Languages

Pages

Legal

Emerging Issues in Government Accounting & AuditingRutgers UniversityNovember 30, 2017

1

Today’s Agenda• State Fiscal Outlook• Legislative and Regulatory Issues• Uniform Guidance Implementation• Accounting and Auditing Issues• Other Emerging Issues

2

State Fiscal OutlookCloudy with a Chance of Storms….

3

NATIONAL OVERVIEW

GDP growth: 1.6% in 2016 compared to 2.6% in 2015 (lowest since 2011)2.4% so far in 2017 (3.1% in second quarter; 3% in third quarter)

Recession: WSJ panel of economists 16% probability of recession in next 12 months (Oct. 2017); down from 20% a year earlier

Unemployment:4.1% in October 2017 (a 16-year low)Household income:2016 – median $59,039, up 3.2%; 2015 up 5.2%

Jobs:October 2017 – 261,000 (the 85th straight month of positive job creation)2016 – 180,0002015 – 230,000

Interest rates:Fed Reserve raised rates .25% in June 2017. Fourth increase since the Great Recession. 95% of economists expect rate increase in Dec. 2017.

Stock Market:2016 – DJIA up 15%“Trump Bump” – S&P 500 up 6% from election day to inauguration day2017 – now over 23,000!

Source: Wall Street Journal

4

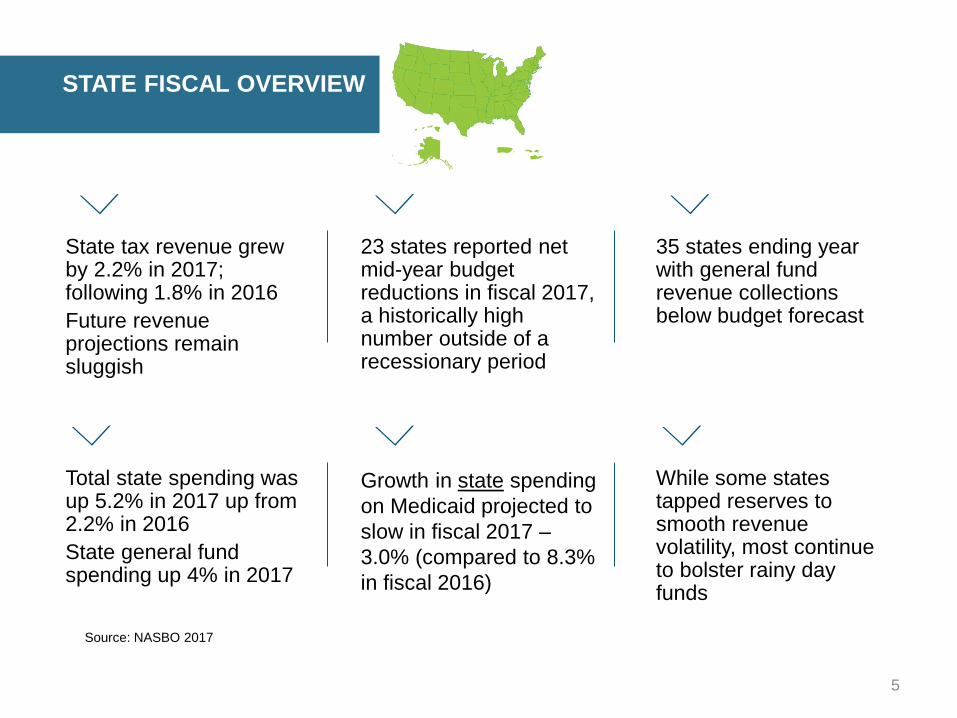

STATE FISCAL OVERVIEW

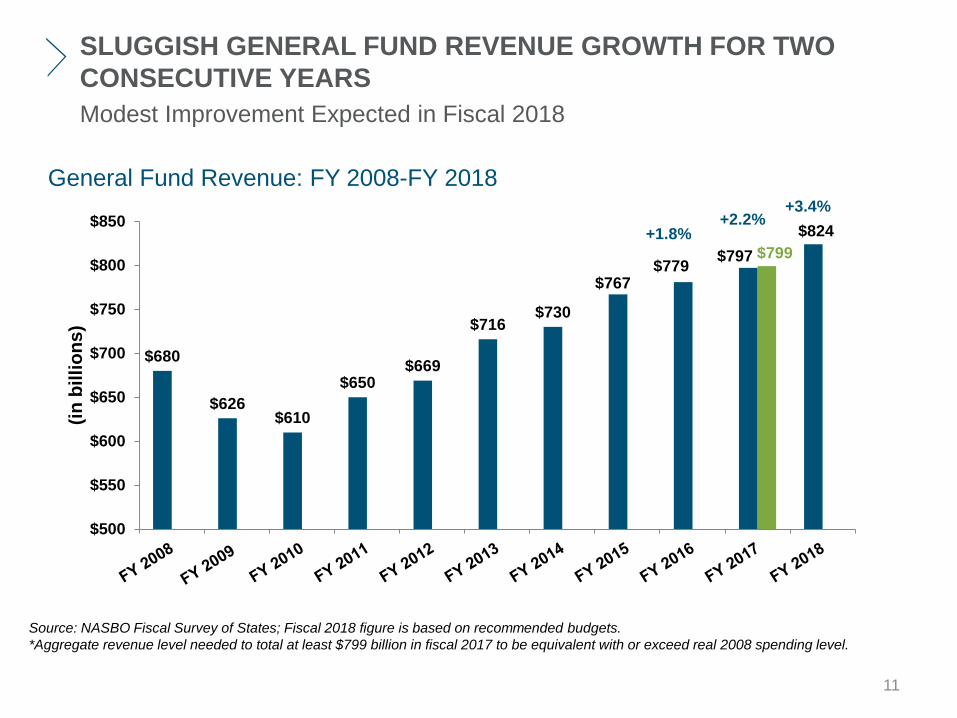

State tax revenue grew by 2.2% in 2017; following 1.8% in 2016Future revenue projections remain sluggish

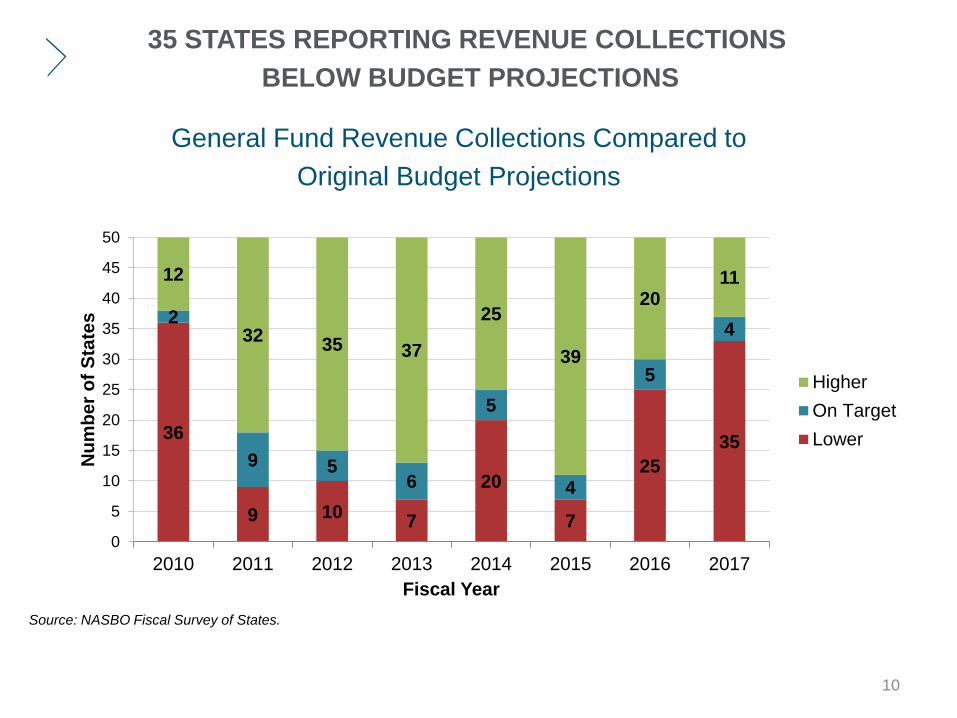

35 states ending year with general fund revenue collections below budget forecast

Total state spending was up 5.2% in 2017 up from 2.2% in 2016State general fund spending up 4% in 2017

Growth in state spending on Medicaid projected to slow in fiscal 2017 –3.0% (compared to 8.3% in fiscal 2016)

