Languages

Pages

Legal

Tecpetrol International S.A. Annual Report and Consolidated Financial Statements for the nine-month period ended at December 31, 2011

2

AnnuAl RepoRt

BoARd MeMBeRs

Independents AudItoR’s RepoRt

ConsolIdAted FInAnCIAl stAteMents FoR the nIne-Month peRIod ended deCeMBeR 31, 2011Consolidated Income Statement Consolidated Statement of Comprehensive IncomeConsolidated Statement of Financial PositionConsolidated Statement of Changes in EquityConsolidated Statement of Cash FlowsNotes to the Consolidated Financial Statements

CoMpleMentARy InFoRMAtIon

4

19

22

24

282930323435

98

Contents

Annual Report and Consolidated Financial Statements / Tecpetrol International S.A. 3

Annual Report

4

5Annual Report and Consolidated Financial Statements / Tecpetrol International S.A.

6

Annual Report

the CoMpAnyTECPETROL INTERNATIONAL S.A. (“the Company”), domiciled in Uruguay, is an investment company for the energy business that belongs to the Techint Group, which owns shares in hydrocarbons production, transport and distribution compa-nies in Argentina, Bolivia, Ecuador, Mexico, Peru, Venezuela, Colombia and the United States of America. The Company is controlled by San Faustin S.A., through its subsidiaries.The Company, through its subsidiaries, develops, operates and invests in busi-nesses in the energy market, carrying out the exploration and production of oil and gas (E&P) and the transport and distribution of gas (G&P).In just over twenty years, it has consolidated its position as an inves-tor in the Latin American energy sector and positionated itself as an interna-tionally qualified operator, strengthen-ing its relationship with key interna-tional partners.

InteRnAtIonAl ConteXtDuring 2011, the world economic sce-nario continued to show evidence of two-speed growth. On the one hand, the developed economies found it hard to return to a path of expansion following the last international finan-cial crisis. On the other, although the emerging economies initially revealed themselves to be far more dynamic, they began to show signs of fatigue in the second half of the year and they are expected to achieve lower global demand levels during 2012. In particular, the United States is under great economy pressure and has re-corded the lowest recovery levels since the Second World War. Job creation has failed to impact significantly on

unemployment rates, and although the economy has managed to avoid falling again into a recession, the outlook is not encouraging. In Europe, the economic situation showed a marked deterioration over 2011. The economy of some countries has presented increasingly problems to repay its national debts despite sup-port from the European Union, the International Monetary Fund (“IMF”) and the European Central Bank. In Latin America, the general pattern is the slowdown of the economy and these countries prepares themselves to handle an international context which is distinctly less favorable in the wake of the increasing problems beset-ting developed nations. The IMF esti-mates over the world trade shows that this downturn will continue during 2012. During the first half of 2011, the dollar continued to fall against most of the other currencies, but managed to buck this trend in the second half of the year. As regards the demand for oil, during 2011 there was a general increase in demand from emerging economies less affected by the crisis, with China and the rest of Asia in the lead, coun-tered by a marked downturn in the developed economies of which the United States and the European Union were the hardest hit. The International Energy Agency (IEA) reported that the slight increase in oil demand during 2011 answered to a minor upturn in economic growth and high fuel prices. In line with the situation described above, the benchmark West Texas Intermediate (WTI) has showed a slight decline since the close of the previous financial period, reaching an average of value of 99 and 103 United States dollars (“US$ ”) per barrel as of December 31 and March 31, 2011, respectively.

Annual Report and Consolidated Financial Statements / Tecpetrol International S.A. 7

For 2012, the Organization of Petroleum Exporting Countries (OPEC) estimates that world oil demand will grow at a slower pace, given the fragility of the world economy and the greater decline in consumption rates in Europe. The IEA estimates that world demand for this commodity in 2012 will be less than predicted as the eco-nomic downturn and high prices will limit consumption.

eConoMIC Results And FInAnCIAl sItuAtIon These Consolidated Financial Statements corresponds to a nine-month period beginning on April 1,

The result for the period ended December 31, 2011 showed net profits of US$217.3 million, which represented

2011 and closing on December 31, 2011; as a consequence, the comparison of the information included in these Consolidated Financial Statements as of December 31, 2011, with the ac-counting information for the annual period ending on March 31, 2011 may be affected. The main ratios and finan-cial indicators of the Company are dis-closed below. The analysis is based on, and must be read in conjunction with, the audited Consolidated Financial Statements as of December 31, 2011, which were prepared according to the International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”).

a 21% over net sales, in comparison with a 16% in the previous year. The main financial indicators are as follows:

In US$ mIllIonS

Net salesGross profitOperating resultsResult for the periodCash flows provided by operating activitiesIncreases in Property, plant and equipment, net

At December 31, 2011 (9 months)

1,034.9

380.0

300.1

217.3

345.5

238.9

At march 31, 2011 (12 months)

820.1

286.6

178.1

129.4

257.3

216.1

8

huMAn ResouRCesThe Company has since the beginning maintained that one of its priorities for consolidating growth is training human resources to ensure they are qualified and committed, with a broad range of experience across the differ-ent businesses it operates. The sig-nificant investment made in training which sets the Company and its sub-sidiaries apart is a clear sign of com-mitment in this area. At December 31, 2011, the Company employs a work force of 994 people located at its different subsidiaries, of which 71 corresponds to board and management staff. Employees have participated in train-ing activities throughout the current period, both in prestigious universities and as part of in-company activities, giving them the opportunity to take specific technical courses and to attend events held in different countries.

CoMMunIty RelAtIons, enVIRonMent And sAFety

social developmentThrough its operating subsidiaries, the Company works closely with the communities neighboring its opera-tions, contributing to the develop-ment of each community and its insti-tutions. With this purpose, it carries

out and supports social development programs in low-income rural and ur-ban areas, communities and schools in the vicinity of its fields, committing its personnel and the local population to the development of its social programs. The Community Action Plan mainly includes a number of nutrition, education, health, sustain-able development, culture and work training programs.

environmental safety and protectionThe Company and its subsidiaries pursue the priority objective of man-aging their operations to ensure that the physical integrity of the personnel involved as well as third parties is adequately protected, in addition to safeguarding the environment. Health, Safety and Environmental protection (“HSE”) concepts have been integrated within this objective as core management values.

environmentThe Company’s operating subsidiar-ies are currently running a number of different programs to safeguard the environment, such as environmental impact studies, monitoring and contin-gency plans, which analyze the poten-tial impact a new project may have in order to plan the avoidance or minimi-zation of damage to the environment.

LiquiditySolvencyNon-current assets over total assetsNet profit margin

At December 31, 2011

1.64

1.74

0.69

20%

At march 31, 2011

1.62

1.47

0.69

14%

Annual Report and Consolidated Financial Statements / Tecpetrol International S.A. 9

Other environmental programs are also being carried out, such as the appropri-ate disposal of production waters, rein-jecting 100% of these effluents in order to eliminate the risks of contaminat-ing ground and subterranean waters; the acquisition of low-impact seismic equipment; the prevention of oil spills and leaks; erosion control and others.Another key objective is the develop-ment and implementation of new sys-tems and technologies aimed at pre-venting and reducing the impact on the environment. The Argentine subsidiary Tecpetrol S.A. was the first oil company in its country to set up a new technolo-gy for treating oil-contaminated mud in the area of El Tordillo, solving a historic problem that all operating companies working in Argentine Patagonia have had due to climatic conditions. Efforts to protect the environment have been complemented by activities centered on revegetation and refor-estation with native species in the operations carried in Argentina, Peru, Ecuador and Colombia. Furthermore, the management of solid and liquid waste was improved, par-ticularly in the areas of El Tordillo, Los Bastos and Agua Salada in Argentina. Additionally, also in Argentina, the bio-remediation of the soil in El Tordillo and Agua Salada was launched, while works to control erosion continued in Argentina, Peru and Ecuador.In May 2011, Bureau Veritas, the inde-pendent certification organism, held an external audit of the environmen-tal management system at Bermejo (Ecuador), maintaining the ISO 14001 certification, on the basis of which the environmental license was awarded to build the rail, set up the rig and drill the Bermejo Este X-1 well. In Colombia, the processes to obtain the environmental licenses for the

exploratory drilling projects planned in the different blocks (CPO-6, CPO-7A, CPO-7B and CPO-13) were launched, and the licenses for the first three were obtained.In November 2011, the Peruvian Mining, Oil and Energy Society (Sociedad Nacional de Minería Petróleo y Energía de Perú - SNMPE) awarded the prizes for “Sustainable Development 2011” in recognition of the best practices developed in social and environmental fields by companies from the mining and energy sectors. The associate company Transportadora de gas del Peru S.A. (“TgP”) was awarded a prize for its project “Clean from start to finish: compost in the TgP pipeline transport system”. The project is about the treatment of solid organic waste generated during coastline, mountain and rainforest operations in order to create significant environ-mental, economic and social benefits. This process means that 100% of the waste can be reused to produce com-post for the benefit of the communi-ties, as it can be employed to improve soil for revegetation, gardening and crop-growing.

safetyThe key elements for the implementa-tion of a safety policy are leadership and commitment, integrated safety, audits, prevention programs, accident and incident investigation, risk ad-ministration, improvement plans and safety initiatives as well as the ability to manage change.Results obtained are monitored by comparing the safety ratios against the objectives set. The main focus was on managing the effective application of the key elements through a program called HSE Control Panel (STOP, audits, incident reports).

10

The afore-mentioned Bureau Veritas report underlined the continuing effec-tiveness of actions taken in the areas of health, safety and the environment, and allowed Tecpecuador to maintain the ISO 14001 certification initially obtained in April 2005 for a further three-year period.

hydRoCARBons ReseRVes (e&p)Reserves mean the volumes of oil and gas (in oil-equivalent cubic me-ters) which generate or are associated with revenue in the areas where each company operates or has a direct or indirect share, and which the Company has the right to exploit. This includes hydrocarbons volumes related to the service contracts in which the compa-nies do not have ownership either of the reserves or of the hydrocarbons extracted and the volumes expected to be produced for the contracting party under the works contracts. Reserve calculation is a subjective process which attempts to estimate the underground accumulation of crude oil and natural gas which in-volves a certain degree of uncertainty. Proved reserves of hydrocarbons (developed and undeveloped) estimated as of December 31, 2011, are as follows:

Oil millions of cubic meters 13

Gas billions of cubic meters 34

The aforementioned reserves include proved reserves which may be ex-tracted and from which royalties have not been deducted. They have been prepared by the Company’s technical

personnel based on the technological and economic conditions prevailing on June 30, 2011, taking into account the economic evaluation within the terms of the respective contracts or concession.

Annual Report and Consolidated Financial Statements / Tecpetrol International S.A. 11

tRAnspoRt GAs CApACIty (G&p)The transport capacity of the subsid-iary companies is given below:

outlooK And pRoJeCtsThe Company continues to analyze new business options in those coun-tries where currently operates, as well as other countries, that allows it to ful-fill its growth and consolidation strate-gy. The goal continues to be growth for both the E&P and the G&P businesses.

ArgentinaIn the area of El Tordillo, Tecpetrol will continue with the drilling activities, including primary and secondary work-overs, working with several workover rigs. It will continue with the tertiary recovery project using polymer injec-tions. At the production facilities, the main investments concern the drive to fight corrosion which includes the re-coating of pipelines, and the purchase and upgrade of pumping equipment and environmental tasks.

