Languages

Pages

Legal

Enterprice-wide risk managementEnergy Risk Europe, 4th October 2006 London

2

The Statoil groupShort on history – long on achievements

Production (2004): 1.1 mmboepd

Reserves (2004):4.3 bn boe

24,000 employees Activity in 29 countries Operating 2.7 mmboepd

of NCS production Marketing 2/3 of

NCS gas volumes World’s 3rd largest

crude oil seller0 10 20 30 40

Norsk Hydro

Repsol YPF

ConocoPhillips

BG

Eni

Shell

BP

Statoil

Total

ChevronTexaco

ExxonMobil

Competitive returns1)

Return on Average Capital Employed 2004

1 Source: Lehman Brothers Oil and Gas Quarterly Scoresheet (10 February 2005), rolling 12-month ROACE.

Designing an effective enterprise-wide risk management framework

4

Enterprise-wide Risk ManagementCorporate Risk Management (blue font)

Short term Long term

Tactical risk Market (prices)

Credit risk

Operational risk

Strategic risk

Market (prices) Country Tax Reputation

Accidents Catastrophe Environment

Reservoir Project HSE Administrative

Insurable risk via Captive

5

Corporate Risk Committee Corporate Risk Committee (CRC) at group level

(advisory role / responsible for):

Strategic market risk policyo corporate hedging policy and strategieso strategic market views

Insurance policies Insurable risks Credit risk Trading methodologies issues Risk reporting Risk assessments of large projects

with difficult business risks Portfolio risk assessments

Participants: CFO (head of CRC) Head of Country Risk and Social Responsibility Head of Refining & Marketing Head of Oil Trading and Supply Head of Financial Services

E&P Norway International E&P Strategy and Control Natural Gas Finance & Control Natural Gas Long Term Market Corporate Risk Management

Information to CRC / training

CRC decision vehicleCRC advicery role

6

CRC cases (overview 2003-2005)

• Cove Point - overview / mandates• Cove Point expansion• Credit Default Swaps• Energiverk Mongstad• Insurance markets after GoM events• Overview of new country risk reporting • Hedge strategies - part I & II• Main features in Statoil’s risk management• Correlations between Brent and ref. margin &

NOK/USD & STL• Country risk status portfolio• Country risk overview: Libya• Country risk - Status pilot phase• Country risk overview: Algeria• Development country risk• Natural Gas Long Term contracts risks• NG Clearing: purpose and organization• NG trading mandates• NG weather derivatives - gen. disc. about use• NG: risk i gas portfolio and sub optimization• Oil vs gas indexation• Oil price hedging - status prices• Oil price hedging 2004

• PMT project - Tjeldbergodden• Risk capital/-appetite• Risk report October 05• Risk management report corporate tactical• Risk assessment / Enterprise wide Risk

Management• Risk report status• Connection between results and risk capital in

trading• Snorre-incident – economical consequences and

insurance• Statoil’s credit exposure• Statoil’s reputation• Status hedge 2005• Status crude oil market• Status tax risk• Bad scenarios – gap • Bad scenarios – going forward• Bad scenarios part I• Bad scenarios part II• Tactical reporting• Currency risk• Variable premium puts

7

Strategic risk management policySummary

Statoil’s corporate risk management defines crude oil price, natural gas price and production of crude oil and natural gas as the corporate’s core risks.

Main goals in the corporate’s risk management policy:

contribute in ensuring Statoil’s long term strategic development and reaching targets through protecting financial flexibility, i.e. avoiding different categories of financial distress, downrating and protecting cash flow, making the corporate able to

start and accomplish profitable projects/acquisitions andavoiding forced divestments

even in periods with bad market conditions.

Dynamic measurement of risk.

9

Some challenges for the energy sector?

In a bank a currency trader knows that when he has bought some foreign currency, he has a position !

When is an oil trader getting a position? All future potential positions? All proven reserves? All ”lifted” production? All sold cargoes?

