© 2002 William Buck All rights reserved. DataKnowledgeInnovation Financial Viability and the DEEWR...

86

© 2002 William Buck All rights reserved. Data Knowledge Innovation Financial Viability and the DEEWR Financial Financial Viability and the DEEWR Financial Health Assessment Health Assessment Independent Schools Queensland Independent Schools Queensland ISQ State Conference ISQ State Conference Novotel Brisbane 27 August 2009 Novotel Brisbane 27 August 2009

-

date post

20-Dec-2015 -

Category

Documents

-

view

215 -

download

1

Transcript of © 2002 William Buck All rights reserved. DataKnowledgeInnovation Financial Viability and the DEEWR...

© 2002 William Buck All rights reserved.

Data Knowledge Innovation

Financial Viability and the DEEWR Financial Health AssessmentFinancial Viability and the DEEWR Financial Health Assessment

Independent Schools Queensland Independent Schools Queensland

ISQ State Conference ISQ State Conference

Novotel Brisbane 27 August 2009Novotel Brisbane 27 August 2009

Page 2

John Somerset

Qualifications

Graduate Diploma Company Directors Course

Certificate IV in Workplace Training and Assessment

Graduate Diploma in Applied Finance and Investment

Professional Year Institute of Chartered Accountants

Bachelor of Commerce University of Queensland

Accreditations/Memberships

Graduate - Australian Institute of Company Directors

Fellow - Financial Services Institute of Australasia

Member - Institute of Chartered Accountants in Australia

Member - Performance Measurement Association (UK)

Core Expertise

Benchmarking schools (14 years).

Strategic planning, evaluation and reporting.

Corporate governance of schools.

Financial management and performance improvement

Budgeting and board reporting models.

Appointments

Council and Finance - St Paul’s School (2000 – 2008)

Chairman - St Paul’s School Foundation (2006 to 2008)

Director - St Stephen’s College

Chair Finance Committee – St Stephen’s College

Risk Assurance Committee – St Stephen’s College

Member of Executive –Independent Schools Queensland

Chair Finance Committee –Independent Schools Queensland

Page 5

The “Going Concern” principle

DEEWR Schools Assistance Act 2008

The minister will be concerned about the financial viability of a school where

Its liabilities exceed its assets

For a substantial period it is unable to pay its debts as and when due or

Auditor expresses concern about financial viability

Australian Government Auditing and Assurance Standard

Auditor would generally express a financial viability concern where

School is unable to pay its debts as and when they fall due; and

It may be necessary to liquidate or otherwise wind up the operations

Page 6

Auditor will consider

Debts due in next 12 months exceed assets available to pay for them

Borrowings approaching maturity without realistic prospects of renewal

Withdrawal of financial support by debtors and creditors

Operating (cash) losses (historical and/or prospective)

Adverse key financial ratios

Inability to pay debts by due dates

Inability to comply with terms of loan agreements

Page 7

In short

Financial viability will be in question where there is insufficient cash being generated by the school to meet the obligations of the lenders (banks and creditors)

You must make a reasonable operating surplus (profit)

Page 8

Causes of Financial Distress

Over borrow (loans and leases)

Low profit margin or operating losses

Inability to repay debt from fiscal operations

Drop in students (demographics) causing drop in income

Not adjusting expenses (staff) for drop in students

Weak Governance

Not identifying financial distress early

Small financial resource base

Page 9

Causes of Financial Distress

Poor financial monitoring systems

Loss of owner’s support (deep pockets)

Grow too big, too quickly on the back of fee discounts

Non-precise budgeting - long and short term

Non-precise accounting – ignoring auditors management letters

Poor selection of key management personnel

Page 10

Operating Income

Operating Expenditure

Fee Levels State and Commonwealth

Grant Entitlements

Miscellaneous Income Available

Student Numbers

Tuition Administration & Maintenance

Student / Teacher Ratios

Miscellaneous Costs

Curriculum

Mission Statement

What drives Operating Requirements?

Page 11

What Drives Capital Requirements?

Capital Income Capital Expenditure

Facilities RequiredNon-Core Facilities Desired

Eligibility for Special GrantsOther Sources of

Capital Income

Student Numbers

Student / Teacher RatiosCurriculum

Mission Statement

Page 12

From 2009 DEEWR will use benchmarks to test financial viability

Schools Assistance Bill 2008 and Administrative Guidelines state

The financial viability of a school will be assessed utilising a set of financial indicators, with each indicator being assigned a benchmark…

The status of a school’s financial health will be assessed according to the number of benchmarks the school meets…

Schools will be assigned to one of three groups

Page 13

DEEWR Financial Viability Status Groups – out of 9 ratios

Group 1

5 + benchmarks

DEEWR comfortable with viability

Group 2

3- 4 benchmarks

DEEWR a little concerned and will request audited accounts and an action plan for improvement and a two year budget.

