10-1 P ROPERTY, P LANT, A ND E QUIPMENT CHAPTER 10.

70

10-1 PROPERTY, PLANT, AND EQUIPMENT CHAPTER 10 CHAPTER 10

-

Upload

suzan-ellis -

Category

Documents

-

view

227 -

download

0

Transcript of 10-1 P ROPERTY, P LANT, A ND E QUIPMENT CHAPTER 10.

10-1

PROPERTY, PLANT,

AND EQUIPMENT

CHAPTER 10CHAPTER 10

10-2

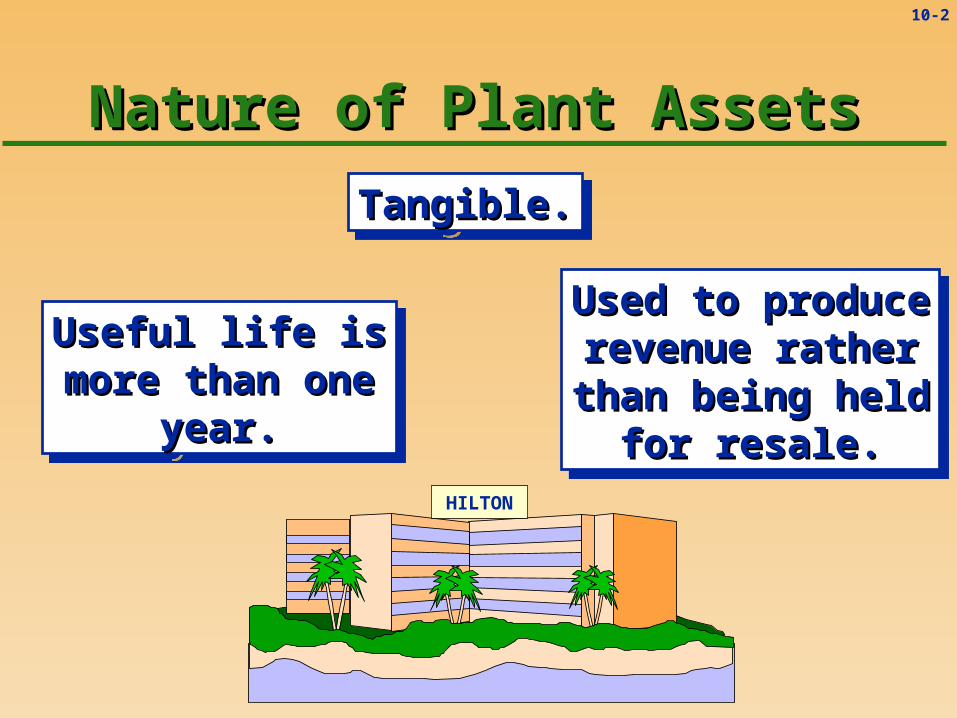

Nature of Plant AssetsNature of Plant Assets

Tangible.Tangible.Tangible.Tangible.

Used to produceUsed to producerevenue ratherrevenue ratherthan being heldthan being held

for resale.for resale.

Used to produceUsed to producerevenue ratherrevenue ratherthan being heldthan being held

for resale.for resale.

Useful life isUseful life ismore than onemore than one

year.year.

Useful life isUseful life ismore than onemore than one

year.year.

HILTON

10-3

Nature of Plant AssetsNature of Plant Assets1. Recordacquisitionof asset.

2. Record depreciation.3. Record subsequent expenditures.

4. Recorddisposalof asset.

Assetcost

Disposalof asset

Salvagevalue

$

Time (useful life)

Decline in asset’s service potential

367

10-4

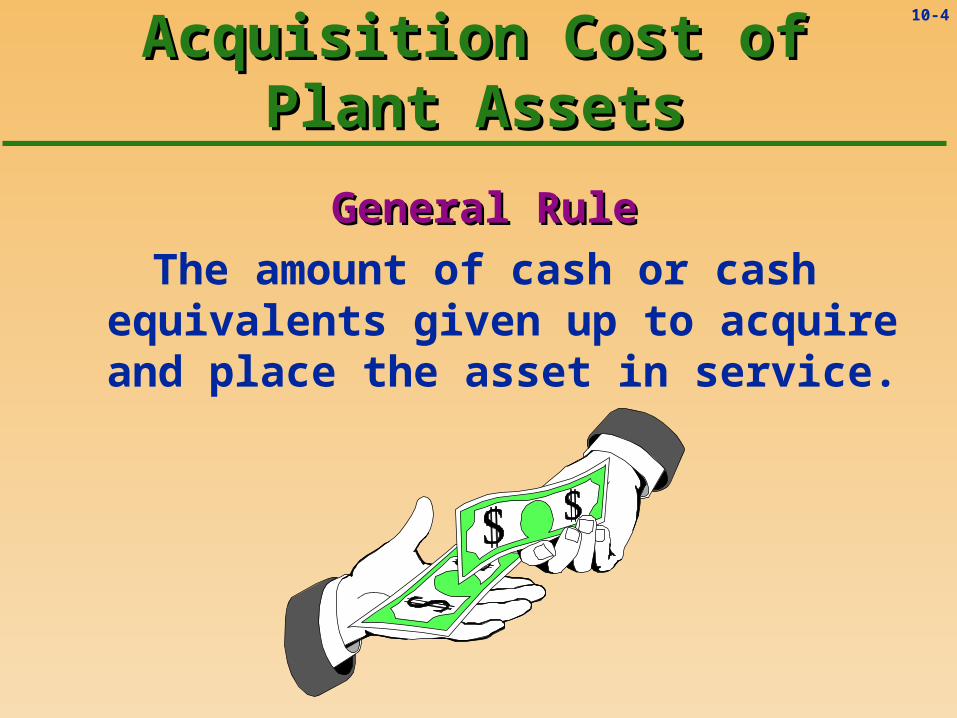

Acquisition Cost ofAcquisition Cost ofPlant AssetsPlant Assets

General RuleGeneral Rule

The amount of cash or cash equivalents given up to acquire and place the asset

in service.

10-5

Computers-R-Us

Acquisition Cost ofAcquisition Cost ofPlant AssetsPlant Assets

More on General RuleMore on General Rule

Includes cost incurred to get the asset

into the position and condition to start

earning revenue.

10-6

Acquisition CostAcquisition CostLandLand

Purchase priceReal estate

commissions Title search

Title transferfees

Title insurancepremiums

10-7

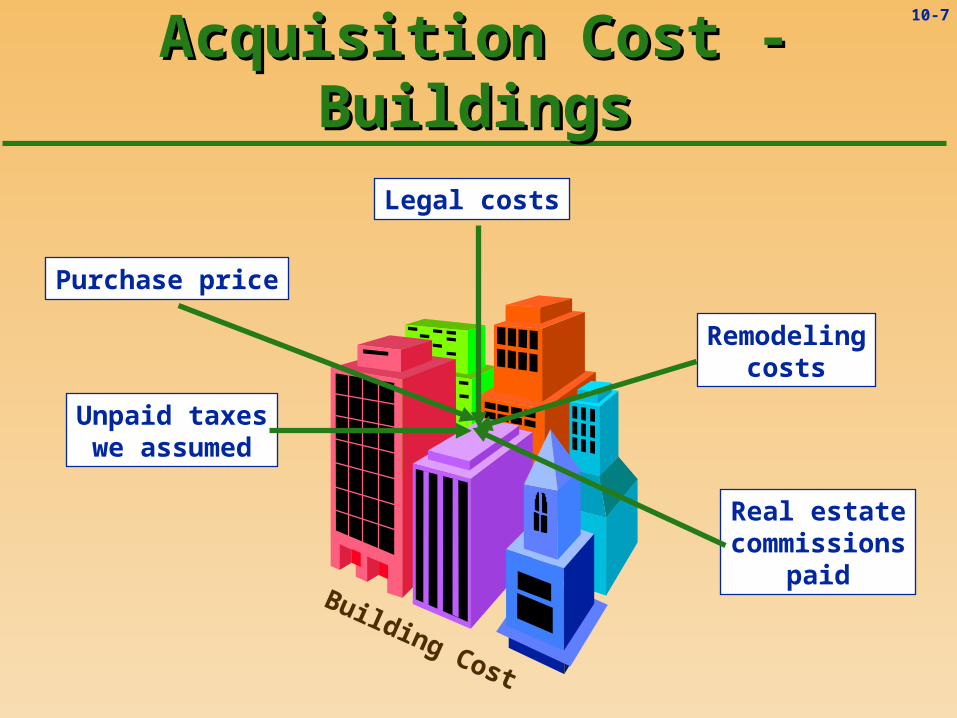

Acquisition Cost - BuildingsAcquisition Cost - Buildings

Purchase price

Remodelingcosts

Unpaid taxeswe assumed

Legal costs

Real estatecommissions

paidBuilding Cost

10-8

““Basket” Purchase of AssetsBasket” Purchase of Assets

When assets are purchased together, separate the cost into the proper

accounts ...

... on the basis of relative fair market value.

10-9

Group Purchase of AssetsGroup Purchase of AssetsOn January 1, we purchase land and

building for $200,000 cash. The appraised value of the building is

$162,500, and the land is appraised at $87,500.

How much of the $200,000 purchase How much of the $200,000 purchase price do we debit to the separate price do we debit to the separate

building and land accounts?building and land accounts?

