05 b 51 Amalgamation

22

Amity School of Business 1 Amity School of Business BBA, Semester II Financial Accounting - II Ms. Kavitha Menon

-

Upload

utkarsh-sinha -

Category

Documents

-

view

221 -

download

0

Transcript of 05 b 51 Amalgamation

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 1/22

Amity School of Business

1

Amity School of Business

BBA, Semester II

Financial Accounting - II

Ms. Kavitha Menon

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 2/22

Amity School of Business

2

Module V

Amalgamation, Absorption

andReconstruction of Companies

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 3/22

Amity School of Business

3

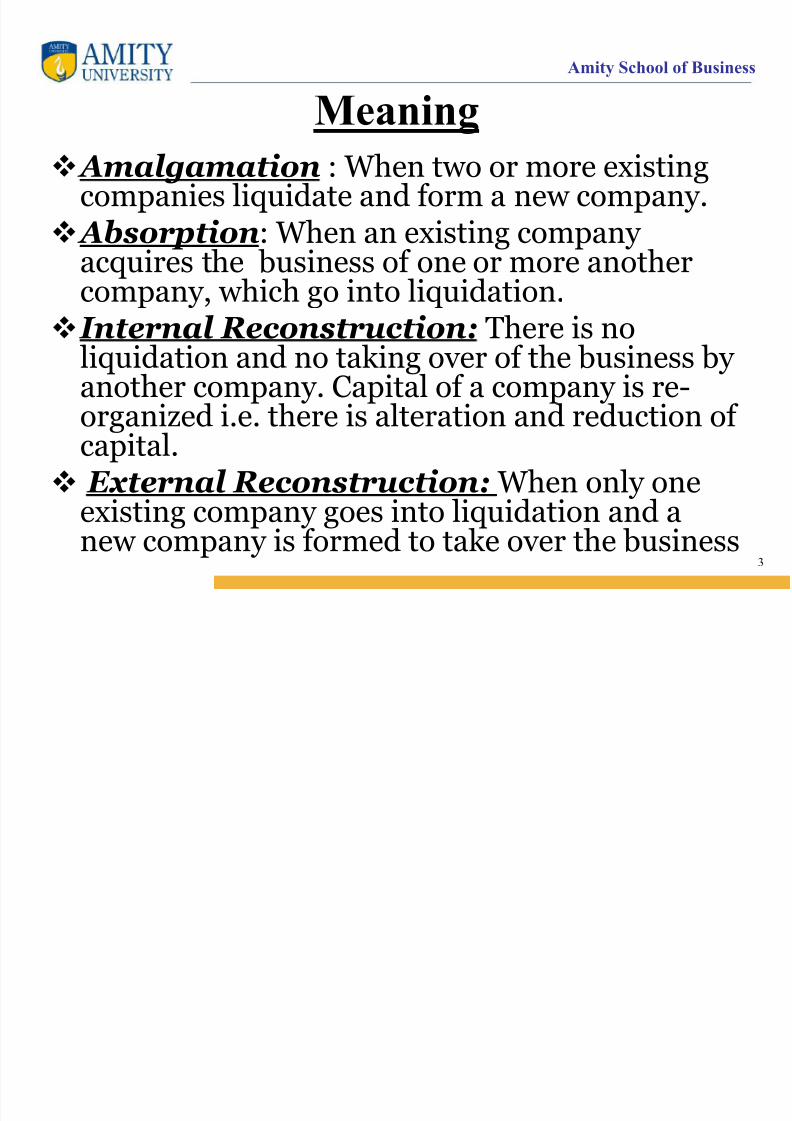

Meaning

Amalgamation : When two or more existingcompanies liquidate and form a new company.

Absorption: When an existing company

acquires the business of one or more anothercompany, which go into liquidation. Internal Reconstruction: There is no

liquidation and no taking over of the business by another company. Capital of a company is re-

organized i.e. there is alteration and reduction of capital.

External Reconstruction: When only oneexisting company goes into liquidation and a

