Languages

Pages

Legal

‘UNION BUDGET – 2013’effect on Indian automotive sector

Parvez

Onkar

Mithilesh

Chandani

Binod

2

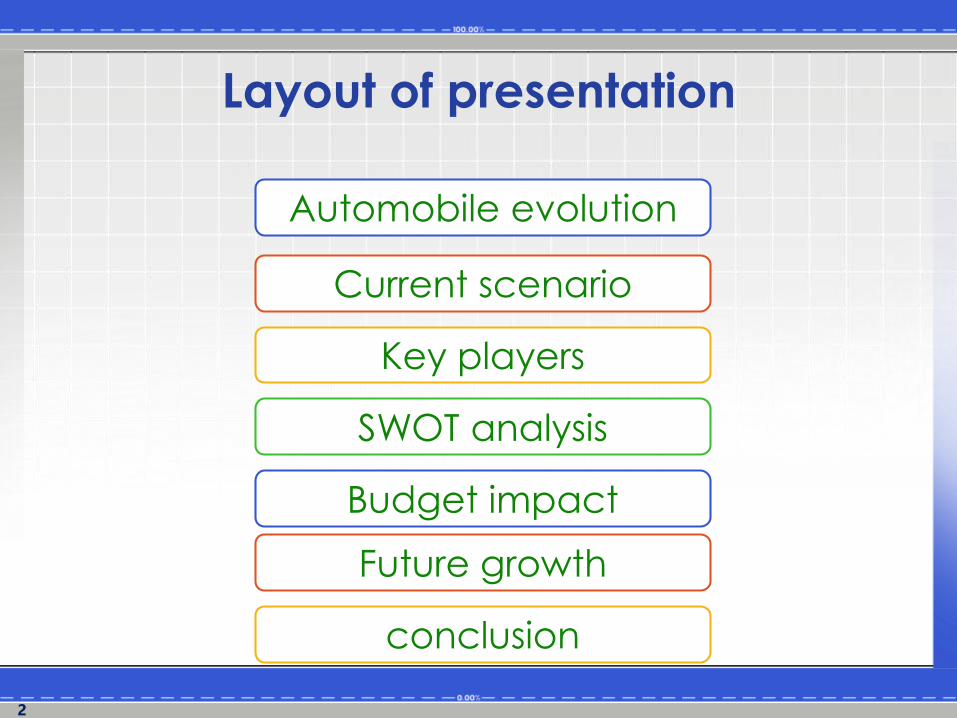

Layout of presentation

Automobile evolution

Current scenario

conclusion

SWOT analysis

Budget impact

Future growth

Key players

3

4

Jeep CJ-3A

5

Indian automobile historyBefore independence car

were imported in India

In 1942 Hindustan Motors Ltd

incorporated

In 1944 Premier Automobiles

Ltd incorporated

In 1983 Maruti Udyog ltd was

started in collaboration with

Suzuki

6

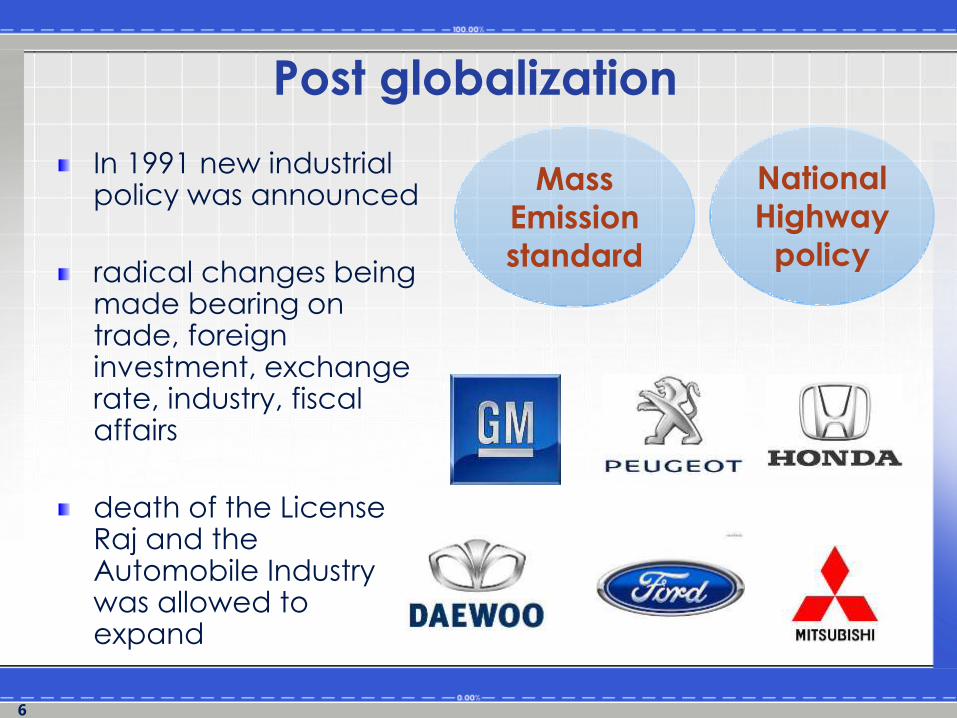

Post globalization

In 1991 new industrial policy was announced

radical changes being made bearing on trade, foreign investment, exchange rate, industry, fiscal affairs

