Languages

Pages

Legal

Better insight + Better process = Better results

Interim Report & Accounts

31 July 2010

JPMorgan Fund ICVC

Click to enter

Contents

1

> JPM Asia Fund

> JPM Balanced Total Return Fund

> JPM Cautious Total Return Fund

> JPM Emerging Markets Fund

> JPM Emerging Markets Infrastructure Fund

> JPM Europe Dynamic (ex-UK) Fund

> JPM Europe Fund

> JPM Global Consumer Trends Fund

> JPM Global Equity Income Fund

> JPM Global (ex-UK) Bond Fund

> JPM Global Financials Fund

> JPM Global Fund

> JPM Global High Yield Bond Fund

> JPM Global Property Securities Fund

> JPM Institutional Asia Fund

> JPM Institutional Continental Europe Fund

> JPM Institutional Japan Fund

> JPM Japan Fund

> JPM Multi-Asset Income Fund

> JPM Multi-Manager Growth Fund

> JPM Natural Resources Fund

> JPM New Europe Fund

> JPM Premier Equity Growth Fund

> JPM Premier Equity Income Fund

> JPM Sterling Corporate Bond Fund

> JPM Strategic Bond Fund

> JPM UK Active 350 Fund

> JPM UK Dynamic Fund

> JPM UK Equity & Bond Income Fund

> JPM UK Focus Fund

> JPM UK Managed Equity Fund

> JPM UK Strategic Equity Income Fund

> JPM UK Strategic Growth Fund

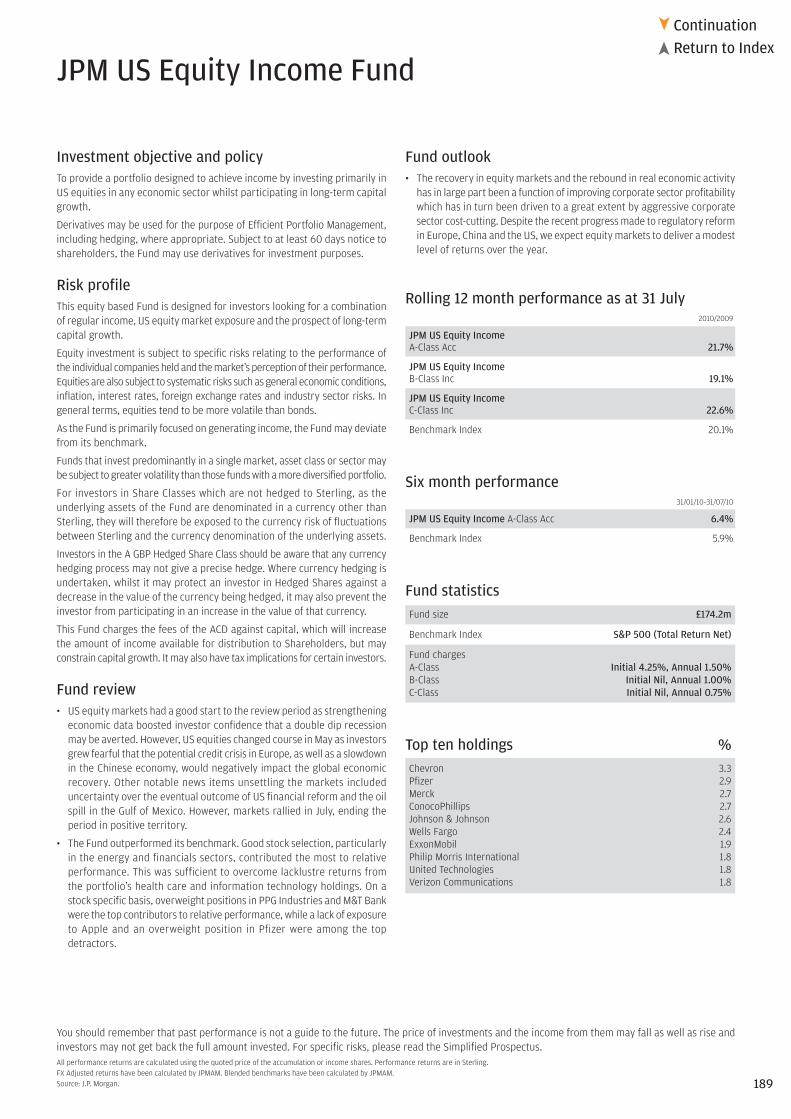

> JPM US Equity Income Fund

> JPM US Fund

> JPM US Select Fund

> Authorised Corporate Director’s (ACD) Report

> Interim Report for the six months to 31 July 2010Find out how the markets have performed over the six months to 31 July 2010

> Aggregated Company financial statements

This material should not be relied on as including sufficient information to support an investment decision.

The opinions and views expressed in this document are those held by J.P. Morgan Asset Management as at 31 July 2010, which are subject tochange and are not to be taken as or construed as investment advice.

For up-to-date performance information please contact J.P. Morgan Asset Management using the numbers shown on the back of this document.

You should remember that past performance is not a guide to the future. The price of investments and the income from them may fall as wellas rise and investors may not get back the full amount invested. The level of tax benefits and liabilities will depend on individual circumstancesand may change in the future.

The investment objective of a fund may allow some flexibility in terms of portfolio composition.

Funds that invest predominantly in a single market, asset class or sector may be subject to greater volatility than those funds with a morediversified portfolio.

The information in this booklet is based on our understanding of law, regulation and HM Revenue and Customs practice as at 31 July 2010.

2

Authorised Corporate Director’s (ACD) ReportWe are pleased to present the Interim Report &Accounts for JPMorgan Fund ICVC for the periodended 31 July 2010.

Authorised StatusJPMorgan Fund ICVC is an Open-EndedInvestment Company (OEIC) with variable capitalauthorised, under Regulation 12 of the OEICRegulations, by the Financial Services Authorityon 6 October 1997.

The Company was launched as a UCITS Schemeon 16 November 2001 and acts as an umbrellacompany comprising of various sub-funds. Itsregistration number is IC00005 and its registeredaddress is Finsbury Dials, 20 Finsbury Street,London EC2Y 9AQ.

Structure & LiabilitiesThe assets of each Fund are treated as separatefrom those of every other Fund and are investedin accordance with the investment objective andinvestment policies applicable to that Fund. Details of the investment objective, the policiesfor achieving these objectives, the performancerecord and a review of the investment activitiesfor each of the Funds can be found in this report.

Each Fund has a specific portfolio of securitiesto which its assets and liabilities are attributable.So far as shareholders are concerned each Fundis managed as a separate entity. However, ifthe assets of any Fund were insufficient to meetthe liabilities attributable to it, the shortfall mayhave to be met out of the assets attributable tothe other Funds in the OEIC. In the event of thishappening, the ACD would advise shareholdersimmediately. Each Fund has different classes ofshares which are applicable to different typesof investor.

Shareholders are not liable for the debts of the OEIC.

A shareholder is not liable to make any furtherpayment to the company after the purchase oftheir shares has been paid for.

Changes to Funds, Prospectusand Instrument of IncorporationDuring the period under review, the followingchanges were made as follows:

Liquidation of JPM Institutional Japan FundThe ACD informed shareholders of JPMInstitutional Japan Fund in March 2010 of the

intention to close the Fund. Approval for this wasreceived from the Financial Services Authorityand all trading and dealings in the Fund weresuspended as of 12:00 on 21 April 2010. An initialdistribution of the pro-rata termination proceedswas paid to shareholders on 23 April 2010.

Shareholders were informed in May 2010 of thefollowing matters which came into effect from2 August 2010:

Collateral Management CostsCollateral Management Costs are incurred bysome Funds when dealing in sophisticatedinvestments and the ACD decided to include suchcosts as part of the Funds’ ‘fixed expenses’. Thischange was made to provide greater certaintyof costs to shareholders.

JPM Premier Equity Income FundThe investment objective and policy was changedto “To provide income and prospects of capitalgrowth by investing primarily in equity and equity-linked securities of UK companies. Otherinstruments as permitted in the stated investmentand borrowing powers of the Company including,but not limited to, fixed interest securities, cashand cash equivalents may be held on an ancillarybasis, as appropriate.”

JPM Emerging Markets FundThe investment objective and policy was changedto “To provide long term capital growth byinvesting primarily in equity and equity-linkedsecurities of emerging markets companies. Otherinstruments as permitted in the stated investmentand borrowing powers of the Company including,but not limited to, fixed interest securities, cashand cash equivalents may be held on an ancillarybasis, as appropriate.”

JPM Global Property Securities FundThe investment objective and policy was changedto “To provide long-term capital growth byinvesting primarily in Real Estate InvestmentTrusts (REITS) and in equity and equity-linkedsecurities of other real estate companies that,at the time of investment, are significant owners,developers or financiers of real estate or thatprovide real estate related services. Otherinstruments as permitted in the statedinvestment and borrowing powers of theCompany including, but not limited to, fixedinterest securities, cash and cash equivalentsmay be held on an ancillary basis, as appropriate.The Fund will aim to hedge non-sterlingexposures back to sterling.”

The following additional changes to the Prospectuscame into effect from 1 September 2010:

• The Swing Pricing threshold was reduced tothe lower of £750,000 and 1% of net asset value.

• Shareholders can no longer request that theACD sells any underlying securities allocatedto them as a result of redemptions in specieunless the ACD specifically agrees to act onsuch instructions and is properly authorised bythe shareholder to do so.

• The ACD has flexibility to adjust the end of anaccounting period by +/- 7 days.

Management and Administration DepositaryThe Royal Bank of Scotland plcThe Broadstone, 50 South Gyle CrescentEdinburgh, EH12 9UZ(Authorised and regulated by the Financial Services Authority)

Independent AuditorsPricewaterhouseCoopers LLPPO Box 90, Erskine House68–73 Queen StreetEdinburgh, EH2 4NH

RegistrarJPMorgan Asset Management Marketing Limited125 London Wall, London, EC2Y 5AJ(Authorised and regulated by the Financial Services Authority)

Investment AdviserJPMorgan Asset Management (UK) Limited125 London Wall, London, EC2Y 5AJ(Authorised and regulated by the Financial Services Authority)

By order of the Authorised Corporate Director,

Ms T McDowall DirectorFor an on behalf of JPMorgan Funds Limited6 September 2010

Mr R ThompsonDirectorFor an on behalf of JPMorgan Funds Limited6 September 2010

3

Return to Index�

Interim Report for the six monthsto 31 July 2010Market reviewGlobal equity markets experienced a volatilesix months as concerns over the sovereign debtcrisis in Europe contributed to fears of a fading recovery. The MSCI World Index did,however, return 4.4% and the JPMorgan GlobalGovernment Bond Index produced a 5.6%return in Sterling terms.

The period began on a positive note as first-quarter earnings were surprisingly strong,suggesting that the recovery was becomingentrenched. The US and Asia produced gooddomestic economic data, as both regionsexperienced strong industrial activity. In theUK, an upward revision of fourth-quarter GDPgrowth to 0.4% helped to ease fears of adouble-dip recession.

In April however, financial markets wobbled asworries that Greece may be unable to serviceits debt spread to other highly indebtedeurozone countries. Rating agencies Standardand Poor’s and Moody’s severely downgradedGreece and followed with downgrades forPortugal, Spain, Ireland and Italy.

As a result of these sovereign debt concerns,peripheral eurozone bond yields widenedsharply and investors fled to quality, benefitinggold and those government bond markets thatare perceived as being the safest haven, notablyGerman Bunds and US Treasuries. Financialstocks were particularly badly hit by concernover the balance sheet exposure of many banksto peripheral European bonds. These concernseased following the European Union and IMF’sannouncement of a EUR 750 billion rescuepackage in May, with additional support pledgedby the European Central Bank.

