Languages

Pages

Legal

© Experian Public

Experian Automotive Quarterly Briefing Fourth quarter 2016 automotive market share trends and registrations

Brad Smith | Director, Automotive Market Statistics

Marty Miller | Senior Product Manager, Vehicles in Operation (VIO)

2 © Experian Public

Today’s presentationPart one

Presentation will be available 24-48 hours after Webinar

Email with a link will be sent to all registrants to download

Questions? Contact us at [email protected]

What’s on the Road

VIO by model year, segment, age and market share

U.S. light duty vehicles through December 31, 2016

U.S. medium and heavy duty vehicles through December 31, 2016

Marty Miller

Senior Product Manager, VIO

3 © Experian Public

Q4 2016 Registrations

Market trends

Geographic performance

Manufacturer, make and model share

Loyalty, conquest and defection

Session overviewPart two

Brad Smith

Director, Automotive

Market Statistics

4 © Experian Public

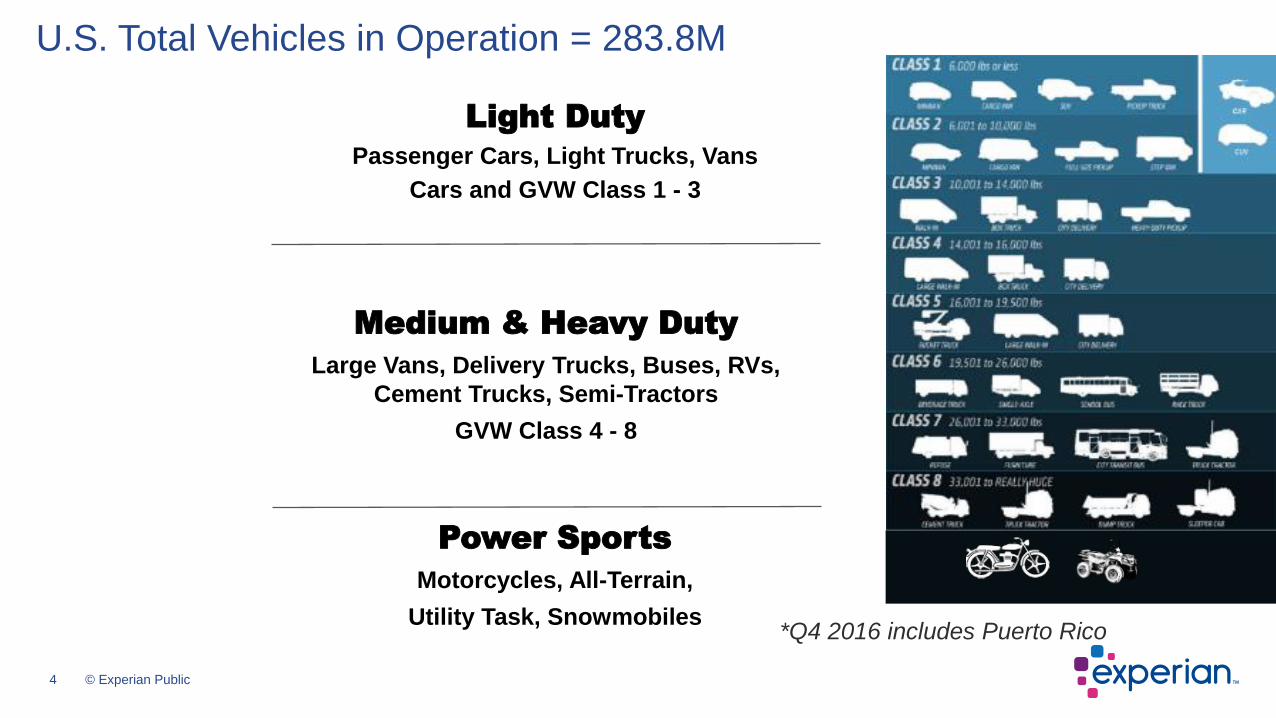

U.S. Total Vehicles in Operation = 283.8M

Light Duty

Passenger Cars, Light Trucks, Vans

Cars and GVW Class 1 - 3

Medium & Heavy Duty

Large Vans, Delivery Trucks, Buses, RVs,

Cement Trucks, Semi-Tractors

GVW Class 4 - 8

Power Sports

Motorcycles, All-Terrain,

Utility Task, Snowmobiles*Q4 2016 includes Puerto Rico

5 © Experian Public

What’s on the road today?

Light Duty Vehicles

Vehicles in Operation

6 © Experian Public

Source: Experian

Automotive as of

December 31, 2016

(U.S. light duty

vehicles only)

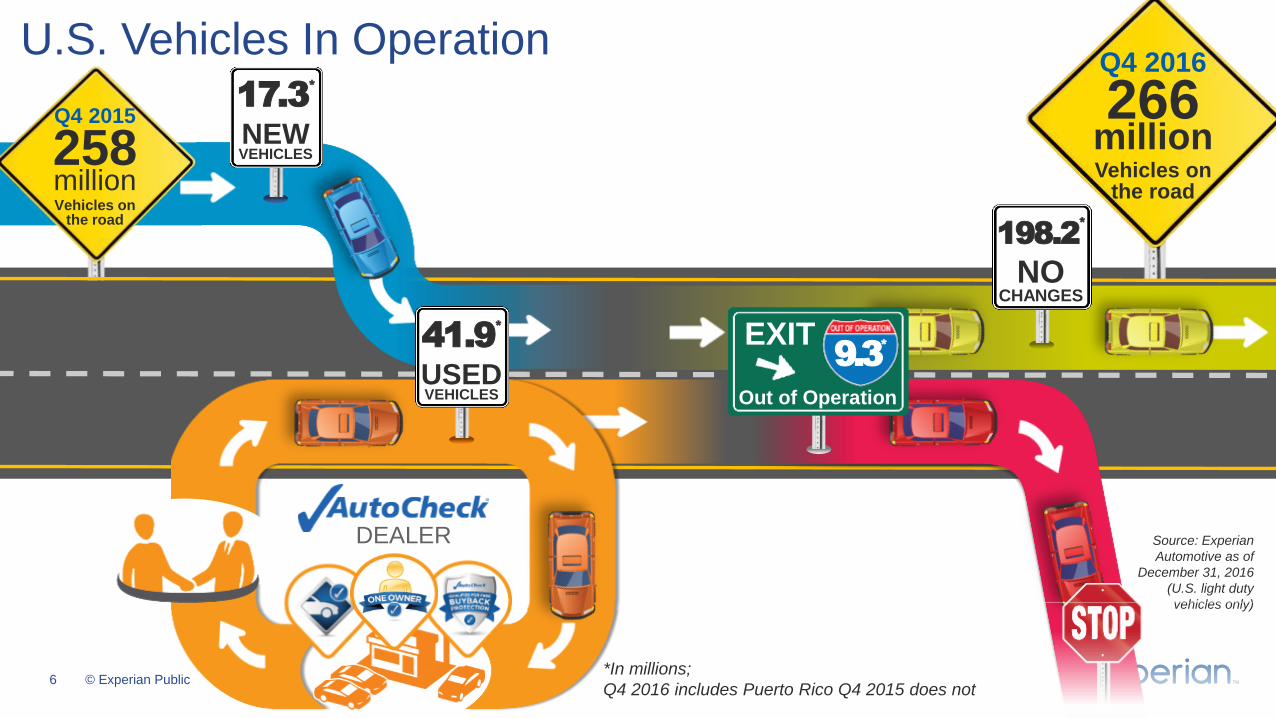

U.S. Vehicles In Operation

Q4 2015

258millionVehicles on

the road

Q4 2016

266millionVehicles on

the road

17.3*

NEWVEHICLES

DEALER

41.9*

USEDVEHICLES

198.2*

NOCHANGES

9.3*

EXIT

Out of Operation

*In millions;

Q4 2016 includes Puerto Rico Q4 2015 does not

7 © Experian Public

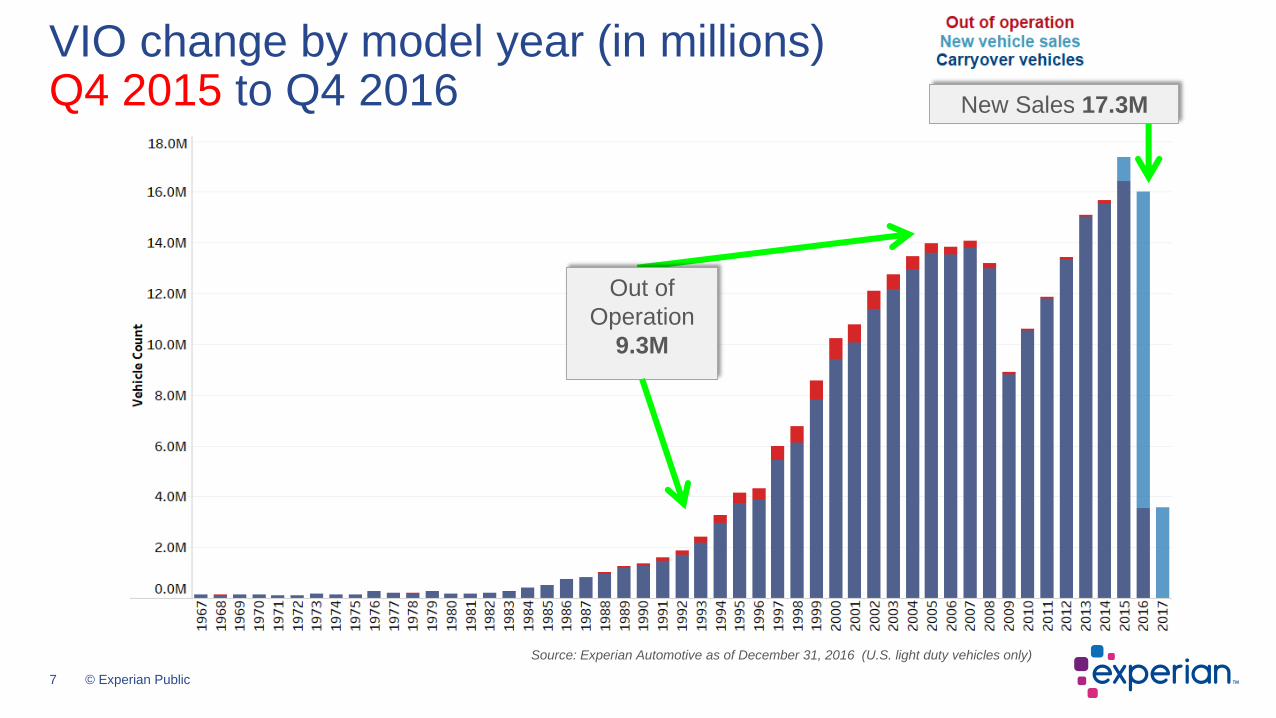

VIO change by model year (in millions)Q4 2015 to Q4 2016 New Sales 17.3M

Out of

Operation

9.3M

Source: Experian Automotive as of December 31, 2016 (U.S. light duty vehicles only)

8 © Experian Public

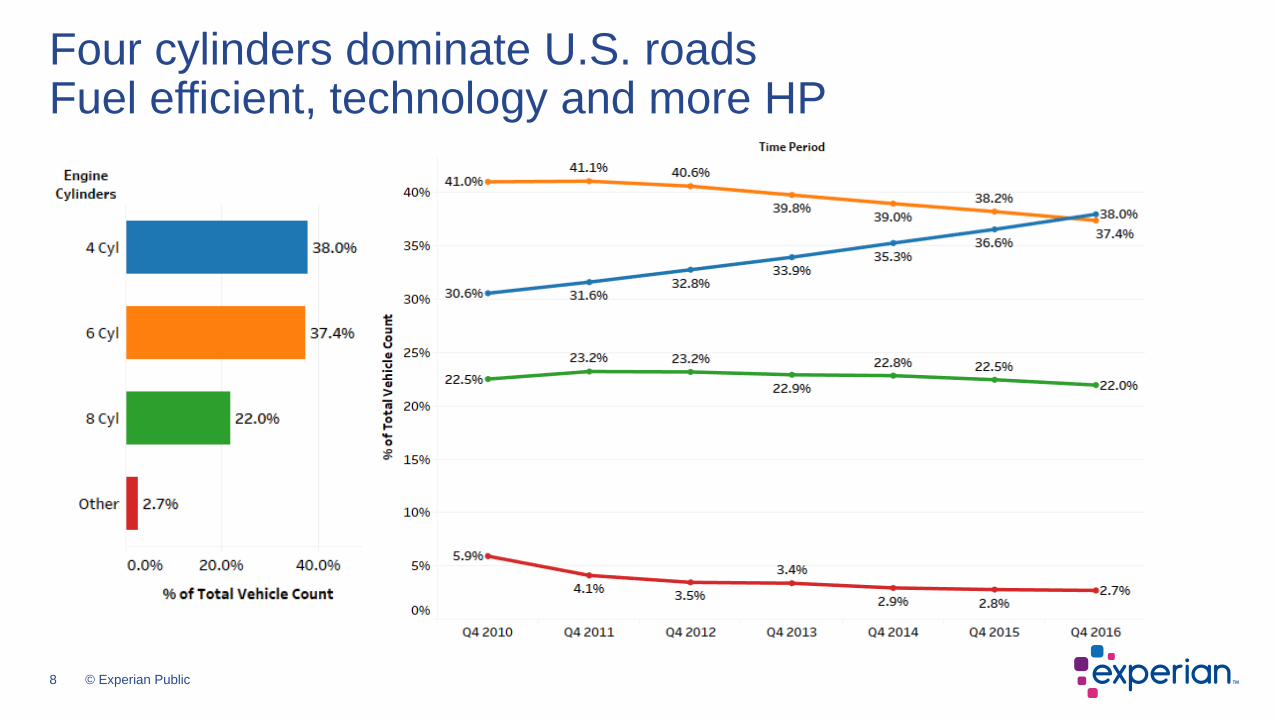

Four cylinders dominate U.S. roadsFuel efficient, technology and more HP

9 © Experian Public

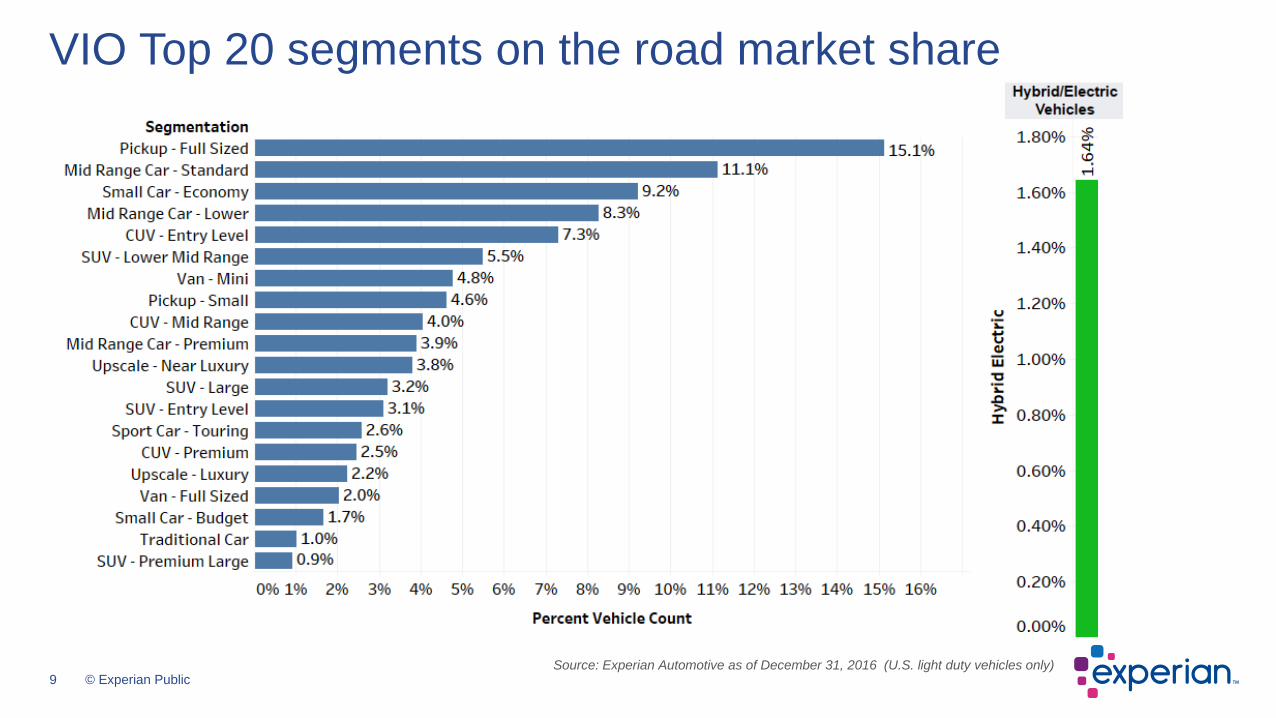

VIO Top 20 segments on the road market share

Source: Experian Automotive as of December 31, 2016 (U.S. light duty vehicles only)

