Languages

Pages

Legal

volvofinans bank ab

inTERiM REPoRT1 JanUaRY - 30 JUnE 2010

The economic growth we saw during the first quarter has continued,

which is indicated by, among other things, the increase in car sales

in Sweden. The number of new registrations is expected to exceed

275 000 units for 2010, which is above the normal level.

Ford’s sale of Volvo Personvagnar AB to the Chinese company

Geely was completed at the beginning of August. The Volvo

dealerships are optimistic, and the order book situation is very positive.

The situation is the same for both Renault and Ford sales.

Other brands that are sold through the Swedish Volvo

dealerships are also moving well, as are trucks,

which are showing increased sales volumes in

all sectors. All in all, we are approaching the

autumn with an air of optimism.

Not least since sales volumes have been

increasing since March. The increase is

affected, not only by new but also used vehicle

sales as well as sales at workshops, which have

been very busy. This benefits Volvofinans Bank

through increased usage of the Volvo Card and Volvo

Truck Card. In addition, we have continued high volumes of fuel.

Sweden’s Riksbank, as expected, raised interest rates at the

beginning of July with the motivation that the Swedish economic

situation is improving. There is also a desire to indicate to Swedish

households that we are moving away from the low interest rate

levels we have had since the beginning of 2009. The indication also

given by a flatter interest curve is that future market interest rates will

remain at reasonable levels, which is positive for car sales.

In April we decided not to apply for a renewal of our affiliation

to the Swedish government’s bank guarantee scheme after the

expiry of our contract on 30th April. The general opinion is that the

Swedish financial market’s functionality have largely recovered from

the effects of the financial crisis. Volvofinans Bank has not taken

advantage of the programme since 3 July 2009, but has instead

financed itself on the market without this guarantee.

Volvofinans Bank reports a successful first half of the year with a profit

of SEK 109.6 million (86.1), an improvement of SEK 23.5 million or

27 %. The stronger profit is the result of somewhat higher margins

and an adaptation of costs. The adaptation of margins to the higher

interest rate levels will not, however, have a significant effect until the

third quarter.

Lending volumes fell slightly (1 %) compared to the previous year,

mainly due to lower vehicle sales in 2009 of both cars and

trucks. The increase in vehicle sales during 2010 will have

a significant effect, first during the second half of the

year. Furthermore the sale of used vehicles has been

historically low at Volvo dealerships, but is now

starting to return to normal. Credit card business

remains at about the same level as last year, but

has increased over recent months.

Credit losses are, as expected, remaining at a low

level and as previously only concern card portfolios.

The increase in losses that has occurred with card

transactions is mainly due to the recession.

As previously, the financing of vehicles shows no losses, which

proves that our business model with the Swedish Volvo dealerships

works well even in times of economic turmoil. Nor has there been

any significant increase in Volvo dealerships’ credit losses during the

period. The Swedish Volvo dealerships’ overall operating profit for the

whole of 2009 increased by just over SEK 400 million and has now

reverted to “normal” levels.

A strong core capital ratio, an historically stable business model

with the Volvo dealerships, the close cooperation with Volvo Cars and

Volvo Trucks, continued minimal credit loss with card transactions

and increased deposit volumes from the general public cause us to

see the future as bright.

MEssaGE fRoM THE PREsiDEnT

The information contained in this report is that which Volvofinans Bank AB (publ), corporate ID no. 556069-0967 is obliged to publish in

accordance with the Swedish Securities Market Act (SFS 2007:528). This report was submitted for publication at 4.30 p.m. on 20 August 2010.

In the event of conflict in interpretation or differences between this annual report and the Swedish version, the latter will prevail.

“The first half of the year has been positive for

Volvofinans Bank”

