1 Installment Sales

26

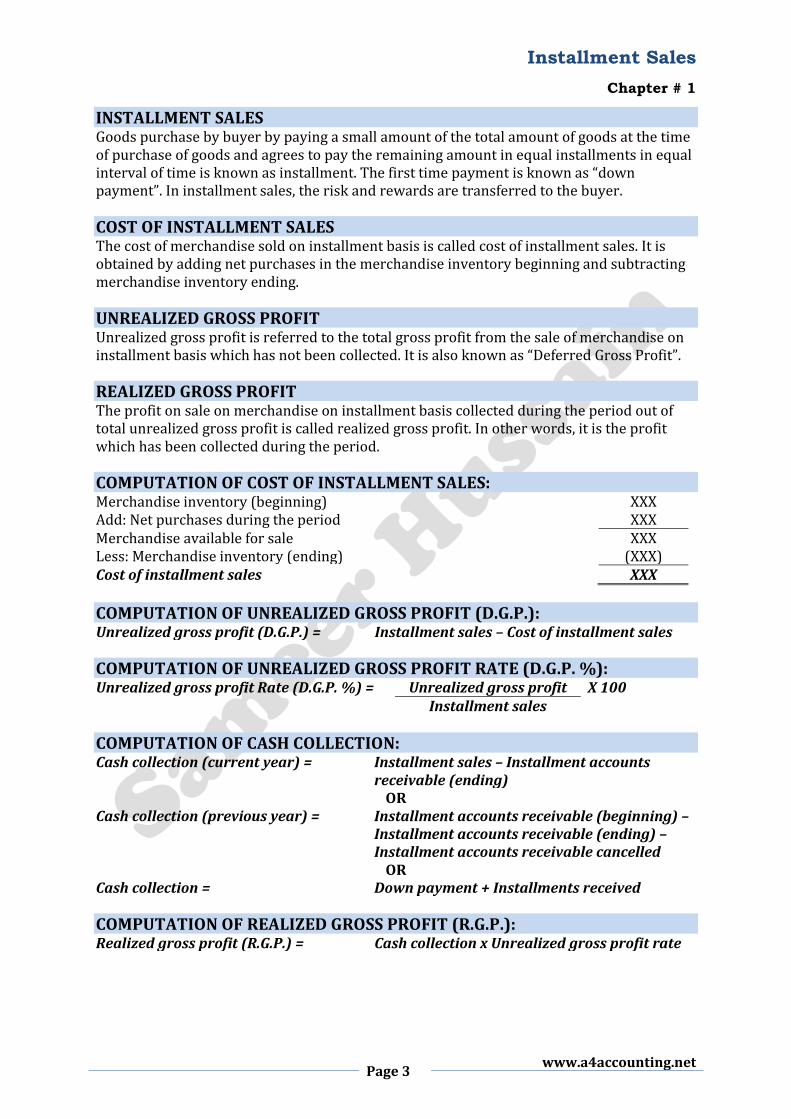

Installment Sales Chapter # 1 Page 3 www.a4accounting.net INSTALLMENT SALES Goods purchase by buyer by paying a small amount of the total amount of goods at the time of purchase of goods and agrees to pay the remaining amount in equal installments in equal interval of time is known as installment. The first time payment is known as “down payment”. In installment sales, the risk and rewards are transferred to the buyer. COST OF INSTALLMENT SALES The cost of merchandise sold on installment basis is called cost of installment sales. It is obtained by adding net purchases in the merchandise inventory beginning and subtracting merchandise inventory ending. UNREALIZED GROSS PROFIT Unrealized gross profit is referred to the total gross profit from the sale of merchandise on installment basis which has not been collected. It is also known as “Deferred Gross Profit”. REALIZED GROSS PROFIT The profit on sale on merchandise on installment basis collected during the period out of total unrealized gross profit is called realized gross profit. In other words, it is the profit which has been collected during the period. COMPUTATION OF COST OF INSTALLMENT SALES: Merchandise inventory (beginning) XXX Add: Net purchases during the period XXX Merchandise available for sale XXX Less: Merchandise inventory (ending) (XXX) Cost of installment sales XXX COMPUTATION OF UNREALIZED GROSS PROFIT (D.G.P.): Unrealized gross profit (D.G.P.) = Installment sales – Cost of installment sales COMPUTATION OF UNREALIZED GROSS PROFIT RATE (D.G.P. %): Unrealized gross profit Rate (D.G.P. %) = Unrealized gross profit X 100 Installment sales COMPUTATION OF CASH COLLECTION: Cash collection (current year) = Installment sales – Installment accounts receivable (ending) OR Cash collection (previous year) = Installment accounts receivable (beginning) – Installment accounts receivable (ending) – Installment accounts receivable cancelled OR Cash collection = Down payment + Installments received COMPUTATION OF REALIZED GROSS PROFIT (R.G.P.): Realized gross profit (R.G.P.) = Cash collection x Unrealized gross profit rate

-

Upload

sameer-hussain -

Category

Documents

-

view

213 -

download

2

description

installment sales

Transcript of 1 Installment Sales

Installment Sales

Chapter # 1

Page 3

www.a4accounting.net

INSTALLMENT SALES Goods purchase by buyer by paying a small amount of the total amount of goods at the time of purchase of goods and agrees to pay the remaining amount in equal installments in equal interval of time is known as installment. The first time payment is known as “down payment”. In installment sales, the risk and rewards are transferred to the buyer.

COST OF INSTALLMENT SALES The cost of merchandise sold on installment basis is called cost of installment sales. It is obtained by adding net purchases in the merchandise inventory beginning and subtracting merchandise inventory ending.

UNREALIZED GROSS PROFIT Unrealized gross profit is referred to the total gross profit from the sale of merchandise on installment basis which has not been collected. It is also known as “Deferred Gross Profit”.

REALIZED GROSS PROFIT The profit on sale on merchandise on installment basis collected during the period out of total unrealized gross profit is called realized gross profit. In other words, it is the profit which has been collected during the period.

COMPUTATION OF COST OF INSTALLMENT SALES: Merchandise inventory (beginning) XXX Add: Net purchases during the period XXX Merchandise available for sale XXX Less: Merchandise inventory (ending) (XXX) Cost of installment sales XXX

COMPUTATION OF UNREALIZED GROSS PROFIT (D.G.P.): Unrealized gross profit (D.G.P.) = Installment sales – Cost of installment sales

COMPUTATION OF UNREALIZED GROSS PROFIT RATE (D.G.P. %): Unrealized gross profit Rate (D.G.P. %) = Unrealized gross profit X 100

Installment sales

COMPUTATION OF CASH COLLECTION: Cash collection (current year) = Installment sales – Installment accounts

receivable (ending) OR

Cash collection (previous year) = Installment accounts receivable (beginning) – Installment accounts receivable (ending) – Installment accounts receivable cancelled

OR Cash collection = Down payment + Installments received

COMPUTATION OF REALIZED GROSS PROFIT (R.G.P.): Realized gross profit (R.G.P.) = Cash collection x Unrealized gross profit rate

Installment Sales

Chapter # 1

www.a4accounting.net Page 4

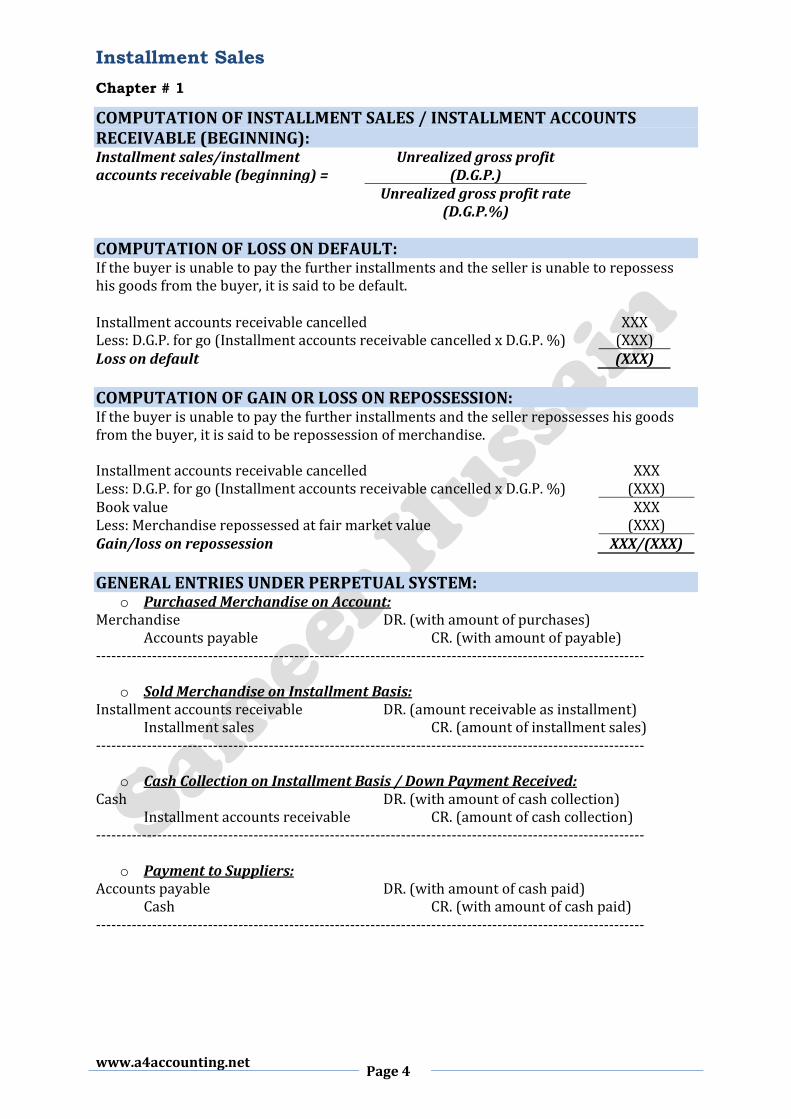

COMPUTATION OF INSTALLMENT SALES / INSTALLMENT ACCOUNTS RECEIVABLE (BEGINNING): Installment sales/installment accounts receivable (beginning) =

Unrealized gross profit (D.G.P.)

Unrealized gross profit rate (D.G.P.%)

COMPUTATION OF LOSS ON DEFAULT: If the buyer is unable to pay the further installments and the seller is unable to repossess his goods from the buyer, it is said to be default. Installment accounts receivable cancelled XXX Less: D.G.P. for go (Installment accounts receivable cancelled x D.G.P. %) (XXX) Loss on default (XXX)

COMPUTATION OF GAIN OR LOSS ON REPOSSESSION: If the buyer is unable to pay the further installments and the seller repossesses his goods from the buyer, it is said to be repossession of merchandise. Installment accounts receivable cancelled XXX Less: D.G.P. for go (Installment accounts receivable cancelled x D.G.P. %) (XXX) Book value XXX Less: Merchandise repossessed at fair market value (XXX) Gain/loss on repossession XXX/(XXX)

GENERAL ENTRIES UNDER PERPETUAL SYSTEM: o Purchased Merchandise on Account:

Merchandise DR. (with amount of purchases) Accounts payable CR. (with amount of payable) ------------------------------------------------------------------------------------------------------------

o Sold Merchandise on Installment Basis: Installment accounts receivable DR. (amount receivable as installment) Installment sales CR. (amount of installment sales) ------------------------------------------------------------------------------------------------------------

o Cash Collection on Installment Basis / Down Payment Received: Cash DR. (with amount of cash collection) Installment accounts receivable CR. (amount of cash collection) ------------------------------------------------------------------------------------------------------------

o Payment to Suppliers: Accounts payable DR. (with amount of cash paid) Cash CR. (with amount of cash paid) ------------------------------------------------------------------------------------------------------------

Installment Sales

Chapter # 1

Page 5

www.a4accounting.net

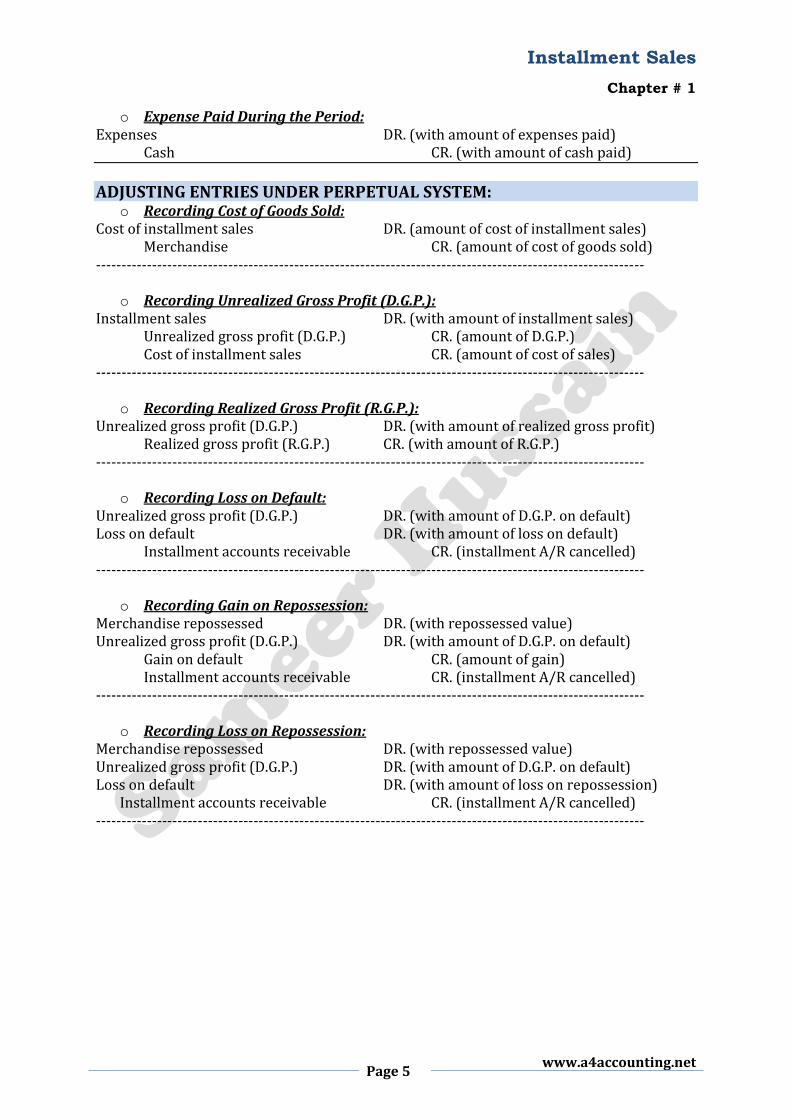

o Expense Paid During the Period: Expenses DR. (with amount of expenses paid) Cash CR. (with amount of cash paid)