death of the License Raj and the Automobile Industry was allowed to expand

Mass

Emission

standard

National

Highway

policy

7

8

Current market situation

The Indian automotive industry has emerged as a

'sunrise sector' in the Indian economy

India is the second fastest growing automobile

market in the world after China

Car segment is growing @ 19% annually

but is now seeing flat or negative growth rate

Stands 1 in two-wheeler sector

9

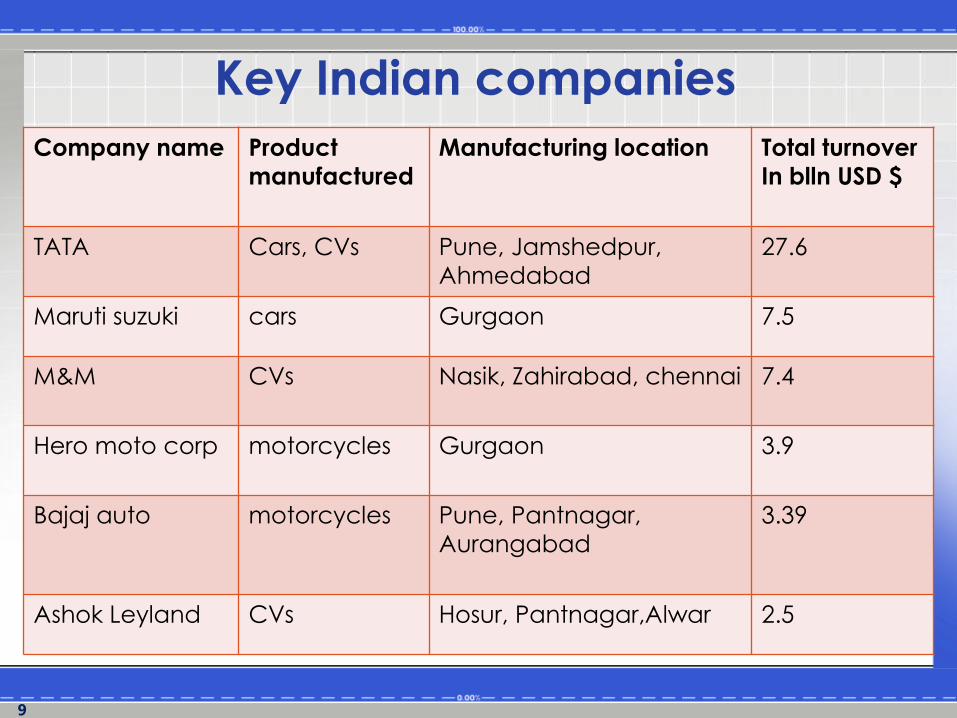

Key Indian companies

Company name Product

manufactured

Manufacturing location Total turnover

In blln USD $

TATA Cars, CVs Pune, Jamshedpur,

Ahmedabad

27.6

Maruti suzuki cars Gurgaon 7.5

M&M CVs Nasik, Zahirabad, chennai 7.4

Hero moto corp motorcycles Gurgaon 3.9

Bajaj auto motorcycles Pune, Pantnagar,

Aurangabad

3.39

Ashok Leyland CVs Hosur, Pantnagar,Alwar 2.5

10

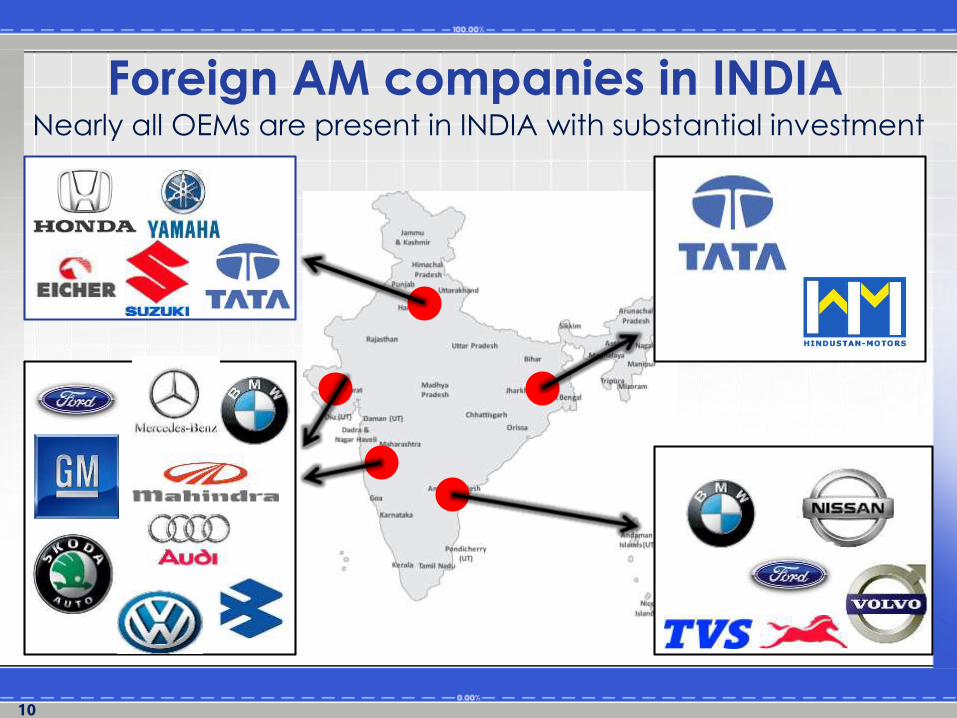

Foreign AM companies in INDIANearly all OEMs are present in INDIA with substantial investment

