Languages

Pages

Legal

Mandatory IFRS Adoption and Accounting Conservatism

Bin Ke,1 Danqing Young2 and Zili Zhuang3

June 28, 2013

We wish to thank Charles Hsu, and workshop participants at xxx for helpful comments. 1 Division of Accounting, Nanyang Business School, Nanyang Technological University, S3-01b-39, 50 Nanyang Avenue, Singapore 639798.Tel: +65 6790 4832. Fax: +65 6791 3697. Email: [email protected]. 2 School of Accountancy, Chinese University of Hong Kong, Shatin, Hong Kong. Tel: +852 3943 7892. Fax: +852 2603 5114. Email:[email protected]. 3 School of Accountancy, Chinese University of Hong Kong, Shatin, Hong Kong. Tel: +852 3943 7776. Fax: +852 2603 5114. Email:[email protected].

ABSTRACT Using a large sample of listed firms from 17 European countries that mandatorily adopted IFRS over the period 2005-2008, we examine the effect of mandatory IFRS adoption on accounting conservatism defined using Basu’s (1997) differential timeliness (DT) measure. An important distinction of our study is that we avoid the common criticisms of the DT measure by comparing the difference in the DT measure under local accounting standards and IFRS for the same firm in the same IFRS reconciliation year. We find no evidence that the mandatory IFRS adoption changes the degree of accounting conservatism for non-financial firms, independent of the firms’ countries of domicile. For financial firms domiciled in strong legal enforcement countries, we find some weak evidence that the mandatory IFRS adoption increases the degree of accounting conservatism. In contrast, for financial firms domiciled in weak legal enforcement countries, we find that the mandatory IFRS adoption results in a decrease in accounting conservatism. Key words: IFRS; conservatism JEL: M41, M48, G14, N20 Data Availability: Data used in this study are publicly available from the sources identified in the paper.

1

1. Introduction

The objective of this study is to examine how the mandatory adoption of

International Financial Reporting Standards (IFRS) affects accounting conservatism

defined using Basu’s (1997) differential timeliness (DT) measure. We test our research

question using the unique IFRS reconciliation data for a comprehensive sample of 2,591

unique firms from 17 European countries that mandatorily adopted IFRS over the

period 2005-2008.

Watts (2003a) defines accounting conservatism as the differential verifiability

required for recognition of profits versus losses. Watts (2003a) indicates that

conservatism has survived in accounting for many centuries and appears to have

increased in the last 30 years. Up to recently, the IASB’s and FASB’s conceptual

frameworks had regarded conservatism as one of the four principal qualitative

characteristics of financial statements. To the surprise of many, the new joint conceptual

framework of the IASB and FASB adopted in September 2010 does not include

conservatism as a desirable quality of financial reporting information (IASB 2010) and

instead considers “faithful representation” as a fundamental quality characteristic of

financial information, which implies a focus on completeness, neutrality, and freedom

from errors.

The shift in the stand of the IASB and FASB has generated a lot of discussions

and controversies due to the widespread mandatory adoption of IFRS around the world

and the fact that many requirements in IFRS differ from those in local standards for

many IFRS adopting countries. Critics argue that the mandatory adoption of IFRS

2

reduces accounting conservatism and ultimately accounting quality for several reasons.

First, Watts (2003a, 2003b) argues that the observed accounting conservatism in many

countries’ local accounting standards is a result of important economic forces such as

contracting and shareholder litigation. It is believed that IFRS’ extensive use of fair

value accounting reduces accounting conservatism and thus the usefulness of

accounting information to investors.

However, it is far from clear whether all the fair value accounting rules under

IFRS will result in less conservative financial reporting relative to local accounting

standards. For example, IFRS2 requires the expensing of employee stock options when

they are granted. This rule could result in more conservative earnings because, except

for UK and Ireland, all the other European countries in our sample did not require the

expensing of stock options prior to the IFRS adoption. Likewise, IAS39 requires firms to

recognize the fair value of derivatives on the balance sheet and the change in the fair

value of derivatives in earnings. For firms operating in countries whose local

accounting standards didn’t require the fair value of derivatives to be recognized on the

balance sheet, the mandatory IFRS adoption could lead to more conservative financial

reporting.

Second, critics claim that as principles-based standards, IFRS inherently lack

detailed implementation guidance and thus afford managers greater flexibility

(Langmead and Soroosh 2009). Nelson et al. (2002) show in a survey of Big 5 U.S. audit

firms that audit partners and managers are less likely to require adjustments to clients’

earnings management attempts when dealing with less precise or relatively looser

3

standards. Hence, there is a risk that the mandatory adoption of IFRS could lead to

more aggressive financial reporting.

However, EU regulators were aware of such risks and passed some new

regulations to facilitate the mandatory adoption of IFRS. For example, the Transparency

Directive was passed in December 2004 which focuses on enforcement mechanisms to

ensure public companies to have appropriate level of transparency to investors. Such

new regulations may reduce managers’ incentives to use principles-based IFRS to

manipulate reported earnings. Therefore, it is an empirical question how mandatory

IFRS adoption affects accounting conservatism.

Three studies (Piot et al. 2011; Andre et al. 2012; Ahmed et al. 2012) have

examined the effect of mandatory IFRS adoption on accounting conservatism. All three

studies use Basu’s (1997) DT measure as one of the proxies for accounting conservatism.

The sample of mandatory IFRS adopters used by both Piot et al. and Andre et al. are all

European firms while close to 90 percent of the mandatory IFRS adopters used by

Ahmed et al. are European firms. A common feature of the three studies’ research

design is that they examine the change in accounting conservatism in the period before

versus the period after the mandatory IFRS adoption (i.e., an inter-temporal approach).

All three studies find evidence of a decline in accounting conservatism after the

mandatory IFRS adoption.

However, as noted by Barth et al. (2011), a limitation of the inter-temporal

approach is that any observed changes in conservatism after the mandatory IFRS

adoption could be due to competing explanations such as concurrent changes in a

4

firm’s economic environment. For example, Christensen et al. (2012) find that

concurrent enforcement changes around the IFRS mandate partially explain the capital

market effects of mandatory IFRS adoption.

The inter-temporal approach’s limitation is especially relevant to the DT measure

because Givoly et al. (2007) show that certain time-variant characteristics of a firm’s

information environment unrelated to conservatism, including the degree of uniformity

in the content of the news during the examined period, the types of events occurring in

the period, and the firm’s disclosure policy, can affect the DT measure. Dietrich et al.

(2007) show more generally that the DT measure suffers from significant biases such

that empirical results could falsely indicate evidence of conservatism even in the

absence of asymmetric timeliness in reported earnings.1

In this study we assess the effect of mandatory IFRS adoption on accounting

conservatism using an alternative approach that does not suffer from the same

limitation as the inter-temporal approach. Specifically, we compare the degree of

accounting conservatism measured using the DT measure under two different sets of

accounting standards, local accounting standards versus IFRS, for the same firm years.

This is made possible because IFRS 1 First-time Adoption of International Financial

Reporting Standards (IASB 2003) requires that when a firm adopts IFRS, it must provide

1 Patatoukas and Thomas (2011) further show that two time-variant empirical regularities, related to scale, combine to cause a bias in the DT measure. Patatoukas and Thomas (2011) advise researchers to avoid using the DT measure. However, Ball et al. (2013) argue that the DT measure is a valid measure of accounting conservatism. Ball et al. show that the scale effects identified by Patatoukas and Thomas (2011) are merely a correlated omitted variable problem and can be easily dealt in a straightforward fashion such as using fixed effects regression. Our research design can also mitigate the bias noted by Pataoukas and Thomas because we compare the DT measure under local standards versus under IFRS for the same firm year.

5

a reconciliation of net income based on local standards to that based on IFRS for the last

year the firm applied local standards (denoted as the reconciliation year). Because our

research design holds constant all the other aspects of a firm’s institutional environment,

any difference in the DT measure across the two sets of accounting standards is likely

attributed to the mandatory IFRS adoption.

Following Barth et al. (2011), we analyze non-financial firms and financial firms

separately because firms in these two major industry groups differ in asset and income

composition, and therefore are affected differently by differences between IFRS and

local accounting standards. For example, IFRS’ extensive use of fair value accounting is

expected to have a greater impact on financial firms than on non-financial firms. Prior

research indicates that legal enforcement matters in the credible implementation of IFRS

(Daske et al. 2008; Li 2010). Hence, we further decompose our sample firms into those

domiciled in strong legal enforcement countries and those domiciled in weak legal

enforcement countries.

For non-financial firms, we find no evidence of a significance difference (increase

or decrease) in the DT measure under local standards and IFRS for either strong legal

enforcement countries or weak legal enforcement countries. For financial firms

domiciled in strong legal enforcement countries, we find no evidence of a significant

decrease in the DT measure after the mandatory IFRS adoption as reported in the prior

literature. Instead, there is some evidence of a significant increase in the DT measure

after the mandatory IFRS adoption. In contrast, for financial firms domiciled in weak

legal enforcement countries, we find evidence that the mandatory IFRS adoption

6

reduces accounting conservatism. However, this latter result should be interpreted with

caution due to the small sample size.

