Scott Hollenbeck – Scott.M.Hollenbeck@irs Barry Johnson – Barry.W.Johnson@irs

Upload

singhranvijayCategory

view

221download

0

8/14/2019 10 10th Ing Irs India

http://slidepdf.com/reader/full/10-10th-ing-irs-india 1/15

ING GROUP

10th Investor Relations Symposium

India

Frank Koster

CEO, ING Vysya Life Insurance, India

London, 16 September 2005

8/14/2019 10 10th Ing Irs India

http://slidepdf.com/reader/full/10-10th-ing-irs-india 2/15

Insurance Asia/Pacific: India, Sept. 2005 2

Key Points to Make

• India is the second fastest growing life insurance market

in Asia

• ING, an early entrant, has management control, and is among

the fastest growing companies

• Business is being sold at healthy margins

• Reach, scale and efficiency hold the key to creating value

8/14/2019 10 10th Ing Irs India

http://slidepdf.com/reader/full/10-10th-ing-irs-india 3/15

Insurance Asia/Pacific: India, Sept. 2005 3

In 10 years time India will have a middle class the size of US,

and it is still up for grabs

Large, growing economy

Growing market (5 year CAGR)

– Retail assets: 24%

– Retail liabilities: 12%

– Life insurance premium: 33% – Pvt. mutual fund assets: 61%

… with increasing affluence … Rapidly increasing revenue poolin financial services

… and openness to internationalfirms

Unique market challenges65.835.5

69.6

79.9

52.6 106.6

2002 2010

188

222

<1,000

1,000 – 2,000

>2,000

Income(Euro)

CAGR

2.1%

9.2%

1.7%

-7.4%

No. of households (m)

EconomyDemographics

4.4%11,75036.30.92%296US

2.4%11,65039.70.15%457EU

6.2%

Growth

(%)

3,319

(#5)

GDP PPP

($ bn)

24.71.40%1,080

(#2)

INDIA

Rank

MedianAge

Growth

(%)

Pop.

(m)

Government committed to reform

FDI growing, new sectors opening

Foreign companies are successful

World-class, young, IT literateworkforce

Legal system, language, culturalproximity to West

Deep, well regulated capital markets.

Free and vibrant press

… changing culture …

Move to nuclear families, increasedhome ownership by younger couples

Declining aversion to debt

Household savings remain high

+54 m

Urban/Rural divide

– Geographical spread

– Only 30 cities with 1m+ people – Top-25 cities account for 10% of

population and 50% of income

Distinct sub-markets

– 15 official languages

– Diverse habits/cultural norms

Inadequate infrastructure

Bureaucracy, corruption,

complex/antiquated regulation

Foreign ownership limitations in

Banking and Life insurance

Source: RBI, NCAER, Worldbank, ING Research

8/14/2019 10 10th Ing Irs India

http://slidepdf.com/reader/full/10-10th-ing-irs-india 4/15

Insurance Asia/Pacific: India, Sept. 2005 4

Integrated brand.

Home Base is Southern India - fastest growing part of India, with 3 of the top-6 metros.

Branding/Regions

Business houses with knowledge of doing business in India: Tata, Birla, Reliance, Bajaj

High-quality local players: HDFC, ICICI, LIC, SBI, UTI, Kotak

Prudential (UK), Allianz,

Sun Life, Standard Life,

AIG, NY Life,Aviva, Met Life

Citigroup, HSBC, StandardChartered, ABN Amro

Competition:

GlobalWho’s who:

Market share 7.4%

Rank 5th (of 14 players)

AUM Euro 390 m

Rank 17 of 30 players

0.7% of deposits/Rank 10

0.8% of Advances/Rank 11(Excl. government banks)

Largest network amongstinternational players (¬ 450branches)

Share / Rank,

Size/Scale

Tied-agents, Banks,Corporate Agents

IFAs, Bank and other thirdparties

Branches, Direct sales staff Distributionchannels:

Individual, Group,Corporate

Retail, Private, Corporate,Institutional

Retail, Private, SME,Agricultural and Social;

Corporate; Wholesale

Customers/Markets:

Traditional Life, UnitLinked, Personal Pensions,Employee Benefits

Mutual Funds - Equity, Debt,Liquid, Balanced, Fund of Funds, and Portfolio MgmtServices

