Languages

Pages

Legal

abbr

1

Time to Produce and Emerging Market Crises ∗

Felipe Schwartzman

January 19, 2010

Abstract

This paper argues that interest rates affect output through their impact on the cost of variable

inputs such as materials and labor. This effect occurs because of time lags in the production process.

To test the theory, I exploit the following cross-sectional implication: industries that usually hold more

inventories relative to their variable costs should react more strongly to changes in the cost of capital.

I find that during emerging market crises there is a large and robust reallocation towards sectors

with low inventory-to-cost ratios. I set up a multi-sector general equilibrium model with production

lags which match the inventory-to-cost ratios in the data. Exogenous shocks calibrated to reproduce

movements in aggregate variables during the crises generate a sectoral reallocation compatible with

the empirical predictions. Furthermore, the model generates a sizeable and quick reaction of aggregate

output in reaction to an isolated interest rate shock, which is consistent with findings in the previous

literature. All these results rely only on the assumption about the production technology, without

any reference to financial or payment frictions.

∗I would like to thank Nobu Kiyotaki and Markus Brunnermeier for advising me in this work. I also thank GeorgeAlessandria, Tiago Berriel, Carlos Carvalho, Bo Honore, Oleg Itskhoki, Ryo Jinnai, Pat Kehoe, Kalina Manova, VirgiliuMidrigan, Fernanda Nechio, Esteban Rossi-Hansberg, Huntley Schaller, Sam Schulhofer-Wohl, Hyun Shin, Chris Sims, MarkWatson, Adam Zawadowski and participants in various workshops and seminars in Princeton for helpful advice. All remainingerrors and omissions are of my entire responsibility.

1 Introduction

This paper argues that interest rates affect output through their impact on the cost of variable inputs

such as materials and labor. The cost of variable inputs increases in the interest rate because of time

lags in the production process. When a firm sets out to produce a good, first it has to acquire raw

materials and put workers to work, and only after a period of time it is able to sell the finished good.

In the interim, the firm foregoes interest income or incurs interest costs. If the interest rate goes up,

the production process becomes more costly so that the firm optimally chooses to reduce its sales.

I exploit the following cross-sectional implication of the theory: industries that usually hold more

inventories relative to their variable costs should react more strongly to changes in the cost of capital.1

The reason is that inventories account for the value of all variable inputs accumulated between the time

of their acquisition and the sale of the corresponding output. As a consequence, the ratio between total

inventories and variable costs captures the importance of the foregone interest rate income associated

with the purchase of variable inputs.2

The empirical analysis focuses on episodes in which the link between capital flows and output

was most likely to be visible. These are the sudden stop episodes identified by Calvoetal:2006b. The

discrete jump in current account surplus observed in these episodes suggest that they were largely

unforeseen shocks. The large and persistent drop in investment/output ratio that follows suggests a

large and persistent increase in the cost of capital. Together these suggest that these episodes provide

interesting natural experiments on the effects of shocks to the cost of capital on output.

I find that in the course of these episodes there is a large and robust reallocation towards sectors

with low inventory-to-cost ratios. Figure ?? shows the reallocation pattern in the data. Each point

refers to a manufacturing industry. The vertical axis depicts the difference in the log of value added

in the year when GDP was at its lowest and the value three years before, averaged over 21 sudden

stop episodes.3 The horizontal axis represents a proxy for the inventory-to-cost ratio calculated for

each industry.4 As I discuss in section ??, the addition of controls reduces the slope of the regression

coefficient, but the correlation is remarkably robust.

The reduced form estimates establish that the reallocation goes in the direction predicted by

the theory. To assess whether time lags in production can plausibly account for the magnitude of

the estimated effects, I set up a multi-sector general equilibrium model with delays between the

1The bulk of inventories are raw materials and work-in-process, the value of which are naturally tied to production plans.Also, finished goods inventories have been found to follow sales quite closely at yearly frequencies, so that it is adequate tointerpret these as factors of production [?].

2As opposed to inventory to sale ratio, since sales also include markups and income of fixed factors which have little rolein the short term decisions.

3I use volume indices for value added4I use data from manufacturing industries in the US, following the tradition initiated by Rajanzingales:1998. Total

inventories are the sum of the stocks of raw materials, work in process and finished good inventories, and the variable costsinclude materials and direct labor costs. Inventories are measured in dollars and costs are measured in dollars per month.Hence the ratio is measured in months. A ratio of 2 implies that firms hold an amount of inventories equivalent to twomonths worth of costs.

3

use of inputs and the completion of the output. I calibrate the production lags so that they are

compatible with the inventory-to-cost ratios in the data. I then simulate a crisis in the model as

a combination of shocks to foreign interest rate and total factor productivity, chosen to match the

magnitude and persistence of changes in GDP and fixed investment. The model is able to generate a

sectoral reallocation in response to a crisis-like event in line with the estimates from the data.

Lastly, I can also use the model to assess the importance of the production time channel for the

impact of interest rate shocks on aggregate output. The model implies that the shock to the foreign

interest rate accounts for about one quarter of the initial drop in output. In particular, because of

the interest rate shock alone, GDP drops about 4% over the first two quarters after the shocks.

This large effect may come across as puzzling given the short lags in the production process. The

main reason is a relatively high level of “substitution”, in the sense emphasized by KingRebelo:1999.

I allow firms to choose capacity utilization and, following the practice in the Small Open Economy

RBC literature, do not allow for wealth effects in labor supply. These assumptions imply that the

supply fixed capital and labor do not impose important constraints on the effect of the shocks.

The notion that interest rates affects the cost of variable inputs is hardly new. However, the

usual mechanisms rely on some form or another of payment frictions. For example, christianoeichen-

baum:1992 propose that firms need to hold cash in order to pay the wage bill, so that if the interest

rate goes up, these payments become more costly. This assumption is problematic when it comes

to emerging market economies that underwent periods of very large inflation. The reason is that,

with a cash-in-advance constraint, the financial cost is increasing not in the real, but in the nominal

interest rates. During inflationary times the variability in inflation, and hence in the nominal interest

rate, was larger by an order of magnitude when compared with the post-stabilization period. Given a

cash-in-advance constraint, this would imply a commensurate difference in the volatility of production

costs and of output.5

NeumeyerPerri:2004 propose that in emerging markets payments are made in real, non-interest

rate bearing assets instead of cash. This assumption allows them to match the negative correlation

between detrended output and the real interest rate on government bonds observed in Argentina, while

encompassing both periods with high and low inflation. Their success has prompted many authors

to use a similar device in more elaborate models of emerging market business cycles.6 While the

assumption is successful in terms of its aggregate implications, Charikehoemagrattan:2005 criticize it

for the lack of an empirical counterpart. This paper resolves the issue by proposing that the purchase

of variable inputs is itself a real, short-term investment, so that no recourse to payment frictions is

needed.

This paper discusses how a change in the cost of capital affects output, but it leaves open the

5Nevertheless, cash-in-advance constraints in the payment of inputs has a long tradition in the emerging market businesscycle literature, for example Cavallo:1981. See AgenorMontiel:2002, Ch. 6 and 7 for a discussion of this early literature.

6See for example christianogustroldos:2004, Mendoza:2006, UribeYue:2006, Otsu:2007 and MendozaYue:2008. An excep-tion is GertlerGilchristNatalucci:2007, in that interest rate shocks affect production quickly through the impact of changesin the real exchange rate on capacity utilization decisions.

4

determination of this cost. This task is undertaken, for example, by Mendoza:2006. The author

demonstrates how a business cycle model with occasionally binding credit constraint at the level of

the economy is able to generate alternating periods of normal business cycle variations and sudden

stops.7 In itself, however, these frictions do not imply a drop in output, and Mendoza recurs to

a payment-in-advance constraint to get this effect. On the empirical side, a similar point can be

made about the studies by Kroszneretal:2006 and Dellariccia:2007. They find that, in banking crises,

industries that rely more on external finance to fund long term investment lose relatively more of their

output. Their empirical results illuminate the effect of banking crises on the cost of capital, but they

leave open how this exposure translates into a drop in output.

The empirical findings in this paper are complemented by independent work by TongWei:2009.

