Languages

Pages

Legal

By Farrukh QUreshi

Sources of the Shariah Framework of Islamic Finance Shariah, Fiqh & Mu’amalat Necessary Requirements of Islamic

Finance Riba, Gharar, Maysir & Others Essential Contracts in Islamic Finance Products and Instruments

2

Before explaining the concept “what is Islamic Banking & Finance” the elaboration of concept “why Islamic Banking” is very important.

Islam is a complete code of life that provides guidance regarding each as pect of life.

3

The primary objectives of Islamic Economic System are as under.

Equal Distribution of wealth Social justice

These objectives can never be achieved in Interest/Riba based economic systems.

4

“Islamic banking has been defined as banking in consonance with the ethos and value system of Islam and governed by the principles laid down by Islamic Sharia’h, in addition to the conventional good governance and risk management rules,”

5

6

Primary Sources

The Holy Quran

Sunnah (the sayings, deeds and endorsements of Prophet Muhammad PBUH)

7

QURAN

- Primary source for discerning the laws of God.

Example : « God has permitted trade and prohibited Riba »Reference : Surat Al Baqara verse 275

8

SUNNAHLiterally means : « Well-known path » - Words or Acts of the Prophet- - Sayings of the Prophet (SAW) used to lay down and

give moral guidance- Acts of the Prophet (SAW) which have a legal content

(ex: method of praying)- - Tacit approval (silence) of the Prophet (SAW) on the

action of one of his companions in his presence or in his knowledge

9

Secondary Sources IJMA’ (Consensus)

QIYAS (Analogy)

IJTIHAD (reasoning of a group of qualified scholars, which is aimed at adapting Islamic rules to the contemporary world)

10

IJMA’ (Consensus)- Literally means agreement on a matter- - In its technical sense, it means « the

consensus of the independant jurists from the Ummah of the Prophet Muhammad (SAW) after his death

- Example : Jurists have reached a consensus (Ijma) that the selling of goods by an party who doesn’t own the goods and without the approval of the goods’ owner is void.

11

QIYASLiterally means measuring or estimating one thing in terms

of another- Technically, it is the assignement of the legal rule of an

existing case found in the texts of the QURAN, the SUNNAH, or IJMA’ to a new case whose legal rule is not found in these sources.

- - Example : « Jurist looked into details of the prohibition of alcohol. After analysis, it was decided that the underlying reason is intoxication . Once this has been defined, the scholars would look at other liquids that intoxicate and extend the legal rule »

12

IJTIHADNumber of meaning of Ijtihad

- Islamic scholars take into account the customs of a place that adress a problem but are not offensive to Sharia

- - In some cases, Islamic Scholars develop their own preference from a solution to an apparently unique problem

- Fundamentaly, it is a personal exercise until other scholars are able to agree with the solution proposed by the innovator.

13

In general, the framework of Islamic finance is the same framework used by the conventional finance practices.

These frameworks are, inter alia legal and regulatory framework, taxation framework, accounting and auditing standards, etc.

Might have different or additional framework, such as accounting and auditing standard, etc, due to its peculiarity.

14

However, Islamic Finance, as the name suggests, has another framework, which is considered the major element that differentiates IBF from the conventional banking and finance.

Any violation of this framework will definitely effect the validity of Islamic finance itself.

Shariah Compliance Framework

15

Three main interrelated terminologies: Shariah, Fiqh & Muamalat

Shariah, when viewed from legal perspective is the fixed elements of Islamic law, i.e. what has been clearly stipulated and mentioned in the text. E.g. five time prayers, prohibition of riba’, etc.

As such, it is revealed in nature

16

Shariah, in this sense, is wide and encompassing various branches of Islam

Normally, it comes in its generality and it emphasizes only on the principles and not the detailed rules (not all the time)

It is the duty of the judge (qadi), mufti and jurisconsult (ulama’) to exert their intellectual efforts in deriving and applying these principles on certain given scenarios.

The result of human reasoning and understanding to the shariah is known as fiqh

Fixed v. Flexible Agreements v. Differences

17

However, in its general usage, it is called al-syariat al-Islamiyyah (Islamic law).

Islamic commercial law is one of the components of Islamic law

Other components of Islamic law include: Islamic law of purification and worship Islamic family law Islamic criminal law Islamic law of evidence and procedure Islamic law of inheritance, etc

The main subjects of Islamic commercial law are commercial contracts and the rules governing them

18

Conclusion of contract by mutual consent

The avoidance of riba’ The avoidance of gharar The avoidance of transactions involving

maysir (gambling) The avoidance of transactions involving

prohibited commodities19

WHAT TO BE AVOIDEDWHAT TO BE AVOIDED

Riba – prohibited in many Quranic verses and sayings of the Prophet s.a.w.

Meaning: riba is every excess in return of which no reward or equivalent counter value is paid, in short, every unjust enrichment is riba

20

Literally: excess, expand, increase, growth

Any unjustified excess above and over the capital, whether in loans (between creditor and debtor) or in trade (with similar commodities)

