Languages

Pages

Legal

Unilever New Zealand Limited

Annual report

For the year ended 31 December 2017

Annual report

For the year ended 31 December 2017

Contents

Auditor's report

Corporate information

Annual report

Consolidated statement of comprehensive income

Consolidated statement of financial position

Consolidated statement of changes in equity

Consolidated statement of cash flows

Notes to the consolidated financial statements

Unilever New Zealand Limited

Page

3

4

5

6

7

8

9

ndeoendent Auditor's Reoort To the shareholders of Unilever New Zealand Limited

Report on the consolidated financial statements

OpinionIn our opInIon, tile ;,ccon1pm1yI11g consolidated

ti11a11c1al statements ot U11ilever New Zeala11d

L1rrnted ltl1e comp,myl ,md its subs1d1ar1es ltile

group) or1 paqes 5 TO 23

presenr ta111v 111 ;,II rn;,wr,al respects the Group·s

fr11crnc1al posItIon ;,s at 37 December 2017 and

its frm-111c1al pertorrnar1ce and casl1 tlows tor t11e

vear ended rn1 nrnt cJate. and

11 comply wItl1 Nr,w ZE,aland Equ1vale11ts to

l11term1tIonal F1r1nnc1;,I Report111q Standards

Reduced D1scloswe Reg1rne

� Basis for opinion

We have audited tile accor11pc1I 1yIng consolidated

trna11c1al statements which comprise

tile consolidated stiltcmerlt ot ti11anc1;,I posItI011

as at 3 7 Decembe1 20 l 7.

tile consolidated stilrnrnent of conHJrehe11sIve

I11corne. co11sol1datcd st,1WrneI11 ot changes 111

equity and consolldaWcJ statement ot casll

flows tor tl1e year tlwn emJed. a11d

notes. 111clud1ng a sLmirnc1rv o1 s1g11ificant

account111g policies and other expl,rnatory

1ntormat1or1

We conducted our audit in accordance with International Standards on Auditing (New Zealand) ('ISAs (NZ)'). We

believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

We are independent of the group in accordance with Professional and Ethical Standard 1 (Revised) Code of

Ethics for Assurance Practitioners issued by the New Zealand Auditing and Assurance Standards Board and the

International Ethics Standards Board for Accountants' Code of Ethics for Professional Accountants (IESBA

Code), and we have fulfilled our other ethical responsibilities in accordance with these requirements and the

IESBA Code.

Our responsibilities under ISAs (NZ) are further described in the auditor's responsibilities for the audit of the

consolidated financial statements section of our report.

Other than in our capacity as auditor we have no relationship with, or interests in, the group.

·-

l _ Other informationThe Directors, on behalf of the group, are responsible for the other information included in the entity's Annual

Report. Our opinion on the consolidated financial statements does not cover any other information and we do

not express any form of assurance conclusion thereon.

In connection with our audit of the consolidated financial statements our responsibility is to read the other

information and, in doing so, consider whether the other information is materially inconsistent with the

consolidated financial statements or our knowledge obtained in the audit or otherwise appears materially

misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this

other information, we are required to report that fact. We have nothing to report in this regard.

$

£fi Use of this independent auditor's report

This independent auditor's report is made solely to the shareholders as a body. Our audit work has been

undertaken so that we might state to the shareholders those matters we are required to state to them in the

independent auditor's report and for no other purpose. To the fullest extent permitted by law, we do not accept

or assume responsibility to anyone other than the shareholders as a body for our audit work, this independent

auditor's report, or any of the opinions we have formed.

A Responsibilities of the Directors for the consolidated financial statements The Directors, on behalf of the company, are responsible for:

- the preparation and fair presentation of the consolidated financial statements in accordance with generally

accepted accounting practice in New Zealand (being New Zealand Equivalents to International Financial

Reporting Standards Reduced Disclosure Regime);

- implementing necessary internal control to enable the preparation of a consolidated set of financial

statements that is fairly presented and free from material misstatement, whether due to fraud or error; and

- assessing the ability to continue as a going concern. This includes disclosing, as applicable, matters related

to going concern and using the going concern basis of accounting unless they either intend to liquidate or to

cease operations, or have no realistic alternative but to do so.

x,l,.. Auditor's responsibilities for the audit of the consolidated financial statements

Our objective is:

- to obtain reasonable assurance about whether the consolidated financial statements as a whole are free

from material misstatement, whether due to fraud or error; and

- to issue an independent auditor's report that includes our opinion.

Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance

with ISAs NZ will always detect a material misstatement when it exists.

Misstatements can arise from fraud or error. They are considered material if, individually or in the aggregate,

they could reasonably be expected to influence the economic decisions of users taken on the basis of these

consolidated financial statements.

A further description of our responsibilities for the audit of these consolidated financial statements is located at

the External Reporting Board (XRB) website at:

http://www. xrb.govt. nz/sta n da rds-for-ass u ra nce-p ractitioners/a ud itors-responsi bi I iti es/audit-re port-7 /

This description forms part of our independent auditor's report.

KPMG

Sydney

29 March 2018

2

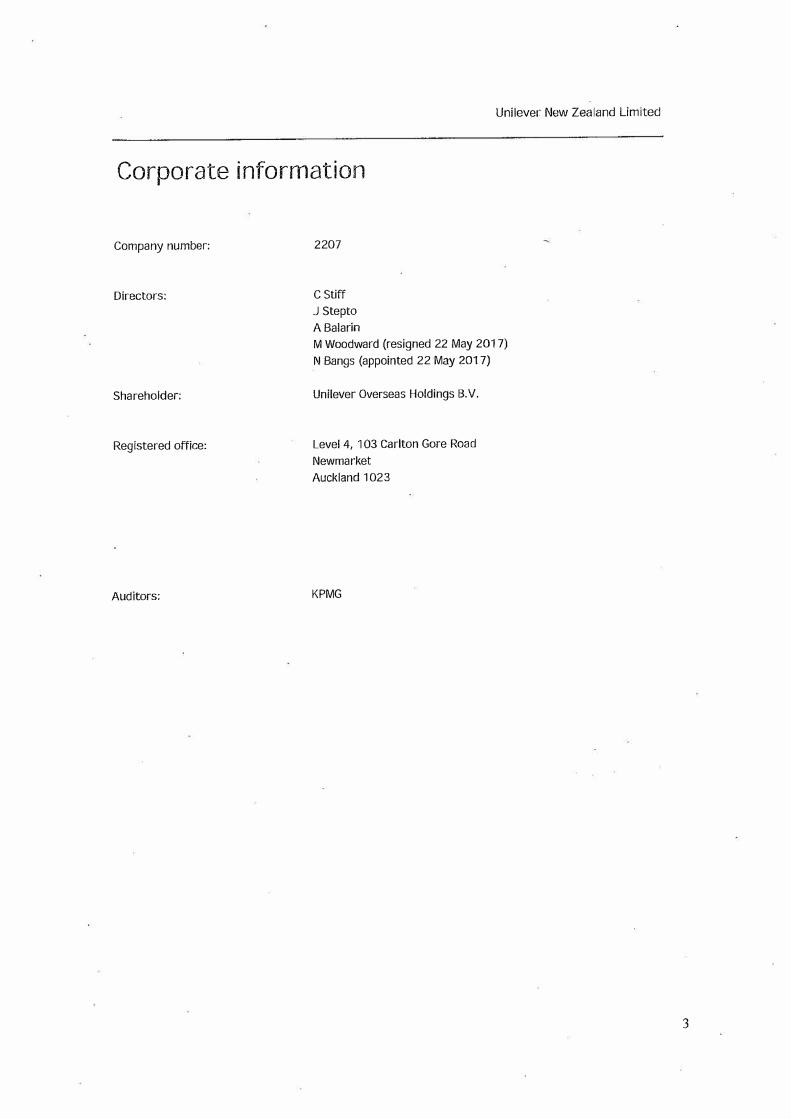

Unilever New Zealand Limited

Corporate information

Company number:

Directors:

Shareholder:

Registered office:

Auditors:

2207

C Stiff

J Stepto

A Balarin

M Woodward (resigned 22 May 2017)

N Bangs (appointed 22 May 2017)

Unilever Overseas Holdings B.V.

Level 4, 103 Carlton Gore Road

Newmarket

Auckland 1023

KPMG

3

Unilever New Zealand Limited

Annual report For the year ended 31 December 2017

The Board of Directors present their Annual Report including the financial statements of the company for the

year ended 31 December 2017 and the auditor's report thereon.