We also examine how the mandatory IFRS adoption affects the timeliness in the

recognition of good news and bad news separately. We find little evidence that the

mandatory IFRS adoption results in significant changes in the recognition of good news

and bad news for non-financial firms. For financial firms domiciled in strong legal

enforcement countries, we find that the recognition of both good news and bad news

becomes more timely under IFRS than under local standards. In contrast, for financial

firms domiciled in weak legal enforcement countries, we find that the recognition of

bad news becomes less timely under IFRS than under local standards; but there is no

evidence of a significant change in the recognition of good news under IFRS versus

under local standards.

Overall, the difference in the results (both the DT measure and the timeliness in

the recognition of good news and bad news separately) between non-financial firms

and financial firms may not be too surprising because IFRS’ extensive use of fair value

accounting is expected to have a greater impact on financial firms. The difference in the

results for financial firms domiciled in strong versus weak legal enforcement countries

suggests that the mandatory IFRS adoption can improve financial firms’ timeliness in

the recognition of both good news and bad news without sacrificing accounting

conservatism, provided that the implementation of the mandatory IFRS adoption is

subject to strong legal enforcement.

7

Our findings on accounting conservatism based on the DT measure are

inconsistent with those from Piot et al. (2011), Andre et al. (2012), and Ahmed et al.

(2012) and provide timely information to the ongoing debate on the economic

consequences of mandatory IFRS adoption.

The rest of the paper is organized as follows. Section 2 discusses the institutional

background and sample selection procedures. Section 3 presents the research design.

Section 4 reports the regression results. Section 5 concludes.

2. Institutional Background and Sample Selection Procedures

Mandatory IFRS adopters are required to follow the procedures described in

IFRS 1 when adopting IFRS for the first time. For firms adopting IFRS in 2005, IFRS 1

requires presentation of statements of financial position for fiscal years ending 2003,

2004, and 2005, and statements of comprehensive income for 2004 and 2005. In making

the transition from local standards to IFRS, firms must (1) derecognize assets and

liabilities recognized in accordance with local standards but not IFRS, (2) recognize

assets and liabilities that are recognized in accordance with IFRS but not local standards,

(3) reclassify amounts following the requirements of IFRS, e.g., reclassifying a financial

instrument as a liability that had previously been recognized as equity in accordance

with local standards, and (4) use measurement principles embodied in IFRS. In addition

and more relevant to our study, all mandatory IFRS adopting firms are required to

provide a reconciliation of the 2003 and 2004 statements of financial position and 2004

net income based on local standards to net income based on IFRS. In this study we take

8

advantage of the two net income figures provided by the mandatory reconciliation to

address our research question.

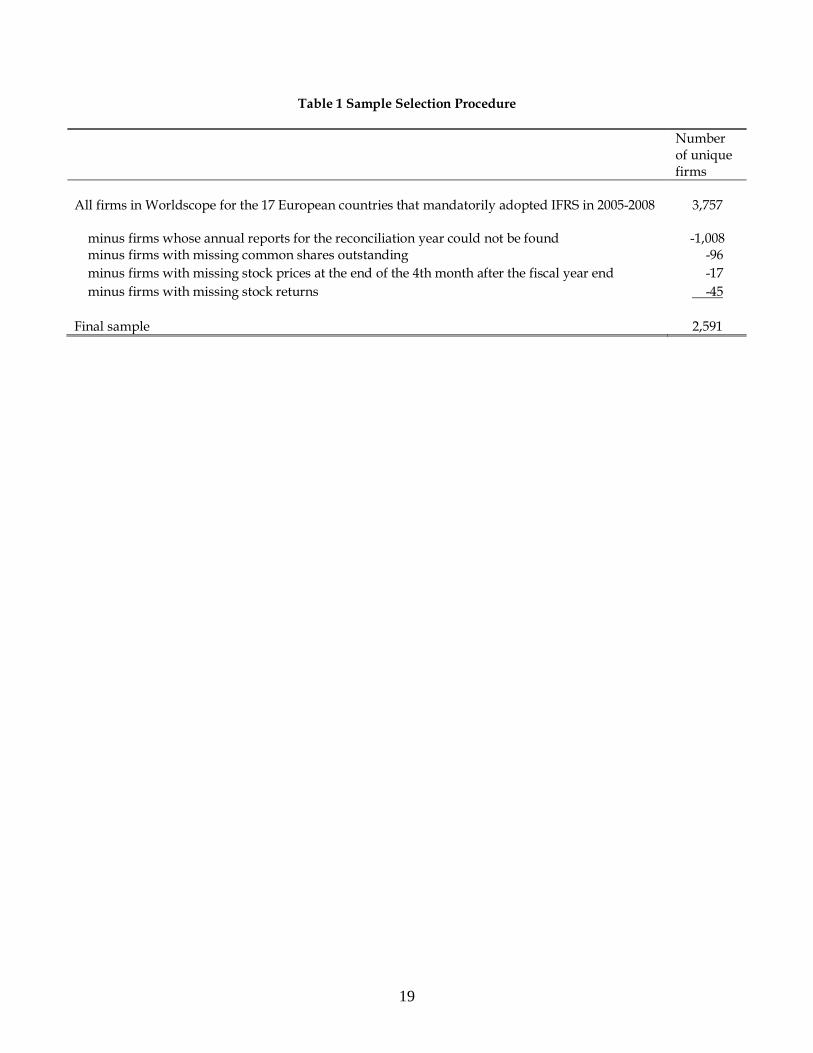

Table 1 shows the sample selection procedures. We started with the population

of 3,757 firms in Worldscope for the 17 European countries that mandatorily adopted

IFRS over the period 2005-2008. We were able to locate the annual reports and hand

collect from the annual reports the reported earnings under both local standards and

IFRS in the reconciliation year for 2,749 firms. After eliminating firms with missing

stock prices and the number of common shares outstanding, we obtain a final sample of

2,591 unique firms.

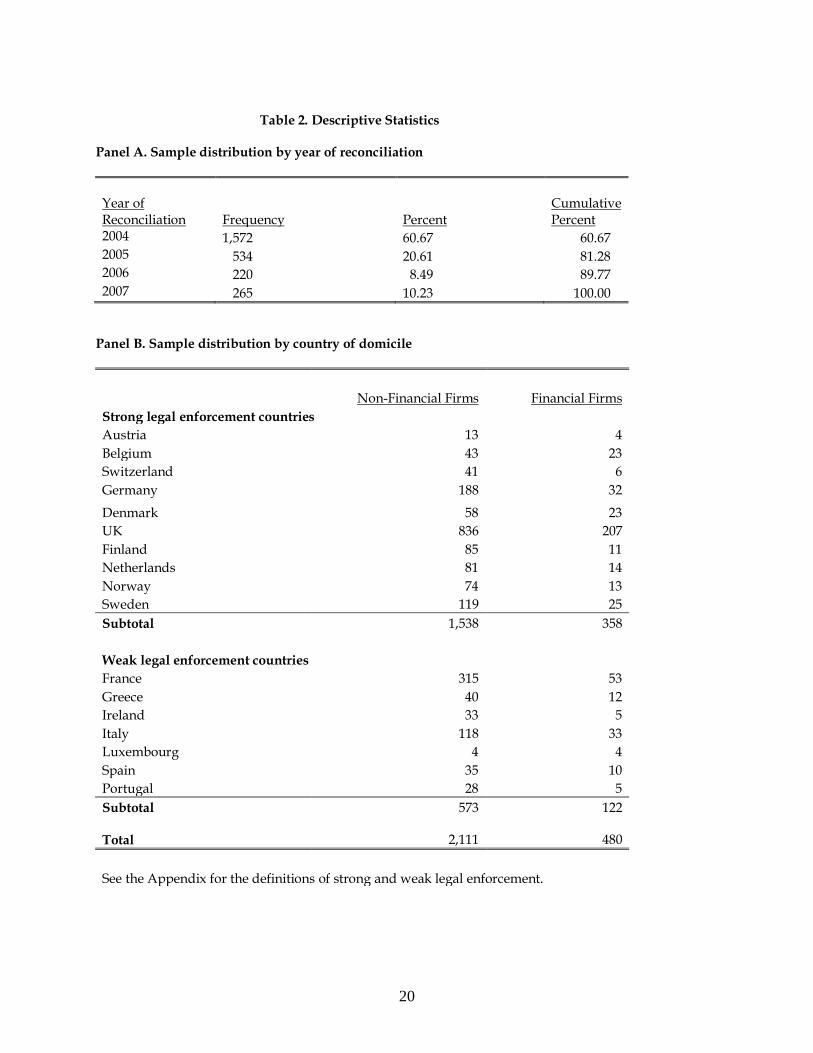

Table 2 shows the descriptive statistics for the final sample. Panel A reports the

distribution of the sample firms by the year of reconciliation. Most prior research

focuses on firms that mandatorily adopted IFRS in 2005 (reconciliation year is 2004).

However, as seen in Panel A, these firms represent only 60.67% of our sample. Panel B

shows the distribution of our sample firms by country for strong and weak legal

enforcement countries separately. DeFond and Hung (2004) show that it is the law

enforcement institutions rather than investor protection laws that matter to investor

protection. Hence, we classify the foreign countries in our sample into the weak and

strong investor protection groups by the median score of law enforcement ratings (7.72)

reported in La Porta et al. (1998).2

2 Luxembourg was not rated by La Porta et al. (1998) and thus is automatically assumed to belong to the weak investor protection country group. However, inferences are robust to treating Luxembourg as a strong investor protection country.

