Languages

Pages

Legal

1

Background paper for the COMPETITIVE COMMERCIAL AGRICULTURE IN

AFRICA STUDY (CCAA)

NIGERIA CASE STUDY

Professor Aderibigbe S. Olomola

Director, Agriculture and Rural Development Department

Nigerian Institute of Social and Economic Research (NISER), Ibadan

Disclaimer:

This background report is being made available to communicate the results of Bank-funded work to the development community with the least possible delay. The manuscript therefore has not been prepared in accordance with the procedures appropriate to formally edited texts. Some sources cited in this report may be informal documents that are not readily available.

The findings and interpretations expressed in this report are those of the author(s) and do not necessarily reflect the views of the Board of Executive Directors of the World Bank or the governments they represent, or those of the Food and Agriculture Organization of the United Nations (FAO).

The World Bank and FAO do not guarantee the accuracy of the data included in this work. The designations employed and the presentation of the material in this work, including the boundaries, colors, denominations, and other information shown on any map do not imply any judgment on the part of the World Bank or FAO concerning the legal status of any territory or the endorsement or acceptance of such boundaries.

2

COMPETITIVE COMMERCIAL AGRICULTURE IN AFRICA:

NIGERIAN CASE STUDY

By

Professor Aderibigbe S. Olomola

Director, Agriculture and Rural Development Department

Nigerian Institute of Social and Economic Research (NISER), Ibadan

FINAL REPORT SUBMITTED TO THE CANADIAN INTERNATIONAL

DEVELOPMENT AGENCY (CIDA) AND THE WORLD BANK

OCTOBER, 2007

3

CURRENCY EQUIVALENTS, WEIGHTS AND MEASURES

Currency Equivalents (as of December 2005)

Currency Unit: Naira (�)

Official Rate: US$1 = �131.7

Naira 1 = US$0.0076

Autonomous Market Rate: US$1 = �142.6

Naira 1 = US$0.0070

Mass and Weight Measure

1000 grammes = 1 Kilogramme (kg) 1000 kilogrammes = 1 Tonne

Area Measure

100 Acres = 1 Hectare (ha)

4

TABLE OF CONTENTS

Table of Contents iii List of Tables v List of Figures viii Abbreviations and Acronyms x Executive Summary xii

CHAPTER

1. INTRODUCTION AND BACKGROUND 1 1.1 Objectives 1 1.2 Conceptual Framework 2 1.3 Methodology 4 1.4 Structure of the Report 7 2. REVIEW OF BROAD DEVELOPMENT EXPERIENCE IN NIGERIA 8

2.1 Macroeconomic Performance 8 2.2 Review of Agricultural Development in Nigeria 10 2.3 Constraints to Competitiveness of Commercial Agriculture in Nigeria 18 3. THE VALUE CHAIN ANALYSIS FOR SELECTED COMMODITIES 23

3.1 Value Chain Analysis of the Cassava Industry 26 3.2 Value Chain Analysis of the Cotton Industry 47 3.3 Value Chain Analysis of the Maize Industry 58 3.4 Value Chain Analysis of the Rice Industry 75 3.5 Value Chain Analysis of the Soybean Industry 94 3.6 Value Chain Analysis of the Sugarcane Industry 108 3.7 Comparative Analysis of Value Chain By Type of Crops 118 3.8 Sensitivity Analysis 127

5

4. SUMMARY, CONCLUSIONS AND POLICY RECOMMENDATIONS 131

4.1 Main Findings and Conclusions on Profitability and Export Competitiveness 131

4.2 Constraints 134 4.3 Opportunities for Improved Agricultural Commercialization and Competitiveness 134 4.4 Recommendations for Improved Agricultural Competitiveness in Nigeria 141

REFERENCES 148

6

LIST OF TABLES

TABLE PAGE

2.1 Selected Macroeconomic Indicators 9 2.2 Phases of Agricultural Development Policies in Nigeria: 1960-2006 11 2.3 Average Credit Disbursed By Trading Banks Under the ACGS, By Zone 14 2.4 Moratorium for Agricultural Loans 15 2.5 Index of Production of Selected Crops: 1961-2005 17 2.6 Share of Agriculture in Total Imports and Non-Oil Exports 17 2.7 Trend in US Agricultural Export Dumping Levels, 1990-2003 22 3.1 Farm Sectors and Locations for the Value Chain Analysis 23 3.2 Basic Features of the Agro-Ecological Regions of the Selected Commodities 24

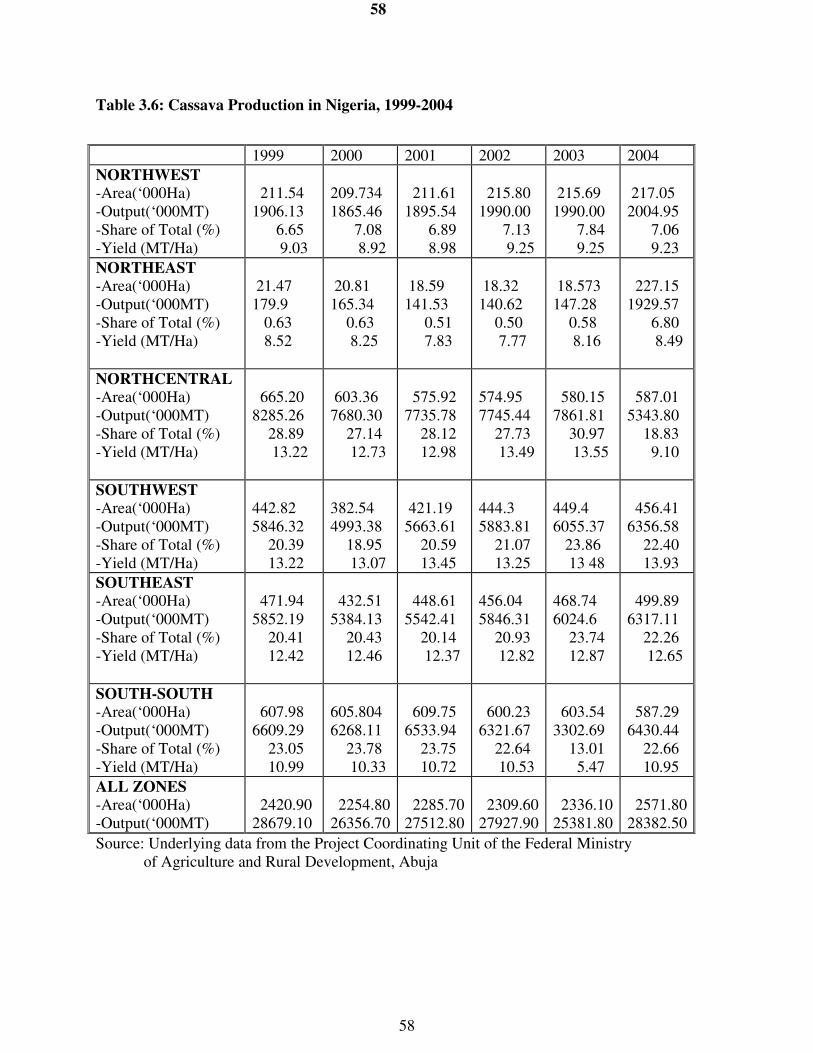

3.3 Gross Margin in Cassava Production in South-west Nigeria 26 3.4 Cassava Starch Value Chain Activity Results 28 3.5 World Cassava Production, 2002 30 3.6 Cassava Production in Nigeria, 1999-2004 33 3.7 Structure of Financial Costs in Cassava Enterprises 37 3.8 Profitability Indicators of Cassava Enterprises (Per MT) 38 3.9 Cassava Value Chain Indicators for 1MT of Final Traded Products 40 3.10 Cassava Profitability and Value Chain Indicators By Level of Commercialization 42 3.11 Comparison of Composition of Cassava Shipment Values in Nigeria (%) 43 3.12 Comparison of Selected Cassava Production Indicators in Nigeria 44 3.13 Build-up of Cassava Final SV in Nigeria By Stage (%) 46 3.14 Cotton Production in Nigeria, 1999-2004 51

7

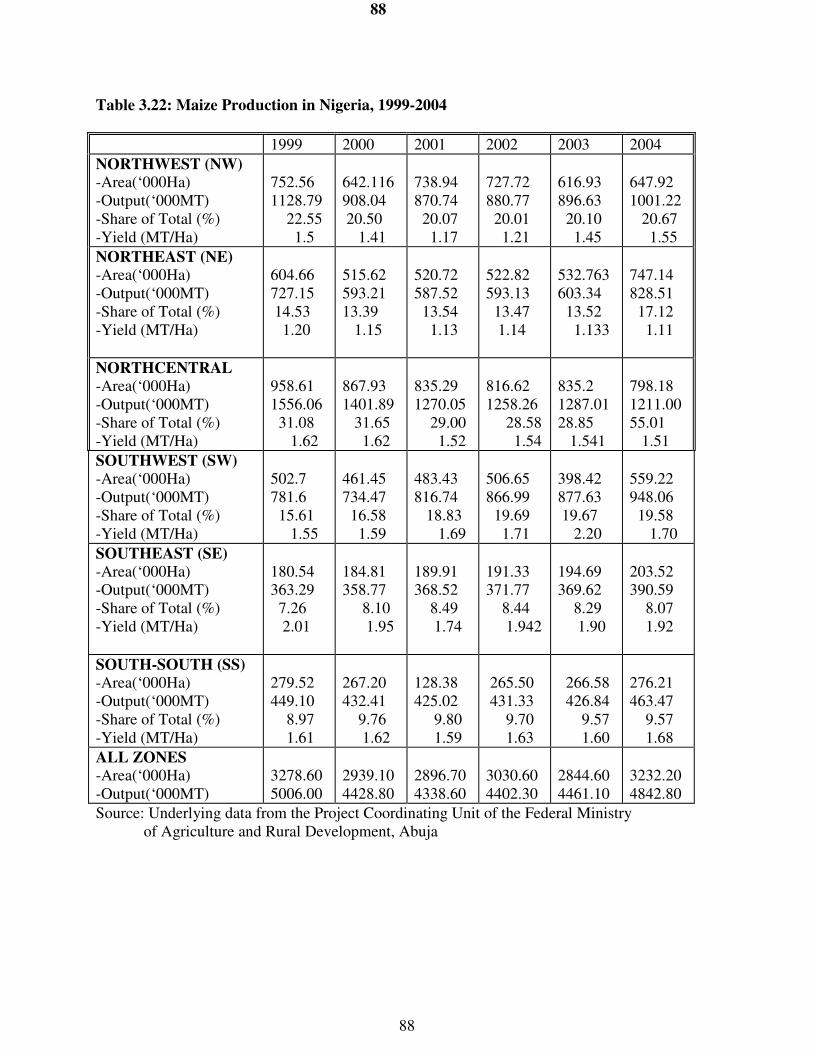

3.15 Structure of Financial Costs in Cotton Enterprises (FAM) 53 3.16 Profitability Indicators of Cotton Enterprises (Per MT) (FAM) 54 3.17 Cotton Value Chain Indicators in Nigeria (Per MT) 56 3.18 Composition of Cotton Shipment Values in Nigeria (%) 56 3.19 Build-up of Cotton Final SV By Stage (%) 56 3.20 Gross Margin in Maize Production in Nigerian Agro-Ecological Zones 59 3.21 Gross Margin Analysis per Ha of Selected Enterprises 59 3.22 Maize Production in Nigeria, 1999-2004 63 3.23 Structure of Financial Costs in Maize Enterprises in Nigeria 67