new company is formed to take over the business

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 4/22

Amity School of Business

4

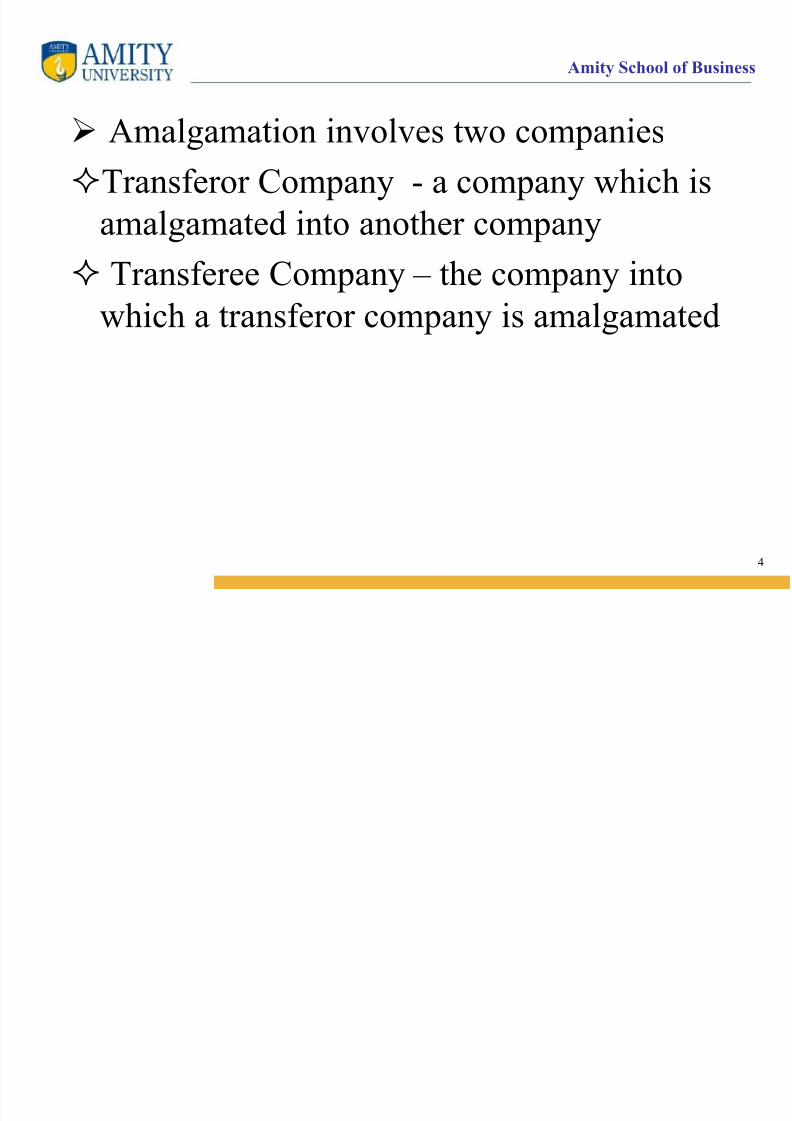

Amalgamation involves two companiesTransferor Company - a company which is

amalgamated into another company

Transferee Company – the company intowhich a transferor company is amalgamated

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 5/22

Amity School of Business

5

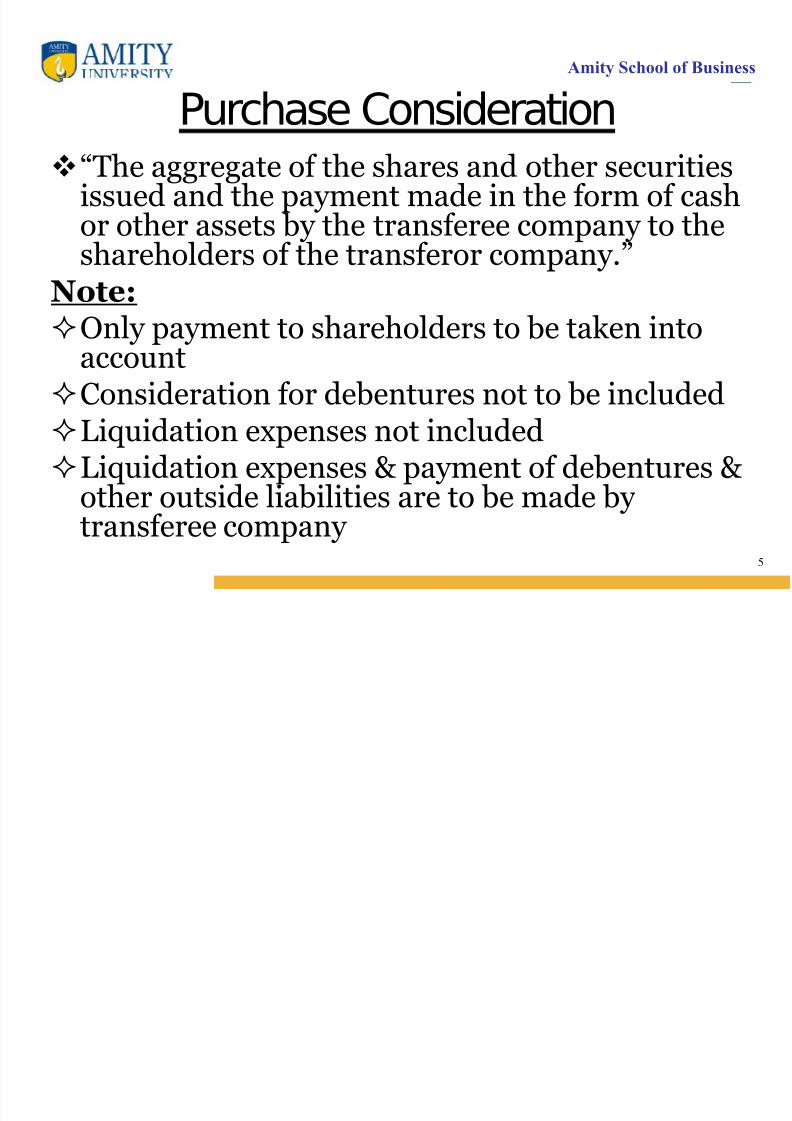

Purchase Consideration“The aggregate of the shares and other securities

issued and the payment made in the form of cashor other assets by the transferee company to theshareholders of the transferor company.”

Note:Only payment to shareholders to be taken into

accountConsideration for debentures not to be includedLiquidation expenses not includedLiquidation expenses & payment of debentures &

