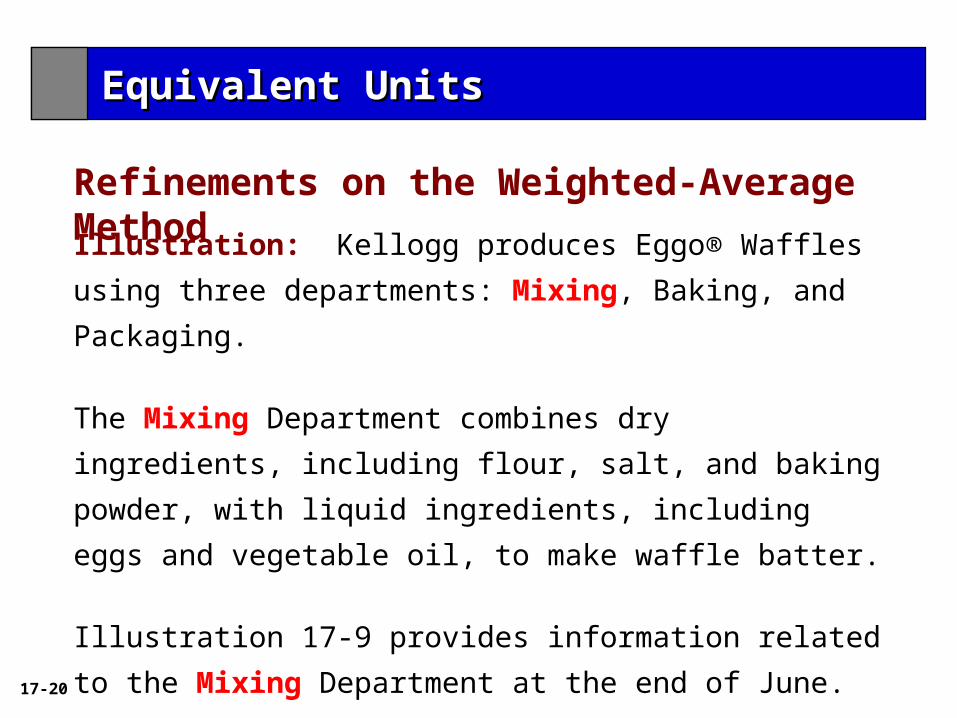

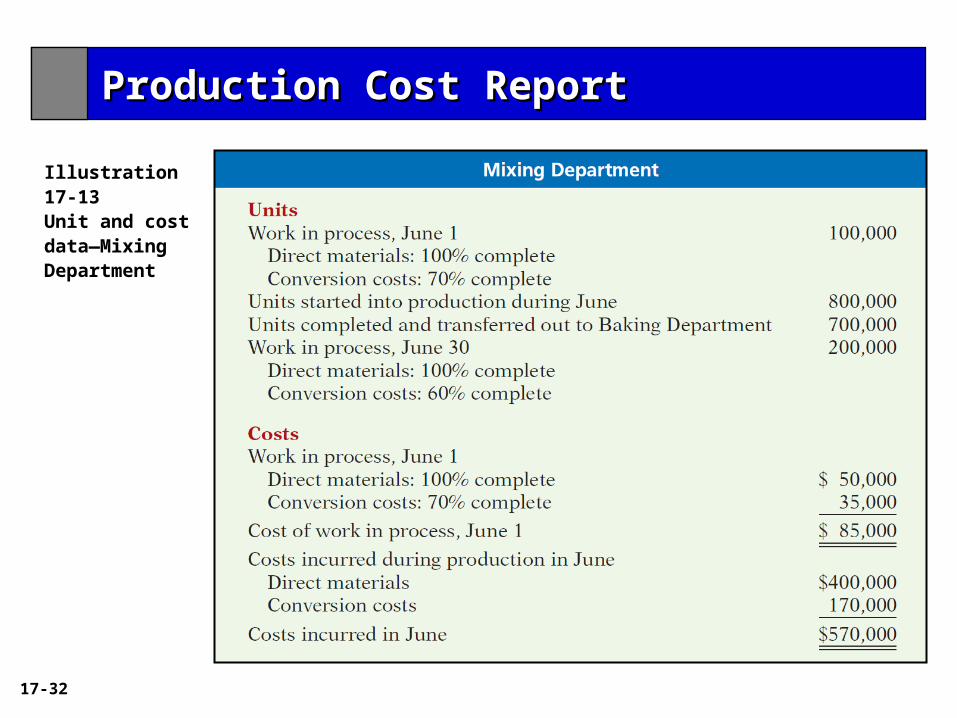

Illustration: Kellogg produces Eggo® Waffles using three

departments: Mixing, Baking, and Packaging.

The Mixing Department combines dry ingredients, including

flour, salt, and baking powder, with liquid ingredients, including

eggs and vegetable oil, to make waffle batter.

Illustration 17-9 provides information related to the Mixing

Department at the end of June.

Refinements on the Weighted-Average Method

Equivalent UnitsEquivalent Units

17-21

Illustration: Info for the Mixing Dept at the end of June.

Equivalent UnitsEquivalent Units

Refinements on the Weighted-Average Method

* Conversion costs = labor costs + overhead costs.

17-22