When is the mark to market zero? When the oil is sold a fixed price? When the oil is sold a the floating market price?

Is it possible to use the same principles for oil, oil products, gas, lng, electrisity, coal???

10

11

Risk comprises both the upside and downside outcomes

Negative impact

Positive impact

Large

Probability0

Large

Oil price

Natural gas price Project

Credit

Country

Catasthropicevents

Currencies

Op. damages / accidents

Production

Pot

. re

puta

tion

eff

ect

12

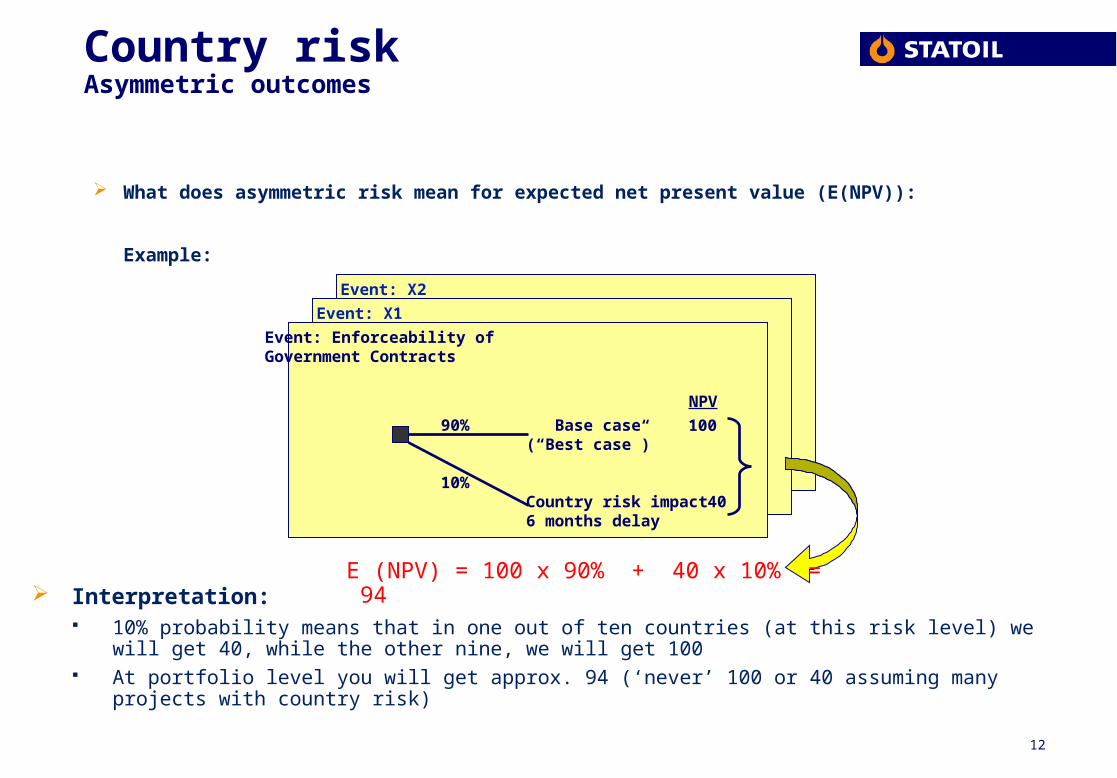

Country riskAsymmetric outcomes

What does asymmetric risk mean for expected net present value (E(NPV)):

Example:

Interpretation: 10% probability means that in one out of ten countries (at this risk level) we will get 40, while the other nine, we

will get 100 At portfolio level you will get approx. 94 (‘never’ 100 or 40 assuming many projects with country risk)

90%

10%

Event: Enforceability of Government Contracts

Base case(“Best case”)

Country risk impact6 months delay

NPV

100

40

E (NPV) = 100 x 90% + 40 x 10% = 94

Event: X1

Event: X2

13

Tax Asymmetry versus tax levelIllustrative

Tax asymmetry

NegativePositive

Low

High

Tax level

NCS

PSC

UK

Buy-

backs

GoM

Neutral”Low upside,

high downside”