10 © Experian Public

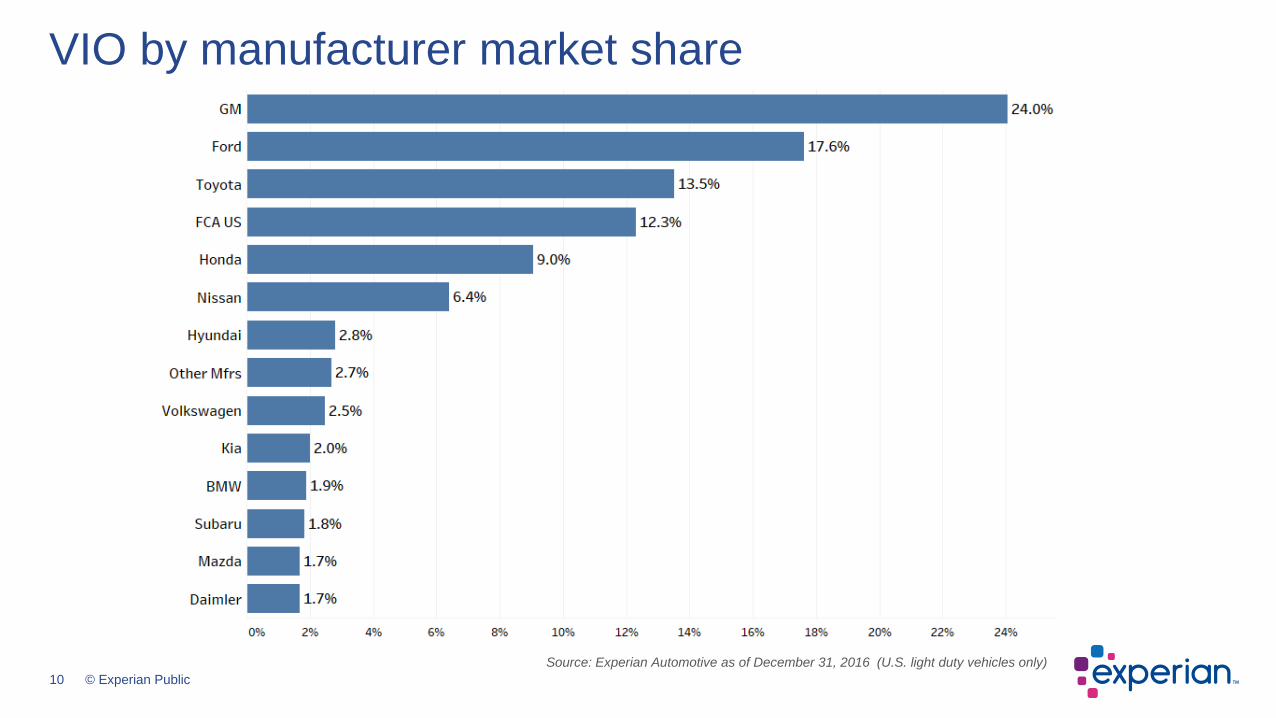

VIO by manufacturer market share

Source: Experian Automotive as of December 31, 2016 (U.S. light duty vehicles only)

11 © Experian Public

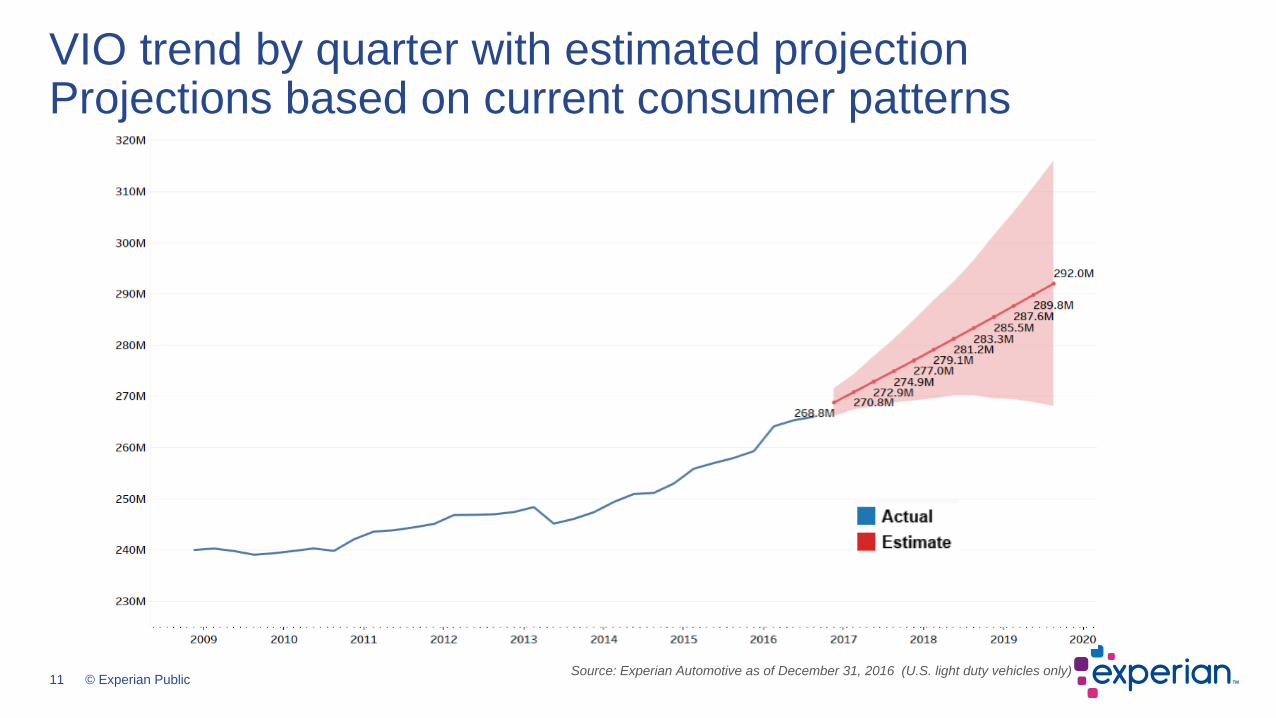

VIO trend by quarter with estimated projectionProjections based on current consumer patterns

Source: Experian Automotive as of December 31, 2016 (U.S. light duty vehicles only)

12 © Experian Public

The aftermarket “Sweet Spot” is defined as 6 to 12 model year old vehicles, and because of their age, are out of the general OEM manufacturer warranty for any repairs.

These vehicles are within a time period when more part replacement or services are needed (e.g. shocks, timing belt service, engine repairs) that may be performed by aftermarket service shops which are supplied by aftermarket part manufacturers and retailers.

Defining the Sweet Spot size helps identify the overall market potential, and changes can have implications to those that service it.

“Post Sweet Spot” vehicles are defined as 13 model years old or older, and identify the models where less costs may be spent to service them due to their age and vehicle value.

“Pre Sweet Spot” vehicles are defined as 5 model years old or newer, and identify the incoming models into the Sweet Spot.

The aftermarket “Sweet Spot” overview“Post” and “Pre” Sweet Spot defined

13 © Experian Public

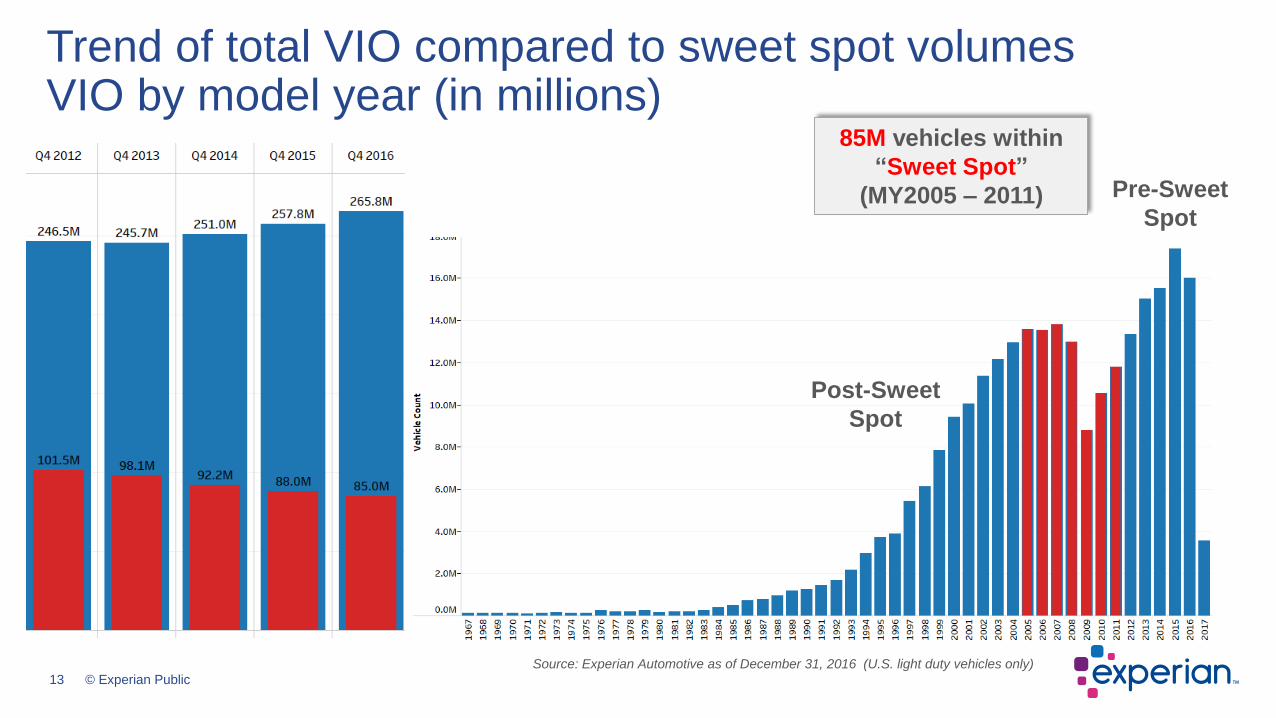

Trend of total VIO compared to sweet spot volumesVIO by model year (in millions)

85M vehicles within

“Sweet Spot”

(MY2005 – 2011) Pre-Sweet

Spot

Post-Sweet

Spot

Source: Experian Automotive as of December 31, 2016 (U.S. light duty vehicles only)

14 © Experian Public

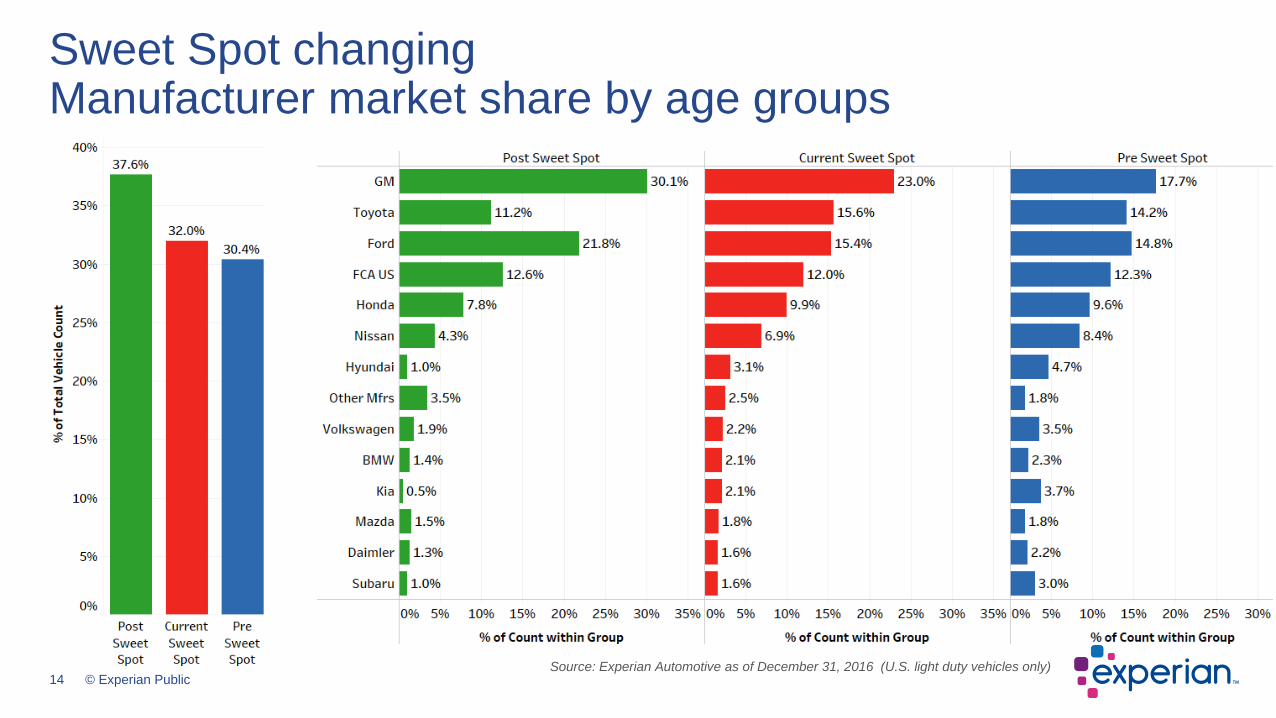

Sweet Spot changingManufacturer market share by age groups

Source: Experian Automotive as of December 31, 2016 (U.S. light duty vehicles only)