9

3. Research Design

We use the following standard cross-sectional regression model (Basu 1997) to

estimate the DT measure:

EPSit = β0 + β1Dit + β2Rit + β3Dit×Rit (1)

See the appendix for all the variable definitions. The dependent variable EPS refers to

either the EPS measured using local accounting standards (denoted as EPS_LOCAL) or

the EPS measured using IFRS (denoted as EPS_IFRS) in the reconciliation year. The

coefficient on R (β2) measures the degree of timeliness in good news recognition. The

sum of the coefficient on R and D×R measures the degree of timeliness in bad news

recognition. The coefficient on D×R (β3) represents the DT measure, i.e., the differential

timeliness in the recognition of bad news vs. good news. A positive coefficient on D×R

is often interpreted as evidence of accounting conservatism in the prior literature.

However, due to the ongoing debate on the interpretation of the coefficient on D×R

(Givoly et al. 2007; Dietrich et al. 2007; Patatoukas and Thomas 2011; Ball et al. 2013), we

refrain from interpreting the coefficient on D×R in its absolute term. Instead, we focus

on the difference in the coefficients on D×R under local accounting standards and IFRS.

If mandatory IFRS adoption results in reduced (increased) accounting conservatism, we

should expect the coefficient on D×R to be smaller (larger) when the dependent variable

is EPS_IFRS rather than EPS_LOCAL.

As noted in the Introduction, the impact of IFRS adoption could be different for

non-financial firms and financial firms and depend on the strength of a country’s legal

10

enforcement. Hence, we report all the regression results for non-financial firms and

financial firms across different legal enforcement regimes separately.

4. Regression Results

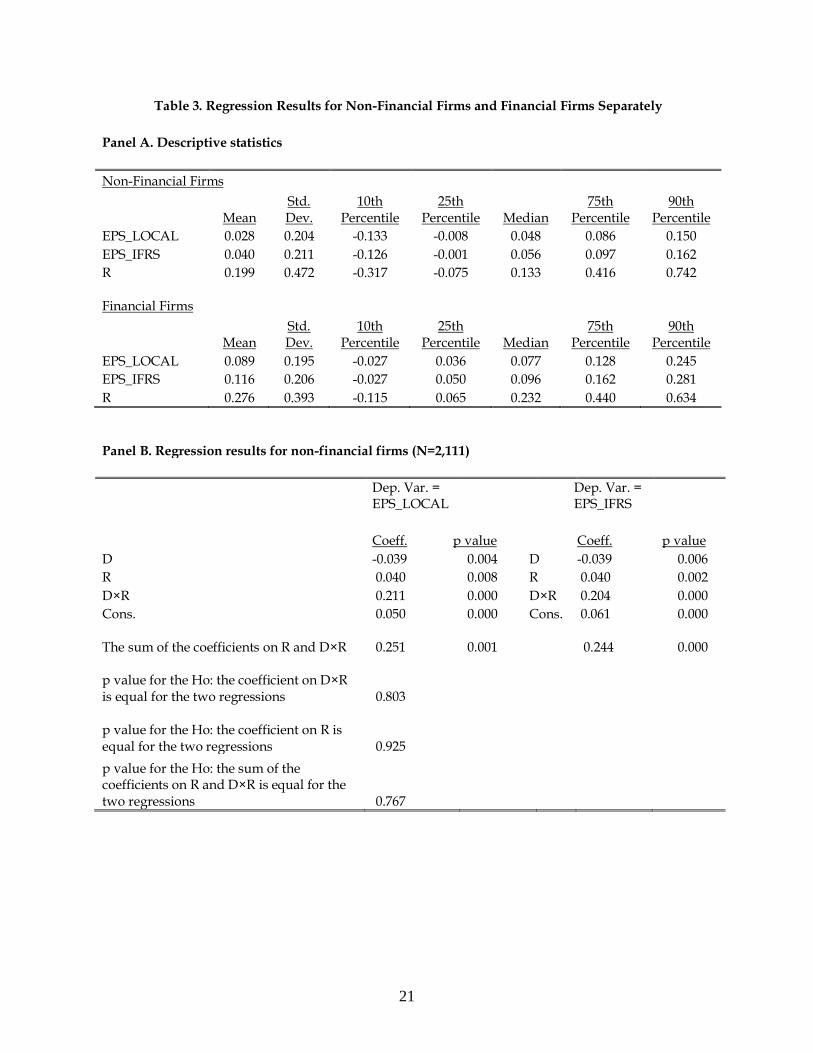

4.1. Regression Results for Non-Financial Firms and Financial Firms

To increase the test power, we first estimate model (1) for non-financial firms and

financial firms separately, without distinguishing the listed firms’ legal enforcement

regimes. Table 3 reports the regression results of model (1). Panel A shows the

descriptive statistics of the key regression variables EPS and R for non-financial firms

and financial firms separately. The mean (median) EPS in the reconciliation year is

significantly higher under IFRS than under local accounting standards for both non-

financial firms and financial firms (p<0.001).

Panel B shows the regression results of model (1) for non-financial firms. We find

that the coefficient on D×R is not significantly different under local accounting

standards versus under IFRS. Hence, there is no evidence that the mandatory IFRS

adoption results in any significant change in accounting conservatism for non-financial

firms. In addition, neither the coefficient on R nor the sum of the coefficients on R and

D×R is significantly different under local accounting standards versus under IFRS,

suggesting there is no difference in the timeliness of both good news and bad news

recognition across the two types of accounting standards.

Turning to financial firms in Panel C, we find that the coefficient on D×R is not

significantly different under local accounting standards versus IFRS, suggesting no

11

evidence that the mandatory IFRS adoption results in any significant change in

accounting conservatism for financial firms. However, we do notice that the coefficient

on R is significantly more positive under IFRS (p=0.042). In addition, the sum of the

coefficients on R and D×R is more positive under IFRS than under local accounting

standards though the two-tailed p value is only 0.179. Thus, there is weak evidence that

the mandatory IFRS adoption makes financial firms’ recognition of both good news and

bad news more timely without adversely affecting the degree of accounting

conservatism.

4.2. Change in Accounting Conservatism by Country’s Legal Enforcement Strength

Prior research suggests the impact of mandatory IFRS adoption on financial

reporting quality depends on the strength of a country’s legal enforcement. Therefore,

we further decompose the sample firms in Table 3 by the legal enforcement quality of

the firms’ countries of domicile. The results are shown in Table 4.