Using data from emerging market firms, the authors show that a high inventory-to-sale ratio was

associated with a relatively large drop in share-prices in the aftermath of the latest global crisis. Their

price evidence complements the quantity evidence presented here. Raddatz:2006 presents another set

of related empirical findings. He finds that industries with high inventory-to-sale ratio are relatively

more volatile in countries with a low level of financial development. His findings emphasize the role

of the financial system in providing liquidity insurance.8

The paper proceeds as follows: Section 2 uses a simple partial equilibrium example to lay out the

link between theory and data. In particular, it shows that if production time is allowed for then

firms which normally hold a higher inventory-to-cost ratio will respond more strongly to interest rate

shocks. Section 3 contains the data analysis. It documents the cross-industry correlation between

the inventory-to-cost ratio and the change in value added during emerging market crises, providing

various robustness checks. Section 4 introduces the general equilibrium business cycle model, discusses

its calibration, and reports the results of the different experiments. Section 5 concludes the paper.

2 Time to produce in Partial Equilibrium

This section discusses, in a partial equilibrium setup, the key cross-sectional prediction of the time to

produce model: shocks to the interest rate have an impact on sales that is largest for firms that have

a large steady state inventory-to-cost ratio.

I construct the argument in two steps. First, I introduce the production function that underlies

the analysis and show that, after a short transition period, the impact of a persistent interest rate

shock on sales is increasing in the share of inputs that a firm has to acquire early on.9

7Like here, the marginal cost of capital in Mendoza:2006 is the same for all firms. Implicitly, the balance sheet constraintsin his model are the ones faced by domestic financial intermediaries as opposed to domestic productive units, as suggestedby Krishnamurthy:2003.

8Markups vary less than inventories across firms, so that inventories to cost and inventories to sale ratios are normallyclosely linked.

9In the exposition below I focus on sales as a measure of economic activity, since these are more conceptually straightfor-ward than value added. I discuss how the results change economic activity is measured using value added instead.

5

Second, I show that this share can be mapped into the ratio between inventories and variable costs.

This is the key insight that drives the paper. This mapping underlies the empirical analysis in section

3 and the calibration in section 4.

2.1 A one time shock to the interest rate

The production function is an application of Kydlandprescott:1982 time to build technology. I use

the term “time to produce” instead of “time to build” to emphasize the rather short-horizon process

of transforming variable inputs into manufactured goods, as opposed to the more time consuming

process of building ships or factories. I take a broad view of production that includes the storage

of inputs and finished goods in order to economize on logistics and avoid stock-outs. This is akin to

Ramey:1989 suggestion that inventories can be usefully modeled as factors of production.10

In order to sell output at t, a firm must acquire inputs in t− 1 and t− 2. The production function

is Cobb-Douglas with decreasing returns to scale, as follows:11

Yt =([Zt (0)]1−ω [Zt−1 (1)]ω

)φ, φ < 1

Where Zt (v) is a composite of inputs acquired in t to generate a sale v periods ahead.

Consider the perfect foresight path of sales after a one time, unexpected shock to the interest

rate. Suppose firms are in steady state and at t = 0 they find that the future path of interest rate

will change. The new interest rate path is a perturbation around the old steady state that decays

geometrically, at a rate η. By assumption, the prices of output and inputs do not change. As a

consequence, this is a partial equilibrium exercise.

I assume that Zt (v) is a composite of the same set of goods irrespective of v, the horizon to which

it is assigned. This implies that I can denote a price index for Zt (v) which is independent of v. The

problem of the firm at t = 0 is:

maxZt(v),Yt

∞∑t=0

t∏s=0

1Rs

[ptYt − qtZt (0)− qtZt (1)]

s.t. : Yt =([Zt (0)]1−ω [Zt−1 (1)]ω

)φZ−1 (1) = z

Where qt and pt are, respectively, a price index for the composite of inputs and the price of the

final goods, and Rt is the interest rate between periods t and t+ 1. The constraint implies that input

10However, the production function approximates the treatment in MacciniMooreSchaller:2004 more closely in that itemphasizes the role of flows of goods into production, rather than stocks

11The decreasing returns to scale may stem from fixed inputs. This is a minor omission since the share of variable inputsin manufacturing production is typically above 80%. In the calibrated model I allow for constant returns to scale at the firmlevel.

6

choices made before t = 0 cannot be changed.

I can rewrite the problem as a sequence of maximization problems:

t=0:

maxZ0(1),Y0

p0Y0 − q0Z0 (0)

s.t. : Y0 =(Z0 (0)1−ω zω

)φ

The cost of inputs acquired at t = −1 is sunk, but not the ones acquired in t = 0. The profit

maximizing output is:

Y0 = χ0zωφ

(q0p0

)− (1−ω)φ1−(1−ω)φ

Where χ0 is a constant term. Note that output is insensitive to the interest rate. This is because

all inter-temporal decisions relevant for period t production were made beforehand.

t≥ 1:

From t ≥ 1 onward, the problem of the firm is:

maxZt(v),Yt

ptYt − qtZt (0)−Rt−1qt−1Zt−1 (1)

s.t. : Yt =([Zt (0)]1−ω [Zt−1 (1)]ω

)φ

Now, the profit maximizing output is

Yt = χ

[(Rt−1qt−1)

ω (qt)1−ω

pt

]− φ1−φ

Where again χ is a constant term. This implies that

dYtYt

= − φ

1− φωdRt−1

Rt−1

Since dRtRt

= η dRt−1

Rt−1, I can write the relationship between current output and current interest rate

as:

7

dYtYt

= − φ

1− φ

ω

η

dRtRt

The impact is increasing in ω, the share of date t − 1 inputs in the production of date t output.

Industries where this share is higher will react more strongly to the interest rate.

Another result which is important is that the effect is increasing in φ1−φ . This is as a measure of the

linearity of the production function with respect to variable inputs. If the production function is more

linear, small changes in cost of inputs will have a large impact on produced output. The intuition

generalizes readily to an equilibrium setup where output price depends on the chosen quantity. If

demand is inelastic, so that the price changes a lot as the quantity produced increases, the equilibrium

reaction of firms to an increase in costs will be relatively smaller.12

2.2 Inventory-to-Cost ratios and Time to Produce

I start out by defining some accounting concepts. These are ideal versions of the numbers in the data.

I will point out some of the major ways in which the data differs from the ideal cases.

2.2.1 Cost of Goods Sold

The “Cost of Goods Sold” is the replacement cost of all variable inputs used to produce the goods

sold in the measurement period. In the context of this model, this is:

COGSt = Rt−1qt−1Zt−1 (1) + qtZt (0)

The spot prices are inflated by the opportunity cost of capital between the time they the firm

acquires them and the time the final good is sold. This conforms to the convention that accounting

numbers be priced at replacement cost.

Note that cost of goods sold is a flow variable, so that it is measured as dollars per unit of time.

2.2.2 Inventories

Inventories include the value of all inputs acquired by the firm whose corresponding output has not

yet been sold:

INVt = qtZt (1)

The following identity links cost of goods sold and inventories:

INVt = Rt−1INVt−1 − COGSt + acquisition of inputst12The correspondence is not immediate, since, in a competitive framework, firms take prices as given, so that they do not

fully take the concavity of the revenue function for the industry into account.

8

Where previous period inventories are inflated by the interest rate so that they are valued at

replacement cost. While in practice the valuation of costs and inventories deviates from the ideal

represented above, the rest of accounting identity above is normally respected.13

2.2.3 Inventory-to-Cost Ratio

The inventory-to-cost ratio is:

INVt

COGSt=

qtZt (1)Rt−1qt−1Zt−1 (1) + qtZt (0)

Under perfect foresight, the Cobb-Douglas assumption implies that:

INVt

COGSt=ωφYt+1

φYt

This is a forward looking variable, since inventories reflect future production plans. It will fluctuate

with the business cycle as firms change their production plans. Note that since inventories are a stock

variable, measured in dollars, and the cost of goods sold is a flow variable, measured in dollars per

unit of time, the inventory-to-cost ratio is measured in units of time.

For the purposes of this paper, the interesting quantity is the steady state inventory-to-cost ratio,

that is, the one obtained when Yt = Yt−1 for all t. This satisfies:

INVCOGS

=qZ (1)

RqZ (1) + qZ (0)

Again, applying the Cobb-Douglas assumption:

INVCOGS

=ωφY

φY= ω

Recall that ω plays an important role in characterizing the impact of the interest rate shock on

sales. In particular, from t ≥ 1 onwards, the impact is increasing in ω. This implies that the impact

of an interest rate shock is, everything else constant, increasing in the inventory-to-cost ratio.