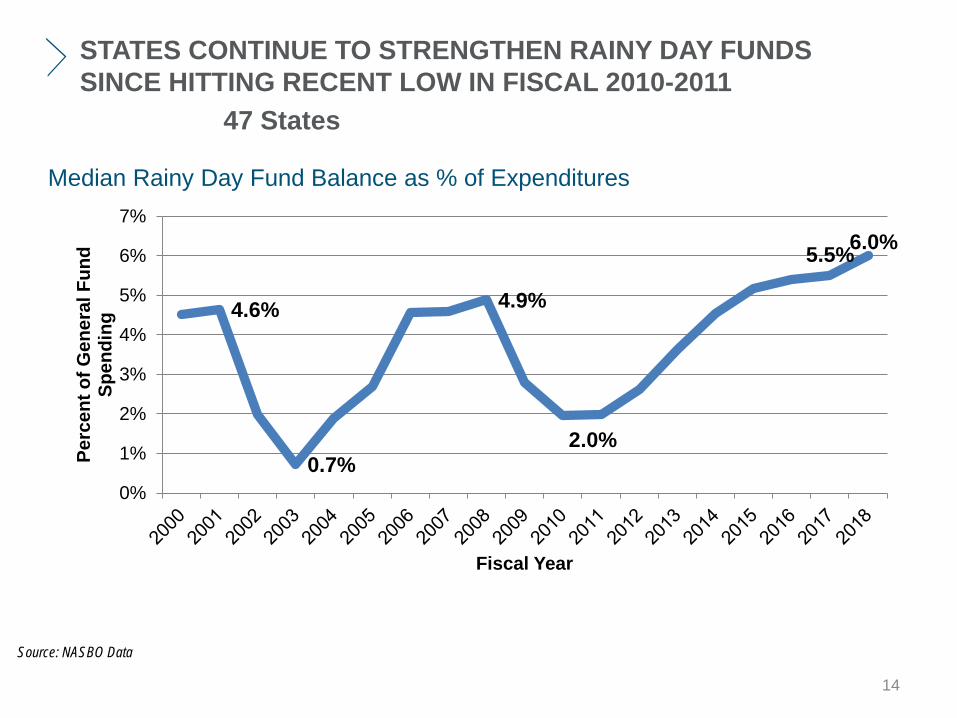

While some states tapped reserves to smooth revenue volatility, most continue to bolster rainy day funds

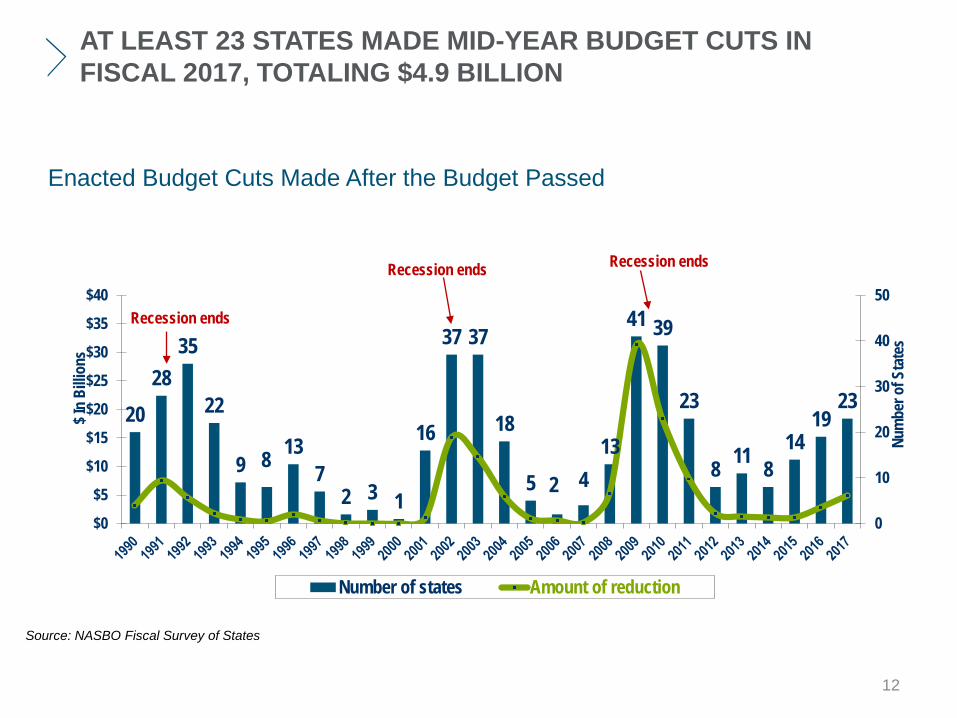

23 states reported net mid-year budget reductions in fiscal 2017, a historically high number outside of a recessionary period

Source: NASBO 2017

5

GENERAL FUND SPENDING

6

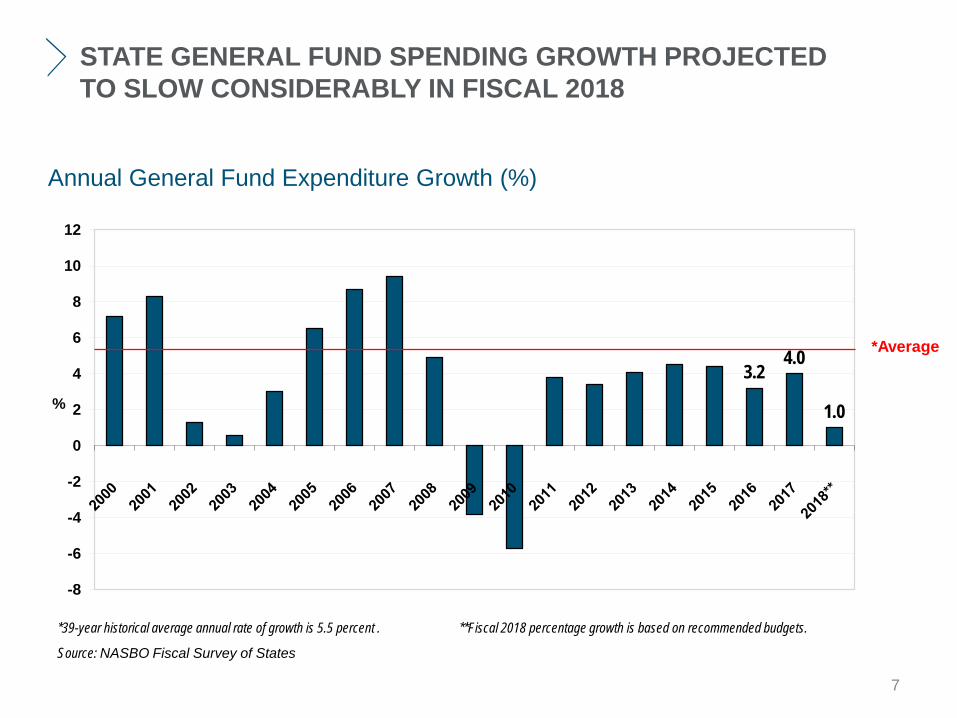

STATE GENERAL FUND SPENDING GROWTH PROJECTED TO SLOW CONSIDERABLY IN FISCAL 2018

Annual General Fund Expenditure Growth (%)

3.24.0

1.0

-8

-6

-4

-2

0

2

4

6

8

10

12

%

*Average

*39-year historical average annual rate of growth is 5.5 percent . **Fiscal 2018 percentage growth is based on recommended budgets.

Source: NASBO Fiscal Survey of States

7

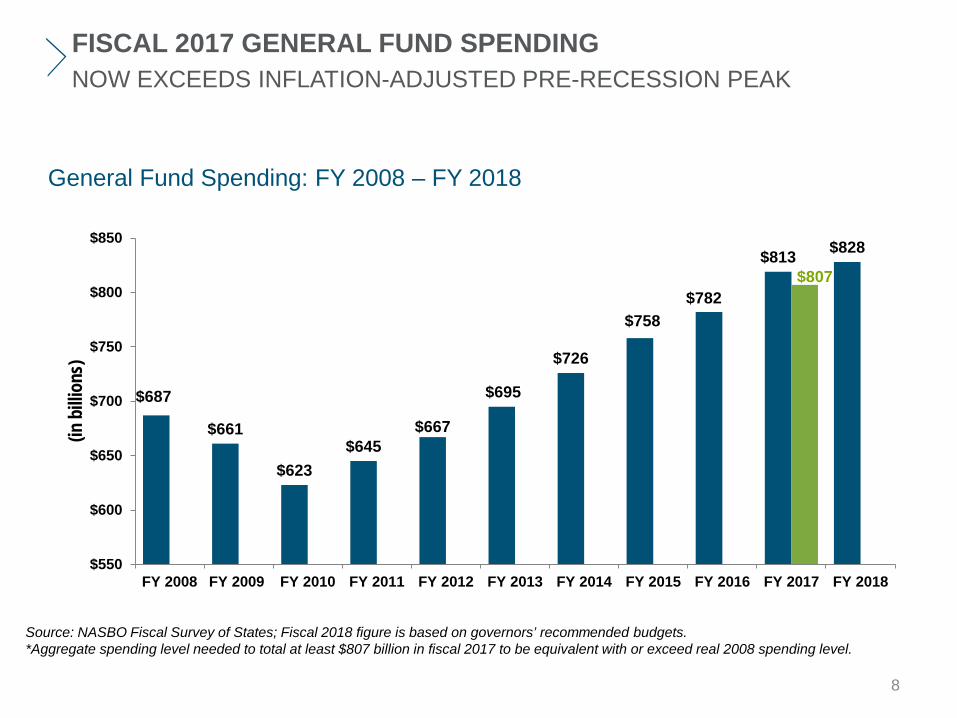

FISCAL 2017 GENERAL FUND SPENDING NOW EXCEEDS INFLATION-ADJUSTED PRE-RECESSION PEAK

General Fund Spending: FY 2008 – FY 2018

$687

$661

$623$645

$667

$695

$726

$758$782

$813 $828

$807

$550

$600

$650

$700

$750

$800

$850

FY 2008 FY 2009 FY 2010 FY 2011 FY 2012 FY 2013 FY 2014 FY 2015 FY 2016 FY 2017 FY 2018

(in b

illion

s)

Source: NASBO Fiscal Survey of States; Fiscal 2018 figure is based on governors’ recommended budgets.*Aggregate spending level needed to total at least $807 billion in fiscal 2017 to be equivalent with or exceed real 2008 spending level.

8

GENERAL FUND REVENUE

9

35 STATES REPORTING REVENUE COLLECTIONSBELOW BUDGET PROJECTIONS

General Fund Revenue Collections Compared to Original Budget Projections

36

9 10 7

20

7

2535

2

9 56

5

4

5

4

12

32 35 37

25

39

2011

0

5

10

15

20

25

30

35

40

45

50

2010 2011 2012 2013 2014 2015 2016 2017

Num

ber o

f Sta

tes

Fiscal Year

HigherOn TargetLower

Source: NASBO Fiscal Survey of States.