Deadline 4 weeks of receipt of request from DEEWR

Group 3

2 or fewer benchmarks

DEEWR quite concerned and will request engagement of qualified independent consultant to assess finance, governance and develop a management plan and a five year budget.

Deadline 6 weeks from mandatory meeting with DEEWR

Recurrent funding will be reduced to monthly installments until school moves to group 1 or 2

Page 17

Balance Sheet – A “picture” at a point in time

What you Own Assets

Less -

What you Owe Liabilities (debts)

Equals =

What you are Worth Equity (Retained Earnings)

Page 18

Balance Sheet – A “picture” at a point in time

Current Assets = Cash or things convertible to cash within 12 months

Current Liabilities = Debts payable within 12 months

Non-Current Assets = longer than 12 months to convert to cash

Non-Current Liabilities = longer than 12 months to pay

Page 19

Profit & Loss – A “picture” over time

Also called an Income Statement

Income Sale of services (Fees, grants, other)

Less

Expenses Costs incurred in operating the school

Equals

Net Operating surplus (Profit)

Page 20

The “Aim” of the Game

1. Earn more than you spend

2. Own more than you owe

Page 21

The “Aim” of the Game

Your School Entity

(Internal World)

Income in $1,000

Expenses out $900The Outside World

Balance Sheet Profit & Loss

Page 22

The value of the entity grows by $100

Extra $100 Cash

Expenses out $900

Income in $1,000

The Outside World

Balance Sheet Profit & Loss

Page 23

Reinvest $100 on a building

Extra $100 Cash

Building worth $100(Entity did not grow) Builder paid $100

Building supplied

The Outside World

Balance Sheet Just a flow of cash. No increase in wealth. Just A reallocation of assets from cash to building

Page 24

Moral of the Story

Must be able to pay your debts when due

Question 1 Are we solvent (can we pay our debts when due)?

You must make a surplus (profit) with the outside World

Question 2 Are we efficient?

Continue to reinvest in new assets

Question 3 Are we sustainable?

Question 4 How much debt is prudent?

Page 26

Measuring Performance

Financial statements provide absolute quantities - $

Convert quantities to ratios (eg. cost per student) for meaningful comparisons

We are better informed by comparing one quantity to another

Ratio Analysis

Page 27

Benchmarks – A Point of Reference

Make INFORMED decisions

A reference point or hurdle

What is a reasonable

Operating surplus (profit)?

Debt?

Staff number?

Benchmarks are your guiding tracks

Page 28

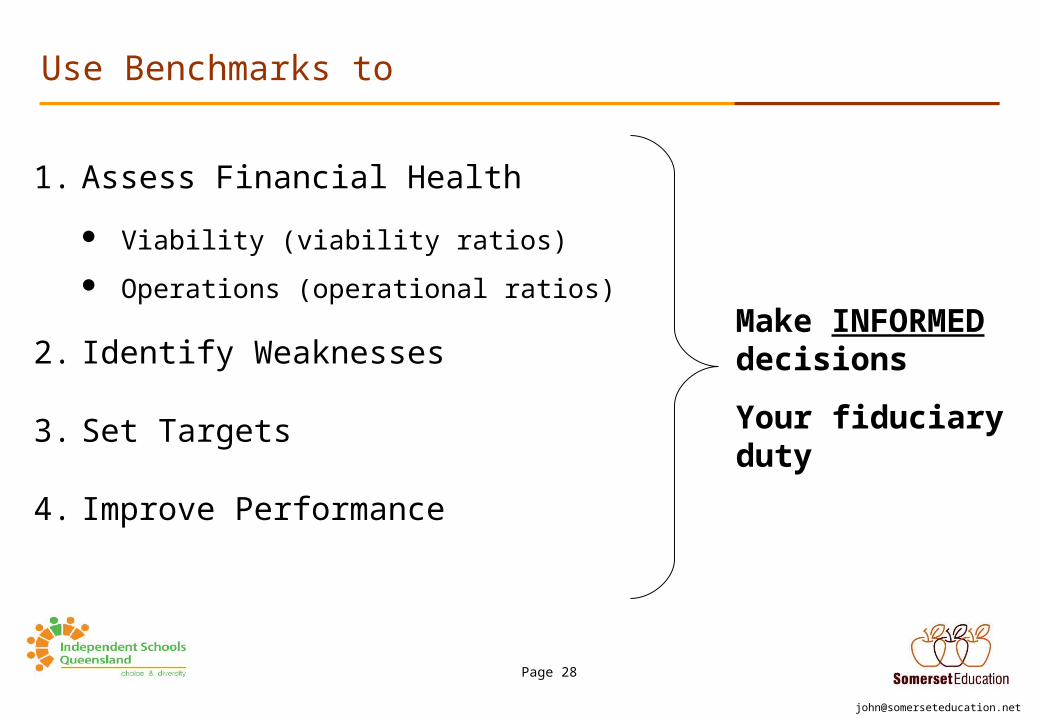

Use Benchmarks to

1. Assess Financial Health

Viability (viability ratios)