GAS (in Mm3/day)

Transportadora de Gas del Norte S.A. (Argentina)

Litoral Gas S.A. (Argentina)

Transportadora de gas del Perú S.A. (Peru)

Transportadora de Gas del Mercosur S.A. (Argentina)

Utilization percentage

97.4%

95.6%

83.0%

-

Daily transport

53,005

7,587

12,509

-

Total daily transport capacity

54,400

7,936

15,007

2,800

In the Neuquina basin, Tecpetrol will continue with the drilling activities, in-cluding the exploratory wells foreseen in the Gas Plus program. Furthermore, the construction of infrastructure works in Los Bastos and Agua Salada is planned, including pipelines and storage tanks in order to expand hy-drocarbons transport and processing capacities.In Río Atuel, the exploratory work cur-rently under way will continue, includ-ing the drilling of wells according to the commitments undertaken with the province of Mendoza. Negotiations are expected to continue with the provinces with a view to ex-tending the areas of El Tordillo and Aguaragüe. Regarding the commercialization of hy-drocarbons in Argentina, it is estimated that sales will continue to be made as in previous years.

14

peruFollowing the award in November 2010 of Bloque 174, in the Ucayali Basin, the field exploration and exploitation contract was signed on September 23, 2011. This stipulates that if the sub-sidiary Tecpetrol Lote 174 SAC finds commercial reserves, it has the right of ownership over the hydrocarbons ex-tracted while Perupetro S.A. will ensure the contractual obligations are met. Bloque 174 covers a surface area of some 264,000 hectares and has a very encouraging outlook as regards the discovery of hydrocarbons. Tecpetrol Lote 174 SAC has been granted a 7-year period for the exploration phase, 30 years for exploitation if oil is found, and 40 years if the find is of natural gas and associated liquids. The commitment undertaken for the first few years includes the reprocessing of existing seismic information on the field and the registration of 150 km of 2D seismic surveys, or exploratory tasks for a given number of explora-tion work units. Although the contract presents a num-ber of logistical, community-related, environmental and geological chal-lenges in the middle of the Peruvian Amazonian jungle, it also offers a wealth of opportunities to continue ex-panding the Company’s presence and experience in this country. The Camisea operations are also expected to continue in Bloque 88 (San Martín and Cashiriari), and in Bloque 56 (Pagoreni and Mipaya), which have been supplying 100% of the requirements of Perú LNG S.R.L. (PLNG), reaching 620 MMcf/d (million cubic feet per day) since June 2010, when the company began commercial operations. Furthermore, on April 18, 2011, an ad-dendum to the natural gas transport

concession contract was signed by the Ministerio de Energía y Minas de Perú (Peruvian Ministry of Energy and Mining) and the associated company TgP, regulating TgP’s commitment to a phased expansion of the gas carriage system with a target of 920 MMcf/d, taking into account the new objectives set by the expansion project. Towards the end of July 2011, the en-vironmental impact study presented by TgP was approved, a requirement enabling it to progress with the expan-sion of the natural gas (NG) and lique-fied natural gas (LNG) carriage system in the “Selva-Loop Sur” section. This expansion involves the installation of two new 55 km-long gas and liq-uids pipelines to be connected to the current pipeline network in order to increase its NG transport capacity to 1,540 MMcf/d and its LNG transport ca-pacity to 120,000 bpd. In addition, the Loop-Sur project includes the construc-tion of a LNG pumping station as well as the auxiliary systems and equip-ment required for this kind of facility. This expansion, for which an invest-ment of some US$600 million has been earmarked, will allow new gas demands to be met, in particular with regard to the needs for the greater generation of energy in power stations.

MexicoDuring 2011, the investments planned were made in a drilling rig for the Bloque Misión contract. The strategy envisaged seeks to establish a balance between the development of existing fields and the search for new reserves in the form of exploratory projects, which strengthen the possibility for future developments in the block. Additionally, the drilling campaign with one rig, and the building of facili-ties are expected to continue in the

Annual Report and Consolidated Financial Statements / Tecpetrol International S.A. 15

fields of Santa Anita, Cali and Trapiche throughout 2012, as well as the con-struction of new installations on the basis of the results achieved by the exploratory wells. As regards production, increases in excess of 250% of gas and of 900% of liquids have been achieved since the outset of the contract. At business level, from 2004 to 2011, over US$580 million have been invested, which rep-resents approximately 400% over the minimum amounts committed for the first eight years. Under the aegis of the contract of the technological development laboratory in the Coyotes field (Mexico), signed between the subsidiary Burgos Oil Services S.A. de C.V. (“BOS”) and PEMEX Exploración y Producción (“PEP”), BOS finalized and presented PEP with the first stage of the geo-sciences and production studies as well as the exploitation plan which will serve as a basis for the future development of the Coyotes field. Furthermore, several well workovers were carried out and the idea is to continue with these for the remainder of 2012. At the end of the contractual period in December 2012, the labora-tory contract is expected to be updated to envisage a longer period. Additionally, during 2011, the first mul-tifractured horizontal well was success-fully drilled and completed, a major achievement from both the technical and operational points of view, as this is the first such project in the Coyotes field. The engineering objective here was to access a greater part of the reservoir, reaching more than one formation and improving the invest-ment-production ratio. The technique introduced by BOS for this horizontal multifractured drilling project is widely used in the U.S. to develop shale gas

wells and extract gas from clay soils. In this case, a similar system was used to produce oil. Currently the option of continuing with a series of other hori-zontal well drilling projects is being analyzed. One of the key objectives, which involves the generation of value for PEP, can be reached by introducing better operating practices. The success-ful drilling and completion of these wells will demonstrate the consolida-tion of this process.

united statesFollowing the acquisition of Tecpetrol Corporation in March 2010, work continued during 2011 to consolidate operations in the United States. In this context, Tecpetrol Corporation has continued with the process to op-timize operations and new stakes have been acquired in some of the fields in the Ann Mag area, as well as explo-ration and eventual exploitation rights in other fields.

ColombiaThe Ministerio de Ambiente, Vivienda y Desarrollo Territorial (Environment, Housing and Development Ministry) awarded Tecpetrol Colombia S.A.S. the environmental licenses for the exploratory blocks CPO-6, CPO-7A and 7B, authorizing drilling to commence in these locations. Exploratory drilling has started in areas of over 164 and 180 thousand hectares (CPO-6 and CPO-7A, respectively) to be extended during 2012, in order to meet the contractual commitments made for Phase 1. Approval is still awaited for the license pending which corresponds to Bloque CPO-13 and which will complete the drilling campaign. Furthermore, at Bloque CPO-13, an agreement was reached to begin seismic surveys with-in the Resguardo El Tigre field, which

16

began in December 2011. This means that an additional 200 km will be added to the over 2,000 km of seismic sur-veys recorded in 2010 in an area of great exploratory interest.

ecuadorIn February 2011, the amendment con-tract between the State of Ecuador, represented by the Secretaría de Hidrocarburos (Hydrocarbons Secretariat), and the subsidiary compa-ny Tecpecuador S.A. was signed, thus adopting a model for the provision of integrated services for the explora-tion and exploitation of hydrocarbons, according to the first temporary dispo-sition given in the Law amending the Law of Hydrocarbons and the Internal Tax Regime Law. The contract is appli-cable until July 30, 2019.This renegotiation also stipulates the pre-cretaceous basin exploration. This is a high-risk objective, as there are no records of the existence of oil systems at these levels. On January 31, 2012 two contracts were signed with the Ecuadorian state oil company EP PETROECUADOR to provide specific services including financing from Tecpetrol in order to carry out activities aimed at optimizing production and improving recovery and exploration, as well as providing advice for the optimization of variable operating costs. These contracts cover the fields Libertador-Atacapi and Shushufindi-Aguarico, where Tecpetrol will be the operator in the former. The agreements have a duration of 15 years, and include investments planned in the region of US$1,300 million for Sushsufindi and US$385 million for Libertador. As a result of these awards and the current Bermejo contract, Tecpetrol will be involved through the provision of

its services in some 15% of the total output of hydrocarbons in Ecuador.

BoliviaDuring 2011, gas reserves were found in the Huamapampa formation in the Bloque Aquío where the subsidiary Tecpetrol de Bolivia S.A. holds a 20% stake. There is still major exploratory potential in deeper reservoirs (Icla and Santa Rosa formations) which remains to be researched by the subsidiary and its partners. As from 2015 the flow is expected to reach 6.5 MMm3 per day.

The Board thanks the Company´s personnel for their dedication and achievements during this period.

Annual Report and Consolidated Financial Statements / Tecpetrol International S.A. 17

18

Board Members

pResIdentCarlos Arturo Ormachea

VICepResIdentEnrico Fabián Repetto Mariño

dIReCtoRJorge Emilio Perazzo Puppo

dIReCtoRCarlos Manuel Franck

dIReCtoRCatalina Alicia Ilicic Sincovich

Annual Report and Consolidated Financial Statements / Tecpetrol International S.A. 19

Independent Auditor’s Report

To the Shareholders, Board of Directors and Managementof Tecpetrol International S.A.

We have audited the accompanying consolidated financial statements of Tecpetrol International S.A. which comprise the consolidated statement of financial position as of December 31, 2011, and the related consolidated statements of income, comprehensive in-come, changes in equity and cash flows for the period then ended, and a summary of signifi-cant accounting policies and other explanatory notes.

Management’s Responsibility for the Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with International Financial Reporting Standards and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with the International Standards on Auditing. These Standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control to be relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

OpinionIn our opinion, the accompanying consolidated financial statements present fairly, in all material aspects, the consolidated financial position of Tecpetrol International S.A. as of December 31, 2011, and of their fi-nancial performance and cash flows for the period then ended in accordance with International Financial Reporting Standards.

Montevideo, Uruguay, March 23, 2012

Consolidated Financial Statements for the nine-month period ended at December 31, 2011

24

25Annual Report and Consolidated Financial Statements / Tecpetrol International S.A.

Contents

Consolidated Income statementConsolidated statement of Comprehensive IncomeConsolidated statement of Financial positionConsolidated statement of Changes in equityConsolidated statement of Cash Flows

notes to the Consolidated Financial statements 1. General information2. summary of significant accounting policies2.1 Basis of preparation2.2 Consolidation2.3 Foreign currency translation 2.4 Property, plant and equipment. Exploration, evaluation and development assets2.5 Intangible assets2.6 Inventories2.7 Trade and other receivables2.8 Cash and cash equivalents2.9 Equity2.10 Borrowings2.11 Income tax2.12 Employee benefits2.13 Employee’s statutory profit sharing2.14 Provisions2.15 Trade and other payables2.16 Revenue recognition2.17 Cost of sales2.18 Financial Instruments2.19 Derivative financial instruments and hedging activities3. new accounting standards4. Financial risk management4.1 Financial risk factors4.2 Financial instruments by category4.3 Fair value estimation5. Critical accounting estimates and judgments6. operating costs 7. selling expenses 8. Administrative expenses9. labor costs10. other operating items11. Financial results 12. Income tax 13. property, plant and equipment. exploration, evaluation and development assets

26

14. Intangible assets15. Investments in associated companies16. Impairment of long-term assets. property, plant and equipment 17. Available-for-sale financial assets18. Inventories19. other receivables and prepayments20. trade receivables21. Cash and cash equivalents22. dividends per share23. Borrowings24. employee benefits25. provisions26. trade and other payables27. deferred income tax28. derivative financial instruments29. Contingencies30. situation of associated companies transportadora de Gas del norte s.A. and transportadora de Gas del Mercosur s.A.31. principal guarantees, commitments and restrictions32. Related party balances and transactions33. principal subsidiaries and jointly-controlled entities34. dividends35. subsequent events

27Annual Report and Consolidated Financial Statements / Tecpetrol International S.A.