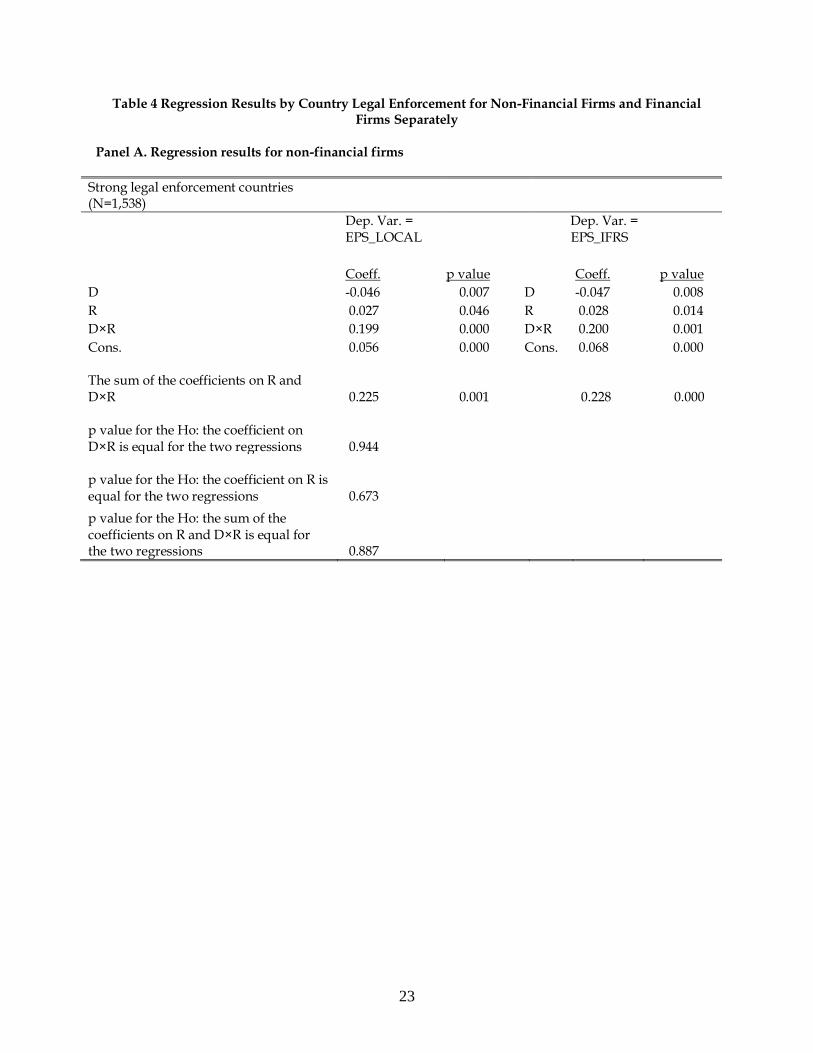

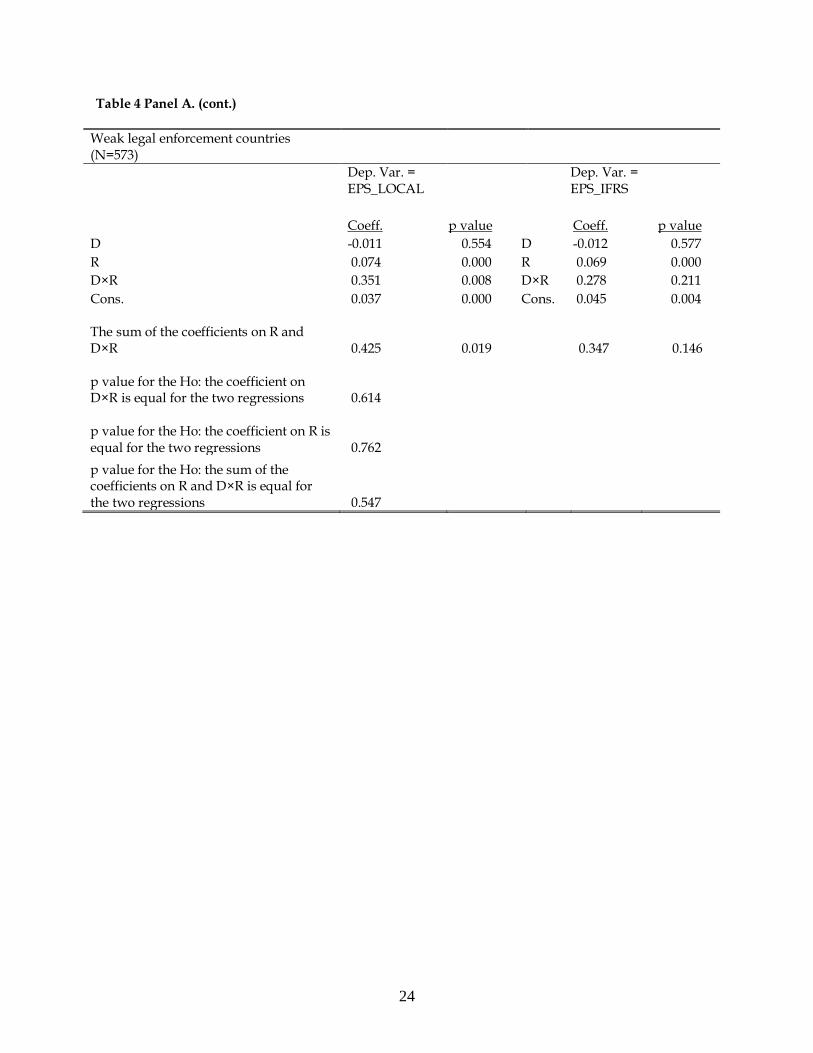

For non-financial firms (see Panel A of Table 4), the decomposition does not

significantly alter our inferences of Table 3. Specifically, for both strong and weak legal

enforcement firms, the coefficient on D×R continues to be insignificantly different under

local accounting standards versus under IFRS.

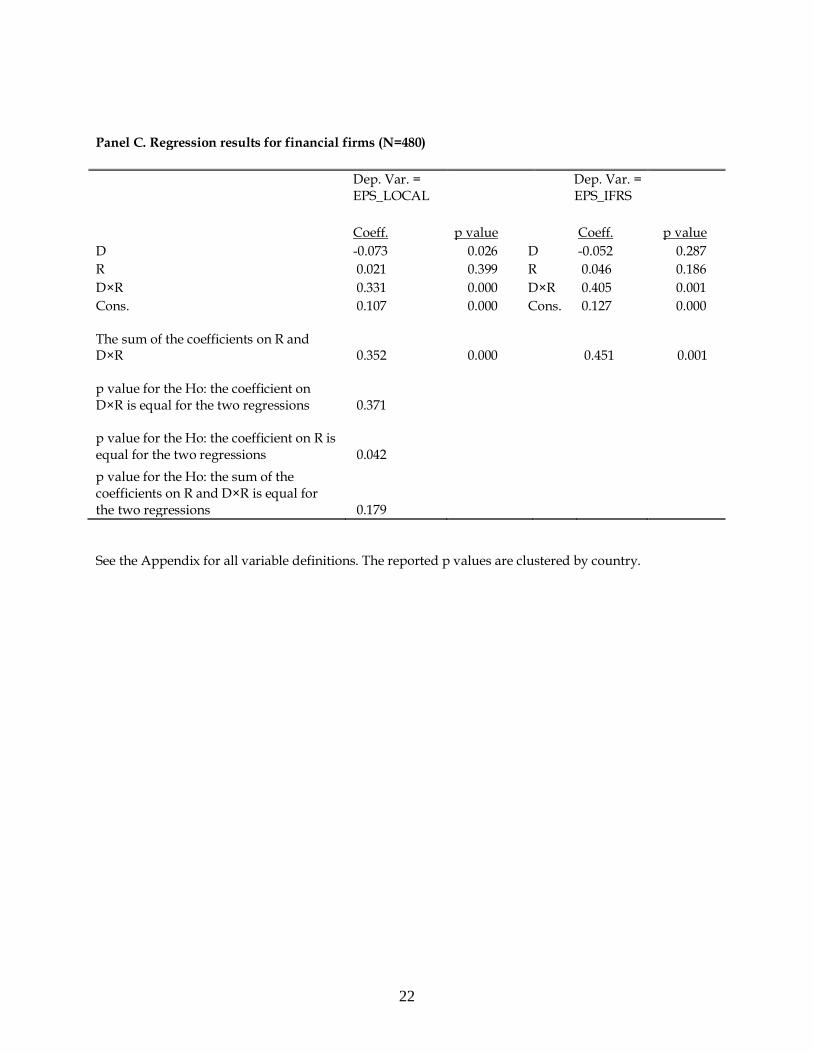

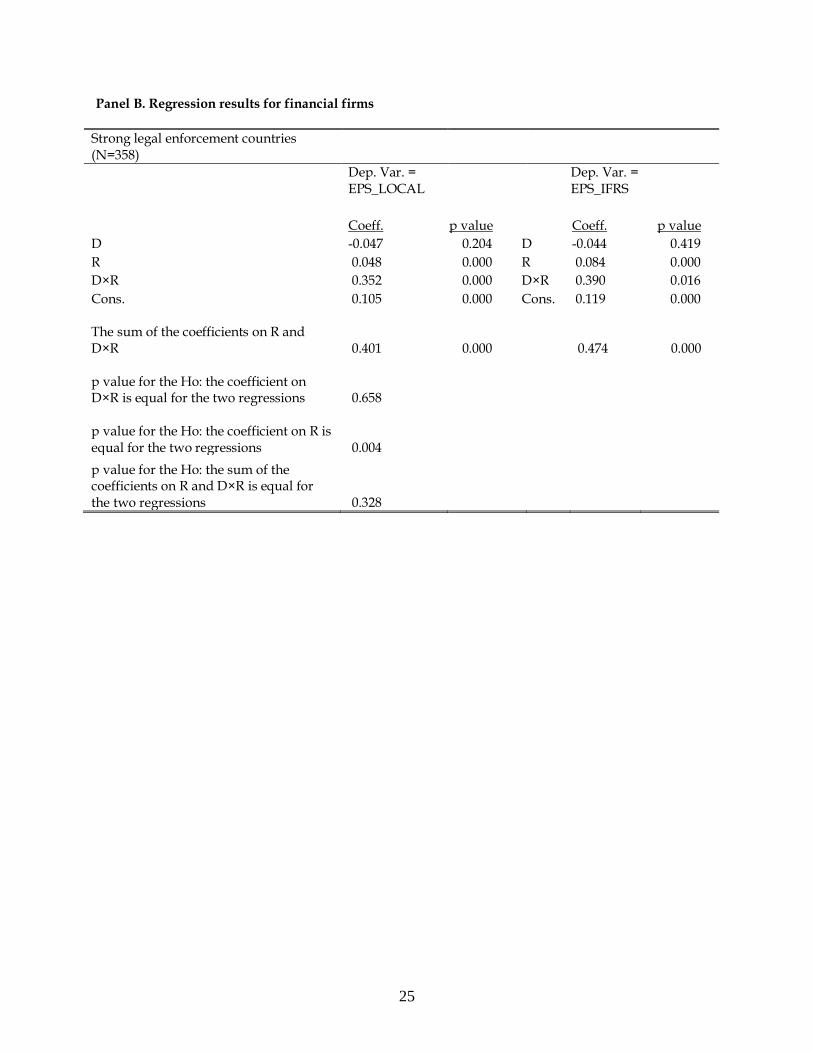

For financial firms, however, our inferences in Panel B of Table 4 change relative

to those in Table 3. For financial firms domiciled in strong legal enforcement countries,

we continue to find no evidence of a significant difference in accounting conservatism

under local accounting standards versus under IFRS. In addition, the coefficient on R

12

continues to be significantly larger under IFRS than under local accounting standards

(p=0.004) while the difference between the sums of the coefficients on R and D×R

remains insignificant, suggesting that the timeliness of the bad news recognition does

not change significantly under IFRS.

