Languages

Pages

Legal

Value Stream Performance management through lean accountingPerformance measurements that matter in the Lean enterPrise

SAP Insightmanaging Value stream Performance

in standard cost accounting, false precision often occurs in the way product costs are represented. since precision is a limit to accuracy, false precision leads to unjustified confidence in the accuracy of the product cost.

content

4 Executive Summary

5 The Transformation from Standard to Lean Cost Accounting

5 Precision Versus accuracy 6 standard Versus Lean 6 Product Versus Value stream

costing 8 changing Versus not changing

9 Profitability and Cost Management in the Lean Enterprise

9 aligning Lean enterprise Processes

9 one application for a Lean transformation

9 Pulling the Lean accounting Profit Lever

9 Learn more today

About the Author

in his role as manufacturing value network director for saP america inc., Dave strothmann is responsible for building customer communities, providing thought leadership, and influencing product strategy for saP. advancing state-of-the-art software support for lean manufacturing is an area of special interest.

strothmann has 24 years of experience in industrial manufacturing management, software product management, and marketing. this includes 9 years in the software industry for enterprise resource planning and 15 years in the industrial manufacturing industry fulfilling a variety of roles and responsibilities.

strothmann holds a bachelor of science in marketing from northern illinois university.

Dave Strothmann manufacturing Value network DirectorsaP america inc.

in fact, standard accounting methods are actively antilean. they generate wasteful variance reporting processes that nourish endless hours of non- value-added work. they foster batch production and high inventory. they are unable to identify lean improve-ments. and they provide reports that are difficult for people to understand.

instead of fighting against lean, the challenge is to update your managerial and financial accounting methods to align with today’s lean business pro-cesses. a comprehensive lean profit-ability and cost management solution can overcome this challenge. it enables value stream performance management with lean accounting techniques that support enterprise-wide managerial and financial reporting for the lean enterprise.

this powerful tool for lean allows you to create, maintain, and update agile and adaptable analytical models that reflect actual and direct value stream cost and profitability, with little or no allocation of overhead expenses. a lean profitability and cost management solution provides a holistic view of organizational perfor-mance based on the productivity and profitability of lean value streams.

this saP insight explores the trans-formation from standard to lean cost accounting via a lean profitability and

cost management solution and answers the questions you are certain to ask along the way, including the following:• What are the differences between

standard and lean cost accounting methods?

• What impact are my standard account-ing methods having on my lean trans-formation efforts?

• What challenges can we overcome with a profitability and cost manage-ment solution?

• What benefits can we expect to realize by concentrating on the lean value stream?

executiVe Summarythe focus is on VaLue

a lean enterprise is focused on increased value to the customer, the elimination of wasteful work and non-value-added activities, and increased throughput to create opportunities for profitable growth. Because the focus of lean is on value, lean looks at costing from the value stream.

if your company is transforming into a lean enterprise but you still rely on standard costing methods, your lean initiatives could be in jeopardy. standard costing focuses on product costing and cannot support the value stream costing that lies at the heart of lean accounting.