Beginning work in process is not part of the

equivalent-units-of-production formula … WHY NOT ?

Equivalent UnitsEquivalent Units

17-23

Conversion CostsConversion Costs

Conversion costs are those costs required to convert raw materials into finished goods that are ready for sale.

Conversion costs = Direct labor + Manufacturing overhead

Examples of costs that may be considered conversion costs are: Direct labor & benefits Equipment depreciation Equipment maintenance Factory rent Factory supplies Factory insurance Factory utilities Factory supervisors

Most conversion costs are likely to be “manufacturing overhead”.

17-24

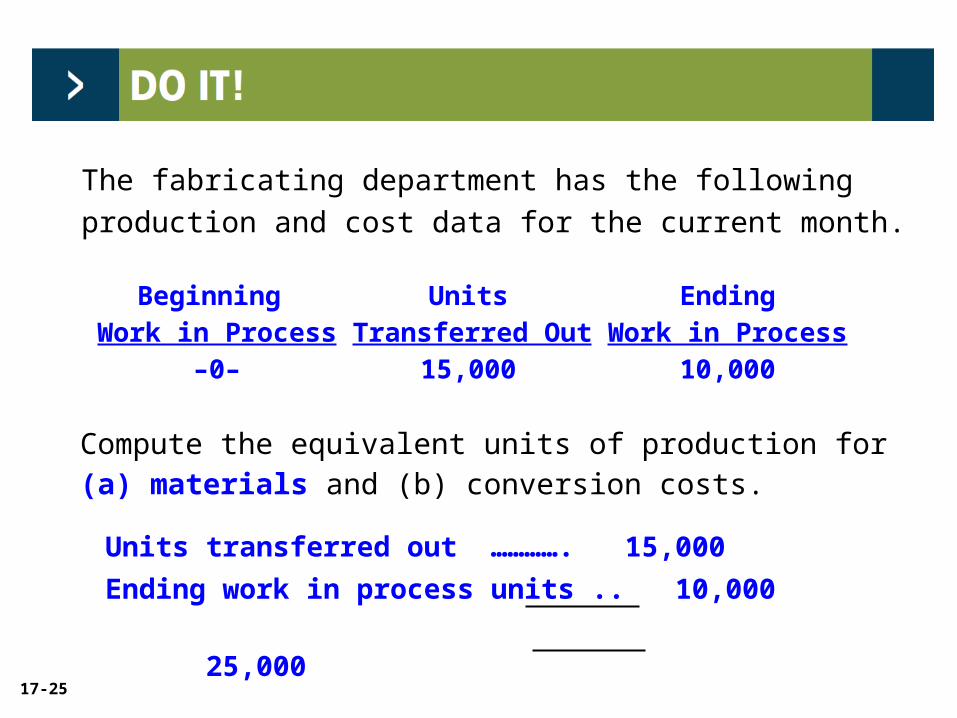

The fabricating department has the following production and

cost data for the current month.