15 © Experian Public

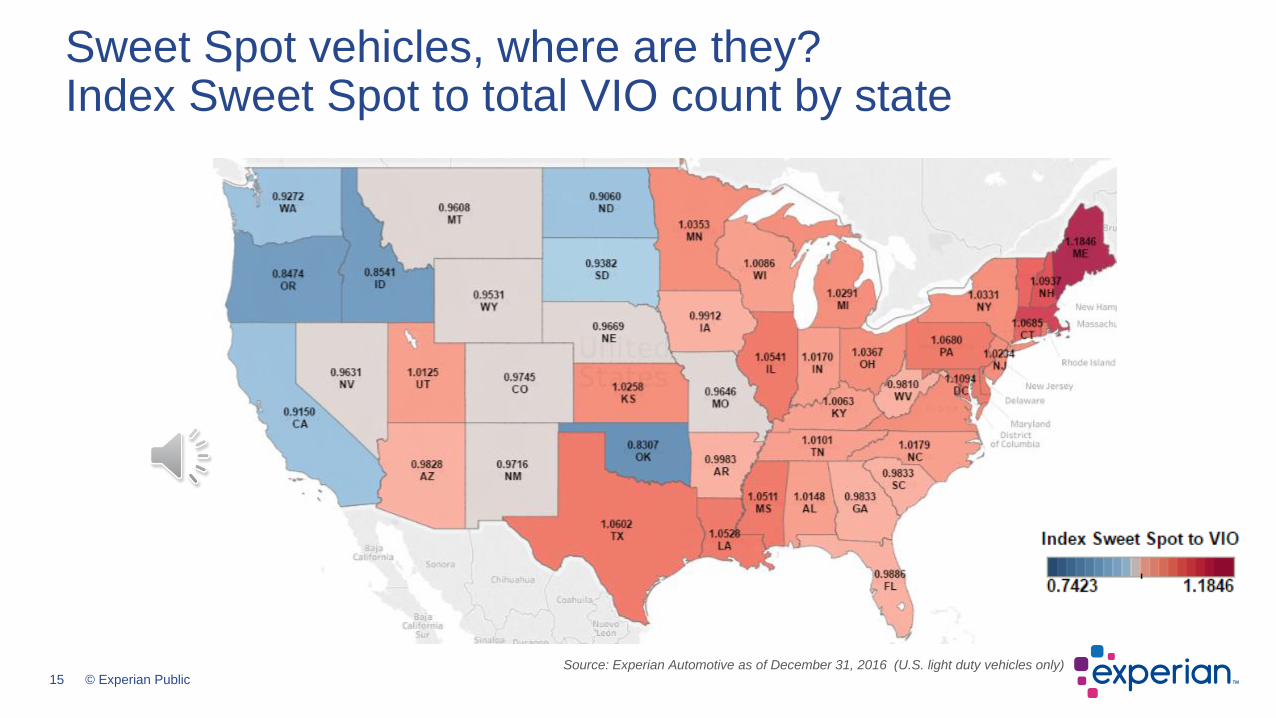

Sweet Spot vehicles, where are they?Index Sweet Spot to total VIO count by state

Source: Experian Automotive as of December 31, 2016 (U.S. light duty vehicles only)

16 © Experian Public

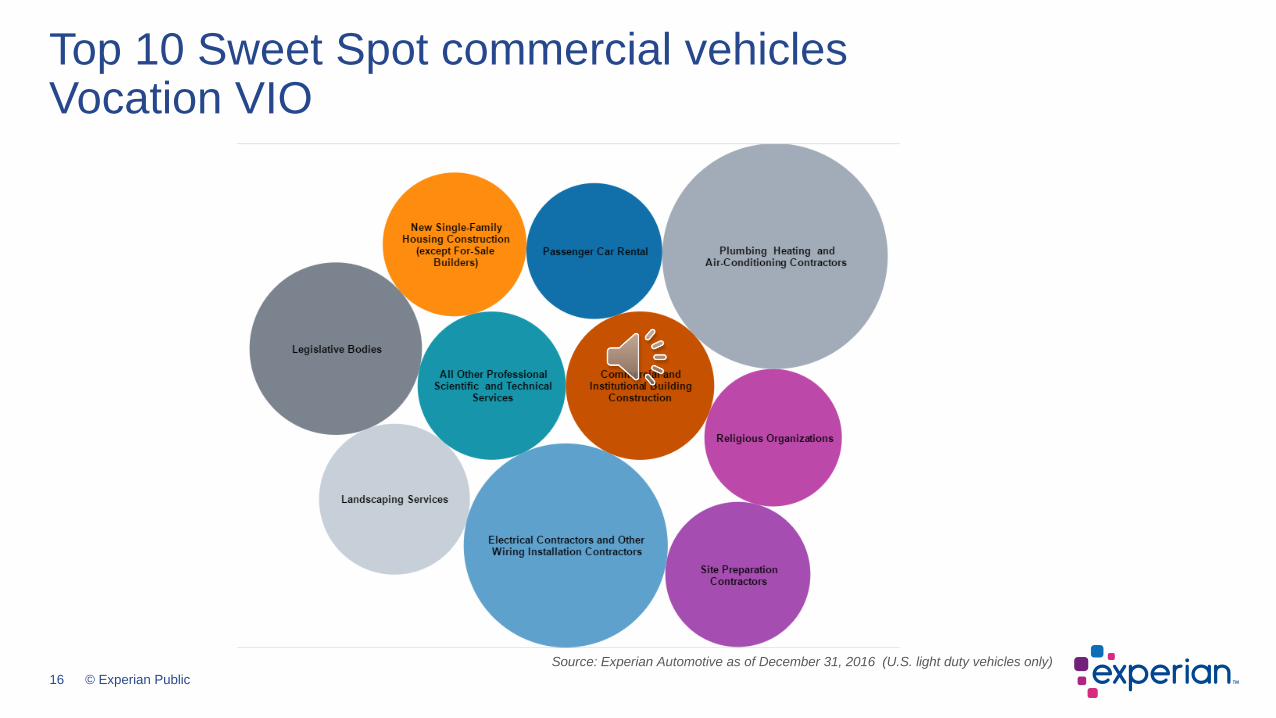

Top 10 Sweet Spot commercial vehiclesVocation VIO

Source: Experian Automotive as of December 31, 2016 (U.S. light duty vehicles only)

17 © Experian Public

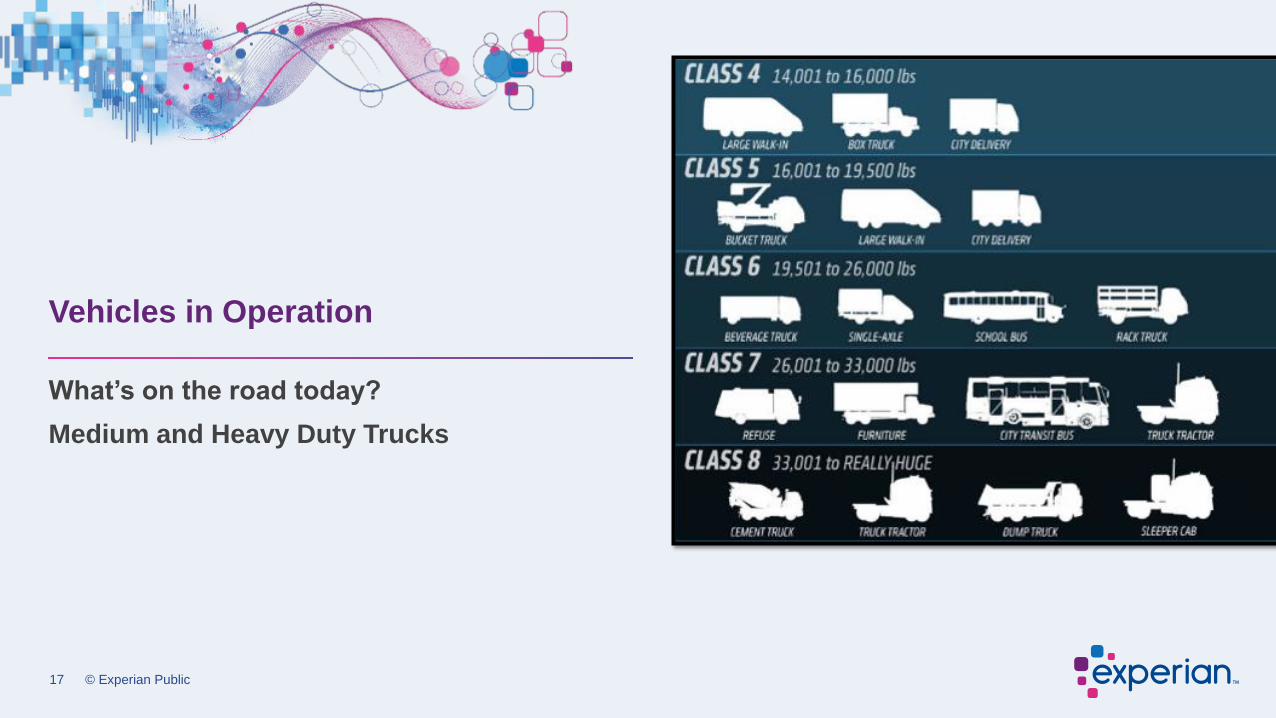

What’s on the road today?

Medium and Heavy Duty Trucks

Vehicles in Operation

18 © Experian Public

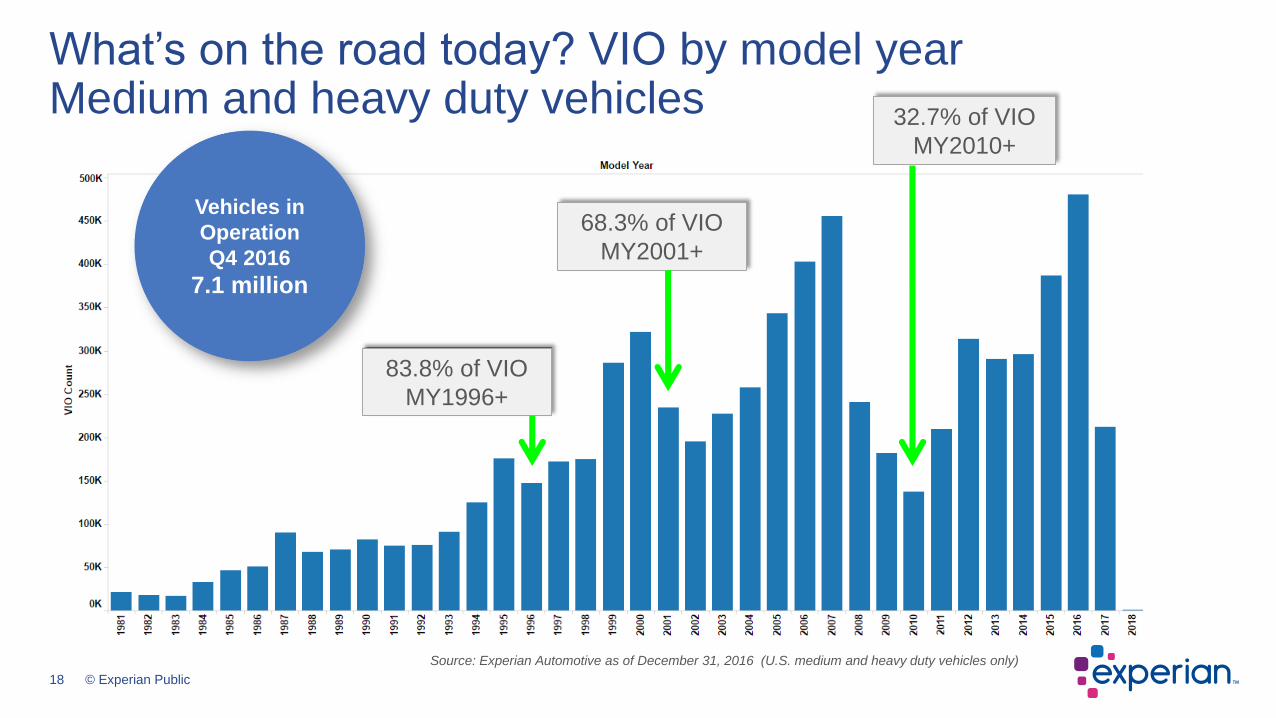

What’s on the road today? VIO by model yearMedium and heavy duty vehicles

32.7% of VIO

MY2010+

68.3% of VIO

MY2001+

83.8% of VIO

MY1996+

Vehicles in

Operation

Q4 2016

7.1 million

Source: Experian Automotive as of December 31, 2016 (U.S. medium and heavy duty vehicles only)

19 © Experian Public

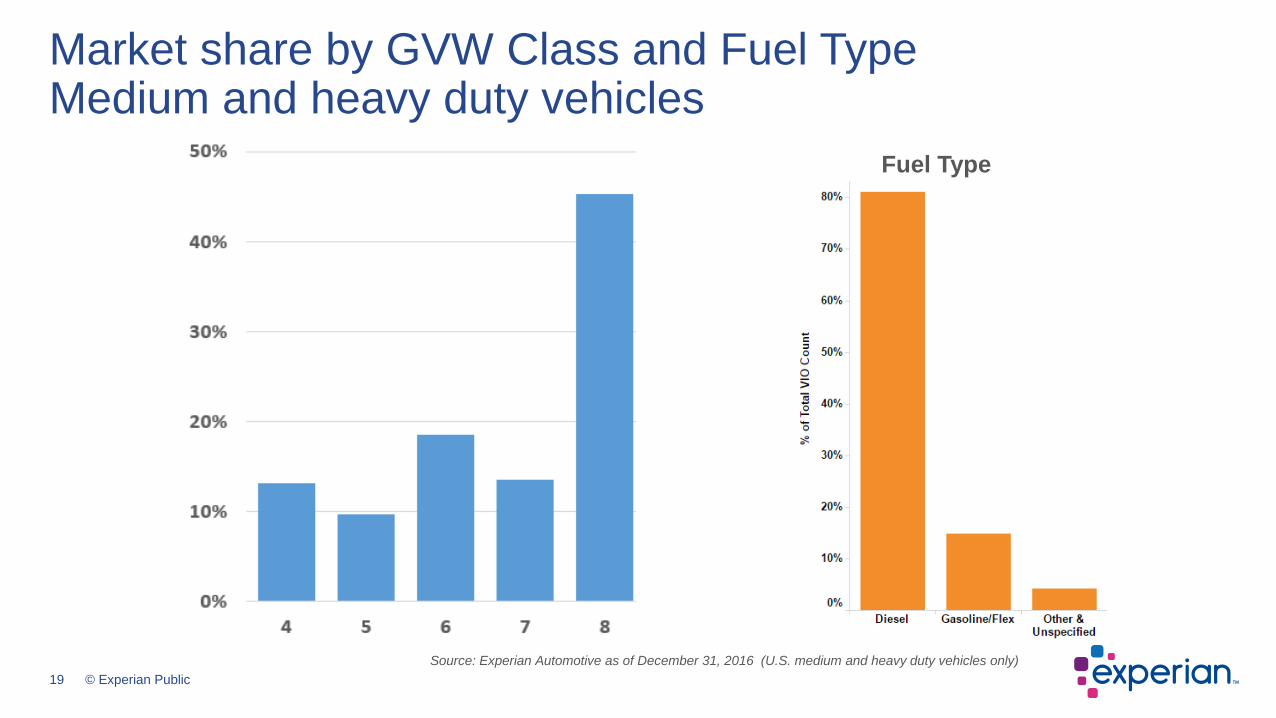

Market share by GVW Class and Fuel TypeMedium and heavy duty vehicles

GVW Class Fuel Type

Source: Experian Automotive as of December 31, 2016 (U.S. medium and heavy duty vehicles only)

