Languages

Pages

Legal

Barclays Consumer Conference

7th September 2015

Forward-looking Statements Disclaimer

2

This presentation contains oral and written statements that are or may be “forward-looking statements” with respect to certain of Ocado’s plans and its current goals and expectations relating to its future financial condition, performance and results. These forward-looking statements are usually identified by words such as ‘anticipate’, ‘target’, ‘expect’, ‘estimate’, ‘intend’, ‘plan’, ‘goal’, ‘believe’ or other words of similar meaning. By their nature, all forward-looking statements involve risk and uncertainty because they are based on current expectations and assumptions but relate to future events and circumstances which may be beyond Ocado’s control. There are important factors that could cause Ocado’s actual financial condition, performance and results to differ materially from those expressed or implied by these forward-looking statements, including, among other things, UK domestic and global political, social, economic and business conditions, market-related risks such as fluctuations in interest rates and exchange rates, the policies and actions of regulatory authorities, the impact of competition, the possible effects of inflation or deflation, variations in commodity prices and other costs, the ability of Ocado to manage supply chain sources and its offering to customers, the effect of any acquisitions by Ocado, combinations within relevant industries and the impact of changes to tax and other legislation in the jurisdictions in which Ocado and its affiliates operate. Further details of certain risks and uncertainties are set out in our Annual Report for 2014, which can be found at www.ocadogroup.com. Ocado expressly disclaims any undertaking or obligation to update the forward-looking statements made in this presentation or any other forward-looking statements we may make except as required by law. Persons receiving this presentation should not place undue reliance on forward-looking statements which are current only as of the date on which such statements are made.

Contents

Ocado at a glance Online grocery: opportunity and challenge Ocado’s unique business model Intellectual property, technology and strategic customers Summary

3

Award winning customer proposition Commercialising knowledge

Unique business model Proprietary intellectual property

• No stores, centralised fulfilment • Highly automated • Technology driven

• Write and develop all software • Proprietary, physical fulfilment

asset solution • End to end fully integrated

system for online grocery retail

• Morrisons first external customer • Running morrisons.com, launched

Jan 2014 • Targeting international

opportunities

Ocado at a glance

World’s largest dedicated online grocery supermarket

Online Supermarket of the Year 2015

Voted Best Online Grocer for sixth consecutive year

Best Online Grocer for Vegetarians 2015

Best Online Supermarket 2015

4

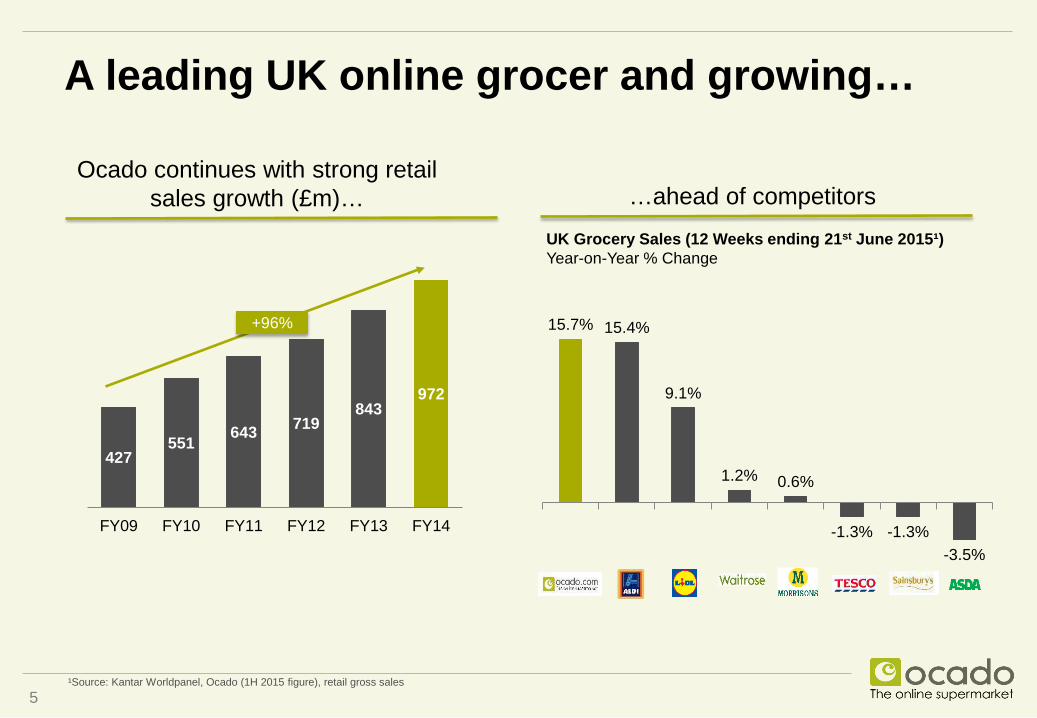

427 551 643 719

843 972

FY09 FY10 FY11 FY12 FY13 FY14

5

A leading UK online grocer and growing…

Ocado continues with strong retail sales growth (£m)… …ahead of competitors

+96% 15.7% 15.4%

9.1%

1.2% 0.6%

-1.3% -1.3% -3.5%

UK Grocery Sales (12 Weeks ending 21st June 2015¹) Year-on-Year % Change

¹Source: Kantar Worldpanel, Ocado (1H 2015 figure), retail gross sales

Contents

Ocado at a glance Online grocery: opportunity and challenge Ocado’s unique business model Intellectual property, technology and strategic customers Summary