However, as austerity measures required totackle huge budget deficits were introduced inmany countries concern set in again as investorsfeared the new age of austerity may berestrictive to global growth. Growth concernswere also focused on China over the period asgovernment measures to stop the domesticproperty market from overheating led to theunderperformance of Chinese stocks for thehalf year. Concerns mounted in May as industrialdata pointed to a slowdown in Chinese domesticgrowth, which provoked fears of a stalling globalrecovery.

Concerns over the pace of economic growthwere also prominent in the US, as the recoveryfailed to open up new jobs and private payrollsrose by less than expected, eroding thespending power of US households. In the UK,the new coalition government announcedswingeing cuts to public spending as part ofthe June austerity budget, adding to concernthat severe cuts to spending may compromisethe recovery.

The end of the period saw a boost to sentimentfollowing the release of surprisingly strongsecond-quarter corporate earnings data in theUS, Europe and Asia. The European Union’srelease of positive bank stress test results,showing the majority of European banks areadequately capitalised, further eased concernsover the sovereign debt crisis.

Market outlookAlthough sentiment improved in July, concernsover the pace of the recovery are likely toremain at the forefront of investors’ minds forsome time. Despite evidence of a slowdown inChina, the country’s growth outlook remainsattractive. The Chinese authorities are choosingto steer a pragmatic course and should avoidthe perils of aggressive tightening of monetarypolicy. The US and European economies,however, are likely to experience a drag togrowth from the reversal of fiscal stimulus,especially after tightening measures are put inplace. In Europe, including the UK, this effectcould be more marked in the short-term asausterity measures are already being carriedout. The key question is whether there will bea recovery in private sector demand to offseta retrenchment in the public sector. A successfulrebalancing of activity would be supportive forequities and other risk assets.

Equity valuations are attractive in manymarkets, but investors will be looking forevidence that earnings momentum remainsstrong. Government bonds, meanwhile, appearfully valued at current levels but could benefitif volatility persists.

JPMorgan Asset Management (UK) Limited11 August 2010

4

Return to Index�

ContinuationReturn to Index�

�

JPM Asia Fund

5

Investment objective and policyTo provide long-term capital growth from investment primarily in the securitiesof companies quoted or trading in Asia (excluding Japan).

Risk profileThis equity based Fund is designed to give broad market exposure (whichmay include emerging markets and smaller companies) to stock marketsacross the Asia ex-Japan region.

Equity investment is subject to specific risks relating to the performance ofthe individual companies held and the market’s perception of theirperformance. Equities are also subject to systematic risks such as generaleconomic conditions, inflation, interest rates, foreign exchange rates andindustry sector risks. In general terms, equities tend to be more volatile than bonds.

The Fund may be invested in emerging markets, which may be subject toadditional political and economic risks, low liquidity, poor transparencyand greater financial risks.

The underlying assets of the Fund are denominated in currencies other thanSterling and are not hedged back to Sterling. Investors will therefore beexposed to the currency risk of fluctuations between Sterling and the currencydenomination of the underlying assets.

Fund review• Over the six month review period, the Fund produced a positive return

but underperformed its benchmark. Asset allocation (overweight HK/Chinaand Thailand; underweight Singapore, Philippines and Malaysia) wasneutral and underperformance was mainly due to negative stock selectionin Korea and Taiwan.

• Asian markets were volatile at the start of the year on concerns over Greekfiscal stress, Chinese policy tightening and fears over US bank regulation.Markets staged an unconvincing rally from mid-February. The Fundbenefited from its overweight position in Thailand.

• The latter part of the period proved more difficult for the Fund, againsta backdrop of heightened concerns over European sovereign debt, Chinesepolicy tightening and global growth. The Fund’s overweight in China andunderweight in ASEAN markets were detrimental for returns, as was ourdecision to eschew classic defensive stocks such as utilities and telecoms.

Fund outlook• We are cautiously optimistic about the outlook for Asia. We remain

concerned about the external environment, as earnings forecasts for theUS in 2011 look high and we expect external demand for Asian exportsnext year to be anaemic.

• That said, the Asian consumption story, particularly in China, continuesto offer high growth and the Fund is well exposed to this sector. Overall,Asian equities are reasonably priced and balance sheets look strong.

You should remember that past performance is not a guide to the future. The price of investments and the income from them may fall as well as rise andinvestors may not get back the full amount invested. For specific risks, please read the Simplified Prospectus.All performance returns are calculated using the quoted price of the accumulation shares. Performance returns are in Sterling.FX Adjusted returns have been calculated by JPMAM. Blended benchmarks have been calculated by JPMAM.Source: J.P. Morgan.A On 01/03/09 the Fund’s benchmark was changed from MSCI AC Far East ex Japan Net to the MSCI AC Asia ex Japan (Total Return Net) Index.Benchmark Source: MSCI. Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express of implied warranties or representations with respect to such data(or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect toany of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling computing or creating the data have any liability for any direct,indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted withoutMSCI’s express written consent.

• If China can engineer a soft economic landing in the second half of 2010,then we think further upside exists. The slowdown in sequential growthin China should soon bring an end to policy tightening, boosting regionalmarkets.

• Valuations appear reasonable and for the second half of 2010 the Fundremains overweight in Hong Kong/China and Thailand and underweightin Singapore, Malaysia and Taiwan.

Rolling 12 month performance as at 31 July2010/2009 2009/2008 2008/2007 2007/2006 2006/2005

JPM Asia A-Class Acc 17.0% 13.6% -13.7% 51.4% 8.1%

JPM AsiaB-Class Acc 17.7% – – – –

Benchmark IndexA 21.0% 12.8% -10.5% 41.6% 9.5%

Six month performance31/01/10–31/07/10

JPM Asia A-Class Acc 8.6%

Benchmark IndexA 10.9%

Fund statisticsFund size £111.0m

Benchmark IndexA MSCI AC Asia ex Japan (Total Return Net)

Fund chargesA-Class Initial 4.25%, Annual 1.50%B-Class Initial Nil, Annual 1.00%

Top ten holdings %Samsung Electronics 4.7China Construction Bank ‘H’ 4.3KB Financial Group 3.2China Life Insurance ‘H’ 2.9Industrial & Commercial Bank of China ‘H’ 2.5Hon Hai Precision Industry 2.3HDFC Bank 2.2Tencent 2.2CNOOC 1.9Wharf 1.9

6

ContinuationReturn to Index�

�

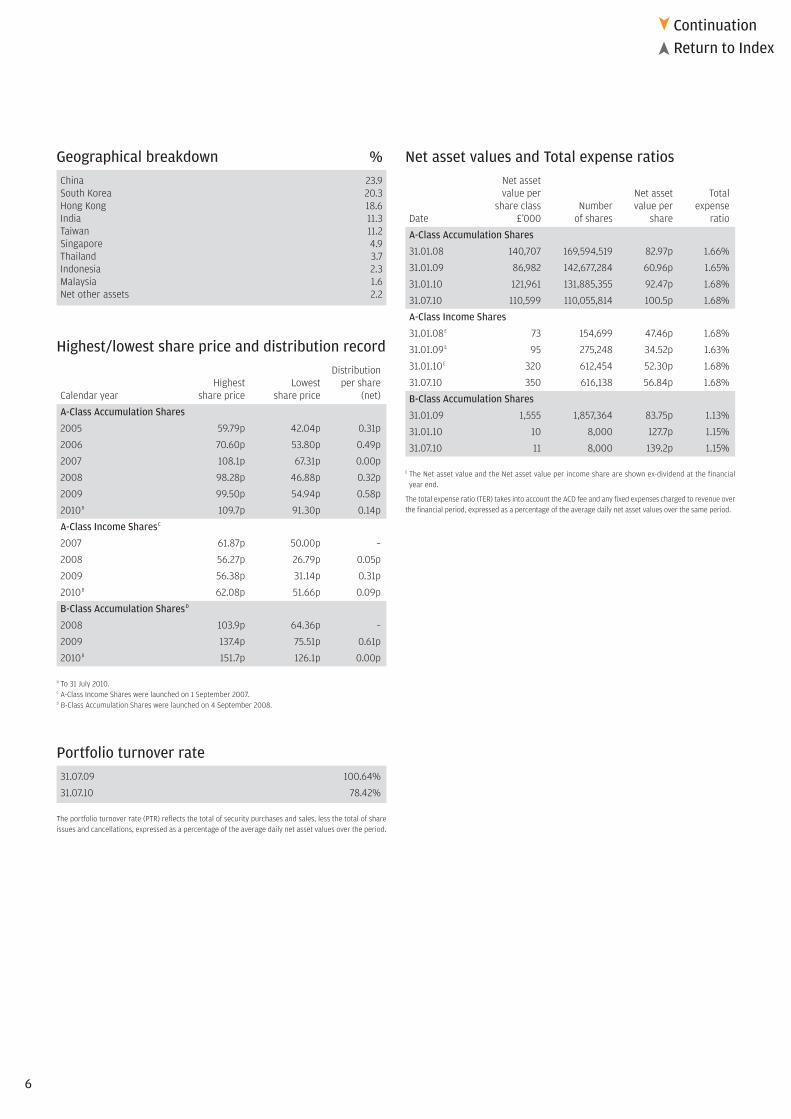

Geographical breakdown %China 23.9South Korea 20.3Hong Kong 18.6India 11.3Taiwan 11.2Singapore 4.9Thailand 3.7Indonesia 2.3Malaysia 1.6Net other assets 2.2

Highest/lowest share price and distribution recordDistribution

Highest Lowest per shareCalendar year share price share price (net)

A-Class Accumulation Shares

2005 59.79p 42.04p 0.31p

2006 70.60p 53.80p 0.49p

2007 108.1p 67.31p 0.00p

2008 98.28p 46.88p 0.32p

2009 99.50p 54.94p 0.58p

2010B 109.7p 91.30p 0.14p

A-Class Income SharesC

2007 61.87p 50.00p –

2008 56.27p 26.79p 0.05p

2009 56.38p 31.14p 0.31p

2010B 62.08p 51.66p 0.09p

B-Class Accumulation SharesD

2008 103.9p 64.36p –

2009 137.4p 75.51p 0.61p

2010B 151.7p 126.1p 0.00p

B To 31 July 2010.C A-Class Income Shares were launched on 1 September 2007.D B-Class Accumulation Shares were launched on 4 September 2008.

Portfolio turnover rate31.07.09 100.64%

31.07.10 78.42%

The portfolio turnover rate (PTR) reflects the total of security purchases and sales, less the total of shareissues and cancellations, expressed as a percentage of the average daily net asset values over the period.

Net asset values and Total expense ratiosNet assetvalue per Net asset Total

share class Number value per expenseDate £’000 of shares share ratio

A-Class Accumulation Shares

31.01.08 140,707 169,594,519 82.97p 1.66%

31.01.09 86,982 142,677,284 60.96p 1.65%

31.01.10 121,961 131,885,355 92.47p 1.68%

31.07.10 110,599 110,055,814 100.5p 1.68%

A-Class Income Shares

31.01.08E 73 154,699 47.46p 1.68%

31.01.09E 95 275,248 34.52p 1.63%

31.01.10E 320 612,454 52.30p 1.68%

31.07.10 350 616,138 56.84p 1.68%

B-Class Accumulation Shares

31.01.09 1,555 1,857,364 83.75p 1.13%

31.01.10 10 8,000 127.7p 1.15%

31.07.10 11 8,000 139.2p 1.15%

E The Net asset value and the Net asset value per income share are shown ex-dividend at the financial year end.

The total expense ratio (TER) takes into account the ACD fee and any fixed expenses charged to revenue overthe financial period, expressed as a percentage of the average daily net asset values over the same period.