The shareholders of the company have exercised their right under section 211 (3) of the Companies Act 1993

('the Act") and unanimously agreed that this Annual Report need not comply with any of paragraphs (a), and

(e) to (i) of section 211 (1) of the Act.

Signed on behalf of the

C Stiff

Director

J Stepto

Director

29 March 2018

of Directors:

4

Unilever New Zealand Limited

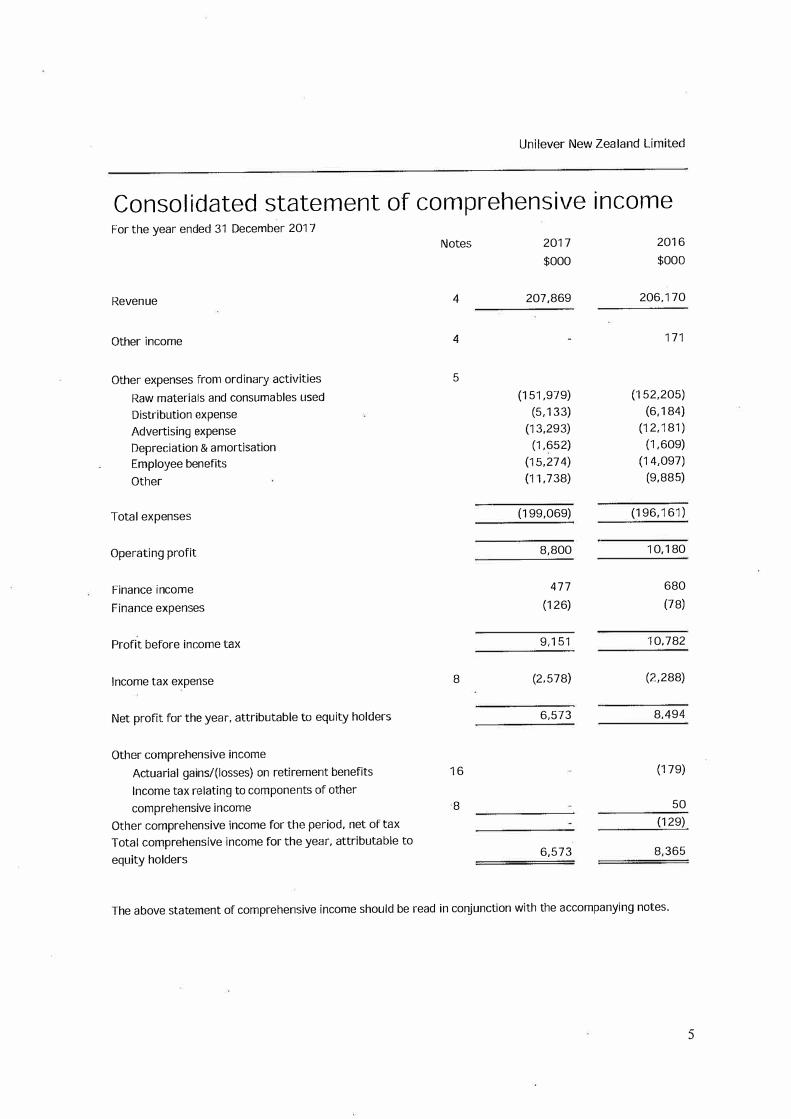

Consolidated statement of comprehensive income For the year ended 31 December 2017

Notes 2017 2016

$000 $000

Revenue 4 207,869 206,170

Other income 4 171

Other expenses from ordinary activities 5

Raw materials and consumables used (151,979) (152,205)

Distribution expense (5,133) (6,184) Advertising expense (13,293) (12,181)

Depreciation & amortisation (1,652) (1,609) Employee benefits (15,274) (14,097)

Other (11,738) (9,885)

Total expenses (199,069) (196,161)

Operating profit 8,800 10,180

Finance income 477 680

Finance expenses (126) (78)

Profit before income tax 9,151 10,782

Income tax expense 8 (2,578) (2,288)

Net profit for the year, attributable to equity holders 6,573 8.494

Other comprehensive income

Actuarial gains/(losses) on retirement benefits 16 (179)

Income tax relating to components of other

comprehensive income 8 50

Other comprehensive income for the period, net of tax (129)

Total comprehensive income for the year, attributable to

equity holders 6,573 8,365

The above statement of comprehensive income should be read in conjunction with the accompanying notes.

5

Unilever New Zealand Limited

Consolidated statement of financial position As at 31 December 2017

Notes 2017 2016

Current assets $000 $000

Cash and cash equivalents 31,326 30,373

Trade and other receivables 6 16,054 18,057

Inventories 7 2,206 1,759

Income tax refund due 124

49,586 50,313

Non-current assets

Property, plant and equipment 9 5,324 5,775

Intangible assets 10 22,534 22,916

Deferred income tax asset 8 1,316 922

29,174 29,613

Total assets 78,760 79,926

Current liabilities

Trade and other payables 11 16,426 17,544

Interest bearing liabilities 12 3,100 3,521

Income tax liabilities 1,829

Provisions 13 87 80

21,442 21,145

Non-current liabilities

Provisions 13 274 252

274 252

Total liabilities 21,716 21,397

Net assets 57,044 58,529

Equity

Contributed equity 14 48,684 48,684

Reserves 210 222

Retained earnings 8,150 9,623

Total equity 57,044 58,529

The above consolidated statement of financial position should be read in conjunction with the accompanying

notes.

For and on behalf

Director

Board who authorised these financial statements for issue on 29 March 2018:

J Stepto

Director

6

Unilever New Zealand Limited

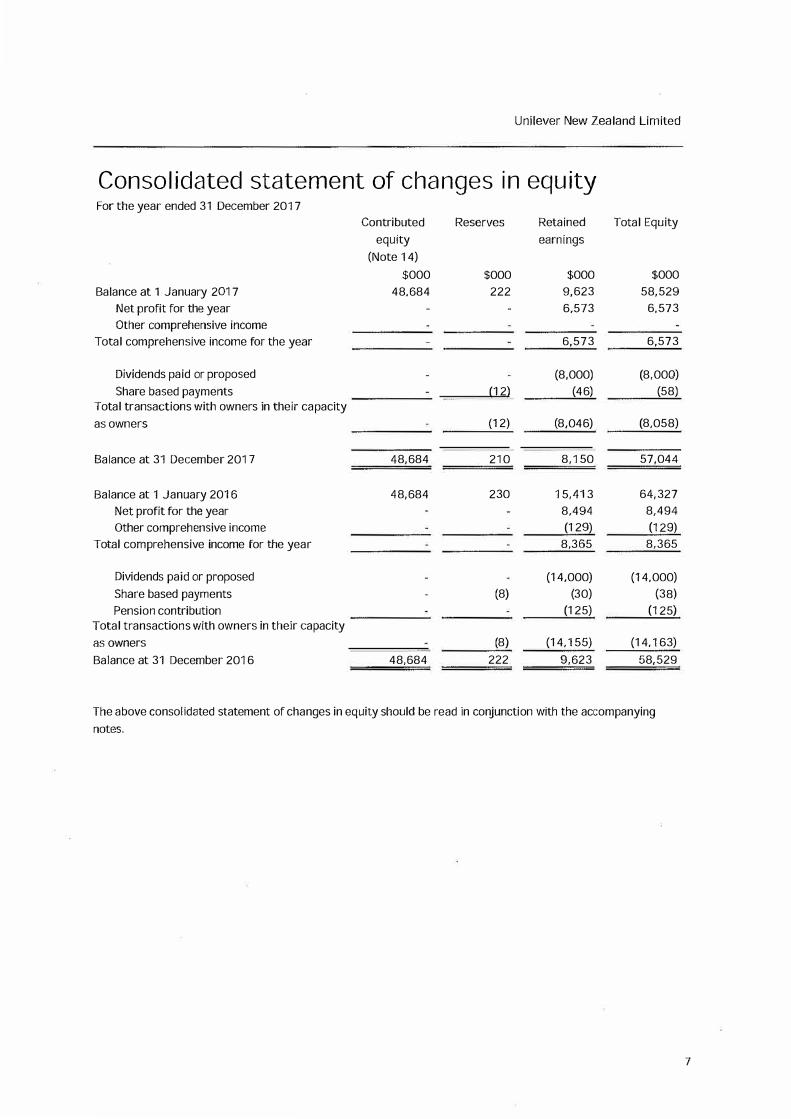

Consolidated statement of changes in equity For the year ended 31 December 2017

Contributed Reserves Retained Total Equity

equity earnings

(Note 14)

$000 $000 $000 $000

Balance at 1 January 2017 48,684 222 9,623 58,529

Net profit for the year 6,573 6,573 Other comprehensive income

Total comprehensive income for the year 6,573 6,573

Dividends paid or proposed (8,000) (8,000) Share based payments (12) (46) (58)

Total transactions with owners in their capacity

as owners (12) (8,046) (8,058)

Balance at 31 December 2017 48,684 210 8,150 57,044

Balance at 1 January 2016 48,684 230 15,413 64,327

Net profit for the year 8.494 8.494

Other comprehensive income (129) (129)Total comprehensive income for the year 8,365 8,365

Dividends paid or proposed (14,000) (14,000) Share based payments (8) (30) (38) Pension contribution (125) (125)

Total transactions with owners in their capacity

as owners (8) (14,155) (14.163)

Balance at 31 December 2016 48,684 222 9,623 58,529

The above consolidated statement of changes in equity should be read in conjunction with the accompanying

notes.