21

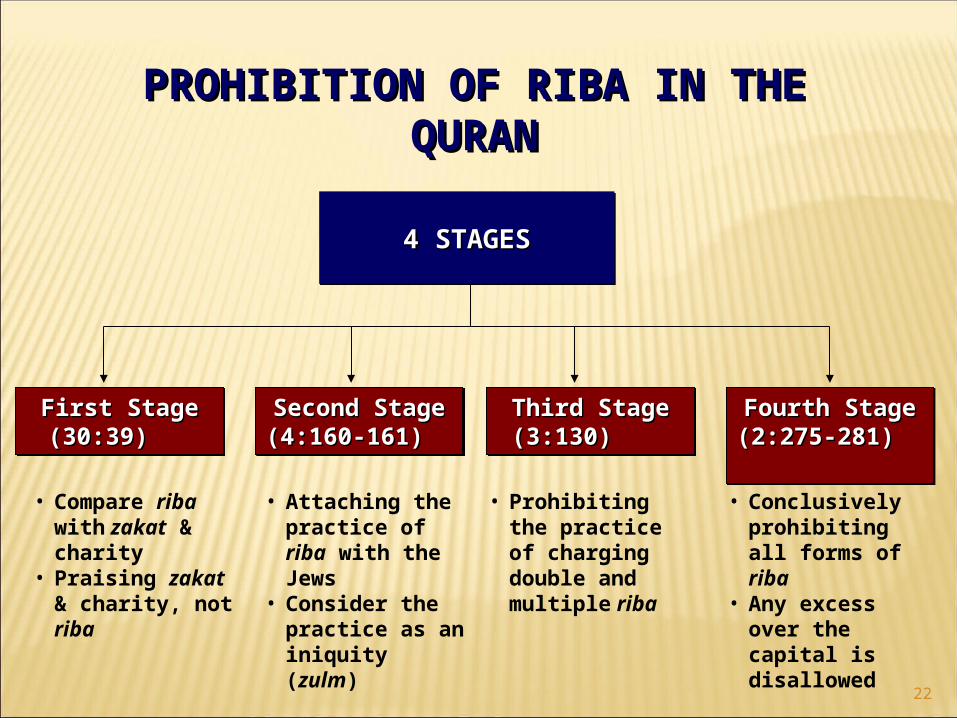

PROHIBITION OF RIBA IN THE PROHIBITION OF RIBA IN THE QURANQURAN

First StageFirst Stage (30:39) (30:39)

Second StageSecond Stage(4:160-161) (4:160-161)

Third StageThird Stage(3:130) (3:130)

Fourth StageFourth Stage(2:275-281) (2:275-281)

• Compare riba with zakat & charity

• Praising zakat & charity, not riba

• Attaching the practice of riba with the Jews

• Consider the practice as an iniquity (zulm)

• Prohibiting the practice of charging double and multiple riba

• Conclusively prohibiting all forms of riba

• Any excess over the capital is disallowed

4 STAGES4 STAGES

22

“and that which you give in gift (to others), in order that it may increase (your wealth by expecting to get a better one in return) from other people’s property, has no increase with Allah…”

23

“… and their taking of Riba though they were forbidden from taking it and their devouring of men’s substance wrongfully…. and we have prepared... a painful torment.”

24

“O you who believe, Eat not Riba doubled or multiplied, but fear Allah that you may be successful.”

25

“those who eat riba will not stand (on the Day of Resurrection) except like the standing of a person beaten by Shaitan leading him to insanity. That is because they say: trading is only like Riba,” whereas Allah has permitted trading and forbidden Riba. So whosoever receives an admonition from his Lord and stops eating Riba, shall not be punished for the passt; his case is for Allah (to judge); but whoever returns (to riba), such are the dwellers of the Fire – they will abide therein forever.

26

Allah will destroy riba and will give increase for sadaqat (deeds of charity, alms).

…. O you who believe, be afraid of Allah

and give up what remains (due to you) from Riba (from now onward), if you are really believers

27

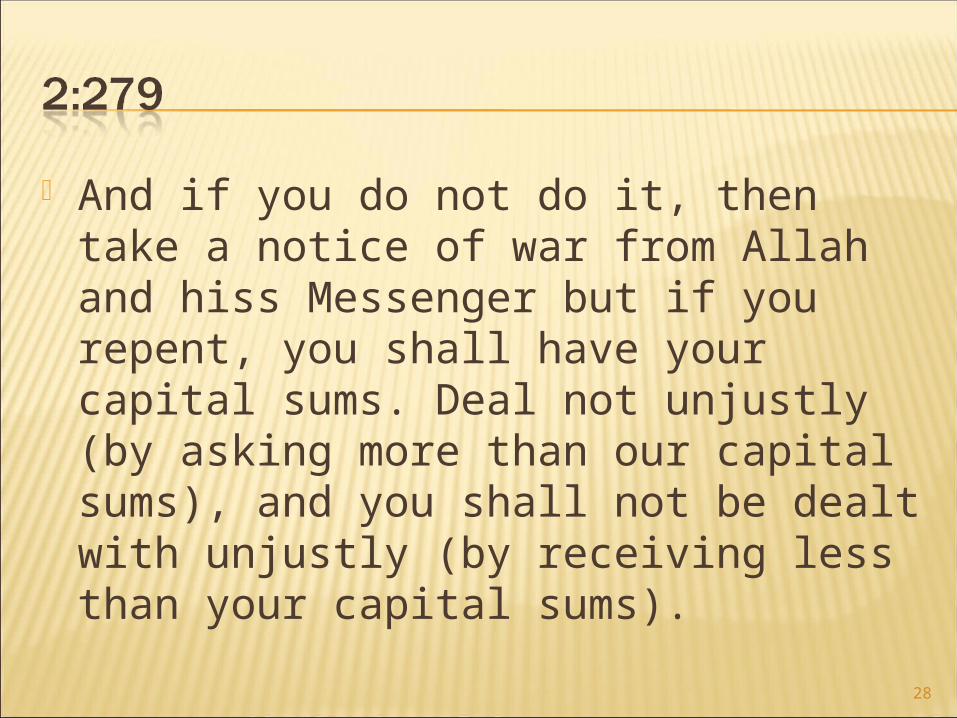

And if you do not do it, then take a notice of war from Allah and hiss Messenger but if you repent, you shall have your capital sums. Deal not unjustly (by asking more than our capital sums), and you shall not be dealt with unjustly (by receiving less than your capital sums).