7

ContinuationReturn to Index�

�

Market value Total netInvestment Holding £’000 assets %

Portfolio statementAs at 31 July 2010

China – 23.9% (17.3%)Agricultural Bank of China 3,008,000 870 0.8 Aluminium Corp of China 1,284,000 729 0.7 Angang Steel 192,000 186 0.2 China Construction Bank ‘H’ 8,750,000 4,759 4.3 China Life Insurance ‘H’ 1,146,000 3,263 2.9 China National Building Material ‘H’ 1,318,000 1,597 1.4 China Petroleum & Chemical ‘H’ 3,394,000 1,751 1.6 China Shenhua Energy ‘H’ 849,000 2,098 1.9 China Vanke ‘B’ 1,297,298 1,086 1.0 CNOOC 1,986,000 2,141 1.9 Industrial & Commercial Bank of China ‘H’ 5,750,000 2,819 2.5 Jiangxi Copper ‘H’ 513,000 729 0.7 Tencent 196,000 2,424 2.2 Yanzhou Coal Mining 1,444,000 1,984 1.8

South Korea – 20.3% (19.1%)Daelim Industrial 34,400 1,244 1.1 GS Engineering & Construction 24,700 1,066 1.0 Hana Financial Group 51,497 981 0.9 Hyosung 24,000 1,063 1.0 Hyundai Heavy Industries 13,000 1,887 1.7 KB Financial Group 125,800 3,503 3.2 Korea Electric Power 67,000 1,203 1.1 LG Electronics 20,000 1,081 1.0 Lotte Shopping 7,700 1,484 1.3 POSCO 5,000 1,330 1.2 Samsung Electronics 11,898 5,210 4.7 Samsung Engineering 23,200 1,549 1.4 Shinsegae 2,400 734 0.7

Hong Kong – 18.6% (21.1%)BOC Hong Kong 769,000 1,262 1.1 Cheung Kong 224,000 1,735 1.6 China Resources Land 1,000,000 1,362 1.2 China Yurun Food Group 900,000 1,878 1.7 Glorious Property 6,295,000 1,317 1.2 GOME Electrical Appliances 4,723,000 1,050 0.9 Hang Lung Properties 663,000 1,765 1.6 Hidili Industries International Development 555,000 322 0.3 Hutchison Whampoa 207,000 874 0.8 Jardine Matheson 42,800 1,085 1.0 Kerry Properties 443,000 1,428 1.3 Li Ning 862,500 1,832 1.6 Lifestyle International 648,500 858 0.8 Orient Overseas International 250,000 1,253 1.1 Pacific Basin Shipping 1,201,000 582 0.5 Wharf 602,000 2,112 1.9

India – 11.3% (11.3%)Ambuja Cements 393,000 640 0.6 Bharat Heavy Electricals 33,000 1,112 1.0 HDFC Bank 85,000 2,499 2.2 Hindalco Industries 403,000 893 0.8 Infosys Technologies 50,000 1,927 1.7 Infrastructure Development Finance 350,000 900 0.8 Maruti Suzuki India 50,400 837 0.8 Reliance Industries 104,000 1,452 1.3 Rural Electrification 90,551 393 0.3 Tata Motors 100,000 1,170 1.1 Tata Power 44,000 804 0.7

Market value Total netInvestment Holding £’000 assets %

Taiwan – 11.2% (16.0%)Acer 840,423 1,445 1.3 Advanced Semiconductor Engineering 3,121,529 1,572 1.4 Compal Electronics 2,091,000 1,758 1.6 Formosa Plastic 766,980 1,028 0.9 Fubon Financial 756,000 596 0.5 Hon Hai Precision Industry 970,575 2,513 2.3 Innolux Display 1,671,000 1,160 1.0 MediaTek 95,684 832 0.7 Taishin Financial Holdings 1,779,623 509 0.5 Taiwan Fertilizer 657,000 1,168 1.0

Singapore – 4.9% (4.5%)CapitaLand 804,500 1,498 1.3 DBS Group 262,000 1,779 1.6 Keppel 232,000 1,019 0.9 Neptune Orient Lines 1,222,000 1,181 1.1

Thailand – 3.7% (3.8%)Bank of Ayudhya (Alien Market) 2,450,000 1,004 0.9 Banpu (Alien Market) 53,000 658 0.6 Krung Thai Bank (Alien Market) 3,452,000 879 0.8 PTT Chemical Public Company (Alien Market) 372,000 747 0.7 Siam Cement Non-Voting Depository Receipt 149,400 799 0.7

Indonesia – 2.3% (4.3%)Bank Danamon 1,654,000 635 0.6 Indo Tambangraya Megah 165,000 444 0.4 Telekomunikasi Indonesia ‘B’ 891,000 537 0.5 United Tractors 615,166 887 0.8

Malaysia – 1.6% (1.3%)Parkson Retail Group 1,626,000 1,782 1.6

Investment assets 108,543 97.8

Net other assets 2,417 2.2

Net assets 110,960 100.0

Unless otherwise stated the above securities are admitted to official stock exchange listings or trade on aregulated market.

The comparative percentage figures in brackets are at 31 January 2010.

8

ContinuationReturn to Index�

�

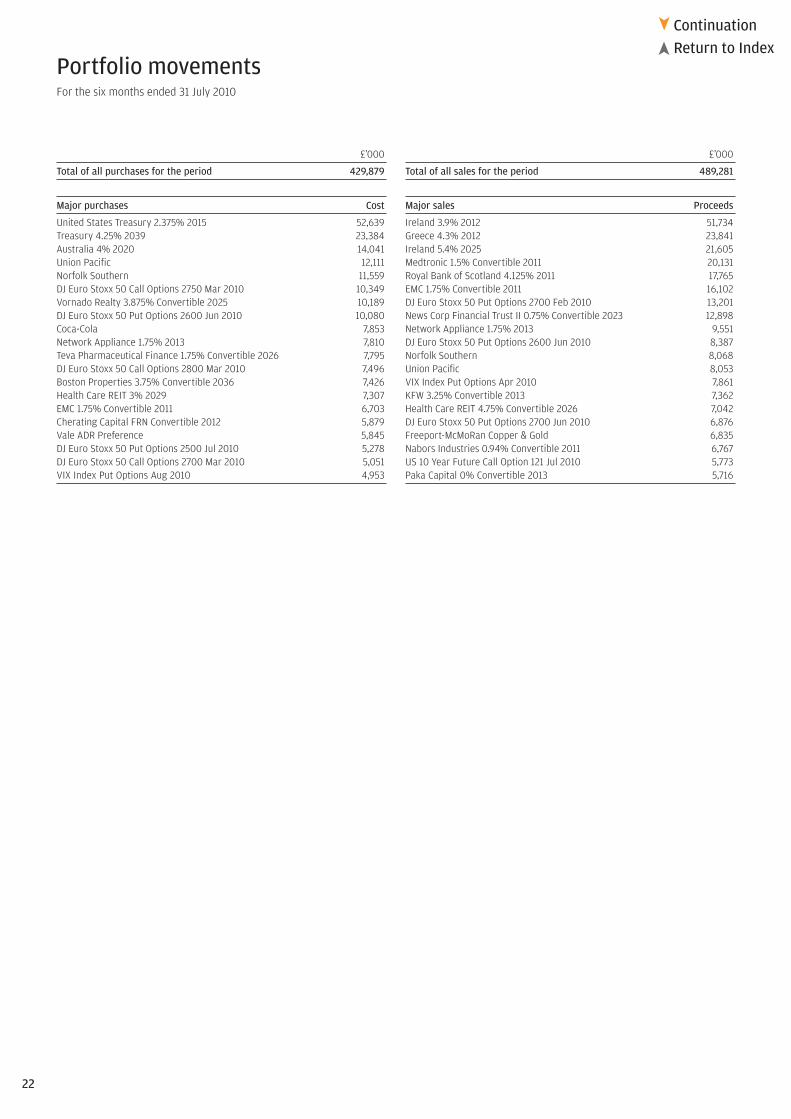

£’000

Total of all purchases for the period 53,339

Major purchases Cost

LG Electronics 2,847Yanzhou Coal Mining 2,501Glorious Property 2,093Hyundai Heavy Industries 1,915Krung Thai Bank 1,844BOC Hong Kong 1,542Neptune Orient Lines 1,488POSCO 1,346KB Financial Group 1,317China Life Insurance ‘H’ 1,108Tata Motors 1,060GOME Electrical Appliances 1,058Shin Kong Financial 1,026Siam Cement Non-Voting Depository Receipt 1,020ICICI Bank 962China Construction Bank ‘H’ 909Hyosung 908Samsung Electronics 898Hindalco Industries 879Acer 854

£’000

Total of all sales for the period 75,024

Major sales Proceeds

Samsung Electronics 3,631Shinhan Financial Group 2,492Industrial & Commercial Bank of China ‘H’ 2,244Kangwon Land 2,180China Mobile 2,037China Overseas Land & Investments 2,031Siam Cement Non-Voting Depository Receipt 1,954Jardine Matheson 1,727China Construction Bank ‘H’ 1,691China Steel 1,677Hindalco Industries 1,668Richtek 1,589LG Electronics 1,483United Microelectronics 1,359Siam Commercial Bank (Alien Market) 1,349Reliance Industries 1,338China Life Insurance ‘H’ 1,306Hong Kong Exchanges & Clearing 1,288PTT Chemical Public Company 1,254Bank Danamon 1,207

Portfolio movements For the six months ended 31 July 2010

9

Return to Index�

Financial statements

Statement of total return(Unaudited)

For the six months ended 31 July2010 2009

£’000 £’000 £’000 £’000

Income

Net capital gains 9,553 33,415

Revenue 1,659 1,168

Expenses (1,059) (799)

Net revenue before taxation 600 369

Taxation (144) (43)

Net revenue after taxation 456 326

Total return before distributions 10,009 33,741

Finance costs: Distributions (38) 31

Change in net assets attributable to shareholders from investment activities 9,971 33,772

Statement of change in net assets attributable to shareholders(Unaudited)

For the six months ended 31 July2010 2009

£’000 £’000 £’000 £’000

Opening net assets attributable to shareholders 122,291 88,632

Amounts receivable onissue of shares 4,145 8,545

Amounts payable on cancellation of shares (25,447) (8,542)

(21,302) 3

Change in net assets attributable to shareholders from investment activities (see above) 9,971 33,772

Closing net assets attributable to shareholders 110,960 122,407

As the comparatives in the above table are for the previous interim period, the Net assets at the end ofthat period will not agree to the Net assets at the start of the current period.

Balance sheet(Unaudited)

As at31 July 2010 31 January 2010

£’000 £’000 £’000 £’000

ASSETS

Investment assets 108,543 120,654

Debtors 588 4,677

Cash and bank balances 2,947 2,489

Total other assets 3,535 7,166

Total assets 112,078 127,820

LIABILITIES

Creditors (1,118) (5,528)

Distribution payable on income shares – (1)

Total liabilities (1,118) (5,529)

Net assets attributable to shareholders 110,960 122,291

10

ContinuationReturn to Index�

�

JPM Balanced Total Return Fund

Investment objective and policyTo achieve over a longer-term horizon higher returns than those availablefrom money market instruments denominated in Sterling by investingprimarily in equity securities, fixed income securities, convertible bonds andshort-term securities of issuers located in any country. The Fund may investin such securities issued by issuers in emerging countries worldwide.Additionally, subject to market conditions the Fund may invest up to 90%in cash and cash equivalents. Asset and country allocations may vary overtime to reflect market conditions and opportunities. The Fund may investup to 90% in government and public securities (see section 3.10(e) of thefull Prospectus). The Fund may use derivatives for investment purposes orEfficient Portfolio Management including hedging where appropriate.

Risk profileThis multi-asset Fund invests in equities (which may include investment inemerging markets and smaller companies), bonds, convertible bonds, cashand cash equivalents, typically maintaining a bias towards equities.

