1 ECGD3110 Systems Engineering & Economy Lecture 3 Interest and Equivalence.

23

1 1 ECGD3110 ECGD3110 Systems Engineering & Economy Systems Engineering & Economy Lecture 3 Lecture 3 Interest and Equivalence Interest and Equivalence

-

Upload

jocelin-fitzgerald -

Category

Documents

-

view

218 -

download

2

Transcript of 1 ECGD3110 Systems Engineering & Economy Lecture 3 Interest and Equivalence.

11

ECGD3110ECGD3110Systems Engineering & EconomySystems Engineering & Economy

Lecture 3Lecture 3Interest and EquivalenceInterest and Equivalence

22

Estimating BenefitsEstimating Benefits

For the most part, we can use exactly the For the most part, we can use exactly the same approach to estimate benefits as to same approach to estimate benefits as to estimate costs:estimate costs:– Fixed and variable benefitsFixed and variable benefits– Recurring and non-recurring benefitsRecurring and non-recurring benefits– Incremental benefitsIncremental benefits– Life-cycle benefitsLife-cycle benefits– Rough, semi-detailed, and detailed benefit estimatesRough, semi-detailed, and detailed benefit estimates– Difficulties in estimationDifficulties in estimation– Segmentation and index modelsSegmentation and index models

Major differences between benefit estimation Major differences between benefit estimation and cost estimation:and cost estimation:

– Costs are more likely to be underestimatedCosts are more likely to be underestimated– Benefits are most likely to be overestimatedBenefits are most likely to be overestimated– Benefits tend to occur further in the future than costsBenefits tend to occur further in the future than costs

33

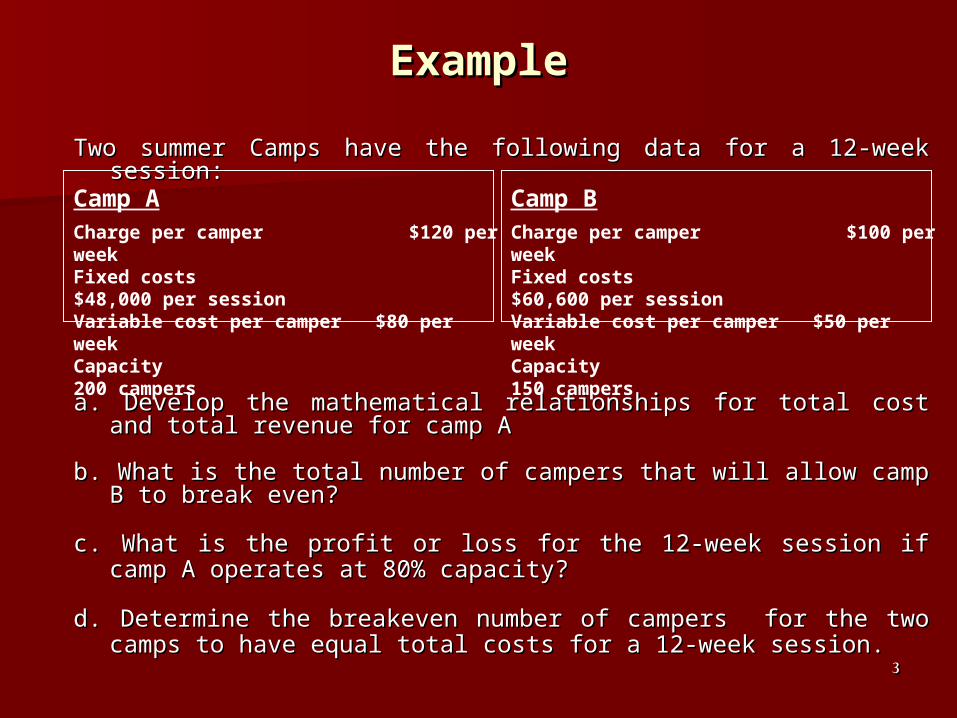

ExampleExample

Two summer Camps have the following data for a 12-week session:Two summer Camps have the following data for a 12-week session: a. Develop the mathematical relationships for total cost and total a. Develop the mathematical relationships for total cost and total

revenue for camp Arevenue for camp A

b. What is the total number of campers that will allow camp B to break b. What is the total number of campers that will allow camp B to break even?even?

c. What is the profit or loss for the 12-week session if camp A operates c. What is the profit or loss for the 12-week session if camp A operates at 80% capacity?at 80% capacity?

d. Determine the breakeven number of campers for the two camps to d. Determine the breakeven number of campers for the two camps to have equal total costs for a 12-week session.have equal total costs for a 12-week session.

