Languages

Pages

Legal

pwc

Portfolio review: Reviving those languishing investments

26th March 2003

PricewaterhouseCoopersReviving those languishing investments 2

Agenda

Introduction and welcomeBackground Market situationImpact of languishing investments on portfolio returnsThe Control WatershedEarly warning signsExperiencing a turnaroundLessons from the marketplaceSummary and Q&A

PricewaterhouseCoopersReviving those languishing investments 3

Summary

Need to inject time effort and energy in your languishing investmentsReal value-add for the exitWatch out for the loss of controlWarning signs are there to see……act on themBut it is hard work – and needs close attentionPrevention is better than the cure

PricewaterhouseCoopersReviving those languishing investments 4

Discussions, interviews and assignments with

BanksPE Houses

Background research

PricewaterhouseCoopersReviving those languishing investments 5

Market situation-it’s getting harder

Increased competition for deals

Much greater vendor sophistication

Increasing requirement to demonstrably add value to deals

Increasing number of unexited companies in portfolios

Dramatic decline in stock markets has eliminated PE arbitrage

Limited scope for exit via IPO

Exit valuations and multiples likely to be lower

Increased competition for future funds

So what is your new valueSo what is your new value--added? added?

PricewaterhouseCoopersReviving those languishing investments 6

PE house approaches vary widely

Passive Investor

“ Management’s role to run the business”

• Non-exec board participation• Monthly figures• Annual review• No team allocated to portfolio

company management• Financial expertise driven

CorporateOwner

“Our role to create the value, working closely with management”

• More than one non-exec appointment

• KPI reporting• Joint strategy development• Involvement in business detail• PE house staff dedicated to

portfolio companies

PricewaterhouseCoopersReviving those languishing investments 7

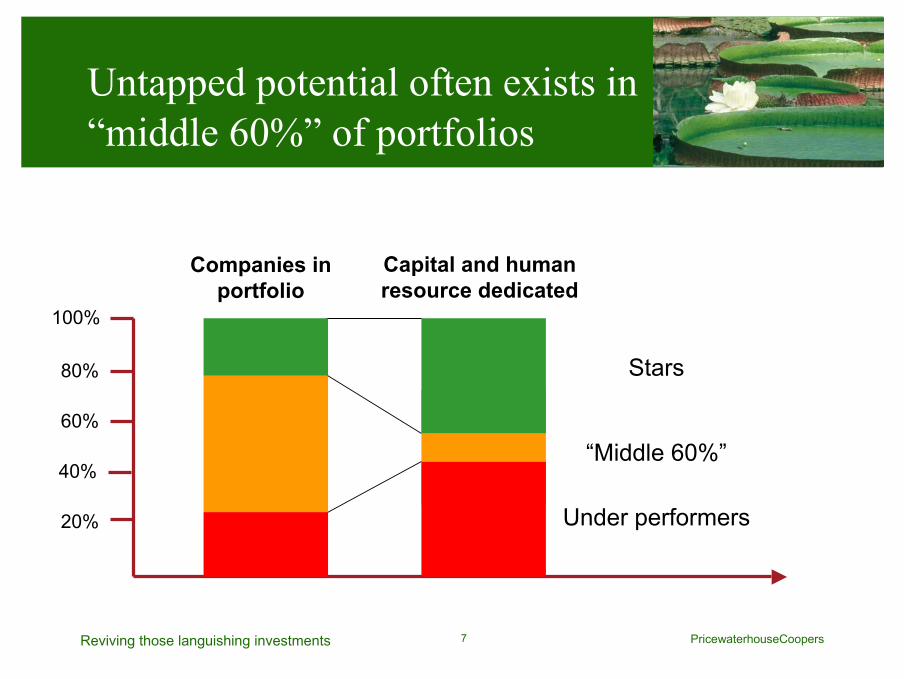

Companies in portfolio

Capital and human resource dedicated

20%

80%

100%

Stars

“Middle 60%”

