Languages

Pages

Legal

Roadshow Presentation February 2015

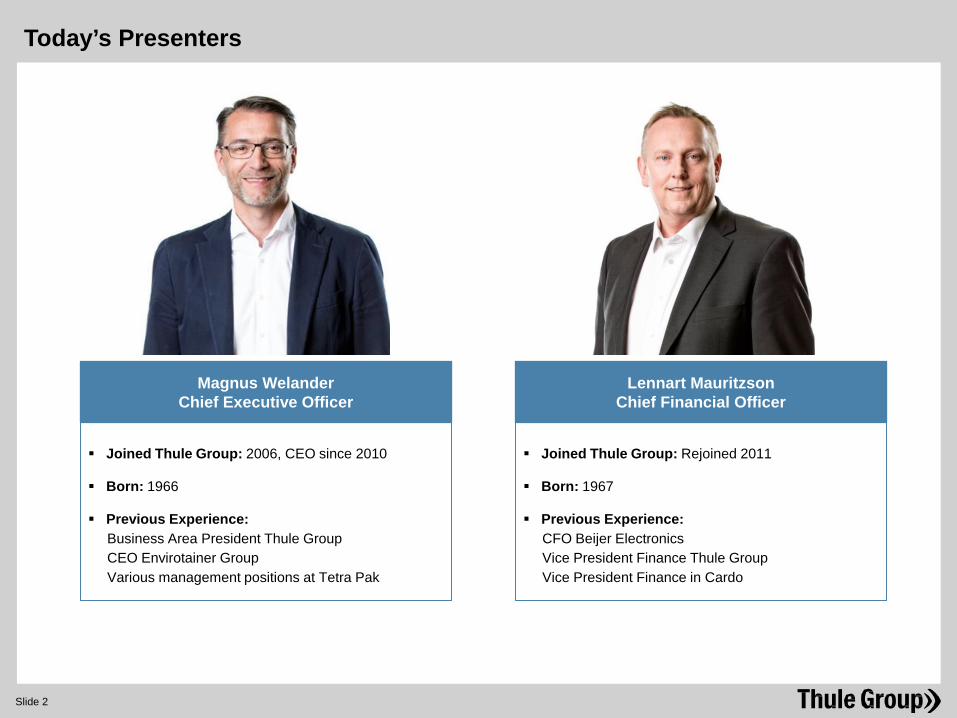

Today’s Presenters

Magnus Welander Chief Executive Officer

Lennart Mauritzson Chief Financial Officer

Slide 2

Joined Thule Group: 2006, CEO since 2010

Born: 1966

Previous Experience: Business Area President Thule Group CEO Envirotainer Group Various management positions at Tetra Pak

Joined Thule Group: Rejoined 2011

Born: 1967

Previous Experience: CFO Beijer Electronics Vice President Finance Thule Group Vice President Finance in Cardo

Slide 3

The Thule Group Vision – Active Life, Simplified

Slide 4

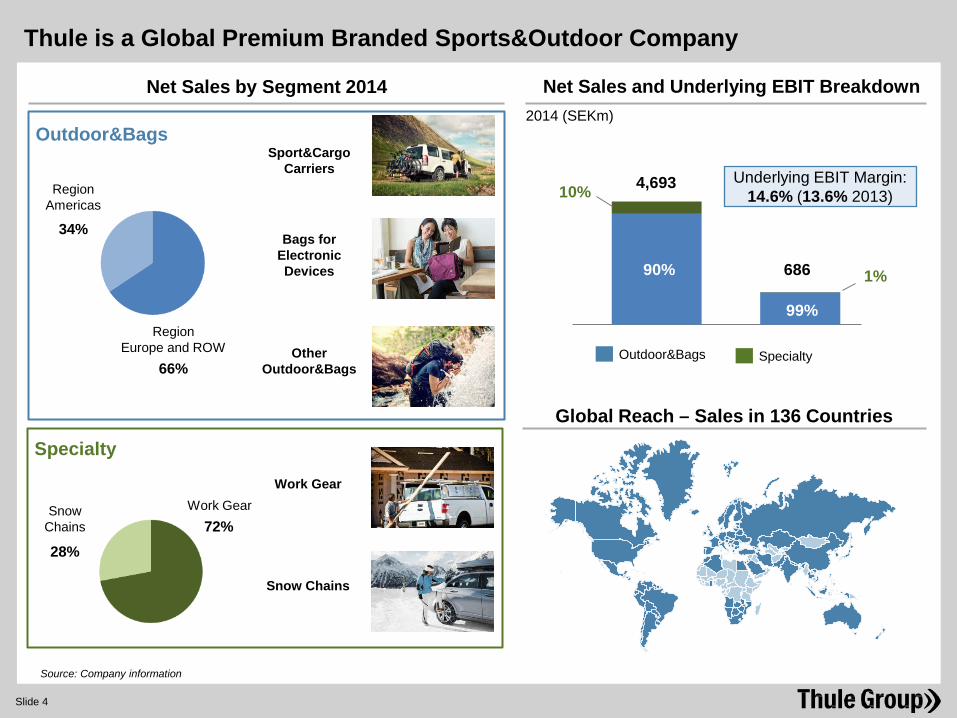

Source: Company information

Thule is a Global Premium Branded Sports&Outdoor Company

Net Sales by Segment 2014

Sport&Cargo Carriers

Bags for Electronic Devices

Other Outdoor&Bags

Work Gear

Snow Chains

Outdoor&Bags

Specialty

Region Americas

Region Europe and ROW

Work Gear Snow Chains 72% 28%

34%

66%

Net Sales and Underlying EBIT Breakdown

4,693

686

2014 (SEKm)

Underlying EBIT Margin: 14.6% (13.6% 2013)

Global Reach – Sales in 136 Countries

90%

10%

1%

99%

Outdoor&Bags Specialty

Slide 5

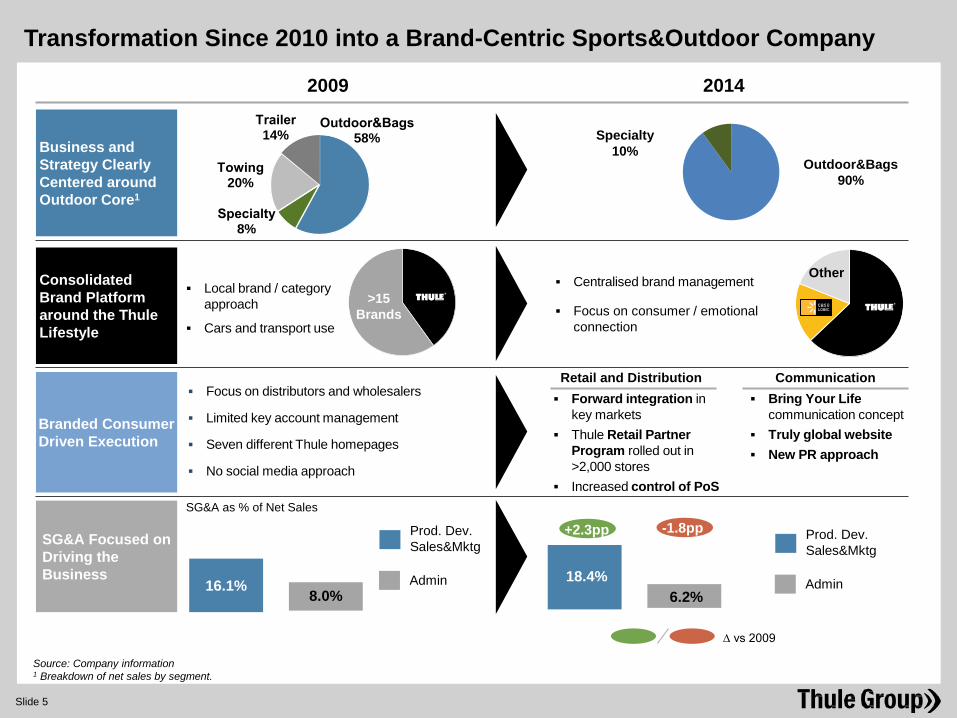

Point 1 2009 2014

Business and Strategy Clearly Centered around Outdoor Core1

Consolidated Brand Platform around the Thule Lifestyle

Branded Consumer Driven Execution

SG&A Focused on Driving the Business

Local brand / category approach

Cars and transport use

Centralised brand management

Focus on consumer / emotional connection

Focus on distributors and wholesalers

Limited key account management

Seven different Thule homepages

No social media approach

Retail and Distribution Communication Forward integration in

key markets Thule Retail Partner

Program rolled out in >2,000 stores

Increased control of PoS

Bring Your Life communication concept

Truly global website New PR approach

SG&A as % of Net Sales

>15 Brands

Other

Outdoor&Bags58%

Specialty8%

Towing20%

Trailer14%

Source: Company information 1 Breakdown of net sales by segment.