Operations (operational ratios)

2. Identify Weaknesses

3. Set Targets

4. Improve Performance

Make INFORMED decisions

Your fiduciary duty

Page 29

How to pass your DEEWR test

DEEWR Benchmarks

ASBA/Somerset Financial Performance Survey (FPS)

Your TestYour Coach/Tutor

• Diagnose

• Treat

• Improve

Page 30

DEEWR Financial Health Assessment Benchmarks

DEEWR ratio

Description Hurdle benchmark Type of ratio Year applied

1 Student/Teacher ratio Primary SES >104 = 12Primary SES < 105 = 17Secondary SES >104 = 9Secondary SES < 105 = 12.5

Operational

(but a crucial ratio)

2009

2 Enrolment change on previous year Maximum Minus 20% Viability 2009

3 % change in recurrent income compared to AGSRC % Minimum 0% Operational 2009

4 Change in net tuition income per student Minimum 4% Operational 2009

5 Salaries as % recurrent income Maximum 75% Operational 2009

6 Total Borrowings / Recurrent Income Maximum 100% Viability ? 2009

7 Interest Cover Minimum 2 times Viability 2009

8 Principal + Interest as % of Recurrent Income Maximum 10% Viability ? 2011

9 Cash surplus as % of Recurrent Income Minimum 3% Viability ? 2011

10 Recurrent Income – Recurrent Expenditure as a % Recurrent Income

Minimum 5% Viability 2009

11 Current assets / Current Liabilities (Current ratio) Minimum 1:1 Viability ? 2011

12 Government grants as % of Recurrent Income Maximum 70% Operational 2009

13 Bad and Doubtful debts as % of Gross fees Maximum 5% Operational 2011

Page 31

Comments on the DEEWR Benchmarks for 2009/2010Ratio Description Research Comments Retain

Remove xVary !

1 Student/Teacher ratio 50% of schools failed 80% of failing schools appear viable

Strong correlation to costs

But poor indicator of viability x2 Enrolment change on previous

year

3% of schools failed

ID < 1/3rd of schools likely to be unviable

Some correlation with viability 3

% change in recurrent income compared to AGSRC %

33% of schools failed 90% of failing schools appear viable

No correlation with viability x

4

Change in net tuition income per student

39% of schools failed

90% of failing schools appear viable

No correlation with viability

DEEWR including boarding ? x 5 Salaries as % recurrent income

41% of schools failed

50% of these schools not viable, but

Failed to ID 90% of unviable schools

Significant income missed

Not a reliable measure of viability

Now includes on-costs but hurdle not increased

x

6 Total Borrowings / Recurrent Income

6% of schools failed

65% of failing schools appear viable

Failed to ID 50% of unviable schools

Unreliable measure in current form

Suggest change in formula from recurrent income to profit (EBIDA)

!

7 Interest Cover 22% of schools failed

77% of failing schools appear viable

But correctly ID 94% of unviable schools

Include capital fees to halve sample of failing schools

Exclude schools with no debt

10

Recurrent Income – Recurrent Expenditure as a % Recurrent Income

38% of schools failed

80% of failing schools appear viable

But correctly ID 98% of unviable schools

Include capital fees and other ops.

Lower hurdle to 3%

Should reduce sample of failing schools by 1/3rd

12

Government grants as % of Recurrent Income

49% of schools failed

90% of failing schools appear viable

Failed to ID 70% of unviable schools

No correlation with viability x

Page 32

How to Improve your Financial Performance ASBA/Somerset Financial Survey

Are we Solvent?

Cash flow adequacy

Working capital ? – better to predict cash at bank

DEEWR equivalent

DEEWR 11 (2011)

Are we Efficient?

Net operating margin

Income per student

Discounts

Expenses per student

Staffing ratios

DEEWR 10

DEEWR 1

Are we Sustainable?