ADJUSTING ENTRIES UNDER PERPETUAL SYSTEM: o Recording Cost of Goods Sold:

Cost of installment sales DR. (amount of cost of installment sales) Merchandise CR. (amount of cost of goods sold) ------------------------------------------------------------------------------------------------------------

o Recording Unrealized Gross Profit (D.G.P.): Installment sales DR. (with amount of installment sales) Unrealized gross profit (D.G.P.) CR. (amount of D.G.P.) Cost of installment sales CR. (amount of cost of sales) ------------------------------------------------------------------------------------------------------------

o Recording Realized Gross Profit (R.G.P.): Unrealized gross profit (D.G.P.) DR. (with amount of realized gross profit) Realized gross profit (R.G.P.) CR. (with amount of R.G.P.) ------------------------------------------------------------------------------------------------------------

o Recording Loss on Default: Unrealized gross profit (D.G.P.) DR. (with amount of D.G.P. on default) Loss on default DR. (with amount of loss on default)

Installment accounts receivable CR. (installment A/R cancelled) ------------------------------------------------------------------------------------------------------------

o Recording Gain on Repossession: Merchandise repossessed DR. (with repossessed value) Unrealized gross profit (D.G.P.) DR. (with amount of D.G.P. on default)

Gain on default CR. (amount of gain) Installment accounts receivable CR. (installment A/R cancelled)

------------------------------------------------------------------------------------------------------------

o Recording Loss on Repossession: Merchandise repossessed DR. (with repossessed value) Unrealized gross profit (D.G.P.) DR. (with amount of D.G.P. on default) Loss on default DR. (with amount of loss on repossession)

Installment accounts receivable CR. (installment A/R cancelled) ------------------------------------------------------------------------------------------------------------

Installment Sales

Chapter # 1

www.a4accounting.net Page 6

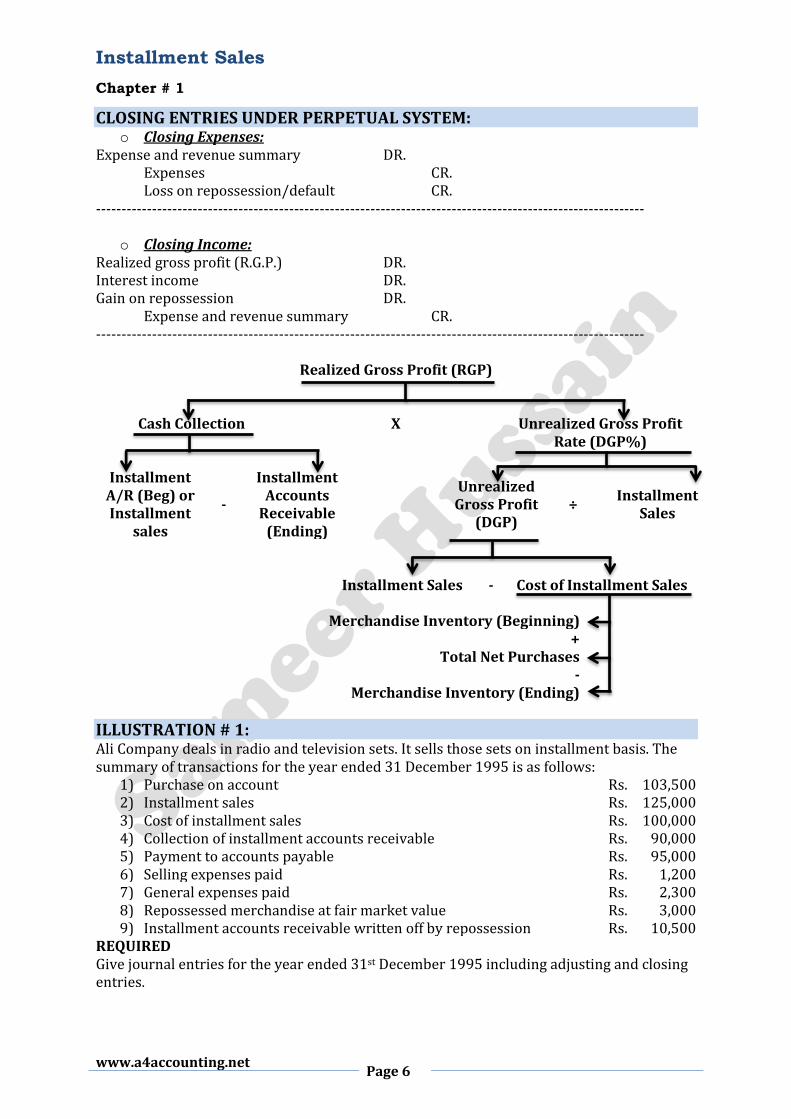

CLOSING ENTRIES UNDER PERPETUAL SYSTEM: o Closing Expenses:

Expense and revenue summary DR. Expenses CR. Loss on repossession/default CR. ------------------------------------------------------------------------------------------------------------

o Closing Income: Realized gross profit (R.G.P.) DR. Interest income DR. Gain on repossession DR. Expense and revenue summary CR. ------------------------------------------------------------------------------------------------------------

Realized Gross Profit (RGP)

Cash Collection X Unrealized Gross Profit Rate (DGP%)

Installment

A/R (Beg) or Installment

sales

-

Installment Accounts

Receivable (Ending)

Unrealized Gross Profit

(DGP) ÷

Installment Sales

Installment Sales -

Cost of Installment Sales

Merchandise Inventory (Beginning)

+ Total Net Purchases

- Merchandise Inventory (Ending)

ILLUSTRATION # 1: Ali Company deals in radio and television sets. It sells those sets on installment basis. The summary of transactions for the year ended 31 December 1995 is as follows:

1) Purchase on account Rs. 103,500 2) Installment sales Rs. 125,000 3) Cost of installment sales Rs. 100,000 4) Collection of installment accounts receivable Rs. 90,000 5) Payment to accounts payable Rs. 95,000 6) Selling expenses paid Rs. 1,200 7) General expenses paid Rs. 2,300 8) Repossessed merchandise at fair market value Rs. 3,000 9) Installment accounts receivable written off by repossession Rs. 10,500

REQUIRED Give journal entries for the year ended 31st December 1995 including adjusting and closing entries.

Installment Sales

Chapter # 1

Page 7

www.a4accounting.net

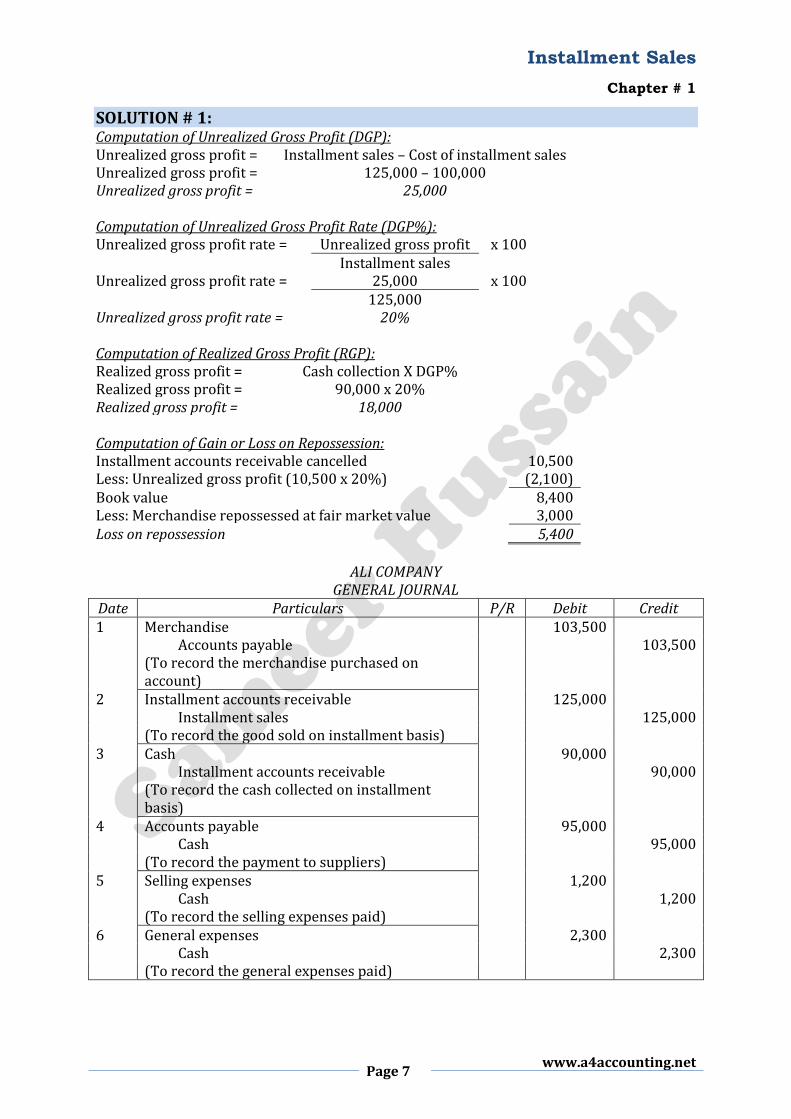

SOLUTION # 1: Computation of Unrealized Gross Profit (DGP): Unrealized gross profit = Installment sales – Cost of installment sales Unrealized gross profit = 125,000 – 100,000 Unrealized gross profit = 25,000 Computation of Unrealized Gross Profit Rate (DGP%): Unrealized gross profit rate = Unrealized gross profit x 100 Installment sales Unrealized gross profit rate = 25,000 x 100 125,000 Unrealized gross profit rate = 20% Computation of Realized Gross Profit (RGP): Realized gross profit = Cash collection X DGP% Realized gross profit = 90,000 x 20% Realized gross profit = 18,000 Computation of Gain or Loss on Repossession: Installment accounts receivable cancelled 10,500 Less: Unrealized gross profit (10,500 x 20%) (2,100) Book value 8,400 Less: Merchandise repossessed at fair market value 3,000 Loss on repossession 5,400

ALI COMPANY GENERAL JOURNAL

Date Particulars P/R Debit Credit 1 Merchandise 103,500 Accounts payable 103,500 (To record the merchandise purchased on

account)

2 Installment accounts receivable 125,000 Installment sales 125,000 (To record the good sold on installment basis) 3 Cash 90,000 Installment accounts receivable 90,000 (To record the cash collected on installment

basis)

4 Accounts payable 95,000 Cash 95,000 (To record the payment to suppliers) 5 Selling expenses 1,200 Cash 1,200 (To record the selling expenses paid) 6 General expenses 2,300 Cash 2,300 (To record the general expenses paid)

Installment Sales

Chapter # 1

www.a4accounting.net Page 8

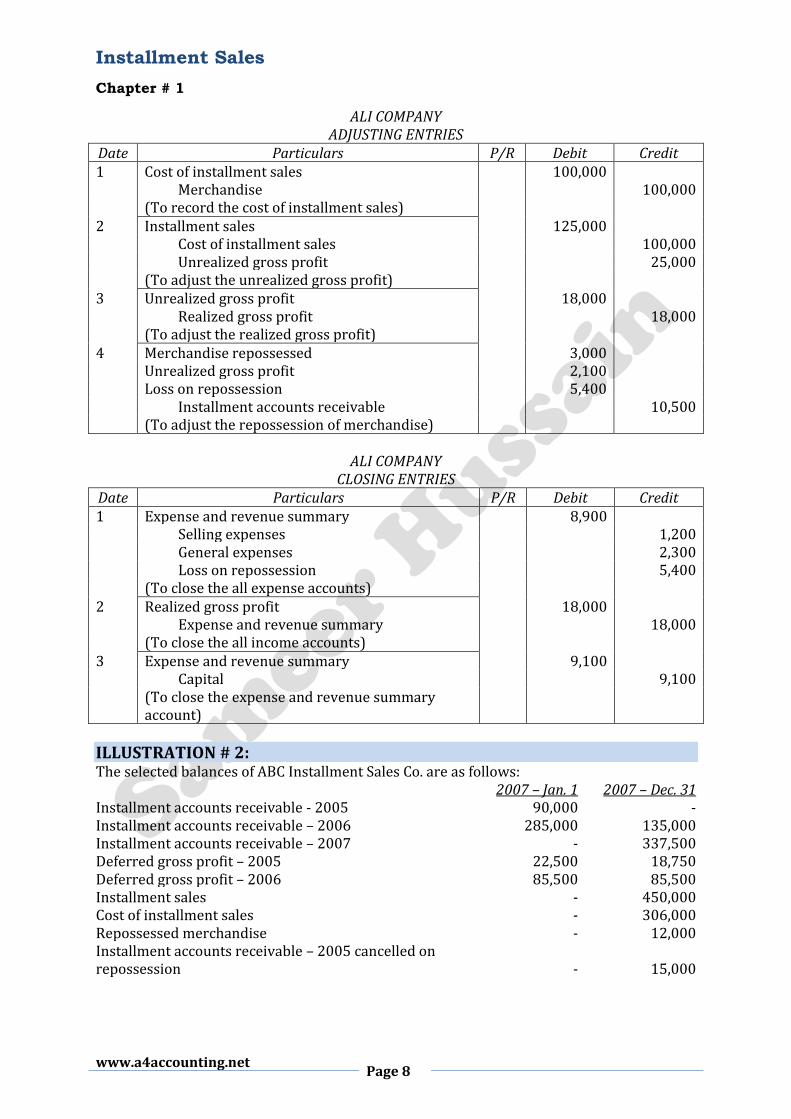

ALI COMPANY ADJUSTING ENTRIES

Date Particulars P/R Debit Credit 1 Cost of installment sales 100,000 Merchandise 100,000 (To record the cost of installment sales) 2 Installment sales 125,000 Cost of installment sales 100,000 Unrealized gross profit 25,000 (To adjust the unrealized gross profit) 3 Unrealized gross profit 18,000 Realized gross profit 18,000 (To adjust the realized gross profit) 4 Merchandise repossessed 3,000 Unrealized gross profit 2,100 Loss on repossession 5,400 Installment accounts receivable 10,500 (To adjust the repossession of merchandise)

