Languages

Pages

Legal

Preferred Stock Freeze

Copyright 2005 Dwight Drake. All Rights Reserved.Business Planning: Closely Held Enterpriseswww. drake-business-planning.com

Family Corp

Common Stock Cumulative Preferred

Parent

No hope with S corp - One Class of Stock Requirement Double tax hit on preferred dividend Real Killer - preferred value under 2701 based sole on market value of cumulative yield. All other value in common under 2701 Hence, strategy only works with extreme annual growth rate

Gift Common Stock Children

Law T510 - Estate and Gift Tax-Instructor: Dwight Drake

2701 – The Anti-Freeze Statute.

When 2701 doesn’t apply:

1. Non-family transfers.2. Market quotations readily available to value applicable

retained interests (“ARI”).3. ARI same class as interest transferred.4. ARI is proportional to interests transferred.

When does 2701 apply:

1. Transfer to family member.2. Transferor retains ARIs.3. Conditions 1 to 4 above don’t apply.

Consequence of 2701: All ARIs except “qualified payment”valued at zero and junior security transferred, at minimum, must satisfy 10% rule.

Law T510 - Estate and Gift Tax-Instructor: Dwight Drake

2701 – The Anti-Freeze Statute.

What is “applicable retained interest’?

• “Distribution right” – right to receive distribution on stock where, after transfer, T and family own 50% of stock.

• Liquidation, put, call or conversion right (but not proportionalconversions).

What is “qualified payment”?

• Cumulative dividend or partnership equivalent.• Any payment within legal document that is elected to be

treated as “qualified payment.”

Downside of “qualified payment” – If not paid, 2701(d) kicks in to subject failures to pay, plus interest, to added estate and gifttaxes.

Unrelated Party Common Stock Sale

Copyright 2005 Dwight Drake. All Rights Reserved.Business Planning: Closely Held Enterpriseswww. drake-business-planning.com

6-21

Family Corp

$ 3 Mill Common$ 2 Mill Non-cum Preferred

Parent

Parent Income Tax = $ 3 mill less common stock basis

Common StockUnrelated Party

$ 3 Mill Cash, Notes

Preferred Stock 2701 Trap

Copyright 2005 Dwight Drake. All Rights Reserved.Business Planning: Closely Held Enterpriseswww. drake-business-planning.com

6-21

Family Corp

$ 3 Mill Common$ 2 Mill Non-cum Preferred

Parent

Parent Income Tax = $ 3 mill less common stock basis PlusTaxable Gift of $2 million. Plus - Parent still owns preferred

Common StockRelated Party

$ 3 Mill Cash, Notes

Grantor Retained Annuity Trust

Copyright 2005 Dwight Drake. All Rights Reserved.Business Planning: Closely Held Enterpriseswww. drake-business-planning.com

Trust

AnnuityTerm of Years

Parent &Estate

Fixed Annuity Amount

Fixed Annuity Term

Annuity Paid Annually

No Debt, Etc.

No additions or others

Mortality Risk of Deal

Yield Risk of Deal

A “Darling”

Children

PropertyRemainder

GRAT Something For Nothing Example

Copyright 2005 Dwight Drake. All Rights Reserved.Business Planning: Closely Held Enterpriseswww. drake-business-planning.com

Trust

Annuity $ 336,291 yr.Term - 5 Yr

Parent &Estate

7529 Rate 5.4%

Zero Remainder Value

Annuity Funded Heavily From Principal

5 Yr Mortality Risk

Any Remainder Pass Transfer Tax FreeChildren

Property$ 1.44 Mill

Remainder

Copyright 2005 Dwight Drake. All Rights Reserved.Business Planning: Closely Held Enterpriseswww. drake-business-planning.com