6

1 Source: IGD, data is year to April 2015

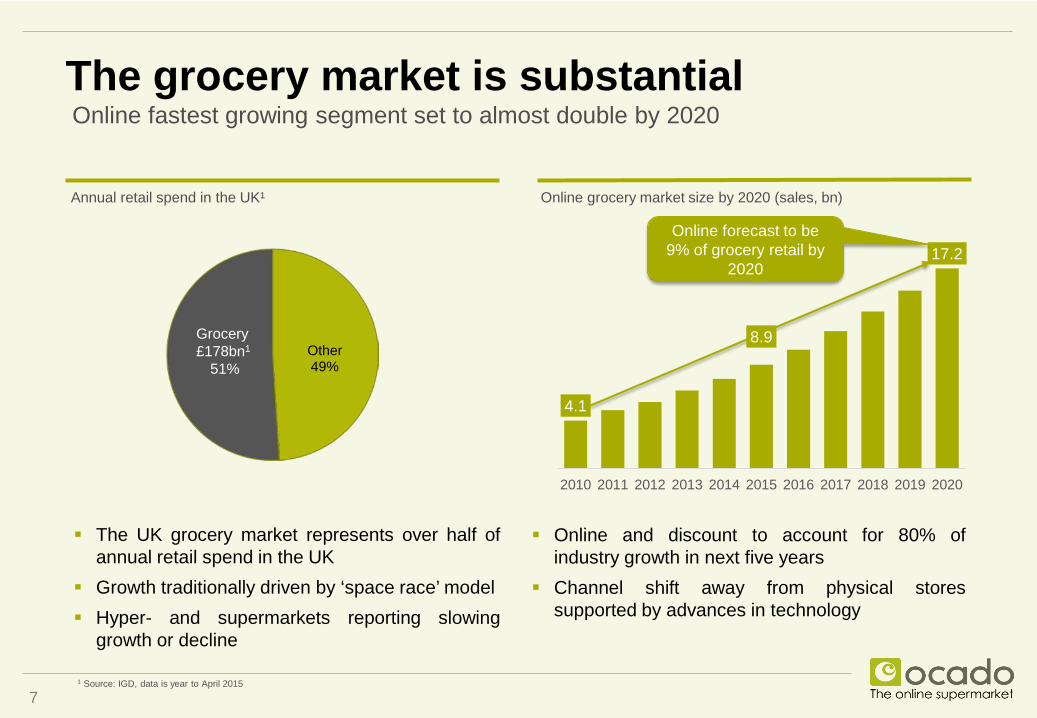

The grocery market is substantial Online fastest growing segment set to almost double by 2020

7

Annual retail spend in the UK¹

The UK grocery market represents over half of

annual retail spend in the UK Growth traditionally driven by ‘space race’ model Hyper- and supermarkets reporting slowing

growth or decline

4.1

8.9

17.2

2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Online grocery market size by 2020 (sales, bn)

Online forecast to be 9% of grocery retail by

2020

Online and discount to account for 80% of industry growth in next five years

Channel shift away from physical stores supported by advances in technology

Other 49%

Grocery £178bn1

51%

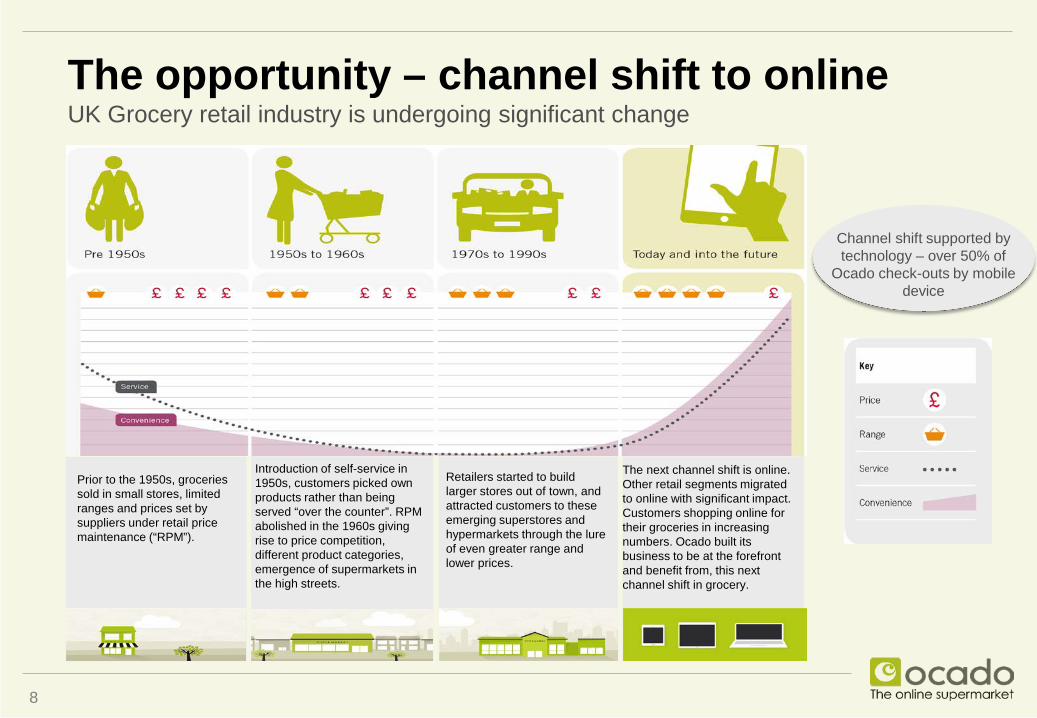

The opportunity – channel shift to online UK Grocery retail industry is undergoing significant change

Retailers started to build larger stores out of town, and attracted customers to these emerging superstores and hypermarkets through the lure of even greater range and lower prices.