10

SLUGGISH GENERAL FUND REVENUE GROWTH FOR TWO CONSECUTIVE YEARSModest Improvement Expected in Fiscal 2018

General Fund Revenue: FY 2008-FY 2018

$680

$626$610

$650$669

$716$730

$767$779 $797

$824$799

$500

$550

$600

$650

$700

$750

$800

$850

(in b

illio

ns)

Source: NASBO Fiscal Survey of States; Fiscal 2018 figure is based on recommended budgets. *Aggregate revenue level needed to total at least $799 billion in fiscal 2017 to be equivalent with or exceed real 2008 spending level.

+1.8%+2.2%

+3.4%

11

AT LEAST 23 STATES MADE MID-YEAR BUDGET CUTS IN FISCAL 2017, TOTALING $4.9 BILLION

Enacted Budget Cuts Made After the Budget Passed

2028

35

22

9 8 137

2 3 1

16

37 37

18

5 2 413

41 39

23

8 11 814

1923

0

10

20

30

40

50

$0

$5

$10

$15

$20

$25

$30

$35

$40

Num

ber o

f Sta

tes

$ In

Billio

ns

Number of states Amount of reduction

Recession ends

Recession ends Recession ends

Source: NASBO Fiscal Survey of States

12

STATE SAVINGS ACCOUNTS(RAINY DAY FUNDS)

13

STATES CONTINUE TO STRENGTHEN RAINY DAY FUNDS SINCE HITTING RECENT LOW IN FISCAL 2010-2011

47 States

Median Rainy Day Fund Balance as % of Expenditures

Source: NASBO Data

4.6%

0.7%

4.9%

2.0%

5.5%6.0%

0%

1%

2%

3%

4%

5%

6%

7%

Perc

ent o

f Gen

eral

Fun

d Sp

endi

ng

Fiscal Year

14

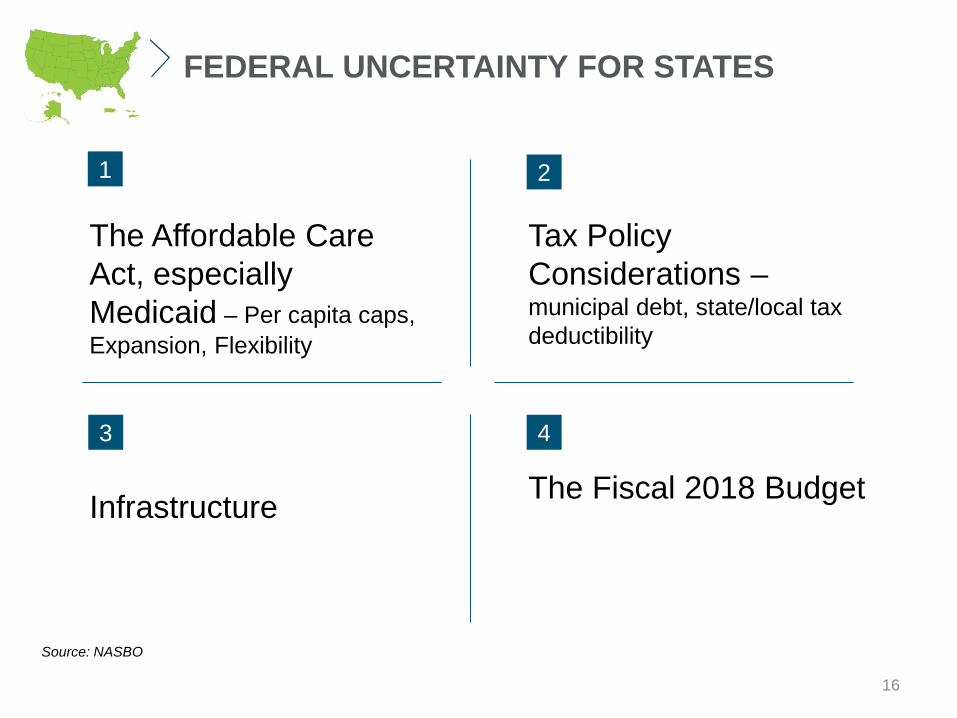

FEDERAL OUTLOOK FOR STATES

15

1 2

3 4

FEDERAL UNCERTAINTY FOR STATES

The Affordable Care Act, especially Medicaid – Per capita caps, Expansion, Flexibility

Tax Policy Considerations –municipal debt, state/local tax deductibility

Infrastructure The Fiscal 2018 Budget

16

Source: NASBO

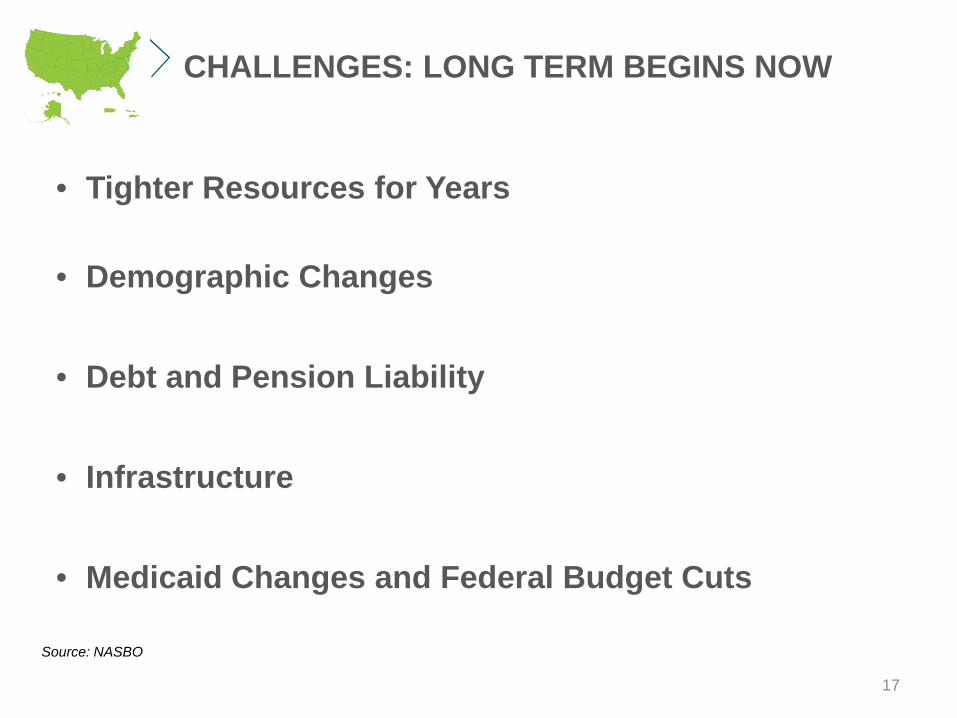

CHALLENGES: LONG TERM BEGINS NOW

• Tighter Resources for Years

• Demographic Changes

• Debt and Pension Liability

• Infrastructure

• Medicaid Changes and Federal Budget Cuts

17

Source: NASBO

Legislative and Regulatory Issues

18

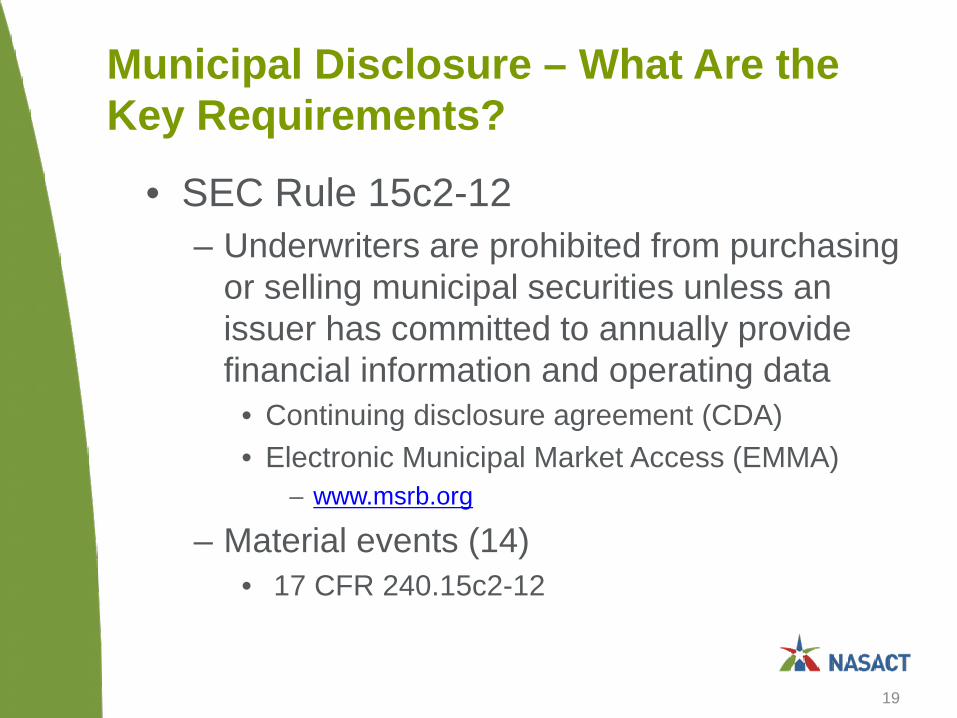

Municipal Disclosure – What Are the Key Requirements?

