Languages

Pages

Legal

Mobile Outlook 2012An insiderRESEARCH Special Report

by Kevin Benedict, Founder, Netcentric Strategies

Sponsored by:

insiderRESEARCH is the independent research arm of WIS Publishing (publisher of SAPinsider), conducting studies across the worldwide base of SAP and SAP BusinessObjects customers. Each insiderRESEARCH report is tailored to deliver comprehensive, accurate, and actionable results. For more information, contact [email protected].

WIS Publishing is the leading independent provider of information to professionals who deploy, manage, support, configure, and customize SAP solutions. More than 250,000 professionals in 61 countries rely on products and events from WIS Publishing to improve their company’s ROI in information technology.

Mobile Outlook 2012 © 2012 is published by Wellesley Information Services, LLC (WIS), a division of UCG, at 20 Carematrix Drive, Dedham, MA, 02026. Although WIS uses reasonable care to produce this and other insiderRESEARCH studies, we cannot assume any liability for its contents.

SAP is a registered trademark of SAP AG in Germany and in several other countries. All other registered trademarks are the property of their respective holders.

This report is the exclusive property of WIS and may not be reproduced in any form without written consent.

1Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

Mobile Outlook 2012

by Kevin Benedict, Founder, Netcentric Strategies

Executive Summary ..................................................................................................................................................................... 2

Findings ........................................................................................................................................................................................... 4

Demographics .............................................................................................................................................................. 5

Mobile Strategy in the Enterprise ......................................................................................................................... 7

Mobile Strategy Influencers ..................................................................................................................................12

Development Strategy ............................................................................................................................................14

Applications, Devices, Platforms, and Skills .....................................................................................................15

Approaching Your Day-to-Day Infrastructure .................................................................................................23

Development Tools ..................................................................................................................................................24

Vendor Considerations ...........................................................................................................................................26

About Our Sponsors ..................................................................................................................................................................28

2 Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

Executive SummaryIn the past few years, SAP and IBM have purchased mobile platform vendors, leaving the rest of the industry scrambling to satisfy customer demand for mobile solutions. Why is this? It is because enterprise mobility is the emerging interface of business applications. This interface is not just a new kind of technology or user interface (UI) — rather it represents a lifestyle and a transformational way of conducting business.

Mobile solutions can free decision makers — who have long been held hostage to their cubicles and desks — to go where they can have the biggest impact on the business. This may be at a remote job site or in front of customers or suppliers. Today, decision makers and their mobile workforces can take their entire business operation with them on smartphones and tablets. Real-time visibility and access to business intelligence and big data on their mobile devices gives them the best information possible to make good and quick decisions, no matter their location. This capability is known by many different names, including situational awareness, network-centric operations, or simply managing the real-time enterprise. Whatever you call it, it is changing the world of business.

The ability to have real-time visibility into operations, asset and resource locations, jobs, sales and production statuses, customer and supplier issues, and other mission-critical information, all tied to real-time business analytics and available on mobile devices of your choice, opens the doors to completely new strategies for running your business. These strategies can lead to incredible competitive advantages, improved efficiencies, and higher productivity levels. Enterprise mobility can be, and is, transformational.

Entire industries such as healthcare, media, advertising, retail, field services, and banking are experiencing a rapid transformation today in large part due to digitization, the Internet, and mobile technologies. There are very few individuals, businesses, or industries today that are not feeling the effect of mobility. Mobility is more than a technology — it is an historic event.

This report is a snapshot of where SAP customers are today, and where they expect to be in the near future, when it comes to mobility. We have identified many challenges involving training, staffing, education, technology choices, design, development, deployment, support, and change management methodologies. Organizations have difficult choices to make on business and technology strategies, platforms, security, mobile devices, and support and maintenance budgets.

Kevin BenedictFounder Netcentric Strategies

Kevin Benedict is an independent mobility analyst with 22 years of experience in the enterprise applications market, including executive roles at MobileDataforce and Crossgate. Kevin is an SAP Mentor and a frequent speaker at SAP industry events.

About the Author

3Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

Among other findings, this report reveals that:

• The percentage of organizations with a comprehensive, enterprise-wide mobile strategy will more than double in the next three years, from 32% to 67%.

• Three quarters of organizations expect their mobile applications to be supported on multiple devices three years from now.

• Almost a third (32%) of organizations will deploy five or more mobile applications in the next twelve months.

• Organizations are increasingly looking in house for development and implementation of mobile applications, yet they lack clear requirements from the business side.

This report is not just a list of opinions on enterprise mobility. It is a view into the plans, strategies, challenges, and ambitions of many different industries and how they are rapidly adopting mobile technologies and evolving their strategies to maximize their return on investment.