ALI COMPANY CLOSING ENTRIES

Date Particulars P/R Debit Credit 1 Expense and revenue summary 8,900 Selling expenses 1,200 General expenses 2,300 Loss on repossession 5,400 (To close the all expense accounts) 2 Realized gross profit 18,000 Expense and revenue summary 18,000 (To close the all income accounts) 3 Expense and revenue summary 9,100 Capital 9,100 (To close the expense and revenue summary

account)

ILLUSTRATION # 2: The selected balances of ABC Installment Sales Co. are as follows: 2007 – Jan. 1 2007 – Dec. 31 Installment accounts receivable - 2005 90,000 - Installment accounts receivable – 2006 285,000 135,000 Installment accounts receivable – 2007 - 337,500 Deferred gross profit – 2005 22,500 18,750 Deferred gross profit – 2006 85,500 85,500 Installment sales - 450,000 Cost of installment sales - 306,000 Repossessed merchandise - 12,000 Installment accounts receivable – 2005 cancelled on repossession - 15,000

Installment Sales

Chapter # 1

Page 9

www.a4accounting.net

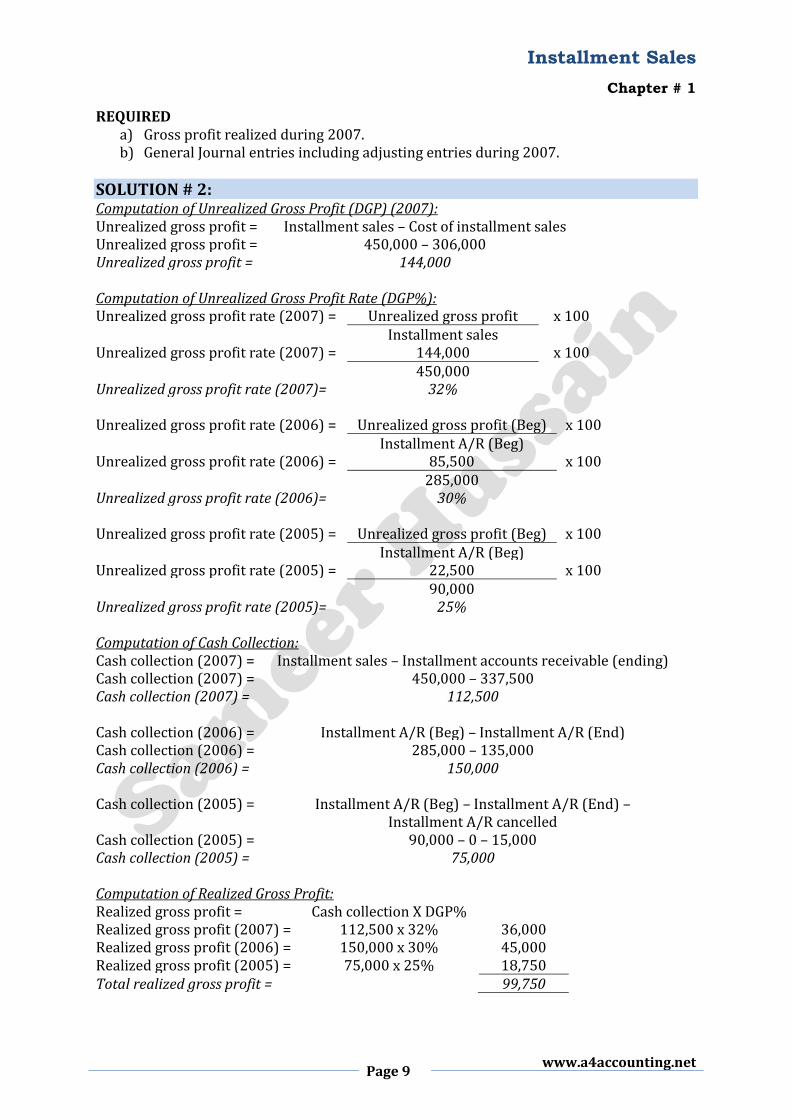

REQUIRED a) Gross profit realized during 2007. b) General Journal entries including adjusting entries during 2007.

SOLUTION # 2: Computation of Unrealized Gross Profit (DGP) (2007): Unrealized gross profit = Installment sales – Cost of installment sales Unrealized gross profit = 450,000 – 306,000 Unrealized gross profit = 144,000 Computation of Unrealized Gross Profit Rate (DGP%): Unrealized gross profit rate (2007) = Unrealized gross profit x 100 Installment sales Unrealized gross profit rate (2007) = 144,000 x 100 450,000 Unrealized gross profit rate (2007)= 32%

Unrealized gross profit rate (2006) = Unrealized gross profit (Beg) x 100 Installment A/R (Beg) Unrealized gross profit rate (2006) = 85,500 x 100 285,000 Unrealized gross profit rate (2006)= 30%

Unrealized gross profit rate (2005) = Unrealized gross profit (Beg) x 100 Installment A/R (Beg) Unrealized gross profit rate (2005) = 22,500 x 100 90,000 Unrealized gross profit rate (2005)= 25%

Computation of Cash Collection: Cash collection (2007) = Installment sales – Installment accounts receivable (ending) Cash collection (2007) = 450,000 – 337,500 Cash collection (2007) = 112,500 Cash collection (2006) = Installment A/R (Beg) – Installment A/R (End) Cash collection (2006) = 285,000 – 135,000 Cash collection (2006) = 150,000

Cash collection (2005) = Installment A/R (Beg) – Installment A/R (End) – Installment A/R cancelled

Cash collection (2005) = 90,000 – 0 – 15,000 Cash collection (2005) = 75,000

Computation of Realized Gross Profit: Realized gross profit = Cash collection X DGP% Realized gross profit (2007) = 112,500 x 32% 36,000 Realized gross profit (2006) = 150,000 x 30% 45,000 Realized gross profit (2005) = 75,000 x 25% 18,750 Total realized gross profit = 99,750

Installment Sales

Chapter # 1

www.a4accounting.net Page 10

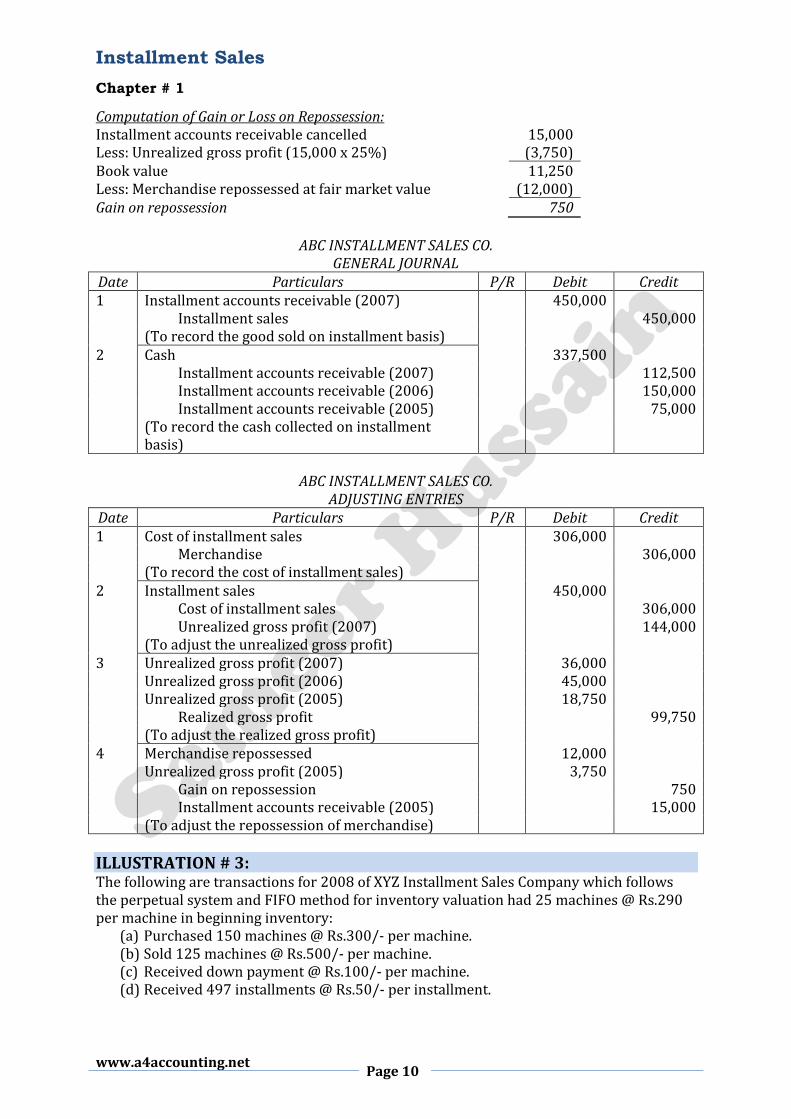

Computation of Gain or Loss on Repossession: Installment accounts receivable cancelled 15,000 Less: Unrealized gross profit (15,000 x 25%) (3,750) Book value 11,250 Less: Merchandise repossessed at fair market value (12,000) Gain on repossession 750

ABC INSTALLMENT SALES CO. GENERAL JOURNAL

Date Particulars P/R Debit Credit 1 Installment accounts receivable (2007) 450,000 Installment sales 450,000 (To record the good sold on installment basis) 2 Cash 337,500 Installment accounts receivable (2007) 112,500 Installment accounts receivable (2006) 150,000 Installment accounts receivable (2005) 75,000 (To record the cash collected on installment

basis)

ABC INSTALLMENT SALES CO.

ADJUSTING ENTRIES Date Particulars P/R Debit Credit 1 Cost of installment sales 306,000 Merchandise 306,000 (To record the cost of installment sales) 2 Installment sales 450,000 Cost of installment sales 306,000 Unrealized gross profit (2007) 144,000 (To adjust the unrealized gross profit) 3 Unrealized gross profit (2007) 36,000 Unrealized gross profit (2006) 45,000 Unrealized gross profit (2005) 18,750 Realized gross profit 99,750 (To adjust the realized gross profit) 4 Merchandise repossessed 12,000 Unrealized gross profit (2005) 3,750 Gain on repossession 750 Installment accounts receivable (2005) 15,000 (To adjust the repossession of merchandise)

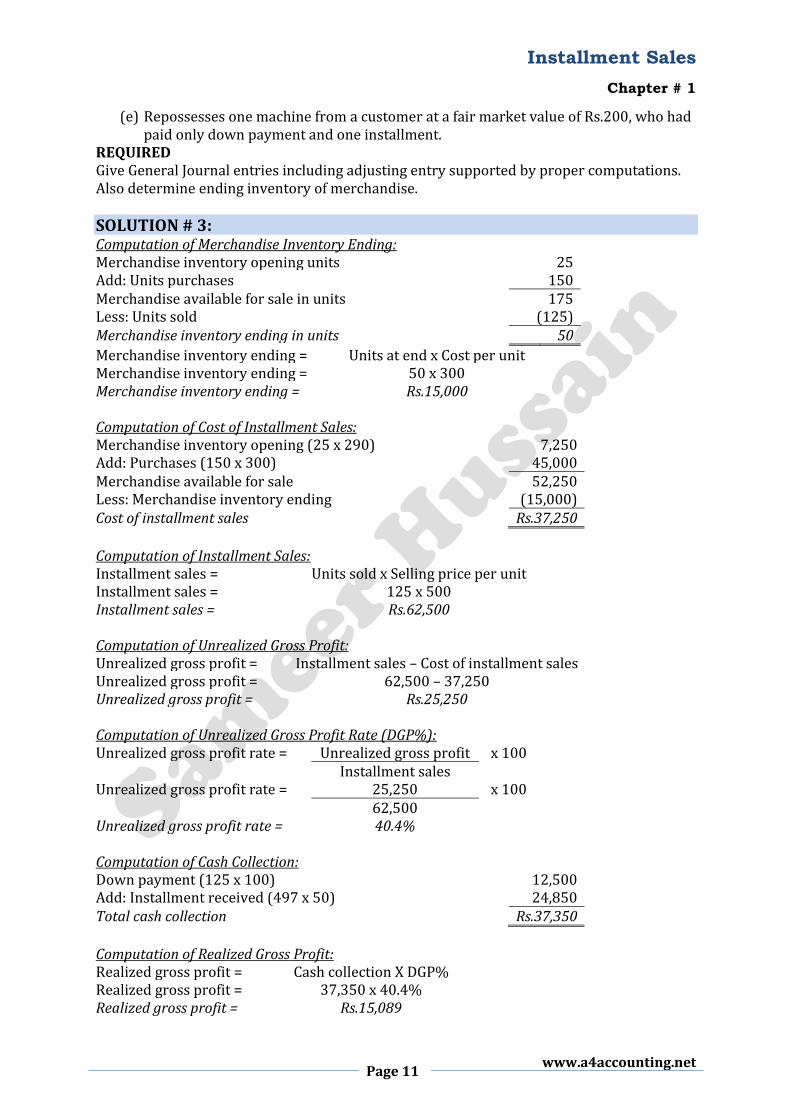

ILLUSTRATION # 3: The following are transactions for 2008 of XYZ Installment Sales Company which follows the perpetual system and FIFO method for inventory valuation had 25 machines @ Rs.290 per machine in beginning inventory:

(a) Purchased 150 machines @ Rs.300/- per machine. (b) Sold 125 machines @ Rs.500/- per machine. (c) Received down payment @ Rs.100/- per machine. (d) Received 497 installments @ Rs.50/- per installment.

