Scorecard And Dashboard And Metrics Oh My! - fmi*igf … · linked to TM1 •Inability to ... and...

62

Scorecard And Dashboard And Metrics ... Oh My! FMI PD Week 2012

-

Upload

dinhkhuong -

Category

Documents

-

view

221 -

download

0

Transcript of Scorecard And Dashboard And Metrics Oh My! - fmi*igf … · linked to TM1 •Inability to ... and...

Scorecard And Dashboard And Metrics ... Oh My! FMI PD Week 2012

Today’s presenters

Panelists:

Mario Malouin, Vice-President and Chief Financial Officer, Canadian Air

Transport Security Authority (CATSA)

Jean-Paul Lemieux, Director, Trade Commissioner Service (TCS) Planning and

Client Service Support Division, Department of Foreign Affairs and International

Trade Canada

Facilitators:

Cathy Green, Senior Managing Consultant, Strategy and Transformation, IBM

Canada

Liz Geiger, Associate Partner, Business Analytics and Optimization, Canadian

Public Sector and Health Market, IBM Canada

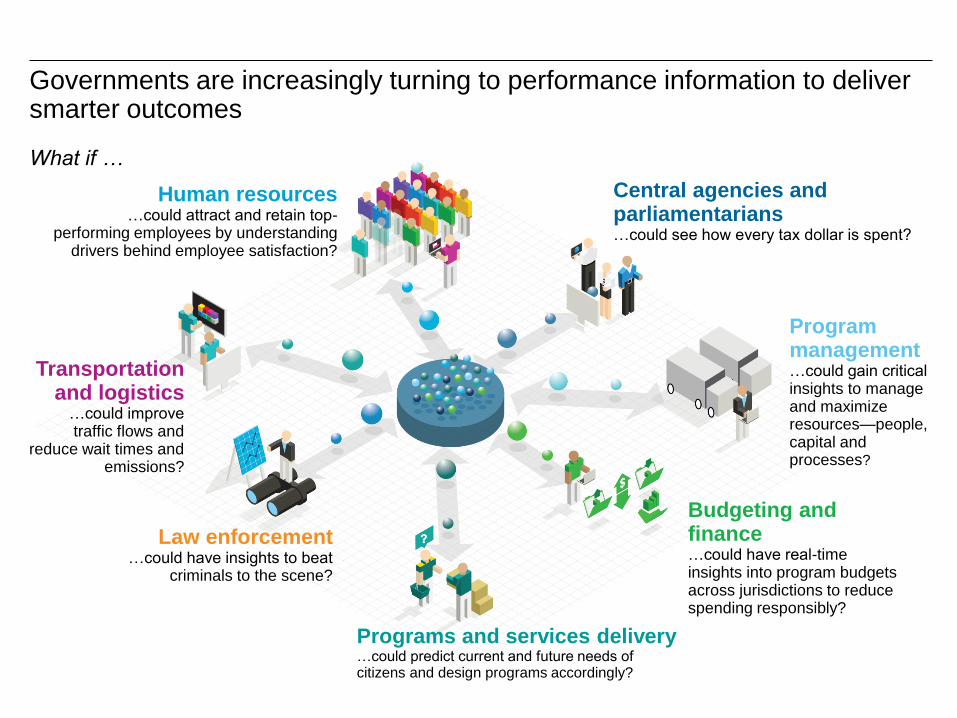

Governments are increasingly turning to performance information to deliver smarter outcomes What if …

Transportation and logistics

…could improve traffic flows and

reduce wait times and emissions?

Programs and services delivery …could predict current and future needs of citizens and design programs accordingly?

Program management …could gain critical insights to manage and maximize resources—people, capital and processes?

Central agencies and parliamentarians …could see how every tax dollar is spent?

Budgeting and finance …could have real-time insights into program budgets across jurisdictions to reduce spending responsibly?

Law enforcement …could have insights to beat

criminals to the scene?

Human resources …could attract and retain top-

performing employees by understanding drivers behind employee satisfaction?

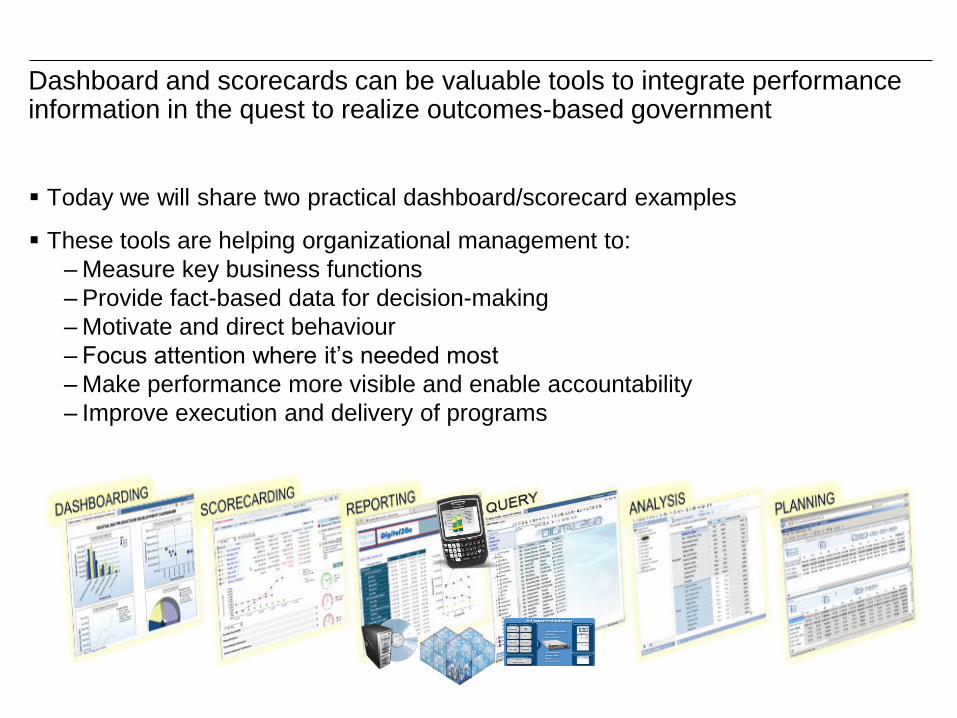

Dashboard and scorecards can be valuable tools to integrate performance information in the quest to realize outcomes-based government

Today we will share two practical dashboard/scorecard examples

These tools are helping organizational management to:

– Measure key business functions

– Provide fact-based data for decision-making

– Motivate and direct behaviour

– Focus attention where it’s needed most

– Make performance more visible and enable accountability

– Improve execution and delivery of programs

Agenda

CATSA – Operating in a Volatile, Uncertain, Complex and Ambiguous (VUCA)

World (25 minutes)

DFAIT – Performance Measurement Initiatives in Support of DFAIT's

Commercial Program (25 minutes)

Questions and Panel Discussion (20 minutes)

Mario Malouin, CPA, CA, MA Vice-President and Chief Financial Officer

Canadian Air Transport Security Authority

Tuesday, November 27, 2012 Ottawa Convention Centre

Ottawa, Ontario

Scorecard and Dashboard

and Metrics…Oh My!