11

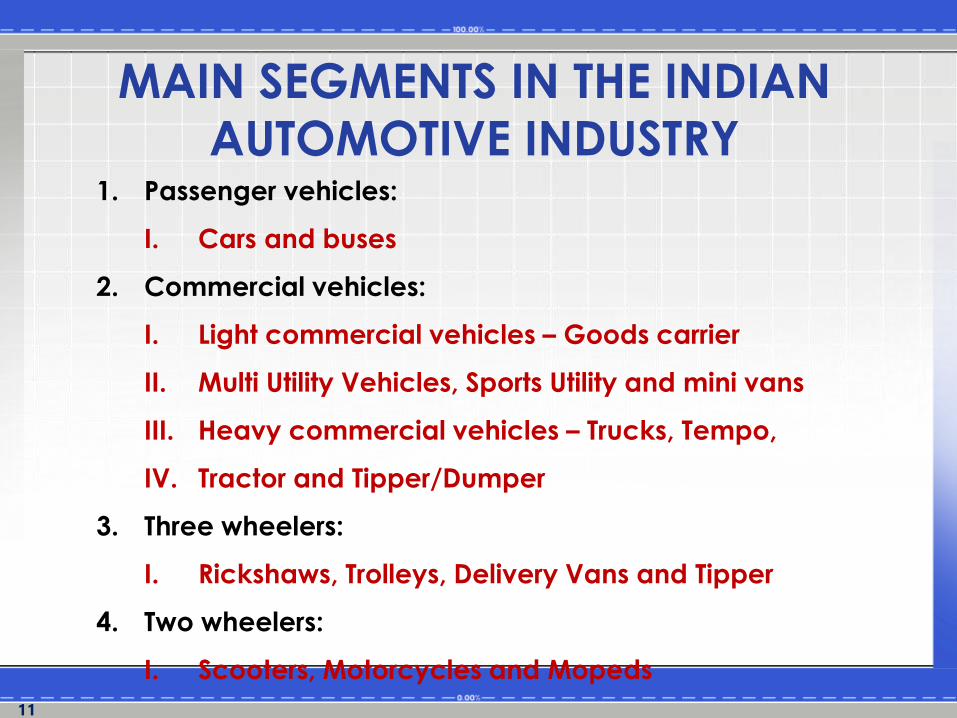

MAIN SEGMENTS IN THE INDIAN

AUTOMOTIVE INDUSTRY 1. Passenger vehicles:

I. Cars and buses

2. Commercial vehicles:

I. Light commercial vehicles – Goods carrier

II. Multi Utility Vehicles, Sports Utility and mini vans

III. Heavy commercial vehicles – Trucks, Tempo,

IV. Tractor and Tipper/Dumper

3. Three wheelers:

I. Rickshaws, Trolleys, Delivery Vans and Tipper

4. Two wheelers:

I. Scooters, Motorcycles and Mopeds

12

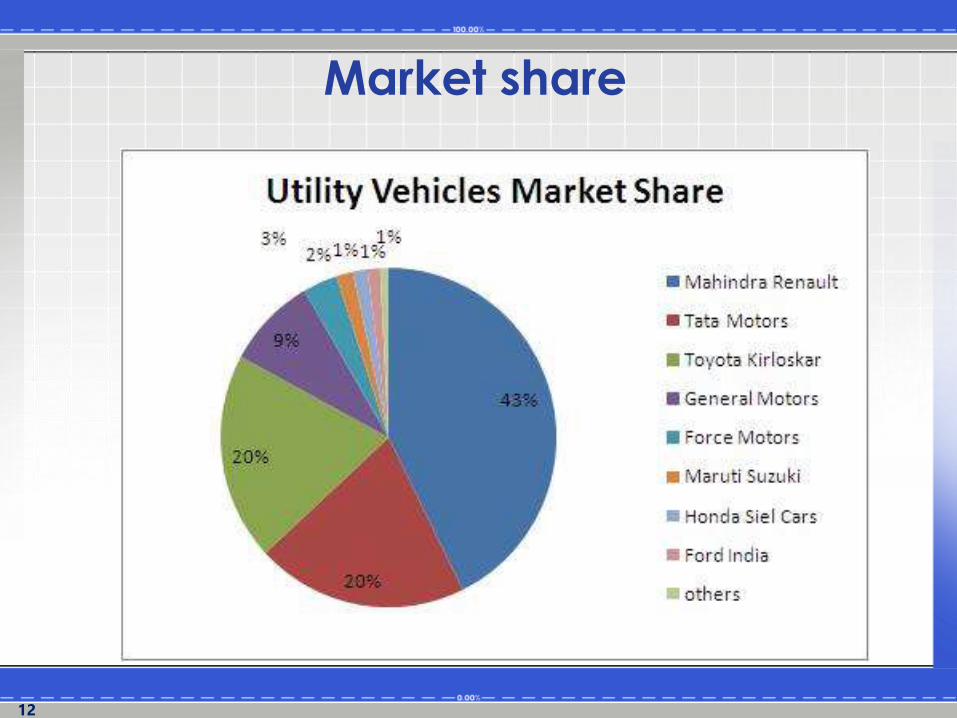

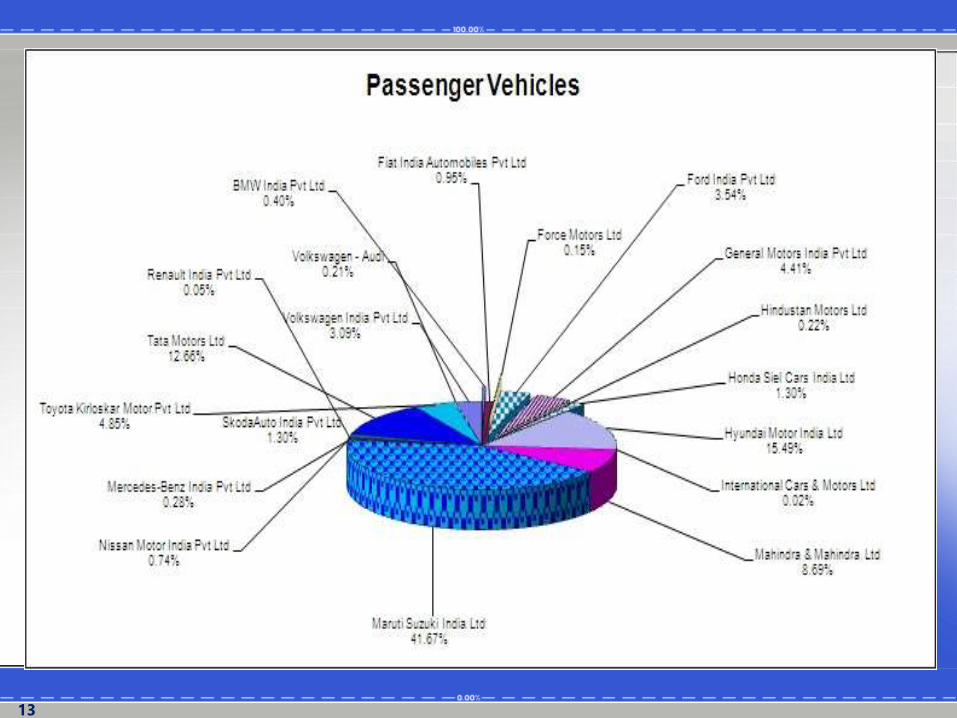

Market share

13

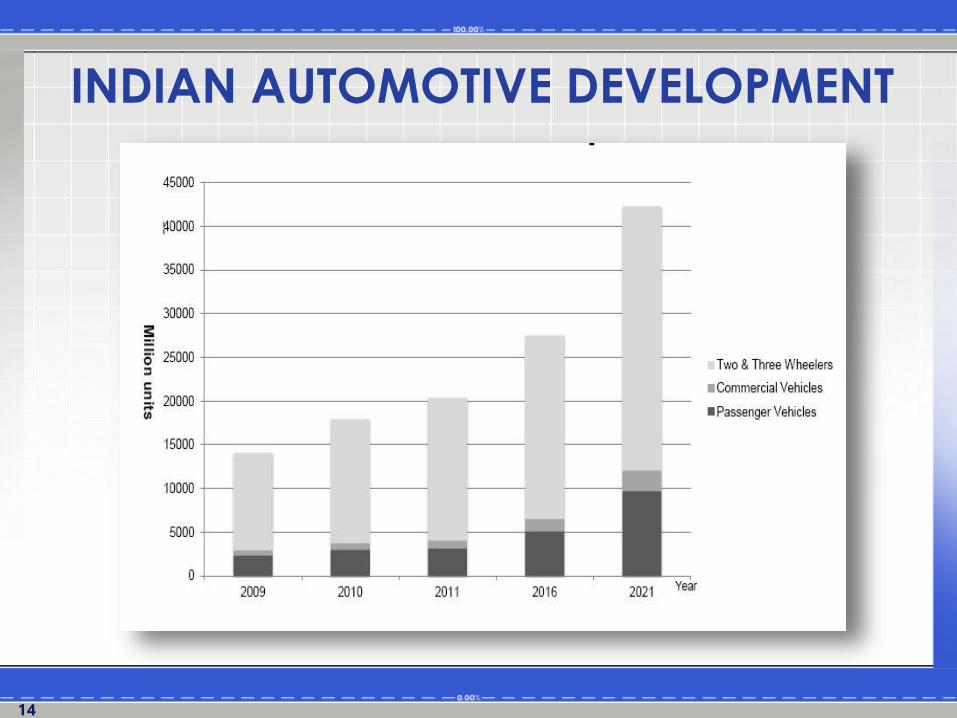

14

INDIAN AUTOMOTIVE DEVELOPMENT

15

16

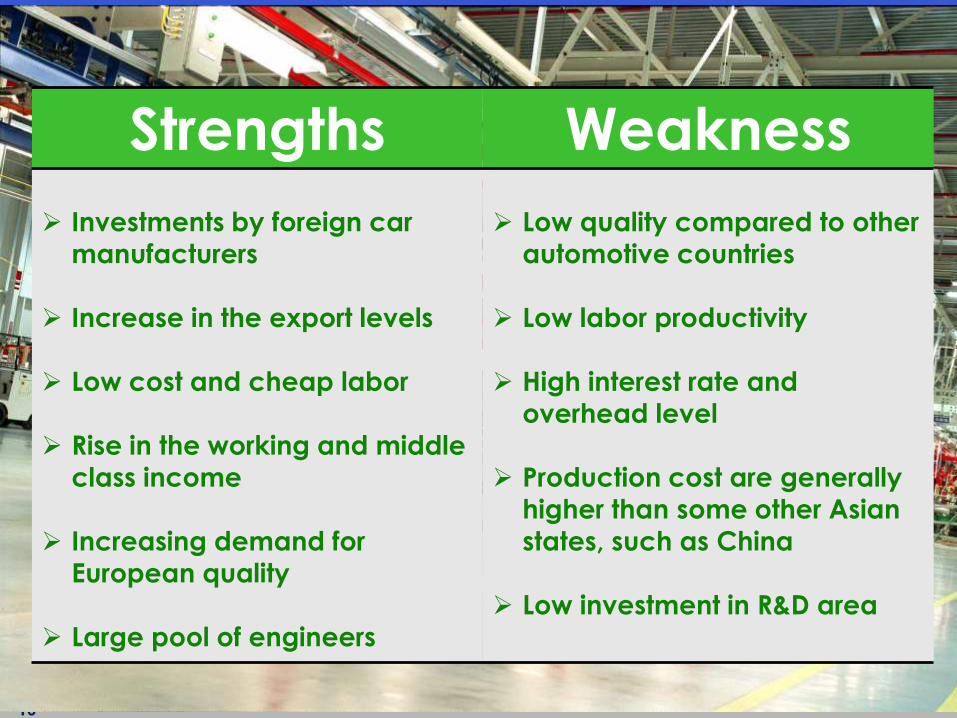

Strengths Weakness

Investments by foreign car

manufacturers

Increase in the export levels

Low cost and cheap labor

Rise in the working and middle

class income

Increasing demand for

European quality

Large pool of engineers

Low quality compared to other