Installment Sales

Chapter # 1

Page 11

www.a4accounting.net

(e) Repossesses one machine from a customer at a fair market value of Rs.200, who had paid only down payment and one installment.

REQUIRED Give General Journal entries including adjusting entry supported by proper computations. Also determine ending inventory of merchandise.

SOLUTION # 3: Computation of Merchandise Inventory Ending: Merchandise inventory opening units 25 Add: Units purchases 150 Merchandise available for sale in units 175 Less: Units sold (125) Merchandise inventory ending in units 50

Merchandise inventory ending = Units at end x Cost per unit Merchandise inventory ending = 50 x 300 Merchandise inventory ending = Rs.15,000

Computation of Cost of Installment Sales: Merchandise inventory opening (25 x 290) 7,250 Add: Purchases (150 x 300) 45,000 Merchandise available for sale 52,250 Less: Merchandise inventory ending (15,000) Cost of installment sales Rs.37,250

Computation of Installment Sales: Installment sales = Units sold x Selling price per unit Installment sales = 125 x 500 Installment sales = Rs.62,500

Computation of Unrealized Gross Profit: Unrealized gross profit = Installment sales – Cost of installment sales Unrealized gross profit = 62,500 – 37,250 Unrealized gross profit = Rs.25,250

Computation of Unrealized Gross Profit Rate (DGP%): Unrealized gross profit rate = Unrealized gross profit x 100 Installment sales Unrealized gross profit rate = 25,250 x 100 62,500 Unrealized gross profit rate = 40.4%

Computation of Cash Collection: Down payment (125 x 100) 12,500 Add: Installment received (497 x 50) 24,850 Total cash collection Rs.37,350

Computation of Realized Gross Profit: Realized gross profit = Cash collection X DGP% Realized gross profit = 37,350 x 40.4% Realized gross profit = Rs.15,089

Installment Sales

Chapter # 1

www.a4accounting.net Page 12

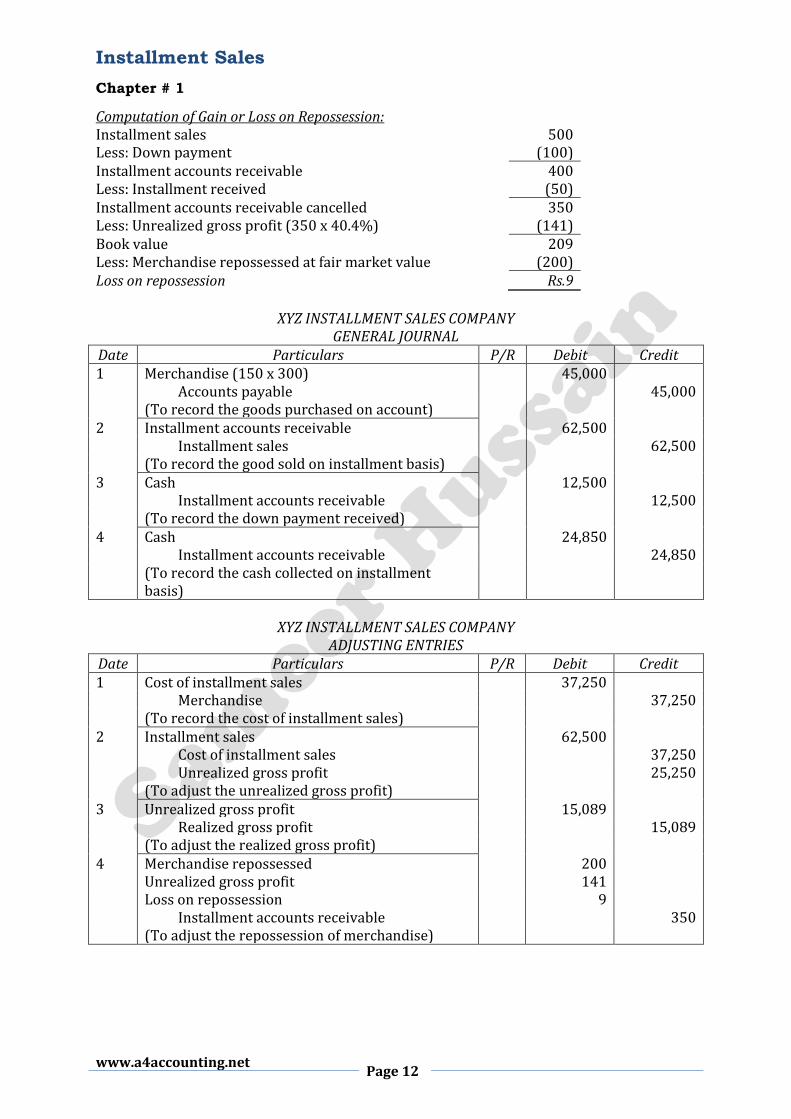

Computation of Gain or Loss on Repossession: Installment sales 500 Less: Down payment (100) Installment accounts receivable 400 Less: Installment received (50) Installment accounts receivable cancelled 350 Less: Unrealized gross profit (350 x 40.4%) (141) Book value 209 Less: Merchandise repossessed at fair market value (200) Loss on repossession Rs.9

XYZ INSTALLMENT SALES COMPANY GENERAL JOURNAL

Date Particulars P/R Debit Credit 1 Merchandise (150 x 300) 45,000 Accounts payable 45,000 (To record the goods purchased on account) 2 Installment accounts receivable 62,500 Installment sales 62,500 (To record the good sold on installment basis) 3 Cash 12,500 Installment accounts receivable 12,500 (To record the down payment received) 4 Cash 24,850 Installment accounts receivable 24,850 (To record the cash collected on installment

basis)

XYZ INSTALLMENT SALES COMPANY ADJUSTING ENTRIES

Date Particulars P/R Debit Credit 1 Cost of installment sales 37,250 Merchandise 37,250 (To record the cost of installment sales) 2 Installment sales 62,500 Cost of installment sales 37,250 Unrealized gross profit 25,250 (To adjust the unrealized gross profit) 3 Unrealized gross profit 15,089 Realized gross profit 15,089 (To adjust the realized gross profit) 4 Merchandise repossessed 200 Unrealized gross profit 141 Loss on repossession 9 Installment accounts receivable 350 (To adjust the repossession of merchandise)

Installment Sales

Chapter # 1

Page 13

www.a4accounting.net

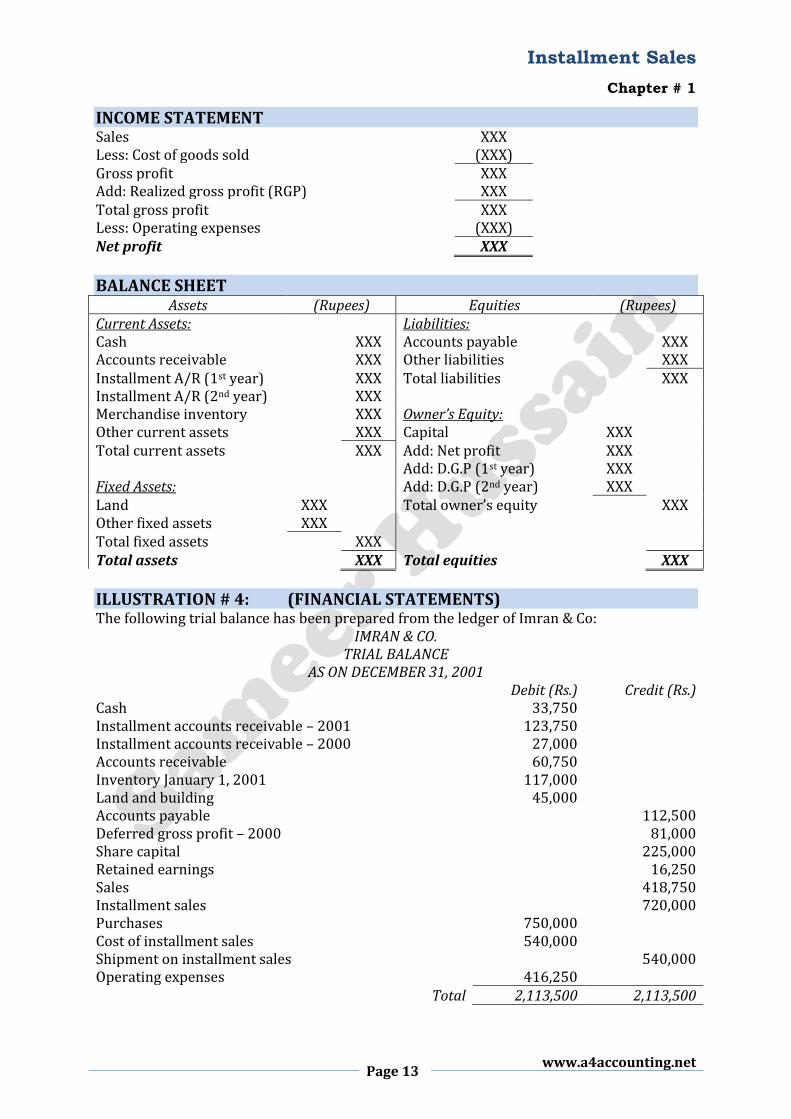

INCOME STATEMENT Sales XXX Less: Cost of goods sold (XXX) Gross profit XXX Add: Realized gross profit (RGP) XXX Total gross profit XXX Less: Operating expenses (XXX) Net profit XXX

BALANCE SHEET Assets (Rupees) Equities (Rupees)

Current Assets: Liabilities: Cash XXX Accounts payable XXX Accounts receivable XXX Other liabilities XXX Installment A/R (1st year) XXX Total liabilities XXX Installment A/R (2nd year) XXX Merchandise inventory XXX Owner’s Equity: Other current assets XXX Capital XXX Total current assets XXX Add: Net profit XXX Add: D.G.P (1st year) XXX Fixed Assets: Add: D.G.P (2nd year) XXX Land XXX Total owner’s equity XXX Other fixed assets XXX Total fixed assets XXX Total assets XXX Total equities XXX

ILLUSTRATION # 4: (FINANCIAL STATEMENTS) The following trial balance has been prepared from the ledger of Imran & Co:

IMRAN & CO. TRIAL BALANCE

AS ON DECEMBER 31, 2001 Debit (Rs.) Credit (Rs.) Cash 33,750 Installment accounts receivable – 2001 123,750 Installment accounts receivable – 2000 27,000 Accounts receivable 60,750 Inventory January 1, 2001 117,000 Land and building 45,000 Accounts payable 112,500 Deferred gross profit – 2000 81,000 Share capital 225,000 Retained earnings 16,250 Sales 418,750 Installment sales 720,000 Purchases 750,000 Cost of installment sales 540,000 Shipment on installment sales 540,000 Operating expenses 416,250

Total 2,113,500 2,113,500

Installment Sales

Chapter # 1

www.a4accounting.net Page 14

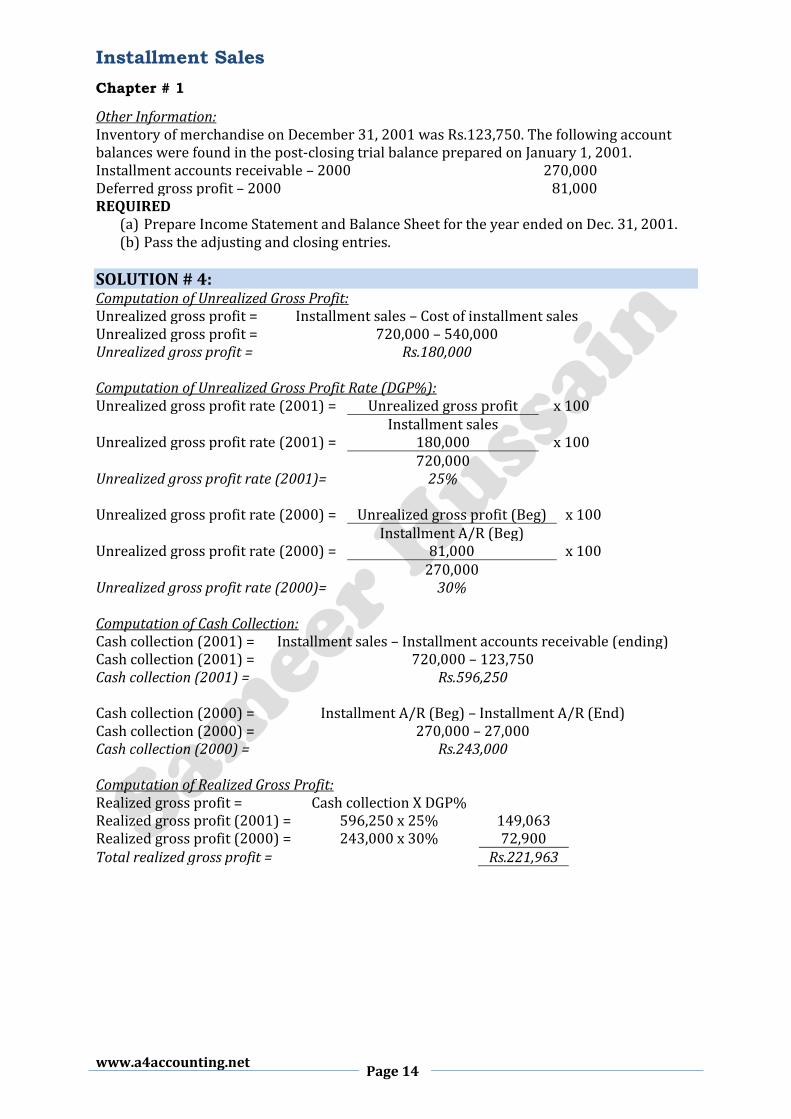

Other Information: Inventory of merchandise on December 31, 2001 was Rs.123,750. The following account balances were found in the post-closing trial balance prepared on January 1, 2001. Installment accounts receivable – 2000 270,000 Deferred gross profit – 2000 81,000 REQUIRED

(a) Prepare Income Statement and Balance Sheet for the year ended on Dec. 31, 2001. (b) Pass the adjusting and closing entries.