If the persistence parameter η is close to 1, then

dYtYt

∼=INV

COGSφ

1− φ

dRtRt

13In particular, accounting practices differ depending on whether inventories are valued at the cost of the inputs boughtmost recently (Last In First Out) or at the price of the oldest inputs who have not yet been deducted from inventories (FirstIn First Out) or still other practices

9

So that the impact of interest rate on output is directly proportional to the inventory-to-cost ratio.

This latter result generalizes to arbitrary convex production functions with inputs included many

periods in advance. The discussion of is in Appendix B.

2.2.4 Caveats

A few caveats are worth mentioning. First, inventory and costs rarely if ever account for financing

costs. This problem is not particularly important if the period of time considered is not very large. In

the data, inventory turnover ratios for the manufacturing sector are around 2 months. This implies

that the financing costs are fairly small.

Second many important costs may not be accounted for in the cost of goods sold and in inventories,

notably maintenance cost of capital and administrative labor. However, it is normally the case that

whatever costs are accounted for under “cost of goods sold”, they are also included in inventories,

including direct labor costs. This implies that the ratio is approximately correct if the omitted costs

have a time profile similar to the included ones.

Third, the actual measurements of productive activity are based on value added and not on sales.

Because value added data includes the change in inventories, it has a forward looking component.

This implies that the reaction of value added to interest rate shocks should be faster than the reaction

of sales. However, as the economy evolves along the perfect foresight path, the two measures become

tightly linked, as demonstrated in Appendix A.

3 Data Analysis

This section presents the empirical results. It shows that during emerging market crises there is a

strong reallocation towards sectors with lower inventory-to-cost ratio. The data analysis in this section

shows that the reallocation does not reflect other plausible explanations and is a robust feature of

emerging market crises, having occurred in the 80’s and the 90’s, in Latin America and in other

continents. Last, this section shows that the reallocation was persistent, so that it was not a mere

reflection of short run inventory adjustment dynamics.

3.1 Events

The analysis centers on events that Calvoetal:2006b identify as output collapses following Systemic

Sudden Stops.14 The list of episodes is in table ?? These are restricted to emerging market economies,

and consist of large output drops that occurred together with unusually large reversals in current

account. In order to isolate “systemic” episodes, the authors focus on periods when international

rates at which emerging market countries borrowed were relatively high. This filter helps assure that

the episodes were somehow linked to the difficult foreign financial environment. The dates picked

14See the above mentioned paper and Calvoetal:2004 for further details of how exactly these events were selected.

10

by the authors are broadly consistent with independent identifications of financial crises based on

domestic credit [?] and banking crises [?]. This suggests that there is a causal or at least starkly

amplifying effect from the increase in cost of capital to aggregate output. Table 1 lists the events.

They concentrate in the early eighties, the late nineties and, to a lesser extent, the mid nineties. This

clustering of events provides further indication of the exogenous timing of the shock.

3.2 Empirical Specification

I run the following OLS regression:

yi,k,t∗ − yi,k,t∗−h = βτk + γXik + δ (yi,k,−h − yi,k,t∗−h−6) + εik + αi

Where yi,k,t∗−h is log value added in industry k, episode i, h years from the trough of the crisis

(Example: value added in the production of apparel in South Korea 1998 episode, as measured in

1995). On the right hand side the constant term varies with the episode, τk is inventory-to-cost ratio

for industry k, Xik is a vector of controls, the values of which varies by episode and industry. The last

term is a control for prior trend. The hypothesis is that β < 0, so that firms with longer production

time do relatively worse.

Value added data is taken from the data-set compiled by UNIDO. These are originally produced

by statistical offices of UN member countries and then brought together by UNIDO. The industries

are classified according to three digit ISIC Rev. 2.15

In the benchmark regressions, I set h = 3 because the start of the crisis is not always clear cut and

in some instances multiple years may pass between the initial shock and the trough of GDP. As part

of the robustness checks, I experiment with different values for h.

Errors may be correlated both within episodes or within industries. To account for these, the

standard errors are robust to overlapping clusters at both the industry and episode level, as proposed by

Cameronetal:2006.16 Thus the error term for shoes in the Korea, 1998 episode may be correlated both

with machinery in Korea 1998 and shoes in Argentina, 2001. Because it allows for more widespread

correlation between error terms, this technique typically produces standard errors which are more

conservative than the more usual one way clustering procedures.

I remove all observations where the dependent variable was more than 3 interquartile ranges from

the median. Also, when using the Annual Survey of Manufacturing data, I do not include the tobacco

industry. The reason is that tobacco has a ratio between inventories and costs equal to 8 months.

This is more than twice the value for the non-metallic mineral products, the industry with the second

15I do not include non crisis data in the left hand side of the regressions. The reason is that the data-set includes areasonable amount of methodological breaks in the time series that are not properly documented by UNIDO. This problemis specially severe among developing countries. By restricting the number of years of data used by each country to thosearound the crisis I restrict the possibility of having these breaks contaminate the results. The use of three digit level ISICRev. 2 classification allows me to have data for the early 80’s

16I implement these in STATA using the cgmreg.ado file produced by the authors.

11

highest inventory-to-cost ratio.

3.3 Inventory-to-Cost Ratio

As emphasized in section ??, to a first order approximation the sensitivity of a firm to an interest

rate shock is increasing in the steady-state inventory-to-cost ratio. This is the hypothesis I test.

However, it is impossible to get reliable measures of inventory-to-cost ratios for most countries in the

sample. For this reason, I use measures based on US firms. The idea is that their inventory-to-cost

ratios should reflect the underlying production technology, so that it should be a reasonable proxy for

inventory-to-cost ratios in other countries. Moreover, since the business cycle in the US is relatively

milder, inventory-to-cost ratios measured at particular periods are more likely to be close to their

steady state levels. To the extent that the proxy is imperfect the measurement error will tend to

attenuate the results.

The benchmark measure of production time is based on the 2005 and 2006 Annual Survey of

Manufactures of the US Census Bureau. It is the ratio between total inventories and production costs

as measured by the value of materials plus the cost of production labor. Together, these account for

the bulk of the cost of goods sold as it usually appears in firm’s balance sheets. The main advantage

of this survey is that it is representative of the manufacturing sector as a whole. However, the main

disadvantages is that, with data from two years, the observations hardly qualify as a steady state

measure. Furthermore, because the data is not directly based on accounting documents, there is no

guarantee that costs and inventories are valued consistently. In particular, it is possible that inventories

include cost components beyond materials and production labor or otherwise take into account a

different definition of production labor. Finally, privately owned firms may at times manipulate

inventory numbers for tax efficiency purposes and, for this reason, may choose not to answer the

survey accurately.

An alternative measure is based on firm level balance sheet data from COMPUSTAT, which guar-

antees that the accounting measures are consistent. The inventory-to-cost ratio for a given industry

is the median of the ratio across firms and years. I first take medians over data disclosed in December

and June separately. The final number is an arithmetic average of the two. This procedure minimizes

the role of seasonal bias.17 Because COMPUSTAT includes observations spanning over twenty years

of data, business cycle fluctuations are smoothed out, giving extra credibility to the steady state as-

sumption. The disadvantage of COMPUSTAT is that it only includes listed firms, so that its sample

is hardly representative of all firms.

The two measures previously discussed focus on American firms and the working assumption is

that the technological characteristics of US firms are sufficiently informative about the technological

characteristics of firms in crisis countries. In order to have some indication on whether this is the case,

I also use a measure of inventory turnover from the Korean Financial Survey Analysis. In contrast

17By far most of the observations are in December, so that such a correction is helpful.

12

to the measure based on the Annual Survey of Manufacturing, this gives equal weight to firms of

different sizes. The main advantage is that this avoids measurement error associated with idiosyncratic

decisions of very large producers, a particular problem in South Korea given its high rate of industrial

concentration. The turnover measure is defined as inventories/sales as opposed to inventories/costs,

which means that the numbers should be slightly smaller since sales are typically larger than costs.

Table ?? has the descriptive statistics for the three variables. The average production time is highest

in the COMPUSTAT sample, at 2.5 months, with a slightly smaller number for the Korean data.

