Languages

Pages

Legal

Outlook for Woodchip Imports in China

Bob Flynn

Director, International Timber, RISI

JOPP Seminar, Tokyo, June11, 2013

As recently as 2003, China was the fourth largest supplier of

hardwood chips to Japan; but since 2006 China has been a

net woodchip importer, and is now the 2nd largest chip importer

-2,000

-1,000

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Tho

usa

nd

BD

MT

China: Imports and Exports of Hardwood Chips

Imports Exports

Agenda

• Why does China need to import woodchips?

– World’s biggest producer of paper and paperboard

– Growing domestic pulp production

– Shortage of domestic timber resources

• Historical trend in woodchip imports in China

– Hardwood

– Softwood

• Outlook for woodchip imports in China

China has become the world’s largest paper and paperboard

producer; 70% of furnish is recovered paper, but consumption

of wood pulp has also been increasing rapidly

0

10

20

30

40

50

60

70

80

Millio

n T

on

ne

s

China: Fiber Consumption for Paper and Paperboard Production

Non-Wood Pulp

Wood Pulp

Recovered Paper

What’s ahead for China’s paper industry?

• China’s 12th Five-year Plan provides “strong guidance”

for the paper industry:

– Primary focus on domestic market, rather than producing for

export.

– “Forest-Paper” integration includes acquiring forest resources

outside of China.

– Recovered paper collection and consumption is encouraged.

– Industry consolidation to increase.

– Effluent reduction, energy conservation and mill closures.

China’s growth in per capita income will mean

rising consumption of paper--- although

electronic media will have an impact

0

20

40

60

80

100

120

140

0 5,000 10,000 15,000 20,000 25,000 30,000 35,000

Kg

/Pe

rso

n

Per Capita GDP in US Dollars

Graphic Paper Consumption and Per Capita Real GDP

Japan

South Korea

China

Source: RISI,

China Pulp

Market: A

Comprehensive

Analysis and

Outlook, 2012

RISI projects that newsprint production and

demand in China will decrease over the next

decade

0

1,000

2,000

3,000

4,000

5,000

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

China's Newsprint Production and Demand Forecast, 2012-2022

Production Demand

Source: RISI,

China Pulp

Market: A

Comprehensive

Analysis and

Outlook, 2012

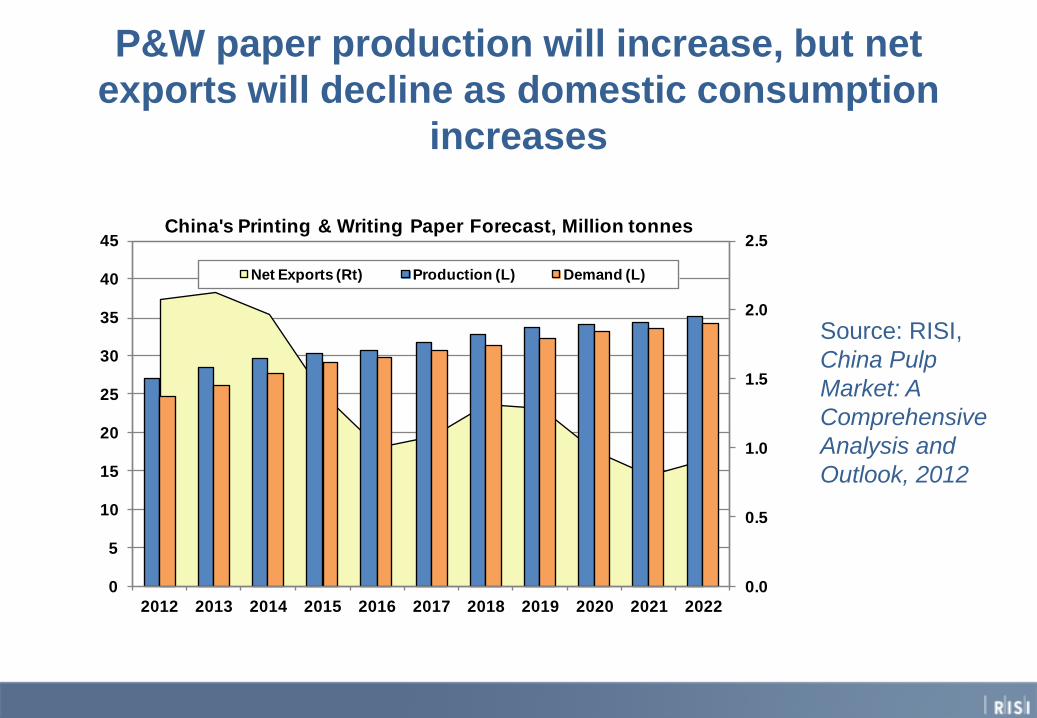

P&W paper production will increase, but net

exports will decline as domestic consumption

increases

0.0

0.5

1.0

1.5

2.0

2.5

0

5

10

15

20

25

30

35

40

45

2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

China's Printing & Writing Paper Forecast, Million tonnes

Net Exports (Rt) Production (L) Demand (L)