A Full Strategic Corporate Partnership is

a Critical Success Factor to the

Achievement of an Organization’s

Strategic Objectives in a Volatile,

Uncertain, Complex and Ambiguous

(VUCA) World.

Financial Management Institute of Canada

Professional Development Week

7

Table of Contents

Page

Current Environment 3

CATSA 14

Balance Scorecard 18

Boarding Pass Security System (BPSS) 21

Planning Budgeting and Forecasting Tool (PBFT) 28

Looking Forward 34

Success Factors 37

8

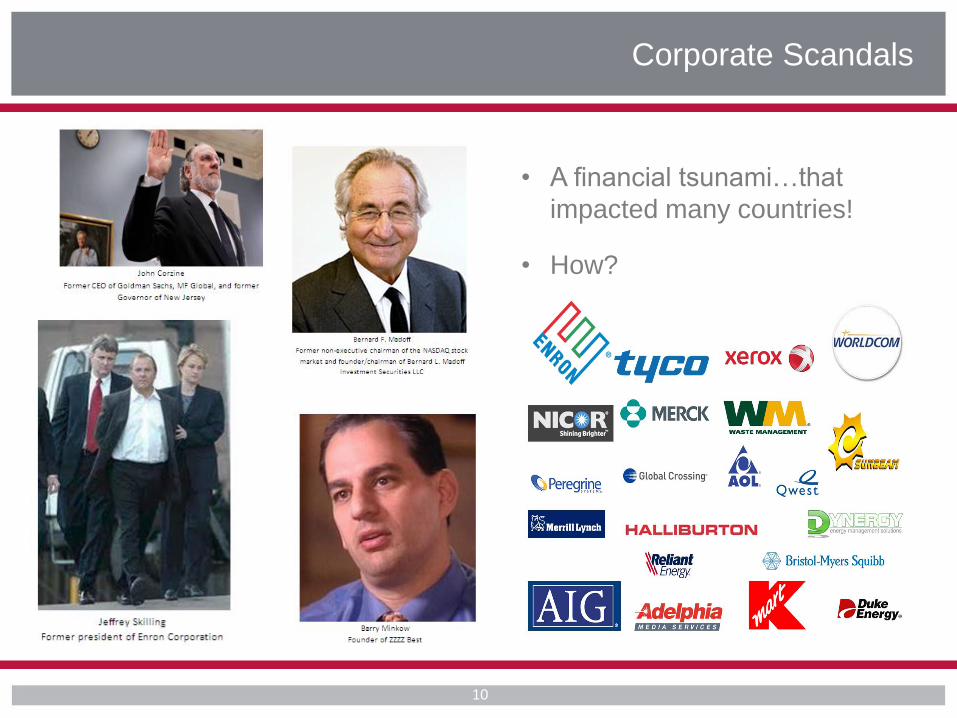

Current Environment

• Corporate scandals

• 9/11

• Both had a global influence

Interdependence

9

• A financial tsunami…that

impacted many countries!

• How?

Corporate Scandals

10

• In the immediate aftermath of 9/11, the aviation security system underwent its most significant change worldwide

• Literally overnight, it became an urgent global priority to enhance counter-terrorism capabilities and preparedness

• In Canada, the federal Budget of December 2001 contained a $2.2 billion package of new funding for civil aviation security improvements. The Budget also announced the creation of the Canadian Air Transport Security Authority (CATSA)

9/11

11

In times of crisis

or instability,

events can

transcend

borders and

spread globally

12

Interdependence

• Strong interdependence creates a

VUCA world

• In a VUCA world, top leaders are

faced with dilemmas that have no

solutions and yet they are still

required to make sound decisions

• Traditional leadership skills aren’t

enough

13

VUCA

Since we live in a VUCA world

in which financial resources are

more and more limited, CFOs

and finance function must

adapt. But how?

Adaptation

14

"The task of leadership is

to create an alignment of

strengths, making our

weaknesses irrelevant." - Peter Drucker

15

Alignment

• To guide a company, CFOs should be in tune with the markets, and

able to give early warning signals to the organization, and help the

organization think through how to adjust quickly enough to market

signals

• The Finance function should be a visionary in the business and not

just a storyteller

Alignment

16

"Growing complexity, talent

scarcity, and technology deficits

are most likely to put the finance

function’s effectiveness at risk."

CFO Research Services and

KPMG 2012 Global CFOs on

the Art of Constructive Change

17

18

19

CATSA

20

Secure critical elements of the air

transportation system:

• Pre-Board Screening (PBS)

• Hold-Baggage Screening

(HBS)

• Non-Passenger

Screening (NPS)

• Restricted Area Identity Card

(RAIC)

