Languages

Pages

Legal

PROSPECTS OF RENEWABLE AND NON-RENEWABLE

ENERGY SOURCES IN SOUTH ASIAN ECONOMIES: AN

ANALYSIS

BY

SADIA ALI

Registration No: 2013-GCUF-05034

Thesis submitted in partial fulfillment of

the requirement for the degree of

DOCTOR OF PHILOSOPHY

IN

ECONOMICS

DEPARTMENT OF ECONOMICS

GOVERNMENT COLLEGE UNIVERSITY FAISALABAD

2017

ii

CERTIFICATE OF APPROVAL

This is to certify that the research work presented in this thesis, entitled, “Prospects of

Renewable and Non-Renewable Energy Sources in South Asian Economies: An Analysis”

was conducted by Mrs. Sadia Ali (Regd. No 2013-GCUF-05034) under the supervision of Dr.

Sofia Anwar.

iii

CERTIFICATE BY SUPERVISORY COMMITTEE

We certify that the contents and form of a thesis submitted by Miss Sadia Ali,

registration No. 2013-GCUF-05034 has been found satisfactory and in accordance with

the prescribed format. We recommend it to be processed for the evaluation by the

External Examiner for the award of the degree.

Supervisor

Co-Supervisor

Member of Supervisory Committee

Chairperson

Dean / Academic Coordinator

iv

AUTHORS DECLARATION

I Sadia Ali, Reg. No 2013-GCUF-05034, here by state that my Ph.D. thesis title

“Prospects of Renewable and Non-Renewable Energy Sources in South Asian

Economies: An Analysis” is my own work and has not been submitted previously by

me for taking any degree from Government College University, Faisalabad or anywhere

else in the country/ world. At any time if my statement is found to be incorrect even

after my graduate the university has the right to withdraw my Ph.D. degree.

v

PLAGIARISM UNDERTAKING

I solemnly declare that research work presented in the thesis titled “Prospects of

Renewable and Non-Renewable Energy Sources in South Asian Economies: An Analysis”

is solely my research work with no significant contribution from any other person. Small

contribution/help wherever taken has bees been duly acknowledged and that complete thesis

has been written by me.

I understand the zero-tolerance policy of the HEC and Government College University,

Faisalabad towards plagiarism. Therefore, as an author of the above titled thesis declare that no

portion of my thesis has been plagiarized and any material used as reference is properly

referred/cited.

I undertake that if l am found guilty of any formal plagiarism in the above titled thesis

even after award of Ph.D. degree, the University reserve the rights to withdraw/revoke my Ph.D.

degree and that HEC and the University has the right to publish my name on the

HBC/University Website on which names of students are placed who submitted plagiarized

thesis.

vi

DEDICATION

Dedicated to

“My Parents”

For Their Love, Encouragement and Prayers

“Muhammad Amir Javed”

For His Support and Believe in Richness of Learning

“Muhammad Husnain Amir, Muhammad Ali Amir and Zainab Amir”

For Their Love, Prayers and Made Me Keen for Learning

vii

ACKNOWLEDGEMENTS

First of all, I would praise the Almighty Allah, the Gracious and the Most Merciful, for

giving me the quality and inspiration to complete this examination.

I might want to thank my Supervisor, Dr. Sofia Anwar not just for her few astute

remarks concerning the bearing and the substance of this proposition, yet in addition

for her human state of mind and for being understanding. She prepared me how to make

inquiries and express my thoughts. She indicated me diverse approaches to approach

an exploration issue and the need to steady keeping in mind the end goal to achieve any

objective. She showed me how to buckle down. I sincerely value the time she has

committed to regulate my exploration.

I might want to formally recognize and thank various individuals, particularly my co-

supervisor, Dr. Samia Nasreen who empowered, supported and helped me through the

testing a very long time of my Ph. D examinations. Thanks to Dr. Muhammad Rizwan

Yasin for agreeing to serve on my committee. I am also thankful to Dr Muhammad

Sohail Amjad Makhdom for his encouragement and support during my PhD.

Last, yet not slightest, I thank my family: my parents, for giving me life in the first

place, for instructing, educating, support and consolation to seek my interests. My

husband, my siblings for tuning in to my protests and dissatisfactions, and for having

faith in me.

SADIA ALI

viii

TABLE OF CONTENTS

CERTIFICATE OF APPROVAL…………………………………………ii

CERTIFICATE BY SUPERVISORY COMMITTEE………………………..….......iii

AUTHORS DECLARATION…………………………………………....…………..iv

PLAGIARISM UNDERTAKING…………………….…………………………........v

DEDICATION………………………………………………………………………..vi

ACKNOWLEDGEMENTS…………………………………………………....….…vii

ACRONYMS AND ABREVIATIONS……………….…………………………....xxii

ABSTRACT………………………………………………………………………..xxiii

1. INTRODUCTION……………………….………………………………….………1

1.1 Research Motivation…………………………………………………………..…...8

1.2 Research objectives………………………………………………………….……..9

1.3 Research Contribution………………………………………………………..…..10

1.4 Research Structure………….…………………………………………………….10

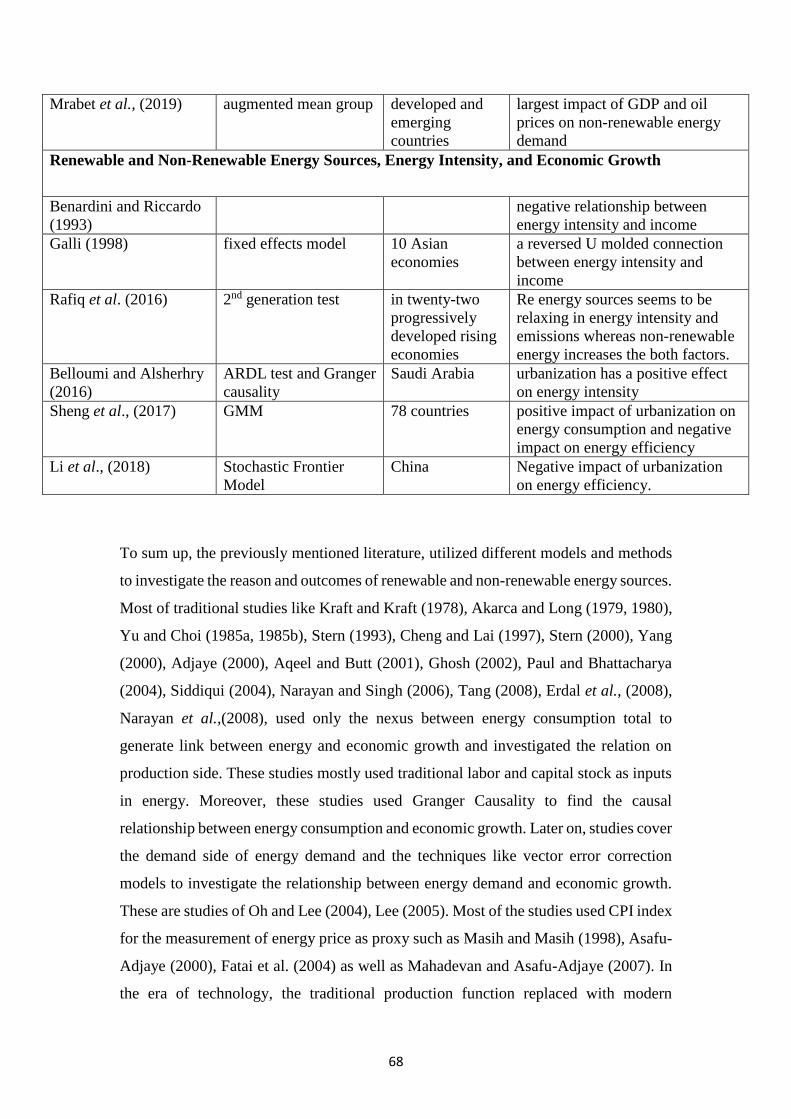

2. REVIEW OF LITERATURE………………………..…………………………….12

2.1 Empirical Literature.........................................................................................…...12

2.1.1 Renewable and nonrenewable energy and economic growth..…………………11

2.1.2 Renewable and nonrenewable energy consumption and environment

quality…………………………………………………………………………...……30

2.1.3 Demand for Renewable and nonrenewable energy…….…………...…………..38

2.1.4 Renewable and Non-Renewable Energy Sources, Energy Intensity, Economic

Growth………………………………………………………………………………..47

2.2 Theoretical Literature………………………………………………….…………51

2.2.1 Prospects and Potential of Renewable and Non-Renewable Energy

Sources………………………………………….……………………..…….…….....51

3. METHODOLOGY....…………..……………………………………………...71

ix

3.1 Data……………………………………………………………………….………71

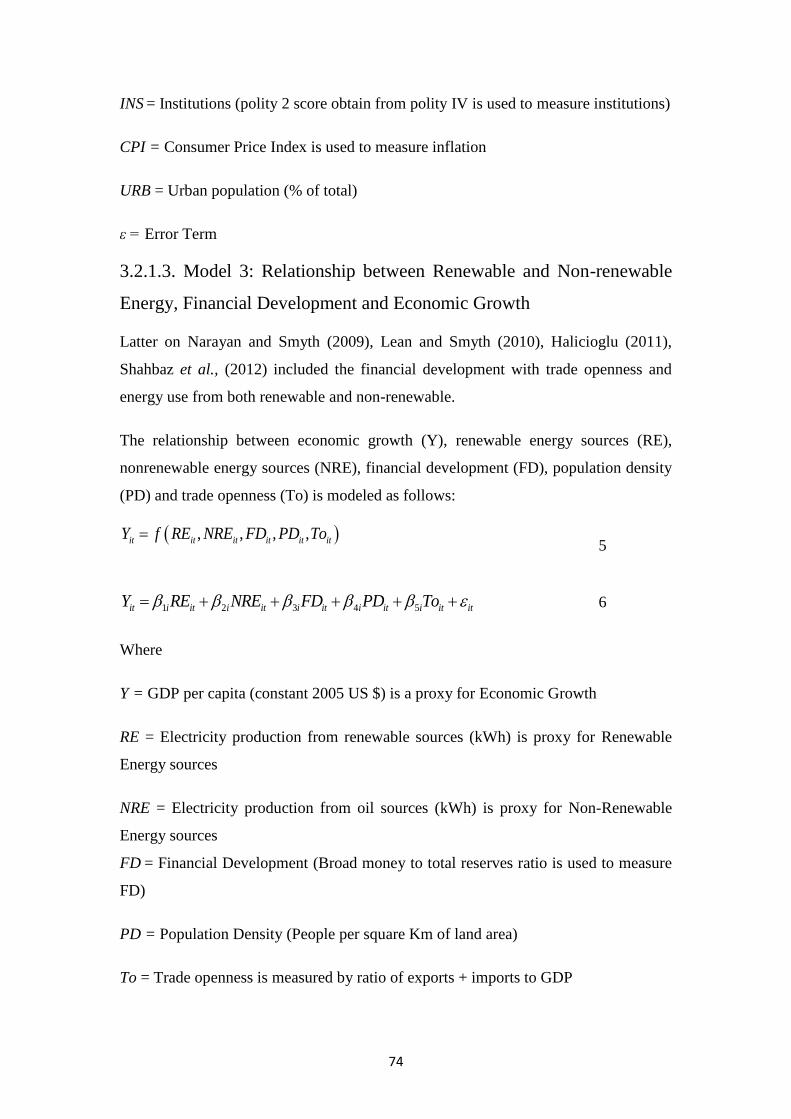

3.2 Model Specification……………………………………………………………....71

3.2.1 Renewable and nonrenewable energy with growth……..…..…………………..72

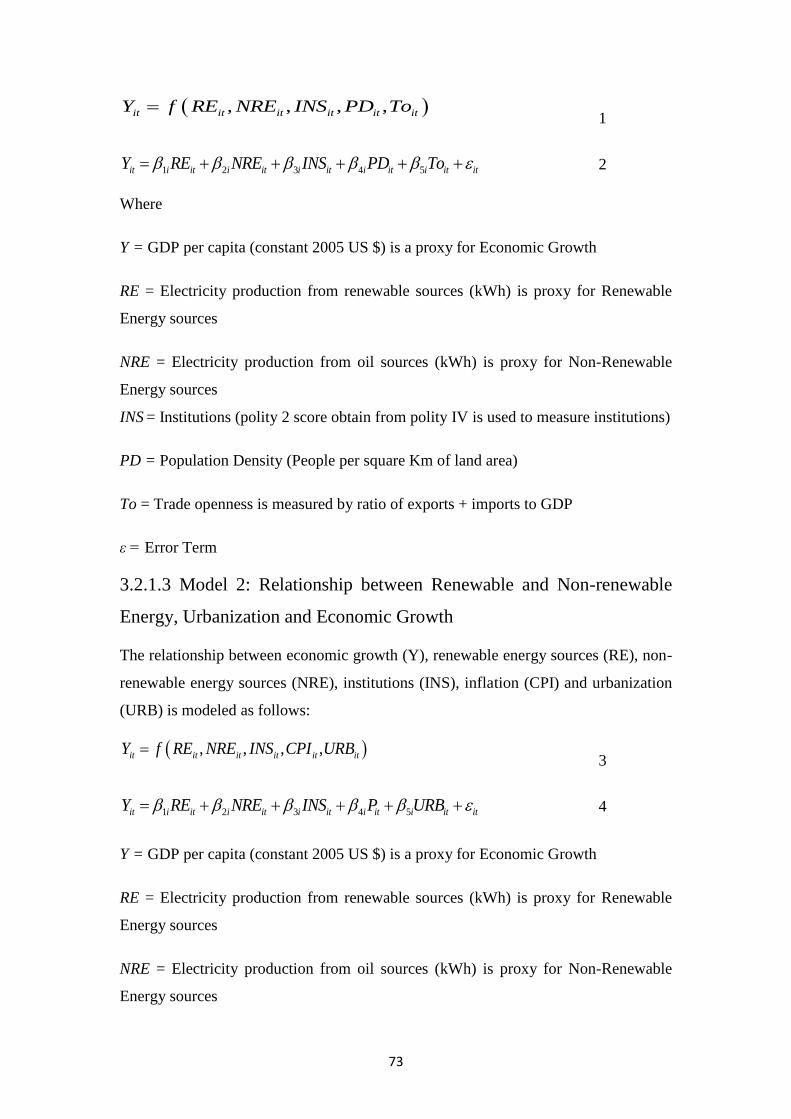

3.2.1.1 Model 1. Relationship between Renewable and Non-renewable Energy,

Institutions and Economic Growth …………………………………………..………72

3.2.1.2 Model 2: Relationship between Renewable and Non-renewable Energy,

Urbanization and Economic Growth…………..…………………………..………….73

3.2.1.3 Model 3: Relationship between Renewable and Non-renewable Energy,

Financial Development and Economic Growth ………………...….………………....74

3.2.1.4 Data Sources…...…………...….…………………………………..…………75

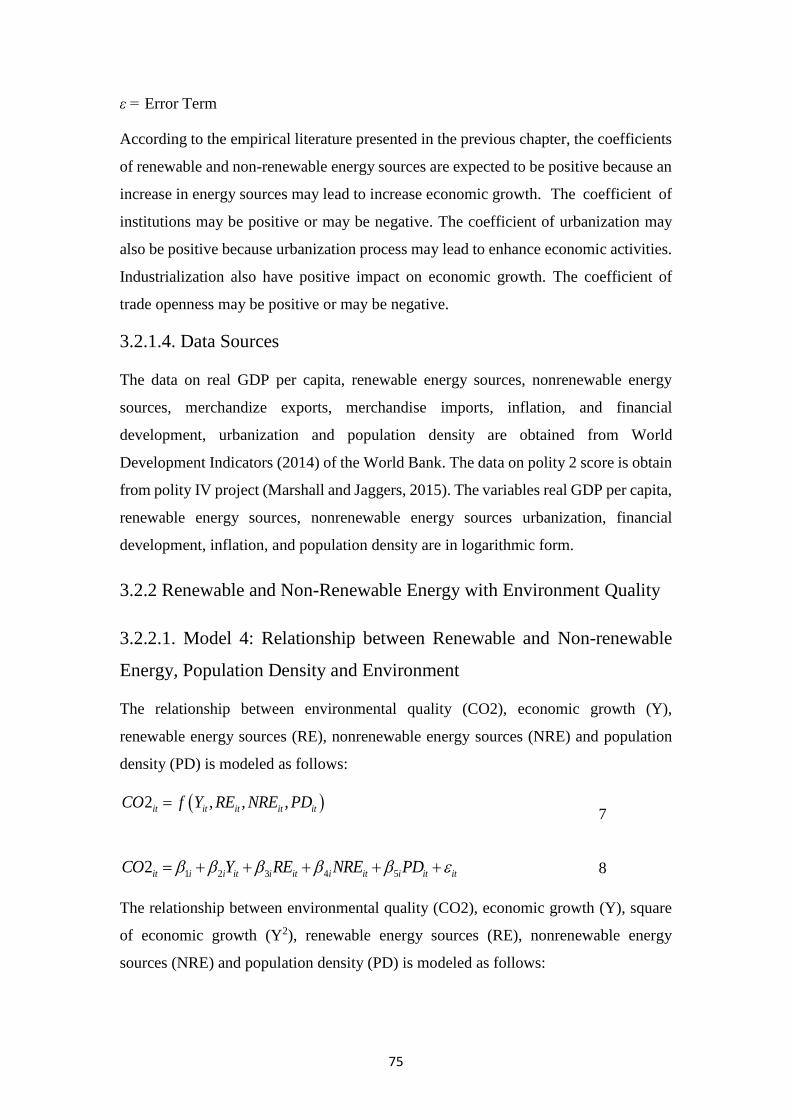

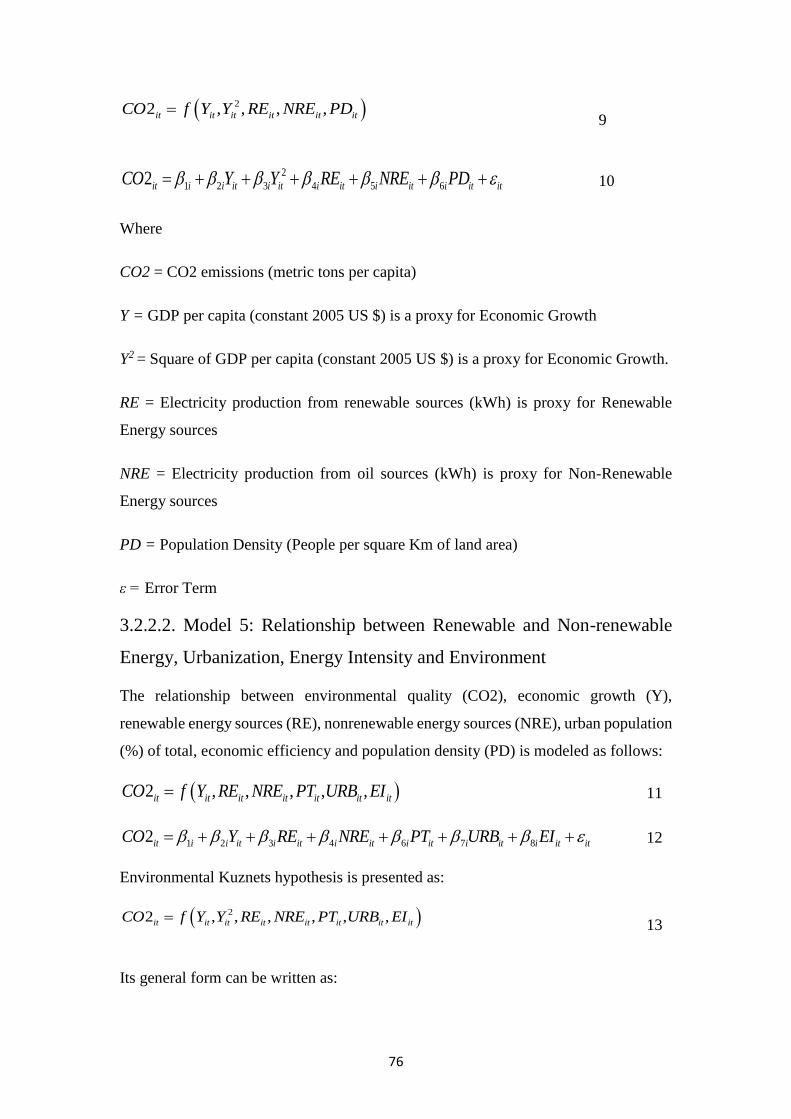

3.2.2 Renewable and nonrenewable energy with Environment Quality…….….……..75

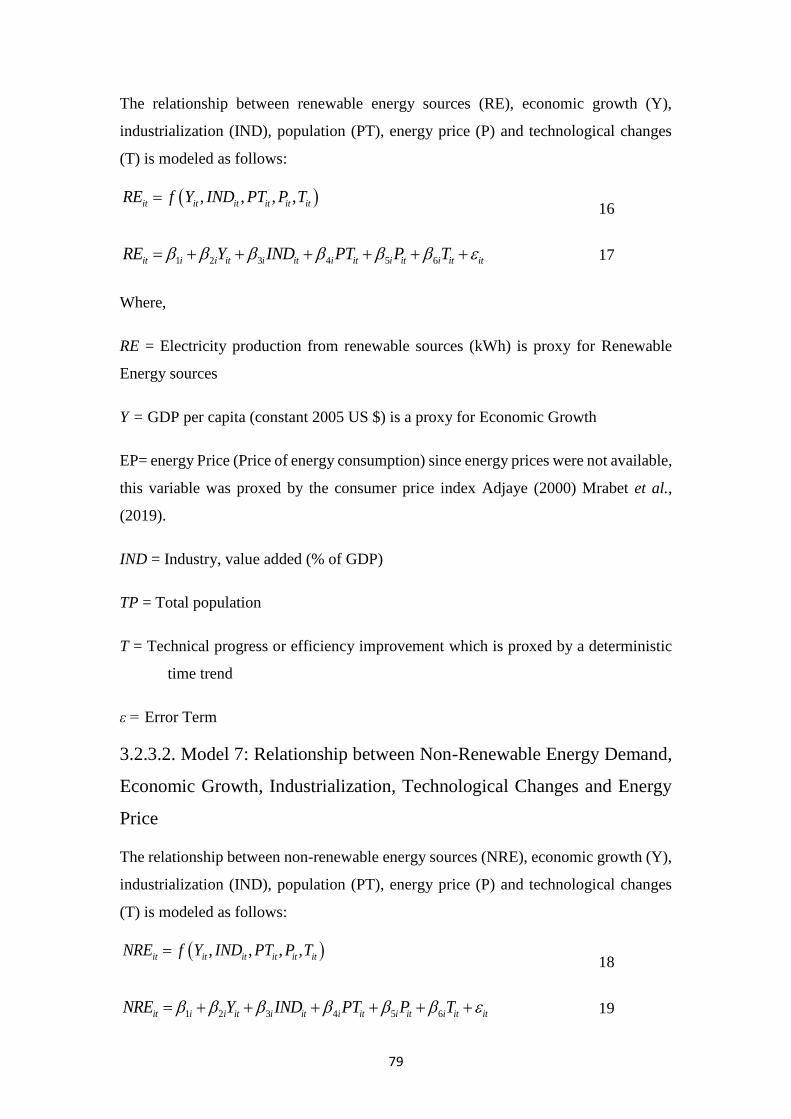

3.2.2.1 Model 4: Relationship between Renewable and Non-renewable Energy,

Population Density and Environment ………………………..……………...………..75

3.2.2.2 Model 5: Relationship between Renewable and Non-renewable Energy,

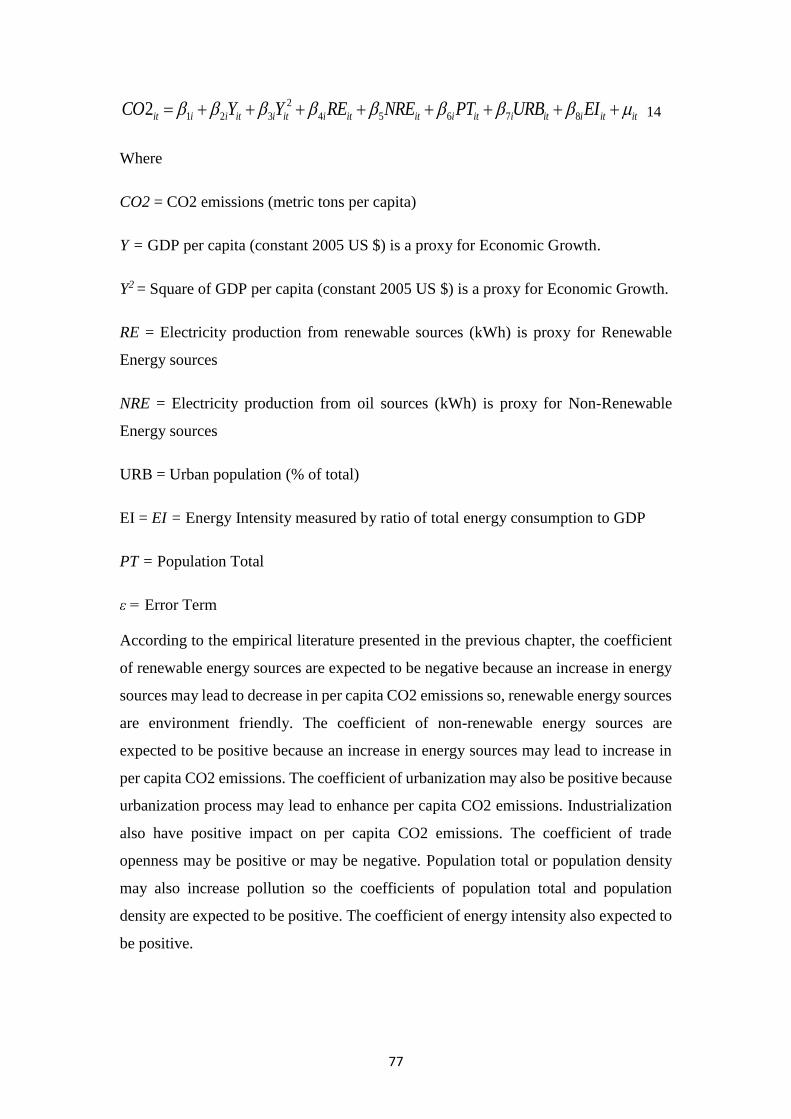

Urbanization, Energy Intensity and Environment …….…………………..….……....76

3.2.2.3 Data Sources……………………………………………………………….…78

3.2.3 Demand Elasticity of Renewable and nonrenewable energy…………...………78

3.2.3.1 Model 6: Relationship between Renewable Energy Demand, Economic Growth,

Industrialization, Technological Changes and Energy Price ………………..……….78

3.2.3.2 Model 7: Relationship between Non-Renewable Energy Demand, Economic

Growth, Industrialization, Technological Changes and Energy Price …………….…79

3.2.3.3 Data Sources…………………………………………………………….……81

3.2.4 Renewable and nonrenewable energy with energy Efficiency……………….…81

3.2.4.1 Model 8: Relationship between Renewable and Non-renewable Energy,

Economic Growth, Urbanization and Energy Intensity ………………...…….………82

3.2.4.2 Model 9: Relationship between Renewable and Non-renewable Energy,

Economic Growth, Trade Openness and Energy Intensity ……………...……………82

3.2.4.3 Model 10: Relationship between Renewable and Non-renewable Energy,

Economic Growth, Industrialization, Technological Progress and Energy Intensity....82