”High upside,

low downside”

14

Risk and reward our different businesses

0 %

5 %

10 %

15 %

20 %

25 %

Basis oil NCSBasis nat. gas NCSTransportnet/processplants NCSUpstream oil internat.RetailRefiningPetrochemical

Moderate risk

Reward

Moderate to high riskLow risk

15

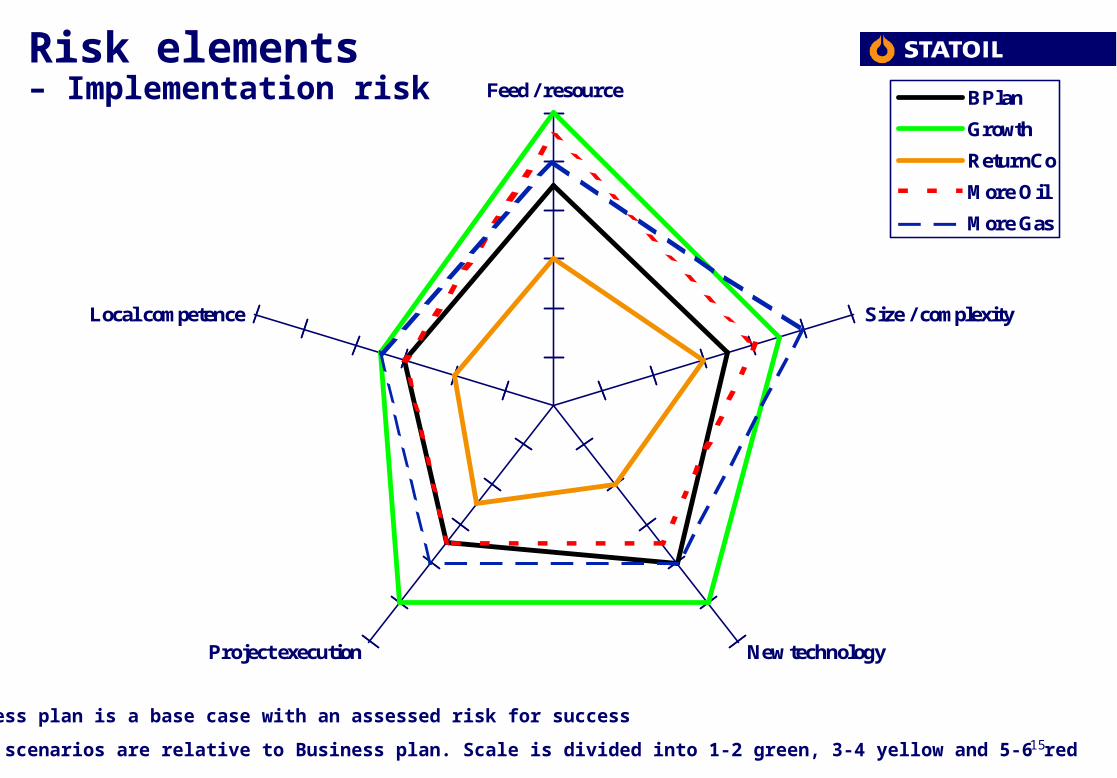

Risk elements – Implementation risk Feed / resource

Size / complexity

New technologyProject execution

Local competence

BPlan

Growth

ReturnCo

More Oil

More Gas

Business plan is a base case with an assessed risk for success

Other scenarios are relative to Business plan. Scale is divided into 1-2 green, 3-4 yellow and 5-6 red

Monitoring, controlling and reviewing your risk management framework.