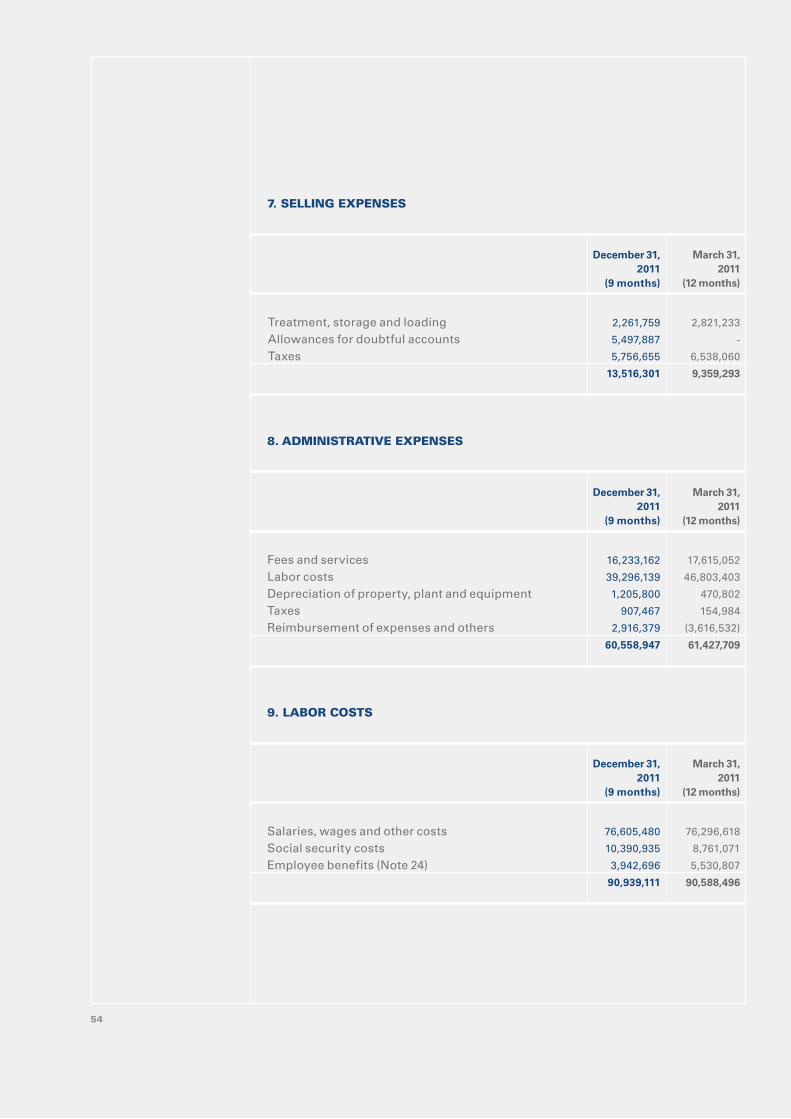

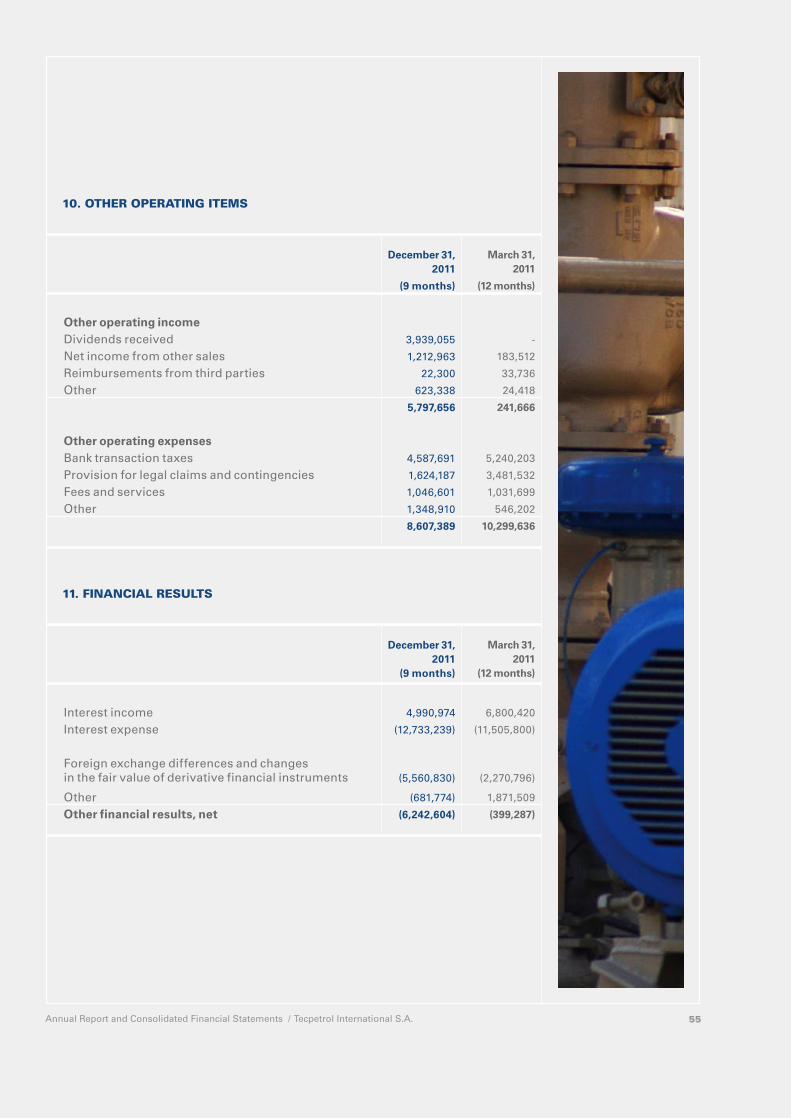

Continuing operationsNet sales Operating costsGross profit

Selling expensesAdministrative expensesExploration costsOther operating incomeOther operating expensesoperating results

Interest incomeInterest expenseOther financial results, netIncome before equity in earnings of associated companies and income tax

Equity in earnings of associated companiesIncome before income tax

Income taxResult for the period

Attributable to:Equity holders of the CompanyNon-controlling interests

December 31,

2011

(9 months) (*)

1,034,912,579

(654,891,736)

380,020,843

(13,516,301)

(60,558,947)

(3,023,917)

5,797,656

(8,607,389)

300,111,945

4,990,974

(12,733,239)

(6,242,604)

286,127,076

20,608,276

306,735,352

(89,449,740)

217,285,612

217,525,673

(240,061)

notes

6

7

8

10

10

11

11

11

15

12

march 31,

2011

(12 months) (*)

820,132,384

(533,511,615)

286,620,769

(9,359,293)

(61,427,709)

(27,615,743)

241,666

(10,299,636)

178,160,054

6,800,420

(11,505,800)

(399,287)

173,055,387

20,322,013

193,377,400

(63,942,285)

129,435,115

129,877,528

(442,413)

(Amounts in United States dollars, unless otherwise stated)

(*) See Note 1.

The accompanying notes 1 to 35 are an integral part of these Consolidated Financial Statements.

Consolidated Income Statement

28

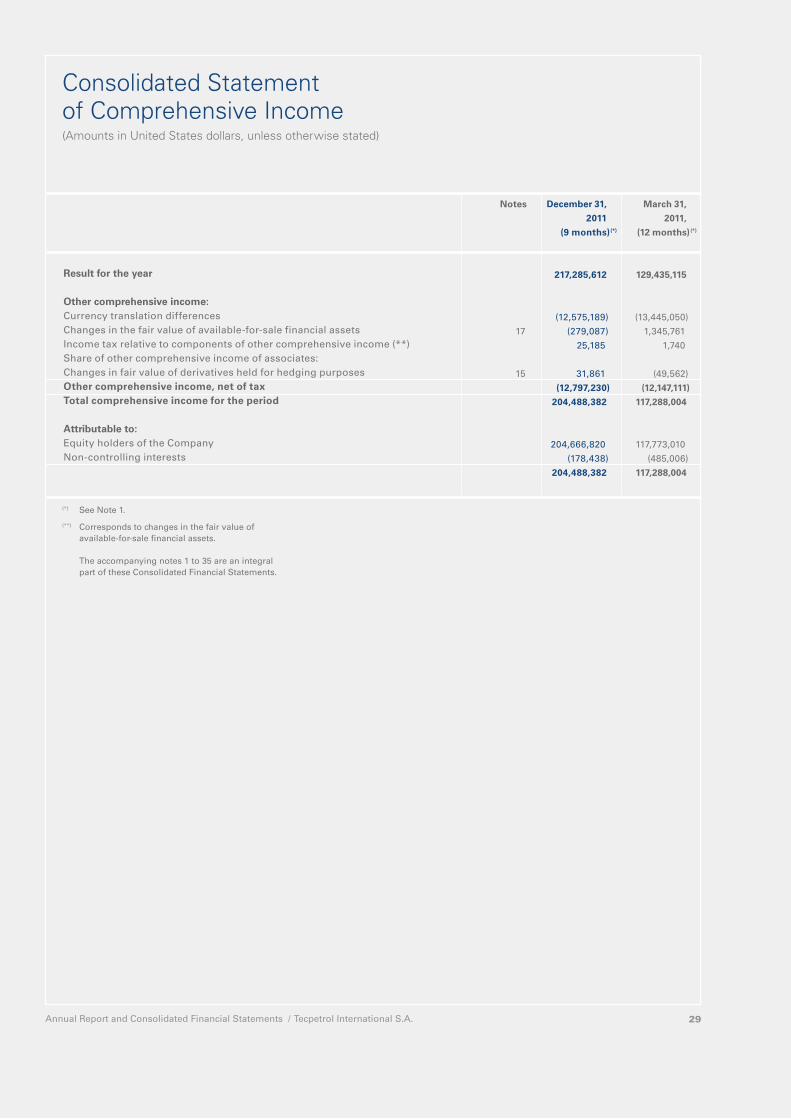

Result for the year

other comprehensive income:Currency translation differencesChanges in the fair value of available-for-sale financial assets Income tax relative to components of other comprehensive income (**)Share of other comprehensive income of associates:Changes in fair value of derivatives held for hedging purposesother comprehensive income, net of taxTotal comprehensive income for the period

Attributable to:Equity holders of the CompanyNon-controlling interests

December 31,

2011

(9 months) (*)

217,285,612

(12,575,189)

(279,087)

25,185

31,861

(12,797,230)

204,488,382

204,666,820

(178,438)

204,488,382

notes

17

15

march 31,

2011,

(12 months) (*)

129,435,115

(13,445,050)

1,345,761

1,740

(49,562)

(12,147,111)

117,288,004

117,773,010

(485,006)

117,288,004

(Amounts in United States dollars, unless otherwise stated)

(*) See Note 1.

