1 Rating Trends and Outlook Basic Industries Moody’s 2002 Corporate Finance Credit Outlook...

60

1 Rating Trends and Outlook Basic Industries Moody’s 2002 Corporate Finance Credit Outlook Investor Briefing New York, January 15, 2002

-

date post

22-Dec-2015 -

Category

Documents

-

view

216 -

download

0

Transcript of 1 Rating Trends and Outlook Basic Industries Moody’s 2002 Corporate Finance Credit Outlook...

1

Rating Trends and Outlook

Basic Industries

Moody’s 2002 Corporate Finance Credit Outlook Investor Briefing

New York, January 15, 2002

2

Paper and Forest Products

Mark Gray

Senior Vice President

3

Outline

• Ratings Trends and Activity

• Credit Issues and Ratings Outlooks

• Sector Trends and Outlook

4

0

2

4

6

8

10

12

No.

of I

ssue

rs

Global Forest & Paper Products - Rated Issuers

Total No. of Issuer: 59

5

Global Forest & Paper Rated Issuers

0

2

4

6

8

10

12

Nu

mb

er

of

Issu

ers

2001

2000

Total No. of Issuers: 59

6

Consolidated Industry Debt in the U.S.

Long Term Debt

01020304050607080

Year

in B

illi

on

$

7

Global Forest & Paper Issuers - Mean Ratings

Ba1

Baa3

Ba2

8

Global Forest & Paper Issuers - Rating Changes (LTM)

Investment Grade:

Upgrades: 1

Downgrades: 7

Speculative Grade:

Upgrades: 8

Downgrades: 12

9

Industry FundamentalsPulp and Paper

• Near-term Outlook: Negative. – Demand Driven Downcycle. – Lower Consumer Confidence on Recession and

Sept. 11.

• Intermediate / Longer Term Outlook: Positive. – Little New Capacity Construction– More High Cost Capacity Shut Down– Greater Sector Concentration / Producer Discipline

10

Industry FundamentalsBuilding Materials

• Near-term Outlook: Very Negative– Over-supply– Housing starts may dip on lower consumer

confidence– Canadian quota issue unresolved (lumber)– Fragmented markets with desperate

participants.

11

The Bottom Line

• Recovery in 2002, if– The economy avoids a deep and

prolonged recession, and

– The active and visible portion of the war ends relatively quickly.

12

Overall Ratings Outlook:Negative

• Cash Flow Weak Over the Near Term.

• Lots of Debt Remaining From Acquisitions.

• Weaker Market for Asset Sales.

• Event Risk Still High.

• Liquidity Becoming An Issue (Baa and Below)

13

Sector Outlooks

Market Pulp Stable/neg Positive

Uncoated Freesheet Stable/neg Positive

Newsprint Negative Positive

Packaging grades Negative Stable/pos

Coated paper Stable/neg Neutral/neg

Panels Negative Neutral/neg

Sector Short term Int/long

14

NBSK Pulp Price and Norscan Inventories

0

100

200

300

400

500

600

700

800

900

1000

Dec-93

Jun-94

Dec-94

Jun-95

Dec-95

Jun-96

Dec-96

Jun-97

Dec-97

Jun-98

Dec-98

Jun-99

Dec-99

Jun-00

Dec-00

Jun-01

Aug-01

Oct-01

(US

D/T

)

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

Inve

ntor

ies

- Mill

ions

of

Tons

NBSK Pulp Prices Norscan InventoriesSource: Pulp & Paper Week

15

Pulp

• Sharp Slowdown in the U.S. Economy

• Strong U.S.$

Intermediate-term: Positive (demand recovery)• Economic Recovery in 2002.

• Current Weakening Trend of the U.S. Dollar.

Longer- term: Negative (over-supply)• New Capacity (South American and Asia) Likely

to Outstrip Demand Growth.

Near-term: Negative (weak demand)

16

US Uncoated Free Sheet Consumption

11.5

12.0

12.5

13.0

13.5

14.0

14.5

15.0

15.519

93

1994

1995

1996

1997

1998

1999

2000

2001

E

2002

E

2003

E

Mil

lio

ns

of

Sh

ort

To

ns

Consumption

Source: American Forest and Paper Association, Pulp and Paper Forcaster, and Miller

Freeman.

17

US Uncoated Free Sheet Capacity

12.5

13.0

13.5

14.0

14.5

15.0

15.519

93

1994

1995

1996

1997

1998

1999

2000

2001

E

2002

E

2003

E

Mil

lio

ns

of

Sh

ort

To

ns

Capacity

Source: American Forest and Paper Association, Pulp and Paper Forcaster, and Miller

Freeman.