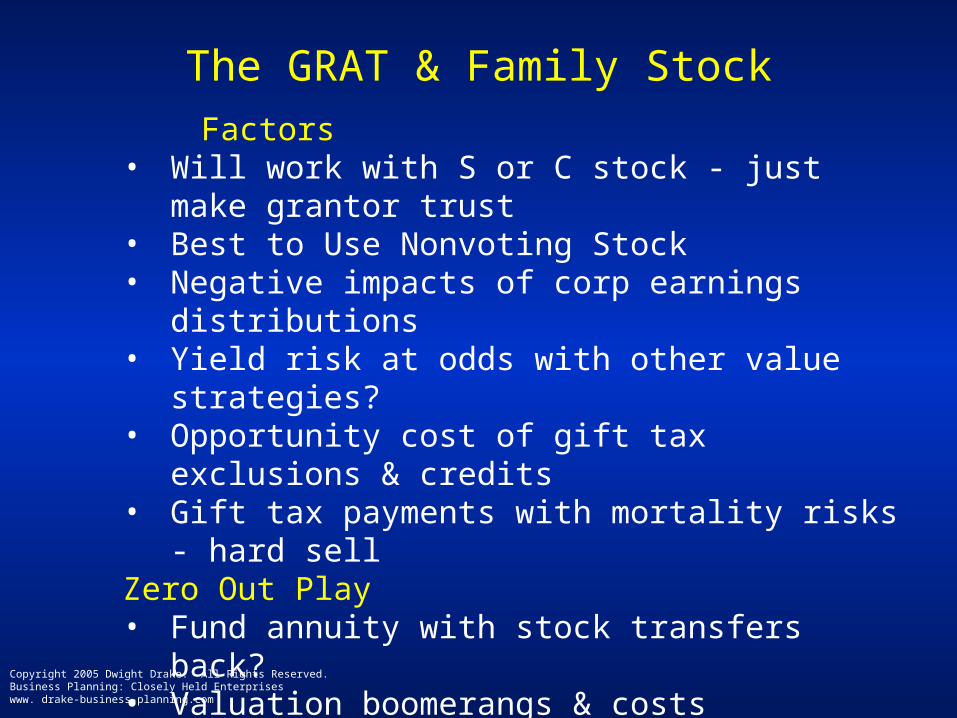

The GRAT & Family Stock

Factors • Will work with S or C stock - just make grantor trust• Best to Use Nonvoting Stock• Negative impacts of corp earnings distributions• Yield risk at odds with other value strategies? • Opportunity cost of gift tax exclusions & credits • Gift tax payments with mortality risks - hard sellZero Out Play• Fund annuity with stock transfers back?• Valuation boomerangs & costs• Impacts on health of business• Big costs and risks v. how much real benefit• Screwy message to inside kids

3 YEAR GRIT

Copyright 2005 Dwight Drake. All Rights Reserved.Business Planning: Closely Held Enterpriseswww. drake-business-planning.com

Trust

All trust incomeTerm - 3 Yr

Parent

Term value zero

Remainder Value 100%

Parent pays gift taxes

Gift taxes in parent estate if death within 3 yr

Parent death within 3 yr term triggers basis step-up

Trade-off is appreciation included in estate

Nullity if parent survives 3 yr term

Children

PropertyRemainder

Copyright 2005 Dwight Drake. All Rights Reserved.Business Planning: Closely Held Enterpriseswww. drake-business-planning.com

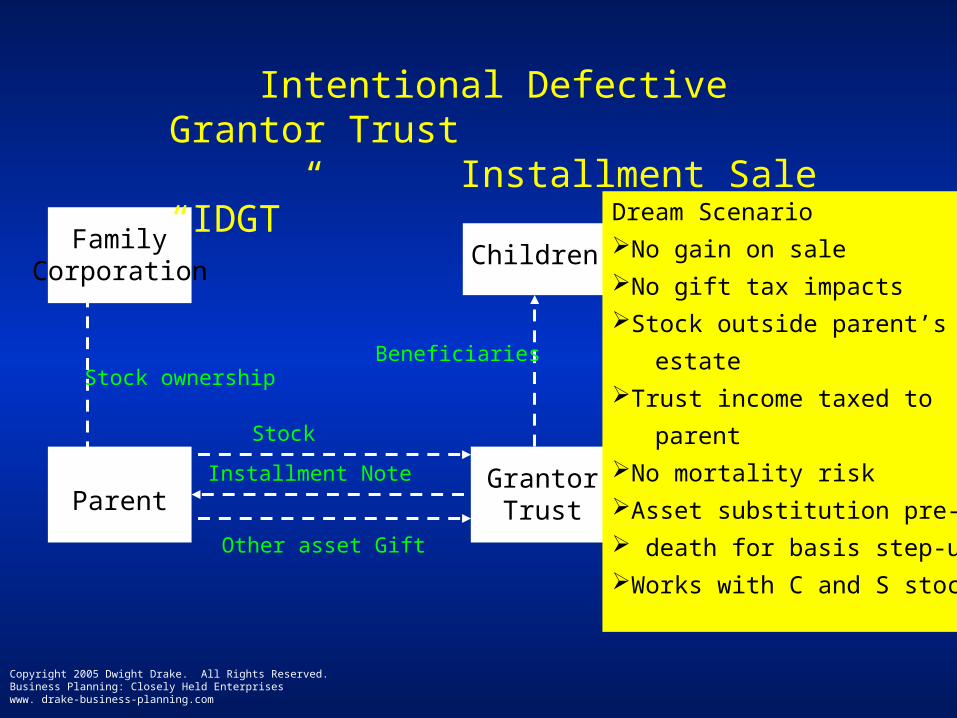

Parent

FamilyCorporation

GrantorTrust

Intentional Defective Grantor Trust Installment Sale “IDGT”

