![Index [] · Vishnu Shloka - Shanthakaram Bhujagashayanam 4 Sri Venkatesa Suprabatham 5 Sri Venkatesa Stotram 15 Sri Venkatesa Prapti 18 Sri Venkatesa Mangalashasanam 24 Sri Venkatesa](https://static.fdocuments.net/doc/165x107/5d6795b488c993306c8b64db/index-vishnu-shloka-shanthakaram-bhujagashayanam-4-sri-venkatesa-suprabatham.jpg)

![INDEX [clists.nic.in]clists.nic.in/ddir/PDFCauselists/patna/2016/Apr/...Sri Hari Shankar Singh, A.R. Criminal Disposal Section Sri Akhilesh Kumar Singh, A.R. Cr. Appeal Sri Rajesh](https://static.fdocuments.net/doc/165x107/5f1b9acde142b31d530c36e2/index-sri-hari-shankar-singh-ar-criminal-disposal-section-sri-akhilesh.jpg)

Languages

Pages

Legal

Presenter

Date

Results of the 2013 SRI Index review Corli le Roux, Head of SRI Index and Sustainability

Makhiba Mollo, SRI Index Associate

Overview of timeline

2

Initial public research commenced during June 2013

Company preliminary profiles sent out in three tranches between July and

September

• Companies given two weeks to respond to profiles

• USB responsible for researching most companies

Engagement with controversial issues and borderline cases during September

and November 2013

Results approved by Advisory Committee on 19 November 2013

Individual results distributed on 26 November 2013

Research methodology – criteria overview

3

Covers four areas of measurement

• Environment

• Society

• Governance and related sustainability concerns

• Climate change

Entry level threshold for each of the four areas of measurement

Environmental impact classification

• Aligned to sector’s overall environmental impacts relative to economic contribution of the relevant

activity to company revenue

• Currently no impact classification for social, governance or climate change

Research methodology – criteria overview (2)

4

No new indicators this year

However, two significant moves in evolution of index

• Only publicly available information considered

• Entire FTSE/JSE All Share Index automatically assessed

Experience of the process

5

157 companies assessed in 2013 (108 in 2012)

• 105 of these submitted detailed profile/survey responses – 66.9% of total (84% in 2012)

– Represents high level of engagement – increases robustness of data collection process

– Small caps with few employees find difficulty in responding

• Top 40 best responders – 92.5% of Top 40 companies responded with additional information

(83% in 2012)

Overview of results

6

46% of total assessed universe has qualified (70% in 2012)

5 companies qualifying for the first time

• 3 of these assessed for the first time

• 2 previously assessed but first time to qualify

Number of constituents in 2013:

72

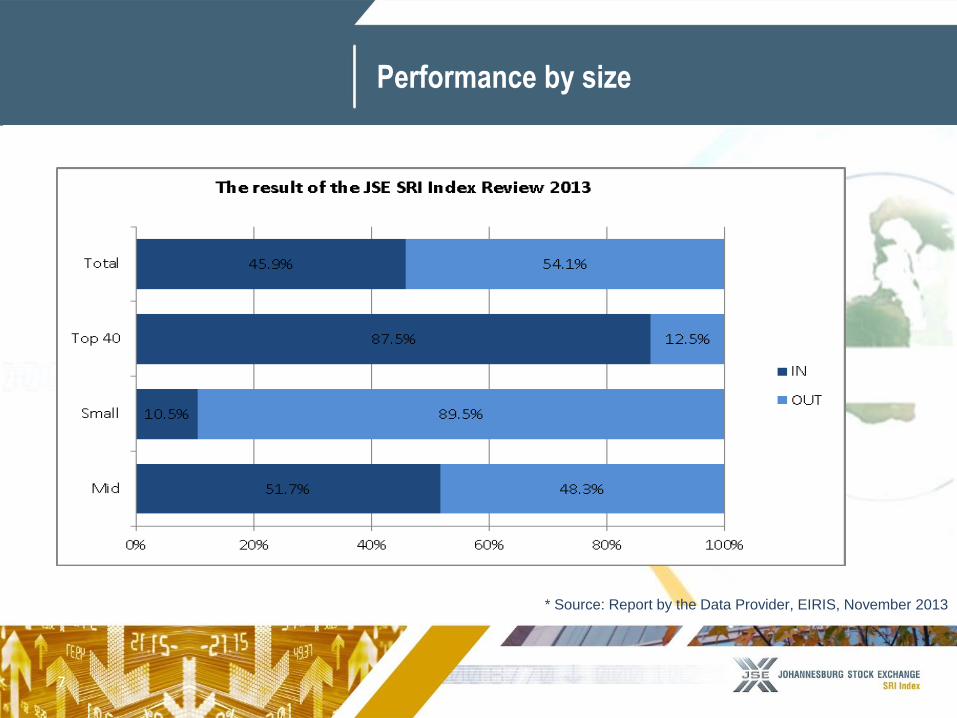

Performance by size

7

* Source: Report by the Data Provider, EIRIS, November 2013

8

31 32

34 34

36

34

36 36 36 35

17

13

17 18

23

30

33

31

33

31

3

4

7

5

4 4

5

7 7

6

0

5

10

15

20

25

30

35

40

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013

Nu

mb

er o

f co

mp

anie

s

Year of assessment

Top 40

Mid Cap

Small Cap

Performance by size (2)

Sector performance

9

100% qualification by companies in life insurance sector (again)

Other strong sectors

• Mining

15 out of 19 qualified

Makes up 20.8% of total number of constituents

• General Industrials

83% qualified

• Banks

71.4% qualified

Individual research areas: Environment

10

65.6% of all assessed met environmental requirements in 2013

(79.6% in 2012)