3.2.4.4 Data Sources………………………………………………………………….83

x

3.3 Econometrics Methodology……………...…………………………………….…84

3.3.1 Time-Series Methodology………………..………………………………….....84

3.3.1.1 Unit Root Tests…………….…………………………………………………84

3.3.1.2 Johansen Co-integration Test ……………………………………………..….85

3.3.2 Panel Data Methodology…………………………………………...…………...88

3.3.2.1 Panel Unit Root Tests………………………………………………………....88

3.3.2.1.1 LLC Unit Root Test…….………………………..………………...………..88

3.3.2.1.2 IPS Unit Root Test………………………..………………………………...90

3.3.2.2 Panel Co-integration Test…………………………………………..…………91

3.3.2.2.1 Estimation of Panel Co-integration Regression……….……………...…….93

3.3.3 Panel Granger Causality Test …………………………………………………..94

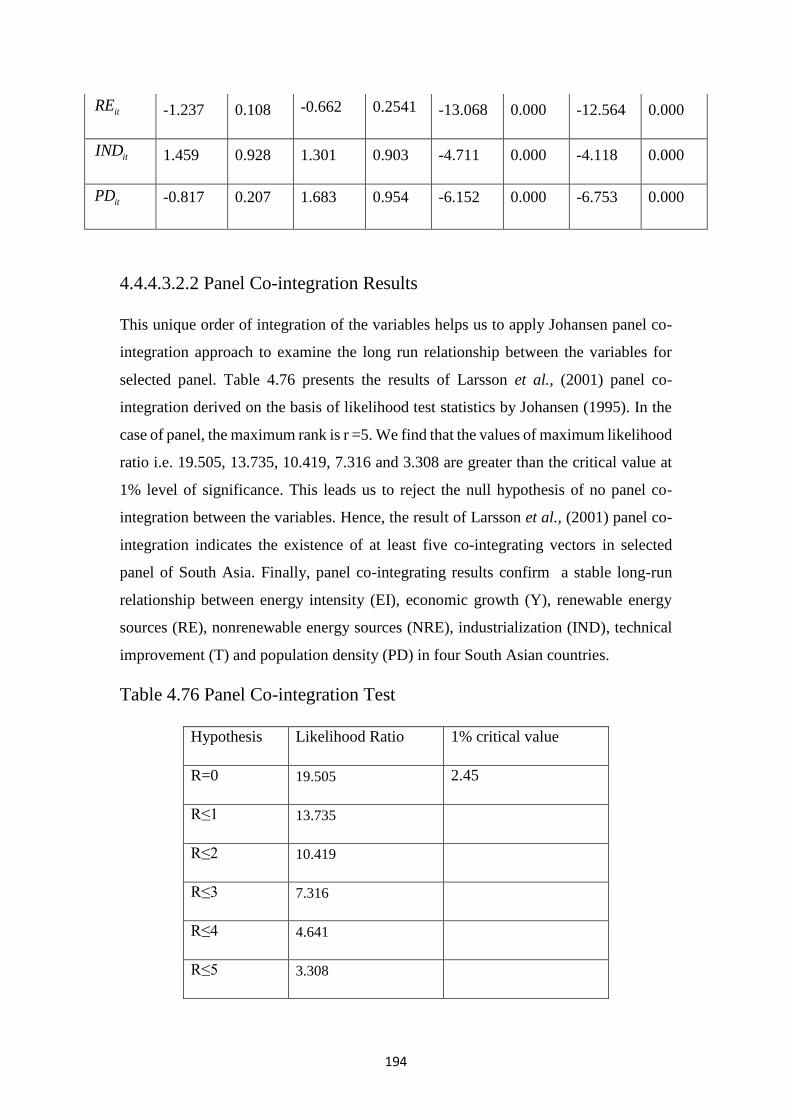

4. RESULTS AND DISCUSSIONS……………………….…………………………96

4.1 An Overview of South Asian Economies…….…….………….…………...…….96

4.1.1 Economic Structure………………..…………………………………………...96

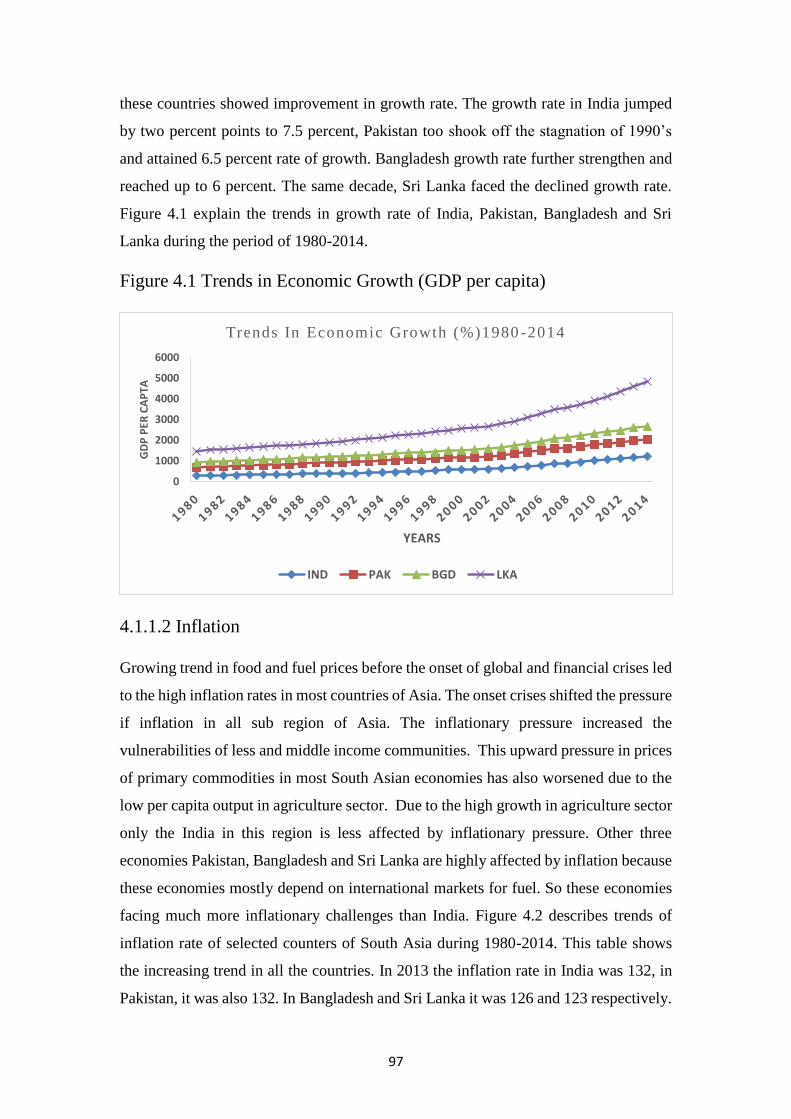

4.1.1.1 Economic Growth………………..……………………………………...……96

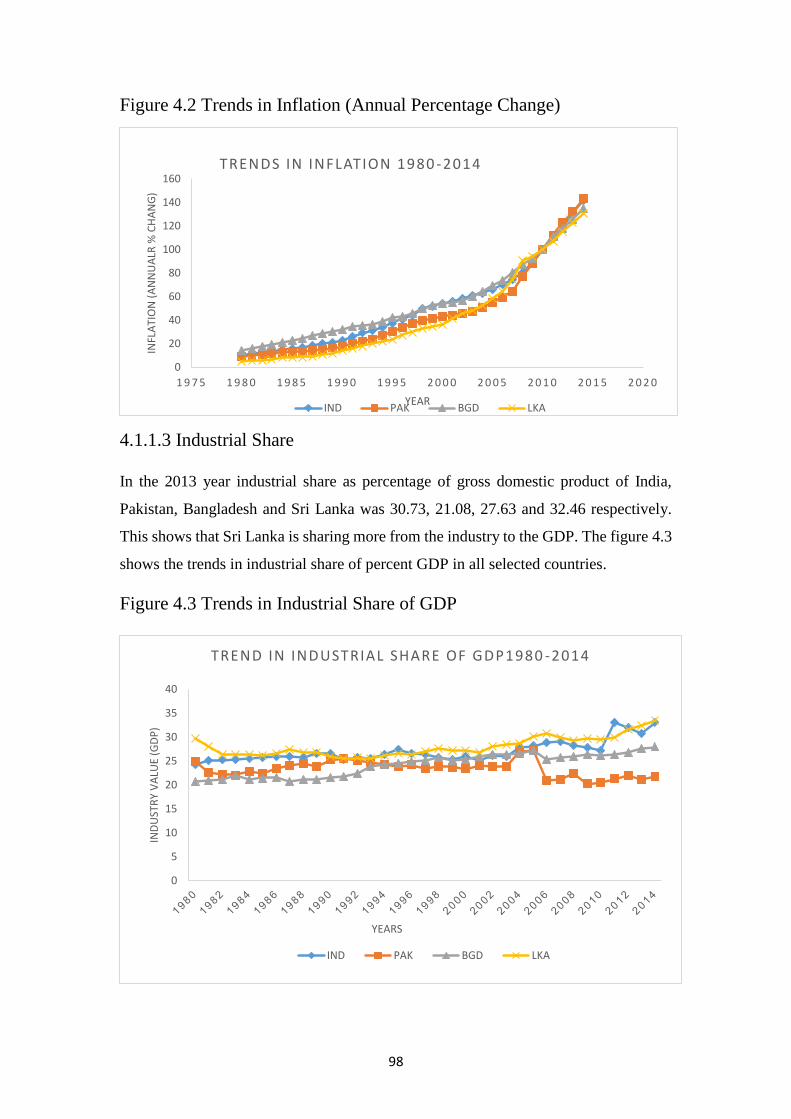

4.1.1.2 Inflation………...………………..……………………………………...……97

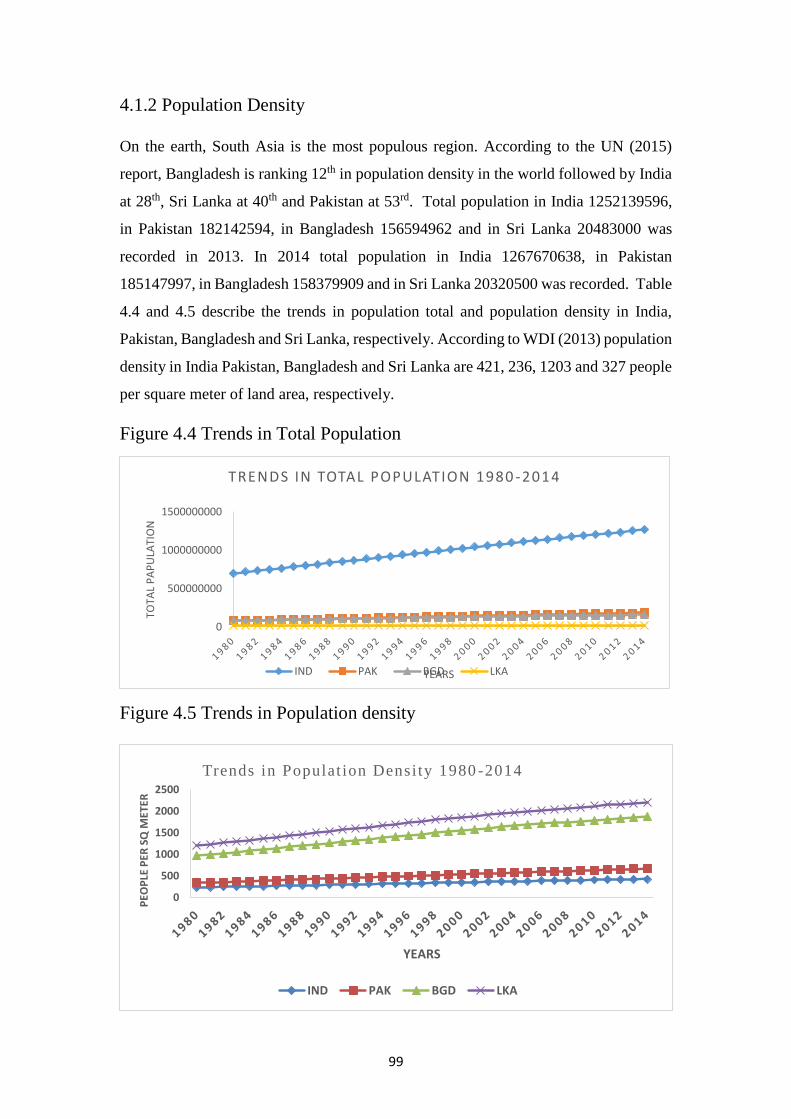

4.1.1.3 Industrial Share …………..……..………………………….…………...……98

4.1.2 Population Desity ….……………...………………………….…………...……99

4.1.3 Environment………………..……..……………………….…………….....…100

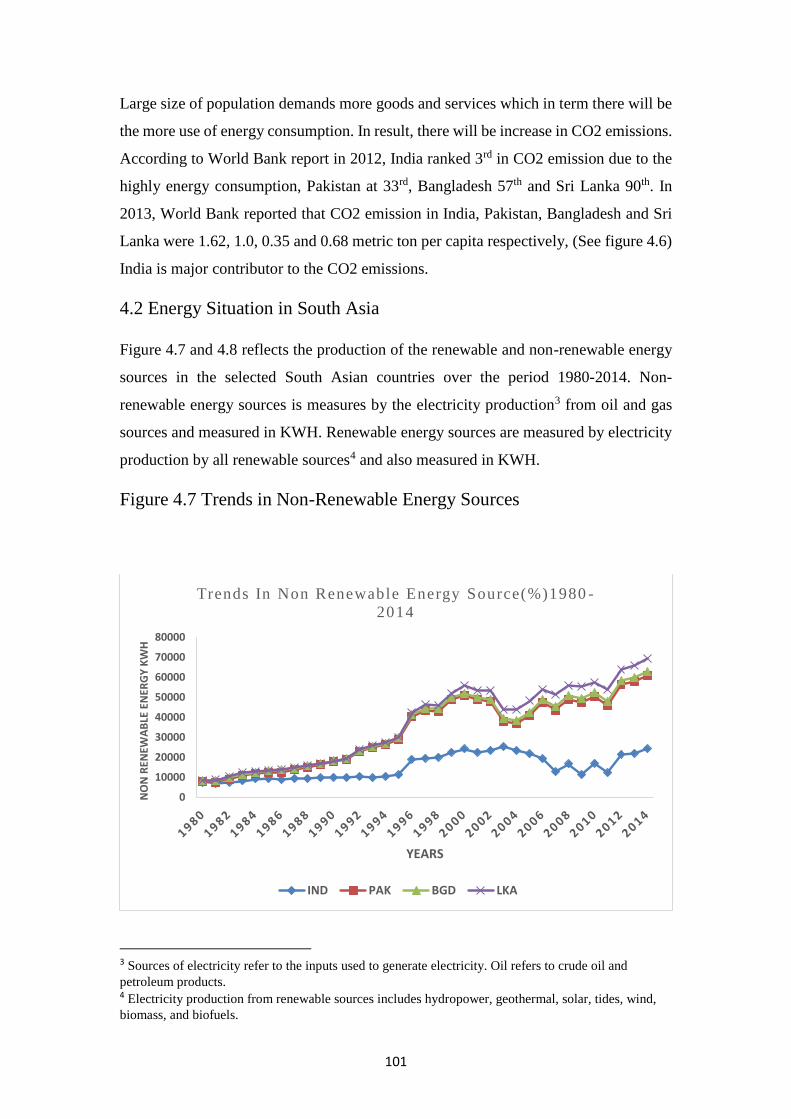

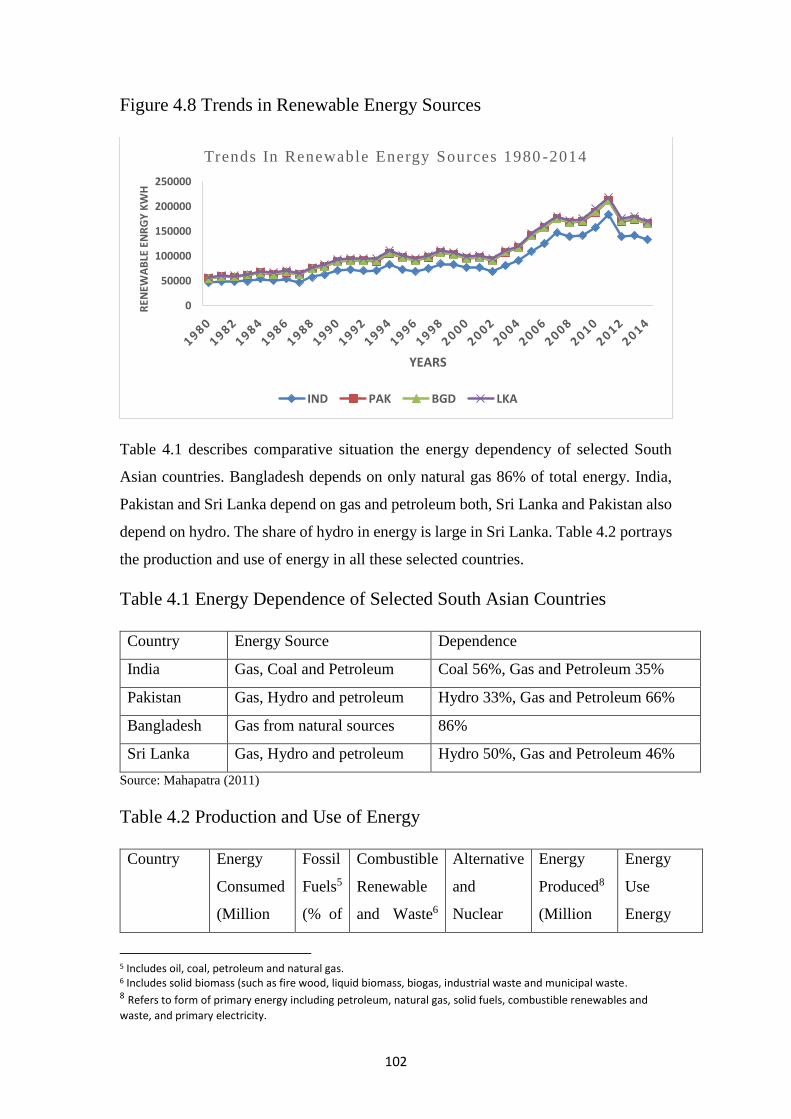

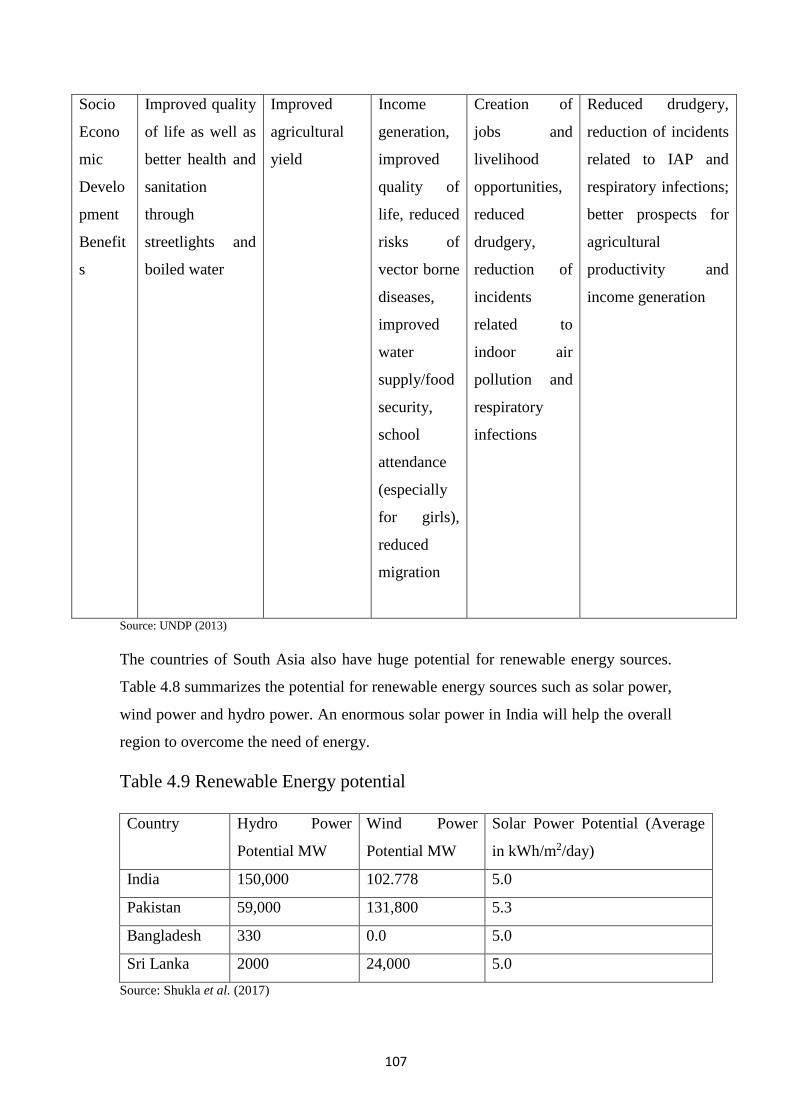

4.2 Energy Situation In South Asia ………………..………….………………….…101

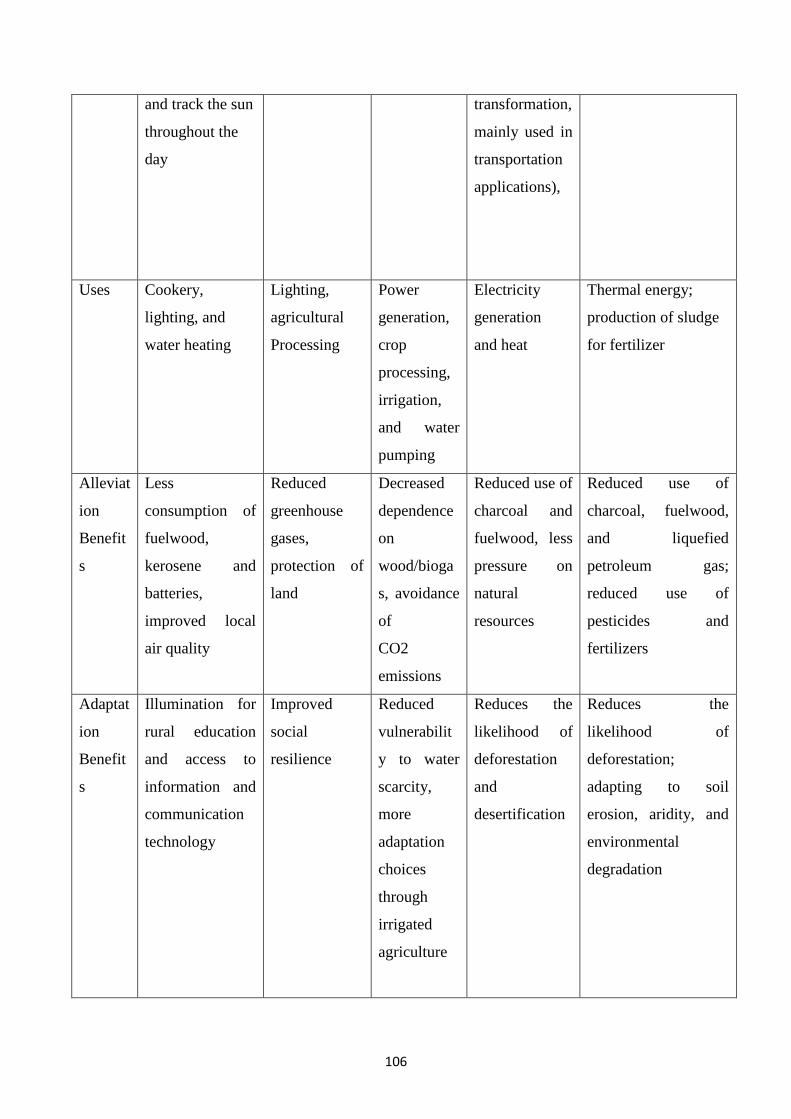

4.3 Importance and Potential of Renewable Energy Sources ……………............…105

xi

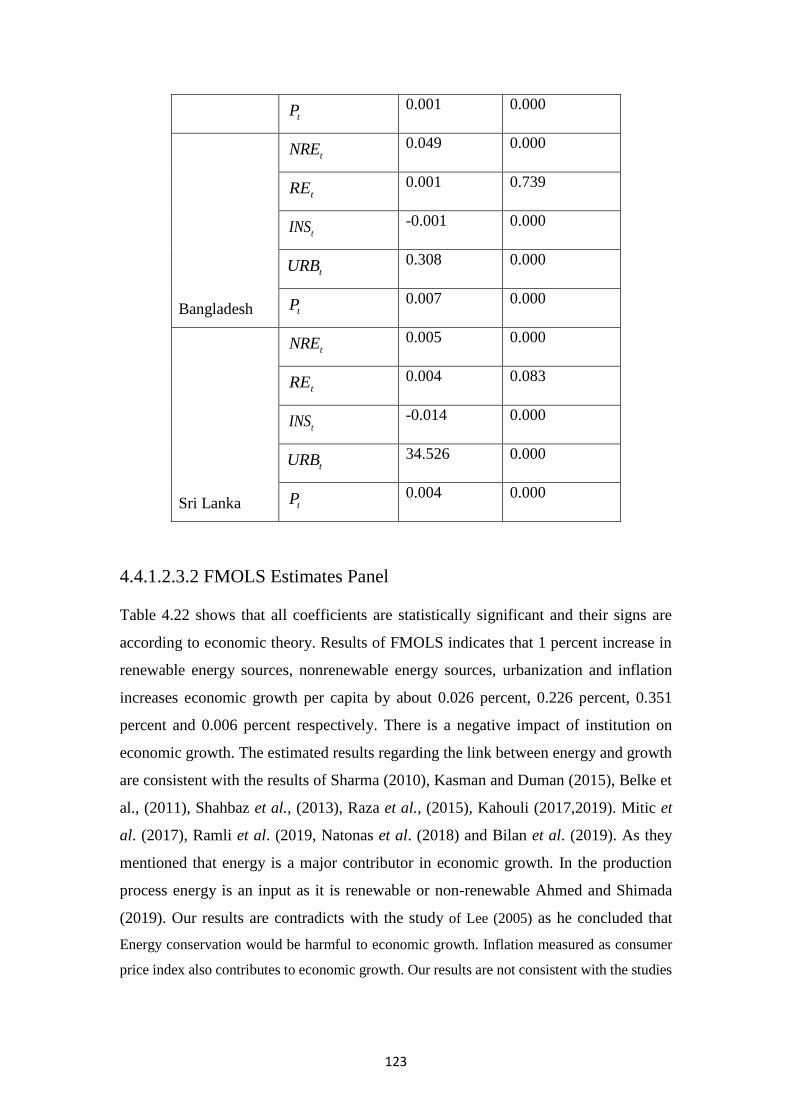

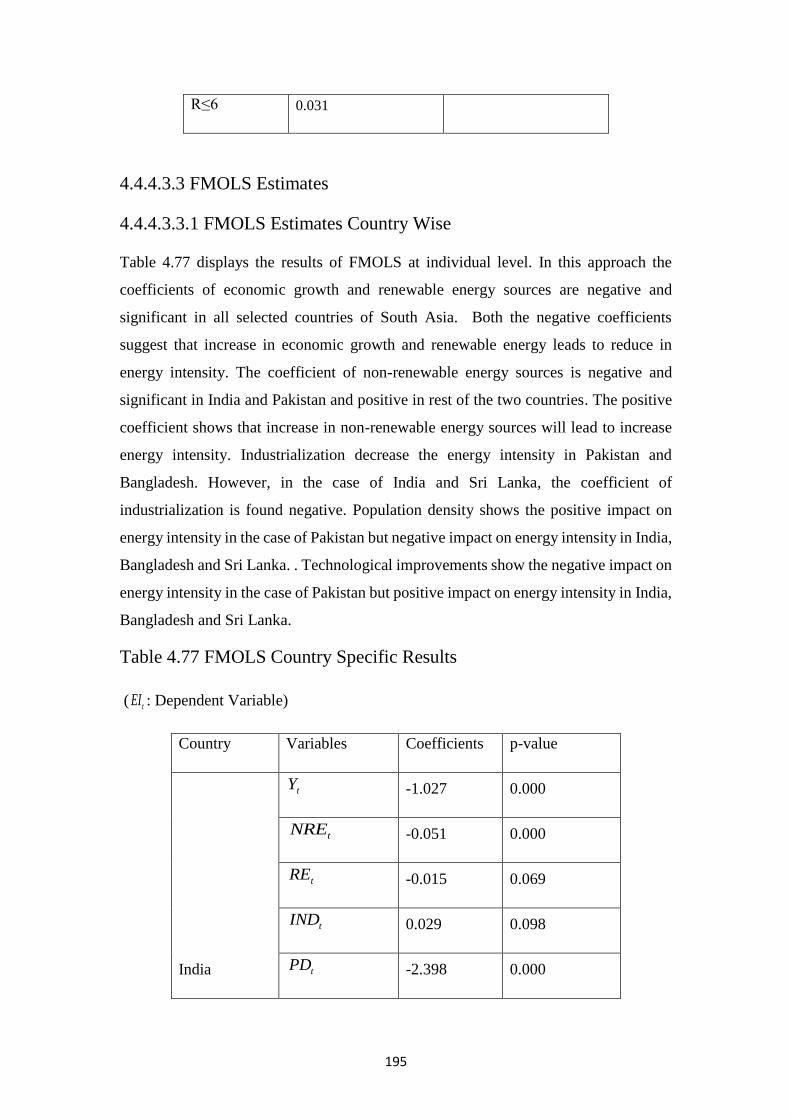

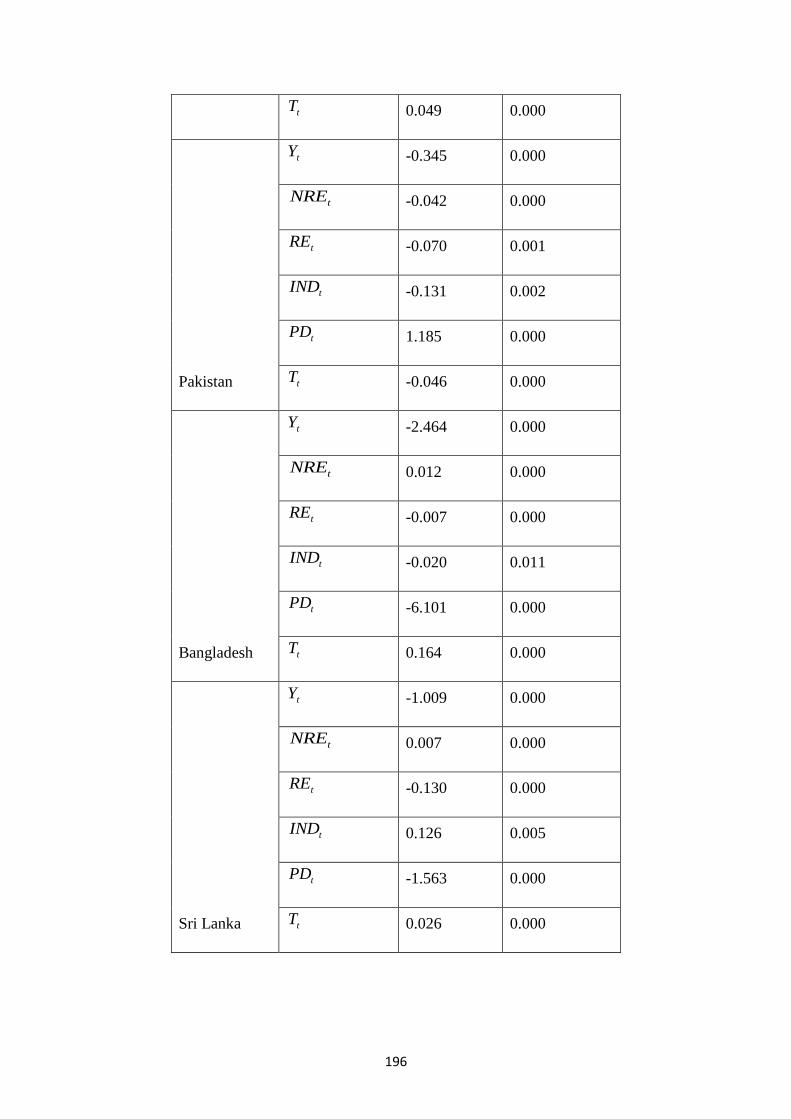

4.4 Empirical results and discussions……………………………………………..…108

4.4.1 Impact of renewable and nonrenewable energy on economic growth……....…108

4.4.1.1 Model 1: Relationship between Renewable and Non-renewable Energy,

Institutions and Economic Growth ………..……………………………..…….….108

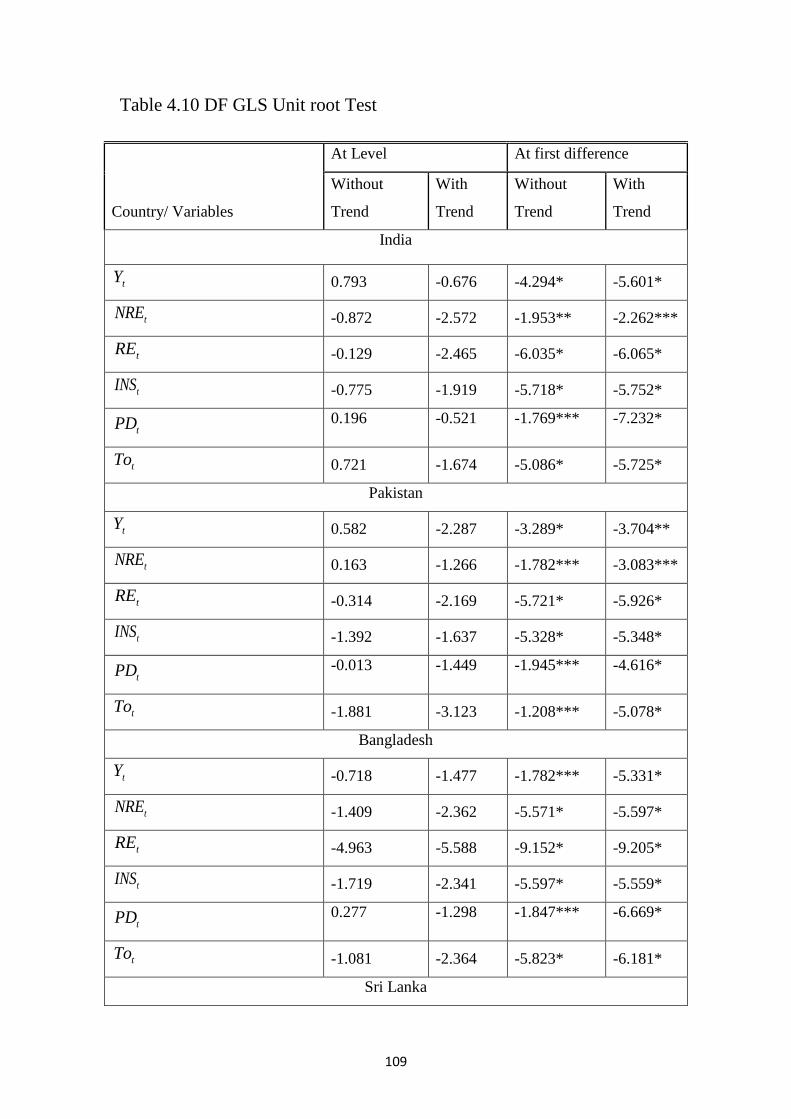

4.4.1.1.1. Time Series Results…………………………………….……...................108

4.4.1.1.1.1. Unit Root Test Results………………………..…..……………….…...108

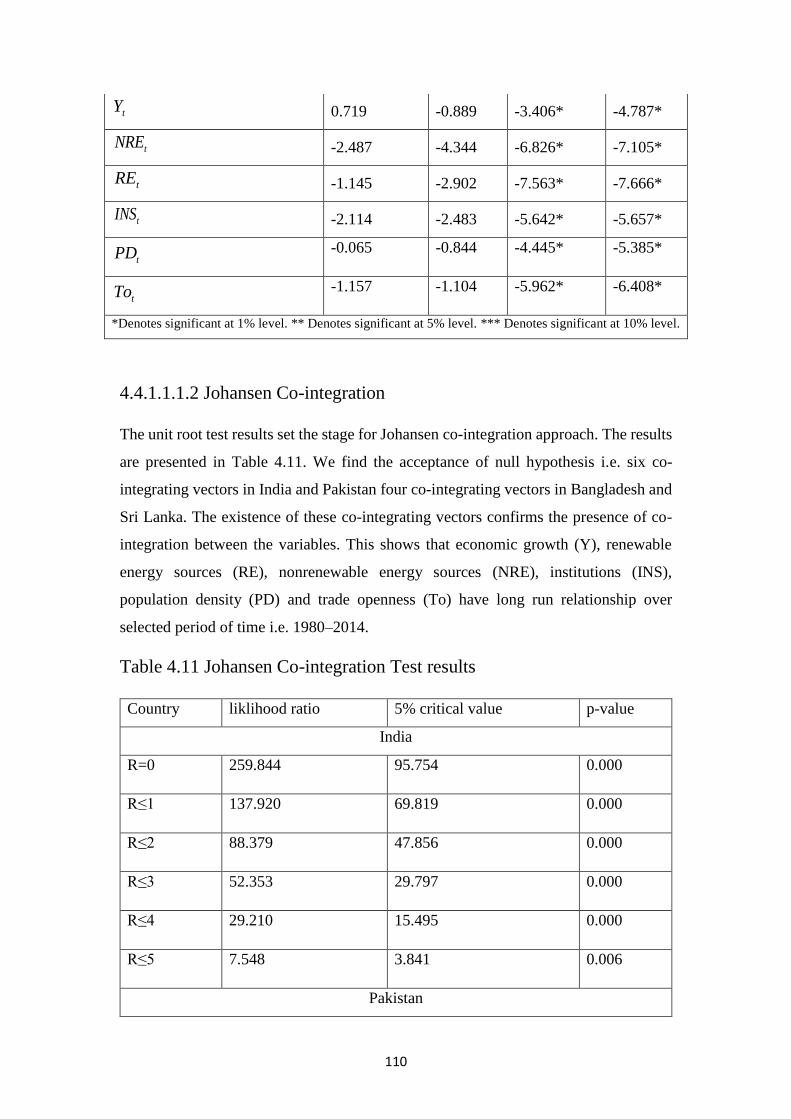

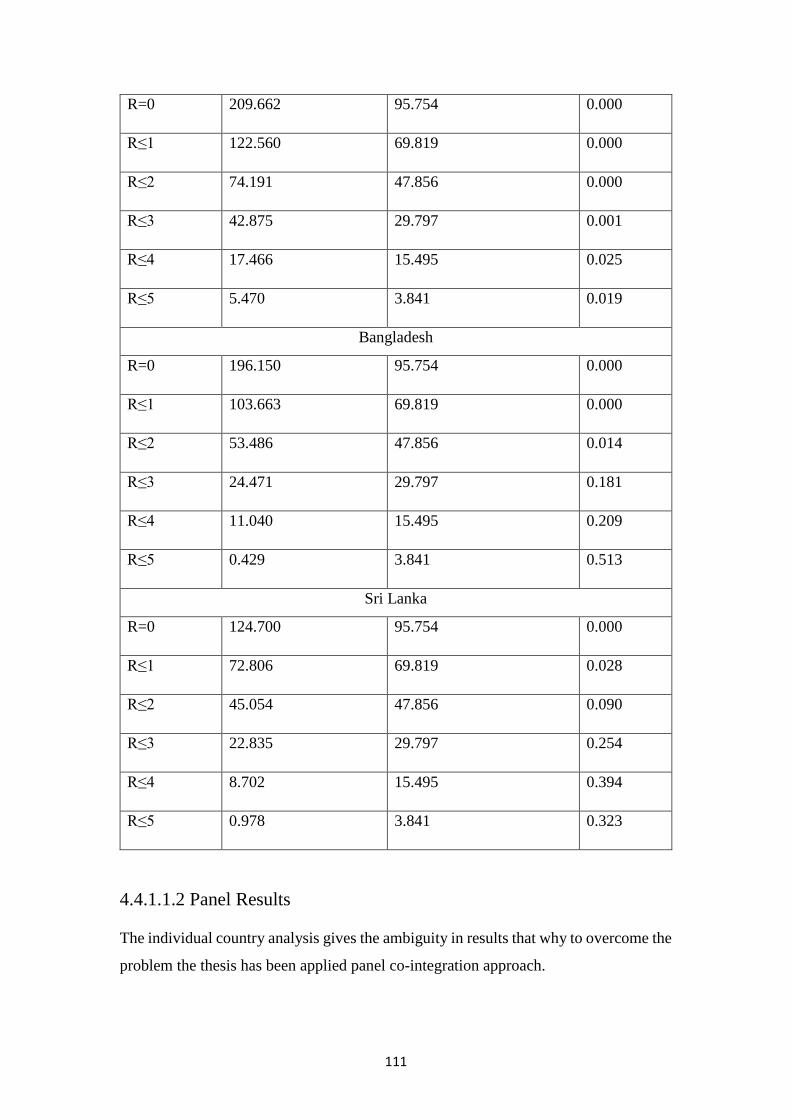

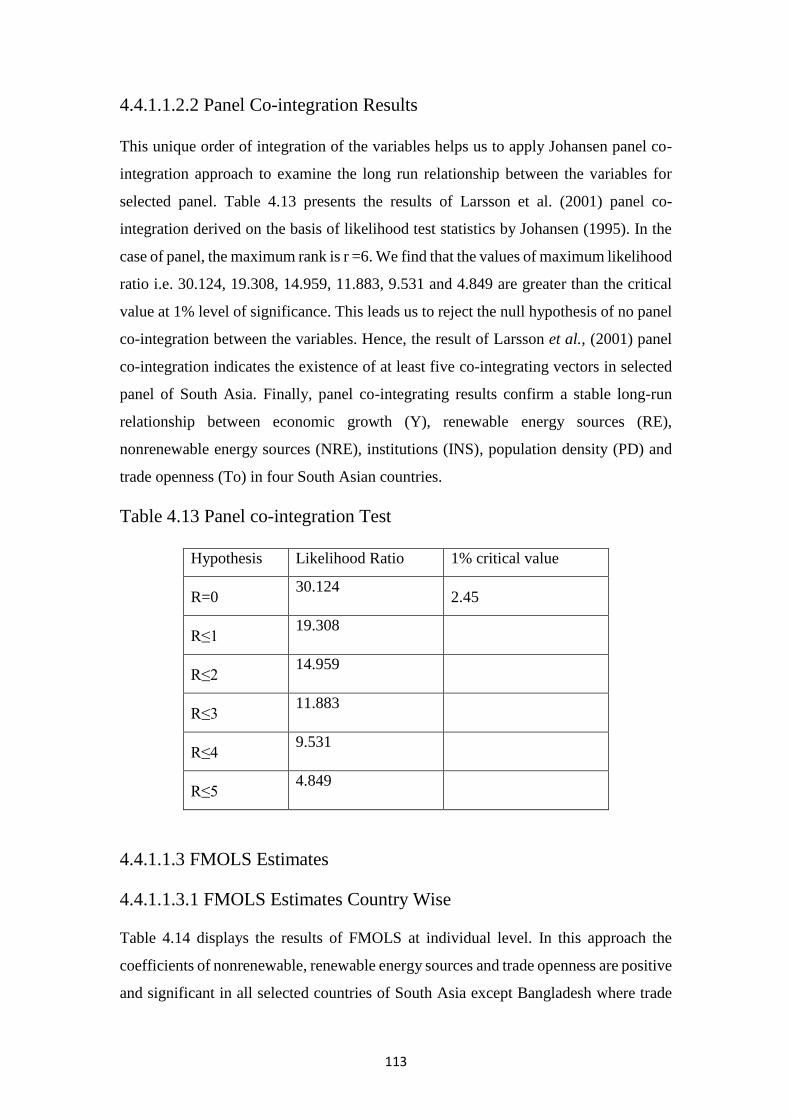

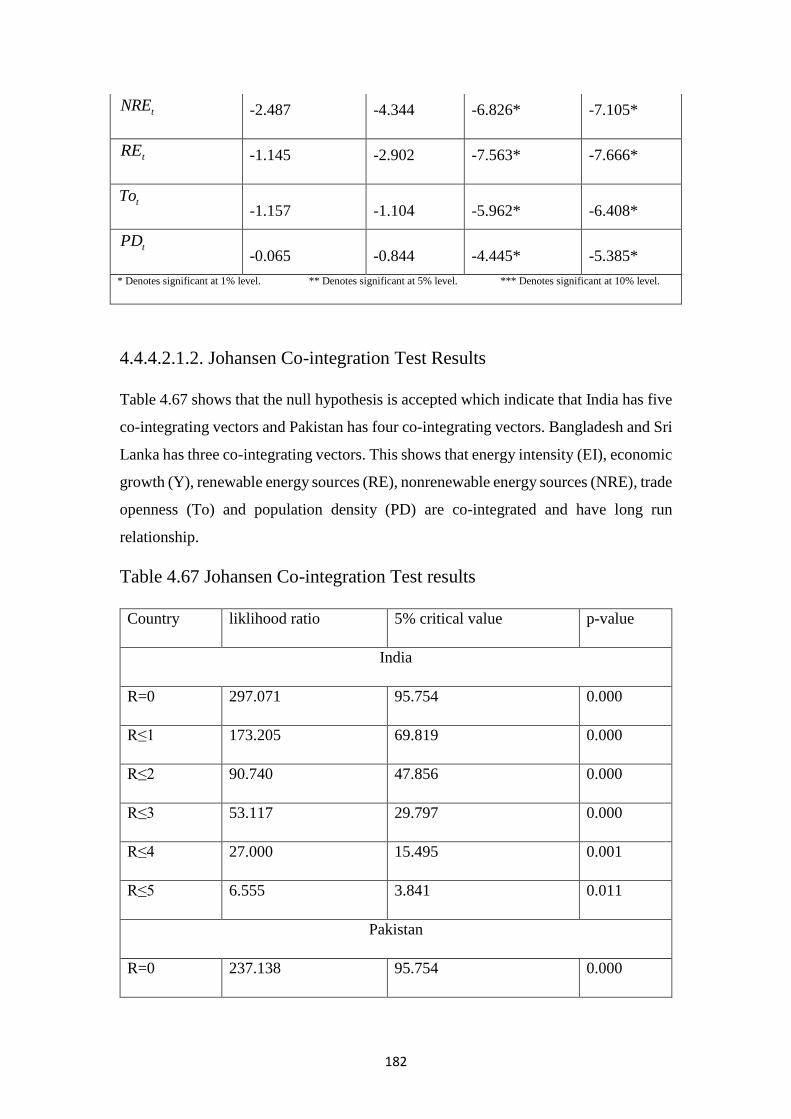

4.4.1.1.1.2. Johansen Co-integration Test Results…………………………..……....110

4.4.1.1.2 Panel Results…………………………………………………………....…111

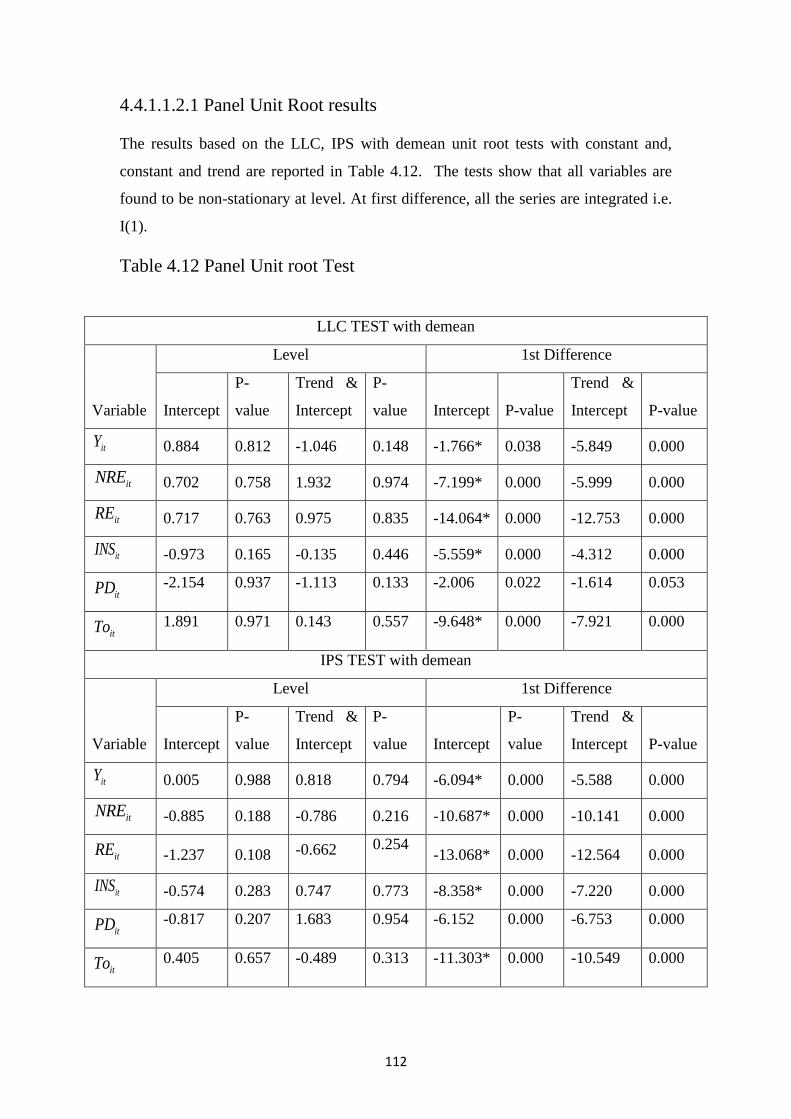

4.4.1.1.2.1 Panel Unit Root Results………………………………………..….…….112

4.4.1.1.2.2 Panel Co-integration Results………………………...…………………..113

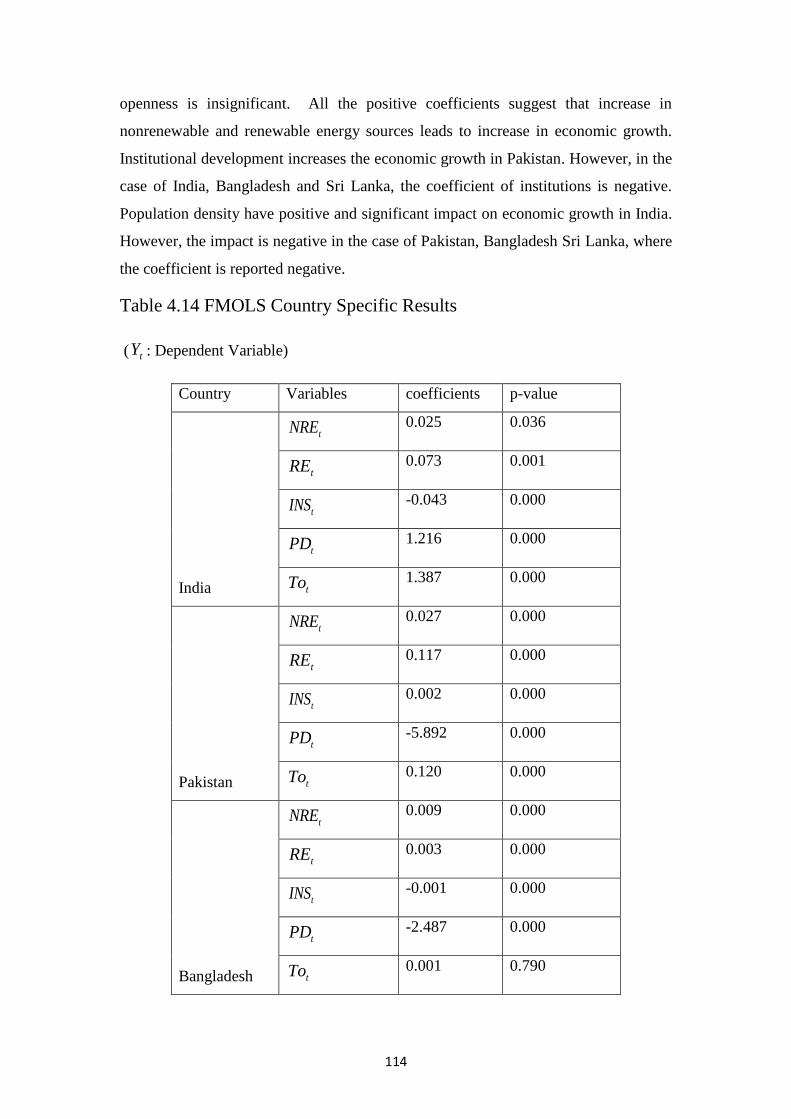

4.4.1.1.3 FMOLS Estimates……………...…………………………...…..…………113

4.4.1.1.3.1 FMOLS Estimates Country Wise…………………………….…………113

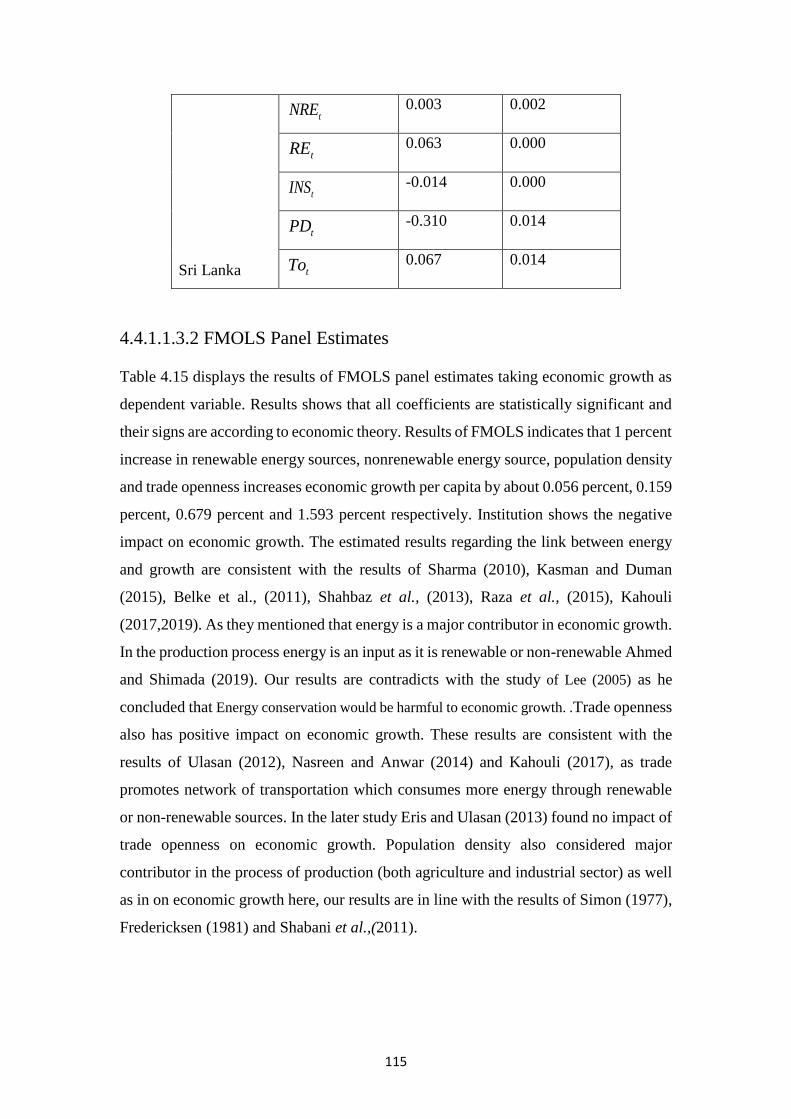

4.4.1.1.3.2 FMOLS Panel Estimates……………………….……………………..…115

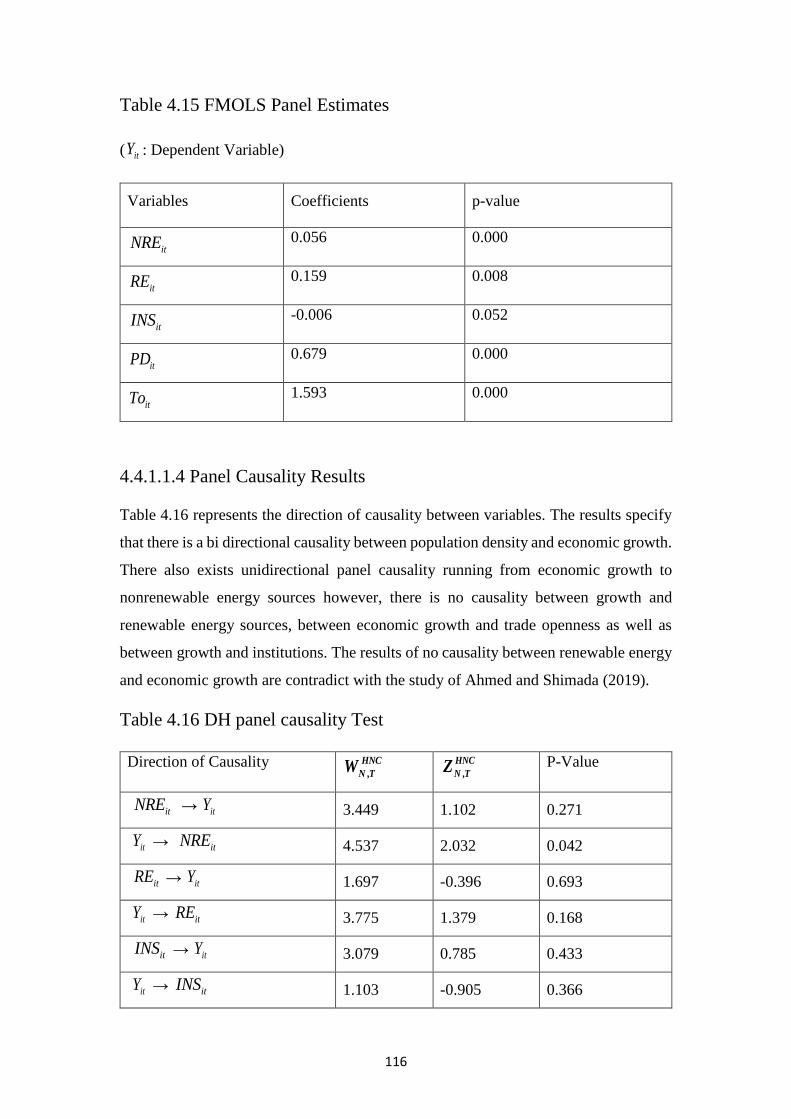

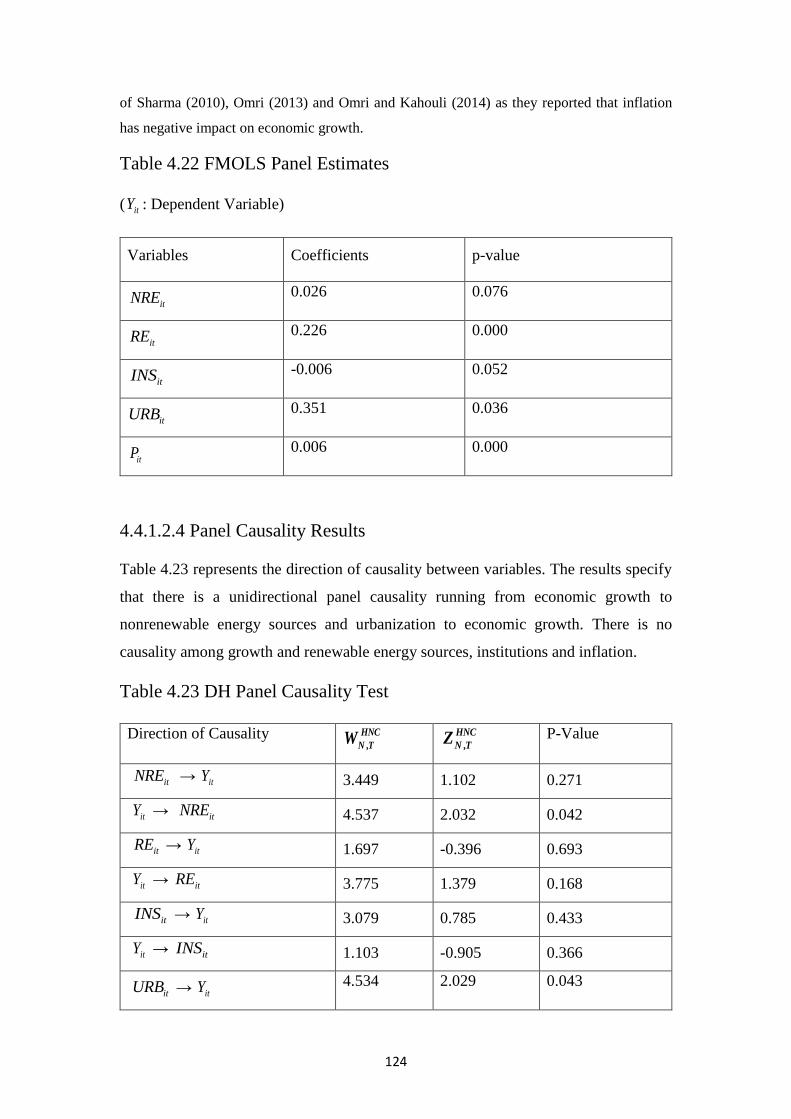

4.4.1.1.4 Panel Causality Results…………...…………………………………...…..116

4.4.1.2 Model 2: Relationship between Renewable and Non-renewable Energy,

Urbanization and Economic Growth ……………………………………………..…117

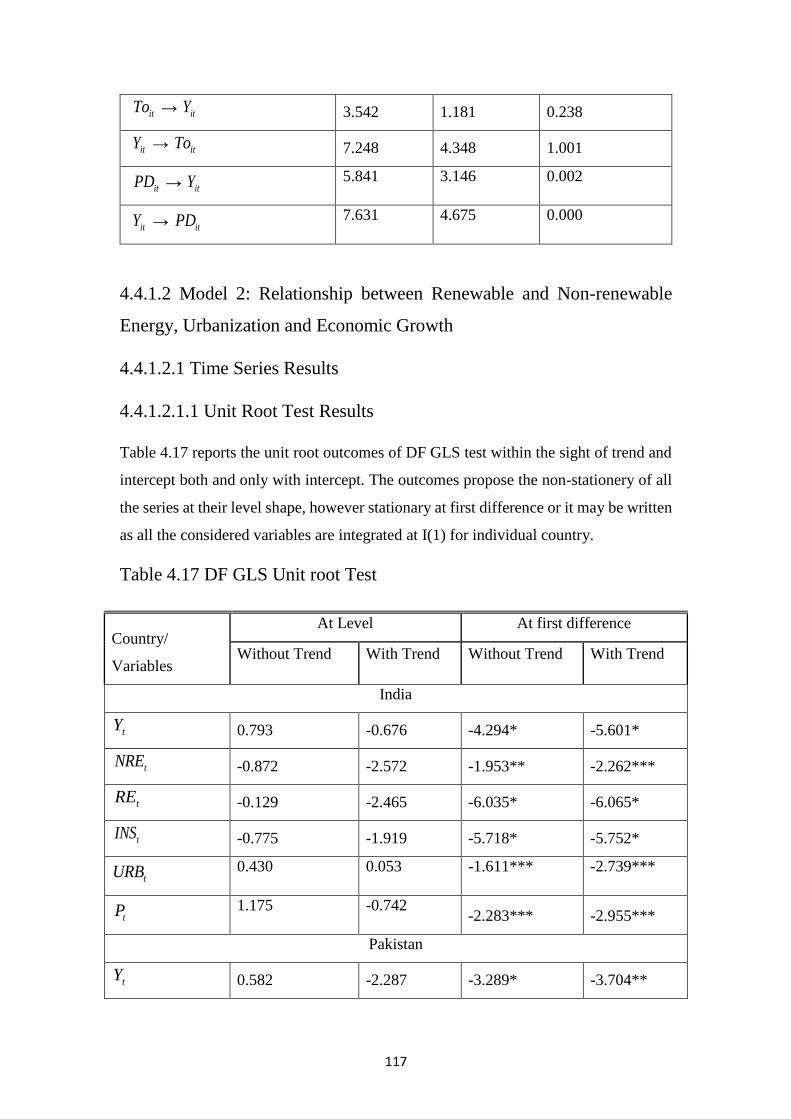

4.4.1.2.1 Time Series Results……………………………………………………..…117

4.4.1.2.1.1 Unit Root Test Results……………………………...……………..…….117

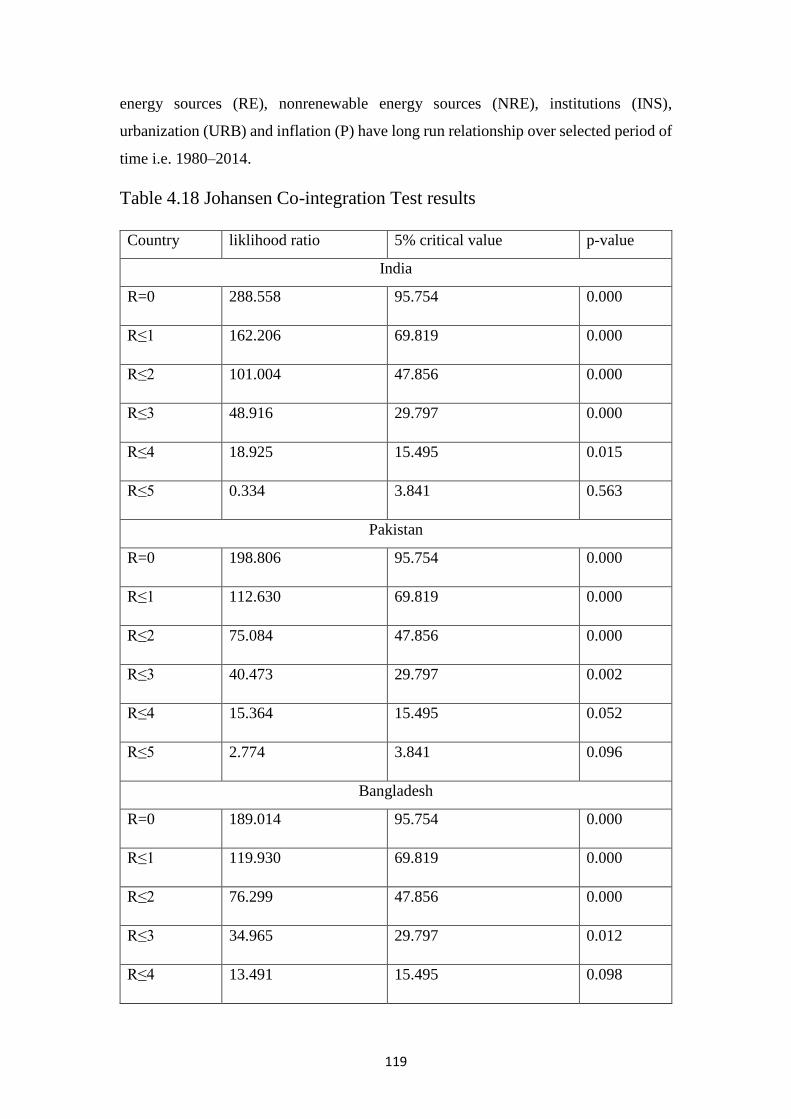

4.4.1.2.1.2 Johansen Co-integration Test Results………………………....………...118

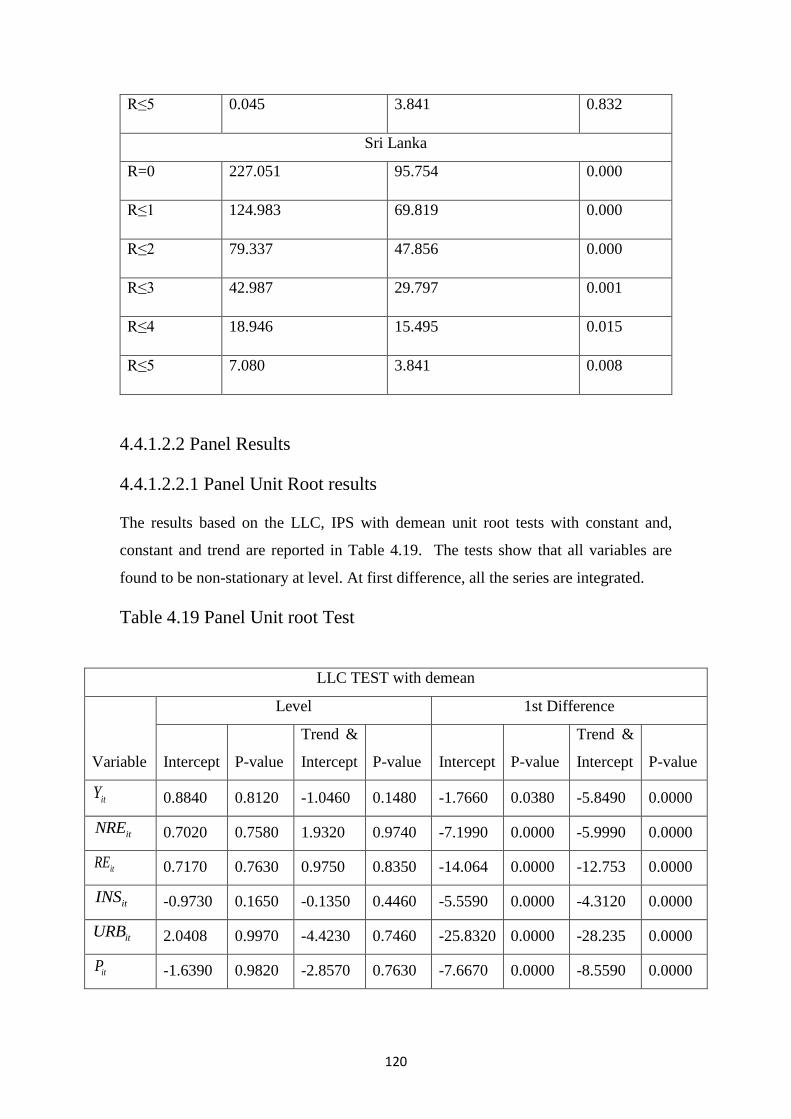

4.4.1.2.2 Panel Results………………………...…………………..……………...…120

4.4.1.2.2.1 Panel Unit Root Results ……………………………..…..………….…..120

4.4.1.2.2.2 Panel Co-integration Results…………………………..…..…………….121

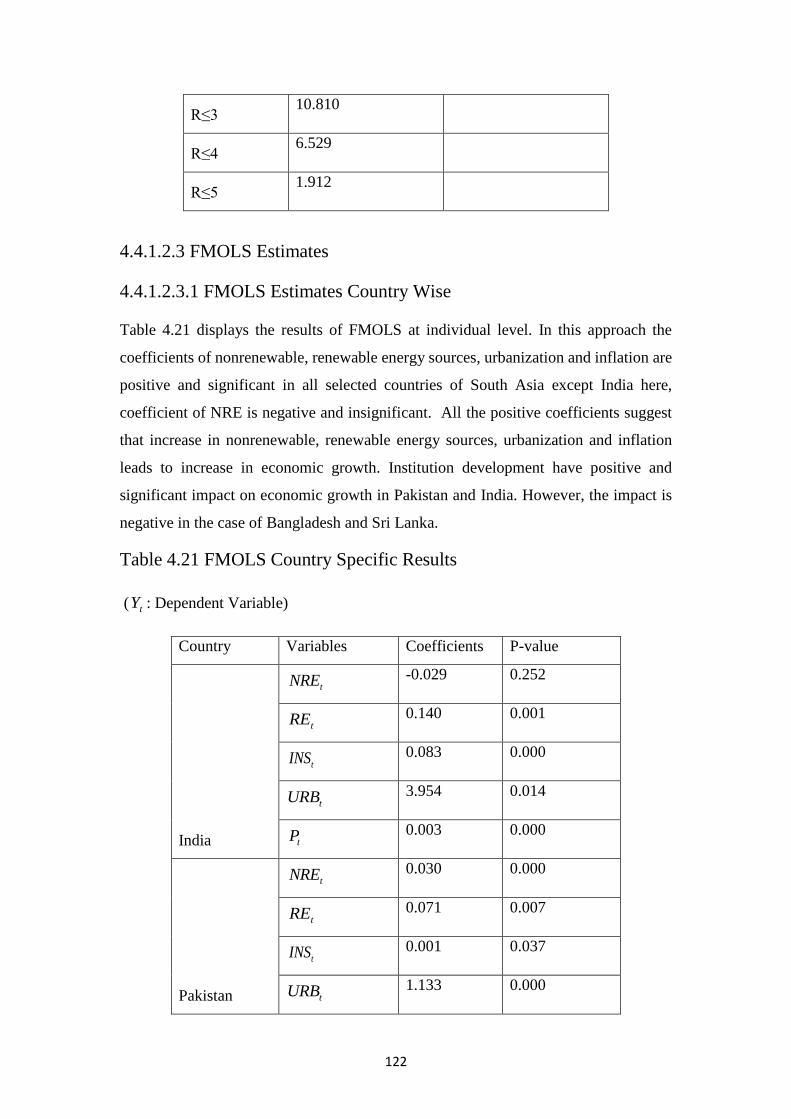

4.4.1.2.3 FMOLS Estimates……………………………...………………………….122

4.4.1.2.3.1 FMOLS Estimates Country Wise……………………………….………122

4.4.1.2.3.2 FMOLS Panel Estimates………………………………………...………123

xii

4.4.1.2.4 Panel Causality Results……………………………………………..……..124

4.4.1.3 Model 3: Relationship between Renewable and Non-renewable Energy,

Financial Development and Economic Growth ………….…….………………..….125

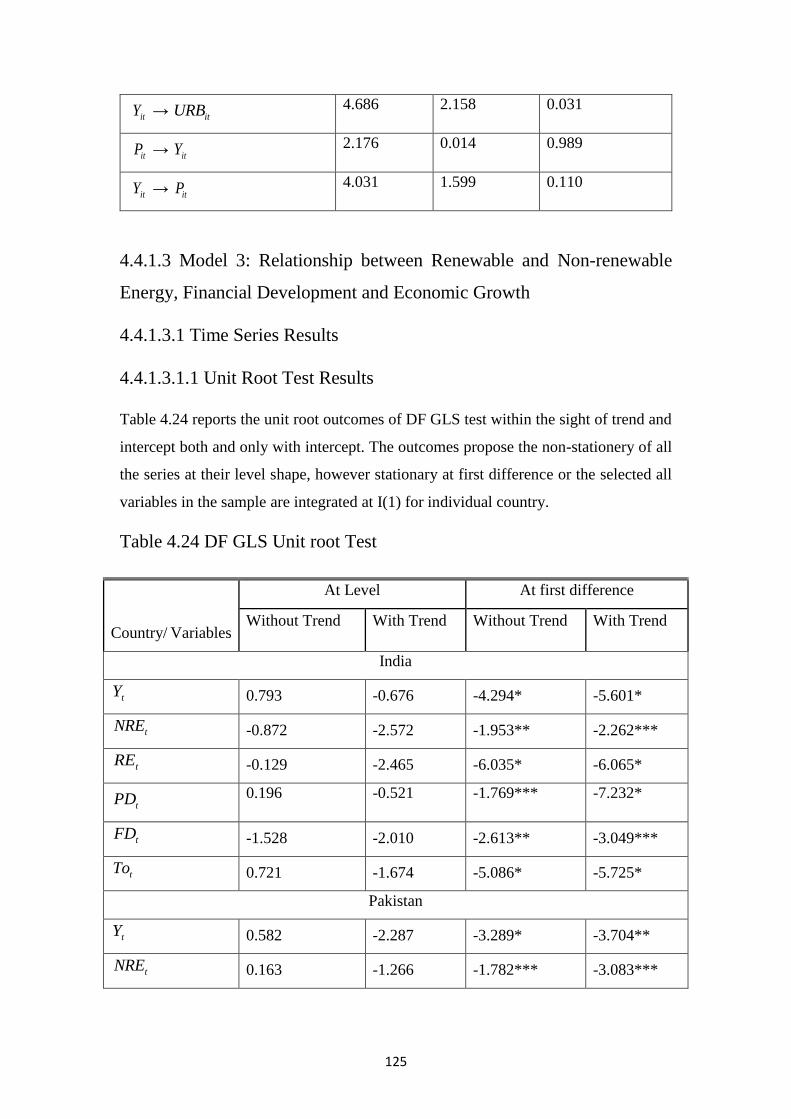

4.4.1.3.1 Time Series Results………..…….………………….…………………..…125

4.4.1.3.1.1 Unit Root Test Results……………………………….…...…………..…125

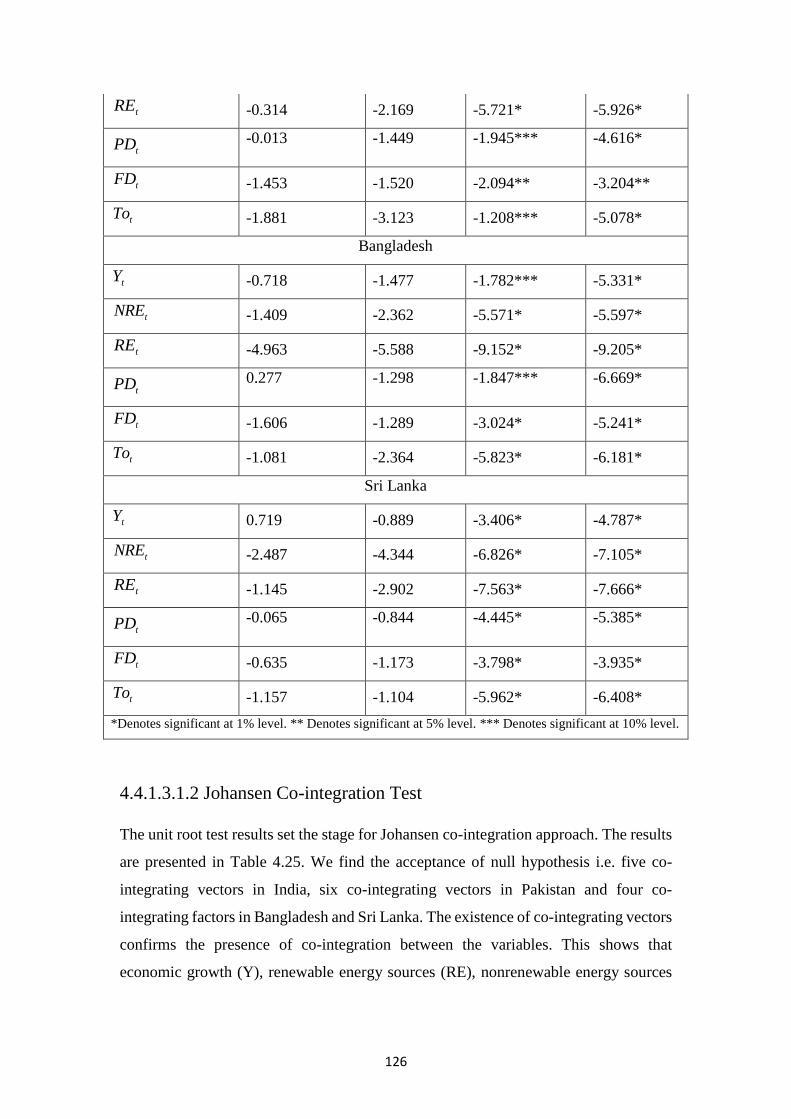

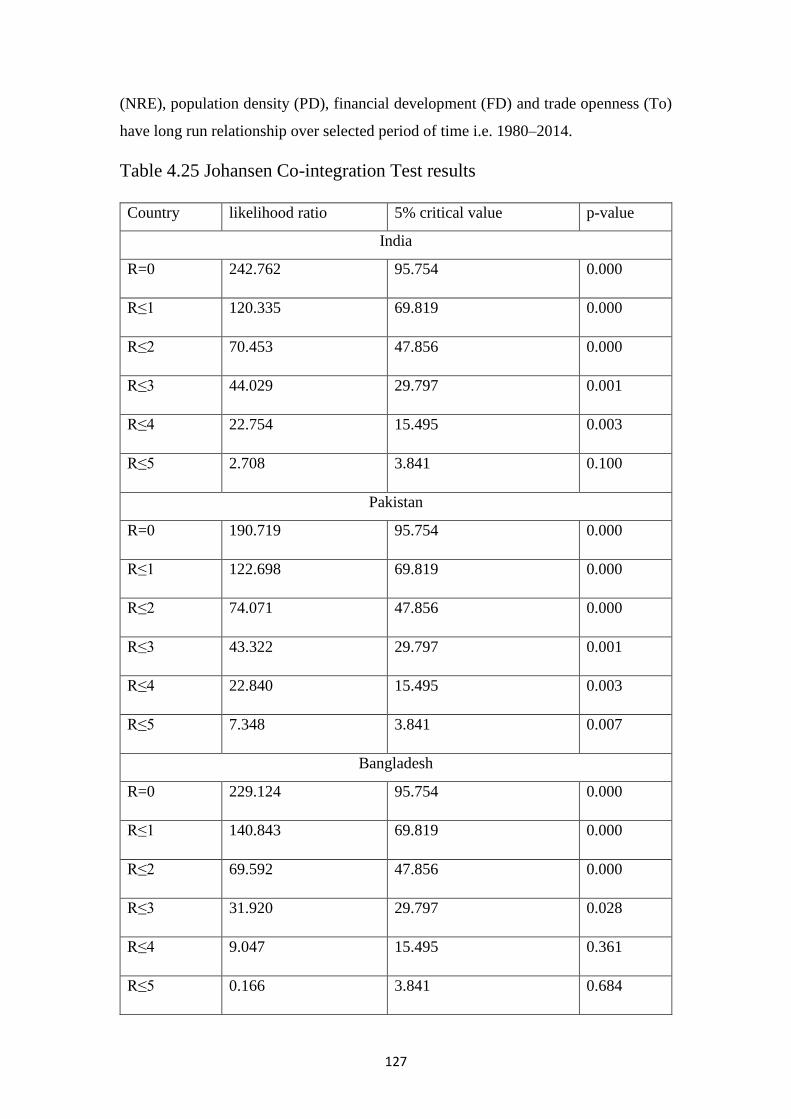

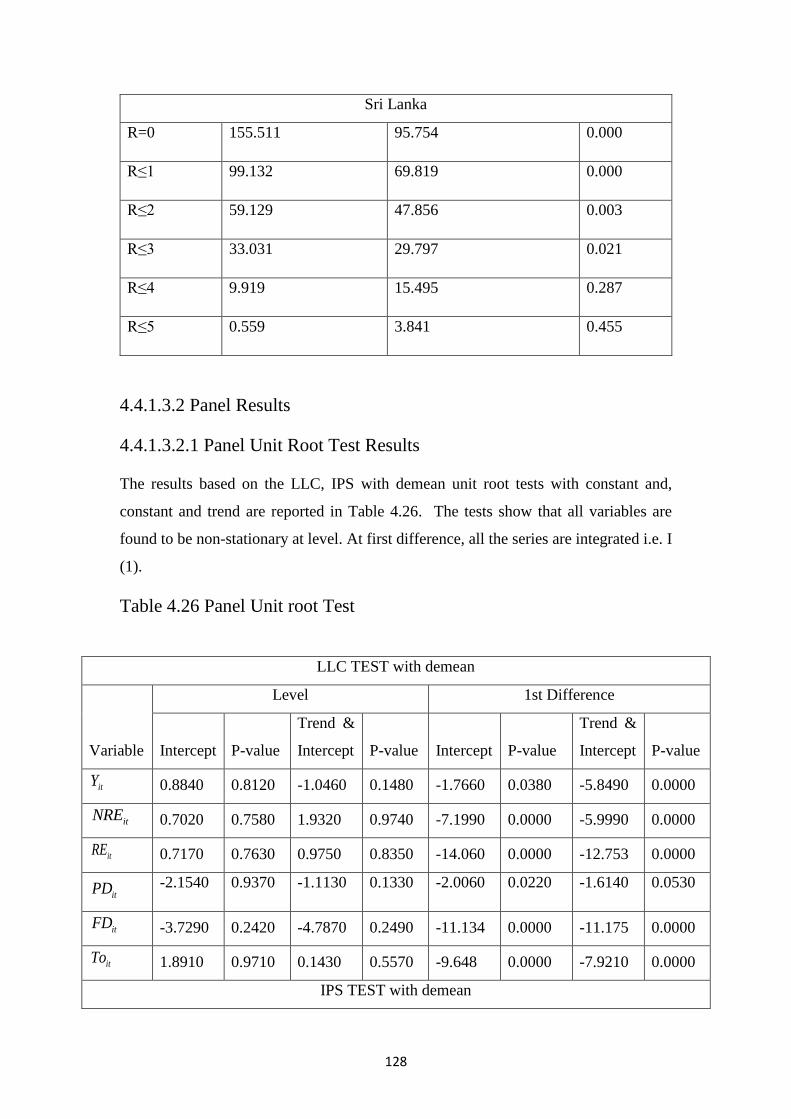

4.4.1.3.1.2 Johansen Co-integration Test Results…………....………………...……126

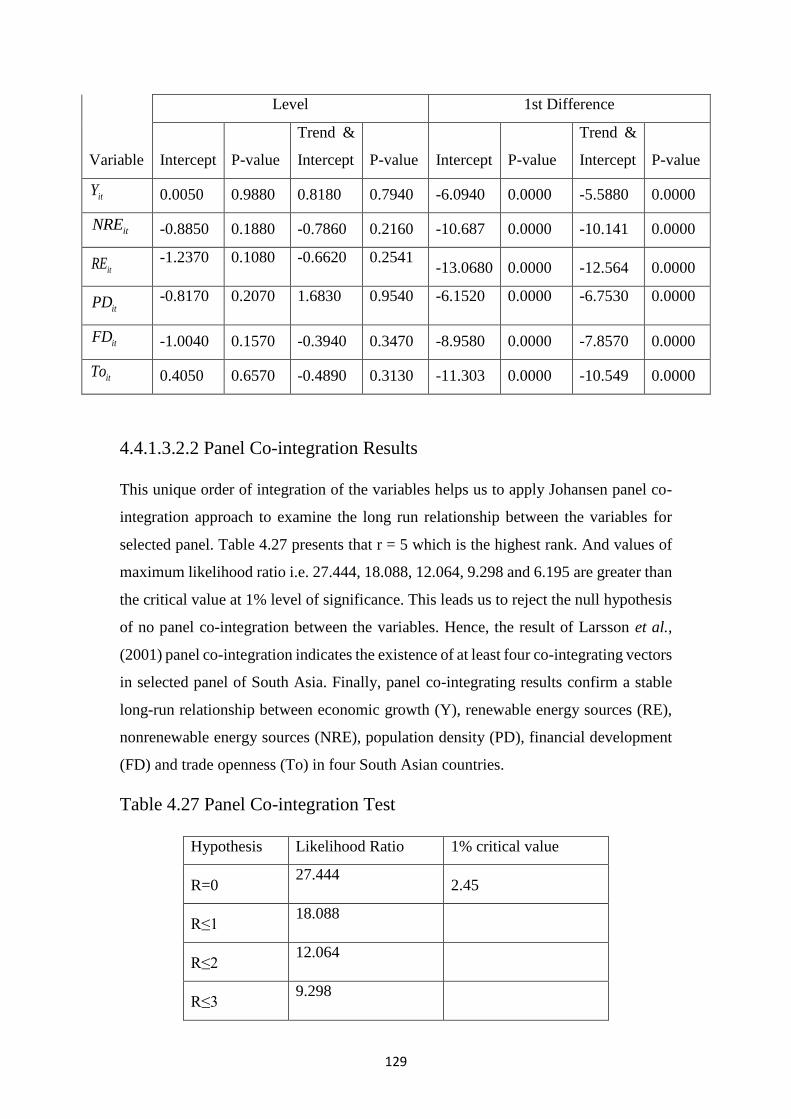

4.4.1.3.2 Panel Results……………………………………………...……….……...128

4.4.1.3.2.1 Panel Unit Root Results………….………………………………...……128

4.4.1.3.2.2 Panel Co-integration Results………………………………………….....129

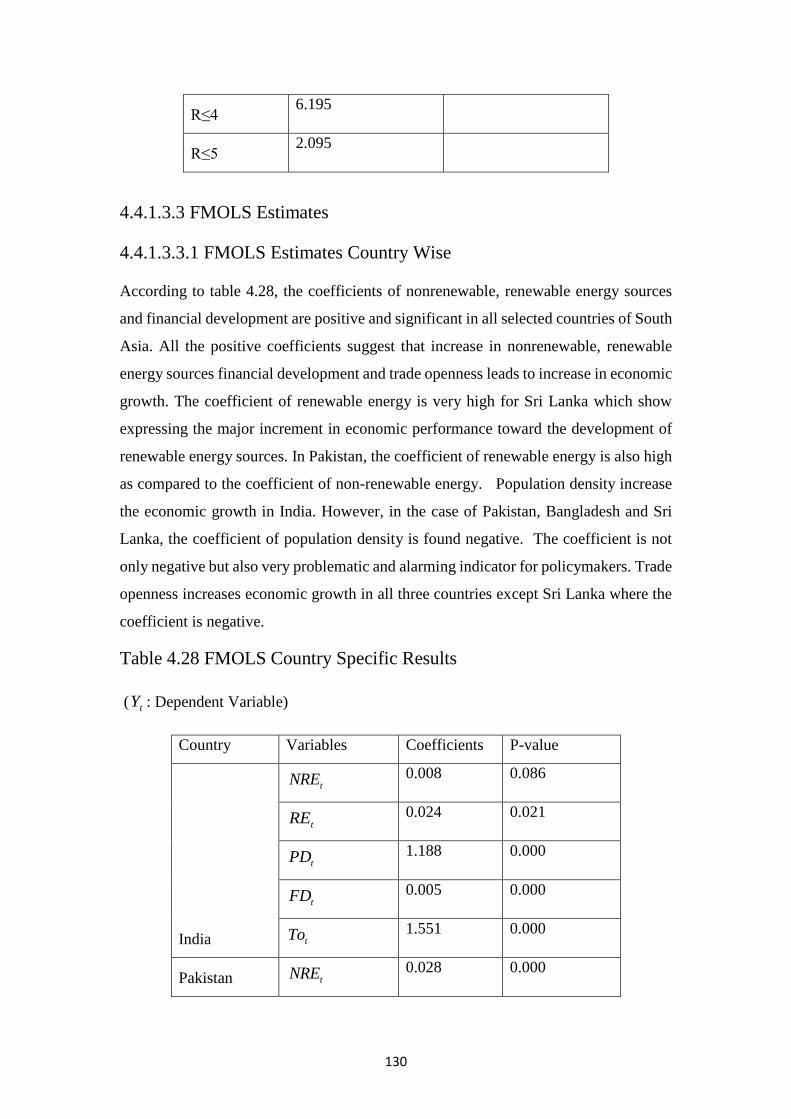

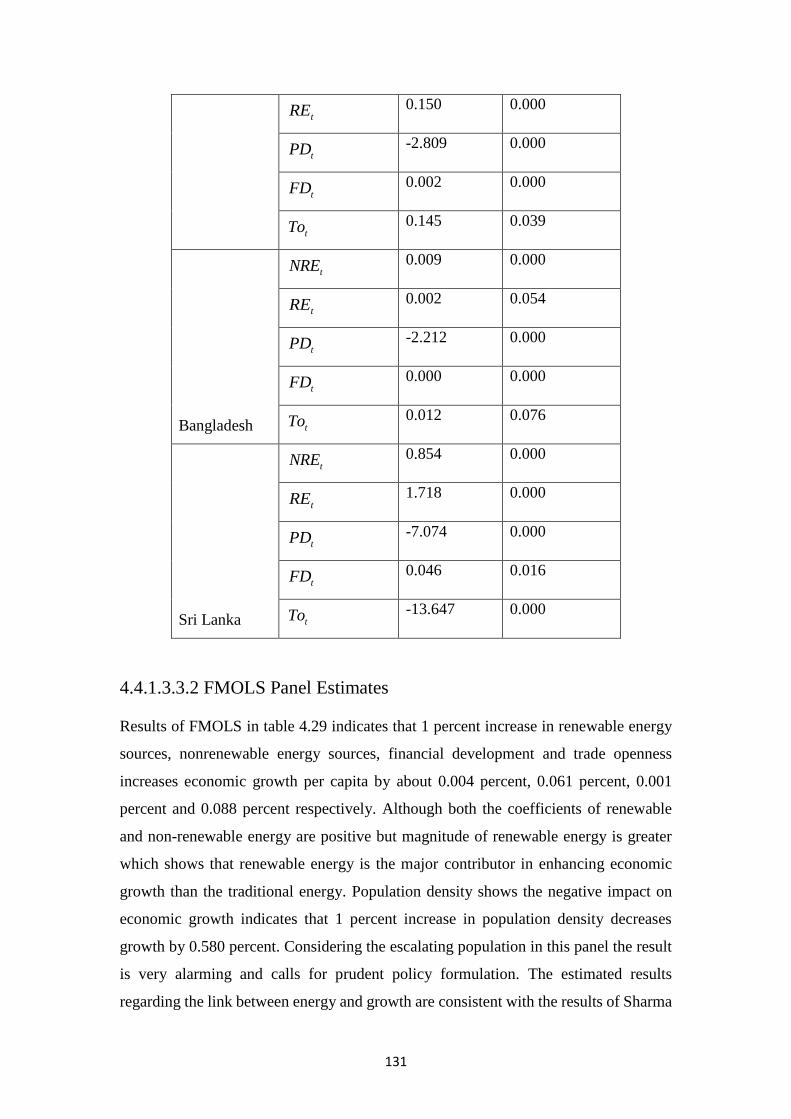

4.4.1.3.3 FMOLS Estimates……………………………………………………...….130

4.4.1.3.3.1 FMOLS Estimates Country Wise………..………………………………130

4.4.1.3.3.2 FMOLS Panel Estimates………………………………………………...131

4.4.1.3.4 Panel Causality Results……………………………………………………132

4.4.2. Impact of Renewable and Non-Renewable Energy Sources on Environmental

Quality………………………………………………………………………...…….133

4.4.2.1 Model 4: Relationship between Renewable and Non-renewable Energy,

Population Density and Environment ………………………………………………133

4.4.2.1.1 Time Series Results………………………………..………………………133

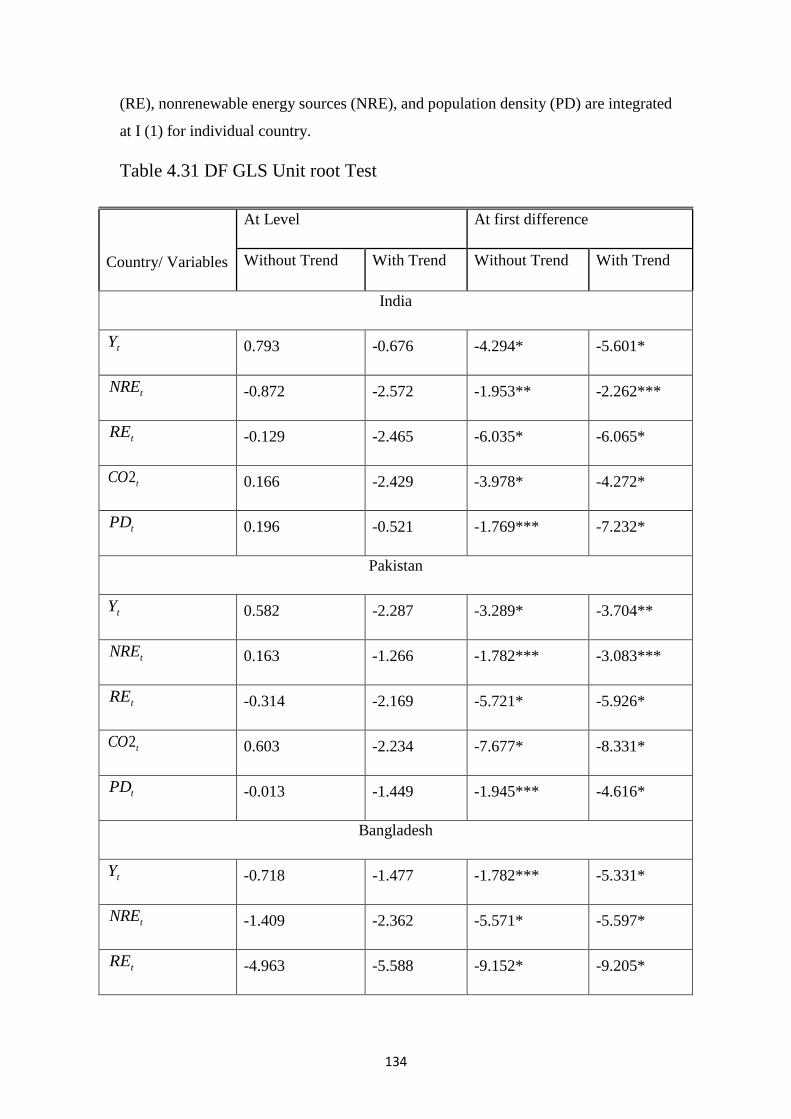

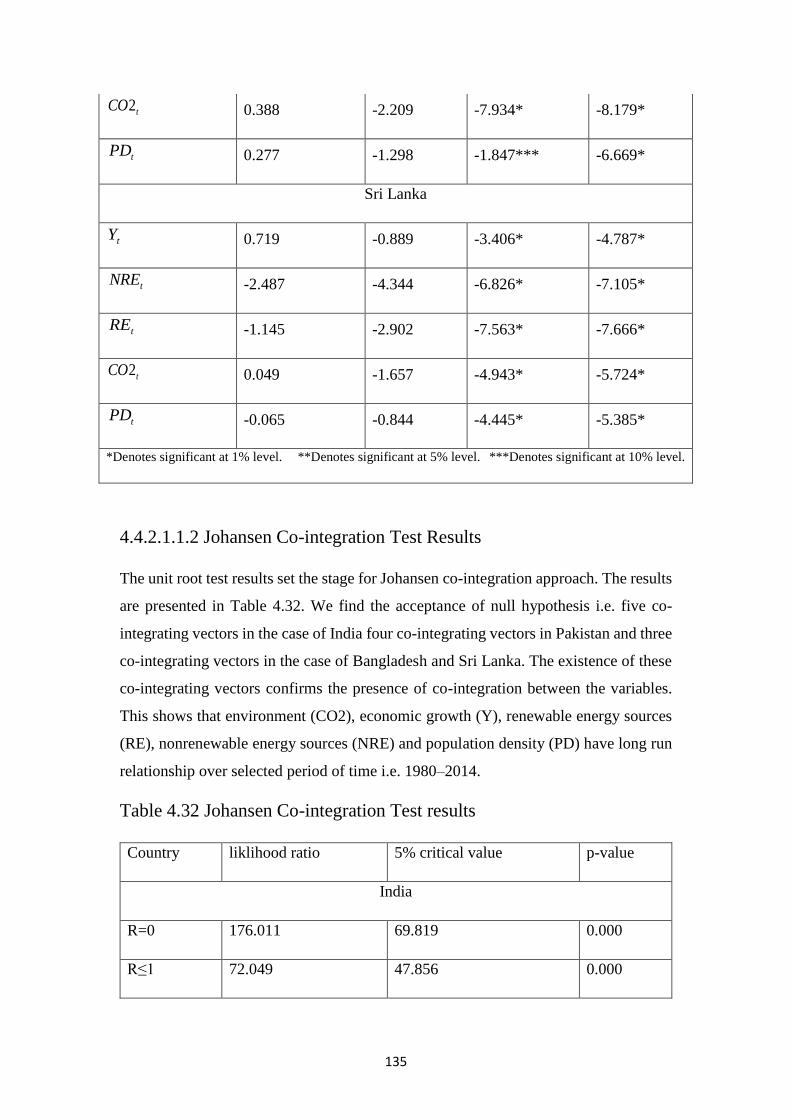

4.4.2.1.1.1 Unit Root Test Results…………………….…..……………………..….133

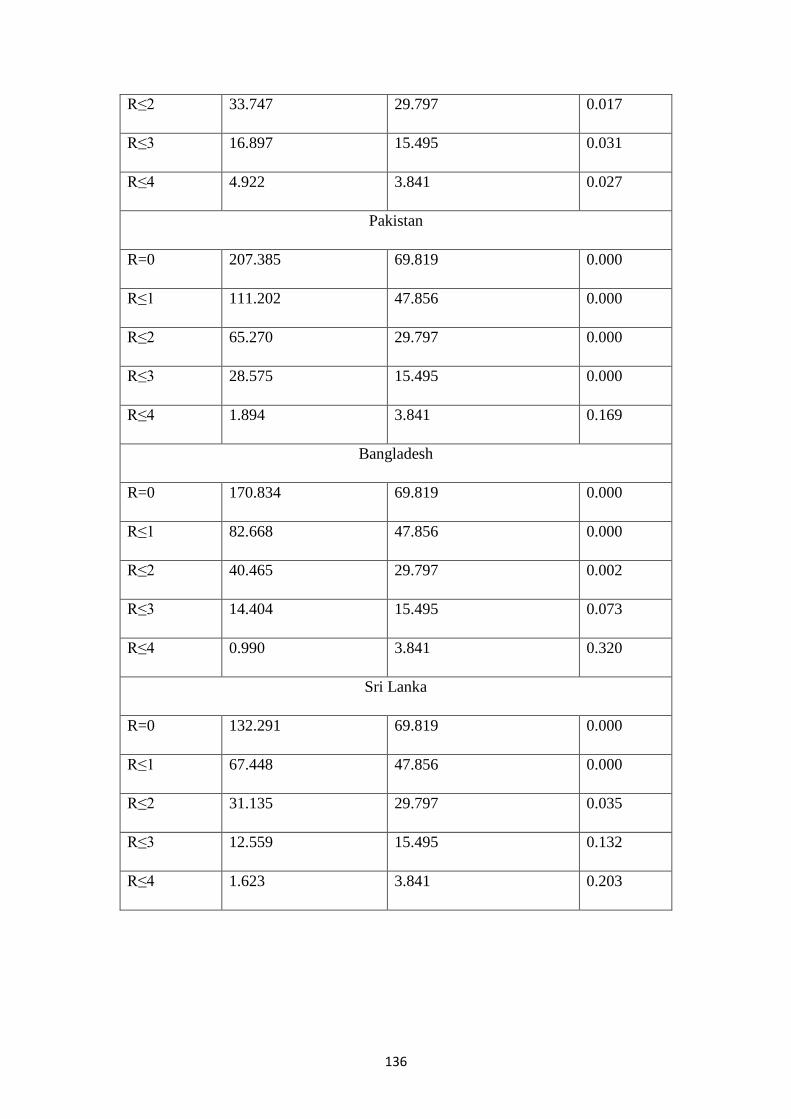

4.4.2.1.1.2 Johansen Co-integration Test Results……..…...…………...…………...135

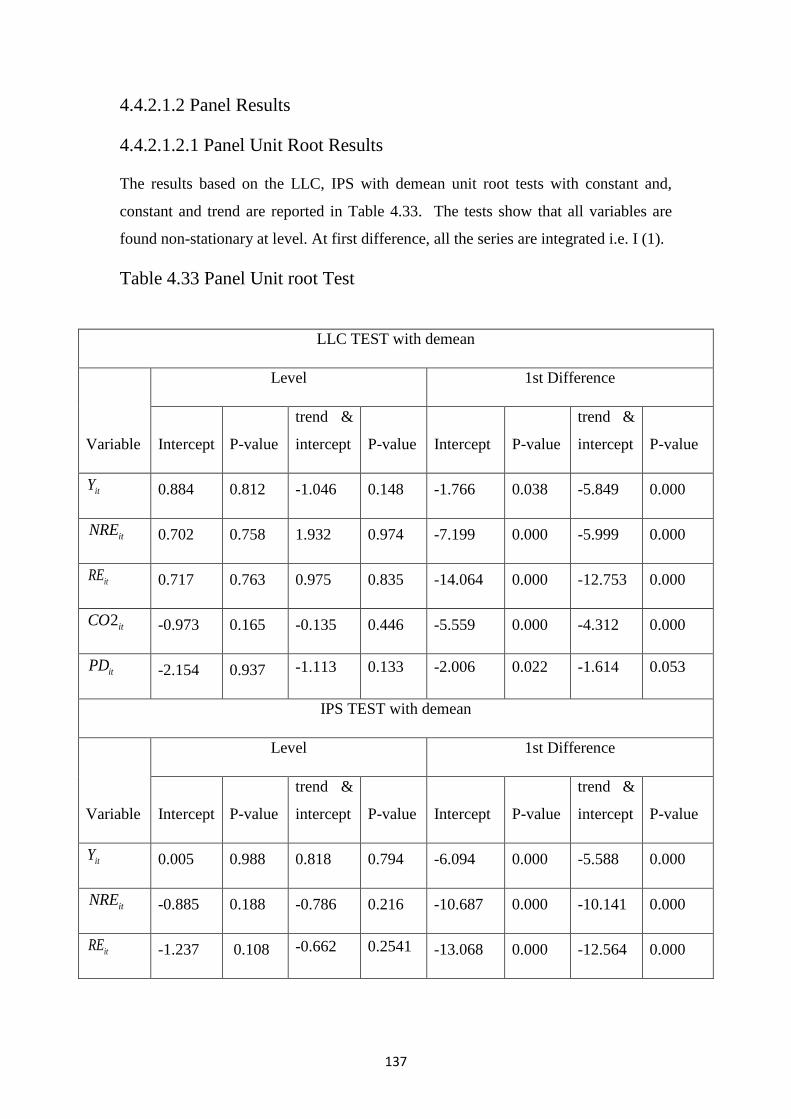

4.4.2.1.2 Panel Results…………………………………….……………………...…137

4.4.2.1.2.1 Panel Unit Root Results…………………………………………………137

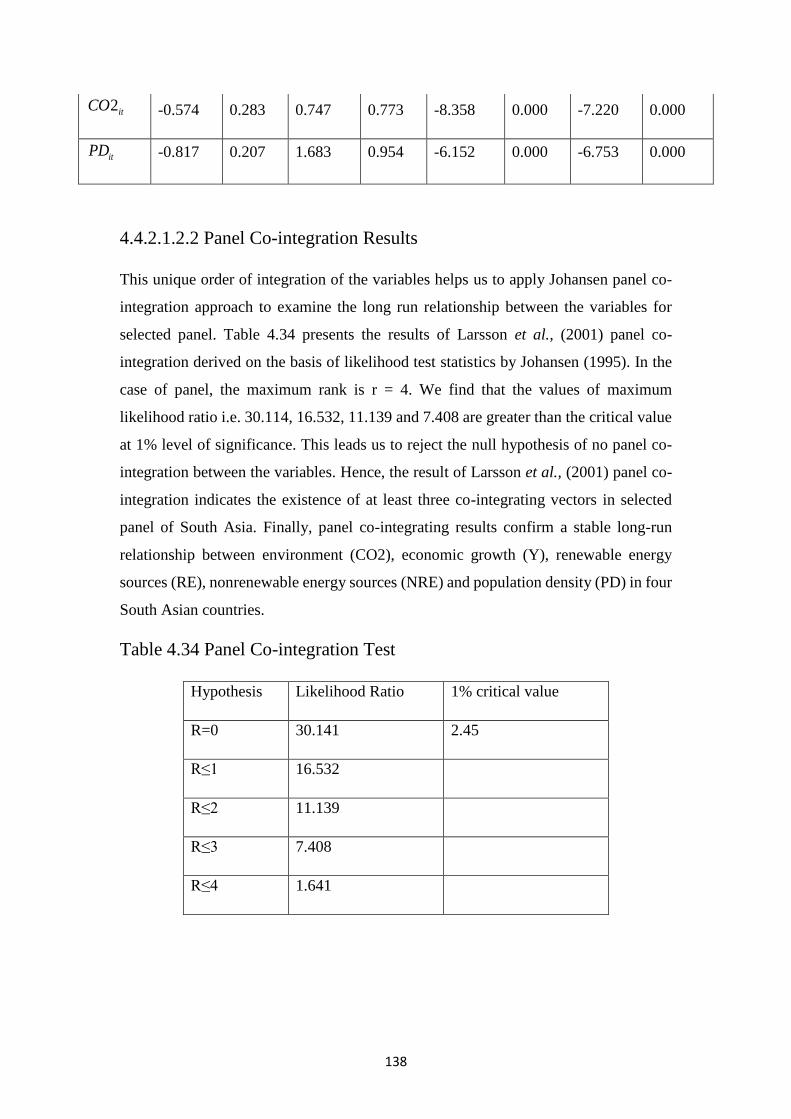

4.4.2.1.2.2 Panel Co-integration Results………...………………………………..…138

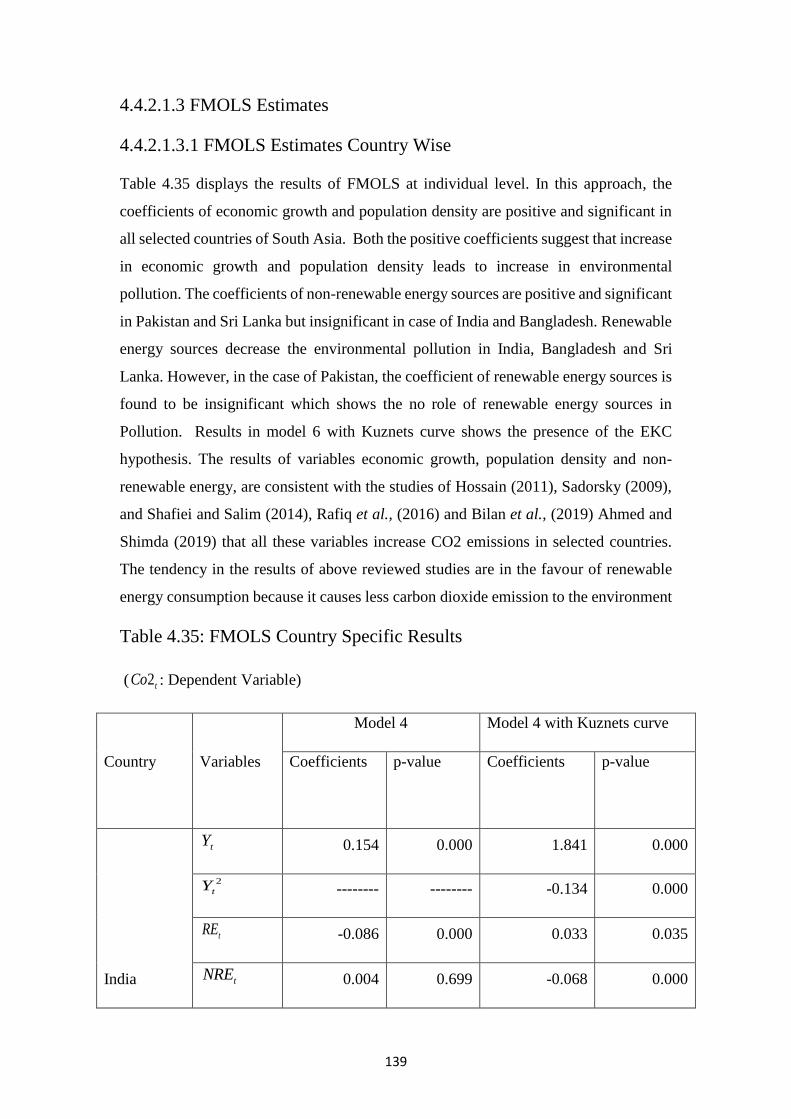

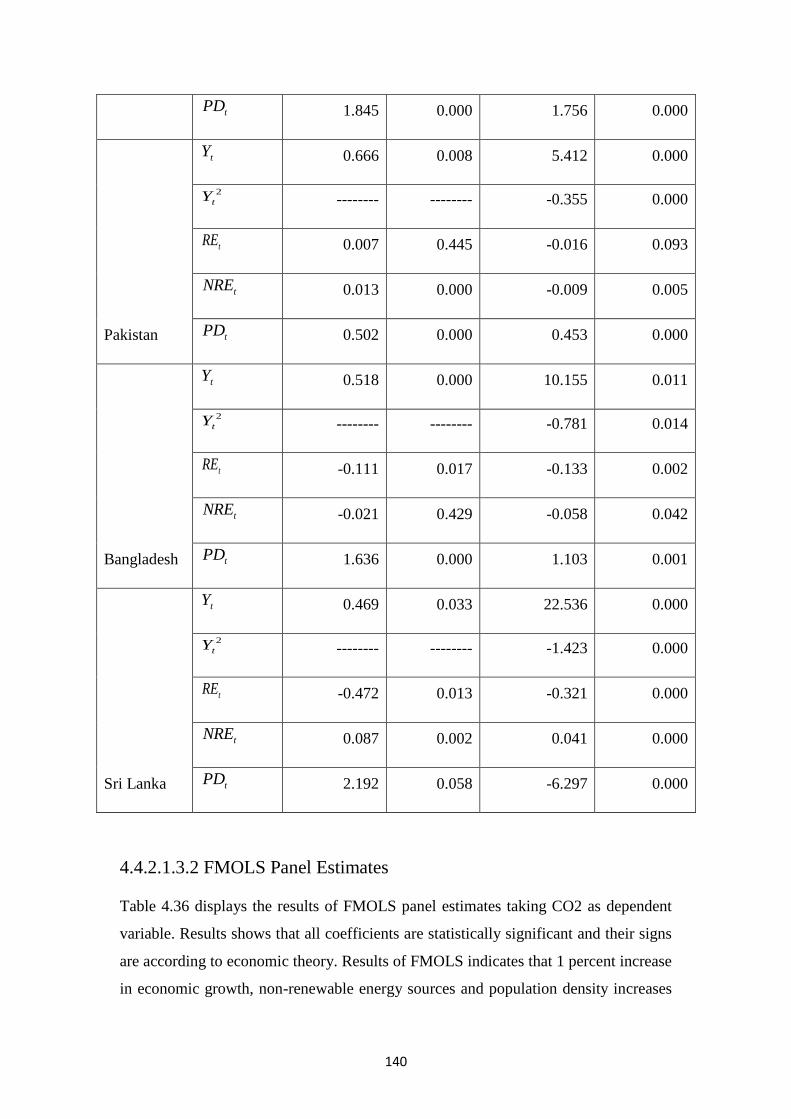

4.4.2.1.3 FMOLS Estimates…………………..………………………………..……139

4.4.2.1.3.1 FMOLS Estimates Country Wise……………………………………..…139

4.4.2.1.3.2 FMOLS Panel Estimates……...……..………………………………..…140

4.4.2.1.3.4 Panel Causality Results………………………………………….………142

xiii

4.4.2.2 Model 5: Relationship between Renewable and Non-renewable Energy,

Urbanization, Energy Intensity and Environment…..………………………...…….143

4.4.2.2.1 Time Series Results………………………………..………………………143

4.4.2.2.1.1 Unit Root Test Results…………………….…..……………………..….143

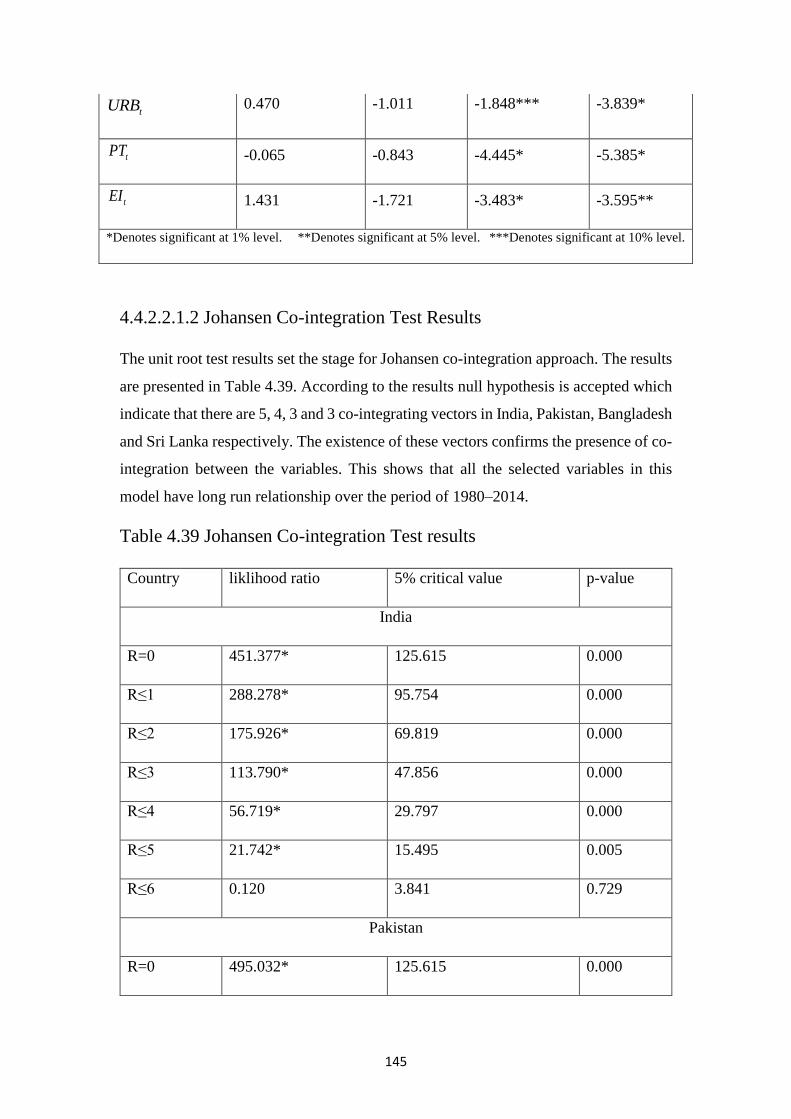

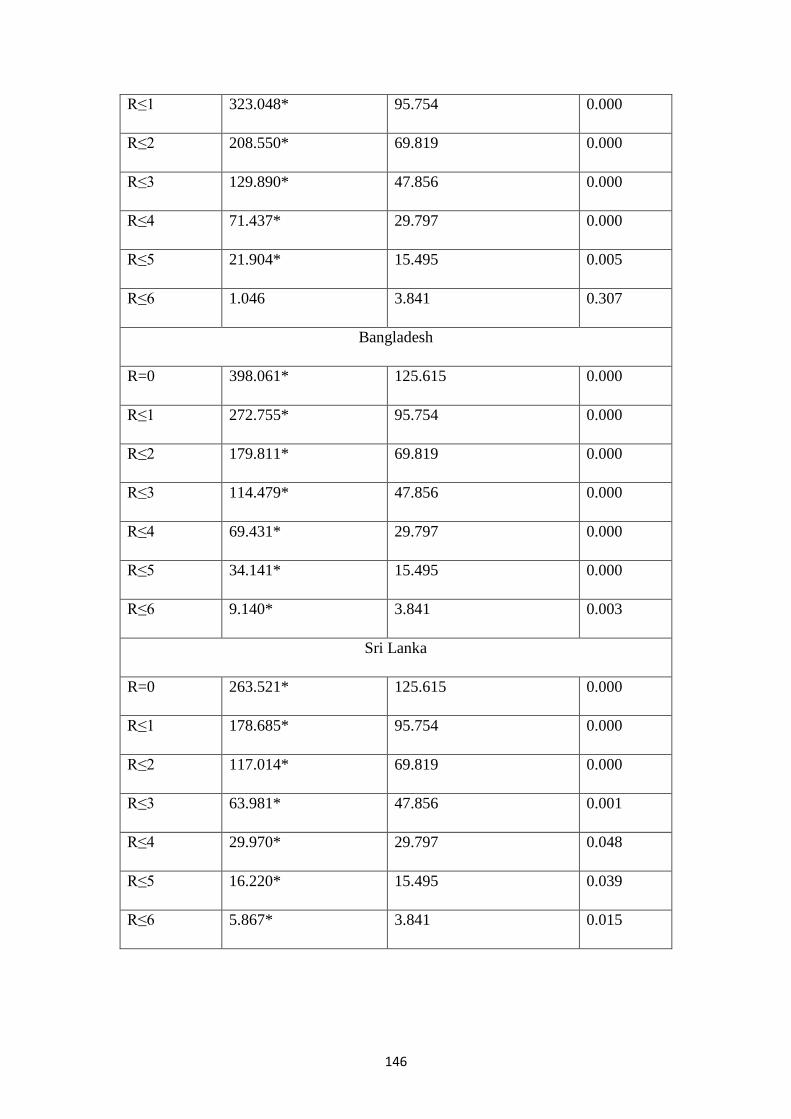

4.4.2.2.1.2 Johansen Co-integration Test Results……..…...…………...…………...145

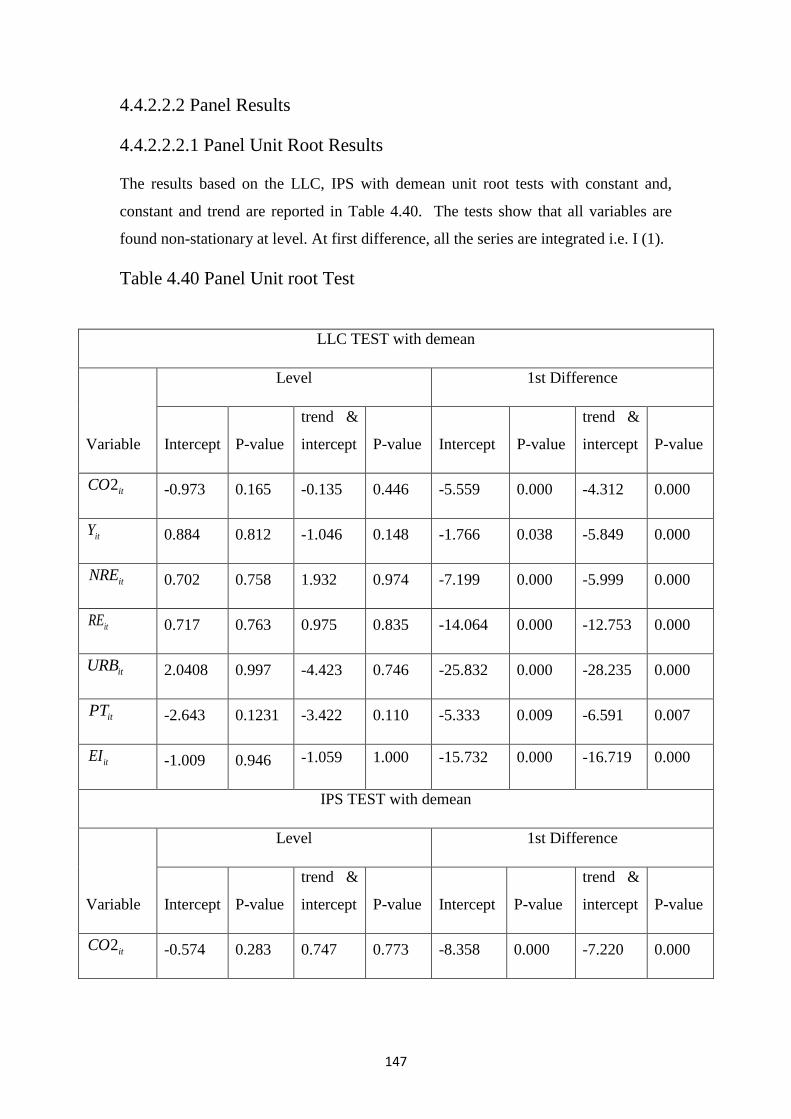

4.4.2.2.2 Panel Results…………………………………….……………………...…147

4.4.2.2.2.1 Panel Unit Root Results…………………………………………………147

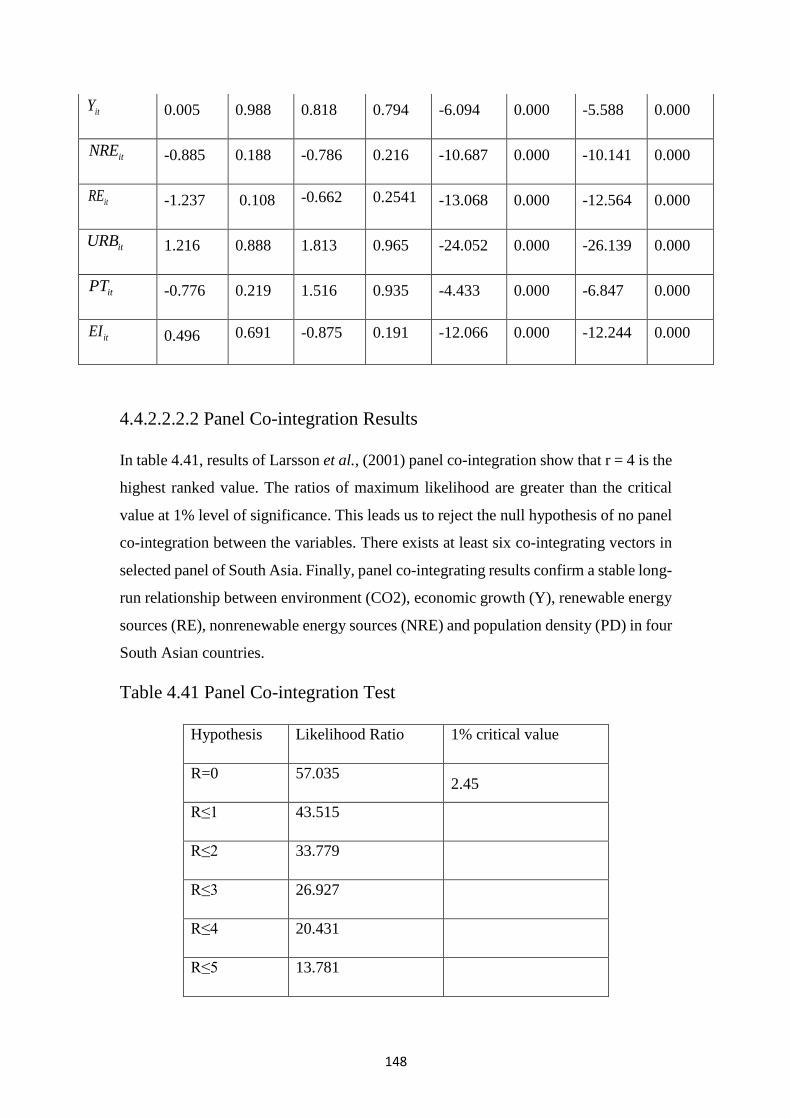

4.4.2.2.2.2 Panel Co-integration Results………...………………………………..…148

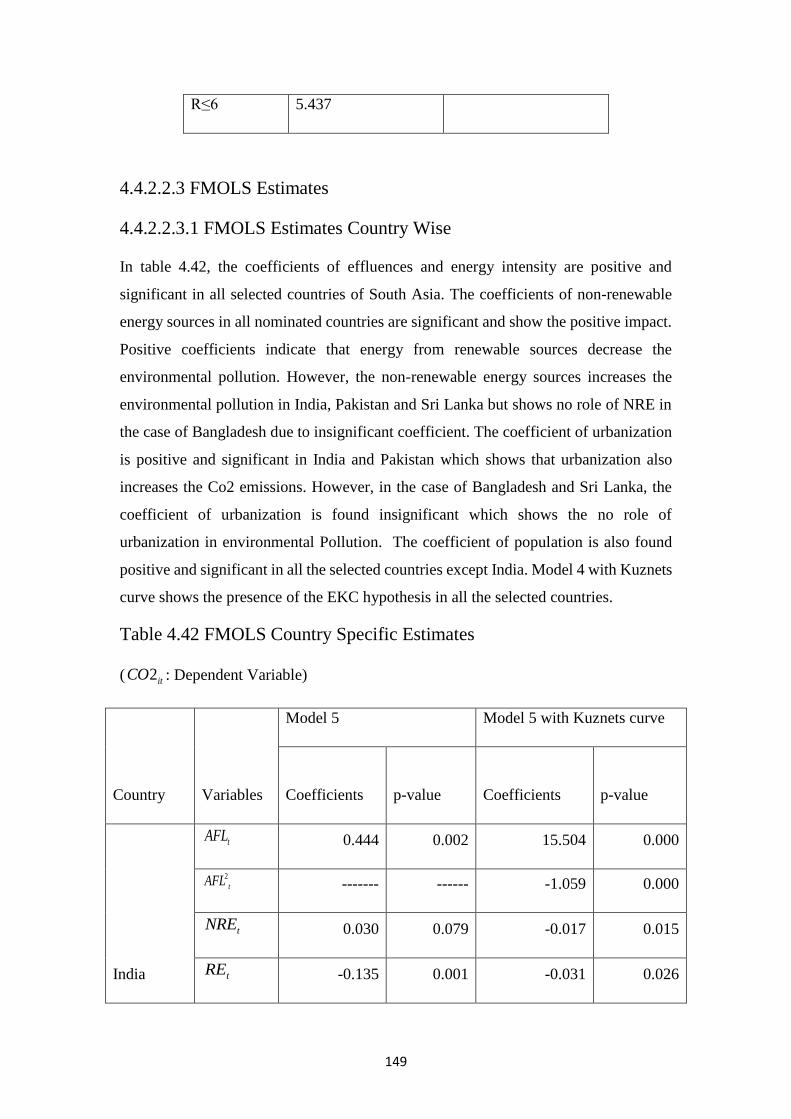

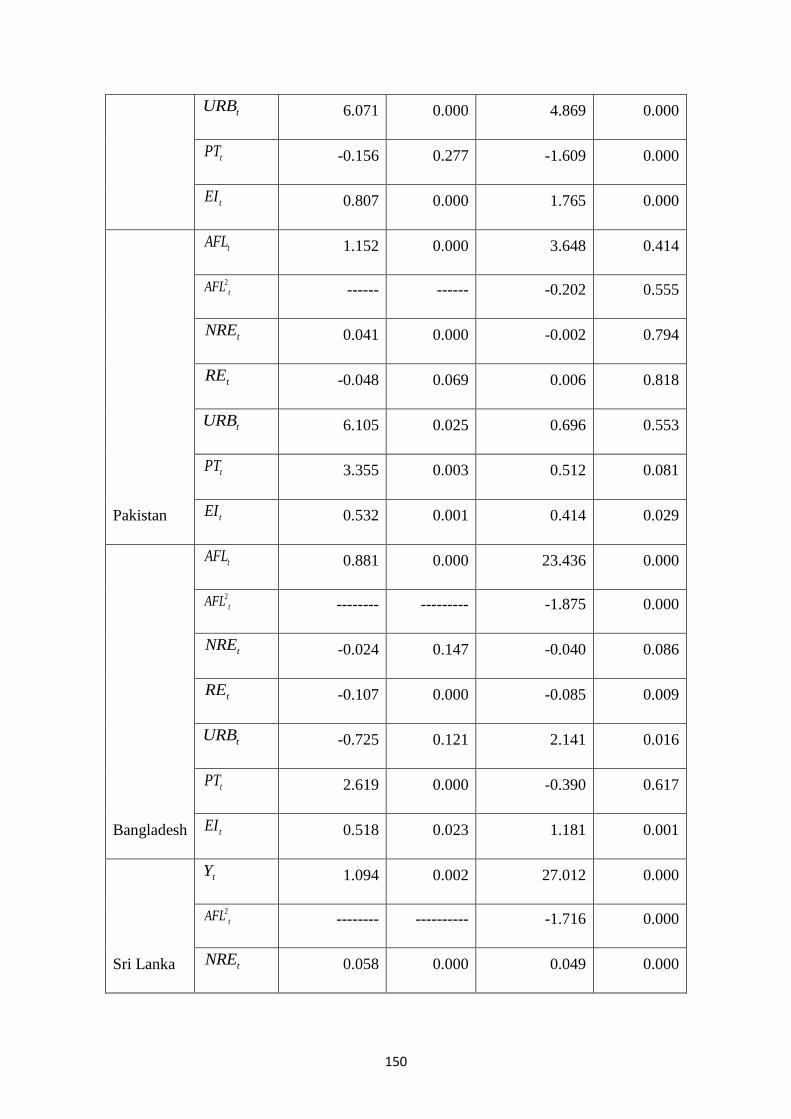

4.4.2.2.3 FMOLS Estimates…………………..………………………………..……149

4.4.2.2.3.1 FMOLS Estimates Country Wise……………………………………..…149

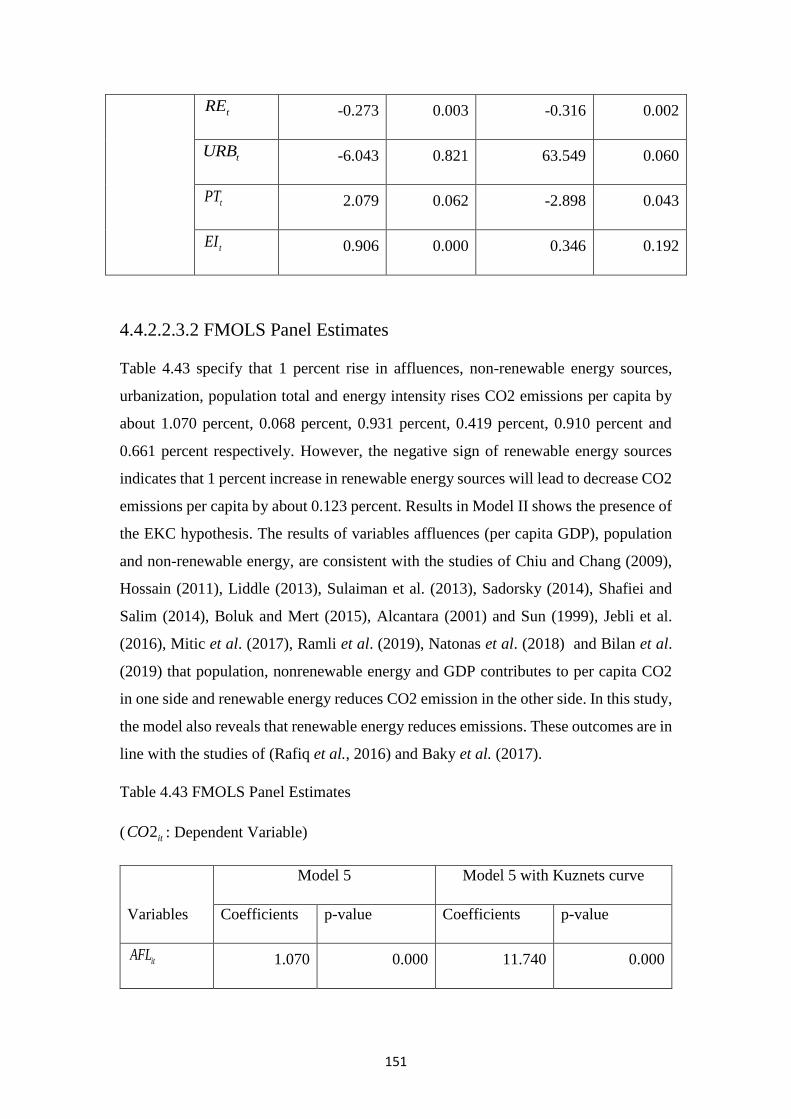

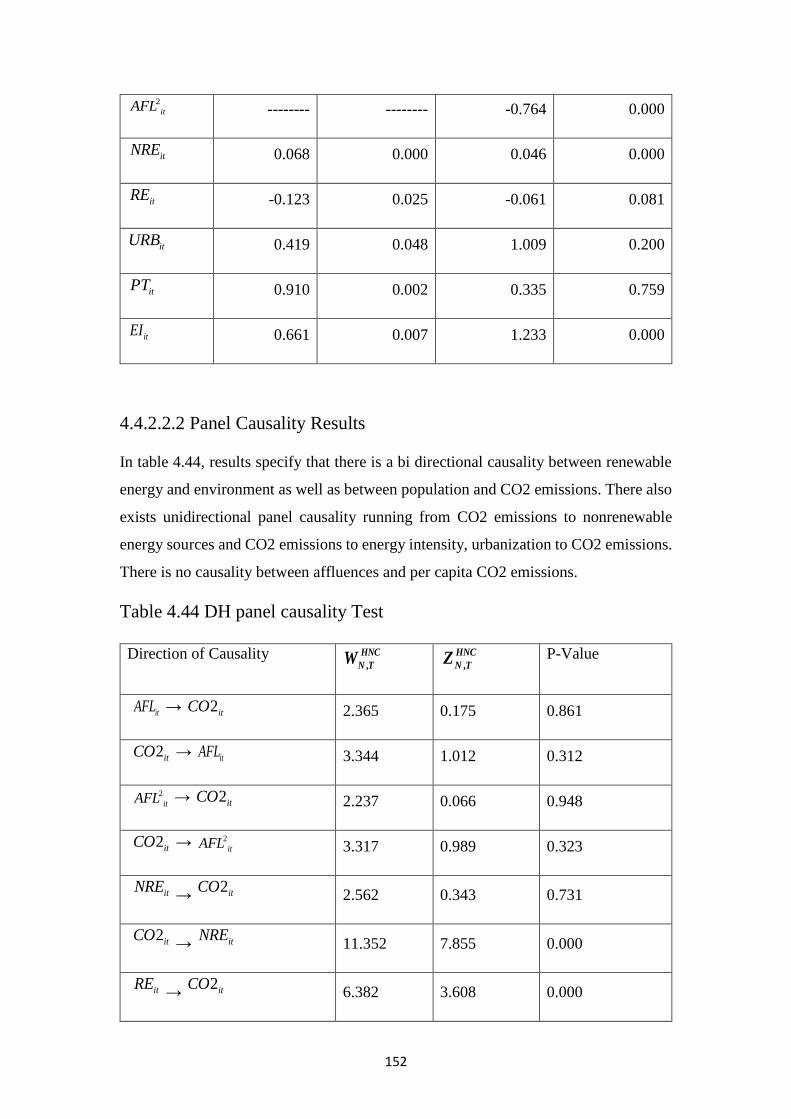

4.4.2.2.3.2 FMOLS Panel Estimates……...……..…………………………………..151

4.4.2.2.3.4 Panel Causality Results………………………………………….………152

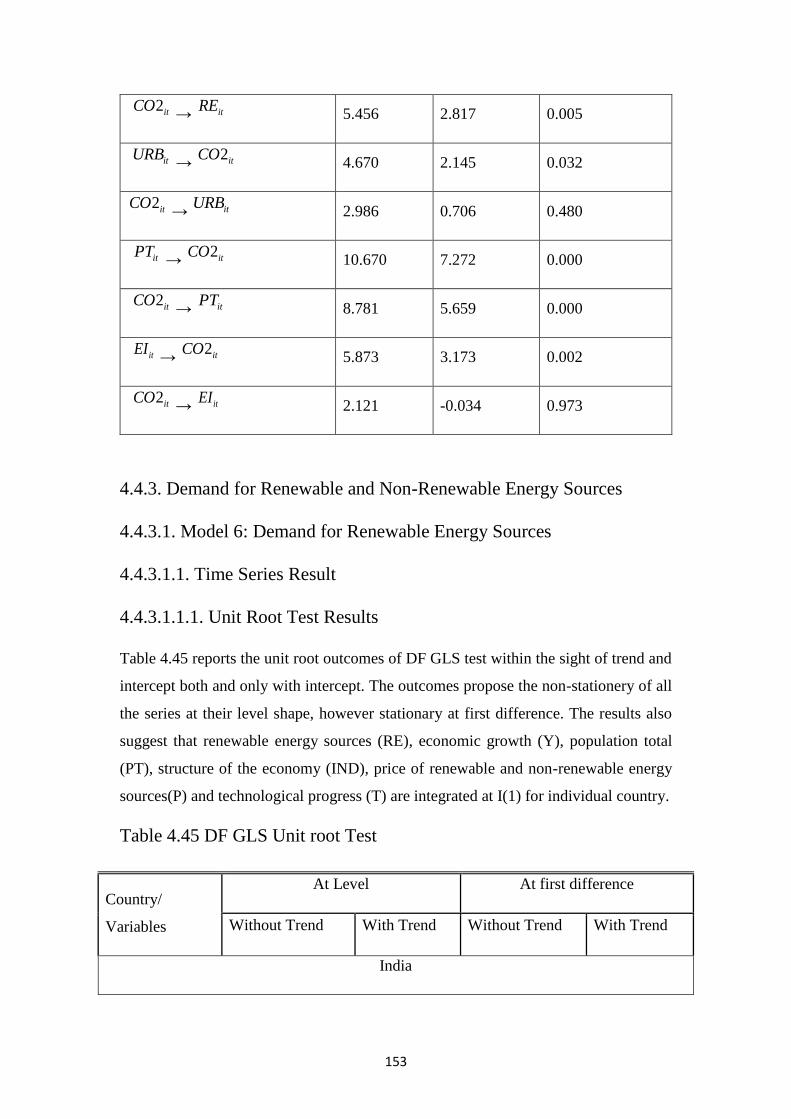

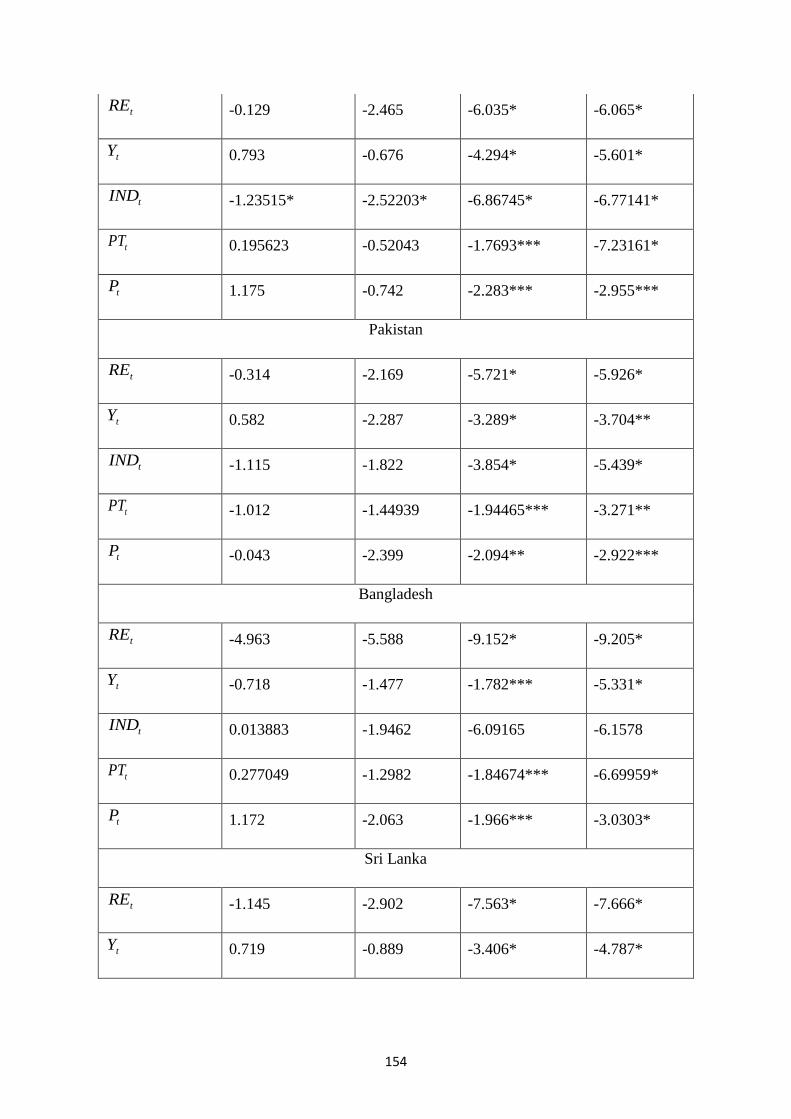

4.4.3 Demand for Renewable and Non-Renewable Energy Sources…………...……153

4.4.3.1 Model 6: Demand for Renewable Energy Sources……………………….….153

4.4.3.1.1 Time Series Results…………………………………………………….….153

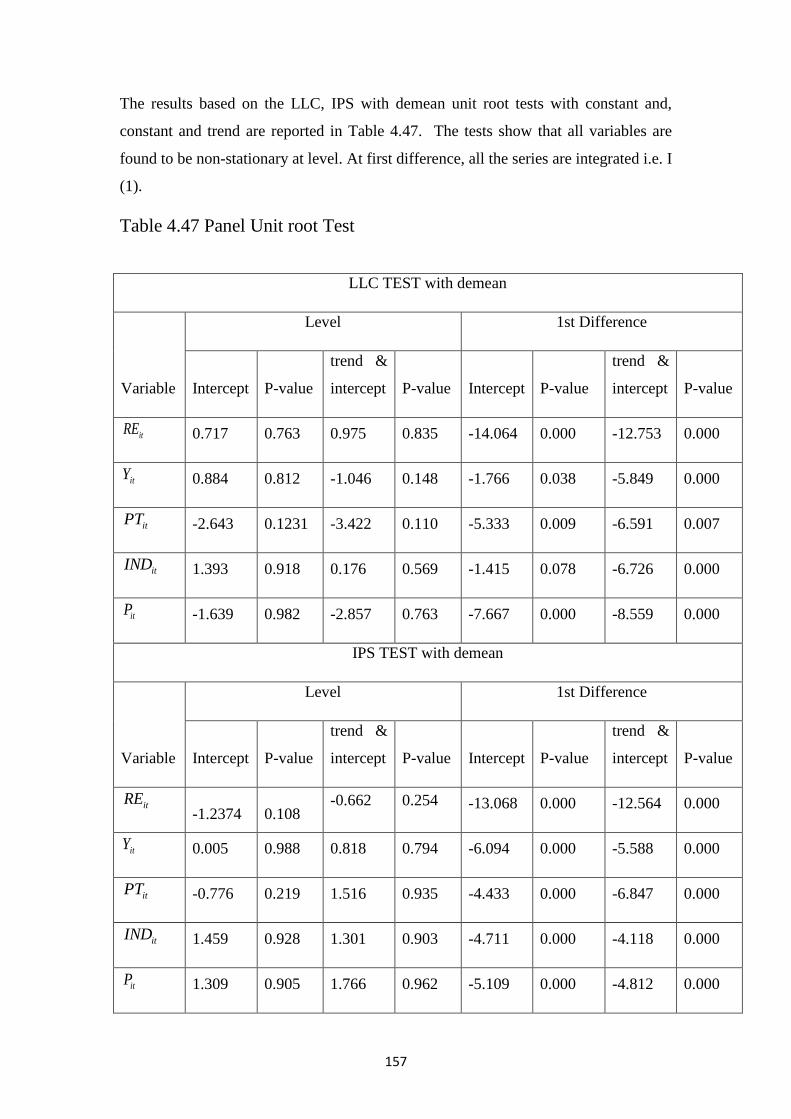

4.4.3.1.1.1 Unit Root Test Results……………………………………………...…...153

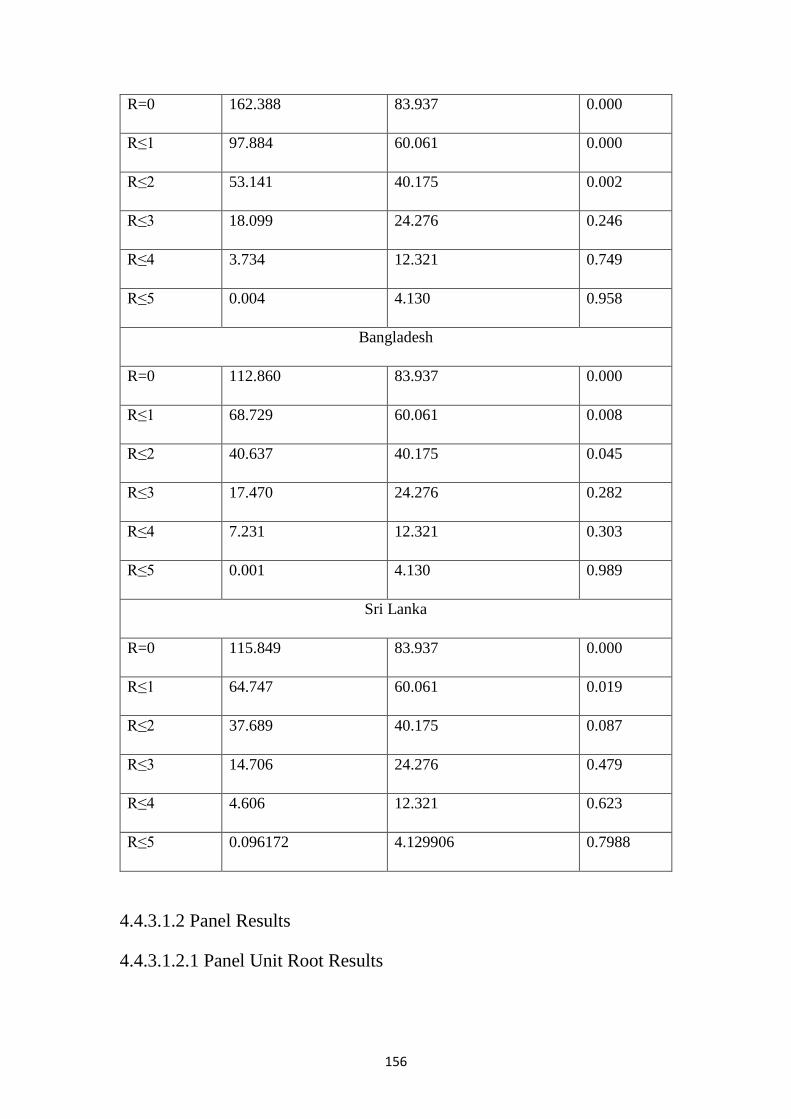

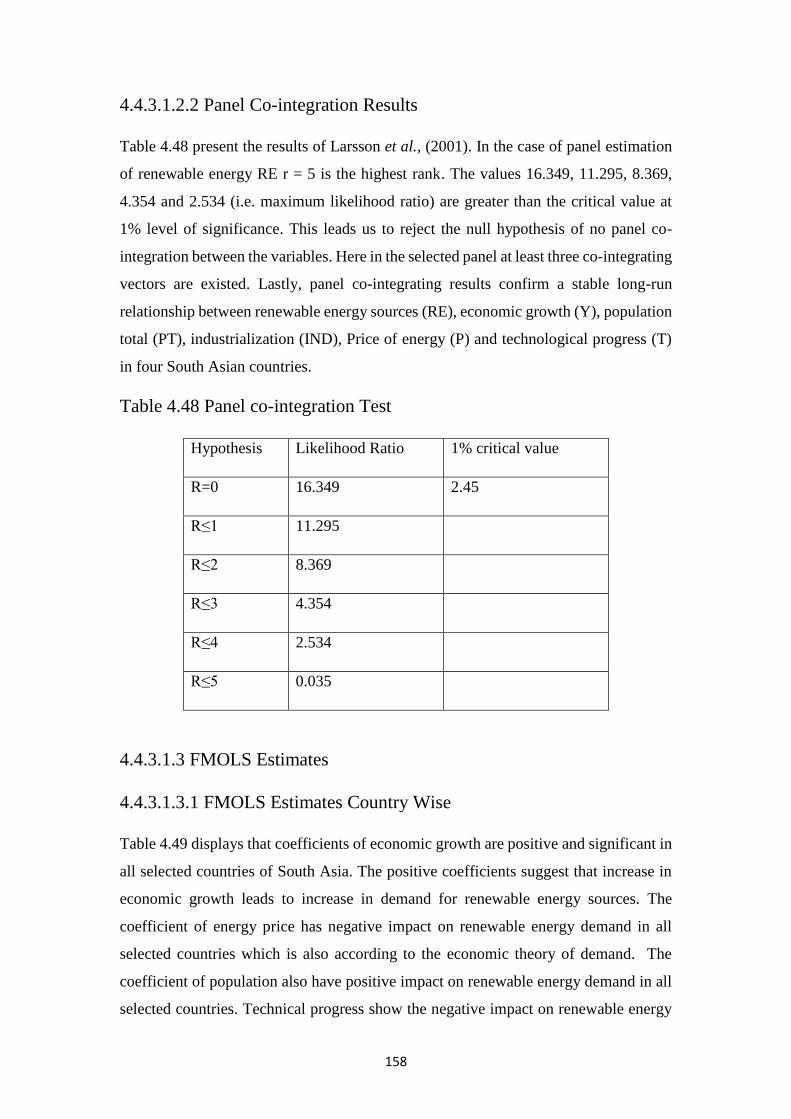

4.4.3.1.1.2 Johansen Co-integration Test Results………………………………...…158

4.4.3.1.2 Panel Results……...…………………………………….…………………156

4.4.3.1.2.1 Panel Unit Root Results…………..…………………………..…...…….156

4.4.3.1.2.2 Panel Co-integration Results……………………………………..……...158

4.4.3.1.3 FMOLS Estimates……………………………………………………...….158

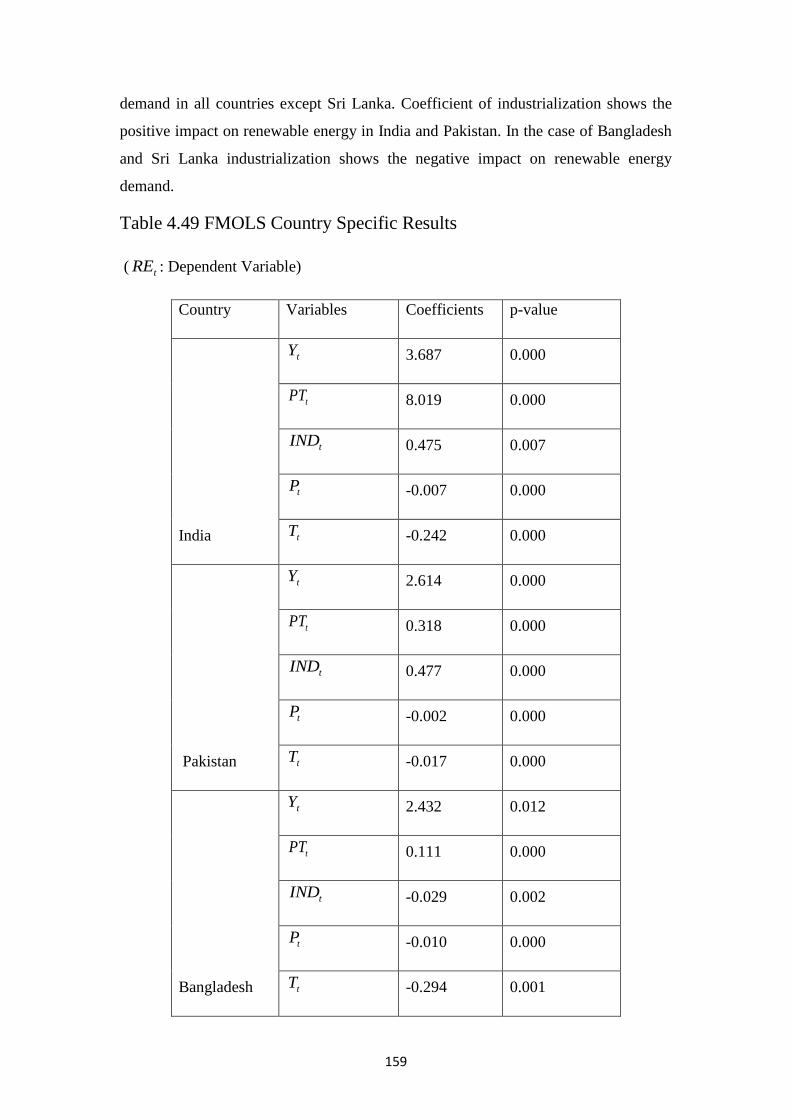

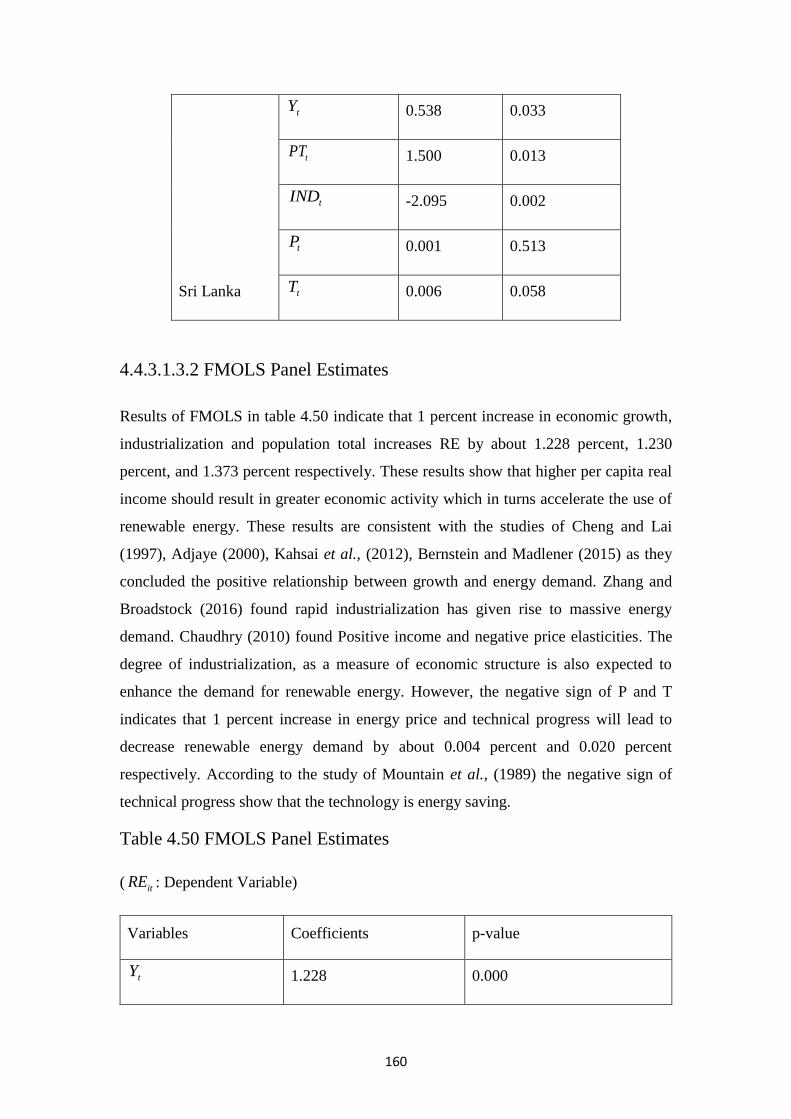

4.4.3.1.3.1 FMOLS Estimates Country Wise………………………………..………158

4.4.3.1.3.2 FMOLS Panel Estimates………………………………………………...160

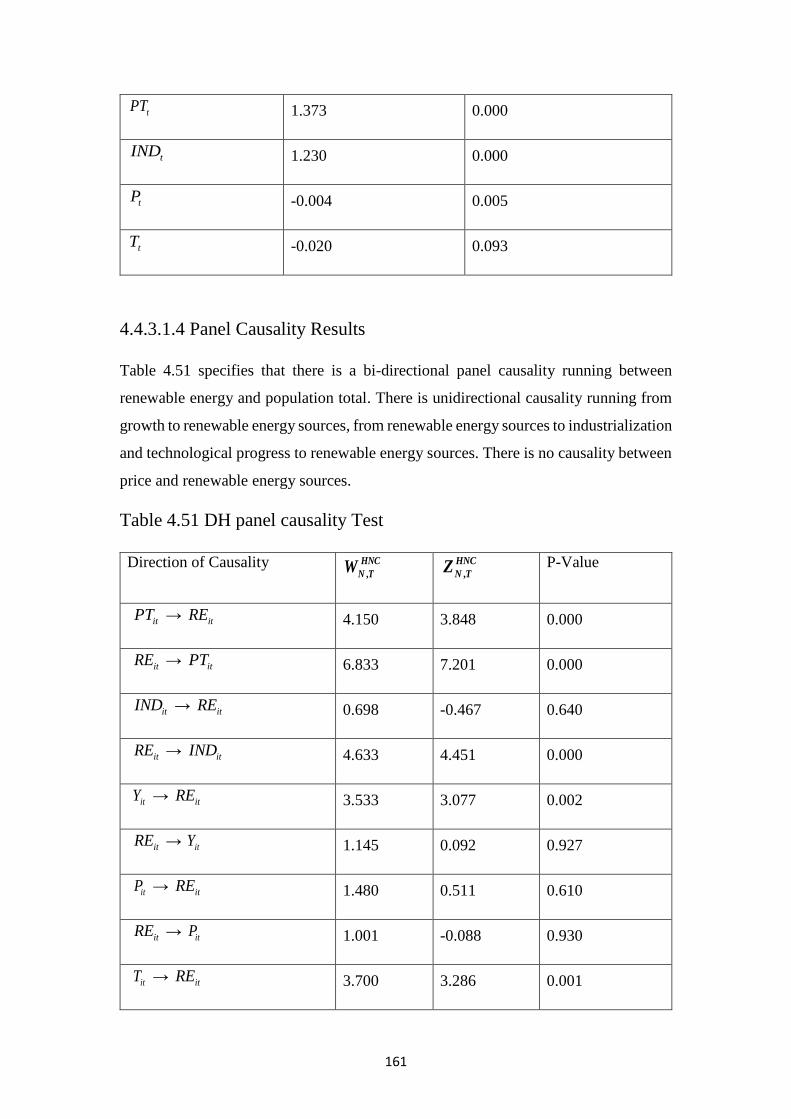

4.4.3.1.4 Panel Causality Results……………………………………………………161

4.4.3.1.5 Test of Forecasting Renewable Energy Demand…………………………162

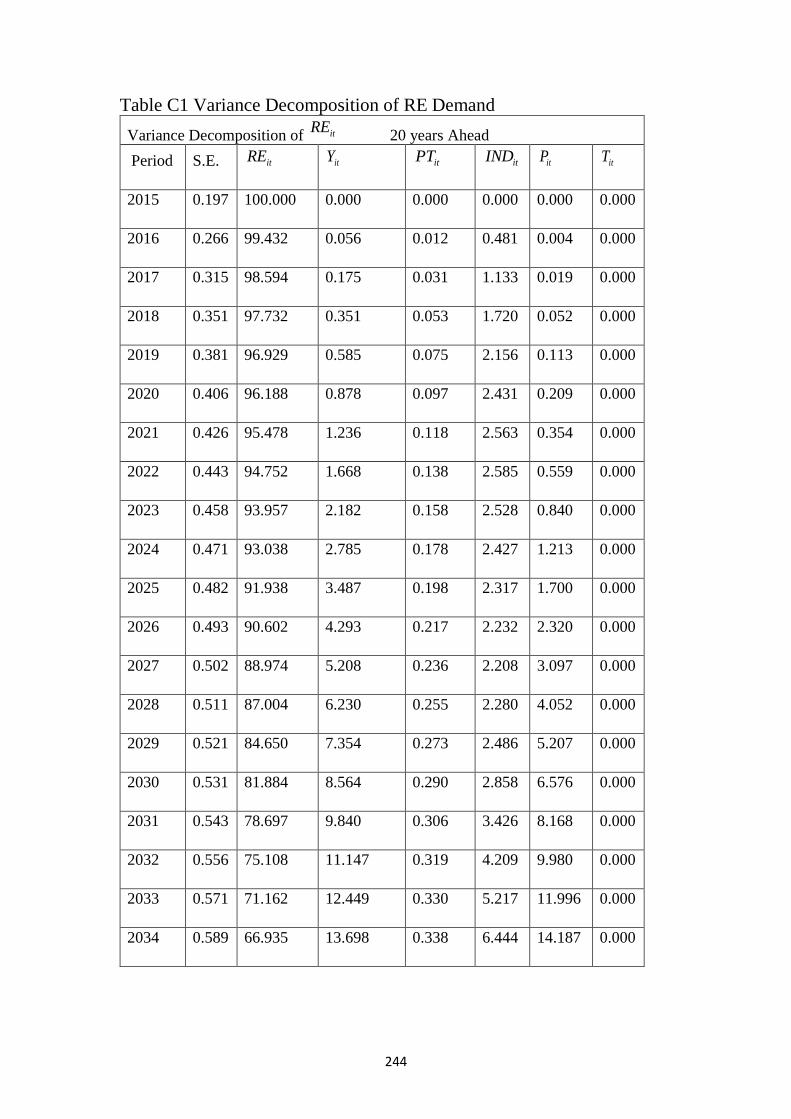

4.4.3.1.5.1 Variance Decomposition of RE Demand…...………………...…….…...162

xiv

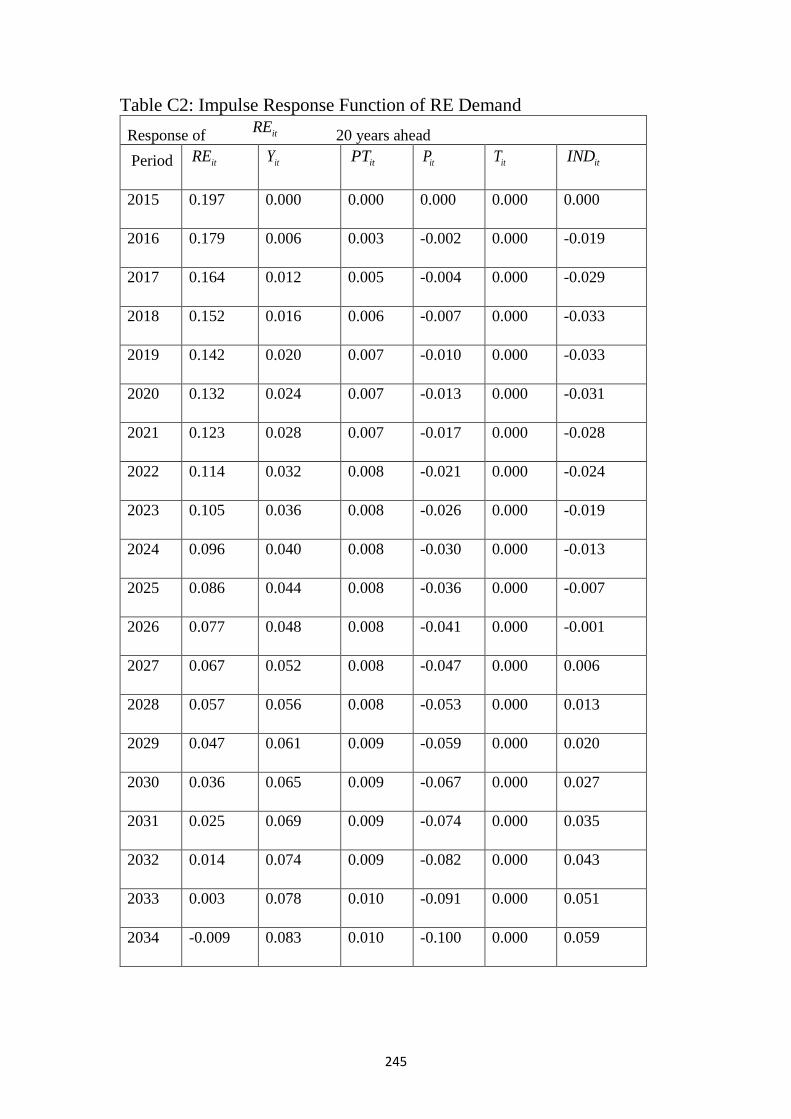

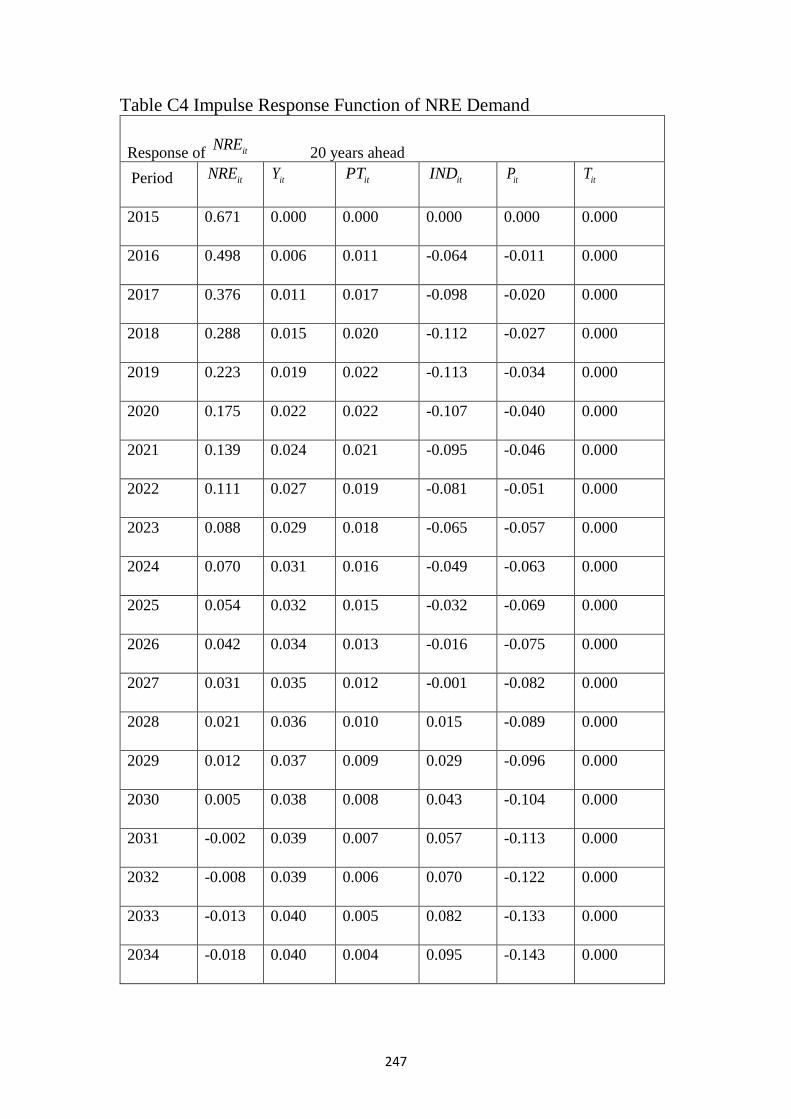

4.4.3.1.5.2 Impulse Response Function of RE Demand…………………………......162

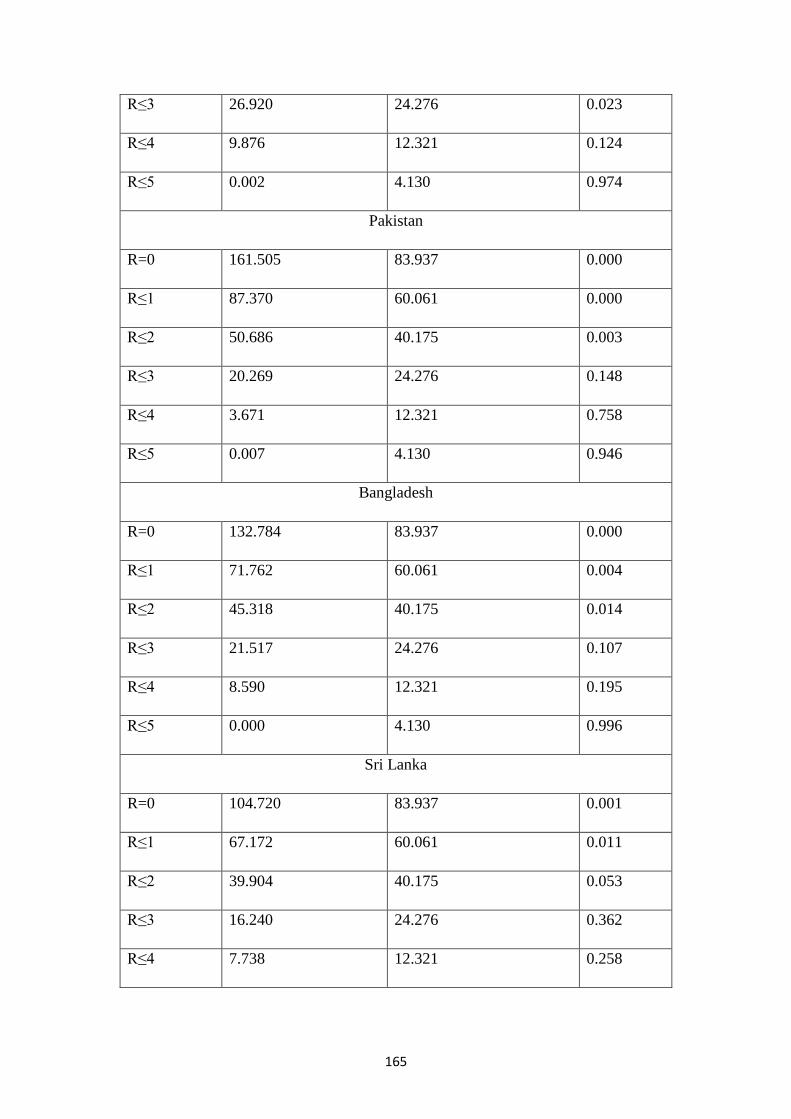

4.4.3.2. Model 7: Demand for Non-Renewable Energy Sources…………...………..162

4.4.3.2.1 Time Series Results…….………………….………………………………162

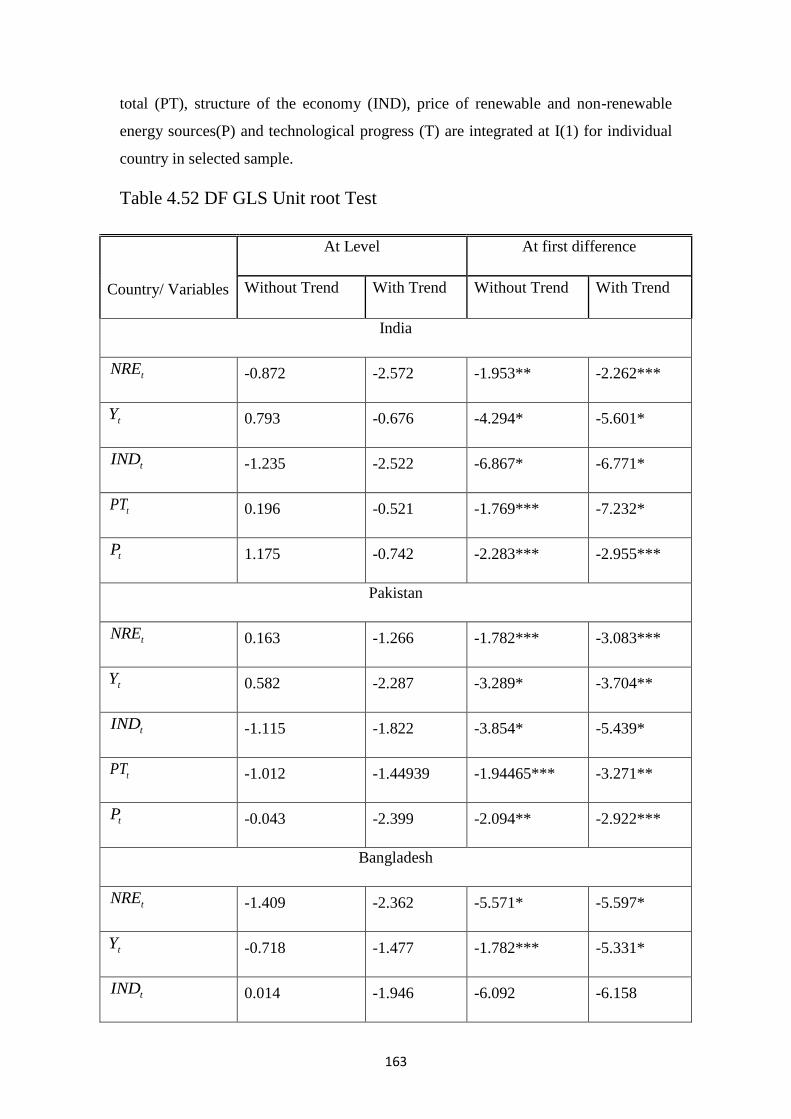

4.4.3.2.1.1 Unit Root Test Results……………………………………………….….162

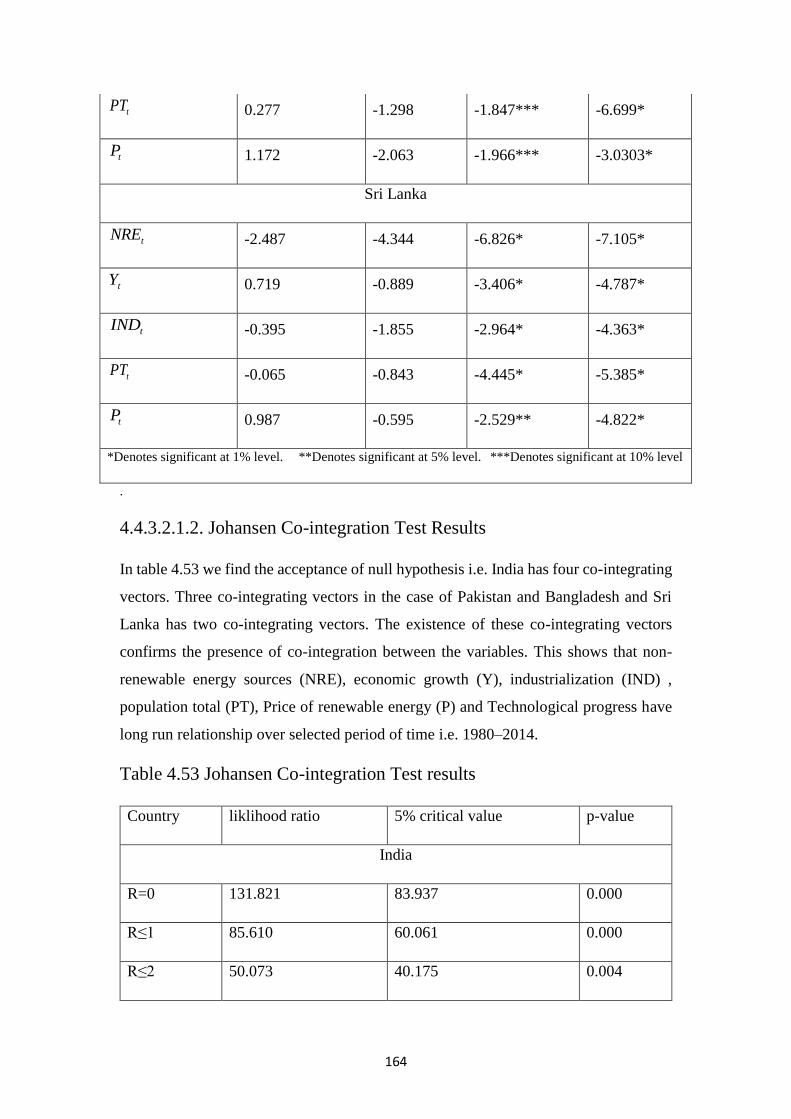

4.4.3.2.1.2 Johansen Co-integration Test Results…………………………………...164

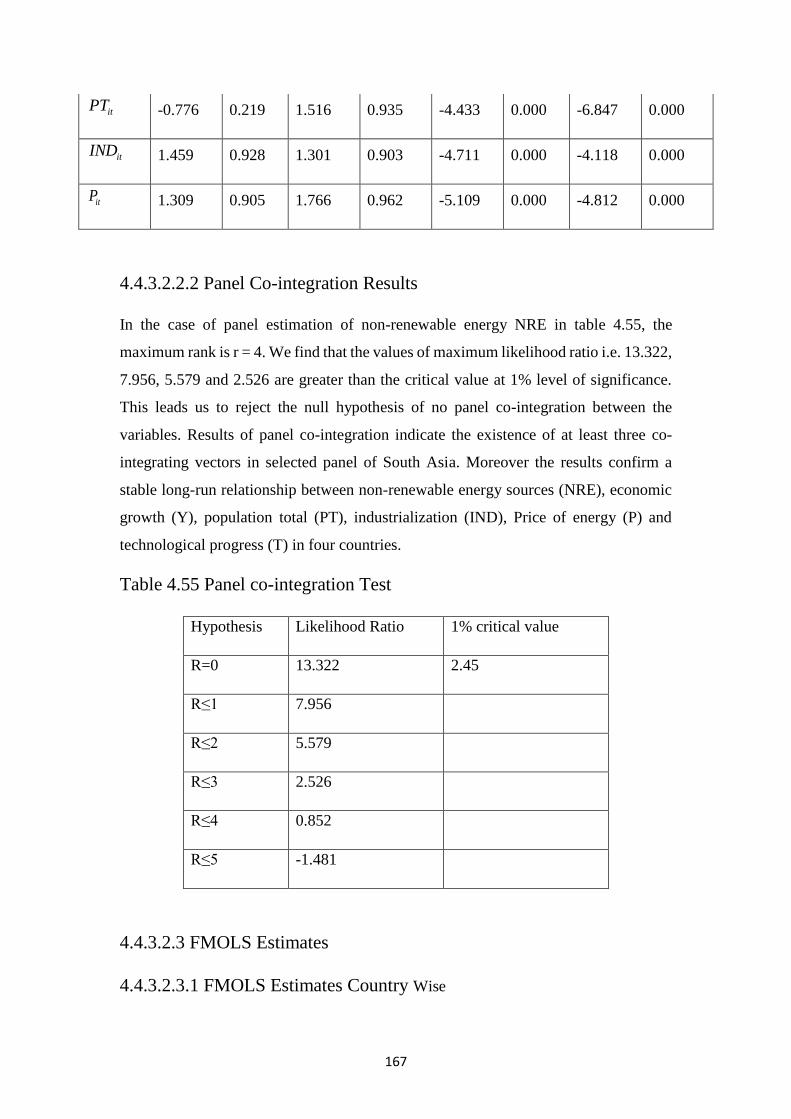

4.4.3.2.2 Panel Results..……………………………………………………………..166

4.4.3.2.2.1 Panel Unit Root Results…………………………………………………166

4.4.3.2.2.2 Panel Co-integration Results…………………………………………….167

4.4.3.2.3 FMOLS Estimates……………………………………………….………...167

4.4.3.2.3.1 FMOLS Estimates Country Wise………………………………….…….167

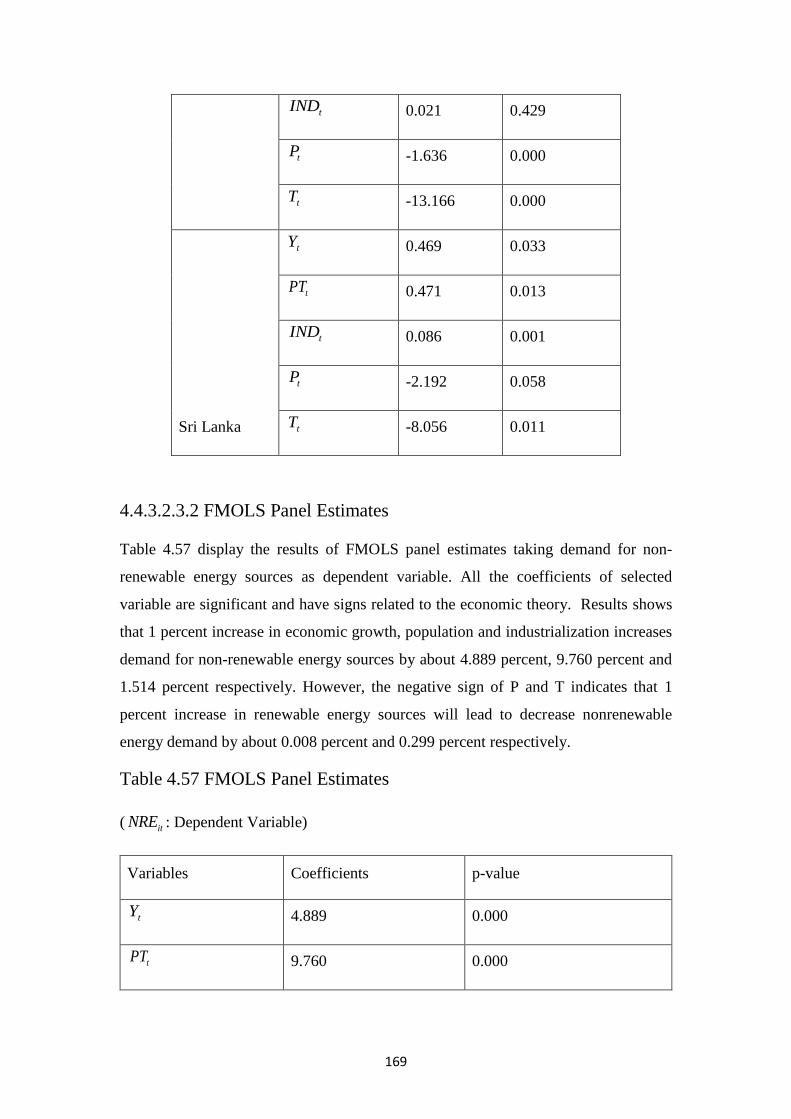

4.4.3.2.3.2 FMOLS Panel Estimates…………………………………………….…..169

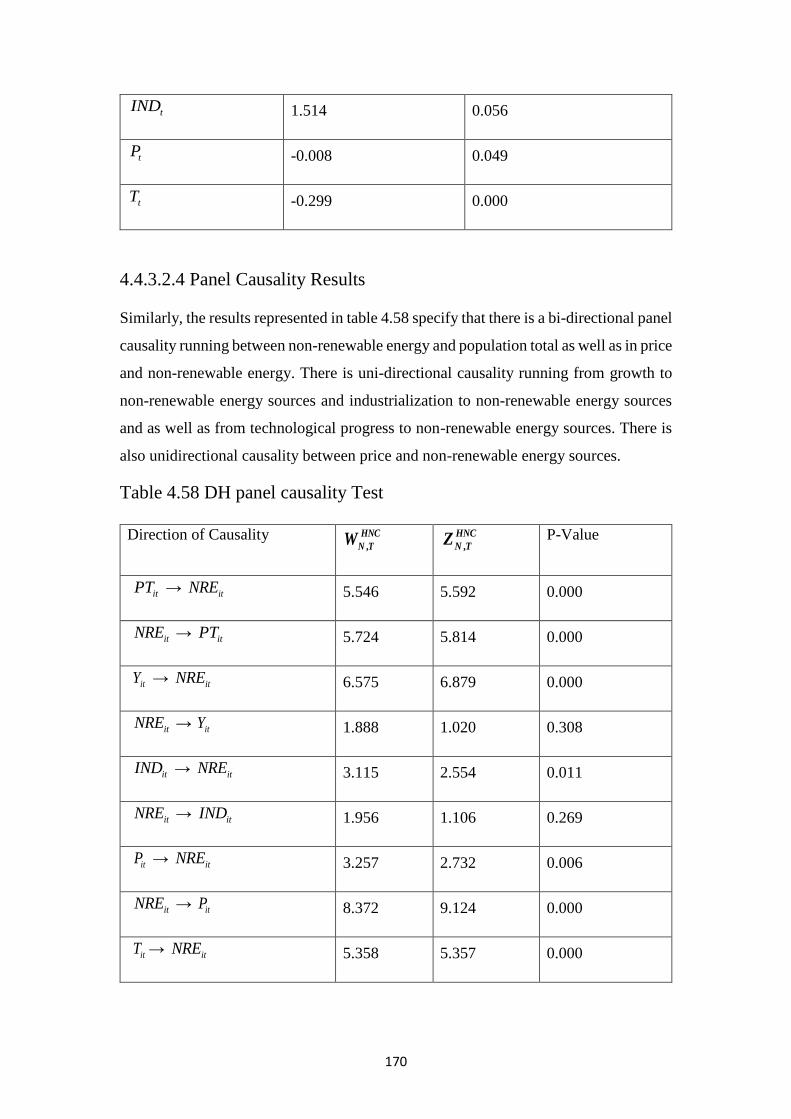

4.4.3.2.4 Panel Causality Results………………………………………………....…170

4.4.3.2.5 Test of Forecasting Non-Renewable Energy Demand……………………171

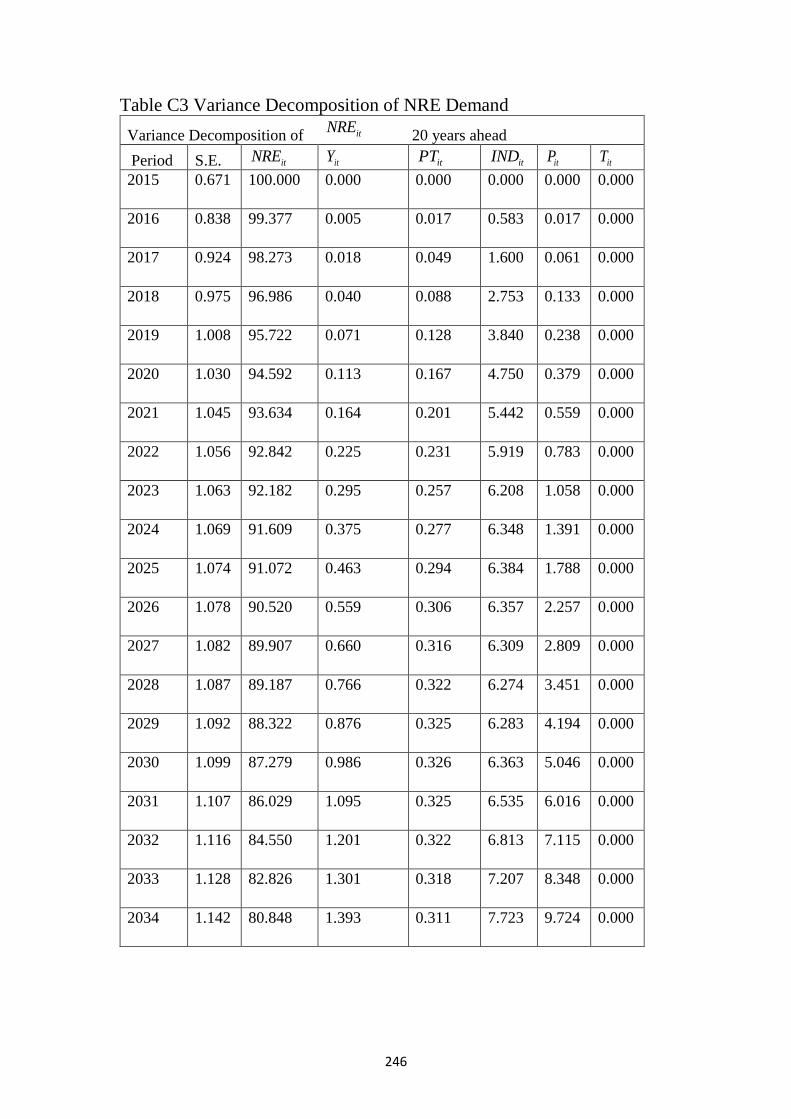

4.4.3.2.5.1 Variance Decomposition of NRE Demand……………………………...171

4.4.3.2.5.2 Impulse Response Function of NRE Demand…………………………...171

4.4.4. Impact of Renewable and Non-Renewable Energy Sources on Energy

Intensity……………………………………………………………………..171

4.4.4.1 Model 8: Relationship between Renewable and Non-renewable Energy,