other outside liabilities are to be made by transferee company

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 6/22

Amity School of Business

6

Methods of calculating purchase consideration

Lump Sum Method

Net Payment Method Net Assets Method

Shares Exchange Method

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 7/22

Amity School of Business

7

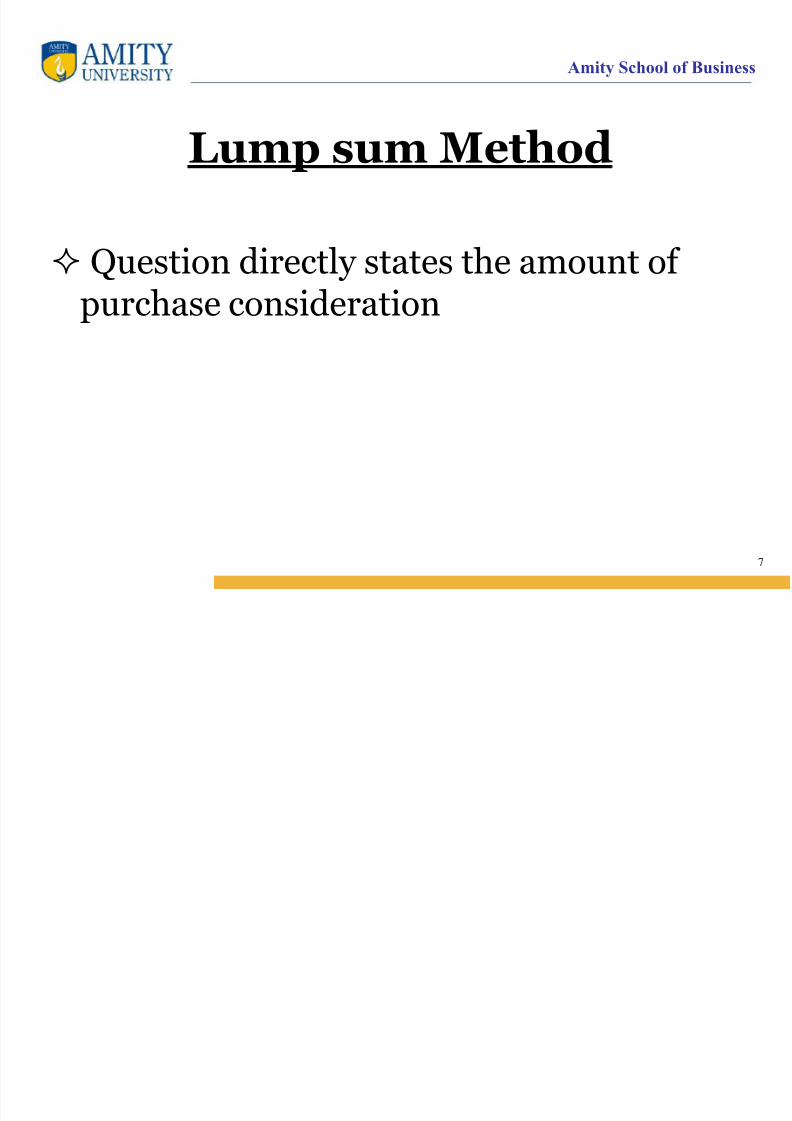

Lump sum Method

Question directly states the amount of purchase consideration

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 8/22

Amity School of Business

8

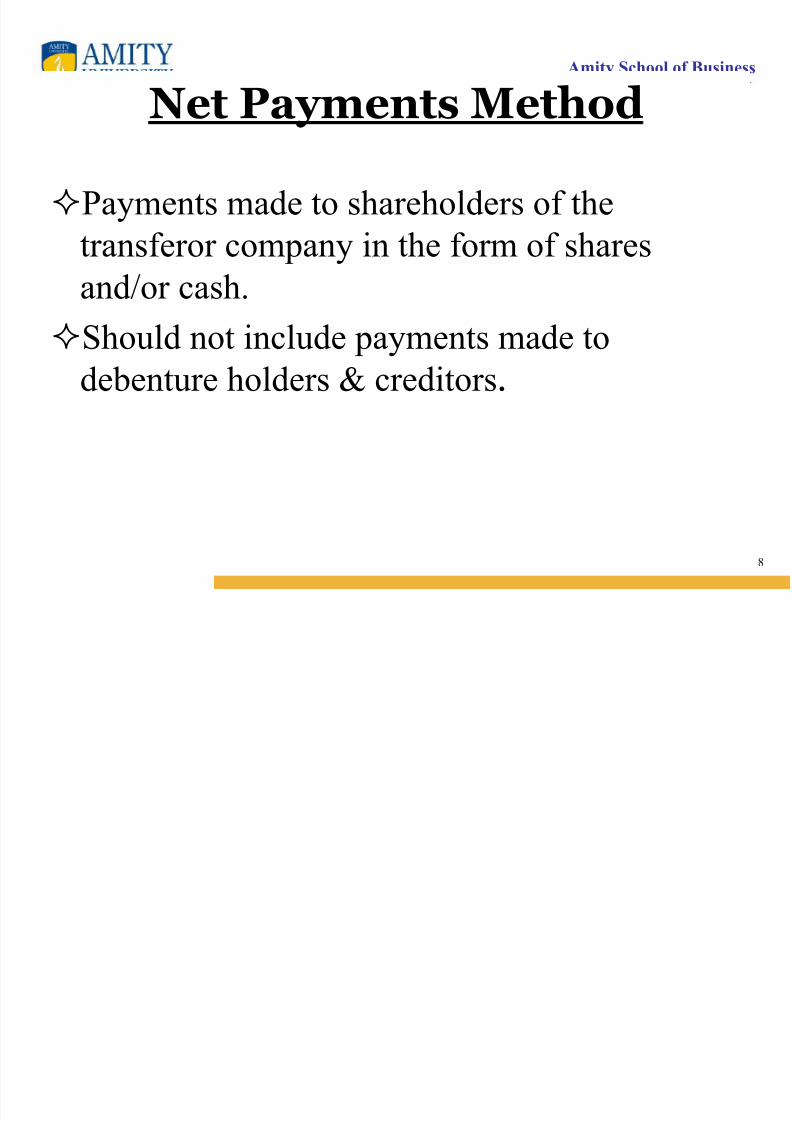

Net Payments Method

Payments made to shareholders of the

transferor company in the form of shares

and/or cash.

Should not include payments made to

debenture holders & creditors.

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 9/22

Amity School of Business

9

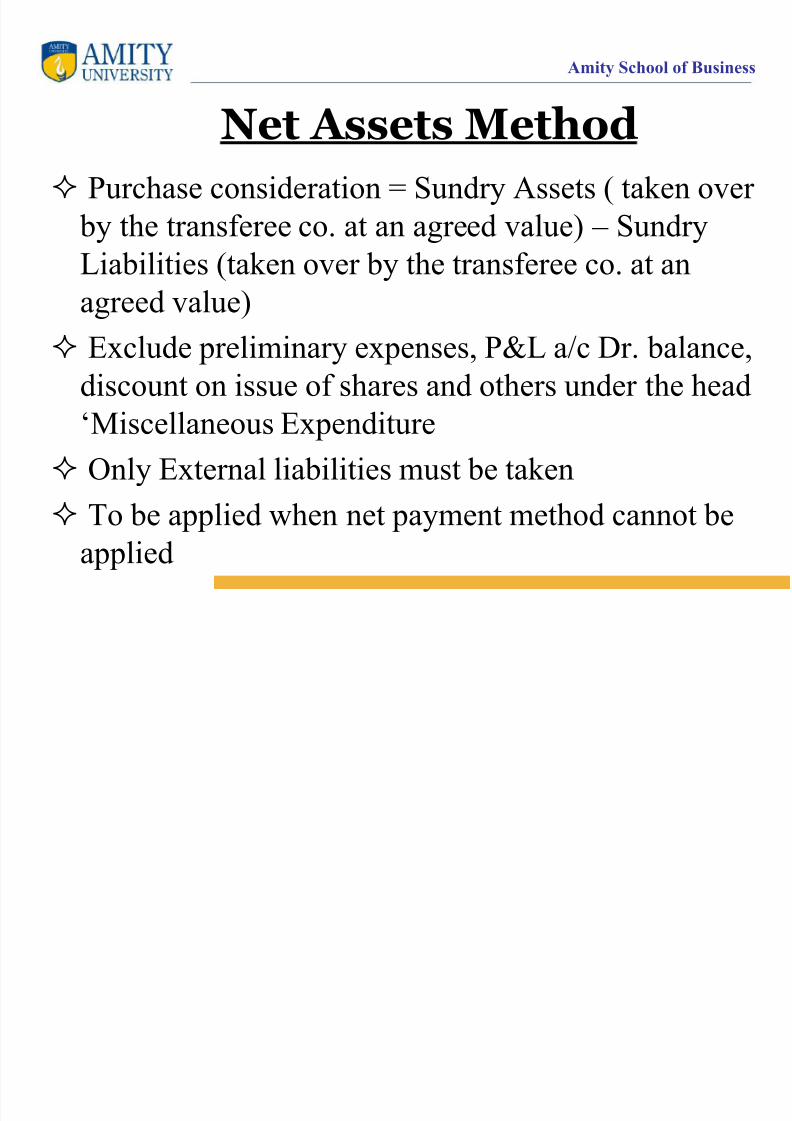

Purchase consideration = Sundry Assets ( taken over

by the transferee co. at an agreed value) – Sundry

Liabilities (taken over by the transferee co. at anagreed value)