The next channel shift is online. Other retail segments migrated to online with significant impact. Customers shopping online for their groceries in increasing numbers. Ocado built its business to be at the forefront and benefit from, this next channel shift in grocery.

Prior to the 1950s, groceries sold in small stores, limited ranges and prices set by suppliers under retail price maintenance (“RPM”).

Introduction of self-service in 1950s, customers picked own products rather than being served “over the counter”. RPM abolished in the 1960s giving rise to price competition, different product categories, emergence of supermarkets in the high streets.

8

Channel shift supported by technology – over 50% of

Ocado check-outs by mobile device

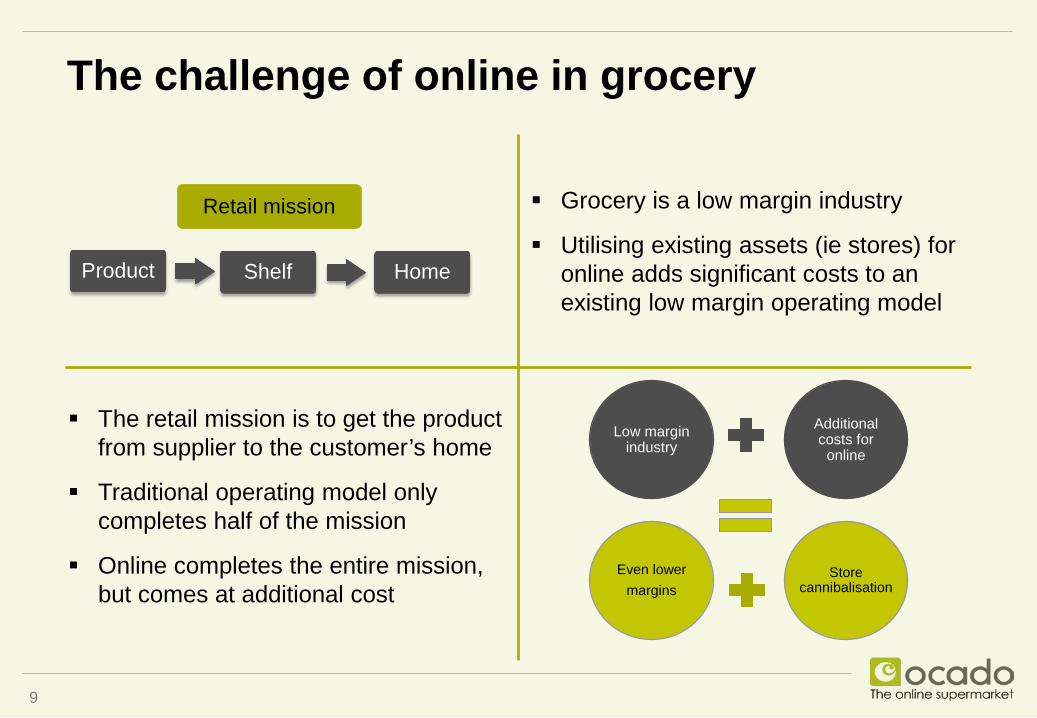

The challenge of online in grocery

9

Product Shelf Home

Retail mission

The retail mission is to get the product from supplier to the customer’s home

Traditional operating model only completes half of the mission

Online completes the entire mission, but comes at additional cost

Even lower margins

Store cannibalisation

Low margin industry

Additional costs for

online

Grocery is a low margin industry

Utilising existing assets (ie stores) for online adds significant costs to an existing low margin operating model

Contents

Ocado at a glance Online grocery: opportunity and challenge Ocado’s unique business model Intellectual property, technology and strategic customers Summary

10

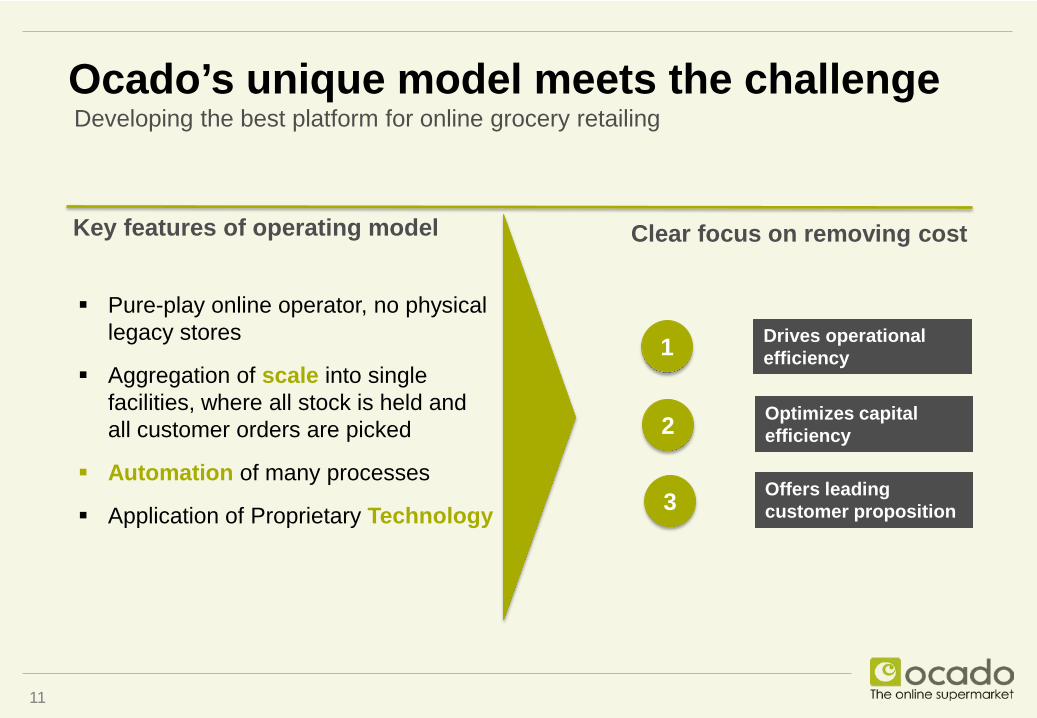

Ocado’s unique model meets the challenge Developing the best platform for online grocery retailing