Economic Growth, Urbanization and Energy Intensity ………………..……171

4.4.4.1.1 Time Series Results……….………………………………………….……171

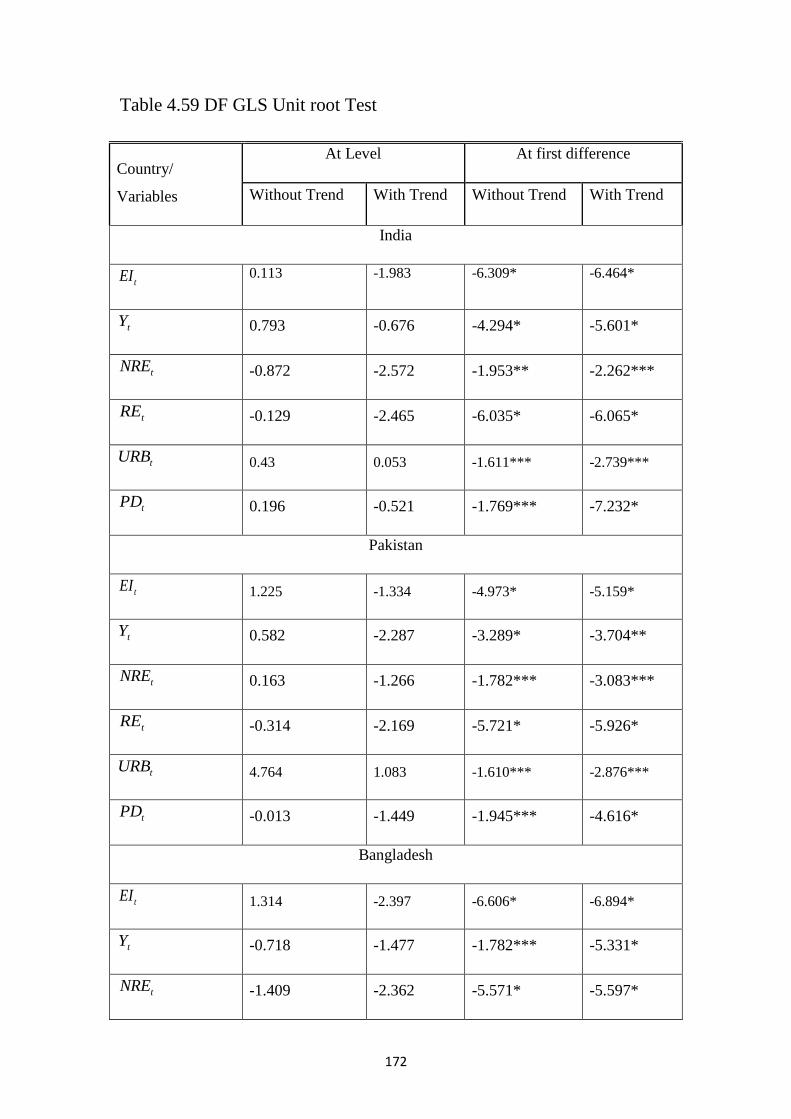

4.4.4.1.1.1 Unit Root Test Results….…………………………………………...…..171

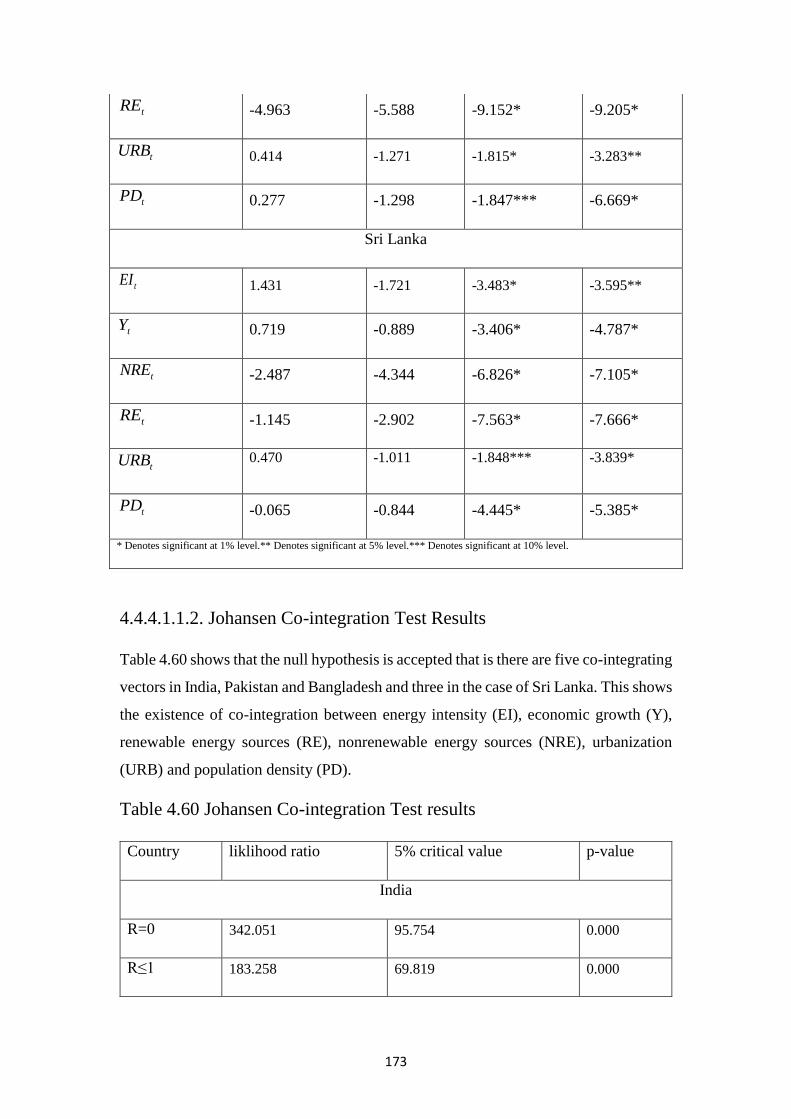

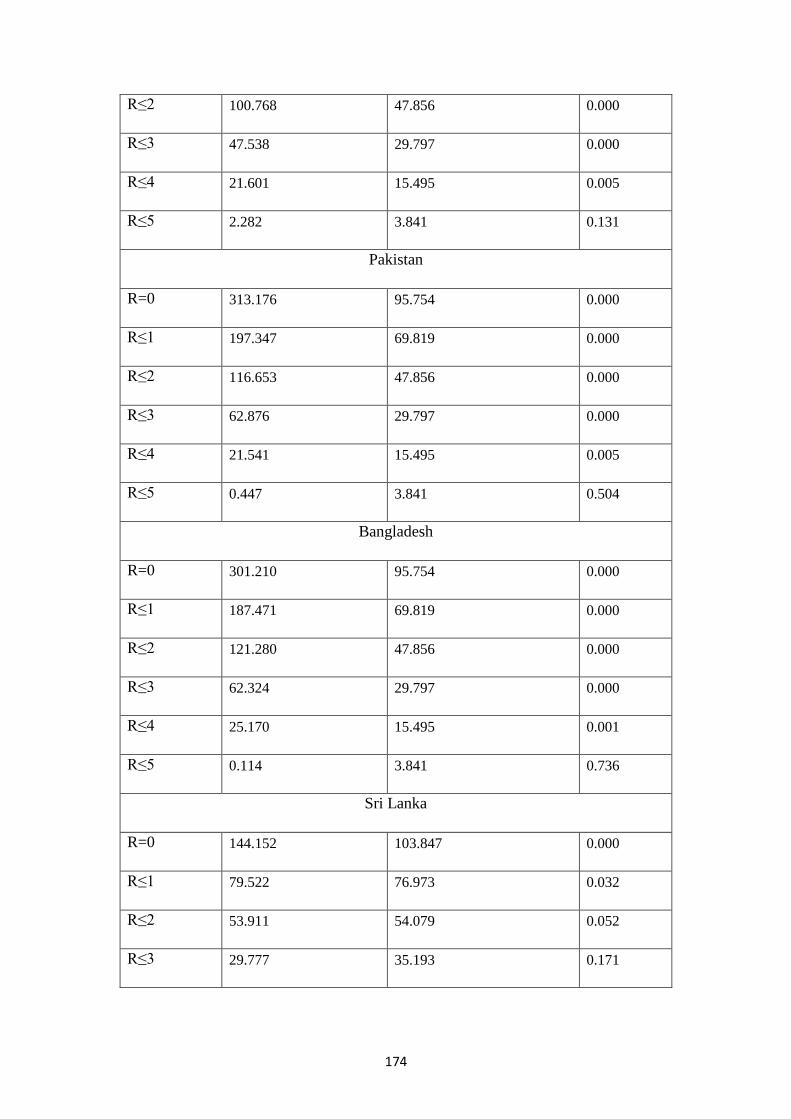

4.4.4.1.1.2 Johansen Co-integration Test Results………………………………...…173

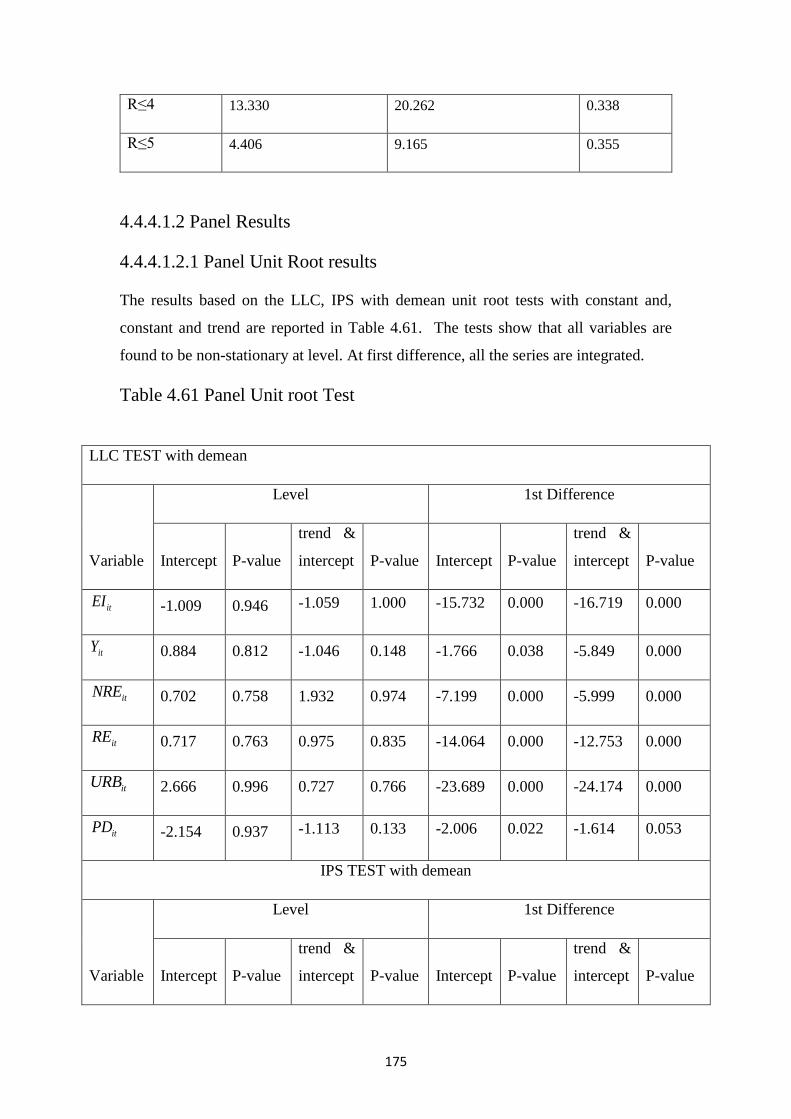

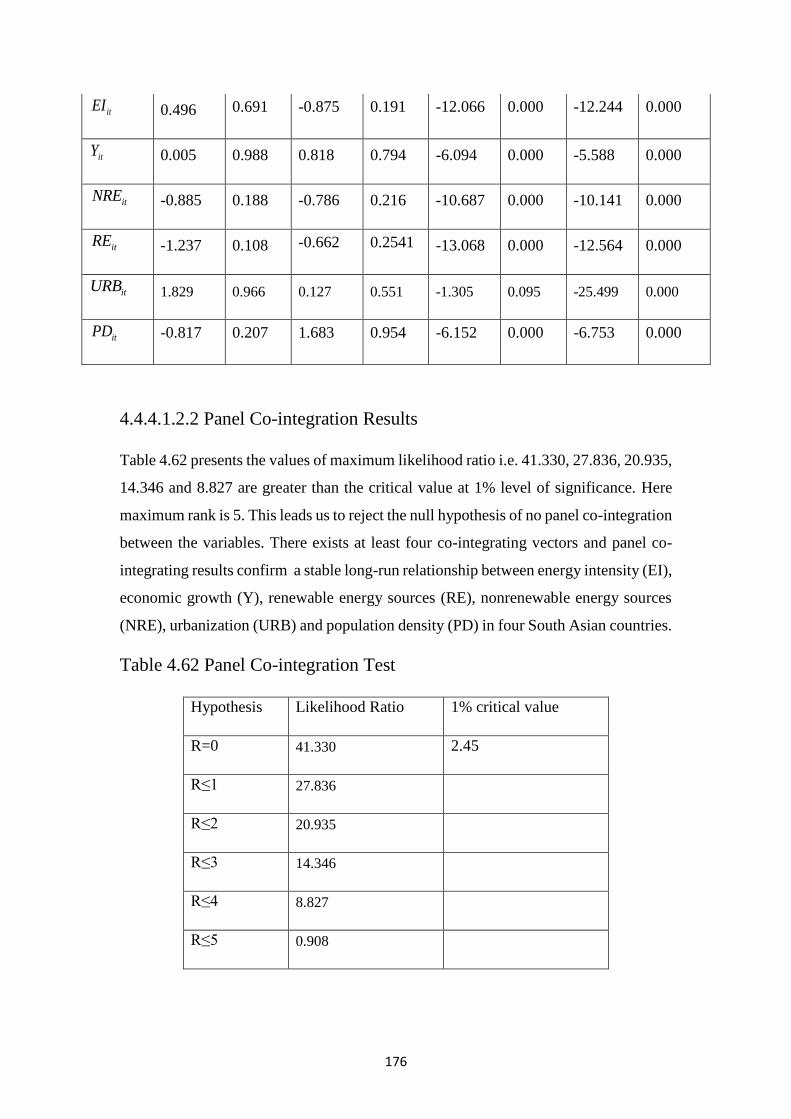

4.4.4.1.2 Panel Results………………………………………………………………175

4.4.4.1.2.1 Panel Unit Root Results………………………………………………....175

4.4.4.1.2.2 Panel Co-integration Results…………………………………………….176

4.4.4.1.3 FMOLS Estimates…………………………………………..……..………177

xv

4.4.4.1.3.1 FMOLS Estimates Country Wise……………………………....………..177

4.4.4.1.3.2 FMOLS Panel Estimates…………………………………….……..……178

4.4.4.1.4 Panel Causality Results……………………………………….………...…179

4.4.4.2 Model 9: Relationship between Renewable and Non-renewable Energy,

Economic Growth, Trade Openness and Energy Intensity ………………………….180

4.4.4.2.1 Time Series Results………………………………………….…………….180

4.4.4.2.1.1 Unit Root Test Results…………………………………………………..180

4.4.4.2.1.2 Johansen Co-integration Test Results……………….…………………..182

4.4.4.2.2 Panel Results………………………………………………………………183

4.4.4.2.2.1 Panel Unit Root Results……………………………………………...….183

4.4.4.2.2.2 Panel Co-integration Results…………………………………………….185

4.4.4.2.3 FMOLS Estimates……………………………………….…...……………185

4.4.4.2.3.1 FMOLS Estimates Country Wise……………………………………..…185

4.4.4.2.3.2 FMOLS Panel Estimates……………………………………….………..187

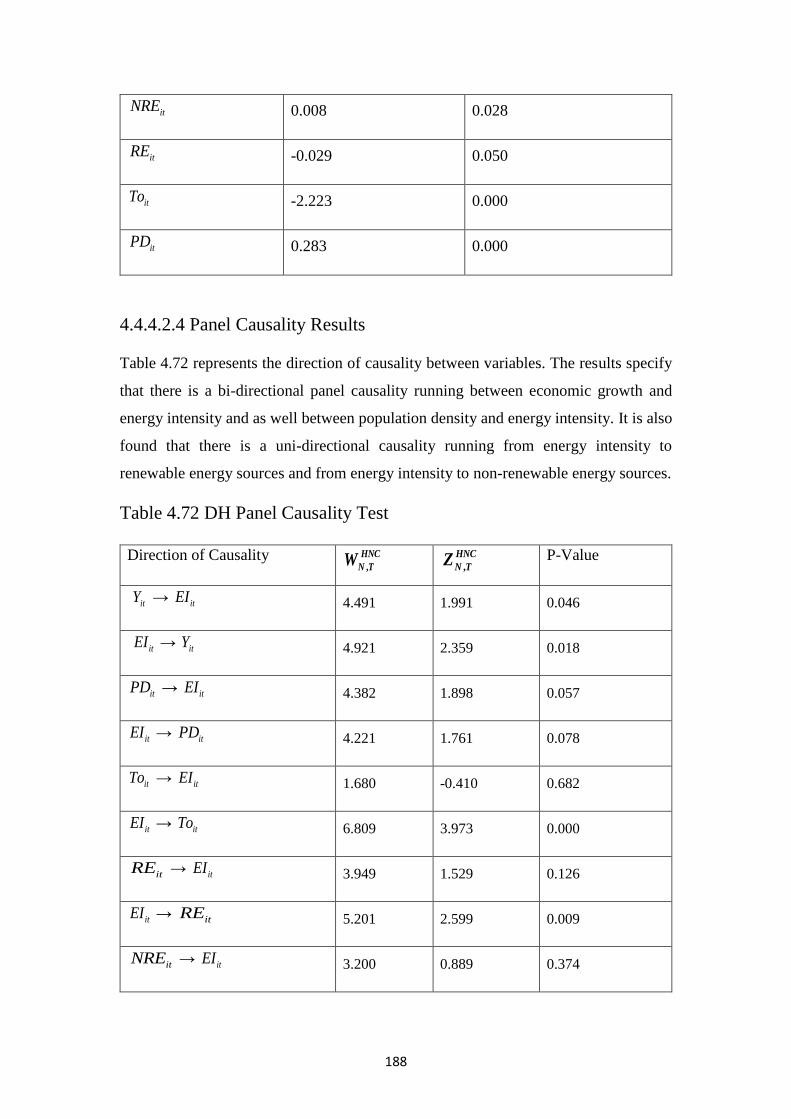

4.4.4.2.4 Panel Causality Results…………………...………………………...……..188

4.4.4.3. Model 10: Relationship between Renewable and Non-renewable Energy,

Economic Growth, Industrialization, Technological Progress and Energy Intensity

………………………………………………………………………………….…...189

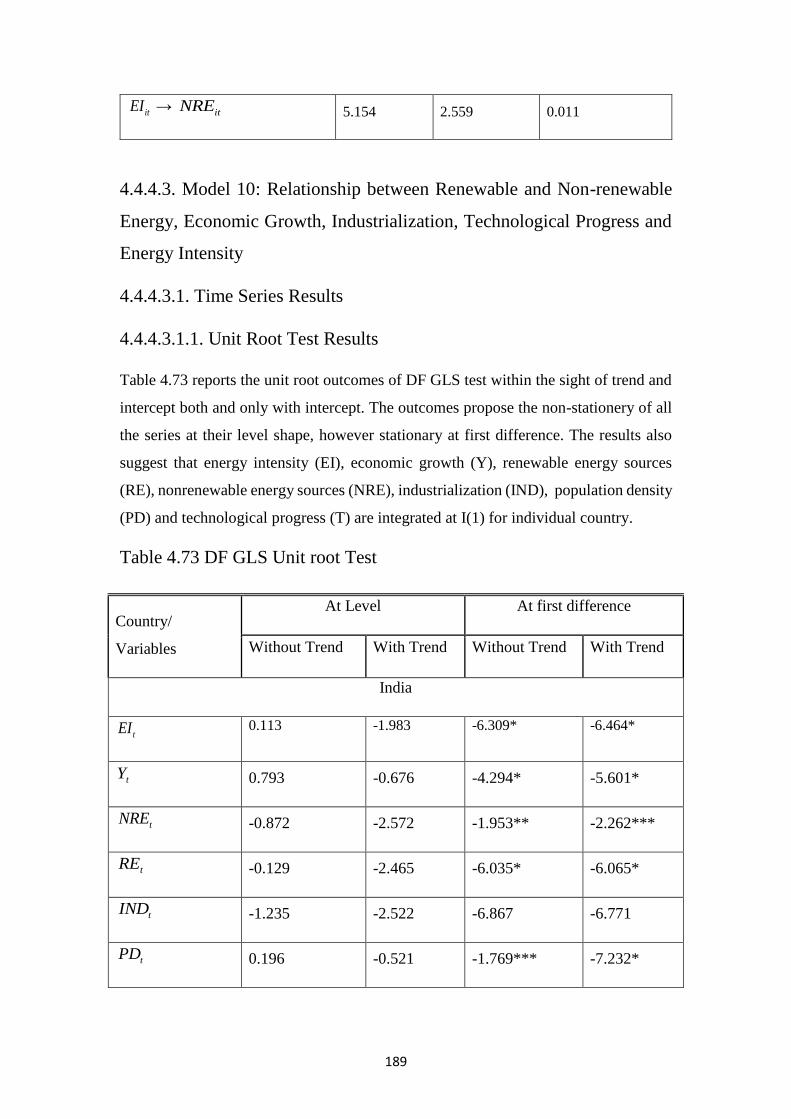

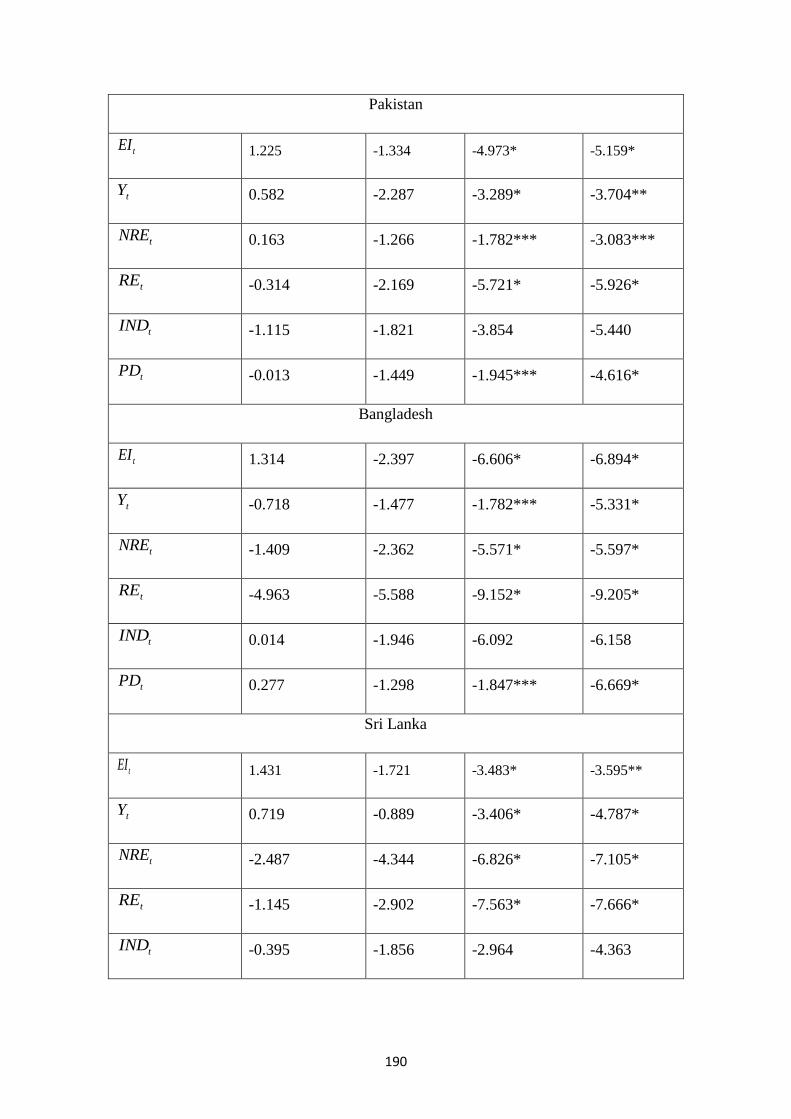

4.4.4.3.1. Time Series Results……………………………………………………….189

4.4.4.3.1.1. Unit Root Test Results……………………………………….…………189

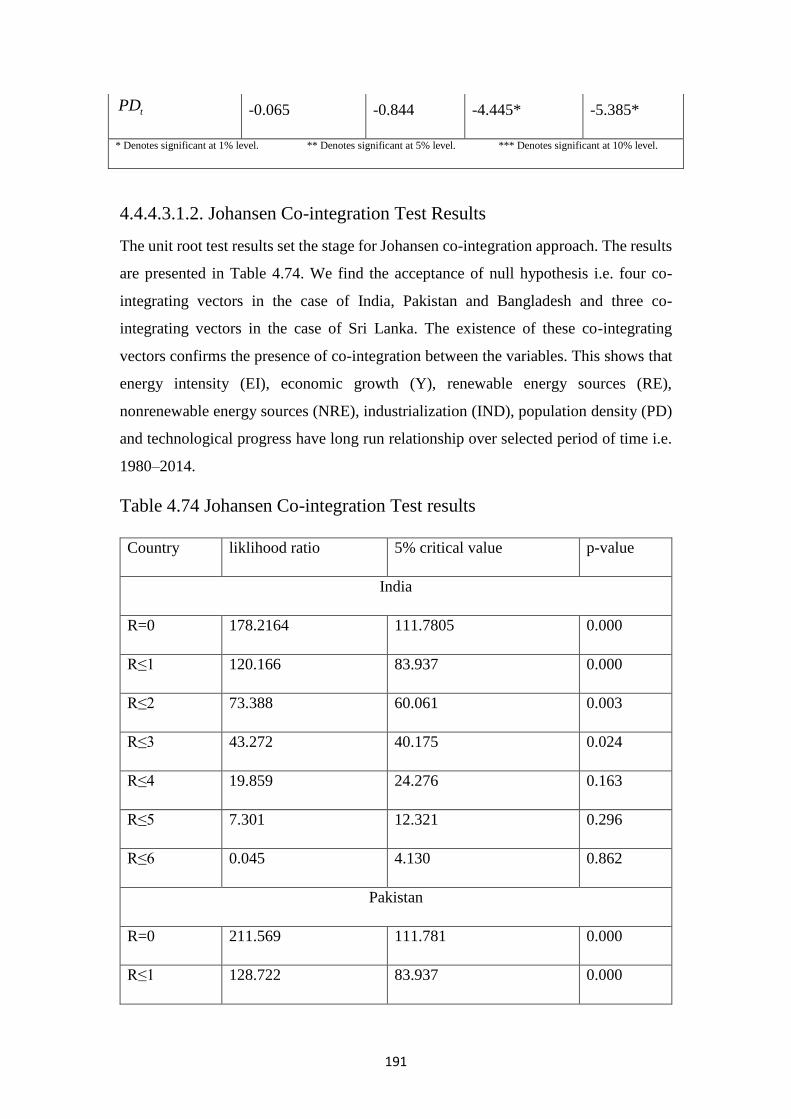

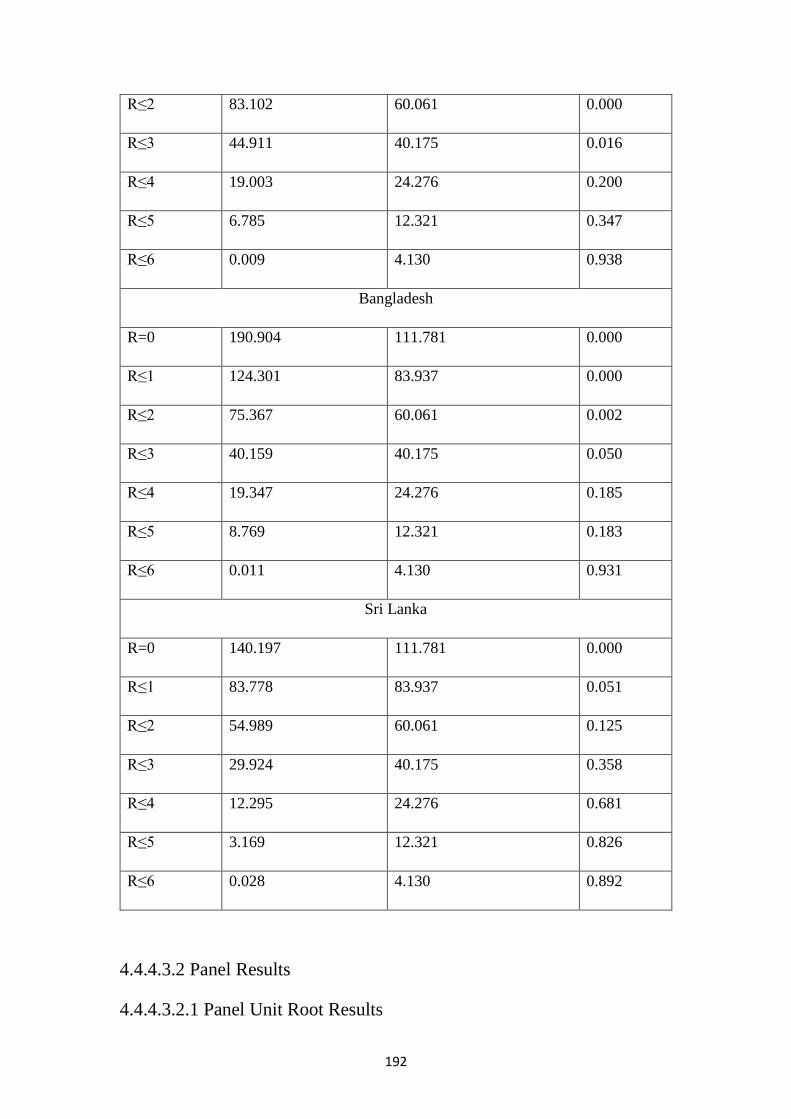

4.4.4.3.1.2. Johansen Co-integration Test Results…………………………………..191

4.4.4.3.2 Panel Results …………………………………………………………..….192

4.4.4.3.2.1 Panel Unit Root Results………………………………………………....192

4.4.4.3.2.2 Panel Co-integration Results………………………………...…………..194

4.4.4.3.3 FMOLS Estimates…………………………………………………………195

4.4.4.3.3.1 FMOLS Estimates Country Wise……………….………………...…..…195

xvi

4.4.4.3.3.2 FMOLS Panel Estimates…………………………………………..…….196

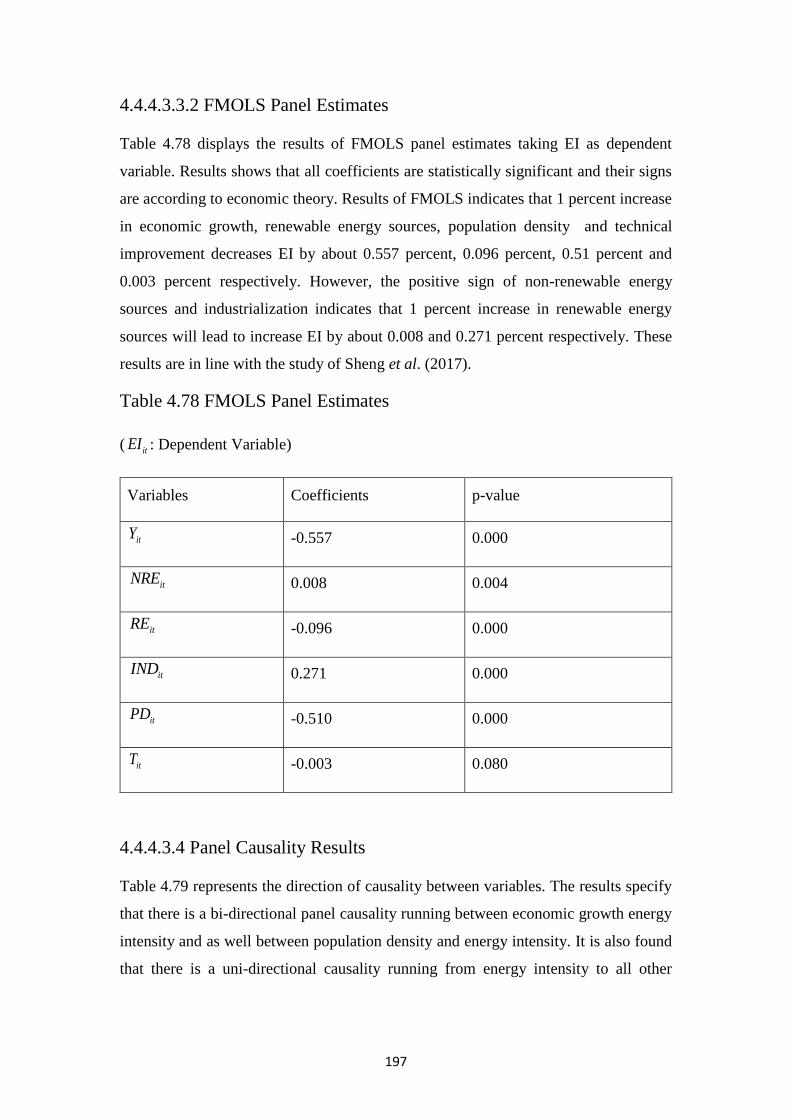

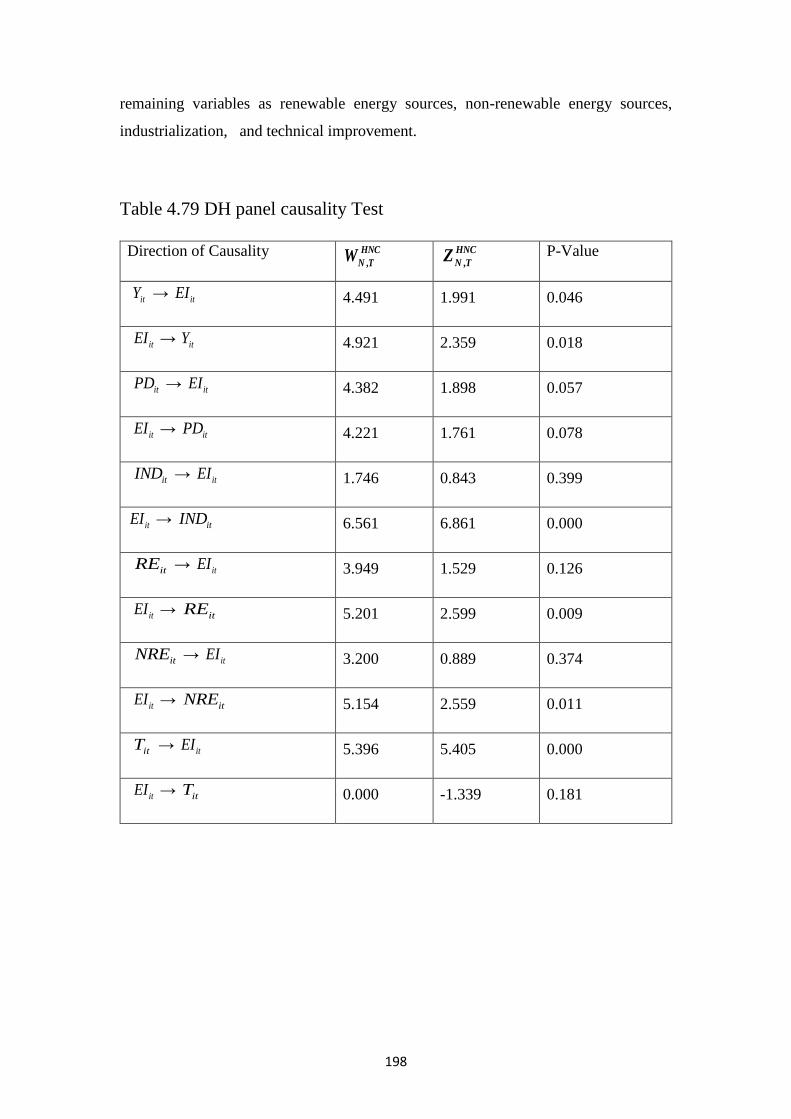

4.4.4.3.4 Panel Causality Results……………………………………………….…...197

5. CONCLUSIONS AND RECOMENDATIONS…………………………….....…199

5.1 Summary and Conclusion…….……………………………………………...….199

5.2 Policy recommendation...………………………………………………….........202

REFRENCES……………………………………………………………………….204

Appendices ………………………………………………………………………....238

xvii

LIST OF TABLES

Table 2.1. Summary of Empirical studies……………………………………………65

Table 4.1 Energy Dependence of Selected South Asian Countries………………….102

Table 4.2 Production and Use of Energy ……………………………………………102

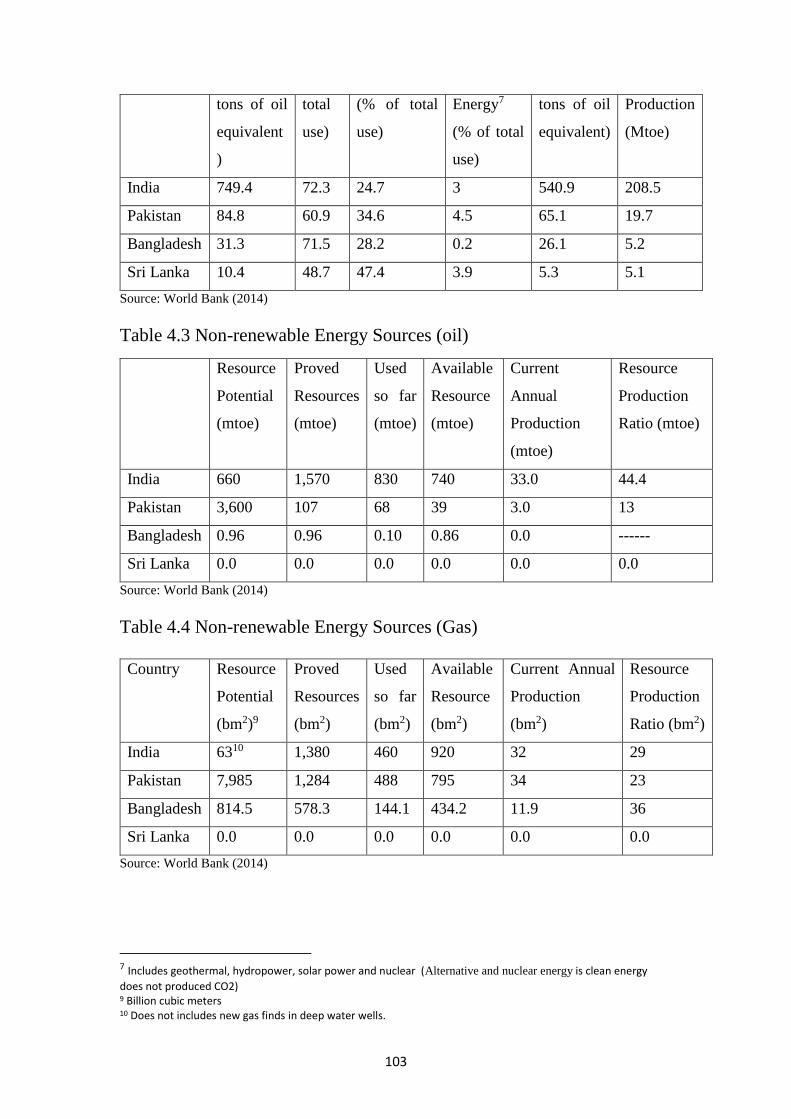

Table 4.3 Non-renewable Energy Sources (oil)……………………………..………103

Table 4.4 Non-renewable Energy Sources (Gas)……………..………………….....103

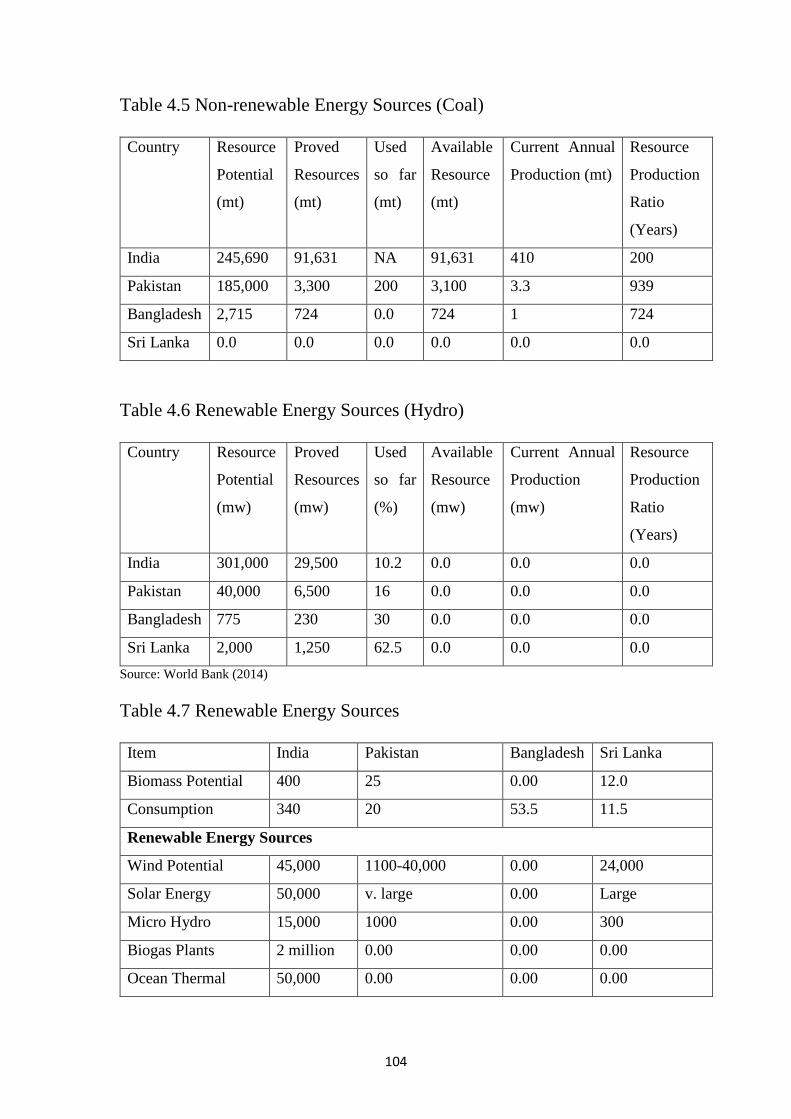

Table 4.5 Non-renewable Energy Sources (Coal)…………………………..………104

Table 4.6 Renewable Energy Sources (Hydro)………………………………...……104

Table 4.7 Renewable Energy Sources……………………………………………….104

Table 4.8 Importance of Renewable and Non-renewable energy sources……..……105

Table 4.9 Renewable Energy potential………………………………………………107

Table 4.10 DF GLS Unit root Test……………..…….……………………...…..….109

Table 4.11 Johansen Co-integration Test results.....………………………...……….110

Table 4.12 Panel Unit root Test…..……………………………………….....………112

Table 4.13 Panel co-integration Test …………………………..………...….………113

Table 4.14 FMOLS Country Specific Results…………...………………,………….114

Table 4.15 FMOLS Panel Estimates………………………...………...…….………116

Table 4.16 DH panel causality Test …………………………………..……..………116

Table 4.17 DF GLS Unit root Test …………………………….…..……………......117

Table 4.18 Johansen Co-integration Test results……………..…..…………………119

Table 4.19 Panel Unit root Test…..…………………………..……..………………120

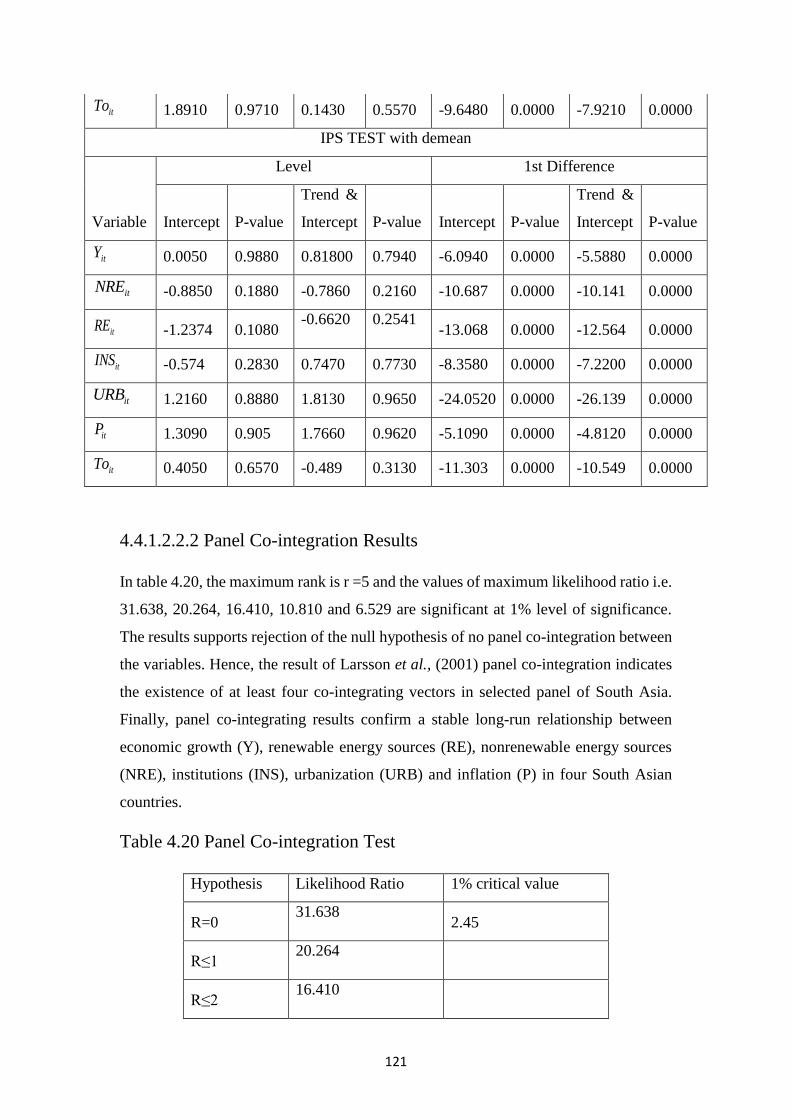

Table 4.20 Panel Co-integration Test ……………………………...………………..121

Table 4.21 FMOLS Country Specific Results…………………….…………………122

Table 4.22 FMOLS Panel Estimates……………………………...…………………124

xviii

Table 4.23 DH Panel Causality Test ………………………….……………………..124

Table 4.24 DF GLS Unit root Test…………………...……………………………..125

Table 4.25 Johansen Co-integration Test results.…………………………...……….127

Table 4.26 Panel Unit root Test……………………..……………………..……..…128

Table 4.27 Panel co-integration Test …………………….…………….………...…129

Table 4.28 FMOLS Country Specific Results………………………………….…...130

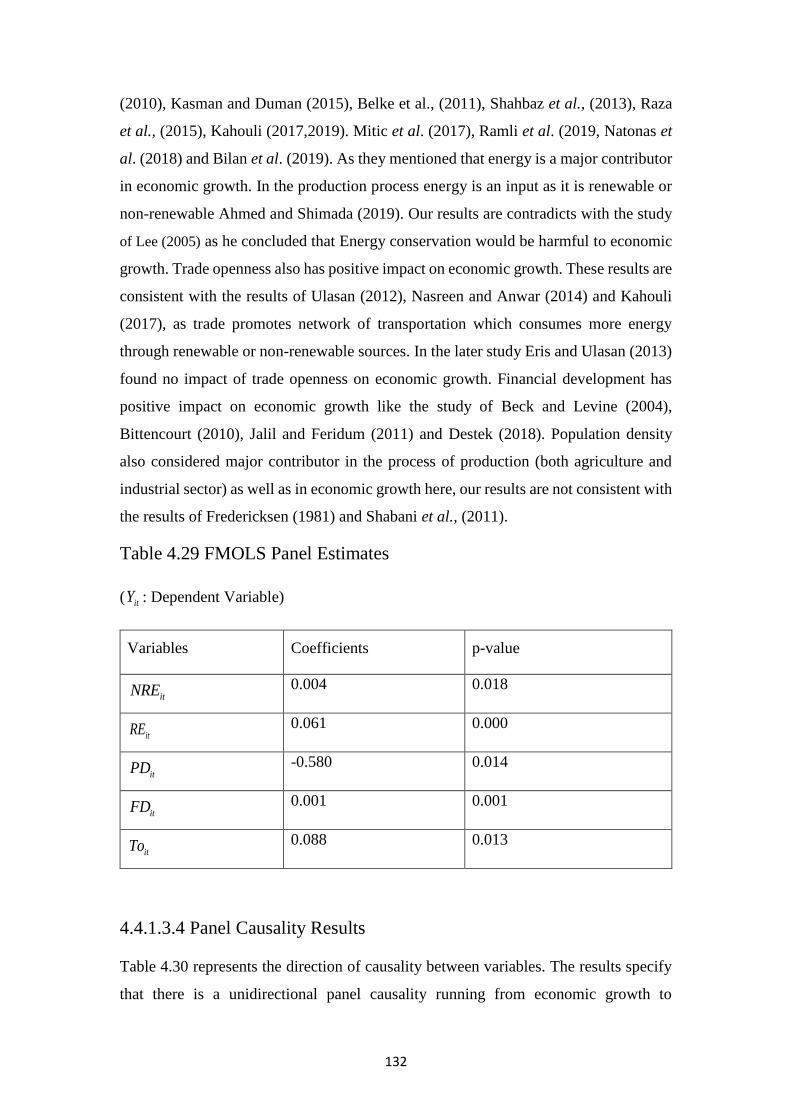

Table 4.29 FMOLS Panel Estimates…………………………………….……….….132

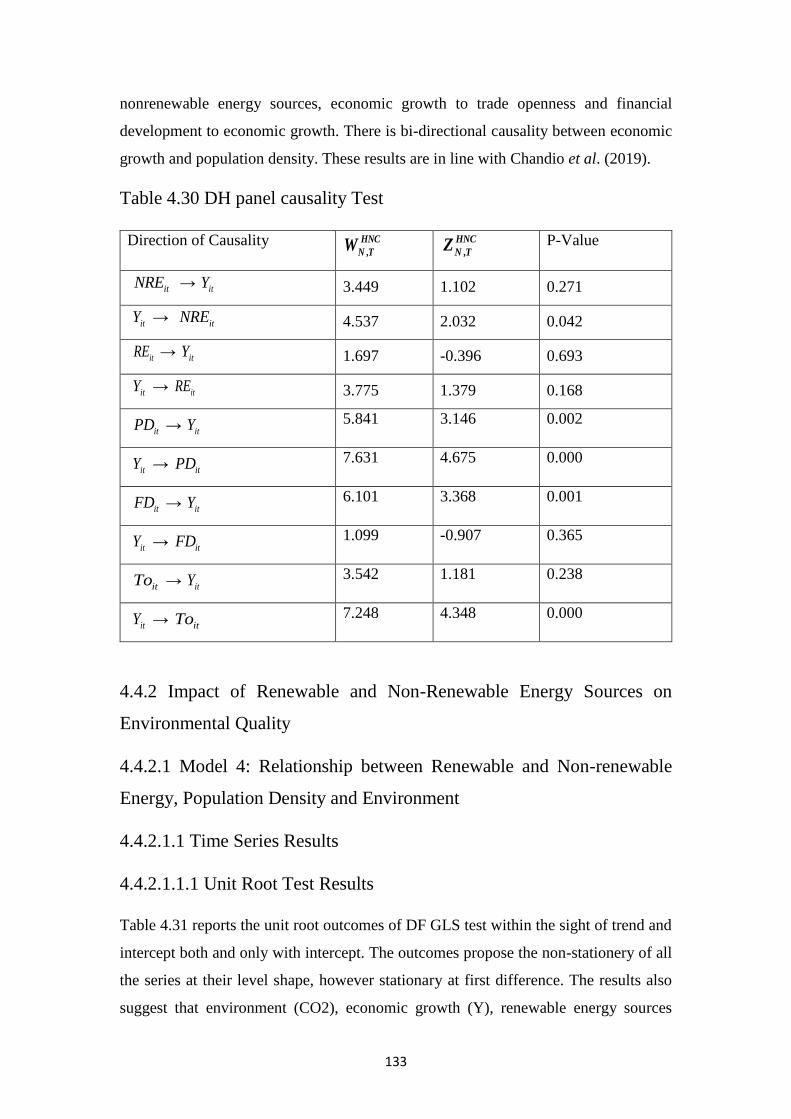

Table 4.30 DH panel causality Test ……………………………….……..……….…133

Table 4.31 DF GLS Unit root Test …………………………………………..….......134

Table 4.32 Johansen Co-integration Test results…………………….………..….…135

Table 4.33 Panel Unit root Test…………………………………………..…………137

Table 4.34 Panel Co-integration Test …………………..…………………………..138

Table 4.35 FMOLS Country Specific Results………………………………………139

Table 4.36 FMOLS Panel Estimates……………………………………..…….……141

Table 4.37: FMOLS Country Specific Results ……………………………………...142

Table 4.38 DF GLS Unit root Test…………………...………………………….….143

Table 4.39 Johansen Co-integration Test results.…………………………...………145

Table 4.40 Panel Unit root Test……………………..……………………..………..147

Table 4.41 Panel co-integration Test ………………...………………….………..…148

Table 4.42 FMOLS Country Specific Results……………………………………....149

Table 4.43 FMOLS Panel Estimates……………………………………..…….……151

Table 4.44 DH panel causality Test …………………………..…………..…….…...152

Table 4.45 DF GLS Unit root Test…………………...………………….……….….153

Table 4.46 Johansen Co-integration Test results.…………………………...………155

xix

Table 4.47 Panel Unit root Test……………………..……………………..………..157

Table 4.48 Panel co-integration Test …………………..……………….………..…158

Table 4.49 FMOLS Country Specific Results……………………………………....159

Table 4.50 FMOLS Panel Estimates…………………………………….……..……160

Table 4.51 DH panel causality Test ……………………………………..……..…...161

Table 4.52 DF GLS Unit root Test…………………...………………….……….….163

Table 4.53 Johansen Co-integration Test results.…………………………...………164

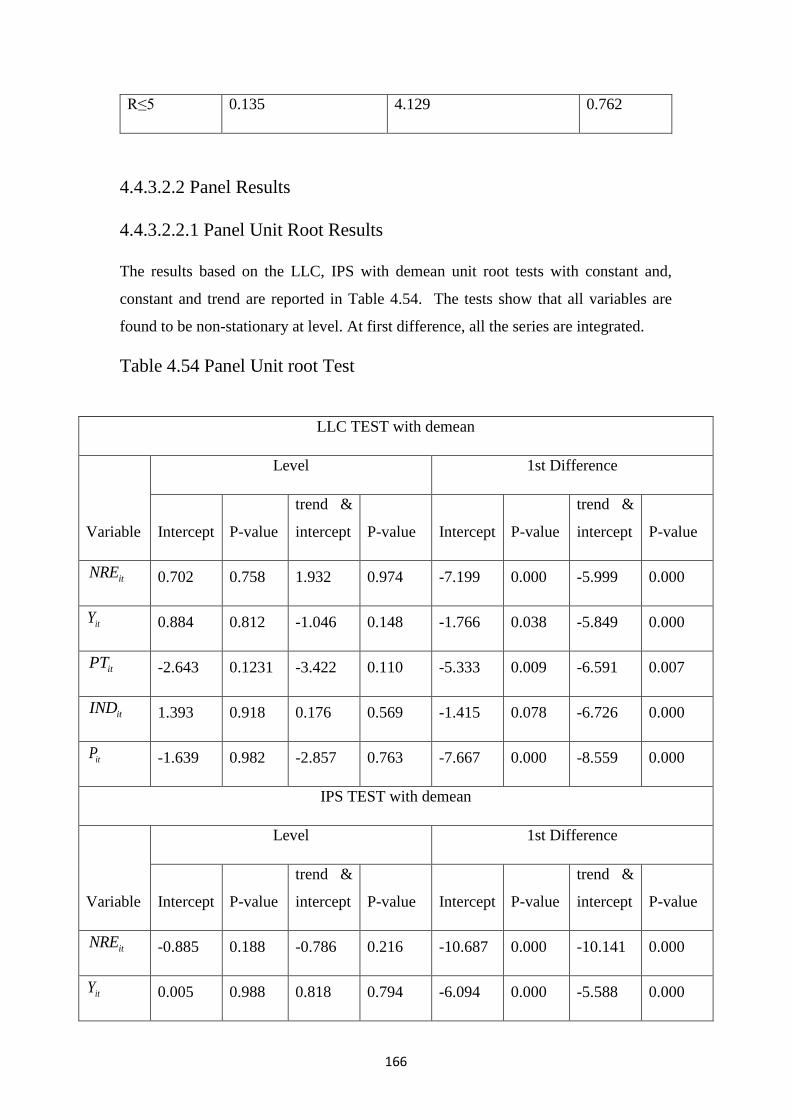

Table 4.54 Panel Unit root Test……………………..……………………..…….…..166

Table 4.55 Panel co-integration Test ………………..………………….………...…167

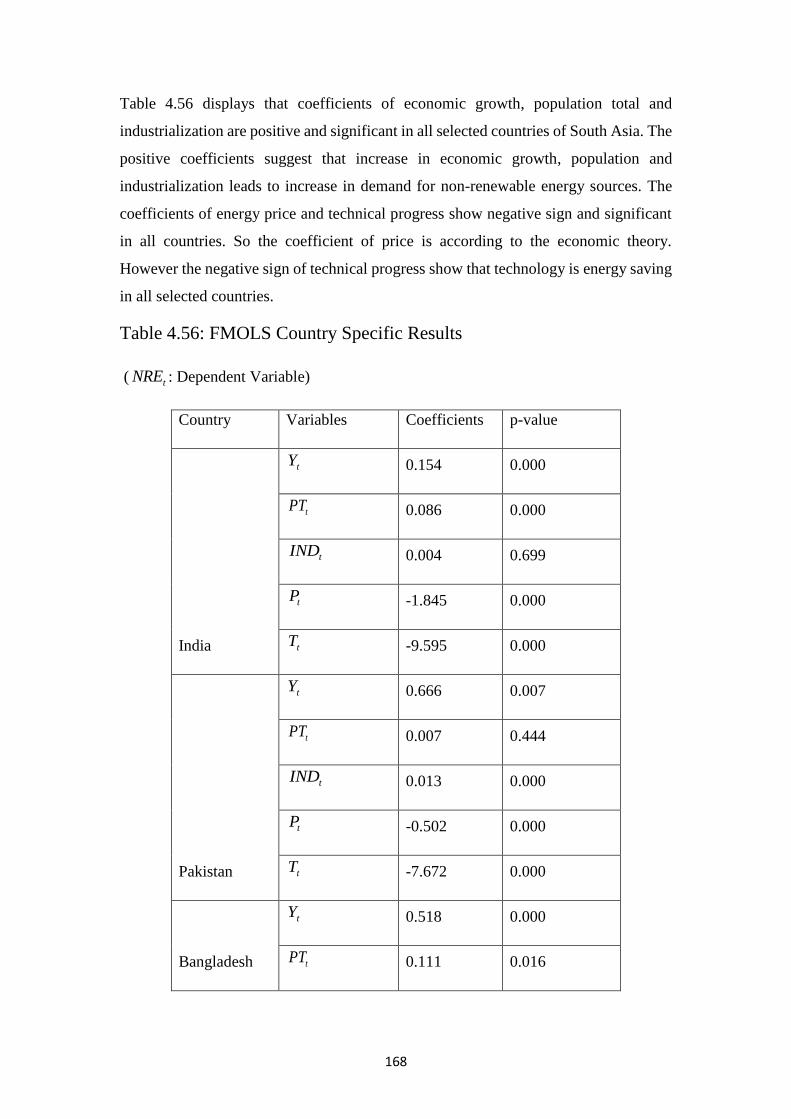

Table 4.56 FMOLS Country Specific Results…………………………………….....168

Table 4.57 FMOLS Panel Estimates…………………………………….…….….…169

Table 4.58 DH panel causality Test ……………………………………..…….…....170

Table 4.59 DF GLS Unit root Test…………………...………………….….………172

Table 4.60 Johansen Co-integration Test results.…………………………...……….173

Table 4.61 Panel Unit root Test……………………..……………………..………..175

Table 4.62 Panel co-integration Test ……………………….………….….…….….176

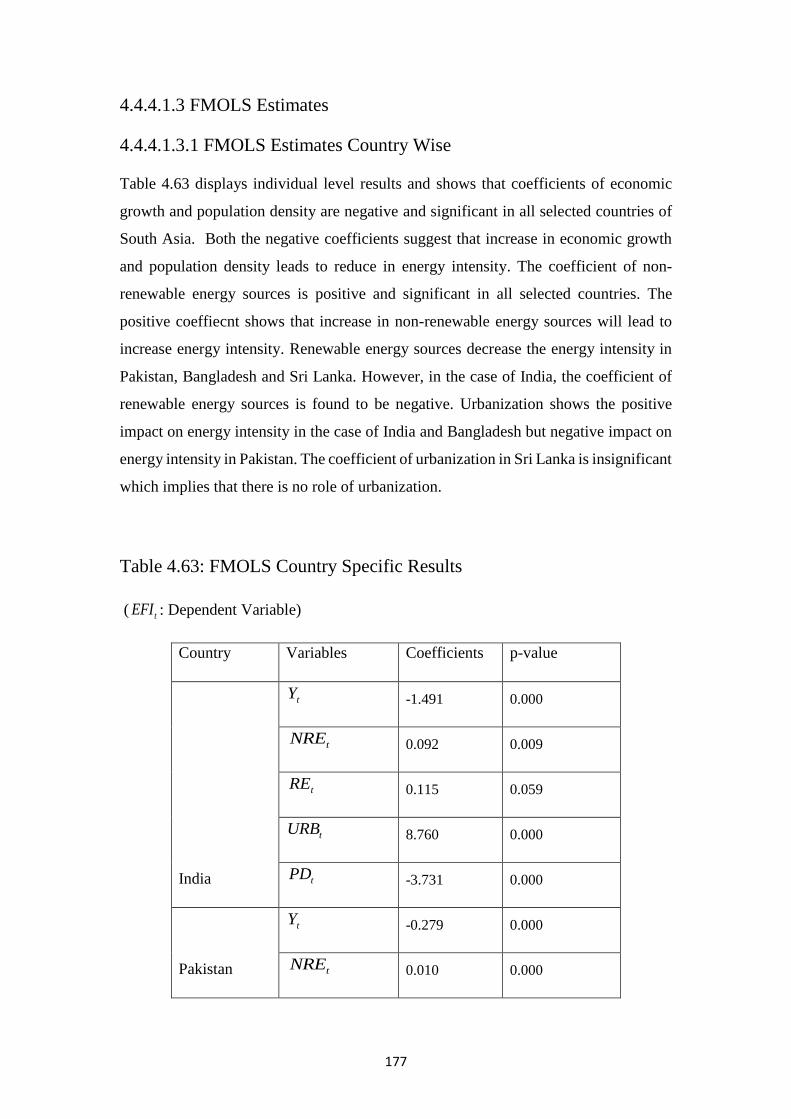

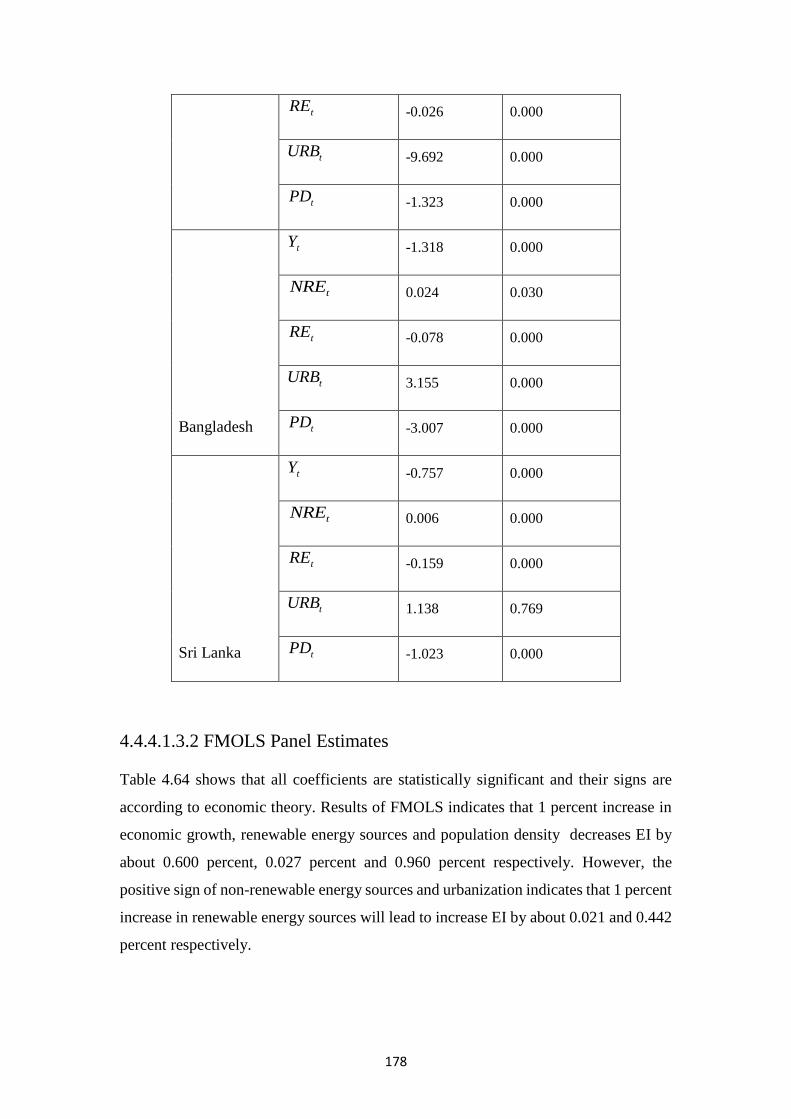

Table 4.63 FMOLS Country Specific Results……………………………………....177

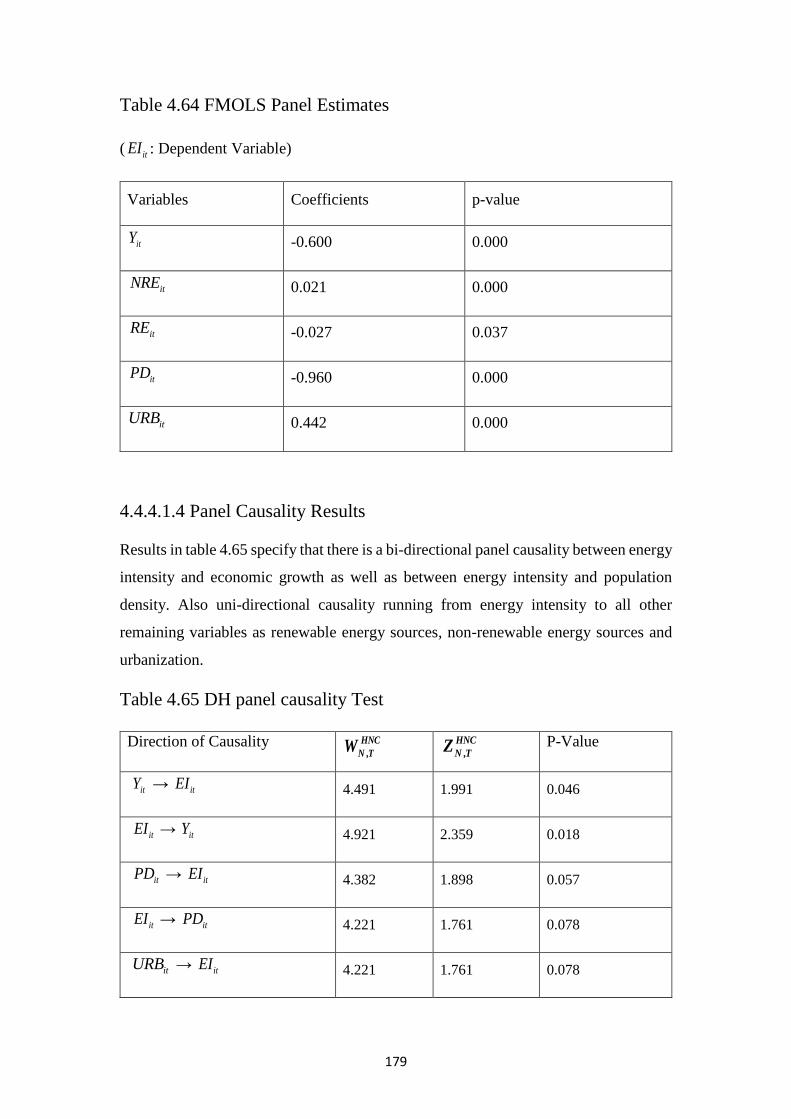

Table 4.64 FMOLS Panel Estimates…………………………………….…….……179

Table 4.65 DH panel causality Test ……………………………………..…….….....179

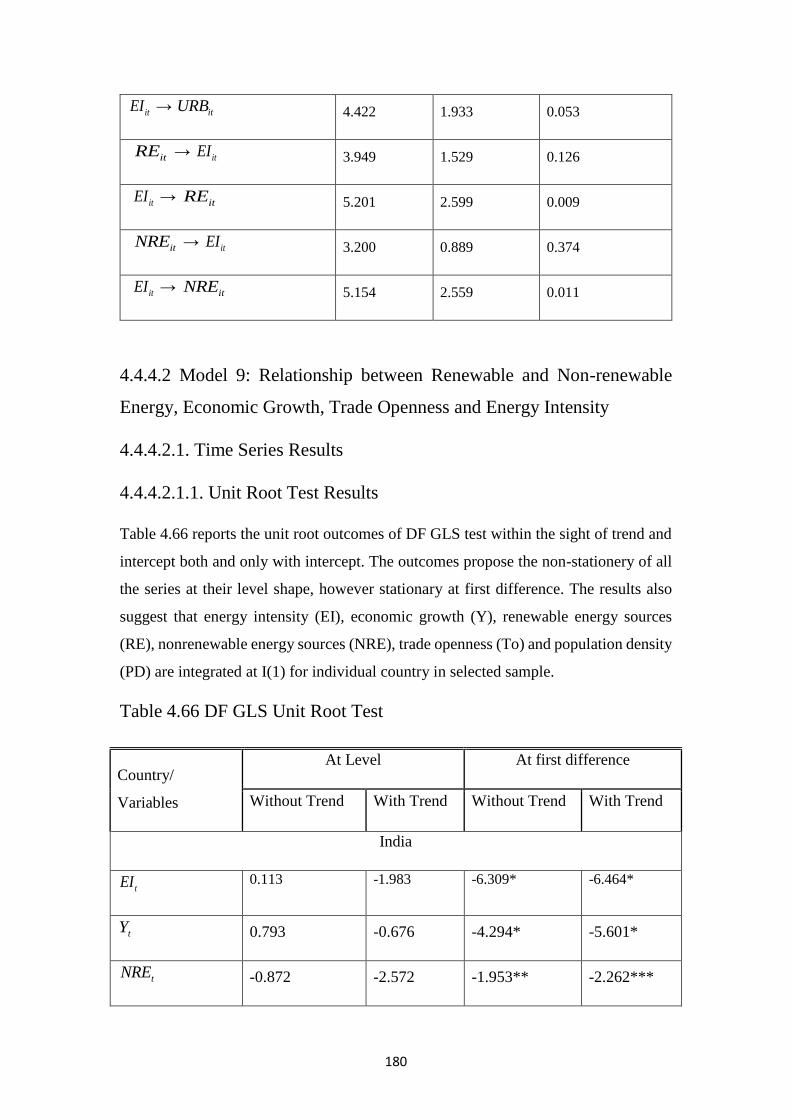

Table 4.66 DF GLS Unit root Test…………………...………………….………….180

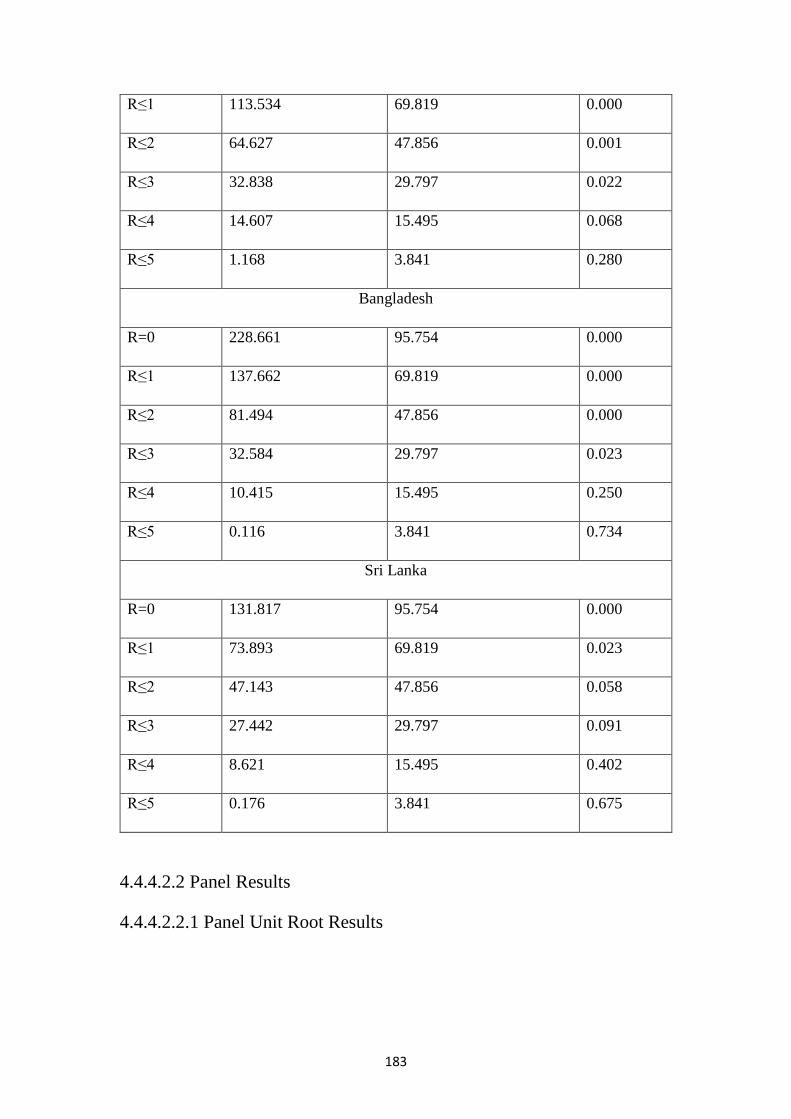

Table 4.67 Johansen Co-integration Test results.…………………………...………182

Table 4.68 Panel Unit root Test……………………..……………………..………..184

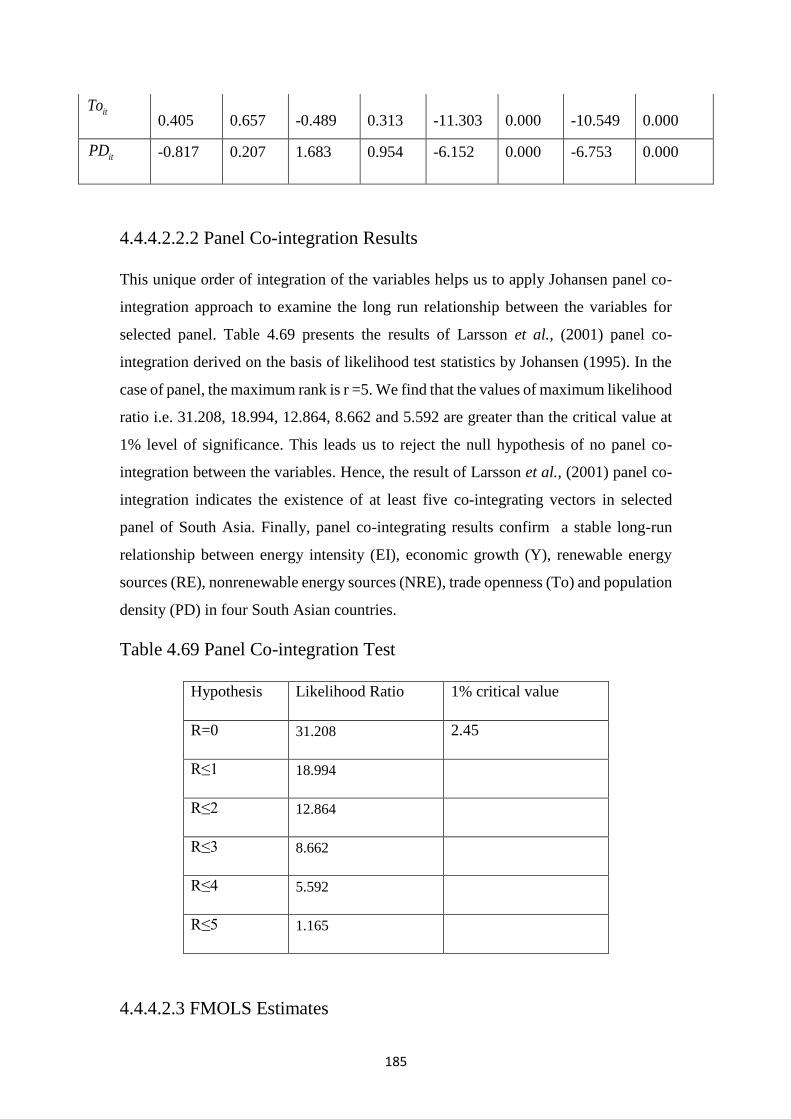

Table 4.69 Panel co-integration Test …………………………….…….…..…….…185

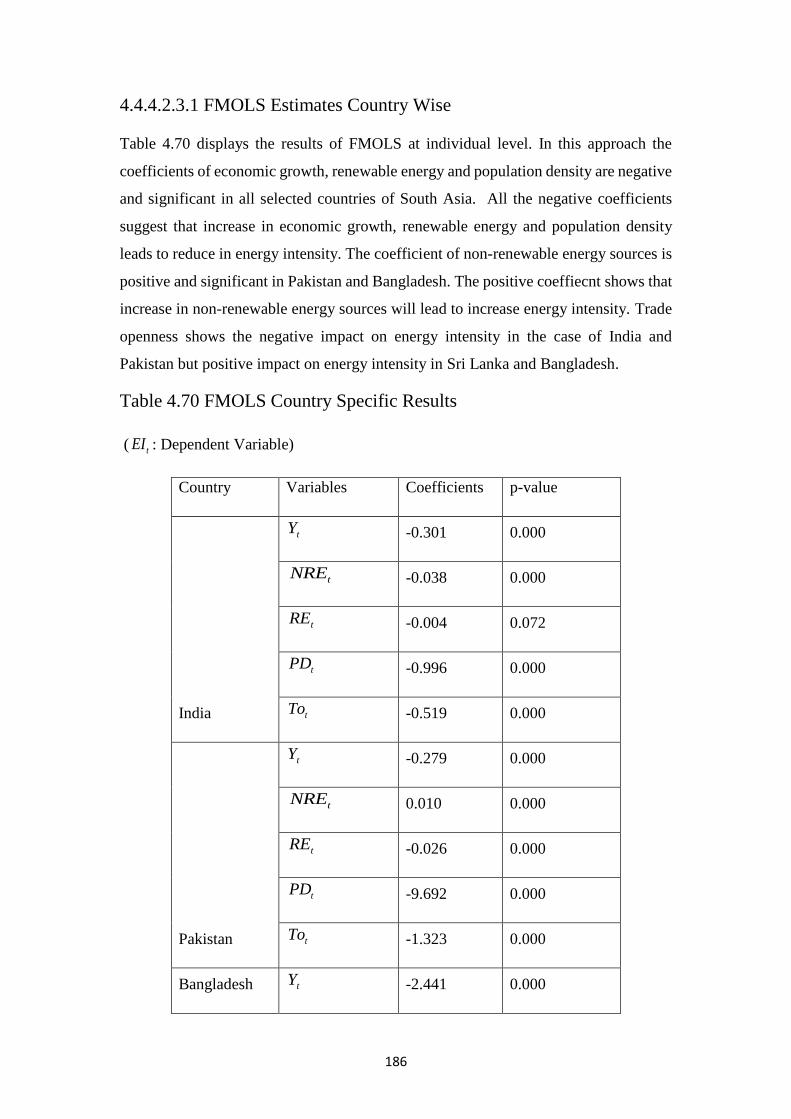

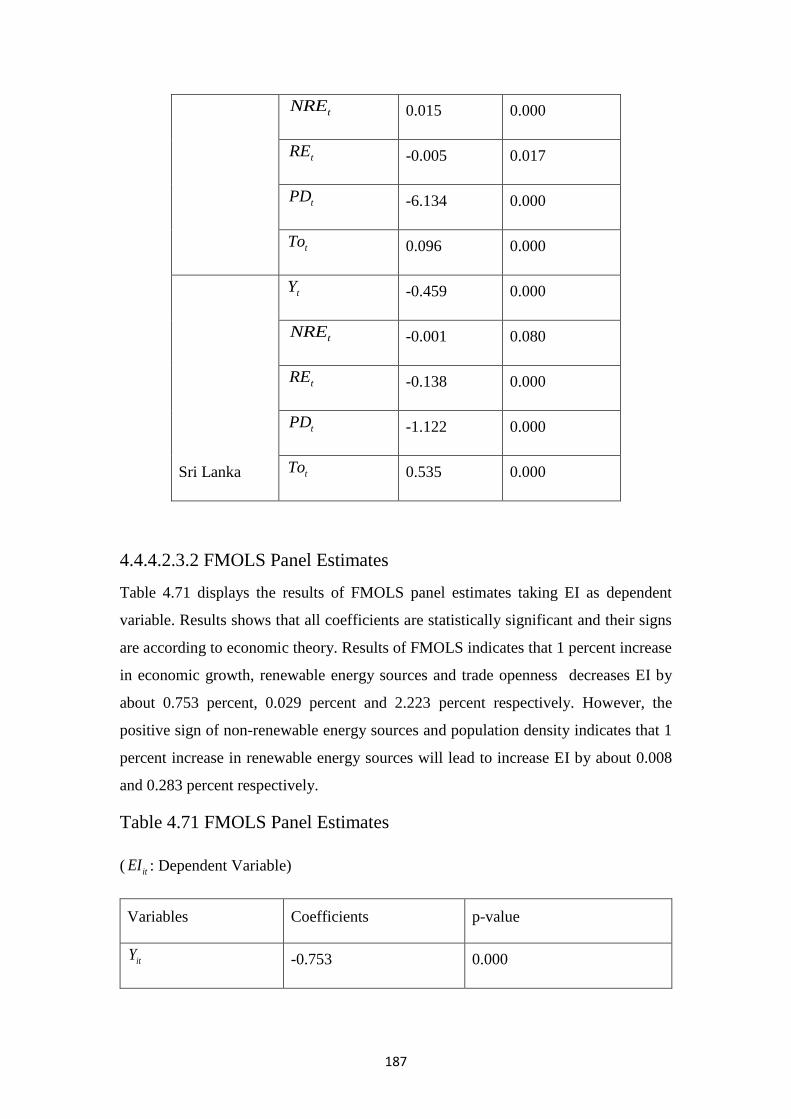

Table 4.70 FMOLS Country Specific Results……………………………….……....186

xx

Table 4.71 FMOLS Panel Estimates…………………………………….…….……187

Table 4.72 DH panel causality Test ……………………………………..……...…...188

Table 4.73 DF GLS Unit root Test…………………...………………….…….…….189

Table 4.74 Johansen Co-integration Test results.…………………………...….……191

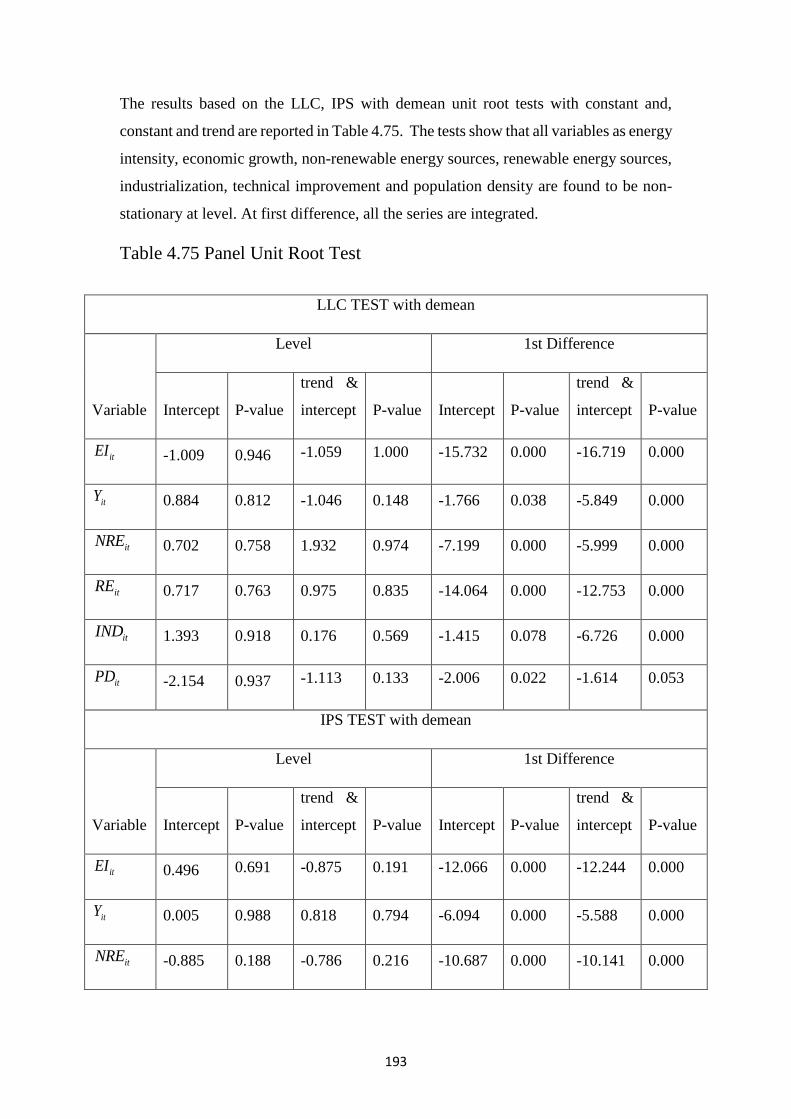

Table 4.75 Panel Unit root Test……………………..……………………..………..193

Table 4.76 Panel co-integration Test ………………………….……….……...….…194

Table 4.77 FMOLS Country Specific Results………………………………….…....195

Table 4.78 FMOLS Panel Estimates…………………………………….……..……197

Table 4.79 DH panel causality Test ……………………………………..……..…...198

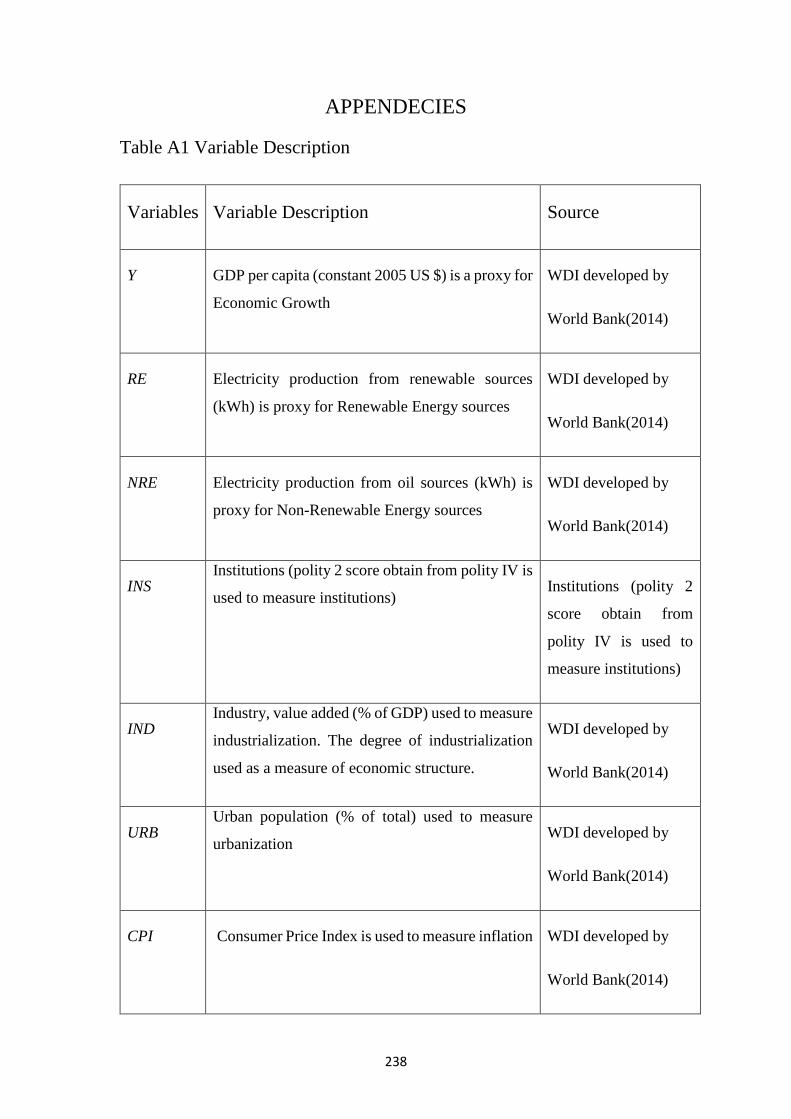

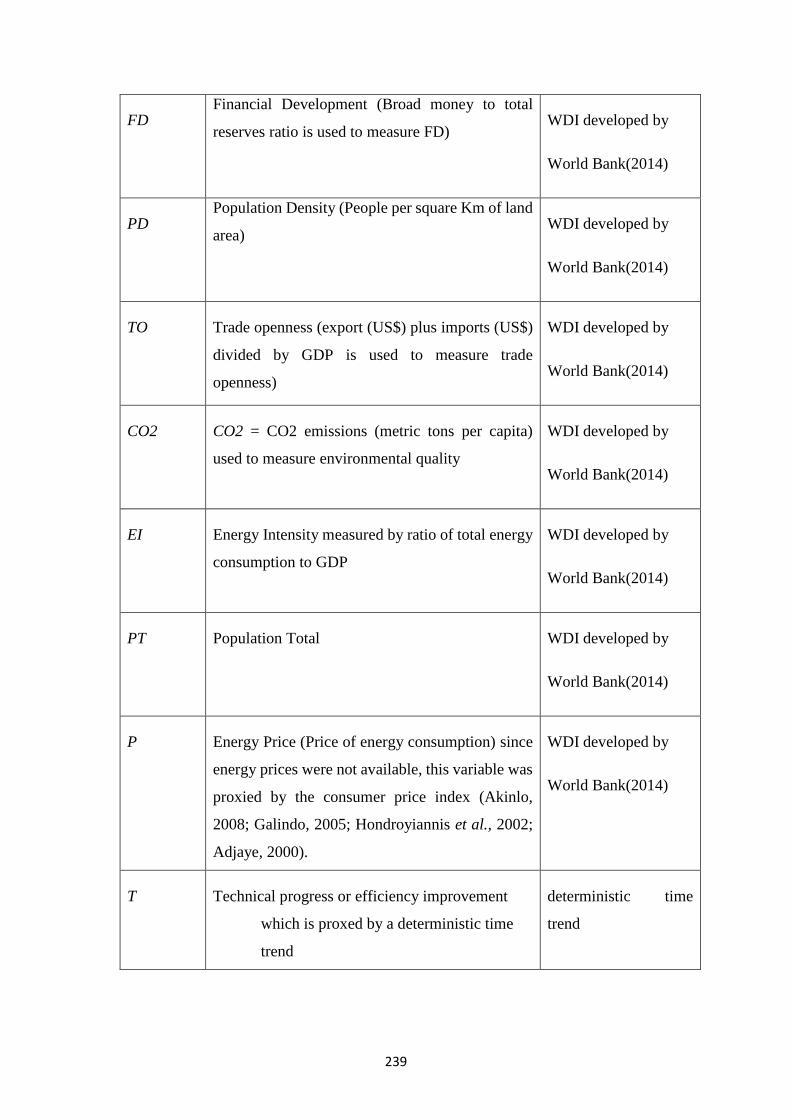

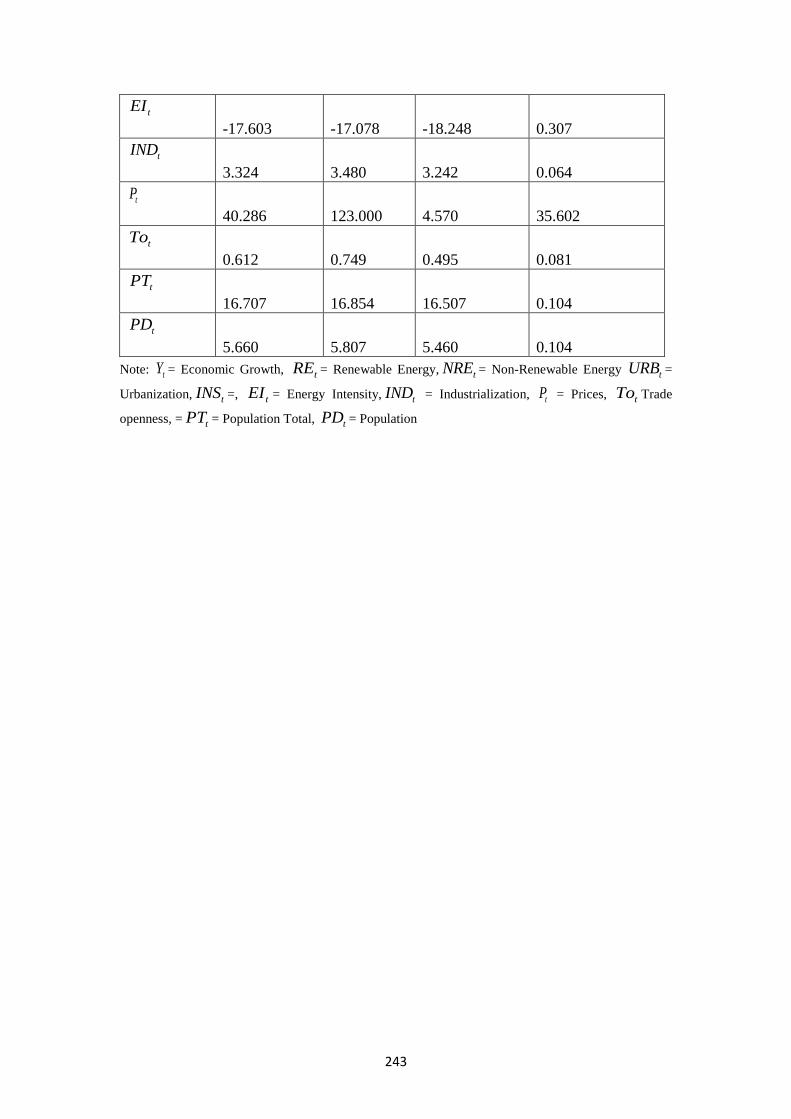

Table A1 Variable Description ………………………………………….……..……238

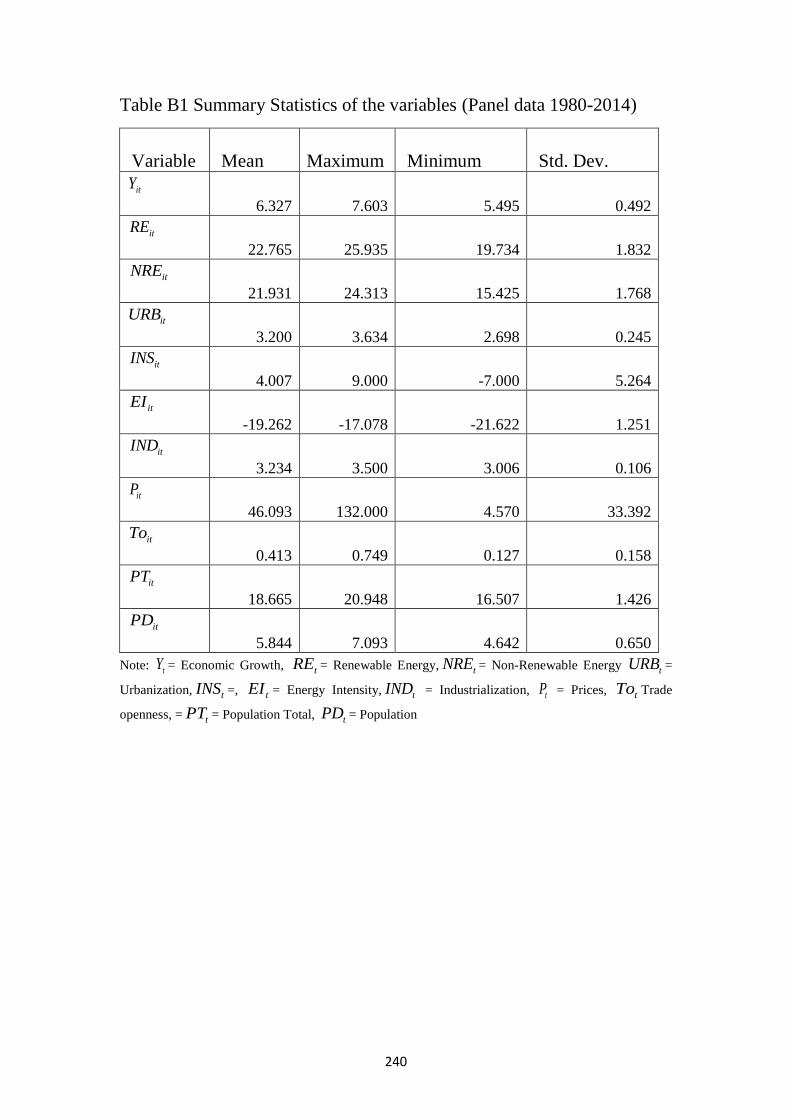

Table B1 Summary Statistics of the variables Panel data 1980-2014………………240

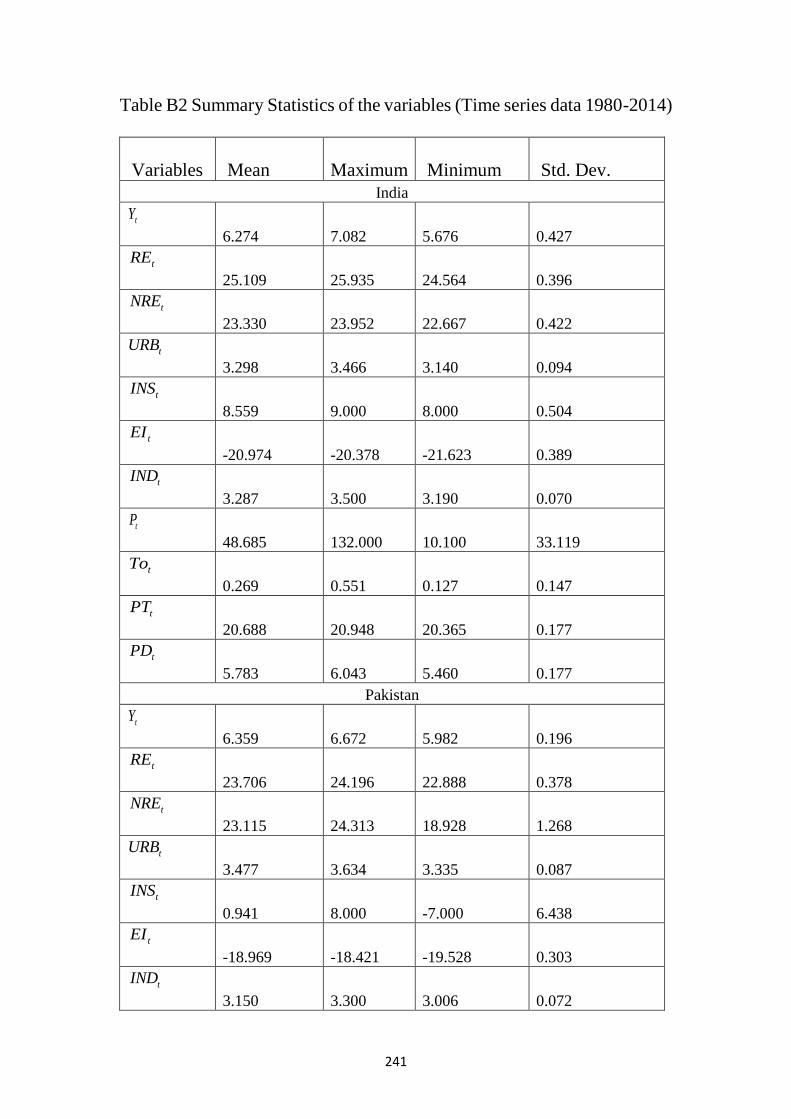

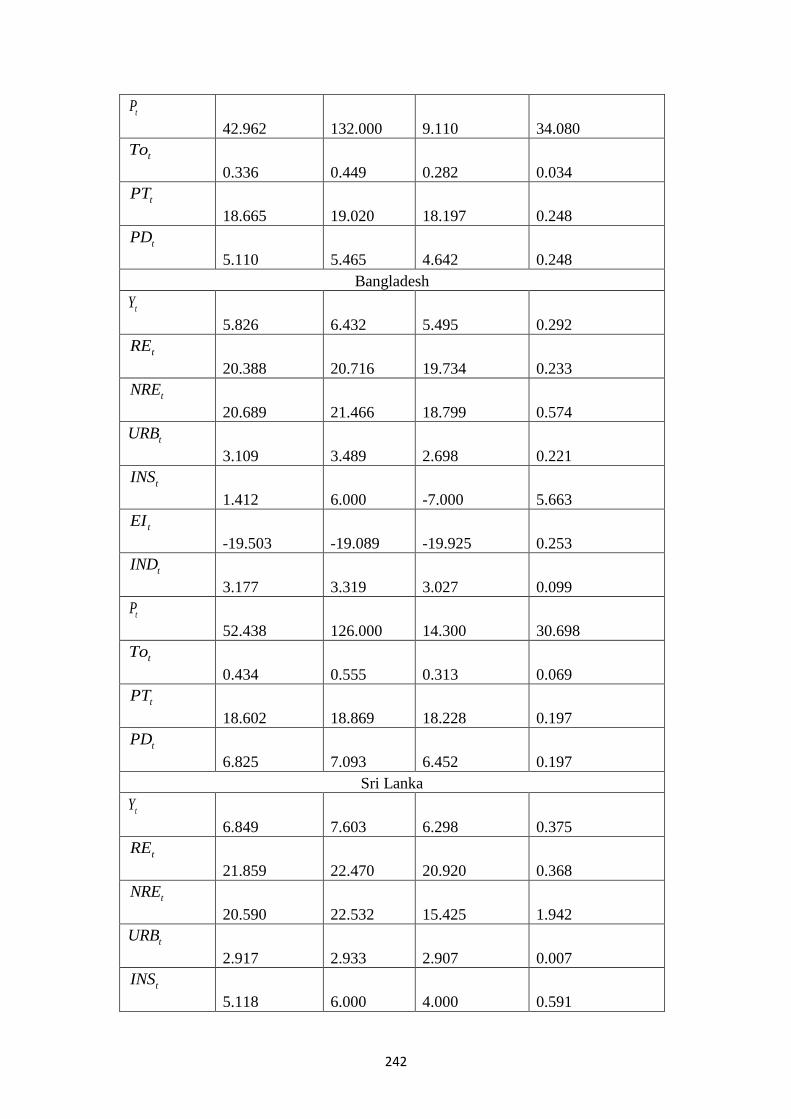

Table B2 Summary Statistics of the variables Time Series data 1980-2014….…….241

Table C1 Variance Decomposition of RE Demand…………………………………244

Table C2 Impulse Response Function of RE Demand………………………………245

Table C3 Variance Decomposition of NRE Demand……………….……………….246

Table C4 Impulse Response Function of NRE Demand……………………………..247

xxi

LIST OF FIGURES

Figure 4.1: Trends in Economic Growth.…….………………………………...……..97

Figure 4.2: Trends in Inflation ……………….………………….………...………….98

Figure 4.3: Trends in Industrial share of GDP……………...….…………..………….98

Figure 4.4: Trends in Total Population ………………….…….…………..………….99

Figure 4.5: Trends Population Density………………….…….…………..………….99

Figure 4.6: Trends in per capita Co2 ………………………….…………...….……100

Figure 4.7: Trends in Non-Renewable energy Sources…………………….…….…101

Figure 4.8: Trends in Renewable energy Sources…………………………..………102

xxii

ACRONYMS AND ABBREVIATIONS

DF Dickey-Fuller

ECM Error Correction Mechanism