Depreciation

Reinvestment

Debt per student

Interest cover DEEWR 7

Page 35

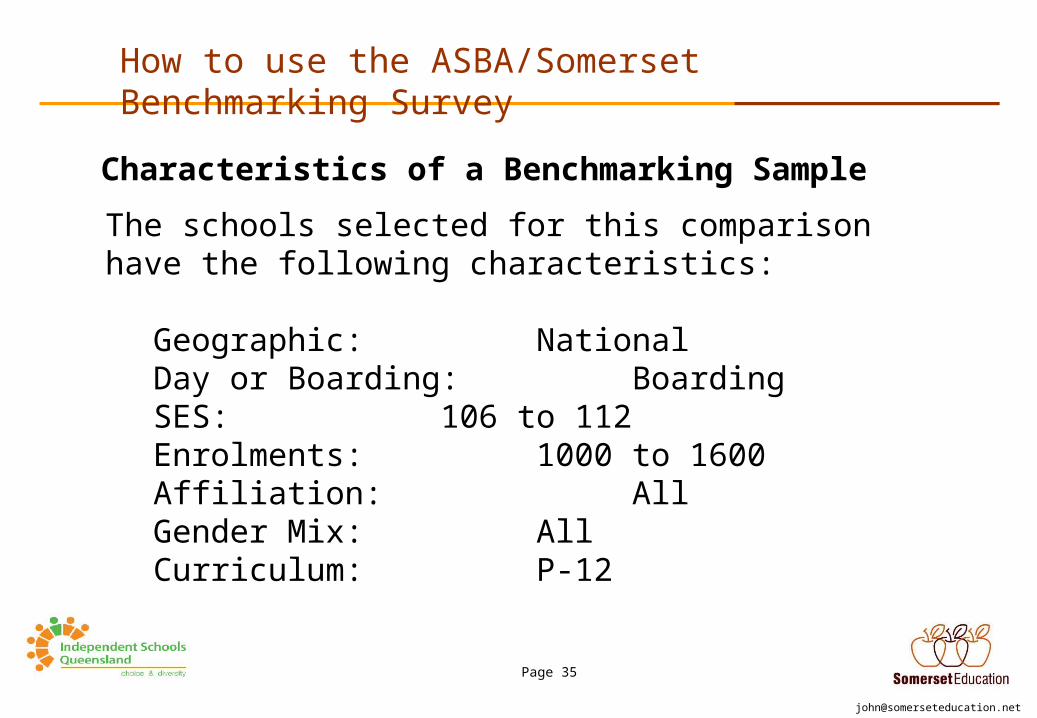

How to use the ASBA/Somerset Benchmarking Survey

The schools selected for this comparison have the following characteristics:

Geographic: NationalDay or Boarding: BoardingSES: 106 to 112Enrolments: 1000 to 1600Affiliation: AllGender Mix: AllCurriculum: P-12

Characteristics of a Benchmarking Sample

Page 36

Actual Sample Average

1,300 1,260

Student Enrolments

Exa

mp

le S

cho

ol

Average: 1,260

0

200

400

600

800

1000

1200

1400

1600

Source: ASBA/Somerset Education Non Government Schools Financial Performance Survey

Page 37

Answering the Key Questions – Key Ratios

Are we Solvent?

Cash flow adequacy

Working capital ? – better to predict cash at bank

Are we Profitable?

Net operating margin

Income per student

Expenses per student

Staffing ratios

Are we Sustainable?

Depreciation

Reinvestment

Debt per student

Interest cover

Page 38

Answering the Key Questions – Key Ratios

Are we Solvent?

Cash flow adequacy Working capital ? – better to predict cash at bank

Are we Profitable?

Net operating margin Income per student Expenses per student

Staffing ratios

Are we Sustainable?

Depreciation Reinvestment Debt per student Interest cover

Page 39

Cash Flow Management

Cash Flow Adequacy = Net cash from operations

Capital and debt expenditure

= Ability to generate cash to meet primary cash requirements

Rule of thumb = 1.0 times

Page 40

Actual Sample Average

0.53 0.92

Cash Flow Adequacy

Exa

mp

le S

cho

ol

Average: 0.92

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

1.60

1.80

Source: ASBA/Somerset Education Non Government Schools Financial Performance Survey

Page 41

National Average

0.91

Cash Flow Adequacy

-

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Source : ASBA/Somerset Education Non-Governmant Schools' Financial Performance Survey 2008 School Year

Average = 0.91 (Excluding catholic Systemic schools)

Page 42

Liquidity Ratios

Working Capital ratio = Current assets

Current liabilities

= number of time that you can pay current creditors (debts)

Rule of thumb = at least 1 times

Page 43

Actual Sample Average

0.20 0.90

Working Capital

Exa

mp

le S

cho

ol

Average: 0.90

0.00

0.50

1.00

1.50

2.00

2.50

Source: ASBA/Somerset Education Non Government Schools Financial Performance Survey

Page 44

National Average

1.01

Working Capital

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Source : ASBA/Somerset Education Non-Government Schools' Financial Performance Survey 2008 School Year

Average = 1.01 (Excluding Catholic Systemic schools)

Page 45

Answering the Key Questions – Key Ratios

Are we Solvent?

Cash flow adequacy Working capital ? – better to predict cash at bank

Are we Profitable?

Net operating margin Income per student Expenses per student

Staffing ratios

Are we Sustainable?

