Languages

Pages

Legal

MASFAA Government Relations CommitteeChristine McGuire, Boston University

Bernard Pekala, Boston College

February 8, 2006President Bush signed the Higher Education

Reconciliation Act of 2005 (the “HERA”), Pub. L. 109 171, which made significant changes to the Higher Education Act of

1965, as amended (the “HEA”), and reauthorized the Federal Family Education

Loan (FFEL) Program.

Negotiated Rulemaking Required by the Department

Finished in April without consensus on the whole package of regulations.

Student Lending Accountability, Transparency and Enforcement Act

(SLATE)

Mirrors codes of conduct embedded in agreements entered into between NY Attorney General, lenders and

institutions.

Final Regulations(Federal Register, November 1, 2007)

Preferred Lender Lists must contain at least three unaffiliated lenders.

No lender who offers the institution any benefits may be on a PLL.

Must be reviewed & updated annually. Lenders may not automatically be

assigned through award packaging for first time borrowers.

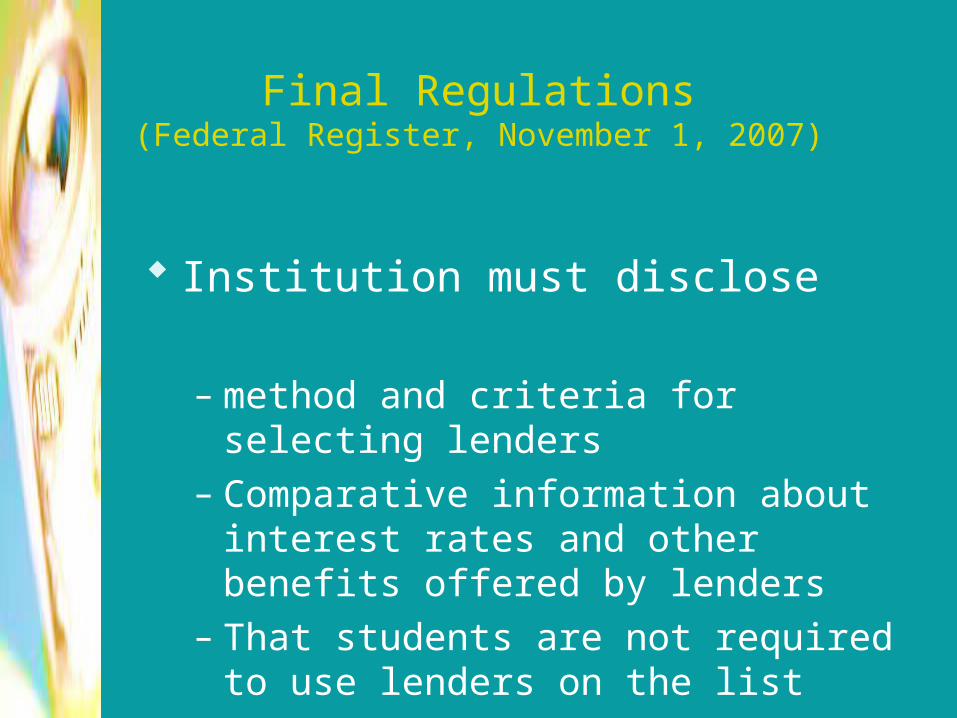

Final Regulations(Federal Register, November 1, 2007)

Institution must disclose

– method and criteria for selecting lenders– Comparative information about interest

