Languages

Pages

Legal

Transfield ServicesInfrastructure Summit – 11 June 2015Keeping infrastructure development on track – planning for the long-termGraeme Hunt – Managing Director and Chief Executive Officer

Disclaimer and important information2

This presentation is for information purposes only. The content of this presentation is provided as at the date of this presentation (unless otherwise

stated). Reliance should not be placed on information or opinions contained in this presentation and, subject only to any legal obligation to do so

Transfield Services Limited (‘Transfield Services’) does not have any obligation to correct or update content.

This presentation does not and does not purport to contain all information necessary to an investment decision, is not intended as investment or

financial advice and must not be relied upon as such. Any decision to buy or sell securities or other products should be made only after seeking

appropriate financial advice.

This presentation is of a general nature and does not take into consideration the investment objectives, financial situation or particular needs of any

particular investor.

Any investment decision should be made solely on the basis of your own enquiries. Before making an investment in Transfield Services, you should

consider whether such an investment is appropriate to your particular investment objectives, financial situation or needs.

To the maximum extent permitted by law, Transfield Services disclaims all liability (including, without limitation, any liability arising from fault,

negligence or negligent misstatement) for any loss arising from this presentation or reliance on anything contained in or omitted from it or otherwise

arising in connection with this.

All amounts are in Australian Dollars, unless otherwise stated.

Transfield Services overview

Our story began in infrastructure4

2001 – Transfield Services was listed on the ASX

1987 – Awarded the Sydney Harbour Tunnel contract under “Build-Own-Operate-Transfer” (BOOT) scheme

1956 – Transfield was founded

1950s-1960s – Rapid growth with new divisions added to include steel fabrication, transmission lines, bridge building, aircraft manufacturing, galvanizing and general construction

1993 – Operations and Maintenance Division commenced operations at Mobil Altona, first contract in Hydrocarbons sector

1990s – Large contracts won through BOOT scheme, largest being the A$2billion Melbourne City Link Project

2006 Entry into the US via acquisition

of USM, followed by acquisition of Hofincons leading to entry into India

Formation of Flint Transfield Services (“FTS”) joint venture with Flint Services in Canada

2010 – Acquisition of Easternwell, a leading Australian services provider to the mining, oil & gas and infrastructure sectors

2012 Transdev 50/50 partnership, Harbour

City Ferries, appointed by the NSW Government to operate and maintain Sydney Ferries

Expansion of Transfield Worley Power Services (“TWPS”) JV

2013 Awarded A$200m contract to

provide maintenance and operations services to QGC upstream coal seam gas (CSG) assets in Queensland

Awarded a A$170m contract with NBN comprising Passive Fibre Network design in Sydney

Sale of 50% share in Transfield Worley New Zealand JV to existing partner WorleyParsons for A$30m

Easternwell integrated with Resources and Energy business

2014 Awarded A$1.22bn,

20 month contract for garrison and welfare support to the Australian Department of Immigration and Border Protection for offshore processing centres in Nauru and Manus Island

Sale of Hofincons and Middle East businesses

2004 – Acquisition of Serco NZ doubled the size of operations in New Zealand

2007 Entry into Chile via InserTS

joint venture Transfield Services

Infrastructure Fund, comprising interests in power stations and wind farms, floated on ASX, with Transfield Services holding c.49% of securities on issue

2011 Signed A$133mn contract with

NBN to design and construct Victoria’s fibre optic network

Sale of North American facilities maintenance company (USM) to EMCOR Group. Total cash value was US$255m