17

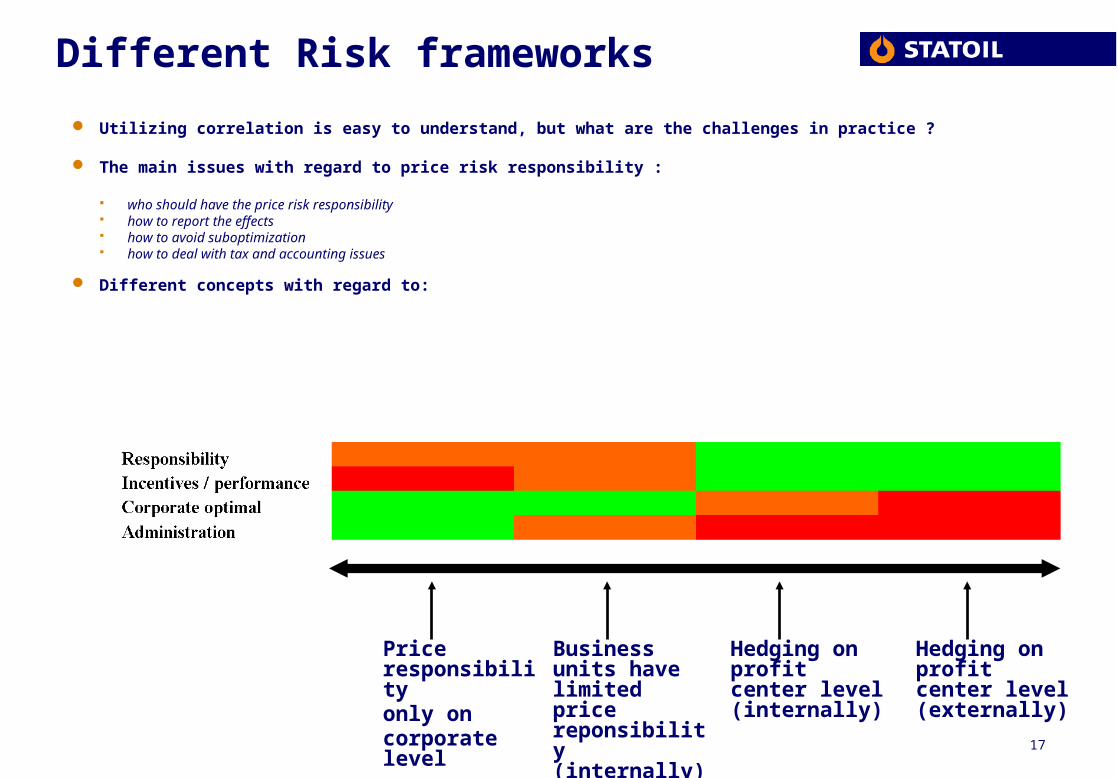

Different Risk frameworks

Utilizing correlation is easy to understand, but what are the challenges in practice ?

The main issues with regard to price risk responsibility :

who should have the price risk responsibility how to report the effects how to avoid suboptimization how to deal with tax and accounting issues

Different concepts with regard to:

Hedging on profit center level (internally)

Price responsibilityonly oncorporate level

Hedging on profit center level (externally)

Business units have limited price reponsibility (internally)

18

Reviewing VAR

Decide on a probabilty of loss Decide on a frequency Very low probability high frequency events give more comfort (99.9% daily var)

But….how do you test this? On average you’re going to exceed your VAR once every 1000 days (or four years)

Higher probability lower frequency events give better testability (75% weekly var) But….you lose more than your VAR every one week out of four How do you know what you could lose in extreme movements

However VAR is calculated, the methodology must have the following characteristics It should be reproducable It should be runnable on aggregate portfolios and should aggregate risk It should make sense for simple portfolios (I.e. if a swap has a VAR of X, twice the

position should give double the VAR) It should be “non-linear”. Options aren’t a “free risk strategy”. It should be timely.

