Languages

Pages

Legal

The Affordable Care Act At 5

David Blumenthal, MD, MPP

President, The Commonwealth Fund

Health Journalism 2015

Silicon Valley, CA

April 25, 2015

2

What’s Happened So Far?

3

Insurance Market Reforms,

Consumer Protections

All new health plans

required to provide

free preventive care

• 71 million received at least one free

preventive care service

• 47 million estimated to be covered for

women’s preventive services with no

cost-sharing

Prohibition on

preexisting condition

exclusions for children

• 17.6 million children projected to

benefit

Bans on annual and

lifetime benefit limits

• 105 million estimated to have had

lifetime benefit limits

• 18 million had annual limits

Source: Centers for Medicare & Medicaid Services.

4

Insurance Market Reforms,

Refunds to Consumers

Limits on nonmedical

spending by health

plans

• Consumer rebates and reduced

overhead exceeded $5 billion in

between 2011 and 2013

Premium rate review• Consumer savings of $1 billion

in 2013

Source: McCue, Hall; Centers for Medicare & Medicaid Services.

5

Insurance Market Reforms, Young Adults

• 2.9 million more young

adults ages 19-25

covered by parent’s

policy between 2010-

2014.

Source: Centers for Medicare & Medicaid Services.

6

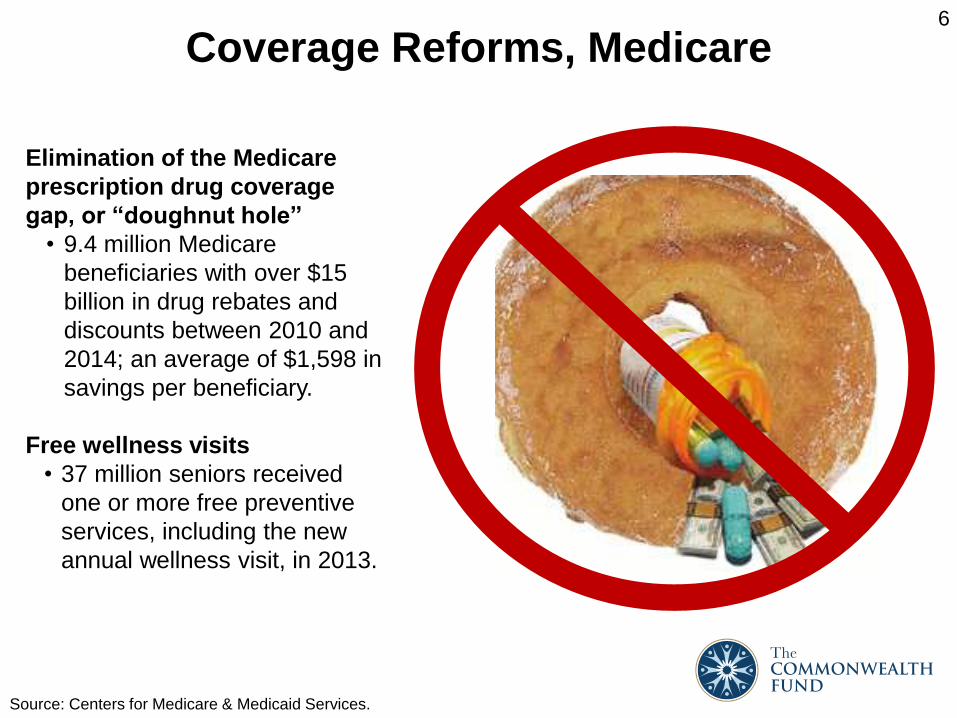

Coverage Reforms, Medicare

Elimination of the Medicare

prescription drug coverage

gap, or “doughnut hole”

• 9.4 million Medicare

beneficiaries with over $15

billion in drug rebates and

discounts between 2010 and

2014; an average of $1,598 in

savings per beneficiary.

Free wellness visits

• 37 million seniors received

one or more free preventive

services, including the new

annual wellness visit, in 2013.

Source: Centers for Medicare & Medicaid Services.