CATSA Background

21

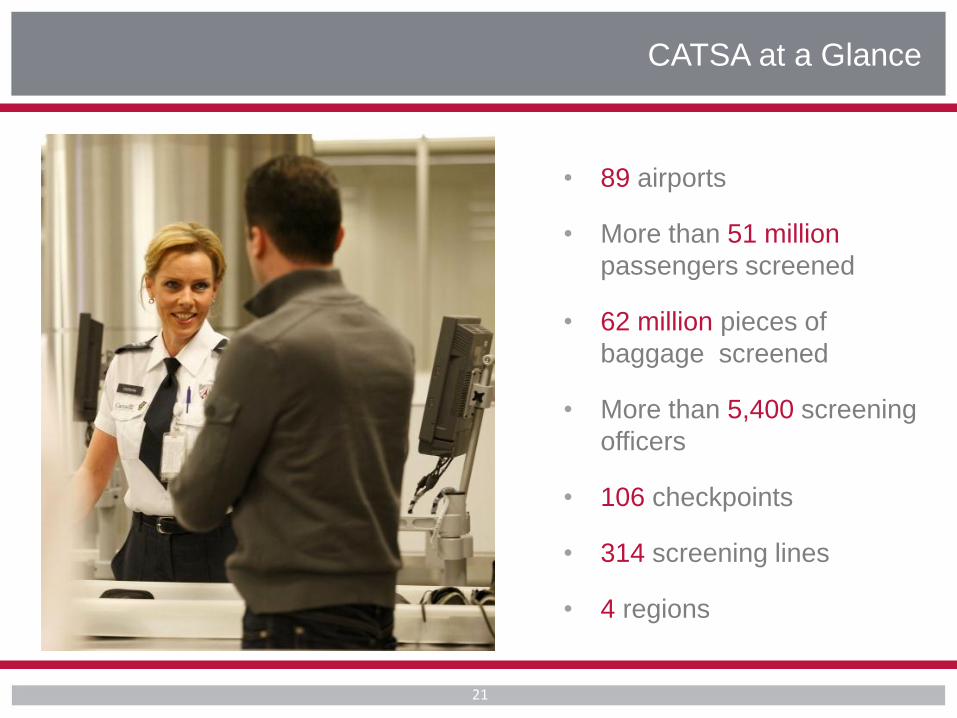

• 89 airports

• More than 51 million

passengers screened

• 62 million pieces of

baggage screened

• More than 5,400 screening

officers

• 106 checkpoints

• 314 screening lines

• 4 regions

CATSA at a Glance

22

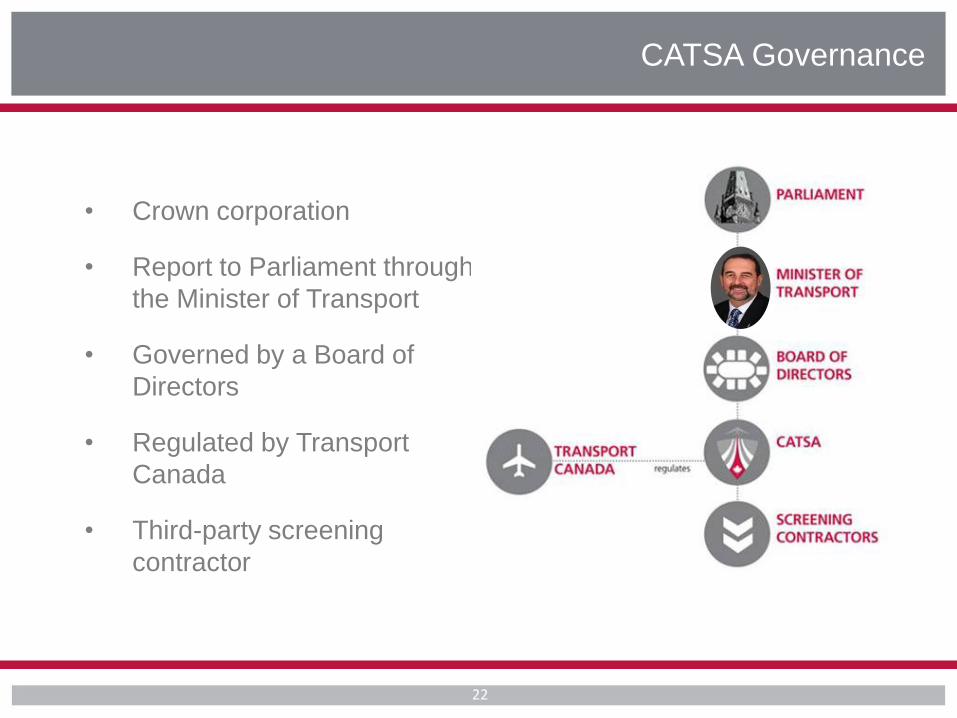

• Crown corporation

• Report to Parliament through

the Minister of Transport

• Governed by a Board of

Directors

• Regulated by Transport

Canada

• Third-party screening

contractor

CATSA Governance

23

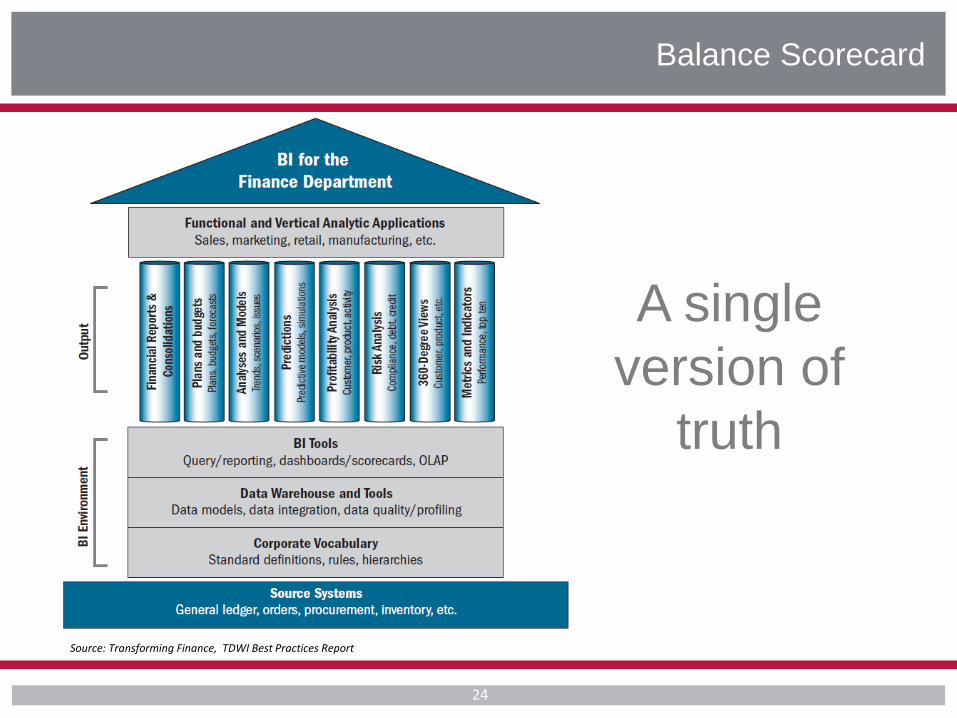

Balance Scorecard

A single

version of

truth

Balance Scorecard

Source: Transforming Finance, TDWI Best Practices Report

24

25

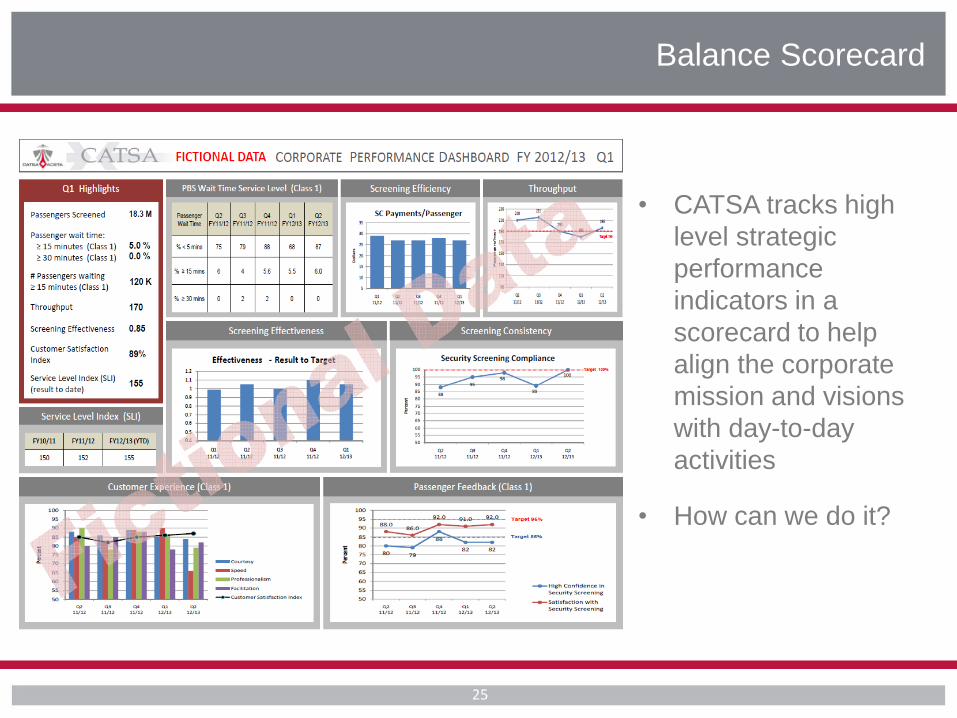

Balance Scorecard

• CATSA tracks high

level strategic

performance

indicators in a

scorecard to help

align the corporate

mission and visions

with day-to-day

activities

• How can we do it?

26

Boarding Pass Security System (BPSS)

27

• Automated boarding pass

verification

• Class 1 airports

• Developing expansion

plans

BPSS

28

• Enhanced:

• Validation of boarding

passes

• Security resolution

• Performance monitoring

BPSS Benefits

29

• Paper boarding passes

• Electronic boarding passes

Boarding Pass Verification

30

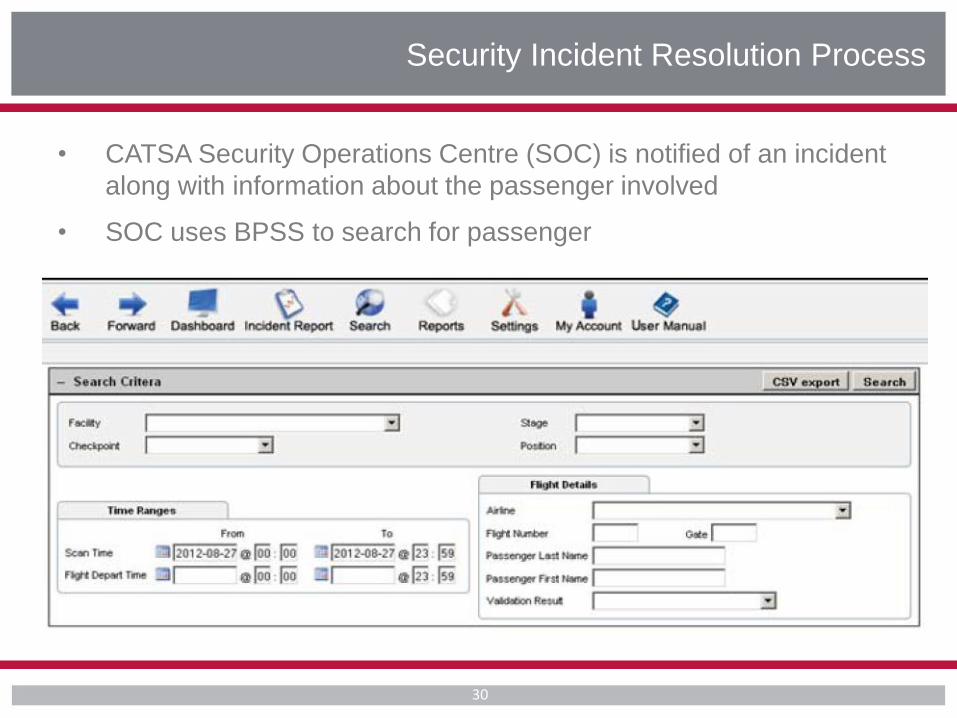

Security Incident Resolution Process

• CATSA Security Operations Centre (SOC) is notified of an incident

along with information about the passenger involved

• SOC uses BPSS to search for passenger

31

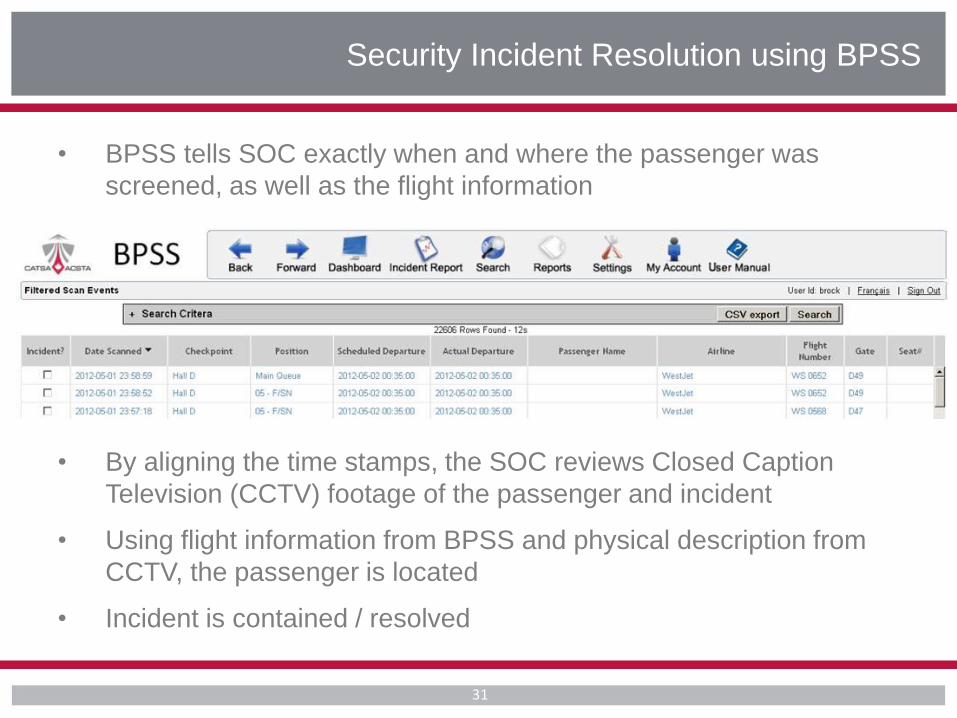

Security Incident Resolution using BPSS

• BPSS tells SOC exactly when and where the passenger was

screened, as well as the flight information

• By aligning the time stamps, the SOC reviews Closed Caption

Television (CCTV) footage of the passenger and incident

• Using flight information from BPSS and physical description from

CCTV, the passenger is located

• Incident is contained / resolved

32

• Vital to daily operations

• Improves customer service

• Wait-time information

• Data sharing initiative

• Planning, Budgeting and

Forecasting our cost…

BPSS Performance Management

33

Planning Budgeting and Forecasting Tool (PBFT)