19

Checking VAR

Data data data data data You must retain data on actual historical outcomes for books, portfolios, etc

Historical daily PnL numbers for last night’s positions (this is critical) Historical daily PnL numbers for each book including day trades (which you already

do…) Historical daily VAR numbers at a variety of probability levels (75%,90%,95%,99%?) This should be done at each level of aggregation

Once you have accumulated enough data (3 months?,6 months?) back test and mine the data. If your VAR methodology is correct, then the distribution of actual PnL for last night’s trades should match the distribution that your VAR implies. For example, one day in four, last night’s positions should lose more than your 75% VAR,

one day in 10, last night’s positions should lose more than your 90% VAR. The volatility of your total daily PnL is a more traditional risk return measure: the

sharpe ratio.

20

Presentation of ”the risk picture” for top management.

Executive board Monthly Annually

21

Section I: Tactical Risk

Low to medium risk in tactical trading.

The main market risk is in physical oil and plain paper instruments like futures, swaps and forwards, only minor risk in options, and we see that risk is focused on products like Brent, WTI, Fuel oil, gasoline and naphta.

VaR per instrument typeBase & Proprietary

Physical Futures Forwards Swaps Options

Base Propr.

VaR per physical productBase & Proprietary

Brent WTI ME crd Gasoline Distillates Fuel oils Naphtha LPG

Base Spec

VaR figures (95% - 1 day)

ChangeO&S Mandate VaR last month

Base 22,00 -1,76Proprietary 4,00 -0,43

Base + Proprietary 50 20,00 -2,01

Long Term DebtBase 20 13,00 -0,06Proprietary 5 2,00 0,08

Base + Proprietary 25 14,50 0,03

NGUK 2 1,50 0,20US 2 1,50 0,20

Aggregate VaRBase - 28,00 -2,20Base & Proprietary - 29,00 -2,30

O&S Base and Prop Trading

9-11 Scenario Stress Test Results vs. VAR @95%

-50-47-44-41-38-35-32-29-26-23-20-17-14-11

-8-5-214

02.ju

n.0

4

08.ju

n.0

4

21.ju

n.0

4

09.ju

l.04

21.ju

l.04

30.ju

l.04

25.a

ug

.04

06.s

ep.0

4

09.s

ep.0

4

14.s

ep.0

4

17.s

ep.0

4

22.s

ep.0

4

27.s

ep.0

4

30.s

ep.0

4

05.o

kt.0

4

08.o

kt.0

4

13.o

kt.0

4

18.o

kt.0

4

21.o

kt.0

4

26.o

kt.0

4

29.o

kt.0

4

05.n

ov.

04

10.n

ov.

04

17.n

ov.

04

22.n

ov.

04

25.n

ov.

04

30.n

ov.

04

mU

SD

9-11 stress test PERCENTVAR @95%, 1day

O&S Total Portfolio 9-11 Scenario Stress Test Results vs. VAR @95%

-30

-20

-10

0

10

20

30

03.01.05 31.01.05 28.02.05 28.03.05 25.04.05

mUSD

9-11 stress testPERCENTVAR @95%, 1day

22

Section II: Strategic Risk

The Kernel distribution is based on market forward prices and historical volatilities and correlations.

Brent forwards at historical very high level. Option prices at low level due to high forward level combined with moderate volatility in the market

Brent forward curves

25

30

35

40

45

50

2006 2007 2008 2009 2010

25 Feb 05

28 Jan 05

15 Des 04

USD/bbl

Hedge Status

Instrument Period Strike Hedged% of production

after taxUSD/bbl (mill bbls)

Put option Brent X Y Z %Put option Brent X Y Z %Put option Brent X Y Z %

Brent put options 2006(quarterly settled)