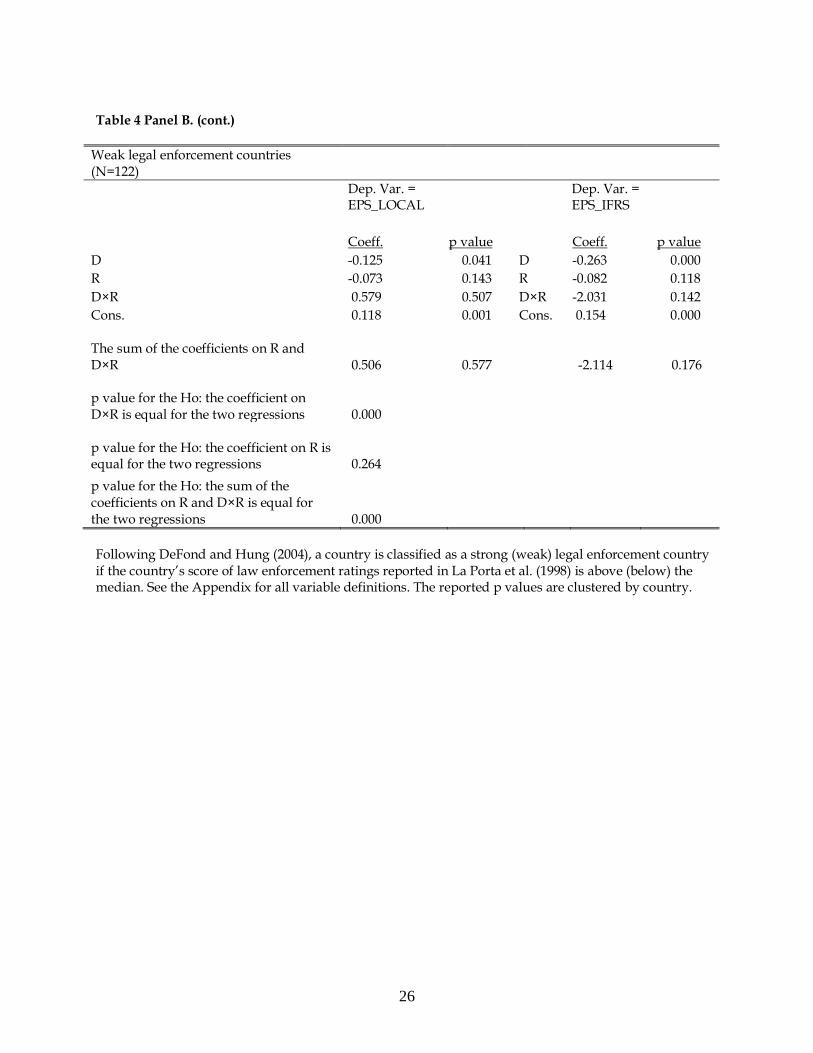

Turning to financial firms domiciled in weak legal enforcement countries, we

find that the coefficient on D×R is significantly smaller under IFRS than under local

accounting standards, suggesting that the degree of accounting conservatism declines

after the mandatory IFRS adoption for financial firms domiciled in weak legal

enforcement countries. This latter evidence is consistent with the concern of IFRS critics

that weak legal enforcement reduces the implementation credibility of mandatory IFRS

adoption, which in turn reduces the degree of accounting conservatism in reported

earnings. However, this result should be interpreted with caution due to the small

sample size (N=122). With regard to the timeliness of good news and bad news

recognition, we find that the coefficient on R is insignificantly different between local

accounting standards and IFRS, but the sum of the coefficients on R and D×R is

significantly smaller under IFRS than under local accounting standards. This latter

evidence suggests that the mandatory IFRS adoption in weak legal enforcement

countries reduces financial firms’ timeliness of bad news recognition.

4.3. The Differences between Local Accounting Standards and IFRS

The regression results reported in Tables 3 and 4 are based on the implicit

assumption that the mandatory IFRS adoption is an economically significant event for

13

the affected firms. However, this is unlikely to be true for the countries whose local

accounting standards were already fairly close to the IFRS prior to the mandatory

adoption. Accordingly, we follow Bae et al. (2008) by eliminating the countries whose

local standards don’t differ significantly from the IFRS. Specifically, Bae et al. (2008,

Table 1) manually code the differences between local standards and IFRS for 21 major

IAS items. We eliminate the following countries whose differences between local

standards and IFRS are no greater than 7 (i.e., one third of the 21 IAS items): UK,

Ireland, Netherlands, and Norway. With the exception of Ireland, all the deleted firms

belong to high legal enforcement countries.

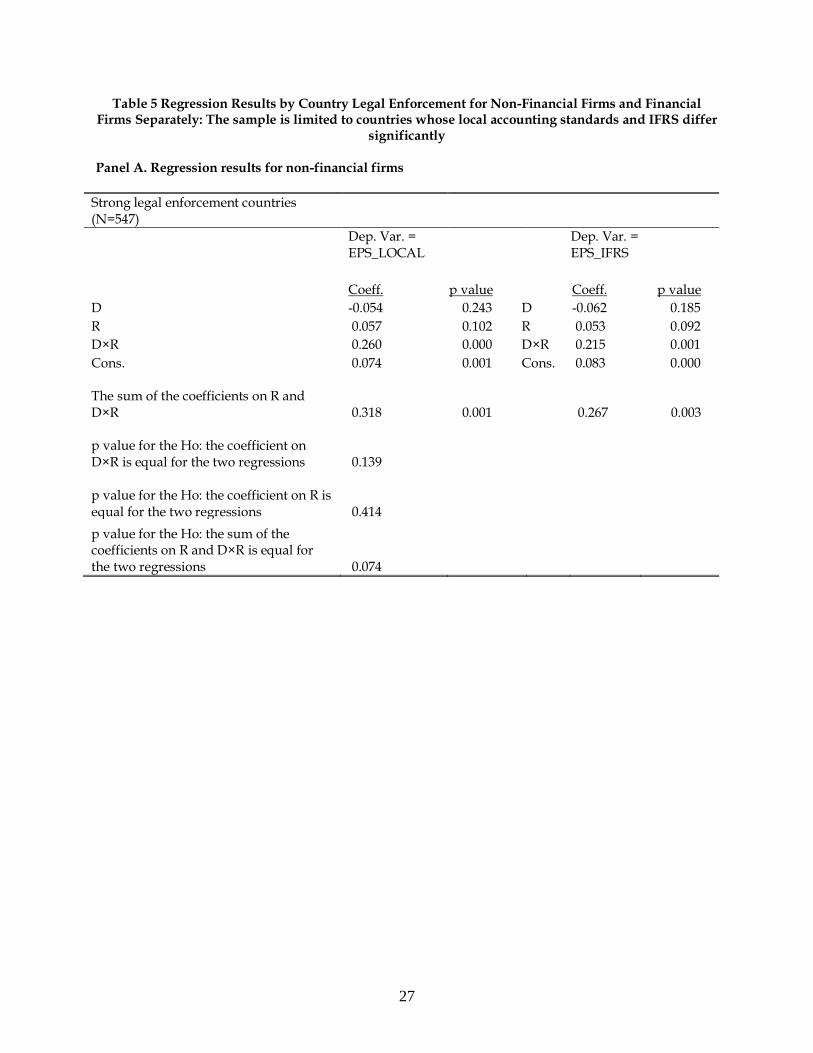

Table 5 shows the replication of the regression models in Table 4 using this

smaller sample. Focusing on the results for non-financial firms in Panel A, we continue

to find no evidence that the coefficient on D×R differs significantly under local

standards versus under IFRS for both strong legal enforcement countries and weak

legal enforcement countries. The only noticeable change relative to Table 4 is that the

sum of the coefficients on R and D×R is now smaller (i.e., less timely) under IFRS than

under local standards, but the difference is only marginally significant (p=0.074).