4 SAP Insight – Value stream Performance management through Lean accounting

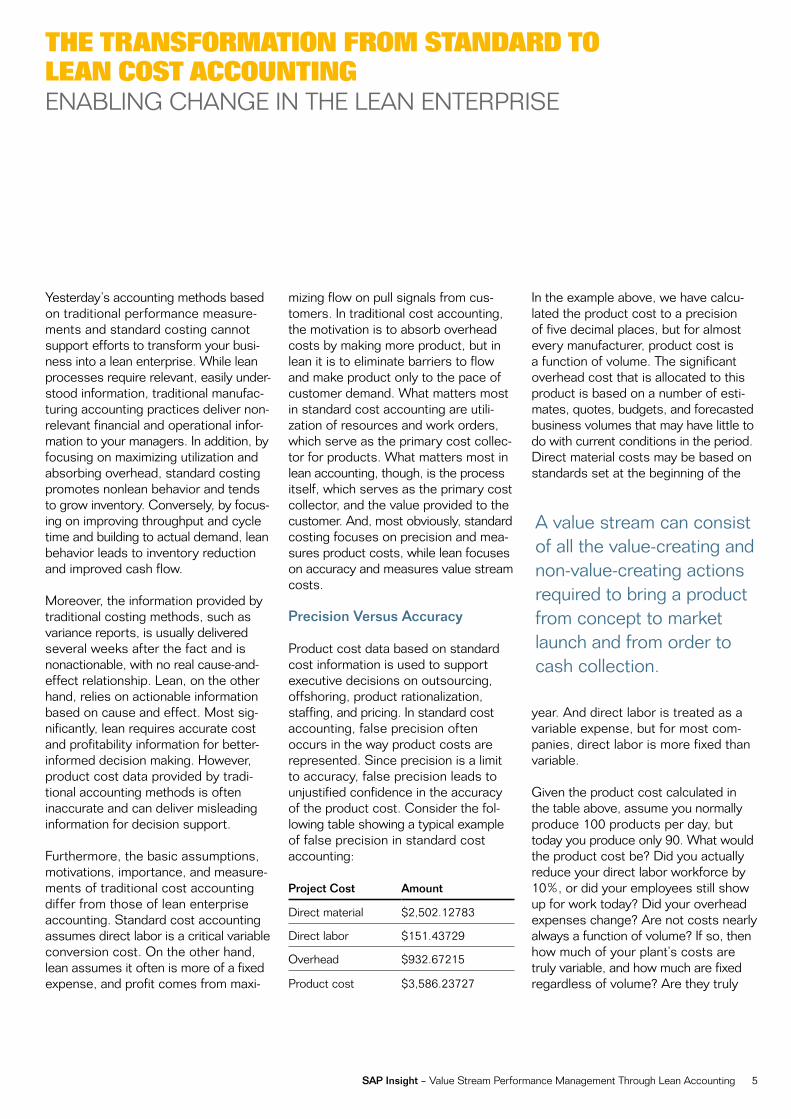

in the example above, we have calcu-lated the product cost to a precision of five decimal places, but for almost every manufacturer, product cost is a function of volume. the significant overhead cost that is allocated to this product is based on a number of esti-mates, quotes, budgets, and forecasted business volumes that may have little to do with current conditions in the period. Direct material costs may be based on standards set at the beginning of the

year. and direct labor is treated as a variable expense, but for most com-panies, direct labor is more fixed than variable.

Given the product cost calculated in the table above, assume you normally produce 100 products per day, but today you produce only 90. What would the product cost be? Did you actually reduce your direct labor workforce by 10%, or did your employees still show up for work today? Did your overhead expenses change? are not costs nearly always a function of volume? if so, then how much of your plant’s costs are truly variable, and how much are fixed regardless of volume? are they truly

Yesterday’s accounting methods based on traditional performance measure-ments and standard costing cannot support efforts to transform your busi-ness into a lean enterprise. While lean processes require relevant, easily under-stood information, traditional manufac-turing accounting practices deliver non-relevant financial and operational infor - mation to your managers. in addition, by focusing on maximizing utilization and absorbing overhead, standard costing promotes nonlean behavior and tends to grow inventory. conversely, by focus-ing on improving throughput and cycle time and building to actual demand, lean behavior leads to inventory reduction and improved cash flow.

moreover, the information provided by traditional costing methods, such as variance reports, is usually delivered several weeks after the fact and is nonactionable, with no real cause-and-effect relationship. Lean, on the other hand, relies on actionable information based on cause and effect. most sig-nificantly, lean requires accurate cost and profitability information for better- informed decision making. however, product cost data provided by tradi-tional accounting methods is often inaccurate and can deliver misleading information for decision support.

furthermore, the basic assumptions, motivations, importance, and measure-ments of traditional cost accounting differ from those of lean enterprise accounting. standard cost accounting assumes direct labor is a critical variable conversion cost. on the other hand, lean assumes it often is more of a fixed expense, and profit comes from maxi-

mizing flow on pull signals from cus-tomers. in traditional cost accounting, the motivation is to absorb overhead costs by making more product, but in lean it is to eliminate barriers to flow and make product only to the pace of customer demand. What matters most in standard cost accounting are utili-zation of resources and work orders, which serve as the primary cost collec-tor for products. What matters most in lean accounting, though, is the process itself, which serves as the primary cost collector, and the value provided to the customer. and, most obviously, standard costing focuses on precision and mea-sures product costs, while lean focuses on accuracy and measures value stream costs.