Equity investment is subject to specific risks relating to the performance ofthe individual companies held and the market’s perception of theirperformance. Equities are also subject to systematic risks such as generaleconomic conditions, inflation, interest rates, foreign exchange rates andindustry sector risks. In general terms, equities tend to be more volatile than bonds.

Bond prices can fluctuate significantly depending not only on the globaleconomic and interest rate conditions but also on the general credit marketenvironment and the creditworthiness of the issuer.

The investment policy of the Fund permits the use of derivatives and/orforward transactions for investment purposes, potentially increasing thevolatility and therefore risk of the Fund.

Total return funds seek to provide a positive return but this is not guaranteedand they should not be used as a substitute for traditional liquidity funds orcash accounts. As the priority of these funds is to provide positive returns,they will not perform in line with stock markets.

This Fund charges the fees of the ACD against capital, which will increasethe amount of income available for distribution to Shareholders, but mayconstrain capital growth. It may also have tax implications for certain investors.

Fund review• The six-month period to the end of July 2010 was a volatile time for markets.

In this environment, the Fund produced a positive return and outperformedits cash benchmark.

• We saw disappointing performance over the six month period in our GlobalDynamic stock picking module in comparison to the MSCI World Index,with positive excess returns coming only in March and April. The Fund’sequity sensitivity (delta) averaged around 55% but ranged from a high of75% to a low of 41%.

• Currency positions were negative over the period, with our short JapaneseYen versus Norwegian Krone trade suffering in May as the Yen strengthened.Fixed income positions were broadly positive, as several trades, includingan inflation-protected Australian bond position and particularly our longin German five- and ten-year government bonds added value, the latterdue to the flight to quality in May, which saw both German and US bondsrally. We also maintained a small allocation to convertibles over the period.

You should remember that past performance is not a guide to the future. The price of investments and the income from them may fall as well as rise andinvestors may not get back the full amount invested. For specific risks, please read the Simplified Prospectus.All performance returns are calculated using the quoted price of the accumulation shares. Performance returns are in Sterling.FX Adjusted returns have been calculated by JPMAM. Blended benchmarks have been calculated by JPMAM.Source: J.P. Morgan.

Fund outlook• Our outlook remains stable. We do not expect a global double-dip recession,

but continue to anticipate a slow and gradual recovery with both fixedincome and equity markets trading in broad ranges, possibly for manyyears to come. Over the rest of the year, we expect to continue favouringthe Asian and, to a lesser degree, European equity markets, where wefeel there is an attractive valuation discount.

Rolling 12 month performance as at 31 July2010/2009 2009/2008 2008/2007

JPM Balanced Total ReturnA-Class Acc 5.8% -3.8% -3.1%

JPM Balanced Total ReturnI-Class Acc 6.6% -3.1% -2.4%

Benchmark Index 0.5% 2.6% 6.0%

Six month performance31/01/10–31/07/10

JPM Balanced Total Return A-Class Acc 2.4%

Benchmark Index 0.3%

Fund statisticsFund size £11.9m

Benchmark Index 1 Month LIBOR GBP (Gross)

Fund chargesA-Class Initial 4.25%, Annual 1.50%I-Class Initial Nil, Annual 0.75%

Top ten holdings %Treasury 4.5% 2013 9.1Australia 4% 2020 3.9Canada 5% 2037 3.2Treasury 5% 2012 2.7Treasury 8% 2013 2.0KFW 3.25% Convertible 2013 1.5Nestle 0.7Chevron 0.6Cisco Systems 0.6Wells Fargo 0.6

ContinuationReturn to Index�

�

Sector breakdown %Equities 58.0Fixed interest securities 20.9Convertible bonds 2.2Forward currency contracts 1.5Options 0.5Futures 0.2Net other assets 16.7

In line with current accounting practice the sector breakdown includes the unrealised profit and loss onderivate holdings and consequently the economic market exposure of the Fund cannot be fully determinedfrom the above disclosure.

Highest/lowest share price and distribution recordDistribution

Highest Lowest per shareCalendar year share price share price (net)

A-Class Accumulation Shares

2006 52.63p 49.61p –

2007 55.17p 51.95p 0.64p

2008 54.89p 44.65p 0.95p

2009 53.46p 43.72p 1.02p

2010A 56.08p 51.12p 0.65p

A-Class Income Shares

2006 52.63p 49.61p –

2007 54.68p 51.56p 0.63p

2008 54.23p 43.32p 0.93p

2009 50.96p 42.24p 0.99p

2010A 53.14p 48.21p 0.59p

I-Class Accumulation Shares

2006 105.6p 99.26p –

2007 111.4p 104.4p 2.37p

2008 111.1p 90.89p 2.70p

2009 109.5p 89.20p 2.41p

2010A 115.4p 105.4p 1.53p

I-Class Income Shares

2006 105.6p 99.26p –

2007 109.6p 103.2p 2.34p

2008 108.6p 86.65p 2.62p

2009 102.4p 84.53p 2.27p

2010A 107.0p 97.24p 1.41p

A To 31 July 2010.

Portfolio turnover rate31.07.09 34.59%

31.07.10 15.67%

The portfolio turnover rate (PTR) reflects the total of security purchases and sales, less the total of shareissues and cancellations, expressed as a percentage of the average daily net asset values over the period.

Net asset values and Total expense ratiosNet assetvalue per Net asset Total

share class Number value per expenseDate £’000 of shares share ratio

A-Class Accumulation Shares

31.01.08 4,505 8,526,650 52.83p 1.72%

31.01.09 5,606 11,866,420 47.24p 1.67%

31.01.10 8,053 15,543,846 51.81p 1.68%

31.07.10 8,731 16,457,633 53.05p 1.68%

A-Class Income Shares

31.01.08 2,238 4,303,604 52.01p 1.74%

31.01.09 2,883 6,318,157 45.63p 1.67%

31.01.10 2,083 4,244,130 49.10p 1.68%

31.07.10 2,212 4,441,323 49.81p 1.68%

I-Class Accumulation Shares

31.01.08 897 839,337 106.9p 0.75%

31.01.09 809 840,337 96.29p 0.75%

31.01.10 496 465,872 106.4p 0.75%

31.07.10 510 465,872 109.5p 0.75%

I-Class Income Shares

31.01.08 863 830,000 104.0p 0.75%

31.01.09 758 831,000 91.24p 0.75%

31.01.10 440 445,722 98.68p 0.75%

31.07.10 449 446,722 100.5p 0.75%

The Net asset value and the Net asset value per income share are shown ex-dividend.

The total expense ratio (TER) takes into account the ACD fee and any fixed expenses charged to revenue overthe financial period, expressed as a percentage of the average daily net asset values over the same period.

11

Market value Total netInvestment Holding £’000 assets %

Portfolio statementAs at 31 July 2010

Equities – 58.0% (59.0%)United States of America – 27.9%Abbott Laboratories 947 30 0.2 ACE 602 20 0.2 Actuant ‘A’ 1,131 15 0.1 Adobe Systems 740 14 0.1 AerCap Holdings 1,580 13 0.1 AFLAC 833 27 0.2 Altria Group 2,346 33 0.2 American Electric Power 510 12 0.1 American Express 1,075 31 0.2 Ameriprise Financial 675 19 0.2 AmerisourceBergen 879 16 0.1 Anadarko Petroleum 1,133 36 0.3 Analog Devices 1,326 25 0.2 Apple 417 69 0.6 Ashland 529 18 0.2 AT&T 2,949 49 0.4 Atlas Air Worldwide Holdings 540 20 0.2 Autoliv 503 19 0.2 Axis Capital 690 14 0.1 Bank of America 6,618 60 0.5 Baxter International 861 24 0.2 BE Aerospace 1,109 21 0.2 Cameron International 453 11 0.1 Capital One Financial 784 21 0.2 Casey’s General Stores 420 10 0.1 CBS ‘B’ 1,493 14 0.1 Cephalon 427 16 0.1 Chevron 1,581 77 0.6 Cimarex Energy 527 23 0.2 Cisco Systems 4,959 74 0.6 Citigroup 23,103 61 0.5 Cognizant Technology Solutions 625 22 0.2 Comcast ‘A’ 2,030 25 0.2 Concho Resources 350 14 0.1 ConocoPhillips 550 19 0.2 Cooper 765 19 0.2 Cooper Industries 232 7 0.1 Cooper Tire & Rubber 897 12 0.1 Corning 1,518 18 0.2 CSX 915 31 0.2 Cummins 426 22 0.2 Danaher 842 21 0.2 Deere & Co 370 15 0.1 Dell 2,298 19 0.2 Devon Energy 409 16 0.1 Dow Chemical 1,183 21 0.2 Dr Pepper Snapple Group 900 21 0.2 DTE Energy 544 17 0.1 Eaton 338 17 0.1 El Paso 2,985 24 0.2 EMC 2,360 30 0.2 Emerson Electric 721 23 0.2 Endo Pharmaceutical 930 14 0.1 F5 Network 341 19 0.2 Finisar 1,340 15 0.1 Ford Motor Company 2,502 21 0.2 Forest Laboratories 750 13 0.1 Fossil 460 12 0.1 GameStop ‘A’ 1,196 15 0.1 Gannett 2,239 19 0.2 General Electric 6,005 62 0.5 Genworth Financial 2,440 25 0.2 Goldman Sachs Group 264 26 0.2 Goodrich 449 21 0.2 Google ‘A’ 120 37 0.3 Guess 1,077 25 0.2 Halliburton 752 15 0.1 Hartford Financial Services Group 1,023 15 0.1 Hess 573 20 0.2 Hewlett Packard 1,193 35 0.3 IBM 674 55 0.5 Intel 3,038 41 0.3 Interpublic Group 3,261 19 0.2 Jones Lang LaSalle 533 26 0.2 Kansas City Southern 500 12 0.1 Lam Research 510 14 0.1 Las Vegas Sands 1,234 21 0.2 Lennar 1,751 17 0.1 Lexmark International ‘A’ 584 14 0.1

Market value Total netInvestment Holding £’000 assets %

Lifepoint Hospitals 410 8 0.1 Limited Brands 957 16 0.1 Macy’s 2,111 25 0.2 Marathon Oil 878 19 0.2 Marvell Tech Group 1,576 15 0.1 McKesson 409 17 0.1 Mead Johnson Nutrition ‘A’ 565 19 0.2 Merck 2,912 65 0.5 Microsoft 2,096 35 0.3 Morgan Stanley 1,040 18 0.2 Motorola 2,950 14 0.1 Mylan Laboratories 2,031 23 0.2 Network Appliance 924 25 0.2 Newell Rubbermaid 1,785 18 0.2 Newfield Exploration 386 13 0.1 Newmont Mining 974 35 0.3 News Corp ‘B’ 2,363 22 0.2 Norfolk Southern 839 30 0.2 Northrop Grumman 480 18 0.2 Occidental Petroleum 502 25 0.2 ONEOK 750 22 0.2 Pfizer 5,963 58 0.5 Philip Morris International 891 29 0.2 Phillips Van Heusen 604 20 0.2 Pier 1 Imports 3,557 16 0.1 Pioneer Natural Resources 411 15 0.1 PNC Financial Services Group 653 25 0.2 Principal Financial Group 1,263 21 0.2 Progress Energy 676 18 0.2 Prudential Financial 968 35 0.3 QEP Resources 720 15 0.1 Qualcomm 1,034 26 0.2 Questar 970 10 0.1 Red Hat 845 17 0.1 Reynolds American 629 23 0.2 Rowan 1,004 16 0.1 Royal Caribbean Cruises 1,097 20 0.2 Sandisk 455 13 0.1 Smucker (J.M.) 480 19 0.2 Sothebys ‘A’ 1,183 21 0.2 Starbucks 825 13 0.1 Starwood Hotels ‘B’ 772 24 0.2 State Street 550 14 0.1 The Travelers Companies 521 17 0.1 TIBCO Software 2,320 20 0.2 Tiffany & Co 990 26 0.2 Time Warner 1,017 20 0.2 Time Warner Cable 402 14 0.1 Treehouse Foods 380 12 0.1 Tyson Foods ‘A’ 1,527 17 0.1 United Parcel Service ‘B’ 470 19 0.2 United Technologies 623 28 0.2 UNUM Group 970 14 0.1 US Bancorp 1,685 26 0.2 Veeco Fei Inccom 541 15 0.1 VF 438 22 0.2 Viacom ‘B’ 777 16 0.1 Walt Disney 1,052 23 0.2 Watson Pharmaceuticals 579 15 0.1 Wellpoint 471 15 0.1 Wells Fargo 4,084 73 0.6 Whirlpool 303 16 0.1 Whiting Petroleum 400 22 0.2 Williams-Sonoma 1,099 19 0.2 Xerox 4,189 26 0.2 Zimmer 510 17 0.1 United Kingdom – 7.6%Aggreko 892 14 0.1 Anglo American 1,022 26 0.2 AstraZeneca 714 23 0.2 Autonomy 926 15 0.1 Aviva 5,260 19 0.2 Barclays 11,645 39 0.3 BG Group 2,520 26 0.2 BP 10,341 42 0.3 British American Tobacco 1,153 26 0.2 Britvic 3,539 17 0.1 BT Group 12,205 17 0.1 Burberry Group 2,687 23 0.2 Cairn Energy 4,413 21 0.2 Centrica 6,370 20 0.2