• SEC Rule 15c2-12– Underwriters are prohibited from purchasing

or selling municipal securities unless an issuer has committed to annually provide financial information and operating data

• Continuing disclosure agreement (CDA)• Electronic Municipal Market Access (EMMA)

– www.msrb.org

– Material events (14)• 17 CFR 240.15c2-12

19

Municipal Disclosures – SEC Proposes Amendments to Rule 15c2-12

• Proposal issued on March 1, 2017– Improves investor protection and enhances

transparency in municipal securities market• Addresses concern about private bank lending

– Comments due by May 15, 2017– 111 pages in length!– Effective date: three months after adoption

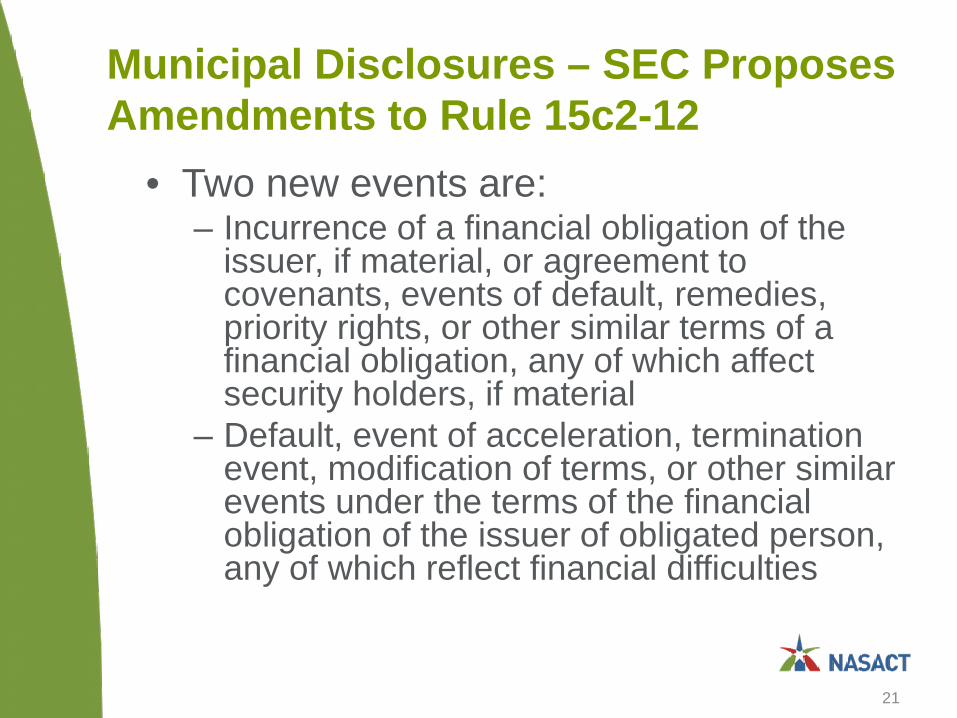

• Adds two new event notices under continuing disclosure undertakings– Currently there are 14 listed events– Requires notice within 10 days of the

occurrence

20

Municipal Disclosures – SEC Proposes Amendments to Rule 15c2-12

• Two new events are:– Incurrence of a financial obligation of the

issuer, if material, or agreement to covenants, events of default, remedies, priority rights, or other similar terms of a financial obligation, any of which affect security holders, if material

– Default, event of acceleration, termination event, modification of terms, or other similar events under the terms of the financial obligation of the issuer of obligated person, any of which reflect financial difficulties

21

Municipal Disclosures – SEC Proposes Amendments to Rule 15c2-12

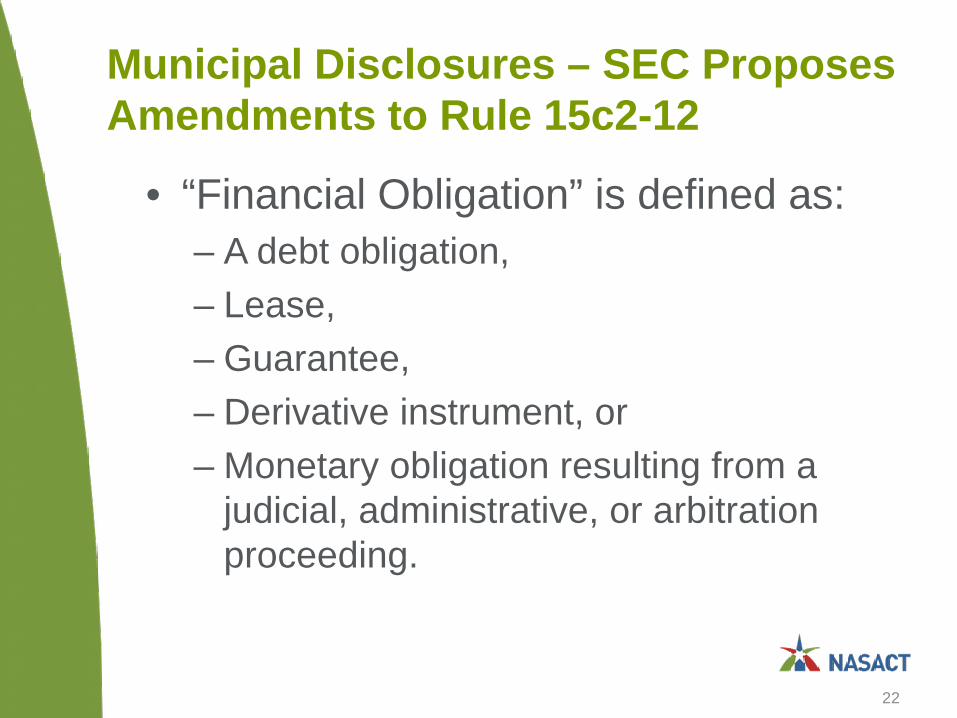

• “Financial Obligation” is defined as:– A debt obligation,– Lease,– Guarantee,– Derivative instrument, or– Monetary obligation resulting from a

judicial, administrative, or arbitration proceeding.

22

Municipal Disclosures – SEC Proposes Amendments to Rule 15c2-12

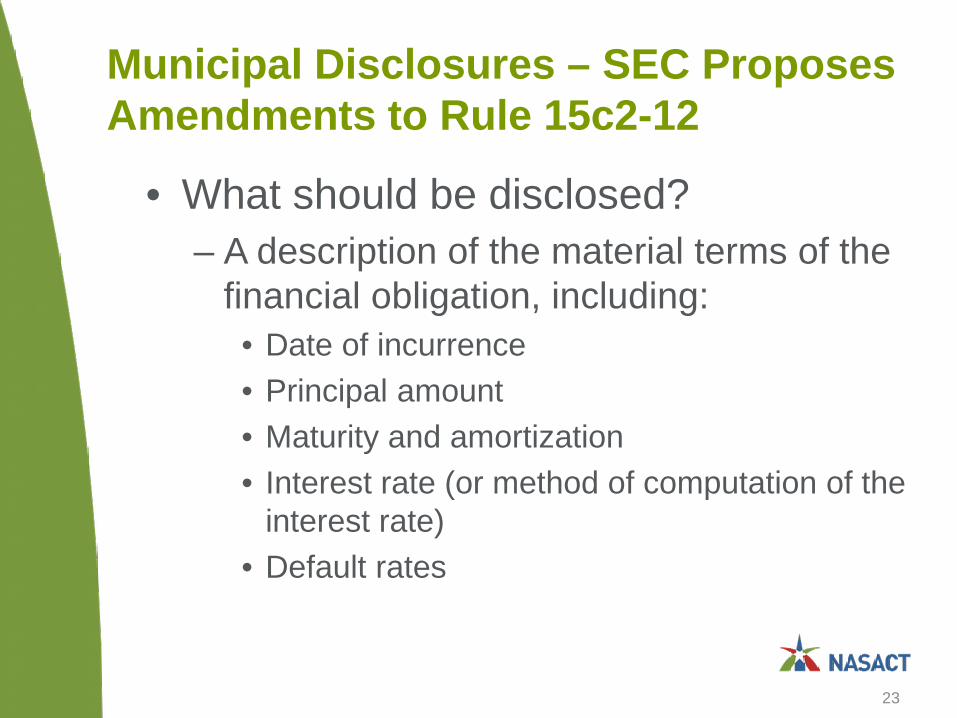

• What should be disclosed?– A description of the material terms of the

financial obligation, including:• Date of incurrence• Principal amount• Maturity and amortization• Interest rate (or method of computation of the