Under performers

60%

40%

Untapped potential often exists in “middle 60%” of portfolios

PricewaterhouseCoopersReviving those languishing investments 8

Why performance starts to drift

Performance targets not achievedCulture doesn’t make the transition to owner/managerManagement disillusionment/departuresInvestment manager boredom and lack of focus“Satisfactory underperformance” not noticedCompetitors attack on signs of weaknessDownward spiral

PricewaterhouseCoopersReviving those languishing investments 9

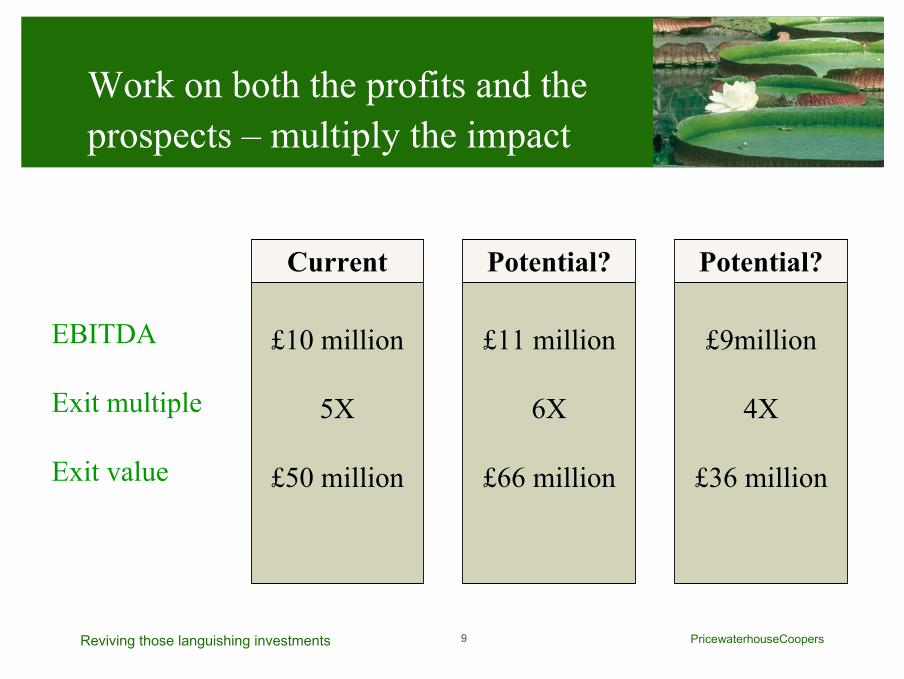

Work on both the profits and the prospects – multiply the impact

EBITDA

Exit multiple

Exit value

£10 million

5X

£50 million

Current

£11 million

6X

£66 million

Potential?

£9million

4X

£36 million

Potential?