7

Unilever New Zealand Limited

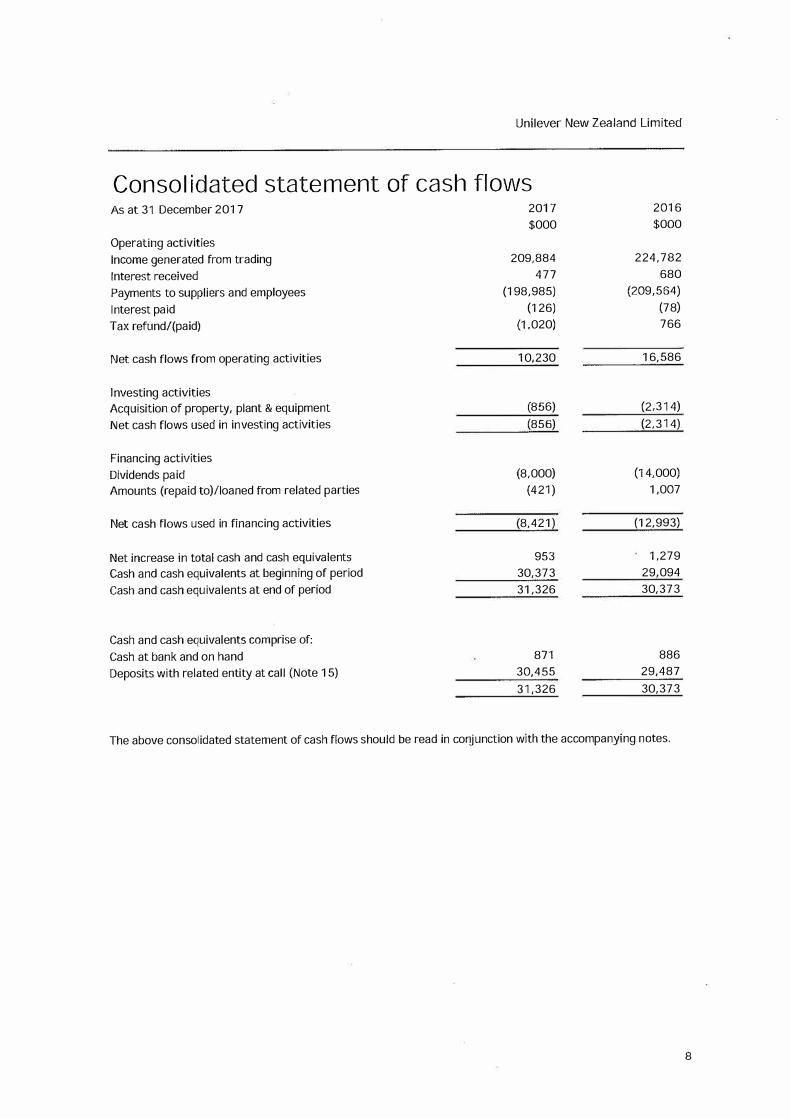

Consolidated statement of cash flows As at 31 December 2017

Operating activities

Income generated from trading

Interest received

Payments to suppliers and employees

Interest paid

Tax refund/(paid)

Net cash flows from operating activities

Investing activities Acquisition of property, plant & equipment

Net cash flows used in investing activities

Financing activities

Dividends paid Amounts (repaid to)/loaned from related parties

Net cash flows used in financing activities

Net increase in total cash and cash equivalents Cash and cash equivalents at beginning of period

Cash and cash equivalents at end of period

Cash and cash equivalents comprise of:

Cash at bank and on hand

Deposits with related entity at call (Note 15)

2017

$000

209,884

477

(198,985)

(126)

(1,020)

10,230

(856)

(856)

(8,000)

(421)

(8,421)

953

30,373

31,326

871

30,455

31,326

2016

$000

224,782

680

(209,564)

(78)

766

16,586

(2,314)

(2,314)

(14,000)

1,007

(12,993)

1,279

29,094

30,373

886

29,487

30,373

The above consolidated statement of cash flows should be read in conjunction with the accompanying notes.

8

Unilever New Zealand Limited

Notes to the consolidated financial statements For the year ended 31 December 2017

Corporate information

The consolidated financial statements of Unilever New Zealand Limited ("the company") and its subsidiaries (together

referred to as "the group") for the year ended 31 December 2017 were authorised for issue in accordance with a

resolution of directors.

Unilever New Zealand Limited is incorporated in New Zealand under the Companies Act 1993.

The nature of the operations and principal activities of the group during the year include the sale of detergents, personal

products, culinary foods, edible fats, ice cream, tea and other products. There has been no change in the principal

activities of the group during the year.

2 Summary of significant accounting policies

a) Basis of preparation

The consolidated financial statements have been prepared in accordance with generally acceptable accounting

practice (NZ GAAP) in New Zealand. They comply with New Zealand equivalents to International Financial Reporting

Standards - Reduced Disclosure Regime ("NZ IFRS RDR""), as appropriate for a Tier 2 for-profit entity.

The group is a Tier 2 for-profit entity and has elected to report in accordance with Tier 2 for-profit accounting

standards as issued by the External Reporting Board (XRB). The company is eligible to report in accordance with Tier

2 for-profit accounting standards on the basis it is not publicly accountable and it is not a large for-profit public

sector entity.

The consolidated financial statements are presented in New Zealand dollars and all values are rounded to the nearest

thousand dollars ($000) unless stated otherwise.

b) Statement of compliance

The financial statements have been prepared in accordance with New Zealand equivalents to International Financial

Reporting Standards Reduced Disclosure Regime (NZ IFRS RDR).

c) Basis of consolidation

The consolidated financial statements comprise the operations of the company and its subsidiaries as at 31

December each year.

Subsidiaries are consolidated from the date on which the group gains control and cease to be consolidated from the

date on which the group loses control. Subsidiaries use consistent accounting policies of the group to recognise

transactions and have the same balance date.

Subsidiaries are all those entities over which the group has the power to govern the financial and operating policies

so as to obtain benefits from their activities. The existence and effect of potential voting rights that are currently

exercisable or convertible are considered when assessing whether a group controls another entity.

All material transactions between subsidiaries or between the company and subsidiaries are eliminated on

consolidation. The results of subsidiaries acquired or disposed of during the year are included in the consolidated

statement of comprehensive income from the date of acquisition or the date of disposal.

A change in the ownership interest of a subsidiary, without a loss of control, is accounted for as an equity

transaction.

9

Unilever New Zealand Limited

Notes to the consolidated financial statements For the year ended 31 December 2017

d) Business combinations

Business combinations are accounted for using the acquisition method. The acquisition method of accounting

involves recognising at acquisition date, separately from goodwill, the identifiable assets acquired, liabilities assumed

and any non-controlling interest in the acquiree. The identifiable assets acquired and liabilities assumed are

measured at their acquisition date fair values. Acquisition-related costs are expensed as incurred and recognised in

profit or loss.

The difference between the above items and the fair value of the consideration is recorded as either goodwill or

discount on acquisition. After initial recognition, goodwill is measured at cost less any accumulated impairment

losses. For the purpose of impairment testing, goodwill acquired in a business combination is, from the acquisition

date, allocated to each of the group's cash-generating units expected to benefit from the combination, irrespective of

whether other assets or liabilities of the acquiree are assigned to those units.