Precision Versus Accuracy

Product cost data based on standard cost information is used to support executive decisions on outsourcing, offshoring, product rationalization, staffing, and pricing. in standard cost accounting, false precision often occurs in the way product costs are represented. since precision is a limit to accuracy, false precision leads to unjustified confidence in the accuracy of the product cost. consider the fol-lowing table showing a typical example of false precision in standard cost accounting:

the tranSformation from Standard to lean coSt accountingenaBLinG chanGe in the Lean enterPrise

Project Cost Amount

Direct material $2,502.12783

Direct labor $151.43729

overhead $932.67215

Product cost $3,586.23727

a value stream can consist of all the value-creating and non-value-creating actions required to bring a product from concept to market launch and from order to cash collection.

5SAP Insight – Value stream Performance management through Lean accounting

represented properly in your current data? Your product costs may be very precise, but are they really accurate?

Standard Versus Lean

in many respects, standard accounting methods could not be more opposite than they are from lean accounting methods. for example, standard cost-ing methods help to drive large, work-intensive, non-value-added, batch-driven processes – inevitably resulting in higher inventory levels. Lean processes are tight, focused, streamlined, and efficient – designed to result in lower inventory.

standard cost reporting and lean report-ing are different, too, and have different objectives. Lean reporting is intended to identify and analyze lean improvements, small and large, happening throughout the organization, whereas standard accounting reports cannot identify the financial impact of lean improvements. furthermore, because standard costing still measures key performance indica-tors (KPis) like utilization and overhead absorption, the reporting actually works against lean processes – eventually driv-ing up inventory instead of reducing it.

another antilean characteristic of stan-dard cost accounting is that few people in the organization understand the reports that are generated. the dichotomy is that these are the very reports used to make important decisions. add to this the fact that standard accounting uses standard product costs that are inaccu-rate and misleading in decisions con-cerning many aspects of your business, from quoting to pricing and profitability to sourcing and product rationalization – all decisions that impact the bottom line.

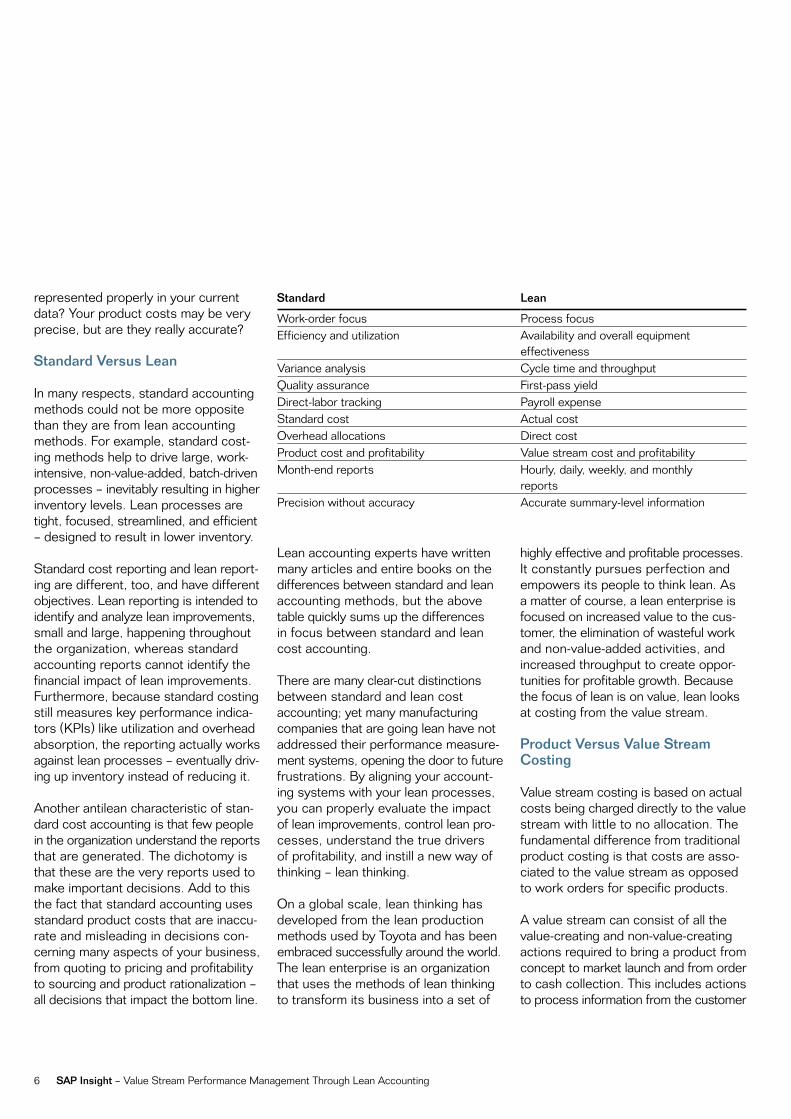

Lean accounting experts have written many articles and entire books on the differences between standard and lean accounting methods, but the above table quickly sums up the differences in focus between standard and lean cost accounting.