4 Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

Findings

5Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

Demographics

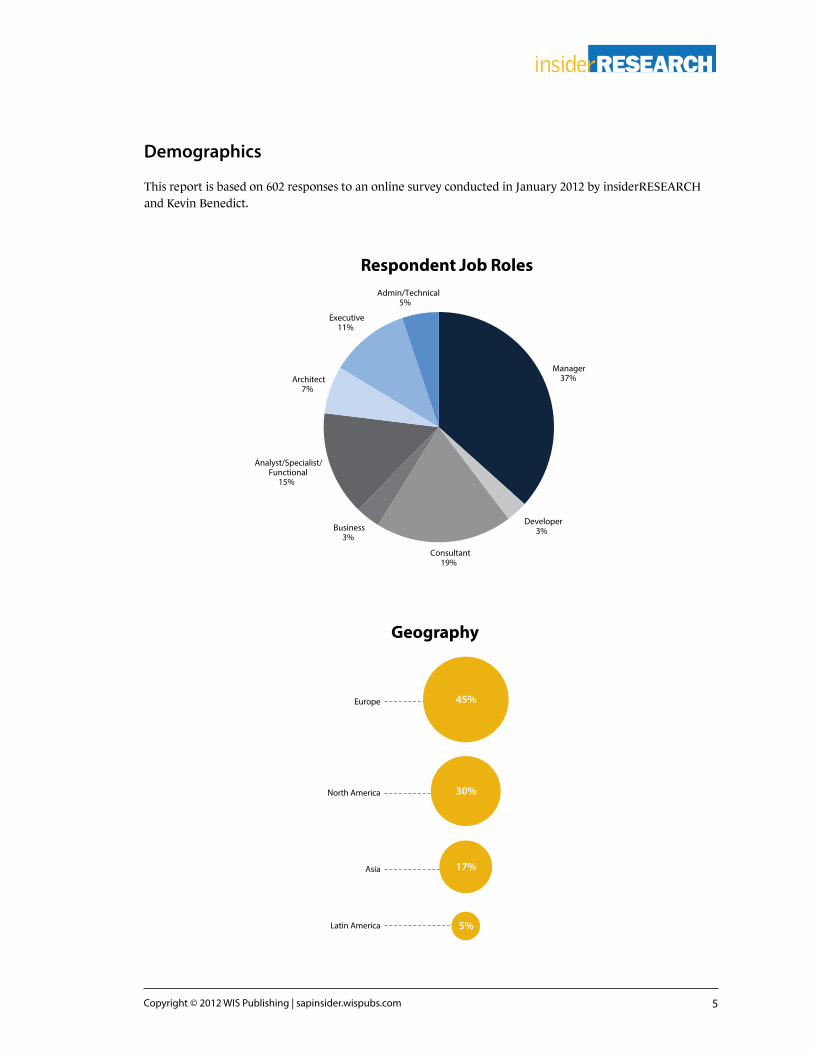

This report is based on 602 responses to an online survey conducted in January 2012 by insiderRESEARCH and Kevin Benedict.