Figure ?? shows the joint distribution between the Korean data (in the horizontal axis) and the two

US based measures (in the vertical axis). There is a reasonable amount of correlation between them,

between 0.5 and 0.6, summarized in table ??. The correlation between the Korean and American data

implies that taking US numbers as representative of other countries may not be so off the mark.

3.4 Controls

In this section I describe the controls. I include controls that account for a large range of alternative

forces that may lead to a sectoral reallocation. These are important to the extent that they are

correlated both with the inventory turnover ratio and the change in value added in the crisis period.

Table ?? has the descriptive statistics for the control variables. Table ?? has the correlations with the

dependent variables. In what follows, I discuss each one of them in detail.

3.4.1 Demand Side

Industries that specialize on investment or durable goods should be more impacted in a crisis since the

demand for these products is more pro-cyclical.18 On the other hand, firms that are export oriented

should experience a smaller drop in output.

I infer the share of output that is destined to the production of exports, investment goods and

durable consumer goods using input-output matrices made available by OECD.19 To measure the

demand for durable consumer goods consumption, I assume that all the consumption from certain

sectors is durable.20 I use country specific input-output matrices whenever possible, otherwise I

use an average for the region.21 I allow for indirect demand effects through the supply chain. As

a consequence, the control variable takes into account that the demand for basic metals is heavily

affected by the demand for investment goods.

18see, for example, the behavior of investment described by Calvoetal:2006b.19Thus basic metals are destined to the production of investment goods even though this only occurs indirectly. The

Leontief inverse gives the indirect destinations of output.20I define as durable consumption all the consumption of wood products, furniture, non-metallic mineral, machinery and

equipment and likewise use the Leontief inverse to account for indirect effects.21Thus, for example, the input-output structure for Malaysia is the average between South Korea and Indonesia.

13

3.4.2 Cost

During a sudden stop, there are massive realignments in relative prices. One particular case of interest

are imported inputs, which usually become more expensive. In the opposite direction, the reduced

demand for labor in a crisis should reduce wages. To capture these effects I include the share of labor

and imported inputs into production. For completeness, I also include a control for material share.

This is interesting since firms with high share of materials will have less sunk costs and will be more

willing to adjust its production to new circumstances.

3.4.3 Normal Cyclicality

The results may not capture the particular effect of the sudden stop, but just the usual effect of a

downturn. To proxy for the typical cyclicality of an industry, first I regress the growth in output of

each country/industry on GDP using overlapping three year windows as my observations but excluding

the 3 year period included in the left hand side of the main regression. I then collect the coefficients

and average them over industries. footnoteI also experimented with a measure of cyclicality based

only on US data. The results are largely similar, and are available upon request.

3.4.4 External Dependence

Rajanzingales:1998 define External Dependence as

External Dependence =Capital Expenditure - Cash Flow

Capital Expenditure

They calculate averages of this ratio for listed firms in the US. Rajan and Zingales argue that

the ratio captures technological aspects of production, in particular, the extent to which investment

is front-loaded when compared to production. Everything else constant, if access to finance is more

expensive, industries that require more up-front investment should do relatively worse. Dellaric-

cia:2007 and Kroszneretal:2006 have applied this insight to banking crises, and they find an important

role for external dependence. For comparability, I use the same numbers for external dependence as

Rajanzingales:1998.

3.4.5 Size

The empirical corporate finance literature has often focused on size as a determinant of differences in

the supply of finance available to different firms.22 Firm size may also matter because large firms are

more likely to be exporters.23 The UNIDO dataset has data on employment and number of establish-

ments by industries. I calculate for each country/industry pair the average employment/establishment

22See Fazzarietal:1988 for the seminal paper and GertlerGilchrist:1994 for an application specific to interest rate shocks.However, see also Kaplanzingales:1992 for a critique.

23See Melitz:2003.

14

ratio.24

3.5 Results

Table ?? shows the regression results with the turnover ratio from the Annual Survey of Manufacturing

as the dependent variable. Each column corresponds to a different measure of the turnover ratio. The

results are consistent and, for the measures based on US firms, statistically significant. The coefficient

on the turnover ratio of Korean firms is slightly higher. This is because for Korean firms the data

corresponds to inventory-to-sale ratio and sales are larger than costs.

The results for the controls are interesting in themselves. Most of them have the expected sign,

with exception of external dependence, which is positive, and the wage share, which is negative. The

coefficient on wage share is surprising, since it is highly statistically and economically significant. A

standard deviation change in the wage share implies a drop of 4.3% in output, which is an effect of the

same order as the inventory turnover. The exact reason for this coefficient constitutes a puzzle. One

possible explanation is that there are lags between the training and hiring of workers and production

of goods which are not adequately captured by inventories. Also, the evidence sits in nicely with the

suggestion by NeumeyerPerri:2004 that an interest rate shock increases primarily the cost of labor

input.

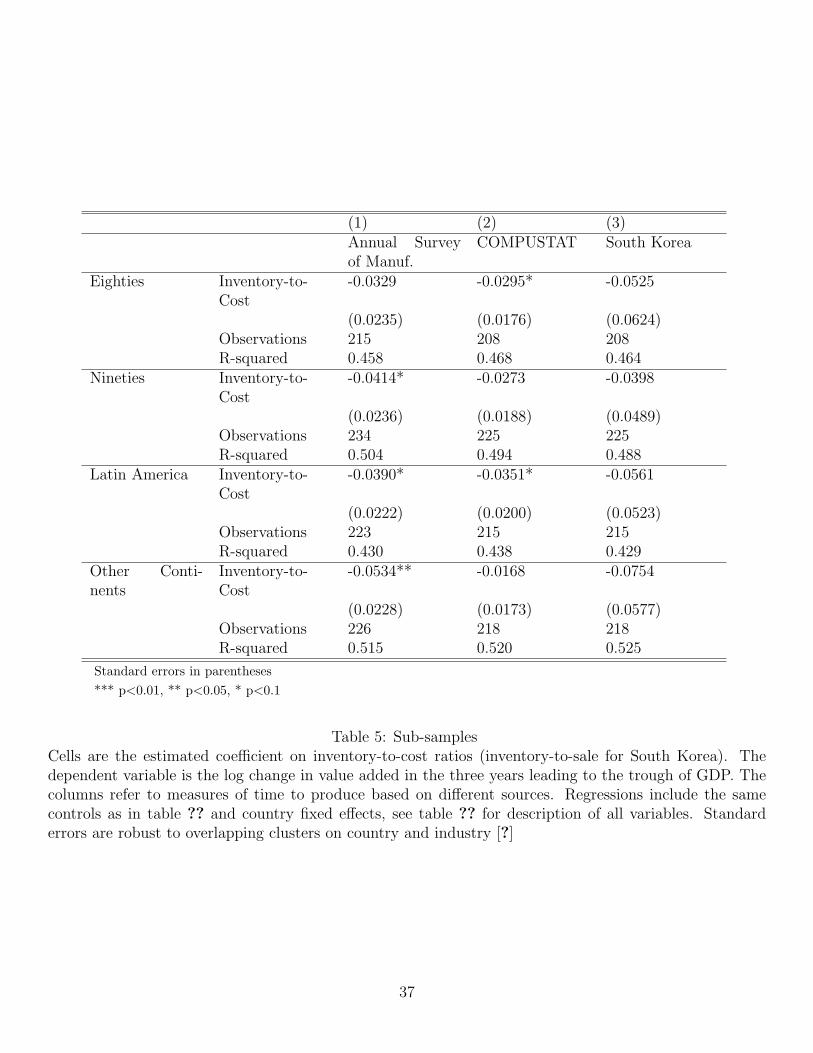

3.5.1 Sub-samples

Crisis episodes were heavily concentrated in certain time periods and geographic regions. About half

of the crises in the sample took place in the early eighties and the other half between the mid to late

nineties (and Argentina in 2001). Geographically, about half of the crises were in Latin America and

the rest distributed between Asia, Africa, Russia and the Middle East. I assess whether the coefficient

on the inventory-to-cost ratio is robust to splitting the sample in different ways.