11

Key features of operating model

Pure-play online operator, no physical legacy stores

Aggregation of scale into single facilities, where all stock is held and all customer orders are picked

Automation of many processes

Application of Proprietary Technology

Offers leading customer proposition

Drives operational efficiency

Optimizes capital efficiency

Clear focus on removing cost

1

2

3

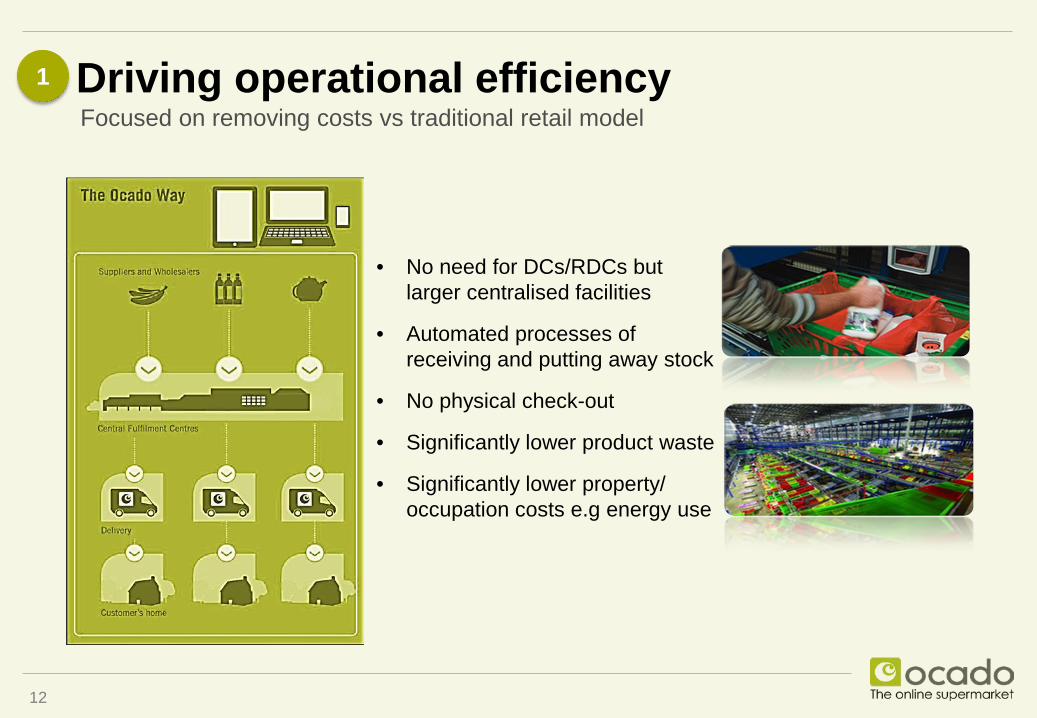

Driving operational efficiency

12

1 Focused on removing costs vs traditional retail model

• No need for DCs/RDCs but larger centralised facilities

• Automated processes of receiving and putting away stock

• No physical check-out

• Significantly lower product waste

• Significantly lower property/ occupation costs e.g energy use

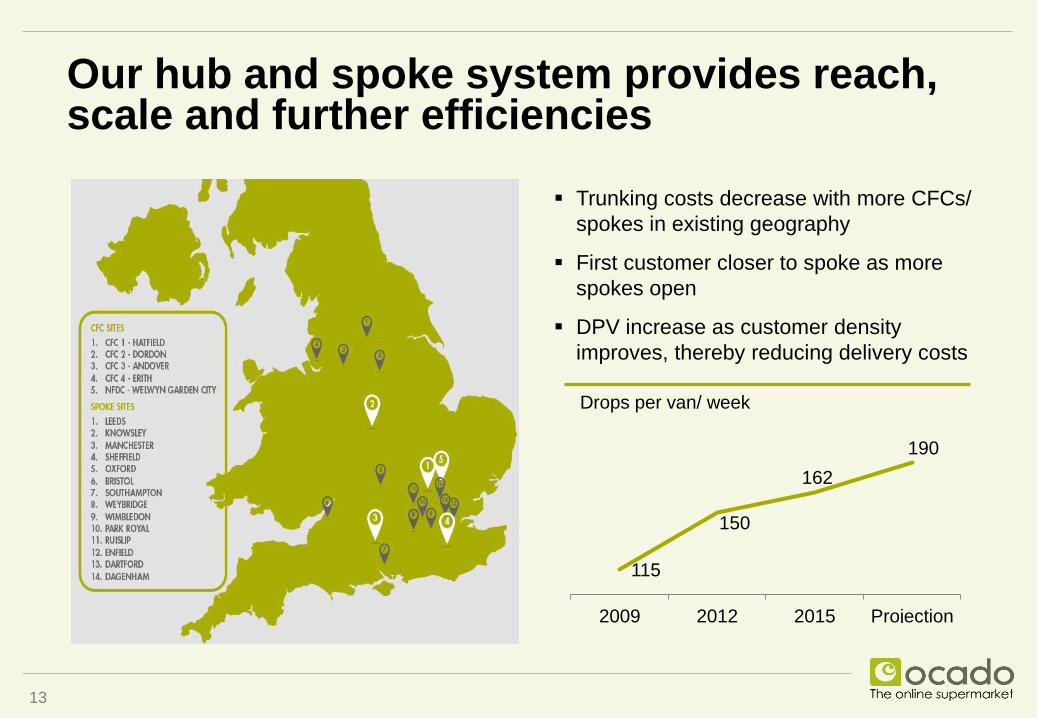

115

150

162 190

2009 2012 2015 Projection

Drops per van/ week

Trunking costs decrease with more CFCs/ spokes in existing geography

First customer closer to spoke as more spokes open

DPV increase as customer density improves, thereby reducing delivery costs

13

Our hub and spoke system provides reach, scale and further efficiencies

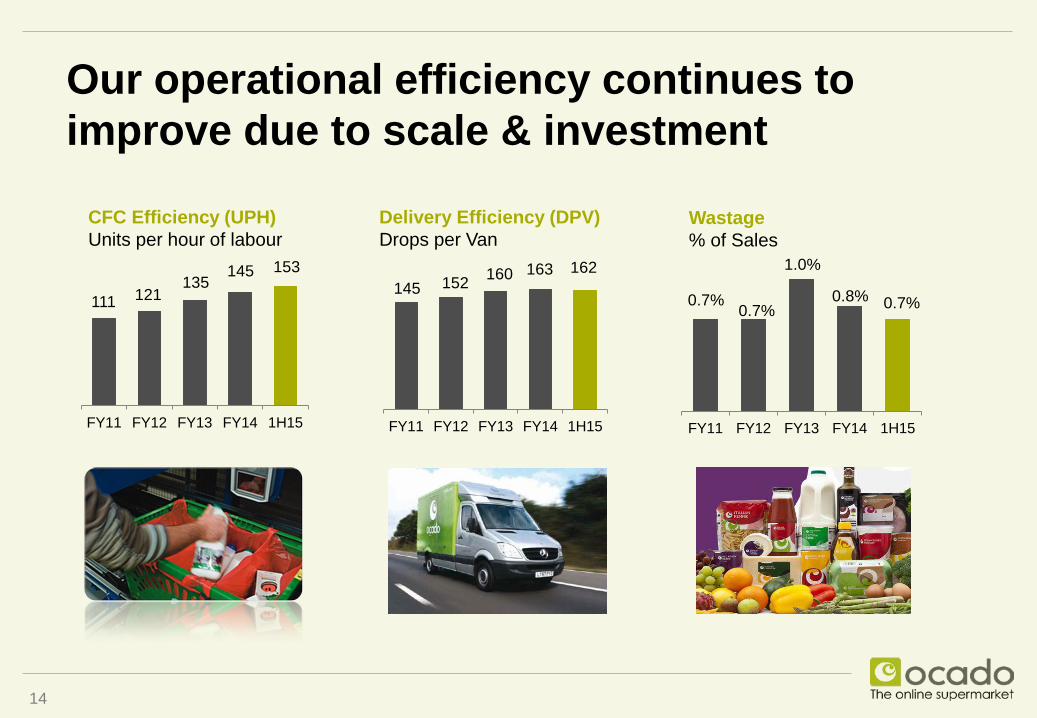