North America

Asia

Latin America

Europe

Manager 37%

Developer 3%

Consultant 19%

Business 3%

Analyst/Specialist/ Functional

15%

Architect 7%

Executive 11%

Admin/Technical 5%

Respondent Job Roles

45%

30%

17%

Geography

5%

6 Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

21% 20%

15%

44%

$0 - $30 million $30 - $500 million $500 million - $1 billion Over $1 billion

Respondent Company Revenues

5%

21%

26%

43%

43%

51%

Other

I develop mobile applications

I provide technical support for mobile applications

I am a user of mobile applications

I provide functional or business supportfor mobile applications

I set or in�uence the strategy for ourmobile deployments

Involvement in Mobility

*Multiple answers accepted

7Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

Mobile Strategy in the Enterprise

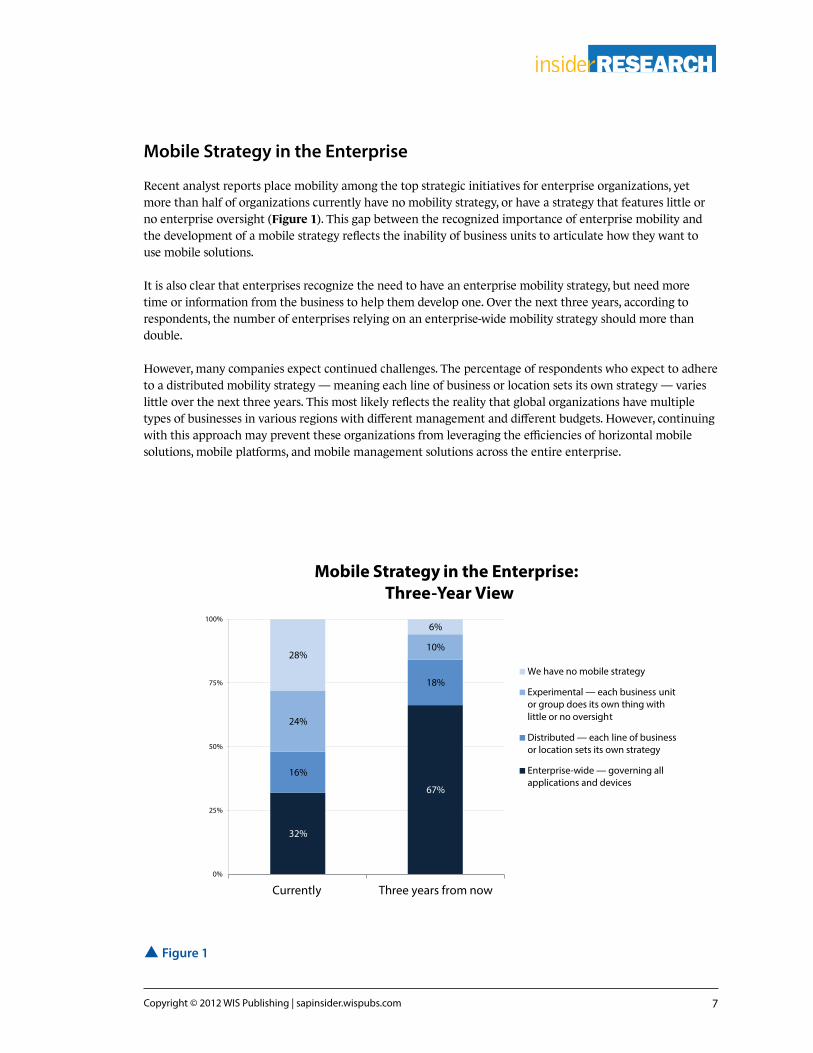

Recent analyst reports place mobility among the top strategic initiatives for enterprise organizations, yet more than half of organizations currently have no mobility strategy, or have a strategy that features little or no enterprise oversight (Figure 1). This gap between the recognized importance of enterprise mobility and the development of a mobile strategy reflects the inability of business units to articulate how they want to use mobile solutions.

It is also clear that enterprises recognize the need to have an enterprise mobility strategy, but need more time or information from the business to help them develop one. Over the next three years, according to respondents, the number of enterprises relying on an enterprise-wide mobility strategy should more than double.

However, many companies expect continued challenges. The percentage of respondents who expect to adhere to a distributed mobility strategy — meaning each line of business or location sets its own strategy — varies little over the next three years. This most likely reflects the reality that global organizations have multiple types of businesses in various regions with different management and different budgets. However, continuing with this approach may prevent these organizations from leveraging the efficiencies of horizontal mobile solutions, mobile platforms, and mobile management solutions across the entire enterprise.

32%

67%

16%

18%

24%

10% 28%

6%

0%

25%

50%

75%

100%

Currently Three years from now

Mobile Strategy in the Enterprise: Three-Year View

We have no mobile strategy

Experimental — each business unitor group does its own thing withlittle or no oversight

Distributed — each line of businessor location sets its own strategy

Enterprise-wide — governing allapplications and devices

p Figure 1

8 Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

More than half of companies have yet to find the right formula to make enterprise mobility a truly transformational experience (Figure 2). In my experience, companies that adopt mobile technologies without re-engineering business processes and workflows to take advantage of real-time data exchanges on mobile devices spend a lot of money with little return.

As organizations continue to create their mobility strategies, the business must determine how they plan to use mobile solutions to meet business goals. Mobility vendors and service providers should focus on educating clients and helping them develop mobile strategies.

12%

37%

28%

13% 10%

Very effective Somewhat effective Neither effectivenor ineffective

Somewhat ineffective Very ineffective

Perceived E�ectiveness of Mobile Strategies

p Figure 2

9Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

When it comes to building a mobile strategy, organizations face many different types of challenges (Figure 3). The most important challenges center on business strategies around mobility — not synchronizing data from mobile devices to an ERP system or extending ERP applications to mobile devices. These technical challenges have well-documented solutions.

The more important challenge is for the business to decide how mobility fits into the organization’s current and future business strategies. It’s up to business leadership to determine how mobility solutions are best utilized in their industry and communicate these solutions to the IT team.

1%

1%

1%

2%

2%

2%

3%

5%

6%

6%

7%

7%

10%

11%

11%

14%

14%

User adoption

Vendor support

Application design

Managing expectations

Marketing and visibility

Ongoing support

Device management

Implementation/change management

Time, resources, or skills

Integration with back end

Keeping up with change

Executive/business support

Security

Budget

Choosing platform/technologies

Identifying/prioritizing business cases

Developing strategy

Top Challenges to Building Mobile Strategy

p Figure 3

10 Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

The results shown in Figure 4 illustrate the real importance of enterprise mobility. In a competitive global economy, these are areas of focus (increased productivity, improved customer engagement, etc.) that separate the best in class from the rest.

However, the business must articulate what specific features are necessary to deliver on these expectations and plans. For example, each of the 34% of organizations looking for a competitive advantage through mobility must answer several key questions. What kind of mobile solutions are they looking for? What kinds of features will give them an advantage? The answers may be increased marketing effectiveness, better customer service, or increased sales by on-site field services technicians, among others. These requirements need to be documented and shared with the IT organization in order to develop a mobile strategy that will deliver a competitive advantage.

However, the challenges cited by our respondents are unlikely to be solved by a single mobility solution or platform. The challenge is to deliver as many solutions as possible with a standard mobile platform. If a single platform is not realistic, then the organization should attempt to deliver results with as few platforms as possible.

