Languages

Pages

Legal

ICF International | icfi.com © ICF 2015 00

MRO Market Forecast & Trends

3 November 2015 - Singapore

Presented by:

David StewartVice President, ICF [email protected]

ICF International | icfi.com © ICF 2015 1

MRO Market Forecast

Takeaways

Trends

ICF International | icfi.com © ICF 2015 2

MRO Market Forecast

Agenda MRO Market Forecast & Trends

ICF International | icfi.com © ICF 2015 33

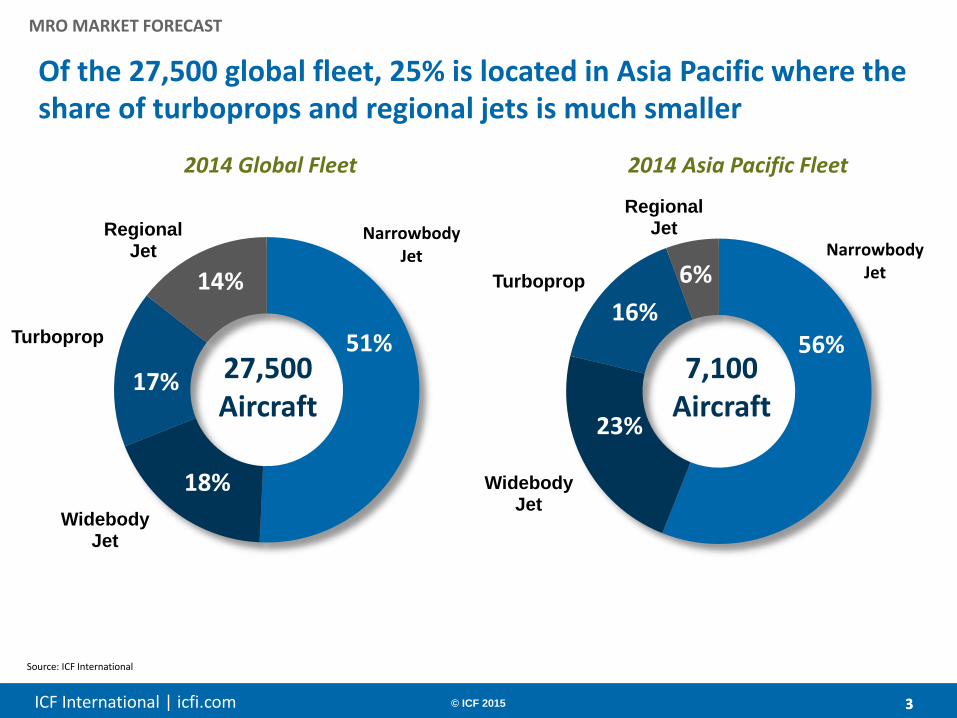

Of the 27,500 global fleet, 25% is located in Asia Pacific where the share of turboprops and regional jets is much smaller

MRO MARKET FORECAST

Source: ICF International

Narrowbody Jet

Widebody Jet

Turboprop

Regional Jet

6%

16%

23%

56%

Narrowbody Jet

Widebody Jet

Turboprop

Regional Jet

14%

17%

18%

51%27,500Aircraft

7,100Aircraft

2014 Global Fleet 2014 Asia Pacific Fleet

ICF International | icfi.com © ICF 2015 44

The Asian fleet will see a large growth over the next decade and the second fastest growth globally of 4.7% CAGR; +4,200 A/C

MRO MARKET FORECAST

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

2014 2024

Africa

Middle East

South America

Europe

Asia Pacific

North America

Air Transport Fleet Growth 2014–2024

Source: ICF International, ACAS September 2014

3.8%

2.7%

4.7%

1.4%

5.3%

4.8%

27,500

37,900CAGR

3.2% Average

~7,15025%

~11,35030%

Highlights

Air travel growth of ~3.8%

~19,000 aircraft deliveries

~8,600 aircraft retirements

AsiaPacificAsia

Pacific

ICF International | icfi.com © ICF 2015 55

The current air transport MRO market is $62.1B; Asia Pacific accounts for ~27% of global demand (~$16.9B)

MRO MARKET FORECAST

Engines

Components

Line

Airframe

Modifications

15%

17%

22%

40%

6%North

America

Asia Pacific

Europe

Middle East

South America

Africa

29%

27%

27%

7%

6% 4%

2014 Global MRO Demand

Source: ICF InternationalForecast in 2014 $USD, exclusive of inflation

$62.1BTotal

$62.1BTotal

By MRO Segment By Region

ICF International | icfi.com © ICF 2015 66

$60.7B

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

2014 2024

Modifications

Heavy Airframe

Line

Components

Engine

The global MRO market is expected to grow to $90B by 2024, at 3.8% per annum

MRO MARKET FORECAST

Global MRO Spend 2014–2024 ($B)

15%

17%

22%

40%

13%

17%

24%

38%

6%

8%

Highlights

Average growth is forecast to be 3.8% CAGR

The strongest drivers of growth are the engine and component markets

Reduced labor intensity of airframe heavy checks as the fleet renews and increased intervals

Aircraft upgrades (e.g. interiors, winglets) drive high modifications growth

2.6%

3.7%

4.5%

3.5%

5.9%

CAGR

3.8% Average

$90B

$62.1B

Source: ICF InternationalForecast in 2014 $USD, exclusive of inflation

ICF International | icfi.com © ICF 2015 77

Over the next decade, MRO growth will be 3.8% with Asia Pacific and China driving this growth….