SOLUTION # 4: Computation of Unrealized Gross Profit: Unrealized gross profit = Installment sales – Cost of installment sales Unrealized gross profit = 720,000 – 540,000 Unrealized gross profit = Rs.180,000

Computation of Unrealized Gross Profit Rate (DGP%): Unrealized gross profit rate (2001) = Unrealized gross profit x 100 Installment sales Unrealized gross profit rate (2001) = 180,000 x 100 720,000 Unrealized gross profit rate (2001)= 25%

Unrealized gross profit rate (2000) = Unrealized gross profit (Beg) x 100 Installment A/R (Beg) Unrealized gross profit rate (2000) = 81,000 x 100 270,000 Unrealized gross profit rate (2000)= 30%

Computation of Cash Collection: Cash collection (2001) = Installment sales – Installment accounts receivable (ending) Cash collection (2001) = 720,000 – 123,750 Cash collection (2001) = Rs.596,250 Cash collection (2000) = Installment A/R (Beg) – Installment A/R (End) Cash collection (2000) = 270,000 – 27,000 Cash collection (2000) = Rs.243,000

Computation of Realized Gross Profit: Realized gross profit = Cash collection X DGP% Realized gross profit (2001) = 596,250 x 25% 149,063 Realized gross profit (2000) = 243,000 x 30% 72,900 Total realized gross profit = Rs.221,963

Installment Sales

Chapter # 1

Page 15

www.a4accounting.net

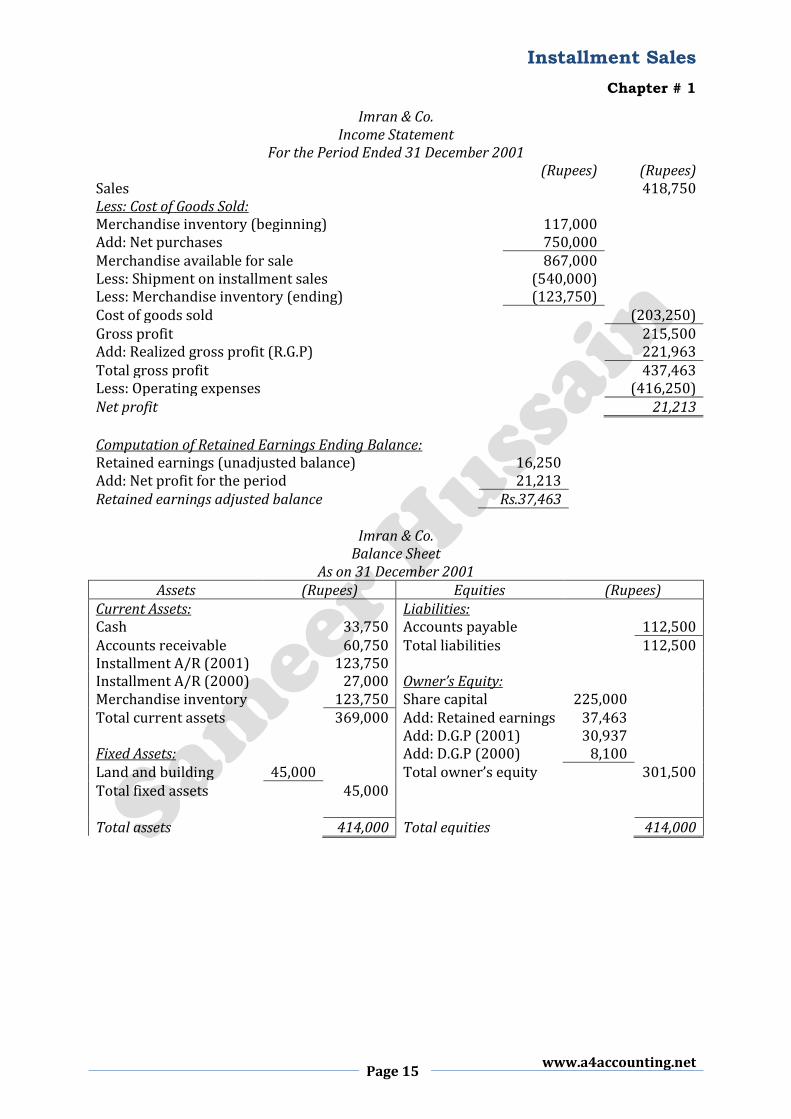

Imran & Co. Income Statement

For the Period Ended 31 December 2001 (Rupees) (Rupees) Sales 418,750 Less: Cost of Goods Sold: Merchandise inventory (beginning) 117,000 Add: Net purchases 750,000 Merchandise available for sale 867,000 Less: Shipment on installment sales (540,000) Less: Merchandise inventory (ending) (123,750) Cost of goods sold (203,250) Gross profit 215,500 Add: Realized gross profit (R.G.P) 221,963 Total gross profit 437,463 Less: Operating expenses (416,250) Net profit 21,213

Computation of Retained Earnings Ending Balance: Retained earnings (unadjusted balance) 16,250 Add: Net profit for the period 21,213 Retained earnings adjusted balance Rs.37,463

Imran & Co. Balance Sheet

As on 31 December 2001 Assets (Rupees) Equities (Rupees)

Current Assets: Liabilities: Cash 33,750 Accounts payable 112,500 Accounts receivable 60,750 Total liabilities 112,500 Installment A/R (2001) 123,750 Installment A/R (2000) 27,000 Owner’s Equity: Merchandise inventory 123,750 Share capital 225,000 Total current assets 369,000 Add: Retained earnings 37,463 Add: D.G.P (2001) 30,937 Fixed Assets: Add: D.G.P (2000) 8,100 Land and building 45,000 Total owner’s equity 301,500 Total fixed assets 45,000 Total assets 414,000 Total equities 414,000

Installment Sales

Chapter # 1

www.a4accounting.net Page 16

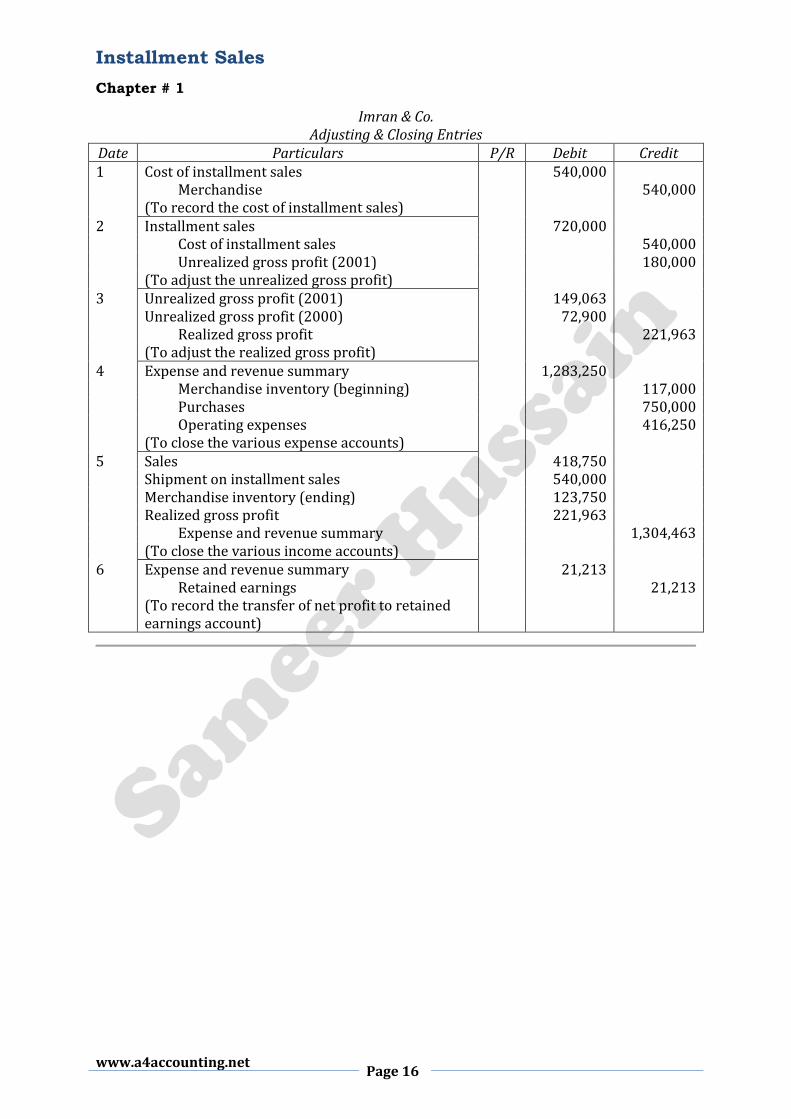

Imran & Co. Adjusting & Closing Entries

Date Particulars P/R Debit Credit 1 Cost of installment sales 540,000 Merchandise 540,000 (To record the cost of installment sales) 2 Installment sales 720,000 Cost of installment sales 540,000 Unrealized gross profit (2001) 180,000 (To adjust the unrealized gross profit) 3 Unrealized gross profit (2001) 149,063 Unrealized gross profit (2000) 72,900 Realized gross profit 221,963 (To adjust the realized gross profit) 4 Expense and revenue summary 1,283,250 Merchandise inventory (beginning) 117,000 Purchases 750,000 Operating expenses 416,250 (To close the various expense accounts) 5 Sales 418,750 Shipment on installment sales 540,000 Merchandise inventory (ending) 123,750 Realized gross profit 221,963 Expense and revenue summary 1,304,463 (To close the various income accounts) 6 Expense and revenue summary 21,213 Retained earnings 21,213 (To record the transfer of net profit to retained

earnings account)

Installment Sales

Chapter # 1

Page 17

www.a4accounting.net

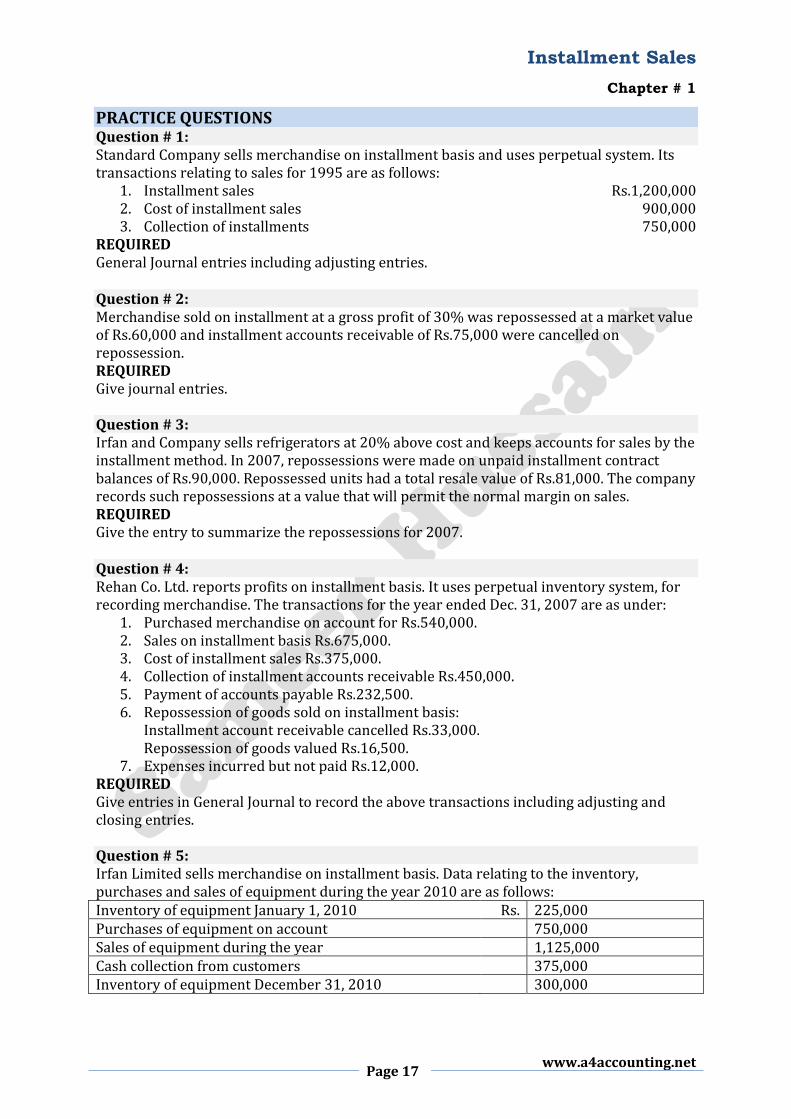

PRACTICE QUESTIONS Question # 1: Standard Company sells merchandise on installment basis and uses perpetual system. Its transactions relating to sales for 1995 are as follows:

1. Installment sales Rs.1,200,000 2. Cost of installment sales 900,000 3. Collection of installments 750,000

REQUIRED General Journal entries including adjusting entries. Question # 2: Merchandise sold on installment at a gross profit of 30% was repossessed at a market value of Rs.60,000 and installment accounts receivable of Rs.75,000 were cancelled on repossession. REQUIRED Give journal entries. Question # 3: Irfan and Company sells refrigerators at 20% above cost and keeps accounts for sales by the installment method. In 2007, repossessions were made on unpaid installment contract balances of Rs.90,000. Repossessed units had a total resale value of Rs.81,000. The company records such repossessions at a value that will permit the normal margin on sales. REQUIRED Give the entry to summarize the repossessions for 2007. Question # 4: Rehan Co. Ltd. reports profits on installment basis. It uses perpetual inventory system, for recording merchandise. The transactions for the year ended Dec. 31, 2007 are as under:

1. Purchased merchandise on account for Rs.540,000. 2. Sales on installment basis Rs.675,000. 3. Cost of installment sales Rs.375,000. 4. Collection of installment accounts receivable Rs.450,000. 5. Payment of accounts payable Rs.232,500. 6. Repossession of goods sold on installment basis:

Installment account receivable cancelled Rs.33,000. Repossession of goods valued Rs.16,500.