1212

ContinuationReturn to Index�

�

13

ContinuationReturn to Index�

�

Portfolio statement – continuedAs at 31 July 2010

Market value Total netInvestment Holding £’000 assets %

Cookson Group 4,626 20 0.2 Enquest 11,332 13 0.1 Eurasian Natural Resources 2,308 21 0.2 GKN 13,287 18 0.2 GlaxoSmithKline 2,111 24 0.2 IMI 1,930 14 0.1 Inchcape 6,268 19 0.2 Informa 4,522 18 0.2 ING Groep 5,602 35 0.3 Intercontinental Hotels Group 1,586 18 0.2 Lloyds Banking Group 38,742 27 0.2 Man Group 8,418 19 0.2 Petrofac 1,287 16 0.1 Petropavlovsk 1,520 15 0.1 Prudential 3,128 18 0.2 Rio Tinto 1,323 44 0.3 Royal Bank of Scotland Group 37,609 19 0.2 Standard Chartered 3,352 63 0.5 Travis Perkins 1,744 15 0.1 Vodafone Group 47,867 72 0.6 Weir Group 1,236 14 0.1 WPP 3,088 21 0.2 Xstrata 3,503 36 0.3 Japan – 4.0%Aisin Seiki 1,000 18 0.2 Asahi Glass 4,000 26 0.2 East Japan Railway 600 25 0.2 Honda Motor 1,800 36 0.3 Isuzu Motors 9,000 17 0.1 Itochu 3,900 20 0.2 JX Holdings 3,700 13 0.1 Komatsu 1,600 22 0.2 Kubota 5,000 25 0.2 Marubeni 8,000 27 0.2 Mitsubishi 2,100 29 0.2 Mitsui & Co 1,700 14 0.1 Nidec 400 24 0.2 Nintendo 100 18 0.2 Nippon Telegraph & Telephone 1,000 27 0.2 Nissan Motor 4,200 21 0.2 Nitto Denko 600 13 0.1 Orix 400 20 0.2 Sumitomo Electric 3,200 24 0.2 Suzuken 800 18 0.2 Yahoo 76 19 0.2 Yamada Denki 380 16 0.1 France – 2.9%Alstom 550 18 0.2 AXA 3,077 36 0.3 BNP Paribas 874 38 0.3 Pernod-Ricard 432 22 0.2 PPR 351 30 0.2 Rhodia 1,779 24 0.2 Sanofi-Aventis 1,230 46 0.4 Schneider Electric 304 22 0.2 Societe Generale 987 37 0.3 Technip 467 20 0.2 TOTAL S.A. 1,603 52 0.4 Switzerland – 2.8%Compagnie Financiere Richemont ‘A’ 902 23 0.2 Credit Suisse 1,468 44 0.4 Holcim 505 22 0.2 Nestle 2,469 79 0.7 Novartis 1,918 60 0.5 Roche (Genusscheine) 298 25 0.2 Swatch Group 71 14 0.1 UBS 1,670 18 0.2 Zurich Financial Services 241 36 0.3 Germany – 2.1%BASF 673 25 0.2 Bayer 517 19 0.2 BMW 532 18 0.2 Deutsche Bank 582 26 0.2 Deutsche Telekom 2,195 19 0.2 E.ON 1,020 19 0.2 Lanxess 579 18 0.2 Linde 244 18 0.2 Siemens 415 26 0.2 Symrise 1,020 16 0.1 Volkswagen Non-Voting Preference 332 22 0.2

Market value Total netInvestment Holding £’000 assets %

Canada – 1.7%BCE 832 16 0.1 Lundin Mining 8,396 21 0.2 Niko Resources 270 18 0.2 Pacific Rubiales Energy 1,056 16 0.1 Quadra FNX Mining 1,670 13 0.1 Research In Motion 492 18 0.2 Talisman Energy 2,401 26 0.2 Teck Resources ‘B’ 867 19 0.2 Telus Corp 570 15 0.1 Telus Non-Voting 150 4 – Toronto-Dominion Bank 390 18 0.2 Western Canadian Coal 4,064 11 0.1 Netherlands – 1.2%Ahold 2,170 18 0.2 CSM 957 18 0.2 KPN 2,089 19 0.2 Philips Electronics 836 16 0.1 Royal Dutch Shell ‘A’ 3,405 60 0.5 Australia – 0.9%BHP Billiton 2,492 58 0.5 Challenger Financial Services Group 2,029 4 – Flight Centre 1,522 16 0.1 MacQuarie Group 983 21 0.2 Seek 3,578 15 0.1 China – 0.9%China Construction Bank ‘H’ 41,000 22 0.2 China Merchants Bank ‘H’ 19,357 33 0.2 CNOOC 22,000 24 0.2 Guangzhou R&F Properties ‘H’ 14,000 14 0.1 Yanzhou Coal Mining ‘H’ 14,000 19 0.2 Hong Kong – 0.8%Cathay Pacific Airways 14,000 20 0.2 Hang Lung Properties 12,000 32 0.2 Orient Overseas International 3,500 18 0.2 Wharf 5,000 18 0.2 Spain – 0.6%Banco Santander 3,371 28 0.2 Industria de Diseno Textil 554 24 0.2 Telefonica 1,959 28 0.2 Italy – 0.5%Intesa Sanpaolo 10,089 22 0.2 Telecom Italia 26,276 17 0.1 Unicredito Italiano 13,636 24 0.2 Mexico – 0.5%America Movil ADR 643 21 0.2 Banco Compartamos 3,356 12 0.1 NII Holdings 800 19 0.2 India – 0.4%ICICI Bank ADR 938 23 0.2 Yes Bank 5,133 21 0.2 South Korea – 0.4%Hyundai Motor 241 19 0.2 Samsung Electronics 56 24 0.2 Sweden – 0.4%Atlas Copco ‘A’ 2,320 24 0.2 Volvo ‘B’ 2,219 18 0.2 Denmark – 0.4%Carlsberg ‘B’ 397 23 0.2 D/S Norden 736 19 0.2 Belgium – 0.3%Bekaert 93 12 0.1 Delhaize Group 318 15 0.1 KBC Groep 517 15 0.1 Norway – 0.3%Acergy 1,668 17 0.1 Telenor 2,004 19 0.2 Taiwan – 0.3%Hon Hai Precision Industry GDR 2,650 15 0.1 Taiwan Semiconductor Manufacturing ADS 2,996 20 0.2 Brazil – 0.2%Petrobras ADS 1,082 25 0.2 Ireland – 0.2%Bank of Ireland 32,191 22 0.2 Singapore – 0.2%Singapore Airlines 3,000 22 0.2

14

ContinuationReturn to Index�

�

Market value Total netInvestment Holding £’000 assets %

Portfolio statement – continuedAs at 31 July 2010

Finland – 0.2%Metso 810 20 0.2 Indonesia – 0.2%Bank Rakyat Indonesia 26,000 18 0.2 Israel – 0.1%Teva Pharmaceutical Industries ADR 532 16 0.1

Fixed interest securities – 20.9% (18.8%)Sterling – 13.8%Treasury 5% 2012 £300,000 320 2.7 Treasury 4.5% 2013 £1,000,000 1,084 9.1 Treasury 8% 2013 £200,000 241 2.0 Australian Dollar – 3.9%Australia 4% 2020 AUD 500,000 465 3.9 Canadian Dollar – 3.2%Canada 5% 2037 CAD 500,000 376 3.2

Convertible bonds – 2.2% (2.8%)Euro – 1.9%KFW 3.25% Convertible 2013 u200,000 175 1.5 Rhodia 0.5% Convertible 2014 u121,200 46 0.4 Swiss Franc – 0.3%Pargesa 1.75% Convertible 2014 CHF 70,000 41 0.3

Forward currency contracts – 1.5% (0.6%)Australian DollarForward foreign currency position

16/09/10 £636,873 637 5.4 Forward foreign currency position

16/09/10 AUD (1,107,865) (637) (5.4)Canadian DollarForward foreign currency position

16/09/10 £244,266 244 2.0 Forward foreign currency position

16/09/10 CAD (371,431) (231) (2.0)Forward foreign currency position

16/09/10 £399,935 400 3.4 Forward foreign currency position

16/09/10 CAD (643,754) (401) (3.4)Danish KronaForward foreign currency position

16/09/10 £15,103 15 0.1 Forward foreign currency position

16/09/10 DKK (135,273) (15) (0.1)EuroForward foreign currency position

16/09/10 £83,611 84 0.7 Forward foreign currency position

16/09/10 u(100,000) (83) (0.7)Forward foreign currency position

16/09/10 £1,345,133 1,345 11.3 Forward foreign currency position

16/09/10 u(1,618,909) (1,352) (11.4)Hong Kong DollarForward foreign currency position

16/09/10 £285,965 286 2.4 Forward foreign currency position

16/09/10 HKD (3,277,684) (271) (2.3)Forward foreign currency position

16/09/10 HKD 1,571,357 130 1.1 Forward foreign currency position

16/09/10 £(133,119) (133) (1.1)Japanese YenForward foreign currency position

16/09/10 ¥11,835,808 88 0.7 Forward foreign currency position

16/09/10 $(136,000) (87) (0.7)Forward foreign currency position

16/09/10 £617,415 617 5.2 Forward foreign currency position

16/09/10 ¥(83,216,540) (618) (5.2)Forward foreign currency position

16/09/10 ¥6,246,102 46 0.4 Forward foreign currency position

16/09/10 £(46,869) (47) (0.4)

Market value Total netInvestment Holding £’000 assets %

Norwegian KroneForward foreign currency position

16/09/10 NOK 5,174,938 541 4.5 Forward foreign currency position

16/09/10 $(820,000) (527) (4.4)Forward foreign currency position

16/09/10 NOK 5,667,125 593 5.0 Forward foreign currency position

16/09/10 ¥(78,787,205) (585) (4.9)Singapore DollarForward foreign currency position

16/09/10 £75,904 76 0.6 Forward foreign currency position

16/09/10 SGD (156,460) (74) (0.6)Swedish KronaForward foreign currency position

16/09/10 £37,553 38 0.3 Forward foreign currency position

16/09/10 SEK (434,805) (38) (0.3)Swiss FrancForward foreign currency position

16/09/10 £405,702 406 3.4 Forward foreign currency position

16/09/10 CHF (682,900) (422) (3.5)US DollarForward foreign currency position

16/09/10 £4,223,095 4,223 35.5 Forward foreign currency position

16/09/10 $(6,250,613) (4,014) (33.7)Forward foreign currency position

16/09/10 $900,568 578 4.9 Forward foreign currency position

16/09/10 £(595,501) (596) (5.0)Forward foreign currency position

16/09/10 $914,825 587 4.9 Forward foreign currency position

16/09/10 u(735,000) (614) (5.2)