Loans, Deposits, Transactionservices, Treasury, WealthManagement

Products/BusinessLines:

26%64%44%Ownership

Life InsuranceBankingAsset

ManagementBusiness

segments

ING is the only global player in banking, asset management

and insurance with management control

Source: AMFI, RBI, IRDA, ING Research

Partners

• Presence in batteries, real estate,building materials and mutual funds

• New ventures in retail, media andcommunications

• Group Turnover > Euro 800 m

• Good track record in JVs with

international players

• Leading cement producer withrevenues over Euro 470 m

• JV with Holcim

• Leading investment banking,securities and distribution firmcovering retail and institutional clients

RR Group

GAC

Enam

8/14/2019 10 10th Ing Irs India

http://slidepdf.com/reader/full/10-10th-ing-irs-india 5/15

Insurance Asia/Pacific: India, Sept. 2005 5

Life Insurance sector has opened up…

Foreign ownership limited to 26%; 49% awaited

Mandatory obligation to sell in rural areas

Commission capped at low levels Separate broker regulations

Referral regulation developed for bancassurance

Investment function can not be outsourced

Movement towards risk based capital for solvency

1938 Act under review

Strongly improving regulation and relaxing foreign

ownership rules

… and regulations are steadily evolving

IRDA set up as the regulator. First licenses issued2000

Government announces liberalization of the sector 1998

LIC formed by an Act. Amalgamated 246 life

insurance companies then operating in India

1956

Insurance Act consolidated and amended1938

ING Vysya Life obtains license to set up business2001

Liberalization

Nationalization

Regulation of the Market

Emergence of Private Insurance Market

First Life Insurance company starts1818

0

20

40

60

80

2005 2010 2015 2020 2025

Total contribution in Euro bn

Pensions is due to open shortly

Objective of the reform is to:

- Revamp unfunded, defined-benefit pension system to

reduce government expenditure (currently 1.5% of GDP,

1/4th of fiscal deficit)

- Extend coverage (currently at ~10% of working population)

Proposed system similar to Pillar 3 on voluntary basis:

- Workers can put their money with private fund managersin various types of schemes.

- New system will also cover employees from small firms.

Timing:

- Interim pensions regulator established.

- Bill expected to be approved by parliament by year-end.

Source: IRDA, CMIE

8/14/2019 10 10th Ing Irs India

http://slidepdf.com/reader/full/10-10th-ing-irs-india 6/15

Insurance Asia/Pacific: India, Sept. 2005 6

Inforce Premium (Euro m)

0

50

100

150

200

K o r e a

T a i w a n

A u s t r a l i a

I n d i a

C h i n a

F r a n c e

U K

G e r m a n y

2004

2015

… insurance is fastest growing financial saving

Source: RBI

3.53.1

2.7

1.6

1.1

India is the second fastest growing Life Insurance market in

Asia, second only to China

0

2

4

6

8

10

12

2000-01 2001-02 2002-03 2003-04 2004-05

New Premium

Total Premium

13% 11% 10%

32%38%

10%

18%

19%

18%

3%

8%3%

9%

3%2%3%

46%

14%

8%

18% 14%

1980 1990 2002

Post 2000, market took-off…

Several factors driving industry growth…

50% of population is less than 25 years of age

GDP to grow at >6% and insurance penetration taking off

Average income at Euro 1,800 p.a and growing at 6% annually

Embedded Savings culture; 24% of Household Income

10% of population insured (30% of insurable population)

3% of population has retirement benefits (10% of work force)

Absence of Social Security framework

…poised for even more growth…

Non Bank DepositsCurrency

BankDeposits

Shares

ProvidentFunds

Life Insurance

Others

43 % 45 % 50 %% of TotalSavings

…quadrupling by 2015

Source: Swiss RE, APRIASource: IRDA Fiscal Year Reports Source: Swiss Re Sigma, NCAER

33%

New PremiumCAGR

GDP per capital (USD)

2

4

6

8

10

1,000 10,000

Threshold for insurance pick-up

I n s u r a n c e p r e m i u m ( % o

f G D P )