rates and other benefits offered by lenders

– That students are not required to use lenders on the list

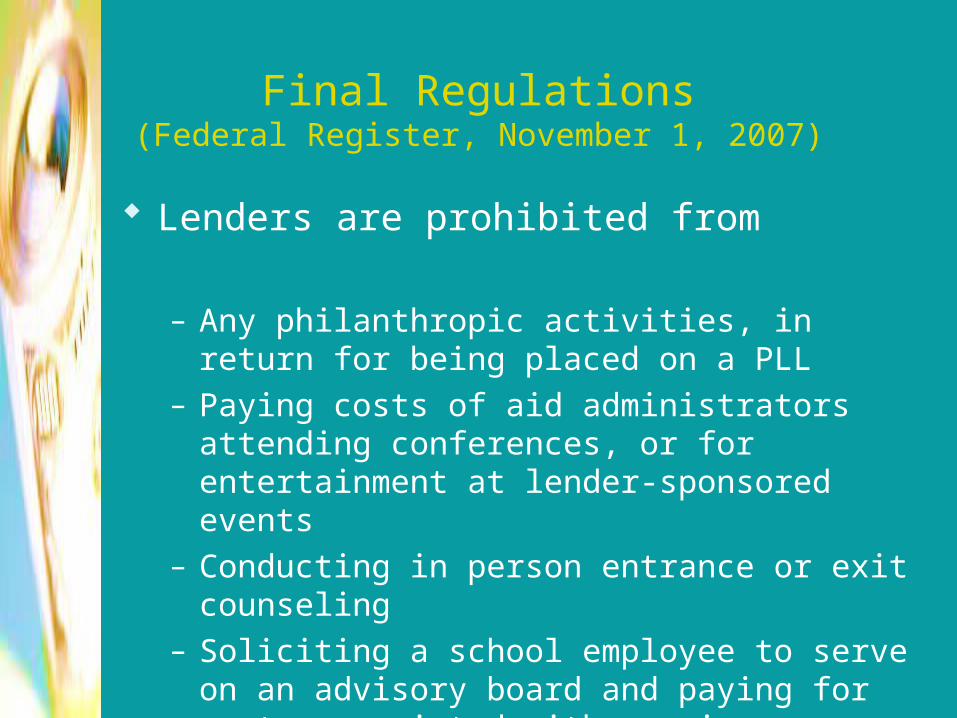

Final Regulations(Federal Register, November 1, 2007)

Lenders are prohibited from

– Any philanthropic activities, in return for being placed on a PLL

– Paying costs of aid administrators attending conferences, or for entertainment at lender-sponsored events

– Conducting in person entrance or exit counseling– Soliciting a school employee to serve on an

advisory board and paying for costs associated with serving on an advisory board

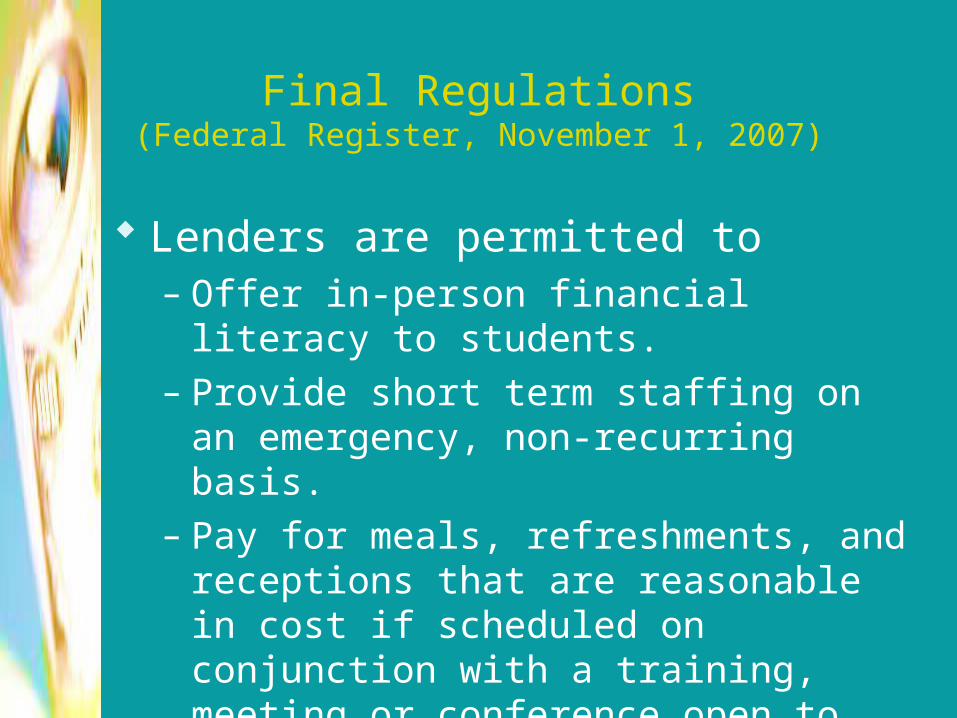

Final Regulations(Federal Register, November 1, 2007)

Lenders are permitted to– Offer in-person financial literacy to

students.– Provide short term staffing on an

emergency, non-recurring basis.– Pay for meals, refreshments, and

receptions that are reasonable in cost if scheduled on conjunction with a training, meeting or conference open to all attendees.

Higher Education Opportunity Act (HEOA) of 2008

Added a new Title to the Higher Education Act

Title X: Private Student Loan Improvement

o Specific legislation regarding non-federal educational loans

o Connected the Higher Education legislation to the “Truth in Lending Act”

Higher Education Opportunity Act (HEOA) of 2008

Title X: Private Loans

Defines a “gift” as: “means or gratuity, favor, discount, entertainment, hospitality, loan or other item having more than a de minimis monetary value, including services, transportation, lodging, or meals, whether provided in kind, by purchase of a ticket, payment in advance, or reimbursement after the expense has been incurred.

