120108145113_p3_1

16

16 th AFA Int’l Fertilizers Forum & Exhibition February 2 - 4, 2010 Cairo Semiramis Intercontinental Hotel, Egypt Outlook for World Fertilizer Demand, Supply and Supply/Demand Balances Mr. Patrick Heffer Director IFA Agriculture Service France

-

Upload

afa-association -

Category

Documents

-

view

212 -

download

0

description

http://www.afa.com.eg/uploads/papers/2010/files/120108145113_p3_1.pdf

Transcript of 120108145113_p3_1

16th AFA Int’l Fertilizers Forum & Exhibition

February 2 - 4, 2010

Cairo Semiramis Intercontinental Hotel, Egypt

Outlook for World Fertilizer Demand, Supply and Supply/Demand Balances

Mr. Patrick Heffer Director

IFA Agriculture Service

France

1/24/2010

1

OUTLOOK FOR WORLD OUTLOOK FOR WORLD FERTILIZER DEMAND, SUPPLY FERTILIZER DEMAND, SUPPLY AND SUPPLY/DEMAND AND SUPPLY/DEMAND BALANCESBALANCES

Patrick Patrick Heffer and Michel Prud’hommeHeffer and Michel Prud’hommeIFAIFA

16th AFA Int’l Annual Fertilizers Forum & Exhibition2-4 February 2010, Cairo, Egypt

ECONOMIC CONTEXTECONOMIC CONTEXT

1/24/2010

2

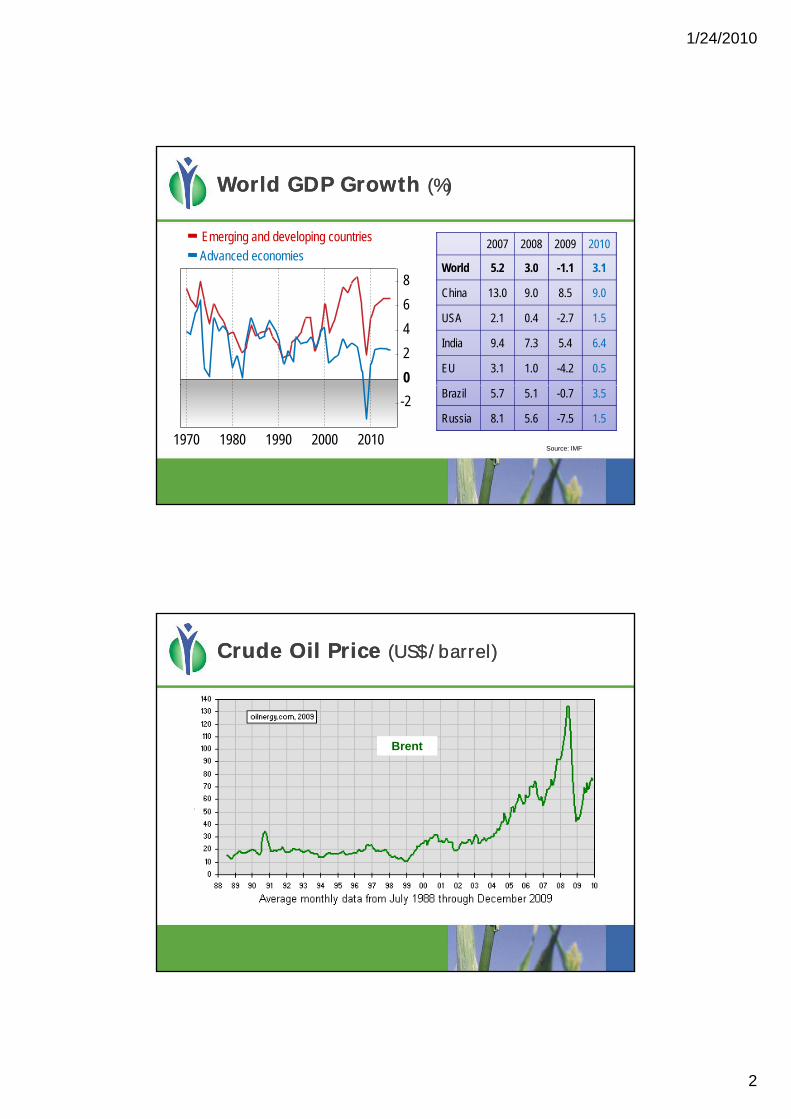

World GDP Growth World GDP Growth (%)(%)