20 © Experian Public

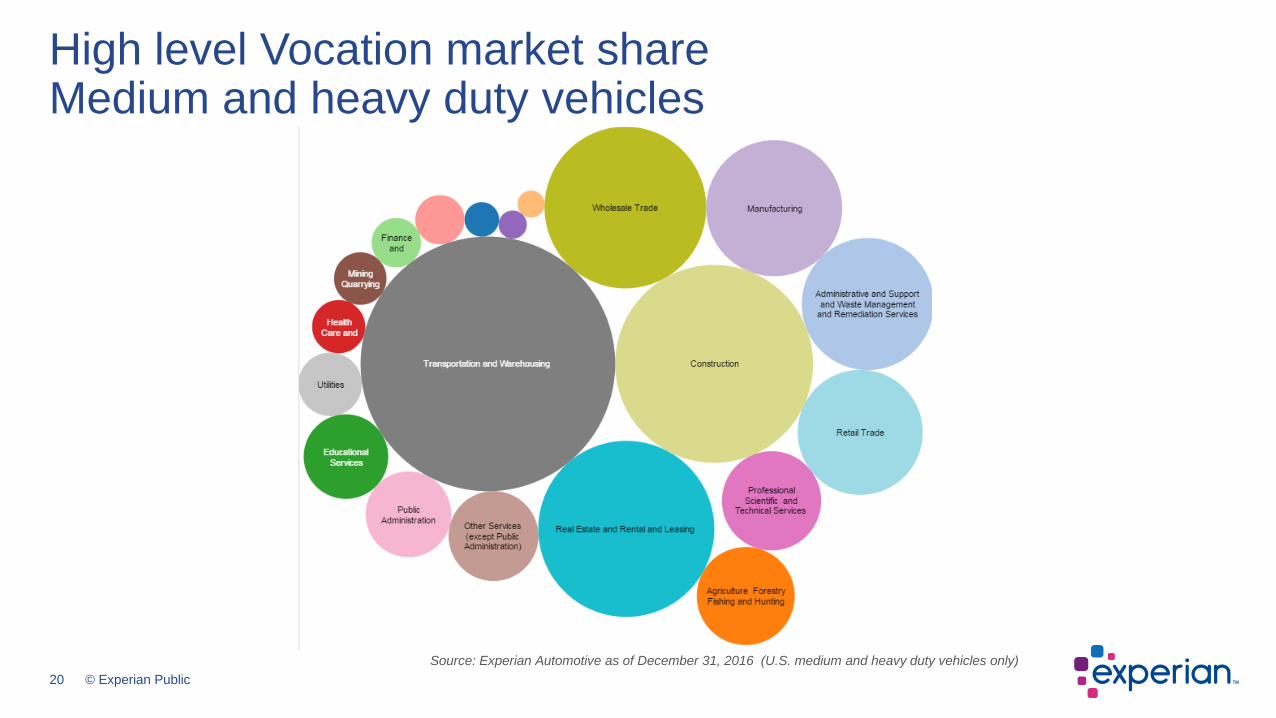

High level Vocation market shareMedium and heavy duty vehicles

Source: Experian Automotive as of December 31, 2016 (U.S. medium and heavy duty vehicles only)

© Experian [Public, Confidential, Internal, Restricted – choose the appropriate category]

U.S. Market Overview

• New registration totals• Year over year changes in performance• Share by sales category• Impact of demographics on purchasing behavior• Share across geographies and vehicle segments• Brand leaders

22 © Experian Public

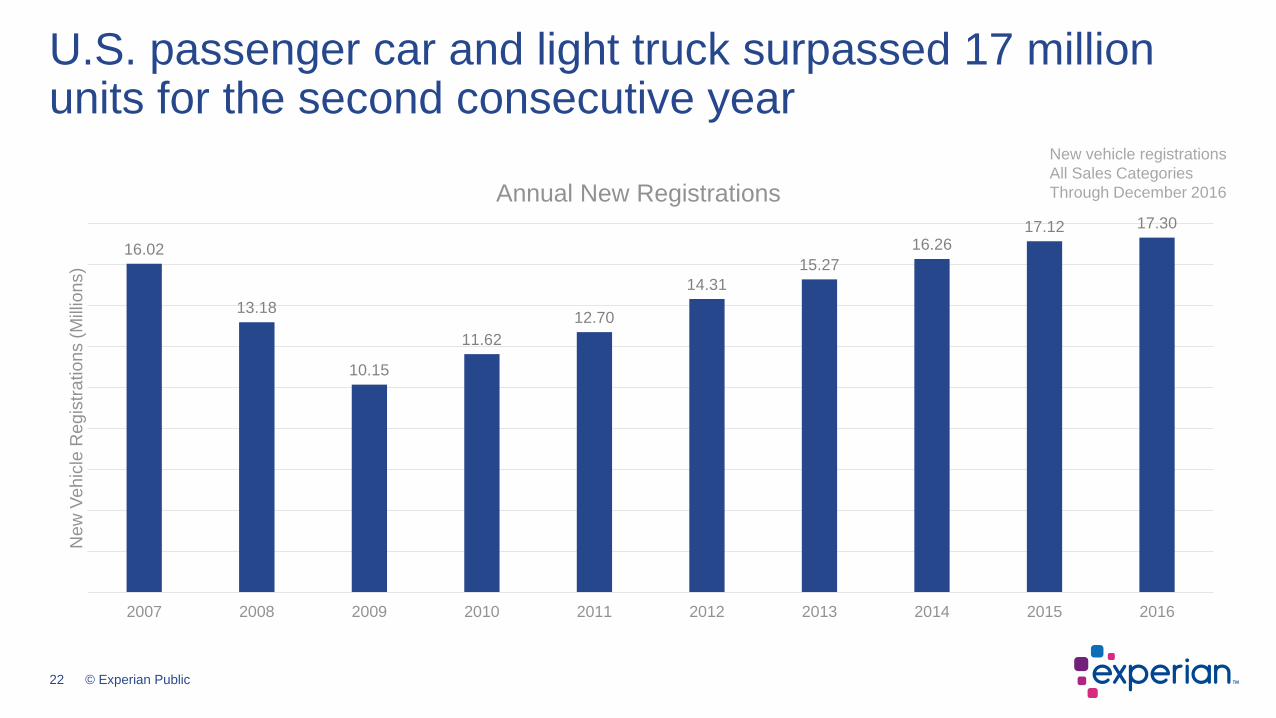

16.02

13.18

10.15

11.62

12.70

14.31

15.27

16.2617.12 17.30

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

New

Veh

icle

Reg

istr

ations (

Mill

ion

s)

Annual New Registrations

U.S. passenger car and light truck surpassed 17 million units for the second consecutive year

New vehicle registrations

All Sales Categories

Through December 2016

23 © Experian Public

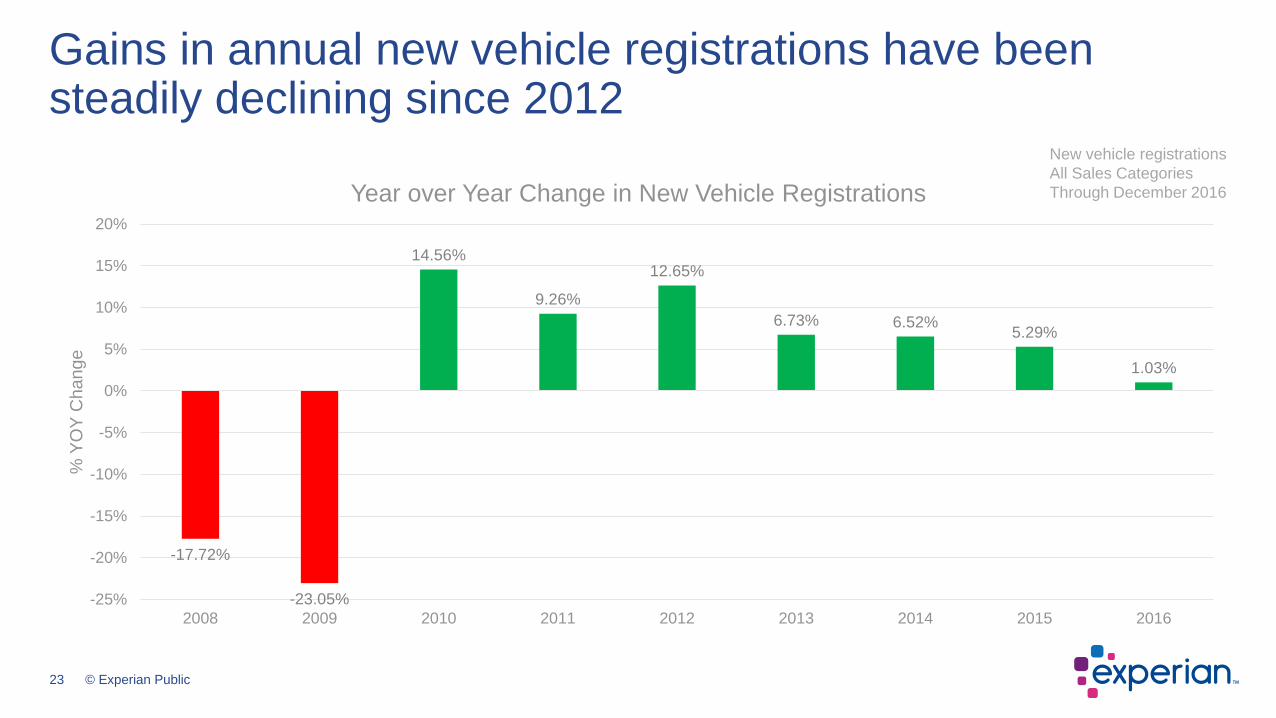

-17.72%

-23.05%

14.56%

9.26%

12.65%

6.73% 6.52%5.29%

1.03%

-25%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

2008 2009 2010 2011 2012 2013 2014 2015 2016

% Y

OY

Cha

ng

e

Year over Year Change in New Vehicle Registrations

Gains in annual new vehicle registrations have been steadily declining since 2012

New vehicle registrations

All Sales Categories

Through December 2016

24 © Experian Public

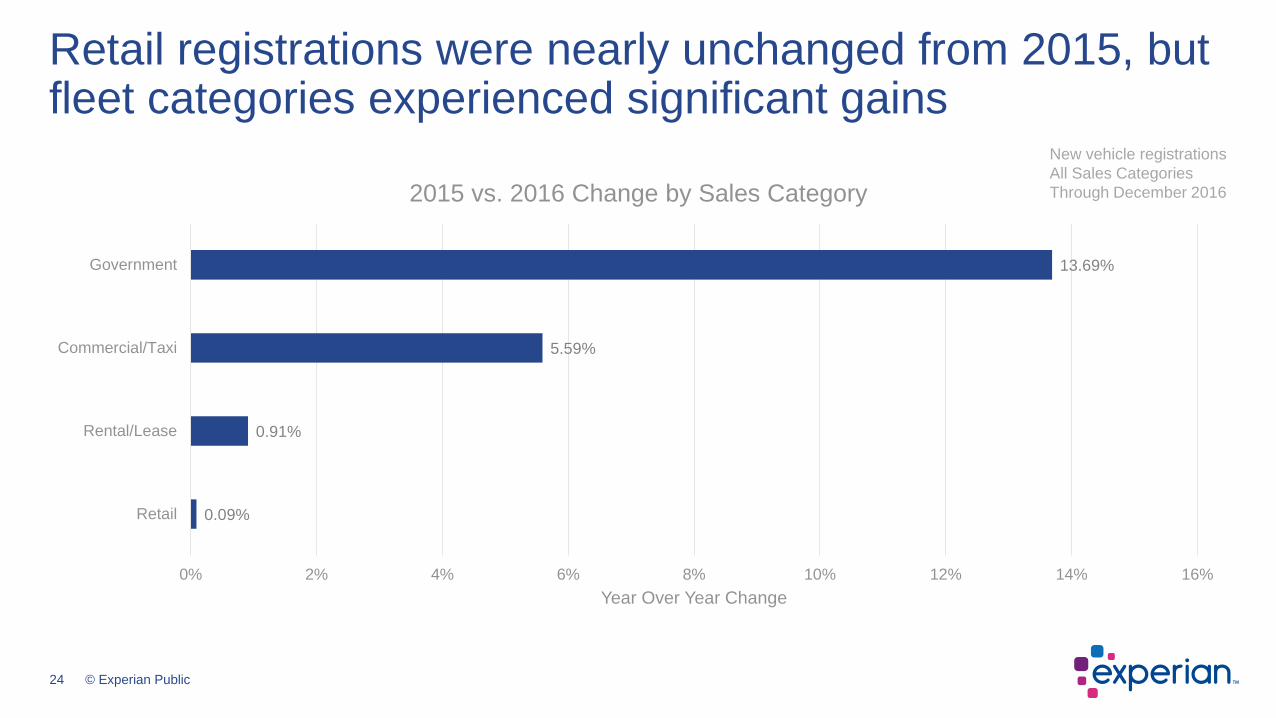

0.09%

0.91%

5.59%

13.69%

0% 2% 4% 6% 8% 10% 12% 14% 16%

Retail

Rental/Lease

Commercial/Taxi

Government

Year Over Year Change

2015 vs. 2016 Change by Sales Category

Retail registrations were nearly unchanged from 2015, but fleet categories experienced significant gains