MRO MARKET

Source: ICF analysisForecast in 2014 $USD, exclusive of inflation * absolute growth in annual spend

US$ Billions

$0.0

$10.0

$20.0

$30.0

$40.0

$50.0

$60.0

$70.0

$80.0

$90.0

$100.0

2014 2024

Africa

Eastern Europe (Incl. CIS)

Latin America

Middle East

China

Asia/Pacific (Excl. China)

Western Europe

North America

2014-2024 Annual MRO Spend By Region

6.8%

1.7%

1.2%

CAGR

3.8% Average

$62.1B

$90.1B

6.7%

5.2%

6.1%

6.4%

4.9%

Africa

E. Europe

L. America

M. East

China

APAC (ex. China)

W. Europe

N. America

Highlights

Highest % growth rates are the Middle East and China regions

Highest absolute growth (in $ terms) in Asia Pacific and China

2024 annual spend in China and Asia Pacific combined $12B higher than in 2014

$5.8B

$11.1B

$11.2B

$18B

ICF International | icfi.com © ICF 2015 8

Agenda MRO Market Forecast & Trends

Trends

ICF International | icfi.com © ICF 2015 9

The aftermarket has evolved from being an afterthought to a market of significant importance and a revenue opportunity

TRENDS

1980 – 2000 Post-2000s

Airlines

Maintenance mainly a cost centre

LCC’s drive new approach to managing maintenance -increased outsourcing

Limited focus on aftermarket; Rolls-Royce ahead of the game

Significant growth of point-of-aircraft sale MRO contracts by OEMs to recover design/ development costs

OEMs

MROs Supply mostly in-house –

few large airline MRO suppliers and hugely fragmented independent sector

Growth of integrated component services

Globalization of demand

The aftermarket has evolved from a cost centre to a highly competitive market

ICF International | icfi.com © ICF 2015 10

Engine OEMs have the most mature and strongest OEM position across the main air transport aftermarket segments

TRENDS

55%

35%

2% 0%

20%

25%

44%

82%

25%

40%

54%

18%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Engineoverhaul

ComponentO&R

AirframeHeavy

Linemaintenance

Non-OEMMRO

Airline in-house

OEM

Source: ICF International

Highlights

OEMs tend to have the strongest share in the more material intensive markets (e.g. engine overhaul)

Component OEM market share lower than engine OEMs

Aircraft OEMs have an almost non-existent position in the airframe-related aftermarket

Air Transport Supply (2015)

ICF International | icfi.com © ICF 2015 11

The ramp up and introduction of new generation aircraft creates the opportunity to change the aftermarket supply chain

TRENDS

Source: ICF International

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2015 2016 2017 2018 2019 2020 2021 2022 2023 2024

Aircraft deliveries (units)Highlights

New aircraft with higher reliability, lower manhours and complex technology change the business case for establishing MRO capability

…especially with greater airline focus on financial returns

This is a catalyst to change the MRO supply model….

Creating new opportunity for OEMs and aftermarket providers

Mature Aircraft

New Generation Aircraft

ICF International | icfi.com © ICF 2015 12

ICF believes there are three key trends that are defining the future of the Aftermarket

TRENDS

Control of operational data

Control of the Workscope

Control of the Assets

Critical to success in market participation and in gaining operational feedback for design and reliability improvement

Critical to success in driving parts choice and aftermarket margins

Critical to success in growing integrated service market

ICF International | icfi.com © ICF 2015 13

A key challenge for aviation stakeholders is how best to realize value from the terabytes of data being generated

TRENDS:

Source: ICF Analysis

Number of AHM Parameters

767: 10,000

A320: 15,000

787: 100,000

777 787

~ 28MB

< 1MB

Transmittable Data(MB/Flt)

Aircraft Data Generation(TB/Year)

2012 2022

~ 137TB

~11TB

~1,100%

increase

DATA

Data ownership versus data access and use are of great concern to operators, and data processing business models are unproven (except at engine OEMs?)