2007 2008 2009 2010

World 5 2 3 0 1 1 3 1

Emerging and developing countries

Advanced economiesWorld 5.2 3.0 -1.1 3.1

China 13.0 9.0 8.5 9.0

USA 2.1 0.4 -2.7 1.5

India 9.4 7.3 5.4 6.4

EU 3.1 1.0 -4.2 0.5

8

6

4

2

0

Source: IMF

Brazil 5.7 5.1 -0.7 3.5

Russia 8.1 5.6 -7.5 1.5

1970 1980 1990 2000 2010

-2

Crude Oil Price Crude Oil Price (US$/barrel)(US$/barrel)

Brent

1/24/2010

3

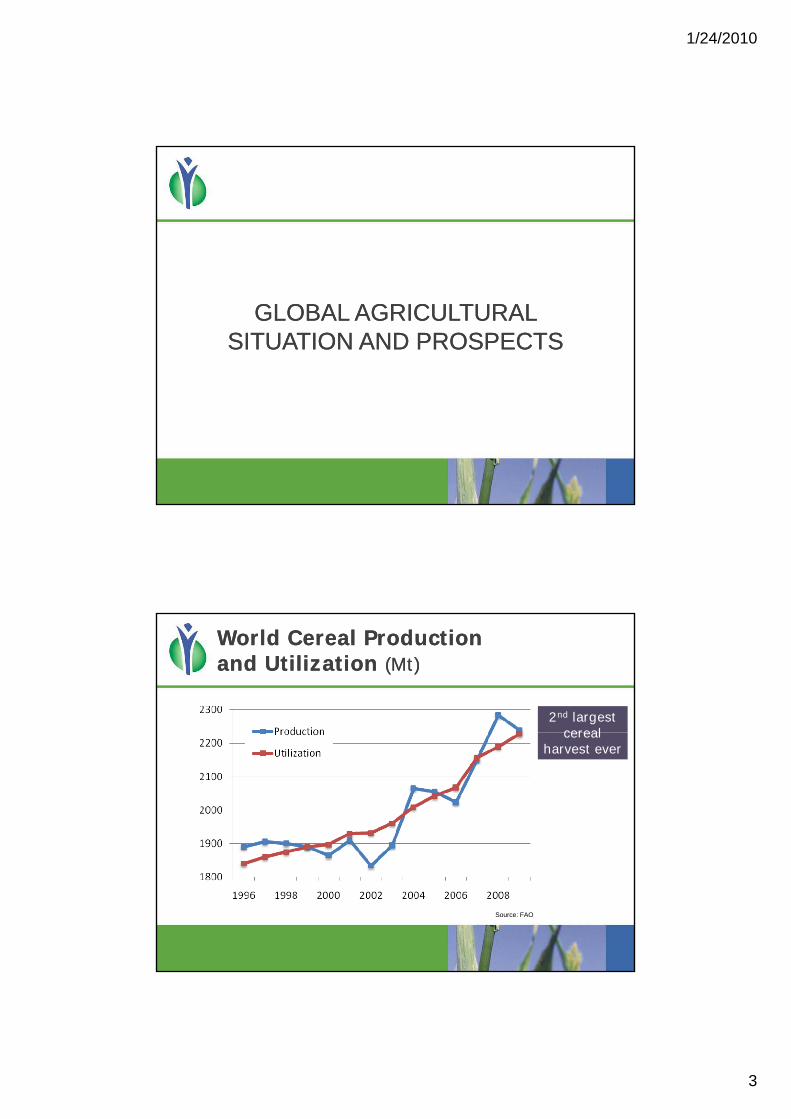

GLOBAL AGRICULTURAL GLOBAL AGRICULTURAL SITUATION AND PROSPECTSSITUATION AND PROSPECTS

World Cereal ProductionWorld Cereal Productionand Utilization and Utilization (Mt)(Mt)