10-10

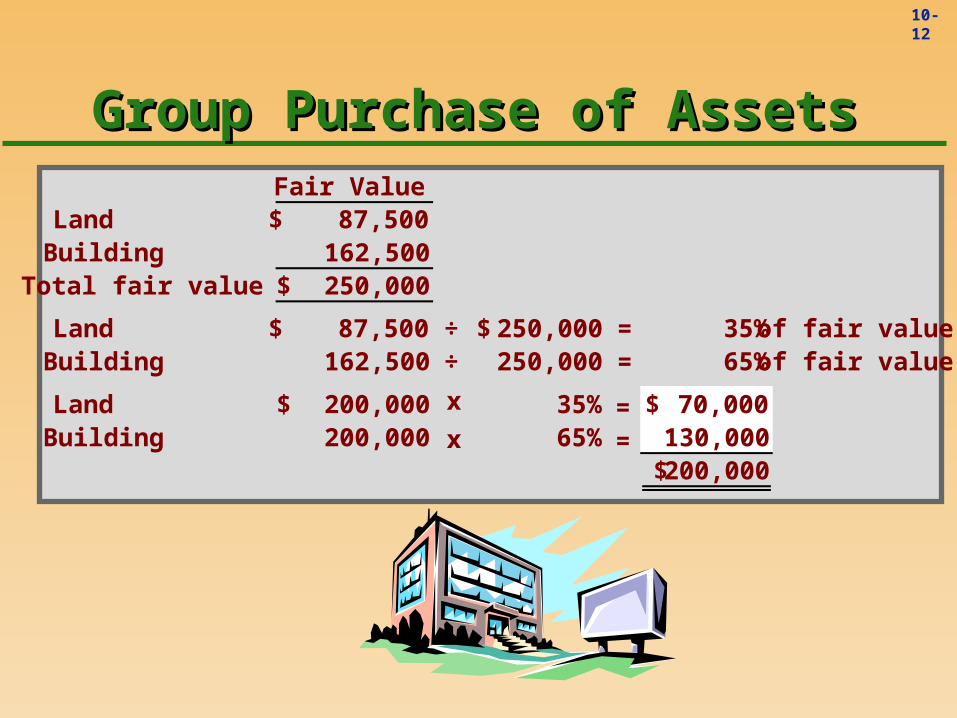

Group Purchase of AssetsGroup Purchase of AssetsFair Value

Land 87,500$ Building 162,500 Total fair value 250,000$

10-11

Group Purchase of AssetsGroup Purchase of AssetsFair Value

Land 87,500$ Building 162,500 Total fair value 250,000$

Land 87,500$ ÷ 250,000$ = 35% of fair valueBuilding 162,500 ÷ 250,000 = 65% of fair value

10-12

Group Purchase of AssetsGroup Purchase of AssetsFair Value

Land 87,500$ Building 162,500 Total fair value 250,000$

Land 87,500$ ÷ 250,000$ = 35% of fair valueBuilding 162,500 ÷ 250,000 = 65% of fair value

Land 200,000$ 35% 70,000$ Building 200,000 65% 130,000

200,000$

x

x==

10-13

Acquisition Cost - EquipmentAcquisition Cost - Equipment

Net purchaseprice

Transportationcosts

Installationcosts

Testingcosts

Insurancewhile intransit

10-14

Acquisition CostAcquisition CostSelf-Constructed AssetsSelf-Constructed Assets

The cost should include all materials used and labor directly traceable to the construction as well as indirect costs

such as interest, utilities, and supervision.

10-15

Noncash AcquisitionsNoncash Acquisitions

A plant asset may be acquired in exchange for noncash items, such

as land, stock or notes payable.

10-16

Noncash AcquisitionsNoncash Acquisitions

Fair market value is the price received for an item sold in the normal course of business.

Accountants generally record noncash exchanges at fair market value.

Let’s trade this guyLet’s trade this guyfor a new pitcher!for a new pitcher!

10-17

Noncash AcquisitionsNoncash Acquisitions

General RuleGeneral RuleRecord the asset received at the fair market value of the asset received or

the fair market value of the asset given up, whichever is more clearly evident.

10-18

Noncash AcquisitionsNoncash Acquisitions

If fair market value cannot be determinedcannot be determined, use appraised value to record a noncash

transaction.

As an expert, Ibelieve he’s worth

$3,500,000.

10-19

Noncash AcquisitionsNoncash Acquisitions

Book value is the asset’s cost less accumulated depreciation.

We would only assign book value of the asset given up to the asset received

when better information is unavailableunavailable.You don’t know what you’re

talking about! No way is thisplayer worth $3,500,000.

10-20

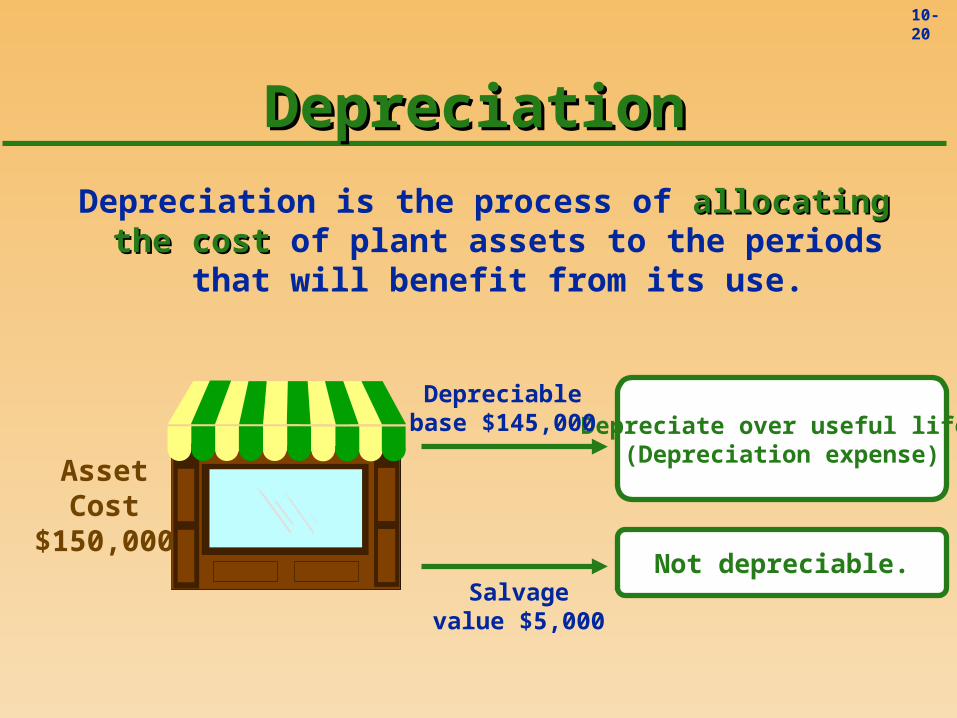

DepreciationDepreciation

Depreciation is the process of allocating the cost allocating the cost of plant assets to the periods that will benefit from

its use.

AssetCost

$150,000

Depreciate over useful life.(Depreciation expense)

Not depreciable.

Depreciablebase $145,000

Salvagevalue $5,000

10-21

DepreciationDepreciationDepreciation is the process of allocating the cost allocating the cost of plant assets to the periods

that will benefit from its use.

Depreciation is a cost allocation processcost allocation process and has nothing to do with asset valuation.

10-22

DepreciationDepreciation

Factors Affecting DepreciationFactors Affecting DepreciationAsset costEstimated salvage valueEstimated useful lifeDepreciation method used

10-23

Depreciation MethodsDepreciation Methods

Straight-line

Units-of-production

Accelerated methods Sum-of-the-years’-digits Double-declining-balance

10-24

Straight-Line DepreciationStraight-Line Depreciation

DepreciationDepreciation ExpenseExpense

Asset Cost - Asset Cost - Est.Est. Salvage Value Salvage Value Est.Est. Useful Life Useful Life

==

10-25

Straight-Line DepreciationStraight-Line DepreciationExampleExample

On January 1, Ace, Inc. purchased equipmentfor $27,500 cash. The equipment has an

estimated useful life of 5 years and anestimated salvage value of $2,500.

What is the annual straight-linedepreciation expense?

10-26

Straight-Line DepreciationStraight-Line DepreciationExampleExample

Asset cost 27,500$ Less: salvage value (2,500) Basis for depreciation 25,000 Useful life ÷ 5 Annual depreciation 5,000$

10-27

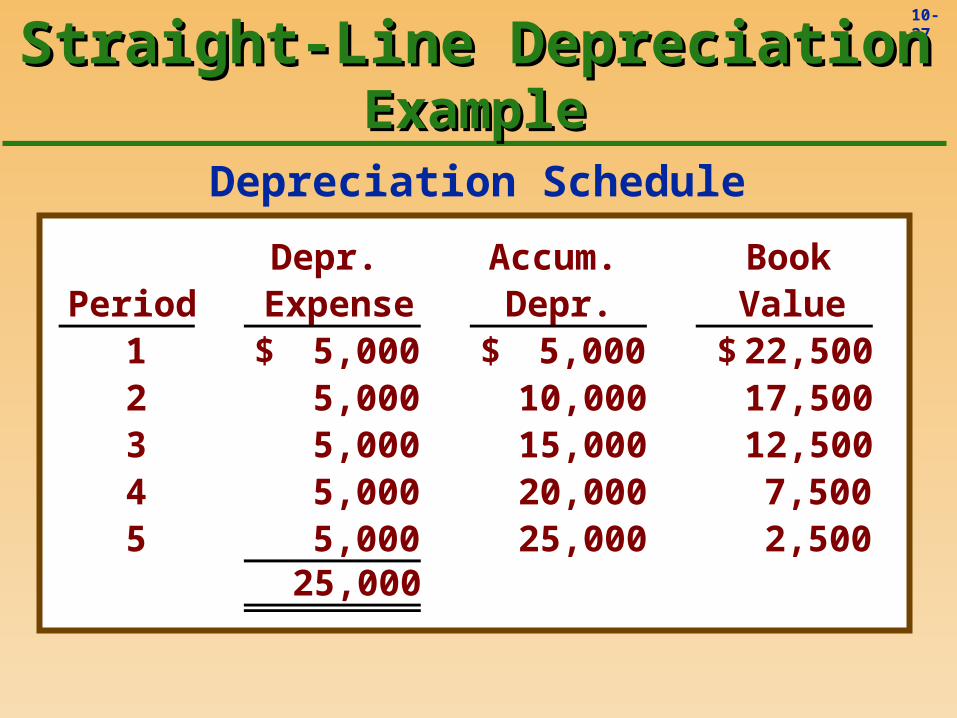

Straight-Line DepreciationStraight-Line DepreciationExampleExample

PeriodDepr.