The results are in table ??. The point estimate of the coefficient on inventory-to-cost ratios is

remarkably robust. For the US based measures, the coefficient is robust in 5 out of 8 cases. Given

that samples are half the size, it is not surprising that the statistical significance is reduced.25

The robustness of the coefficients is specially interesting, since in the early eighties, the crises

were followed by a much larger increase in inflation than in the nineties. The results provide further

evidence that cash-in-advance constraints were not playing an important role in production decisions.

3.5.2 Alternative time windows and persistence

A further robustness check involves changing the window over which I consider the drop in output.

The results are summarized in table ??. In the first rows I shorten the window by using a year closer

24I also experiment with the employment/establishment ratio in the year before the crisis. The results are virtuallyidentical.

25I have also run regressions that only include East Asian countries. However, there are only four of those in the sample,Korea, Malaysia, Thailand and Indonesia. The standard errors become even larger and the results unstable.

15

to the trough as the benchmark. The coefficients are robustly negative, although they tend to be less

significant and the coefficient smaller. As mentioned above, shorter time windows include cases where

the crisis was already under way in the initial year. Furthermore, estimates based on shorter windows

are likely to be more noisy, which by itself should imply larger standard errors.

The windows in the last two rows compare value added three years before the trough of the crisis

with, respectively, three and five years after the trough. The coefficients provide information about

the persistence in the reallocation once the recovery has taken place. The somewhat surprising result

is that the reallocation is quite persistent. This is important because it indicates that the findings are

most likely not associated with short-term inventory adjustment. Given a total inventory turnover

ratio of less than three months and an even smaller number as far as finished goods inventories are

concerned, these dynamics should have been exhausted once the recovery is under way.26

4 Quantitative Model

4.1 Model Setup

The model economy has multiple sectors, allowing for investigation of the impact of different shocks

on the cross-section of industries. In particular, it has NT tradable sectors corresponding to manufac-

turing sectors. Since this is a general equilibrium model, I also allow for NNT non-tradable sectors in

order to have a comprehensive depiction of the economy.

4.1.1 Household

Let st denote the history of states of nature up to time t. There is a representative household who

takes prices as given and is able to borrow and lend abroad at an exogenous riskless gross interest rate

er(st). The household supplies labor and consumes both durable and non-durable goods. The utility

function of this household is time-separable with period utility given by

u(C

(st

),KH

(st

), L

(st

))=

11− σ

[γd 1ρC

(st

) ρ−1ρ +

(1− γd

) 1ρKH

(st

) ρ−1ρ

] ρρ−1

−L

(st

)1+ 1ψ

1 + 1ψ

1−σ

Where C(st

)is non-durable consumption and D

(st

)is the stock of durable goods held by the

household, L(st

)is labor supply.

This utility function follows GHH:1988. Its essential property is that the labor supply does not

respond to wealth of the household, only to wages. One motivation is that labor supply is costly

26In particular Alessandriaetal:2008 study the implications of inventory adjustment dynamics for the response of importsand import prices in the aftermath of devaluations. They find large effects which, however, exhaust themselves in less thana year.

16

because it implies a loss in output from home production or self employment. Such an interpre-

tation is particularly suitable for developing countries, where a large fraction of the population is

self-employed.27

4.1.2 Production Functions

The production function of each sector is:

Y i(st

)=

τ i∏v=0

Zi(st−v, v

)ωi(v)∑

ωi (v) = 1

Where Yi is the production of the input i. Zi(st−v; v

)denotes a composite of goods acquired in

period t− v to produce the finished good which is sold v periods ahead. It is defined as:

Zi(st, v

)= γiea(s

t) (ui

(st; v

)Ki

(st; v

))αiK (Li

(st; v

))αiL (Mi

(st; v

))1−αiL−αiK

Where ui(st−1; v

)denotes the rate of utilization of fixed capital at t.

4.1.3 Capital Accumulation, Utilization and Maintenance Costs

Capital is sector specific and is produced by combining old capital and investment goods:28

Ki

(st

)=

[(1− δKi

) (Ki

(st−1

)) ζ−1ζ +

(δKi

) 1ζ

(Ii

(st

)) ζ−1ζ

] ζ−1ζ

Durable consumer goods are produced in a similar fashion:

KH

(st

)=

[(1− δD

) (KH

(st−1

)) ζ−1ζ +

(δH

) 1ζ (IH

(st

)) ζ−1ζ

] ζ−1ζ

Whenever a firm uses capital, it has to make up for wear and tear. This maintenance requirement

is increasing in capacity utilization. The required spare parts satisfy:29

27The motivation for strong wealth effects in labor supply relies to a large extent on the observation that there is not aclear long run trend in average hours worked [?]. However, there is a clear increase in labor force participation in emergingmarket economies. See, for example, Young:1995 for the Asian Tigers.

28

Let Ki(st) = K(I(st),K(st−1)

). The parametrization below is such that G satisfies the following conditions:

K = K (δK,K) ,∂K (δK,K)

∂I= 1,

∂K (δK,K)∂K

= 1− δ

29In the calibration, I choose units so that in steady state u = 1 and the firm does not have maintenance costs. If capacityutilization is below steady state, the firm has spare parts, that they can sell at market prices for alternative uses. This

17

Ωi

(st

)=

χ

1 + ξ

[ui

(st

)1+ξ − 1]Ki

(st

)4.1.4 Composite Goods

Non-durable consumption C(st

), fixed investment Ii

(st

), durable consumption good investment

IH(st

), materials Mi

(st

)and spare parts Ωi

(st

)are composites of the goods produced in the

NT +NNT sectors and imported goods. These composites are represented by CES aggregates:

X(st

)=

∑j∈1,...,NT+NNT

(γjX

) 1ρ (Xj

(st

)) ρ−1ρ

+(1−

∑j∈1,...,NT+NNT γ

jX

) 1ρ (X∗ (

st)) ρ−1

ρ

ρρ−1

Where X stands in for C, Ii, Ωi or Mi. X∗ (st

)is the amount of imported goods used for the

production of X and∑γiX < 1.

4.1.5 Foreign Trade

While the economy is small with respect to capital markets, it is large relative to product market. This

is the case, for example, if countries produce different varieties that are not perfect substitutes.30 This

assumption implies that tradable sectors have to respond at least somewhat to changes in domestic

demand.

The tradable sectors face the following inverse demand function:

pi(st

)= χi

[EXP i

(st

)]− 1θ

Where pi(st

)is the price of good i with respect to the foreign good and EXP i

(st

)are exports of

sector i good. I assume that services, construction and real estate are non-tradable.

For the tradable sectors, exports are identical to the total output from sector i minus the sum of

the domestic demands for this good:

EXP i(st

)= Y i

(st

)− Ci

(st

)− IiH

(st

)−

∑j∈1,...,NT+NNT

(M ij

(st

)+ Iij

(st

)+ Ωi

j

(st

))For non-tradables, exports are equal to zero:

EXP i(st

)= 0 if i is non-tradable

assumption is made for tractability, but does not have any important consequence.30It is a common assumption in the literature. See GertlerGilchristNatalucci:2007 and KehoeRuhl:2008. Note that this

does not imply monopolistic power if many producers in a country produce the same variety. All that is required is that thecountry be sufficiently big relative to the world demand for that variety.

18

Total imports are the sum of all foreign goods demanded for different uses:

IMP(st

)= C∗

(st

)+ I∗H

(st

)+

∑j∈1,...,NT+NNT

(M∗j

(st

)+ I∗j

(st

)+ Ω∗

j

(st

))I take these foreign goods to be the numeraire, so that their price is identical to 1. The current

account identity is:

B(st

)−R

(st−1

)B

(st−1

)= IMP

(st

)−

∑i∈1,...,NT

pi(st

)EXP i

(st

)Where B

(st

)is the amount of net foreign debt held by domestic households.

4.1.6 Resource Constraints

While capital is sector specific, its utilization can be shuffled around for the production of goods to

be finalized at different horizons. This implies the following resource constraint for capital stock for

sector k:

∑v

ui(st; v

)Ki

(st; v

)≤ ui

(st

)Ki

(st

)Raw materials respect an analogous resource constraint:

∑v

Mi

(st, v

)≤Mi

(st

)In contrast, labor is perfectly mobile between sectors. This implies the following labor market

clearing condition

∑k∈1,...,NT+NNT

n∑v

Li(st, v

)≤ L

(st

)Finally, there is a market clearing condition in the non-tradable sectors. This is:

Ci(st

)+ IiH

(st

)+Gi +

∑j∈1,...,NT+NNT

(M ij

(st

)+ Iij

(st

)+ Ωi

j

(st

))≤ Y i

(st

)Where Gi are government purchases, assumed to be constant over time.