2

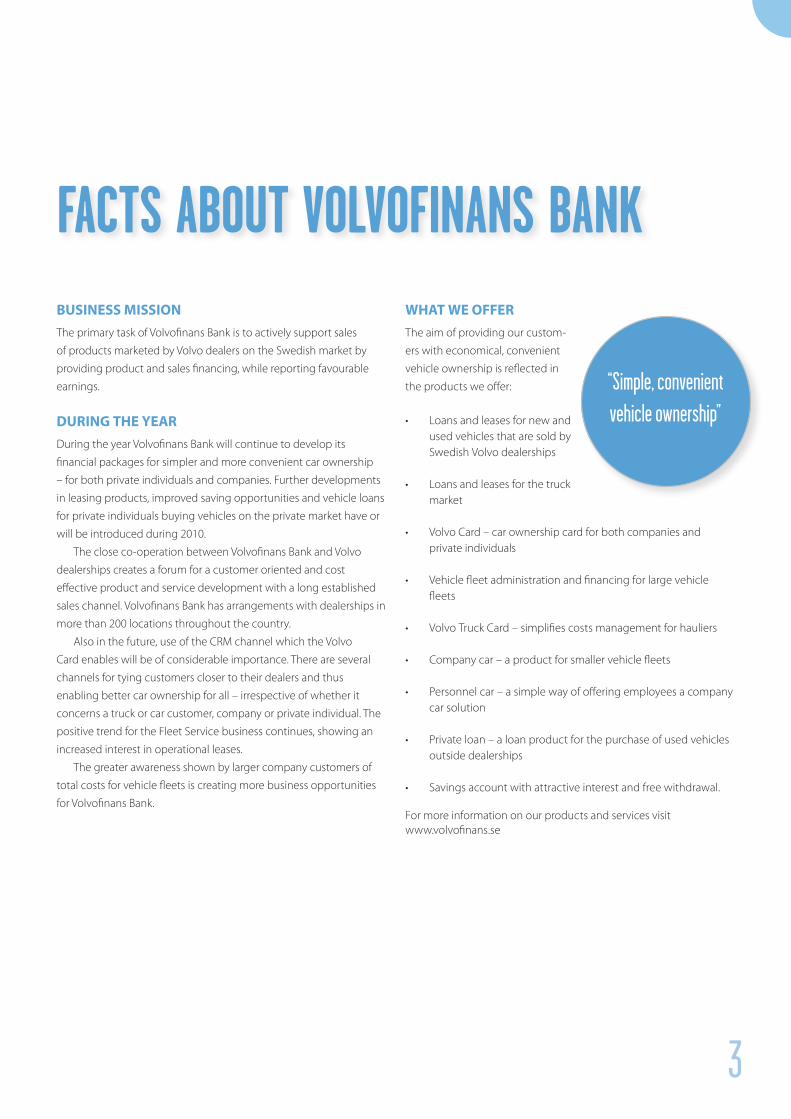

BUSINESS MISSIONThe primary task of Volvofinans Bank is to actively support sales

of products marketed by Volvo dealers on the Swedish market by

providing product and sales financing, while reporting favourable

earnings.

DURING THE YEARDuring the year Volvofinans Bank will continue to develop its

financial packages for simpler and more convenient car ownership

– for both private individuals and companies. Further developments

in leasing products, improved saving opportunities and vehicle loans

for private individuals buying vehicles on the private market have or

will be introduced during 2010.

The close co-operation between Volvofinans Bank and Volvo

dealerships creates a forum for a customer oriented and cost

effective product and service development with a long established

sales channel. Volvofinans Bank has arrangements with dealerships in

more than 200 locations throughout the country.

Also in the future, use of the CRM channel which the Volvo

Card enables will be of considerable importance. There are several

channels for tying customers closer to their dealers and thus

enabling better car ownership for all – irrespective of whether it

concerns a truck or car customer, company or private individual. The

positive trend for the Fleet Service business continues, showing an

increased interest in operational leases.

The greater awareness shown by larger company customers of

total costs for vehicle fleets is creating more business opportunities

for Volvofinans Bank.

WHAT WE OFFERThe aim of providing our custom-

ers with economical, convenient

vehicle ownership is reflected in

the products we offer:

• Loans and leases for new and used vehicles that are sold by Swedish Volvo dealerships

• Loans and leases for the truck market

• Volvo Card – car ownership card for both companies and private individuals

• Vehicle fleet administration and financing for large vehicle fleets

• Volvo Truck Card – simplifies costs management for hauliers

• Company car – a product for smaller vehicle fleets

• Personnel car – a simple way of offering employees a company car solution

• Private loan – a loan product for the purchase of used vehicles outside dealerships

• Savings account with attractive interest and free withdrawal.

For more information on our products and services visit www.volvofinans.se

“Simple, convenient vehicle ownership”

faCTs aboUT volvofinans bank

3

OWNERSHIp SITUATIONSince its establishment in 1959, Volvofinans Bank has been 50 %

owned by Swedish Volvo dealerships via their holding company AB

Volverkinvest. The Sixth Swedish National Pension Fund (AP-fonden)

owns 40 % and Volvo Car Corporation (Volvo Personvagnar AB) 10 %.