1956 1987 1990 1993 2001 2007 20132010 2011 2012 20142004 2006

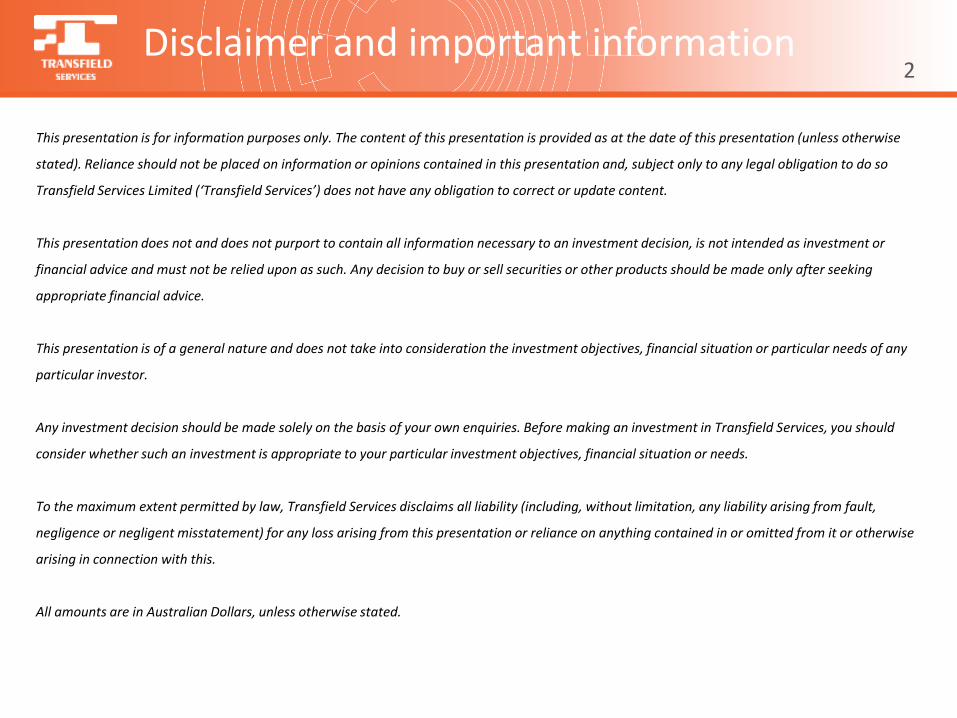

Infrastructure – a core focus5

Our Sectors

Infrastructure

Defence, Social & property

Resources & Industrial

Americas Workforce of 19,000 | 9 countries | 9 sectors | 200+ clients

Our Services

Logistics and Facilities Management

ConsultingOperations andMaintenance

Well Servicing ConstructionCare & Welfare

What we do – selected examples6

We maintain and operate Sydney’s Harbour City Ferries for the NSW Government in partnership with Transdev

We provide shutdown maintenance and drilling services to various mining and oil & gas operators globally,including for Woodside

We maintain coal seam gas wells and other plants in Queensland for QGC’s CSG to LNG program utilising Easternwell’s well servicing rigs and provide services across the value chain

We install telecommunications networks for the National Broadband Network in Australia and the Ultrafast Broadband Network in NZ

We provide garrison and welfare services for the Australian Government on Nauru and Manus Island

We operate and/or maintain civil, mechanical, electrical and tolling assets for the Hills M2 Motorway and Lane Cove Tunnel in Sydney, City Link and East Link in Melbourne, and Presidio Parkway in the US

We provide estate management and garrison support services to the Australian Department of Defence on bases in Victoria,South Australia, Tasmania, Western Australia and the Northern Territory. We alsoprovide emergency servicesand maintain the Defence force national stores on every Australian base

We provide operations and maintenance services to oil & gas assets in both the upstream and downstream sectors in the US for clients such as Chevron, Exxon Mobil and Valero

Now is the time to work on infrastructure

8

I. It’s more than capital recycling

II. Why we must have consistent policy

III. The social benefits of smart long-term asset management

Outline

Infrastructure asset recycling9

Government Asset Recycling

• Australia’s Infrastructure funding deficit is around $700 billion

• Australia’s population is projected to rise from 23 million to 38 million by 2050, requiring significant upgrades in infrastructure

• Funding these projects represents a challenge; government revenue bases are shrinking and increased debt threatens credit metrics

• Governments to privatise up to ~$100bn of infrastructure

• Asset recycling facilitates larger scale deployment of capital than PPPs

Private Sector Asset Recycling

• Australia has reached the peak of an expansionary investment cycle in the resources and energy sectors

• The emphasis is now on ‘sweating the assets’ in order to optimise the investment

• Private enterprise may be holding non-core assets on balance sheet

• Australia is expected to become the largest LNG exporter by 2022, and selling infrastructure is a feasible strategy for releasing capital

• The LNG sector holds approximately $60bn of potentially divestible infrastructure to fund future opportunities

The energy sector has reached the peak of its expansionary cycle while state governments are under pressure to repair balance sheets. A period of significant asset recycling in both public and private sectors is on the horizon

Funding ShortfallsLimitations on Debt

FinancingDemand for New

Infrastructure

End of Expansionary Phase

Non-core Infrastructure on Balance Sheets

Need to Liberate Capital

Public Sector

Private Sector

Source: ANZ, Utilities and Infrastructure Market Update. March 2014.