0,00

0,20

0,40

0,60

0,80

20.9.04 20.10.04 20.11.04 20.12.04 20.1.05 20.2.05

$ 24

$ 22

$ 20

USD/bbl

23

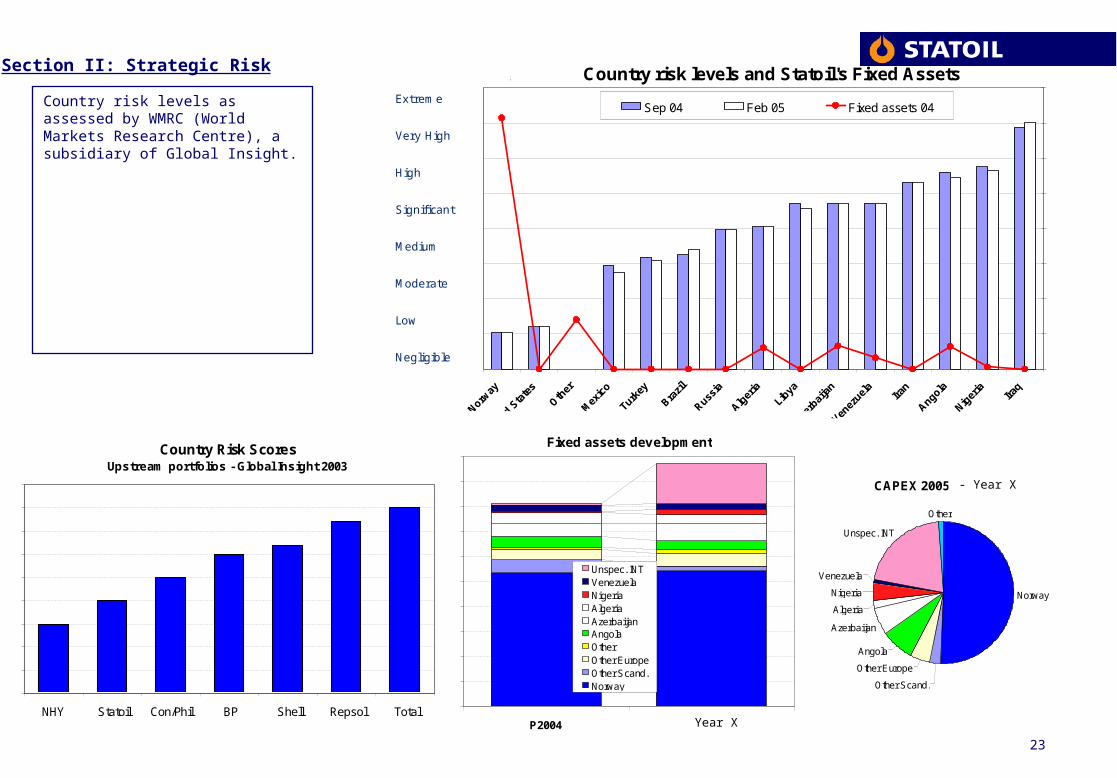

Section II: Strategic Risk

Country risk levels as assessed by WMRC (World Markets Research Centre), a subsidiary of Global Insight.

Extreme

Very High

High

Significant

Medium

Moderate

Low

Negligible

Country Risk ScoresUpstream portfolios - Global Insight 2003

NHY Statoil Con/Phil BP Shell Repsol Total

Country risk levels and Statoil's Fixed Assets

Sep 04 Feb 05 Fixed assets 04

Fixed Assets

RiskScores

Fixed assets development

P2004 2 009

Unspec. INTVenezuelaNigeriaAlgeriaAzerbaijanAngolaOtherOther EuropeOther Scand.Norway

CAPEX 2005 - 2009

Norway

Other Scand.