ExpenseAccum. Depr.

Book Value

1 5,000$ 5,000$ 22,500$ 2 5,000 10,000 17,500 3 5,000 15,000 12,500 4 5,000 20,000 7,500 5 5,000 25,000 2,500

25,000

Depreciation Schedule

10-28

Straight-Line DepreciationStraight-Line DepreciationExampleExample

$-

$5,000

$10,000

$15,000

$20,000

$25,000

1 2 3 4 5

Depr. Expense

Accum. Depr.

Book Value

10-29

Units-of-Production DepreciationUnits-of-Production Depreciation

DepreciationDepreciation Per UnitPer Unit

== Asset Cost - Asset Cost - Est.Est. Salvage Value Salvage Value Est.Est. Total Units of Production Total Units of Production

10-30

DepreciationDepreciation Per PeriodPer Period

= Depreciation Number of UnitsDepreciation Number of Units Per Unit ProducedPer Unit Produced

x

Units-of-Production DepreciationUnits-of-Production Depreciation

DepreciationDepreciation Per UnitPer Unit

== Asset Cost - Asset Cost - Est.Est. Salvage Value Salvage Value Est.Est. Total Units of Production Total Units of Production

10-31

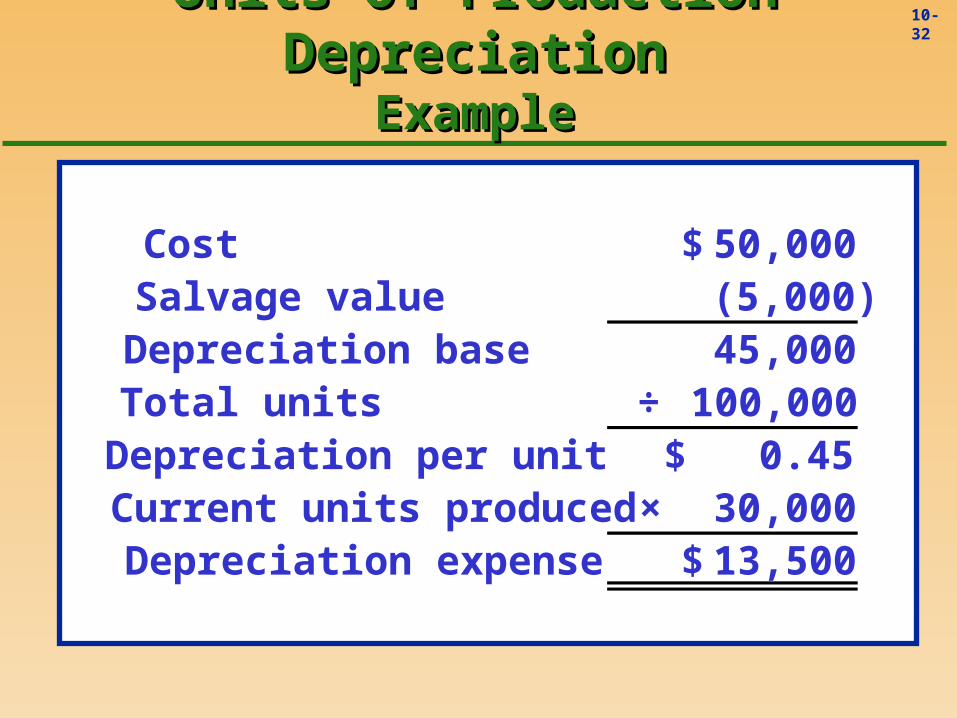

Units-of-Production DepreciationUnits-of-Production DepreciationExampleExample

On January 1, we purchase equipment for $50,000 cash. The equipment is expected to produce 100,000 units during its life and has

an estimated salvage value of $5,000.

If 30,000 were produced this year, what is the amount of depreciation expense?

10-32

Units-of-Production DepreciationUnits-of-Production DepreciationExampleExample

Cost 50,000$ Salvage value (5,000) Depreciation base 45,000 Total units ÷ 100,000 Depreciation per unit 0.45$ Current units produced × 30,000 Depreciation expense 13,500$

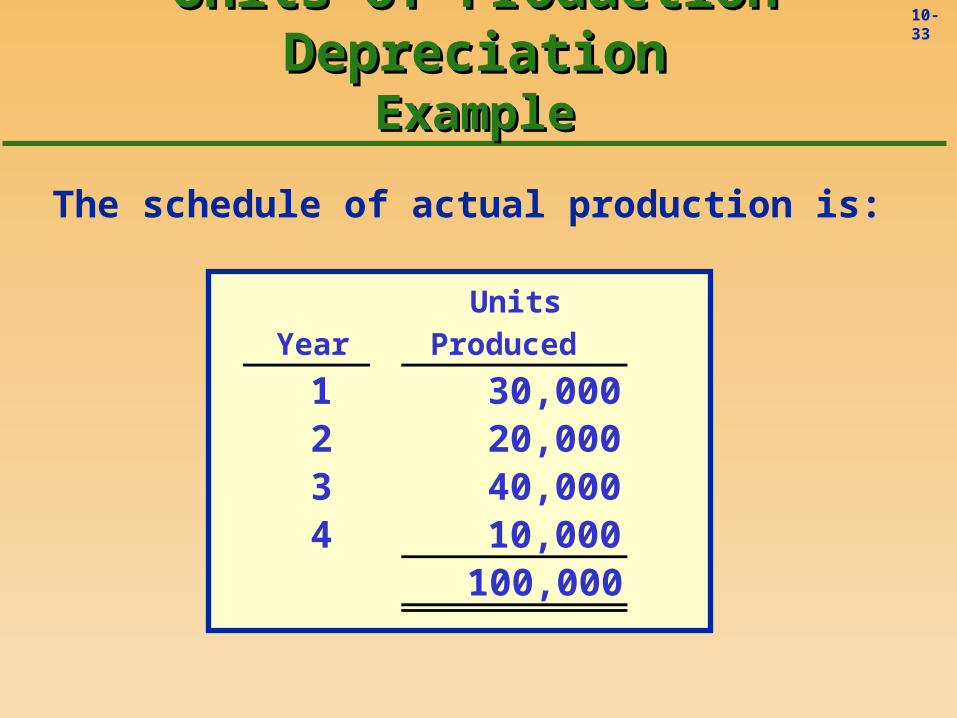

10-33

Units-of-Production DepreciationUnits-of-Production DepreciationExampleExample

The schedule of actual production is:

Year Units

Produced

1 30,000 2 20,000 3 40,000 4 10,000

100,000

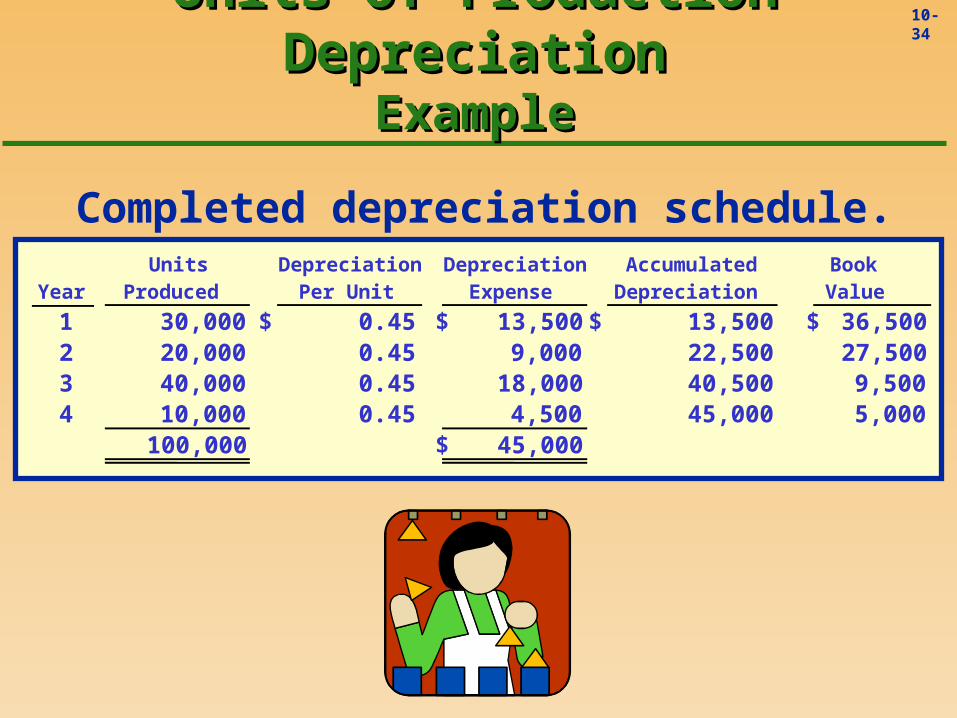

10-34

Units-of-Production DepreciationUnits-of-Production DepreciationExampleExample

Completed depreciation schedule.