Stock

Installment Note

Stock ownership

Other asset Gift

Children

Beneficiaries

Dream Scenario

No gain on sale

No gift tax impacts

Stock outside parent’s

estate

Trust income taxed to

parent

No mortality risk

Asset substitution pre-

death for basis step-up

Works with C and S stock

Copyright 2005 Dwight Drake. All Rights Reserved.Business Planning: Closely Held Enterpriseswww. drake-business-planning.com

IDGT Issues

What we think we know:• Dual status possible• No gain on sale to grantor trust• No gift tax on income tax payments by parent• No estate inclusion under 2036 if parent outlive note

What we are not sure of:• Gift tax impact going in if interest rate is applicable federal rate• Estate inclusion under 2036 if death before note paid• Debt v. retained equity on note – need for other assets equal to

10%

What we don’t know• Tax treatment on note payments post death – IRD?

• Gain recognition on note on grantor trust status termination

• Basis impacts on death with grantor trust termination

Copyright 2005 Dwight Drake. All Rights Reserved.Business Planning: Closely Held Enterpriseswww. drake-business-planning.com

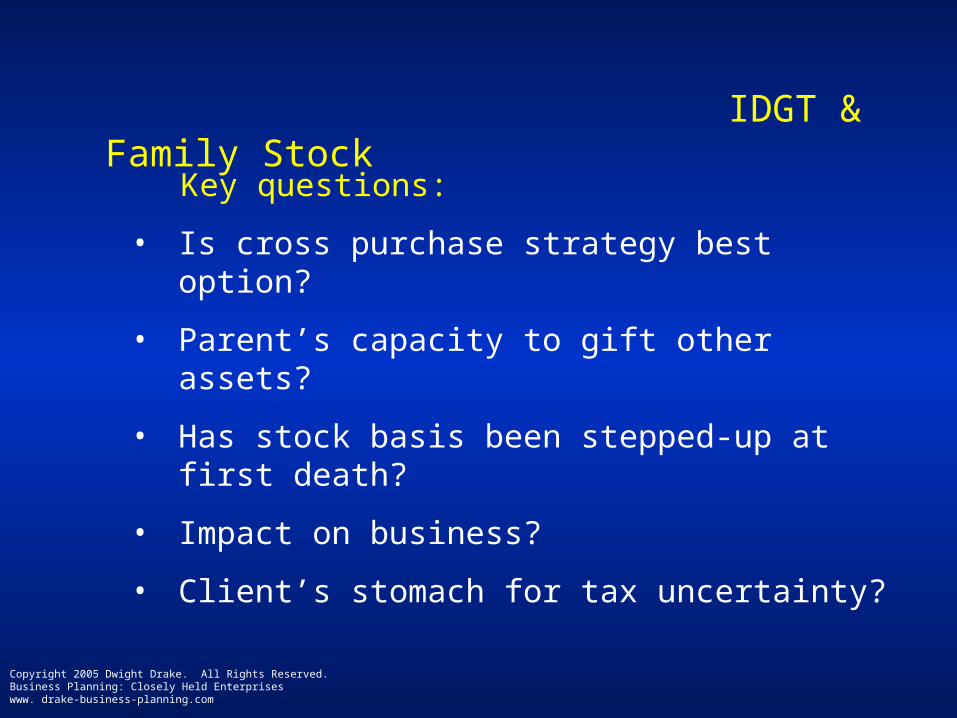

IDGT & Family Stock

Key questions:

• Is cross purchase strategy best option?

• Parent’s capacity to gift other assets?

• Has stock basis been stepped-up at first death?

• Impact on business?

• Client’s stomach for tax uncertainty?

Copyright 2005 Dwight Drake. All Rights Reserved.Business Planning: Closely Held Enterpriseswww. drake-business-planning.com

Parents

Assets

Limited Partnership

Children

Distributions

Family LP Disappearing Act

Assets DistributionsLPUnits

Distributions

S Corp

Gift of Assets

GP Units

Assets

Stock

Bottom Line Goal: Valuation Discounts in Parent’s Estate

Top Related