Goodwill is tested annually for impairment, or immediately if events or changes in circumstances indicate that it

might be impaired and carried at cost less accumulated impairment losses. Impairment losses on goodwill are not

reversed.

e) Foreign currency transactions

Transactions in foreign currencies are initially recorded in the functional currency by applying the exchange rates

ruling at the date of the transaction. Foreign exchange gains and losses resulting from the settlement of such

transactions and from the translation at year-end exchange rates of monetary assets and liabilities denominated in

foreign currencies are recognised in profit or loss.

f) Revenue

Revenue is recognised and measured at the fair value of the consideration received or receivable. Amounts

disclosed as revenue are net of returns, trade allowances, rebates and duties and taxes paid. Sales are recorded

when goods have been delivered to a customer, pursuant to a sales order and the associated risks have been passed

to the customer.

Rental income

Income from rental and sub-leased property is recognised on a straight-line basis over the term of the lease.

Interest income

Interest income is recognised as interest accrues using the effective interest method.

g) Income tax

Income tax assets and liabilities are measured at the amount expected to be recovered from or paid to taxation

authorities. The tax rates and tax laws used to compute the amount are those enacted or substantively enacted at

balance date.

Deferred income tax is provided on all temporary differences at the balance date between the tax bases of assets and

liabilities and their carrying amounts for financial reporting purposes.

Deferred income tax is calculated using the liability method on temporary differences between the carrying amounts

of assets and liabilities and their tax bases. However, deferred tax is not provided on the initial recognition of

goodwill or on the initial recognition of an asset or liability unless the related transaction is a business combination or

affects tax or accounting profit or on the investment in subsidiaries where there is no probability in the foreseeable

future that the temporary difference will reverse and taxable profit will be available against which the temporary

difference can be utilised.

10

Unilever New Zealand Limited

Notes to the consolidated financial statements For the year ended 31 December 2017

g) Income tax (continued)Deferred tax assets are recognised to the extent it is probable the underlying tax loss or deductible temporarydifference will be able to be utilised against future taxable income. This is assessed based ·on the group's forecast offuture operating results, adjusted for significant non-taxable income and expenses and specific limits on the use ofany unused tax losses or credits.

Changes in deferred tax assets or liabilities are recognised as a component of tax income or expense in profit or loss,except where they relate to items that are recognised in other comprehensive income or directly in equity, in whichcase the related deferred tax is also recognised in other comprehensive income or equity, respectively.

h) Property, plant and equipmentProperty, plant and equipment are recorded at cost less accumulated depreciation and impairment. Initial costincludes purchase consideration and those costs attributable to bringing the asset to the location and conditionnecessary for its intended use.

Subsequent expenditure relating to an item of property, plant and equipment is added to its gross carrying amountwhen such expenditure either increases the future economic benefits, or is necessarily incurred to enable futureeconomic benefits to be obtained. The carrying amount of any replaced part is derecognised.

All other repairs and maintenance expenditure is recoqnised in profit or loss as incurred.

Depreciation is calculated on a straight line base over the estimated useful life of the asset. The residual value ofassets is reviewed and adjusted if appropriate at each balance date. The following rates have been used:

- Plant and equipment- Leasehold improvements

Disposal

7%- 25% 2.50%

An item of property, plant and equipment is derecognised upon disposal or when no further future economic benefits are expected from its use or disposal. Any gain or loss arising on derecognition of the asset (calculated as the difference between the net disposal proceeds and the carrying amount of the asset) is included in profit or loss in the year the asset is derecognised.

i) Impairment of non-financial assetsIntangible assets with an indefinite useful life are not subject to amortisation and are tested annually for impairment.

Intangible assets subject to amortisation and all other non-financial assets are reviewed for impairment wheneverevents or changes in circumstances indicate that the carrying amount may not be recoverable.

The recoverable amount is the higher of an asset's fair value less costs to sell and value in use. For the purposes of assessing impairment, assets are compared at the lowest levels for which there are separately identifiable cash inflows (cash-generating units).

If any such indication exists and where the carrying values exceed the estimated recoverable amount, the assets arewritten down to their recoverable amount.

Impaired non-financial assets, other than goodwill, are tested for possible reversal of the impairment wheneverevents or changes in circumstances indicate that the impairment may have reversed.

11

Unilever New Zealand Limited

Notes to the consolidated financial statements For the year ended 31 December 2017

j) Intangible assets (excluding goodwill)Intangible assets are carried at cost less any accumulated amortisation and impairment losses. Internally generatedintangible assets, excluding capitalised development costs, are not capitalised and expenditure is recognised in profitor loss in the year in which the expenditure is incurred.

The useful lives of intanQible assets are assessed to be either finite or indefinite.

Intangible assets with finite lives are amortised over the useful life and assessed for impairment whenever there is an indication that the intangible asset may be impaired. The amortisation period and the amortisation method for an intangible asset with a finite useful life is reviewed at least at each financial year-end. The amortisation expense on intangible assets with finite lives is recognised in profit or loss.

Intangible assets with indefinite useful lives are not amortised but are assessed for impairment annually either individually or at the cash-generating unit level. The assessment of indefinite life is reviewed annually to determine whether the indefinite life continues to be supportable. If not, the change in the useful life is made on a prospective basis.

A summary of the policies applied to the group's intangible assets is as follows: Computer software - finite, amortised on a straiqht line basis over 5 yearsDistribution riqhts - infinite

Gains or losses arising from derecognition of an intangible asset are measured as the difference between the net disposal proceeds and the carrying amount of the asset and are recognised in profit or loss when the asset is derecognised.

Research and development

Research costs are expensed as incurred.

An intangible asset arising from development expenditure on an internal project is recognised only when the group can demonstrate the technical feasibility of completing the intangible asset so that it will be available for use or sale, its intention to complete and its ability to use or sell the asset, how the asset will generate future economic benefits, the availability of resources to complete the development and the ability to measure reliably the expenditure attributable to the intangible asset during its development. Following initial recognition of the development expenditure, the cost model is applied requiring the asset to be carried at cost less any accumulated amortisation and impairment losses. Any expenditure capitalised is amortised over the period of expected benefit from the related project.

Subsequent expenditure

Subsequent expenditure relating to intangible assets is added to its gross carrying amount when such expenditure either increases the future economic benefits, or is necessarily incurred to enable future economic benefits to be obtained.

12

Unilever New Zealand Limited

Notes to the consolidated financial statements For the year ended 31 December 2017

k) Inventories

Inventories are stated at the lower of cost or net realisable value.

Cost comprises the purchase price of finished goods and direct materials, on a weighted average basis, import duties,

transport and handling costs and, where applicable, direct labour and an appropriate proportion of variable and

fixed overhead expenditure, the later being allocated on the basis of normal operating capacity.

Net realisable value is the estimated selling price in the ordinary course of business less the estimated costs of

completion and the estimated costs necessary to make the sale.

I) Financial instruments

All financial instruments are initially recognised at the fair value of the consideration received/transferred less, in the

case of financial assets and liabilities not recorded at fair value through profit or loss, directly attributable

transaction costs. Subsequently the group applies the following accounting policies for financial instruments:

Cash and cash equivalents

Cash and cash equivalents comprise cash at bank and in hand and short-term deposits with an original maturity of

three months or less that are readily convertible to known amounts of cash and which are subject to an insignificant

risk of changes in value.

Loans and receivables

Loans and receivables consist of trade and other receivables (note 6). Loans and receivables are carried at

amortised cost using the effective interest method. Gains and losses are recognised in profit or loss when the loans

and receivables are derecognised or impaired. These are included in current assets, except for those with maturities

greater than 12 months after balance date, which are classified as non-current.

Financial liabilities

Financial liabilities at amortised cost consist of trade and other payables (note 11) and interest-bearing liabilities

(note 12).

Trade payables and other payables are recognised when the group becomes obliged to make future payments

resulting from the purchase of goods and services. The amounts are unsecured and usually paid within 30 days of

recognition. Trade payables are not discounted given their short term nature.

Financial liabilities at amortised cost are measured using the effective interest rate (ElR) method. Gains and losses

are recognised in profit or loss when the liabilities are derecognised as well as through the ElR amortisation process.

Financial liabilities are classified as current liabilities unless the group has an unconditional right to defer settlement

of the liabilities for at least 12 months after balance date.

m) Impairment of financial assets

Financial assets are assessed for indicators of impairment at balance date. Financial assets are impaired where there

is objective evidence, as a result of one or more events occurring after initial recognition, the estimated future cash

flows have been impacted.