Euro m

8/14/2019 10 10th Ing Irs India

http://slidepdf.com/reader/full/10-10th-ing-irs-india 7/15

Insurance Asia/Pacific: India, Sept. 2005 7

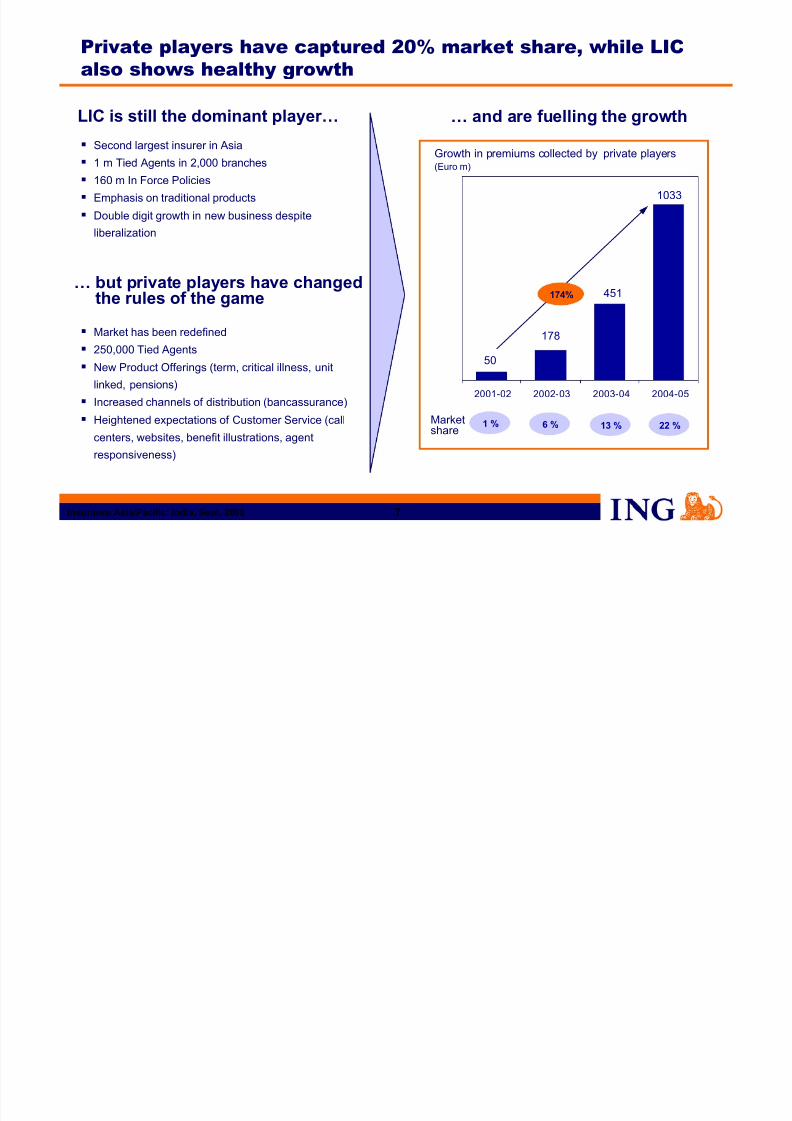

Private players have captured 20% market share, while LIC

also shows healthy growth

Market has been redefined

250,000 Tied Agents

New Product Offerings (term, critical illness, unit

linked, pensions)

Increased channels of distribution (bancassurance)

Heightened expectations of Customer Service (call

centers, websites, benefit illustrations, agent

responsiveness)

LIC is still the dominant player…

… but private players have changedthe rules of the game

Second largest insurer in Asia

1 m Tied Agents in 2,000 branches

160 m In Force Policies

Emphasis on traditional products

Double digit growth in new business despite

liberalization

… and are fuelling the growth

50

178

451

1033

2001-02 2002-03 2003-04 2004-05

Marketshare

174%

1 %

Growth in premiums collected by private players(Euro m)