there are many clear-cut distinctions between standard and lean cost accounting; yet many manufacturing companies that are going lean have not addressed their performance measure-ment systems, opening the door to future frustrations. By aligning your account-ing systems with your lean processes, you can properly evaluate the impact of lean improvements, control lean pro-cesses, understand the true drivers of profitability, and instill a new way of thinking – lean thinking.

on a global scale, lean thinking has developed from the lean production methods used by toyota and has been embraced successfully around the world. the lean enterprise is an organization that uses the methods of lean thinking to transform its business into a set of

highly effective and profitable processes. it constantly pursues perfection and empowers its people to think lean. as a matter of course, a lean enterprise is focused on increased value to the cus-tomer, the elimination of wasteful work and non-value-added activities, and increased throughput to create oppor-tunities for profitable growth. Because the focus of lean is on value, lean looks at costing from the value stream.

Product Versus Value Stream Costing

Value stream costing is based on actual costs being charged directly to the value stream with little to no allocation. the fundamental difference from traditional product costing is that costs are asso-ciated to the value stream as opposed to work orders for specific products.

a value stream can consist of all the value-creating and non-value-creating actions required to bring a product from concept to market launch and from order to cash collection. this includes actions to process information from the customer

Standard Lean

Work-order focus Process focus efficiency and utilization availability and overall equipment

effectivenessVariance analysis cycle time and throughputQuality assurance first-pass yieldDirect-labor tracking Payroll expensestandard cost actual costoverhead allocations Direct costProduct cost and profitability Value stream cost and profitabilitymonth-end reports hourly, daily, weekly, and monthly

reports Precision without accuracy accurate summary-level information

6 SAP Insight – Value stream Performance management through Lean accounting

used to transform the customer’s prod-uct during the manufacturing process.