4%

17%

20%

27%

31%

33%

34%

46%

46%

53%

70%

Other

My organization has not deployed any mobile apps

Pressure from business workers

Marketing purposes

Reduce costs

Improve visibility and accountability

Competitive advantage

Enable �eld sales sta�

Provide business intelligence to decision makers

Improve customer interactions

Increase productivity

Reasons for Building Mobile Strategy

9%

10%

14%

14%

35%

Competitive advantage

Provide business intelligence to decision makers

Improve customer interactions

Enable �eld sales sta�

Increase productivity

Most Important Reasons

p Figure 4 *Multiple answers accepted

11Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

These results also demonstrate that companies expect improvements in both top-line and bottom-line revenue numbers from enterprise mobility solutions. Three of the top four reasons cited for building a mobility strategy focus on improving the productivity of the mobile workforce, including sales and management. The more free your sales and management personnel become, the better your customer interactions will likely be, which could lead to competitive advantages. These business priorities must be translated into a list of requirements needed to deliver results. These requirements will then be used to define the right mobile strategy and technology.

Only 30% of organizations identified business leadership (CEOs and line of business leaders) as ultimately responsible for setting mobile strategy today (Figure 5). Ideally, this responsibility would be shared between

33% 36%

28% 20%

16%

13%

14%

14%

3%

4%

3%

3%

2%

1%

1%

1%

8%

0%

25%

50%

75%

100%

Today Three years from now

Mobility Strategy Responsibility: Three-Year View

I don't know

CMO

CFO

Other

Application managers

CEO

Line of business leadership

IT management

CIO

p Figure 5

12 Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

business and IT — with the business first laying out a business strategy and IT putting that strategy to work. In many industries, mobile technologies are changing the whole business environment (think print media, digital media, healthcare, field services, and enterprise asset management). If the business understands the dynamics that shape its industry and what is possible with mobility, it can work closely with IT to take advantage of it. If the business views enterprise mobility as simply a technology issue, it risks obsolescence.

Over the next three years, our respondents suggested the IT organization will play an increasingly larger role in setting mobile strategy, while the business will play a smaller one. This may reflect an expectation that the business will have articulated how it wishes to use mobility between now and then, and the responsibility will have shifted to the IT organization to deliver on the strategy.

Mobile Strategy Influencers

While the line of business is rarely responsible for setting mobile strategy, it is still a very influential force in that strategy (Figure 6). This makes perfect sense — the line of business has the most intimate knowledge of

Internal In�uencers

Line of business management

Executives

IT management

Most in�uential

Least in�uential

End usersConsultants

Technology vendors

p Figure 6 *Relative scale calculated by median ranking score

13Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

External In�uencers

Security

Integration with back-end data

Cost of development/deployment

Integration with application infrastructure

Application maintenance/management

Most in�uential

Least in�uential

Device management

Need to support multiple devices

p Figure 7 *Relative scale calculated by median ranking score

their business and how mobile solutions can impact their areas of responsibilities. As a result, they should be the key influencers.

Giving thousands of mobile workers access to confidential and mission-critical data on their mobile devices offers enormous benefits and huge risks. Many enterprises are delaying the benefits of mobile solutions out of security concerns (Figure 7). It is important to know there are many very good security systems designed to provide security on mobile devices. These vendors may be your existing systems management and enterprise security providers that now offer mobile security extensions, or dedicated mobile device management vendors that offer both cloud and on-premise solutions.

It is also no surprise that enterprises are focused on back-end integration — the lifeblood of a large organization. SAP’s own mobile solutions and services are rapidly maturing and getting stronger every quarter with SAP NetWeaver Gateway and new versions of the Sybase Unwired Platform.