Transformation Since 2010 into a Brand-Centric Sports&Outdoor Company

-1.8pp +2.3pp

∆ vs 2009

Prod. Dev. Sales&Mktg

Admin

Prod. Dev. Sales&Mktg

Admin 16.1% 8.0% 18.4%

6.2%

Outdoor&Bags 90%

Specialty 10%

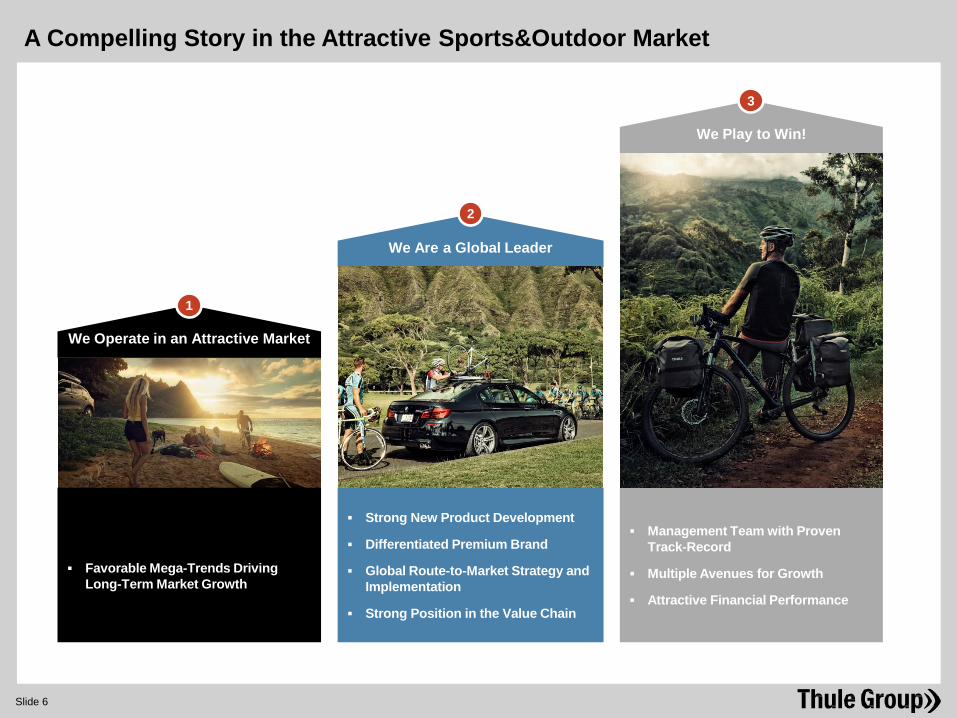

We Are a Global Leader

We Operate in an Attractive Market

Strong New Product Development

Differentiated Premium Brand

Global Route-to-Market Strategy and Implementation

Strong Position in the Value Chain

Management Team with Proven Track-Record

Multiple Avenues for Growth

Attractive Financial Performance

Favorable Mega-Trends Driving

Long-Term Market Growth

We Play to Win!

1

2

3

Slide 6

A Compelling Story in the Attractive Sports&Outdoor Market

Slide 7

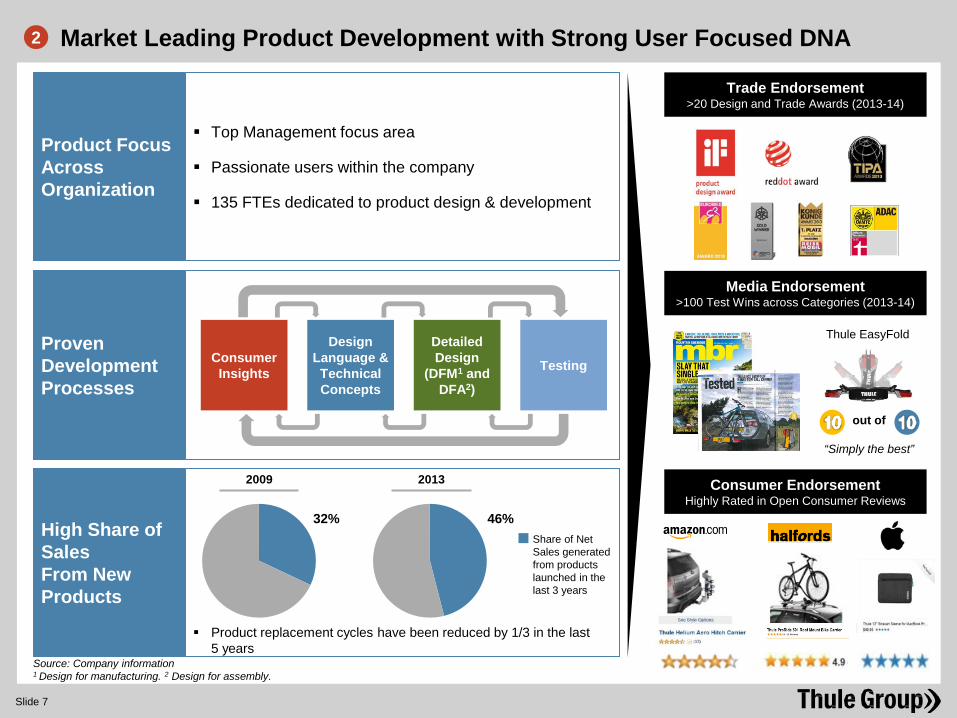

Trade Endorsement >20 Design and Trade Awards (2013-14)

Media Endorsement >100 Test Wins across Categories (2013-14)

Consumer Endorsement Highly Rated in Open Consumer Reviews

Thule EasyFold

“Simply the best”

out of

Proven Development Processes

Product Focus Across Organization

Top Management focus area

Passionate users within the company

135 FTEs dedicated to product design & development

Consumer Insights

Design Language & Technical Concepts

Detailed Design

(DFM1 and DFA2)

Testing

Source: Company information 1 Design for manufacturing. 2 Design for assembly.