Camp ACharge per camper $120 per weekFixed costs $48,000 per sessionVariable cost per camper $80 per weekCapacity 200 campers

Camp BCharge per camper $100 per weekFixed costs $60,600 per sessionVariable cost per camper $50 per weekCapacity 150 campers

44

Time Value of MoneyTime Value of Money

Question:Question: Would you prefer $100 today or $120 after Would you prefer $100 today or $120 after 1 year? 1 year?

There is a There is a time value of moneytime value of money. . Money is a Money is a valuable asset, and people would pay to have money valuable asset, and people would pay to have money available for use. The charge for its use is called available for use. The charge for its use is called interest rateinterest rate. .

Question:Question: Why is the interest rate positive?Why is the interest rate positive?

Argument 1:Argument 1: Money is a valuable resource, which can be “rented,” Money is a valuable resource, which can be “rented,” similar to an apartment. Interest is a compensation for using similar to an apartment. Interest is a compensation for using money.money.

Argument 2:Argument 2: Interest is compensation for uncertainties related to Interest is compensation for uncertainties related to the future value of the money.the future value of the money.

55

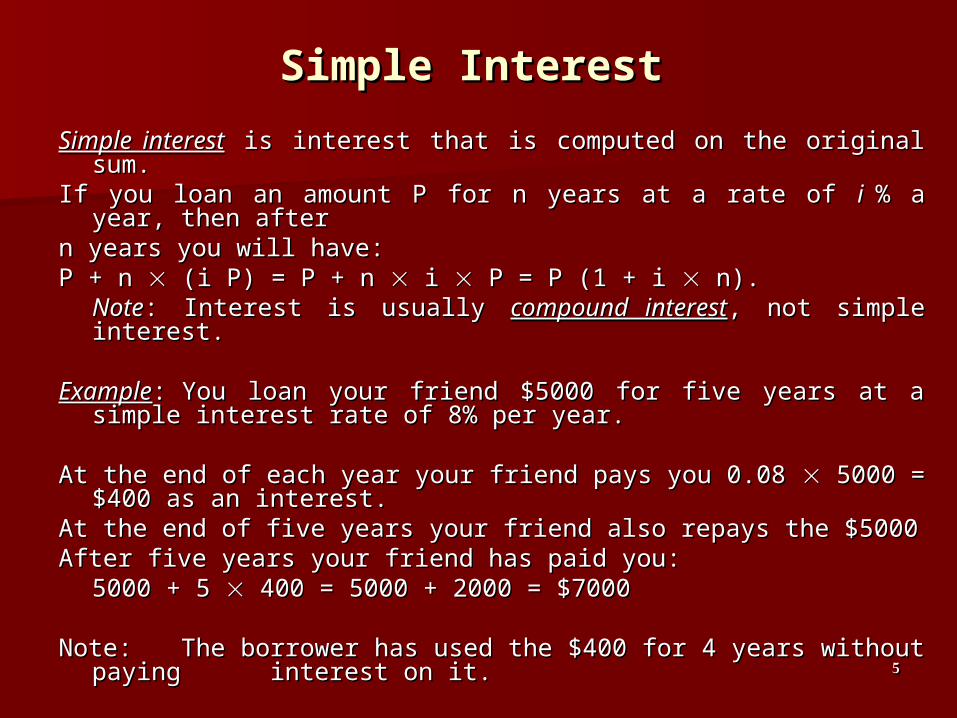

Simple InterestSimple Interest

Simple interestSimple interest is interest that is computed on the original sum. is interest that is computed on the original sum.If you loan an amount P for n years at a rate of If you loan an amount P for n years at a rate of i i % a year, then % a year, then

after after n years you will have: n years you will have: P + n P + n (i P) = P + n (i P) = P + n i i P = P (1 + i P = P (1 + i n).n).