Depreciation Reinvestment Debt per student Interest cover

Page 46

Operating Efficiency

Net Operating margin (Adj.) = Operating Result*

Total Revenue* Before interest, depreciation and amortisation

For every dollar in income, how much remains after all expenses

2008 Industry Average 10.7%

Page 47

Actual Sample Average

7.0% 11.5%

Net Operating Margin (Adj)

Exa

mp

le S

cho

ol

Average: 11.53%

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

16.0%

18.0%

20.0%

Source: ASBA/Somerset Education Non Government Schools Financial Performance Survey

Page 48

National Average

10.7%

Net Operating Margin (before interest and depreciation)

-20%

-10%

0%

10%

20%

30%

40%

Source : ASBA/Somerset Education Non-Government Schools' Financial Performance Survey 2008 School Year

Average = 10.7% (excludes Catholic Systemic schools)

Page 49

Profit Trends (Lowest in 12 years)

0%

2%

4%

6%

8%

10%

12%

14%

2008 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998 1997

Page 50

Actual Sample Average

$16,270 $15,440

Total Income per Student

Exa

mp

le S

cho

ol

Average: $15,440

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

$20,000

Source: ASBA/Somerset Education Non Government Schools Financial Performance Survey

Page 51

National Average

$13,943

Total Income Per Student

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

Source : ASBA/Somerset Education Non-Government Schools' Financial Performance Survey 2008 School Year

Average = $13,943 (Excluding Catholic Systemic schools)6% increase from 2007

Page 52

Actual Sample Average

$15,100 $13,535

Operating Expenses per Student

Exa

mp

le S

cho

ol

Average: $13,535

$0

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

$18,000

Source: ASBA/Somerset Education Non Government Schools Financial Performance Survey

Page 53

National Average

$12,372

Total Operating Expenses Per Student (excl int. and Depn.)

$-

$5,000

$10,000

$15,000

$20,000

$25,000

$30,000

Source : ASBA/Somerset Education Non-Government Schools' Financial Performance Survey 2008 School Year

Average = $12,372 (Excluding Catholic Sustemic)7% increase from 2007

Page 54

Actual Sample Average

$8,174 $7,516

Teacher Salaries per Student

Exa

mp

le S

cho

ol

Average: $7,516

$-

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

Source: ASBA/Somerset Education Non Government Schools Financial Performance Survey

Page 55

Staffing

Student/Teacher ratio = Number of students

Full-Time teacher equivalent

= Average number of students per EFT teacher

Best Practice = Depends on the school

Page 56

Actual Sample Average

15.4 14.7

Primary Student-to-Teacher Ratio

Exa

mp

le S

cho

ol

Average: 14.67

0.0

5.0

10.0

15.0

20.0

25.0

Source: ASBA/Somerset Education Non Government Schools Financial Performance Survey

Page 57

National Average

15.3

Primary Student/Teacher Ratio

-

5.0

10.0

15.0

20.0

25.0

30.0

Source : ASBA/Somerset Education Non-Government Schools' Financial Performance Survey 2008 School Year

Average = 15.3 (Excluding Catholic Systemic)

Page 58

Primary Student/Teacher ratio

14.5

15

15.5

16

16.5

17

2008 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998

Page 59

Actual Sample Average

10.5 10.3

Secondary Student-to-Teacher Ratio

Exa

mp

le S

cho

ol

Average: 10.33

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

Source: ASBA/Somerset Education Non Government Schools Financial Performance Survey

Page 60

National Average

11.3

Secondary Student/Teacher Ratio

-

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Source : ASBA/Somerset Education Non-Government Schools' Financial Performance Survey 2008 School Year

Average = 11.3 (Excluding Catholic Systemic schools)

Page 61

Secondary Student/Teacher ratio

10.5

11

11.5

12

12.5

13

2008 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998

Page 62

Answering the Key Questions – Key Ratios

Are we Solvent?

Cash flow adequacy Working capital ? – better to predict cash at bank

Are we Profitable?

Net operating margin Income per student Expenses per student

Staffing ratios

Are we Sustainable?

Depreciation Reinvestment Debt per student Interest cover

Page 63

Asset Position and Sustainability

Depreciation Impact = Depreciation expenditure

Net cash from operations

= Extent to which assets wear out relative to the cash you are generating from operations.