automotive countries

Low labor productivity

High interest rate and

overhead level

Production cost are generally

higher than some other Asian

states, such as China

Low investment in R&D area

17

Opportunities Threats

Growing population in the

country

Focus from the government in

improving the road

infrastructure

Rising living standards

Increase in income level

Better car technology is

demanded

Rising rural demand

Less skilled labor

Lack of technologies for Indian

companies

Increase in the import tariff and

technology cost

Imports of two wheelers from

the Chinese market in India

Smaller players that do not

fulfill international standards

Increased congestion in the urban areas

18

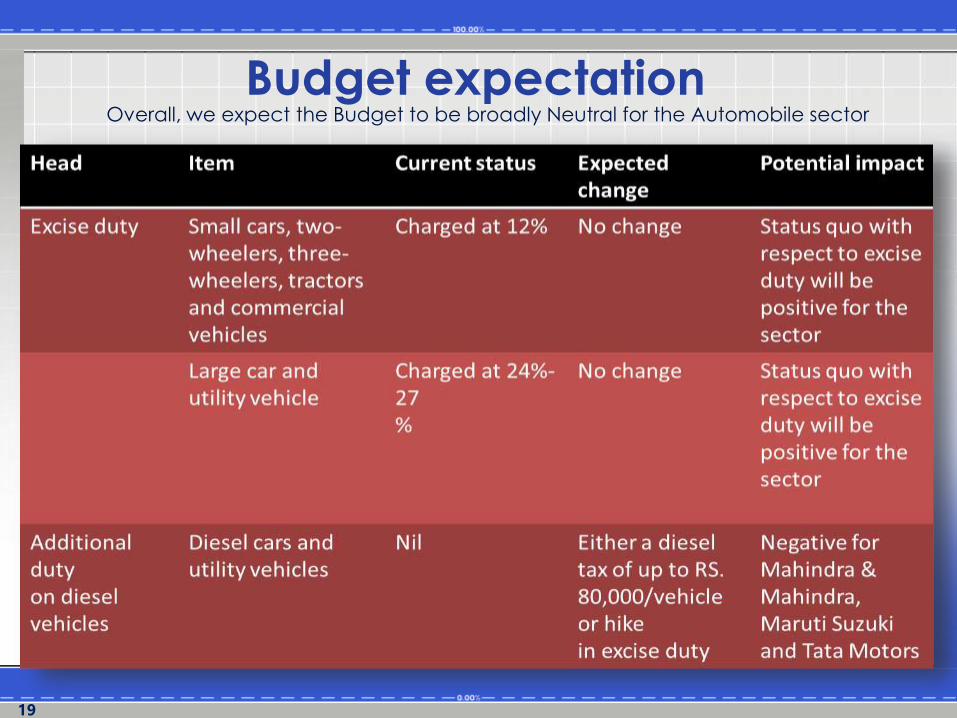

19

Budget expectationOverall, we expect the Budget to be broadly Neutral for the Automobile sector