Our operational efficiency continues to improve due to scale & investment

14

111 121 135

145 153

FY11 FY12 FY13 FY14 1H15

CFC Efficiency (UPH) Units per hour of labour

145 152 160 163 162

FY11 FY12 FY13 FY14 1H15

Delivery Efficiency (DPV) Drops per Van

0.7% 0.7%

1.0%

0.8% 0.7%

FY11 FY12 FY13 FY14 1H15

Wastage % of Sales

Once at scale . . . A virtuous cycle turns online into mainstream channel

• Store densities fall

• Volumes decline further

• Less scope to improve customer proposition

• Fixed costs increase as % Sales

• Online growth accelerates decline

Online m

igration

Store based vicious spiral

15

Ocado’s virtuous cycle

Lower prices, wider range generates faster

growth

Growth allows further investment into

customer proposition

Growth further erodes buying power

disadvantage

At scale logistics cost benefit outweighs

buying power disadvantage

Cost base erodes

Virtuous Cycle

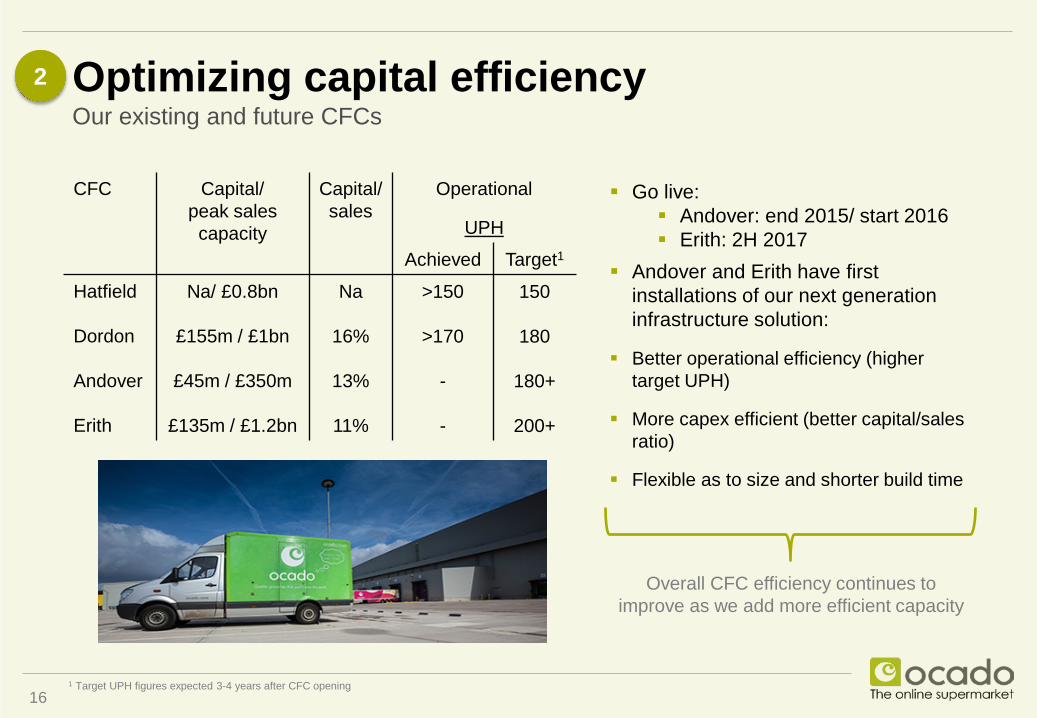

Optimizing capital efficiency Our existing and future CFCs

CFC Capital/ peak sales capacity

Capital/ sales

Operational

UPH

Achieved Target1

Hatfield Dordon Andover Erith

Na/ £0.8bn £155m / £1bn

£45m / £350m

£135m / £1.2bn

Na

16%

