企業永續成長的競爭力 -從 ... - proj.ftis.org.tw · © 2012 勤業眾信版權所有...

23

© 2012 勤業眾信版權所有 保留一切權利 企業永續成長的競爭力 -從企業社會責任創造競爭優勢 永續經營服務團隊 企業風險服務部門 勤業眾信聯合會計師事務所 2012 / 5

Transcript of 企業永續成長的競爭力 -從 ... - proj.ftis.org.tw · © 2012 勤業眾信版權所有...

© 2012 勤業眾信版權所有 保留一切權利

企業永續成長的競爭力 -從企業社會責任創造競爭優勢 永續經營服務團隊

企業風險服務部門

勤業眾信聯合會計師事務所

2012 / 5

© 2012 勤業眾信版權所有 保留一切權利

報告大綱

企業為何需要企業社會責任

企業社會責任簡介

企業社會責任推動力

如何推動企業社會責任

結語

Q&A

© 2012 勤業眾信版權所有 保留一切權利

企業為何需要企業社會責任

© 2012 勤業眾信版權所有 保留一切權利

企業的責任是….

4

企業非賺錢不可,賺錢非成長不可,成長非創新不可, 創新非要人才不可,人才非要品德不可。

高希均教授

企業家最大及唯一的責任,就是賺錢。 企業的社會責任就是幫股東賺錢。

諾貝爾經濟奬得主 傅利曼教授

© 2012 勤業眾信版權所有 保留一切權利

社會公益的實踐-Timberland

落實社會回饋

的企業先鋒

• Path of Service(服務途徑)」計畫-藉由給於員工有薪假期,從事社區服務,實際回饋社會。

• 藉由社會回饋,提高員工對於企業之認同。

非營利團體合作

之永續整合策略

• 藉由與義工團體(City

Year)之長期合作,除提供社會服務之外,更於其組織內,建立永續發展部門,負責其永續相關之規劃與執行。

詳細且確實的成分標示

• Timberland鞋類產品,均有精確的產品成分標籤,完整列出產品對環保的影響、對社區的影響及產品製造地。

• 贏得消費者信賴

• 提高公司聲譽

• 良好的員工關係

• 吸引人才-連續9年選為「前一百家最想進入的公司」

成效

5

© 2012 勤業眾信版權所有 保留一切權利

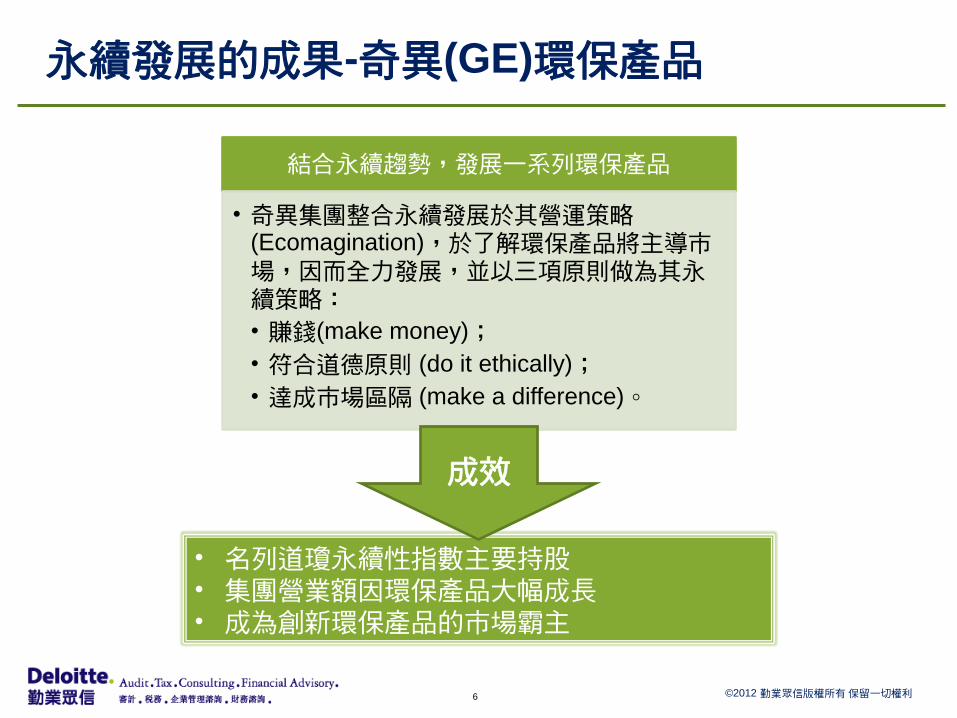

永續發展的成果-奇異(GE)環保產品

結合永續趨勢,發展一系列環保產品

• 奇異集團整合永續發展於其營運策略(Ecomagination),於了解環保產品將主導市場,因而全力發展,並以三項原則做為其永續策略:

• 賺錢(make money);

• 符合道德原則 (do it ethically);