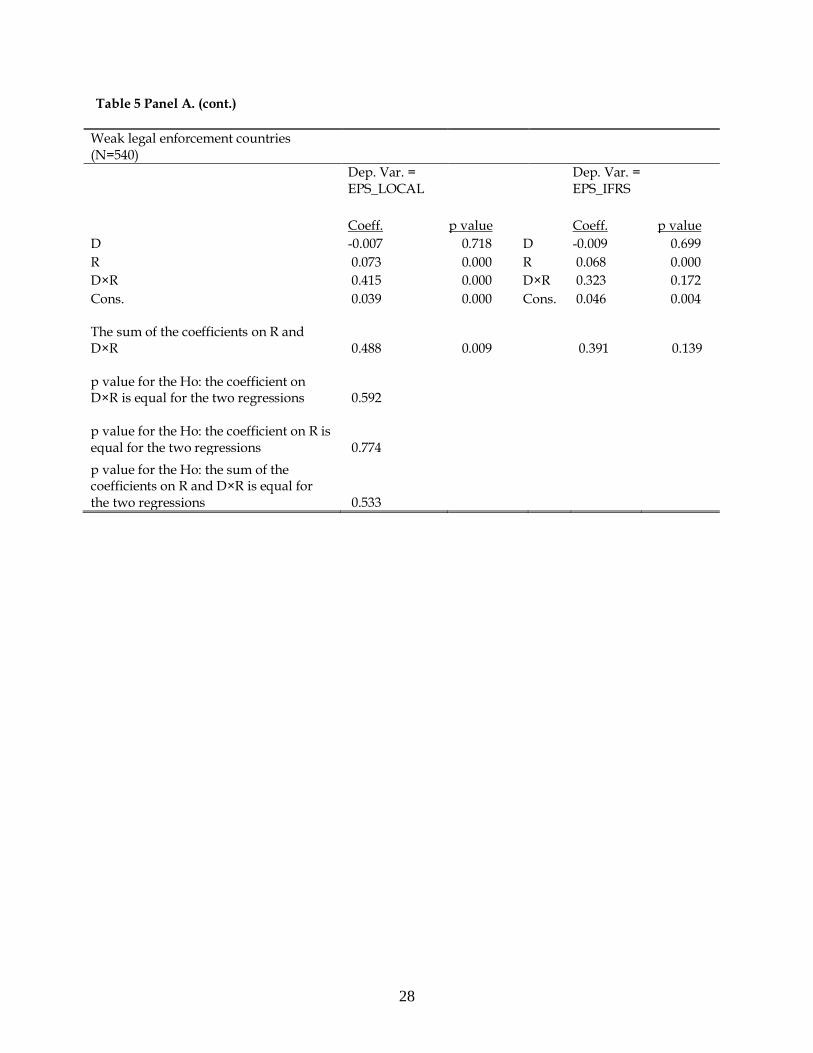

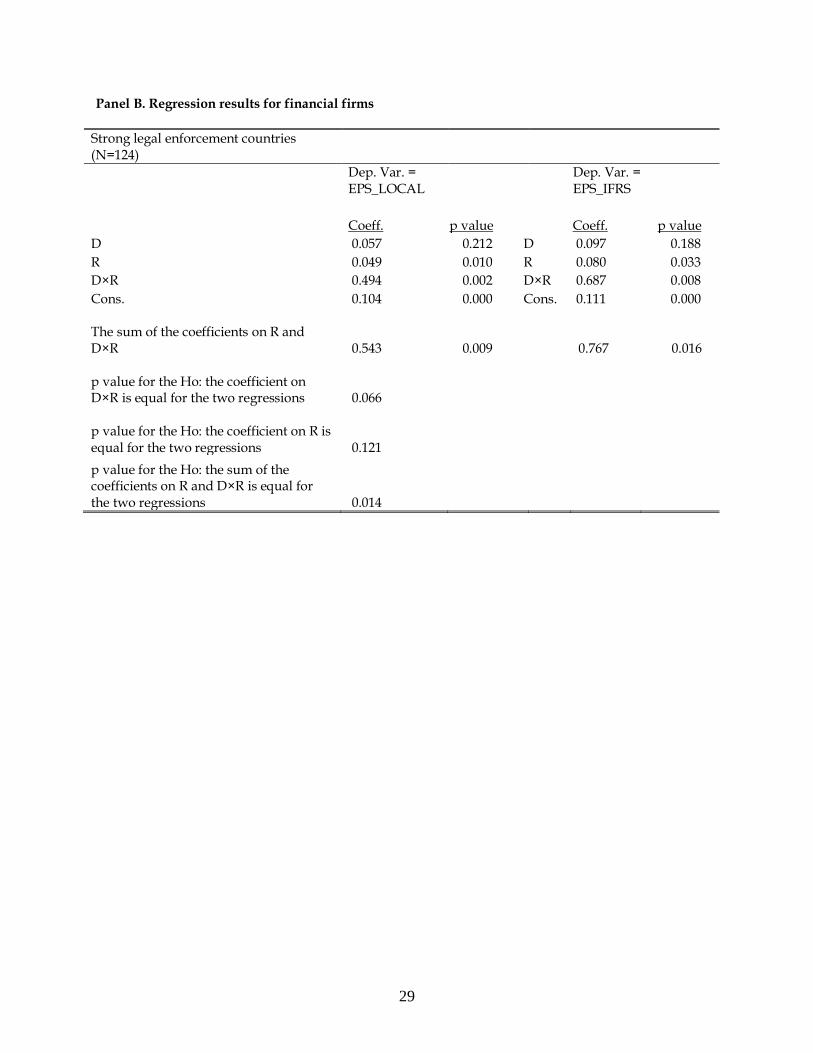

Turning to the results for financial firms in Panel B, we find that the coefficient

on D×R becomes marginally more positive under IFRS than under local standards for

financial firms domiciled in strong legal enforcement countries (p value=0.066). This

evidence suggests that the mandatory IFRS adoption results in an increase rather than a

decrease in conservatism for financial firms domiciled in strong legal enforcement

countries. This finding is contrary to the conventional wisdom. The reason for this

14

result lies in the fact that after the mandatory IFRS adoption the timeliness of bad news

recognition increases to a greater extent than the timeliness of good news recognition.

Specifically, the coefficient on R (good news) increases from 0.049 to 0.080 (p

value=0.121) while the sum of the coefficients on R and D×R (bad news) increases from

0.543 to 0.767 (p value=0.014). The increase in the timeliness of the bad news recognition

is significant (p value=0.014) while the increase in the timeliness of the good news

recognition is not (p value=0.121).

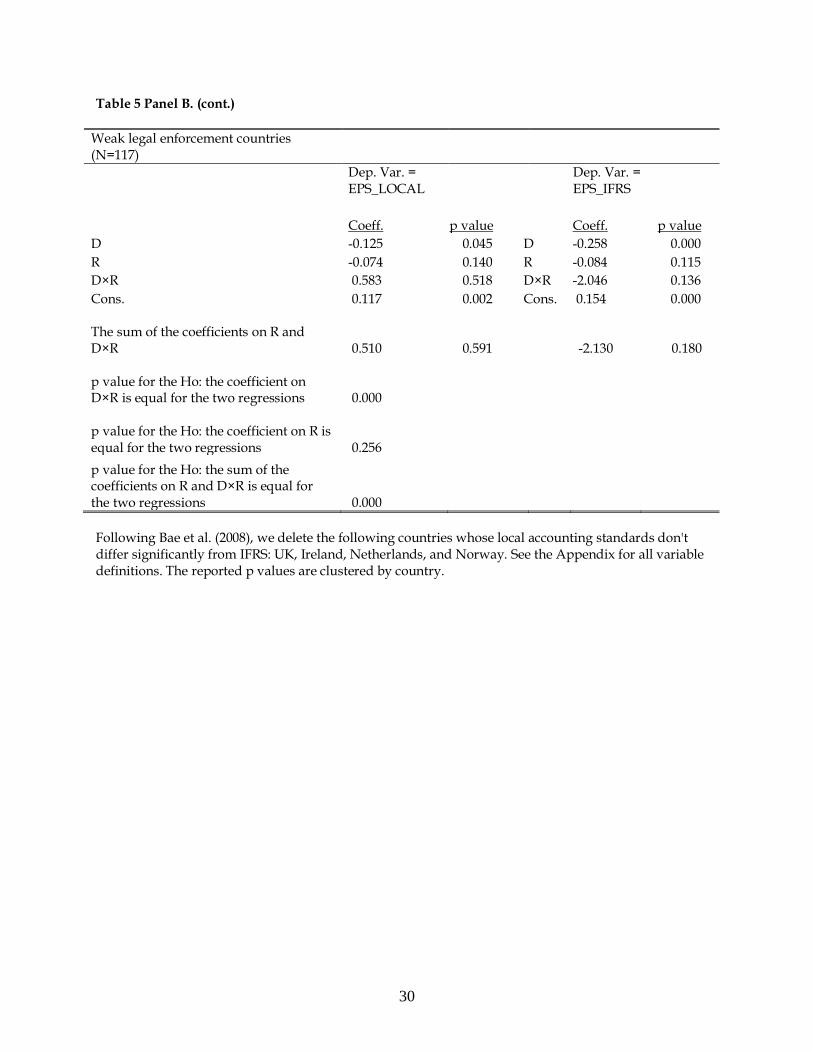

For financial firms domiciled in weak legal enforcement countries, the coefficient

on D×R continues to be smaller under IFRS than under local standards, and the

difference is statistically significant (p=0.000). In addition, we continue to observe a

significant difference in the sum of the coefficients on R and D×R (p =0.000). Similar to

Table 4, the decline of accounting conservatism under IFRS for firms domiciled in weak

legal enforcement countries is mainly driven by the decrease in the timeliness of

recognizing bad news under IFRS. Again, readers should exercise caution when

interpreting the results in Table 5 due to the small sample sizes.

5. Conclusion

The objective of this study is to examine the effect of mandatory IFRS adoption

on accounting conservatism defined using Basu’s (1997) differential timeliness (DT)

measure. We test our research question using a large sample of listed firms from 17

European countries that mandatorily adopted IFRS over the period 2005-2008. An

important distinction of our study is that there are two sets of net income figures

15

measured using local standards and IFRS for the same firm in the IFRS reconciliation

year. Hence, we able to avoid the common criticisms of Basu’s DT measure by holding

constant a firm’s institutional environment. For non-financial firms, we find little

evidence that the mandatory IFRS adoption results in significant changes in the degree

of accounting conservatism for firms domiciled either in strong legal enforcement

countries or weak legal enforcement countries. For financial firms, we find some weak

evidence that the mandatory IFRS adoption results in an increase in accounting

conservatism for firms domiciled in strong legal enforcement countries but we find a

significant decrease in accounting conservatism for firms domiciled in weak legal

enforcement countries.