3.24 Financial and Profitability Indicators of Maize Enterprises in Nigeria 68 3.25 Value Chain Indicators for Maize Enterprises in Nigeria 70 3.26 Maize Profitability and Value Chain Indicators By Level of Commercialization 71 3.27 Comparison of Composition of Maize Shipment Values in Nigeria 72 3.28 Comparison of Selected Maize Production Indicators 74 3.29 Gross Margin in Rice Production in Nigeria 75

3.30 Comparison of Domestic and Import Price of Rice in Nigeria 76 3.31 Rice Production in Nigeria, 1999-2004 80 3.32 Structure of Financial Costs of Rice Enterprises in Nigeria 84 3.33 Profitability Indicators of Rice Enterprises in Nigeria (Per MT) 86 3.34 Value Chain Indicators for Rice Enterprises in Nigeria (Per MT) 88 3.35 Rice Profitability and Value Chain Indicators By Level of Commercialization 90 3.36 Comparison of Composition of Rice Shipment Values in Nigeria (%) 91 3.37 Comparison of Selected Rice Production Indicators in Nigeria 93 3.38 Build-up of Rice Final SV By Stage (%) 93

8

3.39 Soybean Production in Nigeria, 1999-2004 96 3.40 Structure of Financial Costs in Soybean Enterprises in Nigeria 99 3.41 Financial and Profitability Indicators of Soybean Enterprises in Nigeria (Per MT) 100

3.42 Soybean Value Chain Indicators in Nigeria (Per MT) 102 3.43 Soybean Profitability and Value Chain Indicators By Level of Commercialization 104 3.44 Comparison of Composition of Soybean Shipment Values in Nigeria (%) 105 3.45 Comparison of Selected Soybean Production Indicators in Nigeria 105 3.46 Build-up of Soybean Final SV By Stage (%) 107 3.47 Sugar Supply in Nigeria, 1990-2000 110 3.48 Sugar-Cane Production in Nigeria, By Zones, 1999-2004 112 3.49 Structure of Financial Costs in Sugar-cane Enterprises in Nigeria 114 3.50 Profitability Indicators of Sugar-cane Enterprises in Nigeria (Per MT) 115 3.51 Sugar-cane Value Chain Indicators in Nigeria (Per MT) 116 3.52 Composition of Sugar-cane Shipment Values in Nigeria (%) 117 3.53 Deviations of SVs From Parity Prices of Selected Commodities in Nigeria 126 3.54 Ranking of Selected Commodities in Order of Degree of Competitiveness 126 3.55 Changes in Profitability Indicators With 50% Increase in Yield and 50% Reduction in

Transport Cost 128

3.56 Changes in Shipment Value With 50% Increase in Yield and 50% Reduction in

Transport Cost 129

4.1 Summary of Main Findings By Crops 132 4.2 Value Chain Constraints of Agricultural Commodities in Nigeria 136

4.3 Achievements and Challenges of the Presidential Initiatives on Agriculture 139 4.4 Key Strategies for Improved Agricultural Competitiveness 142

9

LIST OF FIGURES

FIGURE PAGE

1.1 Stages in the Value Chain 3 2.1 Real Export Prices of Selected Agricultural Commodities, 1993-2003 20 3.1 Production of Cassava By Agro-Ecological Zones in Nigeria 34 3.2 Land Area Cultivated to Cassava in Nigerian Agro-Ecological Zones 34 3.3 Composition of Shipment Value for Cassava Enterprises in Nigeria 45 3.4 Cotton Production in Nigerian Agro-Ecological Zones 52 3.5 Land Area Cultivated to Cotton in Nigerian Agro-Ecological Zones 52 3.6 Trend in Maize Import in Nigeria, 2002-2005 62 3.7 Production of Maize By Agro-Ecological Zones in Nigeria 65 3.8 Land Area Cultivated to Maize in Nigerian Agro-Ecological Zones 65 3.9 Composition of Shipment Value for Maize Enterprises in Nigeria 73 3.10 Import of Paddy Rice in Nigeria, 2002-2005 78 3.11 Import of Paddy Rice in Nigeria, 2002-2005 78 3.12 Rice Production in Nigerian Agro-Ecological Zones 81 3.13 Land Area Cultivated to Rice in Nigerian Agro-Ecological Zones 81 3.14 Comparison of Composition of Shipment Values in Rice Enterprises 92 3.15 Trend in Soybean Import in Nigeria, 2002-2005 95 3.16 Soybean Production By Agro-Ecological Zones in Nigeria 97 3.17 Land Area Cultivated to Soybean in Nigerian Agro-Ecological Zones 97

3.18 Composition of Shipment Value for Soybean Enterprises in Nigeria 106 3.19 Sugar-cane Production in Nigeria, 1990-2000 109

10

3.20 Trend in Sugar Export in Nigeria, 2002-2004 111 3.21 Trend in Sugar Import in Nigeria, 2002-2005 111 3.22 Sugar-cane Production in Nigerian Agro-Ecological Zones 113 3.23 Land Area Cultivated to Sugar-cane in Nigerian Agro-Ecological Zones 113 3.24 Composition of Shipment Value for Sugar-cane 117 3.25 Yield of Selected Crops in Nigeria 119 3.26 Comparison of Unit Cost of Production By Crops in Nigeria 120 3.27 Gross Margins in Selected Farm Sectors in Nigeria, By Crops 121 3.28 Net Profit in Selected Farm Sectors in Nigeria, By Crops 122 3.29 Final Shipment Values for Traded Grain Commodities in Nigeria 124 3.30 Final Shipment Values for Selected Traded Products in Nigeria 125

11

ABBREVIATIONS AND ACRONYMS

ADP Agricultural Development Project ACGS Agricultural Credit Guarantee Scheme AfDB African Development Bank CBN Central Bank of Nigeria DVA Domestic Value Added EBA Everything But Arms ECA Economic Commission for Africa ECF Emerging Commercial Farms EU European Union FAM Family Farm FAO Food and Agriculture Organization GDP Gross Domestic Product IDRC International Development Research and Cooperation IFAD International Fund for Agricultural Development IFPRI International Food Policy Research Institute IITA International Institute for Tropical Agriculture ISO International Sugar Organization LCF Large Commercial Farms MBD Million Barrels Per Day NACB Nigerian Agricultural Cooperative Bank NACRDB Nigerian Agricultural Cooperative and Rural Development Bank NAERLS Nigerian Agricultural Extension Research and Liaison Service

12

NAIC National Agricultural Insurance Corporation NCEMA National Centre for Economic Management and Administration NISER Nigerian Institute of Social and Economic Research NSPRI Nigerian Stored \Products Research Institute RCMP Root Crop Monitoring Programme RTEP Root and Tuber Expansion Programme SAP Structural Adjustment Programme SME Small and Medium-Scale Enterprises SSCN Social Science Council of Nigeria SV Shipment Value UNCTAD United Nation Conference for Trade and Development USDA United State Department of Agriculture

13

EXECUTIVE SUMMARY

INTRODUCTION

Since the inception of democratic governance in 1999, Nigeria has witnessed determined efforts by the government to achieve rapid economic growth and development and to significantly reduce poverty. Real GDP growth rate made a significant jump from an average of 2.8 percent in 1997/1998 to 5.4 percent in 2000. Although it has been difficult to maintain a steady growth thereafter, the GDP growth rate has not fallen to the very low level often recorded before 2000. Indeed, in 2003 the target growth rate of 10 percent set by the government was met for the first and last time between 2000 and 2005. The 10.2 percent growth rate in 2003 was the highest in three decades, and was driven mainly by improvements in agriculture which grew by 7 percent and the oil sector which grew by 23 percent. Despite the improvement in growth performance, low level of savings and investment is still a major constraint. The highest investment ratio obtained so far is 16.2 percent while the savings ratio is 15.6 percent. The highest investment ratio attained since 2000 is far below the minimum investment to GDP ratio of about 30 percent which is required to unleash a poverty-reducing growth rate of at least 7-8 percent per year (see NEED, 2004). Increased private investment requires a stable macroeconomic environment characterized by a low rate of inflation, low rate of interest, stable real exchange rate and well-managed current account and fiscal balances. The inflation rate which came down to a single digit in 2000 (6.9 percent) rose to an all time high of 18.9 percent in 2001. It trended downwards thereafter to a single digit again in 2006 (8.2 percent) although the rate remains higher than the rate as at 2000. The lending rate which also peaked at 31.2 percent in 2001 declined to 18.7 percent in 2006 - a rate still regarded by investors as too high for operating profitably. Invariably, manufacturing capacity utilization which stood at 36.1% in 2000 grew somewhat; but followed a declining trend between 2003 and 2006.

Improvement in macroeconomic management has led to substantial reduction in fiscal deficits, less volatility in exchange rate and rising external reserves. Between 2000 and 2003 the problem of fiscal imbalances actually worsened. Fiscal deficit rose from 2.1 percent of GDP to 4.0 percent in 2001 and peaked at 5.5 percent in 2002. Part of the associated problem is the considerable reduction in the growth of credit to the private sector with adverse consequences on investment and output expansion. However, by 2003, the fiscal deficit was less than 3 percent of GDP and by 2004 it was only 1.7 percent. The external reserves increased from about US$9.91 billion in 2000 to about US$16.955 in 2004. These recent macroeconomic trends indicate that the country is right on the path to macroeconomic stability. The implementation of macroeconomic reforms as well as reforms in various sectors of the economy has been going on relentlessly since 2000, but while macroeconomic stability is being achieved, it appears that desirable outcomes in the areas of employment generation, poverty reduction, export expansion and diversification of the economy are yet to be achieved to a significant extent. The transformation of the agricultural sector and investments in infrastructure development will contribute in no small way to the realization of the development objectives in these areas.