New vehicle registrations

All Sales Categories

Through December 2016

25 © Experian Public

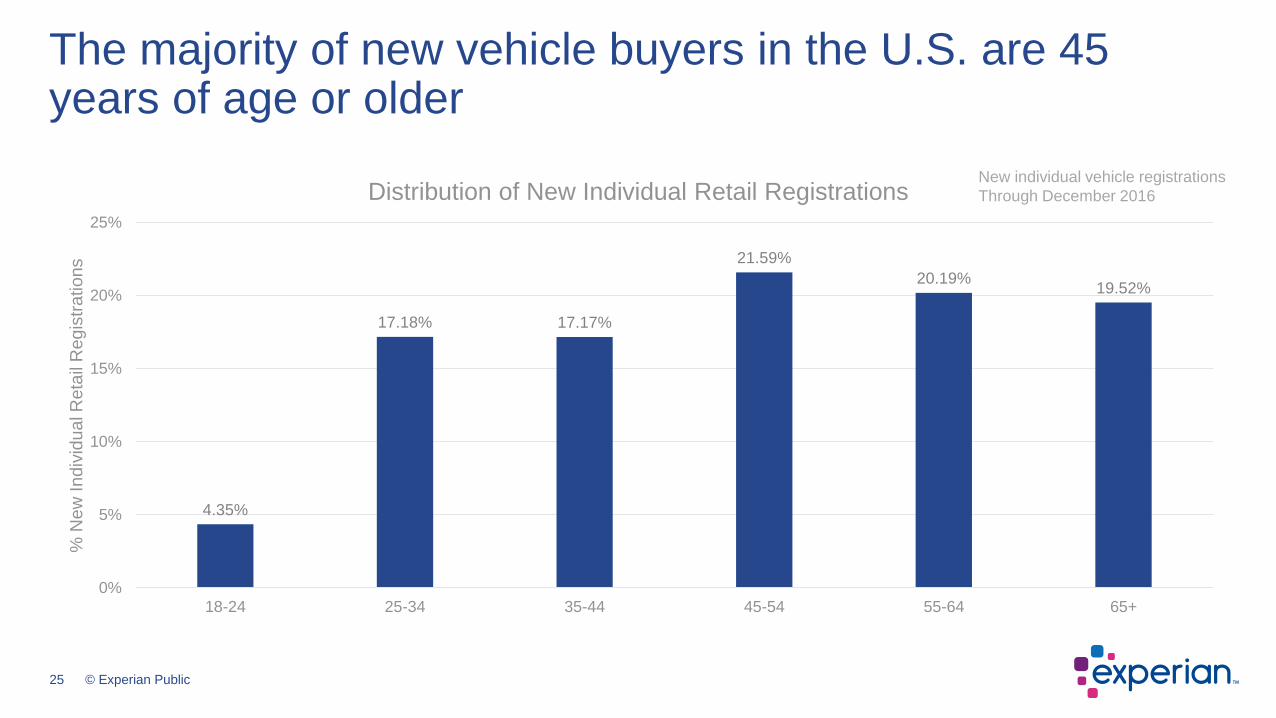

4.35%

17.18% 17.17%

21.59%

20.19%19.52%

0%

5%

10%

15%

20%

25%

18-24 25-34 35-44 45-54 55-64 65+

% N

ew

In

div

idu

al R

eta

il R

eg

istr

ations

Distribution of New Individual Retail Registrations

The majority of new vehicle buyers in the U.S. are 45 years of age or older

New individual vehicle registrations

Through December 2016

26 © Experian Public

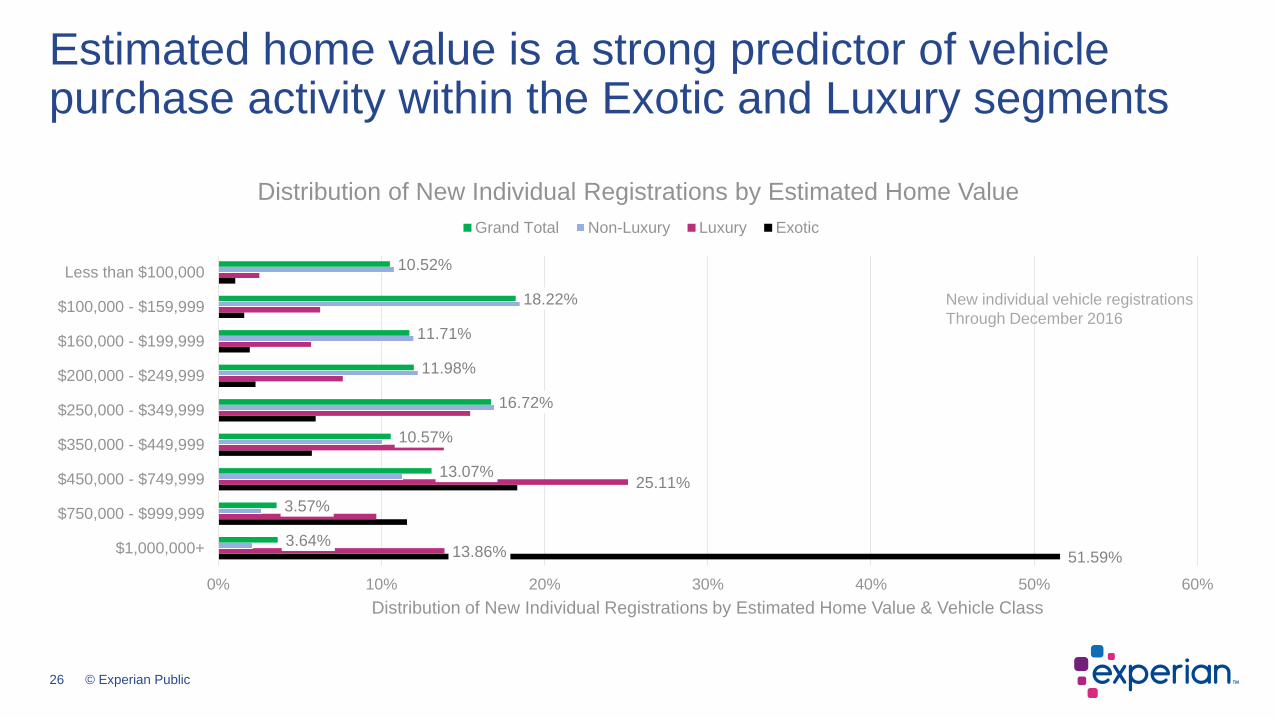

51.59%13.86%

25.11%

3.64%

3.57%

13.07%

10.57%

16.72%

11.98%

11.71%

18.22%

10.52%

0% 10% 20% 30% 40% 50% 60%

$1,000,000+

$750,000 - $999,999

$450,000 - $749,999

$350,000 - $449,999

$250,000 - $349,999

$200,000 - $249,999

$160,000 - $199,999

$100,000 - $159,999

Less than $100,000

Distribution of New Individual Registrations by Estimated Home Value & Vehicle Class

Distribution of New Individual Registrations by Estimated Home Value

Grand Total Non-Luxury Luxury Exotic

Estimated home value is a strong predictor of vehicle purchase activity within the Exotic and Luxury segments

New individual vehicle registrations

Through December 2016

27 © Experian Public

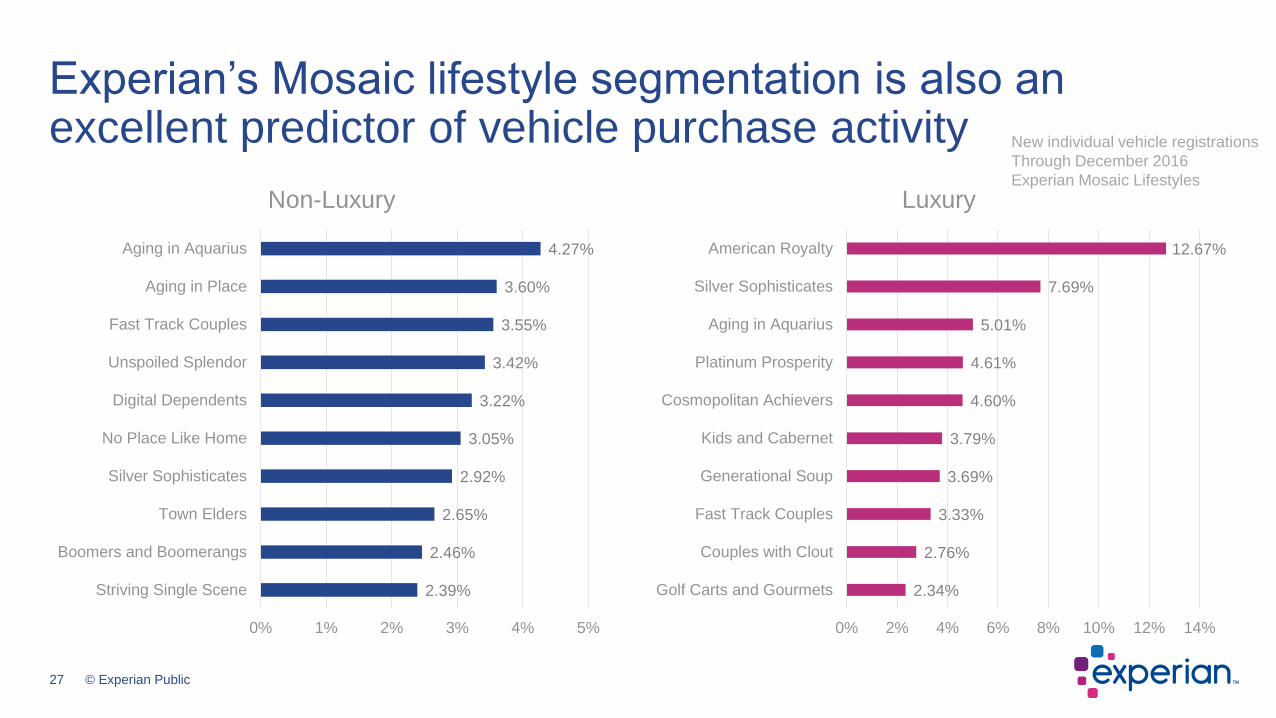

2.39%

2.46%

2.65%

2.92%

3.05%

3.22%

3.42%

3.55%

3.60%

4.27%

0% 1% 2% 3% 4% 5%

Striving Single Scene

Boomers and Boomerangs

Town Elders

Silver Sophisticates

No Place Like Home

Digital Dependents

Unspoiled Splendor

Fast Track Couples

Aging in Place

Aging in Aquarius

Non-Luxury

Experian’s Mosaic lifestyle segmentation is also an excellent predictor of vehicle purchase activity

2.34%

2.76%

3.33%

3.69%

3.79%

4.60%

4.61%

5.01%

7.69%

12.67%

0% 2% 4% 6% 8% 10% 12% 14%

Golf Carts and Gourmets

Couples with Clout

Fast Track Couples

Generational Soup

Kids and Cabernet

Cosmopolitan Achievers

Platinum Prosperity

Aging in Aquarius

Silver Sophisticates

American Royalty

Luxury

New individual vehicle registrations

Through December 2016

Experian Mosaic Lifestyles

28 © Experian Public

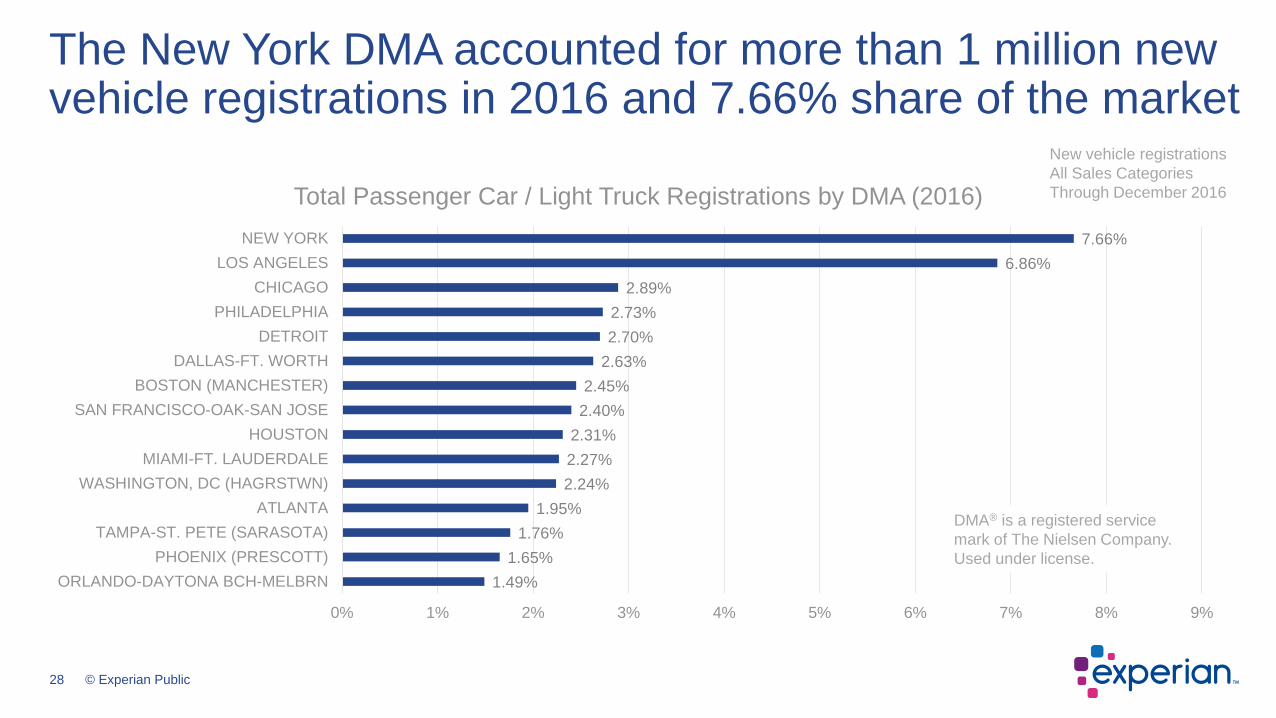

1.49%

1.65%

1.76%

1.95%

2.24%

2.27%

2.31%

2.40%

2.45%

2.63%

2.70%

2.73%

2.89%

6.86%

7.66%

0% 1% 2% 3% 4% 5% 6% 7% 8% 9%

ORLANDO-DAYTONA BCH-MELBRN

PHOENIX (PRESCOTT)

TAMPA-ST. PETE (SARASOTA)

ATLANTA

WASHINGTON, DC (HAGRSTWN)

MIAMI-FT. LAUDERDALE

HOUSTON

SAN FRANCISCO-OAK-SAN JOSE

BOSTON (MANCHESTER)

DALLAS-FT. WORTH

DETROIT

PHILADELPHIA

CHICAGO

LOS ANGELES

NEW YORK

Total Passenger Car / Light Truck Registrations by DMA (2016)

The New York DMA accounted for more than 1 million new vehicle registrations in 2016 and 7.66% share of the market

New vehicle registrations

All Sales Categories

Through December 2016

DMA® is a registered service

mark of The Nielsen Company.

Used under license.