6 % 13 % 22 %

8/14/2019 10 10th Ing Irs India

http://slidepdf.com/reader/full/10-10th-ing-irs-india 8/15

Insurance Asia/Pacific: India, Sept. 2005 8

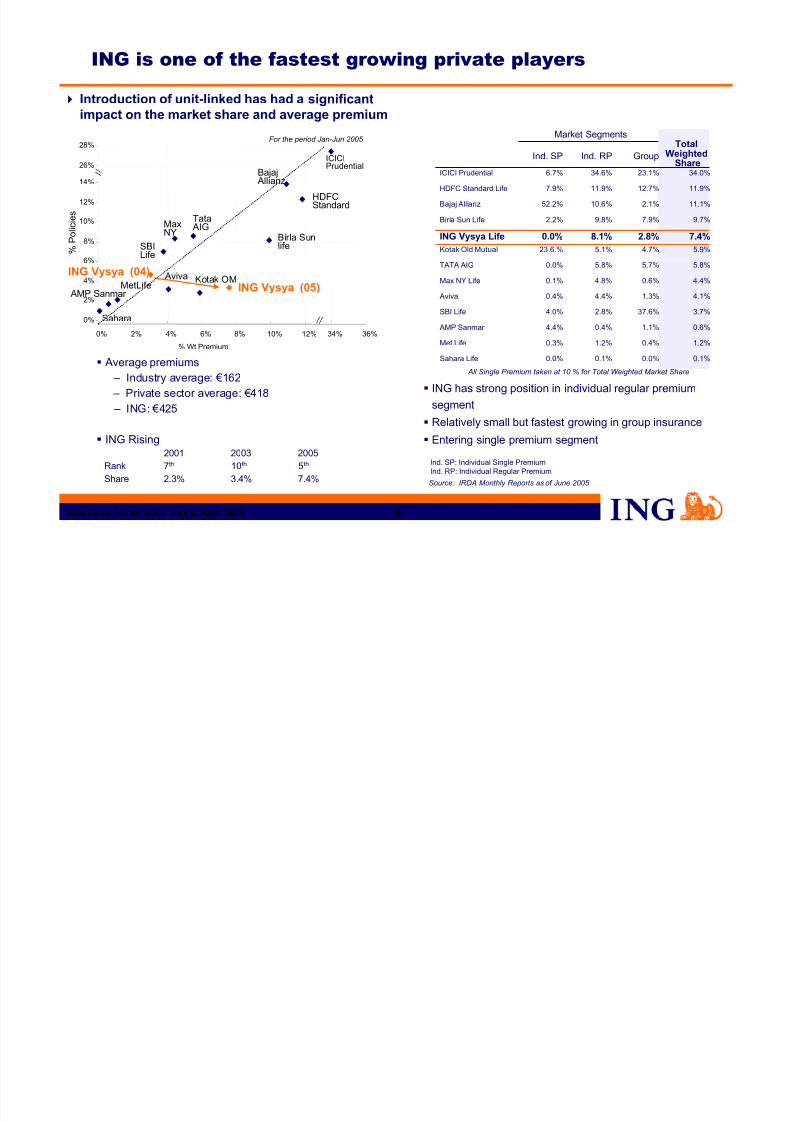

Introduction of unit-linked has had a significantimpact on the market share and average premium

Market Segments

0.1%0.0%0.1%0.0%Sahara Life

3.7%37.6%2.8%4.0%SBI Life

7.4%2.8%8.1%0.0%ING Vysya Life

11.9%12.7%11.9%7.9%HDFC Standard Life

TotalWeighted

ShareGroupInd. RPInd. SP

4.4%0.6%4.8%0.1%Max NY Life

5.8%5.7%5.8%0.0%TATA AIG

9.7%7.9%9.8%2.2%Birla Sun Life

4.1%1.3%4.4%0.4%Aviva

5.9%4.7%5.1%23.6.%Kotak Old Mutual

0.4%

1.1%

2.1%

23.1%

1.2%

0.4%

10.6%

34.6%

1.2%

0.6%

11.1%

34.0%

0.3%Met Life

4.4%AMP Sanmar

52.2%Bajaj Allianz

6.7%ICICI Prudential

Source: IRDA Monthly Reports as of June 2005

Average premiums

– Industry average: €162

– Private sector average: €418 – ING: €425

ING Rising2001 2003 2005

Rank 7th 10th 5th

Share 2.3% 3.4% 7.4%

ING is one of the fastest growing private players

All Single Premium taken at 10 % for Total Weighted Market Share

% P

o l i c i e s

% Wt Premium

Sahara

MetLife

AMP Sanmar

Aviva

MaxNY

TataAIG

SBILife

Birla Sunlife

Kotak OM

HDFCStandard

BajajAllianz

ICICIPrudential

0%

2%

4%

6%

8%

10%

12%

14%

0% 2% 4% 6% 8% 10% 12% 34% 36%

26%

28%

ING Vysya (05)