• 達成市場區隔 (make a difference)。

• 名列道瓊永續性指數主要持股

• 集團營業額因環保產品大幅成長

• 成為創新環保產品的市場霸主

成效

6

© 2012 勤業眾信版權所有 保留一切權利 7

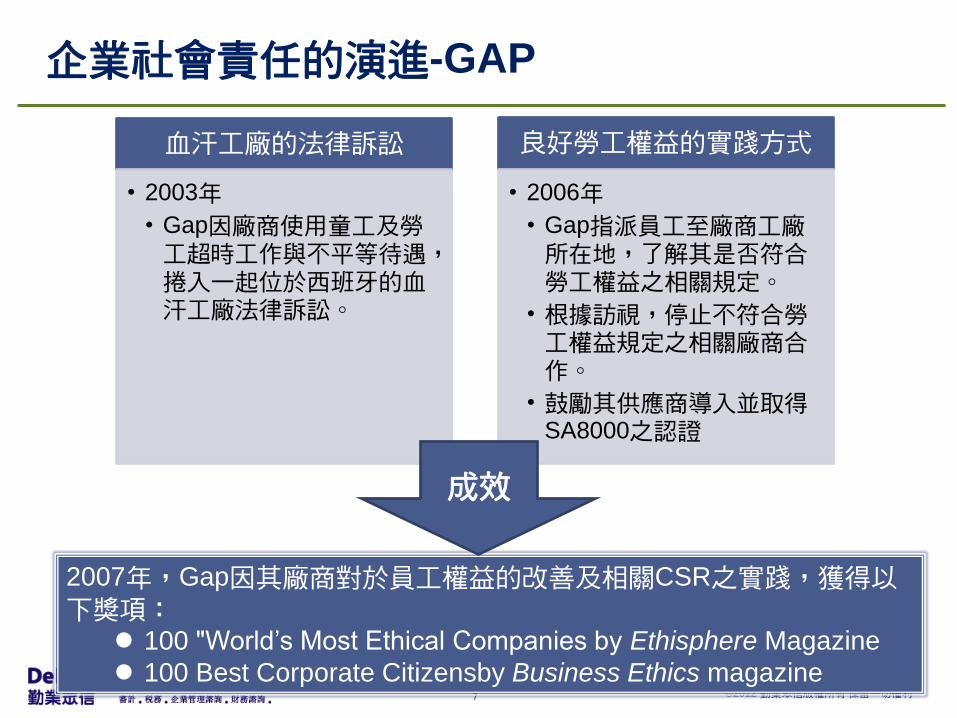

血汗工廠的法律訴訟

• 2003年

• Gap因廠商使用童工及勞工超時工作與不平等待遇,捲入一起位於西班牙的血汗工廠法律訴訟。

良好勞工權益的實踐方式

• 2006年

• Gap指派員工至廠商工廠所在地,了解其是否符合勞工權益之相關規定。

• 根據訪視,停止不符合勞工權益規定之相關廠商合作。

• 鼓勵其供應商導入並取得SA8000之認證

企業社會責任的演進-GAP

2007年,Gap因其廠商對於員工權益的改善及相關CSR之實踐,獲得以下獎項:

100 "World‟s Most Ethical Companies by Ethisphere Magazine

100 Best Corporate Citizensby Business Ethics magazine

成效

© 2012 勤業眾信版權所有 保留一切權利

企業社會責任簡介

企業社會責任定義

企業社會的範圍

企業社會責任規範或倡議

企業社會責任報告書-成果表現

© 2012 勤業眾信版權所有 保留一切權利

企業社會責任/企業永續發展:

Corporate Social Responsibility

& Sustainability (CSR) 企業社會責任定義

經濟

社會

CSR 三重底線

環境

永續發展不單只是“綠化”,而是確保企業的長期生存的能力。

Deloitte Global對於企業社會責任之定義:

企業透過商業運作之持續改善,並經由對環境、社會的敏銳度,以及充分呈現消費者、客戶、商業夥伴與社會大眾,所關注的議題之表現績效,確保企業能夠永續取得經營所需之資源。