Exclude preliminary expenses, P&L a/c Dr. balance,

discount on issue of shares and others under the head

‘Miscellaneous Expenditure

Only External liabilities must be taken

To be applied when net payment method cannot be

applied

Net Assets Method

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 10/22

Amity School of Business

10

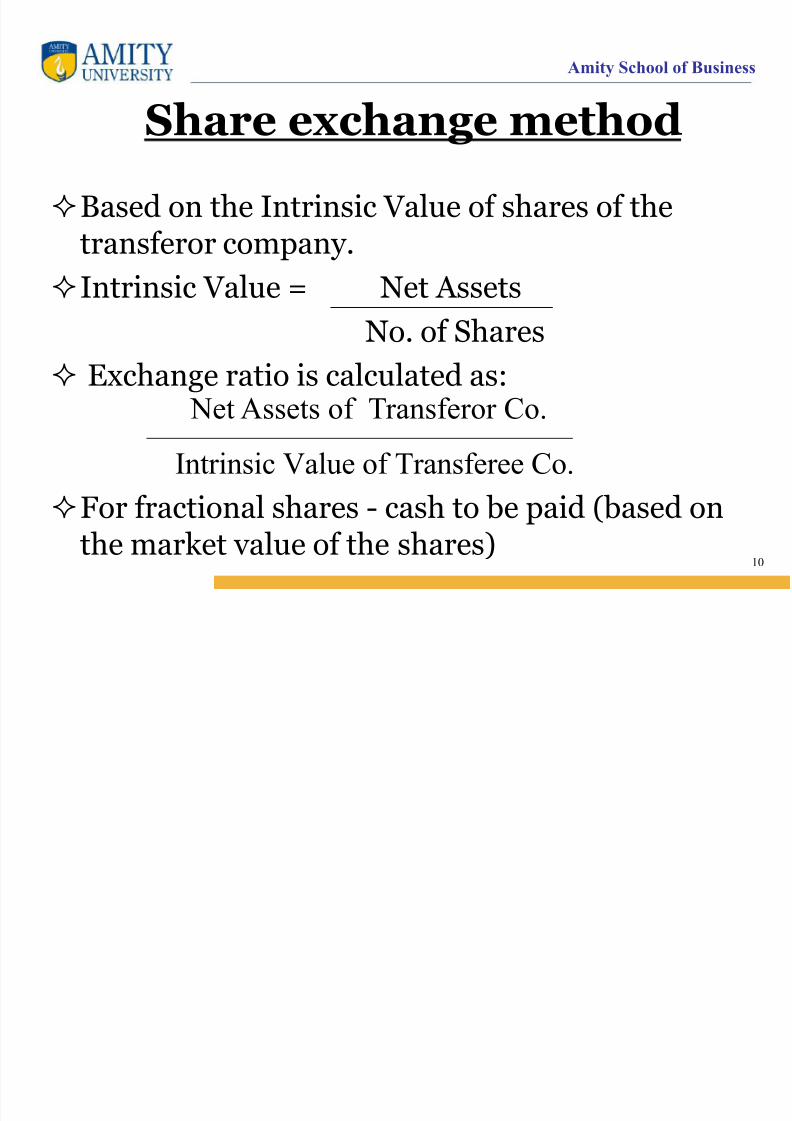

Share exchange methodBased on the Intrinsic Value of shares of the

transferor company.

Intrinsic Value = Net Assets

No. of Shares

Exchange ratio is calculated as:

For fractional shares - cash to be paid (based on

the market value of the shares)

Net Assets of Transferor Co.

Intrinsic Value of Transferee Co.

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 11/22

Amity School of Business

11

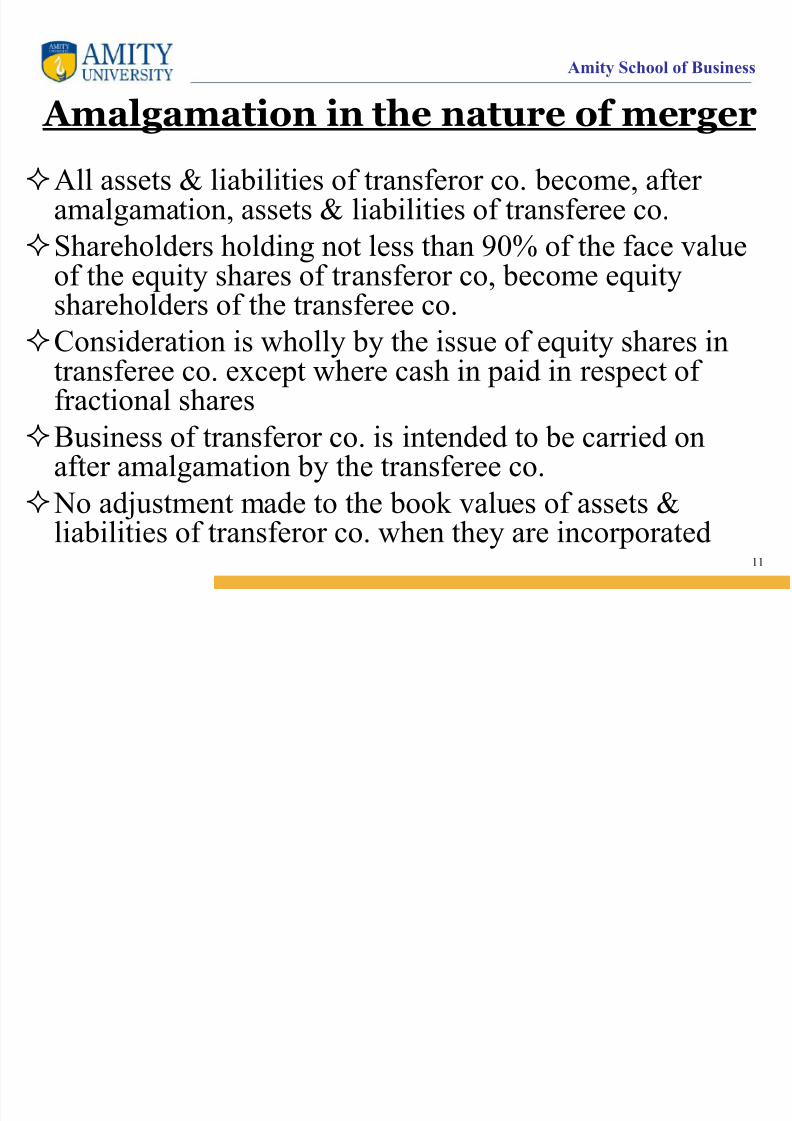

Amalgamation in the nature of merger

All assets & liabilities of transferor co. become, after amalgamation, assets & liabilities of transferee co.

Shareholders holding not less than 90% of the face value

of the equity shares of transferor co, become equityshareholders of the transferee co.

Consideration is wholly by the issue of equity shares intransferee co. except where cash in paid in respect of

fractional sharesBusiness of transferor co. is intended to be carried onafter amalgamation by the transferee co.