7

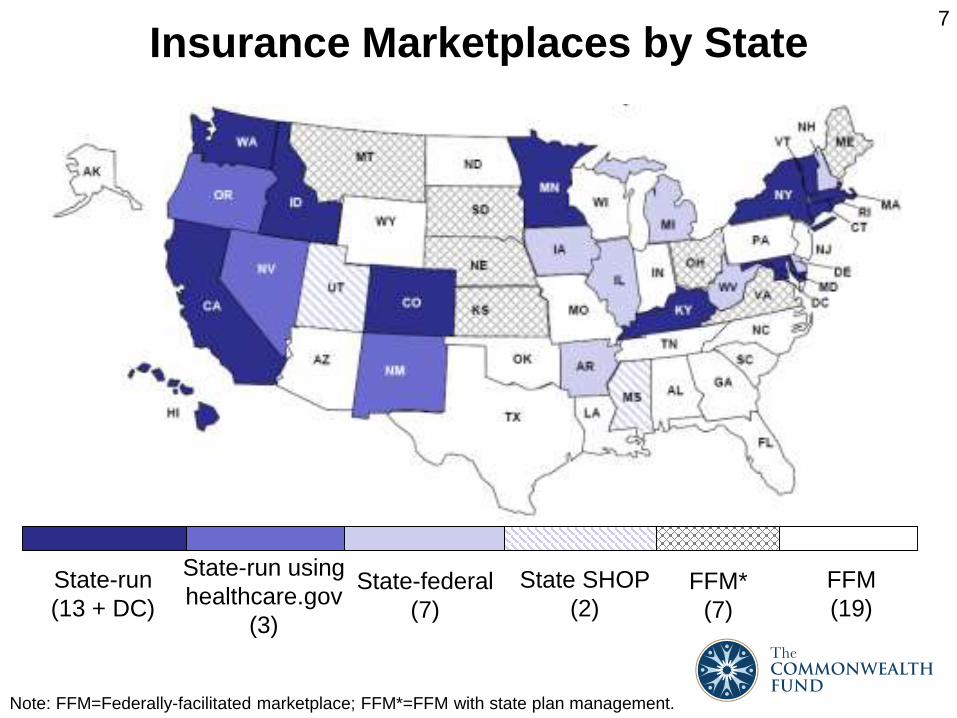

Insurance Marketplaces by State

State-run

(13 + DC)State-federal

(7)

State SHOP

(2)FFM*

(7)

FFM

(19)

Note: FFM=Federally-facilitated marketplace; FFM*=FFM with state plan management.

State-run using

healthcare.gov

(3)

8

Medicaid Expansion by State

Expanding

(22 + DC)

Customized

(6)

Under Discussion

(6)

Not Expanding

(16)

9Over 25 Million People Estimated to Have Insurance Under

the Provisions of the Affordable Care Act, as of March 2015

2.9

11.7 10.8

25.4

0

5

10

15

20

25

30

Change in the number of young adults ages 19-25 covered under a parent's policy*

Enrolled in a marketplace plan**

Enrolled in Medicaid/CHIP***

Total covered under provisions of the

ACA

Millions of people who have gained coverage or enrolled in a new plan under the Affordable Care Act

*Change in number of young adults ages 19-25 covered under a parent’s policy from 2010-2014.

**Number of Americans that have selected or been automatically reenrolled into a 2015 health

insurance plan through the Health Insurance Marketplace (11/15/14 – 2/15/15), including Special

Enrollment Period activity reported through Feb. 22,2015

***Increase in Medicaid and CHIP enrollment between October 2013 and December 2014.

Sources: CMWF Biennial Health Insurance Surveys (2010 and 2014) , HHS-ASPE, and CMS

10Multiple Sources Confirm Decline in Uninsured

Note: Most survey estimates are for adults ages 18-64. The Commonwealth Fund surveys’ estimates

are for adults ages 19-64.

Source: The Commonwealth Fund, Centers for Disease Control, RAND, Urban Institute.