Beginning Units EndingWork in Process Transferred Out Work in Process

–0– 15,000 10,000

Materials are entered at the beginning of the process. The

ending work in process units are 30% complete as to

conversion costs.

Compute the equivalent units of production for (a) materials and

(b) conversion costs.

17-25

Compute the equivalent units of production for (a) materials and (b) conversion costs.

Units transferred out …………. 15,000

Ending work in process units .. 10,000

25,000

The fabricating department has the following production and

cost data for the current month.

Beginning Units EndingWork in Process Transferred Out Work in Process

–0– 15,000 10,000

17-26

Compute the equivalent units of production for (a) materials and (b) conversion costs.

Units transferred out …… 15,000

Equiv Units-ending WIP .. 3,000 (10,000 x 30%)

18,000

The fabricating department has the following production and

cost data for the current month.

Beginning Units EndingWork in Process Transferred Out Work in Process

–0– 15,000 10,000

17-27

Production Cost

Report

17-28

A production cost report is the

Key document used to understand activities.

Prepared for each department and shows Production

Quantity and Cost data.

Four steps in preparation:

Step 1: Compute physical unit flow

Step 2: Compute equivalent units of production

Step 3: Compute unit production costs

Step 4: Prepare a cost reconciliation schedule

Production Cost ReportProduction Cost Report

17-29

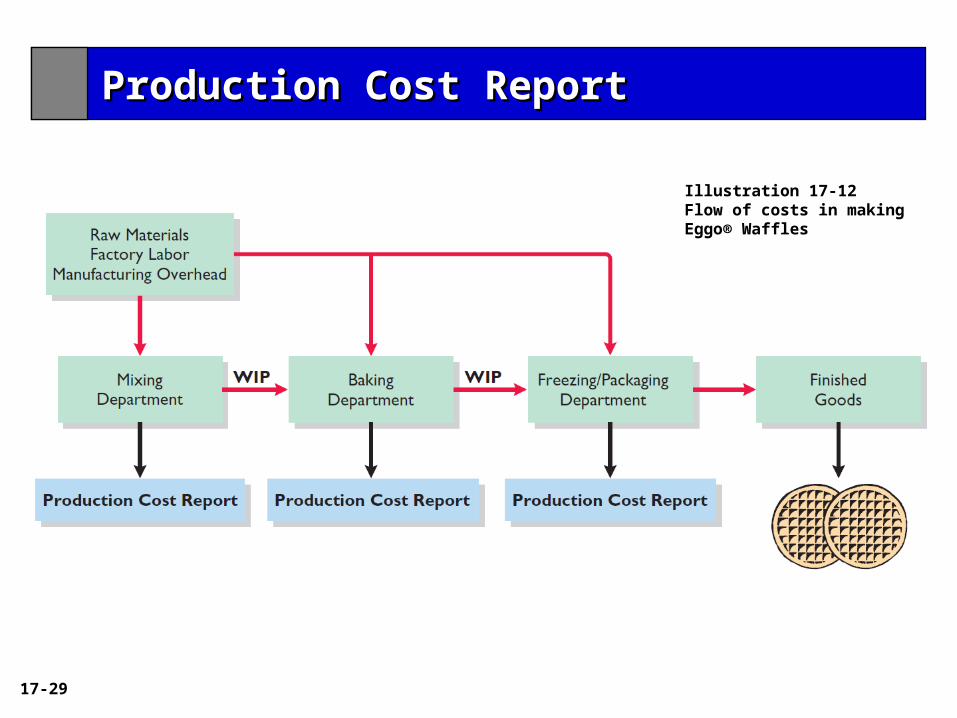

Illustration 17-12Flow of costs in makingEggo® Waffles

Production Cost ReportProduction Cost Report

17-30

17-31

17-32

Illustration 17-13 Unit and cost data—Mixing Department

Production Cost ReportProduction Cost Report

17-33

Physical units - actual units to be accounted for

during a period, regardless of work performed.