20

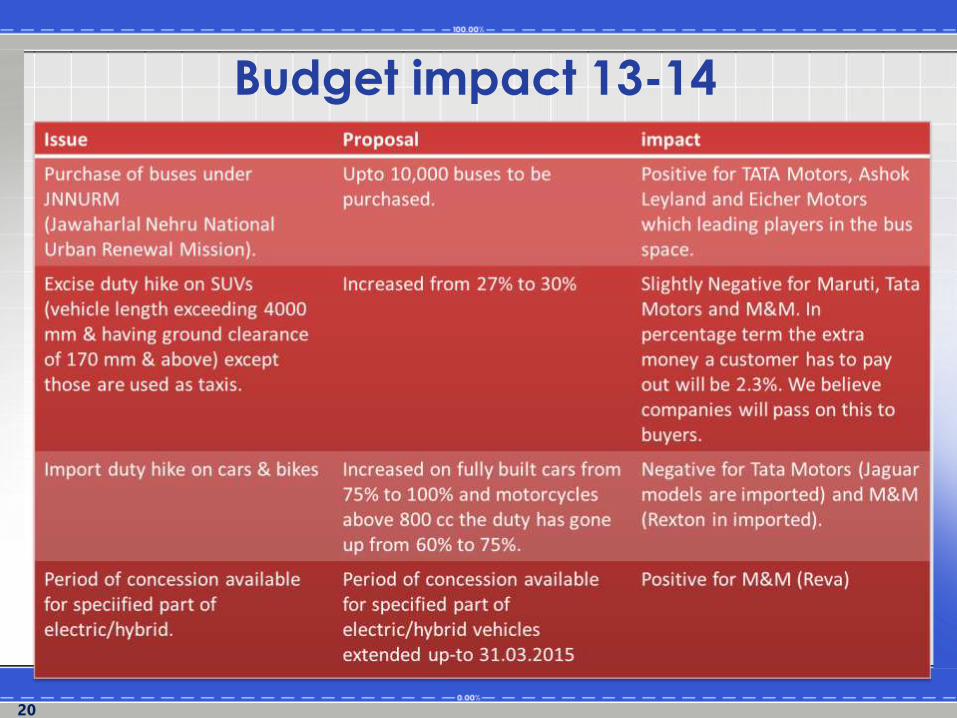

Budget impact 13-14

21

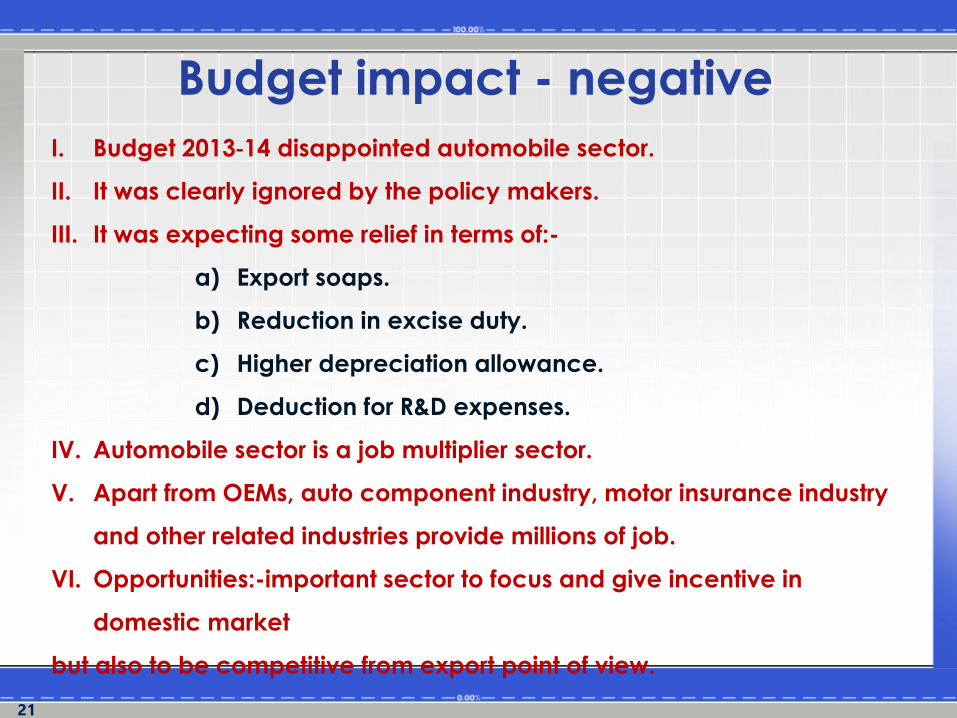

Budget impact - negative

I. Budget 2013‐14 disappointed automobile sector.

II. It was clearly ignored by the policy makers.

III. It was expecting some relief in terms of:-

a) Export soaps.

b) Reduction in excise duty.

c) Higher depreciation allowance.

d) Deduction for R&D expenses.

IV. Automobile sector is a job multiplier sector.

V. Apart from OEMs, auto component industry, motor insurance industry

and other related industries provide millions of job.