For financial assets carried at amortised cost, the amount of the impairment is the difference between the asset's

carrying amount and the present value of the estimated future cash flows, discounted at the original effective

interest rate.

13

Unilever New Zealand Limited

Notes to the consolidated financial statements For the year ended 31 December 2017

m) Impairment of financial assets (continued)

The carrying amount of the financial asset is reduced by the impairment loss directly for all financial assets with the

exception of trade receivables where the carrying amount is reduced through the use of an allowance provision.

When a trade receivable is uncollectible, it is written off against the allowance provision. A trade receivable is

deemed to be uncollectible upon notification of insolvency of the debtor or upon similar evidence the group will be

unable to collect the trade receivable. Changes in the carrying amount of the allowance account are recognised in

profit or loss.

If, in a subsequent period the amount of the impairment loss decreases and the decrease can be related objectively

to an event occurring after the impairment loss was recognised, the previously recognised impairment loss is

reversed.

n) Employee benefits

Wages, salaries, and annual leaveLiabilities for wages and salaries, including non-monetary benefits, and annual leave expected to be settled within 12

months of the reporting date are recognised in respect of employees' services up to the reporting date. They are

measured at the amounts expected to be paid when the liabilities are settled.

Long service leave

The liability for long service leave is measured as the present value of expected future payments to be made in

respect of services provided by employees up to the reporting date using the projected unit credit method.

Consideration is given to expected future wage and salary levels, experience of employee departures and periods of

service. Expected future payments are discounted using market yields at the reporting date on national government

bonds with terms to maturity and currency that match, as closely as possible, the estimated future cash outflows.

Post-employment benefits

Contributions made on behalf of eligible employees to defined contribution funds are recognised in the period they

are _incurred. The defined contribution funds receive fixed contributions from the group whose legal, or constructive

obligation is limited to these contributions only.

The group operated an in-house pension scheme until the fund was closed in September 2016. The scheme was

funded through payments to a trustee-administered fund, determined by periodic actuarial calculations on a defined

benefit scheme. The defined benefit scheme defined the amount of retirement benefit that an employee would

receive that was dependent on one or more factors such as age, years of service and compensation.

The liability recognised in the consolidated statement of financial position in respect of defined benefit pension plans

was the present value of the defined benefit obligation at balance date less the fair value of plan assets, together

with adjustments for actuarial gains or losses and past service costs. Independent actuaries using the projected unit

credit method calculate the defined obligation every three years. The present value of the defined benefit obligation

was determined by discounting the estimated future cash flows using the interest rates of national government

bonds that are denominated in the currency in which the benefits will be paid, and that have terms to maturity

approximating to the terms of the related pension liability.

Actuarial gains and losses arising from experience adjustments and changes in actuarial assumptions were charged

or credited to profit or loss.

14

Unilever New Zealand Limited

Notes to the consolidated financial statements For the year ended 31 December 2017

n) Employee benefits (continued)

Past-service costs were recognised immediately in profit or loss, unless the changes to the pension plan were

conditional on the employee remaining in service for a specified period of time (the vesting period). In that case, the

past-service costs were amortised on a straight-line basis over the vesting period.

Share-based payments

Share-based compensation benefits are provided to employees via the employee share schemes.

The fair value of shares granted under the employee share schemes is recognised as an employee benefit expense

with a corresponding increase in reserves. The fair value is measured at grant date and recognised over the period

during which the employees become unconditionally entitled to the share.

The fair value at grant date is determined using the closing price on the London stock exchange for Unilever PLC

shares and the Amsterdam stock exchange for Unilever NV shares.

At vesting date, the entity recognises any additional cost or releases any excess amortisation charged from grant

date. An invoice is issued from Unilever PLC or Unilever NV at vesting date for their respective shares to the entity

for payment.

o) LeasesFinance leases, which transfer to the group substantially all the risks and benefits incidental to ownership of the

leased item, are capitalised at the inception of the lease at the fair value of the leased asset or, if lower, at the

present value of the minimum lease payments. Lease payments are apportioned between the finance charges and

reduction of the lease liability so as to achieve a constant rate of interest on the remaining balance of the liability.

Finance charges are recognised as an expense in profit or loss.

Operating lease payments are recognised as an expense in profit or loss on a straight line basis over the lease term.

Operating lease incentives are recognised as a liability when received and subsequently reduced by allocating lease

payments between rental expense and reduction of the liability.

p) Provisions

A provision is recognised when the group has a present legal or constructive obligation as a result of a past event, it

is probable that an outflow of economic benefits will be required to settle the obligation and the amount has been

reliably estimated. If the effect is material, provisions are determined by discounting the expected future cash flows

at a pre tax rate that reflects current market rates and, where appropriate, the risks specific to the entity.

The present value of non-current provisions is determined by discounting the balance using a risk free rate.

q) Contributed equity

Ordinary shares are classified as equity. Incremental costs directly attributable to the issue of new shares or options

are shown in equity as a deduction, net of tax, from the proceeds.

r) Goods and Services Tax (GSTI

Revenues, expenses and assets are recognised net of the amount of GST except:where the GST incurred is not recoverable from the taxation authority; and receivables and payables are stated with the amount of GST included.

15

Unilever New Zealand Limited

Notes to the consolidated financial statements For the year ended 31 December 2017

s) Significant accountingjudgements, estimates and assumptions

The preparation of financial statements requires management to make judgements, estimates and assumptions

which effect the reported revenues, expenses, assets and liabilities and the accompanying disclosures. Uncertainty

about these assumptions and estimates could result in outcomes that may require a material adjustment to the

carryinQ amount of assets or liabilities in future periods.

Impairment of assets and goodwill

The group tests annually whether goodwill and other assets have suffered any impairment in accordance with the

accounting polices at 2 d) and 2 m).

Taxation

There may be transactions and calculations for which the ultimate tax determination is uncertain during the ordinary

course of business. Where the final tax outcome of these matters is different from the amounts initially recorded,

such differences impact the current and deferred tax provisions in the period in which such determination is made.

16

Unilever New Zealand Limited

Notes to the consolidated financial statements For the year ended 31 December 2017

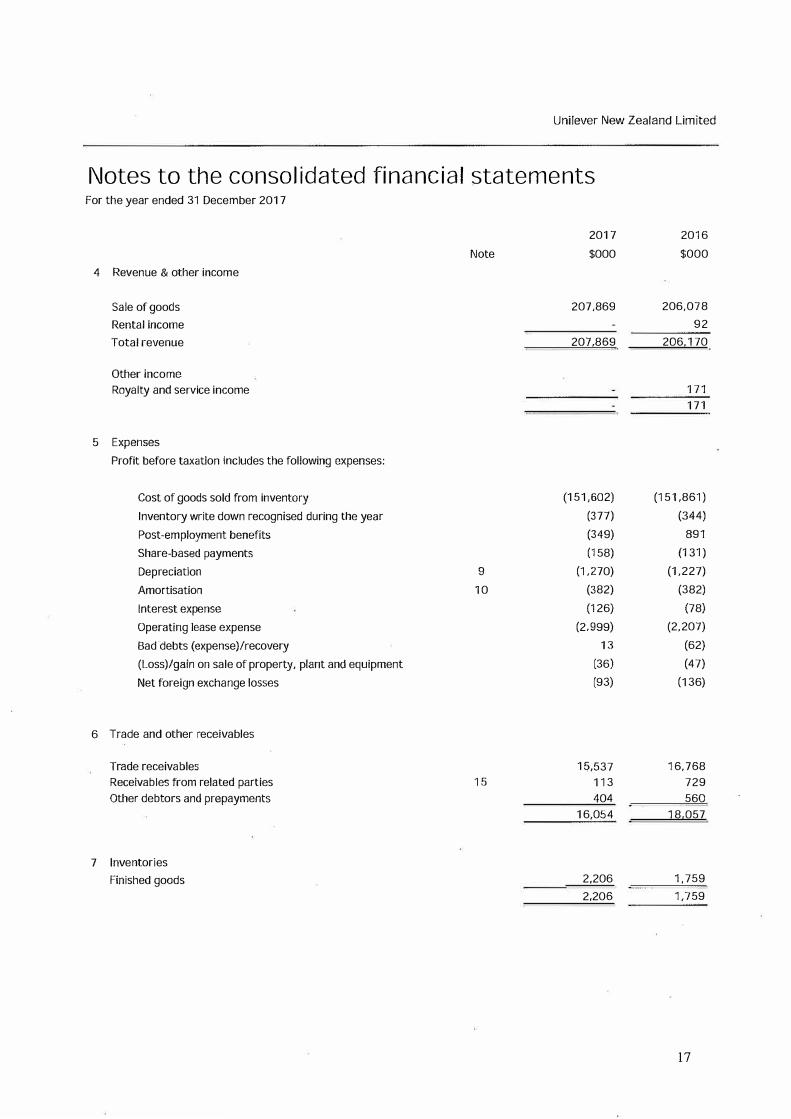

2017 2016 Note $000 $000

4 Revenue & other income

Sale of goods 207,869 206,078 Rental income 92 Total revenue 207,869 206,170

Other income Royalty and service income 171

171

5 Expenses

Profit before taxation includes the following expenses:

