1 PPACA and What It Means for You! Tennessee Grocers & Convenience Store Association Convention...

31

1 PPACA and What It Means for You! Tennessee Grocers & Convenience Store Association Convention Presented: June 14, 2013 Tiffany Downs FordHarrison LLP

-

Upload

griselda-miller -

Category

Documents

-

view

214 -

download

0

Transcript of 1 PPACA and What It Means for You! Tennessee Grocers & Convenience Store Association Convention...

1

PPACA and What It Means for You!

Tennessee Grocers & Convenience Store Association Convention

Presented: June 14, 2013

Tiffany Downs

FordHarrison LLP

2

Patient Protection and Affordable Care Act (PPACA)

• Phased effective dates – 3/23/2010 (immediately upon enactment)– First plan years on or after 9/23/2010– 1/1/2011– 1/1/2013– 3/1/2013– For plan years on or after 1/1/2014– 2018– Upon issuance of regulations

3

Broad Application• Health Care Reform Applies to Group Health Plans

- Fully insured and self funded - Exception to some (but not all) requirements based on size- Sponsored by private or public entities

• Does Not Apply to:- Plans providing HIPAA excepted benefits (health FSAs*,

limited scope dental and vision benefits if provided in separate policy)

- Stand alone retiree plans- Plans that are not group health plans (life, disability, etc.)

*Health care reform does restrict reimbursement of over-the-counter drugs beginning as of 1/1/2011 and limits employee contributions to $2,500 beginning as of 1/1/2013 but coverage mandates do not apply to health FSAs that provide HIPAA excepted benefits.

4

Three Overlapping Requirements• Individual Mandate requires that individuals have “minimal

essential coverage” or pay a penalty

• Large employers (at least 50 full-time employees or equivalents in the control group) must offer “minimum value and affordable coverage” to full-time employees or pay a penalty.

• States (or Federal) are required to establish a health insurance exchange to facilitate purchase of insurance by individuals (and small employers) who do not have access or for which it is unaffordable.

5

2014 Requirements• Individual Mandate

o Individual’s obligation to have “minimum essential coverage” (for self and dependents) or pay a penalty

• Large Employer Mandate (Play or Pay)o Auto-enroll employees if over 200 employees (likely not until

2015)o Offer minimum essential coverage to employee (and children

up to age 26) that provides minimum value and is affordable or pay a penalty

o Penalty is not deductible

6

Exchanges in 2014• Exchanges will allow individuals and

small employers (SHOP) to choose from a menu of insurance products

• Exchanges will verify eligibility, including premium assistance tax credits and cost sharing, and facilitate enrollment

• Exchanges will connect individuals with Medicaid and CHIP, if eligible

• Exchanges will use HHS-managed data services hub to connect to federal data sources (IRS, Social Security, Homeland Security) to determine eligibility

Levels of Coverage under Exchanges

Bronze: 60% Silver: 70%

Gold: 80% Platinum : 90%

7

Individual versus SHOP Exchanges

• Individual– Open to citizens or legal immigrants– Federal subsidies are available based on income– People who are eligible for affordable coverage do not qualify

for subsidies• SHOP

– Small employers buy coverage for their employees– No federal subsidies are available to help employees buy

coverage

8

Eligibility for Tax Subsidies• If an individual does:

o not receive “affordable” employer sponsored coverage (employee contribution exceeds 9.5% of household income); and

o earns between 100% and 400% of the federal poverty level ($44,680 for an individual at 400%), then

o the individual will get a tax subsidy to pay for part or all of the coverage through the individual exchange.