(**) Corresponds to changes in the fair value of available-for-sale financial assets.

The accompanying notes 1 to 35 are an integral part of these Consolidated Financial Statements.

Consolidated Statement of Comprehensive Income

29Annual Report and Consolidated Financial Statements / Tecpetrol International S.A.

ASSETSnon-current assets

Property, plant and equipment. Exploration, evaluation and development assetsIntangible assetsInvestments in associated companiesAvailable-for-sale financial assetsDeferred tax assetsOther financial assets at fair value through profit or lossOther receivables and prepaymentsTrade receivables

Total non-current assets

Current assetsInventoriesOther receivables and prepaymentsIncome tax creditTrade receivablesDerivative financial instrumentsCash and cash equivalents

Total current assetsTotal assets

lIABIlITIES AnD EQUITYEquity

Share capitalLegal reserveOther reservesRetained earningsEquity attributable to the Company´s equity holdersNon-controlling interests

Total equity

non-current liabilitiesBorrowingsDeferred tax liabilitiesEmployee benefitsProvisionsTrade and other payables

Total non-current liabilities

Current liabilitiesBorrowings ProvisionsIncome tax liabilitiesTrade and other payables

Total current liabilities Total liabilities Total equity and liabilities

December 31,

2011

905,519,548

12,352,643

145,388,238

62,300,024

17,585,558

10,647,297

51,247,946

44,977,469

1,250,018,723

42,476,126

49,221,496

5,246,818

137,756,007

228,763

324,430,642

559,359,852

1,809,378,575

371,940,304

34,886,194

(77,118,077)

820,050,662

1,149,759,083

(483,738)

1,149,275,345

163,167,269

73,406,755

17,343,745

53,762,551

12,312,394

319,992,714

106,228,536

11,699,288

34,512,860

187,669,832

340,110,516

660,103,230

1,809,378,575

notes

13

14

15

17

27

19

20

18

19

20

28

21

23

27

24

25

26

23

25

26

march 31,

2011

809,610,557

12,352,643

128,022,788

62,748,755

12,982,291

10,082,007

42,021,925

43,914,773

1,121,735,739

22,436,781

55,150,041

712,594

144,462,917

-

292,705,527

515,467,860

1,637,203,599

371,940,304

28,392,317

(64,259,224)

639,018,866

975,092,263

(305,300)

974,786,963

212,416,426

71,081,256

14,991,900

44,983,952

11,176,343

354,649,877

111,026,678

11,070,478

28,021,820

157,647,783

307,766,759

662,416,636

1,637,203,599

(Amounts in United States dollars, unless otherwise stated)

The accompanying notes 1 to 35 are an integral part of these Consolidated Financial Statements.

Consolidated Statement of Financial Position

30

31Annual Report and Consolidated Financial Statements / Tecpetrol International S.A.

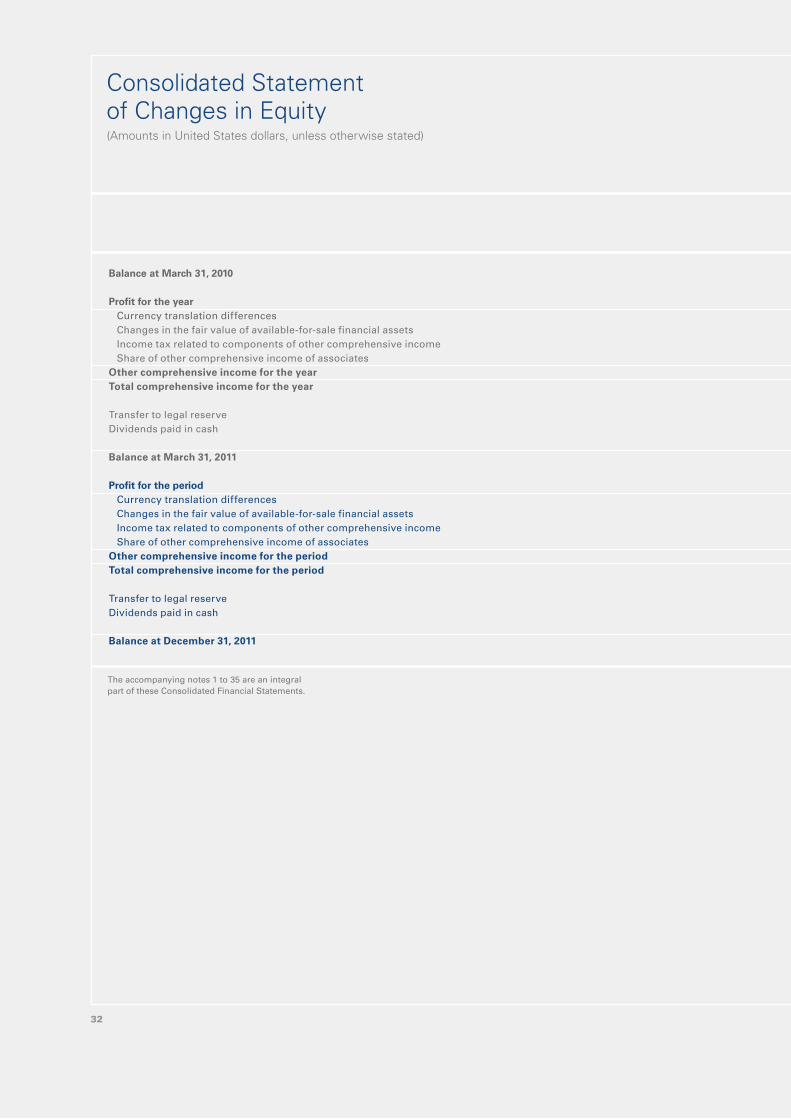

Balance at march 31, 2010

Profit for the yearCurrency translation differences Changes in the fair value of available-for-sale financial assets Income tax related to components of other comprehensive income Share of other comprehensive income of associates

other comprehensive income for the yearTotal comprehensive income for the year

Transfer to legal reserveDividends paid in cash

Balance at march 31, 2011

Profit for the periodCurrency translation differences Changes in the fair value of available-for-sale financial assets Income tax related to components of other comprehensive income Share of other comprehensive income of associates

other comprehensive income for the periodTotal comprehensive income for the period

Transfer to legal reserveDividends paid in cash

Balance at December 31, 2011

(Amounts in United States dollars, unless otherwise stated)

The accompanying notes 1 to 35 are an integral part of these Consolidated Financial Statements.

Consolidated Statement of Changes in Equity

32

Balance at march 31, 2010

Profit for the yearCurrency translation differences Changes in the fair value of available-for-sale financial assets Income tax related to components of other comprehensive income Share of other comprehensive income of associates

other comprehensive income for the yearTotal comprehensive income for the year

Transfer to legal reserveDividends paid in cash

Balance at march 31, 2011

Profit for the periodCurrency translation differences Changes in the fair value of available-for-sale financial assets Income tax related to components of other comprehensive income Share of other comprehensive income of associates

other comprehensive income for the periodTotal comprehensive income for the period

Transfer to legal reserveDividends paid in cash

Balance at December 31, 2011

Total

887,498,959

129,435,115

(13,445,050)

1,345,761

1,740

(49,562)

(12,147,111)

117,288,004

-

(30,000,000)

974,786,963

217,285,612

(12,575,189)

(279,087)

25,185

31,861

(12,797,230)

204,488,382

-

(30,000,000)

1,149,275,345

non-

controlling

interests

179,706

(442,413)

(42,593)

-

-

-

(42,593)

(485,006)

-

-

(305,300)

(240,061)

61,623

-

-

-

61,623

(178,438)

-

-

(483,738)

Total

887,319,253

129,877,528

(13,402,457)

1,345,761

1,740

(49,562)

(12,104,518)

117,773,010

-

(30,000,000)

975,092,263

217,525,673

(12,636,812)

(279,087)

25,185

31,861

(12,858,853)

204,666,820

-

(30,000,000)

1,149,759,083

Retained

earnings

547,131,493

129,877,528

-

-

-

-

-

129,877,528

(7,990,155)

(30,000,000)

639,018,866

217,525,673

-

-

-

-

-

217,525,673

(6,493,877)

(30,000,000)

820,050,662

other

reserves

(52,154,706)

-

(13,402,457)

1,345,761

1,740

(49,562)

(12,104,518)

(12,104,518)

-

-

(64,259,224)

-

(12,636,812)

(279,087)

25,185

31,861

(12,858,853)

(12,858,853)

-

-

(77,118,077)

legal

reserves

20,402,162

-

-

-

-

-

-

-

7,990,155

-

28,392,317

-

-

-

-

-

-

-

6,493,877

-

34,886,194

Share

capital

371,940,304

-

-

-

-

-

-

-

-

-

371,940,304

-

-

-

-

-

-

-

-

-

371,940,304

notes

22

22

Attributable to the Company´s equity holders

33Annual Report and Consolidated Financial Statements / Tecpetrol International S.A.

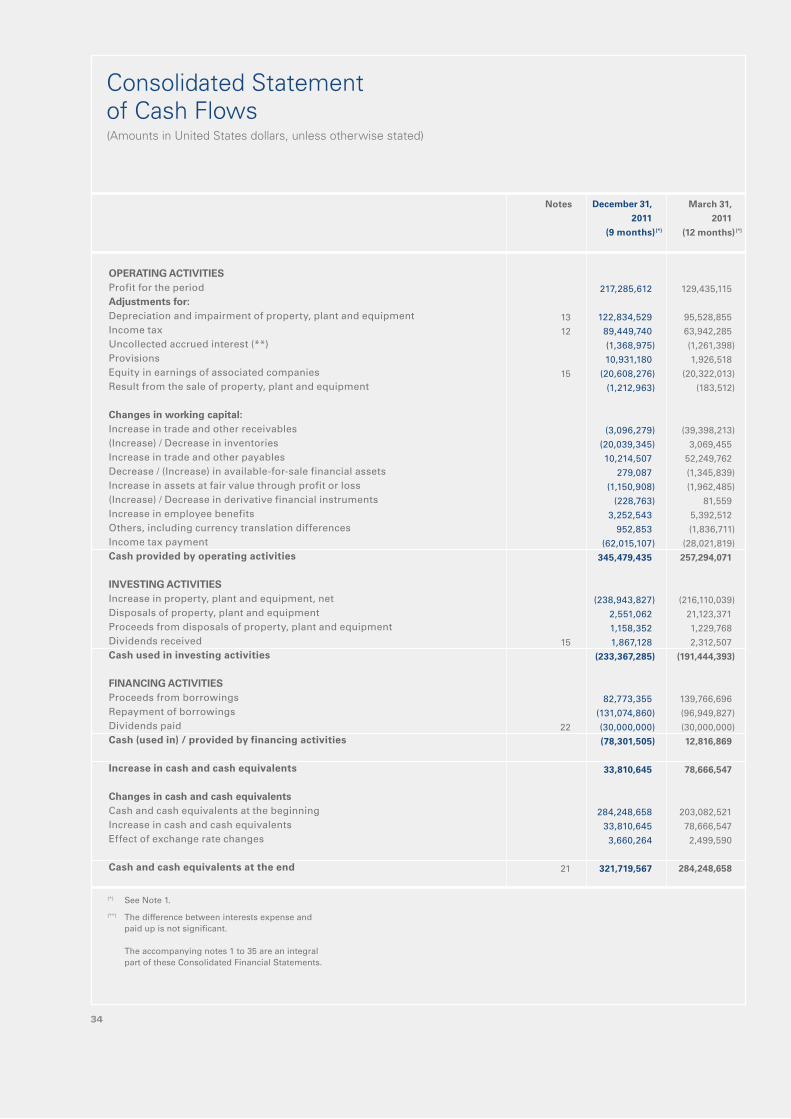

oPERATInG ACTIVITIESProfit for the periodAdjustments for: Depreciation and impairment of property, plant and equipmentIncome tax Uncollected accrued interest (**)ProvisionsEquity in earnings of associated companiesResult from the sale of property, plant and equipment