NoteNote: Interest is usually : Interest is usually compound interestcompound interest, not simple , not simple interest.interest.

ExampleExample: You loan your friend $5000 for five years at a simple : You loan your friend $5000 for five years at a simple interest rate of 8% per year. interest rate of 8% per year.

At the end of each year your friend pays you 0.08 At the end of each year your friend pays you 0.08 5000 = 5000 = $400 as an interest. $400 as an interest.

At the end of five years your friend also repays the $5000At the end of five years your friend also repays the $5000After five years your friend has paid you: After five years your friend has paid you:

5000 + 5 5000 + 5 400 = 5000 + 2000 = $7000 400 = 5000 + 2000 = $7000

Note:Note: The borrower has used the $400 for 4 years without The borrower has used the $400 for 4 years without paying paying interest on it.interest on it.

66

Compound InterestCompound Interest

Compounded interestCompounded interest is interest that is charged on the is interest that is charged on the original sum and un-paid interest.original sum and un-paid interest.

You put $500 in a bank for 3 years at 6% compound You put $500 in a bank for 3 years at 6% compound interest per year.interest per year.

At the end of year 1 you have (1.06) At the end of year 1 you have (1.06) 500 = $530. 500 = $530. At the end of year 2 you have (1.06) At the end of year 2 you have (1.06) 530 = $561.80. 530 = $561.80. At the end of year 3 you have (1.06) At the end of year 3 you have (1.06) $561.80 = $561.80 =

$595.51. $595.51.

Note: Note: $595.51 = (1.06) $595.51 = (1.06) 561.80 561.80 = (1.06) (1.06) 530 = (1.06) (1.06) 530 = (1.06) (1.06) (1.06) 500 = 500 (1.06)= (1.06) (1.06) (1.06) 500 = 500 (1.06)33

77

Single Payment Compound Single Payment Compound FormulaFormula

If you put P in the bank now at an interest rate of If you put P in the bank now at an interest rate of ii for for nn years, years,

the the future amountfuture amount you will have after n years is given by: you will have after n years is given by:

F = P (1+i)F = P (1+i)nn

The term (1+i)The term (1+i)n n is called the is called the single payment compound single payment compound factorfactor..

The factor is used to compute F, The factor is used to compute F, givengiven P, and given P, and given ii and and nn..

Handy Notation. Handy Notation.

(F/P,i,n) = (1+i)(F/P,i,n) = (1+i)nn

F = P (1+i)F = P (1+i)nn = P (F/P,i,n) = P (F/P,i,n)