No adjustment made to the book values of assets &liabilities of transferor co. when they are incorporated

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 12/22

Amity School of Business

12

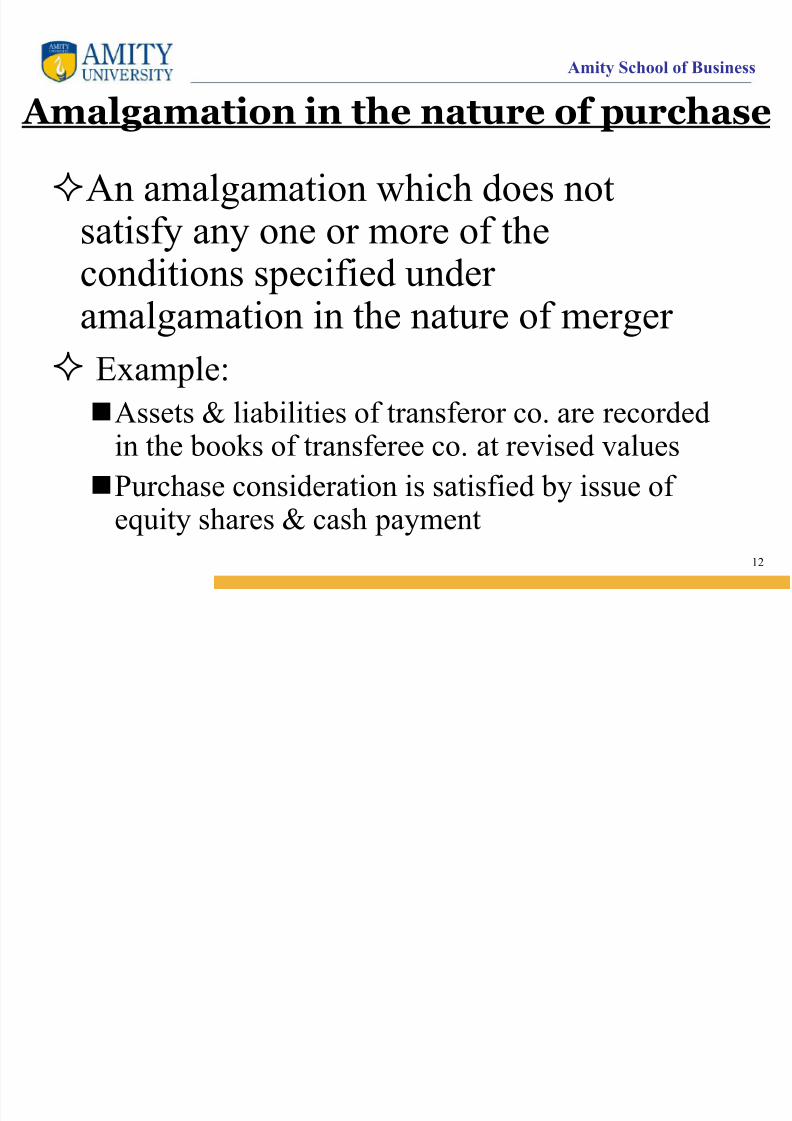

Amalgamation in the nature of purchase

An amalgamation which does notsatisfy any one or more of the

conditions specified under amalgamation in the nature of merger

Example:

Assets & liabilities of transferor co. are recordedin the books of transferee co. at revised values