Options – 0.5% (0.0%)DJ Euro Stoxx 50 Put Options 2000 Sep 2010 58 2 – DJ Euro Stoxx 50 Put Options 2050 Dec 2010 (120) (33) (0.3)DJ Euro Stoxx 50 Put Options 2350 Dec 2010 120 70 0.6 Hang Seng Call Options 23000 Dec 2010 20 27 0.2

Futures – 0.2% (0.3%)AEX Index Futures Aug 2010 2 – – Australia 3 Year Bond Futures Sep 2010 (26) (1) – Australia 10 Year Bond Futures Sep 2010 (8) (7) (0.1)CAC40 10 Euro Futures Aug 2010 6 1 – Canada 10 Year Bond Futures Sep 2010 (11) (3) – DAX Index Futures Sep 2010 1 5 – DJ Euro Stoxx 50 Index Futures Sep 2010 (34) (8) (0.1)Euro BOBL Futures Sep 2010 16 – – Euro Bund Futures Sep 2010 31 14 0.1 FTSE 100 Index Futures Sep 2010 10 8 0.1 FTSE/MIB Index Futures Sep 2010 2 16 0.1 Hang Seng Index Futures Aug 2010 6 3 – H-Shares Index Futures Aug 2010 3 (1) – Long Gilt Futures Sep 2010 (3) (6) – MSCI Sing Index ETS Futures Aug 2010 (3) (1) – S&P 500 E-Mini Futures Sep 2010 (20) (5) – S&P/TSX 60 Index Futures Sep 2010 (3) – – SPI 200 Futures Sep 2010 (2) 3 – Swiss Market Index Futures Sep 2010 (4) 7 0.1 Topix Index Futures Sep 2010 3 (3) – US 2 Year Note Futures Sep 2010 (22) (14) (0.1)US 10 Year Note Futures Sep 2010 9 16 0.1

Investment assets 9,915 83.3

Net other assets 1,987 16.7

Net assets 11,902 100.0

Unless otherwise stated the above securities are admitted to official stock exchange listings or trade on aregulated market.

The comparative percentage figures in brackets are at 31 January 2010.

15

ContinuationReturn to Index�

�

Portfolio statement – continuedAs at 31 July 2010

Market value Portfolio credit ratings £’000

AAA 2,661BBB 41B+ 46

Total bonds 2,748

Equities 6,888Forward currency contracts 189Options 66Futures 24

Investment assets 9,915

16

ContinuationReturn to Index�

�

£’000

Total of all purchases for the period 3,938

Major purchases Cost

Canada 5% 2037 379DJ Euro Stoxx 50 Put Options 2350 Dec 2010 143Citigroup 67Royal Dutch Shell ‘A’ 61General Electric 48DJ Euro Stoxx 50 Put Options 2700 Jun 2010 34Goldman Sachs Group 34Altria Group 31Macy’s 31S&P 500 Call Options 1160 Apr 2010 30Forest Laboratories 29DJ Euro Stoxx 50 Put Options 2850 May 2010 28Lloyds Banking Group 28DJ Euro Stoxx 50 Put Options 2000 Sep 2010 28Philip Morris International 28Petrofac 27Xerox 27Hang Seng Call Options 23000 Dec 2010 27Sothebys ‘A’ 26Nikon 26

£’000

Total of all sales for the period 3,468

Major sales Proceeds

Procter & Gamble 75DJ Euro Stoxx 50 Put Options 2700 Jun 2010 71HSBC 65S&P 500 Call Options 1160 Apr 2010 55DJ Euro Stoxx 50 Put Options 2850 May 2010 44Michelin 0% Convertible 2017 43Wal-Mart Stores 38Royal Dutch Shell ‘B’ 35Bank of America 32ArcelorMittal 30Zimmer 30Mitsui & Co 30State Street 29Microsoft 29Anheuser-Busch InBev 28Royal Bank of Canada 27Estee Lauder ‘A’ 27Transocean 27Mitsubishi Electric 27Nomura Holdings 26

Portfolio movements For the six months ended 31 July 2010

17

Return to Index�

Financial statements

Statement of total return(Unaudited)

For the six months ended 31 July2010 2009

£’000 £’000 £’000 £’000

Income

Net capital gains 156 522

Revenue 147 156

Expenses (97) (73)

Net revenue before taxation 50 83

Taxation (9) (11)

Net revenue after taxation 41 72

Total return before distributions 197 594

Finance costs: Distributions (115) (125)

Change in net assets attributable to shareholders from investment activities 82 469

Statement of change in net assets attributable to shareholders(Unaudited)

For the six months ended 31 July2010 2009

£’000 £’000 £’000 £’000

Opening net assets attributable to shareholders 11,072 10,056

Amounts receivable on issue of shares 2,974 1,166

Amounts payable on cancellation of shares (2,317) (1,555)

657 (389)

Change in net assets attributable to shareholders from investment activities (see above) 82 469

Retained distributions on accumulation shares 91 87

Stamp duty reserve tax – (1)

Closing net assets attributable to shareholders 11,902 10,222

As the comparatives in the above table are for the previous interim period, the Net assets at the end ofthat period will not agree to the Net assets at the start of the current period.

Balance sheet(Unaudited)

As at31 July 2010 31 January 2010

£’000 £’000 £’000 £’000

ASSETS

Investment assets 10,071 9,156

Debtors 130 138

Cash and bank balances 2,035 2,038

Total other assets 2,165 2,176

Total assets 12,236 11,332

LIABILITIES

Investment liabilities (156) (132)

Creditors (165) (122)

Distribution payable on income shares (13) (6)

Total other liabilities (178) (128)

Total liabilities (334) (260)

Net assets attributable to shareholders 11,902 11,072

18

ContinuationReturn to Index�

�

JPM Cautious Total Return Fund

Investment objective and policyTo achieve over a medium-term horizon higher returns than those availablefrom money market instruments denominated in Sterling by investingprimarily in fixed income securities, convertible bonds, equity securities andshort-term securities of issuers located in any country. The Fund may investin such securities issued by issuers in emerging countries worldwide.Additionally, the Fund may invest up to 100% in cash and cash equivalents.Asset and country allocations may vary over time to reflect market conditionsand opportunities. The Fund may invest up to 100% in government andpublic securities (see section 3.10(e) of the full Prospectus). The Fund mayuse derivatives for investment purposes or Efficient Portfolio Management,including hedging, where appropriate.

Risk profileThis multi-asset Fund invests in bonds, convertible bonds, equities (whichmay include investment in emerging markets and smaller companies),cash and cash equivalents with a bias towards bonds.

Bond prices can fluctuate significantly depending not only on the globaleconomic and interest rate conditions but also on the general credit marketenvironment and the creditworthiness of the issuer.

Equity investment is subject to specific risks relating to the performance ofthe individual companies held and the market’s perception of theirperformance. Equities are also subject to systematic risks such as generaleconomic conditions, inflation, interest rates, foreign exchange rates andindustry sector risks. In general terms, equities tend to be more volatile than bonds.

The investment policy of the Fund permits the use of derivatives and/orforward transactions for investment purposes, potentially increasing thevolatility and therefore risk of the Fund.

Total return funds seek to provide a positive return but this is not guaranteedand they should not be used as a substitute for traditional liquidity funds orcash accounts. As the priority of these funds is to provide positive returns,they will not perform in line with stock markets.

Fund review• The six-month period to the end of July 2010 was a volatile time for markets.

In this environment, the Fund produced a positive return and outperformedits cash benchmark.

• May was a difficult month for the Fund, as we held too much directionalrisk and markets fell heavily, with previously profitable positions such asdividend futures coming under extreme selling pressure. March and Julywere good months for the Fund, as risk assets in general posted stronggains following periods of nervousness in markets.

• Over the review period, the Fund’s equity sensitivity (delta) averagedaround 11% but varied considerably from a high of 31% to a low of closeto 0%. We maintained an allocation of around 30% to convertibles overthe period. Fixed income positions worked well to diversify the portfolioin the correction period in February, with strong contributions from someof our more micro spread positions.

• We closed out all of our currency positions in the May de-risking. However,now that the market appears more orderly, we have re-entered into ourfavoured trades, although in smaller sizes.

You should remember that past performance is not a guide to the future. The price of investments and the income from them may fall as well as rise andinvestors may not get back the full amount invested. For specific risks, please read the Simplified Prospectus.All performance returns are calculated using the quoted price of the accumulation or income shares. Performance returns are in Sterling.FX Adjusted returns have been calculated by JPMAM. Blended benchmarks have been calculated by JPMAM.Source: J.P. Morgan.

Fund outlook• Our outlook remains stable. We do not expect a global double-dip recession,

but continue to anticipate a slow and gradual recovery with both fixedincome and equity markets trading in broad ranges, possibly for manyyears to come. We believe this is an environment in which relative valueand tactical risk exposure will likely produce more attractive risk-adjustedreturns than a buy-and-hold strategy.

Rolling 12 month performance as at 31 July2010/2009 2009/2008 2008/2007 2007/2006 2006/2005

JPM Cautious Total ReturnA-Class Acc 4.1% 0.5% 2.8% 5.1% 5.9%

JPM Cautious Total ReturnC-Class Inc 4.9% 1.2% – – –

JPM Cautious Total ReturnI-Class Acc 4.7% 1.1% 3.5% 5.7% 6.6%

Benchmark Index 0.5% 2.6% 6.0% 5.5% 4.7%

Six month performance31/01/10–31/07/10

JPM Cautious Total Return A-Class Acc 0.8%

Benchmark Index 0.3%

Fund statisticsFund size £759.3m

Benchmark Index 1 Month LIBOR GBP (Gross)

Fund chargesA-Class Initial 4.25%, Annual 1.25%C-Class Initial Nil, Annual 0.65%I-Class Initial Nil, Annual 0.65%

Top ten holdings %United States Treasury 2.375% 2015 7.0European Investment Bank 4.25% 2019 4.6Australia 3% 2025 4.0KFW 3.25% Convertible 2013 4.0Treasury 4.25% 2039 3.0Lloyds Banking Group 4% 2011 2.4Transocean 1.625% Convertible 2037 2.2Amgen 0.125% 2011 2.0Australia 4% 2020 1.9Boston Properties 2.875% Convertible 2037 1.5

19

ContinuationReturn to Index�

�

Sector breakdown %Fixed interest securities 31.4Convertible bonds 25.1Equities 17.6Options 2.0Forward currency contracts 1.2Swaps (0.1)Futures (0.3)Net other assets 23.1

In line with current accounting practice the sector breakdown includes the unrealised profit or loss onderivative holdings and consequently the economic market exposure of the Fund cannot be fully determinedfrom the above disclosure.