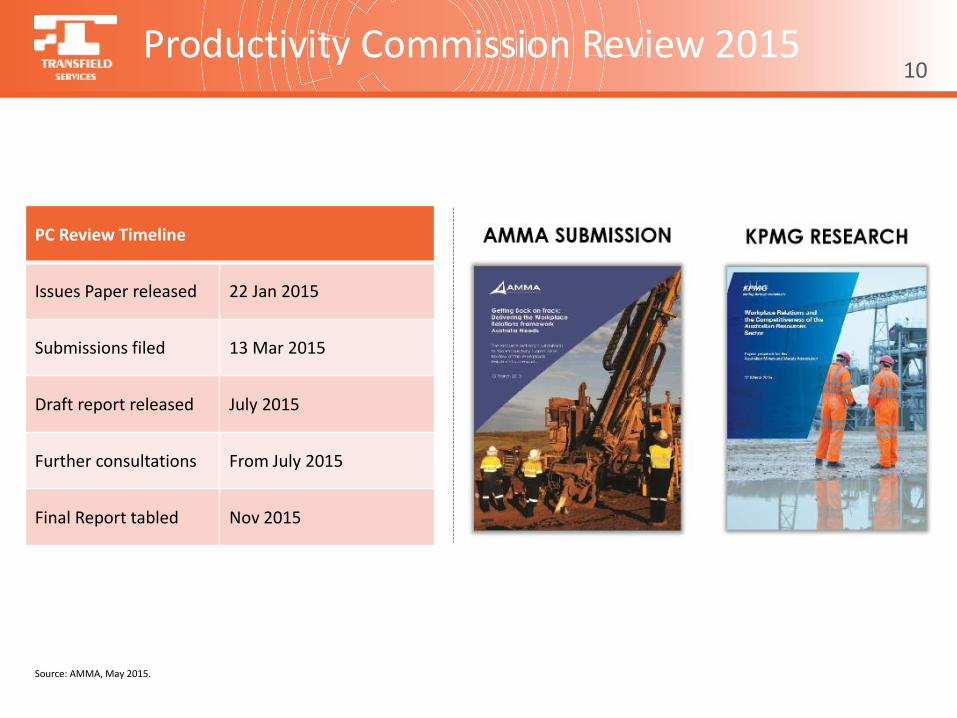

Productivity Commission Review 201510

PC Review Timeline

Issues Paper released 22 Jan 2015

Submissions filed 13 Mar 2015

Draft report released July 2015

Further consultations From July 2015

Final Report tabled Nov 2015

Source: AMMA, May 2015.

KPMG analysis found…11

Source: AMMA, May 2015.

• Resources production costs 50% higher than global average

• Mining productivity declined by 45% in past decade

• From 2001-2012 resource construction wages rose 2.5x national average

• Wage in iron ore sector 21% higher than global average

• Longer approval times for large projects than Canada, UK and NZ

• Environmental approvals can take up to 2 yrs to produce and 1.5 yrs to assess

• Exports expected to account for 67% of 2014/15 mining revenue

• High mineral rents compared to Canada, NZ and US

Funding issues at Federal and State level12

FEDERAL BUDGET DEFICIT2015 -16

$35.1bn

WA2014-15: $1.29bn

deficit

2015-16:

$2.71bn deficit NSW2014-15:

$0.28bn deficit

NT2014-15

$0.06bn deficit QLD

2014-15:

$2.27bn deficit

SA2014-15:

$0.48bn deficit

2015-16: $0.41

surplus

VIC2014-15:

$0.9b surplus

2015-16: $1.2bn

surplus

Source: Western Australia State Budget (2015-16), South Australia State Budget (2014-15), Northern Territory State Budget (2015-16), Queensland State Budget (2014-15), NSW State Budget (2014-15), Victoria State Budget (2015-16).Note: Data sourced from state government budgets as at 6 June 2015.