interest rate)• Default rates

23

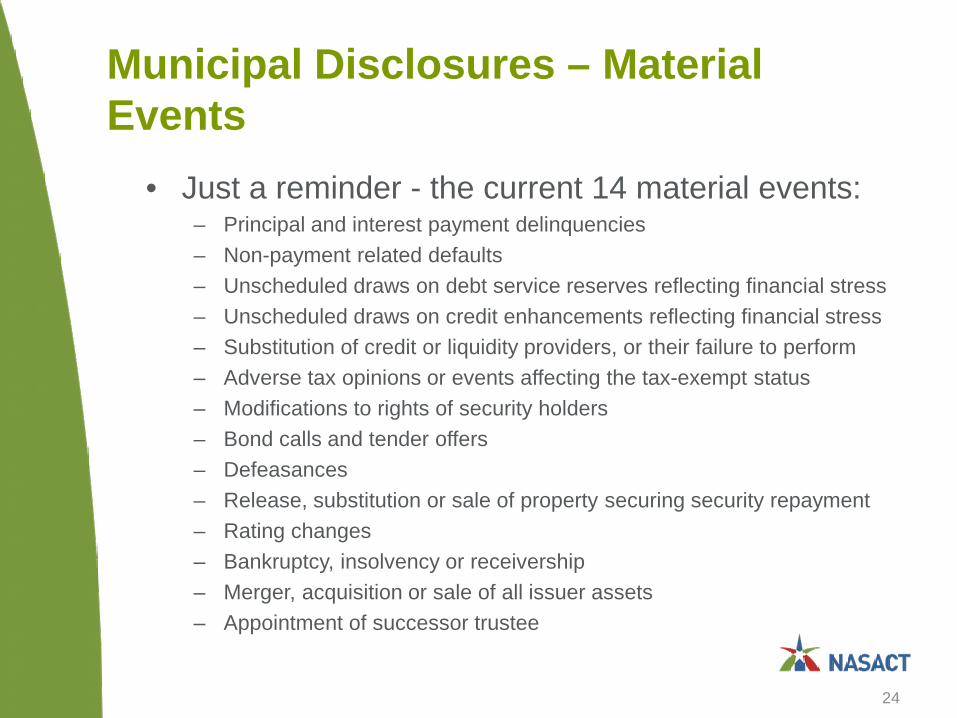

Municipal Disclosures – Material Events

• Just a reminder - the current 14 material events:– Principal and interest payment delinquencies– Non-payment related defaults– Unscheduled draws on debt service reserves reflecting financial stress– Unscheduled draws on credit enhancements reflecting financial stress– Substitution of credit or liquidity providers, or their failure to perform– Adverse tax opinions or events affecting the tax-exempt status– Modifications to rights of security holders– Bond calls and tender offers– Defeasances– Release, substitution or sale of property securing security repayment– Rating changes– Bankruptcy, insolvency or receivership– Merger, acquisition or sale of all issuer assets– Appointment of successor trustee

24

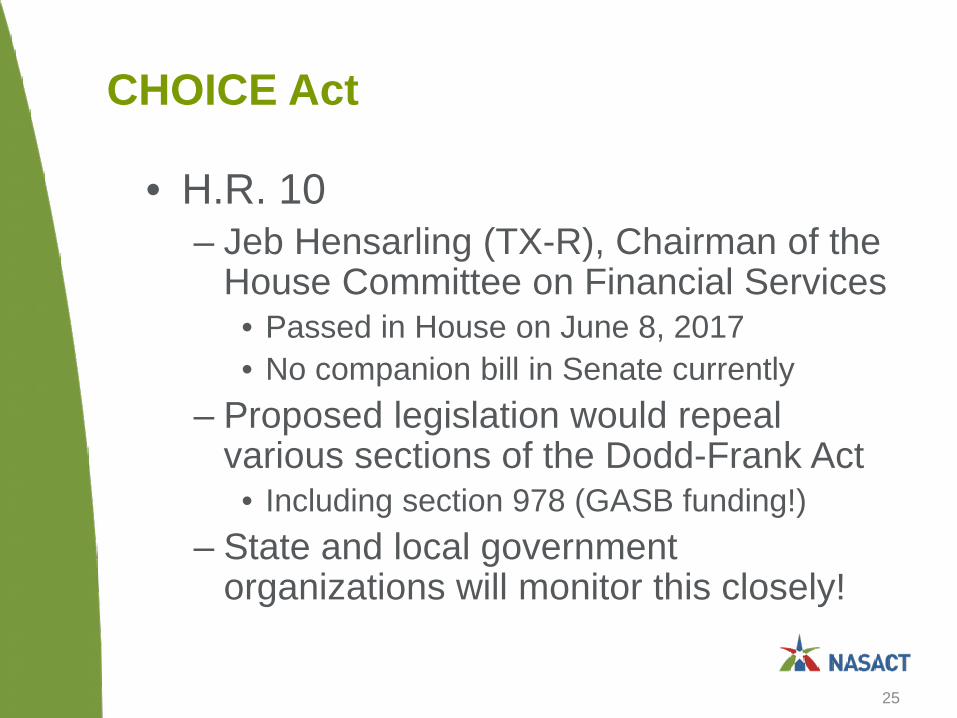

CHOICE Act

• H.R. 10– Jeb Hensarling (TX-R), Chairman of the

House Committee on Financial Services• Passed in House on June 8, 2017• No companion bill in Senate currently

– Proposed legislation would repeal various sections of the Dodd-Frank Act

• Including section 978 (GASB funding!)– State and local government

organizations will monitor this closely!

25

OMB Uniform Guidance

26

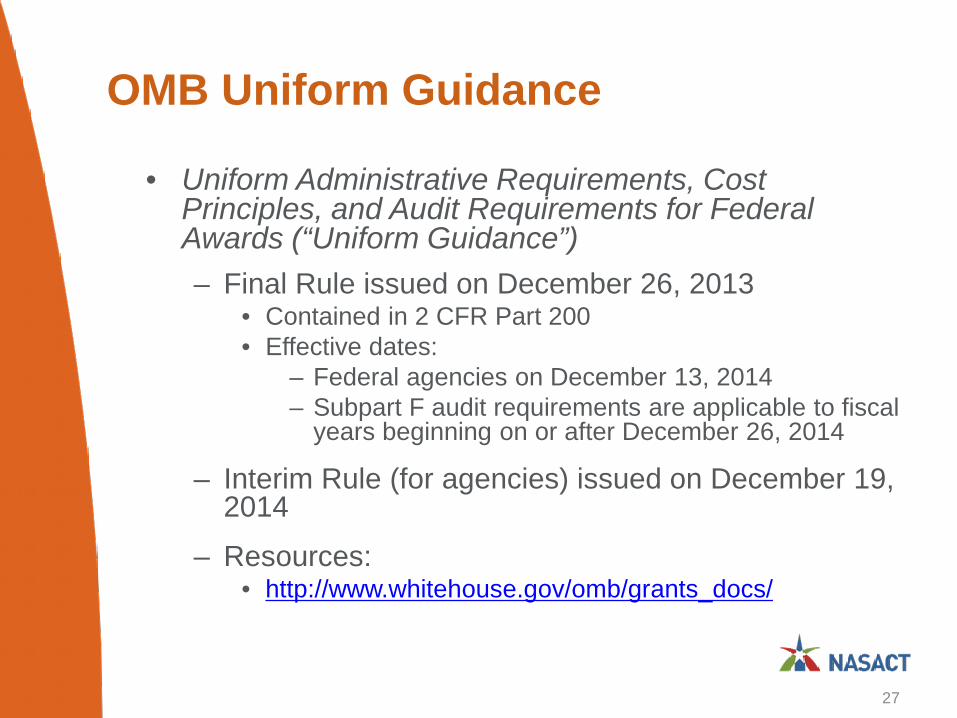

OMB Uniform Guidance

• Uniform Administrative Requirements, Cost Principles, and Audit Requirements for Federal Awards (“Uniform Guidance”)– Final Rule issued on December 26, 2013

• Contained in 2 CFR Part 200 • Effective dates:

– Federal agencies on December 13, 2014– Subpart F audit requirements are applicable to fiscal

years beginning on or after December 26, 2014

– Interim Rule (for agencies) issued on December 19, 2014

– Resources:• http://www.whitehouse.gov/omb/grants_docs/

27

Uniform Guidance Implementation –Current Developments

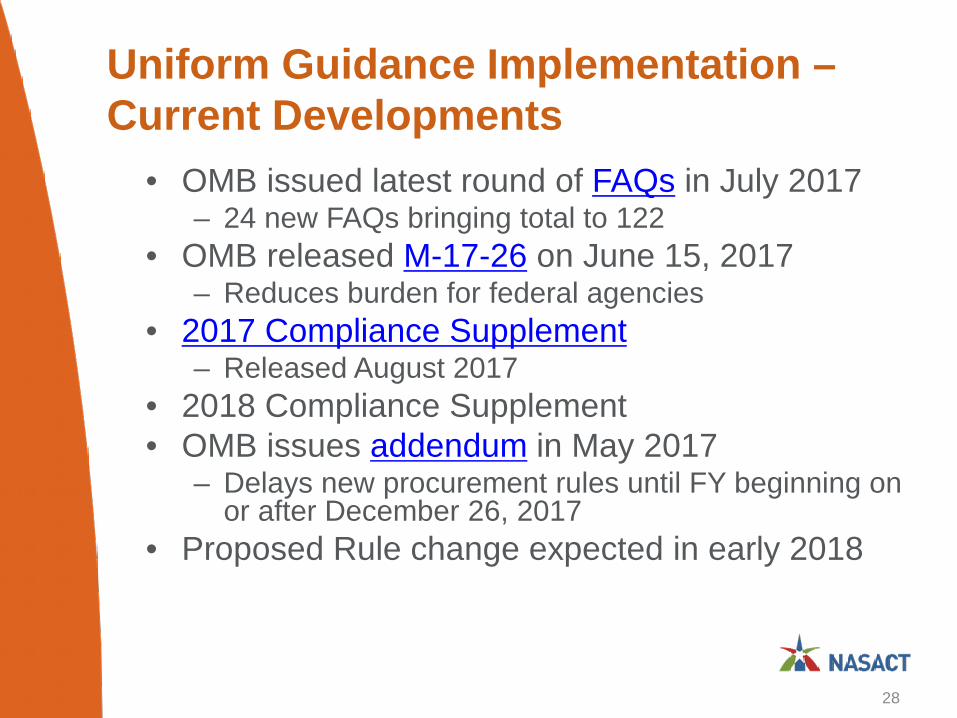

• OMB issued latest round of FAQs in July 2017– 24 new FAQs bringing total to 122