2nd largest cerealcereal

harvest ever

Source: FAO

1/24/2010

4

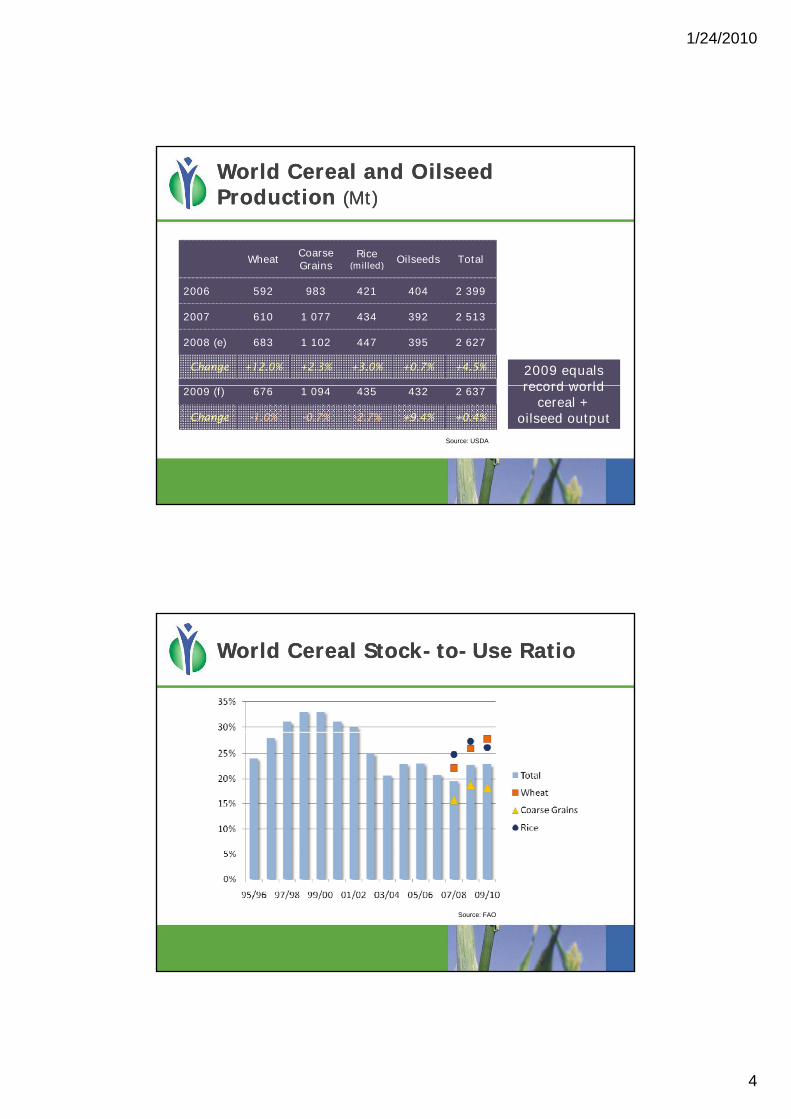

World Cereal and Oilseed World Cereal and Oilseed Production Production (Mt)(Mt)

WheatCoarseGrains

Rice(milled)

Oilseeds TotalGrains (milled)

2006 592 983 421 404 2 399

2007 610 1 077 434 392 2 513

2008 (e) 683 1 102 447 395 2 627

Change +12.0% +2.3% +3.0% +0.7% +4.5% 2009 equals record world2009 (f) 676 1 094 435 432 2 637