Millions of non-elderly adults* who are uninsured

36

29

40.3

33.137

28

40.7

31.435.2

20.2

0

10

20

30

40

50

CM

WF

Bie

nn

ial

Su

rve

y, 2

01

2

CM

WF

Bie

nn

ial

Su

rve

y, 2

01

4

NH

IS,

20

12

NH

IS, J

an

-Ju

ne

2014

CM

WF

AC

A S

urv

ey,

J

uly

-Se

pt.

20

13

CM

WF

AC

A S

urv

ey,

Ap

ril-

Ju

ne

20

14

RA

ND

, S

ep

t. 2

01

3

RA

ND

, M

arc

h 2

014

Urb

an

HP

M S

urv

ey,

Q

3 2

01

3

Urb

an

, Q

1 2

01

5

11People with Incomes Under $48,000 for a Family of Four

Experienced the Largest Declines in Uninsured Rates

Note: FPL refers to federal poverty level. Income levels are for a family of four in 2013.

Source: The Commonwealth Fund Biennial Health Insurance Surveys (2001, 2003, 2005, 2010, 2012, and

2014).

Percent of adults ages 19–64

15

30

6

17

34

7

18

39

9

20

36

7

19

32

9

16

24

7

0

10

20

30

40

50

Total <200% FPL 200% FPL or more

2001 2003 2005 2010 2012 2014

<$47,100 $47,100+

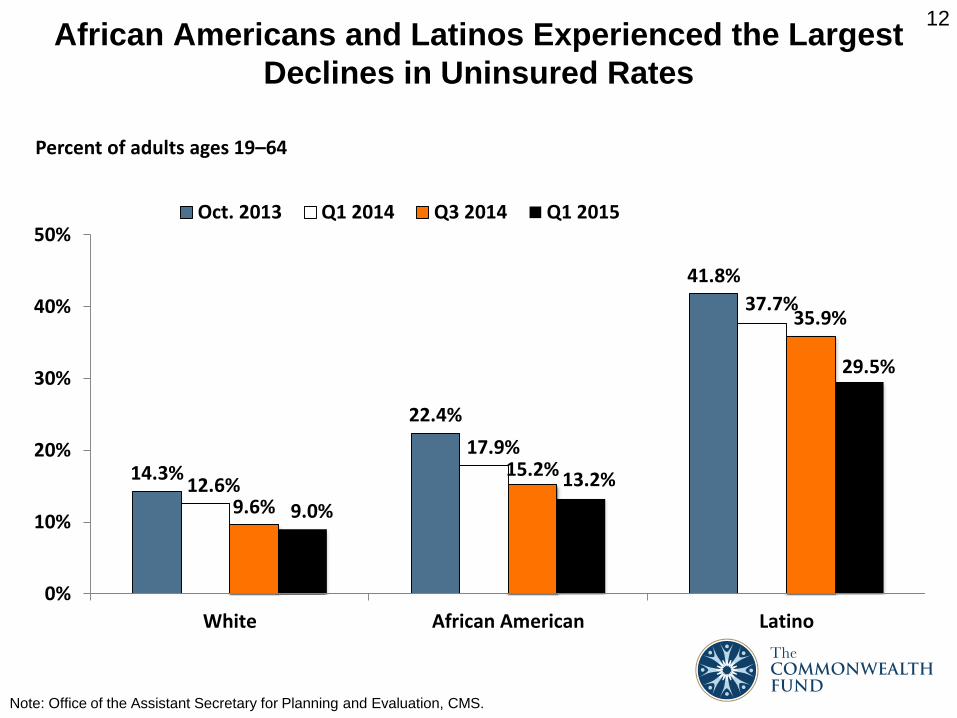

12African Americans and Latinos Experienced the Largest

Declines in Uninsured Rates

Note: Office of the Assistant Secretary for Planning and Evaluation, CMS.

Percent of adults ages 19–64

14.3%

22.4%

41.8%

12.6%

17.9%

37.7%

9.6%

15.2%

35.9%

9.0%

13.2%

29.5%

0%

10%

20%

30%

40%

50%

White African American Latino

Oct. 2013 Q1 2014 Q3 2014 Q1 2015

13

Source: The Commonwealth Fund Affordable Care Act Tracking Survey, April–June 2014.