19

4.1.7 Equilibrium

The economy has a representative household and there are no frictions or missing markets. This

implies that the allocation can be computed as the solution to a planner’s problem. However, this has

to be modified so that the planner does not internalize the impact of choices on pi(st

). Otherwise, the

planner would use market power in the foreign goods market to increase the welfare of home house-

holds at the expense of foreign households. Such coordination is unlikely to occur in a decentralized

equilibrium.

The equilibrium is defined as follows: The social planner takes the functionspi

(st

)k∈1,...,NT

as

given and chooses all remaining functions of st to maximize household welfare subject to technological

and resource constraints described above. The equilibrium is the solution to the planner’s problem

andpi

(st

)k∈1,...,NT

so that for all st,pi

(st

)k∈1,...,NT

=χi

[EXP i

(st

)]− 1θ

k∈1,...,NT

.

4.2 Calibration

4.2.1 Sectors and Shares

The first task is to assign empirical counterparts to the different sectors. I use an average of the

input-output tables in section ??. To do this, first I normalize the entries in each of the tables to total

production in the country. I then average over all of them. the resulting” input-output table has 48

sectors which I aggregate into 20 as follows:

First, I aggregate all the non-manufacturing sectors into three non-tradables: construction and

real estate and a large, residual, “service” sector that includes services, retail, utilities, public admin-

istration and agriculture. I treat mining as a foreign sector since it is highly tradable and employs

very little.31

Singling out the construction sector is interesting because its long production time has motivated

the introduction of time to build technology by Kydlandprescott:1982. It is potentially very important

in so far as aggregate dynamics are concerned. The real estate sector, in turn, is included to absorb

the output of the construction sector. The real estate sector allows the model to have a large and

important construction sector without exaggerating the importance of this type of capital in the

remaining production activities.

As far as the manufacturing sectors are concerned, I assign to each one of them an ISIC Rev. 2 code

in order to be able to match to the data in the emprical section. The correspondence is not perfect.

Some sectors that are differentiated in the empirical section, such as textiles and apparel, only appear

as a single sector in the input-output matrix. On the other hand, the input-output matrix includes

more machinery producing sectors than in the UNIDO data-set. In this latter case, I consolidate the

sectors in order to build equivalents to the ones in section ??.

The sectors that I treat as non-tradable do, as a matter of fact, trade. I treat all their sales abroad

as domestic sales and all the purchases from their counterpart abroad as domestic purchases. I am

31I also experimented with treating agriculture the same way as mining. The results are not sensitive to this assumption.

20

still left with a (small) imbalance. Also, at the aggregate level there is a trade imbalance that does

not come up in the steady state of the model. I remove these imbalances by rescaling the size of the

non-tradable sector and of domestic absorption.

I rescale the labor shares up by a factor of 2, conforming to the findings in Young:1995 and

Gollin:2002 that labor shares in developing countries are frequently underestimated because of the

large number of self-employed workers. This brings the aggregate labor share close to 0.6, which is

the norm of developed countries. Also, I do not allow explicitly for indirect taxes in the model, so that

I split them between labor and capital income.32 Given the input-output table, it is a straightforward

matter to calculate the factor shares for the different sectors as well as the weight of each sector in

each of the different composite goods.33

4.2.2 Time to Produce

I calibrate the production process in each sector as follows. First, for the manufacturing sectors, I set

Y i(st

)= Zi

(st, 0

)1−ωiZi

(st−1, 1

)ωiI choose ωi for each sector so that the inventory-to-cost ratio matches the numbers constructed

from the Annual Survey of Manufacturing.34

The production function for services and real estate sectors is simply:

Y i(st

)= Zi

(st, 0

)Finally, for the construction sector,

Y Const.(st

)= ZConst.

(st, 0

) 14 ZConst.

(st−1, 1

) 14 ZConst.

(st−2, 2

) 14 ZConst.

(st−3, 3

) 14

Counter-Factual Calibrations: For the sake of comparison, I also include some counter-factual

calibrations. I assume that all manufacturing sectors produce instantaneously, so that

Y i(st

)= Zi

(st, 0

)∀i ∈ 1, NT

4.2.3 Export demand, capital accumulation and maintenance cost

The crucial parameter in the demand for net exports is the price elasticity, θ. In fact, the literature on

emerging market business cycles has diverged dramatically on the appropriate value for this parameter,

32For an interesting account of how heterogeneity in indirect taxes provides a foundation for fluctuations in TFP, seeBenjaminMeza:2009.

33The only slight difficulty is in making sure that factor shares reflect the heterogeneity in opportunity cost of capital facedby the different sectors.

34For sectors which encompass more than one sector in my data-set, I pick the number corresponding to the one withrelatively larger value added.

21

with some papers setting it as low as 1 or 2 and many other papers assuming that the economy

is small in the goods markets, so that, effectively, θ → ∞. Econometric estimates diverge, with

Mendoza:1994 finding that there is no Granger causation running from exports to terms of trade, and

SenhadjiMontenegro:1998 estimating price elasticities of export demand as low as 1.5. More relevant

to the present work, Bursteinetal:2005 show that, over some important cases of large exchange rate

depreciations the price of traded goods at the dock dropped very little in foreign currency terms,

which suggests a high elasticity of demand for exports. I use θ = 20 as my benchmark and, in the end

of the paper, present sensitivity analysis with θ = 2 and θ = 200.

For the capital accumulation equations, I set the depreciation of fixed capital δK equal to 10%

yearly for all sectors but real estate. The depreciation rate for the capital of the real estate sector

I set to 2.3% yearly. Finally, the depreciation of durable consumer goods δH to 13%. These values

approximate the rate used by the Bureau of Economic Analysis to depreciate stocks of physical assets

in the US economy.

To calibrate maintenance cost, I set ξ = 0.5 and µ set such that in steady state ui(st

)= 1. As

far as the share parameters are concerned, I assume that they are identical to the investment good,

except that I exclude output from the construction sector.

The remaining parameter is the elasticity of investment to the replacement cost of capital, ζ. This

is hard to calibrate, so that I allow the model to pick it jointly with the interest rate and TFP shocks

(see discussion below).

4.2.4 Remaining Parameters

For the household preferences, there are three parameters to be calibrated, ψ, σ, ρ. I follow Men-

doza:1991 and UribeYue:2006 and take ψ = 2.28 and σ = 2. The household discounts the future at a

rate β. I set that to be equal to 1R in steady state, and choose R so that the steady state interest rate

is 3.5%.

I assume ρ = 2, so that the output of different sectors are substitutes.

4.2.5 Exogenous processes and adjustment costs

The exogenous state determines the path of interest rates, productivity, and foreign demand for

domestic inputs. These are described by the following auto-regressive processes:

r(st

)= (1− ηr) r + ηrr

(st−1

)+ εr (st)

a(st

)= ηaa

(st−1

)+ εa (st)

I pick the steady state interest rate r to match the ratio between investment and total output.

This is about 8.49% per year, which is consistent with the interest rates often observed in emerging

markets.

22

I model the crisis as a simultaneous, one-time shock to both processes. In order to calibrate the

magnitude of the shocks and the persistence parameters, I use the average deviation from trend of

output and capital formation across the crises episodes. In particular, I require that the model matches

the average drop of GDP and fixed capital formation in the trough of the crisis, and that it matches

the change in the deviation from trend in the two years after the trough.35 The calibration targets

are depicted in figure ??. Note in particular that investment drops much more than GDP and that

both series remain fail to revert to their previous trend.

The calibrated parameters are highly dependent on the importance of adjustment costs. If adjust-

ment costs are high, the same drop in investment relative to output will require a larger increase in the

interest rate. Since adjustment costs are particularly important for the short term dynamics of invest-

ment following a shock, I use available quarterly data on investment and GDP from UribeYue:2006.

Their dataset includes information on six episodes which are included in the events studied in this

paper.36 The exact quarter in which the crisis starts is easy to identify. It is the quarter close to the

trough of the crisis in which there was a large increase in the trade balance. As the calibration target,

I use the ratio of average investment/GDP ratio in the trough of the crisis to its value in the first

couple of quarters after the shock.37 This calibration target is depicted in figure ??.