VI. Opportunities:-important sector to focus and give incentive in

domestic market

but also to be competitive from export point of view.

22

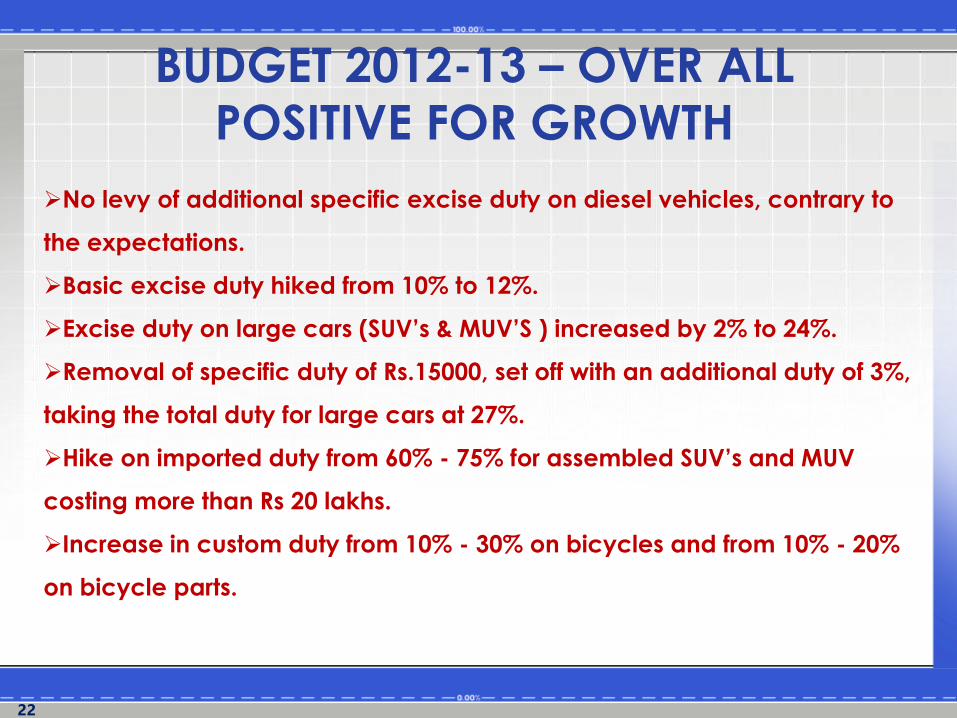

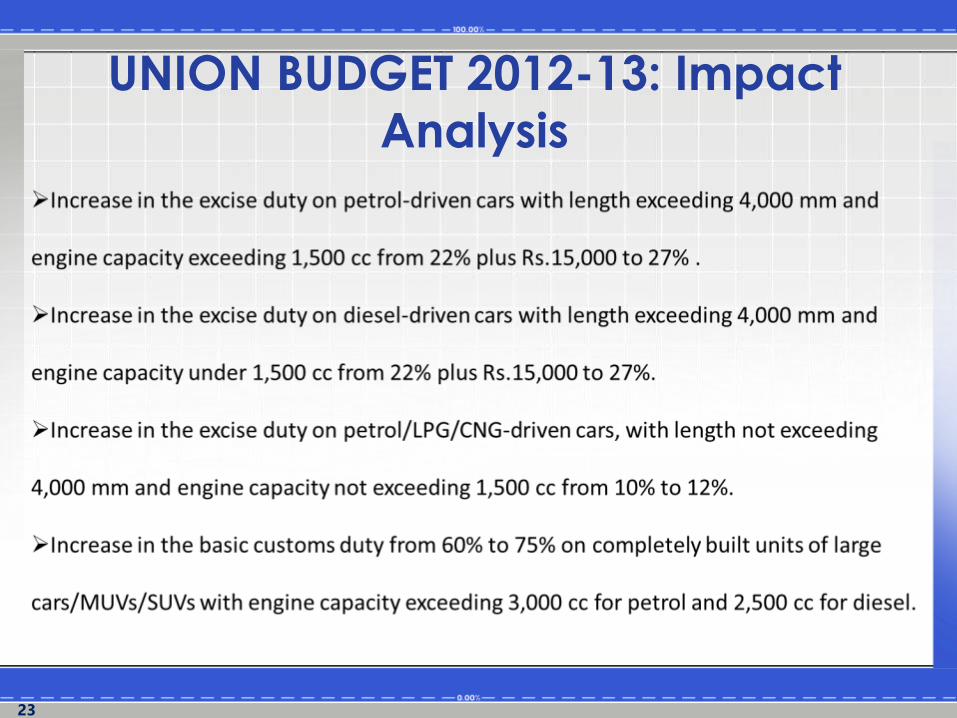

BUDGET 2012-13 – OVER ALL

POSITIVE FOR GROWTH

No levy of additional specific excise duty on diesel vehicles, contrary to

the expectations.

Basic excise duty hiked from 10% to 12%.

Excise duty on large cars (SUV’s & MUV’S ) increased by 2% to 24%.

Removal of specific duty of Rs.15000, set off with an additional duty of 3%,

taking the total duty for large cars at 27%.

Hike on imported duty from 60% - 75% for assembled SUV’s and MUV

costing more than Rs 20 lakhs.