Changes in working capital:Increase in trade and other receivables(Increase) / Decrease in inventoriesIncrease in trade and other payablesDecrease / (Increase) in available-for-sale financial assetsIncrease in assets at fair value through profit or loss (Increase) / Decrease in derivative financial instruments Increase in employee benefits Others, including currency translation differencesIncome tax paymentCash provided by operating activities

InVESTInG ACTIVITIESIncrease in property, plant and equipment, netDisposals of property, plant and equipmentProceeds from disposals of property, plant and equipmentDividends receivedCash used in investing activities

FInAnCInG ACTIVITIESProceeds from borrowings Repayment of borrowingsDividends paidCash (used in) / provided by financing activities

Increase in cash and cash equivalents

Changes in cash and cash equivalentsCash and cash equivalents at the beginningIncrease in cash and cash equivalents Effect of exchange rate changes

Cash and cash equivalents at the end

December 31,

2011

(9 months) (*)

217,285,612

122,834,529

89,449,740

(1,368,975)

10,931,180

(20,608,276)

(1,212,963)

(3,096,279)

(20,039,345)

10,214,507

279,087

(1,150,908)

(228,763)

3,252,543

952,853

(62,015,107)

345,479,435

(238,943,827)

2,551,062

1,158,352

1,867,128

(233,367,285)

82,773,355

(131,074,860)

(30,000,000)

(78,301,505)

33,810,645

284,248,658

33,810,645

3,660,264

321,719,567

notes

13

12

15

15

22

21

march 31,

2011

(12 months) (*)

129,435,115

95,528,855

63,942,285

(1,261,398)

1,926,518

(20,322,013)

(183,512)

(39,398,213)

3,069,455

52,249,762

(1,345,839)

(1,962,485)

81,559

5,392,512

(1,836,711)

(28,021,819)

257,294,071

(216,110,039)

21,123,371

1,229,768

2,312,507

(191,444,393)

139,766,696

(96,949,827)

(30,000,000)

12,816,869

78,666,547

203,082,521

78,666,547

2,499,590

284,248,658

(Amounts in United States dollars, unless otherwise stated)

(*) See Note 1.

(**) The difference between interests expense and paid up is not significant.

The accompanying notes 1 to 35 are an integral part of these Consolidated Financial Statements.

Consolidated Statement of Cash Flows

34

1. GeneRAl InFoRMAtIonTecpetrol International S.A. (the “Company”) and its subsidiaries are mainly engaged in the exploration, development, production, transporta-tion and sale of hydrocarbons in sev-eral countries in America. References in these Consolidated Financial Statements to “Tecpetrol” include Tecpetrol International S.A. and its subsidiaries. The Company is incorporated and domiciled in Uruguay. Its legal address is La Cumparsita 1373, office 302, Montevideo, Uruguay.These Consolidated Financial Statements were authorized for issue by the Board of Directors on March 23, 2012.On March 30, 2011, the Board of Directors decided to modify the clos-ing date of the financial period from March 31 to December 31 of each year. Accordingly, the present period cor-responds to an irregular period of nine months, beginning on April 1, 2011 and ending on December 31, 2011. For this reason, the comparison of the infor-mation covering the period of nine months included in these Consolidated Financial Statements with the accounting information for the financial year ended on March 31, 2011, may be affected. The Financial Statements of Tecpetrol International S.A. at December 31, 2011, to be presented to the Auditoría Interna de la Nación (Uruguyan Internal Audit Office) were prepared in accordance with the Obligatory Financial Reporting Standards in Uruguay and were approved by the Board of Directors on March 23, 2012.

2. suMMARy oF sIGnIFICAnt ACCountInG polICIes The principal accounting policies applied in the preparation of these

Consolidated Financial Statements are set out below:

2.1 Basis of preparationThese Consolidated Financial Statements have been prepared in ac-cordance with International Financial Reporting Standards (“IFRS”), as is-sued by the International Accounting Standards Board (“IASB”), under the historical cost convention, as modified by the revaluation of financial assets and liabilities at fair value, the valuation of inventories and the employee benefits. Certain comparative amounts have been reclassified to conform current period’s presentation.The preparation of financial state-ments, in conformity with IFRS, re-quires management to make certain estimates and assessments that may affect the reported amounts of assets and liabilities, the disclosure of contin-gent assets and liabilities at the report-ing dates, and the reported amounts of income and expenses. Actual results may differ from these estimates.

2.2 Consolidation(a) subsidiariesSubsidiaries are all entities over which the Company has the power to govern the financial and operating policies, generally accompanying a sharehold-ing of more than one half of the voting rights. Subsidiaries are fully consoli-dated from the date on which control is transferred to the Company. They are de-consolidated from the date that this control ceases. The Company applies the purchase method of accounting to account for the acquisition of subsidiaries. The cost of an acquisition is measured as the fair value of the assets given, eq-uity instruments issued and liabilities incurred or assumed at the date of

Notes to the Consolidated Financial Statements

35Annual Report and Consolidated Financial Statements / Tecpetrol International S.A.

exchange. Acquisition related costs are expensed as incurred. Identifiable assets acquired, liabilities and contin-gent liabilities assumed in a business combination are measured at fair value at the acquisition date. Any non-controlling interest in the acquiree is measured either at fair value or at the non-controlling interests proportion-ate share of the acquiree’s net assets. The excess of the cost of acquisition and the amount of any non-controlling interest in the acquiree, over the fair value of the identifiable net assets acquired is recorded as goodwill. If this is less than the fair value of the net assets of the subsidiary acquired, the difference is recognized directly in the Consolidated Income Statement. Inter-company transactions, balances and unrealized gains (losses) on trans-actions between group companies are eliminated for the purposes of consoli-dation. As the functional currency of some subsidiaries is its respective local currency, some financial gains (losses) arising from inter-company transac-tions are generated. These are included in the Consolidated Income Statement under “Other financial results”.The accounting policies of the subsid-iaries have been modified where nec-essary to ensure consistency with the accounting policies adopted by the Company.

(b) Associated companiesAssociates are all entities over which the Company has significant influence generally accompanying a sharehold-ing of between 20% and 50% of the voting rights. Investments in associ-ates are initially recognized at cost and subsequently accounted for by the equity method of accounting. Unrealized results on transactions be-tween the Company and its associated

companies are eliminated to the extent of the Company’s share interest in them. The accounting policies of the associ-ated companies have been modified where necessary to ensure consistency with the accounting policies adopted by the Company. The Company incorpo-rates, where significant, the subsequent operations when financial statements of different dates are used to calculate the equity method of accounting. Investments in associated companies, each one of which is considered a Cash Generating Unit (“CGU”), are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recov-erable, and if appropriate, an impair-ment loss is recorded.

(c) Interests in joint venturesA joint venture is a contractual ar-rangement whereby two or more par-ties undertake an economic activity that is subject to joint control. Joint control exists only when the strategic financial and operating decisions relat-ing to the activities require the unani-mous consent of the parties involved. A jointly-controlled entity is a joint ven-ture that involves the establishment of a company, partnership or other entity to engage in economic activity that the group jointly controls with its partners. The assets and liabilities of a jointly-controlled entity are accounted for by proportionate consolidation. Accounting policies have been modified as necessary to ensure consistency with the policies adopted by the Company.

2.3 Foreign currency translation(a) Functional and presentation currency Items included in the financial state-ments of the Company and its subsidiar-ies are recorded in the currency of the

36

primary economic environment in which the entity operates (functional currency). These Consolidated Financial Statements are presented in United States dollars (“US$”), which is the Company’s func-tional and presentation currency.The functional currency of the subsid-iaries is their local currency or in some cases the United States dollars, when the main economic and financial transactions are denominated in United States dollars.

(b) transactions in currency other than the functional currency Foreign currency transactions are translated into the functional currency using the exchange rates prevail-ing at the dates of the transaction or valuation. Foreign exchange gains and losses resulting from the settle-ment of such transactions and from the translation at year-end exchange rates of monetary assets and liabilities denominated in foreign currencies are recognized in the Consolidated Income Statement, except when deferred in Other Comprehensive income as cash flow hedges. Translation differences on non-monetary balances, such as as-sets held at fair value through profit or loss, are recognized in the Consolidated Income Statement. Translation differenc-es on non-monetary financial assets and liabilities, such as investments classified as available-for-sale financial assets are included in Other comprehensive income. The Share capital account is translated at the exchange rate in effect at the date of each capital contribution. The Legal reserve is translated at the exchange rate applicable in the month in which it is affected by shareholders. (c) translation of financial statementsThe financial statements of the sub-sidiaries whose functional currency is

different to the presentation currency are translated into the presentation currency as follows: (i) assets and liabilities are translated

at the closing rate at each report-ing date and income and expenses are translated at the average rate of the period;

(ii) resulting translation differences are recognized in the Other com-prehensive income as currency translation differences. When a subsidiary is disposed of or sold, the accumulated currency transla-tion difference is recognized as profit or loss at the date of disposi-tion or sale.