Change -1.0% -0.7% -2.7% +9.4% +0.4%

Source: USDA

record world cereal +

oilseed output of 2008

World Cereal StockWorld Cereal Stock--toto--Use RatioUse Ratio

Source: FAO

1/24/2010

5

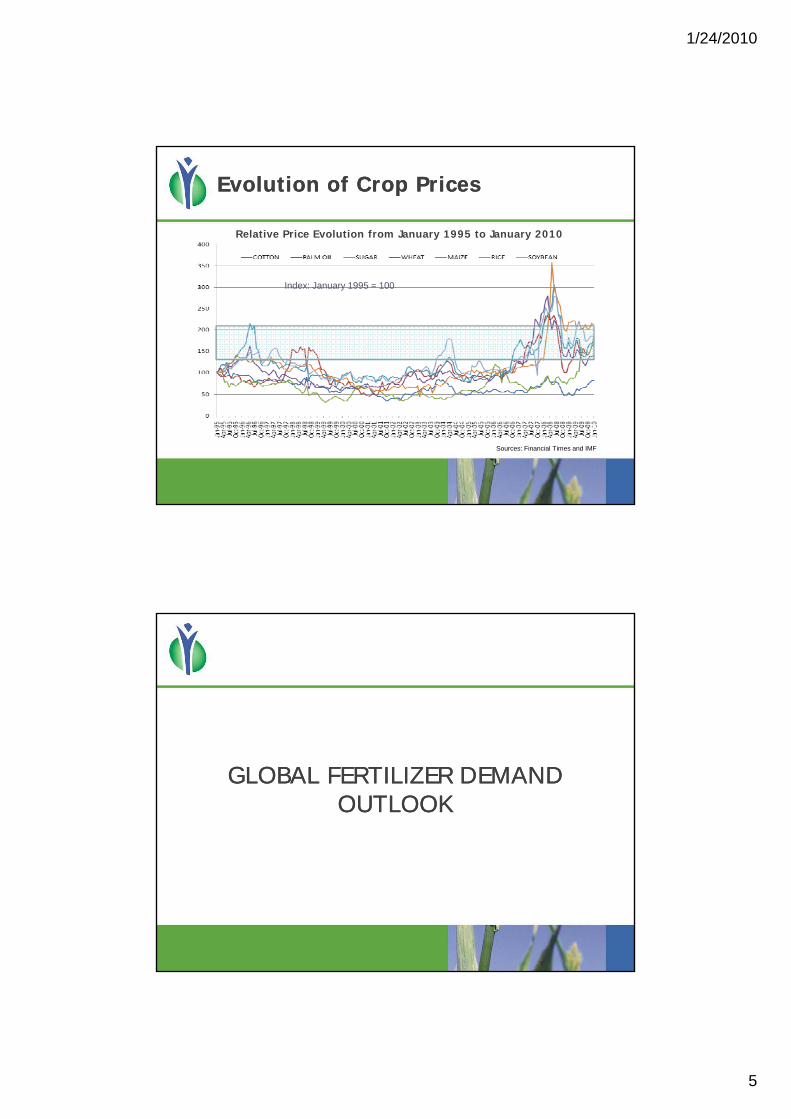

Evolution of Crop PricesEvolution of Crop Prices

Relative Price Evolution from January 1995 to January 2010

Index: January 1995 = 100

Sources: Financial Times and IMF

GLOBAL FERTILIZER DEMAND GLOBAL FERTILIZER DEMAND OUTLOOKOUTLOOK

1/24/2010

6

160

180K2O

P2O5

2007/08

2008/09 (e)

Change2009/10 (f)

Change2010/11 (f)