The calibration based on investment and GDP series is preferable to the use of direct measures of

the interest rate and TFP. Interest rates in emerging markets can be a poor measure of the marginal

cost of funds faced by agents in these economies, specially around times of crisis. On the one hand,

interest rates may reflect risk premia that, per se, do not add to the marginal cost of funds. On the

other hand, many of the crisis economies had fairly regulated financial systems to begin with. From

that perspective, the interest rate could actually be an underestimate of the marginal cost of capital.38

As for TFP, an accurate measurement requires the calculation of hours data which, for most of these

countries, is not available.

The calibration implies a very persistent interest rate shock (ηr = .99) , high adjustment costs

(ζ = 0.91), and a TFP shock that mean-reverts relatively quickly (ηa = .91). The persistent interest

rate is necessary to account not only for the persistence of investment and of GDP, but also in the

drop in the investment/output ratio.

I solve the model by log-linear approximation around the non-stochastic steady state. This is

necessary because of the large number of state variables.39

35See details in Appendix C.36Argentina (2001), Ecuador (1999), Malaysia (1998), Mexico (1995), South Korea (1999), and Turkey (1998).37See details in Appendix C.38Naturally, this discussion suggests that the implicit restriction that all sectors in the economy face the same interest rate

may not be appropriate. Investigating the role, if any, that such a heterogeneity is an important direction for future work.39I solve the model using Dynare.

23

4.3 The Effect of Shocks

This section studies the effect of exogenous shocks in the economy described above. I show the

results for aggregate GDP, gross capital formation and cross-sectoral output. The central purpose

is to understand the role of the time-to-produce technology. In order to emphasize this, I use the

calibration for the exogenous shocks and capital adjustment cost parameters used in the full model.

Figure ?? shows how output and investment react to the shocks under the different assumptions

concerning the existence of time to produce. In order to facilitate the comparison I do not recalibrate

the shocks and adjustment cost parameter for the different models. The interest rate shock is very

persistent, which, in turn, implies a persistent reaction of GDP and investment. In effect, GDP

is declining over time as fixed capital is progressively reduced. In contrast, the reaction of GDP

and investment to the TFP shock are clearly mean-reverting, in line with the mean reversion in the

exogenous shock itself.

Over the long run, interest rate shocks are most potent in the full model. This is not surprising,

since the models without time to produce has one less channel through which the interest rate can

affect output. Interestingly, there is not a discernible difference between models in the reaction to the

TFP shock.

The most interesting differences between the models are in the first couple of quarters following the

shocks. First, they highlight the role of sunk costs in generating delayed responses. Because in both

models there is time-to-build in the construction sector, investment decreases only slowly in the first

four quarters. This is because it is optimal to conclude building projects that were initiated before the

shock hits given that a large part of the requisite effort has already been made.40 A similar dynamic

is visible in the response of GDP to a TFP shock. Instead of dropping immediately and then slowly

recovering, GDP follows a hump-shaped response pattern.

The final result is that, over the first couple of quarters, GDP responds most strongly to an interest

rate shock if manufacturing production takes time. The reason is that, absent production lags, over

the short run manufacturing sectors are very little affected by the interest rate shock. In effect,

they benefit from lower wages and lower price of non-tradable inputs. The possibility to reallocate

labor from non-tradable towards the tradable sector allows the economy to adjust to the interest

rate shock without much initial pain. The result is reminiscent of the findings by KehoeRuhl:2008

and Charikehoemagrattan:2005.41 The interest rate shock does become important over the longer

run for all models, as fixed capital gets depleted. Once time-to-produce is allowed for, firms in the

manufacturing sector react to the interest rate shock with a reduction in output, since now their

40In the model, fixed investment is only accounted for once the final good is ready to be incorporated into the capitalstock. According to the 1993 System of National Accounts, “The time at which gross fixed capital formation is recordedis when the ownership of the fixed assets is transferred to the institutional unit that intends to use them in production.”(http://unstats.un.org/unsd/sna1993/toctop.asp, Ch. 10-B). Thus, the procedure is adequate if in the economies underconsideration all construction activity is performed by institutional units other than the ones who actually use the buildings.This is unlikely to be the case, but it is a better assumption than that all construction is made in house.

41Although in these papers, the counter-intuitive results are made even more dramatic because the authors allow for wealtheffects on labor supply.

24

production costs have increased. Note that the difference between the two models is visible even in

the first quarter, since value added includes the change in inventories, itself a forward looking variable.

Finally, the scatter plots in figure ?? shows the deviation from trend in the value added of each

sector, averaged over the trough of the crisis. The first row depicts results for the full model, whereas

the second row has the results for the model where time to build is only prevalent in the construction

sector. The TFP shock has mainly a level effect, with very little implications for the cross-section

in either model. In contrast, in both models the interest rate shock generates a reallocation in the

direction shown by the data. However, the reallocation is much stronger in the model with production

time in manufacturing.42

4.4 Comparison with Data

Figure ?? compares output in different sectors in the trough of the crisis in the data with what both

the full model and the model where manufacturing sectors produce instantaneously. The data for each

industry refers to an average across countries of the difference between their current output and their

previous trend.

Overall the model generated data tends to over-estimate the performance of manufacturing sectors

relative to the data, as demonstrated by the higher intercept of the regression curves. The model fares

much better is in capturing the slope of the regression line, which I take as a measure of the reallocation

towards sectors with low inventory-to-cost ratios. This is most visible in figure ??, where the data-

points correspond to deviations from means, so that all regression lines have the same intercept. Note

that the model without time to produce in manufacturing has a much flatter slope.

In what follows I discuss the results in more detail, with special attention for the role of different

parameters.

4.4.1 Reallocation from Tradables to Non-Tradables

The average drop in manufacturing is, in the data, larger than the drop in overall GDP.43 44

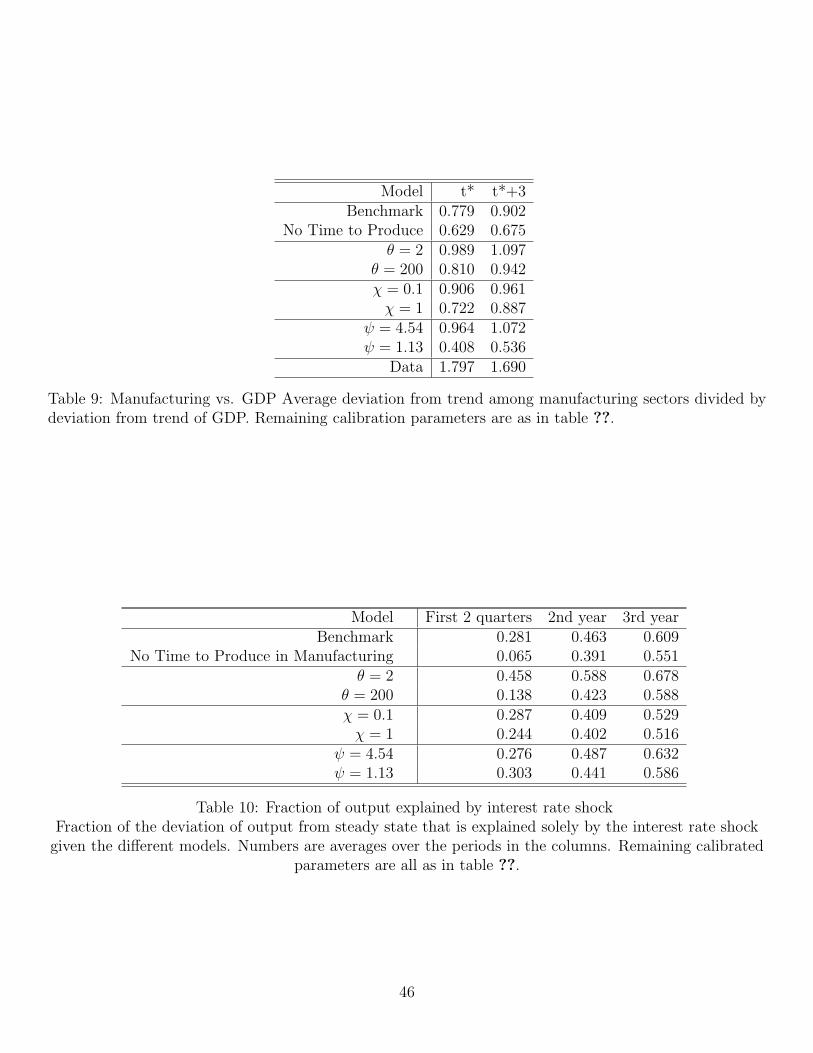

Table ?? shows the average deviation from steady state of output in the manufacturing sector

relative to the deviation from steady state of GDP given different parametrizations of the full model

(to facilitate the comparison, I do not recalibrate the persistence and magnitude of the shocks and the

42The major reason there is a reallocation in the model without production time is because there is a correlation betweenorientation towards the production of investment goods and production time. The slope goes away once this correlation iscontrolled for.