ICF International | icfi.com © ICF 2015 14

Aircraft OEMs are vying to use their leverage to become the arbiters of data for the connected airline…

TRENDS:

• Boeing EDGE: “Information Services” , the

Digital Airline and Gold Care brands

• Notable Aircraft Health Management (AHM)

successes

• “Services by Airbus”: Including E&M e-

solutions

• “Airbus Smarter Fleet” partnership with IBM

- integration of e-solutions

Boeing View of AHM System Architecture

Aircraft OEMs believe that their scale and position in the market make them a natural middleman for data aggregation and analysis

DATA

ICF International | icfi.com © ICF 2015 15

Control of workscope is key to input decisions – hence the historic focus on this by engine OEMs and the former PMA “War”

TRENDS: WORKSCOPE

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Engine

Materials80%

Labour20%

Airframe

Materials20%

Labour80%

Components

Materials55%

Labour45%

Line

Materials15%

Labour85%

Typ

ical

MR

O C

ost

Bre

akd

ow

n

Typical Aftermarket Cost BreakdownInsight

For engine and component activity “Whoever controls the workscope controls the parts decision” – this is a key driver behind related OEM aftermarket strategies

Use of PMA, repairs and surplus are important alternatives to OEM new parts

Source: ICF International

ICF International | icfi.com © ICF 2015 16

The share of integrated programs in component support is set to increase

TRENDS: ASSETS

Component Support Buying Behaviour

Growth Drivers

Small fleet size

Perceived technology risk

Improved ROIC

Maintenance no longer core

Predictable outgoings

Attractive value propositions

Lower investment, less infrastructure

Source: ICF International

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2004 2014 2024

Integrated*

Traditional

Integrated Component Programs

Penetration

777 787/A350

~20% 55%-70%

9%

30%

45%

Control of assets enables aftermarket players to support integrated programs more effectively – The more inventory held by a supplier, the lower the

inventory cost per aircraft supported

ICF International | icfi.com © ICF 2015 17

Takeaways

Agenda MRO Market Forecast & Trends

ICF International | icfi.com © ICF 2015 18

Today, airlines have strong ownership/control of their destiny, but do they make the most of it?

TAKEAWAYS

Who Owns The Workscope?

Who Owns The Assets?

Airlines

StrongKey Weak Improving Worsening

Eng Comp Airframe

Who controls the operational data?

Who controls the workscope?

Who controls the assets?

Source: ICF International

Airlines, as a buyer of aircraft and the owner of the operational data, should push the aftermarket supply chain...to benefit from better,

more cost efficient solutions

ICF International | icfi.com © ICF 2015 19

The Airframe and Component OEMs – who have the most to gain – will be very active and focused on MRO moving forward

TAKEAWAYS

Airlines

OEMs *

Airline MRO

Eng. OEMs

Source: ICF International

WHO HAS MOST TO GAIN(example benefits)

Higher reliability (e.g.,

predictive maintenance)

Lower costs (fuel,

maintenance, less inventory)

Operational data for feedback

into design loop

Increased revenue & margin

Reduce costs and improve

competitiveness

Market access

CURRENT POSITION IN MARKET

Operational data for feedback

into design loop

Increased revenue & margin

ICF International | icfi.com © ICF 2015 20

Large airline integrator MROs are well positioned – in contrast to independent MROs

TAKEAWAYS

Who Owns The Data?

Who Owns The Workscope?

Who Owns The Assets?

Airline MROs

Independent MROs

StrongKey Weak ImprovingWorsening

Who controls the operational data?

Who controls the workscope?

Who controls the assets?

Takeaways

For Airline MROs, significant scale is a must for engine and component markets

The business case for small airline MROs will erode significantly moving forward

Independent MROs have to become the lowest cost producer and/or align with the large airlines or OEMs

ICF International | icfi.com © ICF 2015 21

In summary...

TAKEAWAYS

Airlines have the opportunity to drive efficient solutions and competition into the aftermarket

Airframe and Component OEMs will invest more and increase their focus on aftermarket especially on integrated component packages

(Large) Airline MROs can and need to protect their market position versus the OEMs

Scale and scope of assets under management is vital

ICF International | icfi.com © ICF 2015 22

Last but not least, it is very important not to forget the MRO market for current aircraft is large and growing

TAKEAWAYS

Current Generation

New Generation

Old Generation

5%

22% 73%

Current …

Old Generation

New Generation

3%

24%

73%$16.9B $29.1B

2014 Asia Pacific MRO Demand 2024 Asia Pacific MRO Demand

Source: ICF InternationalForecast in 2014 $USD, exclusive of inflation

...And the supply chain and competition for this current generation of aircraft is not changing so dramatically and is well served by all MROs

23© ICF International 2015

Thank you!For questions regarding this presentation, please contact:

David StewartVice PresidentAerospace & MRO Advisory

+44 (0)7770 410011 [email protected]

icfi.com/aviation

ICF International | icfi.com 24© ICF International 2015 24

M&A Commercial Due Diligence

MRO Market Research & Analysis

Aerospace Manufacturing Strategy

Aviation Asset Valuations & Appraisals

MRO Cost & Performance Benchmarking

MRO Information Technology (IT) Assessment

MRO Strategic Sourcing Support

Supply Chain Management

LEAN Continuous Process Improvement

Military Aircraft Sustainment

ICF International’s Aviation advisory services include the following:

Top Related