29 © Experian Public

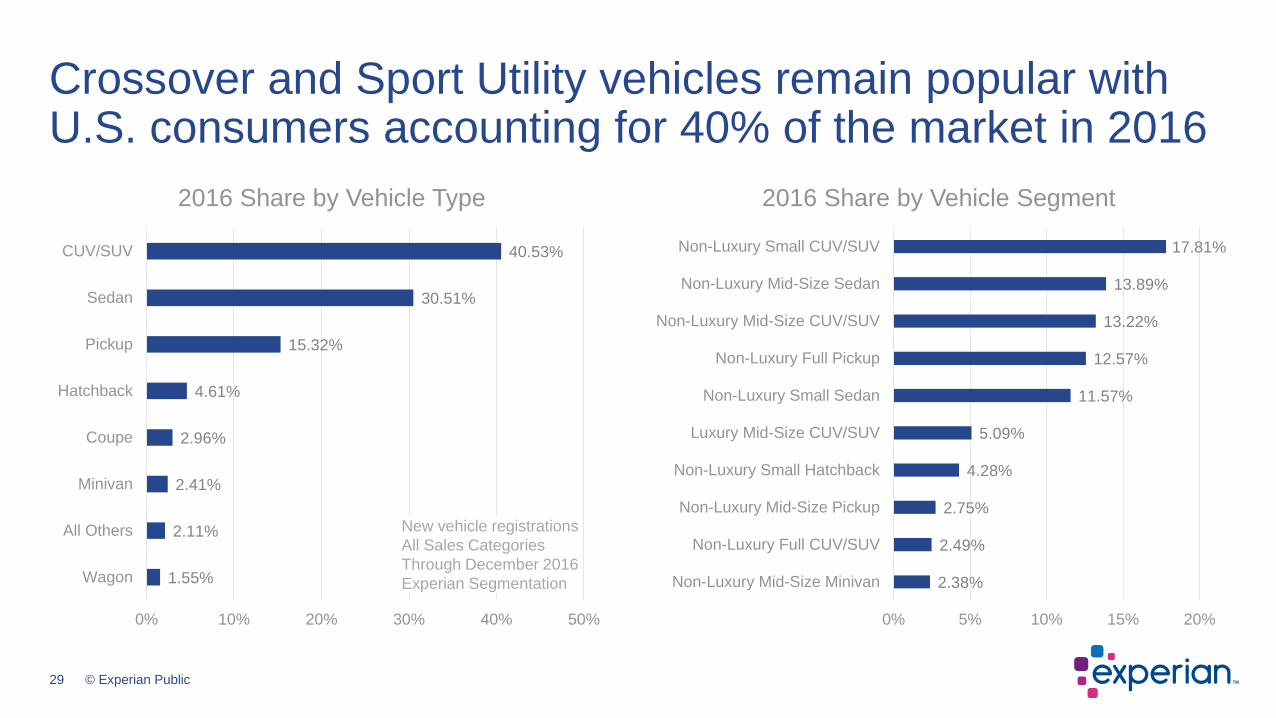

1.55%

2.11%

2.41%

2.96%

4.61%

15.32%

30.51%

40.53%

0% 10% 20% 30% 40% 50%

Wagon

All Others

Minivan

Coupe

Hatchback

Pickup

Sedan

CUV/SUV

2016 Share by Vehicle Type

Crossover and Sport Utility vehicles remain popular with U.S. consumers accounting for 40% of the market in 2016

2.38%

2.49%

2.75%

4.28%

5.09%

11.57%

12.57%

13.22%

13.89%

17.81%

0% 5% 10% 15% 20%

Non-Luxury Mid-Size Minivan

Non-Luxury Full CUV/SUV

Non-Luxury Mid-Size Pickup

Non-Luxury Small Hatchback

Luxury Mid-Size CUV/SUV

Non-Luxury Small Sedan

Non-Luxury Full Pickup

Non-Luxury Mid-Size CUV/SUV

Non-Luxury Mid-Size Sedan

Non-Luxury Small CUV/SUV

2016 Share by Vehicle Segment

New vehicle registrations

All Sales Categories

Through December 2016

Experian Segmentation

30 © Experian Public

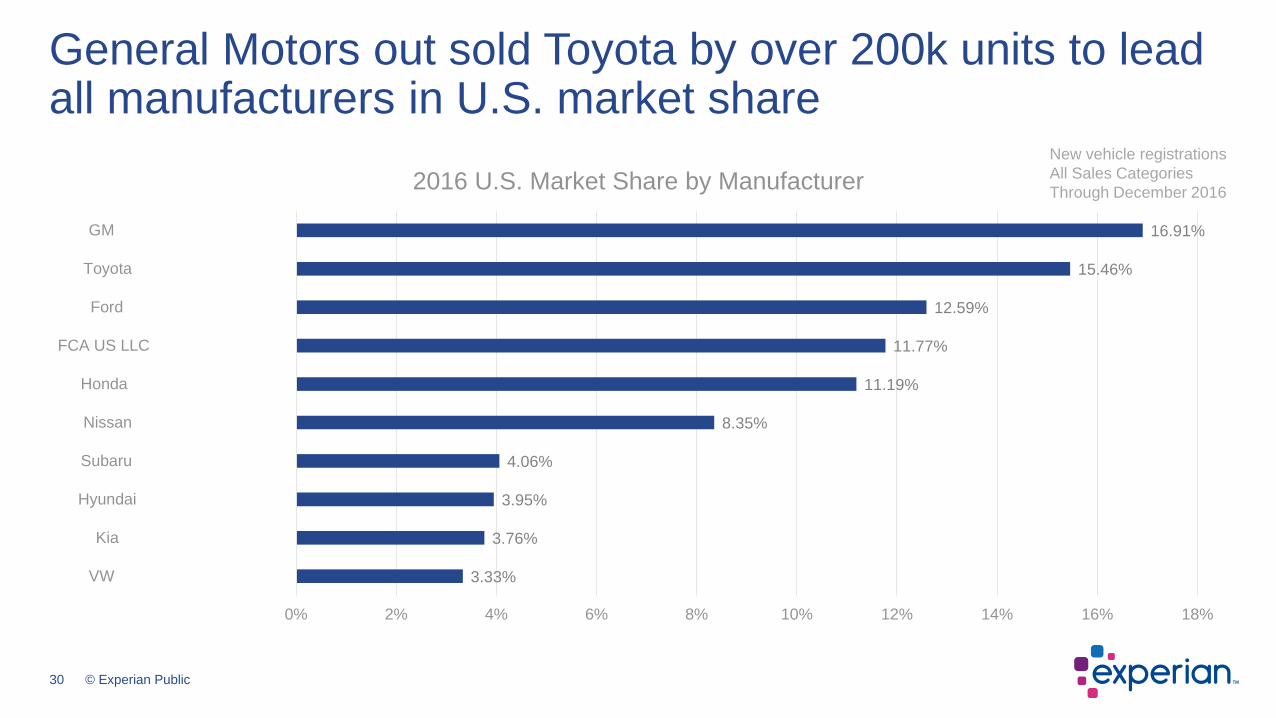

3.33%

3.76%

3.95%

4.06%

8.35%

11.19%

11.77%

12.59%

15.46%

16.91%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

VW

Kia

Hyundai

Subaru

Nissan

Honda

FCA US LLC

Ford

Toyota

GM

2016 U.S. Market Share by Manufacturer

General Motors out sold Toyota by over 200k units to lead all manufacturers in U.S. market share

New vehicle registrations

All Sales Categories

Through December 2016

31 © Experian Public

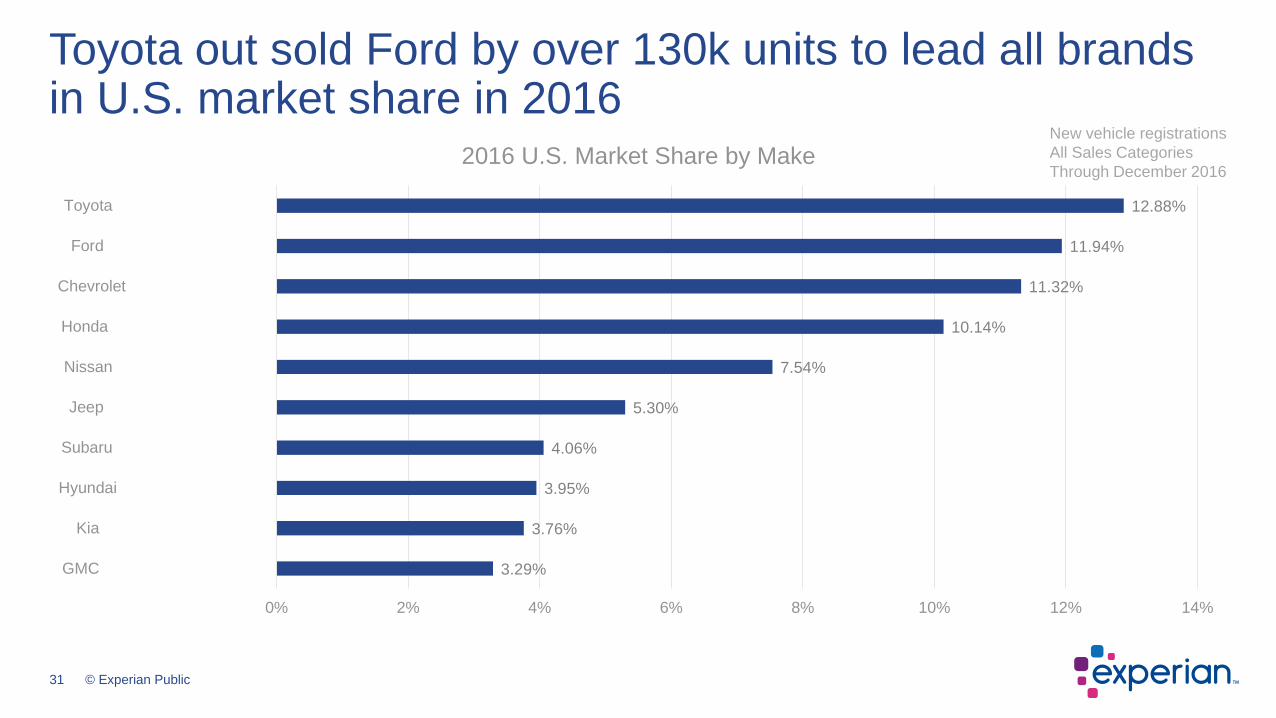

3.29%

3.76%

3.95%

4.06%

5.30%

7.54%

10.14%

11.32%

11.94%

12.88%

0% 2% 4% 6% 8% 10% 12% 14%

GMC

Kia

Hyundai

Subaru

Jeep

Nissan

Honda

Chevrolet

Ford

Toyota

2016 U.S. Market Share by Make

Toyota out sold Ford by over 130k units to lead all brands in U.S. market share in 2016

New vehicle registrations

All Sales Categories

Through December 2016

32 © Experian Public

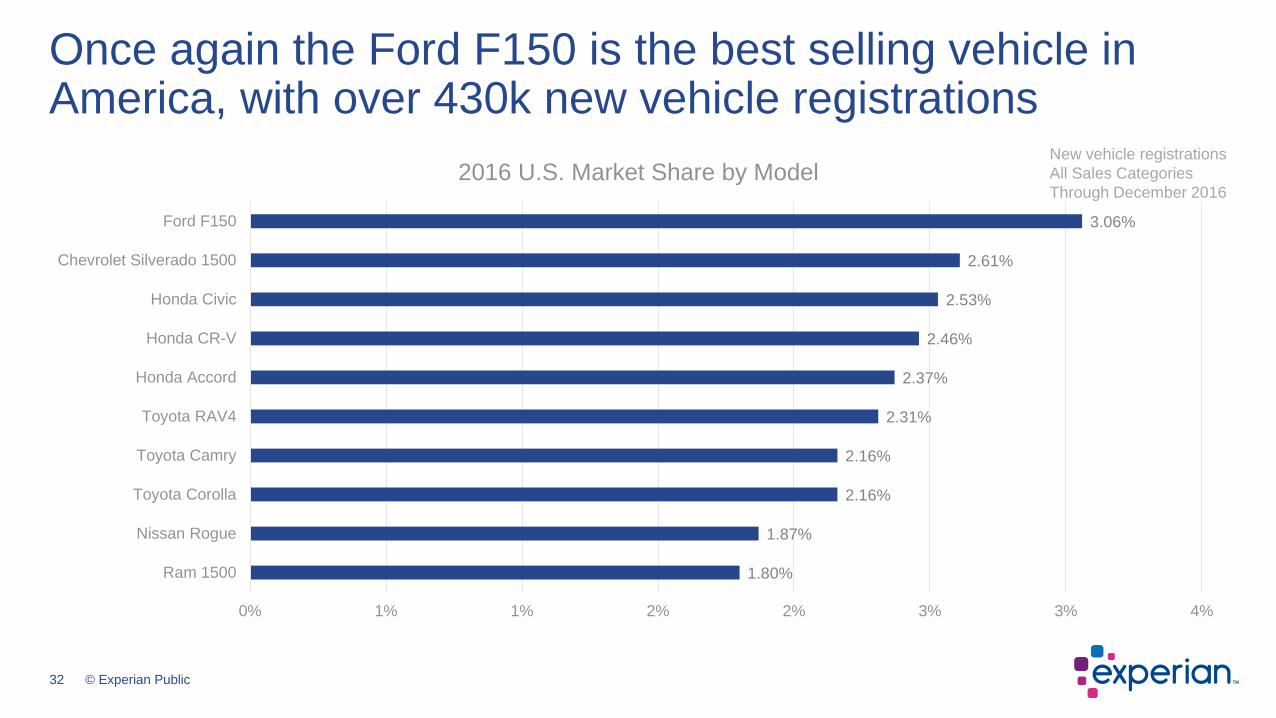

1.80%

1.87%

2.16%

2.16%

2.31%

2.37%

2.46%

2.53%

2.61%

3.06%

0% 1% 1% 2% 2% 3% 3% 4%

Ram 1500

Nissan Rogue

Toyota Corolla

Toyota Camry

Toyota RAV4

Honda Accord

Honda CR-V

Honda Civic

Chevrolet Silverado 1500

Ford F150

2016 U.S. Market Share by Model

Once again the Ford F150 is the best selling vehicle in America, with over 430k new vehicle registrations

New vehicle registrations

All Sales Categories

Through December 2016

© Experian [Public, Confidential, Internal, Restricted – choose the appropriate category]

U.S. Loyalty, Conquest and Defections

• Loyalty trends• Impact of demographics on repurchase loyalty• Loyalty by owned vehicle type• Brand leaders• Conquest to defection ratios

34 © Experian Public

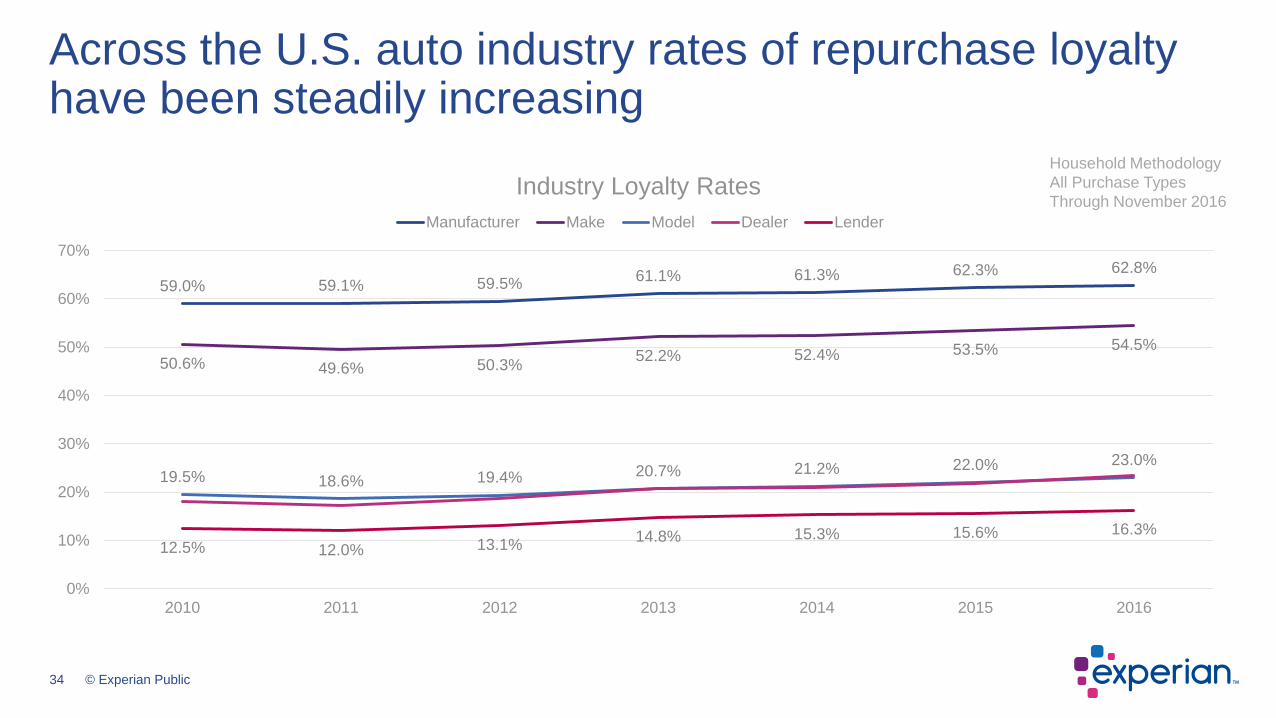

59.0% 59.1% 59.5%61.1% 61.3% 62.3% 62.8%

50.6% 49.6% 50.3%52.2% 52.4% 53.5% 54.5%

19.5% 18.6% 19.4% 20.7% 21.2% 22.0% 23.0%

12.5% 12.0% 13.1%14.8% 15.3% 15.6% 16.3%

0%

10%

20%

30%

40%

50%

60%

70%

2010 2011 2012 2013 2014 2015 2016

Industry Loyalty Rates

Manufacturer Make Model Dealer Lender

Across the U.S. auto industry rates of repurchase loyalty have been steadily increasing