The primary task of Volvofinans Bank is to actively support sales of

products marketed by Volvo dealers on the Swedish market by provid-

ing product and sales financing, while reporting favourable earnings.

Volvofinans Bank AB is the parent company in a Group with a

dormant subsidiary. The subsidiary, Volvofinans Konto Bank AB, was

liquidated in June following withdrawal, by the Swedish Financial

Supervisory Authority on the company’s request, of permission to

conduct banking operations.

VOlUMES/lENDINGSales of new passenger cars in Sweden rose by 34 % compared with

the same period in the previous year. In total 138 079

passenger vehicles were registered (102 794). The

number of Volvo, Renault and Ford registrations

was 40 032 (29 759), and the combined market

share of Volvo and Renault was 29 % (29).

42 % (41) of all passenger car business, new

and used, within the Swedish Volvo dealerships

generates a financial contract with Volvofinans

Bank. New and used vehicle penetration is 45 %

and 38 % respectively. Volvofinans Bank finances the

Swedish Volvo dealers’ truck sales, apart from those that

take place through the AB Volvo-owned Volvo Truck Centre.

Penetration for new trucks was 48 % (50). The total contract portfolio

(loan and leasing contracts) amounted to 187 441 contracts (187 212).

The truck and bus element of the contract portfolio amounts to

8 333 contracts (8 492), which is just over 4 %.

The number of corporate customers for whom Svensk

Vagnparksfinans manages the car administration remains stable.

Administration with cost follow-up was being provided for 31 289

cars (32 491) at the end of the reporting period.

Goods and services purchased using the Volvo Card totalled

approximately SEK 5 billion, and the number of accounts actively

purchasing is half a million per month. Goods and services for SEK

261 million were bought with Volvo Truck Card via the 22 600 card.

The total lend volume for the Group amounted to SEK 22.3 billion

as opposed to SEK 22.6 billion for the previous year.

The truck and bus share of lending was SEK 3.6 billion (3.8), which

corresponds to 16 % of total lending for the previous year.

The Group’s primary segments are the business lines of the

passenger car market and truck market. The geographic distribution

reflects the Group as a whole. The passenger car market segment

includes financing for passenger cars through loans and leases,

vehicle administration and the Volvo Card. The truck market segment

includes financing for trucks and buses as well as Volvo Truck Card.

The operating income, operating profit, number of contracts and

lending volumes for Volvofinans Bank’s lines of business are presented

below. Operating income is defined as the net of interest income,

interest expenses, leasing net, dividends received, net result of

financial transactions, commission income and commission expenses.

Jan-June 2010 Cars Trucks Group

Assets, SEK million (average) 19 696 4 111 23 807

Lending volume, SEK million (average) 19 200 3 979 23 179

Operating revenue, SEK T 247 154 16 138 263 293*

Operating profit, SEK T 102 738 6 895 109 633

Expenses, SEK T 135 873 8 447 144 320*

Number of contracts (average) 209 511 8 298 217 809

Expenses are defined as general administration

expenses and other operating expenses.

Volvofinans Bank is of the opinion that it is not

relevant to divide up its liabilities among the vari-

ous segments. Borrowing is determined by the

total requirement and cannot be attributed to a

specific segment.

INcOMEVolvofinans Bank’s income before credit loss is

SEK 119.0 million (93.0). The primary reason for this improvement

is higher margins and greater interest rate stability. Income

before appropriations and taxes for the period rose by 27 % to

SEK 109.6 million (86.1).

cREDIT RISkS AND cREDIT lOSSESThe Group’s credit risk continues to be very low as most of the credit

risks and residual value risks are borne by the Volvo dealerships.

Problem credits are all receivables that are overdue by more than

90 days. Volvofinans Bank’s problem credits for credit card receivables

total SEK 129.9 million (112.2) and for loan and lease lending

SEK 154.1 million (157.8). The increase in problem credits is due to an

AB Volverk-invest

50 %

VolVofinAns BAnk AB

The swedish Volvo

dealers

sixth AP-fund

10 %40 %Volvo

Personvagnar AB

“Volvofinans Bank’s income

before credit loss expenses

is SEK 119.0 million (93.0)”

30/06/2010 number of contracts

Average contract, sEk T

Collateral value, sEk million

Drawn credit, sEk million

loan to value ratio

Market value, sEk million

surplus, sEk million

surplus,per cent

Loans 114 642 98 11 261 10 814 96 % 16 844 6 030 56 %

Leases 72 799 151 10 966 8 807 80 % 10 697 1 890 21 %

Total 187 441 119 22 227 19 621 88 % 27 541 7 920 40 %

* The amounts differ from the Group’s operating income and expenses because the follow-up of seg-ment performance occurs without any Group eliminations and reclassification

of operational lease assets as finance lease assets.