Product replacement cycles have been reduced by 1/3 in the last 5 years

High Share of Sales From New Products

32% 46%

2009 2013

Share of Net Sales generated from products launched in the last 3 years

Market Leading Product Development with Strong User Focused DNA 2

Long-Term Brand Building Sponsoring – Thule Crew

A Modern Approach to Consumer Communication

Slide 8

Consumer Involvement – Social Media and Uploading

Earned Media – PR focus on Relevant Channels

2

Slide 9

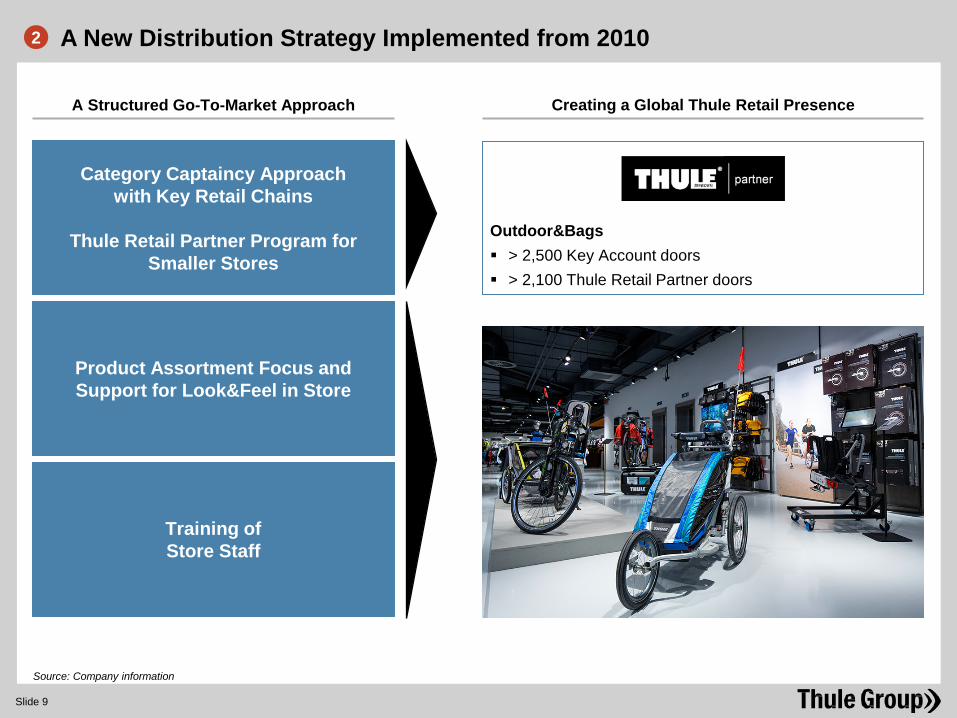

Creating a Global Thule Retail Presence

Category Captaincy Approach with Key Retail Chains

Thule Retail Partner Program for

Smaller Stores

Product Assortment Focus and Support for Look&Feel in Store

Training of Store Staff

A Structured Go-To-Market Approach

Outdoor&Bags > 2,500 Key Account doors > 2,100 Thule Retail Partner doors

Source: Company information

A New Distribution Strategy Implemented from 2010 2

Slide 10

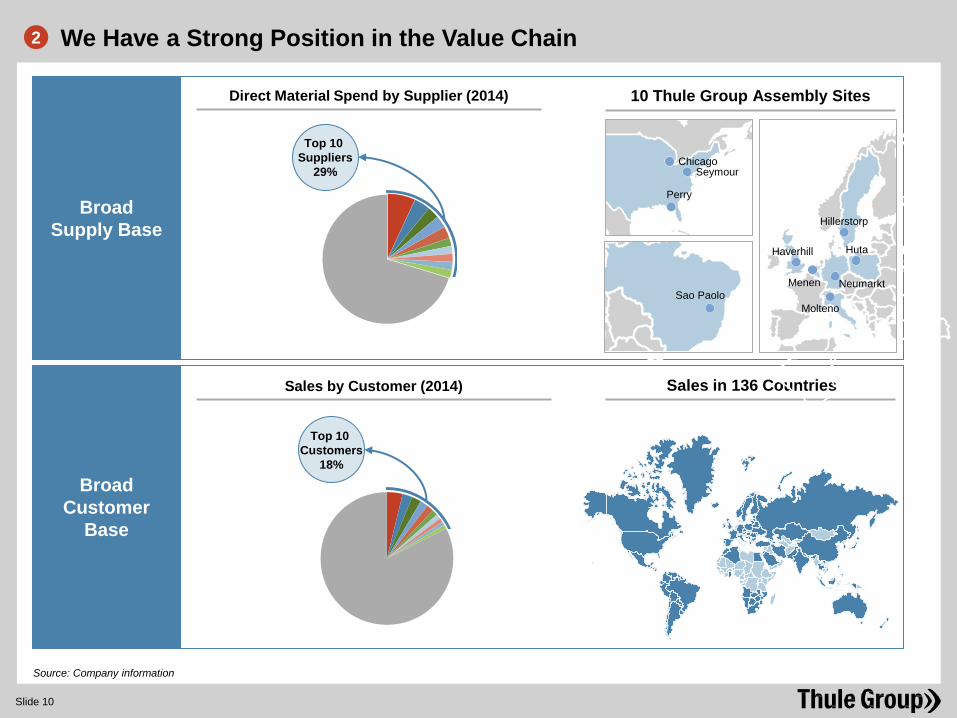

Source: Company information

Broad Supply Base

Broad Customer

Base

Top 10 Suppliers

29%

Direct Material Spend by Supplier (2014)

Top 10 Customers

18%

Sales by Customer (2014)

10 Thule Group Assembly Sites

Sales in 136 Countries

We Have a Strong Position in the Value Chain 2

Perry

Seymour Chicago

Sao Paolo

Huta

Molteno

Hillerstorp

Neumarkt

Haverhill

Menen

Slide 11

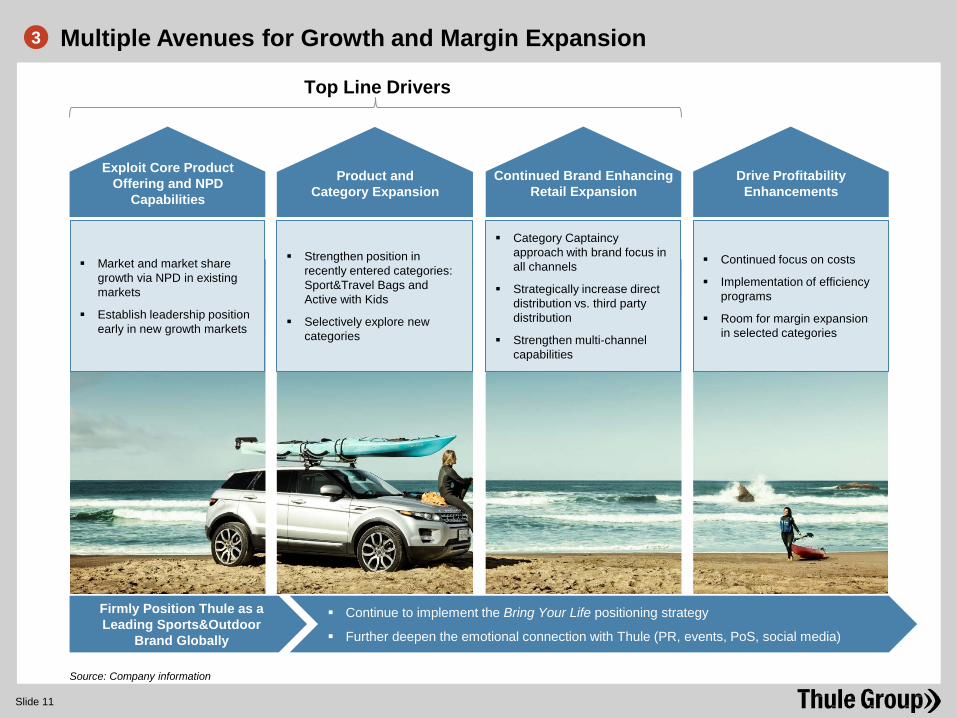

Multiple Avenues for Growth and Margin Expansion 3

Source: Company information

Drive Profitability Enhancements

Continued Brand Enhancing Retail Expansion

Exploit Core Product Offering and NPD

Capabilities

Market and market share growth via NPD in existing markets

Establish leadership position early in new growth markets

Continued focus on costs

Implementation of efficiency programs

Room for margin expansion in selected categories

Firmly Position Thule as a Leading Sports&Outdoor

Brand Globally

Continue to implement the Bring Your Life positioning strategy

Further deepen the emotional connection with Thule (PR, events, PoS, social media)

Product and Category Expansion

Strengthen position in recently entered categories: Sport&Travel Bags and Active with Kids

Selectively explore new categories

Category Captaincy approach with brand focus in all channels

Strategically increase direct distribution vs. third party distribution

Strengthen multi-channel capabilities

Top Line Drivers

Slide 12

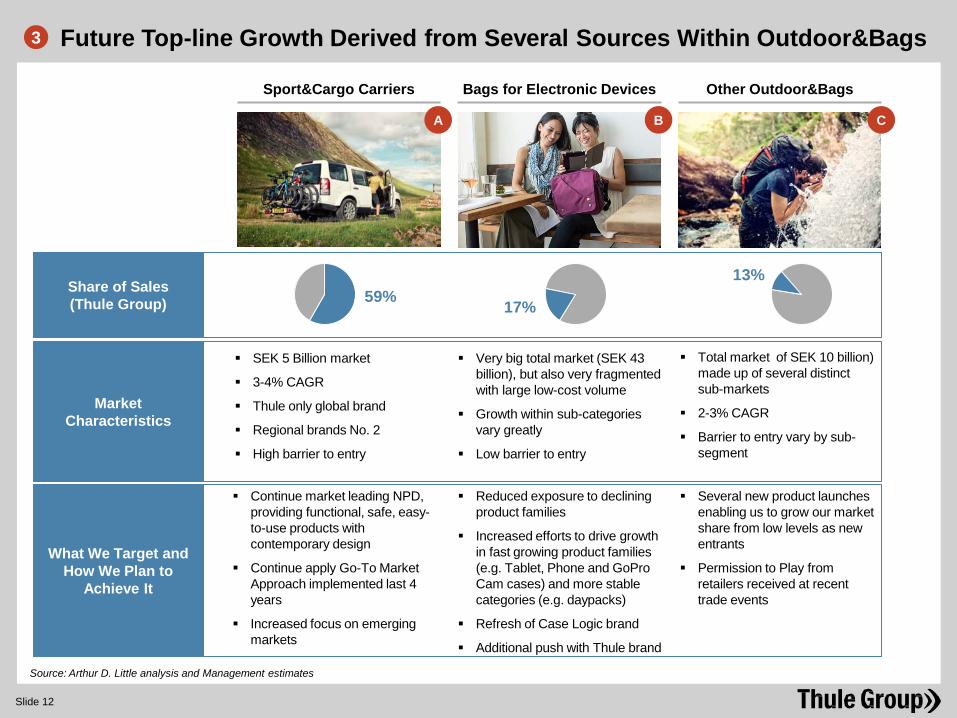

Sport&Cargo Carriers Bags for Electronic Devices Other Outdoor&Bags

Continue market leading NPD, providing functional, safe, easy-to-use products with contemporary design