The agricultural sector provides employment for about 60 percent of the labour force and raw materials for industrial development. Its provision of food for the growing population and income for millions of smallholders is remarkable for the maintenance of peace in the country. Nonetheless, the performance of the sector over the years is far below expectation because development efforts have failed to place it as the foundation for economic growth and development; thus it has not witnessed the desired transformation and the available resource

14

endowment has been grossly underutilized. Its role in terms of foreign exchange and revenue generation that used to be prominent in the 1960s has been relegated to the background while attention is shifted to the development and export of crude oil. Up to the mid-1960s, Nigeria commanded a share in world agricultural exports of more than one percent and had a leading position for several of its export crops. Nigeria supplied more than half of all traded palm kernel, more than a third of all groundnuts, and more than a fifth of all palm oil. As the country shifted towards petroleum exploitation and export agricultural exports declined and by the mid-1980s, Nigeria’s world market share for agricultural products had dwindled to less than 0.1 percent. Today none of the country’s export crops, with the exception of cocoa, commands any significant world market share. With the increasing need to eradicate poverty and put an end to hunger and malnutrition as enshrined in the MDG targets, Nigeria and indeed many African countries are returning to the agricultural sector for possible solution. In Nigeria, various development approaches have been adopted – the market has been relied upon, the government has been directly involved; yet there remains chronic under-investment in the sector and the efforts have not been able to fully unlock the available potentials.

The goal of the Competitive Commercial Agriculture in Africa (CCAA) study is to explore the feasibility of restoring competitiveness and growth in selected African countries by identifying key commodities or products, production systems, and marketing arrangements that have the potential to underpin a rapid development of competitive commercial agriculture. The competitiveness study in Nigeria will inform on the potential for growth of commercial agriculture in the country. The aim of the competitiveness study is to identify commodities or products that are currently competitive or stand good prospects of becoming competitive in domestic, regional, or global markets. The Nigerian case study focuses on six commodities: cassava, cotton, maize, soybeans, rice and sugar. The specific objectives of the study are threefold. a) To review the broader development situation for Nigeria in general and for agriculture in

particular touching issues such as growth, savings and investment, macro–economic and agricultural policy environment, etc.). Specifically the review involves studies on the investment climate affecting agricultural and agro–industrial development such as policies, state of infrastructure, transport costs, land availability, labor availability, credit availability, institutional environment, and other cross cutting factors.

b) To review existing studies on the competitiveness of the selected commodities in the targeted agro–climatic zone. This involves: (i) identifying and briefly describing the target zone, as well as the most important agricultural production trends within the zone, (ii) identifying and reviewing existing value chain studies that have been conducted in the country for the selected commodities. The scope and coverage of the study, the extent to which the study conforms to the methodological guidelines provided, and the overall quality of the study are examined. (iii) summarizing the qualitative and quantitative conclusions that have been drawn about the actual and potential competitiveness of the commodity for the three farm production systems that are being covered in the study, (iv) identifying weak links in the value chain that are the main obstacles to achieving competitiveness and (v) describing the sorts of improvements that existing studies suggest could be made in the value chain to significantly enhance competitiveness.

15

c) To analyze selected commodity chains from farm–gate to foreign destination ports using the value chain approach. Both qualitative and quantitative analyses of the value chains are carried out.

Data for the analysis came mainly from relevant literature and secondary sources including the Project Coordinating Unit of the Federal Ministry of Agriculture and Water Resources, the Central Bank of Nigeria and the Nigerian Bureau of Statistics. To augment the secondary data, smallholders, emerging commercial farmers and large commercial farmers were visited in different production zones in Oyo, Kwara, Niger and Adamawa states to collect relevant data. The author visited the Zimbabwe farmers in Shonga, Kwara state and obtained useful information through the use of questionnaire and interviews. With this personal contact, it was possible to seek further clarifications through telephone conversations even after the visit. Also input suppliers, processors and exporters were visited to obtain necessary information. A number of companies dealing in export of agricultural commodities were visited in Lagos where discussions were held with key representatives who also supplied useful information relating to domestic and international logistics. With the aid of Research Assistants, cassava, rice and sugar processing enterprises were visited in Oyo, Niger and Adamawa states respectively to obtain necessary data.

THE VALUE CHAIN ANALYSIS FOR SELECTED COMMODITIES

The analysis of the selected commodity chains from farm gate to foreign destination port using the value chain approach and follows the algorithm laid out in the Excel Templates specifically designed for this study. In addition to the quantitative aspects of the analysis, priority is also accorded to the qualitative aspects of the chain covering key areas such as world market structure, the Nigerian market structure and a description of the value chain for each commodity from the production stage up till final consumption. The targeted commodities - cassava, cotton, maize, rice, soybean and sugarcane are produced in specific agro-ecological regions which also reflect the zonal classification of all the 36 states in the country. Cassava, rice and maize are produced in virtually all the six regions while cotton is common in the northwest and northeast agro-ecological regions. Sugarcane is produced mainly in the northeast and north-central regions while soybean is produced in all the regions with the exception of south-south. Commercial production of the selected crops vary considerably across the agro-ecological zones. Whereas cassava, maize and rice are produced in commercial quantity in all the zones, cotton soybean and sugar-cane are restricted to specific zones. The NW (Northwest) zone is the leading producer of cotton, followed by the NE (Northeast) and NC (Northcentral) agro-ecological zones. The Northwest is also leading in the production of sugar-cane. Other zones producing sugar-cane are NE, NC and SW. Available data from 1999 to 2004 indicate that the NC is the leading producer of cassava, maize, rice and soybean. During this period, the production of these commodities maintained a positive but haphazard trend although there seems not to be any significant expansion in land area under cultivation. The value chain analysis seeks to examine the main links in the chain (production, assembly, processing, trade) with a view to determining the international competitiveness of the commodity. The analysis is conducted at three levels of operation – family farm (FAM), emerging commercial farm (ECF) and large commercial farm (LCF) and the results are presented accordingly.

16

Value Chain Indicators and Profitability of Cassava Enterprises

With regard to profitability of the cassava FAM, the results show that operating profit and net profit are positive only at the production and processing stages. At the production stage, the gross margin is US$149.89 while net profit is $149.08; whereas at the processing stage, the gross margin and net profit are US$85.18 and US$84.23 respectively. Moreover, the rate of return is higher at the production stage than at the processing stage. Operating profit of cassava ECF is positive at the production, assembly and processing stages. The gross margin per tonne is US$19.19, US$45.15 and US$85.18 respectively. Whereas net profit is positive at the assembly (US$45.15) and processing (US$84.58) stages, it is negative at the production stage indicating the difficulty to ensure viability of commercial production of cassava. The rate of return is about 22 percent at the production stage; but it is slightly higher at the assembly stage (25 percent) while it is highest at the processing stage (27 percent). Profitability indicators follow virtually the same pattern for cassava LCF as that of the cassava FAM. The results show that operating profit and net profit are positive only at the production and processing stages. At the production stage, the gross margin is US$127.80 while net profit is $107.73; whereas at the processing stage, the gross margin and net profit are US$83.44 and US$82.49 respectively. Moreover, the rate of return is higher at the production stage than at the processing stage.

The transformation of cassava from the FAM into various products results in considerable increase in value along the chain. From the farm production stage to the assembly stage SV increased by 579 percent while the increase from assembly to processing is 14 percent. From processing to the stage of final trading, the SV increased by 62 percent in respect of cassava chips, 74 percent in respect of cassava pellets and 66 percent in respect of starch. The transformation of cassava from farm production into cassava starch, cassava chips and cassava pellets at the final trading stage is associated with an increase in shipment value from US$40.33 at the cassava production stage to US$504.81 for cassava chips, US$542.68 for pellets and US$519.96 for starch. This represents an increase in shipment values of about 1152 percent, 1246 percent and 1189 percent in respect of cassava chips, pellets and starch respectively. Cassava production yields a value added (US$36.48) which represents 90% of the shipment value. Value added also represents a high proportion of the shipment value of the cassava products. The proportion varies from 82 percent in the case of cassava chips and starch to 84 percent for pellets. The DVA is made up largely (99 percent) of domestic costs and mark-ups.

The substantial increase in shipment value from the production stage to the stage of final traded product is not unexpected on account of the nature of the conversion of cassava tuber to the cassava products (chips, pellets, starch). A high quantity of raw cassava tuber (about three tones) of cassava tuber is required for the production of one tonne of each product. In view of the fact that the purchase of cassava tubers is included in the computation of shipment value and given the fact that the price of the commodity increases from one stage to another, it is not surprising that significant increase in shipment value is experienced between the production stage and the final traded commodity stage. The final SVs for cassava chips, pellets and starch are US$504.81, US$542.68 and US$519.96 respectively. Compared with the export parity price (US$-4.00) at the final commodity stage, none of these products is competitive at the international market. Apart from the high domestic costs, the very low level of international prices of these products makes them unprofitable and uncompetitive. As regards ECF, the transformation of cassava along the chain results in considerable increase in value. From the farm production stage to the processing stage SV increased by 26 percent. From processing to the stage of final trading, the SV increased by 62 percent in respect of cassava chips, 74 percent

17

in respect of cassava pellets and 66 percent in respect of starch. The transformation of cassava from farm production into cassava starch, cassava chips and cassava pellets at the final trading stage is associated with an increase in shipment value from US$248.63 at the cassava production stage to US$508.55, US$546.97 and US$520.75 at the stage of final trading of cassava chips, pellets and starch respectively. This represents an increase in shipment values of about 105%, 120% and 109% in the case of cassava chips, pellets and starch respectively. Cassava production yields a value added (US$229.76) which represents 92% of the shipment value. Value added also represents a high proportion of the shipment value of the cassava products. The proportion varies from 72 percent in the case of cassava chips, to 73 percent for starch and 75 percent for pellets. About 90 percent of the DVA in the case of cassava chips is made up of domestic costs and mark-ups while the proportion for pellets is 91 percent. For cassava starch, domestic costs and mark-ups account for 90 percent of the DVA. The final SVs for cassava chips, pellets and starch are US$508.55, US$546.97 and US$520.75 respectively. Compared with the export parity price (US$-3.00) at the final commodity stage, none of these products is competitive at the international market. Again apart from the high domestic costs, the very low level of international prices of these products makes them unprofitable and uncompetitive.