• Transform enterprise planning budgeting and

forecasting tool (PBFT):

• Implement an end-to-end business solution

(provide integration)

• Minimize use of Excel spreadsheets (improve

data reliability)

• Implement standard templates/consolidations

• Enable financial/non-financial modeling and

what-if analysis

• Empower end users (Responsibility Managers)

• Reduce reliance on Financial Analysts

• Realize productivity gains in Financial Planning

PBFT

34 34

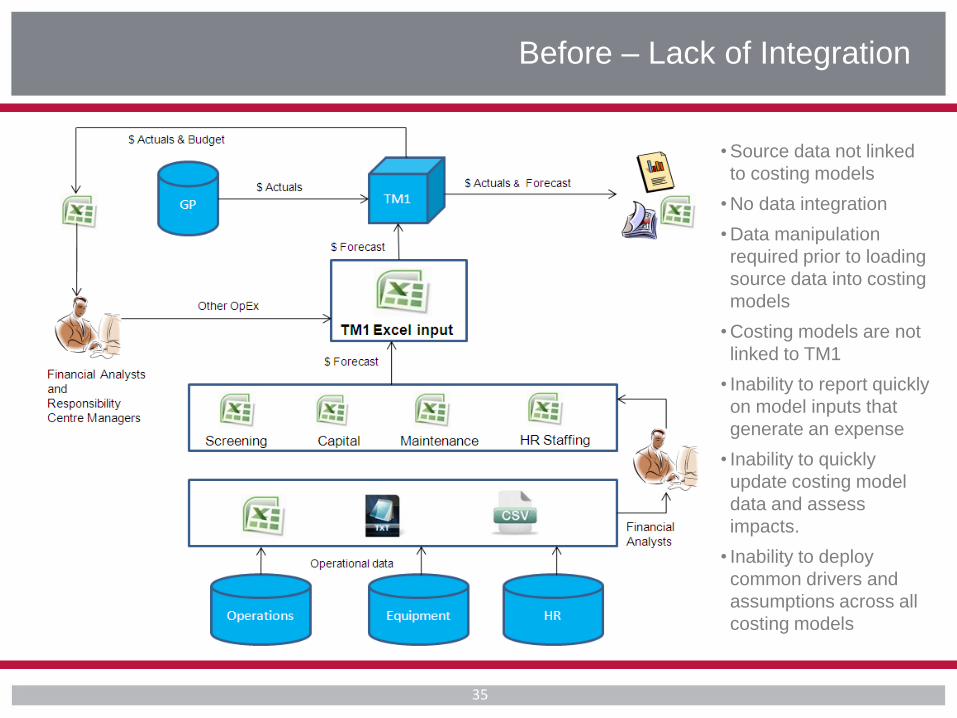

Before – Lack of Integration

35

• Source data not linked

to costing models

• No data integration

• Data manipulation

required prior to loading

source data into costing

models

• Costing models are not

linked to TM1

• Inability to report quickly

on model inputs that

generate an expense

• Inability to quickly

update costing model

data and assess

impacts.