Continue apply Go-To Market Approach implemented last 4 years

Increased focus on emerging markets

Several new product launches enabling us to grow our market share from low levels as new entrants

Permission to Play from retailers received at recent trade events

Share of Sales (Thule Group)

What We Target and How We Plan to

Achieve It

59% 17%

13%

Source: Arthur D. Little analysis and Management estimates

Market Characteristics

Reduced exposure to declining product families

Increased efforts to drive growth in fast growing product families (e.g. Tablet, Phone and GoPro Cam cases) and more stable categories (e.g. daypacks)

Refresh of Case Logic brand

Additional push with Thule brand

A B C

Future Top-line Growth Derived from Several Sources Within Outdoor&Bags 3

SEK 5 Billion market

3-4% CAGR

Thule only global brand

Regional brands No. 2

High barrier to entry

Very big total market (SEK 43 billion), but also very fragmented with large low-cost volume

Growth within sub-categories vary greatly

Low barrier to entry

Total market of SEK 10 billion) made up of several distinct sub-markets

2-3% CAGR

Barrier to entry vary by sub-segment

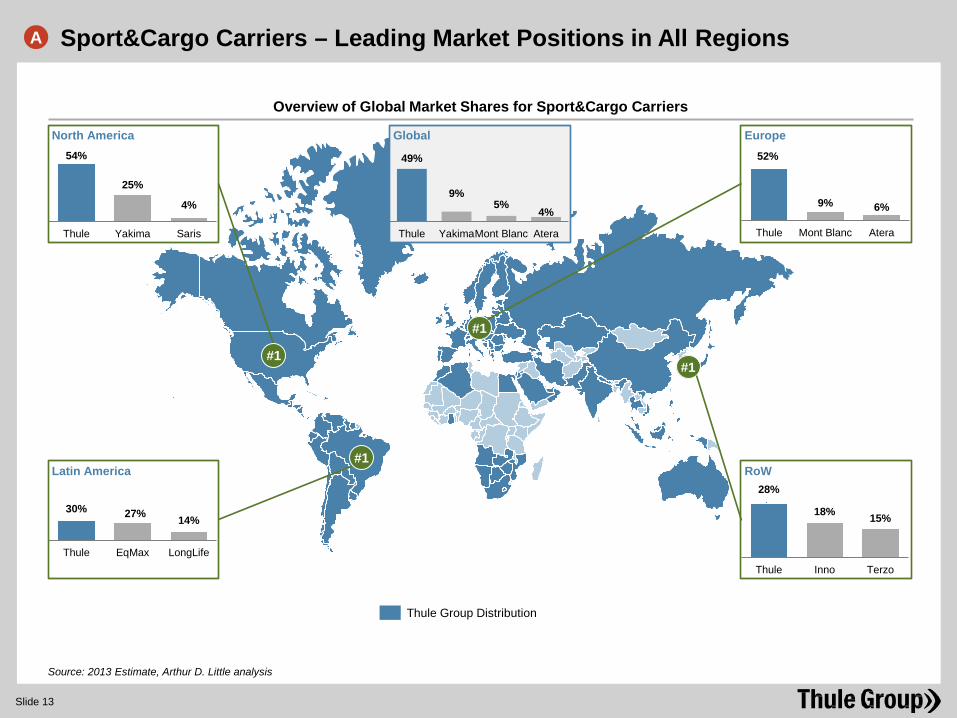

Slide 13

Source: 2013 Estimate, Arthur D. Little analysis

#1

#1

54%

25%

4%

Thule Yakima Saris

North America

Overview of Global Market Shares for Sport&Cargo Carriers

Thule Group Distribution

#1

#1

30% 27% 14%

Thule EqMax LongLife

Latin America

52%

9% 6%

Thule Mont Blanc Atera

Europe

28%

18% 15%

Thule Inno Terzo

RoW

49%

9% 5%

4%

Thule YakimaMont Blanc Atera

Global

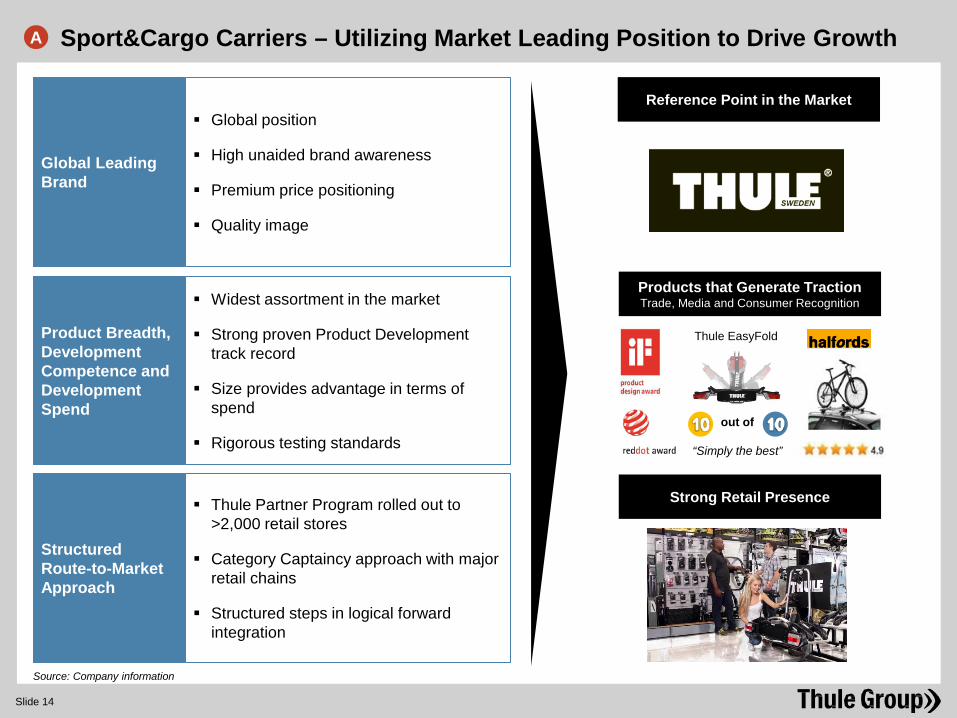

Sport&Cargo Carriers – Leading Market Positions in All Regions A

Slide 14

Widest assortment in the market

Strong proven Product Development track record

Size provides advantage in terms of spend

Rigorous testing standards

Products that Generate Traction Trade, Media and Consumer Recognition

Reference Point in the Market

Strong Retail Presence

Thule EasyFold

“Simply the best”

out of

Product Breadth, Development Competence and Development Spend

Global Leading Brand

Global position

High unaided brand awareness

Premium price positioning

Quality image

Source: Company information

Thule Partner Program rolled out to >2,000 retail stores

Category Captaincy approach with major retail chains

Structured steps in logical forward integration

Structured Route-to-Market Approach

Sport&Cargo Carriers – Utilizing Market Leading Position to Drive Growth A

Slide 15

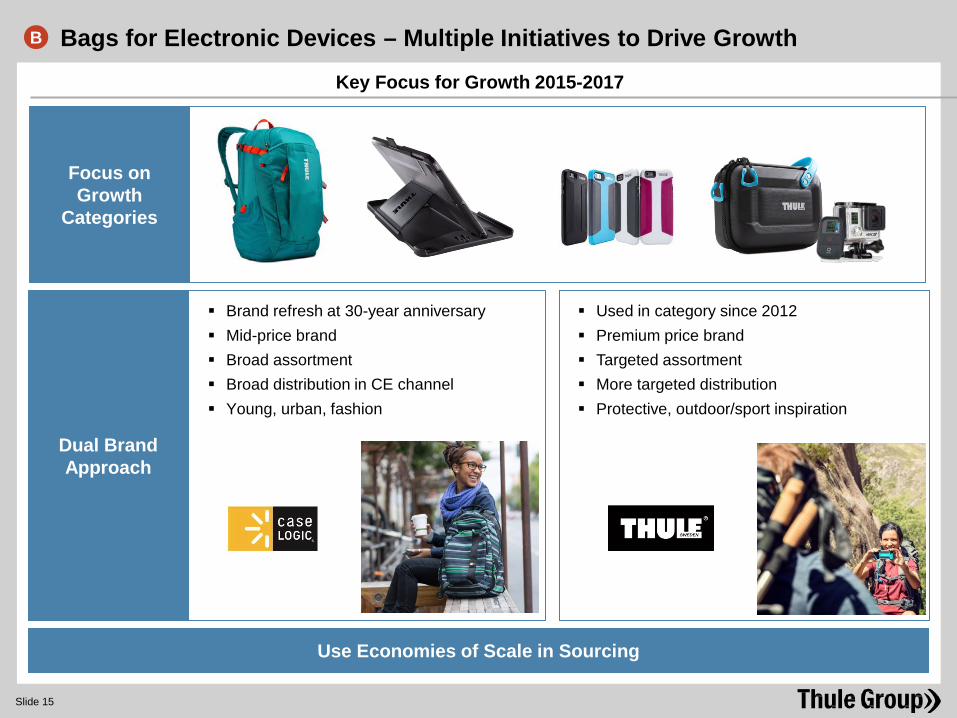

Bags for Electronic Devices – Multiple Initiatives to Drive Growth B

Key Focus for Growth 2015-2017

Dual Brand Approach

Use Economies of Scale in Sourcing

Focus on Growth

Categories

Brand refresh at 30-year anniversary Mid-price brand Broad assortment Broad distribution in CE channel Young, urban, fashion