Overall, how satisfied are you with this new health insurance?

Most Adults Newly Enrolled in Marketplace or

Medicaid Coverage are Satisfied with their Plan

Adults ages 19–64 who selected a private plan or enrolled in Medicaid through marketplace

or have had Medicaid for less than 1 year

43%

35%

6%

8%

8%Very satisfied

Not very satisfied

Somewhat satisfied

Not at all satisfied

Don’t know/refused

14

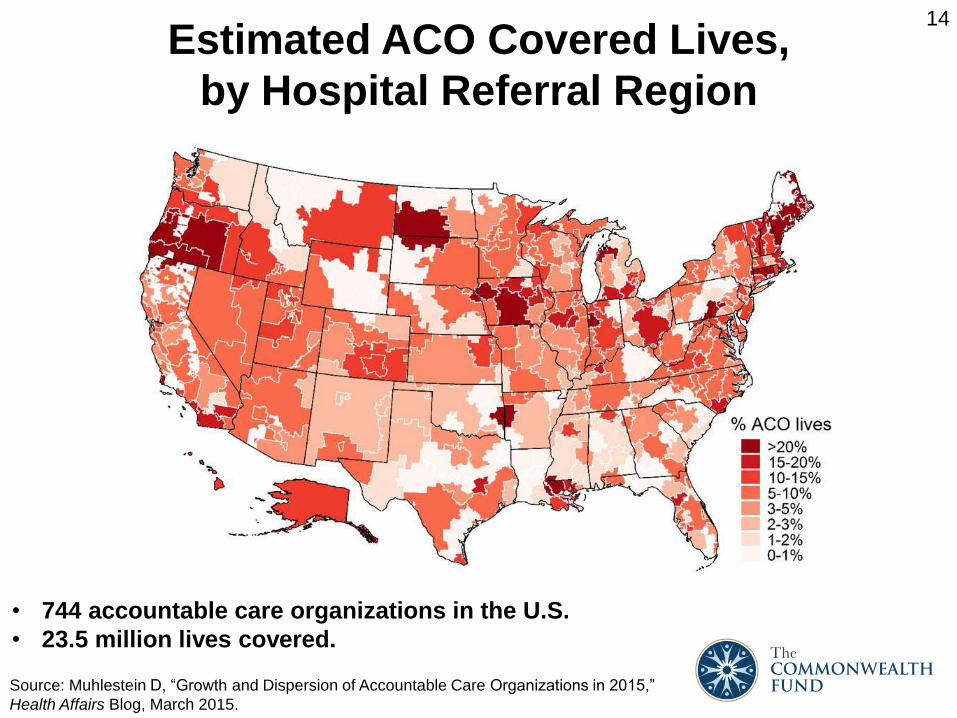

Estimated ACO Covered Lives,

by Hospital Referral Region

• 744 accountable care organizations in the U.S.

• 23.5 million lives covered.

Source: Muhlestein D, “Growth and Dispersion of Accountable Care Organizations in 2015,”

Health Affairs Blog, March 2015.

15

Medicare Hospital Readmissions Declining

Source: Furman J, “The Economic Benefits of the Affordable Care Act,” Presented at Center

for American Progress, April 2, 2015.

Percent, 12-month moving average

16

Decline in Hospital-Acquired Conditions Between

2010 and 2013 Prevents 50,000 Deaths

11,540

4,427

1,998

2,75020,272

1,297

1,150520 6,387

Adverse drug events

Catheter-associated UTIs

CLABIs

Falls

Pressure ulcers

Surgical site infections

Ventilator-associated pneumonia

Post-op venous thromboembolisms

Other

Number of prevented deaths by condition

Source: “Interim Update on 2013 Annual Hospital-Acquired Condition Rate and Estimates of

Cost Savings and Deaths Averted From 2010 to 2013,” December 2, 2014, CMS.

17

Spending Growth Rate Has Slowed in Recent Years

Source: Hartman M, Martin AB, Lassman D, Catlin A; the National Health Expenditure Accounts

Team. “National Health Spending In 2013: Growth Slows, Remains In Step With The Overall

Economy.” Health Affairs. 2014 Dec 3.