13%

11%

>150

>170 - -

150

180

180+

200+

1 Target UPH figures expected 3-4 years after CFC opening 16

Go live: Andover: end 2015/ start 2016 Erith: 2H 2017

Andover and Erith have first installations of our next generation infrastructure solution:

Better operational efficiency (higher target UPH)

More capex efficient (better capital/sales ratio)

Flexible as to size and shorter build time

2

Overall CFC efficiency continues to improve as we add more efficient capacity

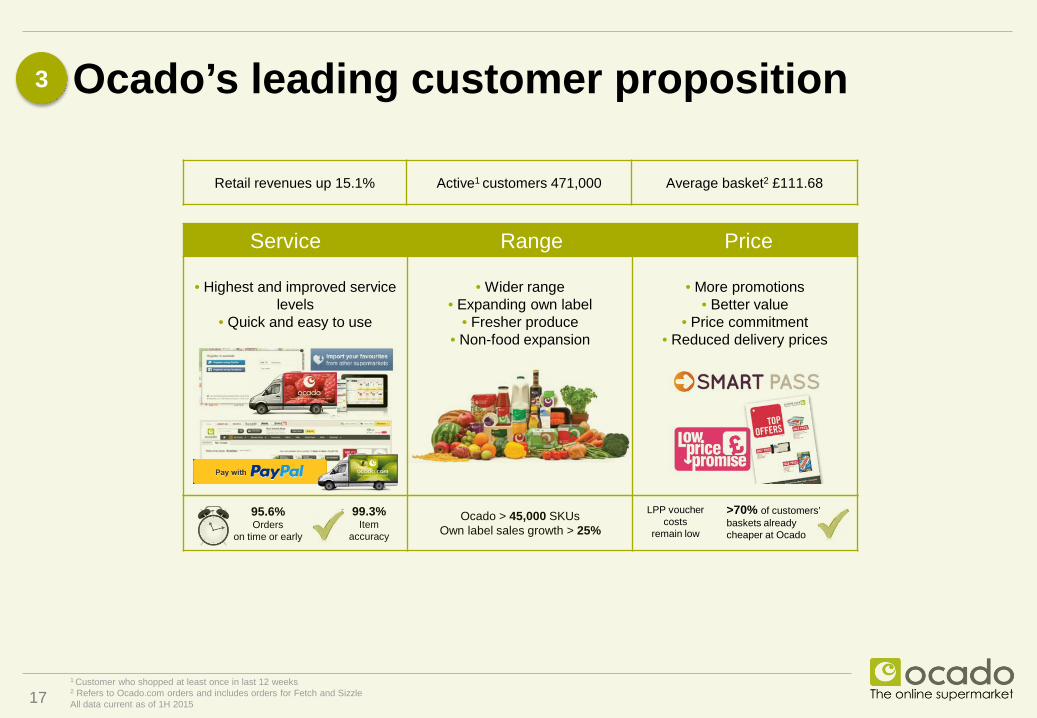

95.6% Orders

on time or early

99.3% Item

accuracy

Ocado > 45,000 SKUs Own label sales growth > 25%

Service Range Price

• Highest and improved service levels

• Quick and easy to use

• Wider range

• Expanding own label • Fresher produce

• Non-food expansion

• More promotions

• Better value • Price commitment

• Reduced delivery prices

>70% of customers’ baskets already cheaper at Ocado

17

Ocado’s leading customer proposition 3

Retail revenues up 15.1% Active1 customers 471,000 Average basket2 £111.68

1 Customer who shopped at least once in last 12 weeks 2 Refers to Ocado.com orders and includes orders for Fetch and Sizzle All data current as of 1H 2015