Source: RISI,

China Pulp

Market: A

Comprehensive

Analysis and

Outlook, 2012

Containerboard will be one of the fastest

growing segments of the industry, with

consumption keeping pace with production

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Tho

usa

nd

To

nn

es

Chinese Total Containerboard Consumption and Production

Consumption Production

Source: RISI, China

Pulp Market: A

Comprehensive

Analysis and

Outlook, 2012

Boxboard production seems set to expand

faster than domestic consumption, so net

exports will increase

0

5,000

10,000

15,000

20,000

25,000

2002 2004 2006 2008 2010 2012 2014 2016 2018 2020 2022

Tho

usa

nd

To

nn

es

Chinese Total Boxboard Consumption and Production

Consumption Production

Source: RISI,

China Pulp

Market: A

Comprehensive

Analysis and

Outlook, 2012

Tissue is a smaller segment, but rapidly

growing in China- which will become the

world’s leading consumer

100

2,100

4,100

6,100

8,100

10,100

12,100

14,100

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022

Th

ou

sa

nd

To

nn

es

China Becomes the Leading Consumer of Tissue

Western Europe North America China

Source: RISI, China

Pulp Market: A

Comprehensive

Analysis and

Outlook, 2012

China’s imports of wood pulp have been growing rapidly, but

domestic production has also been increasing, with output

growing 8% annually since 2004, to more than 9 million tonnes

0

4

8

12

16

China: Production and Imports of Wood Pulp

Imports Production

But imports of woodchips have been growing much faster

than pulp imports, increasing 49% annually since 2004

0

5

10

15

20

25

30

2004 2005 2006 2007 2008 2009 2010 2011 2012E

Ind

ex:

20

04

= 1

China: Index of Pulp Production and Woodchip Imports

Pulp Production

Woodchip Imports

China’s area of eucalyptus plantations doubled between

2006 and 2012 – but will it be enough to meet demand?

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

2006 2012 2015E

Millio

n H

ec

tare

s

China: Area of Eucalyptus Plantations

Other

Guangxi

Some eucalyptus plantations in China are relatively

high quality

Stora Enso has helped to

introduce high-quality

eucalyptus forestry to

China, using modern

technology from the first

step.

While most harvesting in

China is still done by hand,

Stora is developing some

plantations for mechanical

harvesting.

But other plantations are more difficult…

Plantations are often

located on steep slopes,

with poor road connections

to markets.

Agriculture still has priority

in China, with forest

plantations stuck with less

productive sites.

And some plantations are really bad…

Even some flat ground may not be

well suited for growing trees, due

to very infertile soils, lack of

rainfall, etc.

Many Chinese companies think

"cheaper is better", but with

eucalyptus this can be a problem.

Eucalyptus in China has a problem with frost, and may also

have future problems with pests and disease due to very

narrow genetic base

Frost damage to a young

plantation

Bacterial wilt damage to a

Eucalyptus plantation

Pulpwood is expensive in China, as even very small (8cm+)

eucalyptus logs like these are used for veneer, and can cost

US$100/cubic meter or more

The vast majority of China’s woodchip imports have

been hardwood, not softwood

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2008 2012 Jan-Apr 2012 Jan-Apr 2013

Tho

usa

nd

BD

MT

China Woodchip Imports

Hardwood

Softwood

In January-April

2013,

• Imports of

hardwood chips

are 17% higher

than in 2012.

• Imports of

softwood chips

are 122% higher

than in 2012.