Page 64

Actual Sample Average

85% 65%

Depreciation Impact Ratio

Exa

mp

le S

cho

ol

Average:65%

0%

20%

40%

60%

80%

100%

120%

140%

Source: ASBA/Somerset Education Non Government Schools Financial Performance Survey

Page 65

National Average

58%

Depreciation Impact Ratio

0%

50%

100%

150%

200%

250%

300%

Source : ASBA/Somerset Education Non-Governmant Schools' Financial Performance Survey 2008 school Year

Average = 58% (Excluding Catholic Systemic schools)

Page 66

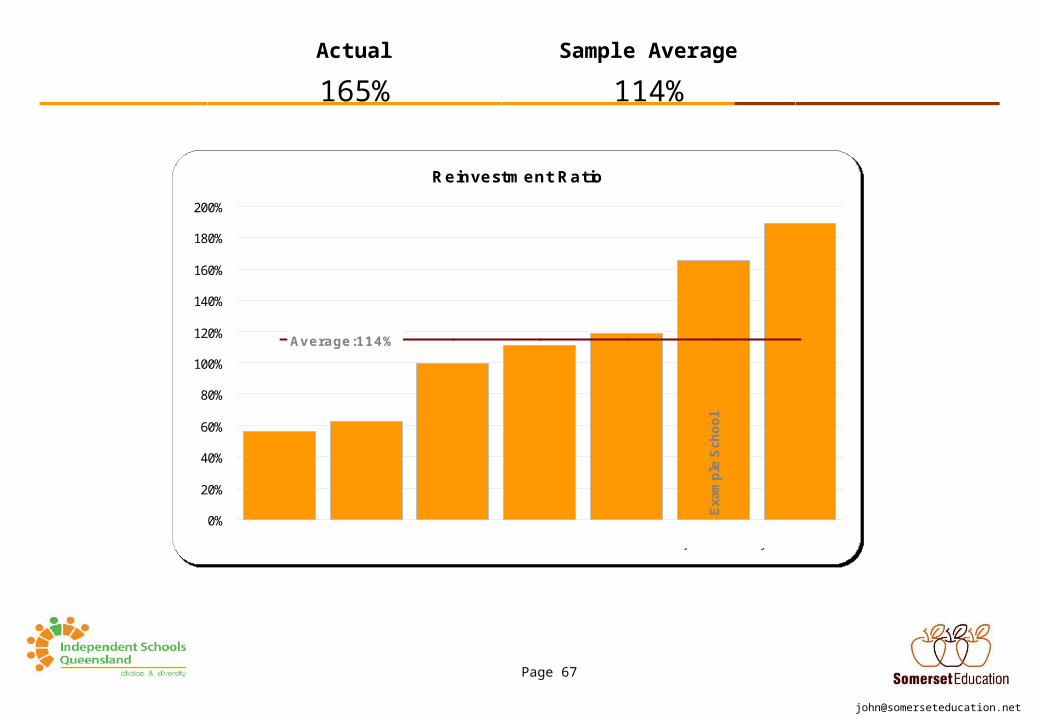

Asset Position and Sustainability

Reinvestment = Capital expenditure

Net cash from operations

= Extent to which you are reinvesting in new equipment relative to the cash you are generating from operations.

Best Practice = 60% to 65%

Page 67

Actual Sample Average

165% 114%

Reinvestment Ratio

Exa

mp

le S

cho

ol

Average:114%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

200%

Source: ASBA/Somerset Education Non Government Schools Financial Performance Survey

Page 68

National Average

132%

Reinvestment Ratio

0%

100%

200%

300%

400%

500%

600%

700%

Source : ASBA/Somerset Education Non-Government Schools' Financial Performance Survey 2008 School Year

Average = 132% (Excludes Catholic Systemic schools)

Page 69

Reinvestment Trends

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

2008 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998

Page 70

Debt per Student

Financial Debt per student = Interest bearing (bank) debt

Student numbers

= Average debt per student

2008 Industry Average = $6,300

Page 71

Actual Sample Average

$6,000 $4,138

Debt per Student

Exa

mp

le S

cho

ol

Average $4,138

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$9,000

$10,000

Source: ASBA/Somerset Education Non Government Schools Financial Performance Survey