Used in category since 2012 Premium price brand Targeted assortment More targeted distribution Protective, outdoor/sport inspiration

Slide 16

Source: Company information

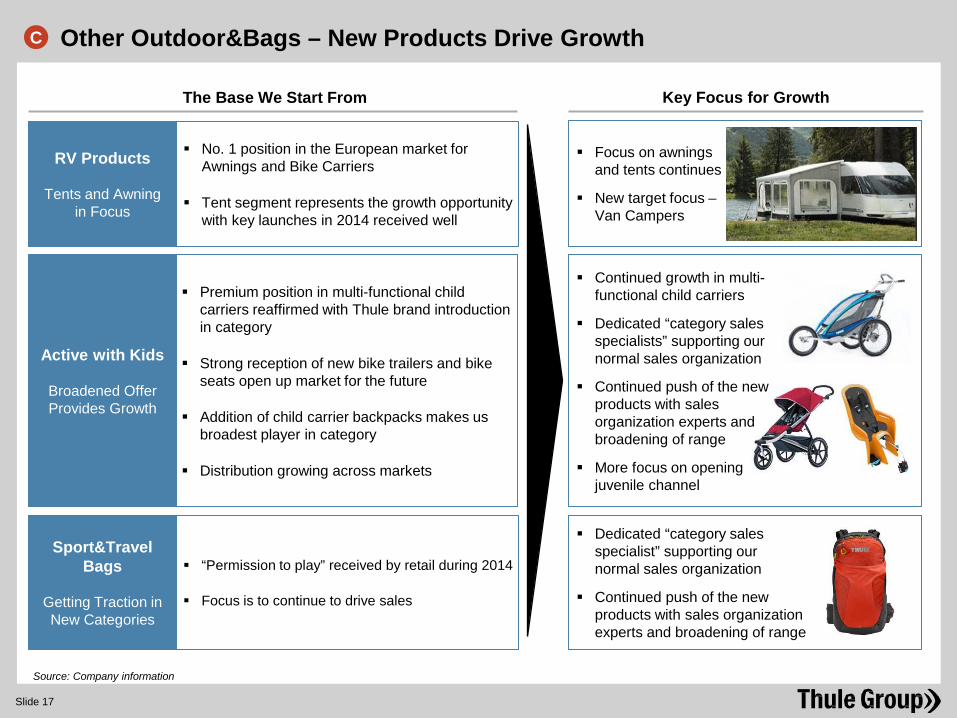

Other Outdoor&Bags – Broad New Product Expansions 2014-2015 C

Slide 17

Key Focus for Growth

Active with Kids

Broadened Offer Provides Growth

Sport&Travel Bags

Getting Traction in New Categories

The Base We Start From

Premium position in multi-functional child carriers reaffirmed with Thule brand introduction in category

Strong reception of new bike trailers and bike seats open up market for the future

Addition of child carrier backpacks makes us broadest player in category

Distribution growing across markets

“Permission to play” received by retail during 2014

Focus is to continue to drive sales

RV Products

Tents and Awning in Focus

No. 1 position in the European market for Awnings and Bike Carriers

Tent segment represents the growth opportunity with key launches in 2014 received well

Dedicated “category sales specialist” supporting our normal sales organization

Continued push of the new products with sales organization experts and broadening of range

Continued growth in multi- functional child carriers

Dedicated “category sales specialists” supporting our normal sales organization

Continued push of the new products with sales organization experts and broadening of range

More focus on opening juvenile channel

Focus on awnings and tents continues

New target focus – Van Campers

Source: Company information

C Other Outdoor&Bags – New Products Drive Growth

2014 Results

Q4 2014 Highlights – Mild and late winter hurts Snow Chain sales

Slide 19 Thule Group – Year-end Q4 2014 Results Update Feb 12, 2015 Slide 19

Net sales1 of SEK 976m (924) Outdoor&Bags +11,4% (+1.9% excluding currency effects) Specialty -15,9% (-22.5% excluding currency effects), due to late winter affecting snow chain sales

Underlying EBIT1 of SEK 37m (45) Specialty Segment EBIT reduced by SEK 22m to SEK 12m (34) Higher SG&A expenses vs. PY in the period in Outdoor&Bags, related to product development and launch preparation

cost for new products categories that will be available in retail in first half of 2015

Items affecting comparability of SEK -52m (-10)

Net income1 of SEK -100m (-52)

Earnings per share1 of SEK -1.11 (-0.62)

Cash flow from operating activities2 was SEK -77m (106)

Thule Group AB (publ) was stock-listed on Nasdaq Stockholm on November 26

New 5-year financing structure in place

New Eastern European Distribution Centre finalized in the quarter

Thule Group chosen as Vendor of the Year in Action Sports from World’s largest Outdoor Retailer (REI)

Thule chosen as Swedish Brand of the Year by Swedish Sport&Outdoor Retailer Association

1 Pertains to continuing operations, excluding operations discontinued during 2014. Correspondingly, the comparison periods have been divided into continuing and discontinued operations.