• OMB released M-17-26 on June 15, 2017– Reduces burden for federal agencies

• 2017 Compliance Supplement – Released August 2017

• 2018 Compliance Supplement• OMB issues addendum in May 2017

– Delays new procurement rules until FY beginning on or after December 26, 2017

• Proposed Rule change expected in early 2018

28

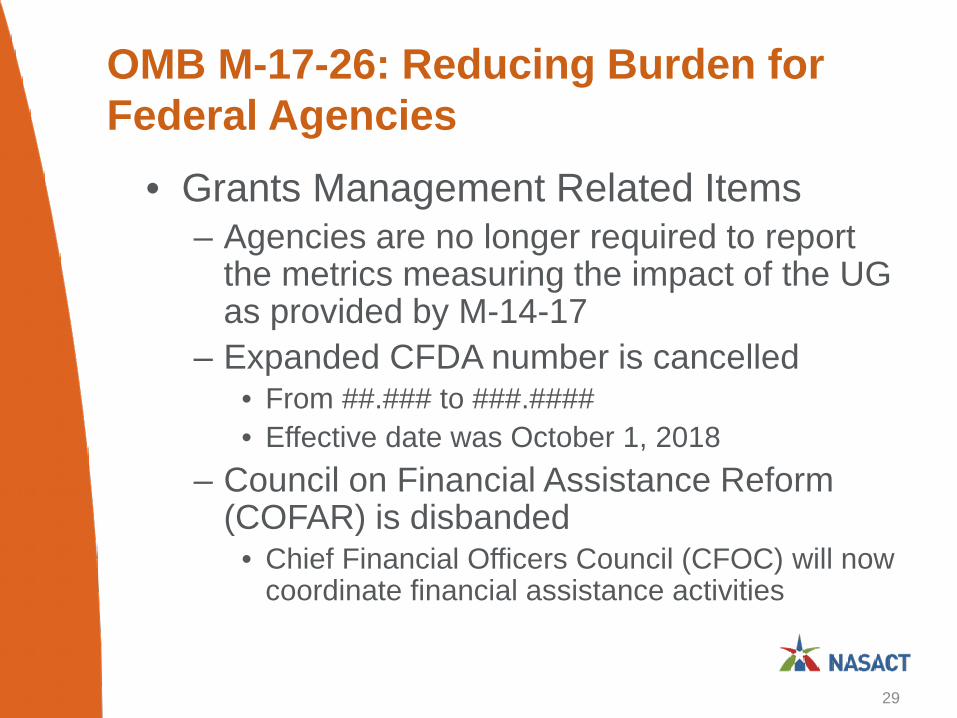

OMB M-17-26: Reducing Burden for Federal Agencies

• Grants Management Related Items– Agencies are no longer required to report

the metrics measuring the impact of the UG as provided by M-14-17

– Expanded CFDA number is cancelled• From ##.### to ###.####• Effective date was October 1, 2018

– Council on Financial Assistance Reform (COFAR) is disbanded

• Chief Financial Officers Council (CFOC) will now coordinate financial assistance activities

29

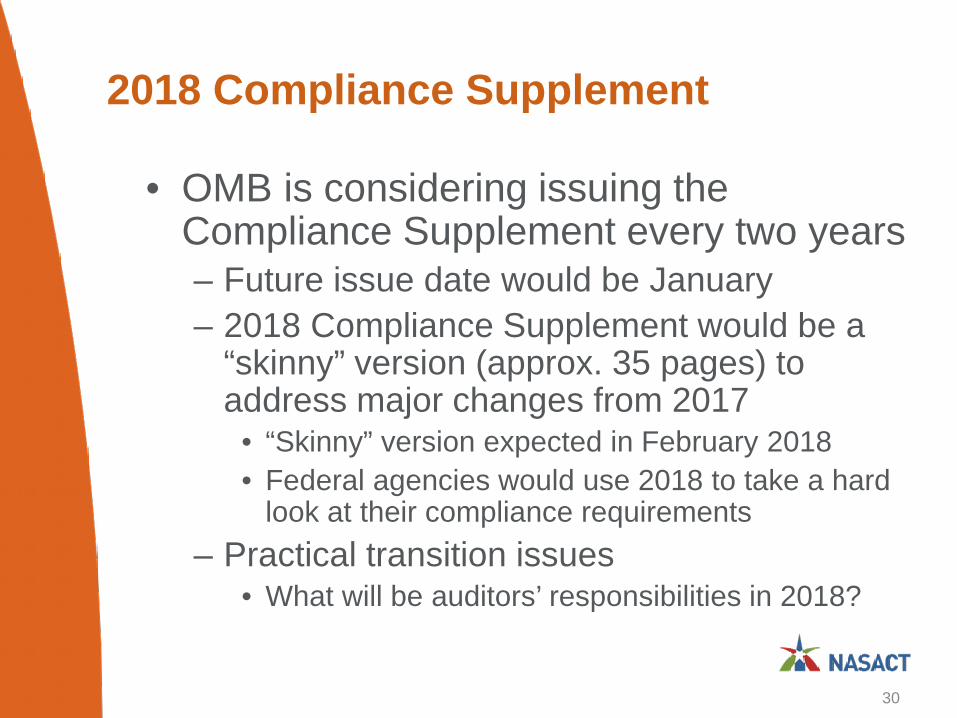

2018 Compliance Supplement

• OMB is considering issuing the Compliance Supplement every two years– Future issue date would be January– 2018 Compliance Supplement would be a

“skinny” version (approx. 35 pages) to address major changes from 2017

• “Skinny” version expected in February 2018• Federal agencies would use 2018 to take a hard

look at their compliance requirements– Practical transition issues

• What will be auditors’ responsibilities in 2018?

30

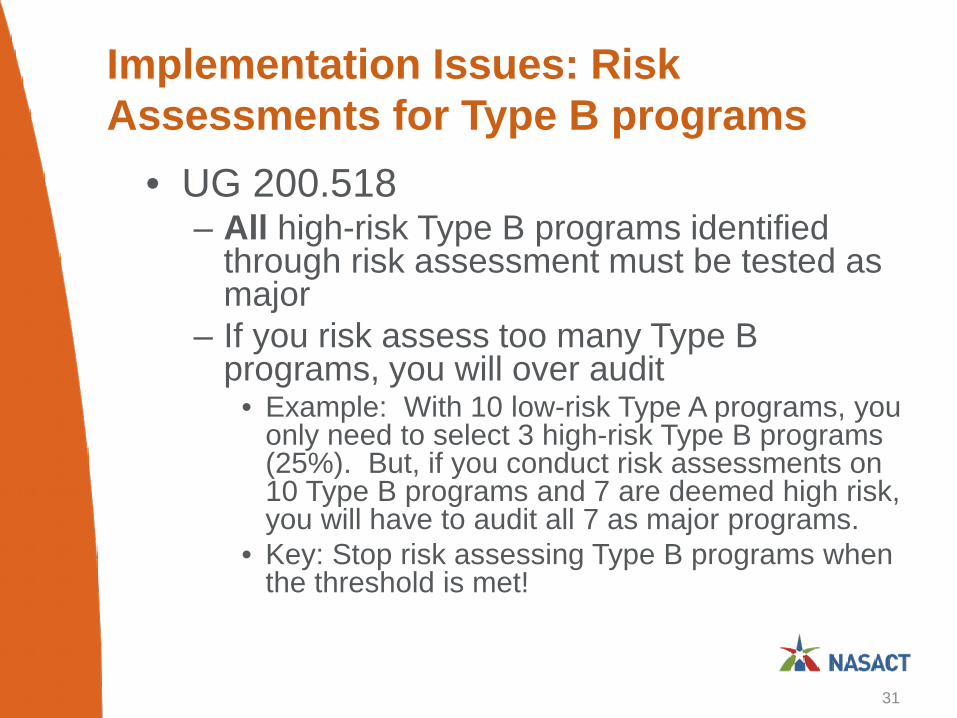

Implementation Issues: Risk Assessments for Type B programs

• UG 200.518– All high-risk Type B programs identified

through risk assessment must be tested as major

– If you risk assess too many Type B programs, you will over audit

• Example: With 10 low-risk Type A programs, you only need to select 3 high-risk Type B programs (25%). But, if you conduct risk assessments on 10 Type B programs and 7 are deemed high risk, you will have to audit all 7 as major programs.

• Key: Stop risk assessing Type B programs when the threshold is met!

31

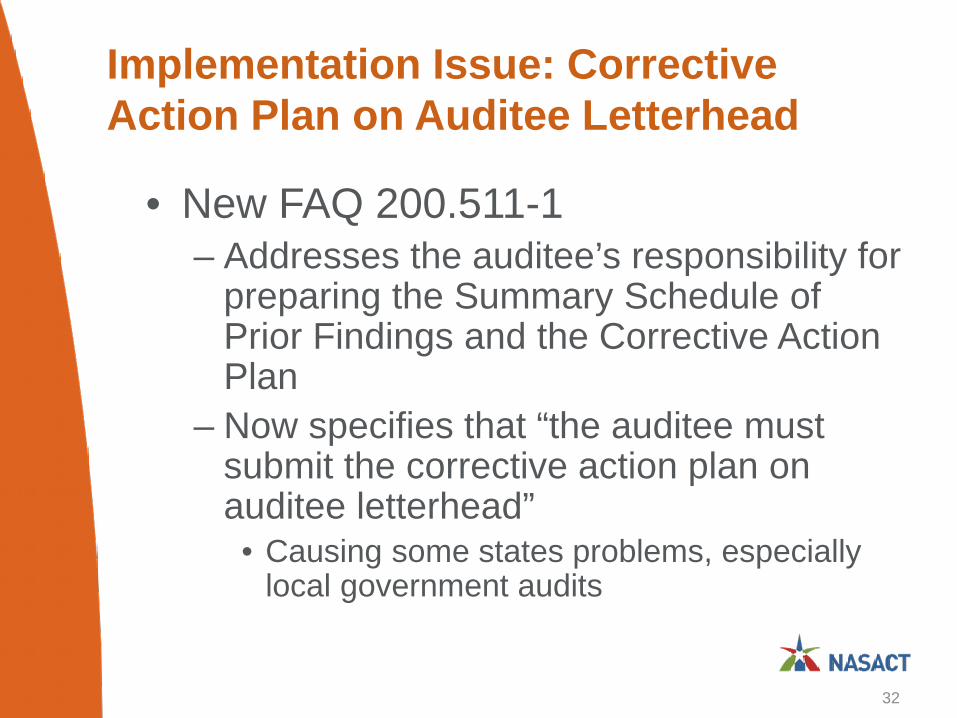

Implementation Issue: Corrective Action Plan on Auditee Letterhead

• New FAQ 200.511-1– Addresses the auditee’s responsibility for

preparing the Summary Schedule of Prior Findings and the Corrective Action Plan

– Now specifies that “the auditee must submit the corrective action plan on auditee letterhead”