Also, in the case of LCF, the transformation of cassava into various products results in considerable increase in value along the chain. From the farm production stage to the assembly stage SV increased by 553 percent while the increase from assembly to processing is 10 percent. From processing to the stage of final trading, the SV increased by 61 percent in respect of cassava chips, 73 percent in respect of cassava pellets and 66 percent in respect of starch. The transformation of cassava from farm production into cassava starch, cassava chips and cassava pellets at the final trading stage is associated with an increase in shipment value from US$43.79 at the cassava production stage to US$506.63 for cassava chips, US$544.39 for pellets and US$522.61 for starch. This represents an increase in shipment values of about 1053 percent, 1139 percent and 1087 percent in respect of cassava chips, pellets and starch respectively. Cassava production of LCF yields a value added (US$41.85) which represents 96% of the shipment value. Domestic Value Added (DVA) also represents a high proportion of the shipment value of the cassava products. The proportion varies from 83% in the case of cassava chips, to 85% for starch and 84% for pellets. In each case over 80% of the DVA is made up of domestic costs and mark-ups. The final SVs for cassava chips, pellets and starch are US$506.63, US$544.39 and US$522.61 respectively. Compared with the export parity price (US$-3.00) at the final commodity stage, none of these products is competitive at the international market. In addition to high domestic costs, the very low level of international prices of these products makes them unprofitable and uncompetitive.

The results show that the costs incurred by FAM in addition to the domestic costs of production constitute a higher proportion of the SV than it is the case for ECF and LCF. The results show that increasing commercialization of cassava production has not led to an improvement in the degree of competitiveness of the commodity in the international market. A comparison of the final shipment values for the cassava products among the three categories of enterprises shows that domestic costs and mark-ups seem to be highest in the case of FAM while they appear to be lowest in the case of ECF. On the other hand, foreign costs seem to be the highest in the case of ECF followed by LCF and lowest in the case of FAM. The highest level of unofficial extras is also observed in the case of ECF. This finding implies that measures aimed at reducing cost at the farm product level in order to improve the competitiveness of the commodity will be different for the various categories of producers. As it turned out, the ECF is a high cost

18

producer with negative returns. The high production cost incurred by the ECF is due to the cost associated with the fixed assets which cost is by far the highest among the three categories of farmers. The net return is apt to improve if there is a reduction in the cost of capital and increased access to markets that offer more remunerative prices.

Impediments to Growth in the Cassava Industry

There are production processing and marketing constraints in the cassava industry. The cost of hiring labour and the tedium encountered in manual cultivation particularly during land preparation with local implements seem to discourage investment in cassava production. With regard to processing, equipment are generally not easily available, and when available, they are usually inefficient, their parts wear down easily, while the public power supply is very unreliable forcing the processors to depend on the expensive alternative of using power generators in the face of ever escalating cost of fuel for the generators. As regards marketing, unattractive prices of products remain a serious problem. A situation where the cost of transportation due to poor state of the access roads, cost of fuel etc are added to the cost of production make the prices offered for the cassava tubers and processed products like garri and flour unattractive.

Value Chain Indicators and Profitability of Cotton Enterprises

The results show that operating profit and net profit are positive at every stage of the cotton value chain. At the production stage, the gross margin is US$28.55 while net profit is US$17.56; whereas at the assembly stage, the gross margin and net profit are US$76.82 and US$69.57. Profitability is lowest at the processing stage judging by the level of gross margin (US$7.70) and net profit (US$5.29). The rate of return attained at the processing stage is about one percent compared to 26 percent at the assembly stage and 7 percent at the production stage. Profit is highest at the trading stage. Cotton lint trade attracts net profit of US$472.88 with 58 percent rate of return while net profit for cotton seed trade is US$278.45 with 91 percent rate of return.

The transformation of cotton into cotton lint and cotton seed results in considerable increase in value along the chain. The transformation of cotton into cotton lint, is associated with an increase in shipment value from US$219.73 at the cotton production stage to US$815.11 at the stage of trading in cotton lint representing an increase of about 271 percent. For cotton seed, the shipment value increases from US$219.73 to US$307.55 or by about 40 percent (Table 3.17). Cotton production yields a value added (US$219.72) which represents 89 percent of the shipment value. Value added also represents a high proportion of the shipment value of both cotton lint (88 percent) and cotton seed (81 percent) trade. In respect of cotton lint, 92 percent of the DVA is accounted for by domestic costs and mark-ups while in the case of cotton seed domestic costs and mark-ups account for 94 percent of the DVA. The final SV for cotton lint (US$815.11) is lower than the export parity price (US$1,196) implying that Nigerian cotton lint is competitive at the international market. With regard to cotton seed, the final SV (US$307.55) is also lower than the export parity price (US$494) implying that the commodity is competitive at the international market. The composition of shipment values shows considerable variation within each stage but not across the various stages in the value chain. In general, domestic costs and mark-ups constitute not less 80 percent of the SV in each of the stages. This is followed by the foreign costs, unofficial expenses and official duties and tax.

19

Impediments to Growth in the Cotton Industry

The major constraints to growth include (i) inadequate and untimely supply of inputs, (ii) seed contamination which often leads to loss of viability and low yields and (iii) absence of institutional arrangement for commodity grading and quality control.

Value Chain Indicators and Profitability of Maize Enterprises

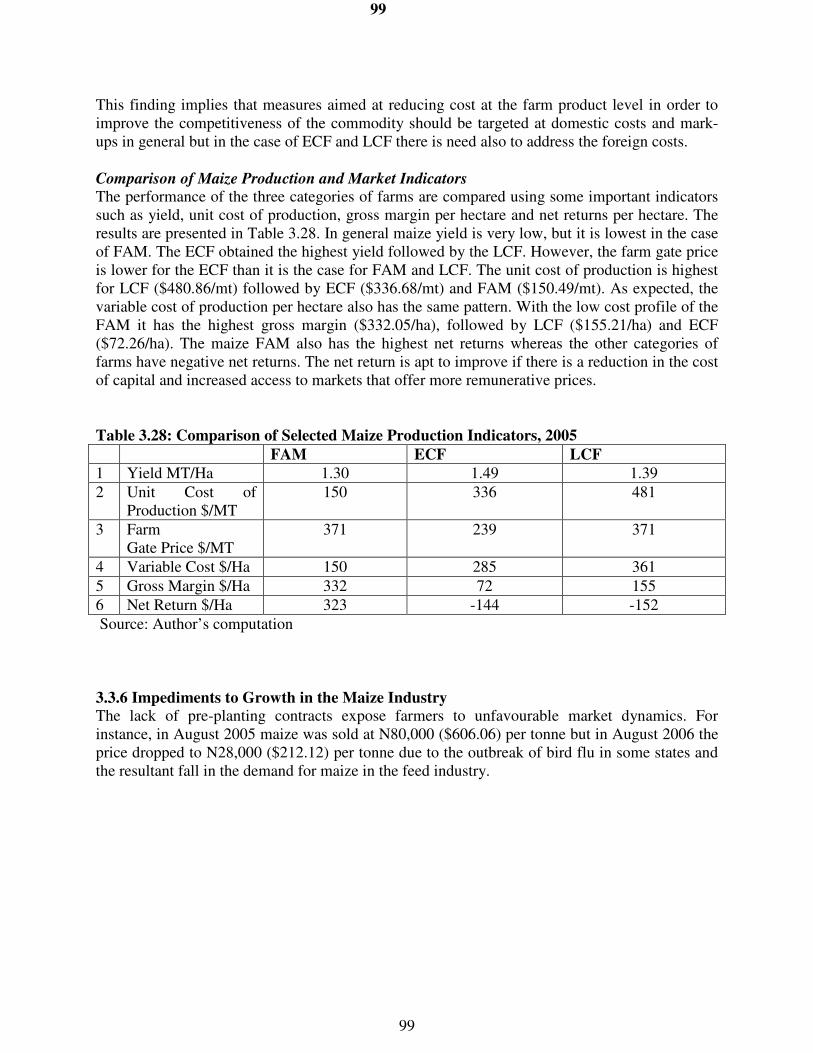

With regard to profitability indicators of the maize FAM, the results show that operating profit and net profit are positive at the production stage whereas the reverse is the case at the assembly stage. At the production stage, the gross margin is US$227.45 while net profit is $220.73. The rates of return at this stage range from 147 percent to 158 percent. The gross margin per tonne for maize ECF is US$48.5. The negative net profit portrays the difficulty in ensuring increased viability on the basis of the current level of investment and commercialization. At the assembly stage both the gross margin and net profit tend to be negative. In the case of the LCF, only operating profit is positive at the production stage. The gross margin per tonne is US$111.70. The negative net profit is an indication that the long term viability of large commercial maize farms may be difficult. At the assembly stage both operating and net profits tend to be negative.

The value chain indicators for the final traded commodity reveal that substantial increase in shipment value occurs between the production stage and final delivery of the commodity. For the maize FAM, the SV increased from US$150.48 to US$414.83 representing an increase of about 176 percent. Maize production is associated with a value added (US$142.26) which represents 95 percent of the shipment value. About 96 percent of the DVA is accounted for by domestic costs and mark-ups. The result shows that the final SV (US$414.83) is higher than the import parity price (US$131.10) implying that Nigerian maize is not competitive in the international market. In the case of the ECF the SV increased from US$336.68 to US$418.03 representing an increase of about 24 percent. ECF maize production yields a value added (US$274.03) which represents 81 percent of the shipment value. About 88 percent of the DVA is accounted for by domestic costs and mark-ups. The result shows that the final SV (US$418.03) is higher than the import parity price (US$131.10) implying that Nigerian maize is not competitive in the international market. As regards LCF maize production is associated with a value added (US$434.94) which represents 90 percent of the shipment value. The DVA is made up entirely of domestic costs and mark-ups. The result shows that the final SV (US$422.73) is higher than the import parity price (US$131.10) implying that Nigerian maize is not competitive in the international market.