43This empirical finding stands in contrast to the findings by TornellWestermann:2002 who document that, in the aftermathof emerging market crises, there is a reallocation from non-tradable to tradable production. To a large extent the discrepancyhas to do with aggregation: manufacturing sectors that fall least also respond for a larger share of manufacturing production.In contrast, I weight all sectors equally in this exercise.

44A similar problem occurs in KehoeRuhl:2008 model of sectoral reallocation in the Mexican crisis. While the authorsclaim success in generating a reallocation towards tradable production, the reallocation implied by the model is much largerthan the one they find in the data.

25

capital adjustment cost parameter). Higher numbers imply that the model predicts that manufacturing

drops relatively more when compared to overall GDP.

When compared to the model where production in the manufacturing sector is instantaneous, the

full model does somewhat better. This is not surprising, since if production is instantaneous, the cost

of manufacturing production will not be directly affected by the interest rate.

The reallocation from non-tradables to tradables is much less pronounced if labor supply is more

elastic. The reason is that with inelastic labor supply, workers displaced from the non-tradable sector

move to manufacturing. If labor supply is elastic, it will be preferable for many of these workers to

stay at home rather than have a low labor productivity in one of the manufacturing sectors.

Another interesting parameter is the elasticity of foreign demand for exports. The relative gains

for the tradable sector are least if this elasticity is low. This is fairly intuitive. With a low elasticity

of demand, there is less to be gained by increasing exports.

Finally, the output loss in the manufacturing sector is relatively larger if capacity utilization costs

are close to linear. The reason is that, with linear capacity utilization costs, small changes in costs

have a large impact on output.

4.4.2 Reallocation within Manufacturing

Where the benchmark model does a much better job is in replicating the reallocation pattern within

manufacturing. This can be seen from the slope of the regression line in the model, which is only

slightly smaller than that for the data. In contrast, the model without production time among

manufacturing industries does a much poorer job. To the extent that it does imply a negative slope,

this is a consequence of other cross-industry differences, such as export orientation.

In order to isolate the role of production time, I regress the model generated data on model

equivalents of the controls included in the regressions in the empirical section of the paper. I use all

the sources of cross-sectoral heterogeneity which are explicitly modeled, leaving out establishment size,

external finance dependence and cyclicality. Table ?? show the estimated coefficient for the inventory-

to-cost ratio in the model, given different parametrizations. The coefficient in the benchmark model

is smaller than in the data, but still within the confidence interval. In contrast, in the model where

production in the manufacturing sector is instantaneous, the coefficient becomes positive.

As far as alternative parametrizations are concerned, the most interesting results are linked to

assumptions about the price elasticity of foreign demand for domestic exports. In order to get a

quantitatively meaningful cross-sectoral reallocation it must be the case that this elasticity is high. If

it goes down to 2, very little cross-sectoral reallocation occurs. The reason is that final price changes

would countervail the impact of the interest rate shock on production costs.

4.4.3 Initial Impact

One important issue for the emerging market literature is the extent to which a sudden capital flight

can in and of itself generate an immediate drop in output. To a large extent, this preoccupation

26

is behind NeumeyerPerri:2004 modeling decisions and Charikehoemagrattan:2005 critique. In the

context of this model, the question is to what extent the interest rate shock alone can account for the

initial drop in output immediately following the crisis shock.45

In the benchmark calibration, the interest rate shock accounts for more or less 25% of the drop

in output in the quarter when the shock hits and the following one. This is substantial, but not

overwhelming. However, it is much larger than what is obtained if there is no production time in the

manufacturing sectors, which is essential zero. The reason is that, absent production time, the planner

can move resources away from the non-tradable sectors towards tradable production in response to

an interest rate shock, so that the resulting movements in demand have very little effect on output.

Also, any effects on the supply side only accrue over longer periods of time, as the fixed capital stock

is depleted.

With time to produce, savings are needed not just to fund fixed investment, but also to fund

variable investment, in the form of materials, labor input and spare parts needed to make up for

capital utilization. Because the maturity time of this form of investment is much shorter, the results

are felt almost immediately.

As far as alternative parameters are concerned, again the most interesting ones are the ones

concerning the price elasticity of exports. The role of the interest rate is largest when the price

elasticity of exports is low. In this case, the planner cannot easily make up for the reduced domestic

demand by increasing output in the exporting sectors since this attempt will be met by increased prices.

Note, however, that in this case a completely different mechanism is at play. While interesting, such a

mechanism is inconsistent with the cross-sectional evidence since, as discussed in section ??, such low

elasticities would imply an inability of the model to generate a pattern of cross-sectoral reallocation

consistent with the data.

5 Conclusion

This paper proposes that production time is an important propagation mechanism for interest rate

changes. It partly accounts for two observations about emerging market economies: that shocks to

the interest rate have a strong and swift impact on output and that in crisis episodes there is a

substantial reallocation towards industrial sectors that use few inventories relative to their costs. It is

similar to NeumeyerPerri:2004 payment-in-advance constraint in so far as the aggregate implications

are concerned, but it is also able to account for cross-sectional facts.

The paper opens up some important avenues for research. First, it highlights the importance of

understanding the role of variable capital investment in order to understand emerging market crises.

While this role was previously emphasized by NeumeyerPerri:2004 as a means to generate reasonable

time-series behavior out of for a Small Open Economy RBC model, as it turns out something along

these lines is also necessary to generate the requisite cross-sectoral behavior. The particular form of

45Such a decomposition is possible because the model is solved using a linear approximation.

27

variable capital emphasized in this paper, summarized in the inventory-to-cost ratios, is interesting in

that it is relatively straightforward to measure and is associated with real quantities. As a consequence,

it does not rely on frictions which are hard to measure and to motivate.

One direction for further work which is closer to the spirit of NeumeyerPerri:2004 contribution

is to investigate the special role of the wage-bill. The regression results imply that labor intensive

industries did relatively worse in the crises, when everything else is constant. This is, on the face of it,

a counter-intuitive finding, that deserves further exploration. One possibility, which is in line with the

argument in this paper, is that labor includes administrative work, which has a longer time horizon

than labor directly applied to the production process. More generally, the need to train new workers

and other costs of hiring may have similar implications. Allowing for a richer labor market structure

seems to be an interesting way forward.

The second avenue for research is an exploration of the links to the credit friction literature. In

the paper, I take the cost of capital as given and look at the effects on production, while much of the

literature does the opposite. The question is whether there is some important insight to be gained by

combining the two. This is specially likely to yield interesting results if credit frictions operate at the

level of the firm, as in currency mismatch models or if the crisis is understood primarily as a failure of

the banking system in channeling funds from consumers to firms.46 In these cases, a mechanism that

operates specifically through the supply is important in order for these frictions to have important

role in so far a short term output dynamics are concerned.

Third, it is worth asking what the results tell us about developed economies. There is nothing, in

principle, that makes the mechanism more relevant to emerging markets than for developed countries.

Understanding whether there are important differences to be considered is in itself an important area

for further research.

Lastly, on a methodological note, the paper illustrates the fruitfulness but also some of the pitfalls

of exploiting cross-sectional data to shed light on macroeconomic mechanisms. On the one hand,

cross-sectional data add a whole new dimension of facts that can be used to discipline macroeconomic

models. On the other hand, counter-factuals based on cross-sectional analysis tends to ignore general

equilibrium effects, so that complementing these with a model is important to have a full appreciation

of the effects in question. More generally, the increasing ability to solve large multi-sector models and

availability of good quality cross-sectional data should allow for even richer explorations along these

lines in the years to come.