EC Energy Consumption

FBR Federal Board of Revenue

EI Energy Intensity

EFI Energy Efficiency

EKC Environment Kuznets Curve

FY Financial Year

GDP Gross Domestic Product

GLS Generalized Least Square

IEA Information Energy Authority

IND Industrialization

OLS Ordinary Least Squares

INS Institutions

FMOLS Fully Modified Ordinary Least Square

NRE Nonrenewable Energy

PD Population Density

RE Renewable Energy

TO Trade Openness

URB Urbanization

WDI World Bank Indicator

xxiii

ABSTRACT

The core target of this exploration is to inspect the effect of renewable and

nonrenewable energy sources on economic growth and environmental degradation in

selected South Asian Economies. The thesis explores renewable and non-renewable

energy sources in four ways. Firstly, it empirically investigates the relationship between

renewable, non-renewable energy, and economic growth. Secondly, it empirically

investigates the impact of renewable and non-renewable energy sources on

environmental quality. Thirdly, it examines the determinants of demand for renewable

and non-renewable energy sources including industrial sector. Fourthly, the study

explores the impact of aforementioned energy sources and economic growth on energy

intensity. The thesis comprises on four South Asian countries: Pakistan, India,

Bangladesh and Sri Lanka for empirical investigation, based on the availability of data.

The study employs both time series and panel data analysis for the period of 1980 to

2014. To analyze the long run and causal relationship between variables, we have

applied Johansson co-integration, Larsson panel co-integration and Granger causality

Dumitrescu and Hurlin (DH) approaches. Empirical results confirm the presence of

long run co-integration between economic growth, renewable energy sources, non-

renewable energy sources, institution quality, population density, financial

development, inflation, and trade openness in various models. The impact of renewable

and non-renewable energy on economic growth is found positive which increases per

capita GDP. The analysis of fully modified ordinary least squares (FMOLS) panel

estimates shows that the values of all coefficients are statistically significant and their

signs are in line with the economic growth theory.

Secondly, the results reveal that economic growth, population density, and non-

renewable energy have a positive impact on per capita CO2 emission. However, the

negative sign of renewable energy sources tends to decrease per capita CO2 emissions,

indicating that environmental quality deteriorates with non-renewable energy sources

and improves in case of renewable energy sources. The findings additionally encourage

the Environmental Kuznets Curve (EKC) hypothesis which accepts an altered U-shaped

path amongst affluence and per capita CO2 emissions. Moreover, the study found the

evidence of bi-directional panel causality between CO2 and renewable energy sources

as well as population destiny. Investigations give the evidence of unidirectional

xxiv

causality running from CO2 to non-renewable energy sources. Results also give proof

evidence of feedback relationship between environment and both energy sources.

In the other model of the causal relationship between environmental quality and energy

intensity with the presence of urbanization with both energy sources and population,

outcomes affirm the existence of co-integration between these factors. FMOLS

discovered the positive effect of affluence, urbanization, energy intensity and non-

renewable energy sources on CO2 emissions. Notwithstanding, the negative indication

of renewable energy sources demonstrate that it will prompt diminishing per capita

CO2.

Thirdly, the empirical analysis of renewable and non-renewable energy demand shows

that the price and income are the major determinants of the demand for energy. The

impact of income on energy demand is positive in both energy sources whereas, in case

of price, it has a negative impact. The results of technological progress show a negative

impact on energy demand, which suggests that technological progress is energy saving.

Results of FMOLS indicate that increase in economic growth, industrialization and

population total increases energy demand (renewable and non-renewable). These

results show that higher per capita real income should result in greater economic

activity which in turns accelerate the use of energy. The degree of industrialization, as

a measure of economic structure, is also expected to enhance the demand for renewable

energy. However, the negative sign of P and T indicates that increase in energy price

and technical progress will lead to decrease energy demand. The negative sign of

technical progress shows that the technology is energy saving.

Lastly, the impact of economic growth, population density and renewable energy on

energy intensity is found negative, which suggests that there is a reduction in energy

intensity with the increase in aforesaid factors. On the other hand, reduction in energy

intensity leads to the improvements in energy efficiency. Results of panel FMOLS

indicate that 1 percent increase in economic growth, renewable energy sources, and

population density decrease the energy intensity by about 0.600 percent, 0.027 percent

and 0.960 percent respectively which leads to increase in energy efficiency. Moreover,

the study found the evidence of bi-directional panel causality between energy intensity

and economic growth, urbanization as well as between energy intensity and population

density. Results provide evidence of feedback relationship between energy efficiency

xxv

and output. There is also unidirectional causality running from energy intensity to

renewable and non-renewable energy sources.

Keywords: Economic Growth, Environmental quality, Renewable energy, Non-

renewable Energy, Institutional quality, Industrialization, Energy Demand, Energy

Price, Population Density, South Asia

1

CHAPTER 1

INTRODUCTION

Energy is a fundamental component of human needs. Although it is not viewed as

compulsory requirement but is essential for the fulfillment of daily human needs (Yuko,

2004). Due to the rapid progress and industrialization improvements, the level and

power of energy utilization is essential for a nation's economic development. The

fundamental sources of energy are separated into two vital categories that is traditional

and maintainable energy sources. Traditional sources can be classified as energy from

non-renewable assets. These sources have various difficulties that include

contamination and an unnatural weather change; this has rolled out nation’s

improvement strategies to support reception of greener innovations in renewable power

sources. Renewable or maintainable energy sources are characterized as energy that can

be accomplished from assets which are actually renewed on a human extent, for

example daylight, biogas, wind, hydropower, tides, waves and geothermal warmth.

Renewable energy sources can be substituted regular or traditional sources in four

recognizable zones: power era, high temp water/space warming, engine fills, and

countryside (off-network) energy administrations. Petroleum product from fossil fuel

which incorporates coal, oil and flammable gas drove world economic development,

however this energizes arrival of carbon dioxide CO2 into the earth air, is viewed as

the fundamental driver of a dangerous atmospheric deviation and environmental change

(Stern, 2006). Renewable sources such as solar, wind, geothermal, tidal, and biomass

have an unlimited supply and these are being recycled or replaced. While energy

coming from fossil fuels, coal, oil and natural gas are non-renewable sources of energy

which is exhaustible up to a limit . We cannot enjoy the benefits of these non-renewable

energy sources forever, because they become unavailable once exhausted or in other

words these are one time use resources. Even the over-consumption of such sources can

leads to its threshold level, from where they cannot be regenerated for centuries.

Energy can be used for illumination, lighting, warming, and cookery on the one hand

and also as a medium of transportation on the other hand. Energy is required for

manufacturing consumer goods as well as capital equipment both in household and

production sectors. Globally, the demand for energy is increasing day by day. The

reasons are multiple, for instance, shift to industrialization, the introduction of new

2

technology, modernization and most importantly the desire for having a more

comfortable standard of living.

Energy is measured as an essential source for the socio-economic development of a

country whether it is renewable energy or non-renewable energy. Thus, each and every

sector of the economy has shared involvement of energy like in agriculture, industry,

transportation, social and public sector, household and business sector or trade, the use

of energy has become inevitable. Most of the developing and underdeveloped nations

are facing the issue of shortage of energy relative to its needs. (Chaudhry et al., 2015).

Traditional sources such as oil, natural gas, coal and electricity from oil are the most

important sources of energy and this energy supply approximately 90 percent of total

energy requirements at world level (Riaz, 1984). The sharp increase in oil prices and a

shortage of energy creates barriers to bring the rapid growth of the economy (Chaudhry

et al., 2015).

Economic growth of a country is denoted by the gain in Gross Domestic Product (GDP)

or the value of country’s output. On the other hand, economic development of a country

is related to the rise in the living standards of people of the country. Which enhances

consumption, investment and income level in a country. Viable development fulfills the

needs of the present with making future generations capable enough to meet their own

necessities.

The energy is used more extensively in those countries where lifestyle is more