The analysis shows that irrespective of the level of commercialization of maize production in Nigeria, the commodity remains uncompetitive in the international market. This finding implies that measures aimed at reducing cost at the farm product level in order to improve the competitiveness of the commodity should be targeted at domestic costs and mark-ups in general but in the case of ECF and LCF there is need also to address the foreign costs. With the low cost profile of the FAM it has the highest gross margin ($332.05/ha), followed by LCF ($155.21/ha) and ECF ($72.26/ha). The maize FAM also has the highest net returns whereas the other categories of farms have negative net returns. The net return is apt to improve if there is a reduction in the cost of capital and increased access to markets that offer more remunerative prices.

20

Impediments to Growth in the Maize Industry

The major constraints to growth in the maize industry include the following. � Inadequate and untimely supply of modern inputs

� Lack of credit facilities for processing enterprises � Unattractive prices of products � High transportation cost arising from high and rising fuel prices � The lack of pre-planting contracts expose farmers to unfavourable market dynamics. For

instance, in August 2005 maize was sold at N80,000 ($606.06) per tonne but in August 2006 the price dropped to N28,000 ($212.12) per tonne due to the outbreak of bird flu in some states and the resultant fall in the demand for maize in the feed industry.

� Poor storage facilities Value Chain Indicators and Profitability of Rice Enterprises

At the FAM level, the results show that except for raw material processing, operating profit and net profit are positive at every stage of the rice value chain. At the production stage, the gross margin is US$339.49 while net profit is US$333.91; whereas at the assembly stage, the gross margin (US$83.33) and net profit remains the same. At the level of trading, both the gross margin and net profit are positive but remain at the same level (US$83.23) since the traders made no significant investment on rice marketing. The rate of return (net profit/total costs) at the marketing stage (12 percent) is the smallest when compared to the 18 percent at the assembly stage and 277 percent at the production stage.

With regard to profitability indicators, the result shows that both operating profit and net profit are also positive at every stage of the value chain with the exception of raw material processing. At the production stage, the gross margin per tonne is US$402.69 while net profit is US$398.75; whereas at the assembly stage, the gross margin (US$79.70) and net profit remain the same. At the level of trading, both the gross margin and net profit are positive but remain at the same level (US$79.83) since the traders made no significant investment on rice marketing. The rate of return (net profit/total costs) at the marketing stage (12 percent) is the lowest when compared to the 17 percent at the assembly stage and 272 percent at the production stage. The pattern of profitability for the LCF category is similar to that of ECF and FAM. At the production stage, the gross margin per tonne is US$373.79 while net profit is US$164.83; whereas at the assembly stage, the gross margin (US$76.52) and net profit remain the same. At the level of trading, gross margin is US$79.45 while net profit remains at the same level. The rate of return (net profit/total costs) at the marketing stage (12 percent) is the lowest when compared to the 16 percent at the assembly stage and 43 percent at the production stage.

The value chain indicators for the final traded commodity reveal that substantial increase in shipment value occurs between the production of paddy and final delivery of milled rice (Table 3.34). With regard to the FAM, the transformation of paddy rice into milled rice is associated with an increase in shipment value from US$120.64 at the paddy production stage to US$462.12 at the assembly stage (or about 283 percent), US$562.27 at the processing stage (or about 22 percent from the previous stage) and US$674.34 at the final delivery point representing an increase of about 20 percent from the previous stage. Rice production is associated with a value added of US$109.54 which represents 91 percent of the shipment value. About 94 percent of the DVA is accounted for by domestic costs and mark-ups. At the final stage of delivery, the value added obtained (US$653.17) represents 97 percent of the shipment value (US$674.34); and 98 percent of the DVA is made up of domestic costs and mark-ups. The final SV (US$674.34) is