2 Pertains to total operations, meaning both continuing and discontinued operations.

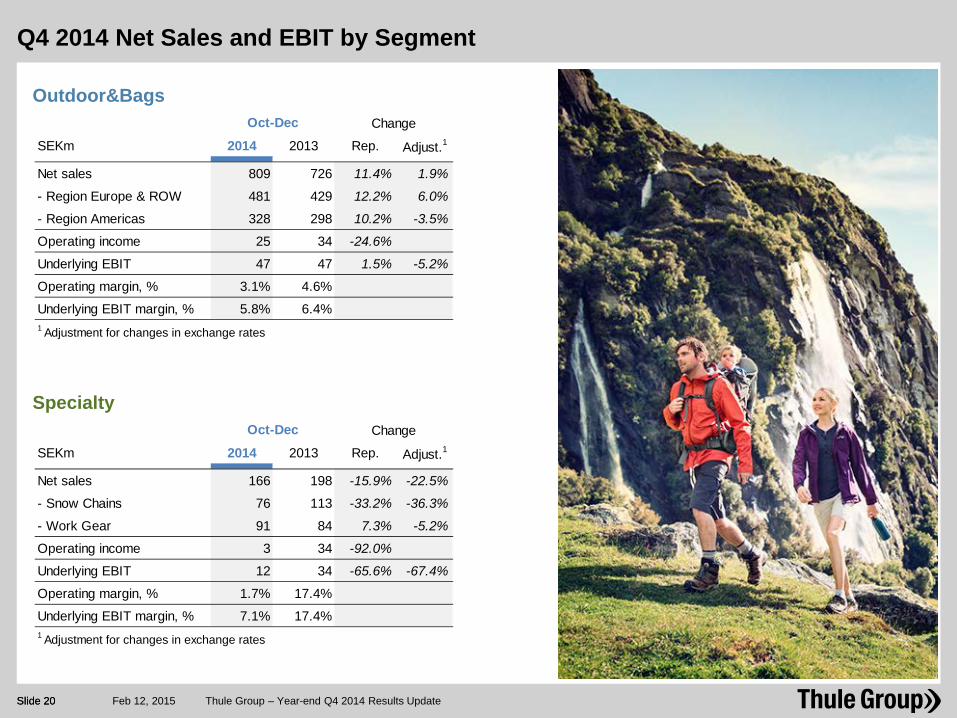

SEKm 2014 2013 Rep. Adjust.1

Net sales 809 726 11.4% 1.9%

- Region Europe & ROW 481 429 12.2% 6.0%

- Region Americas 328 298 10.2% -3.5%

Operating income 25 34 -24.6%

Underlying EBIT 47 47 1.5% -5.2%

Operating margin, % 3.1% 4.6%

Underlying EBIT margin, % 5.8% 6.4%1 Adjustment for changes in exchange rates

Oct-Dec Change

Slide 20

Q4 2014 Net Sales and EBIT by Segment

Thule Group – Year-end Q4 2014 Results Update Feb 12, 2015 Slide 20

Specialty

Outdoor&Bags

SEKm 2014 2013 Rep. Adjust.1

Net sales 166 198 -15.9% -22.5%

- Snow Chains 76 113 -33.2% -36.3%

- Work Gear 91 84 7.3% -5.2%

Operating income 3 34 -92.0%

Underlying EBIT 12 34 -65.6% -67.4%

Operating margin, % 1.7% 17.4%

Underlying EBIT margin, % 7.1% 17.4%1 Adjustment for changes in exchange rates

Oct-Dec Change

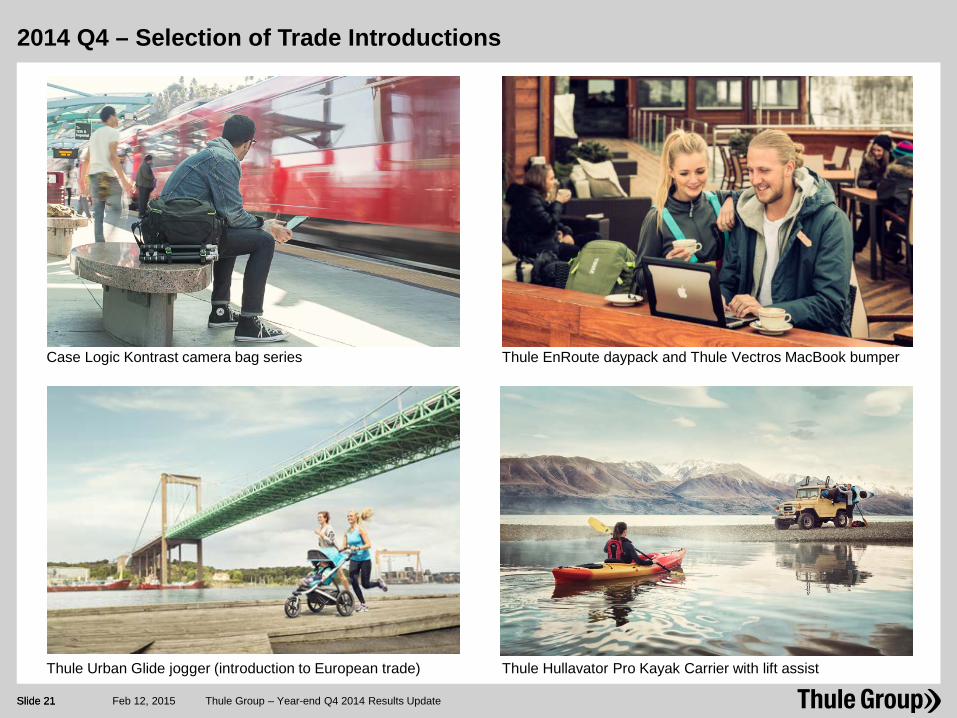

2014 Q4 – Selection of Trade Introductions

Slide 21 Thule Group – Year-end Q4 2014 Results Update Feb 12, 2015 Slide 21

Thule Urban Glide jogger (introduction to European trade) Thule Hullavator Pro Kayak Carrier with lift assist

Case Logic Kontrast camera bag series Thule EnRoute daypack and Thule Vectros MacBook bumper

2014 Full Year Highlights – Outdoor&Bags Segment drives profitable growth

Slide 22 Thule Group – Year-end Q4 2014 Results Update Feb 12, 2015 Slide 22

Net sales1 of SEK 4,693m (4,331) Outdoor&Bags +10.0% (+5.1% excluding currency effects) Specialty -3,8% (-8.4% excluding currency effects)

Underlying EBIT1 of SEK 686m (588)

Underlying EBIT-Margin1 of 14.6 percent (13.6)

Net Income1 of SEK 199m (299)

Earnings per share1 of SEK 2.32 (3.54)

Cash flow from operating activities2 was SEK 355m (390)

Operational cashflow1 in 2014 SEK 637m

Cash conversion1 of LTM underlying EBITDA of 85% (80%)

Net debt / Underlying EBITDA decreased to 3.4x (5.4x)

Dividend of SEK 2.00 per share proposed by the Board

1 Pertains to continuing operations, excluding operations discontinued during 2014. Correspondingly, the comparison periods have been divided into continuing and discontinued operations.

2 Pertains to total operations, meaning both continuing and discontinued operations

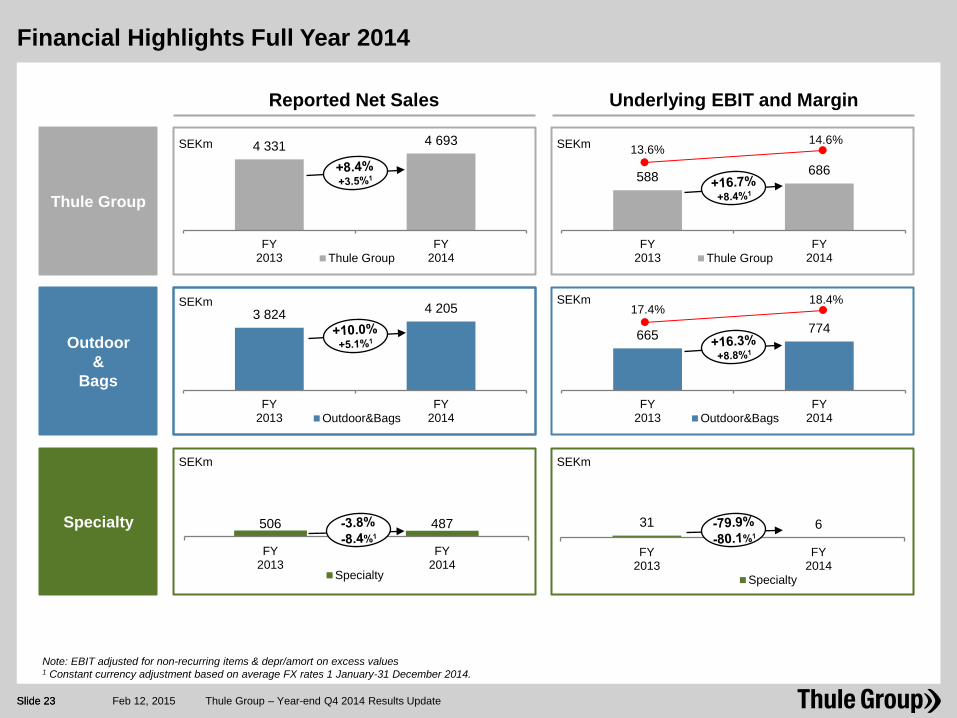

3 824 4 205

FY2013

FY2014Outdoor&Bags

4 331 4 693

FY2013

FY2014Thule Group

Slide 23

Note: EBIT adjusted for non-recurring items & depr/amort on excess values 1 Constant currency adjustment based on average FX rates 1 January-31 December 2014.