Change

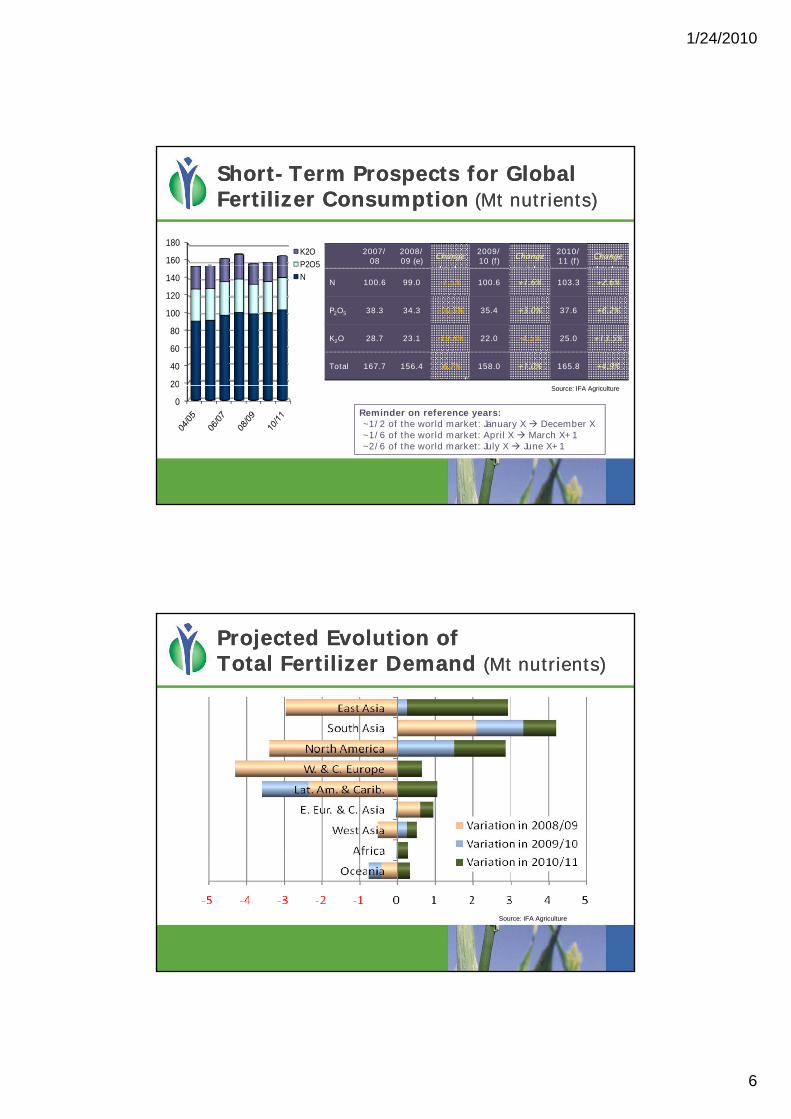

ShortShort--Term Prospects for Global Term Prospects for Global Fertilizer Fertilizer ConsumptionConsumption ((Mt nutrients)Mt nutrients)

20

40

60

80

100

120

140

P2O5

NN 100.6 99.0 -1.5% 100.6 +1.6% 103.3 +2.6%

P2O5 38.3 34.3 -10.5% 35.4 +3.0% 37.6 +6.2%

K2O 28.7 23.1 -19.8% 22.0 -4.5% 25.0 +13.5%

Total 167.7 156.4 -6.7% 158.0 +1.0% 165.8 +4.9%

0

20 Source: IFA Agriculture

Reminder on reference years:~1/2 of the world market: January X December X~1/6 of the world market: April X March X+1~2/6 of the world market: July X June X+1

Projected Evolution of Projected Evolution of Total Fertilizer Demand Total Fertilizer Demand (Mt nutrients)(Mt nutrients)

Source: IFA Agriculture

1/24/2010

7

Some of the Main UncertaintiesSome of the Main Uncertainties

Evolution of the financial and economic downturn

crude oil prices- crude oil prices

- consumer’s (farmer’s) confidence

- access to credit

Yield impact of lower P and K application rates

- 2009: equals the 2008 record grain + oilseed harvest

- prospects for high corn yields in the USA

record wheat yields in France- record wheat yields in France

what impact on long-term farmer’s behaviour?