• Causing some states problems, especially local government audits

32

Implementation Issue: “Smoothing” of Major Programs

• New FAQ 200.518-1• Heavy Audit Burden in Year 3 (2018)

• New high-risk criteria will cause more Type A programs to be deemed low-risk– However, all Type A programs must still be tested as

major at least once every three years– As a result, there will be a heavy audit burden in year

3 due to large number of low-risk Type A programs that must be tested as major

• “Smoothing” of major programs over three-year period is a solution

– 2016 Compliance Supplement allowed “smoothing” technique

• Appendix VII - Other Audit Advisories

33

Implementation Issue: Pension Plan Costs Allowability

• Section 200.431(g)(3)– “For entities using accrual based accounting,

the cost assigned to each fiscal year is determined in accordance with GAAP”

• GASB 68 calculated pension costs differ from the amounts funded

– HHS DCA is currently allowing amounts funded in excess of GASB 68 amount (but awaiting OMB guidance)

– OMB hopes to release a proposed revision in late 2017

• Similar issue for OPEB costs

34

Current Developments: Testing SFA Cluster as Major

• U.S. Department of Education (ED)– Section 487(c) of the Higher Education Act of 1965 (HEA)

requires that each Title IV participating institution submit a financial and compliance audit “on at least an annual basis”

• Conflicts with UG when SFA cluster is not selected as a major program

– ED issued memo on August 5, 2016• If Title IV programs are low risk, institutions should “contact their

respective School Participation Division.”– ED issued guidance on April 28, 2017 regarding FY 2017

single audits • Follow same approach as FY 2016 single audits

– ED is also adding a new special test and provision on Securing Student Information

• Plans to issue in 2018 Compliance Supplement

35

Current Developments: Another Separate Audit Requirement?

• HHS’s Preventive Health and Health Services Block Grant (PHHSBG) – CFDA 93.758– Award notices are stating that this program

shall be selected at a Type B in FY 2018 Single Audits

• States are applying 200.503(e) (Relation to other audit requirements) and providing the incremental costs to test as major

• In at least one case, CDC agreed to pay the additional cost

– Currently consulting with OMB and HHS for proper treatment

36

Transparency IssuesDATA Act

37

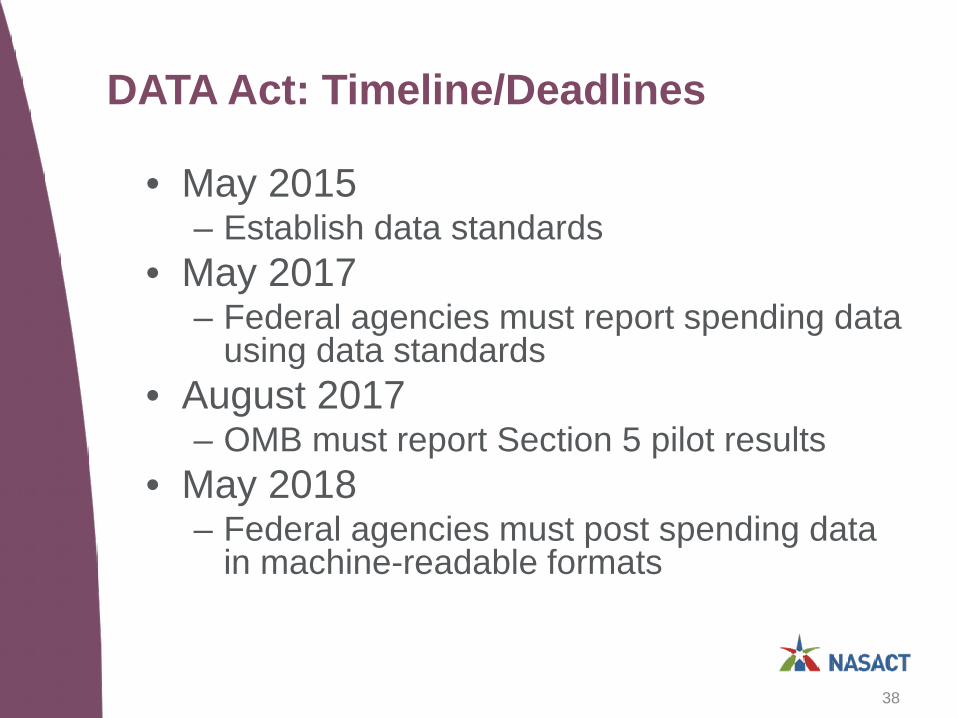

DATA Act: Timeline/Deadlines

• May 2015– Establish data standards

• May 2017– Federal agencies must report spending data

using data standards• August 2017

– OMB must report Section 5 pilot results• May 2018

– Federal agencies must post spending data in machine-readable formats

38

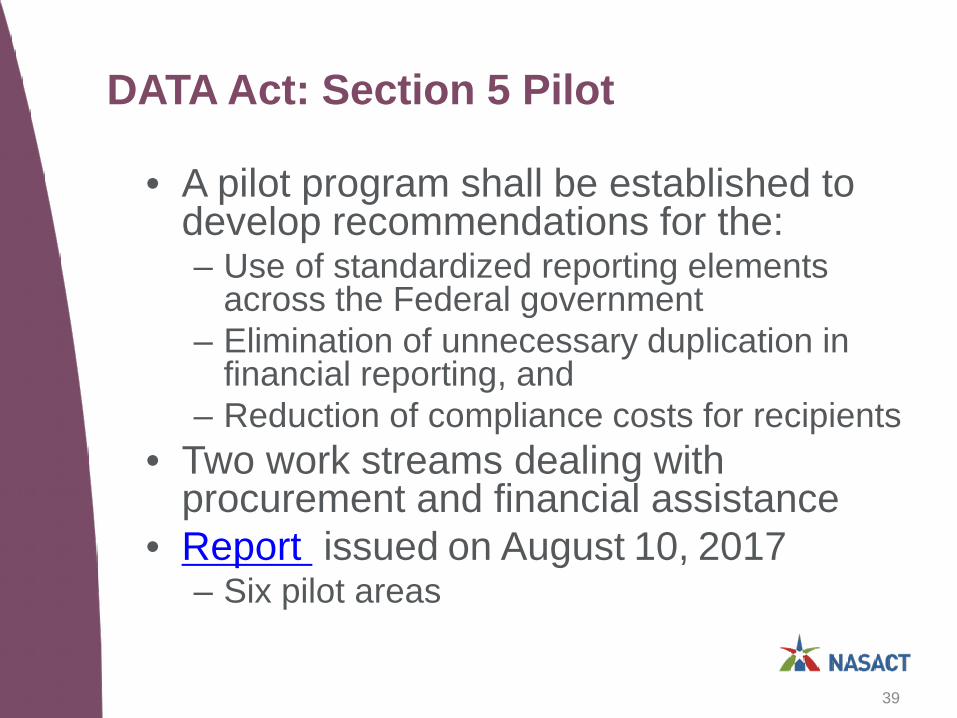

DATA Act: Section 5 Pilot

• A pilot program shall be established to develop recommendations for the:– Use of standardized reporting elements

across the Federal government– Elimination of unnecessary duplication in

financial reporting, and – Reduction of compliance costs for recipients

• Two work streams dealing with procurement and financial assistance

• Report issued on August 10, 2017– Six pilot areas

39

DATA Act: Section 5 Pilot

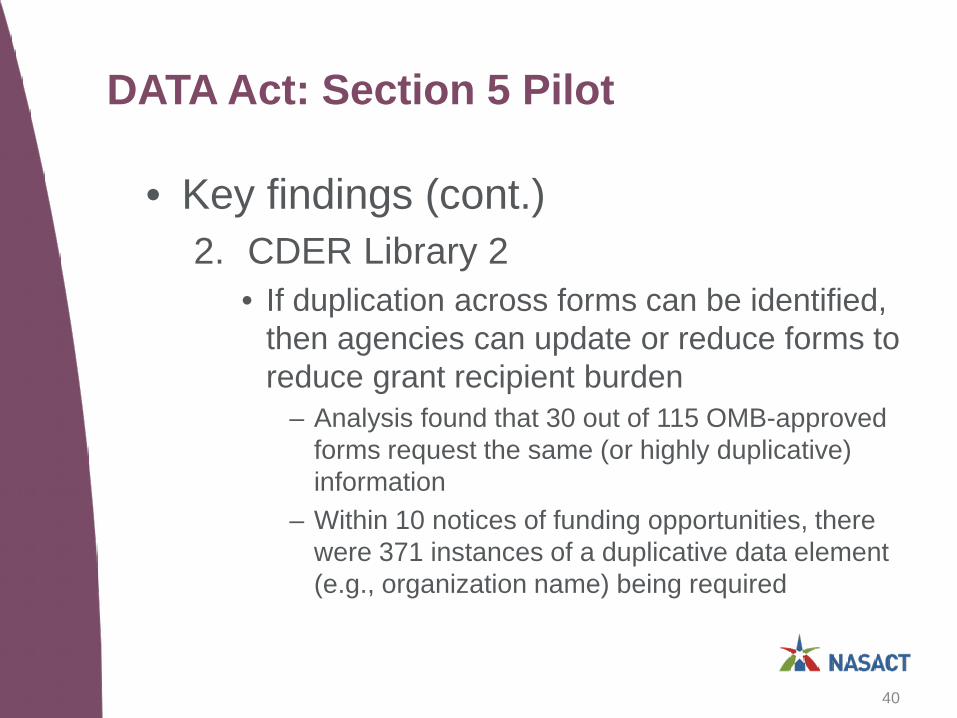

• Key findings (cont.)2. CDER Library 2

• If duplication across forms can be identified, then agencies can update or reduce forms to reduce grant recipient burden