Highest/lowest share price and distribution recordHighest Lowest Distribution

Calendar year share price share price per share

A-Class Accumulation Shares

2005 52.74p 49.88p 0.34p

2006 54.77p 52.55p 1.10p

2007 58.73p 54.62p 1.40p

2008 59.58p 52.88p 1.45p

2009 60.07p 54.70p 0.81p

2010A 61.83p 58.68p 0.50p

A-Class Income Shares

2005 52.39p 49.88p 0.34p

2006 53.28p 51.70p 1.08p

2007 55.71p 52.84p 1.33p

2008 55.91p 49.21p 1.37p

2009 54.75p 50.34p 0.74p

2010A 56.21p 53.17p 0.46p

C-Class Income SharesB

2008 102.8p 90.73p 2.09p

2009 100.9p 92.76p 1.87p

2010A 103.7p 98.01p 1.25p

I-Class Accumulation Shares

2005 52.92p 49.89p 0.46p

2006 55.29p 52.85p 1.42p

2007 59.62p 55.15p 2.11p

2008 60.63p 53.94p 1.84p

2009 61.74p 55.94p 1.18p

2010A 63.68p 60.48p 0.82p

I-Class Gross Accumulation SharesC

2007 108.3p 99.90p 2.85p

2008 110.4p 98.57p 4.19p

2009 113.5p 102.5p 2.77p

2010A 117.2p 111.4p 1.83p

I-Class Income Shares

2005 52.43p 49.89p 0.46p

2006 53.32p 51.74p 1.39p

2007 55.77p 53.39p 1.66p

2008 55.96p 49.26p 1.72p

2009 54.80p 50.37p 1.06p

2010A 56.29p 53.20p 0.72p

A To 31 July 2010.B C-Class Income Shares were launched on 26 February 2008.C I-Class Gross Accumulation Shares were launched on 1 February 2007.

Portfolio turnover rate31.07.09 166.80%

31.07.10 73.23%

The portfolio turnover rate (PTR) reflects the total of security purchases and sales, less the total of shareissues and cancellations, expressed as a percentage of the average daily net asset values over the period.

Net asset values and Total expense ratiosNet assetvalue per Net asset Total

share class Number value per expenseDate £’000 of shares share ratio

A-Class Accumulation Shares

31.01.08 245,630 422,553,848 58.13p 1.40%

31.01.09 514,351 921,532,833 55.81p 1.42%

31.01.10 632,628 1,063,250,961 59.50p 1.42%

31.07.10 652,985 1,087,582,573 60.04p 1.43%

A-Class Income Shares

31.01.08 29,975 54,668,065 54.83p 1.41%

31.01.09 54,701 106,497,214 51.36p 1.39%

31.01.10 59,455 109,909,238 54.09p 1.43%

31.07.10 60,220 110,960,703 54.27p 1.43%

C-Class Income Shares

31.01.09 3,360 3,553,780 94.54p 0.77%

31.01.10 1,931 1,938,109 99.62p 0.77%

31.07.10 2,137 2,137,445 99.95p 0.77%

I-Class Accumulation Shares

31.01.08 3,383 5,729,451 59.04p 0.65%

31.01.09 8,301 14,551,847 57.04p 0.65%

31.01.10 13,781 22,522,053 61.19p 0.65%

31.07.10 12,792 20,650,872 61.94p 0.65%

I-Class Gross Accumulation Shares

31.01.08 18,727 17,443,833 107.4p 0.65%

31.01.09 23,486 22,483,966 104.5p 0.65%

31.01.10 22,797 20,253,443 112.6p 0.65%

31.07.10 24,454 21,416,254 114.2p 0.65%

I-Class Income Shares

31.01.08 3,875 7,068,045 54.83p 0.65%

31.01.09 4,748 9,244,378 51.36p 0.65%

31.01.10 5,831 10,780,377 54.09p 0.65%

31.07.10 6,678 12,306,598 54.26p 0.65%

The Net asset value and the Net asset value per income share are shown ex-dividend.

The total expense ratio (TER) takes into account the ACD fee and any fixed expenses charged to revenue overthe financial period, expressed as a percentage of the average daily net asset values over the same period.

20

ContinuationReturn to Index�

�

Market value Total netInvestment Holding £’000 assets %

Portfolio statementAs at 31 July 2010

Fixed interest securities – 31.4% (35.3%)US Dollar – 11.3%Amgen 0.125% 2011 $23,390,000 14,904 2.0Health Care REIT 3% 2029 $10,693,000 7,097 0.9Rayonier TRS Holdings 3.75% 2012 $5,380,000 3,713 0.5United States Treasury 2.375% 2015 $80,000,000 53,269 7.0Verizon Wireless Capital 5.5% 2014 $9,000,000 6,531 0.9Sterling – 8.0%Anglian Water Services Financing ‘A’

5.25% FRN 2015 £300,000 323 –Aviva 5.9021% 2020 £100,000 78 –Barclays Bank 10% 2021 £226,000 289 –Deutsche Telekom International Finance

7.125% 2012 £300,000 328 –Granite Master Issuer B3 FRN 2054 £350,000 259 –HSBC Finance FRN 2011 £300,000 300 –Lloyds Banking Group 4% 2011 £17,500,000 18,103 2.4Nationwide Building Society 3.75% 2011 £10,000,000 10,318 1.4Roche 5.5% 2015 £5,710,000 6,330 0.8Telereal Securitisation B6 FRN 2033 £1,300,000 670 0.1Treasury 4.25% 2039 £23,000,000 22,834 3.0Unilever 4% 2014 £1,120,000 1,188 0.2Windermere VIII A3 FRN 2015 £889,653 676 0.1Euro – 6.2%EDF 5.125% 2015 u2,100,000 1,948 0.3European Investment Bank 4.25% 2019 u38,000,000 34,886 4.6Magyar Nemzeti Vagyonkezelo 4.4% 2014 u4,300,000 3,484 0.5Rabobank Nederland 4.375% 2016 u3,498,000 3,141 0.4Sanofi-Aventis 3.5% 2013 u660,000 574 0.1Telefonica Emisiones 5.431% 2014 u2,100,000 1,890 0.3Australian Dollar – 5.9%Australia 4% 2020 AUD 15,200,000 14,123 1.9Australia 3% 2025 AUD 49,807,000 30,331 4.0

Convertible bonds – 25.1% (29.5%)US Dollar – 17.9%Boston Properties 3.625% Convertible 2014 $2,476,000 1,629 0.2Boston Properties 3.75% Convertible 2036 $11,240,000 7,766 1.0Boston Properties 2.875% Convertible 2037 $17,347,000 11,067 1.5Carnival Corp 2% Convertible 2021 $12,550,000 8,601 1.1Cherating Capital FRN Convertible 2012 $6,000,000 4,401 0.6Citigroup 7.5% Convertible Preference 2012 $30,654 2,395 0.3First Quantum Minerals 6% Convertible 2014 $2,300,000 2,010 0.3Gilead Sciences 0.625% Convertible 2013 $8,850,000 6,115 0.8Health Care REIT 4.75% Convertible 2013 $1,170,000 815 0.1Liberty Media FRN Convertible 2023 $10,713,000 7,548 1.0Life Technologies 1.5% Convertible 2024 $5,000,000 3,451 0.5Life Technologies 3.25% Convertible 2025 $7,310,000 4,963 0.7Medtronic 1.5% Convertible 2011 $5,770,000 3,695 0.5Nasdaq OMX 2.50% Convertible 2013 $6,120,000 3,796 0.5Prologis 3.25% Convertible 2015 $6,181,000 3,834 0.5Shire 2.75% Convertible 2014 $11,400,000 7,273 1.0Swiss Re FRN Convertible 2021 $9,140,000 5,563 0.7Symantec 1% Convertible 2013 $6,562,000 4,260 0.6Technology Data 2.75% Convertible 2026 $5,506,000 3,597 0.5Teva Pharmaceutical Finance 1.75%

Convertible 2026 $9,230,000 6,548 0.9Transocean 1.5% Convertible 2037 $7,200,000 4,270 0.6Transocean 1.625% Convertible 2037 $26,200,000 16,589 2.2Vornado Realty 3.875% Convertible 2025 $8,645,000 6,237 0.8Wells Fargo ‘A’ 7.5% Convertible Perpetual $12,408 7,767 1.0Euro – 6.0%AXA 2.5% Convertible 2014 u1,710,800 3,099 0.4KFW 3.25% Convertible 2013 u34,400,000 30,097 4.0KFW 1.5% Convertible 2014 u1,600,000 1,580 0.2Portugal Telecom International Finance

4.125% Convertible 2014 u7,000,000 5,873 0.8Rhodia 0.5% Convertible 2014 u12,256,800 4,696 0.6Swiss Franc – 0.7%Pargesa 1.7% Convertible 2013 CHF 8,535,000 5,114 0.7Singapore Dollar – 0.5%Capitaland 2.875% Convertible 2016 SGD 7,750,000 3,794 0.5

Market value Total netInvestment Holding £’000 assets %

Equities – 17.6% (17.8%)United States of America – 8.8%Abbott Laboratories 145,917 4,586 0.6Apple 22,127 3,667 0.5Celgene 70,996 2,446 0.3Coca-Cola 223,573 7,893 1.0Freeport-McMoRan Copper & Gold 89,334 4,056 0.5Hewlett Packard 234,547 6,982 0.9IBM 43,387 3,564 0.5McDonald’s 75,921 3,382 0.4Microsoft 236,905 3,959 0.5Newmont Mining 194,903 6,972 0.9Norfolk Southern 201,862 7,248 1.0The Mosaic Company 56,613 1,729 0.2Union Pacific 155,906 7,440 1.0Walt Disney 161,102 3,486 0.5United Kingdom – 2.8%3i Infrastructure 3,717,663 4,160 0.5BG Group 258,005 2,617 0.3British American Tobacco 188,548 4,175 0.5Reckitt Benckiser Group 118,331 3,705 0.5Unilever 208,142 3,790 0.5Vodafone Group 2,763,242 4,138 0.5China – 1.1%China Life Insurance ‘H’ 1,854,000 5,279 0.7China Shenhua Energy ‘H’ 1,180,000 2,916 0.4France – 0.8%Sanofi-Aventis 92,048 3,407 0.4TOTAL S.A. 96,600 3,144 0.4Brazil – 0.8%Vale ADR Preference 372,846 5,771 0.8Luxembourg – 0.7%ArcelorMittal 272,223 5,306 0.7Taiwan – 0.7%Hon Hai Precision Industry 1,157,000 2,995 0.4MediaTek 257,197 2,235 0.3Japan – 0.6%Daikin Industries 63,000 1,497 0.2Nidec 48,100 2,896 0.4Hong Kong – 0.5%Esprit 122,884 3,909 0.5Switzerland – 0.5%Nestle 987,400 3,942 0.5Singapore – 0.3%Wilmar International 832,000 2,455 0.3

Options – 2.0% (0.0%)DJ Euro Stoxx 50 Call Options 2850 Aug 2010 7,000 982 0.1DJ Euro Stoxx 50 Put Options 2350 Aug 2010 (2,216) (68) –DJ Euro Stoxx 50 Put Options 2650 Aug 2010 2,500 670 0.1Hang Seng Call Options 21400 Sep 2010 629 1,105 0.1Hang Seng Call Options 23000 Dec 2010 1,732 2,326 0.3Imm Euro¢ Put Options Sep 2010 (2,289) (28) –US 10 Year Future Call Options 125 Aug 2010 16,532 3,317 0.4US 10 Year Future Call Options 127 Aug 2010 (1,121) (62) –VIX Index Put Options Aug 2010 (20,200) (778) (0.1)VIX Index Put Options Aug 2010 51,760 5,815 0.8VIX Index Put Options Sep 2010 21,874 1,966 0.3

Forward currency contracts – 1.2% ((0.3)%)Australian DollarForward foreign currency position

23/08/10 £46,923,254 46,923 6.2Forward foreign currency position

23/08/10 AUD (82,912,123) (47,788) (6.3)Canadian DollarForward foreign currency position

23/08/10 £1,912,269 1,912 0.3Forward foreign currency position

23/08/10 CAD (3,070,968) (1,911) (0.3)

21

ContinuationReturn to Index�

�

Portfolio statement – continuedAs at 31 July 2010

Market value Total netInvestment Holding £’000 assets %

EuroForward foreign currency position

23/08/10 £156,712,009 156,712 20.6Forward foreign currency position

23/08/10 u(184,752,877) (154,235) (20.3)Forward foreign currency position

23/08/10 u9,000,000 7,513 1.0Forward foreign currency position

23/08/10 £(7,649,100) (7,649) (1.0)Japanese YenForward foreign currency position

23/08/10 £43,491,432 43,491 5.7Forward foreign currency position

23/08/10 ¥(5,836,293,534) (43,345) (5.7)Norwegian KroneForward foreign currency position