21

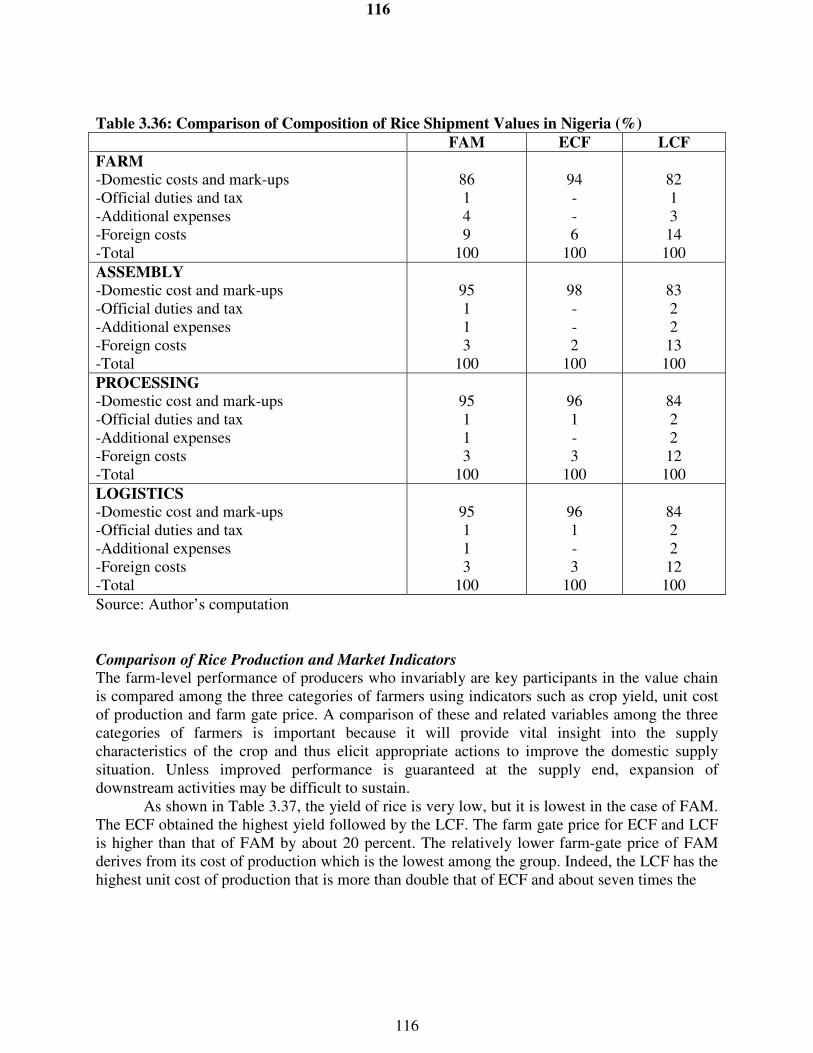

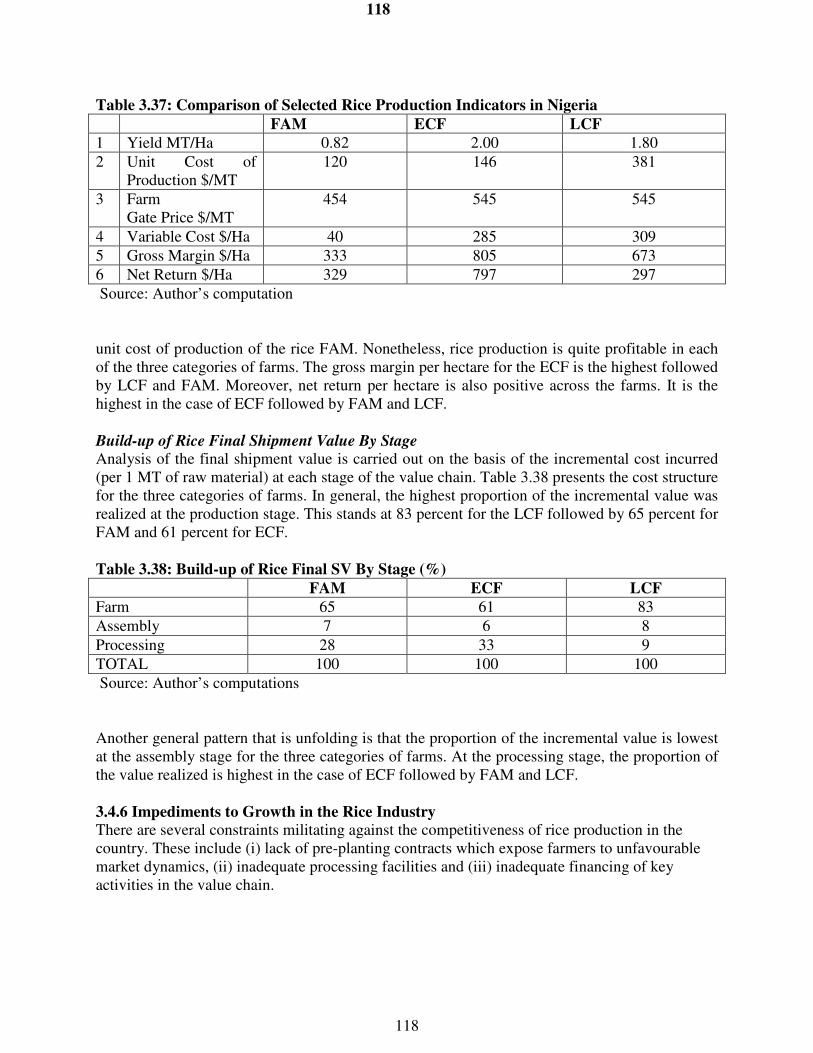

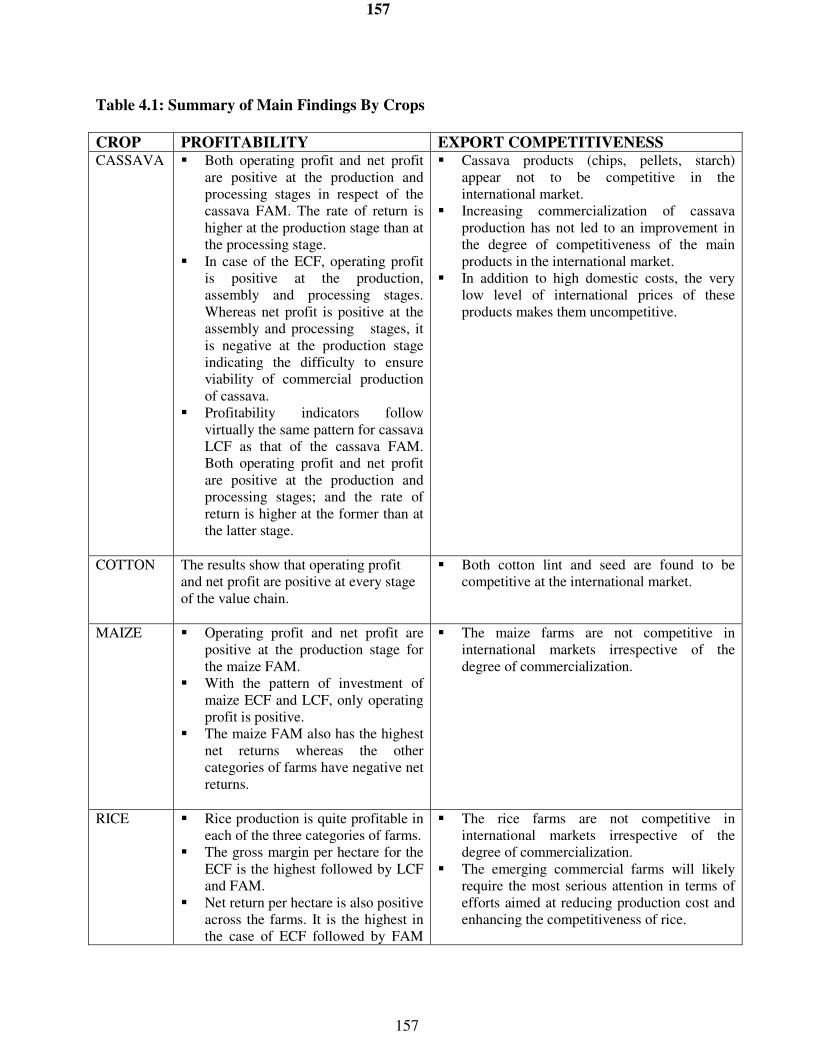

greater than the import parity price (US$330) implying that Nigerian rice is not competitive at the international market. With regard to the ECF, the transformation of paddy rice into milled rice is associated with an increase in shipment value from US$146.70 at the paddy production stage to US$465.76 at the assembly stage (or about 217 percent), US$564.03 at the processing stage (or an increase of 21 percent from the previous stage) and US$677.76 at the final delivery point representing an increase of about 20 percent from the previous stage. Rice production yields a value added (US$137.98) which represents 94 percent of the shipment value and it is entirely accounted for by domestic costs and mark-ups. At the final stage of delivery, the domestic value added obtained (US$659.80) represents 97 percent of the shipment value (US$677.76); and of this DVA, costs and mark-ups account for 99 percent. The final SV (US$677.76) is greater than the import parity price (US$330) implying that Nigerian rice is not competitive at the international market. As regards LCF, the transformation of paddy rice into milled rice is associated with an increase in shipment value from US$380.63 at the paddy production stage to US$468.95 at the assembly stage (or about 23 percent), US$565.24 at the processing stage (or about 21 percent from the previous stage) and US$678.14 at the final delivery point representing an increase of about 20 percent from the previous stage. Rice production yields a domestic value added (US$326.52) which represents 86 percent of the shipment value. Of this DVA, 82 percent is accounted for by domestic costs and mark-ups. At the final stage of delivery, the domestic value added obtained (US$596.08) represents 88 percent of the shipment value (US$678.14); and of this DVA, costs and mark-ups account for 96 percent. The final SV (US$678.14) is greater than the import parity price (US$330) implying that Nigerian rice is not competitive at the international market. At the FAM level, costs incurred in addition to domestic costs of production constitute a higher proportion of SV than it is the case for ECF and LCF. As it turned out, however, Nigerian rice remains uncompetitive in the international market irrespective of the level of commercialization of its production. Nonetheless, rice production is quite profitable in each of the three categories of farms. The gross margin per hectare for the ECF is the highest followed by LCF and FAM. Moreover, net return per hectare is also positive across the farms. It is the highest in the case of ECF followed by FAM and LCF. Overall, it appears that the emerging commercial farms will likely require the most serious attention in terms of efforts aimed at reducing production cost and enhancing the competitiveness of rice. The results also imply that the intensity of efforts will not only vary across the farms but also in terms of the specific components of shipment value.

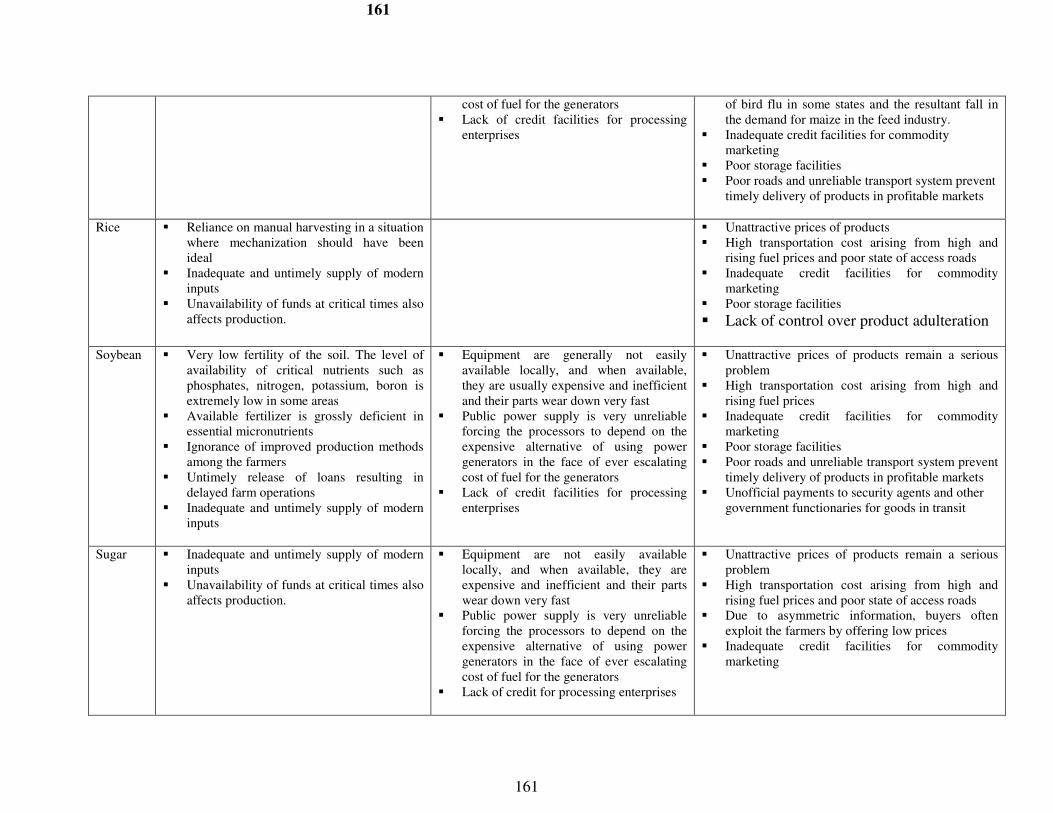

Impediments to Growth in the Rice Industry

There are several constraints militating against the competitiveness of rice production in the country. These include (i) lack of pre-planting contracts which expose farmers to unfavourable market dynamics, (ii) inadequate processing facilities and (iii) inadequate financing of key activities in the value chain. Value Chain Indicators and Profitability of Soybean Enterprises

As regards the FAM, the results show that operating profit and net profit are positive at both the production and assembly stages as well as the final delivery stage. At the production stage, the gross margin is US$159.95 while net profit is US$156.54. The rates of return at this stage range from 76 percent on the basis of net profit to 79 percent based on operating profit. In view of the negligible investment cost at the assembly stage the operating profit (US$9.09) is the same as the

22

net profit and the rate of return is only two percent. At the stage of final delivery, both the gross margin and the net profit have the same value (US$107.89) and the rate of return is about 26 percent. As regards the ECF, both operating profit and net profit are also positive at all stages of the chain. At the production stage, the gross margin per tonne is US$183.46 while at the assembly stage it is US$9.09. At the final delivery stage the operating profit is US$103.79. The rates of return (net profit/total cost) range from 2 percent at the assembly stage to 26 percent at the final delivery stage and 81 percent at the farm production stage. In the case of LCF, both operating profit and net profit are positive at all relevant stages of the chain with the exception of the farm production stage. At the assembly stage, the gross margin per tonne is US$9.09 while at the final delivery stage the operating profit (gross margin) per tonne is US$86.43. The rates of return (net profit/total cost) range from 2 percent at the assembly stage to 22 percent at the final delivery stage.

The value chain indicators for the final traded commodity reveal that substantial increase in shipment value occurs between the production stage and final delivery of the commodity. The SV for the FAM sector increased from US$207.10 to US$422.42 representing an increase of about 104 percent. Soybean production yields a value added (US$154.06) which represents 74 percent of the shipment value. About 95 percent of the DVA is accounted for by domestic costs and mark-ups. The result shows that the final SV (US$422.41) is higher than the import parity price (US$259.56) implying that Nigerian soybean is not competitive in the international market. In the case of ECF, the value chain indicators for the final traded commodity also reveal that substantial increase in shipment value occurs between the production of soybean and final delivery of the commodity. The SV increased from US$232.3 to US$426.52 representing an increase of about 84 percent. Soybean production yields a value added (US$255.71) which represents 110 percent of the shipment value which is accounted for entirely by domestic costs and mark-ups. The result shows that the final SV (US$426.52) is higher than the import parity price (US$259.56) implying that Nigerian soybean is not competitive in the international market. With regard to the LCF sector, the value chain indicators for the final traded commodity reveal that substantial change in shipment value occurs between the production of soybean and final delivery of the commodity. The SV decreased from US$3,146.46 to US$435.23 or by about 86 percent. Soybean production yields a value added (US$587.93) which represents 19 percent of the shipment value out of which 17 percent is accounted for by domestic costs and mark-ups. Foreign costs represents 81 percent of the shipment value at the soybean production stage indicating the high degree of foreign dependence by large commercial farms in terms of imported inputs. The result shows that the final SV (US$435.23) is higher than the import parity price (US$259.56) implying that Nigerian soybean is not competitive in the international market. At the LCF level, costs incurred in addition to domestic costs of production constitute a higher proportion of SV than it is the case for FAM and ECF. As it turned out, however, soybean production in Nigeria remains uncompetitive in the international market irrespective of the level of commercialization. The results point to the fact that domestic costs and mark-ups contribute more to the rising shipment values in the soybean chain than foreign costs as far as the FAM and ECF sectors are concerned whereas in the case of LCF the foreign costs contribute more than domestic costs. Improving the profitability and competitiveness of soybean will therefore, require different policy measures across the farm sectors. Whereas the LCF will benefit more from trade and other related policies, the soybean FAM and ECF may derive greater benefits from sector-specific and other domestic interventions.