Purchase consideration is satisfied by issue of equity shares & cash payment

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 13/22

Amity School of Business

13

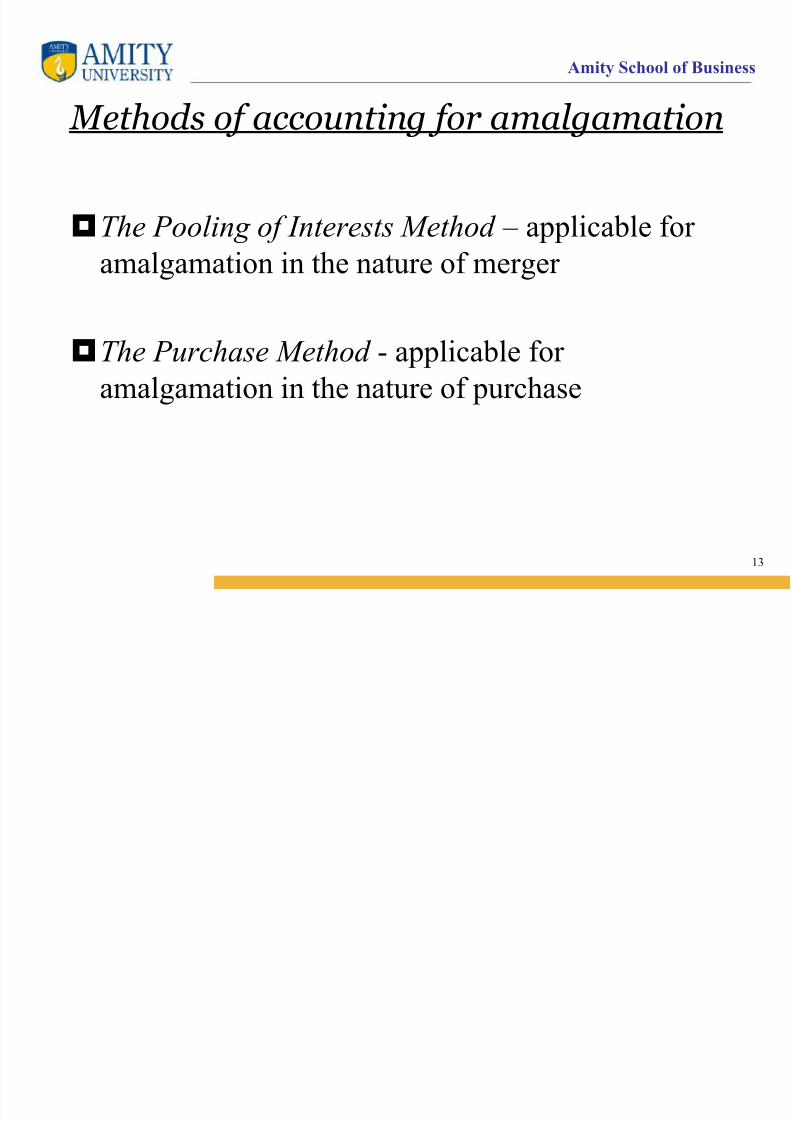

Methods of accounting for amalgamation

The Pooling of Interests Method – applicable for

amalgamation in the nature of merger

The Purchase Method - applicable for

amalgamation in the nature of purchase

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 14/22

Amity School of Business

14

Accounting treatment in thebooks of the transferor company

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 15/22

Amity School of Business

15

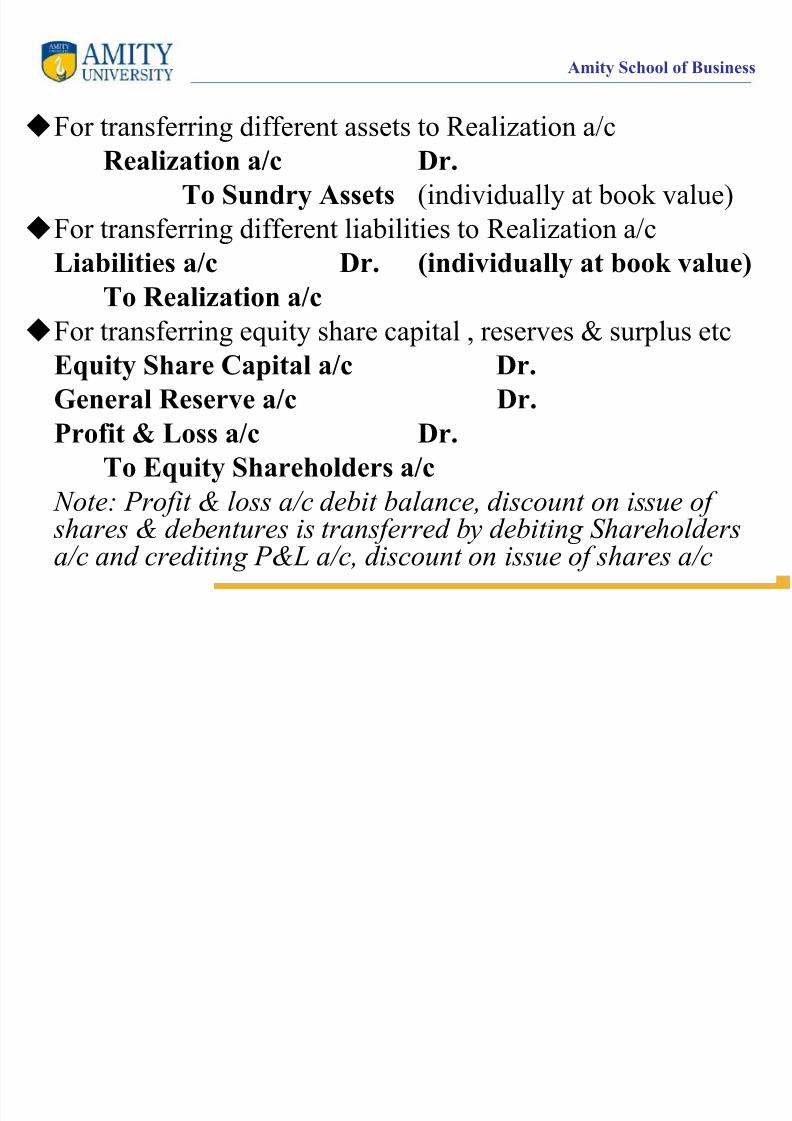

For transferring different assets to Realization a/cRealization a/c Dr.

To Sundry Assets (individually at book value)

For transferring different liabilities to Realization a/c

Liabilities a/c Dr. (individually at book value)

To Realization a/c

For transferring equity share capital , reserves & surplus etc

Equity Share Capital a/c Dr.

General Reserve a/c Dr.

Profit & Loss a/c Dr.

To Equity Shareholders a/c

Note: Profit & loss a/c debit balance, discount on issue of shares & debentures is transferred by debiting Shareholders

a/c and crediting P&L a/c, discount on issue of shares a/c

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 16/22

Amity School of Business

16

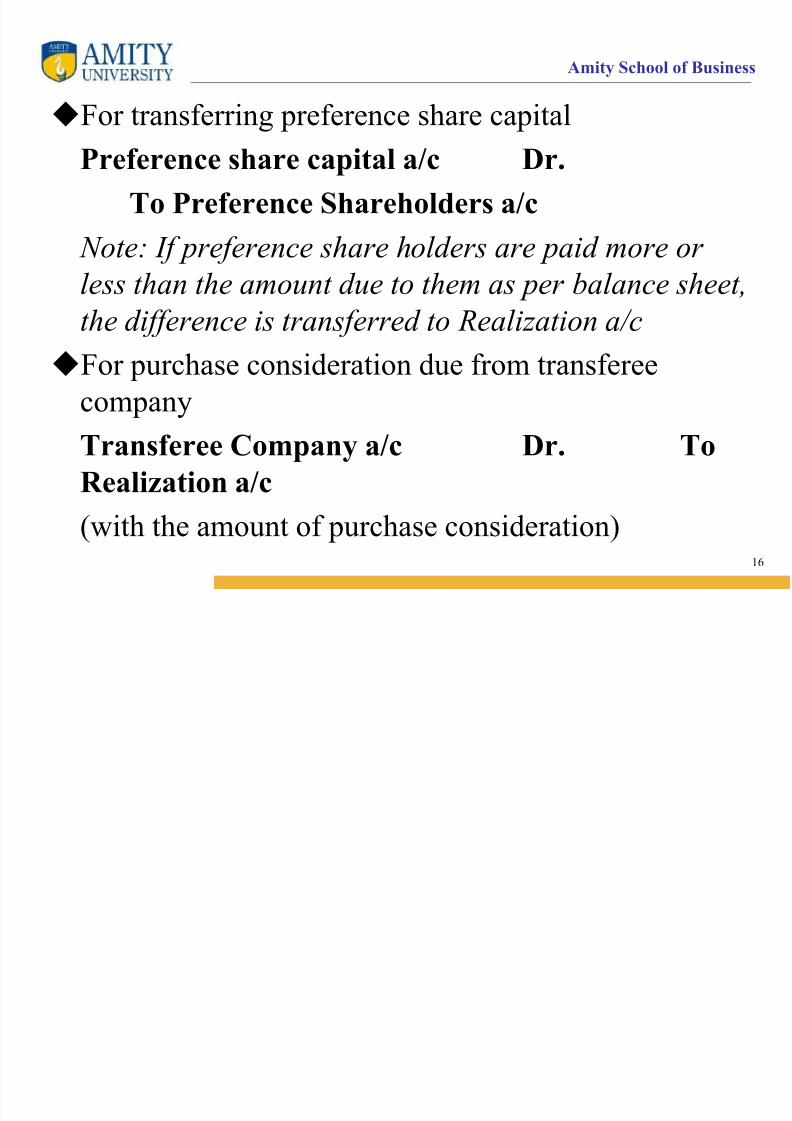

For transferring preference share capital

Preference share capital a/c Dr.