Year Units

Produced Depreciation

Per Unit Depreciation

Expense Accumulated Depreciation

Book Value

1 30,000 0.45$ 13,500$ 13,500$ 36,500$ 2 20,000 0.45 9,000 22,500 27,500 3 40,000 0.45 18,000 40,500 9,500 4 10,000 0.45 4,500 45,000 5,000

100,000 45,000$

10-35

Units-of-Production DepreciationUnits-of-Production DepreciationExampleExample

-

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

50,000

1 2 3 4

Units Produced

Depreciation Expense

Accumulated Depreciation

10-36

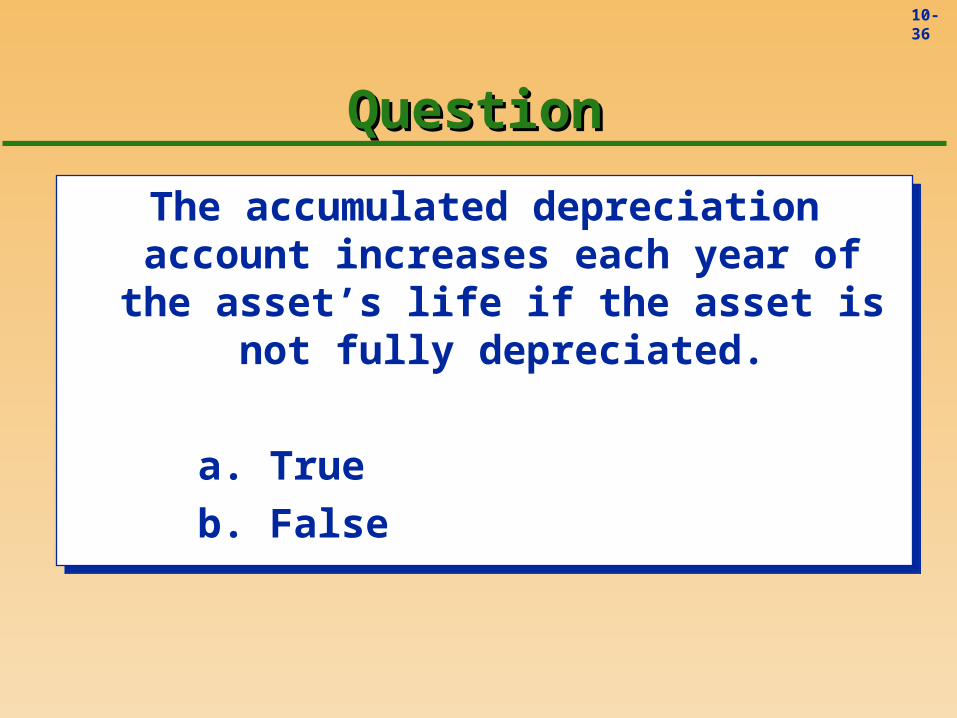

QuestionQuestion

The accumulated depreciation account increases each year of the asset’s life if

the asset is not fully depreciated.

a. True

b. False

The accumulated depreciation account increases each year of the asset’s life if

the asset is not fully depreciated.

a. True

b. False

10-37

Accelerated DepreciationAccelerated Depreciation

Sum-of-the-Years’ Digits

Double-Declining Balance

10-38

Sum-of-Years’-Digits DepreciationSum-of-Years’-Digits Depreciation(SOYD)(SOYD)

SOYD =

n n + 1

2

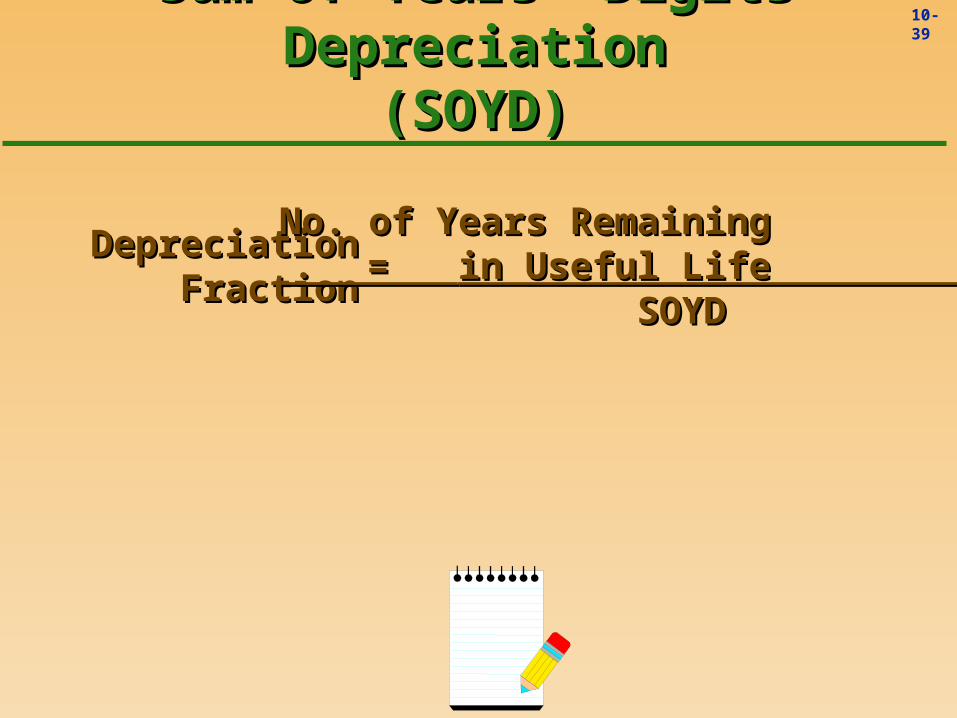

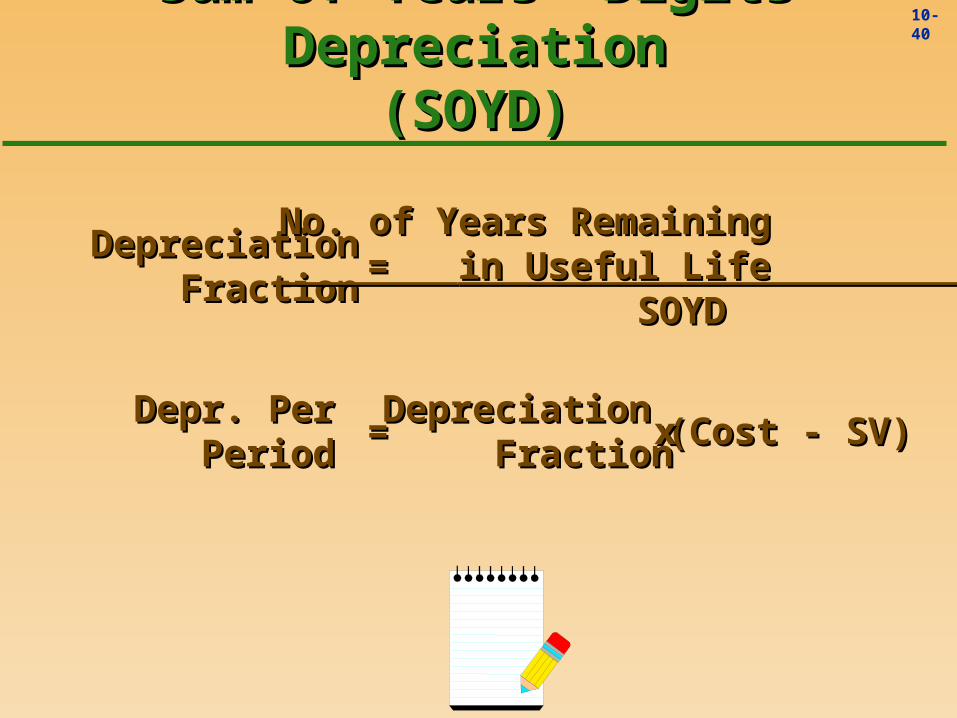

10-39

Sum-of-Years’-Digits DepreciationSum-of-Years’-Digits Depreciation(SOYD)(SOYD)

DepreciationDepreciation FractionFraction

No. of Years RemainingNo. of Years Remaining in Useful Life in Useful Life SOYDSOYD

==

10-40

Depr. PerDepr. Per PeriodPeriod

DepreciationDepreciation FractionFraction (Cost - SV)(Cost - SV)== xx

Sum-of-Years’-Digits DepreciationSum-of-Years’-Digits Depreciation(SOYD)(SOYD)

DepreciationDepreciation FractionFraction

No. of Years RemainingNo. of Years Remaining in Useful Life in Useful Life SOYDSOYD