4

5

increase in the average liability for credit cards, partly as the result of

higher fuel prices and the economic depression. The dealers bear the

credit risk through recourse agreements for the greater part,

SEK 150.1 million, of the problem credits relating to loans and leases.

There are no loans for which interest concessions have been agreed,

and no property has been received to provide security for receivables.

The confirmed customer losses mainly concern credit card-

transactions. Anticipated credit loss impairment for the household

segment is determined using statistical risk models and for the

corporate segment by means of a manual review.

Amounts in sEk T Group Parent Company

Jan-June 2010

Jan-June 2009

Jan-June 2010

Jan-June 2009

Confirmed credit losses

Confirmed credit losses - 8 674 - 5 327 - 8 674 - 5 327

Recovered losses 43 57 43 57

Total - 8 631 - 5 270 - 8 631 - 5 270

Provisions for credit risk

Reserve for anticipatedcredit losses - 710 - 1 542 - 710 - 1 542

Credit losses, net - 9 341 - 6 812 - 9 341 - 6 812

cApITAl pROcUREMENTFinancial instability has occurred periodically during the first half of the

year causing borrowing margins to increase and later fall back. Liquid-

ity on the market has remained good however, and Volvofinans Bank

has successfully borrowed funds in both the short and long term on

the market via the bank’s commercial paper and MTN programmes re-

spectively. Total outstanding financing on the Swedish and European

capital markets amounted to SEK 11.6 billion at the end of the first half

year.

Volvofinans Bank decided not to apply for a renewal of its

affiliation to the Swedish government’s bank guarantee scheme after

the expiry of its contract on 30th April, 2010.

In addition to market borrowing, operations were financed by

the amount of SEK 4.3 billion in the form of bank loans, as well as

customer deposits of SEK 2.3 billion at the end of the first half year. At

the end of the period, 61 % of long-term financing had a remaining

term of more than one year.

RATINGVolvofinans Bank has international credit ratings from Moody’s

Investors Service as follows:

• Short-term financing: P-2

• Long-term financing: Baa2

On 10th May, Moody’s announced that Volvofinans Bank’s rating

for long-term borrowing had been lowered by one level from Baa1 to

Baa2. The rating for short-term borrowing, P-2, was confirmed at the

same time. Moody´s analysis is available for viewing on our website,

www.volvofinans.se.

FINANcIAl RISkSAs the Group operates within the financial sector, the company is

continuously exposed to a number of financial risks.

Liquidity risk is the risk that Volvofinans Bank’s payment obligations

cannot be met on maturity without significant costs in terms of the

means of payment or – in a worst-case scenario – cannot be met by

any means. For shorter periods of liquidity instability, Volvofinans Bank

has a daily surplus liquidity of SEK 500 – 1 500 million. In order to secure

its ability to pay, Volvofinans Bank has entered into agreements with

banks concerning credit facilities that can be utilised at short notice.

Borrowing with a remaining period of less than one year must be

covered at all times by undrawn credit facilities. The total volume of

available facilities at the end of the first half year was SEK 9.6 billion.

Interest rate risk is the current and future risk that net interest

income declines as a result of unfavourable changes in the interest

rate. The vast majority of Volvofinans Bank’s lending and all borrowing

follow the short-term market interest rate, which involves a limited

interest rate risk.

Currency risk is the risk of unfavourable changes in exchange

rates. All of Volvofinans Bank’s lending is in Swedish kronor and any

borrowing in foreign currency is hedged, thus Volvofinans Bank is not

exposed to fluctuations in exchange rates.

cApITAl ADEQUAcYCapital adequacy means that capital requirements are connected to

the total risk profile of the institute, which in the case of Volvofinans

Bank entails a lower minimum capital requirement.

Volvofinans Bank calculates the capital requirement for credit risk

using the standardised method, which means that all exposures are

allocated to one of fifteen exposure categories with a different risk

weighting for each category.

The capital requirement for operational risk is calculated using the

base indicator method, which means that the capital requirement is

15 % of the average operating income for the last three financial years.

EVENTS AFTER THE BAlANcE SHEET DATENo other significant events have occurred since the end of the

reporting period.