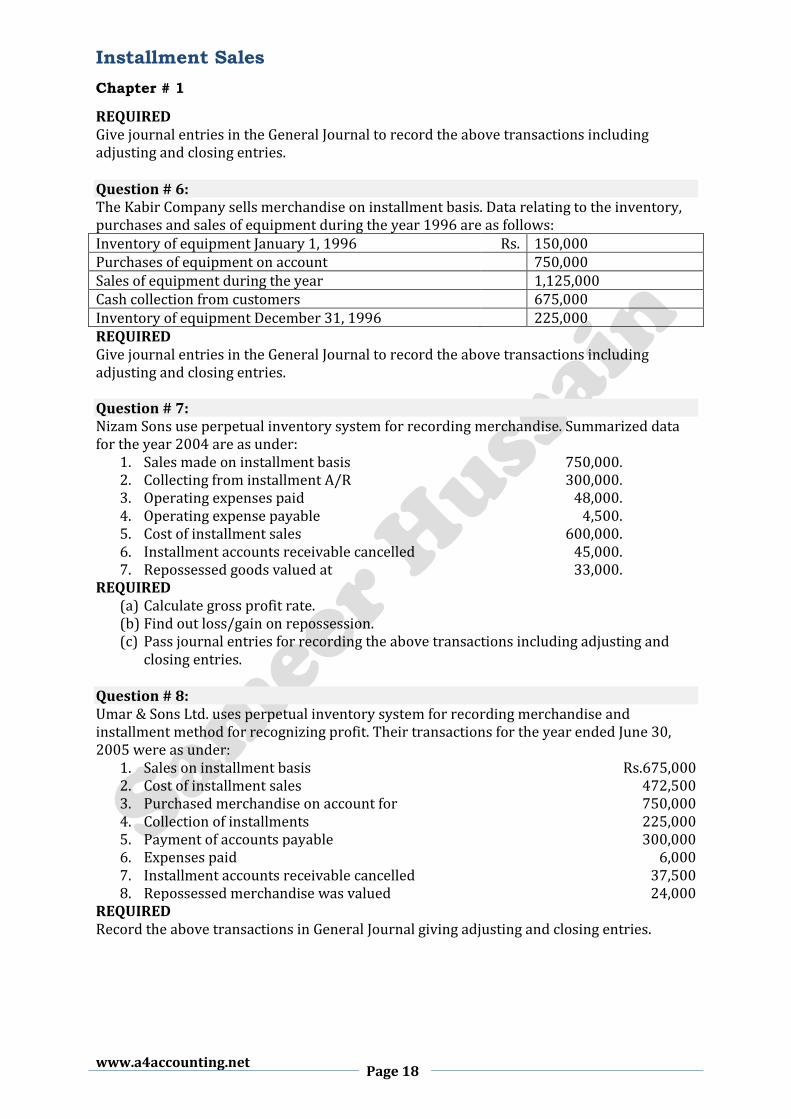

7. Expenses incurred but not paid Rs.12,000. REQUIRED Give entries in General Journal to record the above transactions including adjusting and closing entries. Question # 5: Irfan Limited sells merchandise on installment basis. Data relating to the inventory, purchases and sales of equipment during the year 2010 are as follows: Inventory of equipment January 1, 2010 Rs. 225,000 Purchases of equipment on account 750,000 Sales of equipment during the year 1,125,000 Cash collection from customers 375,000 Inventory of equipment December 31, 2010 300,000

Installment Sales

Chapter # 1

www.a4accounting.net Page 18

REQUIRED Give journal entries in the General Journal to record the above transactions including adjusting and closing entries. Question # 6: The Kabir Company sells merchandise on installment basis. Data relating to the inventory, purchases and sales of equipment during the year 1996 are as follows: Inventory of equipment January 1, 1996 Rs. 150,000 Purchases of equipment on account 750,000 Sales of equipment during the year 1,125,000 Cash collection from customers 675,000 Inventory of equipment December 31, 1996 225,000 REQUIRED Give journal entries in the General Journal to record the above transactions including adjusting and closing entries. Question # 7: Nizam Sons use perpetual inventory system for recording merchandise. Summarized data for the year 2004 are as under:

1. Sales made on installment basis 750,000. 2. Collecting from installment A/R 300,000. 3. Operating expenses paid 48,000. 4. Operating expense payable 4,500. 5. Cost of installment sales 600,000. 6. Installment accounts receivable cancelled 45,000. 7. Repossessed goods valued at 33,000.

REQUIRED (a) Calculate gross profit rate. (b) Find out loss/gain on repossession. (c) Pass journal entries for recording the above transactions including adjusting and

closing entries. Question # 8: Umar & Sons Ltd. uses perpetual inventory system for recording merchandise and installment method for recognizing profit. Their transactions for the year ended June 30, 2005 were as under:

1. Sales on installment basis Rs.675,000 2. Cost of installment sales 472,500 3. Purchased merchandise on account for 750,000 4. Collection of installments 225,000 5. Payment of accounts payable 300,000 6. Expenses paid 6,000 7. Installment accounts receivable cancelled 37,500 8. Repossessed merchandise was valued 24,000

REQUIRED Record the above transactions in General Journal giving adjusting and closing entries.

Installment Sales

Chapter # 1

Page 19

www.a4accounting.net

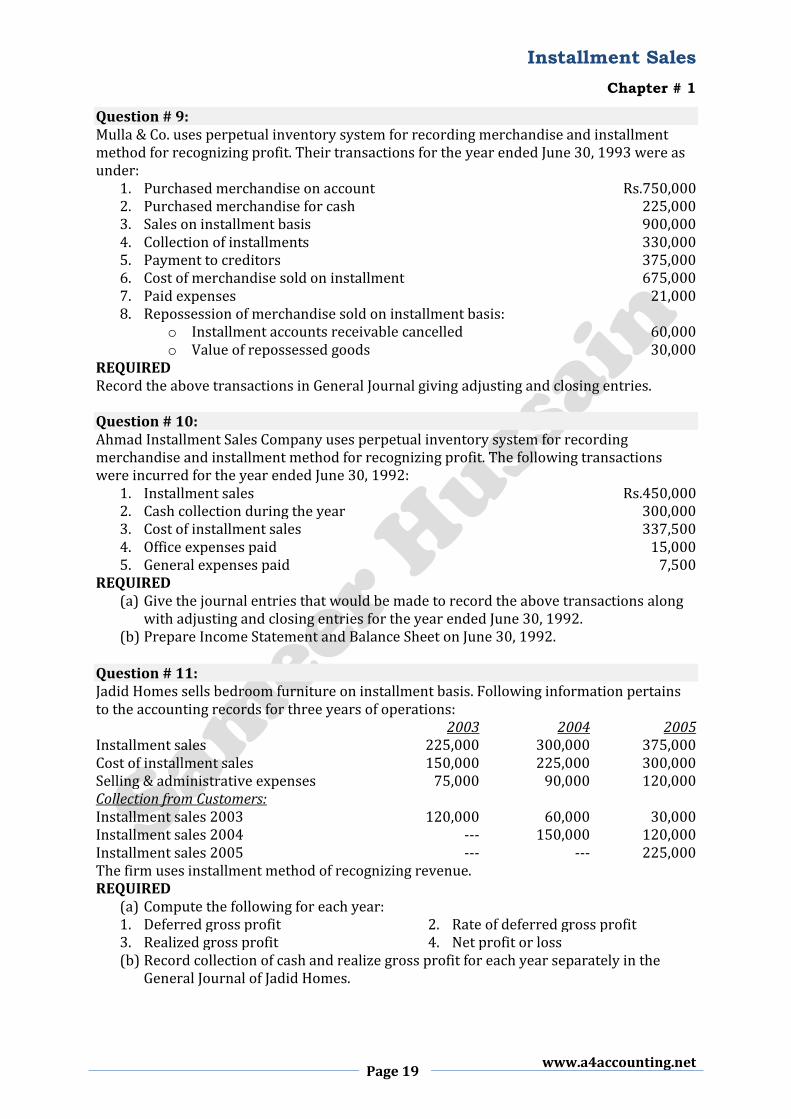

Question # 9: Mulla & Co. uses perpetual inventory system for recording merchandise and installment method for recognizing profit. Their transactions for the year ended June 30, 1993 were as under:

1. Purchased merchandise on account Rs.750,000 2. Purchased merchandise for cash 225,000 3. Sales on installment basis 900,000 4. Collection of installments 330,000 5. Payment to creditors 375,000 6. Cost of merchandise sold on installment 675,000 7. Paid expenses 21,000 8. Repossession of merchandise sold on installment basis:

o Installment accounts receivable cancelled 60,000 o Value of repossessed goods 30,000

REQUIRED Record the above transactions in General Journal giving adjusting and closing entries. Question # 10: Ahmad Installment Sales Company uses perpetual inventory system for recording merchandise and installment method for recognizing profit. The following transactions were incurred for the year ended June 30, 1992:

1. Installment sales Rs.450,000 2. Cash collection during the year 300,000 3. Cost of installment sales 337,500 4. Office expenses paid 15,000 5. General expenses paid 7,500

REQUIRED (a) Give the journal entries that would be made to record the above transactions along

with adjusting and closing entries for the year ended June 30, 1992. (b) Prepare Income Statement and Balance Sheet on June 30, 1992.

Question # 11: Jadid Homes sells bedroom furniture on installment basis. Following information pertains to the accounting records for three years of operations: 2003 2004 2005 Installment sales 225,000 300,000 375,000 Cost of installment sales 150,000 225,000 300,000 Selling & administrative expenses 75,000 90,000 120,000 Collection from Customers: Installment sales 2003 120,000 60,000 30,000 Installment sales 2004 --- 150,000 120,000 Installment sales 2005 --- --- 225,000 The firm uses installment method of recognizing revenue. REQUIRED

(a) Compute the following for each year: 1. Deferred gross profit 2. Rate of deferred gross profit 3. Realized gross profit 4. Net profit or loss (b) Record collection of cash and realize gross profit for each year separately in the

General Journal of Jadid Homes.

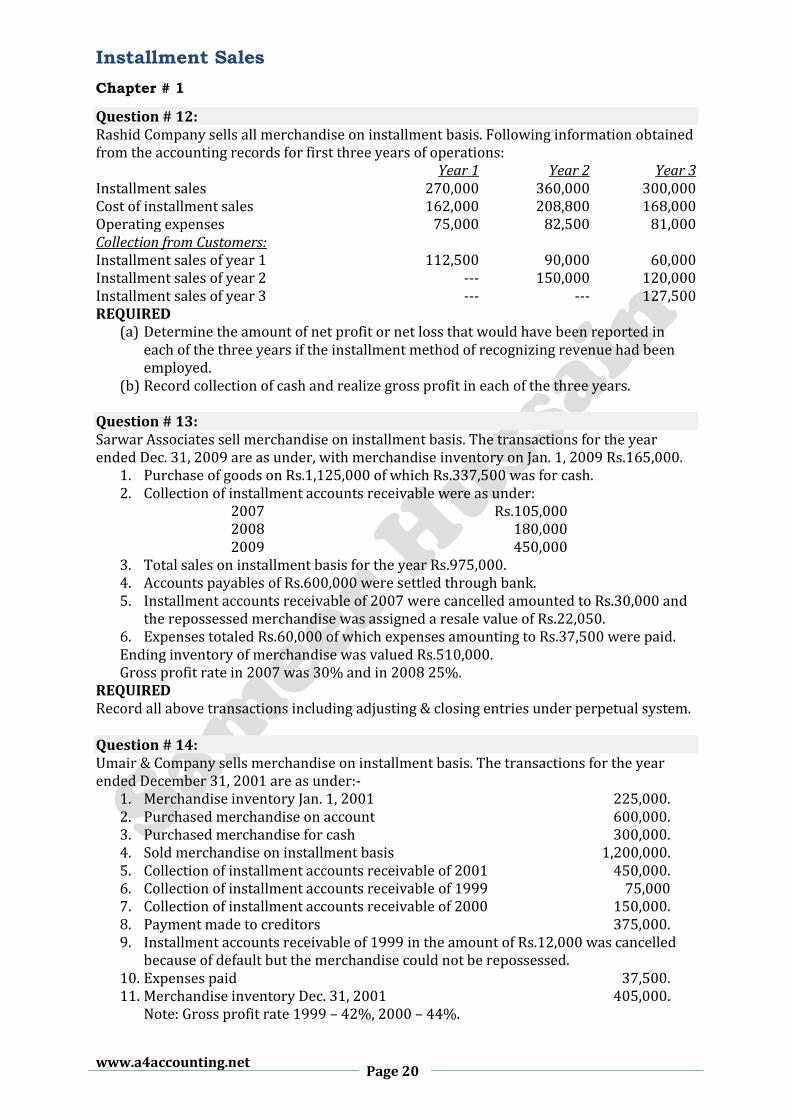

Installment Sales

Chapter # 1

www.a4accounting.net Page 20

Question # 12: Rashid Company sells all merchandise on installment basis. Following information obtained from the accounting records for first three years of operations: Year 1 Year 2 Year 3 Installment sales 270,000 360,000 300,000 Cost of installment sales 162,000 208,800 168,000 Operating expenses 75,000 82,500 81,000 Collection from Customers: Installment sales of year 1 112,500 90,000 60,000 Installment sales of year 2 --- 150,000 120,000 Installment sales of year 3 --- --- 127,500 REQUIRED

(a) Determine the amount of net profit or net loss that would have been reported in each of the three years if the installment method of recognizing revenue had been employed.