9

Small Employer Tax Credit

• Qualified employer- Less than 25 FTE employees- Average annual wages under $50K- Share at least 50% of premium for a “qualifying arrangement”

• Phased Tax credit- 2010-2013 – max credit up to 35% (25% for tax-exempts) of

employer share of premium- 2014 – 2016 – max credit up to 50% (35% for tax-exempts) of

employer share of premium- 50% credit is available for SHOP coverage

• Check the IRS website at: www.irs.gov/newsroom/article/O,,id=220839,00.html

1010

Large Employer’s Obligation• Employers with 50 or more full-time equivalents for prior calendar year must

offer certain health care coverage or pay a penaltyo All common law employees (full-time and part-time) in the control group

are counted to determine if reach 50 thresholdo Must aggregate hours of part-time employees to create total number

of full-time employeeso Exclude the following from the count:

• leased employees (Caution)• partners • sole proprietors• more than 2% shareholders in subchapter S corporation • independent contractors (Caution)

1111

Large Employer’s Obligation

• If reach 50 threshold, there are two potential penalties:

– No Coverage Penalty - coverage only required to be offered for full-time employees (average 30 hours a week or 130 hours a month). This is the “Pay” Penalty of $2,000.

– Unaffordable Coverage Penalty – Employer must pay for 60% of benefit costs (provide minimum value), and coverage must be affordable – not exceed 9.5% of household income. This is the “Play” penalty.

1212

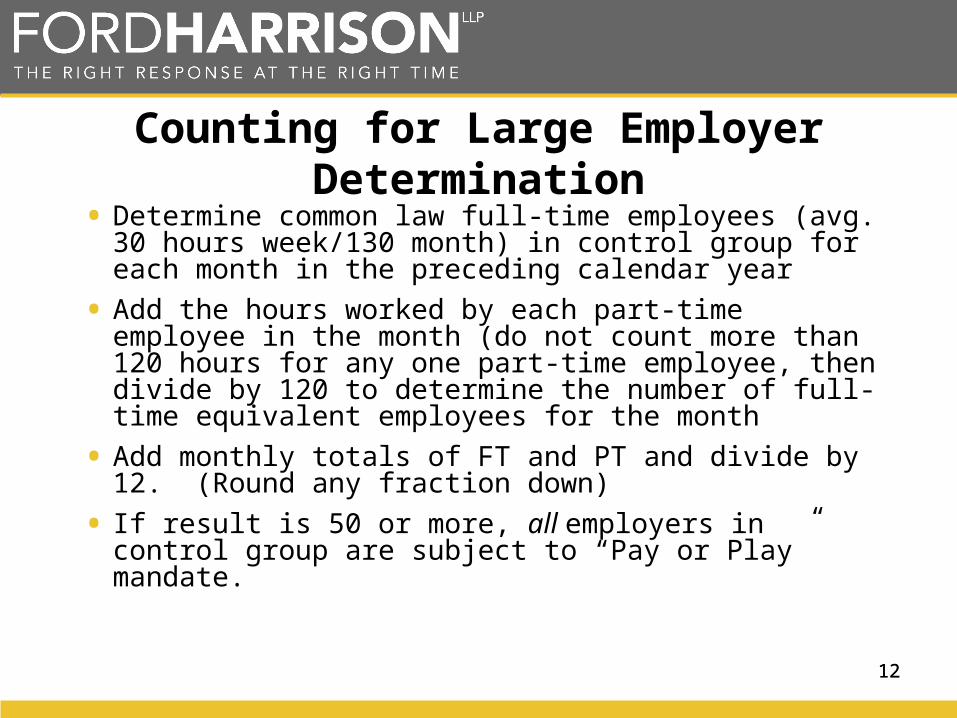

Counting for Large Employer Determination

• Determine common law full-time employees (avg. 30 hours week/130 month) in control group for each month in the preceding calendar year

• Add the hours worked by each part-time employee in the month (do not count more than 120 hours for any one part-time employee, then divide by 120 to determine the number of full-time equivalent employees for the month

• Add monthly totals of FT and PT and divide by 12. (Round any fraction down)

• If result is 50 or more, all employers in control group are subject to “Pay or Play” mandate.

1313

If Large Employer Mandate Applies

• No Coverage Penalty – Must offer “minimum essential coverage” to at least 95% of full-time employees and their dependents (children up to age 26).

• Do not have to offer or provide coverage to spouses.

• Do not have to offer or provide coverage for part-time employees.