Other Europe

Angola

Azerbaijan

Algeria

Nigeria

Venezuela

Unspec. INT

Other

Year X

- Year X

24

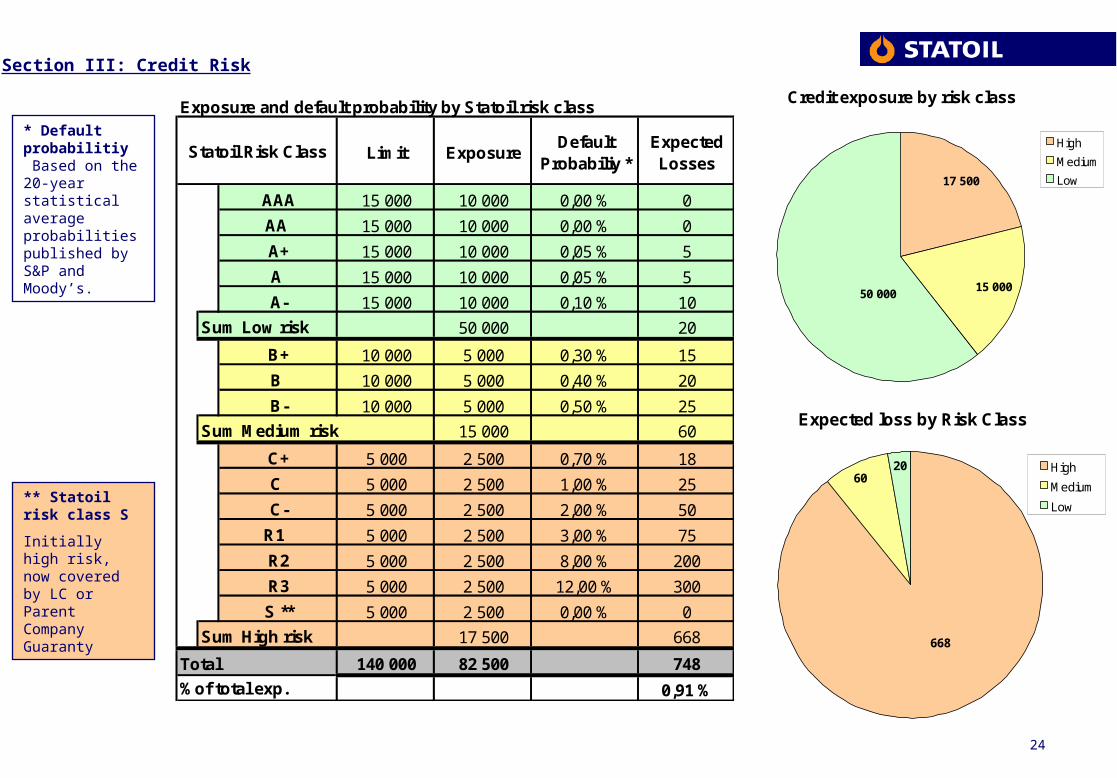

Section III: Credit Risk

* Default probabilitiy Based on the 20-year statistical average probabilities published by S&P and Moody’s.