(b) Record collection of cash and realize gross profit in each of the three years. Question # 13: Sarwar Associates sell merchandise on installment basis. The transactions for the year ended Dec. 31, 2009 are as under, with merchandise inventory on Jan. 1, 2009 Rs.165,000.

1. Purchase of goods on Rs.1,125,000 of which Rs.337,500 was for cash. 2. Collection of installment accounts receivable were as under:

2007 Rs.105,000 2008 180,000 2009 450,000

3. Total sales on installment basis for the year Rs.975,000. 4. Accounts payables of Rs.600,000 were settled through bank. 5. Installment accounts receivable of 2007 were cancelled amounted to Rs.30,000 and

the repossessed merchandise was assigned a resale value of Rs.22,050. 6. Expenses totaled Rs.60,000 of which expenses amounting to Rs.37,500 were paid. Ending inventory of merchandise was valued Rs.510,000. Gross profit rate in 2007 was 30% and in 2008 25%.

REQUIRED Record all above transactions including adjusting & closing entries under perpetual system. Question # 14: Umair & Company sells merchandise on installment basis. The transactions for the year ended December 31, 2001 are as under:-

1. Merchandise inventory Jan. 1, 2001 225,000. 2. Purchased merchandise on account 600,000. 3. Purchased merchandise for cash 300,000. 4. Sold merchandise on installment basis 1,200,000. 5. Collection of installment accounts receivable of 2001 450,000. 6. Collection of installment accounts receivable of 1999 75,000 7. Collection of installment accounts receivable of 2000 150,000. 8. Payment made to creditors 375,000. 9. Installment accounts receivable of 1999 in the amount of Rs.12,000 was cancelled

because of default but the merchandise could not be repossessed. 10. Expenses paid 37,500. 11. Merchandise inventory Dec. 31, 2001 405,000.

Note: Gross profit rate 1999 – 42%, 2000 – 44%.

Installment Sales

Chapter # 1

Page 21

www.a4accounting.net

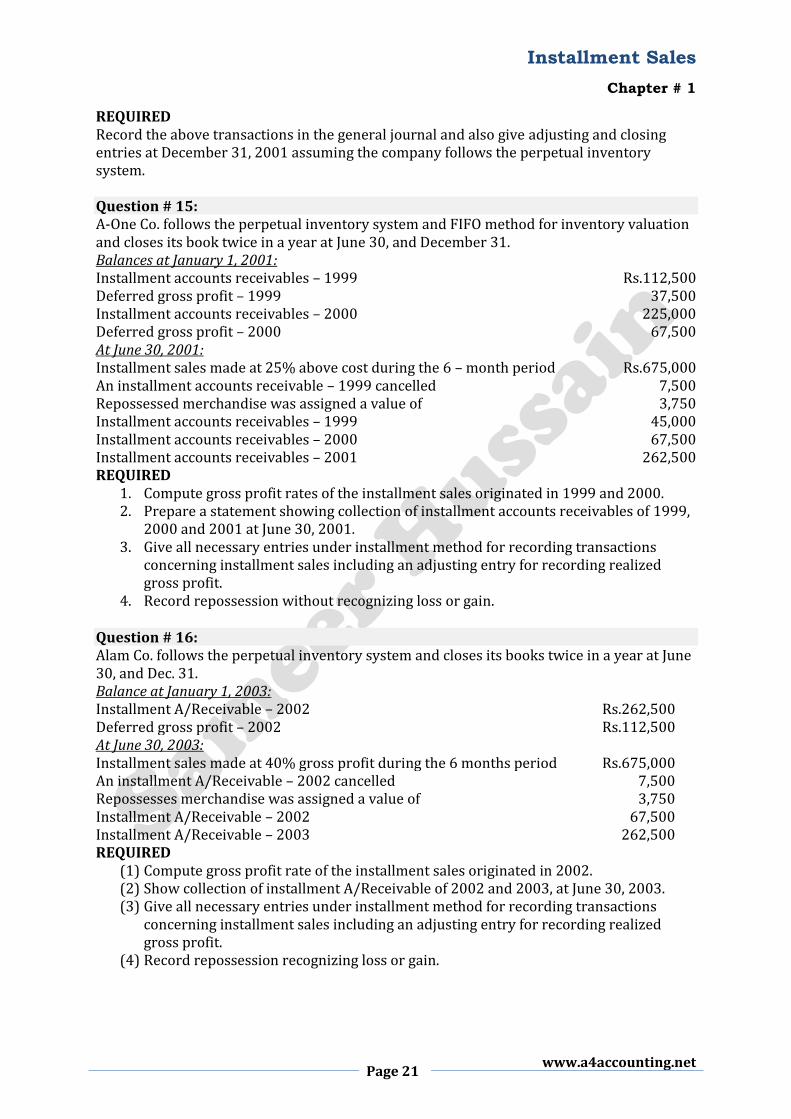

REQUIRED Record the above transactions in the general journal and also give adjusting and closing entries at December 31, 2001 assuming the company follows the perpetual inventory system. Question # 15: A-One Co. follows the perpetual inventory system and FIFO method for inventory valuation and closes its book twice in a year at June 30, and December 31. Balances at January 1, 2001: Installment accounts receivables – 1999 Rs.112,500 Deferred gross profit – 1999 37,500 Installment accounts receivables – 2000 225,000 Deferred gross profit – 2000 67,500 At June 30, 2001: Installment sales made at 25% above cost during the 6 – month period Rs.675,000 An installment accounts receivable – 1999 cancelled 7,500 Repossessed merchandise was assigned a value of 3,750 Installment accounts receivables – 1999 45,000 Installment accounts receivables – 2000 67,500 Installment accounts receivables – 2001 262,500 REQUIRED

1. Compute gross profit rates of the installment sales originated in 1999 and 2000. 2. Prepare a statement showing collection of installment accounts receivables of 1999,

2000 and 2001 at June 30, 2001. 3. Give all necessary entries under installment method for recording transactions

concerning installment sales including an adjusting entry for recording realized gross profit.

4. Record repossession without recognizing loss or gain. Question # 16: Alam Co. follows the perpetual inventory system and closes its books twice in a year at June 30, and Dec. 31. Balance at January 1, 2003: Installment A/Receivable – 2002 Rs.262,500 Deferred gross profit – 2002 Rs.112,500 At June 30, 2003: Installment sales made at 40% gross profit during the 6 months period Rs.675,000 An installment A/Receivable – 2002 cancelled 7,500 Repossesses merchandise was assigned a value of 3,750 Installment A/Receivable – 2002 67,500 Installment A/Receivable – 2003 262,500 REQUIRED

(1) Compute gross profit rate of the installment sales originated in 2002. (2) Show collection of installment A/Receivable of 2002 and 2003, at June 30, 2003. (3) Give all necessary entries under installment method for recording transactions

concerning installment sales including an adjusting entry for recording realized gross profit.

(4) Record repossession recognizing loss or gain.

Installment Sales

Chapter # 1

www.a4accounting.net Page 22

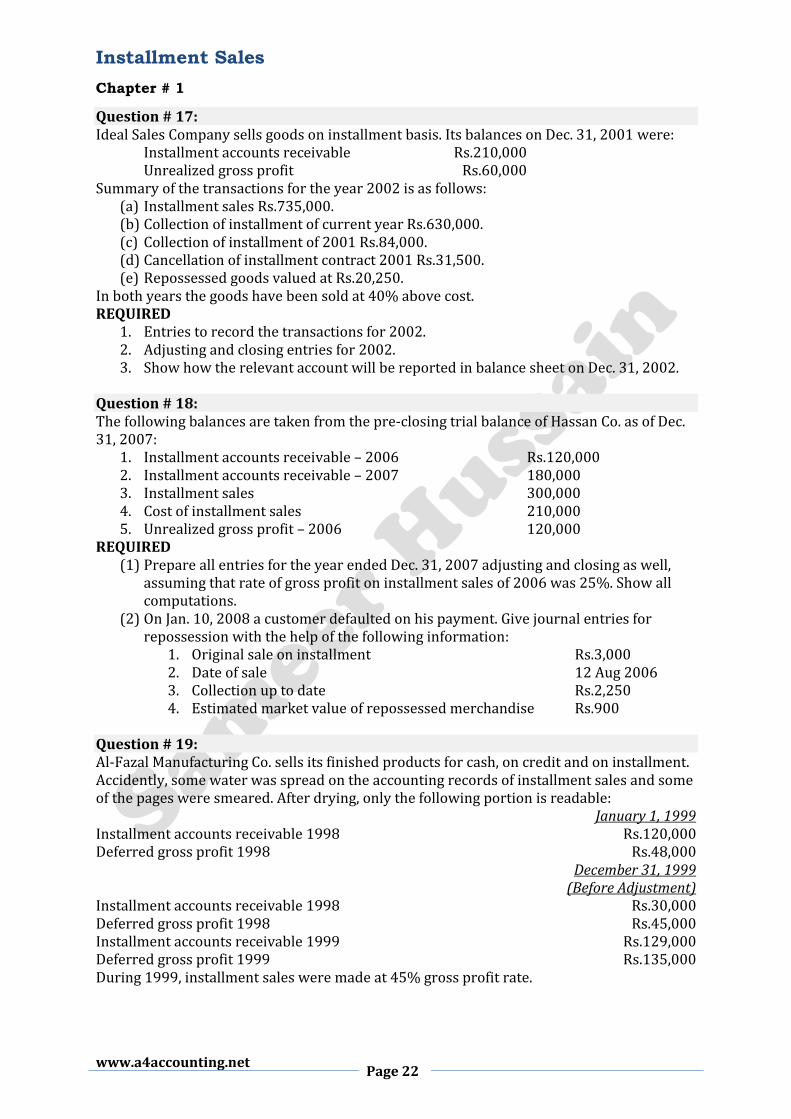

Question # 17: Ideal Sales Company sells goods on installment basis. Its balances on Dec. 31, 2001 were: Installment accounts receivable Rs.210,000 Unrealized gross profit Rs.60,000 Summary of the transactions for the year 2002 is as follows:

(a) Installment sales Rs.735,000. (b) Collection of installment of current year Rs.630,000. (c) Collection of installment of 2001 Rs.84,000. (d) Cancellation of installment contract 2001 Rs.31,500. (e) Repossessed goods valued at Rs.20,250.

In both years the goods have been sold at 40% above cost. REQUIRED

1. Entries to record the transactions for 2002. 2. Adjusting and closing entries for 2002. 3. Show how the relevant account will be reported in balance sheet on Dec. 31, 2002.

Question # 18: The following balances are taken from the pre-closing trial balance of Hassan Co. as of Dec. 31, 2007:

1. Installment accounts receivable – 2006 Rs.120,000 2. Installment accounts receivable – 2007 180,000 3. Installment sales 300,000 4. Cost of installment sales 210,000 5. Unrealized gross profit – 2006 120,000

REQUIRED (1) Prepare all entries for the year ended Dec. 31, 2007 adjusting and closing as well,

assuming that rate of gross profit on installment sales of 2006 was 25%. Show all computations.

(2) On Jan. 10, 2008 a customer defaulted on his payment. Give journal entries for repossession with the help of the following information:

1. Original sale on installment Rs.3,000 2. Date of sale 12 Aug 2006 3. Collection up to date Rs.2,250 4. Estimated market value of repossessed merchandise Rs.900

Question # 19: Al-Fazal Manufacturing Co. sells its finished products for cash, on credit and on installment. Accidently, some water was spread on the accounting records of installment sales and some of the pages were smeared. After drying, only the following portion is readable:

January 1, 1999 Installment accounts receivable 1998 Rs.120,000 Deferred gross profit 1998 Rs.48,000

December 31, 1999 (Before Adjustment)

Installment accounts receivable 1998 Rs.30,000 Deferred gross profit 1998 Rs.45,000 Installment accounts receivable 1999 Rs.129,000 Deferred gross profit 1999 Rs.135,000 During 1999, installment sales were made at 45% gross profit rate.

Installment Sales

Chapter # 1

Page 23

www.a4accounting.net

REQUIRED 1. Reconstruct in general journal form as many summary entries as possible for 1999

under installment method including adjusting and closing entries. Show necessary supporting computations.

2. Give an entry to record repossession assuming that the repossessed merchandise was recorded at its book value.

Question # 20: The selected balances of Akbar Installment Sales Co. are as follows: 1997 – Jan. 1 1997 – Dec. 31 Installment accounts receivable – 1995 180,000 - Installment accounts receivable – 1996 570,000 270,000 Installment accounts receivable – 1997 - 675,000 Deferred gross profit – 1995 45,000 37,500 Deferred gross profit – 1996 171,000 171,000 Installment sales - 900,000 Cost of installment sales - 612,000 Repossessed merchandise - 24,000 Installment accounts receivable – 1995 cancelled on repossession - 30,000 REQUIRED

a) Gross profit percentage for each year. b) Collection of installment accounts receivable of each year during 1997. c) Gross profit realized during 1997. d) General Journal entries made during 1997 on repossession. e) General Journal entries to record the realized gross profit.

Question # 21: The following are the selected assets and equities of Gulbahar Installment Co. on December 31, 2008:

Assets Equities Cash 180,000 Accounts Payable 30,000 Merchandise Inventory 120,000 Deferred Gross Profit – 2007 60,000 Installment A/R 2007 300,000 Capital 510,000 Total Assets 600,000 Total Equities 600,000 Transactions During 2008 Are As Under: Merchandise purchased on accounts 480,000 Installment sales 600,000 Collection from installment accounts receivable – 2007 150,000 Collection from installment accounts receivable – 2008 300,000 Payment of accounts payable 375,000 Installment accounts receivable – 2007 defaulted of 120,000 Merchandise repossessed at fair market value 30,000 Operating expenses paid 15,000 Merchandise inventory-ending (including repossessed merchandise) 180,000 Company uses perpetual inventory system (FIFO basis) for recording merchandise and installment method for recognizing profits. REQUIRED: Give entries in General Journal to record the above data, including adjusting and closing entries for the year 2008.