28

And if the debtor is in a hard time (has no money), then grant him time till it is easy for him to repay; but if you remit it by way of charity, that is better for you if you did but know.

And be afraid of the Day when you shall be brought back to Allah. Then every person shall be paid what he earned, and they shall not be dealt with unjustly.

29

CONT’D…CONT’D… There are also a number of narrations

from the Sunnah on the prohibition of riba

Some of the narrations give general prohibitions of riba, e.g.:“The Prophet of Allah s.a.w. cursed the receiver and the payer of riba, the one who records it and the two witnesses to the transaction and said: they are alike (in guilt)”.

30

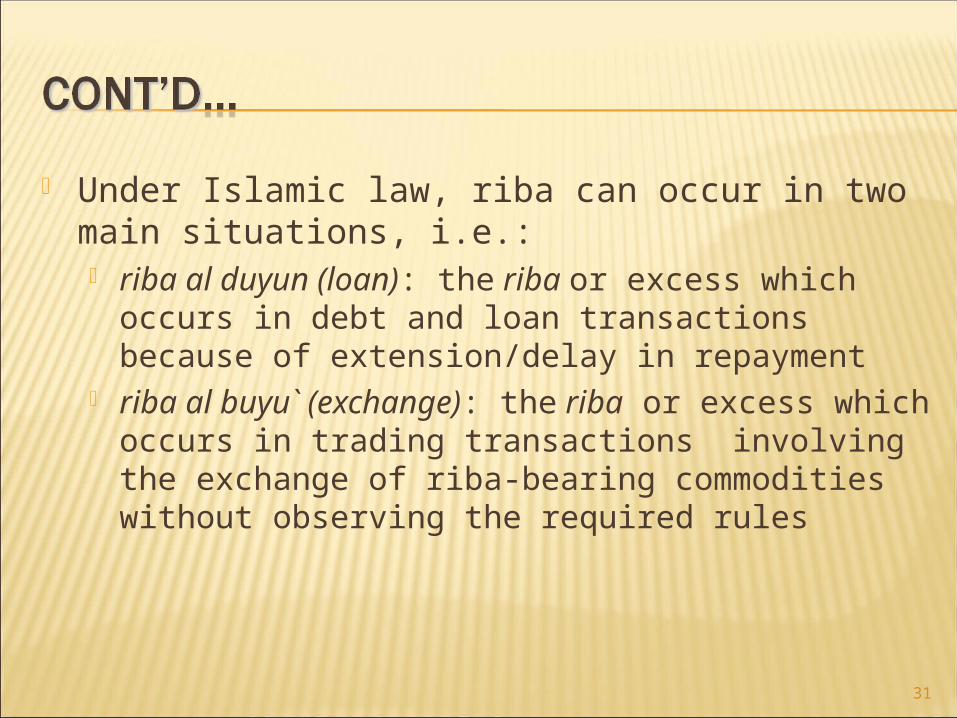

Under Islamic law, riba can occur in two main situations, i.e.: riba al duyun (loan): the riba or excess which

occurs in debt and loan transactions because of extension/delay in repayment

riba al buyu` (exchange): the riba or excess which occurs in trading transactions involving the exchange of riba-bearing commodities without observing the required rules

31

PROHIBITION OF RIBA (LOAN)PROHIBITION OF RIBA (LOAN)

Interpretative Interpretative EffortsEfforts

What amounts toWhat amounts to

TradeTrade UsuryUsury

CriteriaCriteria■Oppressive / unfair distribution

of risk & return■Unjustified enrichment at

expense of others

CriteriaCriteria■ Fair exchange of goods or

value■ Fair distribution of risk &

return

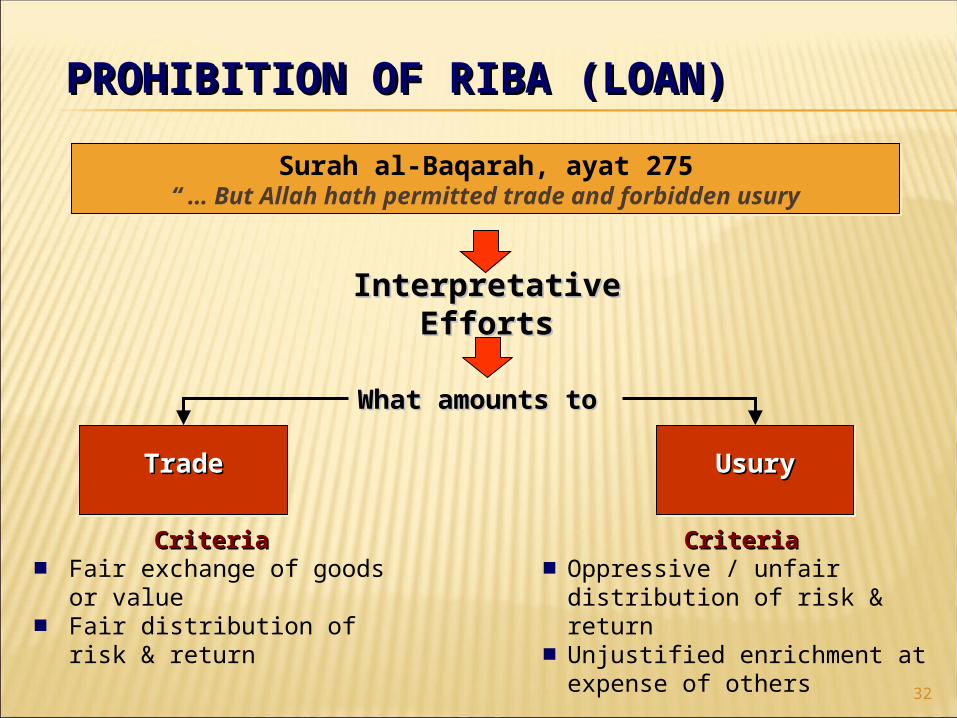

Surah al-Baqarah, ayat 275“ … But Allah hath permitted trade and forbidden usury

32

PROHIBITION OF RIBA PROHIBITION OF RIBA (EXCHANGE)(EXCHANGE)