==

10-41

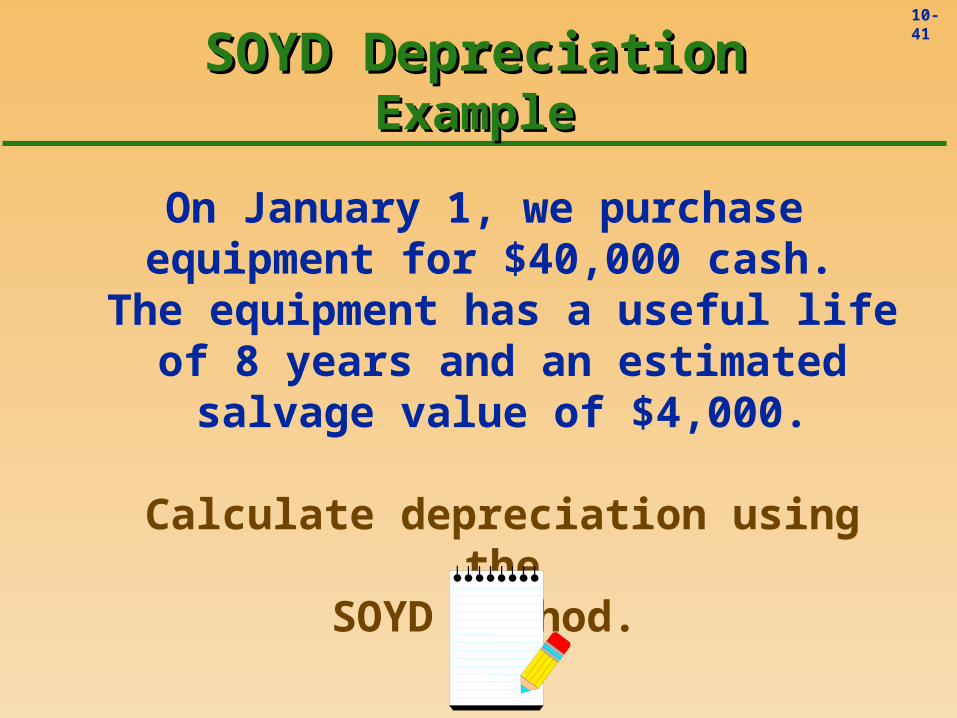

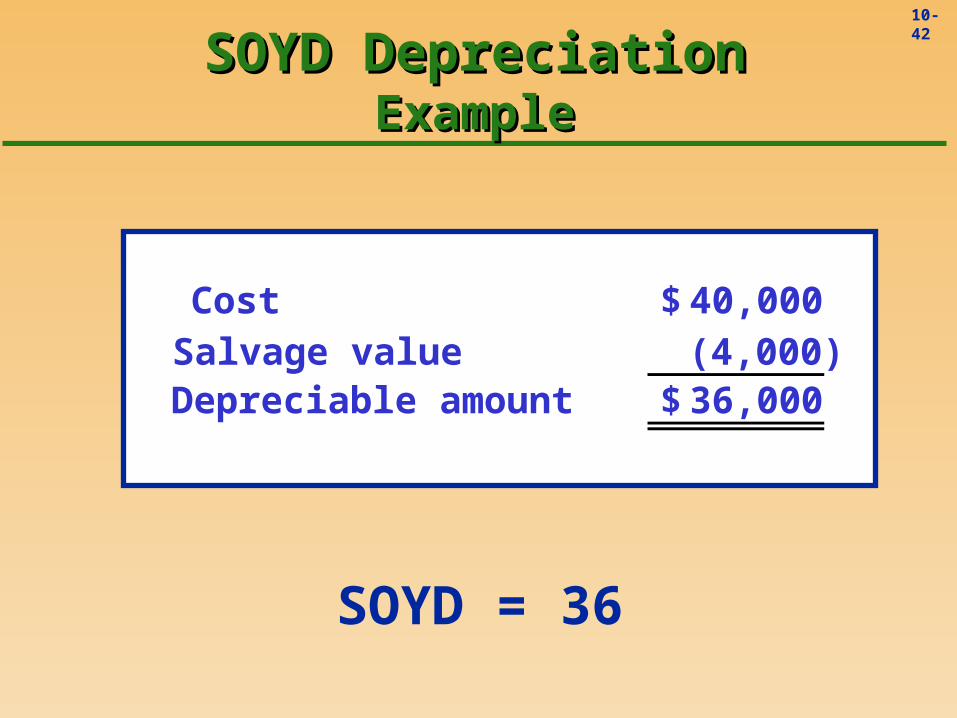

SOYD DepreciationSOYD DepreciationExampleExample

On January 1, we purchase equipment for $40,000 cash. The equipment has a useful life of 8 years and an estimated

salvage value of $4,000.

Calculate depreciation using theSOYD method.

10-42

SOYD = 36

Cost 40,000$ Salvage value (4,000) Depreciable amount 36,000$

SOYD DepreciationSOYD DepreciationExampleExample

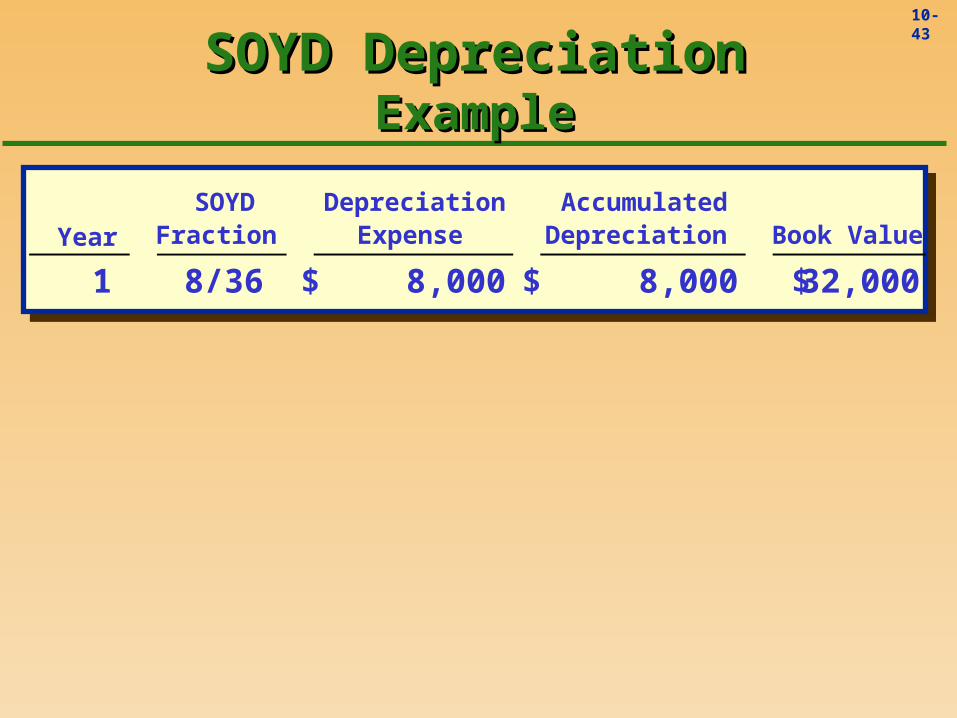

10-43

Year SOYD

Fraction Depreciation

Expense Accumulated Depreciation Book Value

1 8/36 8,000$ 8,000$ 32,000$

SOYD DepreciationSOYD DepreciationExampleExample

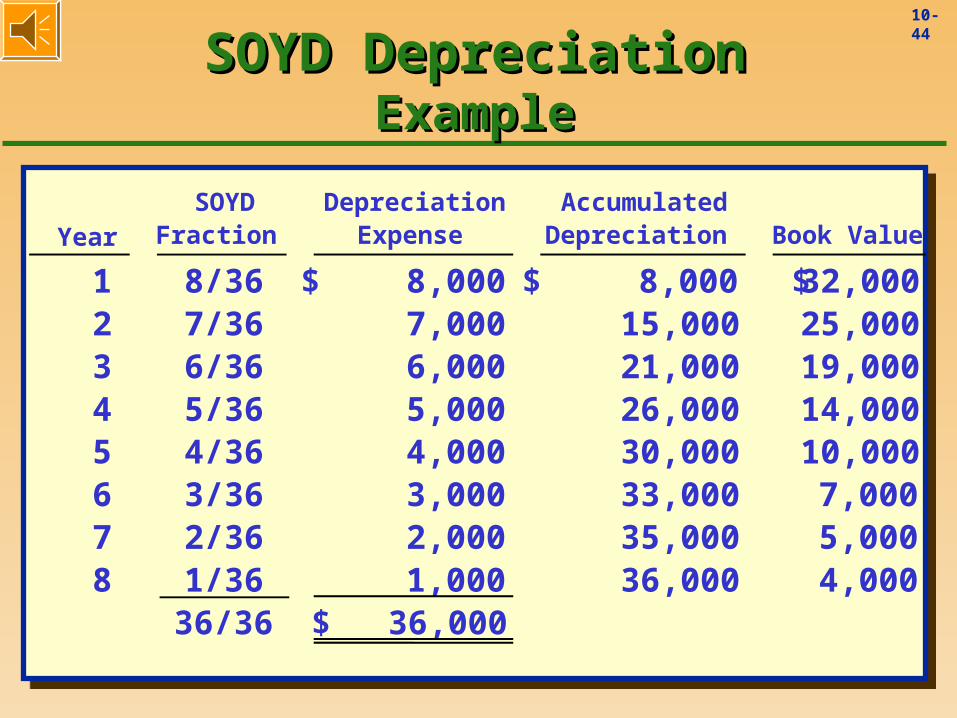

10-44

Year SOYD

Fraction Depreciation

Expense Accumulated Depreciation Book Value

1 8/36 8,000$ 8,000$ 32,000$ 2 7/36 7,000 15,000 25,000 3 6/36 6,000 21,000 19,000 4 5/36 5,000 26,000 14,000 5 4/36 4,000 30,000 10,000 6 3/36 3,000 33,000 7,000 7 2/36 2,000 35,000 5,000 8 1/36 1,000 36,000 4,000