INTERIM REpORTThe interim report provides a true and fair overview of the business, financial position and results of the Parent Company and the

Group and describes significant risks and uncertainty factors with which the Parent Company and the companies forming part of

the Group are faced.

Gothenburg, August 2010

Bert Björn

President

Volvofinans Bank AB

Urmas K ruusval

Chairman of the board

Head of Direct Investments,

Sixth Swedish National Pension Fund,

Gothenburg

Tommy Andersson

Chairman of The Volvo Dealer

Association,

Gothenburg

Thomas Andersson

President, Volvo Personbilar Sverige AB,

Gothenburg

Bob Persson

President, AB Persson Invest,

Östersund

Jan Pettersson

President and CEO, Bilia AB,

Gothenburg

Per Rinder

Senior Adviser, Sixth Swedish National

Pension Fund,

Stockholm

The report for 30 September will be published on 17 November 2010 and will be available on our website www.volvofinans.se

If you have any questions, please contact our President, Bert Björn, on +46 (0)31 83 88 00.

This report has not been the subject of special examination by the company’s auditors.

6

Amounts in sEk million

Parent Company 30/06/2010 Parent Company 30/06/2009

Capital base

Capital base 3 066 2 971

Core capital 2 859 2 761

Supplementary capital 207 210

Capital requirement

Capital requirement for credit risk using the standardised method 1 544 1 582

Capital requirement for operational risk using the base indicator method 87 89

Total minimum capital requirement pursuant to Basel II 1 631 1 671

Total minimum capital requirement pursuant to Basel I 1 829 1 886

Measurement of capital adequacy

Capital adequacy ratio 1.88 1.77

Capital adequacy level 15.04 14.16

Core capital ratio 14.02 13.15

Information concerning capital adequacy disclosed by the Parent Company Volvofinans Bank AB is set out above since the Group is not part of a financial corporate group. The capital adequacy amount is translated from 2009 because of changes in the calculation of risk-weighed amount (adjustment with respect to operational risk).

Amounts in sEk T

Group Parent Company

Jan-Jun 2010 Apr-Jun 2010 Jan-Jun 2009 Apr-Jun 2009 Jan-Jun 2010 Apr-Jun 2010 Jan-Jun 2009 Apr-Jun 2009

Interest income 250 206 124 649 355 270 146 631 196 906 99 737 266 035 114 782

Lease income 350 536 202 808 125 497 62 361 1 220 810 613 501 1 169 840 569 534

Interest expense - 137 192 - 71 659 - 263 489 - 95 522 - 137 192 - 71 659 - 263 489 - 95 522

Dividends received - - - - - - - -

Net result of financial transactions* - 866 204 2 841 3 088 - 866 204 2 841 3 088

Commission income 150 410 78 718 144 351 74 914 150 410 78 718 144 351 74 914

Commission expenses - 20 739 - 9 971 - 15 659 - 8 095 - 20 739 - 9 971 - 15 659 - 8 095

Total operating income 592 355 324 749 348 811 183 377 1 409 329 710 530 1 303 919 658 701

General administration expenses - 115 978 - 57 392 - 114 639 - 57 904 - 115 978 - 57 392 - 114 639 - 57 904

Depreciation of property, plant and equipment - 338 945 - 195 309 - 125 267 - 63 479 - 1 155 919 - 581 090 - 1 080 375 - 538 803

Other operating expenses - 18 458 - 14 031 - 15 984 - 10 611 - 18 458 - 14 031 - 15 980 - 10 606

Total operating expenses - 473 381 - 266 732 - 255 890 - 131 994 - 1 290 355 - 652 513 - 1 210 994 - 607 313

income before credit losses 118 974 58 017 92 921 51 383 118 974 58 017 92 925 51 388

Credit losses, net - 9 341 - 3 993 - 6 812 - 853 - 9 341 - 3 993 - 6 812 - 853

income before appropriations and taxes 109 633 54 024 86 109 50 530 109 633 54 024 86 113 50 535

Appropriations - - - - - - - -

Taxes - 28 833 - 14 208 - 22 647 - 13 290 - 28 833 - 14 208 - 22 648 - 13 291

income 80 800 39 816 63 462 37 240 80 800 39 816 63 465 37 244

* Net income from financial transactions

Currency related - - 74 - - - 74 -

Interest-bearing securities and related derivatives - 866 204 2 767 3 088 - 866 204 2 767 3 088