Interpretative EffortsInterpretative Efforts

ApplicationApplication

Staple FoodStaple Food

RulesRules■Same Type

■At Par■Spot

■Different Type■Spot

RulesRules■Same denomination

■At Par■Spot

■Different denomination■Spot

CurrencyCurrency

Sunnah of the Prophet:Gold for gold, silver for silver, wheat for wheat, barley for barley,

dates for dates, salt for salt - like for like, equal for equal, and hand-to-hand (spot); if the commodities differ, then you may sell as

you wish, provided that the exchange is hand-to-hand or spot transaction.”

33

SUMMARY OF RULES UNDER THE SUMMARY OF RULES UNDER THE HADITHHADITH

• moneymoney11 + money + money11 =2 conditions:

– Equality– Hand-to-hand

• foodfood11 + food + food11 =2 conditions:

– Equality– Hand-to-hand

• moneymoney11 + money + money22 = 1 condition:– Hand-to-hand

• foodfood11 + food + food22 = 1 condition:– Hand-to-hand

• money + foodmoney + food = No condition – free trading

• others + othersothers + others = No condition – free trading

34

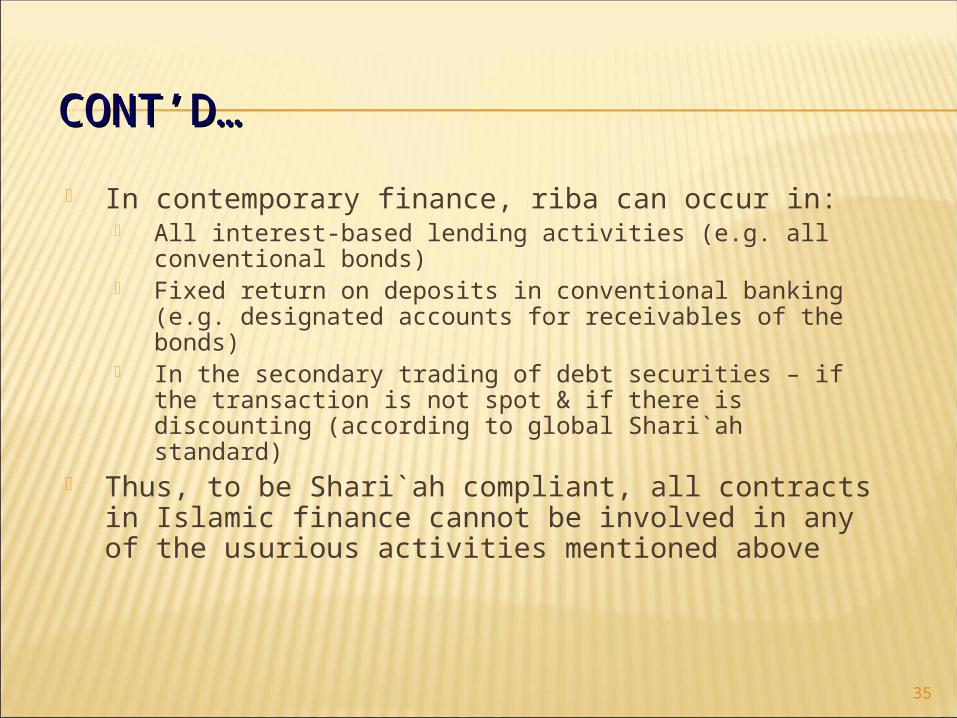

CONT’D…CONT’D… In contemporary finance, riba can occur in:

All interest-based lending activities (e.g. all conventional bonds)

Fixed return on deposits in conventional banking (e.g. designated accounts for receivables of the bonds)

In the secondary trading of debt securities – if the transaction is not spot & if there is discounting (according to global Shari`ah standard)

Thus, to be Shari`ah compliant, all contracts in Islamic finance cannot be involved in any of the usurious activities mentioned above

35

Literally: excess, expand, increase, growth

Any unjustified excess above and over the capital, whether in loans (between creditor and debtor) or in trade (with similar commodities)

36

Riba’ al-Duyun(RIba’ in Loan

Contract)

Riba’ al-buyu’(Riba in exchange Riba in exchange

contractscontracts )