mechanical. So it is important to examine the relationship between energy consumption

and economic growth to formulate energy policies in a country (Chaudhry et al., 2015).

There are number of factors that lead to increasing in demand for renewable energy

sources such as dependency on foreign energy sources, volatility of oil prices,

environmental problems and government policies to promote renewable energy sources

(Apergis & Payne, 2010)

Apergis and Payne (2011) derived four hypothesis relating to energy consumption and

economic growth; First, Growth hypothesis that sights the unidirectional causality

between energy consumption and economic growth. Energy consumption has a vital

role in determining economic growth both directly and indirectly by adding labor and

capital in the production process. If an increase in energy consumption affects economic

growth positively, then there will be a negative impact of energy preservation on

economic growth which is used to reduce consumption of energy. Second,

3

Conservation hypothesis which suggests that if there is a unidirectional causal

connection between economic growth and energy consumption, energy conservation

policies do not affect economic growth negatively. These policies may include a

reduction in greenhouse gas emissions, improvement in energy efficiency, and demand

management measures. Third, Feedback hypothesis that postulates bidirectional

causation between energy consumption and economic growth. It implies that energy

conservation policies may impact economic growth and in turn, economic growth may

also energy conservation policies positively. Lastly, Neutrality hypothesis, it states that

there is no causal link between energy consumption and economic growth. In other

words, energy consumption has no significant impact on real output of a country. In

this hypothesis, energy preservation policies will not affect economic growth inversely.

(Apergis et al, 2012).

Energy utilization is the greatest contributing element to global temperature change,

and additional people mean more energy spending. In fact, 75% of worldwide energy

expenditure happens in urban areas. That utilization is likely to raise as we knew the

movement from 54% of the world’s inhabitants living in city areas in 2014 to 66% by

2050 (Konz, 2015).There are four main essential components of energy use (1) energy

use in residential building, for example, for lighting, boiling, cooking, heating, cooling

and domestic appliances (2) energy use in office building and other non-industrial and

non-residential buildings, such as energy use for lighting, cooling, heating, auxiliary

appliances and office work (3) energy use in building used for entertainment and

leisure, for example shopping malls, theatres and gym centers (4) energy use for urban

traveler transport including both private vehicles and public transportation system

(CCICED Policy Research Report 2009). Rapid urbanization, industrialization, and

development of speculation have a large effect on energy utilization not only in

developed countries but also in developing countries (Shahbaz et al., 2015).

The consumption of energy from renewable sources is expected to rise at the rate of

2.6% per year from 2007 to 2035 whereas; electricity generation share will rise to 23%

in 2035. Hydroelectricity and wind energy shares were 54% and 26% respectively.

These sources have the largest share as compared to other sources of energy (Kaygusuz

et al., 2007; Kaygusuz, 2007; Sovacool, 2009).In 2012 world total energy supply

through RE was 13.2% that increased 22%. IEA has forced to increase that share by

26% in 2020 (IEA, 2015). India is the 5th largest power generator of world energy and

4

its energy demands are rising day by day (Patwardhan, 2010) while China is the world’s

largest power producer (Usage and Population Statistics, 2015) and the 2nd largest

energy consumer (IEA, 2013).

The government of Pakistan made the Alternative Energy Development Board (AEDB)

to promote the renewable energy in Pakistan in May 2013. Its main purpose was to

develop national policies and plans for mobilization of renewable’s with the goal to

attain a 10% share of RE in the total energy mix share in the country by 2015 (Business

Recorder, 2015). Pakistan with huge population is facing very high risks of economy

plus energy crises (Chien & jin, 2008) and country has to tackle this problem of

electricity shortfall at priority (Ahmed et al., 2016). Pakistan has very low oil reserves

so it spends USD 7 billion on the import of fossil fuels for electricity generation

(Khattak et al, 2006; Ashraf et al, 2009). On the backdrop of Inadequate fuel resources

coupled with dwindling economic conditions owing to low capital investment, outdated

power generation system, and liabilities in the forms circular debts supply of energy is

affected badly (GOP, 2014-15).

Potential of renewable or non-renewable energy is energy which can be provided by

specific source annually. Potential depends on technical, economic and geographical

limitations. (Boyle 2004).Energy is an essential part of society and plays a vital role to

improve social and economic living standard of society. With the passage of time man

used various types of resources to generate energy which is starting from wood to

nuclear energy. (Mirza at el., 2008)

Renewable energy resources include wind, solar, hydro, tidal waves, biomass, and

biodiesel, geothermal and non-renewable energy resources include oil, gas, and coal.

Renewable energy resources contribute to 14% of world energy consumption.

(Smaragdaki et al., 2016). In world level the requirement of electricity is increasing

sharply due to population growth and technological development. The demand of

energy overall the world reached 12,730.4 million tons oil equal (mtoe) in 2013, nearly

double that was 6629.8 million Tons oil equivalent in 1980. Among energy resources

Oil has highest percentage for electricity generation 32.9% .It is predictable that by

2100 the global energy demand could boom to 5 times of current energy demand.

Currently fossil fuels full fill three forth of global energy demand. Due to usage of fossil

fuels CO2 emitted in environment which caused greenhouse gases. (Halder et al., 2015)

5

Due to the problem of fossil fuels reduction, problems on energy security and

surroundings issues lead the societies to utilize various sources of energy. Renewable

energy resources are used for electricity production as there are energy scarcities

problems are facing by many countries around the world. As ASEAN countries produce

electricity from fossil fuels. In 2009, about 94.5% of electricity in Malaysia was

produced by usage of fossil fuels. (PTM annual report 2009)

The growth rate of real per capita income of these selected four South Asian countries

is not comparable. According to the statistics revealed by the World Bank in 2014, India

ranked at 7th in the world with having 5.9% growth rate, Sri Lanka ranked at 8th in the

world with 5.7% growth rate and Bangladesh ranked at 12th with 5.2% growth rate. For

the case of Pakistan it ranked at lowest with 2.0% growth rate. South Asia is also one

of the most populous region on the universe.

In South Asia problem of energy, crises are common. Pakistan has to face worst

electricity crises in 2007 when electricity production goes down to 6000 MW.

According to the report of International Energy Agency 38% population is without the

facility for electricity (Nawaz et al). Annual energy demand growth was 8% during

2005 to 2010 if this trend continues than total demand would reach 474 GW in 2050.It

was estimated that Pakistan electricity demand would reach 50,000MW in 2050. (GOP,

2009). In Bangladesh, only 30 % of rural households have the facility to electricity and

in Nepal, load shading goes to almost 20 hours during the dry season (Halder at el.,

2015).

South Asian countries highly depend on imported oil. The region has a vast variety of

resources such as natural gas, oil, coal, wind, solar and hydropower. India is at first

rank in oil resources in South Asia and has the potential of 5,576 million tons of oil

equivalent (Mtoe).Pakistan oil potential is 3,600 million tons and potential in

Bangladesh is 0.96 million tons. Afghanistan tops the region in gas resources with 120

billion cubic meters. Pakistan has the potential of 7,985 billion cubic meters. The

potential of Coal reserves in India are 245,690 million tons, in Pakistan are 185,000

million tons and Bangladesh has 2,715 million tons of coal potential. The region has an

enormous potential for hydro power and only 9% has been utilized. (Regional repot,

2015)

6

There is a huge gap in the region of power demand and supply. Electricity generates

through different resources in India and Pakistan. Bhutan and Nepal depend on

hydropower. Bangladesh is severely reliant on gas and Sri Lanka on oil. Afghanistan

imports from central and west Asia to full fill its energy demand. Nepal has the

80,000MW potential of hydro but installed only 1.83 MW. India, Pakistan, Bhutan have

gross hydropower potential 148,700 MW, 100,00 MW, 30,000MW and installed

capacity is 39,060 MW,6555MW ,1,488MW respectively. Energy assistance could

solve various regional problems but there was a huge potential for each region exist that

need to explore. (Wijayatunga& Fernando, 2013).

Energy is fundamental to the quality of our lives. Nowadays, we are totally dependent

on energy for living and working. It is a key ingredient in all sectors of modern

economies either it is household, industrial, agricultural, transport or any other sector,

it is an important to input for economic development (Turkekul & Unakıtan, 2011).

Energy demand is fulfilled through different sources including both renewable

(sun, wind, wave, biomass and geothermal energies etc) and non-renewable energy

sources (coal, natural gas, oil etc). Energy demand is derived demand (Peach, 2011),