• Inability to deploy

common drivers and

assumptions across all

costing models

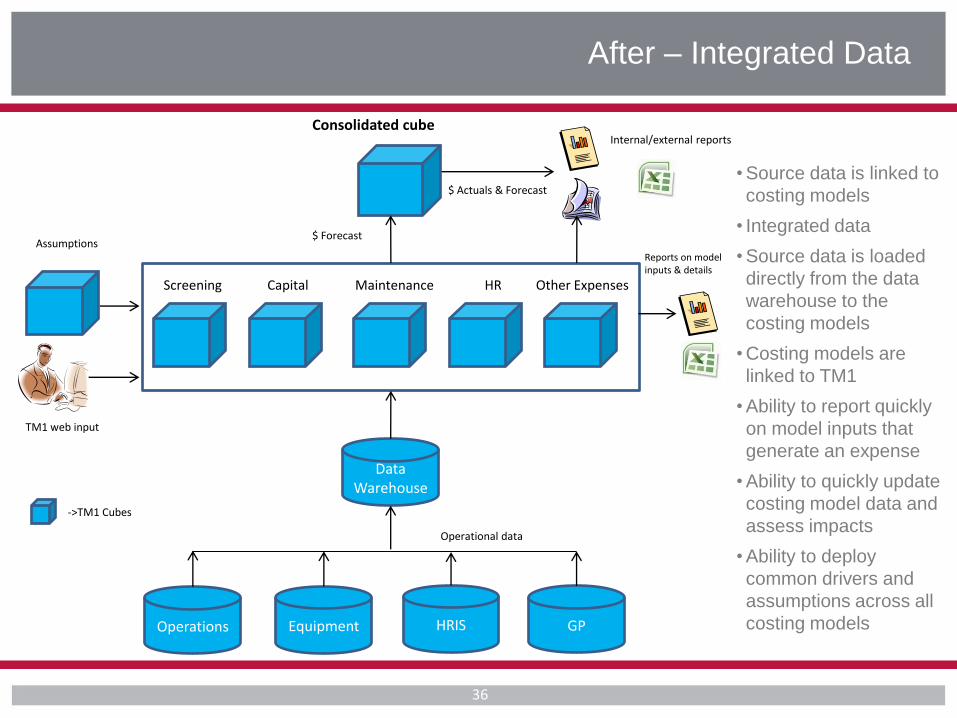

After – Integrated Data

36

Operations HRIS Equipment

$ Actuals & Forecast

Data Warehouse

Screening Capital Maintenance HR

GP

Other Expenses

Assumptions

Consolidated cube Internal/external reports

Reports on model inputs & details

->TM1 Cubes

TM1 web input

Operational data

$ Forecast

• Source data is linked to

costing models

• Integrated data

• Source data is loaded

directly from the data

warehouse to the

costing models

• Costing models are

linked to TM1

• Ability to report quickly

on model inputs that

generate an expense

• Ability to quickly update

costing model data and

assess impacts

• Ability to deploy

common drivers and

assumptions across all

costing models

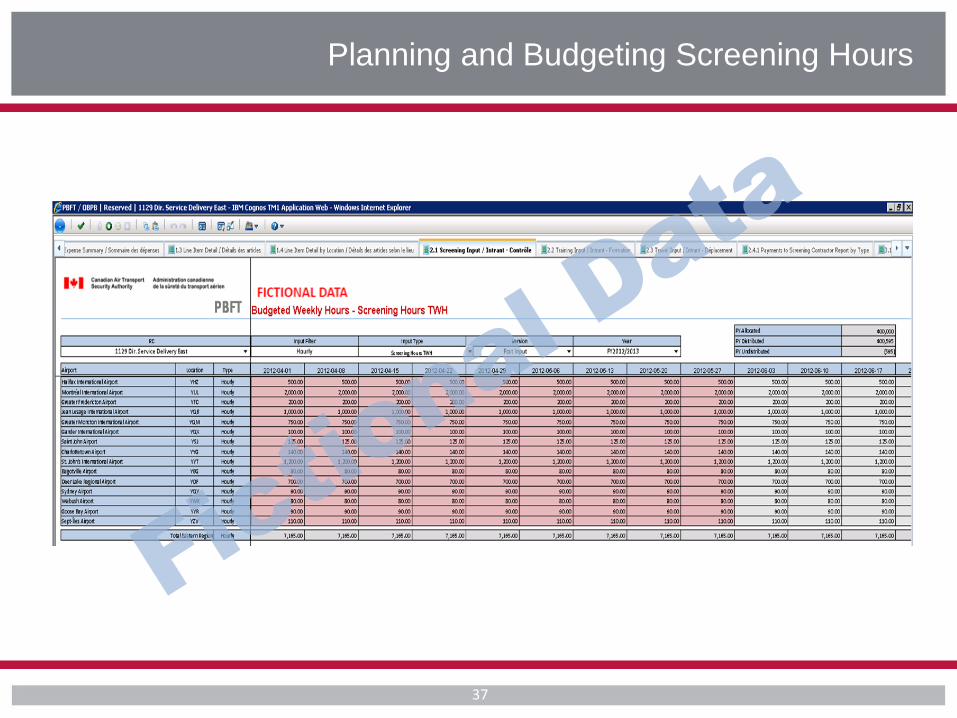

Planning and Budgeting Screening Hours

37

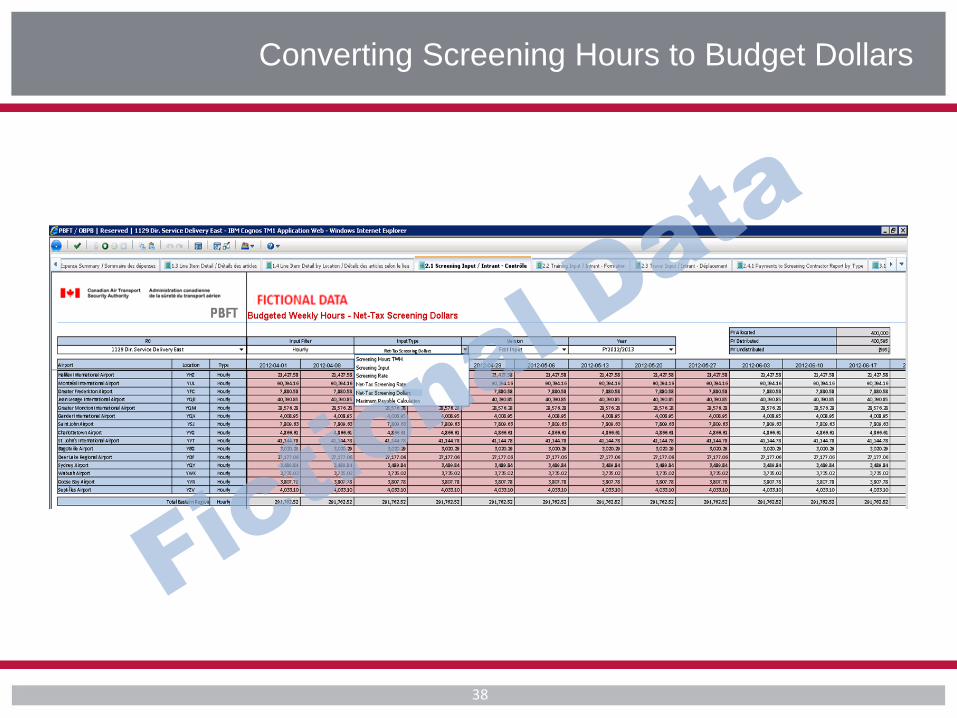

Converting Screening Hours to Budget Dollars

38

39

Looking Forward

40

• Predictive Analytics:

• To leverage organizational

business knowledge by applying

sophisticated analysis techniques

to enterprise data. The resulting

insights lead to actions that

demonstrably change how

resources are assigned.

• Financial Reporting Tool:

• To automate the creation of

statutory and regulatory reports,

providing a collaborative

environment in the creation of

financial data, narrative analysis

and XBRL tagging.

Looking Forward

Combining predictive analytics models with

organizational business knowledge provide

insight into critical issues such as outcome

improvement.

Through measuring uncertainty surrounding

these issues, predictive analytics enables

proactive risk management, refining key

decision making processes through

controlled, iterative testing of potential

actions and their likely intended-and

unintended-consequences. These findings

and their corresponding business rules can

then be deployed within front-line

operational systems to identify measurable

cost savings, repeatable process

improvements, and sustainable competitive

advantages.

41

Looking Forward

42

Success Factors

43

Among the top 10 objectives for the

Finance function over the next 2

years….― hire qualified people and

retain them‖ and ―increase Finance

knowledge‖ (Corporate Finance

Function Survey: The Canadian

Perspective by KPMG)

Passion Capital:

• Passion

• Experience

• Knowledge

Success Factors

Le Service des délégués

commerciaux du Canada Partout où vous faites des affaires

Initiatives de mesure de

rendement soutenant le

Programme commercial

du MAECI

Ministère des Affaires étrangères et du Commerce international

Direction de la Planification et de l’Appui aux services à la clientèle du SDC

IGF – 27 novembre 2012

46

Aperçu de la présentation

• Approche du Service des délégués commerciaux en matière de planification et de mesure du rendement

• Comment sommes-nous arrivés aux fiches de résultats pondérés et l’informatique décisionnelle?

• Tableau de bord de l’Expansion internationale des affaires

• Défis, réalisations et leçons retenues

47

Qu’est-ce que le Service des délégués

commerciaux du Canada? • Composante du Ministère des Affaires

étrangères et du Commerce international du Canada

• Les employés du Service des délégués commerciaux du Canada (SDC) – répartis dans plus de 150 points de par le monde – prodiguent des services aux compagnies canadiennes afin qu’elles obtiennent des succès commerciaux à l’étranger.

• Le mandat de SDC est d’accroître la prospérité des Canadiens et des Canadiennes par l’entremise du commerce international.