Total - 866 204 2 841 3 088 - 866 204 2 841 3 088

CaPiTal aDEQUaCY

sTaTEMEnT of inCoME

7

8

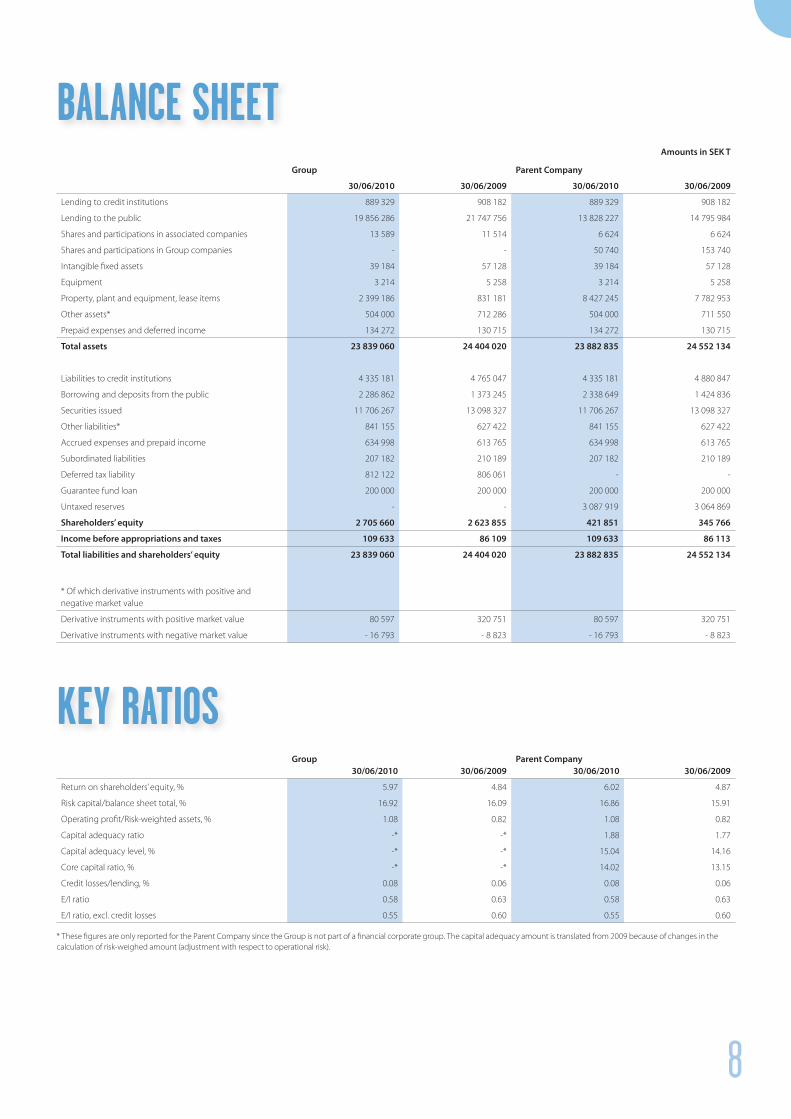

Amounts in sEk T

Group Parent Company

30/06/2010 30/06/2009 30/06/2010 30/06/2009

Lending to credit institutions 889 329 908 182 889 329 908 182

Lending to the public 19 856 286 21 747 756 13 828 227 14 795 984

Shares and participations in associated companies 13 589 11 514 6 624 6 624

Shares and participations in Group companies - - 50 740 153 740

Intangible fixed assets 39 184 57 128 39 184 57 128

Equipment 3 214 5 258 3 214 5 258

Property, plant and equipment, lease items 2 399 186 831 181 8 427 245 7 782 953

Other assets* 504 000 712 286 504 000 711 550

Prepaid expenses and deferred income 134 272 130 715 134 272 130 715

Total assets 23 839 060 24 404 020 23 882 835 24 552 134

Liabilities to credit institutions 4 335 181 4 765 047 4 335 181 4 880 847

Borrowing and deposits from the public 2 286 862 1 373 245 2 338 649 1 424 836

Securities issued 11 706 267 13 098 327 11 706 267 13 098 327

Other liabilities* 841 155 627 422 841 155 627 422

Accrued expenses and prepaid income 634 998 613 765 634 998 613 765

Subordinated liabilities 207 182 210 189 207 182 210 189

Deferred tax liability 812 122 806 061 - -

Guarantee fund loan 200 000 200 000 200 000 200 000

Untaxed reserves - - 3 087 919 3 064 869

shareholders’ equity 2 705 660 2 623 855 421 851 345 766

income before appropriations and taxes 109 633 86 109 109 633 86 113

Total liabilities and shareholders’ equity 23 839 060 24 404 020 23 882 835 24 552 134