• Full disclosure requirement a challenge, particularly for high impact and first timers

Medium impact companies do best in policy, need to improve management

and reporting

Low impact category still strong in reporting

• Lower threshold

High impact companies did best in environmental reporting this year, but

need to address disclosure of management systems

Individual research areas: Society

11

65% of all assessed met social requirements in 2013 (81.5% in 2012)

– Decline due to larger universe and public requirement

Strong themes

– Stakeholder engagement, Community relations

– Demonstrates awareness of external / societal expectations and willingness to engage

– Disclosures around health & safety, BEE and equal opportunities also sufficient

Challenging themes

– Decline in performance across training & development, employee relations, HIV/Aids

– Attributable to public requirement – areas generally addressed, but not sufficiently

available in public domain

– Still room for increased transparency

Individual research areas:

Governance & related sustainability concerns

12

90.4% of all assessed met governance requirements in 2013 (98% in 2012)

Strongest performance area

• Attributed to influence of King III and integrated reporting focus

• Improvement in Board practice

• Decline in other areas –

o Again due to public requirement – areas being addressed but not sufficiently disclosed

Strong areas

• Business value & risk management remains strong

• Broader economic issues

Governance reporting remains challenging area

• Especially for companies being assessed for the first time

Individual research areas: Climate Change

13

56.7% of all assessed met climate change entry level requirements in 2013

(75.9% in 2012)

• Decrease attributable to large number of new Small Cap companies

• Companies assessed last year show improvement

Strongest performance by Top 40 companies – 92.5% meeting entry level

Successful constituents

(in alphabetical order)

14

Advtech Barloworld Growth Point

Properties Liberty Holdings Northam Platinum Sanlam

AECI BHP Billiton Harmony Gold Mining

Company Lonmin plc Oceana Group Santam

African Bank

Investments

The Bidvest Group

Limited Intu Properties Massmart Holdings Old Mutual Sappi Limited

African Oxygen Business Connexion

Group Illovo Sugar

Mediclinic

International Pick n Pay Sasol

African Rainbow

Minerals

British American

Tobacco

Impala Platinum

Holdings Merafe Resources PPC Sibanye Gold

Allied Electronics

Corporation Discovery Holdings Imperial Holdings MMI Holdings Rainbow Chicken Standard Bank Group

Anglo American DRD Gold Investec Mondi Redefine Properties Steinhoff International

Anglo American

Platinum Exxaro Resources JD Group Mpact Remgro Sun International

AngloGold Ashanti FirstRand JSE Limited MTN Group Reunert Tongaat Hulett

ArcelorMittal South

Africa

The Foschini Group

Limited

KAP Industrial

Holdings Nampak RMB Holdings

Truworths

International

Aspen Pharmacare

Holdings Gold Fields Limited Kumba Iron Ore Nedbank

Royal Bafokeng

Platinum Vodacom Group

Barclays Africa Group Grindrod Lewis Group Ltd Netcare Limited SAB Miller plc Woolworths

International Holdings

Best performers

15

Companies that meet additional levels of performance

• All relevant core requirements in social and governance

• Independent chair

• Environmental best performer threshold

• All climate change indicators (except for “Trend data”)

Number of best performers in 2013:

6 Contraction in BP numbers due to requirement for reporting in the public

domain

• Mainly resulted from core indicators in social area not being disclosed

Best performers by size & impact

16

HEADLINE 2013

Top 40 4

Mid Cap 2

Small Cap 0

Total 6

IMPACT 2013

High 2

Medium 1

Low 3

Total 6

17

Best performers 2013

* In alphabetical order

Anglo American Platinum

18

Best performers 2013

* In alphabetical order

Illovo Sugar

19

Best performers 2013

* In alphabetical order

Netcare Limited

20

Best performers 2013

* In alphabetical order

Standard Bank

21

Best performers 2013

* In alphabetical order

Steinhoff International

22

Best performers 2013

* In alphabetical order

Vodacom Group

Quo vadis?

23

Strategy implementation begins in all earnest

• Review of criteria

• Addressing structural sector concerns

• Expanding data availability

• ESG Investor Briefing

Thank you

24

See you in 2014!

25

Advtech Barloworld Growth Point Properties Liberty Holdings Northam Platinum Sanlam

AECI BHP Billiton Harmony Gold Mining

Company Lonmin plc Oceana Group Santam

African Bank

Investments

The Bidvest Group

Limited Intu Properties Massmart Holdings Old Mutual Sappi Limited

African Oxygen Business Connexion

Group Illovo Sugar (BP) Mediclinic International Pick n Pay Sasol

African Rainbow

Minerals

British American

Tobacco

Impala Platinum

Holdings Merafe Resources PPC Sibanye Gold

Allied Electronics

Corporation Discovery Holdings Imperial Holdings MMI Holdings Rainbow Chicken

Standard Bank Group

(BP)

Anglo American DRD Gold Investec Mondi Redefine Properties Steinhoff International

(BP)

Anglo American

Platinum (BP) Exxaro Resources JD Group Mpact Remgro Sun International

AngloGold Ashanti FirstRand JSE Limited MTN Group Reunert Tongaat Hulett

ArcelorMittal South

Africa

The Foschini Group

Limited KAP Industrial Holdings Nampak RMB Holdings Truworths International

Aspen Pharmacare

Holdings Gold Fields Limited Kumba Iron Ore Nedbank

Royal Bafokeng

Platinum Vodacom Group (BP)

Barclays Africa Group Grindrod Lewis Group Ltd Netcare Limited (BP) SAB Miller plc Woolworths

International Holdings

Top Related