14 Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

Development Strategy

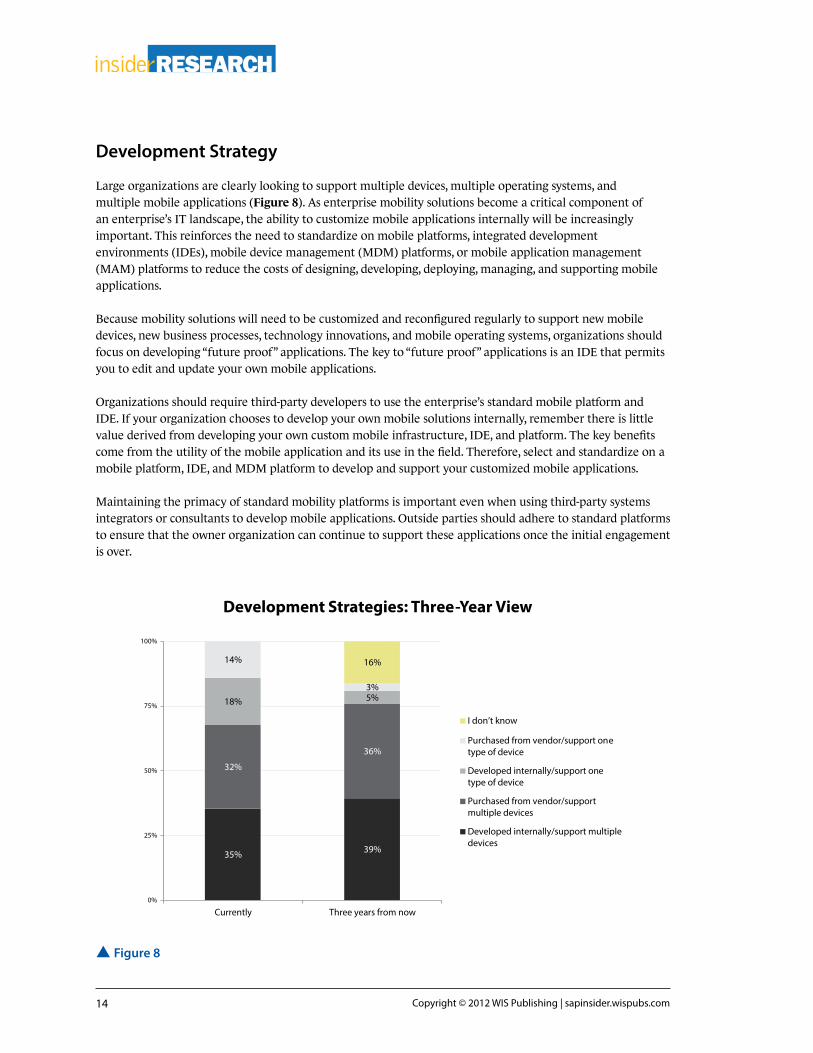

Large organizations are clearly looking to support multiple devices, multiple operating systems, and multiple mobile applications (Figure 8). As enterprise mobility solutions become a critical component of an enterprise’s IT landscape, the ability to customize mobile applications internally will be increasingly important. This reinforces the need to standardize on mobile platforms, integrated development environments (IDEs), mobile device management (MDM) platforms, or mobile application management (MAM) platforms to reduce the costs of designing, developing, deploying, managing, and supporting mobile applications.

Because mobility solutions will need to be customized and reconfigured regularly to support new mobile devices, new business processes, technology innovations, and mobile operating systems, organizations should focus on developing “future proof” applications. The key to “future proof” applications is an IDE that permits you to edit and update your own mobile applications.

Organizations should require third-party developers to use the enterprise’s standard mobile platform and IDE. If your organization chooses to develop your own mobile solutions internally, remember there is little value derived from developing your own custom mobile infrastructure, IDE, and platform. The key benefits come from the utility of the mobile application and its use in the field. Therefore, select and standardize on a mobile platform, IDE, and MDM platform to develop and support your customized mobile applications.

Maintaining the primacy of standard mobility platforms is important even when using third-party systems integrators or consultants to develop mobile applications. Outside parties should adhere to standard platforms to ensure that the owner organization can continue to support these applications once the initial engagement is over.

35% 39%

32%

36%

18% 5%

14%

3%

16%

0%

25%

50%

75%

100%

Currently Three years from now

Development Strategies: Three-Year View

I don’t know

Purchased from vendor/support onetype of device

Developed internally/support onetype of device

Purchased from vendor/supportmultiple devices

Developed internally/support multipledevices

p Figure 8

15Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

When purchasing off-the-shelf mobile applications from vendors, it is important to understand the mobile infrastructure, platforms, and IDEs that are used by the vendor. It is in your best interest to reduce and limit the number of different mobile platforms and infrastructures brought in and supported by your IT organization. If possible, organizations should require mobile application vendors to support their enterprise’s standard mobile platforms. This will reduce both the upfront costs of your mobile applications and the total cost of ownership (TCO).

Applications, Devices, Platforms, and Skills

Despite the recent focus on mobility solutions, only 20% of companies we surveyed have extended five or more business applications to their mobile devices (Figure 9). Many of these organizations are likely supporting multiple applications on multiple devices, with multiple integrations and multiple back-end applications. This is the typical starting point for many organizations. But as mobile applications proliferate, organizations will need to adhere to a standard approach to contain cost and complexity.

17%

64%

14%

4%

2%

None

Less than 5

5 to 10

10 to 15

15 to 20

Number of Mobile Applications Available Today

p Figure 9

16 Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

The good news is that nearly a third of organizations (32%) plan to implement five or more mobile applications in 2012 (Figure 10), and 88% are planning to implement at least one. The bad news is that 52% of organizations still profess to having “little or no oversight” over mobility strategy (refer back to Figure 1). This indicates a potential for serious issues, including inefficiencies, redundancies, and high TCO for mobile solutions.

SAP has been evangelizing enterprise mobility for the past few years, and clearly the installed base has responded, as 38% of companies we surveyed have connected SAP ERP to mobile devices (Figure 11). This puts SAP far ahead of most other ERP vendors.

12%

56%

15%

8%

3%

6%

None

1 to 5

5 to 10

10 to 15

15 to 20

More than 20

Planned Mobile Application Deployments (Next 12 Months)

p Figure 10

17Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

1%

1%

1%

1%

2%

2%

3%

3%

4%

4%

5%

5%

6%

7%

8%

9%

38%

Help Desk

MS

non-SAP BI

Expenses

non-SAP sales

non-SAP HR

non-SAP ERP

SAP HR

Collaboration

SAP CRM

Other (unspeci�ed)

non-SAP CRM

Other SAP app

SAP BI/BW

Database

SAP ERP

Connections with Back-End Business Applications

p Figure 11

18 Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

When it comes to device support, tablets are the big trend today (Figure 12). The advent of instant access to real-time data and business intelligence reports, back-end systems, collaboration environments, and media on a full-size screen that enables powerful and visually stimulating user experiences is revolutionizing business.