Cost of goods sold from inventory (151,602) (151,861) Inventory write down recognised during the year (377) (344)

Post�emp!oyment benefits (349) 891 Share-based payments (158) (131)Depreciation 9 (1,270) (1,227) Amortisation 10 (382) (382)

Interest expense (126) (78) Operating lease expense (2,999) (2,207)

Bad debts (expense)/recovery 13 (62)(Loss)/gain on sale of property, plant and equipment (36) (47)Net foreign exchange losses (93) (136)

6 Trade and other receivables

Trade receivables 15,537 16,768 Receivables from related parties 15 113 729 Other debtors and prepayments 404 560

16,054 18,057

7 Inventories Finished goods 2,206 1,759

2,206 1,759

17

Unilever New Zealand Limited

Notes to the consolidated financial statements For the year ended 31 December 2017

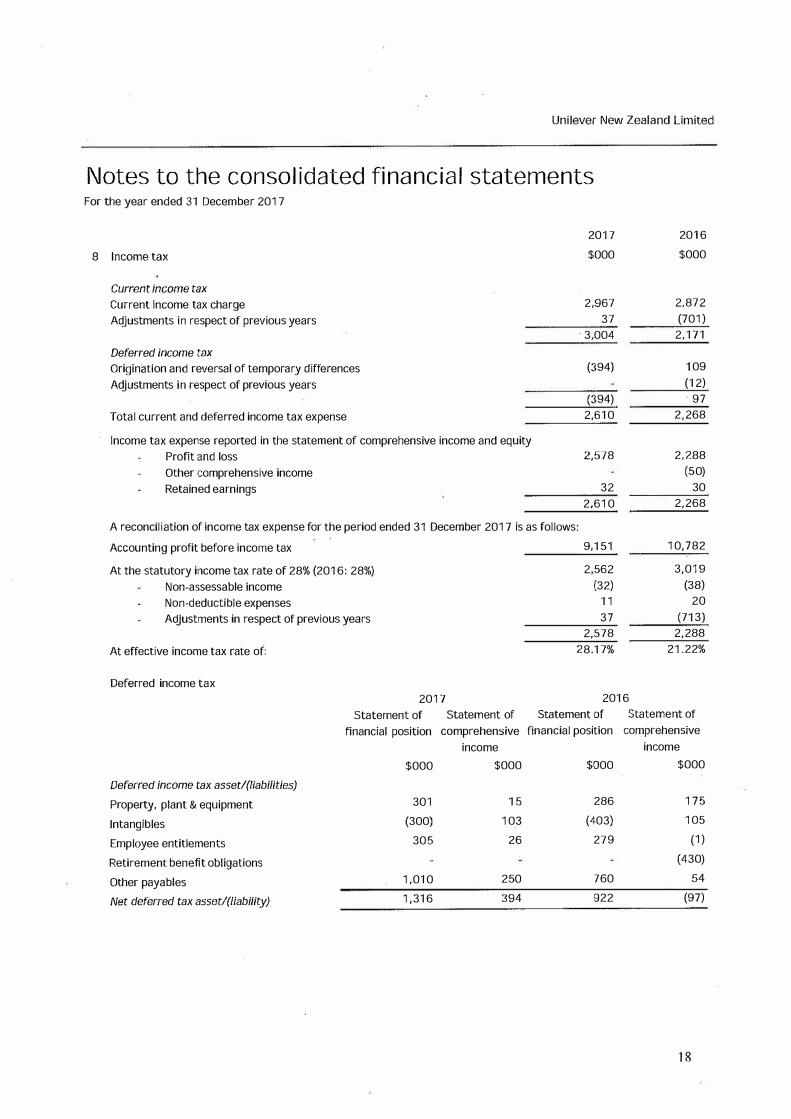

8 Income tax

Current income tax

Current income tax charge Adjustments in respect of previous years

Deferred income tax

Origination and reversal of temporary differences Adjustments in respect of previous years

Total current and deferred income tax expense

Income tax expense reported in the statement of comprehensive income and equity Profit and loss Other comprehensive income Retained earnings

2017

$000

2,967 37

· 3,004

(394)

(394)2,610

2,578

32 2,610

A reconciliation of income tax expense for the period ended 31 December 2017 is as follows:

Accounting profit before income tax

At the statutory income tax rate of 28% (2016: 28%) Non-assessable income Non-deductible expenses Adjustments in respect of previous years

At effective income tax rate of:

Deferred income tax

9,151

2,562 (32)

11 37

2,578 28.17%

2016

$000

2,872 (701)

2,171

109 (12)

97 2,268

2,288 (50)

30 2,268

10,782

3,019 (38)

20

(713) 2,288

21.22%

2017 2016

Statement of Statement of Statement of Statement of

financial position comprehensive financial position comprehensive

income income

$000 $000 $000 $000

Deferred income tax assetl{liabilities)

Property, plant & equipment 301 15 286 175

Intangibles (300) 103 (403) 105

Employee entitlements 305 26 279 (1)

Retirement benefit obligations (430)

Other payables 1,010 250 760 54

Net deferred tax assetl(liability) 1,316 394 922 (97)

18

Unilever New Zealand Limited

Notes to the consolidated financial statement For the year ended 31 December 2017

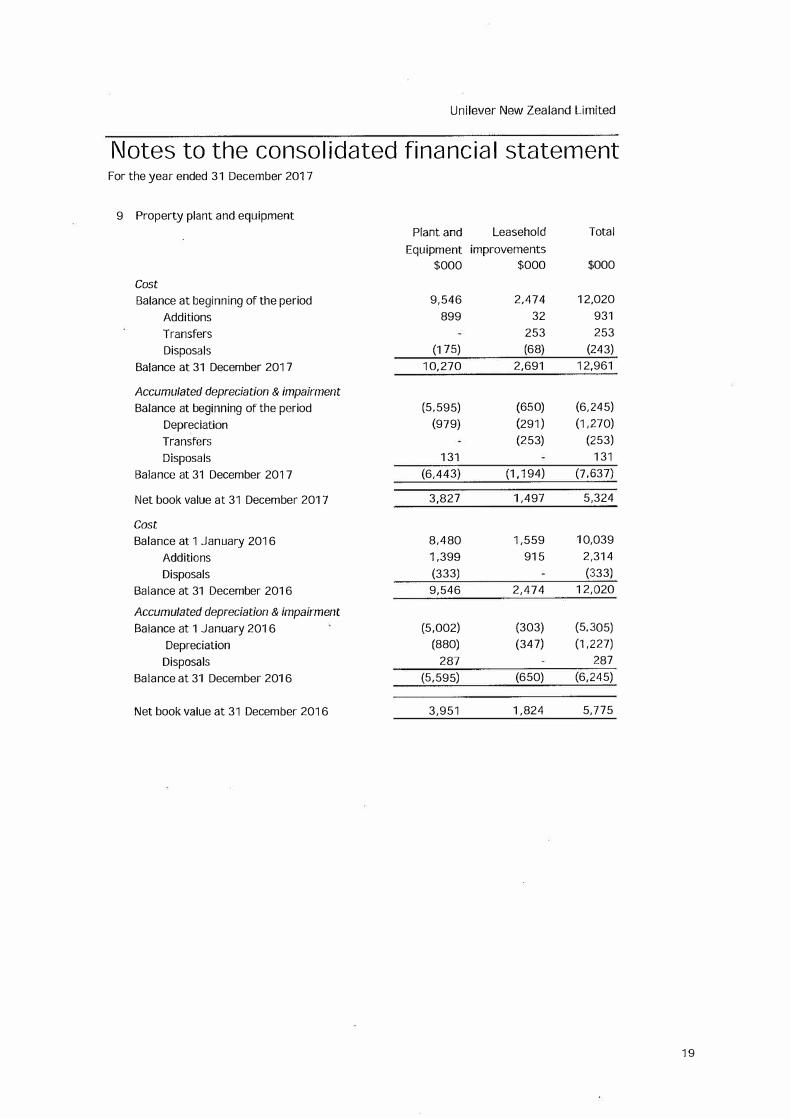

9 Property plant and equipment

Plant and Leasehold Total

Equipment improvements

$000 $000 $000

Cost

Balance at beginning of the period 9,546 2,474 12,020

Additions 899 32 931

Transfers 253 253

Disposals (175) (68) (243)