37

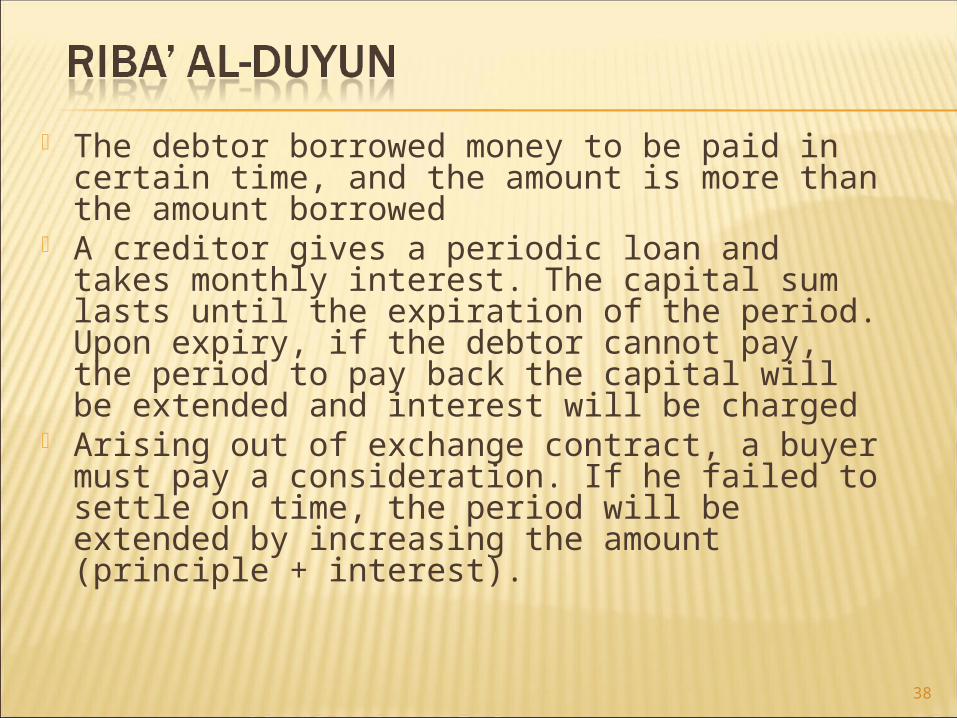

The debtor borrowed money to be paid in certain time, and the amount is more than the amount borrowed

A creditor gives a periodic loan and takes monthly interest. The capital sum lasts until the expiration of the period. Upon expiry, if the debtor cannot pay, the period to pay back the capital will be extended and interest will be charged

Arising out of exchange contract, a buyer must pay a consideration. If he failed to settle on time, the period will be extended by increasing the amount (principle + interest).

38

Mainly based on the saying of the Prophet: “Gold for gold, silver for silver, wheat for wheat, barley for barley, dates for dates, and salt for salt; like for like, hand to hand, in equal amounts; and any increase is riba’”.

39

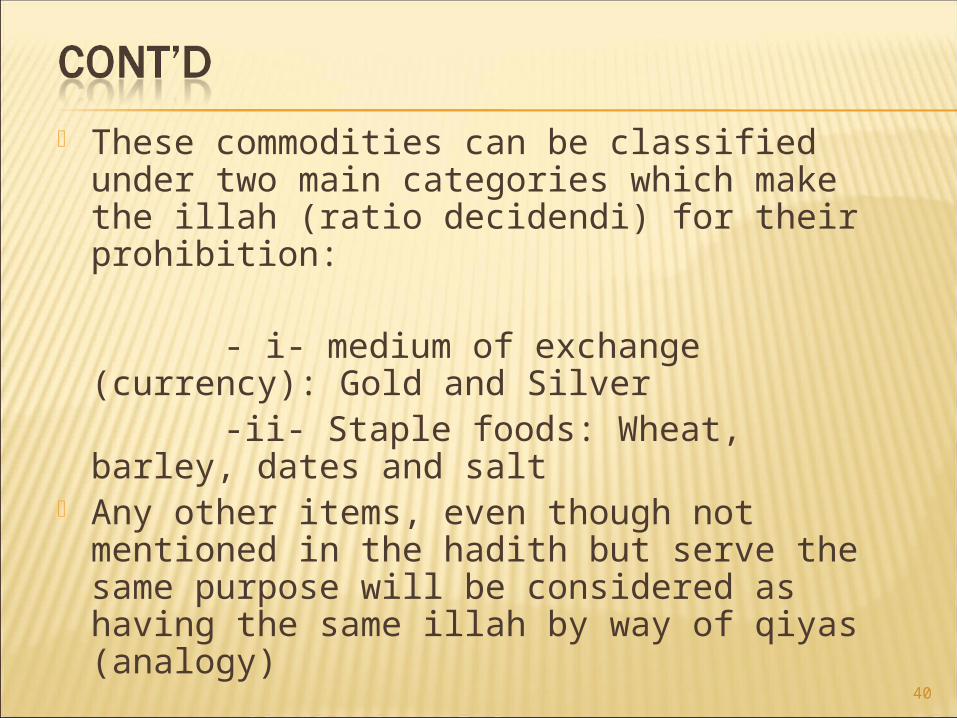

These commodities can be classified under two main categories which make the illah (ratio decidendi) for their prohibition:

- i- medium of exchange (currency): Gold and Silver

-ii- Staple foods: Wheat, barley, dates and salt

Any other items, even though not mentioned in the hadith but serve the same purpose will be considered as having the same illah by way of qiyas (analogy)

40

Riba’ al-duyun in loans and certain controversial contracts (bay’ al-’inah, bay’ al-dayn, etc)

Riba’ al-buyu’ mainly in bay’ al-sarf (exchange of currencies)

41

Meaning of gharar: - Literally: risk, uncertainty, hazard - The sale of probable item whose

existence or characteristics are not certain, due to the risky nature which makes the trade similar to gambling