Evolution of the fertilizer:crop price ratio

GLOBAL FERTILIZER SUPPLY GLOBAL FERTILIZER SUPPLY SITUATION AND OUTLOOKSITUATION AND OUTLOOK

1/24/2010

8

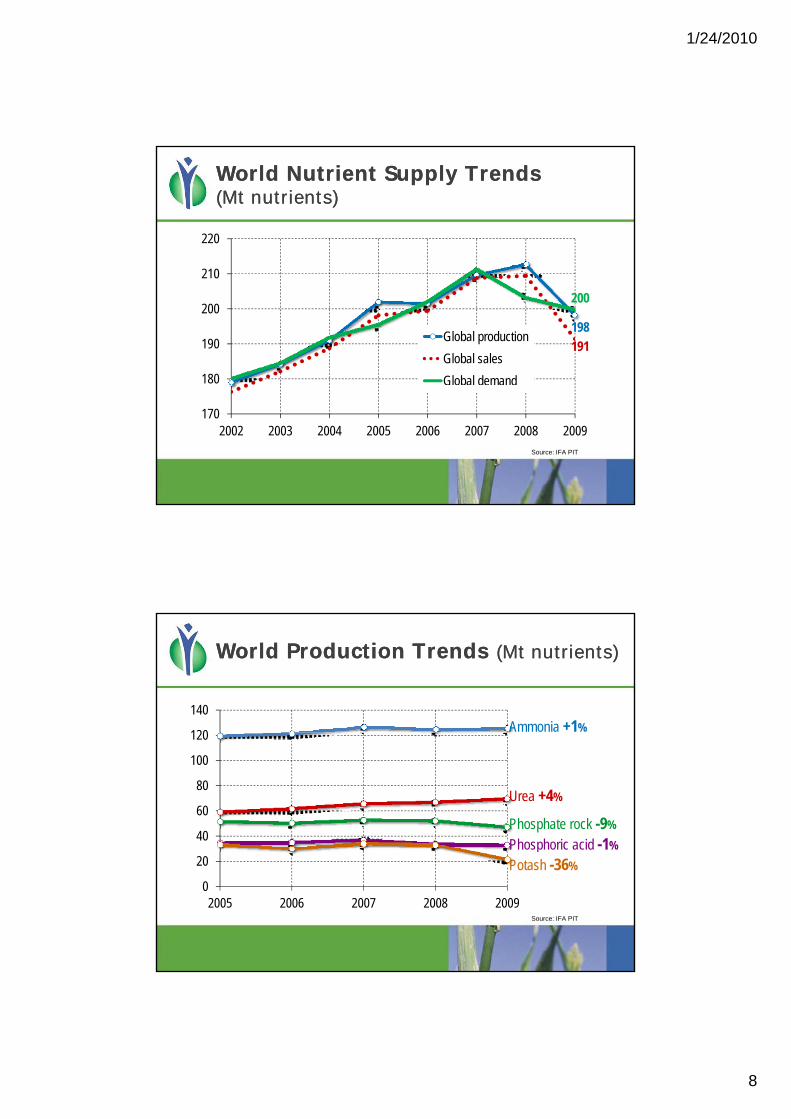

World Nutrient Supply Trends World Nutrient Supply Trends (Mt nutrients)(Mt nutrients)

220

198

191

200

180

190

200

210

Global production

Global sales

Global demand

Global Supply and Demand Outlook for Fertilizers and Raw Materials / Intermediates

1702002 2003 2004 2005 2006 2007 2008 2009

| Source:IFA PIT Committee

Source: IFA PIT

World Production Trends World Production Trends (Mt nutrients)(Mt nutrients)

120

140Ammonia +1%

40

60

80

100

120

Urea +4%

Phosphate rock -9%

Phosphoric acid -1%

Global Supply and Demand Outlook for Fertilizers and Raw Materials / Intermediates

0

20

2005 2006 2007 2008 2009

pPotash -36%

| Source:IFA PIT Committee

Source: IFA PIT

1/24/2010

9

World Operating RatesWorld Operating Rates

Rates in %: production over operating capacity

100%

AmmoniaUrea

PotashPhosphoric Acid

50

60%

70%

80%

90%

Global Supply and Demand Outlook for Fertilizers and Raw Materials / Intermediates

1995 97 99 01 03 05 07 2009 1995 97 99 01 03 05 07 2009

40%

50%

| Source:IFA PIT Committee

Source: IFA PIT

35

40

Exports of Main CommoditiesExports of Main Commodities(Mt nutrients)(Mt nutrients)

Urea

10

15

20

25

30

Urea

Phosphate rockAmmonia

Potash

Sulphur

Global Supply and Demand Outlook for Fertilizers and Raw Materials / Intermediates

