Languages

Pages

Legal

1

Maine Associationof Assessing Officers

Sebasco EstatesSeptember 29, 2011

Why are Wireless Communications Towers & Sites so Difficult to ValueGary J. McCabe, CAE

2

Wireless Valuation Q&A (1)◘ What are we valuing?◘ Wireless communications

infrastructure & equipment?◘ What is wireless communications

infrastructure?◘ Land or land rights◘ Site Improvements◘ Antenna structures (towers,

roof-tops, in-building, utility poles, other)

◘ Base station shelters,MSO facilities

3

Wireless Valuation Q&A (2)

◘ What is wireless communications equipment?

◘ Antennas◘ Cables (coax) & connectors◘ Base station equipment;◘ Modems, routers, switches,

batteries, multiplexers, rectifiers, circuit packs

4

Real Estate vs. Personalty;The 3 Prong Test

1. Annexation2. Adaptation3. Intent◘ New York◘ Pennsylvania◘ Massachusetts

5

New York; Supreme Court of Rockland Co.Nextel v. Spring Valley, 2/2004

To meet the common-law definition of a fixture, personalty must:

1. Be annexed to real property or appurtenant thereto;

2. Be used as part of the realty;3. Intended by the parties to be a

permanent accession to the freehold. Antennas held to be real fixtures even if

removed at end of lease. Ruling is inconsistent with

Commissioner of Revenue treatment of towers as personalty for sales tax purposes.

6

Pennsylvania; Court of Common Pleas,Shenandoah Mobile v. Cumberland Co. 9/2004

Cell tower is taxable real property:1. Tower possessed requisite degree of

attachment by bolts into concrete pad & would require a crane to be removed.

2. Tower is essential to the permanent use of the improvement, concrete pad.

3. The intent of parties was for the tower to become part of the realty.

Court found no inconsistency with PA DOR treatment of towers as personalty for use tax purposes.

7

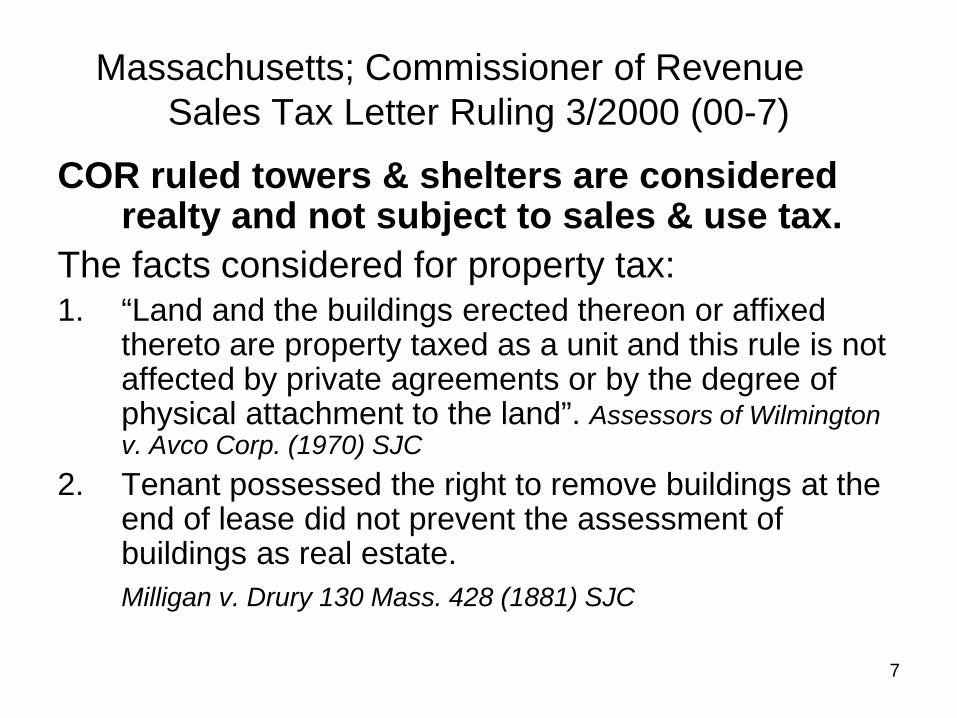

Massachusetts; Commissioner of RevenueSales Tax Letter Ruling 3/2000 (00-7)

COR ruled towers & shelters are considered realty and not subject to sales & use tax.

The facts considered for property tax:1. “Land and the buildings erected thereon or affixed

thereto are property taxed as a unit and this rule is not affected by private agreements or by the degree of physical attachment to the land”. Assessors of Wilmington v. Avco Corp. (1970) SJC

2. Tenant possessed the right to remove buildings at the end of lease did not prevent the assessment of buildings as real estate.Milligan v. Drury 130 Mass. 428 (1881) SJC

Massachusetts Appellate Tax Board

• The cell tower’s attachment to its realty is comparable to the attachment of the silos to their surroundings in New England Milling Co., Inc. v. Assessors of Ayer, Mass. ATB Findings of Fact and Reports 1998-625.