1414

No Coverage Penalty

• Penalty applies if no coverage is offered, ando at least 1 full-time employee enrolls in an Exchange plan, ando That employee is eligible for tax subsidy

• Monthly penalty = $166.67 x number of full-time employees (excluding first 30 employees) ($2,000 annually per employee)

1515

Control Group Rules & The No Coverage Penalty

• Penalties do not apply to entities within control group• Penalties apply on individual employer basis (separate EIN)• 30 employee deduction for No Coverage Penalty is allocated per

rata among the control group based on how many employees in each entity

1616

No Coverage Penalty Example

• Employer with 1,030 full-time employees in 2 divisions (single EIN), 800 FT in one division which offers coverage and 230 FT in another division that does not offer coverage.

• Penalty would be $2,000 x (1,030-30)) equals $2 million.

• But - If 230 employees with no coverage are in a separate entity, the penalty would be based on 223 employees (230 – 7 (22.3% of 30).

• Penalty would be 223 FT x $2,000 equals $446,000.

1717

Unaffordable Coverage Penalty

• Employers with 50 or more full-time employees who only provide “unaffordable” coverage or not “minimal value coverage” to full-time employees are assessed a penalty

• Penalty applies if coverage iso Unaffordable: Employee premium above 9.5% of household

income, and o Does not Provide Minimum Value: employer pays less than 60%,

ando At least one full-time employee declines employer coverage,

enrolls in Exchange plan, and is eligible for a tax subsidy

1818

Unaffordable Coverage Penalty

• Penalty: $250 monthly ($3,000 annually) x number of full-time affected employees.

• Affected Employees are those who did not receive affordable coverage that provides minimum value and who enrolled in coverage at a health insurance exchange and qualified for a subsidy.

1919

Unaffordable Penalty Example

Employer offers coverage to all 130 full-time employees.

• Coverage is unaffordable for 40 full-time employees

• These 40 full-time employees get tax credits to buy coverage in the exchange.

• Employer must pay $120,000 (lesser of the two penalty calculations):o $3,000 x 40 FT employees receiving tax credit =

$120,000; ORo $2,000 x (130-30): 100 FT employees = $200,000.

Source: Kaiser Family Foundation

21

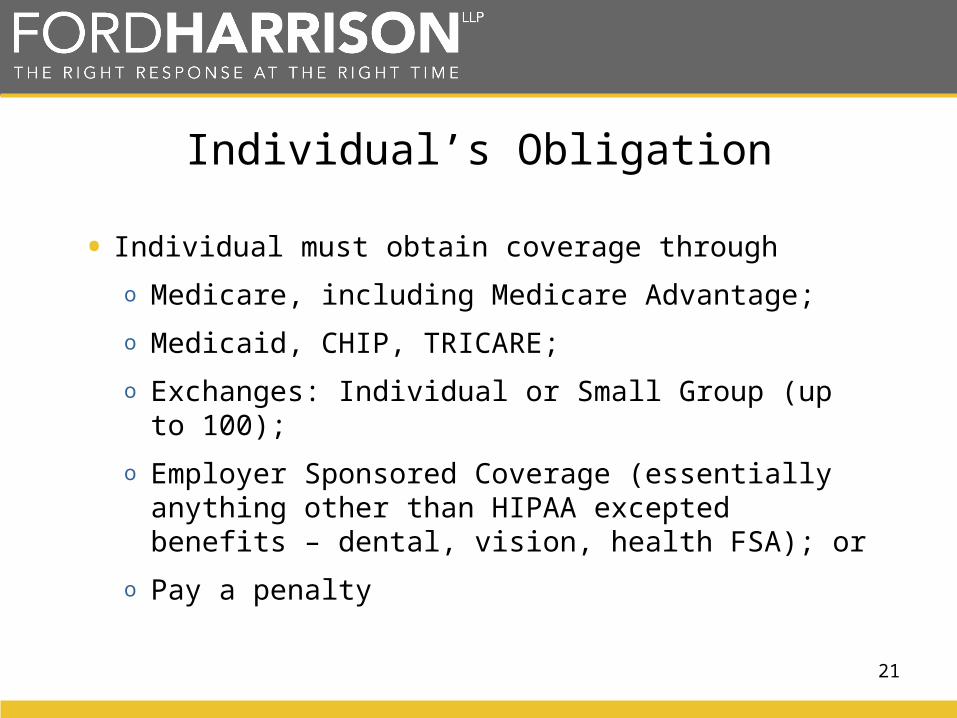

Individual’s Obligation

• Individual must obtain coverage througho Medicare, including Medicare Advantage;o Medicaid, CHIP, TRICARE;o Exchanges: Individual or Small Group (up to 100);o Employer Sponsored Coverage (essentially anything other