LPP voucher costs

remain low

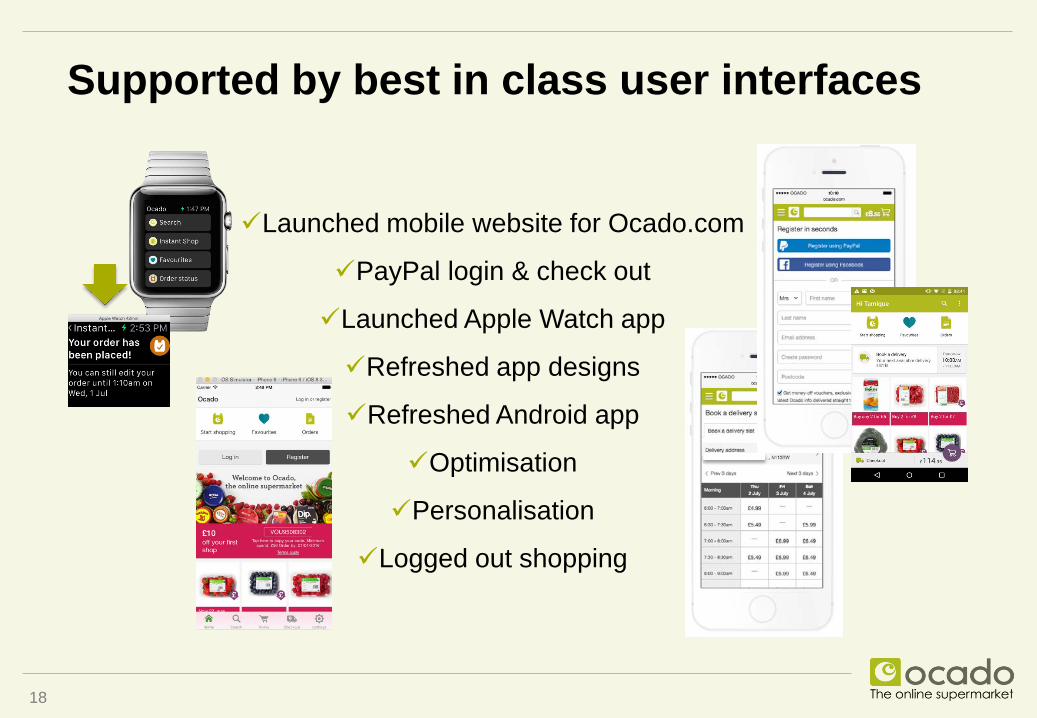

Supported by best in class user interfaces

Launched mobile website for Ocado.com

PayPal login & check out

Launched Apple Watch app

Refreshed app designs

Refreshed Android app

Optimisation

Personalisation

Logged out shopping

18

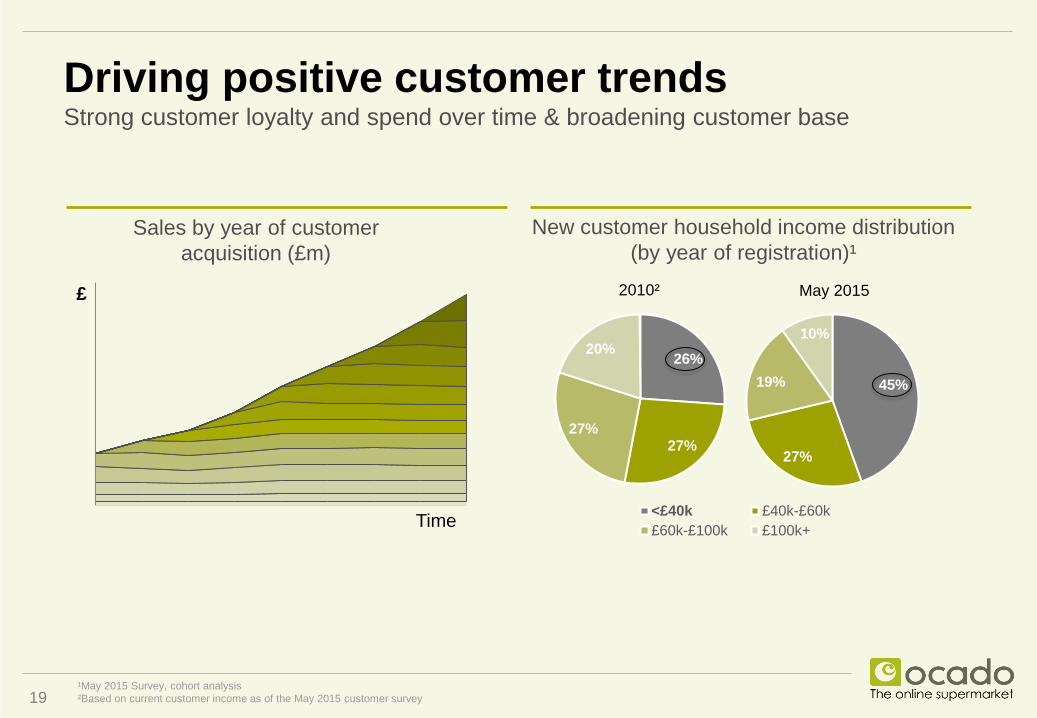

Sales by year of customer acquisition (£m)

45%

27%

19%

10%

<£40k £40k-£60k£60k-£100k £100k+

New customer household income distribution (by year of registration)¹

26%

27% 27%

20%

2010² May 2015

¹May 2015 Survey, cohort analysis ²Based on current customer income as of the May 2015 customer survey 19

Driving positive customer trends Strong customer loyalty and spend over time & broadening customer base

£

Time

Contents

Ocado at a glance Online grocery: opportunity and challenge Ocado’s unique business model Intellectual property, technology and strategic customers Summary