18

UCF Capacity vs. Consumption

11.5

12.0

12.5

13.0

13.5

14.0

14.5

15.0

15.519

93

1994

1995

1996

1997

1998

1999

2000

2001

E

2002

E

2003

E

Mil

lio

ns

of

Sh

ort

To

ns

Consumption

Capacity

Source: American Forest and Paper Association, Pulp and Paper Forcaster, and Miller

Freeman.

19

White Paper

• Near-term Weakness in Pulp • Global Excess Capacity• Asian Swing producers

Intermediate-term: Modestly Positive • Lower Capacity Growth• Higher Consumption Growth

Longer- term: Negative • Expected to Follow Pulp

Near-term: Neutral

20

Tissue

Near-term: • Retail - Stable

–Steady Demand –Possible Downshift in Quality

• Away From Home - Negative–Lower Demand–Greater Competition

21

Containerboard

Near-term: Negative• Slowing economy (domestic demand)• Reduced exports

Longer term: Positive

• Low capacity growth

• Consolidation/producer discipline

• Capacity shutdowns

• US producers have relatively good cost position

22

NA Newsprint Consumption

11.011.512.012.513.013.514.0

1993

1994

1995

1996

1997

1998

1999

2000

2001

E

2002

E

Mil

lio

ns

of

Met

ric

To

ns

Consumption

Source: American Forest and Paper Association, Pulp and Paper Forcaster, Miller Freeman

and Bank of America Industry Research Estimates

23

Newsprint & Groundwood

Near-term: Negative• Slowdown in economy• Buyer resistance• Technology risk

Longer term: Positive• Consolidation/ Supplier discipline • No new capacity• Capacity shutdowns/conversions

24

Coated

Near-term: Negative• Overcapacity (new in Europe, conversions in

U.S.)• Imports• Slow Economy (Weaker Demand)

Longer term: Positive• Consolidation (Potential Industry Shake-out) • Weakening US Dollar

25

Lumber

Near-term: Negative • Lower Housing Starts

• Increased Capacity (Especially in the US South)

• Elimination of Canadian Quota

26

Structural Panels

Near-term: Negative

• New OSB Capacity

• Lower Housing Starts

• Weak Industry Participants

27

Chemicals & Allied ProductsRating Trends and Outlook

John Rogers

Vice President / Senior Credit Officer

Investor Conference January 15, 2002

28

Agenda

Rating Trends

Ratings Outlook

Major Rating Issues

29

Baa2

Ba1

Baa3

Rating TrendsChemicals & Allied Products

30

Rating Outlook US Chemical Companies

• Weak Global Economic Outlook– Accelerating After 9/11– Declines in Europe and Asia

• Timing of Rebound Uncertain– Terrorism Creates Uncertainty– Disconnect Between Industry & Economy