36/36 36,000$

SOYD DepreciationSOYD DepreciationExampleExample

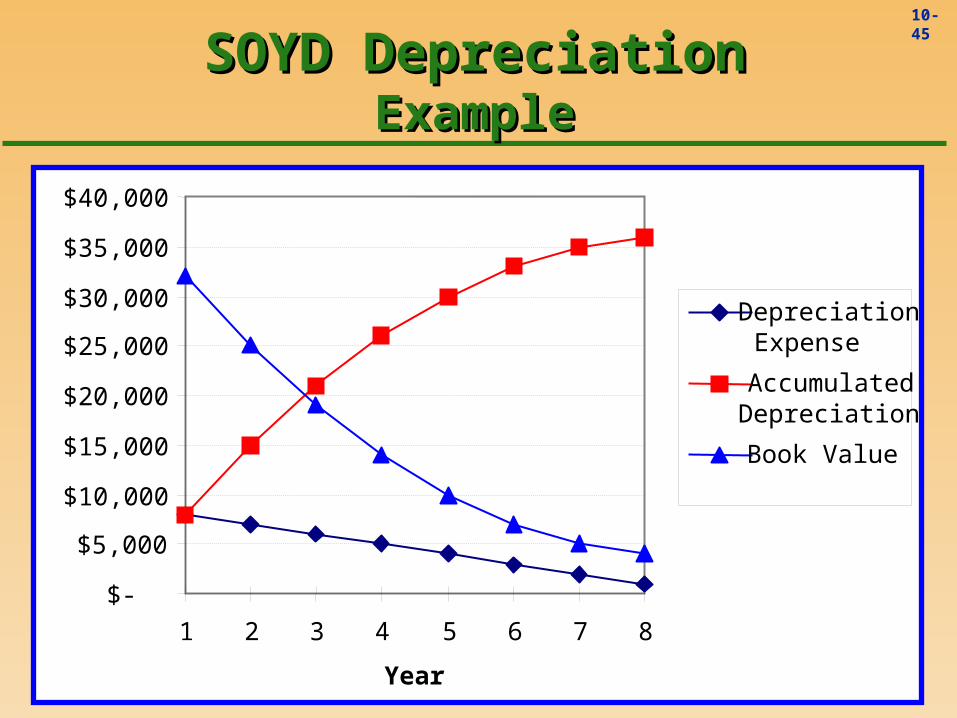

10-45

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

$35,000

$40,000

1 2 3 4 5 6 7 8

Year

DepreciationExpense

AccumulatedDepreciation

Book Value

SOYD DepreciationSOYD DepreciationExampleExample

10-46

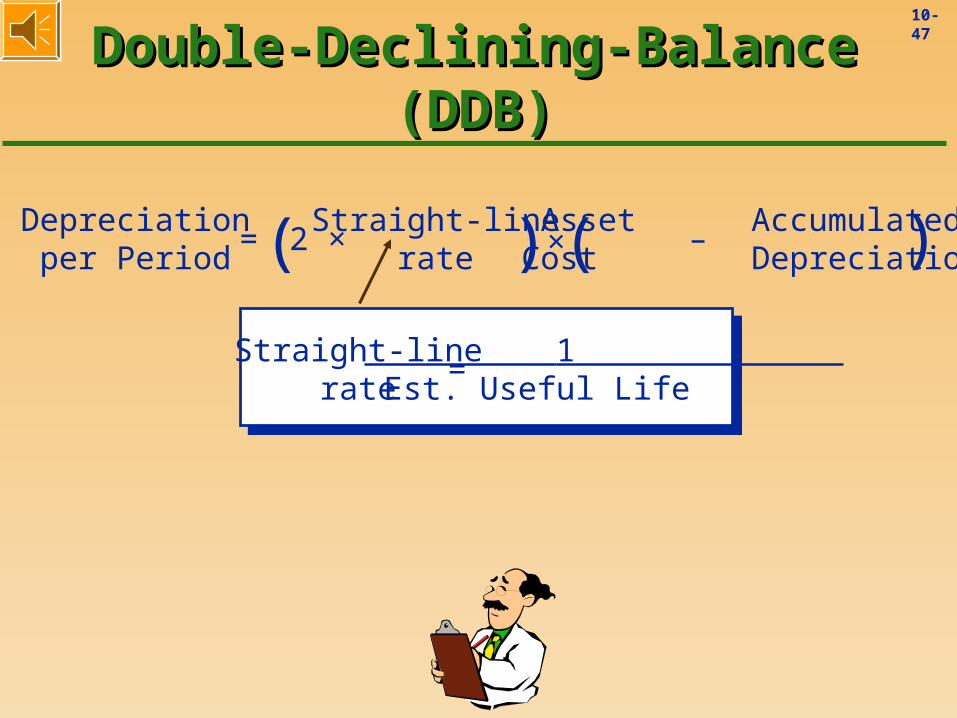

Double-Declining-Balance (DDB)Double-Declining-Balance (DDB)

Depreciationper Period

= 2 ×Straight-line

rate ×Asset AccumulatedCost Depreciation( ) –( )

i.e., Book Value at beginning of period.

i.e., Book Value at beginning of period.

10-47

Double-Declining-Balance (DDB)Double-Declining-Balance (DDB)

Depreciationper Period

= 2 ×Straight-line

rate ×Asset AccumulatedCost Depreciation( ) –( )

Straight-linerate

= 1 Est. Useful Life

10-48

Straight-linerate

= 1 Est. Useful Life

Double-Declining-Balance (DDB)Double-Declining-Balance (DDB)

Depreciationper Period

= 2 ×Straight-line

rate ×Asset AccumulatedCost Depreciation( ) –( )

Ignore salvage value whencalculating DDB depreciation!

10-49

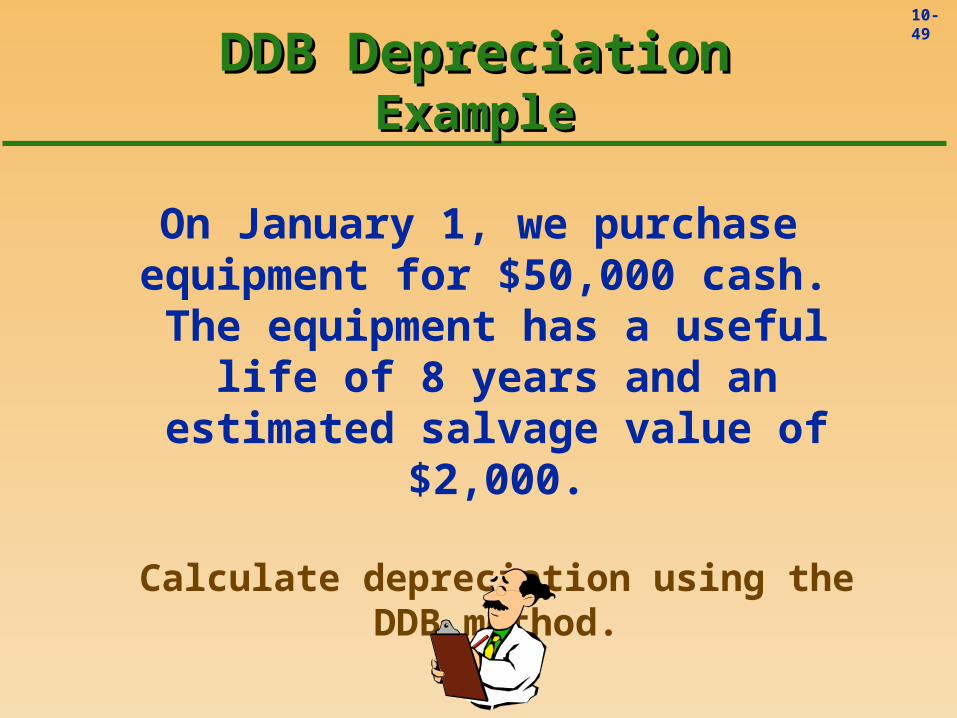

DDB DepreciationDDB DepreciationExampleExample

On January 1, we purchase equipment for $50,000 cash. The equipment has

a useful life of 8 years and an estimated salvage value of $2,000.

Calculate depreciation using the DDB method.