Overall, our findings are contrary to the conventional wisdom that the

mandatory IFRS adoption would lead to a reduction in accounting conservatism. The

reason for this surprising finding is that the adoption of IFRS results in the increased

timeliness in both good news recognition and bad news recognition without affecting

the differential timeliness of bad news recognition versus good news recognition, which

is captured by Basu’s DT measure. Our results are inconsistent with several existing

studies that rely on an inter-temporal approach to assess the impact of mandatory IFRS

adoption on accounting conservatism using Basu’s DT measure. As our approach

doesn’t suffer from the common criticisms of the inter-temporal approach, the evidence

from our study suggests caution for future researchers who wish to use inter-temporal

approach to study the economic consequences of mandatory IFRS adoption.

16

REFERENCES

Ahmed, A.S., M.J. Neel, and D.D. Wang. 2012. Does mandatory adoption of IFRS improve accounting quality? Preliminary evidence. Contemporary Accounting Research, forthcoming.

Andre, Paul, and Andrei Filip. 2012. Accounting Conservatism in Europe and the Impact of Mandatory IFRS Adoption: Do country, institutional and legal differences survive? Working paper.

Bae, K-H., H. Tan, and M. Welker. 2008. International GAAP differences: The impact on foreign analysts. The Accounting Review 83: 593-628.

Ball, Ray, S.P. Kothari, and Valeri Nikolaev. 2013. On estimating conditional conservatism. The Accounting Review 88 (3): 755-787.

Barth, M. E., Landsman, W. R., Lang, M. H. 2008. International accounting standards and accounting quality. Journal of Accounting Research 46 (3): 467-498.

Barth, Mary E., Wayne R. Landsman, Danqing Young, and Zili Zhuang. 2011. Relevance of Differences between Net Income based on IFRS and Domestic Standards for European Firms. Working paper.

Basu, S. 1997. The conservatism principle and the asymmetric timeliness of earnings. Journal of Accounting and Economics 24: 3-37.

Christensen, Hans B., Luzi Hail, and Christian Leuz. 2012. Mandatory IFRS Reporting and Changes in Enforcement. Working paper.

Daske, H., L. Hail, C. Leuz, and R. Verdi. 2008. Mandatory IFRS reporting around the world: early evidence on the economic consequences. Journal of Accounting Research 46: 1085-1142.

Li, S. 2010. Does mandatory adoption of International Accounting Standards reduce the cost of equity capital? The Accounting Review 85: 607-636.

DeFond, M., Hung, M., 2004. Investor Protection and Corporate Governance: Evidence from Worldwide CEO Turnover. Journal of Accounting Research 42, 269-312.

Dietrich, D., K. Muller, and E. Riedl. 2007. Asymmetric timeliness tests of accounting conservatism. Review of Accounting Studies 12 (1): 95-124.

Givoly, D., C. Hayn, and A. Natarajan. 2007. Measuring reporting conservatism. The Accounting Review 82 (1): 65-106.

17

International Accounting Standards Board. 2003. Improvements to International Accounting Standards. IASB, London.

International Accounting Standards Board. 2010. Conceptual Framework for Financial Reporting – Project summary and feedback statement. September: http://www.ifrs.org/NR/rdonlyres/6A6ABF86-D554-4A77-9A4A-E415E09726B6/0/CFFeedbackStmt.pdf.

La Porta, R., F. Lopez-De-Silanes, A. Shleifer, and R. W. Vishny. 1998. Law and finance. Journal of Political Economy 106: 1113–55.

Langmead, J.M., and J. Soroosh. 2009. International financial reporting standards: The road ahead. CPA Journal 79 (3):16−24.

Nelson, M. W., Eliott, J. A., Tarpley, R. L. 2002. Evidence from auditors about managers' and auditors' earnings management decisions. The Accounting Review 77(supplement): 175-202.

Patatoukas, P. and J. Thomas. 2011. More evidence of bias in the differential timeliness measure of conditional conservatism.The Accounting Review 86 (5): 1765-1793.

Piot, C., P. Dumontier, and R. Janin. 2011. IFRS consequences on accounting conservatism within Europe: The role of Big 4. Working paper Université de Grenoble.

Watts, R.L. 2003a. Conservatism in accounting Part I: explanations and implications. Accounting Horizons 17: 207-221.

Watts, R.L. 2003b. Conservatism in accounting Part II: evidence and research opportunities. Accounting Horizons 17: 287-301.

18

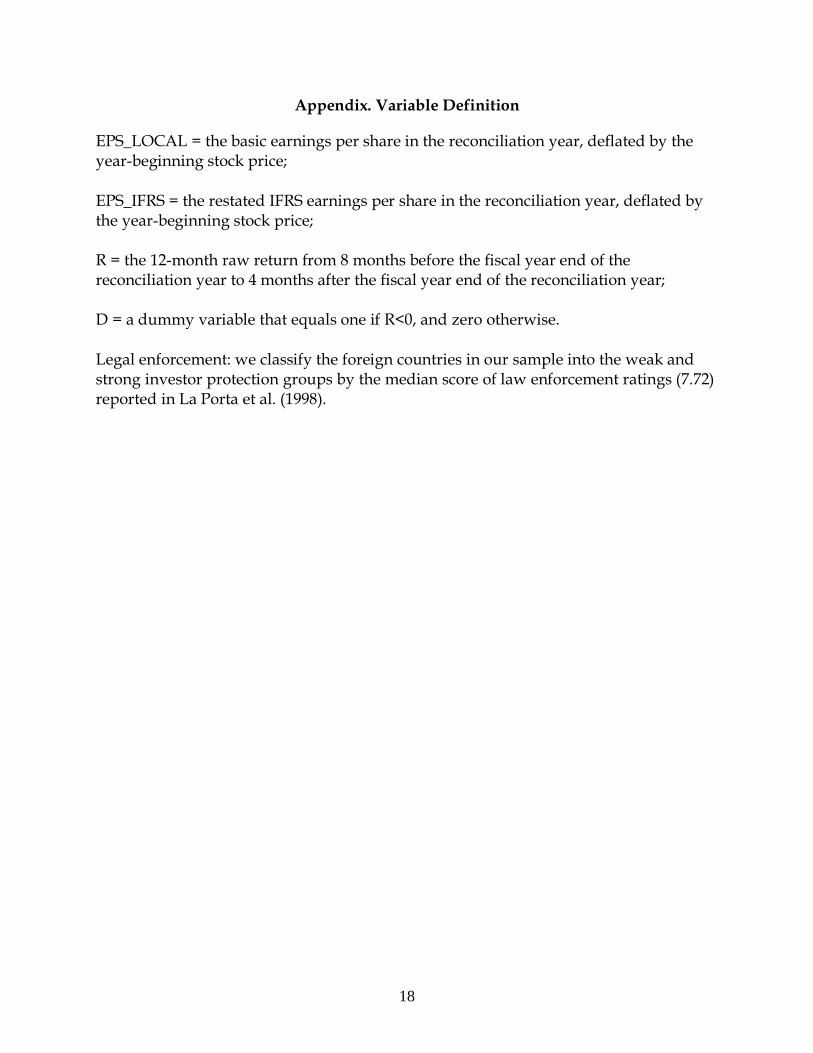

Appendix. Variable Definition

EPS_LOCAL = the basic earnings per share in the reconciliation year, deflated by the year-beginning stock price; EPS_IFRS = the restated IFRS earnings per share in the reconciliation year, deflated by the year-beginning stock price; R = the 12-month raw return from 8 months before the fiscal year end of the reconciliation year to 4 months after the fiscal year end of the reconciliation year; D = a dummy variable that equals one if R<0, and zero otherwise. Legal enforcement: we classify the foreign countries in our sample into the weak and strong investor protection groups by the median score of law enforcement ratings (7.72) reported in La Porta et al. (1998).

19

Table 1 Sample Selection Procedure

Number of unique firms

All firms in Worldscope for the 17 European countries that mandatorily adopted IFRS in 2005-2008

3,757

minus firms whose annual reports for the reconciliation year could not be found

-1,008

minus firms with missing common shares outstanding -96 minus firms with missing stock prices at the end of the 4th month after the fiscal year end -17 minus firms with missing stock returns -45 Final sample

2,591

20

Table 2. Descriptive Statistics

Panel A. Sample distribution by year of reconciliation Year of Reconciliation Frequency Percent

Cumulative Percent

2004 1,572 60.67 60.67 2005 534 20.61 81.28 2006 220 8.49 89.77 2007 265 10.23 100.00

Panel B. Sample distribution by country of domicile

Non-Financial Firms Financial Firms Strong legal enforcement countries Austria 13 4 Belgium 43 23 Switzerland 41 6 Germany 188 32

Denmark 58 23 UK 836 207 Finland 85 11 Netherlands 81 14 Norway 74 13 Sweden 119 25 Subtotal 1,538 358

Weak legal enforcement countries France 315 53 Greece 40 12 Ireland 33 5 Italy 118 33 Luxembourg 4 4 Spain 35 10 Portugal 28 5 Subtotal 573 122 Total 2,111 480

See the Appendix for the definitions of strong and weak legal enforcement.