Balance at 31 December 2017 10,270 2,691 12,961

Accumulated depreciation & impairment

Balance at beginning of the period (5,595) (650) (6,245)

Depreciation (979) (291) (1,270)

Transfers (253) (253)

Disposals 131 131

Balance at 31 December 2017 (6,443) (1,194) (7,637)

Net book value at 31 December 2017 3,827 1,497 5,324

Cost

Balance at 1 January 2016 8,480 1,559 10,039

Additions 1,399 915 2,314

Disposals (333) (333)

Balance at 31 December 2016 9,546 2,474 12,020

Accumulated depreciation & impairment

Balance at 1 January 2016 (5,002) (303) (5,305)

Depreciation (880) (347) (1,227)

Disposals 287 287

Balance at 31 December 2016 (5,595) (650) (6,245)

Net book value at 31 December 2016 3,951 1,824 5,775

19

Unilever New Zealand Limited

Notes to the consolidated financial statements For the year ended 31 December 2017

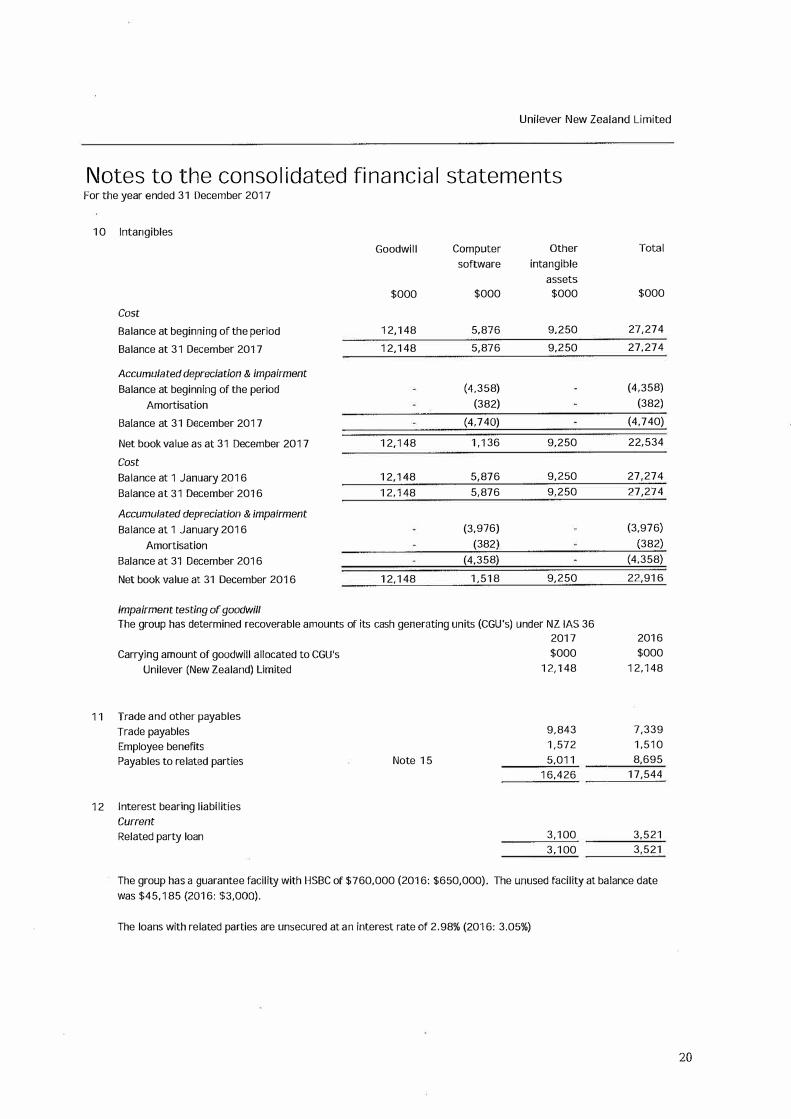

10

11

12

Intangibles

Goodwill Computer Other Total

software intangible assets

$000 $000 $000 $000

Cost

Balance at beginning of the period 12,148 5,876 9,250 27,274

Balance at 31 December 2017 12,148 5,876 9,250 27,274

Accumulated depreciation & impairment

Balance at beginning of the period (4,358) (4,358)

Amortisation (382) (382)

Balance at 31 December 2017 (4,740) (4,740)

Net book value as at 31 December 2017 12,148 1,136 9,250 22,534

Cost

Balance at 1 January 2016 12,148 5,876 9,250 27,274

Balance at 31 December 2016 12,148 5,876 9,250 27,274

Accumulated depreciation & impairment

Balance at 1 January 2016 (3,976) (3,976)

Amortisation (382) (382)

Balance at 31 December 2016 (4,358) (4,358)

Net book value at 31 December 2016 12,148 1,518 9,250 22,916

Impairment testing of goodwill

The group has determined recoverable amounts of its cash generating units (CGU's) under NZ IAS 36 2017 2016

Carrying amount of goodwill allocated to CGU's $000 $000

Unilever (New Zealand) Limited 12,148 12,148

Trade and other payables Trade payables 9,843 7,339

Employee benefits 1,572 1,510

Payables to related parties Note 15 5,011 8,695 16,426 17,544

Interest bearing liabilities Current

Related party loan 3,100 3,521 3,100 3,521

The group has a guarantee facility with HSBC of $760,000 (2016: $650,000). The unused facility at balance date was $45,185 (2016: $3,000).

The loans with related parties are unsecured at an interest rate of 2.98% (2016: 3.05%)

20

Unilever New Zealand Limited

Notes to the consolidated financial statements For the year ended 31 December 2017

13 Provisions Restructuring costs

Opening balance at beginning of year Reversed to profit or loss

Long service leave

Opening balance at beginning of year Recognised during the year Reversed to profit or loss

Recognised in the consolidated statement of financial position as: Current Non-current

For the nature and calculation of long service leave please refer to note 2n).

14 Contributed equity Share capital Ordinary shares - fully paid 24,342,137 (2016: 24,342,137 fully paid)

Ordinary shares have no par value. Each fully paid ordinary share confers on the holder the right to:

One vote on a poll at a meeting of the company on any resolution:

2017 $000

332 32

(3) 361

361

87 274 361

2017 $

48,684

An equal share in distributions (including dividends) approved by the Board of Directors; and An equal share in distribution of the surplus assets of the company on dissolution.

15 Related parties Ultimate and parent entities

2016 $000

396 (396)

355

(23) 332

332

80 252 332

2016 $

48,684

The company's shareholder is Unilever Overseas Holdings B.V, a company registered in the Netherlands. The ultimate parent company is Unilever PLC, a public company registered in the United Kingdom.

Subsidiaries The company has the following subsidiaries:

Name

Unilever New Zealand Superannuation Trustee Limited Unilever New Zealand Trading Limited T2 New Zealand Limited

Country of Nature of incorporation business

New Zealand New Zealand New Zealand

Superannuation Trading

Ben & Jerry's Franchising New Zealand Limited New Zealand Trading Non-Trading

% equity interest 2017 2016

100% 100% 100% 100% 100% 100% 100% 100%

21

Unilever New Zealand Limited

Notes to the consolidated financial statements For the year ended 31 December 2017