than HIPAA excepted benefits – dental, vision, health FSA); or

o Pay a penalty

22

Individual Play or Pay Mandates• Applicable individuals must ensure minimum essential coverage for self

and any dependents each month beginning 1/1/2014• Failure to maintain coverage results in monthly penalty calculated as

1/12th of the greater of:

Tax Year

% of income Dollar Amount Single

Dollar Amount Family

2014 1% $95 $2852015 2% $325 $9752016 2.5% $695 $2,085

23

Individual Play or Pay Mandate• Exceptions to the requirement include the following:

o persons who are not a US Citizen or legal residento those for whom coverage is unaffordable (contributions exceed 8%

household income)o those below 100% of federal poverty levelo incarcerated individualso those with a hardship waivero persons who claim a religious exemptiono individuals without coverage for less than 3 months during the year incur no

penalty

Source: Kaiser Family Foundation

25

Large Employer Considerations

• Categorize employees as Regular full-time OR seasonal/variable hour

• Seasonal employee performs labor on a seasonal basis, as determined by employer in good faith (e.g. retail employees during holiday season)

2626

Full- or Part-time status is unknown

Employee is hired

Is employee expected to be full-time?

Use Measurement Period – Measure actual hours worked for set period (3-12 months)

Offer coverage to employee within 90

days of hire

Employee considered eligible for full-time coverage

Assumes that the employee is “otherwise eligible” at hire date.

Yes

Employee averages

30+ hrs/week

Must Use Stability Period - Effective date of coverage (6-12 months – same as measurement period)

Yes

2727

Standard Measuring PeriodStandard Measuring Period Standard Stability PeriodStandard Stability Period

Standard Measuring PeriodStandard Measuring Period Standard Stability PeriodStandard Stability Period

Initial Measuring PeriodInitial Measuring Period Initial Stability PeriodInitial Stability Period

June 15, 2013

July 1, 2013

June 30,

2014

Nov. 1, 2013

Oct 31,

2014

Aug. 1, 2014

Oct. 31, 2014

Dec. 31, 2014

Jan. 1, 2015

Dec. 31, 2015

Nov. 1, 2014

Oct. 31, 2015

Jan. 1, 2016

Dec. 31, 2016

Jul. 31, 2015

Initial Administrative Periods: 1)Start date until first of month following2)One month after Initial Measurement Period

Initial Measurement Period:12 months beginning first of month following date of hire

Initial Stability Period:12 months but ends on October 31 since Standard Measurement Period begins on November 1

Standard Measurement Period:12 months; Nov. 1–Oct. 31 each year for all employees

Standard Administrative Period:Two months after Standard Measurement Period

Standard Stability Period:12 months; Jan. 1–Dec. 31 each year for all employees

28

Compliance Challenges

• Requirements for Small Employers• Requirements for Large Employers• How to structure workforce• Who to offer health care coverage• Use of measurement period and stability

periods• Minimize penalty and cost of providing health

care

29

Employer Specific Considerations

• Wage demographics

• Hour demographics

• Use of contingent workforce

• Worker turnover

• Local labor markets

• Unions

• Government contractor

• Expected utilization of health coverage

3030

Play or Pay Strategies• Maintain status quo as to eligibility and plan design• Reduce workforce of FT employees• Utilize contingent workforce (but, caution).• Change plan designs

o Offer current coverage (probably minimum essential coverage) o Offer minimum essential plan only (i.e., you accept the risk of

the unaffordable penalty).o Offer both minimum essential coverage and minimum value

plan (i.e., avoid the penalties).• Assess risks with each option and administrative requirements for

reporting information to exchanges and IRS