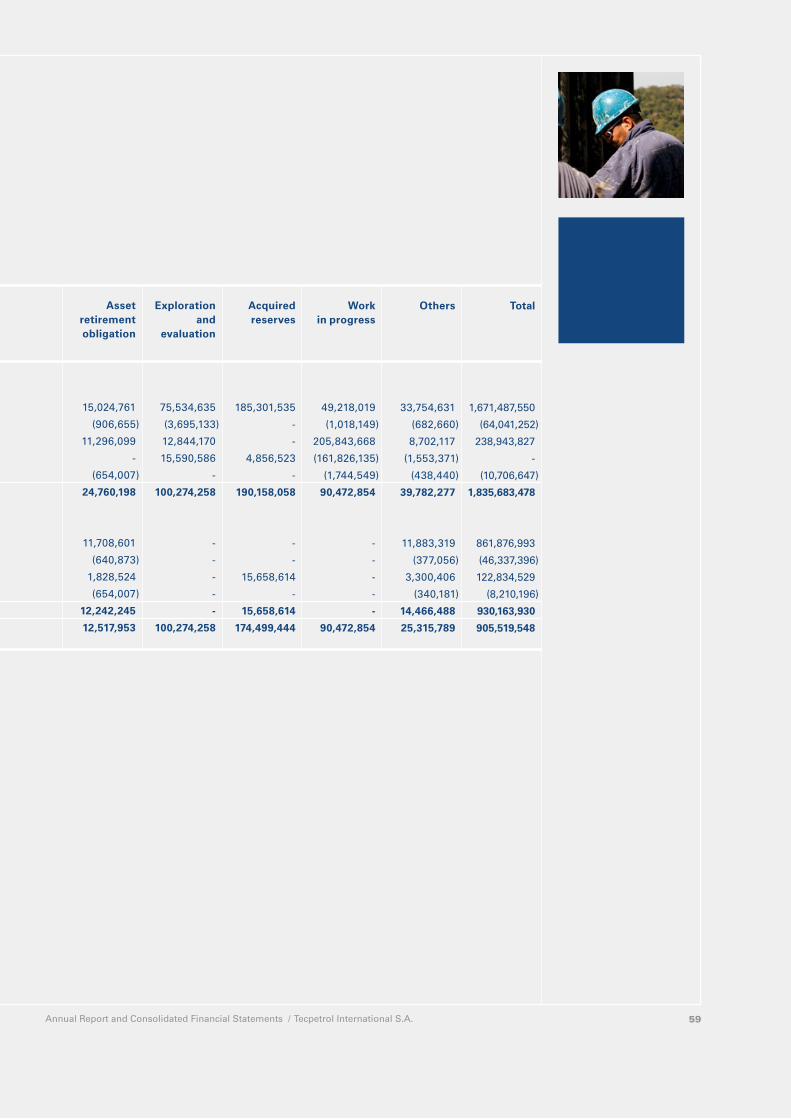

2.4 property, plant and equipment. exploration, evaluation and development assets Exploration and evaluation expenditures are accounted for using the successful efforts method of accounting and are ac-cumulated on a field-by-field basis. Costs related to the exploration and exploitation of fields and to the acqui-sition of rights and concessions related to proved reserves are capitalized. Exploration costs and the acquisition costs for rights and concessions re-lated to probable and possible reserves are initially capitalized. Subsequently, if exploratory results are determined to be unsuccessful on completion and evaluation, these costs are charged to expenses in the period in which this determination is confirmed definitively by studies, technical reports or addi-tional drilling carried out. No deprecia-tion is charged during the exploration and evaluation phases.Field development costs are capital-ized as Property, plant and equipment. These costs include the acquisition and installation of production facili-ties, development drilling costs and

37Annual Report and Consolidated Financial Statements / Tecpetrol International S.A.

project-related engineering.The Company regards wells drilled in producing fields for the purpose of developing proved reserves as devel-opment wells. The Company considers any wells which are neither develop-ment wells nor service wells to be exploratory wells.Workovers of wells used to develop reserves and/or increase production are capitalized and depreciated on the basis of their estimated average useful life. Maintenance costs are charged to income when incurred.Asset retirement obligations costs are calculated as explained in Note 2.14. The Company periodically reevaluates the remaining useful lives of its assets, their residual value and the amortization method and readjusts these if necessary. The depreciation of wells, machinery, equipment and installations has been calculated according to the depletion method over the total proved reserves developed considered in each field as from the month of starting production.The depreciation of exploration and exploitation rights and of the cost of the acquisition of rights and concessions related to proved reserves is calculated using the depletion method over the total amount of proven reserves in each field. The depreciation of the remaining Property, plant and equipment is calcu-lated using the straight line method by applying such annual rates as required to write off their value at the end of their estimated useful lives, as follows:

Vehicles up to 5 years

Furniture and office equipment up to 5 years

Gains and losses from disposals are determined by comparing the pro-ceeds with the carrying amount of the

asset and are recognized within “Other operating income/expenses” in the Consolidated Income Statement.Assets in productive and develop-ment fields are reviewed for impair-ment whenever events or changing circumstances indicates that the car-rying value may not be recoverable. Impairment losses are recognized when the carrying amount of the as-sets is greater than their recoverable amount. The recoverable amount is the higher of the asset’s fair value less cot to sale and its value in use. The value in use is determined on the basis of the present value of net future cash flows expected to arise from the remaining commercial reserves. Assets which have suffered impair-ment losses in previous periods are reviewed at each reporting date in order to assess if the conditions which gave rise to the impairment loss have changed and, if appropriate, reverse the previous recognized im-pairment loss.

2.5 Intangible assetsGoodwillGoodwill represents the excess of the acquisition cost over the fair value of the net identifiable assets acquired as part of a business combination. Goodwill has an indefinite useful life and is subject to an impairment test on an annual basis. Impairment losses on goodwill are not reverted. For the purposes of the recover-ability test, goodwill is allocated to those cash-generating units ex-pected to benefit from the business combination.

2.6 InventoriesHydrocarbon stocks are valued at their net realizable value at the end of each reporting date.

38

Supplies and spare parts are principal-ly valued at cost, using the weighted average cost formula. The recoverable amount is calculated at each reporting date and an allowance is recognized in the Consolidated Income Statement, if necessary.

2.7 trade and other receivablesTrade and other receivables are rec-ognized initially at fair value and sub-sequently measured at amortized cost using the effective interest method, less allowances for doubtful accounts, if necessary. An allowance for doubtful accounts of trade receivables is established when there is objective evidence that the Company will not be able to col-lect the amounts due according to the original terms. Indicators that the trade receivable may be impaired include the debtor experiencing significant financial difficulties, the probability that the debtor will enter in bankruptcy or be subject to insolvency proceed-ings, and default or significant delays in payments. Furthermore, this allow-ance is adjusted periodically based on the age of the receivables. The asset’s carrying amount is shown net of the allowances, where applicable. The al-lowance expense is recognized in the Consolidated Income Statement under “Selling expenses”.

2.8 Cash and cash equivalents For the purposes of the Consolidated Statement of Cash Flows, cash and cash equivalents includes cash in hand, bank deposits, other short-term highly liquid investments with original ma-turities of less than three months and bank overdrafts. In the Consolidated Statement of Financial Position, bank overdrafts are shown within “Borrowings” in current liabilities.

2.9 equity(a) equity componentsThe Consolidated Statement of Changes in Equity includes share capital, legal reserves, other reserves (including the currency translation differences, hedge accounting and the variations in the fair value of available-for-sale financial assets), retained earn-ings and non-controlling interest. (b) share capitalOrdinary shares are classified as Equity. Authorized share capital is 15,000,000 Uruguayan pesos (UY$). Total capital issued and outstanding as of December 31, 2011 and March 31, 2011, amounts to UY$ 9,541,175,037.89 and is represented by a bond corre-sponding to 9,541,175 ordinary bearer shares with a nominal value of UY$ 1,000 per share and a total nomi-nal value of UY$ 9,541,175,000 as well as a provisional certificate for UY$ 37.89 in favor of Techint Investments N.V.

(c) dividend distributionDividends distributions are based on Tecpetrol International S.A. Stand-alone Financial Statements, rather than on its Consolidated Financial Statements, and they are recognized as a liability in the Consolidated Financial Statements in the period in which they are approved by a share-holders’ meeting.

2.10 BorrowingsBorrowings are recognized initially at fair value net of transaction costs in-curred. Subsequently, they are stated at amortized cost.Borrowings are classified as current liabilities unless the Company has the unconditional right to defer the settle-ment of the liability for at least 12 months following the reporting date.

39Annual Report and Consolidated Financial Statements / Tecpetrol International S.A.