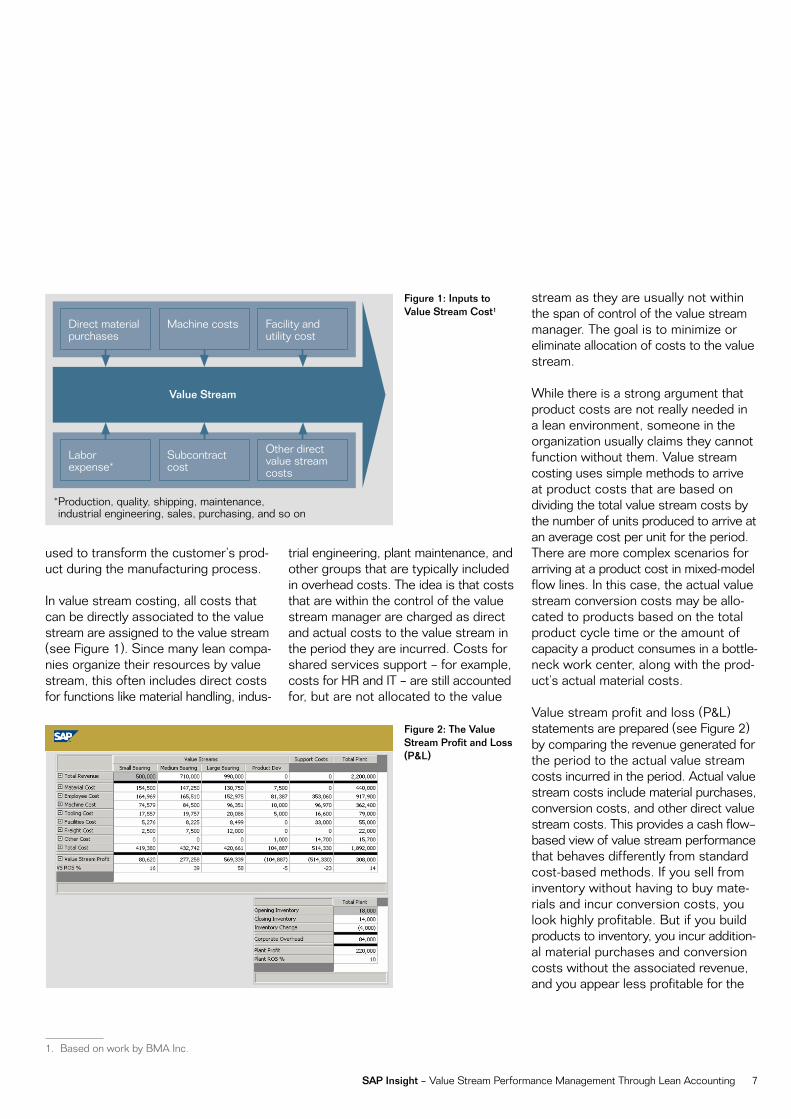

in value stream costing, all costs that can be directly associated to the value stream are assigned to the value stream (see figure 1). since many lean compa-nies organize their resources by value stream, this often includes direct costs for functions like material handling, indus-

trial engineering, plant maintenance, and other groups that are typically included in overhead costs. the idea is that costs that are within the control of the value stream manager are charged as direct and actual costs to the value stream in the period they are incurred. costs for shared services support – for example, costs for hr and it – are still accounted for, but are not allocated to the value

stream as they are usually not within the span of control of the value stream manager. the goal is to minimize or eliminate allocation of costs to the value stream.

While there is a strong argument that product costs are not really needed in a lean environment, someone in the organization usually claims they cannot function without them. Value stream costing uses simple methods to arrive at product costs that are based on dividing the total value stream costs by the number of units produced to arrive at an average cost per unit for the period. there are more complex scenarios for arriving at a product cost in mixed-model flow lines. in this case, the actual value stream conversion costs may be allo-cated to products based on the total product cycle time or the amount of capacity a product consumes in a bottle-neck work center, along with the prod-uct’s actual material costs.

Value stream profit and loss (P&L) statements are prepared (see figure 2) by comparing the revenue generated for the period to the actual value stream costs incurred in the period. actual value stream costs include material purchases, conversion costs, and other direct value stream costs. this provides a cash flow–based view of value stream performance that behaves differently from standard cost-based methods. if you sell from inventory without having to buy mate-rials and incur conversion costs, you look highly profitable. But if you build products to inventory, you incur addition-al material purchases and conversion costs without the associated revenue, and you appear less profitable for the

Figure 1: Inputs to Value Stream Cost1

Figure 2: The Value Stream Profit and Loss (P&L)

Direct material purchases

Labor expense*

machine costs

subcontract cost

facility and utility cost

other direct value stream costs

Value Stream

*Production, quality, shipping, maintenance, industrial engineering, sales, purchasing, and so on

1. Based on work by Bma inc.

7SAP Insight – Value stream Performance management through Lean accounting

period. the value stream and consoli-dated plant-level P&L statements include a return-on-sales calculation that is the primary measure of value stream performance.

also shown on the consolidated plant-level P&L statement are support costs and any non-revenue-generating value

streams, such as new-product develop-ment. these costs are accounted for without being allocated to the value stream. in addition, the change in in -ventory value from the beginning to the end of the period is shown, as well as any corporate overhead tax the plant incurs, which leads to plantwide profit and return on sales percentage.

Changing Versus Not Changing

to be relevant and support today’s technology and business complexities, traditional financial performance mea-surements of companies that invest in lean need to change. Your standard cost variance reports do not deliver the kind of meaningful and actionable information you need to drive lean processes. they actually work against your lean efforts and promote antilean behavior.

there is a better way to manage and control processes and move away from being measured by standard cost variances. a profitability and cost man-agement software application – such as the Businessobjects™ Profitability and cost management application – is one of the cornerstone applications in building the lean enterprise. such an application delivers the costing and value stream performance measure-ments that matter to your organization.

a lean enterprise is focused on increased value to the customer, the elimination of wasteful work and non-value-added activities, and increased throughput to create opportunities for profitable growth. Because the focus of lean is on value, lean looks at costing from the value stream.

a profitability and cost management software application – such as the Businessobjects™ Profit-ability and cost manage-ment application – is one of the cornerstone applica-tions in building the lean enterprise. such an applica-tion delivers the costing and value stream performance measurements that matter to your organization.