0

5

2005 2006 2007 2008 2009

DAPPhosphoric acid

| Source:IFA PIT Committee

Source: IFA PIT

1/24/2010

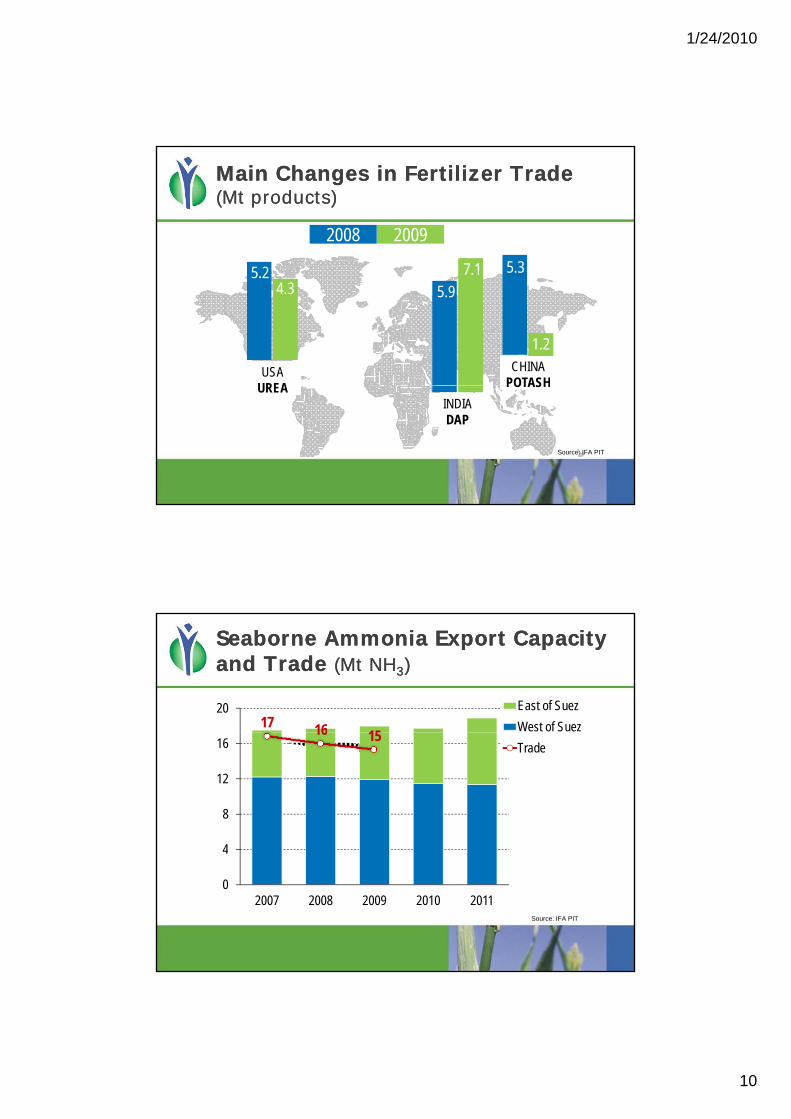

10

Main Changes in Fertilizer TradeMain Changes in Fertilizer Trade(Mt products)(Mt products)

7 1

2008 2009

5 3

5.97.15.2

4.3

CHINAPOTASH

USAUREA

5.3

1.2

Global Supply and Demand Outlook for Fertilizers and Raw Materials / Intermediates

POTASH

INDIADAP

UREA

| Source:IFA PIT Committee

Source: IFA PIT

Seaborne Ammonia Export Capacity Seaborne Ammonia Export Capacity and Trade and Trade (Mt NH(Mt NH33))

17 16 15

20 East of Suez

West of Suez16 15

4

8

12

16 Trade

Global Supply and Demand Outlook for Fertilizers and Raw Materials / Intermediates