88

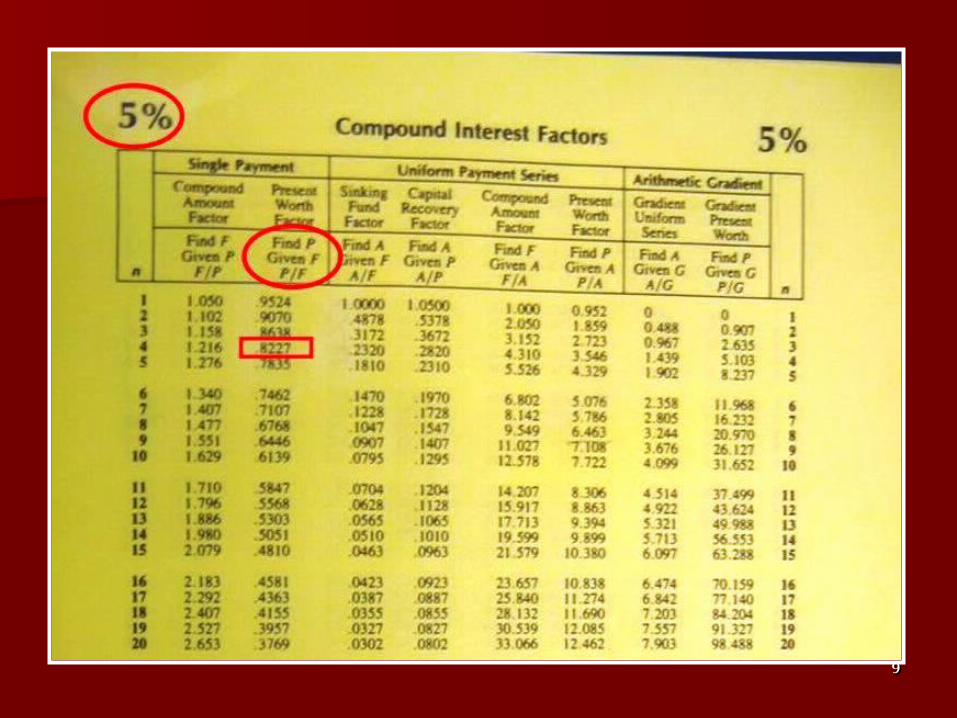

Present ValuePresent Value

ExampleExample If you want to have $800 in savings at the end If you want to have $800 in savings at the end

of four years, and 5% interest is paid of four years, and 5% interest is paid annually, how much do you need to put into annually, how much do you need to put into the savings account today?the savings account today?

We solve P (1+i)We solve P (1+i)nn = F for P with i = 0.05, n = 4, F = $800 = F for P with i = 0.05, n = 4, F = $800 P P = F/(1+i)= F/(1+i)nn = F(1+i) = F(1+i)-n-n ( P = F (P/F,i,n) ) ( P = F (P/F,i,n) )

= 800/(1.05)= 800/(1.05)44 = 800 (1.05) = 800 (1.05)-4-4 = 800 (0.8227) = $658.16 = 800 (0.8227) = $658.16

Single Payment Present Worth FormulaSingle Payment Present Worth Formula

P = F/(1+i)P = F/(1+i)nn = F(1+i) = F(1+i)-n-n

99

1010

Present ValuePresent Value

ExampleExample: You borrowed $5,000 from a bank at 8% interest : You borrowed $5,000 from a bank at 8% interest rate and you have to pay it back in 5 years. There are rate and you have to pay it back in 5 years. There are many ways the debt can be repaid.many ways the debt can be repaid.

Plan APlan A: At end of each year pay $1,000 principal : At end of each year pay $1,000 principal

plus interest due.plus interest due.Plan BPlan B: Pay interest due at end of each year and : Pay interest due at end of each year and

principal at end of five years.principal at end of five years.Plan CPlan C: Pay in five end-of-year payments.: Pay in five end-of-year payments.Plan DPlan D: Pay principal and interest in one payment : Pay principal and interest in one payment

at end of five years.at end of five years.

1111

ExampleExample

Plan APlan A: At end of each year pay $1,000 : At end of each year pay $1,000 principal plus interest due.principal plus interest due.

aa bb cc dd ee ff

YearYear

AmntAmnt..OwedOwed

Int. Int. OwedOwed

Total Total OwedOwed PrincipPrincip..

PaymenPaymentt

TotalTotalPaymentPaymentint*bint*b b+cb+c

11 5,0005,000 400400 5,4005,400 1,0001,000 1,4001,400

22 4,0004,000 320320 4,3204,320 1,0001,000 1,3201,320

33 3,0003,000 240240 3,2403,240 1,0001,000 1,2401,240

44 2,0002,000 160160 2,1602,160 1,0001,000 1,1601,160

55 1,0001,000 8080 1,0801,080 1,0001,000 1,0801,080

SUMSUM 15,00015,000 1,2001,200 16,20016,200 5,0005,000 6,2006,200

1212

Example (cont'd)Example (cont'd)

Plan BPlan B: Pay interest due at end of each year : Pay interest due at end of each year and principal at end of five years.and principal at end of five years.

aa bb cc dd ee ff

YearYear

AmntAmnt..OwedOwed

Int. Int. OwedOwed

Total Total OwedOwed

PrincipPrincip..PaymenPaymen

ttTotalTotal

PaymentPaymentint*bint*b b+cb+c

11 5,0005,000 400400 5,4005,400 00 400400

22 5,0005,000 400400 5,4005,400 00 400400

33 5,0005,000 400400 5,4005,400 00 400400

44 5,0005,000 400400 5,4005,400 00 400400

55 5,0005,000 400400 5,4005,400 5,0005,000 5,4005,400

SUMSUM 25,00025,000 2,0002,000 27,00027,000 5,0005,000 7,0007,000

1313

Example (cont'd)Example (cont'd)

Plan CPlan C: Pay in five end-of-year payments.: Pay in five end-of-year payments.

aa bb cc dd ee ff

YearYear

AmntAmnt..OwedOwed

Int. Int. OwedOwed

Total Total OwedOwed PrincipPrincip..