* Of which derivative instruments with positive and negative market value

Derivative instruments with positive market value 80 597 320 751 80 597 320 751

Derivative instruments with negative market value - 16 793 - 8 823 - 16 793 - 8 823

Group 30/06/2010 30/06/2009

Parent Company 30/06/2010 30/06/2009

Return on shareholders’ equity, % 5.97 4.84 6.02 4.87

Risk capital/balance sheet total, % 16.92 16.09 16.86 15.91

Operating profit/Risk-weighted assets, % 1.08 0.82 1.08 0.82

Capital adequacy ratio -* -* 1.88 1.77

Capital adequacy level, % -* -* 15.04 14.16

Core capital ratio, % -* -* 14.02 13.15

Credit losses/lending, % 0.08 0.06 0.08 0.06

E/I ratio 0.58 0.63 0.58 0.63

E/I ratio, excl. credit losses 0.55 0.60 0.55 0.60

* These figures are only reported for the Parent Company since the Group is not part of a financial corporate group. The capital adequacy amount is translated from 2009 because of changes in the calculation of risk-weighed amount (adjustment with respect to operational risk).

balanCE sHEET

kEY RaTios

9

Amounts in sEk T

Jan - June 2010 Jan - June 2009

Ongoing operations

Operating profit 109 633 86 109

Amortisation 338 945 125 267

Changes in operating assets and liabilities

Lending to credit institutions 574 211 - 310 868

Lending to the public - 341 295 1 075 100

Other assets 207 154 135 020

Liabilities to credit institutions 219 241 - 2 501 884

Borrowing from the public 434 364 652 173

Securities issued - 1 138 923 855 695

Other liabilities 229 543 - 34 949

Cash flows from operating activities 632 873 81 663

Investing activities

Change in intangible fixed assets - 8 666

Change in shares and participations 1 222 -

Change in property plant and equipment - 551 976 - 55 055

Cash flows from investing activities - 550 754 - 46 389

Financing activities

Debenture loans - 2 119 626

Dividend paid - 80 000 - 35 900

Cash flows from financing activities - 82 119 - 35 274

Cash flow for the period

Cash and cash equivalents at start of year - -

Cash flows from operating activities 632 873 81 663

Cash flows from investing activities - 550 754 - 46 389

Cash flows from financing activities - 82 119 - 35 274

Cash and cash equivalents at the end of the period - -

Amounts in sEk T

Group Parent Company

Jan-Jun 2010 Apr-Jun 2010 Jan-Jun 2009 Apr-Jun 2009 Jan-Jun 2010 Apr-Jun 2010 Jan-Jun 2009 Apr-Jun 2009

Income from operational and finance leases 350 536 202 808 125 497 62 361 1 220 810 613 501 1 169 840 569 534

Scheduled amortisation - 329 062 - 190 459 - 114 630 - 58 235 - 1 146 036 - 576 240 - 1 069 738 - 533 559

Interest income 250 206 124 649 355 270 146 631 196 906 99 737 266 035 114 782

Interest expense - 137 192 - 71 659 - 263 489 - 95 522 - 137 192 - 71 659 - 263 489 - 95 522

Accumulated net interest 134 488 65 339 102 648 55 235 134 488 65 339 102 648 55 235

In the Parent Company, all lease agreements are reported as operating leases, while in the Group some of them are reported as finance leases. This means that the net finance leases are reclassified as interest income in the consolidated accounts.