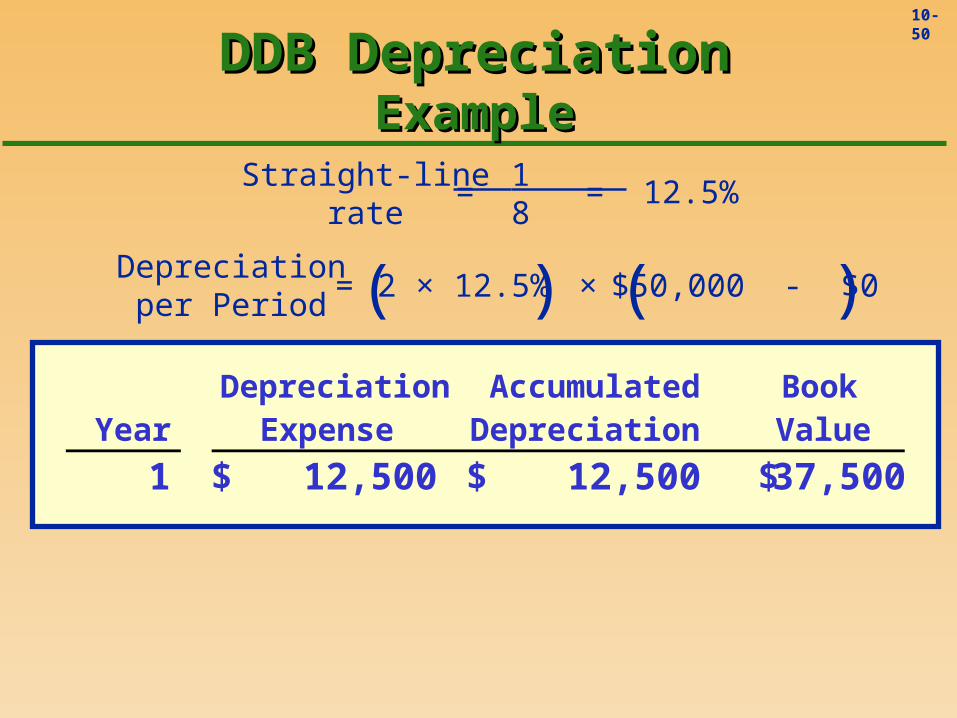

10-50

Year Depreciation

Expense Accumulated Depreciation

Book Value

1 12,500$ 12,500$ 37,500$

Straight-linerate

= 1 8

= 12.5%

Depreciationper Period

= 2 × 12.5% ×( ) ( )$50,000 - $0

DDB DepreciationDDB DepreciationExampleExample

10-51

Year Depreciation

Expense Accumulated Depreciation

Book Value

1 12,500$ 12,500$ 37,500$ 2 9,375 21,875 28,125 3 7,031 28,906 21,094 4 5,273 34,180 15,820 5 3,955 38,135 11,865 6 2,966 41,101 8,899 7 2,225 43,326 6,674 8 1,669 44,994 5,006

44,994$ Hey, shouldn’t the totaldepreciation expense be $48,000?

*

*

*Rounding difference

DDB DepreciationDDB DepreciationExampleExample

10-52

Year Depreciation

Expense Accumulated Depreciation

Book Value

1 12,500$ 12,500$ 37,500$ 2 9,375 21,875 28,125 3 7,031 28,906 21,094 4 5,273 34,180 15,820 5 3,955 38,135 11,865 6 2,966 41,101 8,899 7 2,225 43,326 6,674 8 4,674 48,000 2,000

48,000$

When using DDB it is sometimes necessaryto adjust the last year’s depreciation so

that Book Value will equal Salvage Value.

DDB DepreciationDDB DepreciationExampleExample

10-53

$-

$5,000

$10,000$15,000

$20,000

$25,000

$30,000

$35,000$40,000

$45,000

$50,000

1 2 3 4 5 6 7 8

Year

DepreciationExpense

AccumulatedDepreciation

Book Value

DDB DepreciationDDB DepreciationExampleExample

10-54

Partial-Year DepreciationPartial-Year Depreciation

If an asset is purchased sometime during the year, we have to adjust annual

depreciation for the partial-year period.

June30

10-55

Partial-Year DepreciationPartial-Year DepreciationExampleExample

On June 30, 19X1 we purchased equipment for $75,000 cash. The

equipment has a useful life of 10 years and estimated salvage value of $5,000.

Calculate the straight-line depreciation for the year ended December 31, 19X1.

10-56

Partial-Year DepreciationPartial-Year DepreciationExampleExample

Ann. Depr. = ($75,000 - $5,000) ÷ 10 = $7,000

Depr. Expense = $7,000 × = $3,500 6 12

June30

10-57

Changes in EstimatesChanges in Estimates

UsefulLife?

Because depreciation is based on the estimated estimated useful life and estimated estimated salvage value, depreciation expense is an estimateestimate.

Over the life of an asset, new information may come to light that indicates the original estimated useful life or salvage value was inaccurate.

10-58

Changes in EstimatesChanges in Estimates

If the useful life or salvage value of an asset changes, we must revise depreciation expense for the current and future periods. (i.e., prospectively not retroactively.)

For this change in accounting estimatechange in accounting estimate, we spread the remaining undepreciated cost (book value) over the remaining useful life - like peanut butter.

10-59

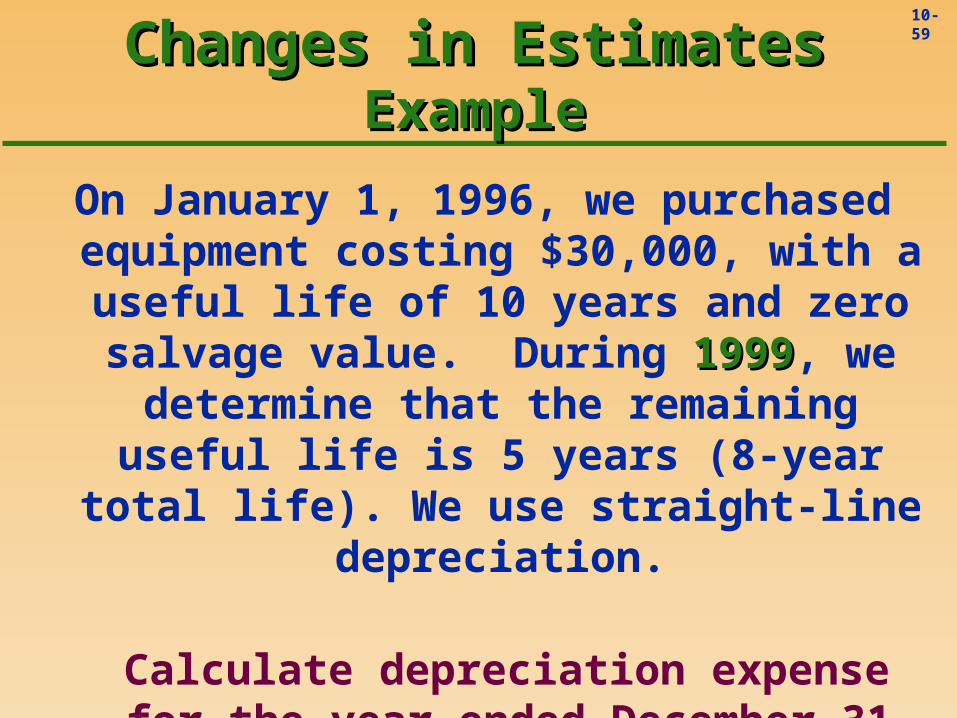

Changes in EstimatesChanges in EstimatesExampleExample

On January 1, 1996, we purchased equipment costing $30,000, with a useful life of 10 years and zero salvage value.

During 19991999, we determine that the remaining useful life is 5 years (8-year

total life). We use straight-line depreciation.

Calculate depreciation expense for the year ended December 31, 1999.

10-60

Changes in EstimatesChanges in EstimatesExampleExample

Cost 30,000$ Salvage value - Depreciation base 30,000 Useful life ÷ 10 Annual depreciation 3,000 1996 - 1998 × 3 Accumulated depreciation 9,000$

10-61

Depreciation for 1999, and subsequentyears, will be $4,200.

Changes in EstimatesChanges in EstimatesExampleExample

Cost 30,000$ Accumulated depreciation (9,000) Book value 21,000 Remaining useful life ÷ 5 Annual depreciation 4,200 $

10-62

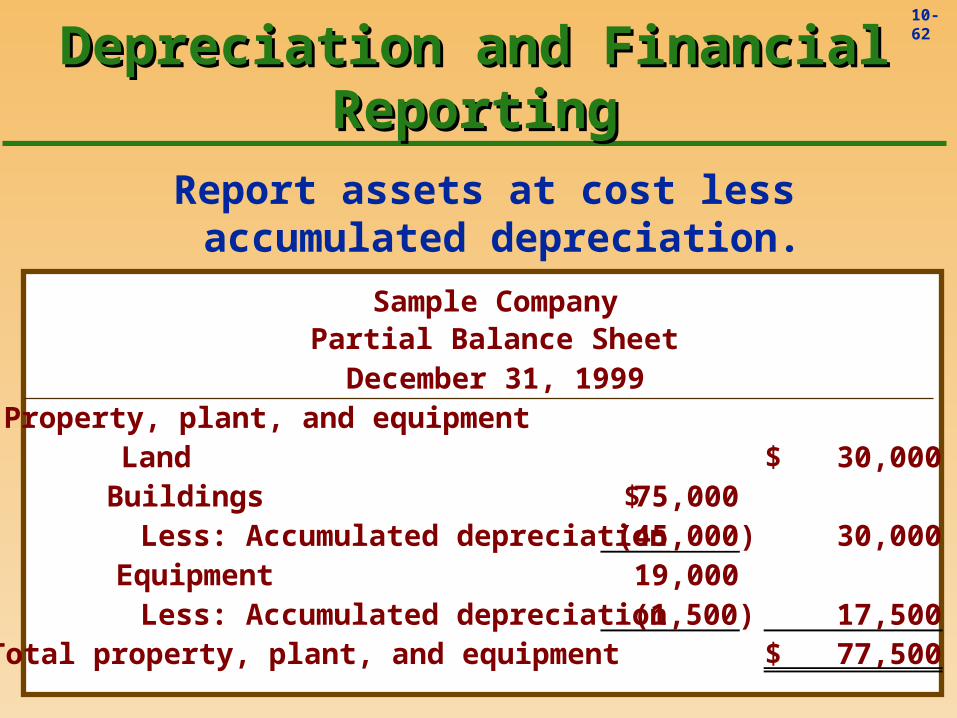

Depreciation and Financial Depreciation and Financial ReportingReporting

Report assets at cost less accumulated depreciation.