PaymenPaymentt

TotalTotalPaymentPaymentint*bint*b b+cb+c

11 5,0005,000 400400 5,4005,400 852852 1,2521,252

22 4,1484,148 332332 4,4804,480 920920 1,2521,252

33 3,2273,227 258258 3,4853,485 994994 1,2521,252

44 2,2332,233 179179 2,4122,412 1,0741,074 1,2521,252

55 1,1601,160 9393 1,2521,252 1,1601,160 1,2521,252

SUMSUM 15,76815,768 1,2611,261 17,02917,029 5,0005,000 6,2616,261

1414

Example (cont'd)Example (cont'd)

Plan DPlan D: Pay principal and interest in one : Pay principal and interest in one payment at end of five years.payment at end of five years.

aa bb cc dd ee ff

YearYear

AmntAmnt..OwedOwed

Int. Int. OwedOwed

Total Total OwedOwed

PrincipPrincip..PaymenPaymen

ttTotalTotal

PaymentPaymentint*bint*b b+cb+c

11 5,0005,000 400400 5,4005,400 00 00

22 5,4005,400 432432 5,8325,832 00 00

33 5,8325,832 467467 6,2996,299 00 00

44 6,2996,299 504504 6,8026,802 00 00

55 6,8026,802 544544 7,3477,347 5,0005,000 7,3477,347

SUMSUM 29,33329,333 2,3472,347 31,68031,680 5,0005,000 7,3477,347

1515

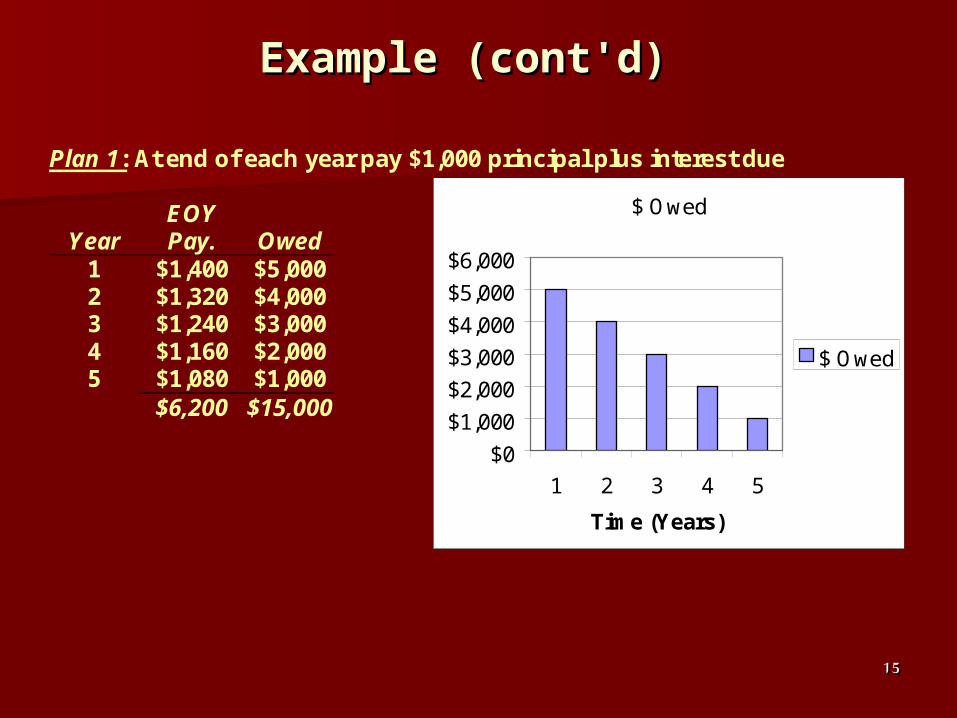

Example (cont'd)Example (cont'd)

Plan 1: At end of each year pay $1,000 principal plus interest due

Year EOY Pay. Owed

1 $1,400 $5,000 2 $1,320 $4,000 3 $1,240 $3,000 4 $1,160 $2,000 5 $1,080 $1,000

$6,200 $15,000

$ Owed

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

1 2 3 4 5

Time (Years)