PricewaterhouseCoopersReviving those languishing investments 10

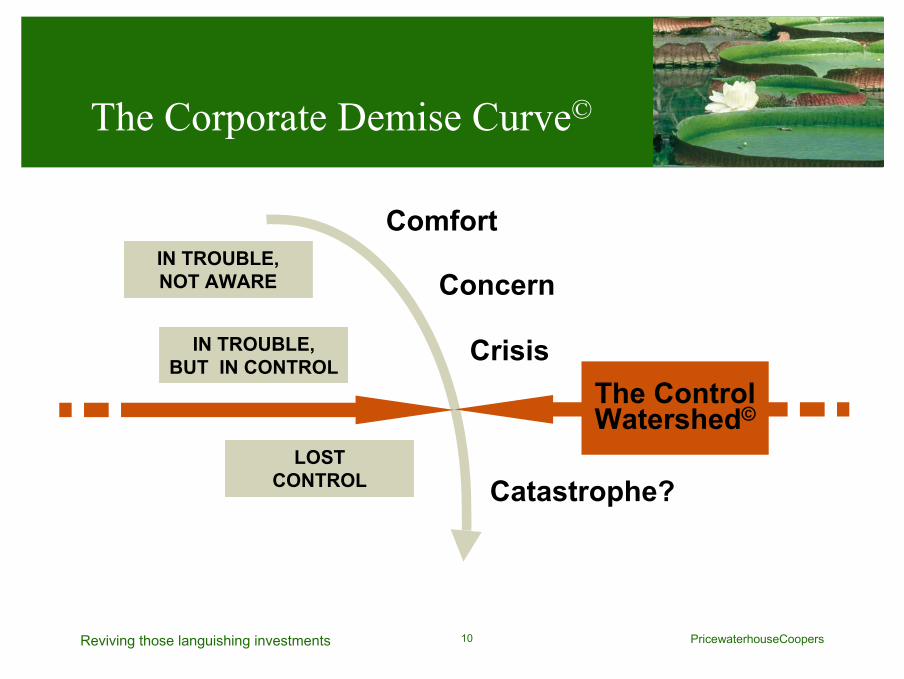

The Corporate Demise Curve©

IN TROUBLE,NOT AWARE

LOST CONTROL

IN TROUBLE,BUT IN CONTROL

The ControlWatershed©

Comfort

Concern

Crisis

Catastrophe?

PricewaterhouseCoopersReviving those languishing investments 11

So what are the warning signs?

Management Financial

Soft

Operational

Embarrassing complexity

Can’t articulatestrategy

Failure tomeet deadlines

Incomparablecomparatives

Director churn

Inability toprioritise

Increasing tensionwith stakeholder

Excessive growth

Infinite ‘one-offs’

Opaque transparency

Wild fluctuations

Regular policy changes

Business plan lacks objectivity

Superficial forecasting

(Non) working capital

Loss of key customers

Unattractive products

Downgrades

PricewaterhouseCoopersReviving those languishing investments 12

So how do you get out of this space?

TURNAROUND POINT

TURNAROUND or EXIT

CHANGE AGENT

APPOINTED

OPERATIONAL SKILLS

THE

TURNAROUND

CORRIDOR©

TACTICAL SKILLS

PricewaterhouseCoopersReviving those languishing investments 13

Experiencing a turnaround –how it feels…

Who am I?Initial prejudicesWhat happened?My view of the processResults achievedLessons learnt

PricewaterhouseCoopersReviving those languishing investments 14

You never know what’s round the corner!

PricewaterhouseCoopersReviving those languishing investments 15

Don’t panic!