21

Table 3. Regression Results for Non-Financial Firms and Financial Firms Separately

Panel A. Descriptive statistics

Non-Financial Firms

Mean Std. Dev.

10th Percentile

25th Percentile Median

75th Percentile

90th Percentile

EPS_LOCAL 0.028 0.204 -0.133 -0.008 0.048 0.086 0.150 EPS_IFRS 0.040 0.211 -0.126 -0.001 0.056 0.097 0.162 R 0.199 0.472 -0.317 -0.075 0.133 0.416 0.742 Financial Firms

Mean Std. Dev.

10th Percentile

25th Percentile Median

75th Percentile

90th Percentile

EPS_LOCAL 0.089 0.195 -0.027 0.036 0.077 0.128 0.245 EPS_IFRS 0.116 0.206 -0.027 0.050 0.096 0.162 0.281 R 0.276 0.393 -0.115 0.065 0.232 0.440 0.634

Panel B. Regression results for non-financial firms (N=2,111)

Dep. Var. = EPS_LOCAL

Dep. Var. = EPS_IFRS

Coeff. p value Coeff. p value D -0.039 0.004 D -0.039 0.006 R 0.040 0.008 R 0.040 0.002 D×R 0.211 0.000 D×R 0.204 0.000 Cons. 0.050 0.000 Cons. 0.061 0.000 The sum of the coefficients on R and D×R 0.251 0.001

0.244 0.000

p value for the Ho: the coefficient on D×R is equal for the two regressions 0.803

p value for the Ho: the coefficient on R is equal for the two regressions 0.925

p value for the Ho: the sum of the coefficients on R and D×R is equal for the two regressions 0.767

22

Panel C. Regression results for financial firms (N=480)

Dep. Var. = EPS_LOCAL

Dep. Var. = EPS_IFRS

Coeff. p value Coeff. p value D -0.073 0.026 D -0.052 0.287 R 0.021 0.399 R 0.046 0.186 D×R 0.331 0.000 D×R 0.405 0.001 Cons. 0.107 0.000 Cons. 0.127 0.000 The sum of the coefficients on R and D×R 0.352 0.000

0.451 0.001

p value for the Ho: the coefficient on D×R is equal for the two regressions 0.371

p value for the Ho: the coefficient on R is equal for the two regressions 0.042

p value for the Ho: the sum of the coefficients on R and D×R is equal for the two regressions 0.179

See the Appendix for all variable definitions. The reported p values are clustered by country.

23

Table 4 Regression Results by Country Legal Enforcement for Non-Financial Firms and Financial Firms Separately

Panel A. Regression results for non-financial firms

Strong legal enforcement countries (N=1,538)

Dep. Var. = EPS_LOCAL

Dep. Var. = EPS_IFRS

Coeff. p value Coeff. p value D -0.046 0.007 D -0.047 0.008 R 0.027 0.046 R 0.028 0.014 D×R 0.199 0.000 D×R 0.200 0.001 Cons. 0.056 0.000 Cons. 0.068 0.000 The sum of the coefficients on R and D×R 0.225 0.001

0.228 0.000

p value for the Ho: the coefficient on D×R is equal for the two regressions 0.944

p value for the Ho: the coefficient on R is equal for the two regressions 0.673

p value for the Ho: the sum of the coefficients on R and D×R is equal for the two regressions 0.887

24

Table 4 Panel A. (cont.)

Weak legal enforcement countries (N=573)

Dep. Var. = EPS_LOCAL

Dep. Var. = EPS_IFRS

Coeff. p value Coeff. p value D -0.011 0.554 D -0.012 0.577 R 0.074 0.000 R 0.069 0.000 D×R 0.351 0.008 D×R 0.278 0.211 Cons. 0.037 0.000 Cons. 0.045 0.004 The sum of the coefficients on R and D×R 0.425 0.019

0.347 0.146

p value for the Ho: the coefficient on D×R is equal for the two regressions 0.614

p value for the Ho: the coefficient on R is equal for the two regressions 0.762

p value for the Ho: the sum of the coefficients on R and D×R is equal for the two regressions 0.547

25

Panel B. Regression results for financial firms

Strong legal enforcement countries (N=358)

Dep. Var. = EPS_LOCAL

Dep. Var. = EPS_IFRS

Coeff. p value Coeff. p value D -0.047 0.204 D -0.044 0.419 R 0.048 0.000 R 0.084 0.000 D×R 0.352 0.000 D×R 0.390 0.016 Cons. 0.105 0.000 Cons. 0.119 0.000 The sum of the coefficients on R and D×R 0.401 0.000

0.474 0.000

p value for the Ho: the coefficient on D×R is equal for the two regressions 0.658

p value for the Ho: the coefficient on R is equal for the two regressions 0.004

p value for the Ho: the sum of the coefficients on R and D×R is equal for the two regressions 0.328

26

Table 4 Panel B. (cont.)

Weak legal enforcement countries (N=122)

Dep. Var. = EPS_LOCAL

Dep. Var. = EPS_IFRS

Coeff. p value Coeff. p value D -0.125 0.041 D -0.263 0.000 R -0.073 0.143 R -0.082 0.118 D×R 0.579 0.507 D×R -2.031 0.142 Cons. 0.118 0.001 Cons. 0.154 0.000 The sum of the coefficients on R and D×R 0.506 0.577

-2.114 0.176

p value for the Ho: the coefficient on D×R is equal for the two regressions 0.000

p value for the Ho: the coefficient on R is equal for the two regressions 0.264

p value for the Ho: the sum of the coefficients on R and D×R is equal for the two regressions 0.000 Following DeFond and Hung (2004), a country is classified as a strong (weak) legal enforcement country if the country’s score of law enforcement ratings reported in La Porta et al. (1998) is above (below) the median. See the Appendix for all variable definitions. The reported p values are clustered by country.

27

Table 5 Regression Results by Country Legal Enforcement for Non-Financial Firms and Financial Firms Separately: The sample is limited to countries whose local accounting standards and IFRS differ

significantly Panel A. Regression results for non-financial firms

Strong legal enforcement countries (N=547)

Dep. Var. = EPS_LOCAL

Dep. Var. = EPS_IFRS

Coeff. p value Coeff. p value D -0.054 0.243 D -0.062 0.185 R 0.057 0.102 R 0.053 0.092 D×R 0.260 0.000 D×R 0.215 0.001 Cons. 0.074 0.001 Cons. 0.083 0.000 The sum of the coefficients on R and D×R 0.318 0.001

0.267 0.003

p value for the Ho: the coefficient on D×R is equal for the two regressions 0.139

p value for the Ho: the coefficient on R is equal for the two regressions 0.414

p value for the Ho: the sum of the coefficients on R and D×R is equal for the two regressions 0.074

28

Table 5 Panel A. (cont.)

Weak legal enforcement countries (N=540)

Dep. Var. = EPS_LOCAL

Dep. Var. = EPS_IFRS

Coeff. p value Coeff. p value D -0.007 0.718 D -0.009 0.699 R 0.073 0.000 R 0.068 0.000 D×R 0.415 0.000 D×R 0.323 0.172 Cons. 0.039 0.000 Cons. 0.046 0.004 The sum of the coefficients on R and D×R 0.488 0.009

0.391 0.139

p value for the Ho: the coefficient on D×R is equal for the two regressions 0.592

p value for the Ho: the coefficient on R is equal for the two regressions 0.774

p value for the Ho: the sum of the coefficients on R and D×R is equal for the two regressions 0.533

29

Panel B. Regression results for financial firms

Strong legal enforcement countries (N=124)

Dep. Var. = EPS_LOCAL

Dep. Var. = EPS_IFRS

Coeff. p value Coeff. p value D 0.057 0.212 D 0.097 0.188 R 0.049 0.010 R 0.080 0.033 D×R 0.494 0.002 D×R 0.687 0.008 Cons. 0.104 0.000 Cons. 0.111 0.000 The sum of the coefficients on R and D×R 0.543 0.009

0.767 0.016

p value for the Ho: the coefficient on D×R is equal for the two regressions 0.066

p value for the Ho: the coefficient on R is equal for the two regressions 0.121

p value for the Ho: the sum of the coefficients on R and D×R is equal for the two regressions 0.014

30

Table 5 Panel B. (cont.)

Weak legal enforcement countries (N=117)

Dep. Var. = EPS_LOCAL

Dep. Var. = EPS_IFRS

Coeff. p value Coeff. p value D -0.125 0.045 D -0.258 0.000 R -0.074 0.140 R -0.084 0.115 D×R 0.583 0.518 D×R -2.046 0.136 Cons. 0.117 0.002 Cons. 0.154 0.000 The sum of the coefficients on R and D×R 0.510 0.591

-2.130 0.180

p value for the Ho: the coefficient on D×R is equal for the two regressions 0.000

p value for the Ho: the coefficient on R is equal for the two regressions 0.256

p value for the Ho: the sum of the coefficients on R and D×R is equal for the two regressions 0.000 Following Bae et al. (2008), we delete the following countries whose local accounting standards don't differ significantly from IFRS: UK, Ireland, Netherlands, and Norway. See the Appendix for all variable definitions. The reported p values are clustered by country.

Top Related