$ Owed

1616

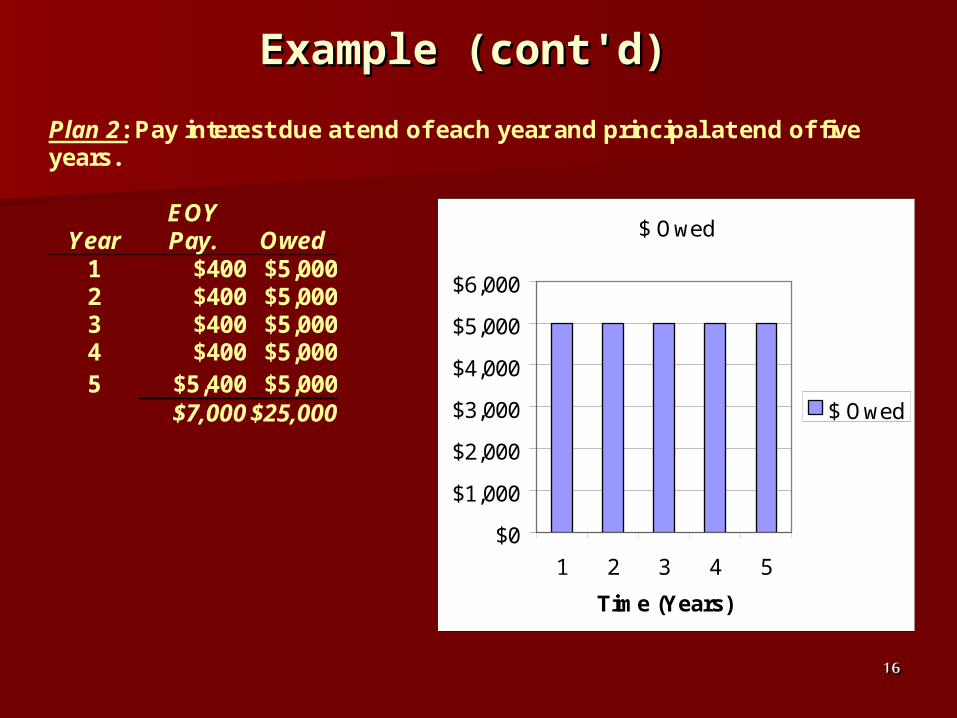

Example (cont'd)Example (cont'd)

Plan 2: Pay interest due at end of each year and principal at end of five years.

Year EOY Pay. Owed

1 $400 $5,000 2 $400 $5,000 3 $400 $5,000 4 $400 $5,000 5 $5,400 $5,000

$7,000 $25,000

$ Owed

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

1 2 3 4 5

Time (Years)