ING Vysya (04)

ING has strong position in individual regular premiumsegment

Relatively small but fastest growing in group insurance

Entering single premium segment

For the period Jan-Jun 2005

Ind. SP: Individual Single PremiumInd. RP: Individual Regular Premium

8/14/2019 10 10th Ing Irs India

http://slidepdf.com/reader/full/10-10th-ing-irs-india 9/15

Insurance Asia/Pacific: India, Sept. 2005 9

1232Banks

35,800

6

3717

25

17

1H ‘03

252,000

31

9,650

88

45

1H ’05 1H ’04

140,000Customers:

16Other Partners

CorporateAgency

6,212Advisors

39Branches

20Cities

Tied Agency

Channel Mix

ING: fast growth, with strict quality and compliance

standards

Criticalillness

Pension

Product Mix

Unit –linked

Group

69%

49%

32%

15%

11%

8%

4%

1%

1%

12%

28%

9%

0%4%

48%

0% 2%7%

2003 2004 1H 2005

A branch opened every week

100 agents hired every week

88%

71%84%

6%5%6%

7%

17%

9%

5% 2%

2003 2004 1H 2005

TiedAgency

ING VysyaBank

EmployeeBenefits

6.5

26.3

44.6

2003 2004 1H 2005

APE (Euro m)IVL by numbers

Alt.Channels

Endowment

Whole life

/ Existing

/ Expanding

Locations markings are indicative

Delhi

Hyderabad

Bhopal

Chandigarh

Kolkatta

Mumbai

Chennai

Bangalore

Ahmedabad

Jaipur

Ludhiana

Trivandrum

Goa

Lucknow Assam

JammuShimla

Dehradun

Patna

Ranchi

Raipur Bhubaneshwar

Exchange Rate Source ING Intranet

8/14/2019 10 10th Ing Irs India

http://slidepdf.com/reader/full/10-10th-ing-irs-india 10/15

Insurance Asia/Pacific: India, Sept. 2005 10

Strong foundations are being laid

Customers Distribution

Rising awareness and serviceexpectations

Tied Channel is the core engine

Two customer groups

1. Urban premium segment

– top 15 cities, 50M people

– aware of companies, product segments,

expect quick and reliable service

2. Mass segment

– Rural and small cities, 300 m people

– Easier to serve but harder to reach,

requires large low-cost distribution

Financial Strength

State of the Art IT set up

Disaster Recovery Plan in place

Work Flow to process larger volumes

Six Sigma Processes to increase

efficiency

Policy issuance turnaround time down

to < 10 days from 14 days in 2003

Operational Efficiency

Investing in brand building

ING awareness grows to 52% from 5% in

2001 Focus on compliance and integrity

Socially responsible corporate: ING

Vysya Foundation plays a key role in

community welfare and development

Benefit from presence in banking,

insurance and asset management

Recruitment of quality advisors earning

better than industry benchmarks

Focus on high productivity: Active Agentproductivity 1,000 Euro per month (up

70% from 2004)