Nearly 90% of China’s hardwood chips are from

Southeast Asia

0

2,000

4,000

6,000

8,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Tho

usa

nd

BD

MT

China: Imports of Hardwood Chips

Other Australia

Indonesia Thailand

Vietnam

Change in

imports by

source in

January-April

2013 vs. 2012: • Vietnam + 42%

• Thailand - 17%

• Indonesia + 8%

• Australia + 70%

• Other - 36%

In some months, China’s imports of

hardwood chips have already exceeded the

volume imported in Japan

0

200

400

600

800

1000

1200Ja

n-0

8

Ap

r-0

8

Jul-

08

Oct

-08

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Tho

usa

nd

BD

MT

Hardwood Chip Imports in Japan and China, 2008 - April 2013

China Japan

Australia has been the primary supplier of

softwood chips to China, although the USA

would also like to sell a lot more to China

-

50

100

150

200

250

300

350

2008 2009 2010 2011 2012

China's Softwood Chip Imports, 2008-2012Thousand BDMT

Australia Russia Brazil

Fiji N Zealand USA

Market shares in

January-April 2013: • Australia 72%

• Fiji 10%

• USA 9%

• Russia 8%

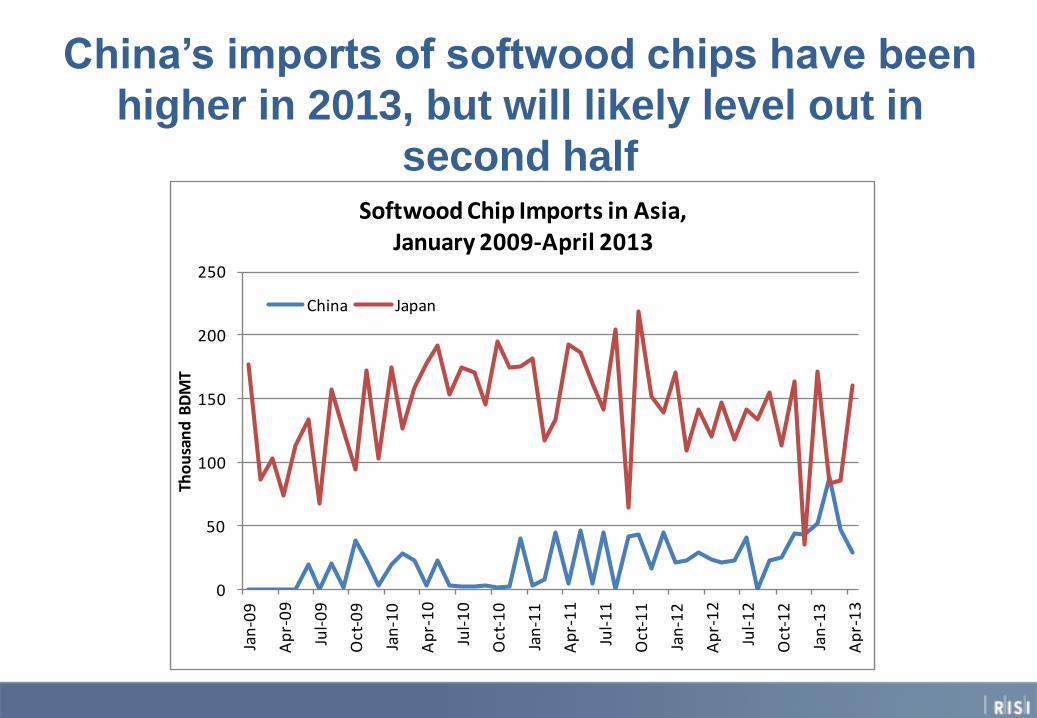

China’s imports of softwood chips have been

higher in 2013, but will likely level out in

second half

0

50

100

150

200

250

Jan

-09

Ap

r-0

9

Jul-

09

Oct

-09

Jan

-10

Ap

r-1

0

Jul-

10

Oct

-10

Jan

-11

Ap

r-1

1

Jul-

11

Oct

-11

Jan

-12

Ap

r-1

2

Jul-

12

Oct

-12

Jan

-13

Ap

r-1

3

Tho

usa

nd

BD

MT

Softwood Chip Imports in Asia, January 2009-April 2013

China Japan

75% of China’s hardwood chip imports in 2012 went to just

two mills: APRIL at Rizhao and APP on Hainan Island

But other hardwood chip importers

have been increasing volumes also

In January-March 2013, market share of “Others” = 30%, up from 25% in 2012

Softwood chip imports have gone to just a few mills,

with little change over time

China’s Hardwood Chip Import Price: Prices

higher in eastern China (Shandong province)

due mostly to higher freight

-

50

100

150

200

250

Ja

n-0

9

Ma

r-0

9

Ma

y-0

9

Ju

l-0

9

Se

p-0

9

No

v-0

9

Ja

n-1

0

Ma

r-1

0

Ma

y-1

0

Ju

l-1

0

Se

p-1

0

No

v-1

0

Ja

n-1

1

Ma

r-1

1

Ma

y-1

1

Ju

l-1

1

Se

p-1

1

No

v-1

1

Ja

n-1

2

Ma

r-1

2

Ma

y-1

2

Ju

l-1

2

Se

p-1

2

No

v-1

2

Ja

n-1

3

Ma

r-1

3

US

D /B

DM

T

Hardwood Chip Price Index, 2009-March 2013 (CIF)