• Les délégués commerciaux offrent une variété de services à leurs clients canadiens:

• Préparation aux marchés étrangers • Contacts qualifiés • Évaluation du potentiel de marché • Résolution de problèmes

48

La planification et la mesure du

rendement du programme commercial du

MAECI 1. Rigoureuse planification annuelle

des programmes commerciaux et

économiques

2. Utiliser les outils de mesure du

rendement

3. Gouvernance interne

4. S'assurer que les exigences de

responsabilité soient satisfaites

49

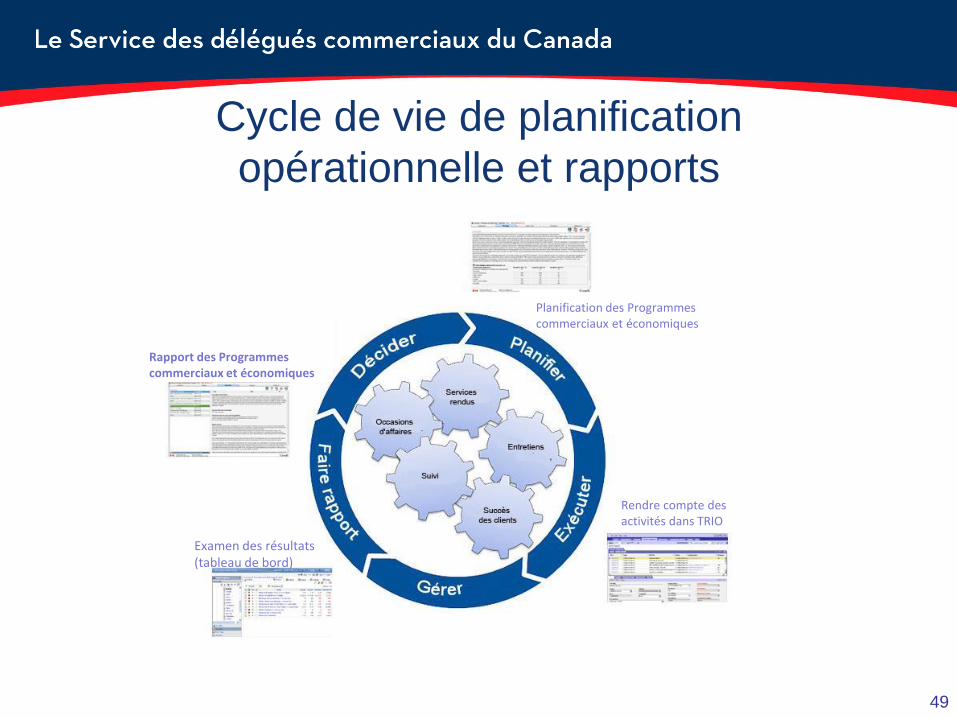

Cycle de vie de planification

opérationnelle et rapports

Examen des résultats (tableau de bord)

Rapport des Programmes commerciaux et économiques

Planification des Programmes commerciaux et économiques

Rendre compte des activités dans TRIO

50

Pourquoi choisir la fiche de résultats

pondérés et l’informatique décisionnelle?

Un cadre commun génère la

cohérence des rapports dans le

monde entier.

Améliore la précision et la

responsabilité de rendre compte

par le Service des délégués

commerciaux.

Renforce l'utilisation des

ressources pour produire des

résultats, en utilisant des données

facilement disponibles et

statistiques

51

Pourquoi utiliser l’approche sur

l’informatique décisionnelle?

• Centralise les informations provenant de multiples systèmes de l'entreprise

• Système transparent qui permet d’augmenter l’imputabilité des gestionnaires

• Facilite l’extraction de données et les capacités de production de rapports

52

À quoi sert le tableau de bord de

l’Expansion internationale des affaires?

• Constitue un élément clé de nos efforts pour suivre les résultats et améliorer les pratiques de gestion

• Offre des renseignements sur les indicateurs qui sont essentiels aux succès de l’organisation et de son programme commercial

• Influence les gestionnaires afin qu’ils se concentrent sur les domaines critiques pour la mission et fournit des renseignements pour la prise de décision

• Présente des données opportunes parce qu’elles sont mises à jour à toutes les fins de semaine