42

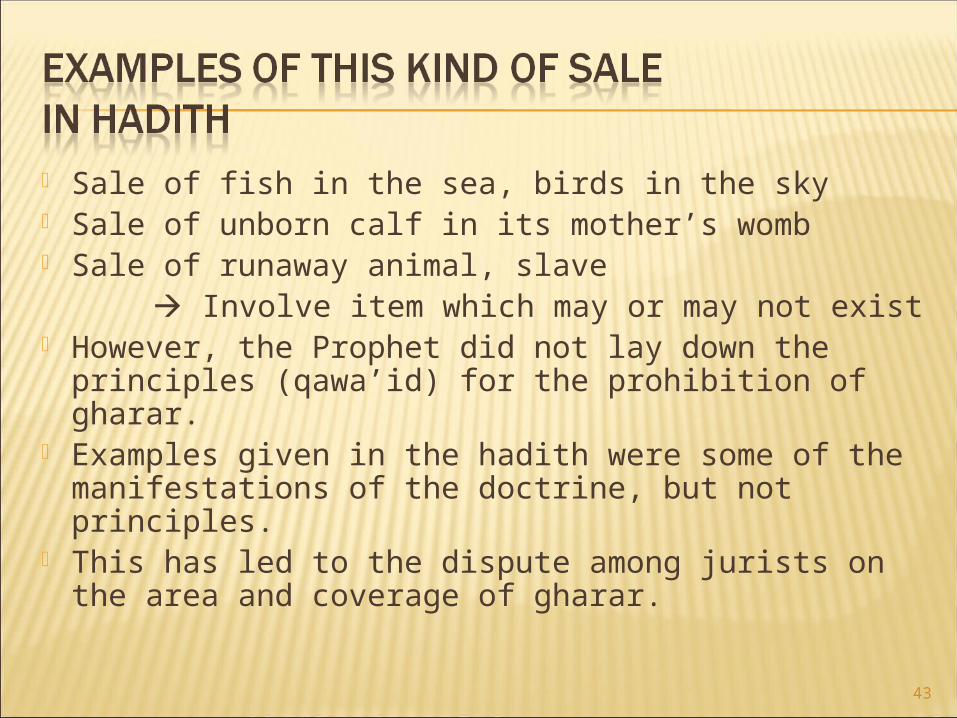

Sale of fish in the sea, birds in the sky Sale of unborn calf in its mother’s womb Sale of runaway animal, slave Involve item which may or may not exist However, the Prophet did not lay down the

principles (qawa’id) for the prohibition of gharar. Examples given in the hadith were some of the

manifestations of the doctrine, but not principles. This has led to the dispute among jurists on the

area and coverage of gharar.

43

GHARARGHARAR Meaning: has a range of negative connotations,

such as, uncertainty, deception, risk, hazard, ignorance etc.

If there is gharar, the contracting party/ies do not really understand the attributes / consequence of the contract

Under Islamic law, gharar is prohibited because its existence in the contract may deny the parties of equal bargaining power and they cannot make informed decisions; or if there is risks on deliverability of the object of the contract

44

PROHIBITION OF GHARARPROHIBITION OF GHARAR

Interpretative EffortsInterpretative Efforts

What amounts toWhat amounts to

Trade by Mutual Trade by Mutual ConsentConsent

CriteriaCriteria■ Offer & Acceptance,

indicating consent■ Elimination of mistake, fraud

etc

CriteriaCriteria■ All illegal & defective

elements in contracts including gharar & uncertainty

Unjust (batil)Unjust (batil)

Surah an- Nisa’: ayat 29“ … squander not your property amongst yourself unjustly

(batil) except it be a trade among you by mutual consent…”

45

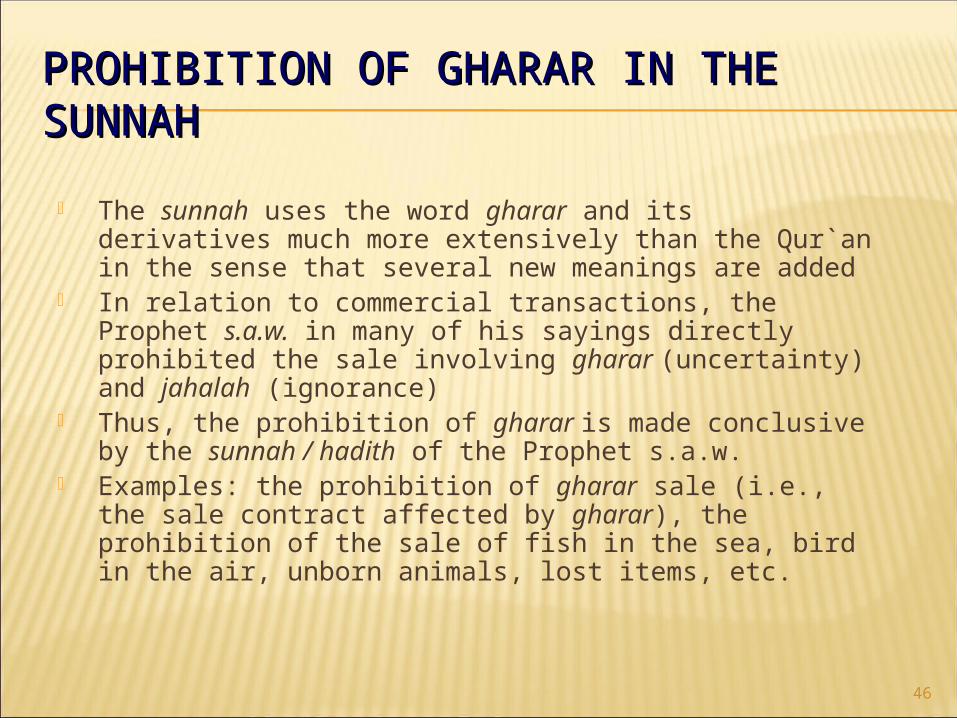

PROHIBITION OF GHARAR IN THE PROHIBITION OF GHARAR IN THE SUNNAH SUNNAH The sunnah uses the word gharar and its

derivatives much more extensively than the Qur`an in the sense that several new meanings are added

In relation to commercial transactions, the Prophet s.a.w. in many of his sayings directly prohibited the sale involving gharar (uncertainty) and jahalah (ignorance)

Thus, the prohibition of gharar is made conclusive by the sunnah / hadith of the Prophet s.a.w.