East China

South China

Source: RISI

International

Pulpwood Trade

Review 2013

Hardwood Chip Price in Rizhao Australian suppliers tried hard to keep their price down, but still higher

than SE Asian suppliers

100

120

140

160

180

200

220

240

Ja

n-0

9

Ma

r-0

9

Ma

y-0

9

Ju

l-0

9

Se

p-0

9

No

v-0

9

Ja

n-1

0

Ma

r-1

0

Ma

y-1

0

Ju

l-1

0

Se

p-1

0

No

v-1

0

Ja

n-1

1

Ma

r-1

1

Ma

y-1

1

Ju

l-1

1

Se

p-1

1

No

v-1

1

Ja

n-1

2

Ma

r-1

2

Ma

y-1

2

Ju

l-1

2

Se

p-1

2

No

v-1

2

Ja

n-1

3

Ma

r-1

3

US

$ p

er

BD

MT

, C

IF

Hardwood Chip Price in Rizhao, 2009 - March 2013

Vietnam

Thailand

Indonesia

Australia

Source: RISI

International

Pulpwood Trade

Review 2013

Project List Paper Grade Pulp

Project Allocation Type

New

Capacity

Purposed Start

Date

APP Qinzhou, Guangxi MEC 350 Jan, 2013

Bohui Dafeng, Jiangsu MEC 400 Q2, 2013

MCC Yinhe Linqing, Shandong MEC 70 early 2013

Xinya Henan MEC 250 2013

Jindaxing Guangxi BHK 170 2013

Lee & Man Wuzhou, Guangxi DIS 103 2013

Oji Paper Nantong, Jiangsu BHK 700 2013

Longjiangfu Heilongjiang UKP 340 Q4, 2013

Dingfeng Zhaoqing, Guangdong BHK 80 2013

Stora Enso Beihai, Guangxi BEK 700 2015

AdvanceAgro Dafeng, Jiangsu BHK 840 2014

Nanping Paper Nanping, Fujian DIS 150 2014

Stora Enso Beihai, Guangxi MEC 200 2015

April Rizhao, Shandong MEC 250 2015

April Rizhao, Shandong MEC 250 2016

Tiger Yuanjiang Paper Yuanjiang, Hunan MEC 200 2014

Chenming Shouguang, Shandong BHK 400 ?

China is expected to maintain a balance between

domestic pulp production and imports

0

5

10

15

20

25

2011 2012 2013F 2014F 2015F 2016F 2017F

Mill

ion

To

nn

es

China: Forecast of Domestic Pulp Production and Pulp Imports

Imports

Production

Note: does not include dissolving pulp

Even our relatively conservative forecast indicates that

China’s market for hardwood chip imports will exceed

Japan’s by 2015

0

2

4

6

8

10

12

2009 2010 2011 2012 2013F 2014F 2015F

Hardwood Chips Import Forcast, China & JapanMillion BDMT

China

Japan

RISI’s 14th Annual Asian Pulp and

Paper Outlook Conference

• June 17-19, 2013, Four Seasons Hotel,

Shanghai – see http://www.risiinfo.com/events/asia_conf/

• June 19, 2013 – RISI seminar on Global

Timberland Investment Trends and

Opportunities for Chinese Investors, see http://www.risiinfo.com/events/asia_conf/timberland_investme

nts_program.html

7th International Woodfibre Resources

and Trade Conference

• Focus on international trade in woodchips and biomass.

• To be held first week in November, 2014, in Chile.

• Aimed at providing networking opportunities for both suppliers and buyers of woodchips and biomass.

• Conference web site www.woodfibreconference.com

RISI’s International

Pulpwood Trade Review

(also known as “the

woodchip bible”) has

provided information on

international trade in

woodchips and biomass

for the past 20 years.

See

www.risi.com/pulpwood

Contact: Bob Flynn

Email: [email protected]

Top Related