23

Impediments to Growth in the Soybean Industry

The major constraints to higher soybean production and utilization in the country are (i) ignorance of improved production methods among the farmers, (ii) inadequate supply of modern inputs, (iii) low output price, (iv) inaccessibility of credit facilities to majority of the farmers and (v) poor storage facilities. Value Chain Indicators and Profitability of Sugar-cane Enterprises

The results show that with the exception of processing, operating profit and net profit are positive at every stage of the value chain. At the production stage, the gross margin per tonne is US$7.25 while net profit is US$4.86; whereas at the assembly stage, the gross margin per tonne (US$6.06) is the same as net profit in view of the negligible investment cost at this stage. As expected, the rate of return (16 percent) at the assembly stage is much lower than at the production stage which is 92 percent on the basis of gross margin and 47 percent based on net profit. Trading in white sugar attracts net profit per tonne of US$105.49 with 13 percent rate of return while net profit for brown sugar trade is US$29.73 with three percent rate of return.

The transformation of sugar-cane into sugar (white and brown sugar) results in considerable increase in value along the chain. The transformation of sugar-cane into white sugar is associated with an increase in shipment value from US$13.14 at the sugar-cane production stage to US$803.60 at the stage of trading in white sugar. For brown sugar, the shipment value increases from US$13.14 to US$955.11. Sugar-cane production yields a value added (US$10.25) which represents 78 percent of the shipment value. About 87 percent of the DVA is made up of domestic costs and mark-ups. At the level of trading, value added also represents a high proportion (98 percent) of the shipment value of both white and brown sugar. About 99 percent of the DVA is accounted for by domestic costs and mark-ups. In general the major components of shipment value are domestic costs and mark-ups, official duties and tax, additional (unofficial) expenses and foreign costs. In the case of sugar-cane, at each stage of the value chain the shipment value consists largely of domestic costs and mark-ups whose share ranges from 67 percent at the production stage to 89 percent at the assembly stage and 99 percent at the processing stage. Although foreign costs seem to be negligible at the processing stage, they represent a sizable proportion at the production stage (22 percent) and assembly stage (7 percent). The final SVs for white sugar (US$803.60) and brown sugar (US$955.11) are both higher than the import parity price (US$409.7) implying that Nigerian sugar is unlikely to be competitive at the international market.

Impediments to Growth in the Sugar-cane Industry

Several problems militate against the performance and growth in the sugar industry. In general the problems cut across the production, processing and marketing stages of the value chain. The main constraints include (i) reliance on estate-based industrial cane production system which is bedeviled with myriads of operational deficiencies and has thus hindered regular supply of raw materials to the sugar factories over the years, (ii) low output price, (iii) restricted market for sugar-cane which has tended to discourage increased production by small-scale farmers, (iv) low yield, (v) reliance on imported cultivars for the estate-based production systems, (vi) low level of capacity utilization in existing sugar mills and (vii) inadequate and irregular supply of sugar-cane to the mills.

24

CONCLUSIONS AND POLICY RECOMMENDATIONS

The analysis of competitiveness of the selected commodities shows that with the exception of cotton, none of the other commodities (cassava, maize, rice, soybean and sugar-cane) is competitive at the international market. Moreover, it is found that the commodities remain uncompetitive irrespective of the level of commercialization at the production level. In other words, the commodities are not competitive in the international market notwithstanding whether or not the producer operates as a small family farm (FAM), emerging commercial farm (ECF) or large commercial farm (LCF). However, in the different farm sectors (FAM, ECF and LCF) the production of the crops appears to be profitable although as expected, the degree of profitability varies by crops and from one sector to another. The results of the analysis show that across the sectors, rice is the most profitable crop. It is followed by soybean, maize, cassava and cotton. For maize, rice, and soybean the unit cost of production increases with rising degree of commercial orientation.

These findings imply that measures aimed at reducing cost at the farm product level in order to improve the competitiveness of the commodity should be targeted at domestic costs and mark-ups in general but in the case of ECF and LCF there is need also to address the foreign costs especially for soybean and maize production which involves the importation of different types of machines and chemical inputs. The results also imply that the intensity of efforts will not only vary across the farms but also in terms of the specific components of shipment value. For instance, in the case of soybean, improving the profitability and competitiveness will require different policy measures across the farm sectors. Whereas the LCF will benefit more from trade and other related policies, the soybean FAM and ECF may derive greater benefits from sector-specific and other domestic interventions. In general, the net return is apt to improve if there is a reduction in the cost of capital and increased access to markets that offer more remunerative prices for the farm products.

Recommendations for Improved Agricultural Competitiveness in Nigeria For improved agricultural competitiveness in Nigeria all the identified constraints in this study as earlier itemized should be the focus of attention with a view to providing enduring solutions within the shortest time possible. In addition, however, there are specific policies and strategies for increased profitability and competitiveness of the selected commodities which should also be considered pari pasu. These can be classified into three broad categories namely; (i) crop-specific interventions, (ii) sector-specific strategies and (iii) macro-related and other strategies. The crop-specific interventions vary from yield improvement and contract farming in the case of cassava, use of animal traction and production credit for cotton, irrigation and establishment of rice processing mills for rice, provision of storage facilities in the case of maize, use of farmers’ associations for input distribution in the case of soybean and development of non-estate-based production systems for sugar-cane. The other recommended strategies are as follows. Sector-specific interventions

-Adequate Funding of Research and Extension for Improved Productivity -Improved Agricultural Financing

-Promotion of Contract Farming to Enhance Market Access -Improved Agricultural Market Information

25

Macro-Related and Other Policies

-Monetary Policy (lowering cost of capital) -Fiscal Policy (favourable exchange rate and tax regimes) -Investment in Infrastructure -Fostering Value Added Enterprises Through Public-Private Parnership -Export Incentives Finally, it is important to stress that the findings of this study have not contradicted popular claims concerning competitiveness in Nigeria. In the case of cassava in particular, it has been argued that Nigeria is in a position of great disadvantage compared to other competitors. For instance, the market price of cassava from Thailand was about a third of the production cost in Nigeria; and that even though Nigeria has been producing about 70 percent of the world cassava, domestic demand and high cost of production have made Nigerian cassava uncompetitive in the world market. Besides, the latest report on trade competitiveness of a sample of 30 African countries placed Nigeria among the five least competitive countries together with Democratic Republic of Congo, Mali, Burkina Faso and Sierra Leone. Nigeria is in this group on account of its poor institutional quality and high inflation as well as low governance and infrastructure scores. Although, efforts to create a more favourable trade environment have been intensified over the years, there seems not to have been any significant reduction in production and marketing costs in the country in general and in the agricultural sector in particular. It is therefore, not surprising that many of the crops included in this study continue to be uncompetitive in the international market.

26

CHAPTER ONE

INTRODUCTION

The main objective of the Competitive Commercial Agriculture in Africa (CCAA) study is to explore the feasibility of restoring competitiveness and growth in selected African countries by identifying key commodities or products, production systems, and marketing arrangements that have the potential to underpin a rapid development of competitive commercial agriculture. Competitiveness will be analyzed using primarily value chain analysis. The CCAA study is concerned with (1) qualitative features of the supply chain, including the policy, institutional, and organizational factors that affect costs and shape relationships among the various actors, and (2) quantitative information about the supply chain, in particular financial costs and time requirements. Here the term “competitiveness” is used to mean competitiveness of a commodity in domestic markets, neighboring countries, and global markets. In a globalizing trading system, prices in all of these markets are ultimately linked to the global market, so broadly speaking the study is concerned with competitiveness in an open international market environment. The ultimate aim of the CCAA study is to promote the growth of commercial agriculture in ways that achieve broad–based poverty reduction.

The competitiveness study in Nigeria will inform on the potential for growth of commercial agriculture in the country. The aim of the competitiveness study is to identify commodities or products that are currently competitive or stand good prospects of becoming competitive in domestic, regional, or global markets. In order to ensure comparability across countries, the CCAA is focusing on tropical savannah zones featuring fairly reliable rainfall in which mixed cereals–root crops systems prevail, often associated with livestock. In West and Central Africa, these zones are commonly referred to as Guinea Savannah. The Nigerian case study focuses on six commodities: cassava, cotton, maize, soybeans, rice and sugar.

1.1 Objectives

The specific objectives of the study are threefold. d) To review the broader development situation for Nigeria in general and for agriculture in

particular touching issues such as growth, savings and investment, macro–economic and agricultural policy environment, etc.). Specifically the review involves studies on the investment climate affecting agricultural and agro–industrial development such as policies, state of infrastructure, transport costs, land availability, labor availability, credit availability, institutional environment, and other cross cutting factors.

e) To review existing studies on the competitiveness of the selected commodities in the targeted agro–climatic zone. This involves: (i) identifying and briefly describing the target zone, as well as the most important agricultural production trends within the zone, (ii) identifying and reviewing existing value chain studies that have been conducted in the country for the selected commodities. The scope and coverage of the study, the extent to which the study conforms to the methodological guidelines provided, and the overall quality of the study are examined. (iii) summarizing the qualitative and quantitative conclusions that have been drawn about the actual and potential competitiveness of the commodity for the three farm production systems that are being covered in the study, (iv) identifying weak links in the value chain that are the main obstacles to achieving competitiveness and (v) describing the

27

sorts of improvements that existing studies suggest could be made in the value chain to significantly enhance competitiveness.

f) To analyze selected commodity chains from farm–gate to foreign destination ports using the value chain approach. Both qualitative and quantitative analyses of the value chains are carried out.