It’s more than capital recycling…13

The impact of public infrastructure on productivity and economic growth

• Investing in the right infrastructure could give Australia a once in a generation opportunity to transition our economy away from such an overwhelming resources focus, with the attendant boom and bust cycle

• Roads, rails, ports, airports, utility networks and social infrastructure are not just the backbone of the nation, they are also the growth engines of our future

The imperative to recycle capital cannot be ignored

• The Federal Government’s Asset Recycling Initiative is critical

• State budgets and balance sheets remain under pressure and the need for new infrastructure has never been greater

• Australia’s infrastructure funding deficit is estimated to be $700bn1

• $5bn in incentive payments to States and Territories who sell or lease assets and reinvest the proceeds in new infrastructure (Asset Recycling Initiative)

Natural owners of infrastructure assets

• Public capital should be allocated based on long-term benefit and recycled as soon as the business cycle allows private capital inflow

• Assets are managed more efficiently by private operators working alone or in alliance with the Government

Impact of technology on delivery and management of infrastructure

• Infrastructure planning cannot occur in isolation, the incorporation of potentially disruptive digital technologies in our planning is crucial

• Technology has the potential to:₋ increase efficiency;₋ increase asset utilisation;₋ reduce operating costs; and₋ impact the overall cost of types of public

infrastructure required over the full lifecycle

Source: Infrastructure Partnerships Australia, Commonwealth Government Budget, Australian Infrastructure Audit – Our Infrastructure Audit (April 2015) and Citibank.

ACCC chairman Rod Sims has stated “the only good reason for government ownership is if there is a particular social objective in mind” noting “when the private sector own assets, that does provide better incentives for better performance”

Consistent policy is imperative14

long-term planning and reform of governance processes for infrastructure has been missing in public policyfor considerable time

The consequences of ‘short sightedness’ have yielded low productivity and high costs

Critical need to minimise delay, indecision and uncertainty between project announcement and start-up.Delays erode return on investment and discourage private sector appetite for risk

Source: SMART, University of Wollongong, ATSE - Infrastructure to meet Australia’s future needs.

Efficient recycling of

public investment

CertaintyDisruptive

digital technologies

Integrity of Process

Incentives

Government infrastructure policies should address

The risk of not providing certainty may result in the attribution of sovereign risk to Australian infrastructure transactions

The cost of inconsistent policy Queensland 15

The outcome of the Queensland state election resulted in $37bn of transactions being cancelled or deferred

3 Feb 2015

THE BRUTAL POLITICS OF PRIVITISATION

STARK AFTER QUEENSLAND ELECTION

SHOCK

The sudden and brutal change of governments in Queensland and

Victoria adds an element of uncertainty to infrastructure projects. In the

case of Queensland, it means $37 billion of transactions have

automatically been taken off the table. It will be a big blow for

investment banks, super funds and companies that anticipated being part

of the sales.

4 Feb 2015

QUEENSLAND ELECTION 2015: LNP DUMPS

ASSET SALES POLICY

The Queensland Liberal National Party has ditched its $37 billion

privatisation plan as part of a last minute attempt to form a minority

government… “They are all in grave doubt. That’s a tragedy for the

international investment community, but that’s a situation Queensland

is in”

The Need For Consistent Policy

• The $37bn in capital set aside by investors for the QLD electricity asset sales will now be reallocated

• Greater competition for NSW T&D assets

• The risk of state governments taking transactions off the table for political reasons will be factored into the price when bidders value infrastructure assets going forward

• In order to get the best price for assets, governments need to implement a consistent policy and reduce political risk for bidders

The cost of inconsistent policyVictoria 16

The cancellation of the East West Link increases the price of risk associated with business in Australia

3 May 2015

FEDERAL BUDGET 2015: DANIEL ANDREWS

REFUSES TO PAY BACK EAST WEST MONEY

Victorian Premier Daniel Andrews has refused to give into demands to

refund $1.5 billion of federal government funding slated for the

cancelled East West Link toll road.