• Further Reduction in Bank Exposure

Ratings Outlook: Negative

31

Rating Outlook (Continued) US Chemical Companies

• Negative Industry Factors– Debt Levels Elevated

• Acquisitions and Share Repurchases

– Event Risk and New Capacity– Impact of Cost Reductions

• Not Visible due to Weak Global Demand

• Unable to Rate Through Cycle– Liquidity Concerns Cause Downgrades

Ratings Outlook: Negative

32

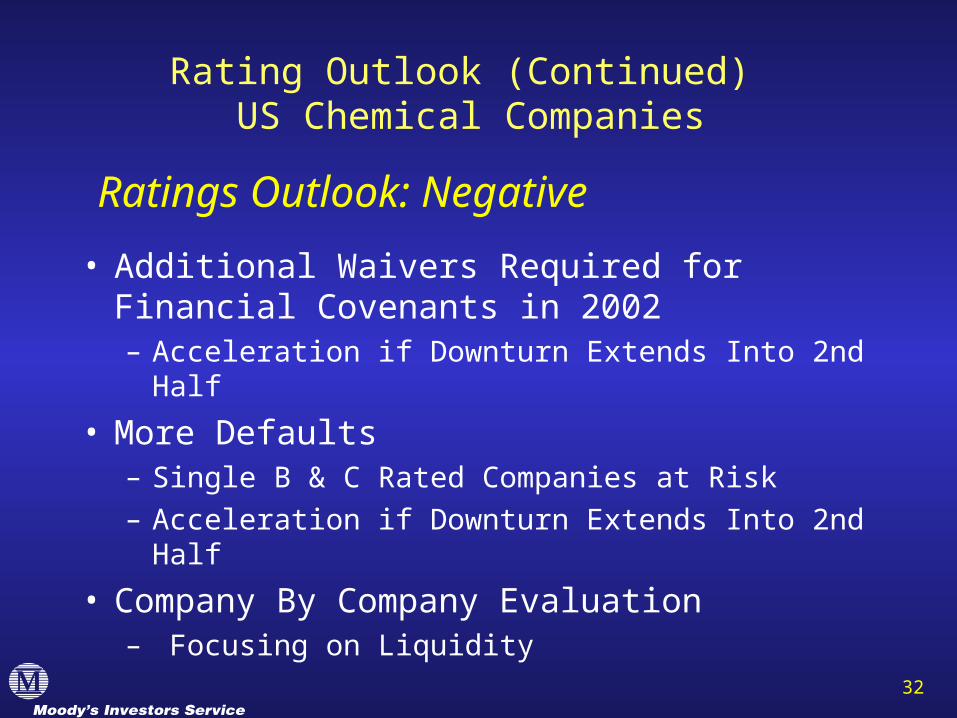

Rating Outlook (Continued) US Chemical Companies

• Additional Waivers Required for Financial Covenants in 2002– Acceleration if Downturn Extends Into 2nd Half

• More Defaults – Single B & C Rated Companies at Risk– Acceleration if Downturn Extends Into 2nd Half

• Company By Company Evaluation– Focusing on Liquidity

Ratings Outlook: Negative

33

Rating Outlook US Industrial Gas Companies

• Debt Levels Closer to Normal• Not as Impacted by Downturn

– Even AP With a Large Chemicals Business

• Debt Levels Likely to Remain Stable– Reduced Capex

• Liquidity is Not a Concern– High Level of Guaranteed Revenues

Ratings Outlook: Stable

34

Rating IssuesChemical and Allied Companies

• Liquidity

• Business Risk

• Management Policies

35

Rating IssuesChemical and Allied Companies

• Liquidity– Financial Covenants

• Weakness Increases Risk• Baa Moving to Smaller, Secured Facilities

– Must Provide Flexibility Throughout 2002– Moody’s Liquidity Assessment

• Greater Analysis on Liquidity for All Issuers

36

Rating IssuesChemical and Allied Companies

• Business Risk– Exposure to Economic Weakness– Commodities - New Capacity/Competition– Specialties - Commoditization/Competition

• Event Risk - All Companies– Acquisitions Greater Negative Impact

37

Major Rating IssuesChemical and Allied Companies

• Management Policies– Changes Due to Economic Weakness

• Growth/Acquisitions• Share Repurchases• Capex/Investments

– Proactive Management of Liquidity and Banking Relationships

– Commitment to Current Rating

38

• Other Operating Risks & Liabilities– Government Policies & Regulations

• MBr, MTBE, PVC/Phthalates, Hal FR• Fertilizers

– Litigation Risk• Product Liability Asbestos, Lead Paint, etc.

– Pension & OPEB Liabilities– Environmental Liabilities

Major Rating Issues (Continued) Chemical & Allied Companies

39

Ratings at Risk Chemical & Allied Companies

Companies Rating Outlook Comment

Great Lakes A2 Negative Flame Retardants

Eastman Baa2 Stable Spin-off/Acq. Synergies

Nova Chemicals Baa2 Negative PE & PS Margins

PolyOne Baa2 Stable Rationalization & Costs

Solutia Baa2 U Review Nylon & Asset Sales

Crompton Baa3 Stable Asset Sales

Ferro Baa3 Negative Acq. Syn. & Asset Sales

RPM Baa3 Stable Asset Sales

40

Ratings at Risk Chemical & Allied Companies

Companies Rating Outlook Comment

Equistar Ba1 Negative Liquidity, Margins

IMC Global Ba1 Negative DAP Recovery

KoSa B.V. Ba1 Stable Polyester Fiber Outlook

Borden Inc. Ba3 U. Review Margins, Use of Cash

Georgia Gulf Ba3 Stable Chlor Alkali / PVC Outlook

OM Group Inc. Ba3 Negative Equity Transaction Pending

Single B and C Rated Companies

Are at More Risk by Definition.

41

Global Chemicals Team

US David Neuhaus, VP & Sr. Analyst John Rogers, VP & Sr. Credit. Officer Diane Vargas, VP & Sr. Analyst

Europe Donald Burri, Sr. Vice President

Japan Noriko Kosaka, VP & Sr. Analyst

42

Metals & Mining

Carol Cowan

VP/Senior Analyst

43

Agenda

• Industry Fundamentals

• Key Rating Drivers

• Future Trends

44

Industry Fundamentals

• Industry Outlook Negative

• Volatile supply/demand environment

• Global commodity prices downward trend

• Depleting asset base

• Leveraged financial profile

• Need for reinvestment for growth

• Geopolitical risks

45

Industry Fundamentals

Source: London Metals Exchange

Metals Prices 1990-December 2001

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

DE

C.