53

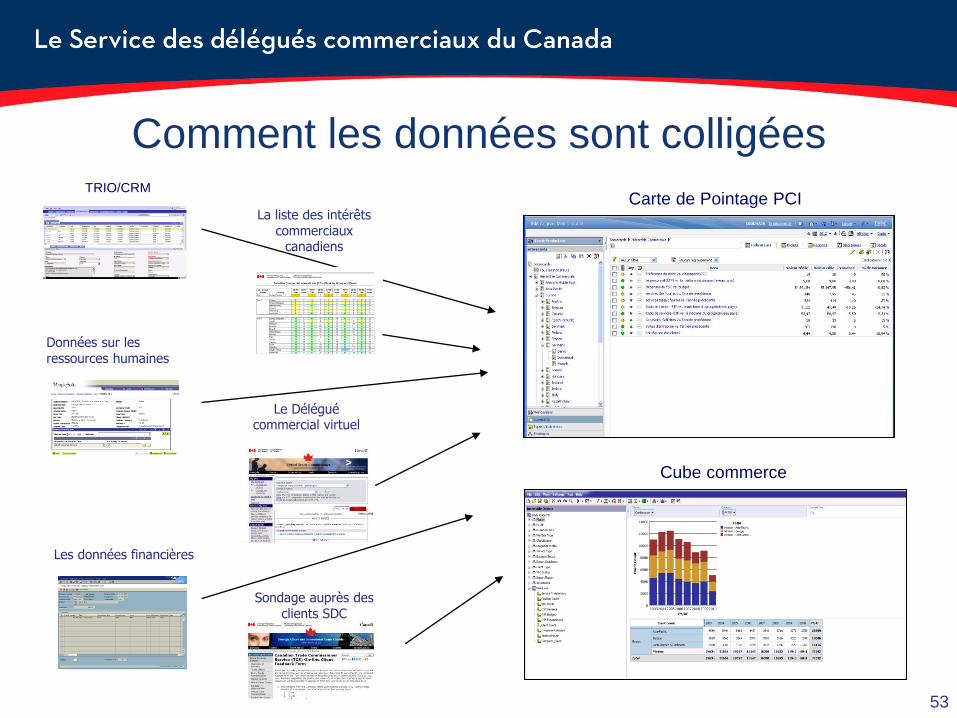

Comment les données sont colligées

Carte de Pointage PCI

Cube commerce

Les données financières

Données sur les ressources humaines

TRIO/CRM

La liste des intérêts commerciaux

canadiens

Le Délégué commercial virtuel

Sondage auprès des clients SDC

54

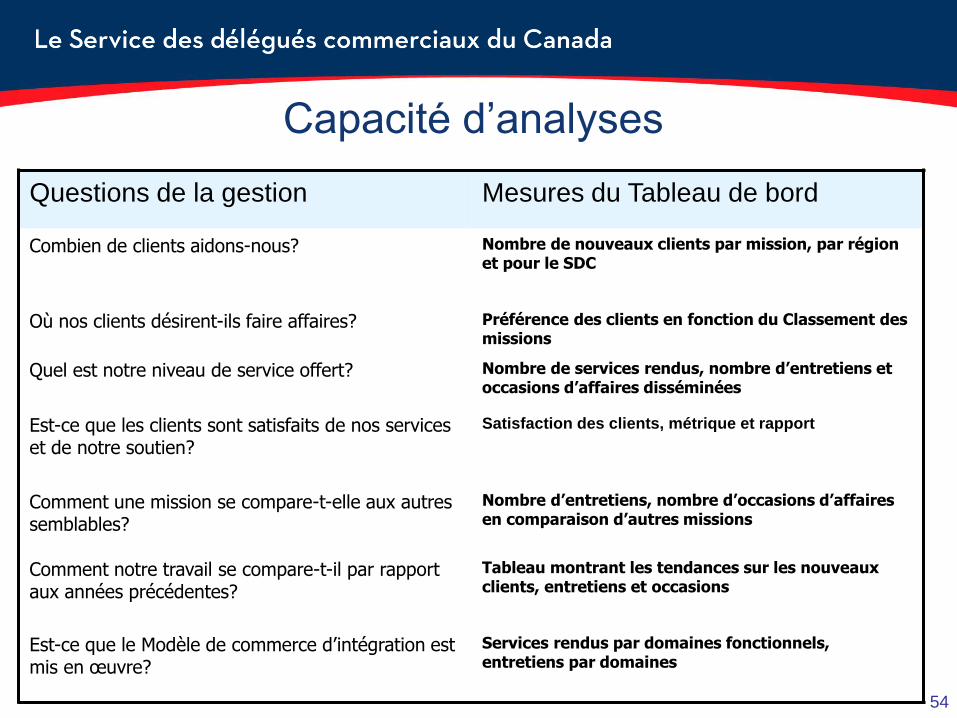

Questions de la gestion Mesures du Tableau de bord

Combien de clients aidons-nous? Nombre de nouveaux clients par mission, par région et pour le SDC

Où nos clients désirent-ils faire affaires? Préférence des clients en fonction du Classement des missions

Quel est notre niveau de service offert? Nombre de services rendus, nombre d’entretiens et occasions d’affaires disséminées

Est-ce que les clients sont satisfaits de nos services et de notre soutien?

Satisfaction des clients, métrique et rapport

Comment une mission se compare-t-elle aux autres semblables?

Nombre d’entretiens, nombre d’occasions d’affaires en comparaison d’autres missions

Comment notre travail se compare-t-il par rapport aux années précédentes?

Tableau montrant les tendances sur les nouveaux clients, entretiens et occasions

Est-ce que le Modèle de commerce d’intégration est mis en œuvre?

Services rendus par domaines fonctionnels, entretiens par domaines

Capacité d’analyses

55

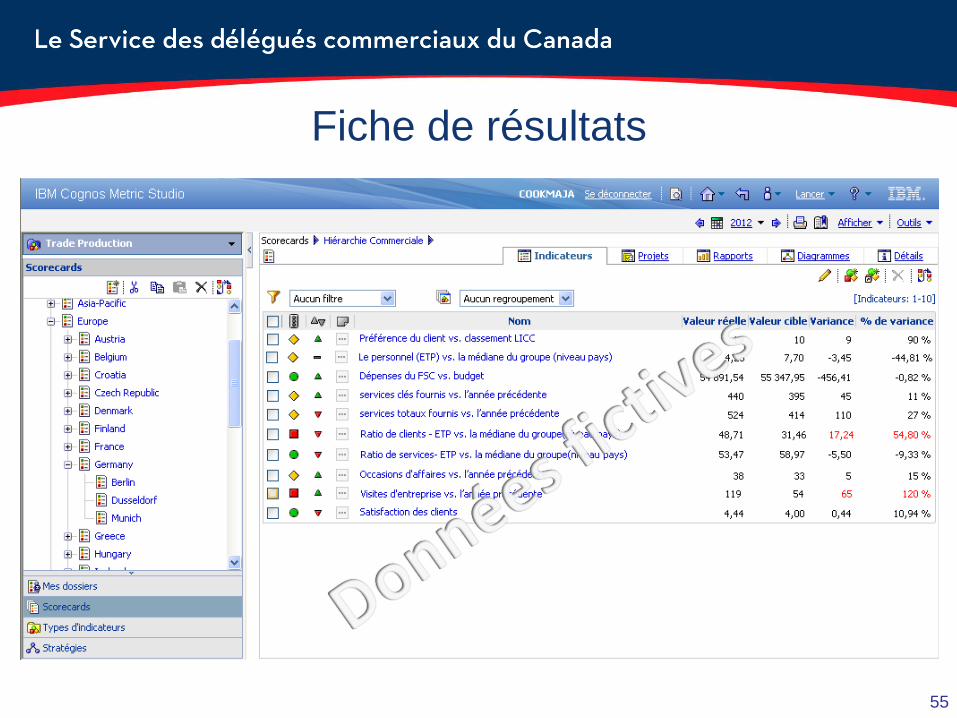

Fiche de résultats

56

Rapports des fiches de résultats

57

Utilité pour la haute direction

• Rapport trimestriel au Conseil de

coordination du commerce international

• Exigences relatives aux rencontres de

breffage

• Données fiables et analyses pour les

équipes d’inspection des missions

• Analyse ad hoc pour des décisions

éclairées

58

Défis Clés

• Définitions/lignes directrices

• Uniformité des rapports

• Formation des

utilisateurs

59

Accomplissements du Tableau de bord

• Met l’accent sur l’imputabilité

• Expose l’importance de l’inscription des données

• Affermit la reddition de compte et améliore la qualité des données dans les systèmes d’entreprise

• Offre un accès rapide à des données pertinentes

60

Leçons retenues

• Tenir des consultations efficaces

• Travailler avec l’informatique pour harmoniser les systèmes corporatifs

• Transparence aide à améliorer la qualité des données et la comformité

• Apprendre des autres et partager les pratiques exemplaires avec les autres ministères

La haute gestion joue un rôle crucial pour mousser l’intérêt sur l’information liée au rendement :

L’information génère l’intérêt pour plus de renseignements

Leçons retenues

61

Avenir de l’informatique décisionnelle

Le MAECI a mis en place un comité de gouvernance sur les activités liées à l’informatique décisionnelle. On a lancé un projet pour trouver les spécialistes en la matière, qui verront à définir les indicateurs de rendement clés pour la création d’une fiche de résultats et d’un tableau de bord à l’échelon sous-ministre adjoint devant servir au Sous-ministre.

• Comité consultatif sur l’informatique décisionnelle

Questions

? ?

?