9

© 2012 勤業眾信版權所有 保留一切權利

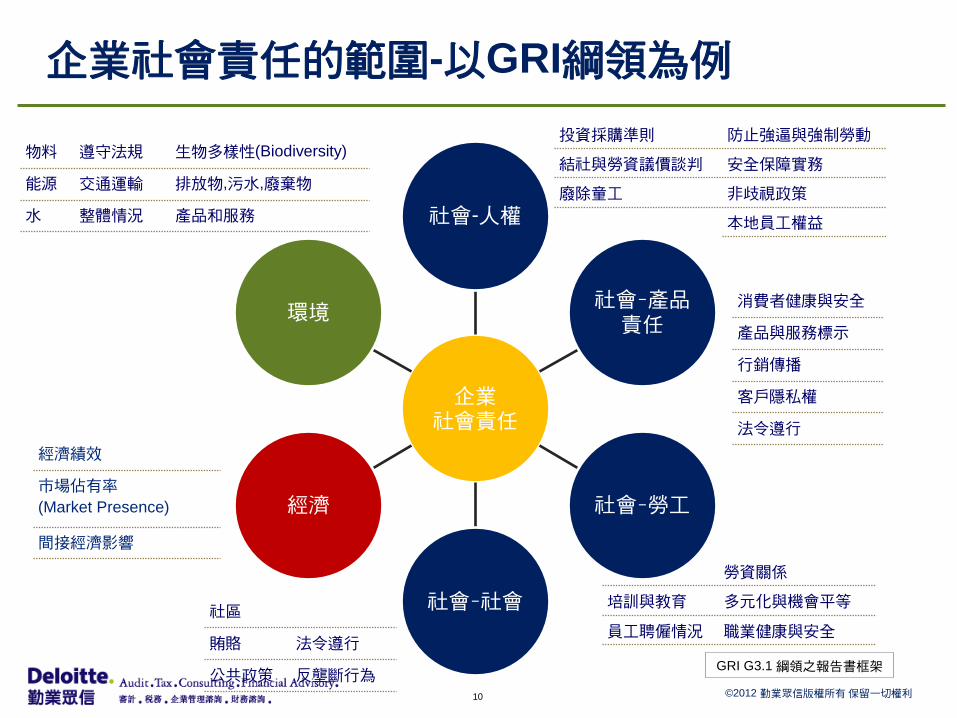

企業社會責任的範圍-以GRI綱領為例

企業 社會責任

社會-人權

社會-產品 責任

社會-勞工

社會-社會

經濟

環境

物料 遵守法規 生物多樣性(Biodiversity)

能源 交通運輸 排放物,污水,廢棄物

水 整體情況 產品和服務

經濟績效

市場佔有率

(Market Presence)

間接經濟影響

消費者健康與安全

產品與服務標示

行銷傳播

客戶隱私權

法令遵行

投資採購準則 防止強逼與強制勞動

結社與勞資議價談判 安全保障實務

廢除童工 非歧視政策

本地員工權益

勞資關係

培訓與教育 多元化與機會平等

員工聘僱情況 職業健康與安全 社區

賄賂 法令遵行

公共政策 反壟斷行為 GRI G3.1 綱領之報告書框架

10

© 2012 勤業眾信版權所有 保留一切權利 11

企業社會責任規範或倡議 CSR已成為國際間逐漸正視的議題,許許多多相關之規範或倡議,對於永續或環境、社會、經濟議題,提出建議作為,以下是較為企業所熟知之倡議或規範:

CSR相關倡議或國際標準

經濟合作暨發展組織多國企業指導

綱領

聯合國全球盟約 / 全球蘇利文原則

全球永續報告協會綱領/ 社會責任當則標準 AA 1000系列 SA 8000 /

國際勞工組織(ILO)各號

公約

ISO 14000環境系列

ISO 26000 社會責任指

引

© 2012 勤業眾信版權所有 保留一切權利 12

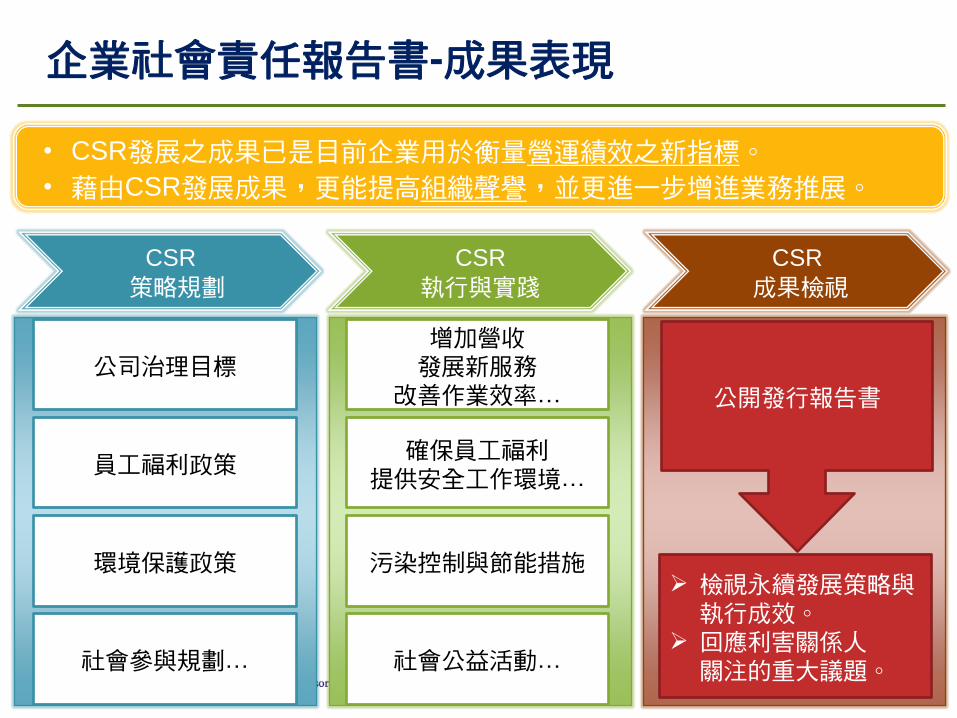

企業社會責任報告書-成果表現

公司治理目標

員工福利政策

CSR

策略規劃

公開發行報告書

CSR

成果檢視

增加營收

發展新服務

改善作業效率…

確保員工福利

提供安全工作環境…

CSR

執行與實踐

污染控制與節能措施 環境保護政策

社會公益活動… 社會參與規劃…

檢視永續發展策略與執行成效。

回應利害關係人

關注的重大議題。

• CSR發展之成果已是目前企業用於衡量營運績效之新指標。

• 藉由CSR發展成果,更能提高組織聲譽,並更進一步增進業務推展。

© 2012 勤業眾信版權所有 保留一切權利

企業社會責任推動力

© 2012 勤業眾信版權所有 保留一切權利 14

CSR 全球趨勢與驅動力

•企業對於永續發展不在只是遵守(Compliance),應為自發性於營運作業中實踐。

•股東、客戶、員工等利害關係人對於對於永續發展之要求與日俱增。

•各國不斷透過政策與法令的推行,激勵企業減少碳排放量。

•新興的貿易措施及稅收措施,鼓勵減少廢棄物產生,並重新賦予廢棄物新價值。

•永續發展策略已逐漸成為企業認同的價值主因之一。

•企業永續發展為整體檢視組織健全性與穩定發展的指標。

法令與規範對於CSR議題日趨重視

CSR規劃與執行

成為企業最急迫

的策略與行動需求

消費者要求企業負起更多社會責任及更具體的成效表現

對於環境與資源

保護的強大聲浪

•愈來愈多新節能高效的產品與方案研究結果,協助企業於永續發展的規劃與實踐。

•再生能源 (e.g.太陽能,風能)的發展,協助企業增加產能供給並減少營運成本。

科技的發展加速

永續發展的考量

•除現今已存在的法令規範外,未來更預期會出現對於環境或氣候相關的法規及準則,將對於企業之產品與服務於創新上,帶來新的機會與挑戰。

© 2012 勤業眾信版權所有 保留一切權利 15

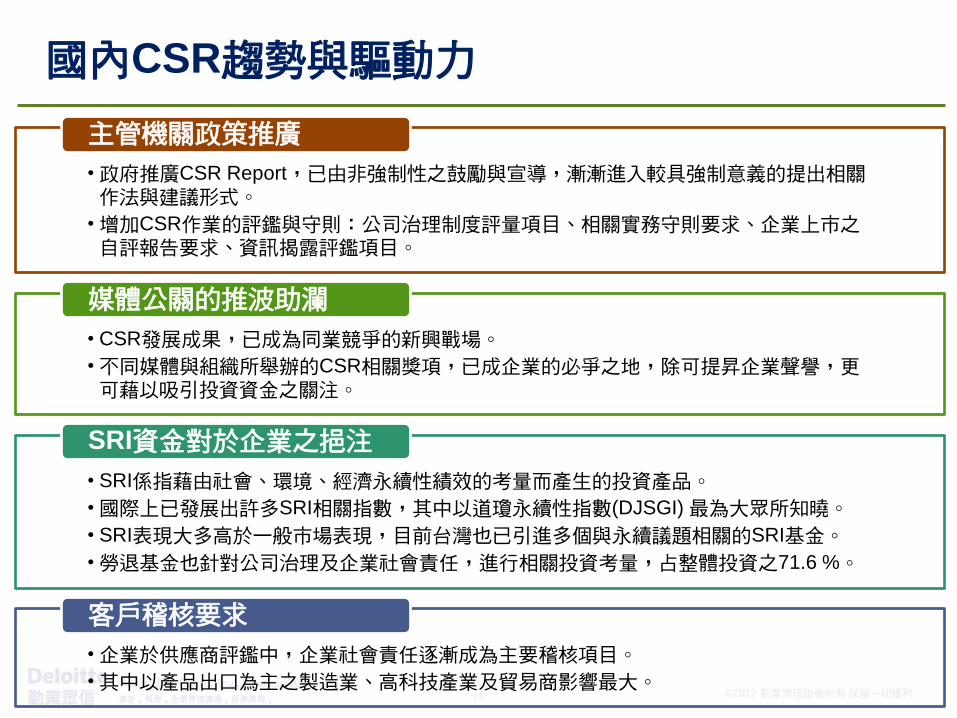

國內CSR趨勢與驅動力

• 政府推廣CSR Report,已由非強制性之鼓勵與宣導,漸漸進入較具強制意義的提出相關作法與建議形式。

• 增加CSR作業的評鑑與守則:公司治理制度評量項目、相關實務守則要求、企業上市之自評報告要求、資訊揭露評鑑項目。

主管機關政策推廣

• CSR發展成果,已成為同業競爭的新興戰場。

• 不同媒體與組織所舉辦的CSR相關獎項,已成企業的必爭之地,除可提昇企業聲譽,更可藉以吸引投資資金之關注。

媒體公關的推波助瀾

• SRI係指藉由社會、環境、經濟永續性績效的考量而產生的投資產品。

• 國際上已發展出許多SRI相關指數,其中以道瓊永續性指數(DJSGI) 最為大眾所知曉。

• SRI表現大多高於一般市場表現,目前台灣也已引進多個與永續議題相關的SRI基金。

• 勞退基金也針對公司治理及企業社會責任,進行相關投資考量,占整體投資之71.6 %。

SRI資金對於企業之挹注

• 企業於供應商評鑑中,企業社會責任逐漸成為主要稽核項目。

• 其中以產品出口為主之製造業、高科技產業及貿易商影響最大。

客戶稽核要求

© 2012 勤業眾信版權所有 保留一切權利

如何推動企業社會責任

© 2012 勤業眾信版權所有 保留一切權利

如何建立企業永續發展架構

策略目標

可行方案

成長 成本與效率

公司治理、永續基礎:

報告書建立與法令規範依循

策略目標 -

如何傳達企業價值

可行方案 -

設定基準線、目標和增強環境與社會表現之規劃

營運作業整合-

驅動永續發展企業的成長和效率

公司治理 、永續基礎、

報告書建立與企業承諾-

創造一個豐富的永續經營

營運作業整合

17

© 2012 勤業眾信版權所有 保留一切權利

永續企業關注的六大面向 • 永續發展不應只是減少碳排放或是參與社會公益活動。

• 永續企業應著重於永續發展準則的六大面向:

永續治理 永續工作環境 永續勞動力 永續供應鏈 永續建築/服務 永續科技

永續企業:

善加運用永續經營的法則,公司才能創造成長、盈利及其自身價值。

* Deloitte definition 18

© 2012 勤業眾信版權所有 保留一切權利

企業永續發展的執行規劃

分析

Analyze

評估

Assess

計畫

Plan

實施Implementation

Tools:

Key output:

• Current performance on CSR initiatives

• Inventory of high importance CSR aspects

• CSR Gaps

• CSR objectives and strategy

• Road map for CSR implementation

• Detailed action plans for the short term

• Feasibility evaluation

• Organizational outline

• Financial implications

• CSR Report

CSR value map

CSR framework Identify

relevance of

CSR aspects

Address

sustainable

value creation

Demonstrate

commitment

and

management

quality

Quantify

performance

Communicate

effectively

Achieve

credibility

• The organiza-

tion‟s relevant

CSR issues

• How has the CSR

issues been

identified

• Management‟s

commitment to

the organization‟s

challenges,

efforts and results

within CSR

• “The tone from

the top”

• The value created

as a result of the

relationship

between the CSR

impact of the

organization and

the people in the

organization,

suppliers,

customers,

community and

CSR related

economic

efficiency

• Quantification of

an organization‟s

CSR performance

• KPI‟s on the

identified CSR

issues

• Management‟s

responsibility for

the content in the

CSR reports

• The credibility of

reports is

enhanced by the

use of styles,

which signal

authenticity

• Awards and

prizes won for

excellent CSR

performance

• Communication

and reporting

• Ability to judge

the completeness

and relevance of

CSR issues

CSR aspects

1. Which issues do you find relevant for you?

1.1 What do you consider as your concerns and challenges within the area: Climate and energy?

1.2. What do you consider as your concerns and challenges within the area: Environment?

1.3. What do you consider as your concerns and challenges within the area: Social?

1.4. What do you consider as your concerns and challenges within the area: Economic?

1.5. Which issues within the CSR agenda are most relevant for you right now?

1.6. Which issues within the CSR agenda do you expect will be most relevant for

you within a period of 2-5 years?

1.7. How do you address these issues?

2. What are your expectations of TORM?

2.1. What are your expectations of TORM within the area: Environment?

2.2. What are your expectations of TORM within the area: Social?

2.3. What are your expectations of TORM within the area: Economic?

2.4. Which issues within the CSR agenda should TORM focus on right now?

2.5. Which issues within the CSR agenda should TORM focus on within a period of 2-5 years?

2.6. How does the CSR performance of TORM impact your decisions?

3. How do you perceive the CSR performance of the shipping industry and of TORM?

3.1. How do you perceive the CSR performance of the shipping industry?

3.2. How do you perceive the CSR performance of TORM?

3.3. Which company do you perceive as best practice within the shipping industry?

4. Which CSR related initiatives would you recommend to management of TORM?

Internal and

external

question

guides

1. Which issues do you find relevant for you?

1.1 What do you consider as your concerns and challenges within the area: Climate and energy?

1.2. What do you consider as your concerns and challenges within the area: Environment?

1.3. What do you consider as your concerns and challenges within the area: Social?

1.4. What do you consider as your concerns and challenges within the area: Economic?

1.5. Which issues within the CSR agenda are most relevant for you right now?

1.6. Which issues within the CSR agenda do you expect will be most relevant for

you within a period of 2-5 years?