To Preference Shareholders a/c

Note: If preference share holders are paid more or

less than the amount due to them as per balance sheet,the difference is transferred to Realization a/c

For purchase consideration due from transferee

companyTransferee Company a/c Dr. To

Realization a/c

(with the amount of purchase consideration)

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 17/22

Amity School of Business

17

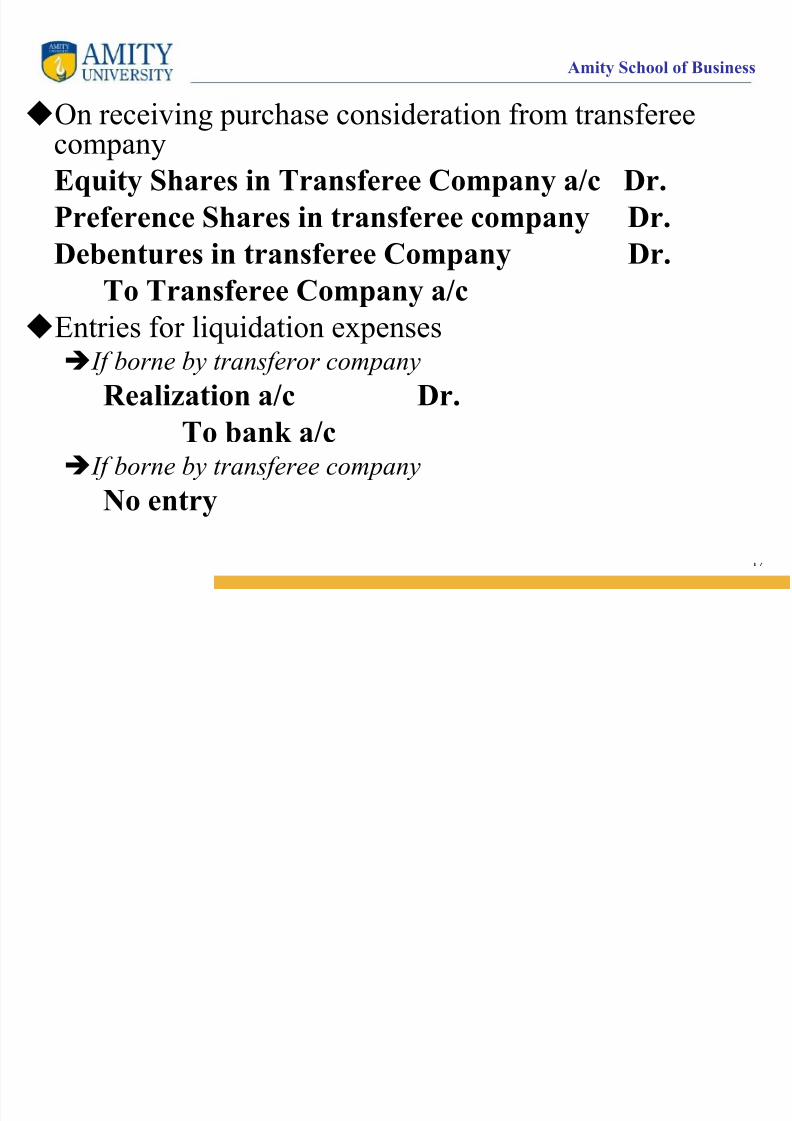

On receiving purchase consideration from transferee

companyEquity Shares in Transferee Company a/c Dr.

Preference Shares in transferee company Dr.

Debentures in transferee Company Dr.

To Transferee Company a/c

Entries for liquidation expenses If borne by transferor company

Realization a/c Dr.

To bank a/c If borne by transferee company

No entry

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 18/22

Amity School of Business

18

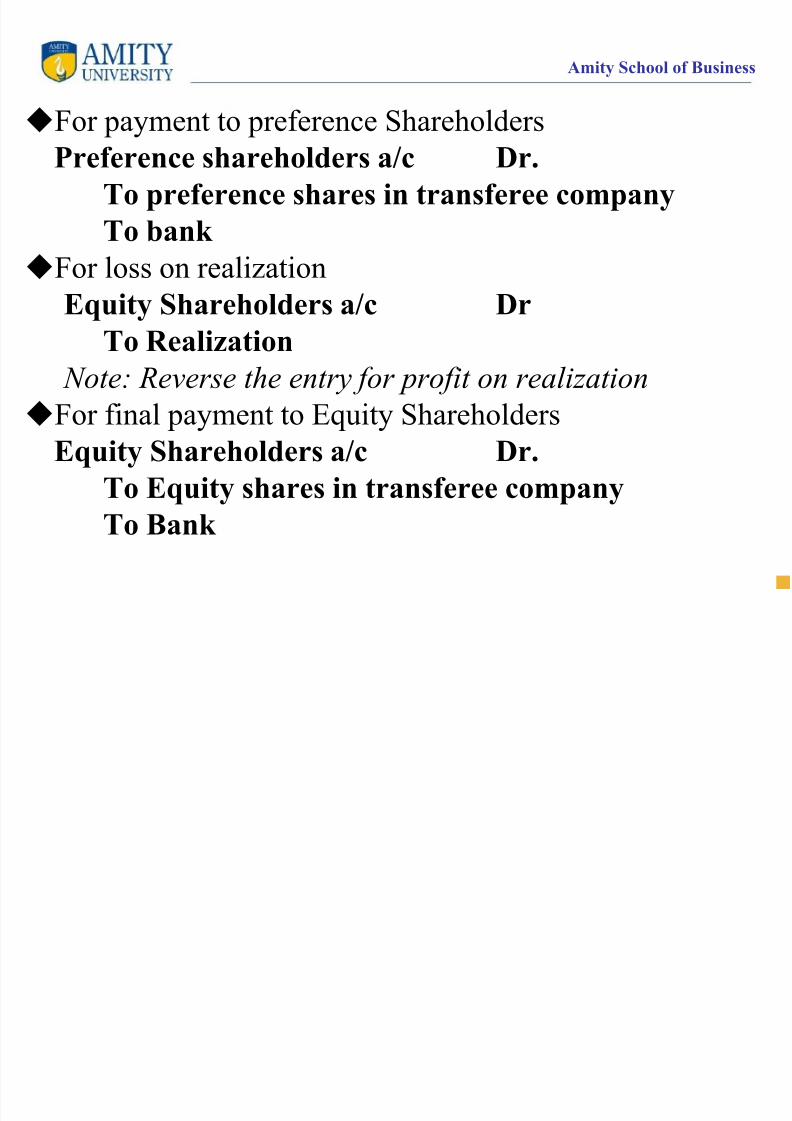

For payment to preference Shareholders

Preference shareholders a/c Dr.

To preference shares in transferee company

To bank

For loss on realizationEquity Shareholders a/c Dr

To Realization

Note: Reverse the entry for profit on realization

For final payment to Equity ShareholdersEquity Shareholders a/c Dr.