8

9

Assessment Jurisdiction: Maine

o Wireless infrastructure:cell towers; real estate (locally valued & taxed).

o Wireless equipment: personal property(centrally taxed)

o Wire-line networks:personal property(centrally taxed).

10

TX

OK AR

LAMS AL GA

FL

SCNCTN

KY

WY

UTCO KS MO

NE

WAMT

IDOR

NVCA

AZ NM

ND

SDMN

IAMI

IL IN OH

WI

VAWV MDDE

PANJ

NY

VTNH ME

MA

CTRI

Personal

Real Estate

Towers Non-Taxable Personalty

Mix of Real Estate & Personal Property

U.S. Property Tax Classification; Cell Towers

11

Where is Al Gore?

On-line Discovery Tools• FCC web-site http://wireless2.fcc.gov• Tower Company web-sites

www.americantower.com/SiteLocator

12

Take I-95 North into Maine. Take exit 24 and turn right onto Rt-196 South. Go 2.5 miles and take Route 1 North. Go 6.5 miles and take exit towards Congress Ave/Western Ave and take a right. Go about a mile and turn left onto a small dirt road (renos bluff)across from stone cutting business. Drive slowly on dirt road and look for tower on the left fairly well hidden by the trees.

Tower Data

Tower Number:

75059

Structure Height (AGL):

140 ft.

Type: Guyed FAA #: 94-ANE-443-OE FCC #: 1022133

13

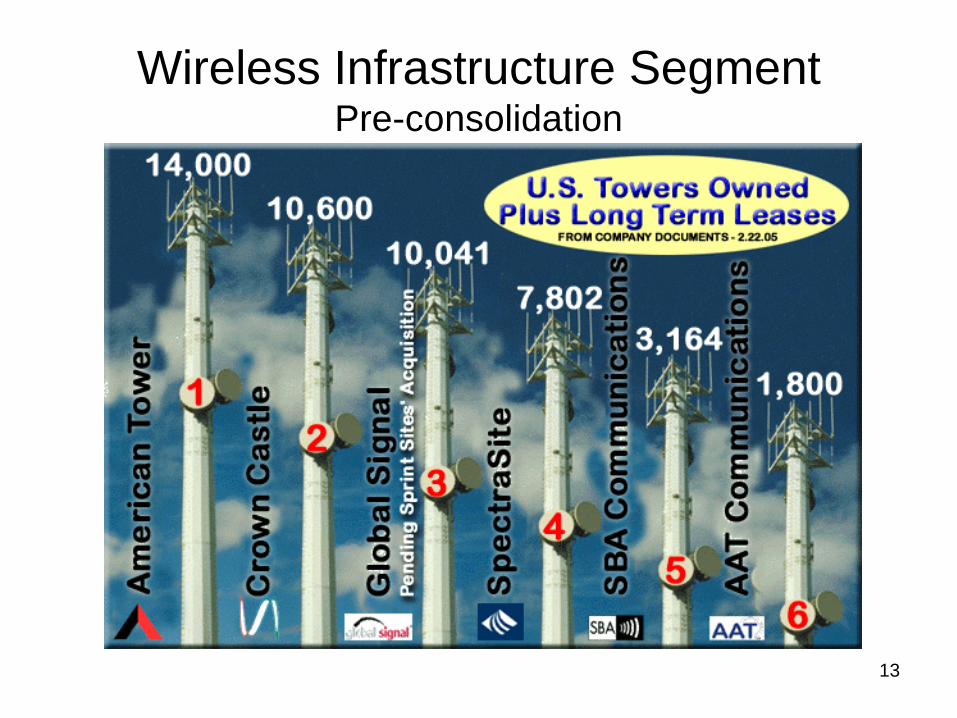

Wireless Infrastructure SegmentPre-consolidation

14

Monopole Self SupportGuyed

Typically 100’-200’ ft.

Typically 200’-400’ ft.

Typically 400’-1200’ ft.