$ Owed

1717

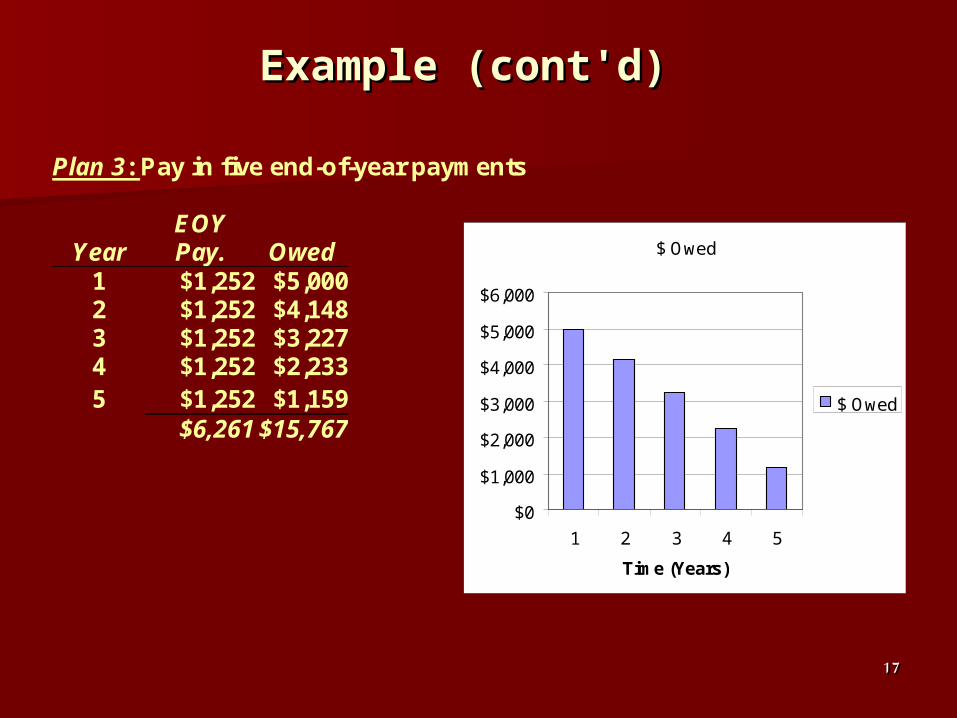

Example (cont'd)Example (cont'd)

Plan 3: Pay in five end-of-year payments

Year EOY Pay. Owed

1 $1,252 $5,000 2 $1,252 $4,148 3 $1,252 $3,227 4 $1,252 $2,233 5 $1,252 $1,159

$6,261 $15,767

$ Owed

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

1 2 3 4 5

Time (Years)

$ Owed

1818

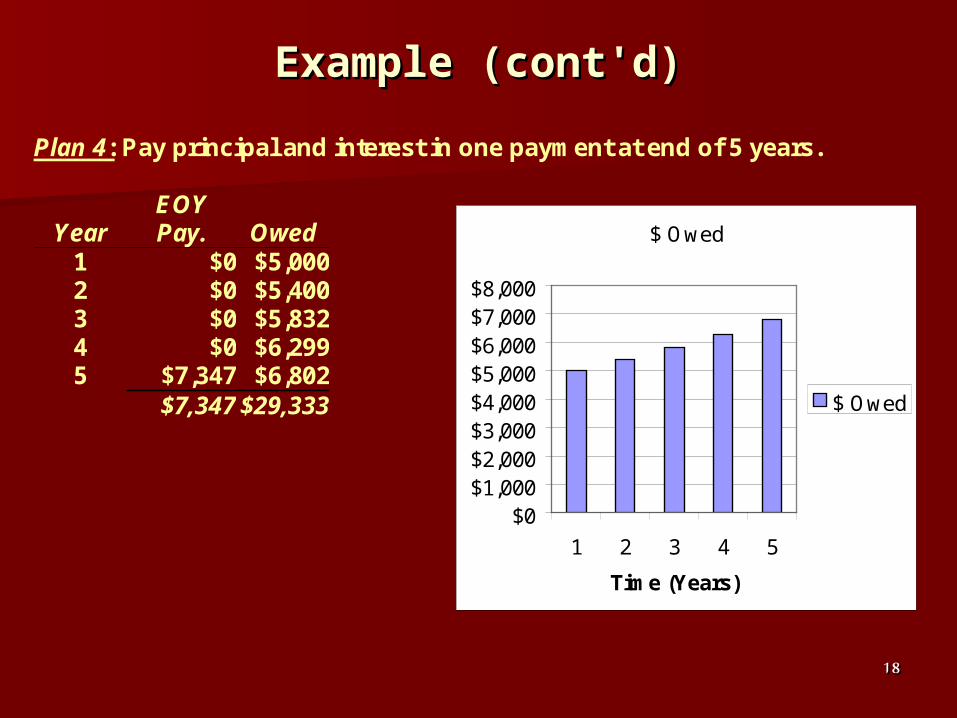

Example (cont'd)Example (cont'd)

Plan 4: Pay principal and interest in one payment at end of 5 years.