PricewaterhouseCoopersReviving those languishing investments 16

You can make a REAL difference

PricewaterhouseCoopersReviving those languishing investments 17

Learning from the market-place

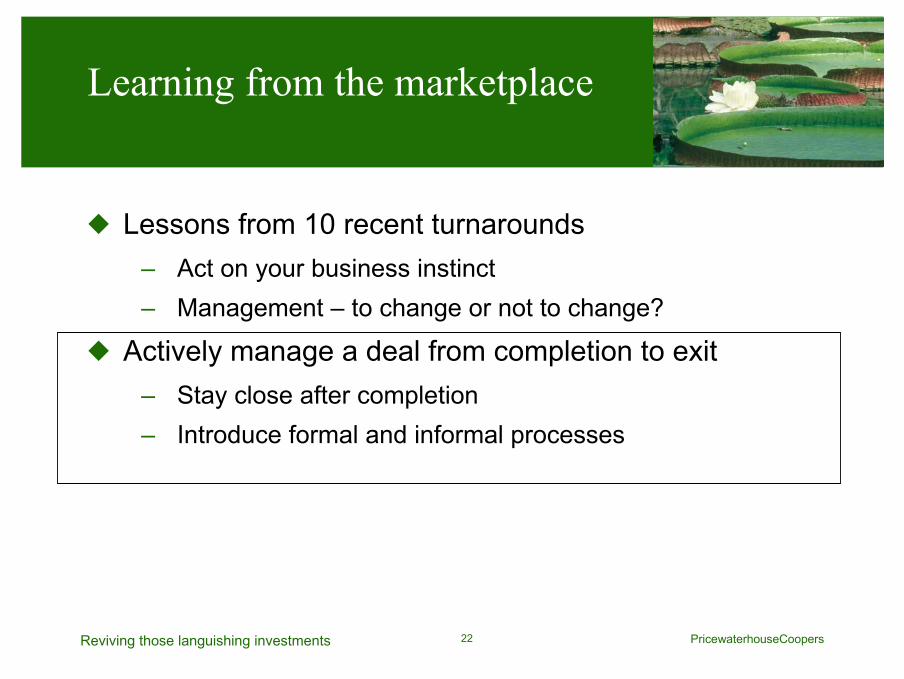

Lessons from 10 recent turnarounds– Act on your business instinct– Management – to change or not to change?

Actively manage a deal from completion to exit– Stay close after completion– Introduce formal and informal processes

PricewaterhouseCoopersReviving those languishing investments 18

Financial Strategic

Operational

CorporateFinance

Approach to turnarounds

Future directionCompetitive positionMarket attractivenessGrowth opportunitiesFuture threatsCustomer perceptionPricing trends

Supply chain performanceManufacturing operationsService deliveryKPI reportingPurchasing

CashWorking CapitalControlsBalancesProcessesForecasting accuracyBlack holes

Exit considerationsValuation impactPotential buyers/targets

PricewaterhouseCoopersReviving those languishing investments 19

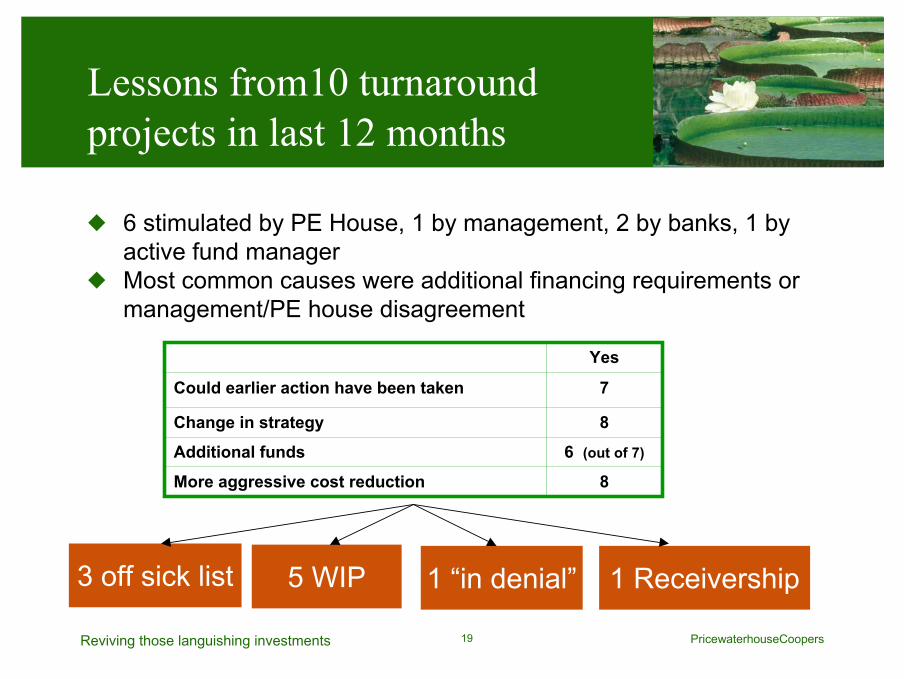

Lessons from10 turnaround projects in last 12 months

6 stimulated by PE House, 1 by management, 2 by banks, 1 by active fund managerMost common causes were additional financing requirements or management/PE house disagreement

8More aggressive cost reduction6 (out of 7)Additional funds

8Change in strategy

7Could earlier action have been taken

Yes

1 Receivership3 off sick list 5 WIP 1 “in denial”

PricewaterhouseCoopersReviving those languishing investments 20

Lessons from turnaround projects –keep or change the management?