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

2001 2003 2005 2007 2009 2011 2013

PercentNHE per capita spending growth

18

Problems: Forced and Unforced

• Unanticipated policy cancellations for non-compliant plans.

• Major failures during rollout of healthcare.gov and some

state exchanges.

• Coverage gap in states not expanding Medicaid.

• The famous 4 words.

19

What’s Next?

20

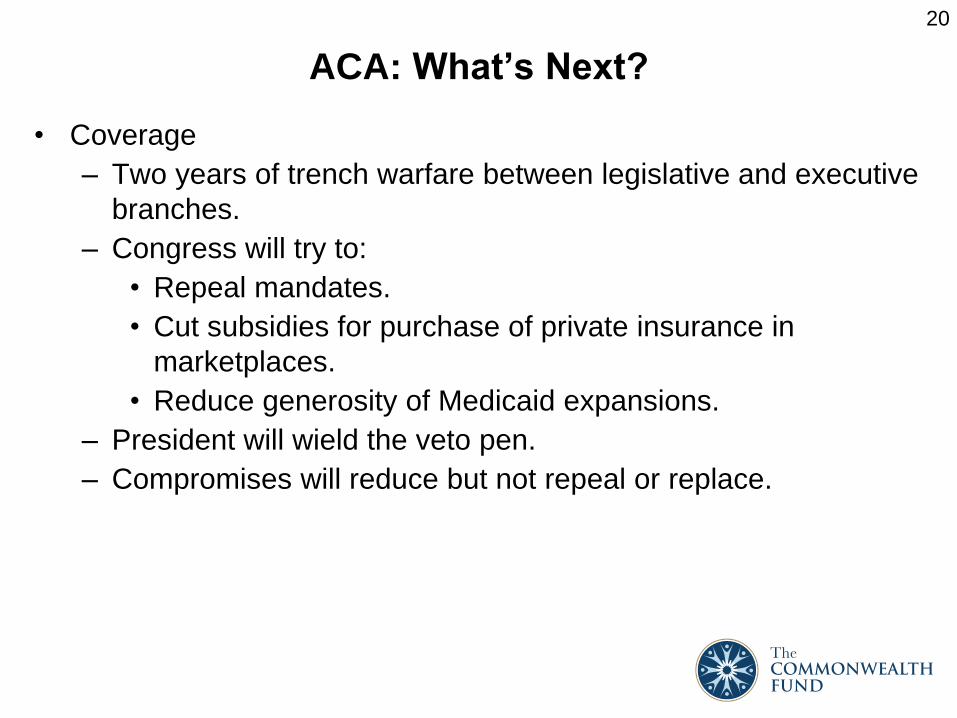

ACA: What’s Next?

• Coverage

– Two years of trench warfare between legislative and executive

branches.

– Congress will try to:

• Repeal mandates.

• Cut subsidies for purchase of private insurance in

marketplaces.

• Reduce generosity of Medicaid expansions.

– President will wield the veto pen.

– Compromises will reduce but not repeal or replace.

21

ACA: What’s Next?

• King v. Burwell

– Challenges the legality of subsidies granted to people

purchasing insurance in the 34 federally run marketplaces.

– Ruling for the plaintiffs would have significant consequences.

• 9.6 million fewer people insured through individual market.

• Premiums increase 47% in 2016.

– Decision expected June or July.

22

ACA: What’s Next?

• King v. Burwell: Possible responses to ruling for the plaintiffs.

– Congress:

• Pass a simple fix.

• Negotiate deal with the President.

• Do nothing.

– States.

• “Establish” an exchange.

– Lack of federal funding.

– Political barriers.

– Could take 12-18 months.

– Supreme Court.

• Grant a temporary stay.

23

ACA: What’s Next?

• Health Delivery System Reform

– General bipartisan support for many elements in the ACA.

– Continued implementation of:

• ACOs.

• Pay for value programs.

• SGR reforms.

• Rationalization of quality metrics.

– Attacks on spending for:

• CMMI.

• PCORI.

• Public health demonstration programs.

24

Question and Answer

Top Related