Increase in custom duty from 10% - 30% on bicycles and from 10% - 20%

on bicycle parts.

23

UNION BUDGET 2012-13: Impact

Analysis

24

25

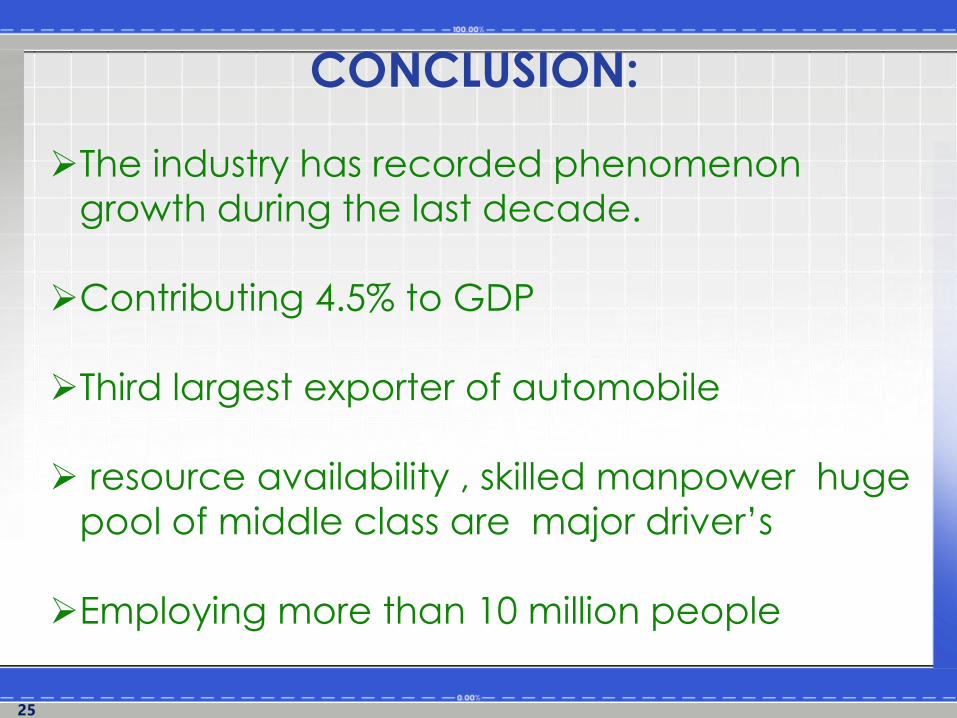

CONCLUSION:

The industry has recorded phenomenon

growth during the last decade.

Contributing 4.5% to GDP

Third largest exporter of automobile

resource availability , skilled manpower huge

pool of middle class are major driver’s

Employing more than 10 million people

26

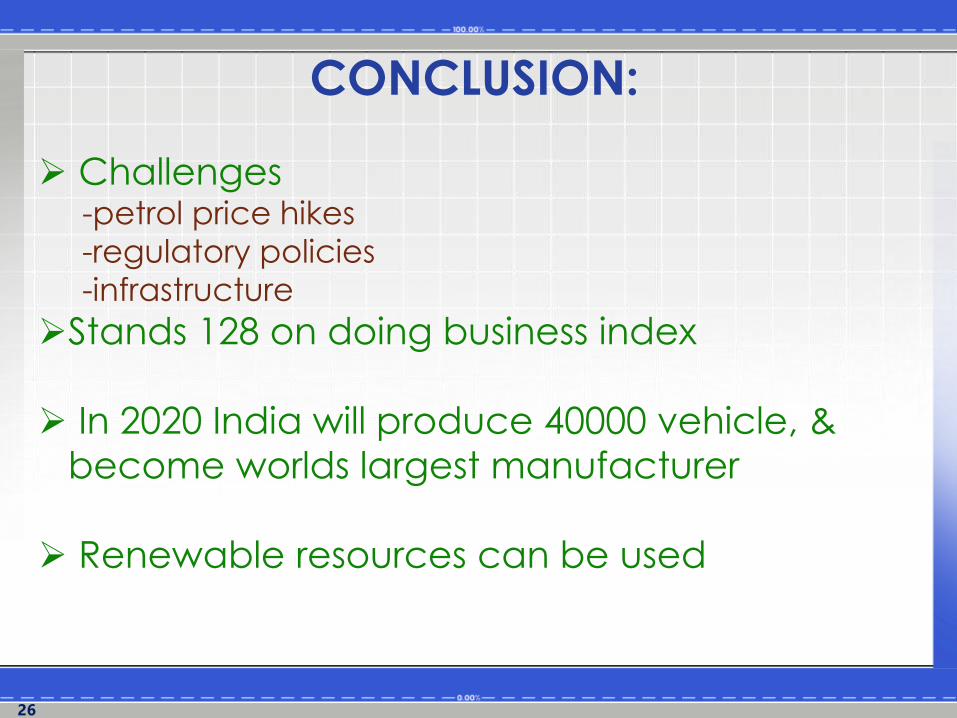

CONCLUSION:

Challenges-petrol price hikes

-regulatory policies

-infrastructure

Stands 128 on doing business index

In 2020 India will produce 40000 vehicle, &

become worlds largest manufacturer

Renewable resources can be used

27

Top Related