15 Apr 2015

VICTORIA TO PAY $339M TO SETTLE EAST

WEST CLAIM

Major developer Lend Lease has walked away from a long-running

brawl over compensation for the scrapping of one of the nation's

largest road projects, under a $339 million deal which opens the way

for the property giant to win future billion-dollar contracts.

Transaction announced

Risks assessed and bids priced

Transaction cancelled

Loss of invested resources

15 Apr 2015

EAST WEST CONTRACTORS CALL FOR long-

term PLANNING AFTER SETTLEMENT

While contractors believe that an agreement allowing reimbursement

of the money invested by a consortium of Lend Lease, France's

Bouygues and Spain's Acciona for the costs of bidding for East West

Link and designing plans to build it is fair, they now regard Australia

as a more risky place to do business.

Resources industry’s reform priorities17

Source: AMMA, May 2015.

Accessible, reliable and competitive agreement options for new and existing projects

Agreement content restricted to employment matters

Balanced rules for strike action

Balanced and practical rules for unions entering workplaces

Balanced safety net protections for employees

What impact could AMMA’s reforms have?18

Source: AMMA, May 2015.

Social benefits of long-term smart asset management 19

Employment growthBusiness expansion around new infrastructure results in significant job creation. Governments should not attempt to hold onto assets with the aim to protect employment

Productivity growthRoads, rail, ports, airports, utility networks and social infrastructure are the backbone of the nation and growth engine for the future. The World Bank estimates that every 10% increase in infrastructure provision increases output by ~1% over the long-term

Efficiency gains

Private sector owned assets provide better incentives for better performance. A University of Melbourne study notes that PPP contracted projects were able to deliver the construction phase of an asset with a delay of 1.4% of agreed time, versus traditionally procured projects which had delays of 26% of the agreed time

Cost savingsIn private hands, costs of operating infrastructure assets decline and projects are delivered more efficiently. Dealing equitably with the affordability of infrastructure services is an important consideration, as a matter of social policy

“If we get our infrastructure right, we will protect Australia’s quality of life at a time of population growth and global economic change” Infrastructure Australia

Optimal capital allocation

Efficient funding of infrastructure is focused on the allocation of project and systematic risks to those parties best able to manage them, both across the public and private sectors

5

4

3

1

2

Source: The Australian Trade Commission (Austrade), Investment Opportunities in Australian Infrastructure. Australian Infrastructure Audit – Our Infrastructure Audit (April 2015).

Case study: Harbour City Ferries20

Our recent, successful transfer of approximately 550 staff from Transport

NSW (Sydney Ferries) to Harbour City Ferries (a Transfield Services –

Transdev JV) demonstrates our capabilities in transition and first generation

outsourcing.

Transfer of 85% of the incumbent workforce

Limited disruption to services through industrial activity since

commencement

Commencement of operations earlier than initially planned

Increase of customer patronage by 2.2%

Independent recognition of our achievements: Transfield won the 2013

Infrastructure Partnerships Australia Award for Operator and Service

Provider Excellence.

Harbour City Ferries

Significant efficiency gains can be derived from first generation outsourcing

Case study: Port of Miami Tunnel21

The Port Miami Tunnel (POMT) was the first major project

built through a public-private partnership (PPP) undertaken

in Miami

Transfield Services was part of the successful design,

construct, operate and maintain consortium with Babcock &

Brown and Bouygues Travaux Publics

The Port Miami Tunnel opened on 3 August 2014

Up to 22,000 vehicles using the tunnel in one day

Transfield Services has safely managed 243 traffic events,

with crews arriving on scene in an average of 6.5 minutes,

restoring traffic flow within 17 mins

Publicly recognised by the US Department of Transportation

Port of Miami Tunnel

The Port of Miami Tunnel showcases best-practice road infrastructure operation and maintenance systems and processes in the United States

Closing remarks22

Now is the time to work on infrastructure

Australia has a funding gap with budget deficits at the federal and state level

Asset recycling across the public and private sectors can provide funding for new infrastructure projects

Consistent policy is imperative to attract investment

Effective capital management will drive productivity, efficiency and economic gains

Thank you

Top Related