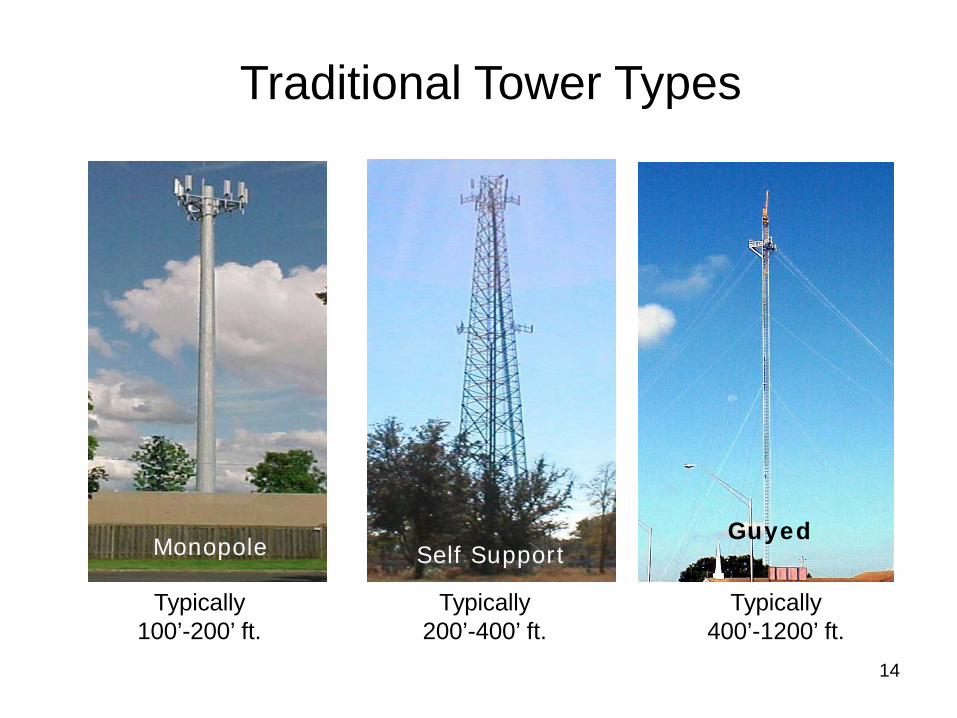

Traditional Tower Types

M&S Self-Support TowersSection 67

HT $/LF HT $/LF50 290 225 80475 390 250 863

100 465 300 975150 612 350 1082200 742 400 1184

Included in the costs are concrete footings, tower erection, painting, platforms, designers’ fees, lighting (if req.), guyed wired (if req.) 15

M&S Monopole TowersSection 67

HT $/LF50 35775 466

100 554150 716200 858

Included in the costs are concrete footings, tower erection, painting, platforms, designers’ fees, lighting (if req.), guyed wired (if req.) 16

M&S Triangular Guyed towersSection 67

Type HT $/LF

24” Radio < 400 6830” Cellular < 400 21340” Microwave < 400 26354” Master TV < 400 523

Included in the costs are concrete footings, tower erection, painting, platforms, designers’ fees, lighting (if req.), guyed wired (if req.)

17

Non-traditional Towers

18

19

DEER ISLE Web exclusive, March 11, 2011Cell tower nears completion

The newly erected cell phone tower on North Deer Isle Road will soon be in operation, according to Blaine Hopkins of Global Tower Assets, LLC, the company that built and owns the tower. Hopkins said the work on the 190-foot tower, located on land leased from Milton and Priscilla Haskell, was delayed by stormy weather in January. The site’s electric power was connected on March 3.

20

DEER ISLE Web exclusive, March 11, 2011Cell tower nears completion (cont.)

The tower’s primary tenant is AT&T. Information on when AT&T will begin service from the site was not available from company officials at press time. However, Hopkins said that AT&T would begin using the tower as soon as possible after testing is completed, which would likely be within 30 days.

21

Cell tower nears completion– page 2Hopkins said that a second cell phone company—name not disclosed—is likely to sign a lease for the next lower space on the tower by April. The tower was designed to hold antennas for up to six cell phone companies.

The Haskell site was the third of three sites where tower permits were issued in the spring of 2010. (See June 24 issue of Island Ad-Vantages.) Hopkins said that with his company’s tower in place, which was an investment of $400,000, it is unlikely that towers on the other permitted sites will be built.

Sears Island

22

Cell Site

Typical Cell Site Land LeaseLESSOR hereby leases to LESSEE a portion of that certain parcel of property, located at Plainfield Road, and being described as a 100’ x 100’ parcel containing 10,000 sq.ft., together with the non-exclusive right -of-way for ingress and egress, seven (7) days a week twenty-four (24) hours a day, over or along a thirty-foot (30’) wide right-of-way extending from the nearest public way, Plainfield Rd., to the leased space, and for the installation and maintenance of utility wires, poles, cables, conduits, and pipes over, under, or along the right-of-way. Terms: 5-years, with 4, 5-year renewal options, with annual percentage increases.Taxes: Paid by LesseeEnd of Term Condition: Removal of tower. 23

Land (site) ValuationBased on Ground Rent

TermYears

PV Factor at 8.0%

AnnualRent

Indicated Value

10 6.71 $12,000 $80,52015 8.56 $12,000 $102,72020 9.82 $12,000 $117,84025 10.67 $12,000 $128,040

24

25

Land Lease ChartSteel in the Air, Inc.

Overall (Tower & Site) Income Approach

• Gross Income from Tower Space Rental to Tower Owner

– LESS site & business expenses= Net Operating Income/ Overall Cap.Rate (based on industry)= Total Cell Site Property ValueIncluding:

• Leased land• Site utilities & access road• Tower & Site Improvements• Buildings provided by Tower Co.

26

Top Related