Examples: the prohibition of gharar sale (i.e., the sale contract affected by gharar), the prohibition of the sale of fish in the sea, bird in the air, unborn animals, lost items, etc.

46

CONT’D…CONT’D… In Islamic law, gharar can be of two degrees:

Excessive or major (gharar fahish) Minor and tolerable (gharar yasir)

Only major /excessive gharar will affect the validity of contracts, where it will render the contract void / voidable, depending on the degree of uncertainty

Gharar affects trading and exchange contracts (mu`awadat); not charitable and unilateral contracts

In banking & finance – gharar can be triggered e.g. – in the sale contract to create the indebtedness if the asset used is uncertain / vaguely identified; the trading of a securitised debt which is unconfirmed / not established, sale of insurance policy

47

Broadly speaking, gharar will effect the validity of contract if it occurs in these areas:

- gharar in kind / type / attribute / quantity of the object

- gharar due to delivery time - gharar due to the price/ mode of

payment - doubt over the ability to deliver

48

Gharar which is excessive (gharar fahish) occurs in exchange contracts (‘uqud al-mu’awadat)

To prevent gharar, the parties to contract must have adequate knowledge and information on the subject matter:

i- Their existence and deliverability ii- Its quality, quantity and attributes

are known iii- Time –frame for payment and

delivery49

OTHER THINGS TO BE AVOIDED…OTHER THINGS TO BE AVOIDED…

Transactions involving the prohibited commodities, e.g., pork and liquor Surah al Maidah (5:3) Surah al Maidah (5:90)

Transactions involving gambling or maysir/qimar Surah al Maidah (5:90)

50

Involves the creation of risk for the sake of risk A combative relationship between two

contracting parties, each of whom undertakes the risk of loss and the loss of one means gain for the other

Apply to all games of pure chance No economic activities are gained in the

practice. The gambler will simply seek to amass wealth without efforts.

Gambling is gharar in its worst scenario. Prohibited by al-Qur’an in Surah al-Maidah (5:90)

51

It is also not allowed to conclude contract on illegal commodities such as pork, liquor etc.

Illegality of certain commodities has been spelt out clearly in the texts of al-Qur’an and Sunnah of the Prophet.

E.g. : - Surah al-Maidah (5:3) - Surah al-Maidah (5: 90)

52

Underlying principles utilised in devising products of IBF is very important as they separate IBF from conventional products.

Contrary to conventional finance, which is specification driven product, Islamic finance is more structure and principle based product

Rules and regulations will differ from one product to another, depending on the structure employed

In general, various underlying Shariah principles have been utilised in devising products of Islamic Banking and Finance.

They can be summarised as below: - Sale based products - Lease based products - Participatory products - Fee based products 53

SHARI`AH COMPLIANCE: MAIN SHARI`AH COMPLIANCE: MAIN PRINCIPLESPRINCIPLES

Mutual consentMutual consent AvoidAvoid

Interest(riba)

Uncertainty(gharar)

Gambling(maysir/qimar)

Other prohibitionse.g. Liquor, pork

Lawful Lawful ContractualContractualObjectiveObjective

CONTRACTS CONTRACTS

54

ENCOURAGEMENT OF TRADE BY ENCOURAGEMENT OF TRADE BY MUTUAL CONSENTMUTUAL CONSENT

The Quran encourages work and trade The Prophet (s.a.w.) himself was a trader The encouragement of trade is evidenced

by the many instruments of trade available during the Prophet's lifetime and in Islamic history thereafter

55

BUSINESS CONTRACTS BUSINESS CONTRACTS RECOGNISED IN ISLAMRECOGNISED IN ISLAM

Contracts of sale and purchase (bay`), including all its subdivisions, like: normal or spot sale mark-up sale (murabahah) deferred payment sale (BBA) sale with advance payment but deferred delivery

(bay` al salam) sale for future delivery of goods with flexible

payment of the price or manufacturing contracts (bay` al istisna`)

sale of currency (sarf), etc.56

CONT’D…CONT’D… Some controversial sales:

Sell and buy back (bay’ al `inah) Sale of Sale of debt (bay` al dayn)

Islam recognises partnership contracts which are mainly based on profit and loss sharing (PLS), e.g.: mudharabah musharakah

A relatively new invention in this regard is: Musharakah mutanaqisah

57

CONT’D…CONT’D…

Islam recognises public and private project financing, e.g.:

Leasing (ijarah) - private; Endowment (waqf) – private/public; State treasury (bayt al mal) – public.

Modern forms of private project financing: Operational lease Financial lease – AITAB (hybrid contract)

58

CONT’D…CONT’D… Islam recognises other additional contracts to provide security to the parties in a contract, i.e., the contracts of security (`uqud al tawthiqat), e.g.:

suretyship/guarantee (kafalah): involves three parties mortgage (rahn): involves two parties

These security contracts are normally combined with other types of contracts, e.g.:

the contract of BBA may be secured by a contract of security involving collateral (rahn)

Other contracts recognised in Islamic law: contracts of trusts (al amanat), e.g.: safe-keeping

(wadi`ah) contracts to do a specified task, e.g.: commision

(ju`alah); agency (wakalah)

59

Banking and finance needs

Right positioning and definition of Islamic banking

Principles filter

Islamic banking and finance solutions

• Prohibition on:

– Interest

– Speculation

– Religious basic sources

– Ijma’ (jurist consensus)– Qiyas (analogy)– Ijtihad (reasoning)

– Musharaka (Partnership)

– Mudaraba (Fund management)

– Murabaha (Purchase-resale)

– Ijara ( Lease)

– Istisna’ ( Manufacturing contract)

– Salam -(Forward sale)

• Asset-backed transactions with investments in real, durable assets

Standart contractsPrinciples sources

• Prohibition of certain investments:− Sectors (e.g.: alcohol, armaments

etc.)− Instruments (e.g. Leveraged

interest products, toxic assets type of derivatives etc.)