1.7. How do you address these issues?

2. What are your expectations of TORM?

2.1. What are your expectations of TORM within the area: Environment?

2.2. What are your expectations of TORM within the area: Social?

2.3. What are your expectations of TORM within the area: Economic?

2.4. Which issues within the CSR agenda should TORM focus on right now?

2.5. Which issues within the CSR agenda should TORM focus on within a period of 2-5 years?

2.6. How does the CSR performance of TORM impact your decisions?

3. How do you perceive the CSR performance of the shipping industry and of TORM?

3.1. How do you perceive the CSR performance of the shipping industry?

3.2. How do you perceive the CSR performance of TORM?

3.3. Which company do you perceive as best practice within the shipping industry?

4. Which CSR related initiatives would you recommend to management of TORM?

CSR aspect

at XX

Customers

Associations

Large

shareholders

Industry

regulators

Future

generations

Pool partners

Third party

certifiers

NGO‟s (non-profit

organizationsMedia

Stakeholder analysis

CSR Map

Environment

Social

Economic

Labor

Air Emissions

Energy and Climate

Spills

Anti-fouling Paint

Waste Management

Ballast Water

Consumables

Cargo Vapors

Tanks and Holds Cleaning

Recycling Ships

Developing Green

Shipping

Community Investments

Eco-efficiency

Value Creation via

Stakeholders

Impact on Global

Economic Development

Human Rights

Product

Society

Conduct and Ethics

Occupational Health,

Safety And Security

Workplace

Attractiveness

Employment

Labor/Management

Relations

Diversity and

Equal Opportunity

Complaints and

Grievance Practices

Prevention of Forced and

Compulsory Labor

Freedom of Association

and Collective Bargaining

Abolition of Child Labor

Non-discrimination

Customer Side Health,

Safety and

Environmental Aspects

Service Labeling

Marketing and

Communication

Anti-competitive Behaviour

Facilitation Management/

Corruption

Public Policy

High importance

Medium importance

Low importance

Identify

relevance of

CSR aspects

Address

sustainable

value creation

Demonstrate

commitment

and

management

quality

Quantify

performance

Communicate

effectively

Achieve

credibility

• Certain CSR

aspects should

be reprioritized

to align with

identif ied

importance and

TORM‟s current

performance.

• Limited CSR

information in

public annual

reporting.

• The high level of

safety and

security could

be documented

and tracked

better via KPIs.

• Focus on

communication

(both internally

and externally),

reporting and

measurement

will bring TORM

in a leading

CSR position in

the shipping

industry.

• Reporting is not

aligned with

external

reporting

standards (GRI

and AA1000).

• Assurance

statement in

environmental

report, however,

no assurance on

full pallet of CSR

aspects.

• Feedback f rom

key opinion

formers on

TORM‟s

performance

has not been

communicated

publicly to

create

credibility.

• Effective CSR

risk manage-

ment system is

lacking.

• No plan for

mitigating

certain CSR

risks (shipping in

general and

TORM specif ic).

• Limited CSR

partnership

approach with

customers and

suppliers.

• Few processes

in place to

capture CSR

issues with

customers/

suppliers/

employees that

could turn into

business

opportunities.

• No clear CSR

agenda in vision,

values and

principles of TORM

(except for environ-

ment and safety).

• No commitment to

UNGC or other

external codes and

standards.

• A number of CSR

aspects are not

covered by

policies.

• Walk the talk is

lacking.

• CSR organization

weak and f rag-

mented. Roles and

responsibilities are

unclear.

• No cross-organiza-

tional ownership.

• Opportunity to

improve CSR

KPIs (currently,

mainly KPIs for

environmental

CSR aspects).

• No processes in

place to

measure the

f inancial and

CSR-related

implications of

initiatives.

• Many valuable

CSR initiatives

are performed at

TORM, but they

are not explicitly

linked to targets.

• Opportunity to

improve bench-

marking on CSR

targets/initia-

tives.

Gap analysis

Evaluation of

performance

• TORM will be among the best places to work

and attract scarce resources.

• Be among the best quartile safety performers

and maintain position as preferred supplier.

• Develop partnerships for community

engagements aligned with TORM‟s core

business.

• TORM‟s CSR strategy responds proactively to stakeholder concerns while creating attractive long -

term shareholder value.

• A broadly balanced approach to CSR addressing all CSR aspects relevant to stakeholders.

• CSR is an integrated part of organizational development, operations and investments.

• The CSR scope of TORM covers the extended value chain.

• Actively working to improve CSR performance within the Blue Denmark.

Out of current strategy scopeTORM CSR position 2009-2011

• TORM will proactively work to contribute to the

environment and climate agenda in an

economically responsible way by applying a

comprehensive eco-ef f iciency approach.

• Be among best quartile environmental

performers.

• The diverse and cross-organizational nature of CSR and its impact at both operational and staf f

function levels requires a broad and cross-disciplinary approach to implementation.

• CSR implementation capabilities and project management skills will be built in parallel.

The people company The eco-efficient company

Living our values – respecting stakeholders

TORM capability development

Broader implementation capabilities

• Ultimately becoming the CO2 neutral ocean shipping company.

• Taking a societal-level responsibility.• Being the visionary „thought leadership‟ brand on green ocean shipping.

The green ocean shipping company

The prerequisite

The enabler

The differentiator

The aspiration

CSR strategy

2010 2011 20122009

• Fix shortcomings in current CSR

performance.

• Initiate building TORM holistic CSR

capabilities.

• Ensure early regulatory compliance

and compliance with TORM‟s CSR

principles and policies.

• Implement eco-ef f iciency quick hit.

• Build CSR measurement and

reporting capabilities.

• Develop new business models

for delivering green shipping.

• Initiate some green shipping

activities.

• Leverage technology to reduce

emissions and environmental

impacts.

• Investment strategy for

environmental leadership.

• Complete building CSR

capabilities.

• Prepare for a proactive role.

• Focus on CSR eco-ef f iciency.

• Develop business improvement

opportunities through innovation.

• Engage with selected customers

and suppliers.

CSR institutionalization

CSR eco-efficiency

and excellence

Selective CSR leadership

Strategy implementation

Building CSR capabilities

CSR project

CSR communication and reporting

2009 2010 2011

Review code of conduct

and prepare for roll-out

Develop

contingency plans

Managing risks

Collaboration

with NGOs

M1

M2 M3

Note: This road map is an outline and not to scale.

Set up project

model

B0 CSR business

intelligence

B6

Build measurement &

reporting capabilities

Build CSR organiza-

tion and processes

B3

B4

Devise CSR prin-

ciples & policies

B2

Set up project

model

B1

CSR communication

and reporting

B5 CSR function &

project management capabilities operational

Road map

Corp. mgmt.