Management – part of the solution or the problem?Management were changed in 2 cases, the jury is out on 3 or 44 had already recently changed management

PricewaterhouseCoopersReviving those languishing investments 21

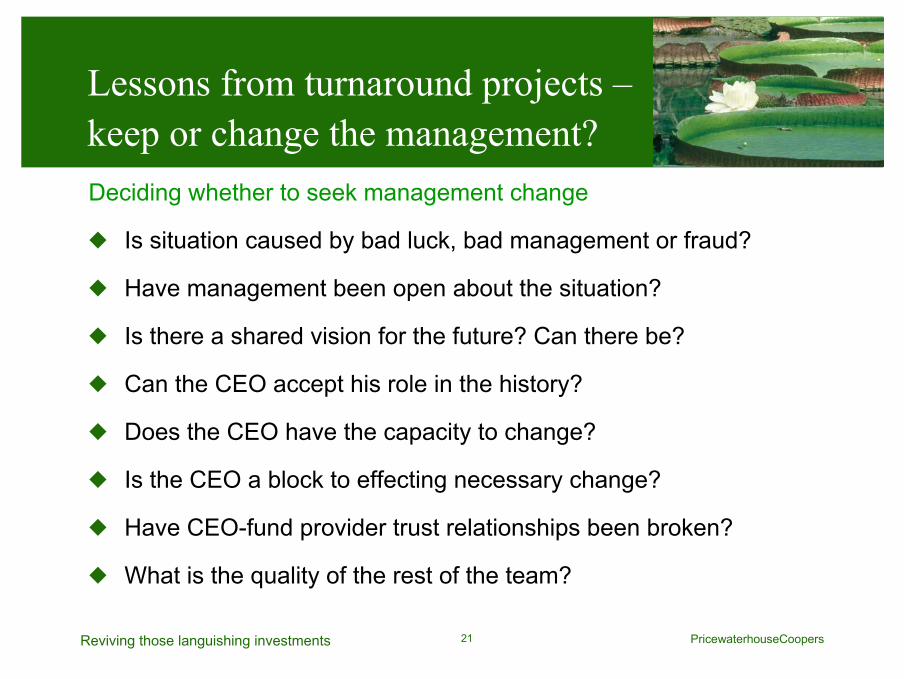

Lessons from turnaround projects –keep or change the management?Deciding whether to seek management change

Is situation caused by bad luck, bad management or fraud?

Have management been open about the situation?

Is there a shared vision for the future? Can there be?

Can the CEO accept his role in the history?

Does the CEO have the capacity to change?

Is the CEO a block to effecting necessary change?

Have CEO-fund provider trust relationships been broken?

What is the quality of the rest of the team?

PricewaterhouseCoopersReviving those languishing investments 22

Learning from the marketplace

Lessons from 10 recent turnarounds– Act on your business instinct– Management – to change or not to change?

Actively manage a deal from completion to exit– Stay close after completion– Introduce formal and informal processes

PricewaterhouseCoopersReviving those languishing investments 23

Stay close after completion, support and monitor closely

Early problem identification and rapid action can significantly reduce the potential downs

Root causes of failure often appear within 6 months Management often struggle under PE ownershipMarkets can and do change very fastCompetitors see deal activity as an opportunity Generally, more cash is needed than expectedClose Investment manager/management relationships can lead to delays in taking corrective action

PricewaterhouseCoopersReviving those languishing investments 24

Best practice process for improving individual company performance

Complete acquisitionTime

Take Control

Business Review

DisposalPreparation

30 days pre deal

1st 100 days

18 to 24 months 12 months pre exit

Post Deal Review

6 to 9 months

Investment Manager time and attention

PricewaterhouseCoopersReviving those languishing investments 25

Need to inject time effort and energy in your languishing investmentsReal value-add for the exitWatch out for the loss of controlWarning signs are there to see……act on themBut it is hard work – and needs close attentionPrevention is better than the cure

SummaryQuestions and answers

PricewaterhouseCoopersReviving those languishing investments 26

Discussion

Top Related