1989

JUN

. 19

90

DE

C.

1990

JUN

. 19

91

DE

C.

1991

JUN

. 19

92

DE

C.

1992

JUN

. 19

93

DE

C.

1993

JUN

. 19

94

DE

C.

1994

JUN

. 19

95

DE

C.

1995

JUN

. 19

96

DE

C.

1996

JUN

. 19

97

DE

C.

1997

JUN

. 19

98

DE

C.

1998

JUN

. 19

99

DE

C.

1999

JUN

. 20

00

DE

C.

2000

JUN

. 20

01

DE

C.

2001

US

$/lb

(A

lum

inum

, Cop

per

and

Zinc

)

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

$4.50

$5.00

$5.50

$6.00

US

$/lb

(N

icke

l)

ALUMINUM ($ / lb.) COPPER ($ / lb.) ZINC ($ / lb.) NICKEL ($ / lb.)

46

Key Rating Drivers

• Cost Management

• Business Growth Strategy and ability to execute

• Cash Flow and Capital Structure

47

Cost Management

• Declining ore grades

• Higher energy cost platform

• Higher labor costs

• Currency exposures - US dollar revenues on local currency cost basis

• Environmental and reclamation costs

• Ability to manage cost base throughout the cycle more challenging

48

Business Growth Strategy

• Reserve exploration and new mine development

• Proven/probable reserve position

• Growth opportunities - acquisition or resource development

• Position on risk sharing - structuring of joint venture, partnership arrangements

• Overall risk tolerance

• Desired financial flexibility to maintain long term strategic growth objectives

49

Capital Structure

• Balance between short and long term debt

• Diversity of funding sources

• Access to debt and equity markets

• Off balance sheet exposures

• Leverage targets, coverage ratios over reasonable time frame

• Financial capacity to take advantage of opportunities and weather economic weakness

50

Future Trends

• New resource development to continue costly

• Production cost positions to be pressured

• Access to equity markets for middle and lower tier companies to continue challenging

• China likely to become a major factor from both a consumption and production perspective

• Consolidation to continue

• Ratings will reflect the widening gap between the haves and the have nots

51

Domestic Steel Industry

Grace Kennedy, CFA/AVP

52

Negative Outlook

• Economic environment remains weak

• Industry Specific Issues:

– Overcapacity

– Legacy Costs related to Pension and Health Care Obligations

• Legislative Relief through import restrictions may ameliorate conditions temporarily

53

Economic Environment

• Declining industrial production

• Capital expenditure budgets curtailed

• Interest rate cuts unlikely to support sustained consumer durable spending

• Rising unemployment

54

Industrial Production Jan 1998 through Nov 2001

2400

2500

2600

2700

2800

2900

3000

Souce: Federal Reserve Statistical Release

Gro

ss V

alu

e o

f P

rod

uct

- s

easo

nal

ly a

dju

sted

55

-30

-20

-10

0

10

20

30

40

1980

1981

1982

1983

1985

1986

1987

1988

1990

1991

1992

1993

1995

1996

1997

1998

2000

2001

% C

han

ge f

rom

Pre

ceed

ing

Per

iod

Source: Bureau of Economic Analysis, December 21, 2001

Capital Investmentssequential quarterly change (in %)

2Q01 -14.6%

3Q01 -8.5%

2Q01 -14.6%

3Q01 -8.5%

56

Rising Unemployment

3

4

5

6

7

8

Souce: Department of Labor

Domestic Unemployment thru Dec. 2001

% o

f re

al o

utpu

t, b

ase

year

199

2in

per

cent 5.8% Dec ‘01

57

Steel Industry-Specific Issues

• Overcapacity– Global excess capacity causing pricing pressure and

under-absorption of operating costs

• High Operating Costs– Many US facilities are older and less efficient

– Retiree healthcare benefits require current cash contributions.

– Pensions may require additional funding due to lower pension plan market values

58

Steel Industry Overcapacity

59

Steel IndustryLegislative Relief

• Section 201 Investigation by U.S. ITC found “serious injury” to domestic industry from imports. In February 2002 the president will determine tariffs that may be effective for four years.

• Retiree healthcare “cost-sharing” bills introduced in the Senate (unlikely to become law)

60

What Would Alter the Outlook?

• Economic conditions supporting increased industrial production

• Rationalization of high-cost plants to align supply with demand.– Consolidation talks among U.S. producers

contingent upon legacy employee cost relief

• Relief from legacy employee cost burden