665 774

FY2013

FY2014Outdoor&Bags

Reported Net Sales

Outdoor &

Bags

Specialty

Underlying EBIT and Margin

SEKm SEKm

588 686

FY2013

FY2014Thule Group

Thule Group

SEKm SEKm

31 6

FY2013

FY2014

Specialty

O&B Americas

SEKm SEKm

506 487

FY2013

FY2014

Specialty

Financial Highlights Full Year 2014

Thule Group – Year-end Q4 2014 Results Update Feb 12, 2015

13.6% 14.6%

17.4% 18.4%

Slide 23

Source: Company information

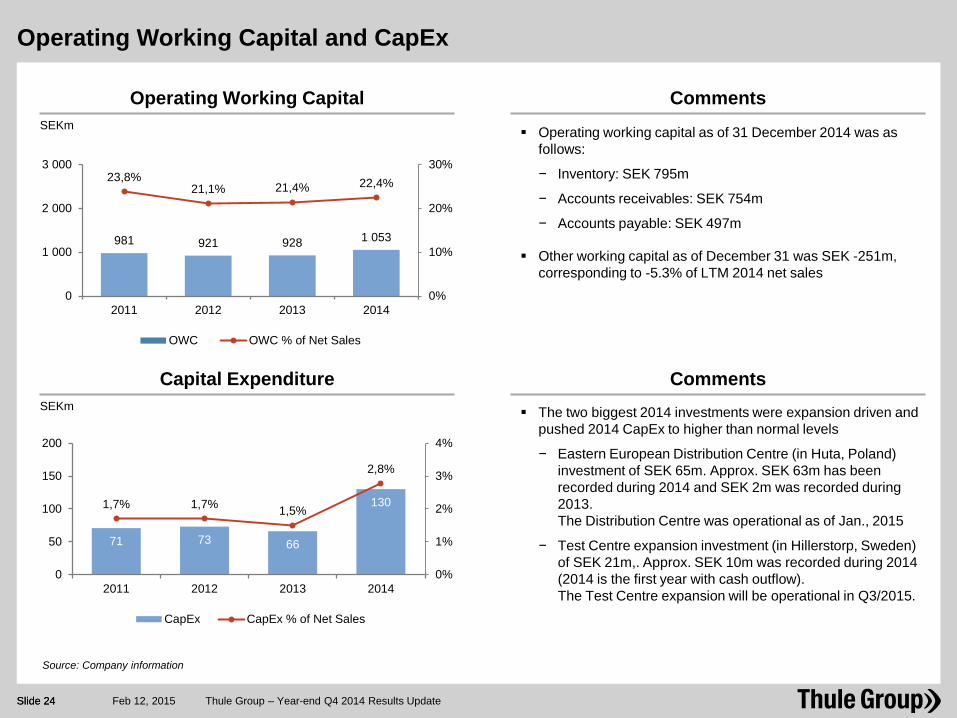

Operating Working Capital and CapEx

Operating Working Capital SEKm

Capital Expenditure

71 73 66

130 1,7% 1,7% 1,5%

2,8%

0%

1%

2%

3%

4%

0

50

100

150

200

2011 2012 2013 2014

CapEx CapEx % of Net Sales

SEKm

Comments

Operating working capital as of 31 December 2014 was as follows:

− Inventory: SEK 795m

− Accounts receivables: SEK 754m

− Accounts payable: SEK 497m

Other working capital as of December 31 was SEK -251m, corresponding to -5.3% of LTM 2014 net sales

Comments The two biggest 2014 investments were expansion driven and

pushed 2014 CapEx to higher than normal levels

− Eastern European Distribution Centre (in Huta, Poland) investment of SEK 65m. Approx. SEK 63m has been recorded during 2014 and SEK 2m was recorded during 2013. The Distribution Centre was operational as of Jan., 2015

− Test Centre expansion investment (in Hillerstorp, Sweden) of SEK 21m,. Approx. SEK 10m was recorded during 2014 (2014 is the first year with cash outflow). The Test Centre expansion will be operational in Q3/2015.

981 921 928 1 053

23,8% 21,1% 21,4% 22,4%

0%

10%

20%

30%

0

1 000

2 000

3 000

2011 2012 2013 2014

OWC OWC % of Net Sales

Slide 24 Thule Group – Year-end Q4 2014 Results Update Feb 12, 2015 Slide 24

Source: Company information

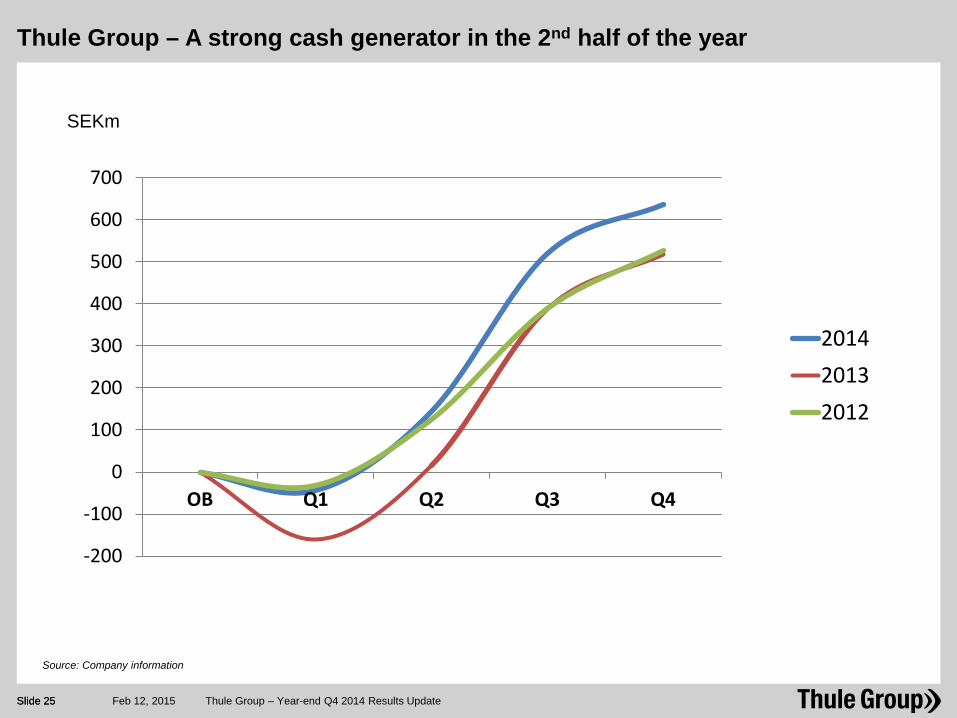

Thule Group – A strong cash generator in the 2nd half of the year

Slide 25 Thule Group – Year-end Q4 2014 Results Update Feb 12, 2015 Slide 25

SEKm

-200

-100

0

100

200

300

400

500

600

700

OB Q1 Q2 Q3 Q4

201420132012

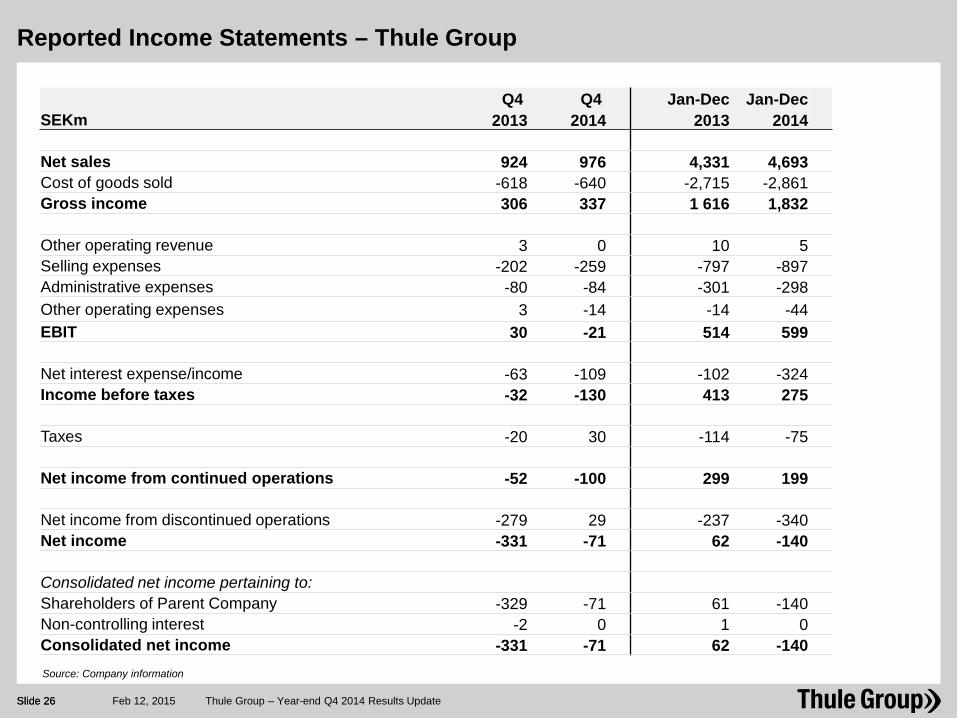

Reported Income Statements – Thule Group

Q4 Q4 Jan-Dec Jan-Dec SEKm 2013 2014 2013 2014 Net sales 924 976 4,331 4,693 Cost of goods sold -618 -640 -2,715 -2,861 Gross income 306 337 1 616 1,832 Other operating revenue 3 0 10 5 Selling expenses -202 -259 -797 -897 Administrative expenses -80 -84 -301 -298 Other operating expenses 3 -14 -14 -44 EBIT 30 -21 514 599 Net interest expense/income -63 -109 -102 -324 Income before taxes -32 -130 413 275 Taxes -20 30 -114 -75 Net income from continued operations -52 -100 299 199 Net income from discontinued operations -279 29 -237 -340 Net income -331 -71 62 -140 Consolidated net income pertaining to: Shareholders of Parent Company -329 -71 61 -140 Non-controlling interest -2 0 1 0 Consolidated net income -331 -71 62 -140 Source: Company information