Household Methodology

All Purchase Types

Through November 2016

35 © Experian Public

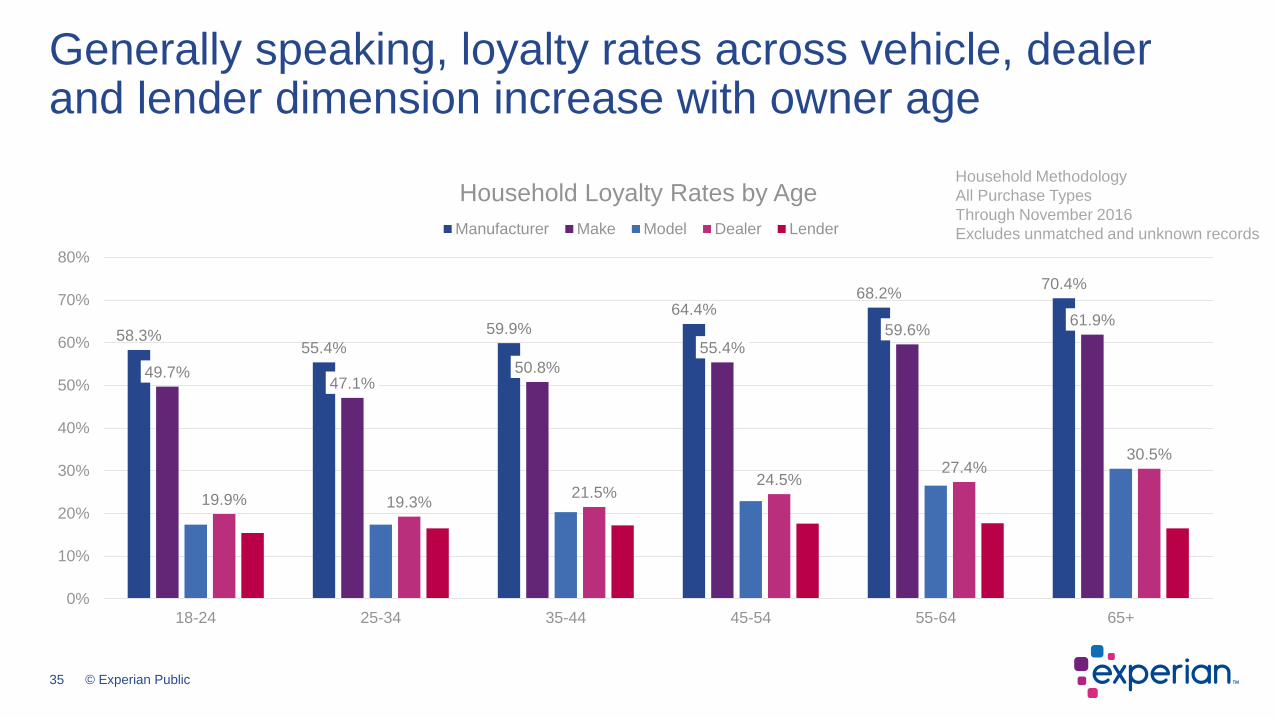

58.3%55.4%

59.9%

64.4%68.2%

70.4%

49.7%47.1%

50.8%

55.4%59.6%

61.9%

19.9% 19.3%21.5%

24.5%27.4%

30.5%

0%

10%

20%

30%

40%

50%

60%

70%

80%

18-24 25-34 35-44 45-54 55-64 65+

Household Loyalty Rates by Age

Manufacturer Make Model Dealer Lender

Generally speaking, loyalty rates across vehicle, dealer and lender dimension increase with owner age

Household Methodology

All Purchase Types

Through November 2016

Excludes unmatched and unknown records

36 © Experian Public

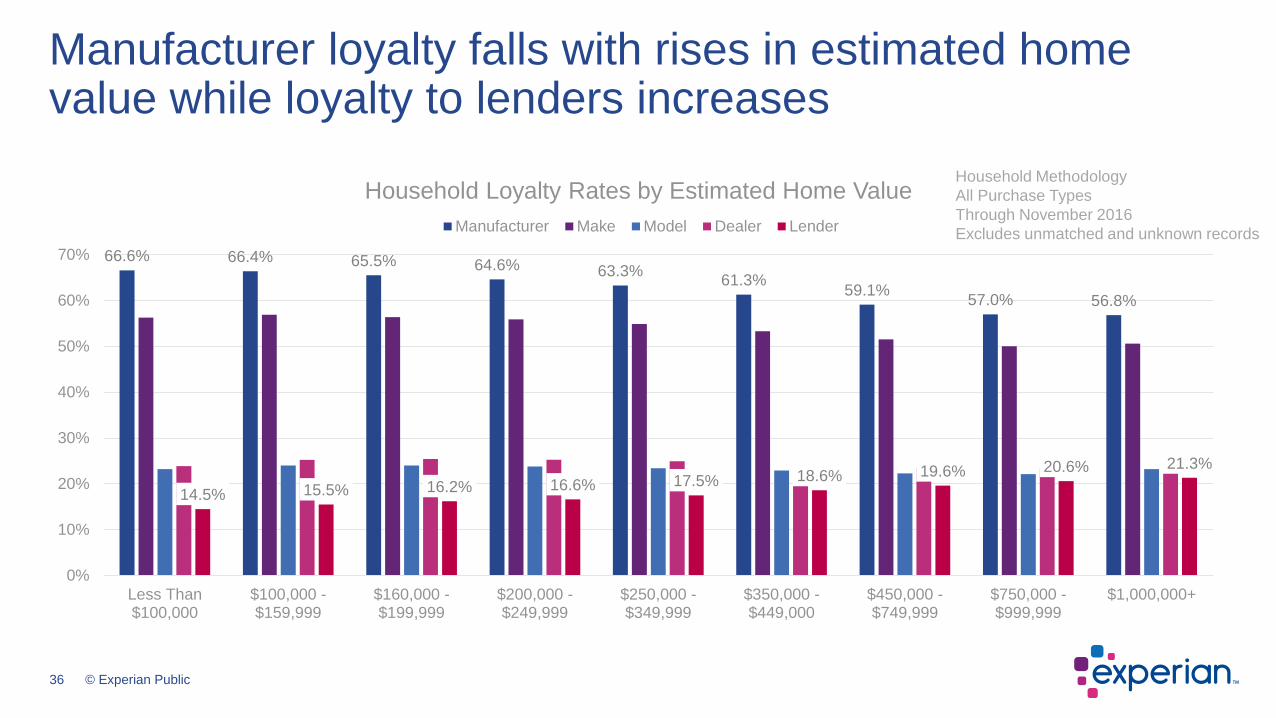

Manufacturer loyalty falls with rises in estimated home value while loyalty to lenders increases

66.6% 66.4% 65.5% 64.6% 63.3%61.3%

59.1%57.0% 56.8%

14.5% 15.5% 16.2% 16.6% 17.5% 18.6% 19.6% 20.6% 21.3%

0%

10%

20%

30%

40%

50%

60%

70%

Less Than$100,000

$100,000 -$159,999

$160,000 -$199,999

$200,000 -$249,999

$250,000 -$349,999

$350,000 -$449,000

$450,000 -$749,999

$750,000 -$999,999

$1,000,000+

Household Loyalty Rates by Estimated Home Value

Manufacturer Make Model Dealer Lender

Household Methodology

All Purchase Types

Through November 2016

Excludes unmatched and unknown records

37 © Experian Public

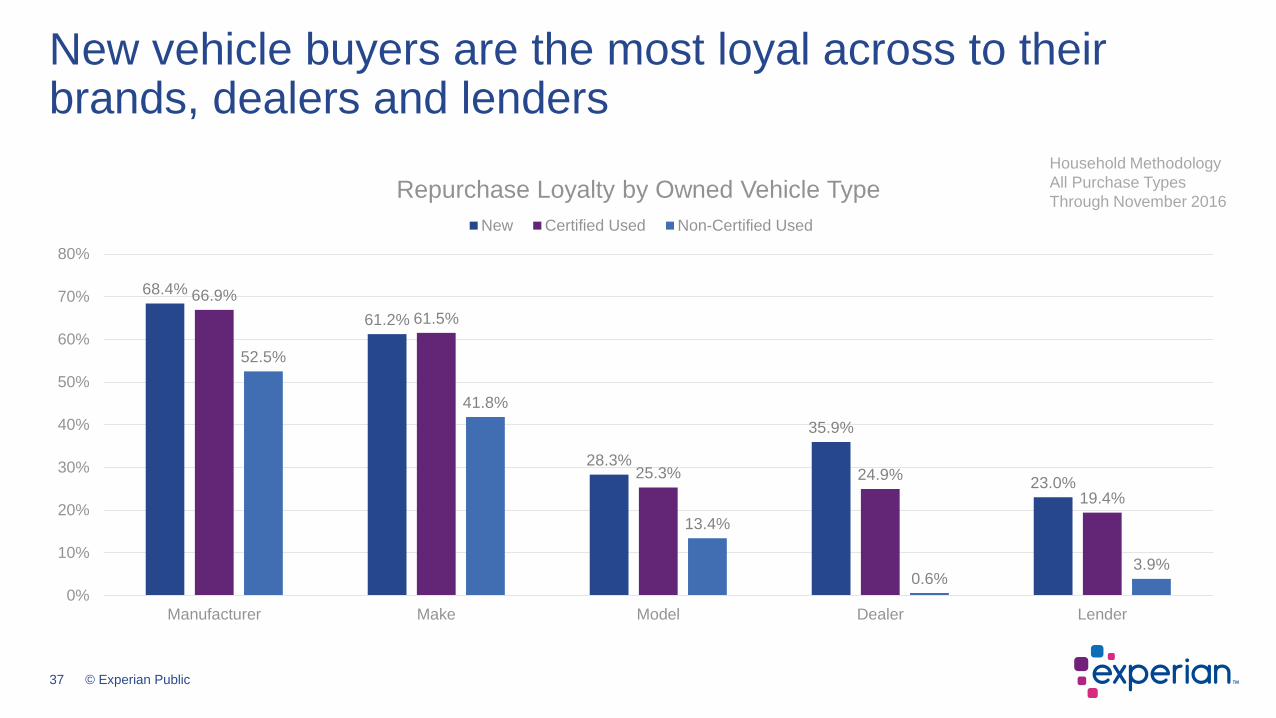

New vehicle buyers are the most loyal across to their brands, dealers and lenders

68.4%

61.2%

28.3%

35.9%

23.0%

66.9%

61.5%

25.3% 24.9%

19.4%

52.5%

41.8%

13.4%

0.6%3.9%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Manufacturer Make Model Dealer Lender

Repurchase Loyalty by Owned Vehicle Type

New Certified Used Non-Certified Used

Household Methodology

All Purchase Types

Through November 2016

38 © Experian Public

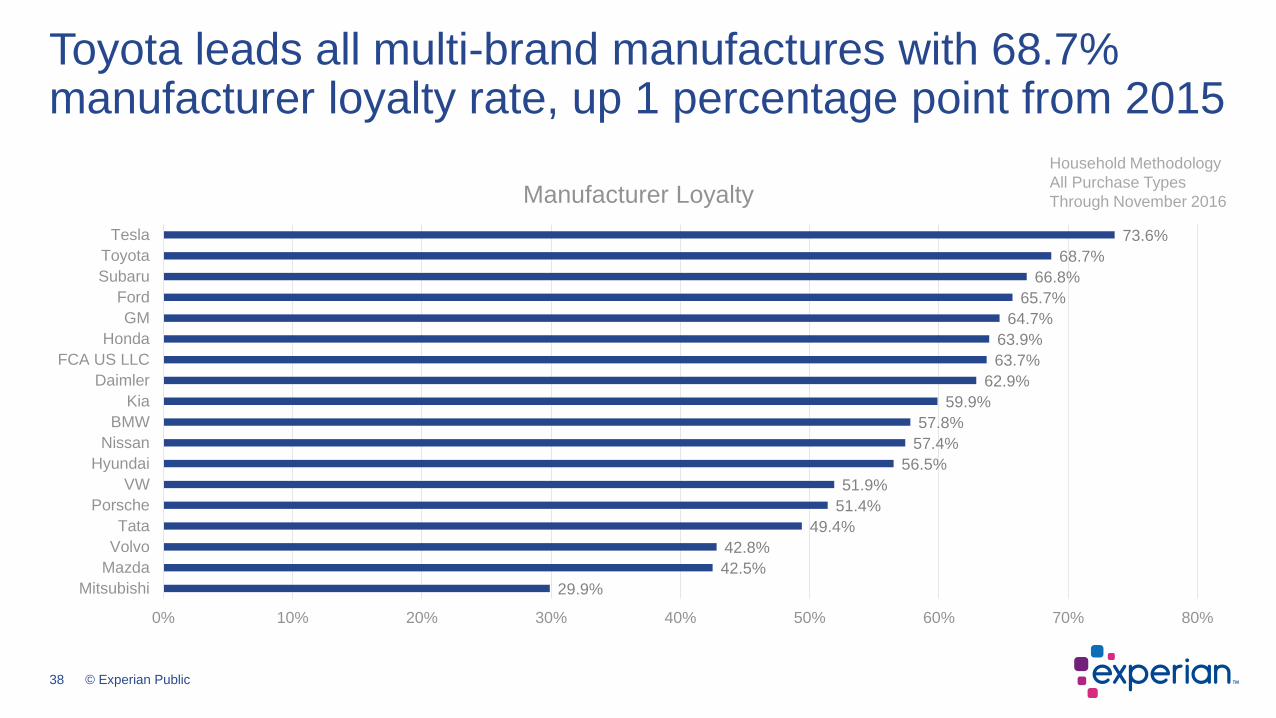

29.9%

42.5%

42.8%

49.4%

51.4%

51.9%

56.5%

57.4%

57.8%

59.9%

62.9%

63.7%

63.9%

64.7%

65.7%

66.8%

68.7%

73.6%

0% 10% 20% 30% 40% 50% 60% 70% 80%

Mitsubishi

Mazda

Volvo

Tata

Porsche

VW

Hyundai

Nissan

BMW

Kia

Daimler

FCA US LLC

Honda

GM

Ford

Subaru

Toyota

Tesla

Manufacturer Loyalty

Toyota leads all multi-brand manufactures with 68.7% manufacturer loyalty rate, up 1 percentage point from 2015