23/08/10 NOK 375,349,862 39,322 5.2Forward foreign currency position

23/08/10 £(39,033,490) (39,033) (5.1)Forward foreign currency position

23/08/10 NOK 344,730,722 36,115 4.8Forward foreign currency position

23/08/10 $(54,691,382) (35,115) (4.6)Singapore DollarForward foreign currency position

23/08/10 £6,346,252 6,346 0.8Forward foreign currency position

23/08/10 SGD (13,349,849) (6,294) (0.8)Swiss FrancForward foreign currency position

23/08/10 £8,371,546 8,372 1.1Forward foreign currency position

23/08/10 CHF (13,448,721) (8,310) (1.1)US DollarForward foreign currency position

23/08/10 £294,048,973 294,049 38.7Forward foreign currency position

23/08/10 $(449,150,263) (288,380) (38.0)Forward foreign currency position

23/08/10 $19,459,718 12,494 1.7Forward foreign currency position

23/08/10 £(12,553,044) (12,553) (1.7)

Swaps – (0.1)% (0.1%)Credit Default Swaps iTraxx Receive

20 Jun 2015 u80,000,000 60 –Goldman Sachs Interest Rate Swaps

Pay 3.02% 16 Jun 2015 CAD (62,400,000) (1,099) (0.1)Goldman Sachs Interest Rate Swaps

Receive 0.038% 16 Jun 2020 CAD 34,400,000 837 0.1Merrill Lynch Interest Rate Swaps

Pay 0.02705% 8 Jul 2015 CAD (62,400,000) (468) (0.1)Merrill Lynch Interest Rate Swaps

Receive 0.035325% 8 Jul 2020 CAD 34,400,000 332 –

Futures – (0.3)% (1.0%)Australia 3 Year Bond Futures Sep 2010 (1,229) (47) –Australia 10 Year Bond Futures Sep 2010 (603) (498) (0.1)DAX Index Futures Sep 2010 233 (142) –DJ Euro Stoxx 50 Futures Dec 2011 3,797 (1,293) (0.2)Euro BOBL Futures Sep 2010 356 10 –Euro Bund Futures Sep 2010 (1,870) 1,344 0.2Long Gilt Futures Sep 2010 614 313 –S&P 500 E-Mini Futures Sep 2010 (4,054) 332 –SGX S&P CNX Futures Aug 2010 (5,007) 497 0.1US 2 Year Note Futures Sep 2010 (1,678) (1,103) (0.2)US 10 Year Note Futures Sep 2010 (627) (1,091) (0.1)

Investment assets 583,642 76.9

Net other assets 175,624 23.1

Net assets 759,266 100.0

Unless otherwise stated the above securities are admitted to official stock exchange listings or trade on aregulated market.

The comparative percentage figures in brackets are at 31 January 2010.

Market value Portfolio credit ratings £’000

AAA 216,476AA+ 3,141AA- 300A+ 7,405A 12,861A- 28,967BBB+ 25,436BBB 63,647BBB- 24,276BB+ 18,637BB 3,834BB- 7,548B+ 4,696B 2,010C 6,796

Total bonds 426,030

Equities 135,747Options 15,245Forward currency contracts 8,636Swaps (338)Futures (1,678)

Investment assets 583,642

22

ContinuationReturn to Index�

�

£’000

Total of all purchases for the period 429,879

Major purchases Cost

United States Treasury 2.375% 2015 52,639Treasury 4.25% 2039 23,384Australia 4% 2020 14,041Union Pacific 12,111Norfolk Southern 11,559DJ Euro Stoxx 50 Call Options 2750 Mar 2010 10,349Vornado Realty 3.875% Convertible 2025 10,189DJ Euro Stoxx 50 Put Options 2600 Jun 2010 10,080Coca-Cola 7,853Network Appliance 1.75% 2013 7,810Teva Pharmaceutical Finance 1.75% Convertible 2026 7,795DJ Euro Stoxx 50 Call Options 2800 Mar 2010 7,496Boston Properties 3.75% Convertible 2036 7,426Health Care REIT 3% 2029 7,307EMC 1.75% Convertible 2011 6,703Cherating Capital FRN Convertible 2012 5,879Vale ADR Preference 5,845DJ Euro Stoxx 50 Put Options 2500 Jul 2010 5,278DJ Euro Stoxx 50 Call Options 2700 Mar 2010 5,051VIX Index Put Options Aug 2010 4,953

£’000

Total of all sales for the period 489,281

Major sales Proceeds

Ireland 3.9% 2012 51,734Greece 4.3% 2012 23,841Ireland 5.4% 2025 21,605Medtronic 1.5% Convertible 2011 20,131Royal Bank of Scotland 4.125% 2011 17,765EMC 1.75% Convertible 2011 16,102DJ Euro Stoxx 50 Put Options 2700 Feb 2010 13,201News Corp Financial Trust II 0.75% Convertible 2023 12,898Network Appliance 1.75% 2013 9,551DJ Euro Stoxx 50 Put Options 2600 Jun 2010 8,387Norfolk Southern 8,068Union Pacific 8,053VIX Index Put Options Apr 2010 7,861KFW 3.25% Convertible 2013 7,362Health Care REIT 4.75% Convertible 2026 7,042DJ Euro Stoxx 50 Put Options 2700 Jun 2010 6,876Freeport-McMoRan Copper & Gold 6,835Nabors Industries 0.94% Convertible 2011 6,767US 10 Year Future Call Option 121 Jul 2010 5,773Paka Capital 0% Convertible 2013 5,716

Portfolio movements For the six months ended 31 July 2010

23

Return to Index�

Financial statements

Statement of total return(Unaudited)

For the six months ended 31 July2010 2009

£’000 £’000 £’000 £’000

Income

Net capital gains 1,778 17,443

Revenue 11,103 10,496

Expenses (5,250) (4,490)

Net revenue before taxation 5,853 6,006

Taxation (160) (93)

Net revenue after taxation 5,693 5,913

Total return before distributions 7,471 23,356

Finance costs: Distributions (5,690) (5,826)

Change in net assets attributable to shareholders from investment activities 1,781 17,530

Statement of change in net assets attributable to shareholders(Unaudited)

For the six months ended 31 July2010 2009

£’000 £’000 £’000 £’000

Opening net assets attributable to shareholders 736,423 608,947

Amounts receivable on issue of shares 73,276 104,464

Amounts payable on cancellation of shares (56,386) (28,428)

16,890 76,036

Change in net assets attributable to shareholders from investment activities (see above) 1,781 17,530

Retained distributions on accumulation shares 4,221 4,240

Stamp duty reserve tax (49) (9)

Closing net assets attributable to shareholders 759,266 706,744

As the comparatives in the above table are for the previous interim period, the Net assets at the end ofthat period will not agree to the Net assets at the start of the current period.

Balance sheet(Unaudited)

As at31 July 2010 31 January 2010

£’000 £’000 £’000 £’000

ASSETS

Investment assets 591,379 629,878

Debtors 10,938 9,295

Cash and bank balances 170,613 118,077

Total other assets 181,551 127,372

Total assets 772,930 757,250

LIABILITIES

Investment liabilities (7,737) (15,653)

Creditors (5,746) (4,989)

Distribution payable on income shares (181) (185)

Total other liabilities (5,927) (5,174)

Total liabilities (13,664) (20,827)

Net assets attributable to shareholders 759,266 736,423

24

ContinuationReturn to Index�

�

JPM Emerging Markets Fund

Investment objective and policyTo provide long term capital growth by investing primarily in equity andequity-linked securities of emerging markets companies. Other instrumentsas permitted in the stated investment and borrowing powers of the Companyincluding, but not limited to, fixed interest securities, cash and cash equivalentsmay be held on an ancillary basis, as appropriate.

Risk profileThis equity based Fund is designed for investors looking for exposure toemerging markets which may include smaller company investments.

Equity investment is subject to specific risks relating to the performance ofthe individual companies held and the market’s perception of their performance.Equities are also subject to systematic risks such as general economic conditions,inflation, interest rates, foreign exchange rates and industry sector risks. Ingeneral terms, equities tend to be more volatile than bonds.

The Fund invests in emerging markets, which may be subject to additionalpolitical and economic risks, low liquidity, poor transparency and greaterfinancial risks.

The underlying assets of the Fund are denominated in currencies other thanSterling and are not hedged back to Sterling. Investors will therefore beexposed to the currency risk of fluctuations between Sterling and the currencydenomination of the underlying assets.

Fund review• Emerging markets have produced modest returns so far this year in

comparison to their strong growth in 2009. The period saw significantvolatility as investors had already discounted much of the short-termrecovery in earnings and then had to contend with rising inflation andinterest rates, concerns over the Chinese economy overheating, and fearsof credit default in the periphery of Europe.

• There was a significant discrepancy in performance by region as Asia hitdouble figures while eastern Europe fell into negative territory. Brazilunderperformed Latin America as fears over Chinese and global growthaffected markets. In EMEA, Poland and Hungary were particularly badlyhit as nervousness over the European debt crisis spread to the region.

• The Fund outperformed its benchmark during the period. Stock selectionin China, Indonesia and Russia was positive for performance. Underweightpositions in Taiwan and Russia and an overweight in Mexico also contributedto returns while stock selection in Brazil and Taiwan detracted. Investmentsin Argentina and an underweight in Thailand also had a negative impacton performance.

Fund outlook• We continue to believe in a half-speed developed market recovery giving

way to a half-speed expansion. While not expecting a relapse in the globalcycle, we note that emerging markets retain far greater policy flexibilitythan developed markets. This is most evident in fiscal terms but alsoapplies to monetary policy as many emerging market central banks havestarted to raise rates, albeit not aggressively, and so may cut again ifneeded.

You should remember that past performance is not a guide to the future. The price of investments and the income from them may fall as well as rise andinvestors may not get back the full amount invested. For specific risks, please read the Simplified Prospectus.All performance returns are calculated using the quoted price of the accumulation shares. Performance returns are in Sterling.FX Adjusted returns have been calculated by JPMAM. Blended benchmarks have been calculated by JPMAM.Source: J.P. Morgan.Benchmark Source: MSCI. Neither MSCI nor any other party involved in or related to compiling, computing or creating the MSCI data makes any express of implied warranties or representations with respect to such data(or the results to be obtained by the use thereof), and all such parties hereby expressly disclaim all warranties of originality, accuracy, completeness, merchantability or fitness for a particular purpose with respect toany of such data. Without limiting any of the foregoing, in no event shall MSCI, any of its affiliates or any third party involved in or related to compiling computing or creating the data have any liability for any direct,indirect, special, punitive, consequential or any other damages (including lost profits) even if notified of the possibility of such damages. No further distribution or dissemination of the MSCI data is permitted withoutMSCI’s express written consent.

• With the strong boost to industrial production from inventory restockingnow waning, we are more confident in being underweight cyclical stocks.Any moderation in global growth will naturally feed through to earningsexpectations in both emerging markets and developed markets.

Rolling 12 month performance as at 31 July2010/2009 2009/2008 2008/2007 2007/2006 2006/2005

JPM Emerging MarketsA-Class Acc 27.0% 0.1% -0.4% 35.9% 23.0%

JPM Emerging Markets B-Class Acc 27.7% – – – –

JPM Emerging MarketsI-Class Acc 27.8% 0.8% 0.2% 36.7% 23.8%

Benchmark Index 27.0% -0.6% -1.9% 38.3% 21.1%

Six month performance31/01/10–31/07/10

JPM Emerging Markets A-Class Acc 11.8%

Benchmark Index 10.2%

Fund statisticsFund size £818.1m