** Statoil risk class S

Initially high risk, now covered by LC or Parent Company Guaranty

Exposure and default probability by Statoil risk class

Limit ExposureDefault

Probabiliy *Expected Losses

AAA 15 000 10 000 0,00 % 0

AA 15 000 10 000 0,00 % 0

A+ 15 000 10 000 0,05 % 5

A 15 000 10 000 0,05 % 5

A- 15 000 10 000 0,10 % 10

Sum Low risk 50 000 20

B+ 10 000 5 000 0,30 % 15

B 10 000 5 000 0,40 % 20

B- 10 000 5 000 0,50 % 25

Sum Medium risk 15 000 60

C+ 5 000 2 500 0,70 % 18

C 5 000 2 500 1,00 % 25

C- 5 000 2 500 2,00 % 50

R1 5 000 2 500 3,00 % 75

R2 5 000 2 500 8,00 % 200

R3 5 000 2 500 12,00 % 300

S ** 5 000 2 500 0,00 % 0

Sum High risk 17 500 668

Total 140 000 82 500 748

%of total exp. 0,91 %

Statoil Risk Class

Credit exposure by risk class

50 000

17 500

15 000

High

Medium

Low

Total exposure: 82500

Expected loss by Risk Class

2060

668

High

Medium

Low

Total expected losses: 748

25

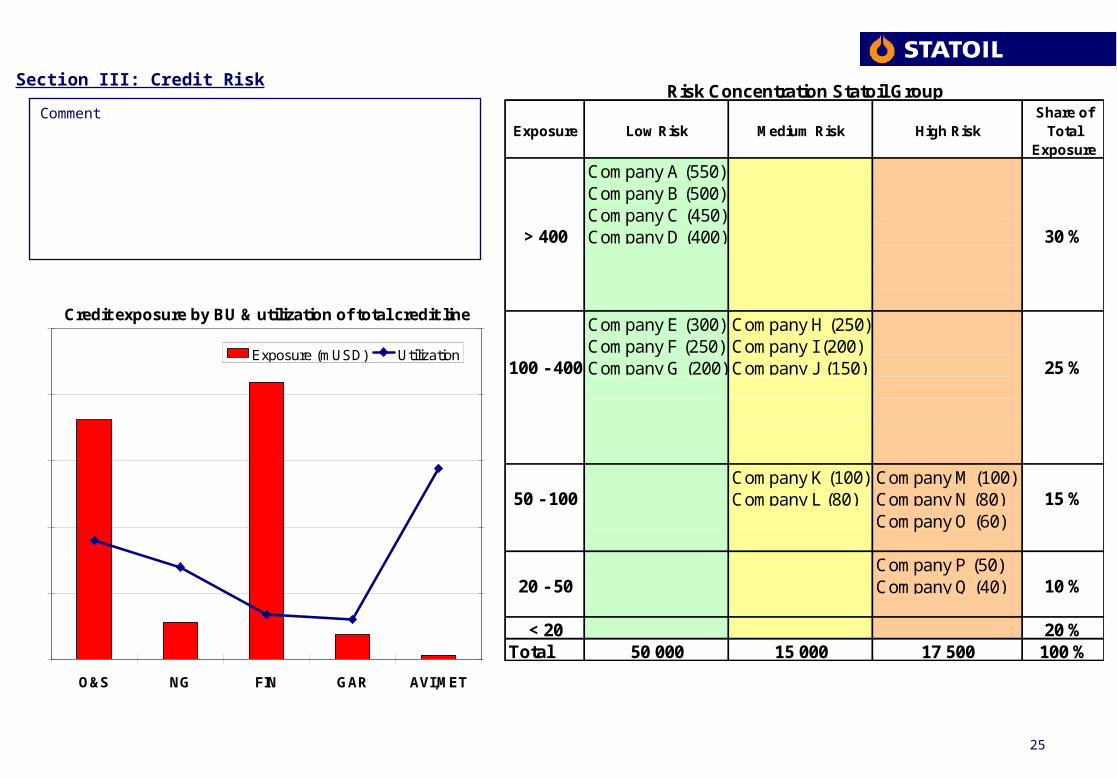

Section III: Credit Risk

Comment

Credit exposure by BU & utilization of total credit line

O&S NG FIN GAR AVI,MET

Exposure (mUSD) Utilization

Exposure Low Risk Medium Risk High Risk Share of

Total Exposure

Company A (550)Company B (500)Company C (450)

> 400 Company D (400) 30 %

Company E (300) Company H (250)Company F (250) Company I (200)

100 - 400 Company G (200) Company J (150) 25 %

Company K (100) Company M (100)50 - 100 Company L (80) Company N (80) 15 %

Company O (60)

Company P (50)20 - 50 Company Q (40) 10 %

< 20 20 %Total 50 000 15 000 17 500 100 %

Risk Concentration Statoil Group

26

Section IV: Insurance

Comment

Comment

Capital structure and exposure

Currentcapital

Oneplatform

Post oneevent

A secondplatform

Post twoevents

Risk Capital

Equity

Overall risk distribution Statoil insured assets

Statoil ASA selfinsurance

STAFOR

OIL / sEnergy

Market

External market inkl.

Lloyds/London, USA &

Europe

Q/S

STAFOR

Mutuals &

STAFOR

STAFOR

Statoil self insurance

STAFOR insurance structure

Insurance by asset

Market

OIL/ sEnergy

Stafor

Statoil ASA self insurance

Top Related