20

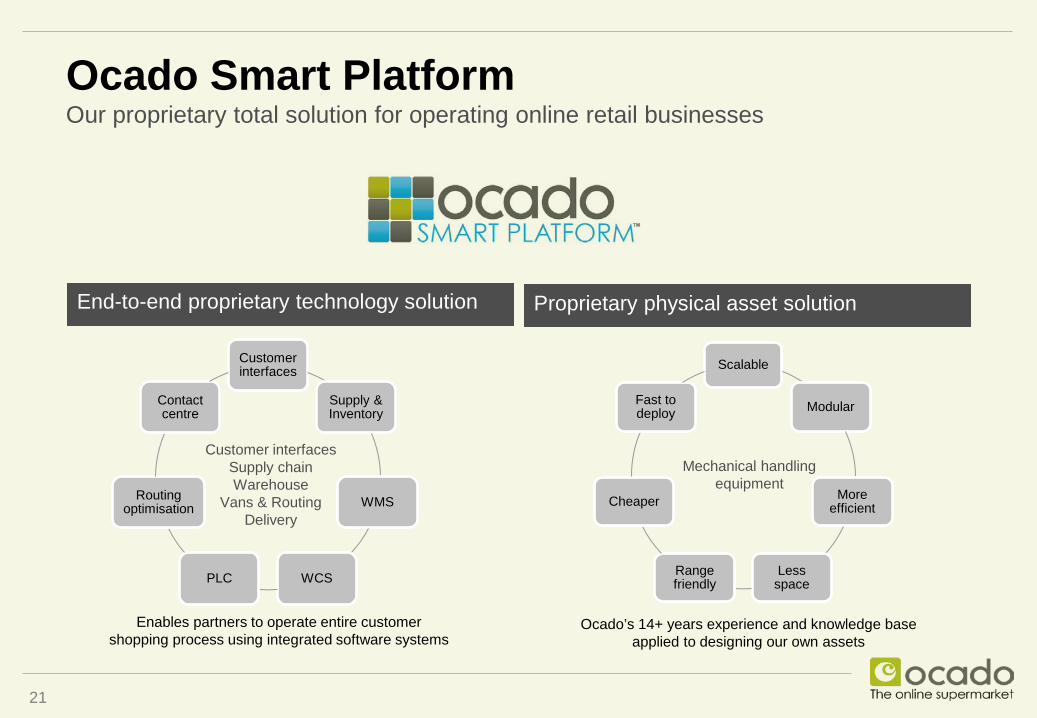

Ocado Smart Platform Our proprietary total solution for operating online retail businesses

End-to-end proprietary technology solution

21

Proprietary physical asset solution

Customer interfaces

Supply & Inventory

WMS

WCS PLC

Routing optimisation

Contact centre

Scalable

Modular

More efficient

Less space

Range friendly

Cheaper

Fast to deploy

Enables partners to operate entire customer shopping process using integrated software systems

Ocado’s 14+ years experience and knowledge base applied to designing our own assets

Customer interfaces Supply chain Warehouse

Vans & Routing Delivery

Mechanical handling equipment

Track record of enabling online businesses Morrisons is Ocado’s first external customer

Launched January 2014 Morrisons announced a 12 month sales

run rate of around £200m in March 2015

22

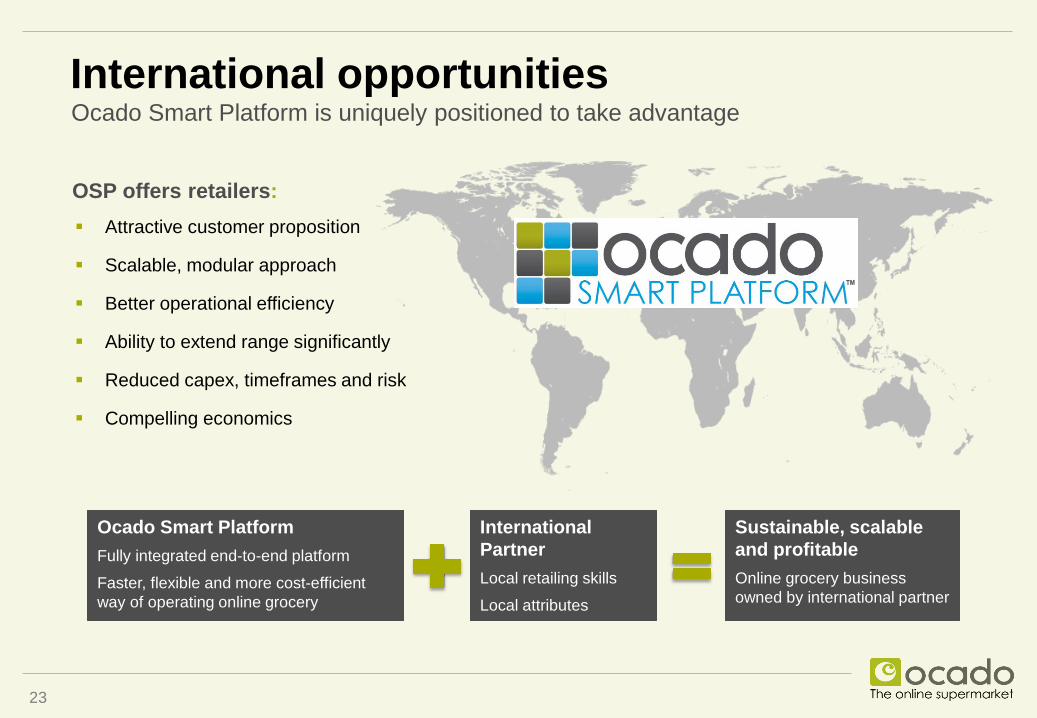

Attractive customer proposition

Scalable, modular approach

Better operational efficiency

Ability to extend range significantly

Reduced capex, timeframes and risk

Compelling economics

OSP offers retailers:

23

International opportunities Ocado Smart Platform is uniquely positioned to take advantage

Ocado Smart Platform Fully integrated end-to-end platform

Faster, flexible and more cost-efficient way of operating online grocery

International Partner Local retailing skills

Local attributes

Sustainable, scalable and profitable Online grocery business owned by international partner

Ocado summary

World’s largest dedicated online grocery supermarket

Global grocery market is huge with channel shift to online growing

Technology and innovation drives superior customer proposition and ‘best in class’ operating model

Commercialising IP offers significant value creation from Ocado Smart Platform internationally

25

Top Related