which is required to meet the demand for lighting, cooking, electricity generation

among many other uses. With the increase in population and technological

advancement, energy consumption also increases, while energy supply is limited which

leads to a price increase (Turkekul & Unakıtan, 2011).

Elasticities are calculated to analyze energy demand and supply, which indicates that

how much responsive the energy demanded and supplied is to the relevant variables.

The major energy demand drivers include price of energy, income and substitute price.

Price elasticity of energy measures the degree of responsiveness of energy

demand/supply to change in energy this will be own price elasticity. Price elasticity is

equal to percentage change in quantity divided by percentage change in price. While

cross-price elasticity shows the sensitivity of energy demand to change in the price of

another energy source. Income elasticity measures the degree of responsiveness to real

income. Income elasticity is equal to percentage change in quantity divided by

percentage change in income (Stiglitz et al., 2013).

According to economic theory own price elasticities are typically negative, indicating

the reciprocal relationship between demand and price, while income and substitute

7

elasticities are expected to be positive. If price elasticity of demand is equal to zero then

it is perfectly inelastic, value between zero and one indicates that demand is inelastic

(this occurs when percentage in demand is less than percentage in price) if value is

greater than one so demand more elastic or perfect elastic (demand is affected to a

greater degree by changes In price) (Fan & Hyndman). Changes in income impact

energy demand more than the other components of demand. (Peach, 2011).

Urbanization is also an important demand driver of energy consumption, as

urbanization increases energy consumption increases (Mensah et al., 2015). In addition

to these factors, climate change also affects the energy consumption and production.

When temperature changes requirement for heating and cooling also changes like we

need air conditions in summer and heater for winter. (Dagher, 2011; Fan & Hyndman,

2011; Jamil & Ahmad, 2011; Peach, 2011; Okajima & Okajima, 2013) analyzed the

impact of climate on energy consumption.

Most of the studies estimate the elasticity of specific source of energy and these are

synonym energy elasticity. For example elasticity of electricity demand or oil demand

can be regarded as the elasticity of energy demand. In other words, specific energy

source is a subset of total energy (Peach, 2011).

Estimation of elasticity has great economic importance. Elasticity allows us to predict

behavioral responses to state energy policy. These elasticities are helpful in the

formulation of tax policy, if energy demand is price inelastic, then with the imposition

of tax on those energy sources will lead the consumers to adjust their expenditures on

other goods (Hamilton, 2011).

Elasticity estimates are helpful to control energy consumption and emission of CO2

(Burke & Liao, 2015). Non-renewable energy sources cause CO2 emission and lead to

global warming. The issue of climate change can be addressed with the use of

renewable energy, as the greenhouse gas emission reduces its use (Sadorsky, 2009).

Along with GHG emission and global warming , the issues of energy security is

emerging , Renewable energy plays an important role in reducing an emerging

country’s dependence on imported energy products (like oil and gas)., one way to deal

with these problems is to substitute renewable energy for non-renewable energy sources

8

(Sadorsky, 2009). Estimation of demand and supply elasticity of energy sources

separately will describe substitute ability of these sources energy (peach, 2011).

Between 2005 and 2030, renewable energy demand in China and India is expected to

grow at an annual average rate of 9.9% and 11.7%, respectively (IEA, 2007, p. 119).The

emerging economies have more opportunity to increase the usage of renewable energy

(Sadorsky, 2009). Emerging economies have more than 40% of existing renewable

electricity capacity, more than 70% of existing solar hot water capacity, and 45% of

biofuels production, for renewable power generation China and India both rank in the

top five countries (REN21, 2008).

1.1 Research Motivation

An extraordinary number of exact investigations have managed distinctive parts of

energy and development issues utilizing both hypothetical and experimental proof. The

audit of writing states that a relationship exists between energy use and economic

development. Be that as it may, with regards to whether energy use is an aftereffect of,

or an essential for, economic progress, there are no certain conclusions in the writing.

Stern and Cleveland (2004) see energy as a fundamental factor of creation

notwithstanding capital, work, and materials and in this manner proposed that energy

is vital for development. As opposed to the above view, Toman and Jemelkova (2003)

contended that economic advancement affects energy use. Empirically, Masih and

Masih (1996) find that energy use is essential for economic development in India. Then

again, Ghosh (2002), who additionally analyzed the connection between energy use and

economic development in India, find that energy use is a consequence of economic

development. In this manner, additionally look into on the connection between energy

use and economic development might be expected to deliver this issue because of the

blended hypothetical perspectives and observational discoveries in the literature.

As specified before, the connection between renewable and non-renewable energy

sources and economic development is related to the financial matters of energy demand.

Energy demand gauges have been utilized by various analysts and strategy chiefs to

research request conduct and furthermore to forecast, request administration and outline

of fitting energy approaches (Halicioglu, 2007). The greater part of these examinations

regularly investigate the long run and here and now effect of GDP and energy price on

9

total utilization of at least one fills, in singular segments. Since non-renewable energy

source has engaged the world economic development for a long time. The consumption

of non-sustainable power sources and the issue of an Earth-wide temperature boost, be

that as it may, have as of late pulled in wide consideration toward creating substitute

energy sources (Simsek and, Simsek, 2013). With the advances in innovation and task

for environmental manageability, renewable energy sources are winding up

progressively noteworthy options. In the meantime, renewable energy sources in the

vast majority of developing and rising economies are to a great extent undeveloped

while at the same time these nations are taking part in a worldwide progress to spotless

and low-carbon energy frameworks.

Thus, the emerging issue for empirical examination in energy led economic

development literature is that whether a progress from nonrenewable energy to, the

renewable energy source can manage economic progress in developing nations (Maji,

2015; Bhattacharya, et al. 2016). In reality, examination of the relative impacts of,

renewable energy and non-renewable energy sources on economic progress gives

profitable experiences to outline and execute reasonable energy and environmental

strategies (Apergis and Payne, 2012; Omri, 2014). The target of the present examination

is to analyze the effect of both, renewable and non-renewable energy sources use on

monetary development in India, Pakistan, Bangladesh and Sri Lanka.

1.2 Research Objectives

The main objective of the study will be to examine the prospects of renewable and non-

renewable energy sources in selected South Asian countries namely: India, Pakistan,

Bangladesh and Sri Lanka over the period of 1980 to 2014. In order to fulfill this central

objective, the specific objectives are as follows:

1. To examine empirically the impact of renewable and nonrenewable energy

sources on economic growth in South Asian economies.

2. To examine empirically the impact of renewable and nonrenewable energy

sources on environmental quality in South Asian economies.

10

3. To examine the determinants of demand for renewable and nonrenewable

energy sources in South Asian countries.

4. To estimate the elasticity of demand for renewable and nonrenewable energy

market in South Asian countries.

5. To examine empirically the impact of renewable and nonrenewable energy

sources on energy intensity in South Asian economies.

6. To explore the potential and prospects for renewable and nonrenewable energy

sources at South Asian economies.

7. To suggest policy implications for the concerned stakeholders to help in

decision making.

1.3 Research Contribution

There is a limited literature on South Asian energy sources including both renewable

and non-renewable energy sources. Previously studies mentioned in literature reviews

explored the relationship between energy consumption and economic development and

environment. This research work fill this gap by considering the renewable and non-

renewable energy sources with their demand elasticity in the south Asian region.

Another contribution of this study will be to undertake both regional level analysis

using panel data techniques and country-specific analysis using time-series data

techniques. Last commitment of this work will be the employment of the most recent

panel data analysis techniques for empirical analysis. Further, it will explore the

causality linkages between indicators by applying the recently evolved causality

procedure of Dumitrescu and Hurlin (2012).

1.4 Research Structure

Keeping in view the above mentioned research objectives of the thesis, the structure of

the research work will be consists of five chapters: first chapter introduces the research

background and gives an overview of the central objectives that can be achieved later