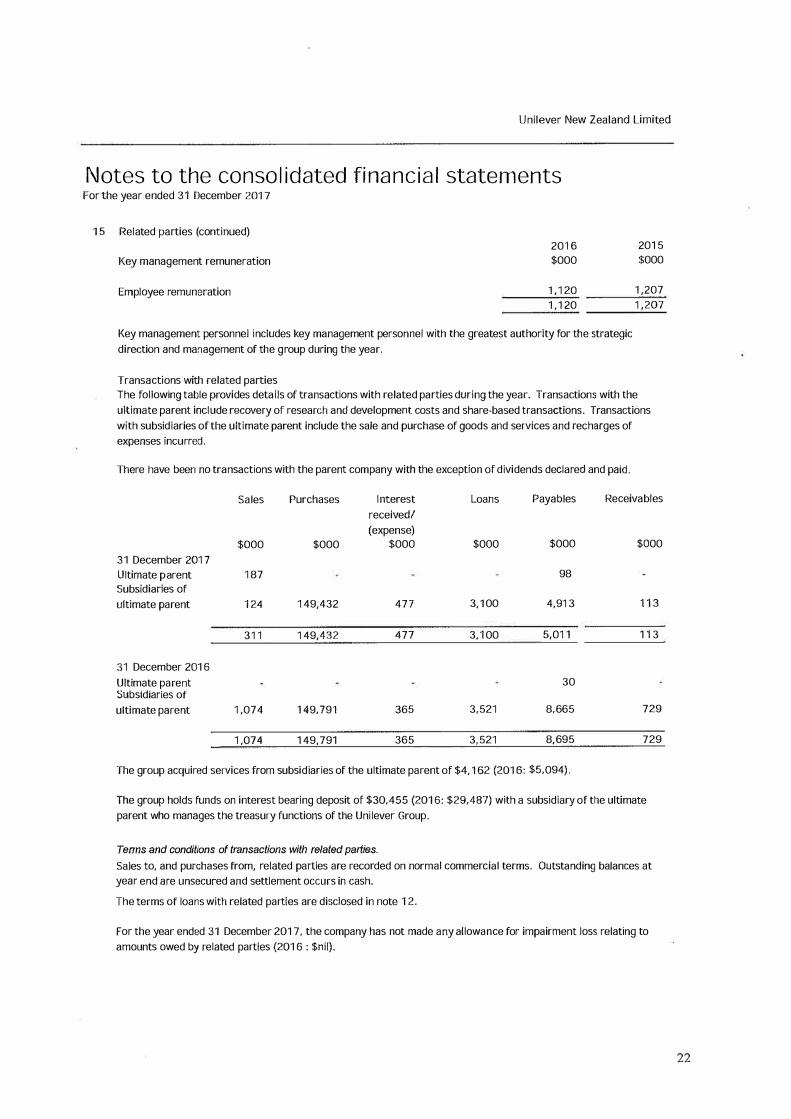

15 Related parties (continued)

Key management remuneration

Employee remuneration

2016

$000

1,120

1,120

Key management personnel includes key management personnel with the greatest authority for the strategic

direction and management of the group during the year.

Transactions with related parties

2015

$000

1,207

1,207

The following table provides details of transactions with related parties during the year. Transactions with the

ultimate parent include recovery of research and development costs and share-based transactions. Transactions

with subsidiaries of the ultimate parent include the sale and purchase of goods and services and recharges of

expenses incurred.

There have been no transactions with the parent company with the exception of dividends declared and paid.

Sales Purchases Interest Loans Payables Receivables

received/

(expense) $000 $000 $000 $000 $000 $000

31 December 2017

Ultimate parent 187 98

Subsidiaries of

ultimate parent 124 149,432 477 3,100 4,913 113

311 149,432 477 3,100 5,011 113

31 December 2016

Ultimate parent 30

Subsidiaries ot

ultimate parent 1,074 149,791 365 3,521 8,665 729

1,074 149,791 365 3,521 8,695 729

The group acquired services from subsidiaries of the ultimate parent of $4, 162 (2016: $5,094).

The group holds funds on interest bearing deposit of $30,455 (2016: $29,487) with a subsidiary of the ultimate

parent who manages the treasury functions of the Unilever Group.

Tenns and conditions of transactions with related parties.

Sales to, and purchases from, related parties are recorded on normal commercial terms. Outstanding balances at

year end are unsecured and settlement occurs in cash.

The terms of loans with related parties are disclosed in note 12.

For the year ended 31 December 2017, the company has not made any allowance for impairment loss relating to

amounts owed by related parties (2016: $nil).

22

Unilever New Zealand Limited

Notes to the consolidated financial statements For the year ended 31 December 2017

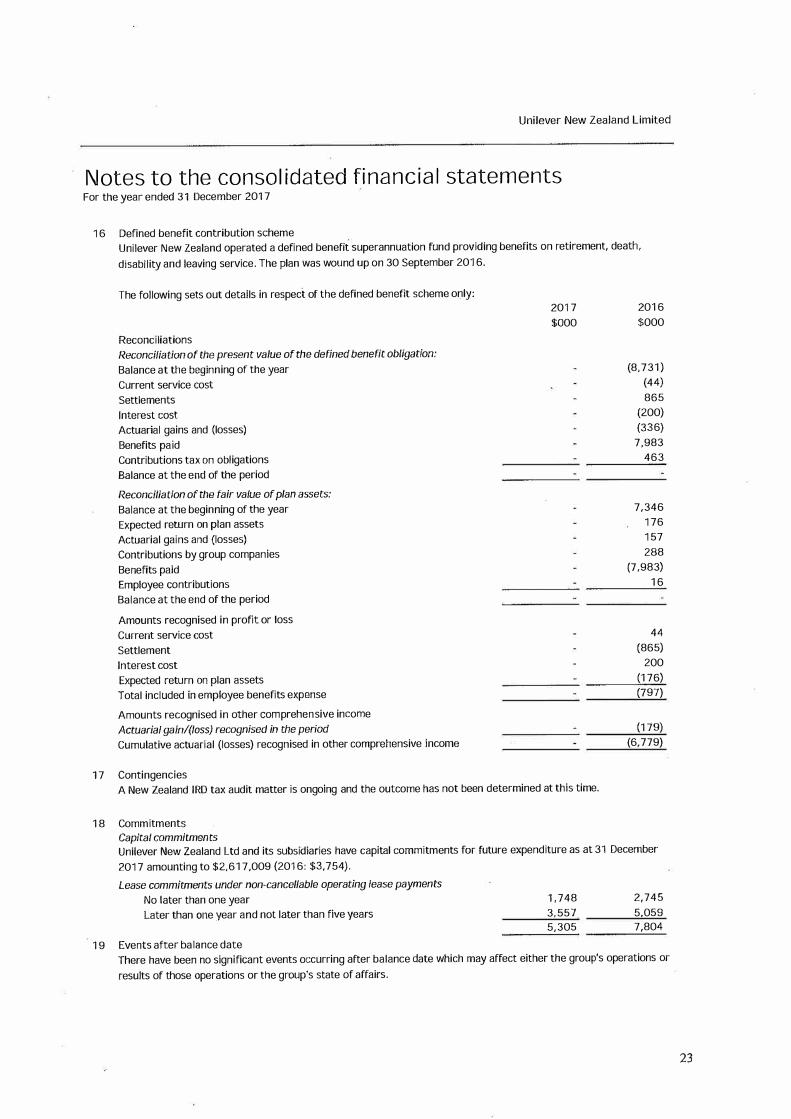

16 Defined benefit contribution scheme Unilever New Zealand operated a defined benefit superannuation fund providing benefits on retirement, death, disability and leaving service. The plan was wound up on 30 September 2016.

The following sets out details in respect of the defined benefit scheme only:

Reconciliations Reconciliation of the present value of the defined benefit obligation:

Balance at the beginning of the year Current service cost Settlements Interest cost Actuarial gains and (losses) Benefits paid Contributions tax on obligations Balance at the end of the period

Reconciliation of the fair value of plan assets:

Balance at the beginning of the year Expected return on plan assets Actuarial gains and (losses) Contributions by group companies Benefits paid Employee contributions Balance at the end of the period

Amounts recognised in profit or loss Current service cost Settlement Interest cost Expected return on plan assets Total included in employee benefits expense

Amounts recognised in other comprehensive income Actuarial gainl(Joss) recognised in the period

Cumulative actuarial (losses) recognised in other comprehensive income

17 Contingencies

2017 $000

A New Zealand IRD tax audit matter is ongoing and the outcome has not been determined at this time.

18 Commitments Capital commitments

2016 $000

(8,731) (44) 865

(200) (336)

7,983 463

7,346 176 157 288

(7,983) 16

44 (865)

200 (176) (797)

(179) (6,779)

Unilever New Zealand Ltd and its subsidiaries have capital commitments for future expenditure as at 31 December 2017 amounting to $2,617,009 (2016: $3,754).

Lease commitments under non-cancel/able operating lease payments

No later than one year Later than one year and not later than five years

19 Events after balance date

1,748 3,557 5,305

2,745 5,059 7,804

There have been no significant events occurring after balance date which may affect either the group's operations or results of those operations or the group's state of affairs.

23

Top Related