Languages

Pages

Legal

Evaluating Information Technology Investments

What systems to build?

Ken Peffers UNLV October 2004

Evaluation Timing

Ex Ante—before investments are committed

Ex Post—after committing resources

Actually evaluation can be made at any time.

During development

Before subsequent investments

Ex Ante Evaluation

Expected benefits/costs

Alignment with strategy

Feasibility

Risk

During Development

EvaluationAt the end of the feasibility study

At the end of the requirements analysis

When the prototype is developed

Six Roles for Evaluation in the Systems Life Cycle1

Ex AnteJustify funding for the project. Get the backing of decision makers by telling a credible story about value created by the project

During ImplementationConvince End users. Win over reluctant end users who weren’t included in the project justification. Adapt language to audience, e.g., not “enhance the firm’s competitive advantage,” but “get fewer irate customer calls.”

1Adapted from Keen, J.M. and B. Digrius, Making Technology Investments Profitable, John Wiley & Sons, 2003.

Six Roles for Evaluation in the Systems Life Cycle1

During Implementation Help control scope creep. Can be pointed to to help keep the project consistent with its originally approved objectives.Cheerleader. Can be pointed to when obstacles sap morale of the project team members. Keep team members motivated by pointing to their role in achieving value for the firm.Executive reminder. Helps keep the executive sponsor aware of the value of the project. Important when new executives come on board.

During operation.Track achieved value. Foundation for feedback loop for measuring value creation.

1Adapted from Keen, J.M. and B. Digrius, Making Technology Investments Profitable, John Wiley & Sons, 2003.

Ex Post Evaluation

Development success

Performance

Performance impacts

Benefits/costs

Profitability Methods of Evaluation

Payback

ROI

Discounted Cash Flow

Option Pricing

Payback

Payback (# of years) =

Investments/Average annual net benefit

Not justified by theory

Useful for small projects to demonstrate obvious value, i.e., very short payoff equivalent to high ROI

Return on Investment

Return on Investment =

Annual net benefit/Investment amount

Use not justified by theory

Convenient and easy to understand

May result in rejection of positive value projects

Problems with ROI

Short term projects with high ROI may be favored over longer term projects more important to the firm

ROI favors small investment, hence projects may be undercapitalized

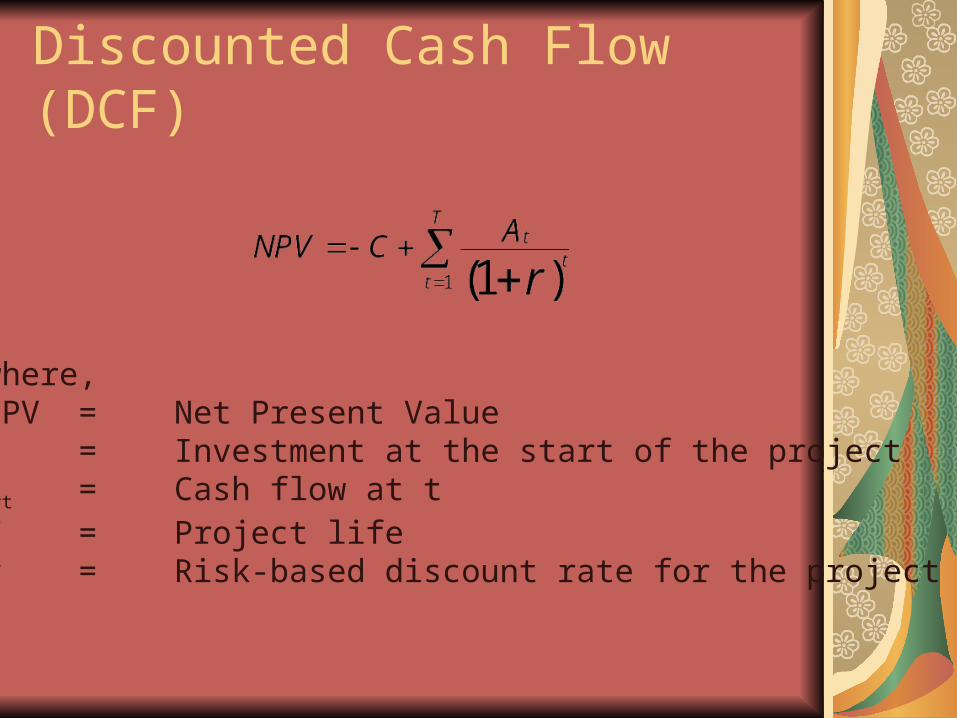

Discounted Cash Flow (DCF)

where,NPV = Net Present ValueC = Investment at the start of the projectAt = Cash flow at tT = Project lifer = Risk-based discount rate for the project

Value maximization

Managers objective to maximize firm value

Value of the firm equals discounted value of all future cash flows

Firm Value Maximization

where,PV = Present Market ValueAt = Cash flow at tT = Firm lifer = Industry required rate of return

DCF Example

One period

C = 10,000

A1 = 6,000

r = 10%

= -10,000 + 6,000/1.1 = -4545.4

Contribution of NPV

Objective

Congruence with value maximization

Better than undiscounted cash flow, simple payback, ROI

Limitations

Estimates of revenues and costsmanipulated to justify projects already selected

Clemens: work through the decisions

Estimations of project risk

Second stage projects

Value of Managerial Flexibility

DCF method assumes 2nd stage projects are undertaken

Actually won’t be undertaken if value less than 0 at time of investment decision

The Value of an Option

In making an initial investment in IT the manager is purchasing an option to make a subsequent investment later if the value of the second stage project is positive

Estimating the model

Necessary to estimate B1, C1, var B1, var C1, corr BCEstimating variation. Intuitively: “there is approximately a 2/3 probability that the revenues (costs) will vary up or down by no more than X%)”Estimating the corr BC. Intuitively: “approximately X% of the variation in revenues is attributable to variations in the development costs. The remainder is attributable to other factors. The corr BC is the squareroot of X.”

Evaluating IS Investments: Clemens

Rank alternativesFind bases of comparison

Difficult to compute NPV

Rational, analytical decisions without precise estimates of NPV

Sensitivity analysis

Decision trees

Balance forms of risk (feasibility)

Clemens, cont

Actively manage riskStrategic necessitiesExecutive championship

Role of critical resourcesIf system to create advantage, it must exploit key resources, capabilities. Think ‘barriers to imitation’Sustainable competitive advantage rare. Think cooperation

Be mindful of the downsideVanishing status quoOptions

Relationship between Strategic and Finance Methods

Since expected value of investment in properly valued assets is zero, positive NPV indicates strategic advantage

If NPV>0 there should be a strategic reason

If investment results in strategic advantage, NPV will be positive

Use of finance based measures not uniformly avowed

Robson: Finance measures lead to “short term evaluations on a quantitative basis that favor risk aversion and cost lowering activities with the financial year as their natural horizon and so are inevitably inappropriate for the high risk long-term projects...”

Why?

Risk aversiondiscount rate too high

Cost lowering activitiesstrategic benefits not fully valued

Long term projectsdiscount rate too high

On the other hand

Technologically enthusiastic managers may over-invest in IT

Just because something can be done doesn’t mean that it should be done.

Successful innovations, projects, and products can be worth less than they cost

The middle course

Use a variety of evaluation methods, both quantitative and qualitative

Use qualitative methods to arrive at good estimates of value for quantitative methods

The middle course

Avoid unrealistically high discount ratesunrealistically conservative valuation of strategic benefits

They can damage the firm by biasing investments toward short term gains and cost reduction and may result in underinvestment in long term, innovative technology.

Top Related