Total units to be accounted for - units started (or

transferred) into production during the period + units

in production at beginning of period.

Total units accounted for - units transferred out

during period + units in process at end of period.

Compute the Physical Unit Flow (Step 1)

Production Cost ReportProduction Cost Report

17-34

Illustration 17-14

Production Cost ReportProduction Cost Report

Compute the Physical Unit Flow (Step 1)

17-35

Mixing Department

Department adds materials at beginning of process and

Incurs conversion costs uniformly during the process.Illustration 17-15

Production Cost ReportProduction Cost Report

Compute Equivalent Units of Production (Step 2)

17-36

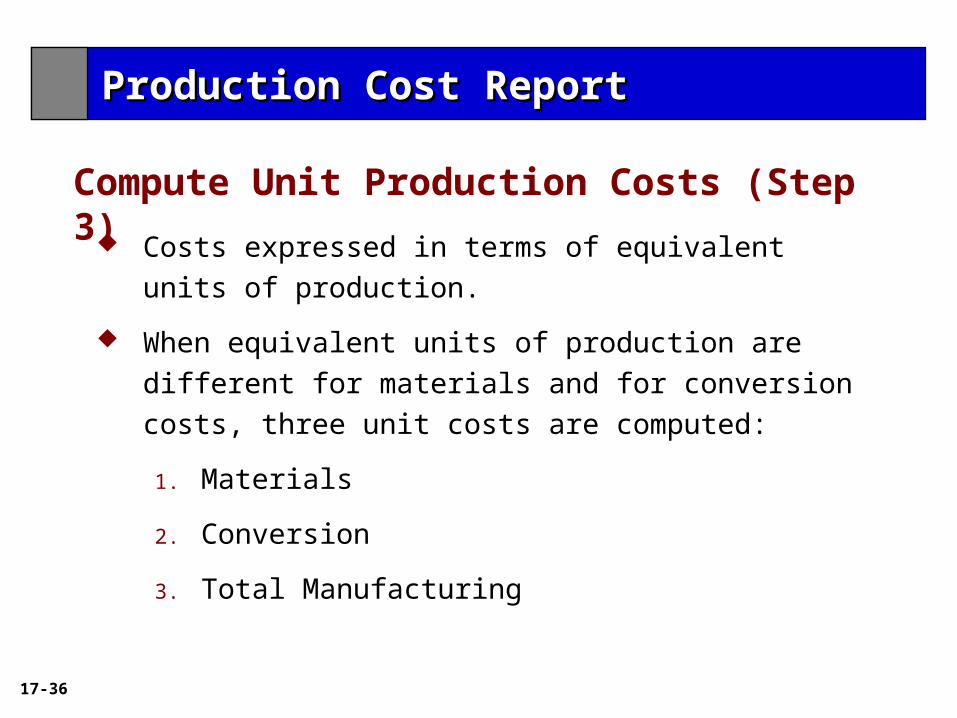

Costs expressed in terms of equivalent units of

production.

When equivalent units of production are different for

materials and for conversion costs, three unit costs are

computed:

1. Materials

2. Conversion

3. Total Manufacturing

Compute Unit Production Costs (Step 3)

Production Cost ReportProduction Cost Report

17-37 LO 6

Compute total materials cost related to Eggo® Waffles:

Work in process, June 1

Direct materials costs $ 50,000

Cost added to production during June

Direct material cost 400,000

Total material costs $450,000

Illustration 17-17

Illustration 17-16

Production Cost ReportProduction Cost Report

Compute Unit Production Costs (Step 3)