Year EOY Pay. Owed

1 $0 $5,000 2 $0 $5,400 3 $0 $5,832 4 $0 $6,299 5 $7,347 $6,802

$7,347 $29,333

$ Owed

$0$1,000$2,000$3,000$4,000$5,000$6,000$7,000$8,000

1 2 3 4 5

Time (Years)

$ Owed

1919

Example (cont'd)Example (cont'd)

Summary of Payment Plans (a) (b) (c) (d)

Plan Total Paid Tot. Int. Area under Ratio:

curve (b)/(c) 1 $6,200 $1,200 $15,000 0.08 2 $7,000 $2,000 $25,000 0.08 3 $6,261 $1,261 $15,767 0.08 4 $7,347 $2,347 $29,333 0.08

Question. What common property do all four plans have? interest rate = (total int. paid)/(area under curve)

or

total int. paid = (interest rate) * (area under curve) Since the areas under the curve vary for the 4 plans, but the interest rate does not, the total interest paid also varies.

2020

Quarterly Compounded Interest Quarterly Compounded Interest RatesRates

Example.Example. You put $500 in a bank for 3 years You put $500 in a bank for 3 years at 6% compound interest per year. Interest at 6% compound interest per year. Interest is is compounded quarterlycompounded quarterly. .

The bank pays you The bank pays you ii = 0.06/4 = 0.015 every 3 = 0.06/4 = 0.015 every 3 months; months; 1.5% for 12 periods (4 periods per year 1.5% for 12 periods (4 periods per year 3 3 years). years). At the end of three years you have: At the end of three years you have:

F F = P (1+i)= P (1+i)nn = 500 (1.015) = 500 (1.015)1212

= 500 (1.19562) = 500 (1.19562) $597.81 $597.81

Note.Note. Usually the stated interest is for a 1-year Usually the stated interest is for a 1-year period. If it is compounded quarterly then an period. If it is compounded quarterly then an interest period is 3 months long. If the interest is interest period is 3 months long. If the interest is i per year, each quarter the interest paid is i/4 i per year, each quarter the interest paid is i/4 since there are four 3-month periods a year.since there are four 3-month periods a year.

2121

Example.Example. In 3 years, you need $400 to pay a debt. In two In 3 years, you need $400 to pay a debt. In two more years, you need $600 more to pay a second debt. more years, you need $600 more to pay a second debt. How much should you put in the bank today to meet How much should you put in the bank today to meet these two needs if the bank pays 12% per year?these two needs if the bank pays 12% per year?

Interest is compounded yearlyInterest is compounded yearly

PP = 400(P/F,12%,3) + 600(P/F,12%,5) = 400(P/F,12%,3) + 600(P/F,12%,5) = 400 (0.7118) + 600 (0.5674) = 400 (0.7118) + 600 (0.5674) = 284.72 + 340.44 = $625.16= 284.72 + 340.44 = $625.16

Interest is compounded monthlyInterest is compounded monthly

P P = 400(P/F,12%/12,3*12) + 600(P/F,12%/12,5*12)= 400(P/F,12%/12,3*12) + 600(P/F,12%/12,5*12)= 400(P/F,1%,36) + 600(P/F,1%,60)= 400(P/F,1%,36) + 600(P/F,1%,60)= 400 (0.6989) + 600 (0.5504) = 400 (0.6989) + 600 (0.5504) = 279.56 + 330.24 = $609.80= 279.56 + 330.24 = $609.80

ExampleExample

2222

Borrower point of view:You borrow money Borrower point of view:You borrow money from the bank to start a business.from the bank to start a business.

Investors point of view:You invest your Investors point of view:You invest your money in a bank and buy a bond.money in a bank and buy a bond.

Year Cash Flow

0 - P 1 0 2 0 3 +400 4 0 5 +600

Year Cash Flow

0 + P 1 0 2 0 3 -400 4 0 5 -600

Example: Points of viewExample: Points of view

2323

The Blue Pages in the text book tabulate:The Blue Pages in the text book tabulate:

Compound Amount FactorCompound Amount Factor

(F/P,i,n) = (1+i)(F/P,i,n) = (1+i)nn

Present Worth FactorPresent Worth Factor

(P/F,i,n) = (1+i)(P/F,i,n) = (1+i)-n-n

These terms are in columns 2 and 3 in the These terms are in columns 2 and 3 in the illustrated factor sheet, identified as illustrated factor sheet, identified as

Compound Amount Factor:Compound Amount Factor: “Find F Given P: “Find F Given P: F/P” F/P”

Present Worth Factor:Present Worth Factor: “Find P Given F: P/F” “Find P Given F: P/F”

Concluding RemarksConcluding Remarks