Tablets are now replacing all of the remaining paper processes, image-rich environments (maps, blueprints, CAD drawings, etc.), spreadsheets, and media that simply did not transfer well onto small smartphone screens in the past.

Unlike traditional IT projects, mobile applications have no clear end. They must be continually updated to support new mobile devices, operating systems, and technologies. This means mobile applications must be understood to be a permanent development effort requiring a permanent budget (Figure 13). It also highlights the fact that standardizing on platforms, IDEs, and MDM platforms is essential to keep the cost of developing and maintaining mobile applications manageable.

These costs grow with each additional mobile application. This phenomenon must be understood by each member of the organization and reflected accurately in future budgets.

Remember that the cost of managing mobile devices extends beyond the initial hardware purchase. It is also important to consider who will pay for mobile data plans, data roaming charges, and the replacement of lost or broken devices. Organizations should consider several device-related questions when setting their mobility strategies: Does the organization plan to allow employees to use their own devices or will it provide devices for them? Will the organization pay for smartphones, tablets, and laptops for everyone, or are there different device support plans for different roles in the company? Is your organization taking advantage of volume mobile device discounts, or is each business unit paying retail prices?

Mobile devices, mobile data plans, and mobile data usage must be carefully monitored and managed to keep costs under control. Some MDM platforms include features for managing the provisioning of devices.

86%

61%

29%

6%

Smartphones Tablets Dedicated devices None

Supported Devices

p Figure 12 *Multiple answers accepted

19Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

“Bring your own device,” or BYOD, plans are becoming increasingly common in the enterprise (Figure 14). Just two years ago, the majority of enterprises would not have supported this type of device management strategy. It will be interesting to see how this trend continues to evolve over time.

1%

1%

2%

12%

13%

13%

16%

17%

26%

CMO

Application managers

Other

I don't know

CFO

Line of business leadership

IT management

CEO

CIO

Budget Control for Mobility Programs

p Figure 13

Yes 59%

No 41%

Support for “Bring Your Own Device” (BYOD)

p Figure 14

20 Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

One of the most surprising revelations of this survey is that only 29% of organizations allow field technicians access to business applications on mobile devices (Figure 15). “Field services” is regularly cited as a high priority area in most enterprise mobility surveys.

Decision makers in both business and IT are demanding and receiving mobile applications. Having access to the information necessary to make good, fast decisions no matter your location seems to be a driving force for the adoption of enterprise mobility.

SAP customers clearly take an expansive view of mobility — defining it in the broadest possible terms (Figure 16). As more consumer devices seep into the enterprise network and more organizations standardize on global platforms, expect even more companies to consider mobility in a similar way.

Our results demonstrate a real desire to improve the productivity of large mobile workforces by supplying them with standardized mobile applications (Figure 17).They also show that mobile workers who require more complex and/or customized mobile solutions, such as enterprise asset management, inspections, surveys, and assessments, have lagged behind. This is likely because of the large amount of required customization, wide use of in-house developed database applications, and relatively small number of workers involved in these areas.

9%

29%

34%

38%

40%

45%

60%

61%

70%

None

Field technicians

Functional workers

Super users

Field sales sta�

IT sta�

IT management

Line of business managers

Executives

Mobile Application Distribution by Job Role

p Figure 15 *Multiple answers accepted

21Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

15% 15%

70%

From anywhere in ouro�ce

From any of our o�cesworldwide

From anywhere in theworld

De�ning Mobile Access: Where Users Can Access Business Applications on Mobile Devices

p Figure 16

9%

13%

15%

16%

16%

17%

21%

23%

39%

40%

43%

44%

Other

Enterprise document management

Inspections, surveys, or assessments

Enterprise asset management

Enterprise content management

Proof of delivery

Supply chain management

Enterprise collaboration and social networking

Field services

Business intelligence reports

Work�ows

Sales/CRM

Top Mobilized Business Applications

p Figure 17 *Multiple answers accepted

22 Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

Most workflow applications are relatively simple, solve very specific issues, and are needed by large numbers of employees (Figure 18). Examples of these kinds of mobile applications include expense reports, vacation requests, travel requests, and invoice and purchase order approvals. The lack of complexity in these applications, plus the relatively small investment required, make these “instant value” applications a popular first step in mobilizing an enterprise.

Mobilizing workflow applications removes friction from many processes. Friction in processes can reduce productivity, increase days sales outstanding (DSO), cause poor cash management, and impact the quality of customer and supplier service. Enabling the mobile workforce to receive workflow alerts, and then to respond to them from anywhere, removes much of this friction.

Top Mobilization Priorities

Work�ows

Field services

Business intelligence and reportingSales/CRM

Enterprise asset management

Proof of delivery

Enterprise content management

Enterprise collaboration and social networking

Highest priority

Lowest priority

Inspections, surveys, assessmentsSupply chain management

Enterprise document management

p Figure 18 *Relative scale calculated by median ranking score

23Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

Approaching Your Day-to-Day Infrastructure

We discovered that many organizations are not prepared to integrate mobile solutions into their day-to-day infrastructure. For example, most organizations do not have a comprehensive plan for managing any of the printed output or stored documentation associated with critical business processes. Only 18% of those surveyed said their users could print from a mobile device, while only 32% said their users could move documents forward in a standard workflow from a mobile device. More than half of those surveyed (55%) agreed with the statement that managing documents from mobile applications is “a big challenge for us” (Figure 19).