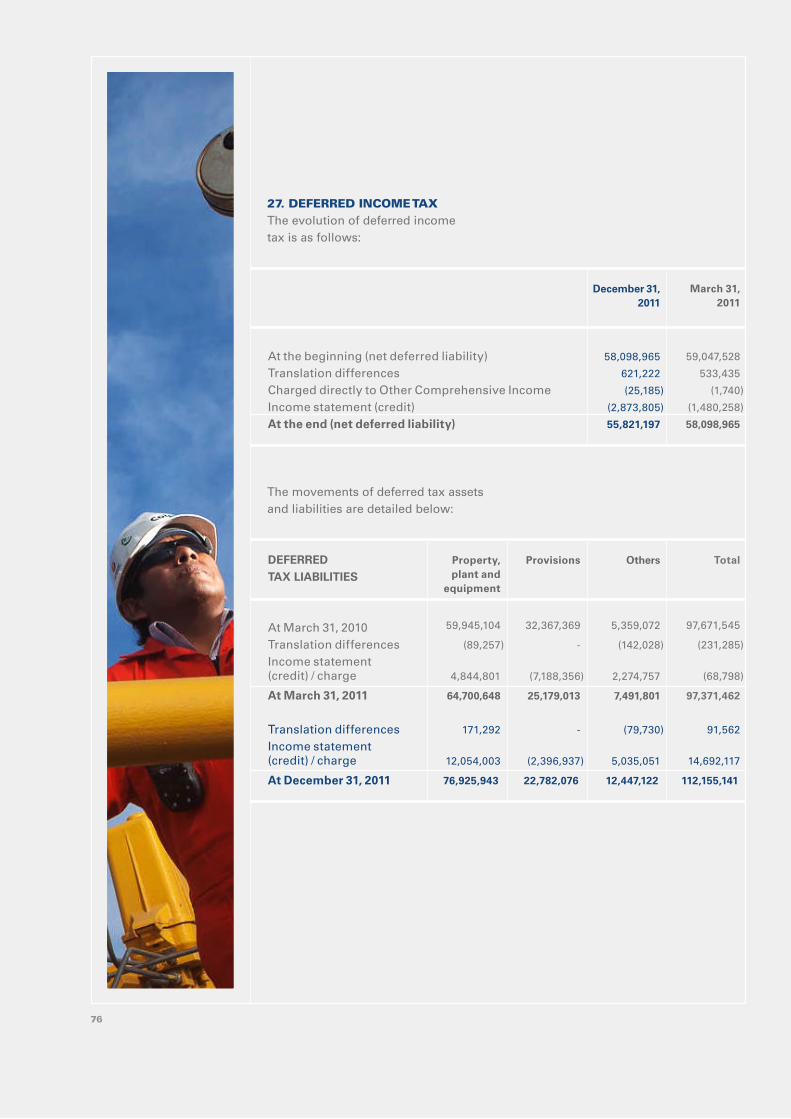

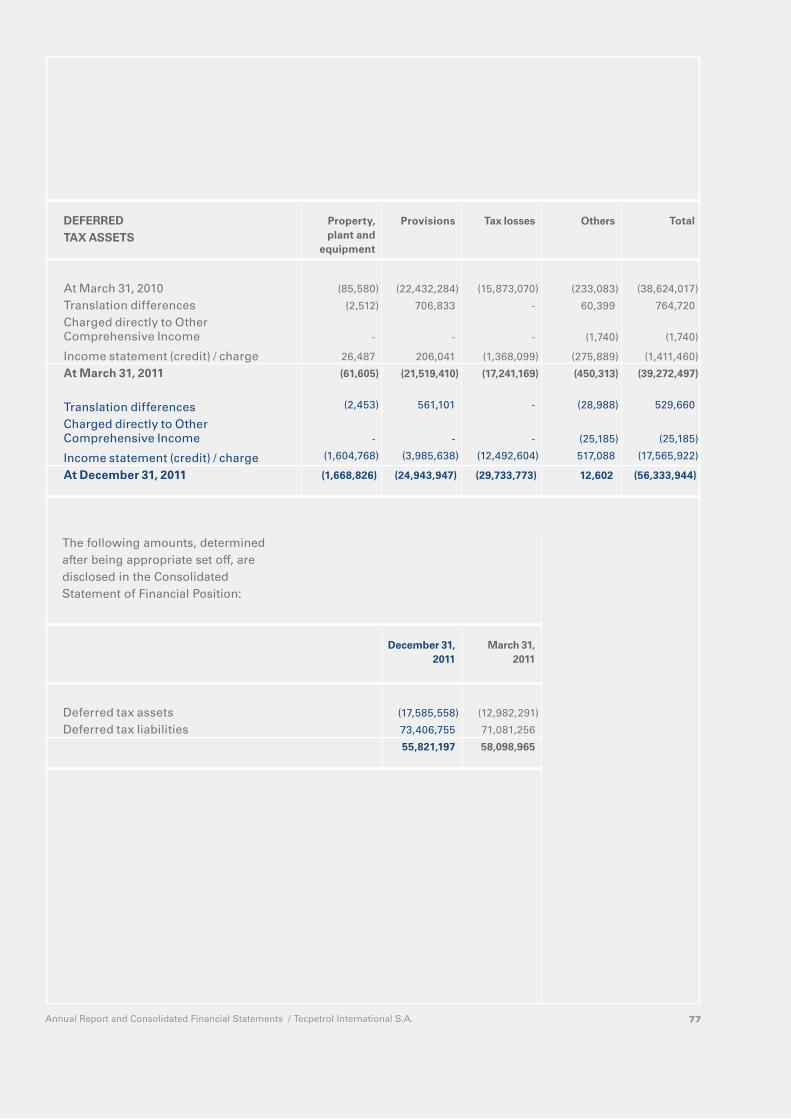

2.11 Income tax The income tax expense for the period comprises current and deferred tax. Tax is recognized in the Consolidated Income Statement, excepting those cases where it is related to items rec-ognized in the Other Comprehensive Income. In this case, tax is also recog-nized in Other Comprehensive Income. Current income tax charges are calculat-ed on the basis of the tax laws existing in the countries in which the Company and its subsidiaries operate and gener-ate taxable income. Tecpetrol periodi-cally evaluates positions taken in tax returns with relation to situations where tax legislation is subject to interpreta-tion and accordingly establishes provi-sions where considered appropriate. Deferred income tax is recognized by applying the liability method on tem-porary differences arising between the tax bases of assets and liabilities and their carrying amounts. The principal temporary differences arise from the depreciation of property, plant and equipment, valuation of inventories and provisions. Deferred tax assets and liabilities are measured at the tax rates expected to apply in the period in which the related tax asset is realized or the tax liability settled, based on the rates and legislation in force at the reporting date. Deferred tax assets are also recognized for net operating loss carryforwards to the extent that it is probable that future taxable income will be available. Tecpetrol reassess unrecognized de-ferred tax assets at each reporting date and recognizes the previously unrecog-nized deferred tax asset to the extent that it has become probable that future taxable income will allow the deferred tax asset to be recovered. Deferred tax assets and liabilities are offset for by each subsidiary when there

is a legally enforceable right to offset current tax assets against current tax li-abilities and when deferred income tax is levied by the same fiscal authorities.

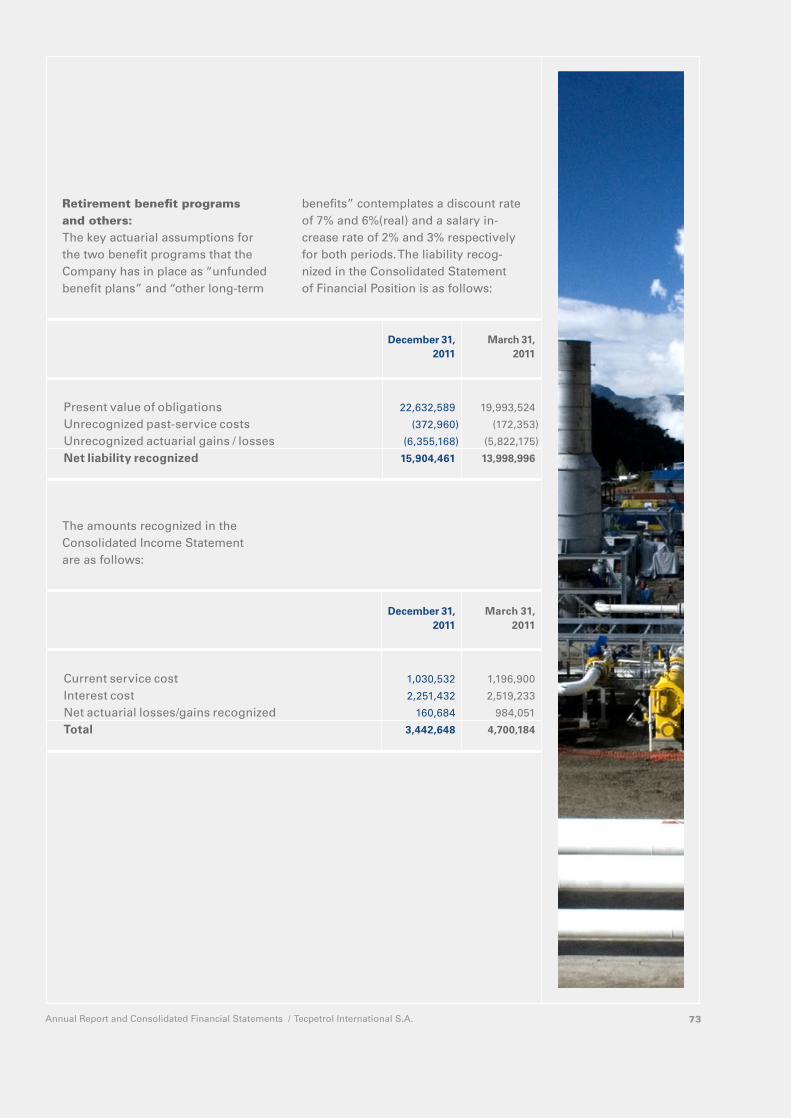

2.12 employee benefits(a) Retirement benefit plans and othersSome subsidiaries have benefit plans such as “unfunded defined benefits” and “other long-term benefits” that are granted over an employee’s working life and after retirement under certain established conditions.Liability provisions for such benefits are recorded at the present value of future flows, and charged to expense during the remaining years of service of the beneficiaries, until all the vesting condi-tions of each benefit have been met. The liability is calculated at least once a year by independent actuaries using the “Projected unit credit” method.The net liability recognized in the Consolidated Statement of Financial Position includes the present value of the obligation plus / minus the actuar-ial gains / losses and the unrecognized past-service costs. Tecpetrol holds an investment in US$ which may be used to pay such ben-efits in whole or in part. These invest-ments are neither part of a specific plan, nor are they held separate from other Tecpetrol assets. Accordingly, the plan is classified as “unfunded” under IFRS definitions.

(b) employee retention and long-term incentive program As from the financial period closed on March 31, 2011, the Company has ad-opted an employee retention and long-term incentive program for certain senior executives in some subsidiaries. According to the program, the benefi-ciaries will be granted with a number

40

of units valued according to the eq-uity book value per Company share (excluding non-controlling interests). The units will be vested over a period of four years and the corresponding subsidiaries will redeem them after a period of ten years from the grant day, with the option for the employee to request the payment as from the seventh year onwards, or when the employee ceases employment from the subsidiary responsible for making the payment, at the equity book value at the date of payment. The beneficia-ries will also receive cash payments equivalent to the dividend paid out per share, each time Tecpetrol International S.A. makes a cash payment to its shareholders.

2.13 employee’s statutory profit sharingIn accordance with the laws in force in the territories of certain subsidiaries of the Company, an annual benefit must be paid to employees, calculated on a similar basis to that used for income tax purposes. The liability is calculated according to IAS 19 – “Employee bene-fits” and is disclosed under “Trade and other payables” in the Consolidated Statement of Financial Position and the corresponding expense charge is classified as “Labor costs” in the Consolidated Income Statement.

2.14 provisionsProvisions are recognized when: a) the Company has present legal or con-structive obligations as a result of past events; b) it is highly probably that an outflow of resources will be required to settle the obligation; and, c) the amount can be reliably estimated.Provisions are measured at the pres-ent value of the expenditures expected to be required to settle the obligation

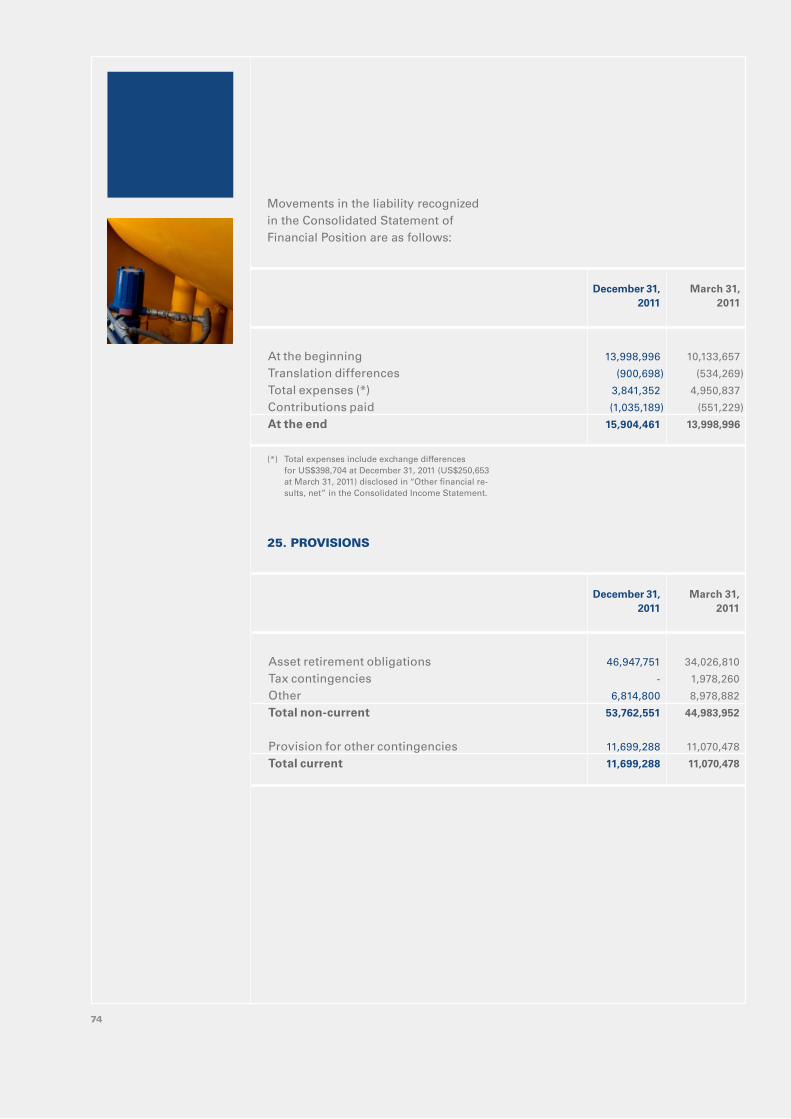

using the appropriate discount rate. Provisions for asset retirement obliga-tions are calculated by establishing the present value of future costs related to the abandonment of each field. When the liability is initially recorded, the Company capitalizes these costs by increasing the carrying amount of the related asset. Over time, the liability is accreted to its present value during each period, and the initially capitalized cost is depreciated over the estimated use-ful life of the related asset, as detailed in Note 2.4. The Company periodically re-evaluates the future costs of asset retirement obligation, based on changes in technology and variations in the costs of restoration necessary to protect the environment. The effects of these re-calculations are included in the financial statements in which they are deter-mined and disclosed as an adjustment to the liability and the related asset.