Leveraging ING Vysya Bank Network

Banking partnerships in expansion

mode

Invested capital Euro 72.5 m, likely

to double in the next 3 years Reserves adequate at ING 90%

test

Emphasis on Managing for Value

Using Technology to create efficiency Create sustainable value

Reputation and Trust

Products

Unit Linked is growing strongly

Balanced product portfolio: Unit-

linked/Traditional

Developing channel specific products Investment guarantees limited to SA and

bonus declared on traditional business

Capital guarantee in personal pensions plan

No mortality or morbidity guarantees

8/14/2019 10 10th Ing Irs India

http://slidepdf.com/reader/full/10-10th-ing-irs-india 11/15

Insurance Asia/Pacific: India, Sept. 2005 11

58%

72%70%

58%

32 %

45%

0%

20%

40%

60%

80%

Q1' 04 Q2 ' 04 Q3 ' 04 Q4 ' 04 Q1' 05 Q2 ' 05

Traditional Pension

Group UL

13.9%

12.7%

15.5%

20.2%

21.0%

22.3%

10.0%

15.0%

20.0%

25.0%

Q1' 04 Q2 ' 04 Q3 ' 04 Q4 ' 04 Q1' 05 Q2 ' 05

Business being sold at healthy margins

Profit margin (VNB/APE) generallyincreasing …

173 158 161182

418 415

0

100

200

300

400

500

Q1' 04 Q2 ' 04 Q3 ' 04 Q4 ' 04 Q1' 05 Q2 ' 05

Average APE per Policy Euro

… and supported by an increase in average premium

… reflecting a change in the product mix…

• Profit margins (VNB/APE) is strong

• Pricing is set well above value discount

rate• Profit margins are generally improving

with changing product mix andincreasing average premium

Excludes business written for a big case in Q2 05 to facilitate like to like comparison

8/14/2019 10 10th Ing Irs India

http://slidepdf.com/reader/full/10-10th-ing-irs-india 12/15

Insurance Asia/Pacific: India, Sept. 2005 12

Alternate channels

There are many opportunities for profitable growth…

Tied agents

Upper Middle Class

Urban markets

Other Bancassurance

Individual Insurance

Endowments

Personal Pensions

Health Insurance

Semi UrbanMass Market

- Kerala

- Hyderabad/

Andhra Pradesh

- Delhi/Punjab

- Bangalore/

Karnataka

Pensions business

Health Products/ Riders

Immediate Annuities

- Madhya Pradesh/Uttar Pradesh- Gujarat/ Rajasthan

- Mumbai/ Maharashtra- Chennai/ Tamil Nadu

Reach

Business

Distribution

Customer

Lead with tied-

agents, add

bancassurance

Expand current &

target new

segments

Products

Prepare PensionsEntry

Dominate South

Build North and

West

Balance the

product portfolio

Current Focus

Unit Linked

Group Business

Single Premium

Direct, Worksite

Rural Market

ING Vysya BankWhole Life

8/14/2019 10 10th Ing Irs India

http://slidepdf.com/reader/full/10-10th-ing-irs-india 13/15

Insurance Asia/Pacific: India, Sept. 2005 13

…but there are significant challenges ahead

Managing Complexity

ING’s ResponsesChallenges

Simple organization structure, withtransparency and clear responsibility/accountability

Have the right people in the right place Develop simple and standardized

processes Performance culture

Multiple distribution channels/products Regional expansion – go beyond urban Leverage Indian partners

Focus on improving operating efficiencies Use ING VNB metrics as management tool Emphasis on long-term growth and

profitability

Reaching Scale

Create Value

8/14/2019 10 10th Ing Irs India

http://slidepdf.com/reader/full/10-10th-ing-irs-india 14/15

Insurance Asia/Pacific: India, Sept. 2005 14

Key Points to Make

• India is the second fastest growing life insurance market

in Asia

• ING, an early entrant, has management control, and is among

the fastest growing companies

• Business is being sold at healthy margins

• Reach, scale and efficiency hold the key to creating value

8/14/2019 10 10th Ing Irs India

http://slidepdf.com/reader/full/10-10th-ing-irs-india 15/15

Insurance Asia/Pacific: India, Sept. 2005 15

Certain of the statements contained herein are statements of future expectations

and other forward-looking statements. These expectations are based on

management's current views and assumptions and involve known and unknown

risks and uncertainties. Actual results, performance or events may differ

materially from those in such statements due to, among other things, (i) general

economic conditions, in particular economic conditions in ING’s core markets,

(ii) performance of financial markets, including emerging markets, (iii) the

frequency and severity of insured loss events, (iv) mortality and morbidity levels

and trends, (v) persistency levels, (vi) interest rate levels, (vii) currency

exchange rates (viii) general competitive factors, (ix) changes in laws and

regulations, (x) changes in the policies of governments and/or regulatory authorities. ING assumes no obligation to update any forward-looking

information contained in this document.

www.ing.com