We are quickly approaching a time when users will expect functionality from mobile applications that is equal to what they expect from desktop or even enterprise ERP applications. Smart organizations will consider solutions to address these issues.

18%

37% 34%

9%

2%

Strongly agree Agree Neither agree nordisagree

Disagree Strongly disagree

“Managing documents generated or moved forward on mobile devices is a big challenge for us.”

p Figure 19

24 Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

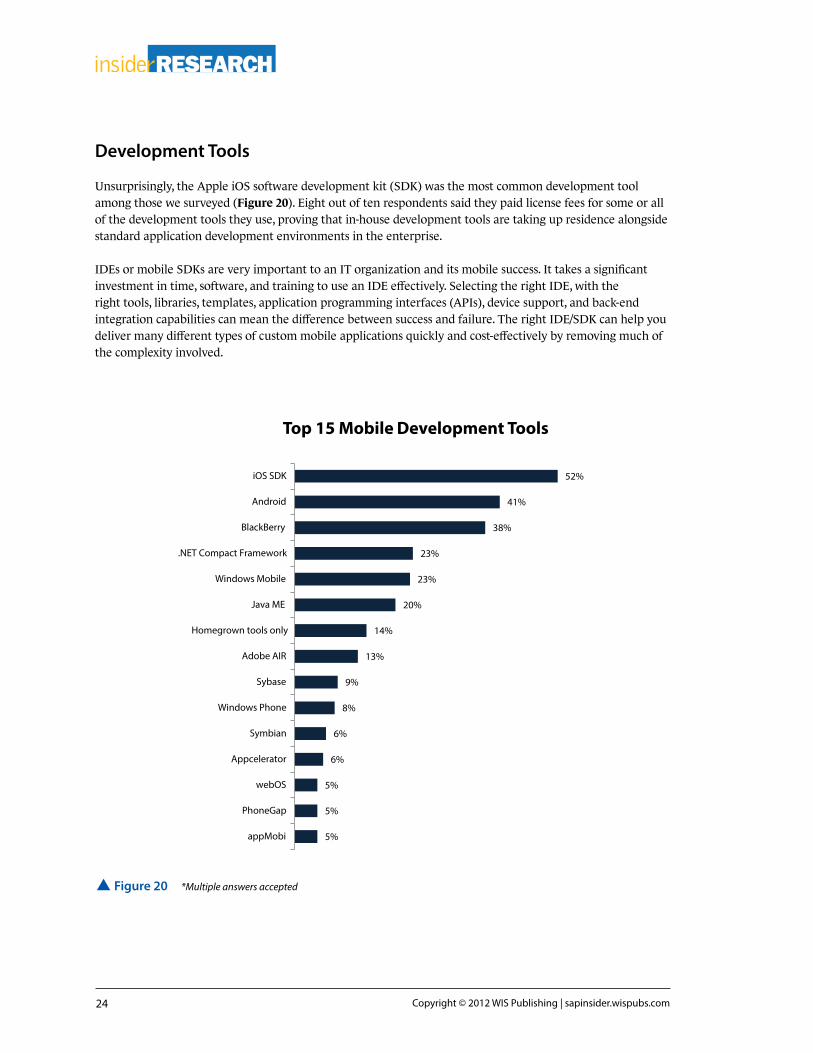

Development Tools

Unsurprisingly, the Apple iOS software development kit (SDK) was the most common development tool among those we surveyed (Figure 20). Eight out of ten respondents said they paid license fees for some or all of the development tools they use, proving that in-house development tools are taking up residence alongside standard application development environments in the enterprise.

IDEs or mobile SDKs are very important to an IT organization and its mobile success. It takes a significant investment in time, software, and training to use an IDE effectively. Selecting the right IDE, with the right tools, libraries, templates, application programming interfaces (APIs), device support, and back-end integration capabilities can mean the difference between success and failure. The right IDE/SDK can help you deliver many different types of custom mobile applications quickly and cost-effectively by removing much of the complexity involved.

5%

5%

5%

6%

6%

8%

9%

13%

14%

20%

23%

23%

38%

41%

52%

appMobi

PhoneGap

webOS

Appcelerator

Symbian

Windows Phone

Sybase

Adobe AIR

Homegrown tools only

Java ME

Windows Mobile

.NET Compact Framework

BlackBerry

Android

iOS SDK

Top 15 Mobile Development Tools

p Figure 20 *Multiple answers accepted

25Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

13%

14%

24%

49%

Buy o� the shelf solutions

Hire new sta�

Outsource

Train current sta�

Plans for Managing Skills Shortages

p Figure 21

Our results show a clear indication that enterprises will strive to keep as much mobile development skill in house as possible. Well over half of those surveyed said their organizations have the skills necessary to develop and maintain mobile applications in house, while 63% said they would train existing staff or hire new staff in the event of a skills shortage (Figure 21).