Installment Sales

Chapter # 1

www.a4accounting.net Page 24

Question # 22: Naseem & Company sells merchandise on installment basis. The summary of transactions for the year ended December 31, 1985 and December 31, 1986 are as follows: 1985 1986 Installment sales 750,000 1,125,000 Collection in respect of 1985 installment sales 450,000 225,000 Collection in respect of 1986 installment sales - 675,000 Purchase on account 615,000 750,000 Selling & general expenses 112,500 255,000 Payment of accounts payable 375,000 750,000 Merchandise inventory ending 150,000 225,000 REQUIRED: Give journal entries for the years ended December 31, 1985 and 1986 including adjusting journal entries. Question # 23: The following are transactions for 1998 of Lahore Installment Sales Company which follows the perpetual system and FIFO method for inventory valuation had 75 machines @ Rs.870 per machine in beginning inventory:

(a) Purchased 450 machines at the rate of Rs.900/- per machine. (b) Sold 375 machines at the rate of Rs.1,500/- per machine. (c) Received down payment at the rate of Rs.300/- per machine on 375 machines. (d) Received 1,497 installments at the rate of Rs.150/- per installment. (e) Repossesses one machine from a customer, who had paid only down payment and

one installment. REQUIRED General journal entries including adjusting entry supported by proper computations. Also determine ending inventory of merchandise. Question # 24: Smart Home Company sells local vacuum cleaners on installment basis. The company uses perpetual system and first in first out method for inventory valuation. The company has 150 vacuum cleaners of Rs.900 each in the beginning inventory. The company completed the following transactions during the year:

(a) Purchased 450 vacuum cleaners at Rs.975 each. (b) Sold 375 vacuum cleaners at Rs.1,500 each. (c) Collected down payment at Rs.300 on each vacuum cleaner. (d) The balance to be collected in 4 equal quarterly installments of Rs.300 each. (e) All installments were collected in full except a customer who failed to pay the last

installment. (f) The equipment was repossessed. The value of repossessed equipment was Rs.150.

REQUIRED (a) General journal entries including adjusting. (b) Cost of installment sales. (c) Gain or loss on repossession and gross profit realized.

Installment Sales

Chapter # 1

Page 25

www.a4accounting.net

Question # 25: The following transactions relate to Al-Abid Co. for 2006 which follows the perpetual inventory system and FIFO method for valuation of inventory. Opening inventory consist of 75 machines @ Rs.840 per machine. They completed the following transactions:

(1) Purchased 525 machines @ Rs.900 per machine on account. (2) Sold 375 machines @ Rs.1,500 each on installments. (3) Received down payment @ Rs.300 per machine on all the sold machines. (4) Received 1,496 installments @ Rs.150 per installment. (5) Repossessed one machine from a customer who had paid only down payment

having market value of Rs.750. REQUIRED Journal entries including adjusting and closing entries. Show all computations. Question # 26: Mifta Installment Company purchased 15 computers from Alam & Bilal Traders @ Rs.50,400 each on credit. The company sold 7 computers on installment @ Rs.63,000 each on September 1, 2008. The terms of installment sales were to pay 25% on each computer as a down payment and the remaining amounts to be collected in 15 monthly installments starting from October 1, 2008. All installments collected on the first day of each month. Three of the computer holders defaulted to pay the installments after the payment of 5th installment and company repossessed the computers which have the fair market value of Rs.25,500 each computer. Mifta Installment Company closes its accounting year on June 30 each year. REQUIRED Compute the following:

1. Amount of installment sales. 2. Amount of down payment received. 3. Monthly installment amount of each computer. 4. Unrealized (deferred) gross profit. 5. Rate of Unrealized (deferred) gross profit. 6. Total amount of installment accounts receivable cancelled. 7. Book value of repossessed merchandise. 8. Gain or loss on repossession. 9. Total amount collected during the period. 10. Amount of realized gross profit.

Question # 27: On January 1, 1997 the X.Y. Co. sold a car for Rs.900,000 on installment basis. Rs.150,000 was received as down payment and balance amount in five quarterly installment including interest. The rate of interest charge on the unpaid balance is 6% per annum. The cost of the car was Rs.675,000. All payments were duly received. The accounting year ends on December 31, each year. REQUIRED Give journal entries including adjusting and closing entries for the year 1997 only.

Installment Sales

Chapter # 1

www.a4accounting.net Page 26

Question # 28: On July 1, 1993, Shaheen Autos sold 10 Suzuki cars on installment basis at Rs.202,500 per car, the cost being Rs.172,125 per car. The terms of sale were:

a) Rs.52,500 per car should be paid at the time of signing the agreement. b) The balance should be paid in 20 quarterly of Rs.7,500 per car. c) Interest at 8% should be paid on the unpaid balances, and be paid along with the

installment amount. REQUIRED Make necessary journal entries including adjusting and closing of entries in the books of Shaheen Autos in respect of the above transactions for the year ended December 31, 1993 assuming that Shaheen Autos closes its books on December 31, every year. Shaheen Autos follows installment method for recognizing profits. Question # 29: Hasnain & Brothers follows installment method for recognizing profits & closes its accounting year on June 30, every year. On September 12, 2010 Hasnain & Brothers purchased 30 computers from Tauseef Computers for Rs.54,000 each on credit. On October 1, 2010 Hasnain & Brothers sold 25 computers @ Rs.67,500 each. The customers paid Rs.30,000 per computer as down payment of October 1, 2010 and agreed to pay the balance in 8 equal quarterly installments (The first quarter started from October 1, 2010). The ownership would be transferred on the payment of the final installment. The installments received on the last day of each quarter. REQUIRED Prepare journal entries including adjusting and closing to record the above transactions only for the year ended June 30, 2011. Question # 30: City Cars deals with two brands of fuel economy local cars namely GL and XL. The selling price of GL cars is Rs.675,000 each while the XL cars are sold for Rs.600,000. The selling price includes a profit margin of 5 percent. A down payment of 20 percent is collected on each car. The balance is collected on 10 monthly installments of equal amounts. The business completed the following transactions during the year: Purchased 10 units of GL cars and 15 units of XL cars on account from New Age Motors Company. Sold 10 units of each type of cars. The down payment and all installments were collected in full by cheque except the following:

(i) A customer failed to pay last three installments due on the XL cars he had purchased. The vehicle was fortified and assigned a value of Rs.225,000. The car was taken by the owner for his personal use.

(ii) A cheque amounting to Rs.108,000 received from a customer who bought a GL car was dishonored.

City Cars incurred and paid the following expenses during the year: Selling expenses 45,000 Administrative expense 105,000 REQUIRED

(a) General Journal entries in City Cars’ book (adjusting and closing are not required). (b) Cost of installment sales for each brand separately. (c) Gross profit realized on each brand of cars. (d) Net profit of City Cars for the year.

Installment Sales

Chapter # 1

Page 27

www.a4accounting.net

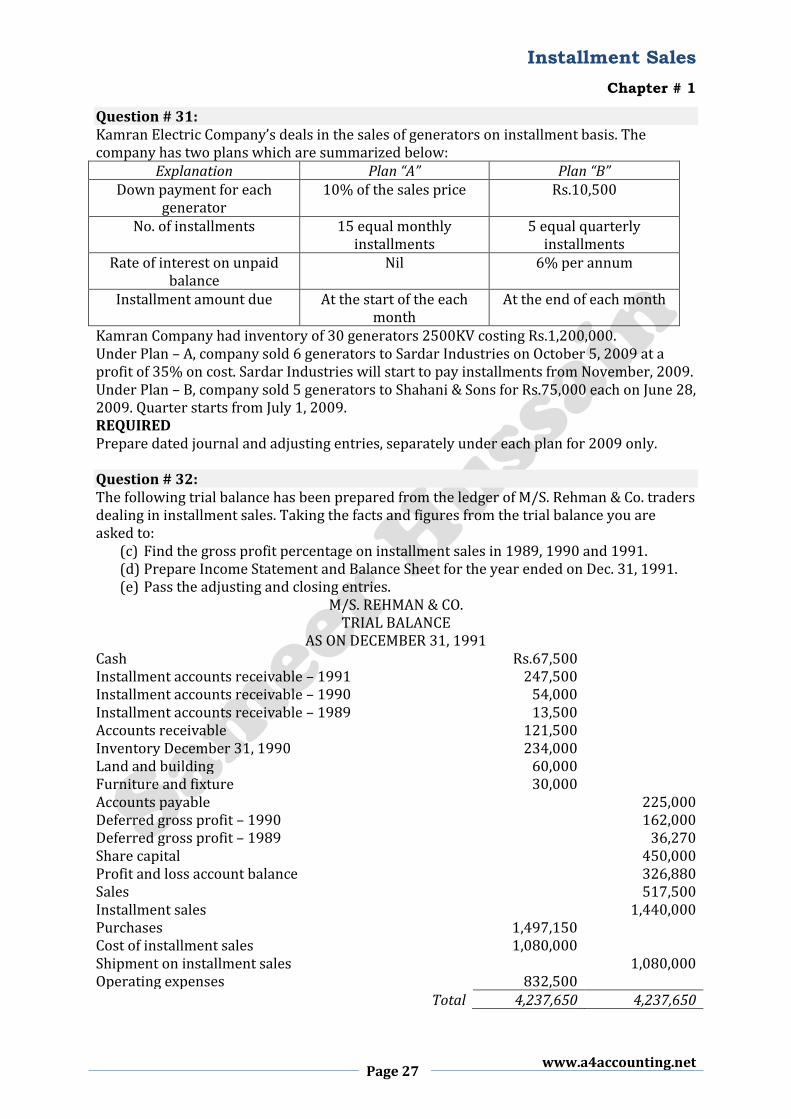

Question # 31: Kamran Electric Company’s deals in the sales of generators on installment basis. The company has two plans which are summarized below:

Explanation Plan “A” Plan “B” Down payment for each

generator 10% of the sales price Rs.10,500

No. of installments 15 equal monthly installments

5 equal quarterly installments

Rate of interest on unpaid balance

Nil 6% per annum

Installment amount due At the start of the each month

At the end of each month

Kamran Company had inventory of 30 generators 2500KV costing Rs.1,200,000. Under Plan – A, company sold 6 generators to Sardar Industries on October 5, 2009 at a profit of 35% on cost. Sardar Industries will start to pay installments from November, 2009. Under Plan – B, company sold 5 generators to Shahani & Sons for Rs.75,000 each on June 28, 2009. Quarter starts from July 1, 2009. REQUIRED Prepare dated journal and adjusting entries, separately under each plan for 2009 only. Question # 32: The following trial balance has been prepared from the ledger of M/S. Rehman & Co. traders dealing in installment sales. Taking the facts and figures from the trial balance you are asked to:

(c) Find the gross profit percentage on installment sales in 1989, 1990 and 1991. (d) Prepare Income Statement and Balance Sheet for the year ended on Dec. 31, 1991. (e) Pass the adjusting and closing entries.

M/S. REHMAN & CO. TRIAL BALANCE

AS ON DECEMBER 31, 1991 Cash Rs.67,500 Installment accounts receivable – 1991 247,500 Installment accounts receivable – 1990 54,000 Installment accounts receivable – 1989 13,500 Accounts receivable 121,500 Inventory December 31, 1990 234,000 Land and building 60,000 Furniture and fixture 30,000 Accounts payable 225,000 Deferred gross profit – 1990 162,000 Deferred gross profit – 1989 36,270 Share capital 450,000 Profit and loss account balance 326,880 Sales 517,500 Installment sales 1,440,000 Purchases 1,497,150 Cost of installment sales 1,080,000 Shipment on installment sales 1,080,000 Operating expenses 832,500

Total 4,237,650 4,237,650

Installment Sales

Chapter # 1

www.a4accounting.net Page 28

Other Information: Inventory of merchandise on December 31, 1991 was Rs.247,500. The following account balances were found in the post-closing trial balance prepared on January 1, 1991. Installment accounts receivable – 1990 540,000 Installment accounts receivable – 1989 117,000 Deferred gross profit – 1990 162,000 Deferred gross profit – 1989 36,270 Question # 33: The Daniyal Electric Products Company manufactures table fans. It is a practice of the company to sell 30% of its production on installment basis. The company recognizes profit on sales on the basis of cash collected from customers. The following are the data for three years:

Years Profit Installment Receivable on January 1, 2010

Collection During 2010

Installment Receivable on December 31, 2010

2008 44% Rs.120,000 Rs.120,000 --- 2009 42% Rs.247,500 Rs.112,500 Rs.135,000 2010 40% Rs.225,000 Rs.450,000

REQUIRED Prepare all journal entries for 2010 from the data above, including those required for the recognition of gross profit at the end of year. Question # 34: Khan and Company reports profits on installment basis. It uses perpetual inventory system for recording merchandise and installment method for recognizing profits. Transactions during 2011 are summarized below:

a) Cost of installment sales Rs.400,000. b) Installment accounts receivable (ending) – 2011 Rs.300,000. c) Installment accounts receivable cancelled – 2010 Rs.40,000. d) Merchandise repossessed at book value which is Rs.32,000. e) Unrealized gross profit (beginning) – 2010 Rs.30,000. f) Installment accounts receivable (ending) – 2010 Rs.20,000. g) Unrealized gross profit percentage remains constant in both the years.

REQUIRED a) Give the necessary General Journal entries including adjusting entries. Show

necessary computations. b) Prepare partial balance sheet as on 31 December 2011 showing installment

accounts receivable and unrealized gross profit.