Defines a “gift” not to include:– Standard informational material related to a

loan, default aversion, default prevention or financial literacy

– Food, refreshments, training, or informational material furnished as part of a training session or through participation in an advisory council

Higher Education Opportunity Act (HEOA) of 2008

Title X: Private Loan

Defines a “gift” not to include:– Philanthropic contributions to a covered

educational institution from a private educational lender that are unrelated to private education loans

Higher Education Opportunity Act (HEOA) of 2008

Title X: Private Loans

Prohibits certain gifts and arrangements – A lender may not directly or indirectly:

Offer gifts in exchange for an advantage or consideration for private education loan activities

Engage in revenue sharing

Higher Education Opportunity Act (HEOA) of 2008

Title X: Private Loans

Co-Branding:

A private educational lender many not use the name, emblem, mascot or logo of the institution, in the marketing of the loan

Advisory Board Compensation:

However, allows for the reimbursement of reasonable expenses incurred as part of service on an advisory board

Higher Education Opportunity Act (HEOA) of 2008

Title X: Private Loans

Prohibits:

Prepayment or Repayment fees or penalites:

Makes it unlawful for any private educational lender to impose a fee or penalty on a borrower for early repayment or prepayment of any private education loan.

Higher Education Opportunity Act (HEOA) of 2008

Title X: Private Loans

Prohibits:

What approach should schools be taking regardless of whether DL or

FFELP?Articulate clear policies regarding:

Institutional gift policyConflict of interest policyDisclose the process for evaluating

the lenders or loans recommended, regardless of Federal or private credit

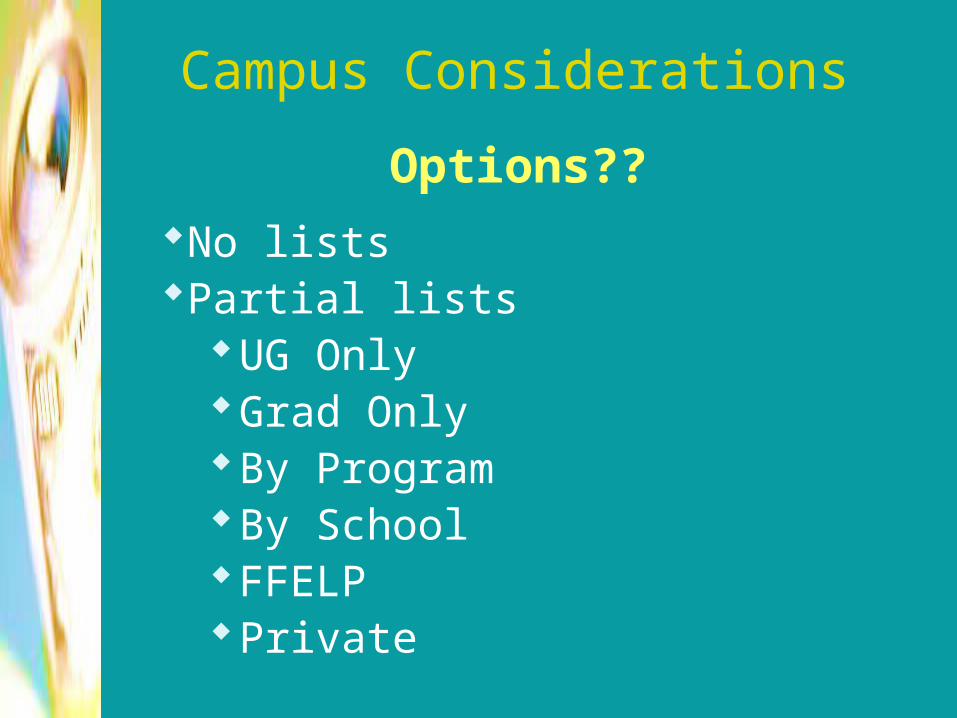

Campus Considerations

Options??

No listsPartial lists

UG OnlyGrad OnlyBy ProgramBy SchoolFFELPPrivate

Campus Considerations

Options??

How many on the listList Types

Inclusive (All)VolumeBenefit

Campus Considerations

Information Collection Options??

Request For ProposalsRequest For Information

MASFAA’s RFI Template

MASFAA Government Relations Committee provided a packet of templates and information in February 2008.

•The professional information was intended as a best practice sharing of information

•NOT intended to be used “as is”

•The templates should have been modified for your campus

•Use of these materials provides no assurance of complete compliance

MASFAA’s RFI Template

ExternalCover LetterRFISavings Answer Sheet

InternalRFI Comparison MatrixSavings Worksheet

DisclosureWebPaper

MASFAA’s RFI Template

FEEDBACK TIME:If you used them, what are your

positive and negative commentsShould we revise for 2009?Should we issue a private loan

version?If you didn’t use them, why not?Would you have if they had been

different?

Approximately 20 schools used the templates as indicated on the MASFAA listserv.

DISCUSSIONDISCUSSIONand and

QUESTIONSQUESTIONS

DISCUSSIONDISCUSSIONand and

QUESTIONSQUESTIONS

Top Related