26 Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

Vendor Considerations

Most organizations rely on their internal development teams to implement mobile business applications (Figure 22). These results will likely change once enterprises move from the proof of concept (POC) phase on the mobile maturity curve to production implementation. When organizations recognize the need to support mobile applications on many different devices, for multiple users with various operating systems, they will seek ways to simplify and standardize. We will see more use of specialized application vendors and consultants for production environments in the future.

4%

9%

13%

23%

29%

67%

Cloud provider

I don't know

We do not have any mobile applications

Application vendor

Consultant

Internal IT team

Primary Responsibility for Implementing New Applications

p Figure 22 *Multiple answers accepted

27Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

The upfront cost of a mobile solution purchased from a vendor is important (Figure 23), but even more important is TCO over time. Does the mobile vendor provide you with the IDE so you can customize the mobile app to meet the future needs of your business, or are you limited by the mobile vendor’s product roadmap and schedule? It is important to factor in lost opportunity costs. If the business requires specific functionality, but your solution has no IDE that you can use to add these features, that is a lost opportunity cost.

An additional important consideration is the mobile platform, or platforms, supported by the mobile vendor. Do they use the Sybase Unwired Platform, or another vendor’s platform? In an ideal world, all of your mobile applications would run perfectly on just one mobile platform. We don’t live in an ideal world, but organizations should attempt to standardize on as few mobile platforms as possible to simplify their IT environment, support, and maintenance, and to reduce TCO. For example, an organization that runs twelve different mobile applications with twelve mobile platforms, developed using twelve different IDEs and integrated into your back-end systems in twelve varying ways, will quickly find the cost and complexity of their mobility solutions to spiral out of control.

Top Factors When Considering a Mobility Vendor

CostTrack record of working with SAP systems

Out of the box functionality

Integration with back-end systems

User experience (UX) of the mobile application

Built-in security features

Devices supported by the application

Operating systems supported by the application

Most important

Least important Consultant’s opinion

p Figure 23 *Relative scale calculated by median ranking score

28 Copyright © 2012 WIS Publishing | sapinsider.wispubs.com

About Our Sponsors

Cognizant (NASDAQ: CTSH) is a leading provider of information technology, consulting, and business process outsourcing services, dedicated to helping the world’s leading companies build stronger businesses. Headquartered in Teaneck, New Jersey (U.S.), Cognizant combines a passion for client satisfaction, technology innovation, deep industry and business process expertise, and a global, collaborative workforce that embodies the future of work. With over 50 delivery centers worldwide and 130,000 employees as of September 30, 2011, Cognizant is a member of the NASDAQ-100, the S&P 500, the Forbes Global 2000, and the Fortune 500 and is ranked among the top-performing and fastest-growing companies in the world.

Excellis Interactive improves the way people interact with your SAP solutions as well as your brand through user experience design. We evolve enterprise software, websites, and mobile solutions into impactful and usable applications by creating the relationship between the way that your users work and the application experience that supports that work. We assemble extraordinary user experiences to increase adoption of your systems, lower training costs, increase transaction throughput, and simplify your support model. We do all this by combining user-centered research, user interface design, process engineering, and experience marketing with your business objectives.

Levi, Ray & Shoup, Inc. (LRS) is an output management software provider founded in 1979 in Springfield, Illinois. Today, LRS has offices and customers around the globe; over half of the Fortune 500 and Fortune 500 Service companies rely on LRS solutions for reliable document delivery. Gartner and other analyst groups recognize LRS as a global IT leader, and Software Magazine consistently ranks LRS among the top 200 software companies in the world.

Syclo is SAP’s mobile co-innovation partner for asset management and CRM field service. We offer SAP customers a proven way to extend their systems to a variety of mobile devices — improving productivity, cutting costs, and providing a 360° view of operations with timely, accurate data from the field. Syclo’s SMART Mobile Suite of ready-to-deploy applications offers enterprises a quick and low-risk approach to mobilizing key business processes like work management, field service, approvals, inventory management, sales, and more. With tight integration with SAP systems, complete configurability, and enterprise-grade support, Syclo has the tools you need to enable your mobile enterprise.

Sky Technologies provides code-free “configure once, run anywhere” mobile enterprise applications to mobilize any SAP process to any device. The SkyMobile solution is available on-premise or via the SkyCloud and features our unique secure container, enabling online/offline capability and code-free cross-platform support. Applications are paired with industry-strength interface management and can be fully integrated with the Sybase Unwired Platform, Afaria, and SAP NetWeaver Gateway. Sky’s solutions are backed by more than 13 years of SAP mobility experience and have been deployed in over 35 countries among a customer base filled with Fortune 1,000 companies. Mobility made easy — it’s what we do.

The Principal Consulting, Inc. (TPC) is an official SAP services partner. TPC provides expert consulting in the SAP marketplace, helping customers of all sizes, across multiple industry segments, realize their business goals through the implementation of SAP products and solutions. TPC only provides senior, high-quality resources who possess the widest breadth of experience. We listen to our clients and have the flexibility to carefully select the “right fit” consultants to ensure the most beneficial, cost-effective solution. The enduring heritage of TPC is found in understanding the needs of our customers and exceeding their expectations.

Top Related