To Equity shares in transferee company

To Bank

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 19/22

Amity School of Business

19

Accounting treatment in thebooks of the transferee company

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 20/22

Amity School of Business

20

Pooling of Interest Method

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 21/22

Amity School of Business

21

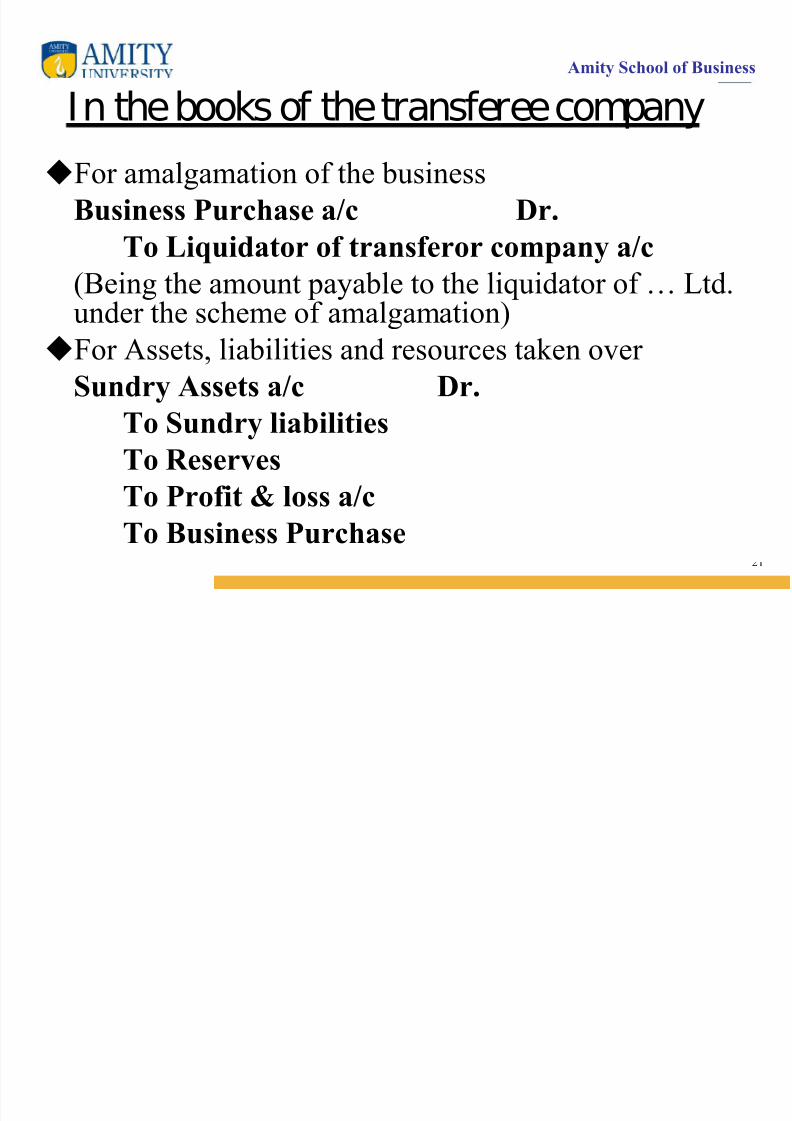

In the books of the transferee company

For amalgamation of the business

Business Purchase a/c Dr.

To Liquidator of transferor company a/c

(Being the amount payable to the liquidator of … Ltd.under the scheme of amalgamation)

For Assets, liabilities and resources taken over

Sundry Assets a/c Dr.

To Sundry liabilitiesTo Reserves

To Profit & loss a/c

To Business Purchase

7/29/2019 05 b 51 Amalgamation

http://slidepdf.com/reader/full/05-b-51-amalgamation 22/22

Amity School of Business

22

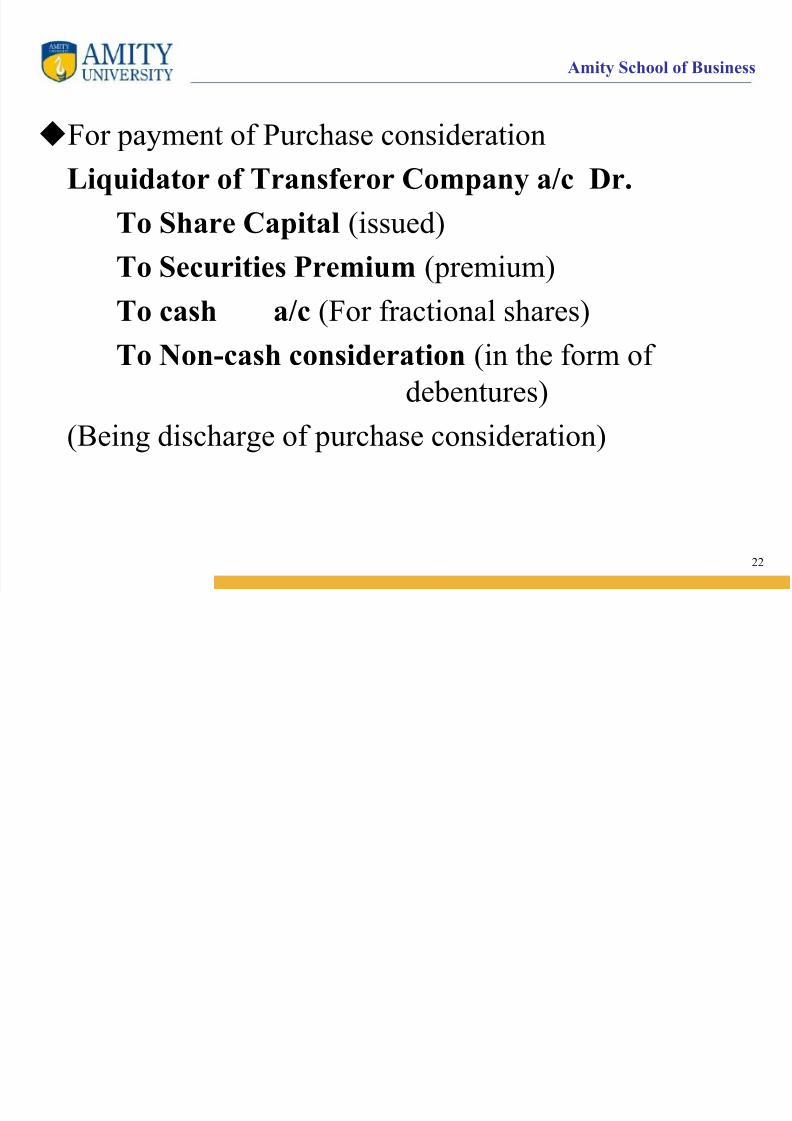

For payment of Purchase considerationLiquidator of Transferor Company a/c Dr.

To Share Capital (issued)

To Securities Premium (premium)To cash a/c (For fractional shares)

To Non-cash consideration (in the form of

debentures)

(Being discharge of purchase consideration)