Central CSR

function

Divisions/

staff functions

Project

capability

CSR network

Management team or

CSR board

Commission‟s work

Releases capability

Releases capability

Commission‟s work

• Sets direction for

CSR in TORM

• Vehicle to implement

change in TORM

• Responsible for adop-

ting new or modifying

existing business

practices to achieve

CSR performance

targets

• Implementation of

cross-function initia-

tives benef iting f rom a

project delivery model

• Responsible for CSR

agenda and for overall

CSR performance

according to stra-

tegy and targets

Organizational design

Objectives:• Make CSR commitments, objectives and targets measureable• Create feedback to management and BoD

• Develop fact-based reporting and communication with stakeholders• Develop CSR Reporting plan (3-5 years) aligned with CSR strategy and communication

plan

Description and objectives of CSR initiative

CSR initiative – Build measurement and reporting capabilities

• Lack of resources, competencies and commitment

• Lack of cross-organizational co-ordination

• Risk of not walking the talk – talking the walk

Project risk assessment

• April 2009

Earliest launch

• Develop CSR principles and policies (B2)

• Business intelligence and communication (B5, B6)

• Ongoing environmental data collection and IT project

• Financial accounts

Dependencies and related ongoing initiatives

Business benefits

• Improved CSR performance: „What gets measured gets managed‟

• Cost reductions

• Reputation and branding; build trust amongst stakeholders

• Improve ratings at SRI benchmarks

• Position TORM among the most preferred suppliers (best quartile)

1. Establish baseline

• Align with Greenhouse Gas Protocol and Global Reporting Initiative (GRI)

• Align with WBCSD/WRI Green House Gas Protocol, and other relevant

aspect specific reporting and measurement norms and standards

2. Select KPIs and benchmarks

• Identify performance indicators and targets to address important CSR aspects

• Identify relevant benchmarks to assess performance externally against peers

• Define KPIs for data collection

3. Develop internal reporting cycle

• Define plan for data collection process

• Integrate with existing data and processes and align with ongoing IT projects

4. Provide feedback to management on progress

• Develop dashboard for progress reports to top and line management

5. Develop CSR reporting plan/strategy

• Decide on CSR reporting for 2009

• Assess current reporting (as-is) ; develop position on future reporting (to-be)

• Identify gaps and resource needs

• Align with CSR strategy and implementation plan

• Decide on external assurance

Primary activities

Action plan number (B4)

• 5 months

Project duration

• IT investments (ongoing

project)