lEasE inCoME anD aCCUMUlaTED nET inTEREsT

ConsoliDaTED CasH floW sTaTEMEnT

10

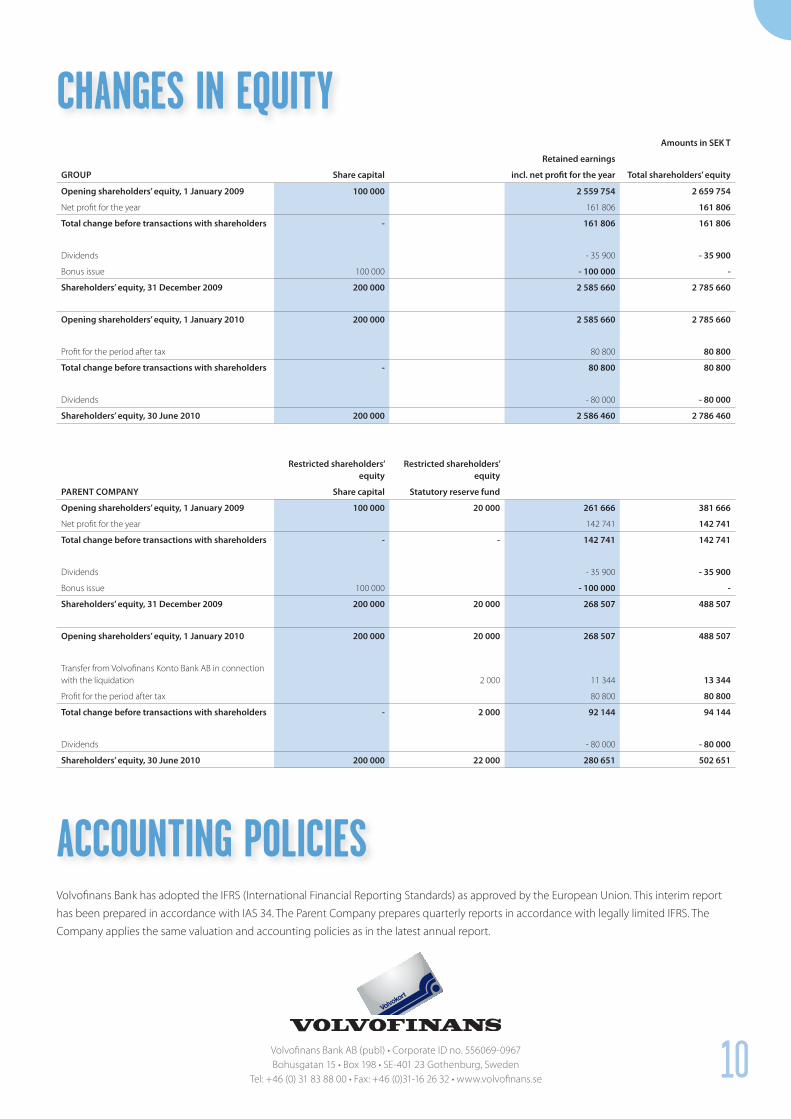

Amounts in sEk T

Retained earnings

GRouP share capital incl. net profit for the year Total shareholders’ equity

opening shareholders’ equity, 1 January 2009 100 000 2 559 754 2 659 754

Net profit for the year 161 806 161 806

Total change before transactions with shareholders - 161 806 161 806

Dividends - 35 900 - 35 900

Bonus issue 100 000 - 100 000 -

shareholders’ equity, 31 December 2009 200 000 2 585 660 2 785 660

opening shareholders’ equity, 1 January 2010 200 000 2 585 660 2 785 660

Profit for the period after tax 80 800 80 800

Total change before transactions with shareholders - 80 800 80 800

Dividends - 80 000 - 80 000

shareholders’ equity, 30 June 2010 200 000 2 586 460 2 786 460

Restricted shareholders’ equity

Restricted shareholders’ equity

PAREnT CoMPAny share capital statutory reserve fund

opening shareholders’ equity, 1 January 2009 100 000 20 000 261 666 381 666

Net profit for the year 142 741 142 741

Total change before transactions with shareholders - - 142 741 142 741

Dividends - 35 900 - 35 900

Bonus issue 100 000 - 100 000 -

shareholders’ equity, 31 December 2009 200 000 20 000 268 507 488 507

opening shareholders’ equity, 1 January 2010 200 000 20 000 268 507 488 507

Transfer from Volvofinans Konto Bank AB in connection with the liquidation 2 000 11 344 13 344

Profit for the period after tax 80 800 80 800

Total change before transactions with shareholders - 2 000 92 144 94 144

Dividends - 80 000 - 80 000

shareholders’ equity, 30 June 2010 200 000 22 000 280 651 502 651

Volvofinans Bank has adopted the IFRS (International Financial Reporting Standards) as approved by the European Union. This interim report

has been prepared in accordance with IAS 34. The Parent Company prepares quarterly reports in accordance with legally limited IFRS. The

Company applies the same valuation and accounting policies as in the latest annual report.

Volvofinans Bank AB (publ) • Corporate ID no. 556069-0967Bohusgatan 15 • Box 198 • SE-401 23 Gothenburg, Sweden

Tel: +46 (0) 31 83 88 00 • Fax: +46 (0)31-16 26 32 • www.volvofinans.se

CHanGEs in EQUiTY

aCCoUnTinG PoliCiEs

Top Related