Sample CompanyPartial Balance Sheet

December 31, 1999Property, plant, and equipment Land 30,000$ Buildings 75,000$ Less: Accumulated depreciation (45,000) 30,000 Equipment 19,000 Less: Accumulated depreciation (1,500) 17,500 Total property, plant, and equipment 77,500$

10-63

Subsequent Expenditures Subsequent Expenditures on Assets (P.382)on Assets (P.382)

Please note:

““Expenditure” = “Expense”Expenditure” = “Expense”

10-64

Subsequent Expenditures Subsequent Expenditures on Assets (P.382)on Assets (P.382)

Increases qualityof services of

the asset.

Extends servicesbeyond original

estimate.

Debit maintenanceexpense

Debit asset account.Debit accumulated

depreciation.

Does not extend thequality or

quantity of services.

Capital expenditure(allocate over life

of asset)

Revenue expenditure(expensed in thecurrent period)

10-65

Subsequent Expenditures Subsequent Expenditures on Assets (P.382)on Assets (P.382)

Increases qualityof services of

the asset.

Debit asset account.

Relates to betterments or improvements.

(e.g., adding air conditioning to a delivery vehicle.)

Relates to betterments or improvements.

(e.g., adding air conditioning to a delivery vehicle.)

10-66

Subsequent Expenditures Subsequent Expenditures on Assets (P.382)on Assets (P.382)

Extends servicesbeyond original

estimate.

Debit accumulateddepreciation.

Relates to extraordinary

repairs.(e.g., replacing the engine in a delivery

vehicle.)

Relates to extraordinary

repairs.(e.g., replacing the engine in a delivery

vehicle.)

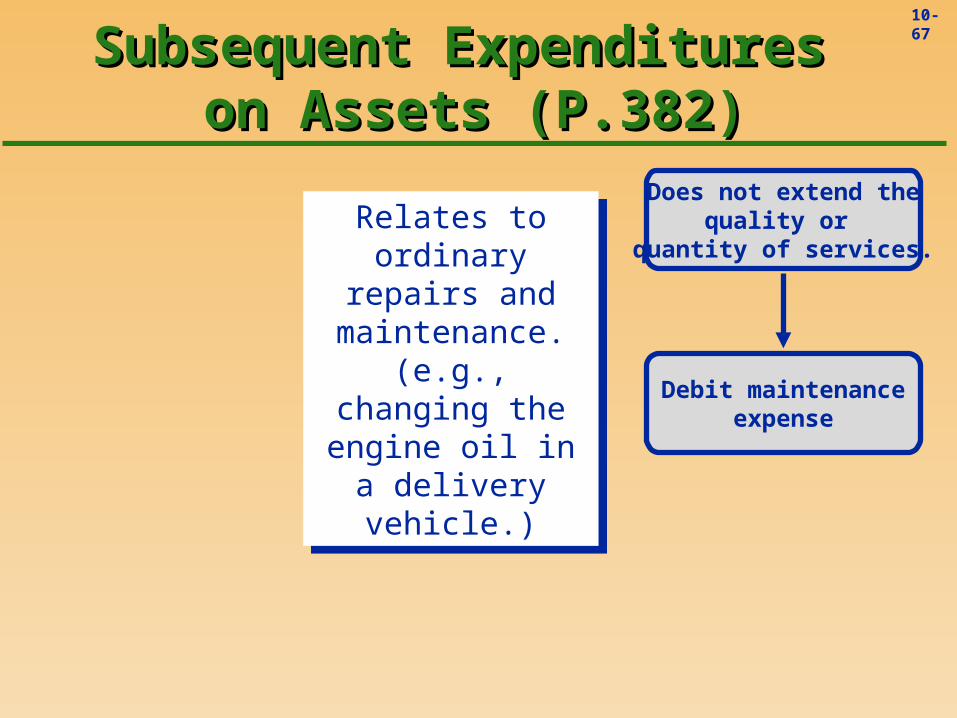

10-67

Subsequent Expenditures Subsequent Expenditures on Assets (P.382)on Assets (P.382)

Debit maintenanceexpense

Does not extend thequality or

quantity of services.Relates to ordinary

repairs and maintenance.

(e.g., changing the engine oil in a

delivery vehicle.)

Relates to ordinary repairs and

maintenance.(e.g., changing the

engine oil in a delivery vehicle.)

10-68

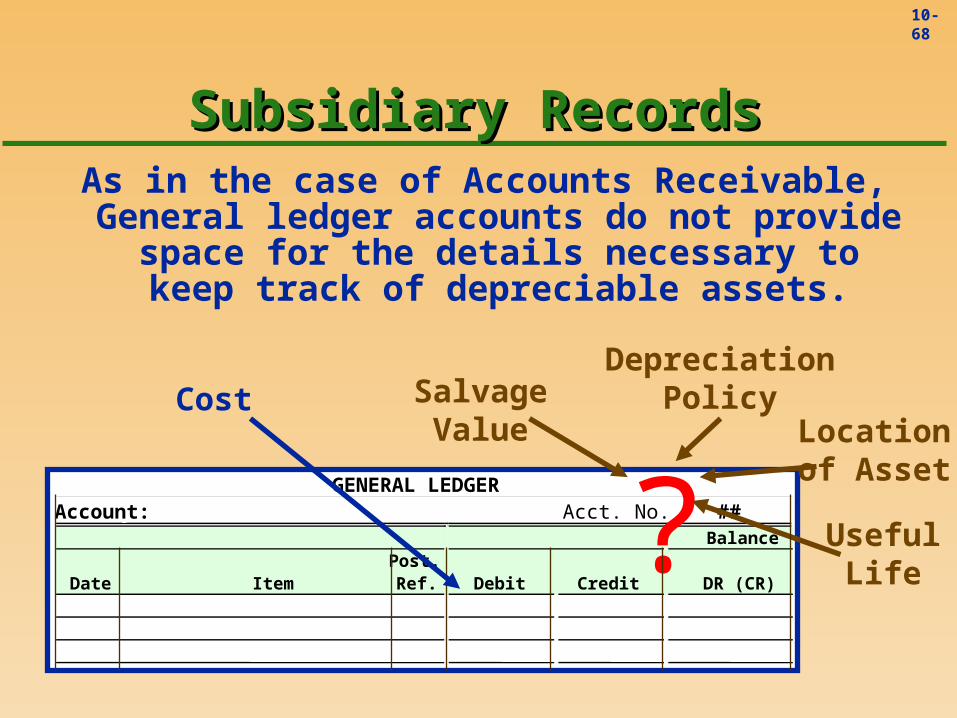

GENERAL LEDGERAccount: Acct. No. ## Balance

Date ItemPost. Ref. Debit Credit DR (CR)

?

Subsidiary RecordsSubsidiary RecordsAs in the case of Accounts Receivable, General ledger accounts do not provide space for the details necessary to keep

track of depreciable assets.

Cost SalvageValue

UsefulLife

Locationof Asset

DepreciationPolicy

10-69

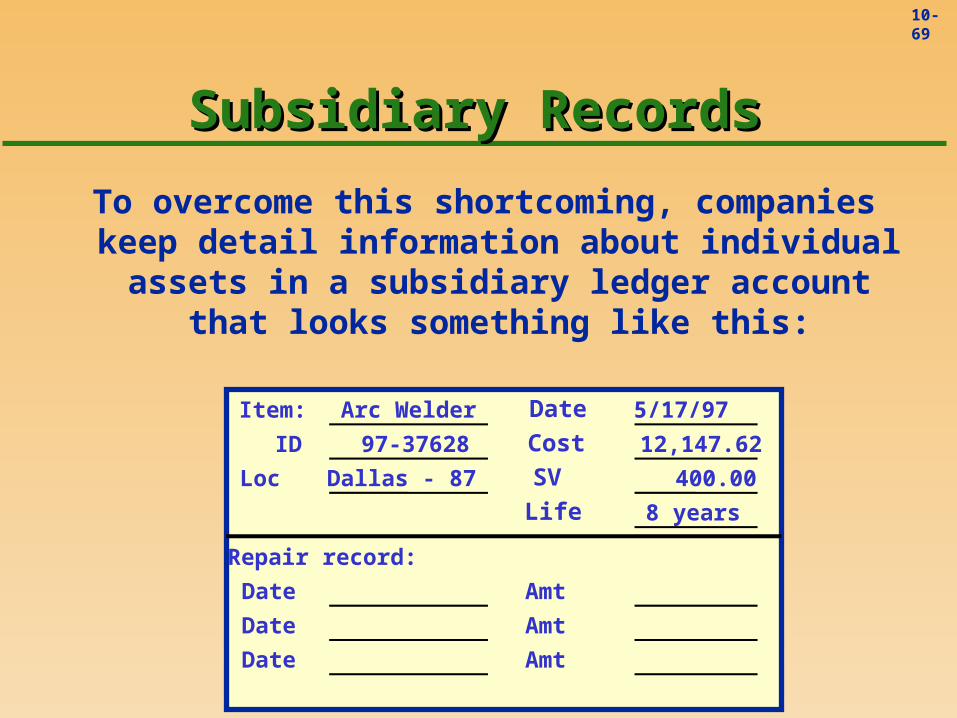

Subsidiary RecordsSubsidiary Records

To overcome this shortcoming, companies keep detail information about individual

assets in a subsidiary ledger account that looks something like this:

Item: Arc Welder Date 5/17/97

ID 97-37628 Cost 12,147.62

Loc Dallas - 87 SV 400.00

Life 8 years

Repair record:

Date Amt

Date Amt

Date Amt

10-70

Well, I guess this computer is about fully depreciated!