• Credit and debt products are not encouraged

Banking and finance needs

Right positioning and definition of Islamic banking

Principles filter

Islamic banking and finance solutions

– Religious basic sources

– Ijma’ (jurist consensus)– Qiyas (analogy)– Ijtihad (reasoning)

– Musharaka (Partnership)

– Mudaraba (Fund management)

– Murabaha (Purchase-resale)

– Ijara ( Lease)

– Istisna’ ( Manufacturing contract)

– Salam -(Forward sale)

Standart contractsPrinciples sources

• With the development and boom of Islamic banking, it became clear that :

− Islamic banking has roots in religion and ethics but it is not a “religion activity” and “not confined to Muslim population”

− Islamic banking is not something “from and for GCC or Muslim world”, it is a global concept− Islamic banking has some limitations and border lines, but it is acknowledged that it can

provide solutions in a wide scope of areas ranging from retail banking to investment banking.

GratuitouGratuitous s

ContractsContractsTrading Trading

ContractsContractsInvestmeInvestme

nt nt ContractsContracts

SupportiSupporting ng

ContractsContracts

Leasing Sale

Bay` Bithaman Ajil (BBA)

Operational Lease

Financial Lease

Murabahah

Salam

Waqf

Loan

Mudarabah

Musharakah

Kafalah

Rahn

Hiwalah

Wadiah

Wakalah

Jualah

Muqasah

Ibra’

Gift

Istisna’ etc.

62

ISLAMIC BANKING

Islamic Banking

SOURCES OF FUND

APPLICATIONS OF FUND

63

64

EQUITY FINANCING

DEBT FINANCING

Fee Based ServicesWakalahKafalah

Sale based financing BBA / Murabahah‘Inah/Tawaruq/dayn

SalamIstisna

Lease Based Financing-Ijarah-AITAB

Comsumer Banking

MudharabahMusharakah

Corporate Banking

Sources of Funds

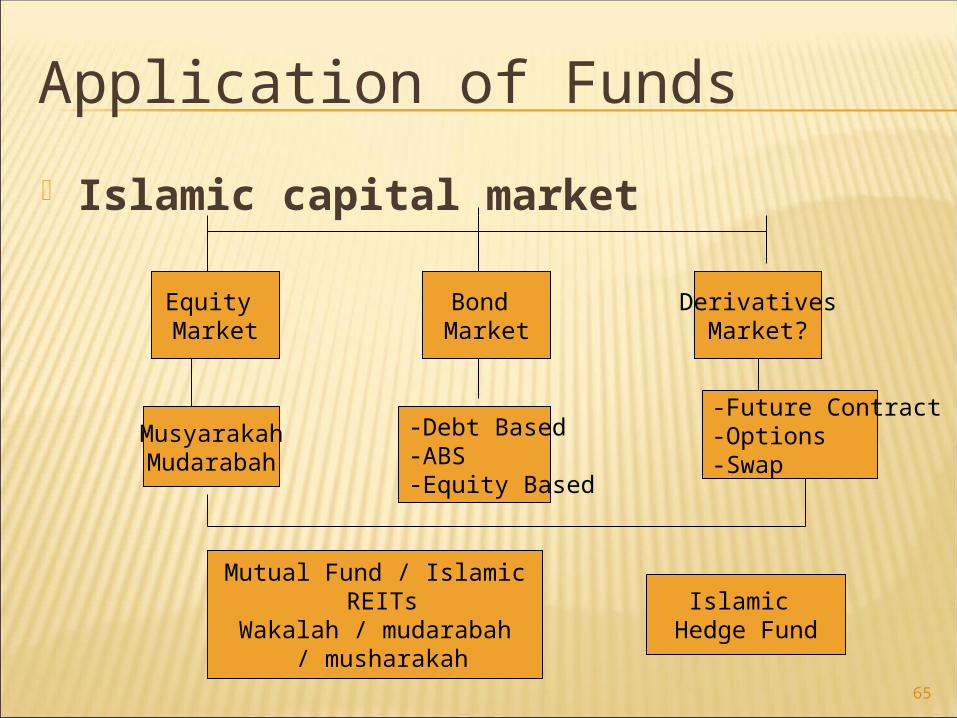

Islamic capital market

Equity Market

Bond Market

DerivativesMarket?

MusyarakahMudarabah

-Debt Based-ABS-Equity Based

-Future Contract-Options-Swap

Mutual Fund / Islamic REITs

Wakalah / mudarabah / musharakah

Islamic Hedge Fund

65

Application of Funds

Besides various frameworks applied to banking practices (be it Islamic or conventional), Shariah framework is a framework which is peculiar to Islamic finance alone

Yet, it forms the very substance of Islamic finance, without which Islamic finance will loss its Islamicity

As such, in practicing Islamic finance, the do’s and don’ts must be clearly observed

Islamic commercial law, from the fact that it subjects to human interpretation and understanding admits differences of opinion, as long as these differences are grounded by valid evidence, produced by capable personnel, done according to the right methodology

66

Top Related