Page 72

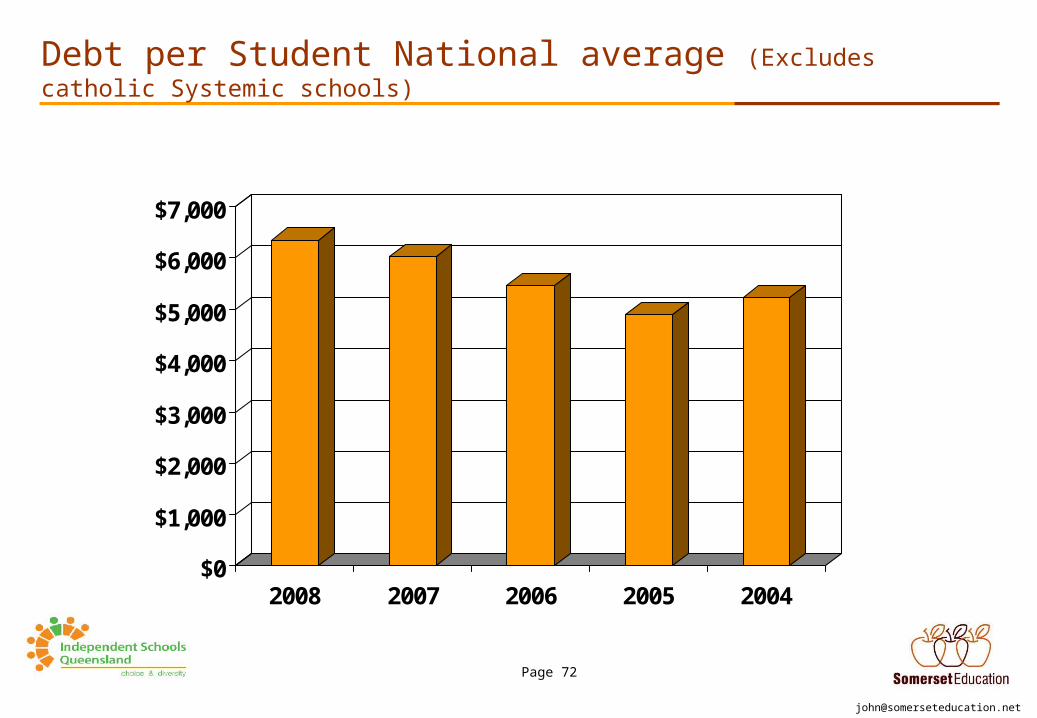

Debt per Student National average (Excludes catholic Systemic schools)

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

2008 2007 2006 2005 2004

Page 73

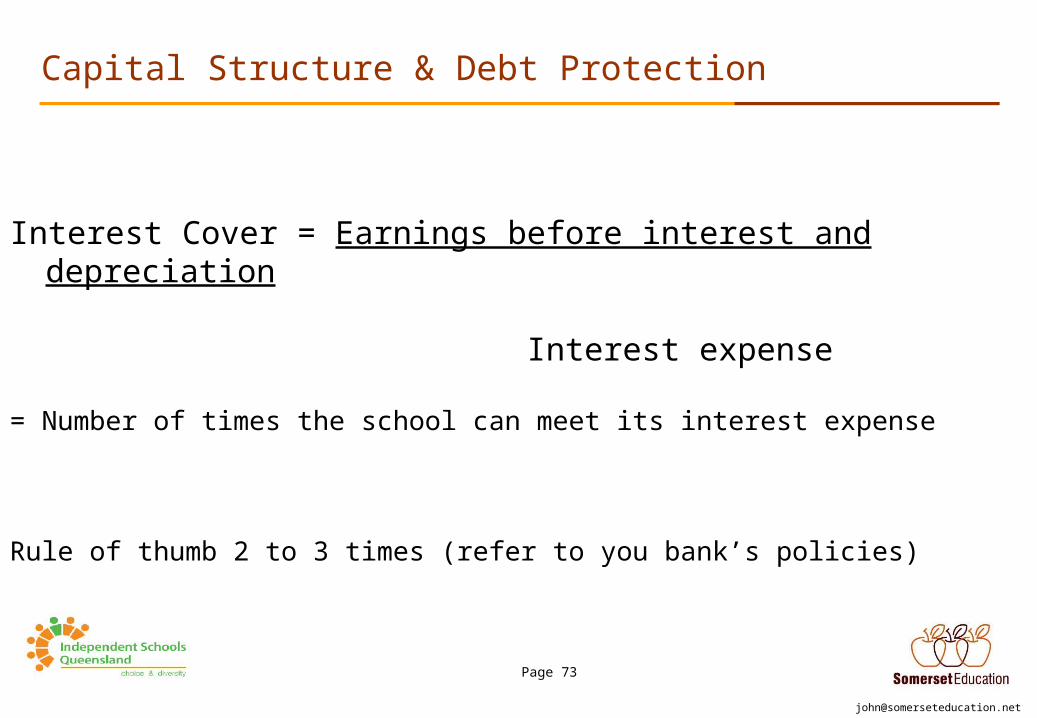

Capital Structure & Debt Protection

Interest Cover = Earnings before interest and depreciation

Interest expense

= Number of times the school can meet its interest expense

Rule of thumb 2 to 3 times (refer to you bank’s policies)

Page 74

Actual Sample Average

3.3 20.5

Interest Cover

Exa

mp

le S

cho

ol Average: 20.5

0.0

10.0

20.0

30.0

40.0

50.0

60.0

Source: ASBA/Somerset Education Non Government Schools Financial Performance Survey