17-38

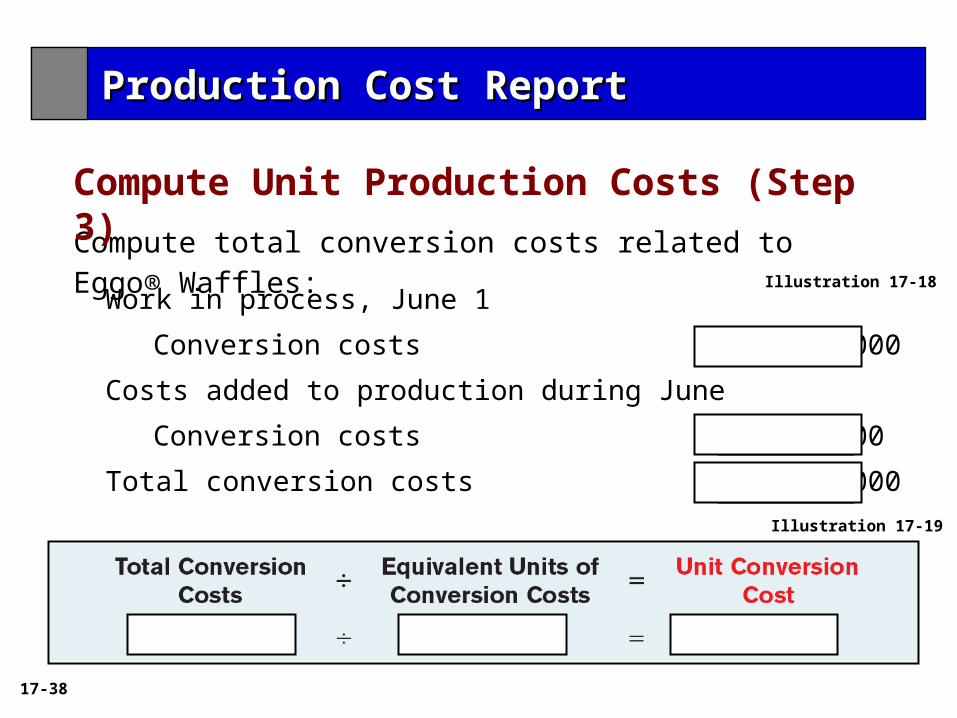

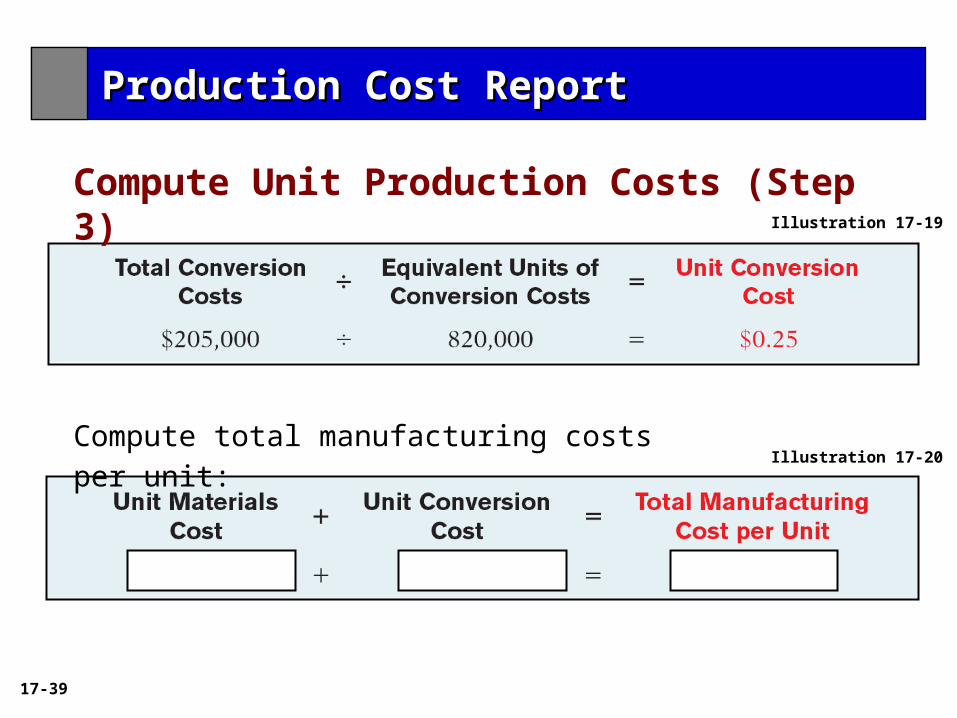

Compute total conversion costs related to Eggo® Waffles:

Work in process, June 1

Conversion costs $ 35,000

Costs added to production during June

Conversion costs 170,000

Total conversion costs $205,000

Illustration 17-19

Production Cost ReportProduction Cost Report

Compute Unit Production Costs (Step 3)

Illustration 17-18

17-39

Compute total manufacturing costs per unit: Illustration 17-20

Production Cost ReportProduction Cost Report

Compute Unit Production Costs (Step 3)Illustration 17-19

17-40

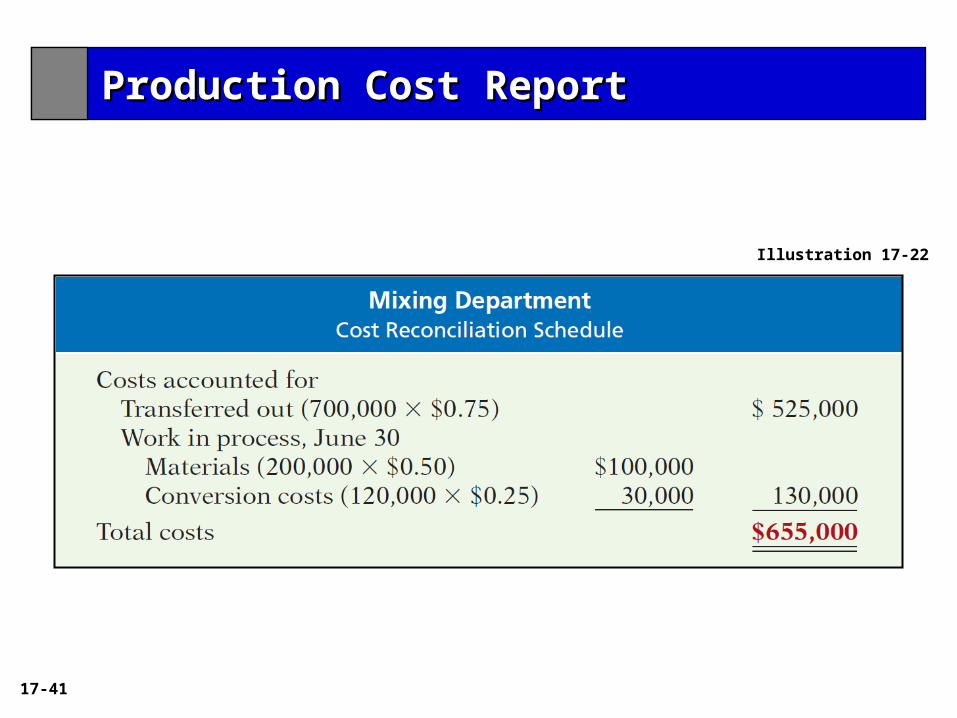

Kellogg charged total costs of $655,000 to the Mixing Department in June, calculated as follows.

Costs to be accounted for

Work in process, June 1 $ 85,000

Started into production 570,000

Total costs $655,000

Illustration 17-21

Production Cost ReportProduction Cost Report

Prepare a Cost Reconciliation Schedule (Step 4)

17-41

Illustration 17-22

Production Cost ReportProduction Cost Report

17-42

Prepare the Production Cost Report

LO 7

Production Cost ReportProduction Cost ReportIllustration 17-23

17-43

Companies often use a combination of a process cost

and a job order cost system.

Called operations costing, this hybrid system is similar

to process costing in its assumption that standardized

methods are used to manufacture the product.

At the same time, the product may have some

customized, individual features that require the use of

a job order cost system.

Costing Systems – Final Comments

Production Cost ReportProduction Cost Report