1.2 CONCEPTUAL FRAMEWORK

Broadly defined, quantitative value chain analysis is focused on the amount of money a customer is willing to pay for a firm’s output. In an open economy, this price is determined competitively and flows upstream from the consumer to each producer and marketing company involved in the growing, collection, transformation, and delivery of that commodity to its terminal market. Supply chain analysis is a complementary concept applied to a network of companies across a given industry. Whereas value chain analysis looks at the upstream accumulation of value as a determinant of international competitiveness, supply chain analysis is a downstream concept that looks at the flow of goods from the supplier to consumer. Both concepts are concerned with the organization of value adding activities while competing in a particular industry, but the key analytical distinction comes in the flow of value between the supplier and consumer. Value chain and supply chain analysis are also concerned with product differentiation and timeliness of delivery. These factors are major determinants of a commodity’s final market price and total value that can be divided between participants in the production and marketing system. Seasonality is an especially important factor in agriculture since the prices of most farm commodities are cyclical depending on world production and patterns in consumer demand. Quality differences are likewise an important source of competitive advantage as is the ability of a country to supply guaranteed minimum quantities according to a specific time schedule. Interpretation of the quantitative value chain indicators, therefore, requires knowledge of conditions in other countries in order to pick the most relevant price with which to compare local production. Value chain analysis has gained considerable popularity in recent years. Although many approaches are taken, value chains essentially represent enterprises in which different producers and marketing companies work within their respective businesses to pursue one or more end-markets. Value chain participants sometimes cooperate to improve the overall competitiveness of the final product, but may also be completely unaware of the linkages between their operation and other upstream or downstream participants. Value chains therefore encompass all of the factors of production including land, labor, capital, technology, and inputs as well as all economic activities including input supply, production, transformation, handling, transport, marketing, and distribution necessary to create, sell, and deliver a product to a certain destination. The main stages of an agricultural value chain as defined for the quantitative methodology are illustrated in the figure below (see Keyser, 2006). In this diagram, dashed arrows flow from input supply to all other stages to show that this is a crosscutting function that affects all participants, not just at the farm level. A dashed arrow is also drawn from farm production to processing to show that some farmers may deliver their crop directly to a factory, thereby fulfilling the assembly function as well. This can either happen as part of a vertically integrated supply chain managed by a large company or because the scale or proximity of an individual’s production to the factory justifies direct delivery.

28

Figure 1.1: Stages of the Value Chain

Some of the main activities that occur at each stage of the value chain include the following.

� Input supply. This stage is concerned with the sourcing of raw materials required for agriculture production, processing, and trade. Inputs may either be procured locally or imported. The final value of an input at its place of use includes all manufacturing costs, transportation costs, customs duty and tax, and unofficial payments incurred up to that point. The efficiency of a country’s input supply system therefore has a major bearing on the performance of the entire value chain.

� Farm production. This stage is concerned with primary agriculture production and ends

with the sale of a raw commodity at the farm gate. These transactions may occur literally at the farm gate or at some other point where the farmer hands over ownership of the product to the next value chain participant. Depending on the crop, some type of primary processing (such as the shelling or bagging of dry grain) may take place at the farm level.

� Assembly. This stage involves the collection of agricultural produce from many farmers

and delivery of the raw material to a factory for industrial processing or packaging. In the case of livestock operations, assembly is defined in a broader sense to include the feedlot process for delivery of fattened animals to an abattoir. Bagging and simple grading of crops can also occur at this stage depending on arrangements made at the first point of sale.

� Processing. The processing stage involves the transformation of agriculture raw materials into one or more finished internationally traded goods. Raw commodities, of course, are also traded and this stage may not apply to every crop. The spreadsheet templates have been designed to accommodate the production of up to three goods from a single raw material.

� Domestic and international logistics. The logistics stage is concerned with the delivery of traded commodities to their final market destination. This may either be a foreign market in the case of exports, or a local market for import substitutes. For import substitutes, the logistics stage ends at the domestic level, but the analysis is still concerned with the cost of importing a similar product from the nearest or most competitive country.

Assembly Processing Farm

Production Logistics

Input Supply

29

1.3 Methodology

From these essential concepts, quantitative value chain analysis has become a multidimensional task that requires careful attention to a great many details and individual product differences. Towards this end, the quantitative methodology focuses on the measurement of accumulated production costs, private financial returns, and time requirements at each stage of the value chain. These measurements of cost components, private profitability, and time requirements are drawn from standard per hectare or per ton budgets for farm production, crop assembly, industrial processing, and logistics to the final delivery point which may be a domestic location in the case of import substitutes or foreign location in the case of export commodities. In value chain analysis, all inputs and outputs carry forward their inherited value from the previous stage. This point may seem obvious enough, but is important to stress in value chain analysis where the focus is on cost levels at different stages as a key determinant of international competitiveness. The competitiveness of Nigerian soybeans as an import substitute, for example, depends on the efficiency of the input supply system, farm production, assembly, processing, and logistics costs up to the final domestic market. The accumulated value at the delivery point must then be compared with the cost of bringing similar quality soybeans into the country from the best alternative source. By looking at the cost composition at each stage of the value chain and comparing these costs with world standards, value chain analysis not only shows if the country is internationally competitive, but also helps to identify key stages where costs can most effectively be reduced.

1.3.1 Value Chain Indicators

In addition to looking at the build-up of total costs at each stage, quantitative value chain analysis is also interested in the type of costs incurred as a product accumulates its value. This helps to identify areas where new policies or process innovations could have the greatest impact on international competitiveness. Because a country is only able to influence prices within its own borders, the analysis is particularly interested in the composition of domestic costs. These costs include legitimate local business expenses and mark-ups, official customs duties and taxes, and any number of unofficial payments that sometimes have to be made to facilitate a particular operation. A product’s total value at any given stage in the value chain, therefore, is equal to the sum of all domestic prices and imported cost components. For the CCAA study, these costs are measured in terms of Domestic Value Added (DVA) and Shipment Value (SV), which constitute the main value chain indicators as follows.

Domestic Value Added (DVA) = Domestic costs and mark-ups [1] + Official duties and tax + Unofficial charges and extra costs Shipment Value (SV) = Domestic Value Added

+ Foreign components [2] DVA and SV are measured according to equations [1] and [2] respectively on a per tonne basis at each stage of the value chain for the following products.

Farm production Farm gate product

Assembly Assembled raw material

30

Processing Processed raw material

International logistics Traded commodity

The final calculation of SV for each traded commodity is the most comprehensive measure of actual and potential competitiveness. For a given product or commodity produced in a specific country, international competitiveness is determined by comparing the SV at the final destination (sale point) with a benchmark. The benchmark will usually be the cost–insurance–freight (cif) reference price for the product or commodity at the specified destination.

The measurements of DVA and SV may also be compared, both in an absolute and relative sense, with international benchmarks established by successful competitors. This is one of the main features of the CCAA value chain analysis and this study compares the final shipment values with the most relevant import and export parity prices against which Nigeria must compete. In cases where production increases substitute for imports (such as rice, maize, soybean and sugar), import parity prices are used. Import parity prices are determined by first finding the price the country is most likely to pay in order to import the commodity and then by adding transportation costs to obtain the landed price in domestic cif terms. In cases where increased production is to be exported (such as cassava and cotton), export parity prices are used. And this is determined by subtracting international transport costs from the international prices to give the domestic fob equivalent.

1.3.2 Financial Costs and Profitability Indicators

Beyond the analysis of cost structures and price components, the quantitative analysis is extended to the private costs and returns that accrue to value chain participants. Since agricultural production and marketing begin with the decisions private investors make, it is important to have a sense of the underlying costs and profitability of competing enterprises and marketing systems. Thus, the main analytical templates are designed to calculate total variable costs, investment costs, gross profit, and net profit on per hectare and per ton basis. The net profit is particularly important because it serves as a useful indicator for assessing the viability of each enterprise. A farm enterprise is expected to continue operating as long as operating profit (gross revenue minus operating costs) is positive. Thus, as long as operating costs are covered, the enterprise will operate. However, unless all fixed costs are covered, the farm enterprise is not tenable in the long run; the tendency is for the operations to terminate when the economic life of the existing fixed assets expire.

Each Excel workbook in the analytical templates includes a similar table summarizing basic financial indicators for a particular stage in the value chain. These indicators are measured in different terms following the value chain conventions listed below. At the assembly, processing and logistics stages, the cost of commodity purchases is also recorded in the summary table in addition to basic variable cost and total investment cost data. For the purpose of calculating gross margin, commodity purchases are treated as a variable cost.

31

Farm Production Farm gate product Per Ha; per MT

Assembly Assembled raw material Per Ha; per MT

Processing Processed raw material Per MT; share from Product

Logistics Traded commodity Per MT processed raw material; per MT traded commodity

Other financial indicators such as the gross and net rates of return are also calculated from the templates. These measures show the rate of return to an investor’s outlay of cash and the ability of the enterprise to cover its long-run depreciation costs respectively and are especially useful in comparing different enterprises. Enterprises with a high ratio provide a better return than those with a low ratio.

• Gross rate of return = gross profit / total variable costs.

• Net rate of return = net profit / total production costs.

With regard to the farm production stage, the returns to hired labor and personal management are calculated automatically in the Template as follows.

• Return per day hired labour = Gross (or net) return / days total employment.

• Return per day total labour = Gross (or net) return / days total employment and family management.

1.3.3 Data

Data for the analysis came mainly from relevant literature and secondary sources including the Project Coordinating Unit of the Federal Ministry of Agriculture and Water Resources, the Central Bank of Nigeria and the Nigerian Bureau of Statistics. To augment the secondary data, small holders, emerging commercial farmers and large commercial farmers were visited in different production zones in Oyo, Kwara, Niger and Adamawa states to collect relevant data. The author visited the Zimbabwe farmers in Shonga, Kwara state and obtained useful information through the use of questionnaire and interviews. With this personal contact, it was possible to seek further clarifications through telephone conversations even after the visit. Also input suppliers, processors and exporters were visited to obtain necessary information. A number of companies dealing in export of agricultural commodities were visited in Lagos where discussions were held with key representatives who also supplied useful information relating to domestic and international logistics. With the aid of Research Assistants, cassava, rice and sugar processing enterprises were visited in Oyo, Niger and Adamawa states respectively to obtain necessary data.

Unlike the situation with the Zimbabwe farmers who were visited through the cooperation of the Permanent Secretary of the Kwara State Ministry of Agriculture and his officials, the cooperation of the Lagos-based expatriate officials of foreign companies dealing in rice, cotton and other crops was difficult to secure during the data collection exercise. In spite of visits, numerous telephone and Internet contacts and promises by them to supply necessary data,

32

they were so tactical in ensuring that at the end no data was supplied. Another remarkable problem during the exercise was the great difficulty encountered in searching out the locations of export companies whose addresses had been obtained from the Internet. Many of the Lagos addresses could not be traced and in some instances where the addresses exist, the “exporters” could not be traced. Some of them who were contacted through their telephone addresses promised to arrange a meeting for us to discuss but those promises were never fulfilled. However, a few of those genuinely involved in the export of agricultural commodities were identified and were helpful in providing the required information.

1.3.4 Limitations of the Study