Slide 26 Thule Group – Year-end Q4 2014 Results Update Feb 12, 2015 Slide 26

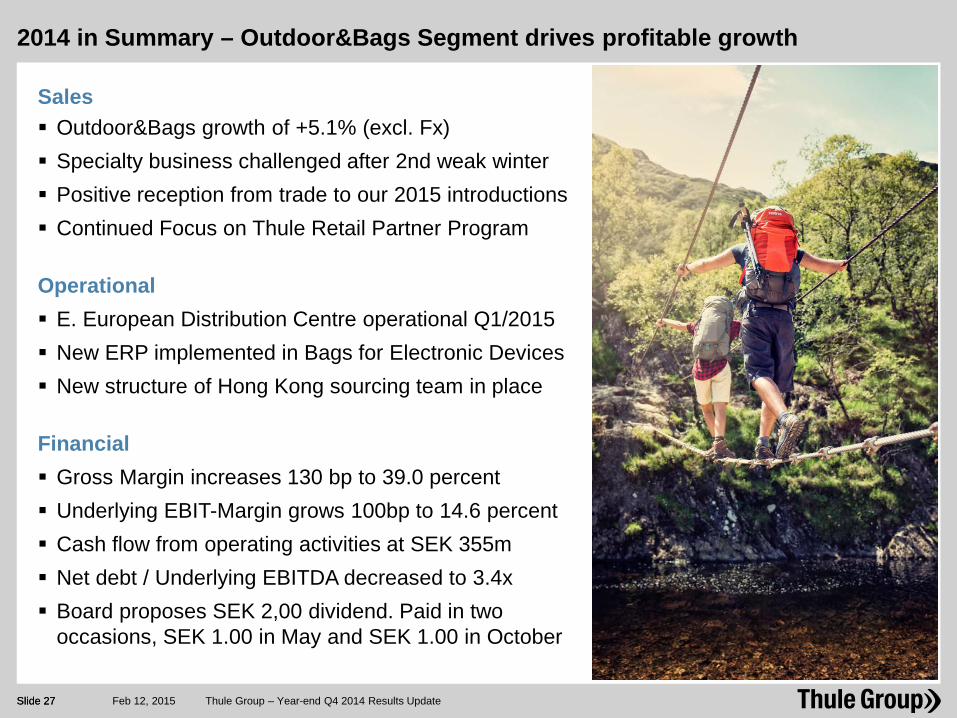

2014 in Summary – Outdoor&Bags Segment drives profitable growth

Slide 27 Thule Group – Year-end Q4 2014 Results Update Feb 12, 2015 Slide 27

Sales Outdoor&Bags growth of +5.1% (excl. Fx) Specialty business challenged after 2nd weak winter Positive reception from trade to our 2015 introductions Continued Focus on Thule Retail Partner Program

Operational E. European Distribution Centre operational Q1/2015 New ERP implemented in Bags for Electronic Devices New structure of Hong Kong sourcing team in place

Financial Gross Margin increases 130 bp to 39.0 percent Underlying EBIT-Margin grows 100bp to 14.6 percent Cash flow from operating activities at SEK 355m Net debt / Underlying EBITDA decreased to 3.4x Board proposes SEK 2,00 dividend. Paid in two

occasions, SEK 1.00 in May and SEK 1.00 in October

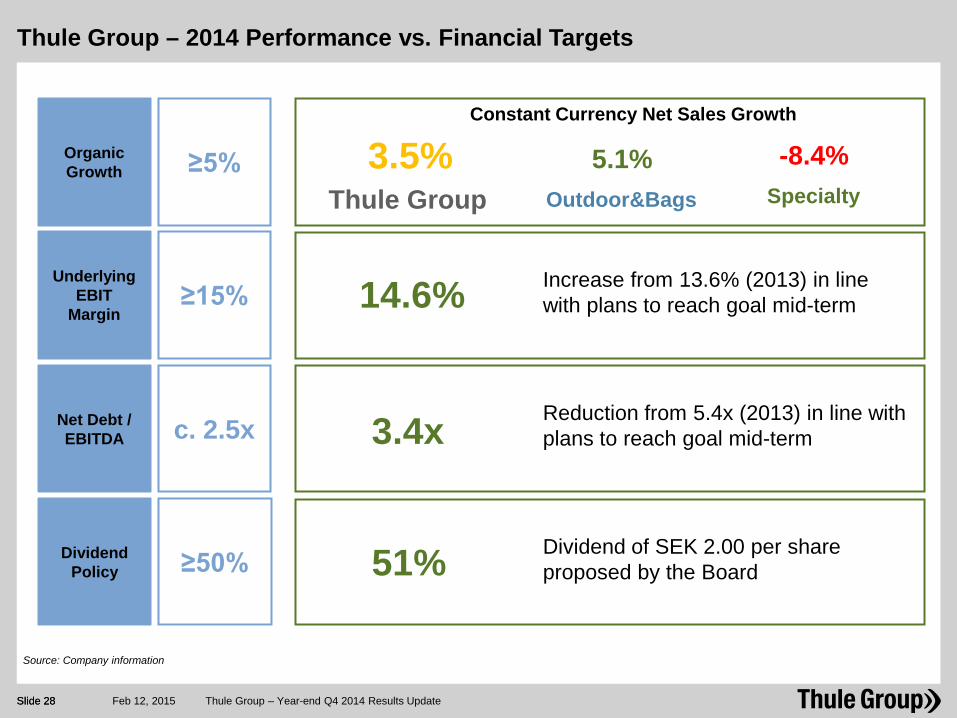

Thule Group – 2014 Performance vs. Financial Targets

Slide 28 Thule Group – Year-end Q4 2014 Results Update Feb 12, 2015 Slide 28

Source: Company information

Dividend Policy ≥50%

Organic Growth ≥5%

UnderlyingEBIT

Margin ≥15%

Net Debt / EBITDA c. 2.5x

Constant Currency Net Sales Growth

3.5% Thule Group

5.1% Outdoor&Bags

-8.4% Specialty

14.6%

3.4x Reduction from 5.4x (2013) in line with plans to reach goal mid-term

Increase from 13.6% (2013) in line with plans to reach goal mid-term

51% Dividend of SEK 2.00 per share proposed by the Board

Focus 2015 is to Capture Profitable Growth with Investments made in 2013-14

Slide 29 Thule Group – Year-end Q4 2014 Results Update Feb 12, 2015 Slide 29

2015 Focus Continue to Drive Profitable Organic Growth

in Outdoor&Bags Segment Continued strong performance in Sport&Cargo Roll-out of new Active with Kids products portfolio Roll-out of Technical Backpacks Get growth Bags for Electronic Devices Continue to manage Specialty cost efficiently Further steps in lean set-up in Snow Chians Production efficiencies in Work Gear Capture gains from Operational Efficiency Ramp-up of Eastern European distribution centre Closing of W. European bags distribution centre Capture gains from more efficient supply chain

Slide 30

Q&A

Disclaimer

This presentation has been prepared by Thule Group AB (publ) (the “Company”) solely for use at this presentation and is furnished to you solely for your information and may not be reproduced or redistributed, in whole or in part, to any other person. The presentation does not constitute an invitation or offer to acquire, purchase or subscribe for securities. By attending the meeting where this presentation is made, or by reading the presentation slides, you agree to be bound by the following limitations.

Statements in this presentation, which are not historical facts, such as expectations, anticipations, beliefs and estimates, are forward-looking statements within the meaning of the United States Private Securities Litigation Reform Act of 1995. Such statements involve risks and uncertainties which may cause actual results to materially differ from those expressed in such forward-looking statements.

This presentation may contain various forward-looking statements that reflect management’s current views with respect to future events and financial and operational performance. The words “believe,” “expect,” “anticipate,” “intend,” “may,” “plan,” “estimate,” “should,” “could,” “aim,” “target,” “might,” or, in each case, their negative, or similar expressions identify certain of these forward-looking statements. Others can be identified from the context in which the statements are made. These forward-looking statements involve known and unknown risks, uncertainties and other factors, which are in some cases beyond the Company’s control and may cause actual results or performance to differ materially from those expressed or implied from such forward-looking statements. These risks include but are not limited to the Company’s ability to operate profitably, maintain its competitive position, to promote and improve its reputation and the awareness of the brands in its portfolio, to successfully operate its growth strategy and the impact of changes in pricing policies, political and regulatory developments in the markets in which the Company operates, and other risks.

The information and opinions contained in this document are provided as at the date of this presentation and are subject to change without notice.

No representation or warranty (expressed or implied) is made as to, and no reliance should be placed on, the fairness, accuracy or completeness of the information contained herein. Accordingly, none of the Company, or any of its principal shareholders or subsidiary undertakings or any of such person’s officers or employees accepts any liability whatsoever arising directly or indirectly from the use of this document.

www.thulegroup.com

Top Related