8 SAP Insight – Value stream Performance management through Lean accounting

Without a profitability and cost man-agement application, it is difficult and frustrating for many companies to devel-op useful costing and value stream per-formance measurements for reporting and decision support that are consistent and sustainable across the enterprise. this is true even for companies with successful lean enterprise transforma-tions. a comprehensive profitability and cost management application must support value stream performance management in your organization with “lean accounting” tools for relevant, timely information that promotes lean behavior.

Aligning Lean Enterprise Processes

Businessobjects Profitability and cost management enables you to control cost and profitability, and therefore your business. With it, you can maximize profit through superior business infor-mation and agility. the application’s costing models surface the true drivers of profitability in your company. it offers intelligent optimization of all cost and profitability drivers – down to the gran-ular level – and effective and accurate measurement of internal service cost and value stream, product, channel, and customer profitability. it can also greatly reduce your it overhead with Web deployment.

One Application for a Lean Transformation

the Businessobjects Profitability and cost management application combines customer and channel profitability with value stream performance management using lean accounting principles in one

application. it includes a sophisticated costing engine and built-in reporting functionality for direct and actual value stream costing, resource consumption costing, and customer and product prof-itability, together with a predefined data model that allows for lean accounting, and value stream–oriented reporting.

Businessobjects Profitability and cost management also provides advanced decision support functionality with mul-tiple concurrent scenarios. scenarios can be quickly created to simulate the effect on value stream profitability from prod-uct rationalization decisions, offshoring decisions, process improvements, and changes in business volume.

the application can be implemented and used at any point in a lean trans-formation – even prior to your organi-zational changes. the application inte-grates easily with microsoft office and third-party reporting and analysis tools and is designed to work across multiple enterprise resource planning solutions and data sources.

Pulling the Lean Accounting Profit Lever

today, across the manufacturing land-scape, the focus is on value and away from standard cost accounting methods that focus on product instead of value stream costing. for many manufacturing companies, the time to pull the lever on lean accounting is now.

a comprehensive profitability and cost management application helps you meet the challenges of lean accounting. it improves your visibility into true value

stream cost and profitability. it promotes lean behavior and enhances the efficien-cy of cost reporting. and it can deliver accurate product costs based on actual value stream costs for a given period.

finally, transitioning from standard to lean cost accounting really comes down to business benefits. a profitability and cost management application helps you see the drivers of your business with a lean eye – including your value stream, your customers, and your distribution channels. it improves the alignment of your processes by matching your operational requirements with flawless execution of strategy. ultimately, a prof-itability and cost management applica-tion gives you incisive control over cost and profitability with the performance measurements that matter most in a lean enterprise.

Learn more todayfor more information about value stream performance management through lean accounting and how it can transform your lean enterprise, call your saP representative or visit saP on the Web at www.sap.com/solutions /performancemanagement/index.epx.

Profitability and coSt management in the lean enterPriSeenaBLinG a hoListic VieW of orGanizationaL Performance

9SAP Insight – Value stream Performance management through Lean accounting

10 SAP Insight – Value stream Performance management through Lean accounting

www.sap.com/contactsap

50 092 221 (08/10) ©2008 by saP aG. all rights reserved. saP, r/3, xapps, xapp, saP netWeaver, Duet, Partneredge, ByDesign, saP Business ByDesign, and other saP products and services mentioned herein as well as their respective logos are trademarks or registered trademarks of saP aG in Germany and in several other countries all over the world.

Business objects and the Business objects logo, Businessobjects, crystal reports, crystal Decisions, Web intelligence, Xcelsius, and other Business objects products and services mentioned herein as well as their respective logos are trademarks or registered trademarks of Business objects s.a. in the united states and in several other countries all over the world. Business objects is an saP company.

all other product and service names mentioned are the trademarks of their respective companies. Data contained in this document serves informational purposes only. national product specifications may vary.

these materials are subject to change without notice. these materials are provided by saP aG and its affiliated companies (“saP Group”) for informational purposes only, without representation or warranty of any kind, and saP Group shall not be liable for errors or omissions with respect to the materials. the only warranties for saP Group products and services are those that are set forth in the express warranty statements accompanying such products and services, if any. nothing herein should be construed as constituting an additional warranty.

Top Related