2.15 trade and other payablesTrade and other payables are recog-nized initially at fair value and subse-quently stated at amortized cost using the effective interest method.

2.16 Revenue recognitionRevenue comprises the sale of goods and services to third parties net of value-added tax, withholding and dis-counts. Revenue from the sale of hy-drocarbons and other assets is recog-nized when all the significant risks and rewards of ownership are transferred to the buyer, at the fair value of the consideration received or receivable.Other revenues are recognized on an accrual basis. Dividends received are recognized when the right to receive payment is established.Revenues from interest are recognized on an accrual basis, using the effective interest method.

41Annual Report and Consolidated Financial Statements / Tecpetrol International S.A.

2.17 Cost of sales The cost of sales is recognized in the Consolidated Income Statement on an accrual basis and classified as “Operating costs”.

2.18 Financial instrumentsThe Company classifies its non-derivative financial instruments into the following categories: at fair value through profit or loss, loans and re-ceivables, available-for-sale assets and other financial liabilities. Classification depends on the nature of the financial instruments and the purpose for which they were acquired. The Company de-termines the classification of its finan-cial instruments at the time of initial recognition, and reassesses their desig-nation at each reporting date. Financial assets and liabilities are recognized and derecognized on their settlement date.

(a) Financial assets at fair value through profit or lossA financial asset is classified in this category if it is held for trading in the short term or if it is so designated by management initially. This category includes cash and cash equivalents and the investments in financial debt instruments held for trading.

(b) loans and receivablesLoans and receivables are non-derivative financial assets with fixed or determin-able payments that are not quoted on an active market. This category includes trade and other receivables. In general, they are classified as current assets ex-cept for those with maturities greater than 12 months following the reporting date.

(c) Available-for-sale financial assets Available-for-sale financial assets are non-derivative financial instruments

that are either designated in this cat-egory or not classified in any of the other categories. They are included in non-current assets unless manage-ment intends to sell the investment within a 12-month period as from the reporting date. Available-for-sale fi-nancial assets are valued at fair value and variations are recognized in Other Comprehensive Income. The Company determines at each reporting date whether there are any impairment indicators. In the case of equity instruments classified as available-for-sale, any significant or prolonged decline in the fair value of fi-nancial assets below its cost is consid-ered as an impairment indicator and, if appropriate, the accumulated losses in Other Comprehensive Income is re-classified to the Consolidated Income Statement.

(d) other financial liabilitiesThis includes borrowings and trade and other payables.

2.19 derivative financial instruments and hedging activitiesDerivative financial instruments are recognized at fair value. Specific tools are used to calculate the fair value of each instrument, which are tested for consistency on a regular basis. Market rates are used for all pricing operations. These include exchange rates, interest rates and other discount rates which mitigate the nature of the underlying risk. The fair value of derivate financial instruments is disclosed in Note 28. The method of recognizing the result-ing gain or loss depends on whether the derivative is designated as a hedg-ing instrument, and if so, on the nature of the item being hedged. Changes in the fair value of derivate financial

42

instruments that are not designated as hedging instruments are immediately recognized in the Consolidated Income Statement under “Other financial re-sults, net”.The full fair value of a hedging instru-ment is classified as a non-current asset or liability if the hedged item has a maturity greater than 12 months, and as a current asset or liability, if the remaining maturity of the hedged item is less than 12 months. Derivatives not designated as hedging instruments are classified as current assets or liabilities.

Cash flow hedgesWhen a derivative is designated as a hedging instrument, the Company documents the relationship between hedging instruments and hedged items at the inception of the transaction, as well as its risk management objectives and strategy for undertaking various hedge transactions. The Company also documents its assessment, both at the inception and on an ongoing basis, of the effectiveness of the derivatives used in hedging transactions to offset chang-es in the cash flows of hedged items.The effective portion of changes in the fair value of derivatives that are desig-nated and qualify as cash flow hedges is recognized in Other comprehensive income. The profit or loss relating to the ineffective portion is recognized immediately in the Consolidated Income Statement under “Other finan-cial results, net”.When a hedging instrument expires or is sold, or when a hedge no lon-ger meets the criteria for hedge ac-counting, any cumulative gain or loss previously recognized in Other Comprehensive income remains in Other Comprehensive Income and is reclassified to the Consolidated

Income Statement when the forecast transaction is ultimately recognized in the Consolidated Income Statement. When a forecast transaction is no longer expected to occur, the cumula-tive gain or loss recognized in Other Comprehensive Income is immediately transferred to the Consolidated Income Statement.

3. new ACCountInG stAndARds(a) new standards, interpretations and amendments to the published standards effective in 2011:There are no new standards, inter-pretations or amendments which are effective for the first time in the current period and have a material impact on the Company.

(b) new standards, interpretations and amendments to published standards which are not yet effective and which have not been early adopted: • IFRS 9, “Financial instruments”

In November 2009, the IASB issued IFRS 9 “Financial instruments” which establishes principles for the disclo-sure of financial assets, simplifying their classification and form of mea-surement. This standard applies to annual periods beginning on or after January 1, 2015. Management has not yet assessed the potential impact that the ap-plication of IFRS 9 may have on the Consolidated Financial Statements.

• IFRS 10, “Consolidated financial statements” In May 2011, the IASB issued IFRS 10 “Consolidated financial statements” which establishes the principles for the presentation and preparation of consolidated financial statements when a company owns one or more

43Annual Report and Consolidated Financial Statements / Tecpetrol International S.A.

other companies. IFRS 10 replaces IAS 27, “Consolidated and separate financial statements” and SIC 12 “Consolidation—Special Purpose Entities”. This standard will be effec-tive for accounting periods begin-ning after January 1, 2013, and its early application is permitted. Management has not yet assessed the potential impact that the appli-cation of IFRS 10 may have on the Consolidated Financial Statements.

• IFRS 11, “Joint arrangements” In May 2011, the IASB issued IFRS 11 “Joint arrangements” which estab-lishes the principles for the presen-tation and preparation of financial statements for the members of a joint arrangement. IFRS 11 replaces IAS 31, “Interests in joint ventures” and SIC 13 “Jointly-controlled enti-ties and non-monetary contributions by venturers”. This standard is effec-tive for accounting periods begin-ning as from January 1, 2013. Management has not yet assessed the potential impact that the appli-cation of IFRS 11 may have on the Consolidated Financial Statements.

• IFRS 12, “Disclosure of interests in other entities” In May 2011, the IASB issued IFRS 12, “Disclosure of interests in other entities” applicable to companies with interests in a subsidiary, associ-ate, joint venture or other forms of investment. IFRS 12 requires that a company disclose information which will allow the users of the financial statements to evaluate the nature and risk associated with risks in other entities and the effects of these on its financial position. This is effec-tive for those annual periods starting as from January 1, 2013. Management has not yet assessed the potential impact that the application of

IFRS 12 may have on the Consolidated Financial Statements.

• IFRS 13 “Fair value measurement” In May 2011, the IASB issued IFRS 13 “Fair value measurement” which es-tablishes a structure to measure fair value and disclosure requirements when fair value measurement is required by a standard. This standard is applicable both to financial and non-financial instruments measured at fair value. It will be effective as from January 1, 2013. Management estimates that the ap-plication of these modifications will not have any material effect on the financial position or results.

• IAS 27, “Separate financial statements” As a consequence of the issue of IFRS 10, “Consolidated financial state-ments”, IAS 27 was modified in May 2011 by the IASB to include only those requirements related to separate financial statements. IAS 27, formerly “Consolidated and separate financial statements” is now “Separate finan-cial statements”. It will be effective as from January 1, 2013. Management estimates that the ap-plication of these modifications will not have any material effect on the financial position or results.

• IAS 28, “Investments in associates and joint ventures” After the issue of IFRS 11, the IASB decided to include joint ventures in IAS 28, as the proportional equity value method also applies to these. It thus changed the name of the stan-dard to “Investments in associates and joint ventures”. This modification is effective as from January 1, 2013. Management has not yet assessed the potential impact that the ap-plication of IAS 28 may have on the Consolidated Financial Statements.

44

• IAS 1, “Presentation of financial statements” On June 16, 2011, the IASB published the amendments to IAS 1, which principally include the parameters related to the objective of improv-ing the consistency and clarity of the presentation of the items presented in Other Comprehensive Income. All entities must apply these modi-fications for the accounting periods beginning on or after July 1, 2012. Management has not yet assessed the potential impact that these modifications may have on the Consolidated Financial Statements.

• IAS 19, “Employee Benefits” On June 16, 2011, the IASB pub-lished the modifications to IAS 19 “Employee Benefits”. These modifica-tions principally cover the elimination of the option to defer the recognition of actuarial profit and loss as well as simplifying the way changes in assets and liabilities arising from defined benefit plans are presented. Entities should apply these modifications to accounting periods beginning on or after January 1, 2013. Management has not yet assessed the potential impact that the appli-cation of these modifications may have on the Consolidated Financial Statements.

Management has evaluated the signifi-cance of other new standards, amend-ments and interpretations not yet effec-tive and has concluded that they are not relevant for the Company.

4. FInAnCIAl RIsK MAnAGeMent

4.1 Financial risk factorsThe activities of the Company and its sub-sidiaries expose it to a variety of financial risks, mostly related to market risks (in-cluding the effects of changes in foreign currency exchange rates, in interest rates and market prices), the concentration of credit risk, liquidity risk and capital risk.The Company’s risk management pro-gram focuses on the unpredictability of financial markets and seeks to mini-mize any potentially adverse effects on its financial performance.

(i) Foreign exchange rate riskThe Company and its subsidiaries are exposed to the risk of exchange rate fluctuations as a result of transactions made currencies other than their func-tional currencies. As the Company’s functional currency is US$, the objec-tive of the foreign currency hedge program is principally to reduce the risk associated with changes in foreign currency exchange rates against its functional currency.Tecpetrol’s exposure to changes in ex-change rates is reviewed periodically. The Company aims to neutralize the poten-tially negative impact of fluctuations in the value of other currencies with respect to its functional currency using derivative financial instruments, if necessary.The following table discloses the expo-sure (in thousands of US$) to different currencies as of December 31, 2011, in-cluding the effect of foreign exchange derivative instruments.

45Annual Report and Consolidated Financial Statements / Tecpetrol International S.A.

The Company estimates that the impact of a favorable or unfavorable change in exchange rates of 1% would have gen-erated a gain / loss of US$1.03 million as of December 31, 2011, and US$0.63 million as of March 31, 2011. The im-pact on Equity would come to US$0.27 million as of December 31, 2011, and US$0.14 million as of March 31, 2011.

(ii) Interest rate risk The Company is exposed to inter-est rate volatility risk, mainly re-lated to short-term investments and borrowings. The following table shows the propor-tions of fixed-rate and variable-rate debt as of each reporting date.

US$EURARSCOPPENMXNDKKUY$

Fixed rate Variable rate

ARS

(24,333)

-

N/A

-

-

-

-

-

CoP

(52,919)

-

-

N/A

-

-

-

-

BoB

(3,053)

-

-

-

-

-

-

-

PEn

(25,037)

-

-

-

N/A