• Investments in data

collection and IT systems

not included

Estimated cost

• 100 man days

• Support from line

organization and finance

Resources

• All CSR aspects

Covered CSR aspects

• Head of CSR function

Responsible

Detailed action plans

19

© 2012 勤業眾信版權所有 保留一切權利

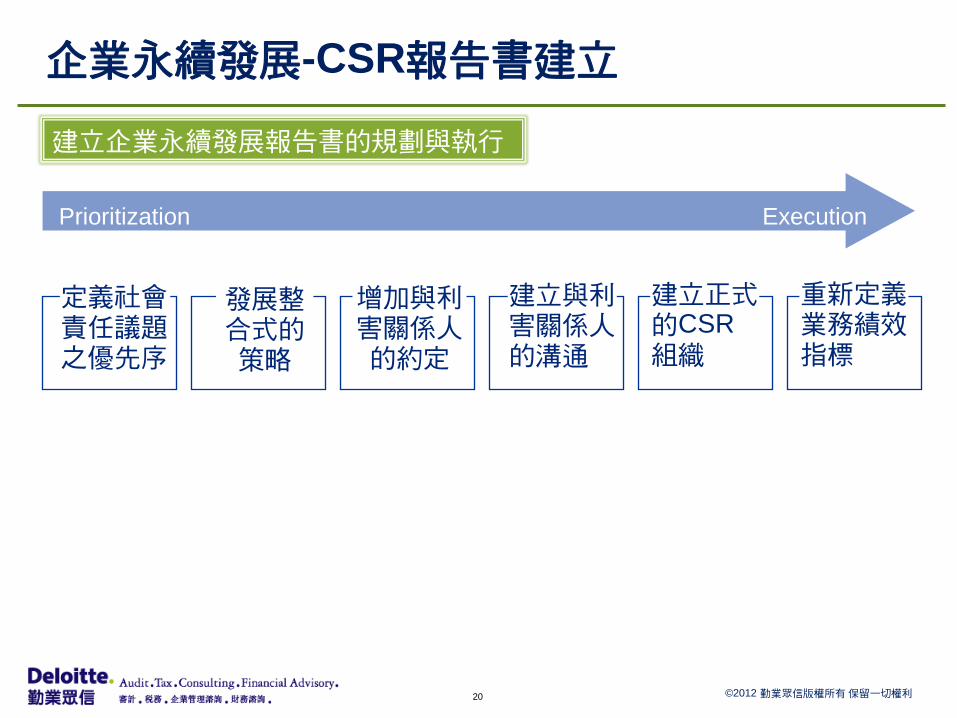

企業永續發展-CSR報告書建立

建立企業永續發展報告書的規劃與執行

Prioritization Execution

定義社會責任議題之優先序

發展整合式的策略

增加與利害關係人的約定

建立與利害關係人的溝通

建立正式的CSR組織

重新定義業務績效指標

20

© 2012 勤業眾信版權所有 保留一切權利

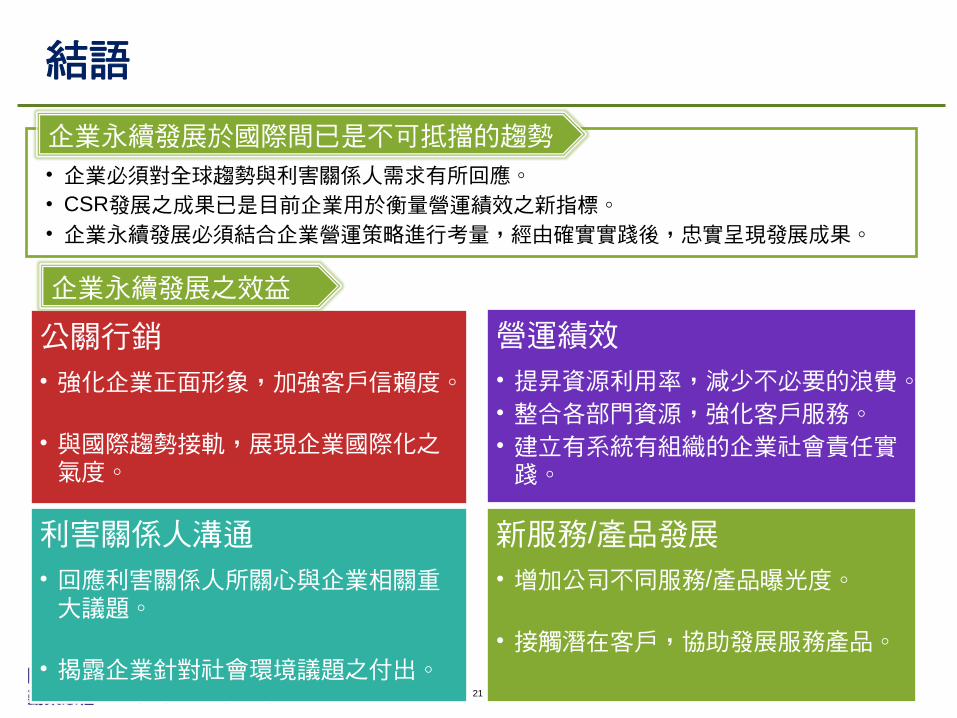

公關行銷

• 強化企業正面形象,加強客戶信賴度。

• 與國際趨勢接軌,展現企業國際化之氣度。

營運績效

• 提昇資源利用率,減少不必要的浪費。

• 整合各部門資源,強化客戶服務。

• 建立有系統有組織的企業社會責任實踐。

利害關係人溝通

• 回應利害關係人所關心與企業相關重大議題。

• 揭露企業針對社會環境議題之付出。

新服務/產品發展

• 增加公司不同服務/產品曝光度。

• 接觸潛在客戶,協助發展服務產品。

結語

• 企業必須對全球趨勢與利害關係人需求有所回應。

• CSR發展之成果已是目前企業用於衡量營運績效之新指標。

• 企業永續發展必須結合企業營運策略進行考量,經由確實實踐後,忠實呈現發展成果。

21

企業永續發展於國際間已是不可抵擋的趨勢

企業永續發展之效益

© 2012 勤業眾信版權所有 保留一切權利

Q&A

萬幼筠 Thomas Wan, 副總經理

Office: +886 2 25459988 #6869

E-mail: [email protected]

吳佳翰 Chia-Han Wu, 副總經理

Office: +886 2 25459988 #5078

E-mail: [email protected]

周嘉明 Charming Chou, 協理

Office: +886 2 25459988 #7702

E-mail: [email protected]

© Deloitte & Touche LLP and affiliated entities.

Deloitte, one of Canada's leading professional services firms, provides audit, tax, consulting, and financial advisory services through more than 6,200 people in 50 offices. Deloitte operates in Québec as Samson Bélair/Deloitte & Touche s.e.n.c.r.l. The firm is dedicated to helping its clients and its people excel. Deloitte is the Canadian member firm of Deloitte Touche Tohmatsu.

Deloitte refers to one or more of Deloitte Touche Tohmatsu, a Swiss Verein, its member firms, and their respective subsidiaries and affiliates. As a Swiss Verein (association), neither Deloitte Touche Tohmatsu nor any of its member firms has any liability for each other's acts or omissions. Each of the member firms is a separate and independent legal entity operating under the names "Deloitte," "Deloitte & Touche," "Deloitte Touche Tohmatsu," or other related names. Services are provided by the member firms or their subsidiaries or affiliates and not by the Deloitte Touche Tohmatsu Verein.

![[CSRone永續報告平台]台灣永續報告現況與趨勢-2016 CSR Report Survey in Taiwan(節錄版本Preview Version)](https://static.fdocuments.net/doc/165x107/5877ba1d1a28ab2c668b679b/csrone2016-csr-report.jpg)

![[CSRone永續報告平台]台灣永續報告現況與趨勢-2016 CSR Report Survey in Taiwan](https://static.fdocuments.net/doc/165x107/5877ba1d1a28ab2c668b6797/csrone2016-csr-report-5919cd0219c15.jpg)