by this research. Second chapter is about the review of the literature related to the

prospects of renewable and non-renewable energy sources. Third chapter provides a

11

theoretical framework for the investigations. This chapter also discuss the methodology

and data sources for the study. The results of the data analysis are presented in fourth

chapter. Conclusions and policy recommendations drawn from the analysis are

discussed in fifth chapter. All reference of the cited literature and appendix are given in

the end.

12

CHAPTER 2

REVIEW OF LITERATURE

Both with regards to developed and developing countries, there has been far reaching

hypothetical and observational exploration to date that endeavors to concentrate on

renewable and nonrenewable energy sources and growth as well as on environmental

degradation. This section presents a brief review of the previous literature in two folds:

empiciiacal as well as theoretical.

2.1 Empirical Literature

According to the research objectives the empirical literature further categorized into

different parts. It explores firstly, the relationship between economic growth and both

energy sources with various model specifications. Secondly, the impact of both energy

sources on CO2 emissions and energy intensity. Thirdly, it investigates the factors of

energy demand and lastly it explores the relationship of energy sources, economic

growth and energy intensity.

2.1.1 Renewable and Non-Renewable Energy and Economic Growth

At the macroeconomic level, various examinations can be discovered supporting each

of the previously mentioned theories. Kraft and Kraft's (1978) investigation of the

United State started the literature. Their examination investigates the connection

between energy utilization and GDP. They found unidirectional causality from gross

domestic progress to vitality utilization yet not the other way around. Yu and Jin (1992)

was the first investigation to apply co-joining investigation to the United States. No

proof is found for a co-incorporating relationship inside the information supporting the

finish of Kraft and Kraft (1978). Co-integration investigation has turned into the

prevailing strategy to test for the nearness of the energy output speculations. Soytas and

Sari (2003) analyzed the G-7 and selected developing economies. They affirm the

finding of no causality from energy utilization to income in the United States. Lee

(2006) utilizing per capita GSP and total energy utilization find bidirectional causality

in the United States. Lee (2005) and Keppler (2007) are astounding outlines of different

economies. This little specimen of the writing proposes an accord has not risen up out

of the exact trial of this issue.

13

Stern (1993) found in the United States of America, the causal relationship between

energy (use) and gross domestic product. He used a weighted index of energy quality

by shifting lower quality energy like coal to higher quality energy like electricity.

Author employed multivariable vector autoregressive and causality tests. In the analysis

he found total use of energy did not Granger cause GDP. Again Stern (2000)

investigated the causal relationship between energy use and gross domestic product in

United States of America from 1948 to 1994. He contradicted the previous studies by

including the factors GDP, labor, capital and quality weighted energy and established

the insignificant role of labor, capital and technical change in output determination.

Cheng and Lai (1997) investigated the causal relationship between energy consumption

and economic growth in on side and the also computed causal relationship between

energy consumption and employment in the other side. Authors employed annual data

on energy consumption, gross domestic product and consumer price index for the case

of Taiwan from 1955 to 1993. They utilized Hsiao’s Granger causality and found a

positive impact of energy on growth and employment and concluded that for the

progress of economy energy is the essential ingredient. Furthermore, they advocated

that the higher level of output will influence the use of energy positively which in turn

raise the employment level.

Adjaye (2000) computed the association between energy use and per capita income for

the case of India, Thailand, Indonesia, and Philippines. He included the variables such

as energy for marketable, per capita income and prices of energy (a proxy of CPI). He

used different time spams for a couple of countries such as from 1973 to 1995 for the

case of India and Indonesia and from 1971 to 1995 for the case of Thailand and

Philippines. By utilizing Granger causality through error correction model he found

unidirectional causality between energy and income for India and Indonesia, whereas

bidirectional causality between energy and income for Thailand and Philippines.Ghosh

(2000) found no long run but unidirectional affiliation between income and electricity

utilization from 1950 to 1997 in India.

In the case of Pakistan Aqeel and Butt (2001) investigated the said Cheng and Lai

(1997) similar relationship with the extension that consumption of petroleum would be

possible due to the rapid growth. He also found there was no relation between the

economy in growth and gas consumption. However, in the power sector, he found that

14

electricity consumption led to economic growth without feedback. Finally, positive

relationship between energy and employment was found.

Altinay and Karagol (2004) estimated the link between energy consumption and

economic progress in Turkey from 1950 to 2000. They measured economic growth by

gross domestic product and energy by consumption of total energy and found no

causality by applying Hsiao’s Granger causality approach. Altinay and Karagol (2004)

also estimated the link between electricity consumption and per capita GDP again in

Turkey from 1950 to 2000 with structural break. Unidirectional causality was found

from electricity consumption to real income by Standard Granger causality approach.

Ghali and Sakka (2004) measured china’s energy situation with the connection of

energy use and per capita income including labor and capital for the era of 1961-1997.

They used multivariable co-integration approach and vector error correction model on

the anticipated structure based on neo-classical single factor aggregate production

technology. The said structure treated capital, labor and energy as separate input. The

empirical results showed that output, labor, capital, and energy share two common

stochastic trends.

Shiu and Lam (2004) measured the connection between electricity use and per capita

income in China for the era of 1971-2001. They found a co-integrated relation between

electricity use and income by applying Johanson (1988) maximum likelihood approach

and also found unidirectional causality running from electricity use to income.

Siddiqui (2004) investigated causality between economic growth and energy use in

Pakistan in the era of 1971-2003. Author measured the part of the energy in economic

progress by including the indicators of labor, capital human capital formation and

exports along with various energy sources (gas and electricity). The study found a

significant impact of electricity on growth whereas, no link between gas and output was

found.

Oh and Lee (2004) investigated the relationship between energy consumption and

growth rate of the economy including labor and capital for Korea on time series data

from 1970 to 1999. Johanson and Juselius (1990) co-integration approach and Granger

causality approach through vector error correction model were applied. They found a

positive long-run relationship between variables and unidirectional causality from

growth to energy. Oh and Lee (2004) reinvestigated the causal relationship in Korea for

15

the era of 1981-2004 and found long-run unidirectional causality from growth to energy

but no causality in short run.

Paul and Bhattacharya (2004) investigated the causality between consumption of

commercial energy and real income with the gross fixed capital formation and labor for

India from 1950-1996. Johansen multivariable approach (1991) was applied and the

positive causal relationship was found in short and long run. Authors concluded that

non-commercial energy should be substituted by commercial energy with the use of

technological progress and increased income in long run.

Yoo (2005) estimated the causal link between electricity use and real income in four

members (Indonesia, Singapore, Malaysia, and Thailand) of the Association of South

East Asian Nations for the era of 1971-2002. Using modern time series techniques he

found two-way causality between electricity use and real income in Malaysia and

Singapore whereas, there was one-way causality between both factors in Indonesia and

Thailand. In other two countries like Malaysia and Singapore, the results indicated that

electricity use had a direct effect on economic progress in turns the economic progress

stimulated more electricity use in both nations.

Lee (2005) computed the causal relationship between energy consumption and gross

domestic product in eighteen developing countries for the era of 1975-2001. He applied

FMOLS (Full modifies ordinary least square) and Granger causality techniques and

found long-run positive relationship between said indicators. He also found short-run

causality from energy consumption to gross domestic product and on the basis of results

he concluded that in developing countries energy conservation would be harmful to

economic growth.

Narayan and Singh (2006) examined the causal link between electricity use, real gross

domestic product and labor force for the case of Fiji. They applied ARDL bounds co-

integration and Granger causality approaches in the era of 1971-2002 and found

electricity use, income, and labor force were only co-integrated when income was used

as an endogenous variable. They also found unidirectional causality from electricity use