0

4

2007 2008 2009 2010 2011

| Source:IFA PIT Committee

Source: IFA PIT

1/24/2010

11

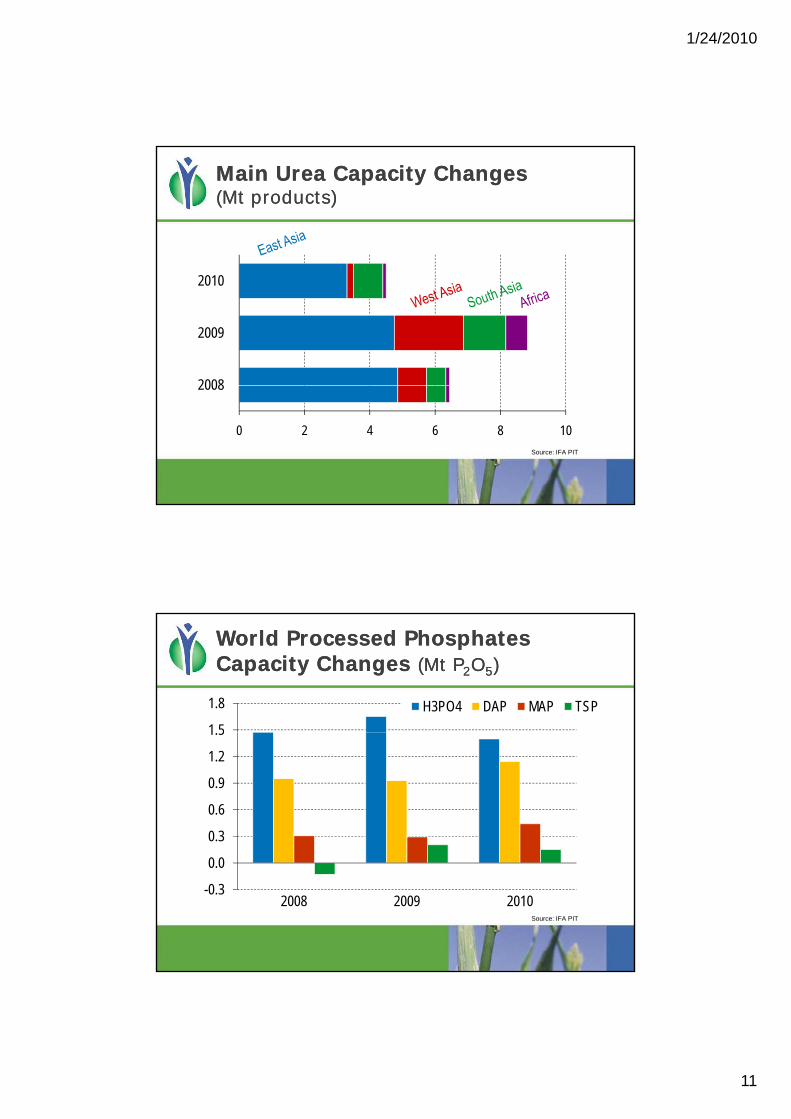

Main Urea Capacity Changes Main Urea Capacity Changes (Mt products)(Mt products)

2008

2009

2010

Global Supply and Demand Outlook for Fertilizers and Raw Materials / Intermediates

0 2 4 6 8 10

2008

| Source:IFA PIT Committee

Source: IFA PIT

World Processed Phosphates World Processed Phosphates Capacity Changes Capacity Changes (Mt P(Mt P22OO55))

1 5

1.8 H3PO4 DAP MAP TSP

0.3

0.6

0.9

1.2

1.5

Global Supply and Demand Outlook for Fertilizers and Raw Materials / Intermediates

-0.3

0.0

2008 2009 2010

| Source:IFA PIT Committee

Source: IFA PIT

1/24/2010

12

Main Potash Capacity Changes Main Potash Capacity Changes (Mt K(Mt K22O)O)

2008

2009

2010

Global Supply and Demand Outlook for Fertilizers and Raw Materials / Intermediates

0.0 0.2 0.4 0.6 0.8 1.0 1.2 1.4 1.6

2008

| Source:IFA PIT Committee

Source: IFA PIT

World Sulphur Supply/Demand World Sulphur Supply/Demand Balance Balance (Mt S)(Mt S)

48 49 4955

Supply Demand

48 49 49

50 45 45 48

2007 2008 2009 2010

Global Supply and Demand Outlook for Fertilizers and Raw Materials / Intermediates

-1.6

3.3 4.8 6.7

Balance

| Source:IFA PIT Committee

Source: IFA PIT

1/24/2010

13

World Nutrient Supply/Demand World Nutrient Supply/Demand BalancesBalances

128133 137

129152

159165

157

Mt ureaMt N

Supply Demand

125 123129

2008 2009 2010

146 149157

2008 2009 2010

36 38 39 38 39 41 Mt K2OMt P2O5

Global Supply and Demand Outlook for Fertilizers and Raw Materials / Intermediates

28 25 28

2008 2009 2010

33 33 35

2008 2009 2010

| Source:IFA Ag Committee

Source: IFA PIT

220

World Nutrient Supply Trends World Nutrient Supply Trends (Mt nutrients)(Mt nutrients)

205

190

200

210

Global productionGlobal sales

Global Supply and Demand Outlook for Fertilizers and Raw Materials / Intermediates

1802004 2005 2006 2007 2008 2009 2010

Global demand

| Source:IFA PIT Committee

Source: IFA PIT

1/24/2010

14

Prospects for Prospects for 20102010

A recovery in demand and stronger sales prospects

Current S/D balances: potentially, high surpluses prevailing in 2009 and through 2010

Limited new capacity outside China and on-going structural changes

Rising volatility of agricultural commodity and energy prices

Improving market conditions in 2010

Increases in production and operating rates

Higher domestic sales and exports

Global Supply and Demand Outlook for Fertilizers and Raw Materials / Intermediates

- A rebound in import demand in Latin America, North America and South-East Asia

- Sustained imports in South Asia - Potential improvement in Europe and Oceania- Uncertainties as regards China

ConclusionConclusion

Projections for 2010/11 are very speculative

Provided the world economic activity recovers, and the agricultural market fundamentals remain positive, global fertilizer demand in 2010/11 could regain positive growth rates

Global Supply and Demand Outlook for Fertilizers and Raw Materials / Intermediates

positive growth rates

1/24/2010

15

For questions/comments:For questions/comments:on the demand side: on the demand side: [email protected]@fertilizer.org

th l id th l id on the supply side: on the supply side: [email protected]@fertilizer.org