Page 75

Quantify Variations

Key Performance Indicator Sample Average

Example School Effect

Net Operating Margin (Adj) 11.5% 7.3%

Total Income per Student $15,440 $16,270

Operating Expense per Student

$13,535 $15,100

Debt per student $4,138 $6,000

Primary Student/teacher ratio 14.7 15.4

Secondary Student/Teacher Ratio

10.3 10.5

Page 76

Quantify Variations

Key Performance Indicator Sample Average

Example School Effect

Net Operating Margin (Adj) 11.5% 7.3% ($900,000)

Total Income per Student $15,440 $16,270 +$1 million

Operating Expense per Student

$13,535 $15,100 +$2 million

Debt per student $4,138 $6,000 +$2.4 million

Primary Student/teacher ratio 14.7 15.4 (1.5) staff

Secondary Student/Teacher Ratio

10.3 10.5 (1.5) staff

Page 77

Limitations of Benchmarks

Different participants at different stages of development and with different ranges of services.

Consistency in accounting.

Ratios only as good as data (Garbage In Garbage Out)

Page 78

School Council and Management working together

Participate in the survey

Quantify variances

Debate with reference to strategy

Make INFORMED decisions

Set policies

Operating margin

Interest cover

Debt per student

Student/teacher ratios

Page 80

Governance –v- ManagementTricker’s Model - International Corporate Governance

Compliance Role Performance Role

External Role

Provide accountability Strategy formulation

Internal Role Monitoring and supervision Policy making

Past and present orientated Future orientated

How much time should you spend in each quadrant?

Where are you now?

What alters your priority?

BoardManagement

Page 81

Budgets – Long term and Short term

“Dollarise” your plan

Building master plan

Past, present and future modus operandi

Funding needs

“3 way” budget

Profit and loss

Balance sheet

Cash flow – cash at bank yearly rests and monthly rests

Compare KPI’s against benchmarks

Net operating margin

Interest cover

Staff ratios

Page 82

Monitoring

Distill information on crucial

Outcomes (operating margins, student/teacher ratios, interest cover) Drivers (student and staff numbers)

Report in a format which is easily understood by all.

Assess past, present and future performance

Somerset Key Indicator (SKI) report Preventative, pro-active decision making

Focus on matters of importance - CAUSE and effect

Interest cover Debt levels Operating margins

84

SKI Report

SKI Report 2007 Actual

2008 Actual2009

BudgetRec. Min.

NSW, SES 110-130, day schools

students 900-2000, Prep -

yr 12

Indexed to 2008 (5% p.a.)

Indexed to 2009 (5% p.a.)

Are we Solvent? (How easily can we pay our debt and capital expenditure needs)

Cash Flow Adequacy 0.15 1.35 0.85 1.04

Working capital ratio 0.7 0.6 1.0 1.22

Percentage trade debtors to fees billed (boarding and tuition) 18.9% 14.9% 9.4% 1.7%

Are we Profitable?

Earnings before interest, depreciation & amortisation (EBIDA) 179,503 933,703 211,868

Your profit would be this figure if you performed at sample average 1,445,722$ 1,498,621$ 1,028,765$

Including Capital Income

EBIDA + Other capital income 218,006$ 1,191,703$ 211,868$

Margin including other capital income 2.1% 10.7% 2.8%

Net cash from operations 181,150-$ 707,368$ 111,868$

Interest Cover (including other capital income) 0.55 2.46 2.12

Profit margin (EBIDA/Gross Income) 1.7% 8.6% 2.8% 13.8%

Income per student (excludes boarding, includes capital fees & levies) 12,169$ 12,991$ 11,564$ 14,609$ 15,339$ 16,106$

Percentage discounts/concessions to fees billed 8.0% 8.1% 0.9% 5.6%

Teaching salaries per student 6,752$ 6,409$ 8,448$ 7,551$ 7,929$ 8,325$

Total expenses per student (excluding boarding, interest and depreciation) 11,962$ 11,878$ 11,082$ 13,073$ 13,727$ 14,413$

Student/Teacher ratio - primary 14.6 16.7 13.0 15

Student/Teacher ratio - secondary 10.1 10.3 10.0 11.4

Are we Sustainable?

Depreciation/amortisation impact -520% 127% 218% 66%

Reinvestment -576% 57% 134% 116%

Debt per student 8,538$ 8,906$ 1,546$ 9,212$ 9,673$ 10,156$

Interest Cover (Earnings before interest and depreciation/interest expense) 0.4 1.9 2.1 3 13.5

Liabilities to equity 584% 768% 97% 82%

= Good result

= Caution on this result

Your School Benchmarks

Page 85

Summary

1. Assess Financial Health

Viability ratios

Operational ratios

2. Identify weaknesses

3. Set targets

4. Accurate, succinct and timely monitoring

Page 86

For further details contact

John Somerset – Director of Somerset Education

Email [email protected]

Internet www.somerseteducation.net

Telephones 1300 781 968

0417 618 899

Address GPO Box 3273

Brisbane, Queensland

Australia 4001