and labor force to income and concluded that conservation policies of energy could be

effect adversely on economic progress. Ho and Siu (2006) estimated the causal link

between electricity use and real income including consumer price index in Hong Kong

by using co-integration and VECM model for the era of 1966-2002. They found long-

run equilibrium link between electricity use and real income and also found

16

unidirectional causality running from electricity use to real income in short run.

Similarly, Yuana et al. (2006) projected the causal connection between electricity use

and real income (GDP) in China for the era of 1978-2004. The results of co-integration

and Granger causality showed the long run relation between variables under

consideration and one way causality running from electricity use to real income.

Rufael (2006) investigated the per capita electricity consumption and per capita real

GDP in 17 Countries of Africa for a period of 1971 to 2001. Time series data were used

to analyze long-run causal relationship between per capita consumption of electricity

and per capita real GDP by applying Pesaran et al. (2001) co-integration test. The

author also used the reformed description of Granger causality test as a result of Toda

and Yamamoto (1995). The author found evidence of log run relation between the said

two variables in 9 countries out of 17 countries and Granger causality in only 12

countries. Similarly, Rufael (2006) found a causal relationship between different kind

of energy from industries and real GDP in the time spam of 1952- 1999 in Shangai.

Author found unidirectional causality running from total energy and coke, electricity

and coal to economic growth. No causality was found between oil and economic

growth.

Lund (2007) determined the renewable energy resources to make strategies for

sustainable development in Denmark. Three technological changes were considered for

sustainable development. These changes were energy saving on demand side,

improvement in producing energy, and use of other sources of renewable energy rather

fossil fuels. This paper discussed the problems/perspectives of conversion of present

energy systems into a 100% renewable energy system. Which include transport sector

in future strategies. It was focused that whether a 100% renewable energy system was

a possibility for Denmark or not. Energy PLAN model was used to analyze the

country’s utilization of renewable energy sources in long run. Results showed all

technological changes lead to decrease in fuel consumption. The conclusion for

development was possible which was that there must be less use of oil transportation

than other sources. Second, use of small CHP plants in the system. Third, include a

focus on the wind power of the electricity supply. If these technological improvements

were achieved the renewable energy system could be created for sustainable

development.

17

Zamani (2007) examined the causal link between energy in various forms and economic

progress for the case of Iran for the era of 1967-2003. The author also analyzed the link

between agricultural and industrial sectors of Iran. The results confirmed the causality

between agricultural and industrial sectors, long-run bidirectional causality between

GDP and energy (gas) was also found.

Tang (2008) examined the causal link between electricity use and economic progress

in Malaysia for the era of 1972-2003. They applied ARDL and VECM models and

found no co-integration in Malaysia. However, the standard Granger’s test and

MWALD test found two way link between electricity use and economic growth.

Erdal et al., (2008) investigated the inter-link between energy consumption and

economic growth in the case of Turkey from the time period of 1970 to 2006. Granger

causality panel root unit tests and co-integration tests were used in this study. There

was bi-directional relationship between economic growth and energy consumption

which differed from previous studies. This showed that increase in energy consumption

increases economic growth. It was recommended that the dependence on external

sources of energy like fossil fuel or imported oil should be reduced in the case of

Turkey. Policies regarding environmental protection and energy supply security should

be taken into consideration.

Lee and Chang (2008) computed the causal relationship between energy consumption,

capital stock, labor input and real gross domestic product in sixteen developing

countries for the era of 1975-2001. He applied FMOLS (Full modifies ordinary least

square) technique to estimate co-integration vectors for heterogeneous panels. They

also applied vector error correction model for dynamic analysis of heterogeneous

panels. They found a positive long run positive relationship between said indicators. In

short run, there existed no causality between variables.

Sadorsky (2009) presented an empirical model of renewable energy consumption for

Group of 7 economies to analyze economic and societal issues regarding energy

security and global warming. In this paper, renewable energy was assumed to be a

substitute for oil. Annual data for G7 countries was collected on renewable energy

consumption, real GDP, population, CO2 emissions and oil prices. Panel co-integration

unit root tests were used to compute long run elasticities and Error correction model

(ECM) approach was used for short term elasticity. In long run real GDP per capita and

CO2 emissions were found to be a driver for renewable energy consumption. While in

18

short run renewable energy consumption were carried by its movement back to long

term equilibrium due to short run shocks. Study suggested that there would be a greater

reliance on renewable energy consumption due to energy security and global warming

concerns.

Apergis and Payne (2009) employed a panel data set for six Central American countries

to show the causal relationship between energy consumption and economic growth by

taking into account the other variables Labor and Capital. Error correction model,

Heterogeneous panel co-integration tests, panel root tests and heterogeneity tests were

used by taking annual data from 1980-2004. Heterogeneous panel co-integration test

revealed that there was the positive impact of real GDP, capital formation and labor

force on energy consumption. While Error correction model extended that there exist

short term as well as long term Granger causality from energy consumption to economic

growth. This study focused and suggested that government must divert its attention to

implement effective energy supply and demand policies in long term.

Ma et al., (2010) surveyed china’s unfavourable energy situations, it's high energy

intensity and need of development programs for environmental protection. Paper

reviewed Renewable energy laws and development policies and gaps in reviewing the

development of the country. Continuous improvement in the mobilization of renewable

energy economy was relayed on Government support programs. More research was

required to investigate and address many issues in China's economy. Renewable energy

researcher and economists needed to pay more attention to Grain-based biofuel energy

production and renewable energy substitution possibilities with fossil energy for

renewable energy economic development.

Lund et al., (2010) discussed 37 tools review individually in detail. The energy tools

were diverse because of their structure, operation, and application. Previous studies did

not provide a vast analysis of any other tools. Each of energy tool reviewed individually

in this paper. It was objected that which energy tool could make 100% renewable

energy system. The survey on these tools was conducted by tools developer’s project

at the University of Limerick. There was no computer single energy tool that solved all

issues related to the inclusion of renewable energy. Relative to the electricity sector,

CHP facility was attainable by the energy PRO tool. Different types of energy tools

were available for different conditions of analysis.

19

Apergis. N and Payne J E (2010) extended the investigations on the causal relationship

between renewable energy consumption and economic growth to the region of Eurasia.

Two panel data sets were used to conduct the empirical analysis. To define the

understanding of the results the data sets included with and without Russia. Panel data

from 1978 to 2007 of 13 countries within Eurasia was taken from World Bank

development indicator. Heterogeneous panel co-integration, panel error correction

model, and FMOLS were applied to estimate the results. Apergis and Danuletiu (2014)

also found same investigations in the case of 8o countries. In the US for the period of

1949-1960 Bowden and Payne (2010) found the positive and significant relationship

among GDP, renewable and non-renewable energy consumption in individual sectors.

Apergis and Payne (2010a) investigated the linkage between sustainable power source

utilization and monetary development over the period 1985-2005 inside the

multivariate structure. Past examinations utilized renewables to address the present

vitality utilization issues yet additionally demonstrated reasonable improvement. The

investigation contained research on twenty OECD nations to think about the degree to

which monetary development was affected by utilization of sustainable power sources.

Heterogeneous board co-coordination finding guaranteed a long-run connection

between genuine GDP, sustainable power source utilization, real gross fixed capital

formation, and the labor force. A panel vector error correction showed the existence of

both short-run and long-run bidirectional connection between utilization of

inexhaustible and financial development. Paper recommended government

arrangements required to diminish nation's reliance on outside sources.

Apergis and Payne (2010b) extended the research on the causal relationship between

renewable energy consumption and economic growth with the inclusion of measures