Household Methodology

All Purchase Types

Through November 2016

39 © Experian Public

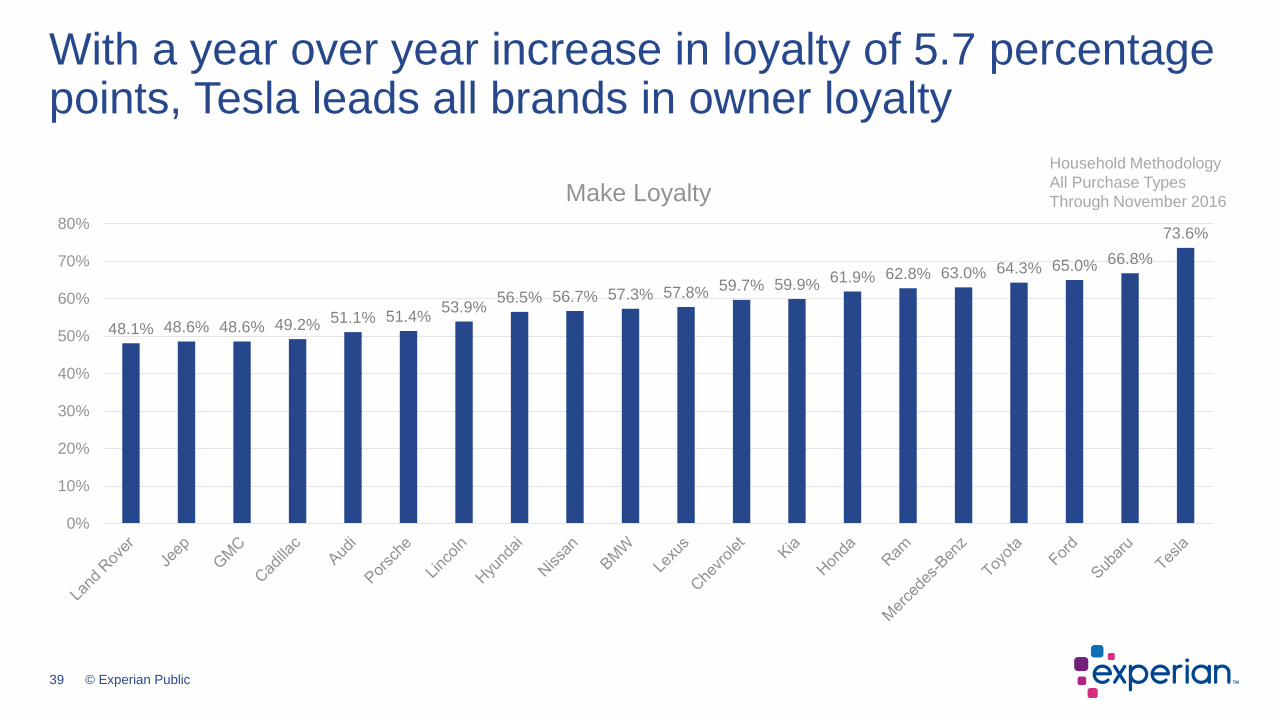

48.1% 48.6% 48.6% 49.2% 51.1% 51.4%53.9%

56.5% 56.7% 57.3% 57.8% 59.7% 59.9%61.9% 62.8% 63.0% 64.3% 65.0% 66.8%

73.6%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Make Loyalty

With a year over year increase in loyalty of 5.7 percentage points, Tesla leads all brands in owner loyalty

Household Methodology

All Purchase Types

Through November 2016

40 © Experian Public

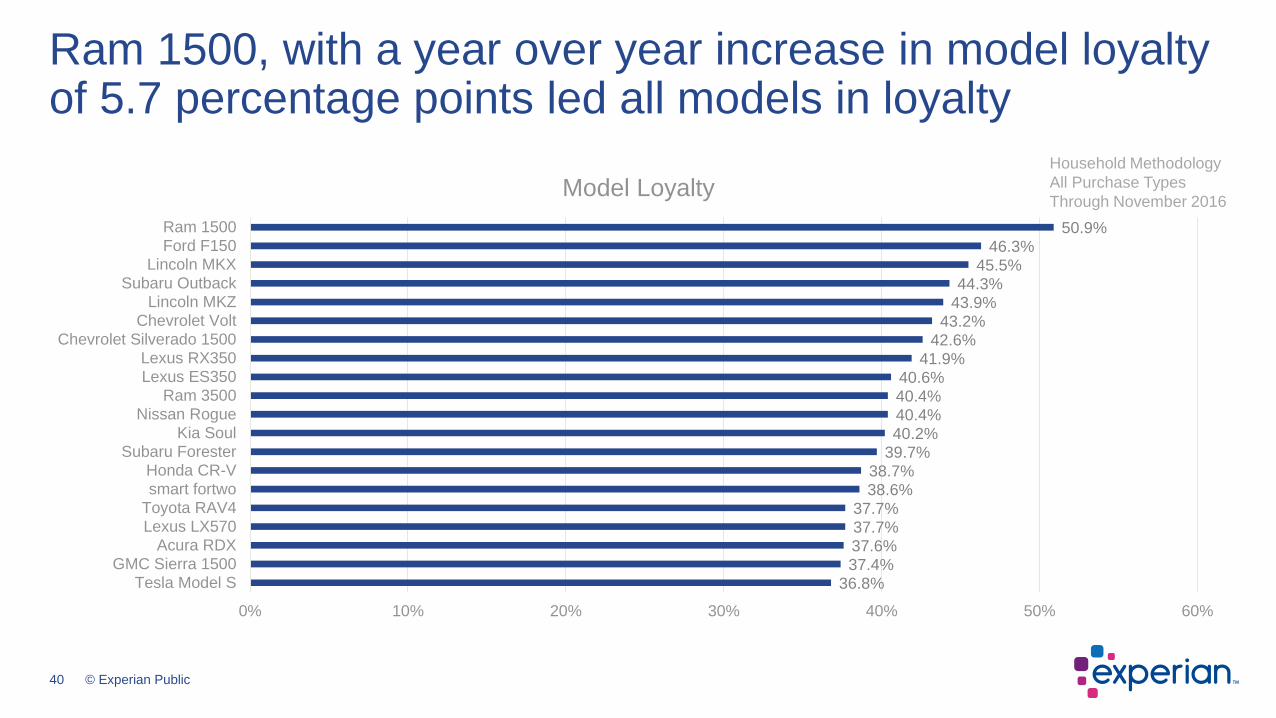

36.8%37.4%

37.6%37.7%37.7%

38.6%38.7%

39.7%40.2%

40.4%

40.4%40.6%

41.9%

42.6%

43.2%

43.9%44.3%

45.5%

46.3%50.9%

0% 10% 20% 30% 40% 50% 60%

Tesla Model S

GMC Sierra 1500

Acura RDX

Lexus LX570Toyota RAV4smart fortwo

Honda CR-VSubaru Forester

Kia Soul

Nissan RogueRam 3500

Lexus ES350Lexus RX350

Chevrolet Silverado 1500

Chevrolet Volt

Lincoln MKZSubaru Outback

Lincoln MKXFord F150

Ram 1500

Model Loyalty

Ram 1500, with a year over year increase in model loyalty of 5.7 percentage points led all models in loyalty

Household Methodology

All Purchase Types

Through November 2016

41 © Experian Public

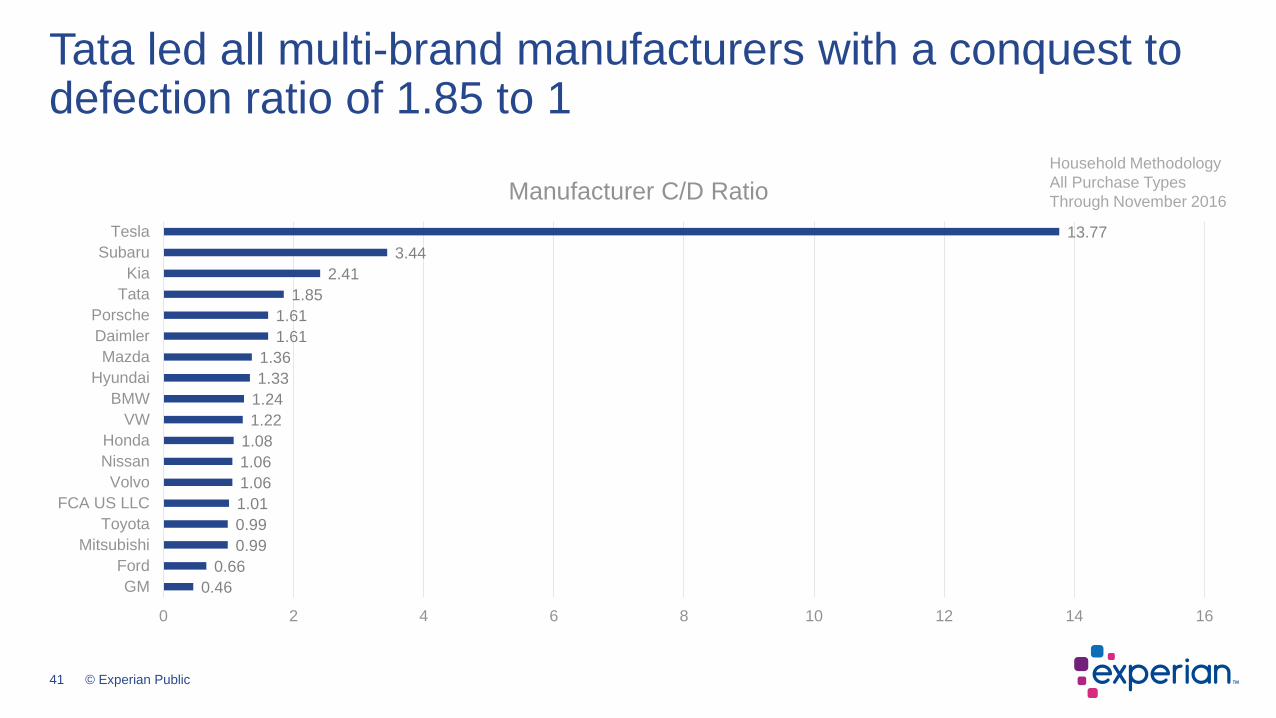

0.46

0.66

0.99

0.99

1.01

1.06

1.06

1.08

1.22

1.24

1.33

1.36

1.61

1.61

1.85

2.41

3.44

13.77

0 2 4 6 8 10 12 14 16

GM

Ford

Mitsubishi

Toyota

FCA US LLC

Volvo

Nissan

Honda

VW

BMW

Hyundai

Mazda

Daimler

Porsche

Tata

Kia

Subaru

Tesla

Manufacturer C/D Ratio

Tata led all multi-brand manufacturers with a conquest to defection ratio of 1.85 to 1

Household Methodology

All Purchase Types

Through November 2016

42 © Experian Public

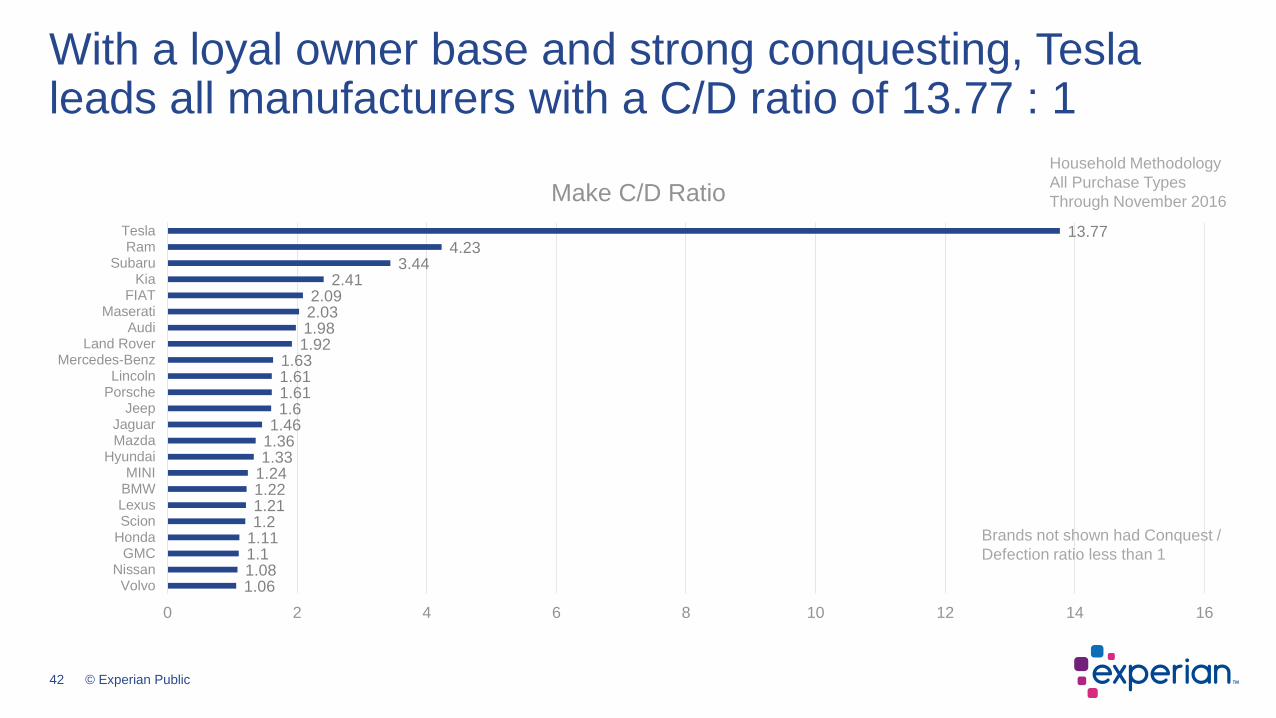

1.061.081.11.111.21.211.221.241.331.361.46

1.61.611.611.63

1.921.982.032.09

2.413.44

4.2313.77

0 2 4 6 8 10 12 14 16

VolvoNissan

GMCHondaScionLexusBMWMINI

HyundaiMazdaJaguar

JeepPorscheLincoln

Mercedes-BenzLand Rover

AudiMaserati

FIATKia

SubaruRam

Tesla

Make C/D Ratio

With a loyal owner base and strong conquesting, Tesla leads all manufacturers with a C/D ratio of 13.77 : 1

Household Methodology

All Purchase Types

Through November 2016

Brands not shown had Conquest /

Defection ratio less than 1

43 © Experian Public

• VIO volumes continue to increase even as the Aftermarket Sweet Spot declines to 85M vehicles

• 4 cylinder vehicles continue to dominate the market thanks to new technologies

• 2016 new vehicle registrations reached 17.3 million units

– Growth is slowing as 2016 totals were 1% greater than 2015

• Retail market was flat when compared to 2015

• Estimated home value is a strong predictor of exotic and luxury vehicle purchase activity

• General Motors led all manufactures with 16.9% share

• Toyota led all brands with 12.9% of the market

• Once again Ford F150 was the best selling vehicle in the U.S. market

• Repurchase loyalty rates continue to climb across vehicle, dealer and lender dimensions

Summary

44 © Experian Public

Today’s presentation

Follow us on Twitter

#EXPAuto

@Experian_Auto

Connect with us on LinkedIn

Experian Automotive

Presentation will be available 24-48 hours after Webinar

Email with a link will be sent to all registrants to download

Questions? Contact us at [email protected]

45 © Experian Public

Thank youExperian Automotive is prepared to meet your needs with an integrated solution statically designed to drive your business forward

©2017 Experian Information Solutions, Inc. All rights reserved. Experian and the Experian marks used herein are trademarks

or registered trademarks of Experian Information Solutions, Inc. Other product and company names mentioned herein are the

trademarks of their respective owners. No part of this copyrighted work may be reproduced, modified, or distributed in any

form or manner without the prior written permission of Experian.

Experian Public

Top Related