– Analysis found that 30 out of 115 OMB-approved forms request the same (or highly duplicative) information

– Within 10 notices of funding opportunities, there were 371 instances of a duplicative data element (e.g., organization name) being required

40

DATA Act: Section 5 Pilot

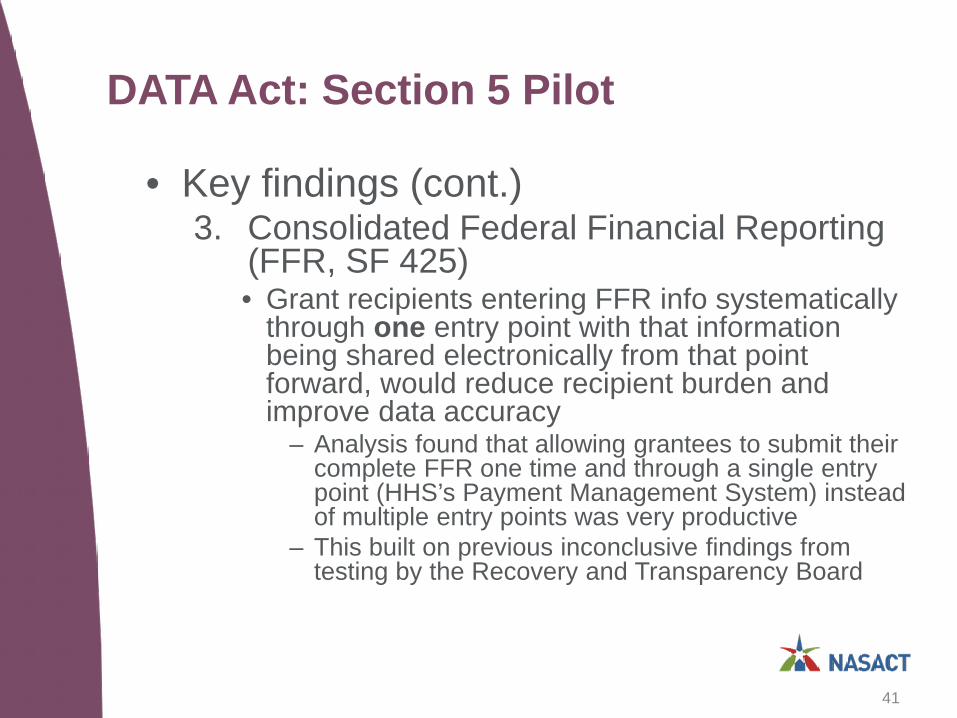

• Key findings (cont.)3. Consolidated Federal Financial Reporting

(FFR, SF 425) • Grant recipients entering FFR info systematically

through one entry point with that information being shared electronically from that point forward, would reduce recipient burden and improve data accuracy

– Analysis found that allowing grantees to submit their complete FFR one time and through a single entry point (HHS’s Payment Management System) instead of multiple entry points was very productive

– This built on previous inconclusive findings from testing by the Recovery and Transparency Board

41

DATA Act: Section 5 Pilot

• Key findings (cont.)4. Single Audit

• If grant recipients do not have to report the same info on duplicative forms (SEFA and SF-SAC), but rather allow information reported once to be auto-populated electronically, grant recipient’s burden would be reduced

– Majority of participants responded that the new SEFA template and FAC pilot reporting tool saves time and increases accuracy

– OMB plans to expose a combined “long SF-SAC form” for comment in February 2018

– Long form will be available for use in 2019, but will not be required

42

DATA Act: Section 5 Pilot

• Report Recommendations – Pursue further standardization to

increase opportunities to streamline reporting

– Seize opportunities to use information technology that can auto-populate reporting fields from existing Federal sources

– Leverage information technology open standards to rapidly develop new tools

43

DATA Act: Resources

• Want to know more?– USA Spending

• https://www.usaspending.gov/Pages/data-act.aspx

– Spending Transparency Collaboration (GitHub)

• https://fedspendingtransparency.github.io/– National Dialogue on Reducing Burden

• https://cxo.dialogue2.cao.gov/a/pages/gsa-challenges

– Open Beta (discusses the schema)• https://openbeta.usaspending.gov

44

Accounting Issues

45

GASB 74 and 75 – Other Postemployment Benefits (OPEB)

• Release and effective dates– Final statements issued in June 2015

• Statement 74 – Plans• Statement 75 - Employers

– Effective dates• Plans – June 2017• Employers – June 2018

46

GASB 74 and 75 – Other Postemployment Benefits (OPEB)

• Built on the new pension standards– Designed to improve OPEB information

for:• decision-making and accountability purposes• comparability across governments• transparency

– Establishes standards for: • liabilities • deferred inflows and outflows of resources• expense/expenditures

47

GASB’s Reexamination of the Reporting Model

• Added to technical agenda on September 1, 2015

• Targeted review (not “wholesale” changes)

• First phase of the project– Financial Reporting Model Improvements

– Governmental Funds– Invitation to Comment (ITC) released

December 7, 2016

48

GASB’s Reexamination of the Reporting Model: Governmental Funds

• ITC addresses potential improvements for financial reporting of governmental funds, including:– Recognition approaches (measurement focus

and basis of accounting)– Format of the governmental funds statement of

resource flows– Specific terminology– Reconciliation to the government-wide

statements– For certain recognition approaches, a statement

of cash flows

49

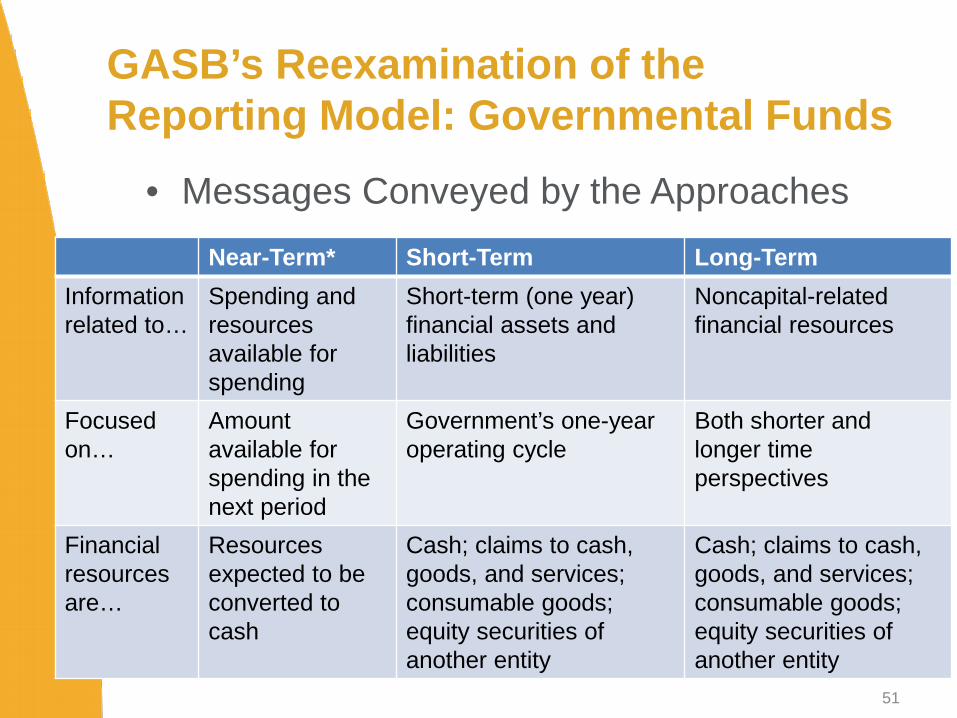

GASB’s Reexamination of the Reporting Model: Governmental Funds

• ITC introduces three alternative recognition approaches for governmental fund financial statements:– Near-term financial resources– Short-term financial resources, and– Long-term financial resources

• These three approaches fall on a continuum—from a closer-to-cash approach at one end to a closer-to-economic resources approach on the other

50

GASB’s Reexamination of the Reporting Model: Governmental Funds

51

Near-Term* Short-Term Long-TermInformation related to…

Spending and resources available for spending

Short-term (one year) financial assets and liabilities

Noncapital-relatedfinancial resources

Focused on…

Amount available for spending in the next period

Government’s one-year operating cycle

Both shorter and longer time perspectives

Financial resources are…

Resources expected to be converted to cash

Cash; claims to cash, goods, and services; consumable goods; equity securities of another entity

Cash; claims to cash, goods, and services; consumable goods; equity securities of another entity

• Messages Conveyed by the Approaches

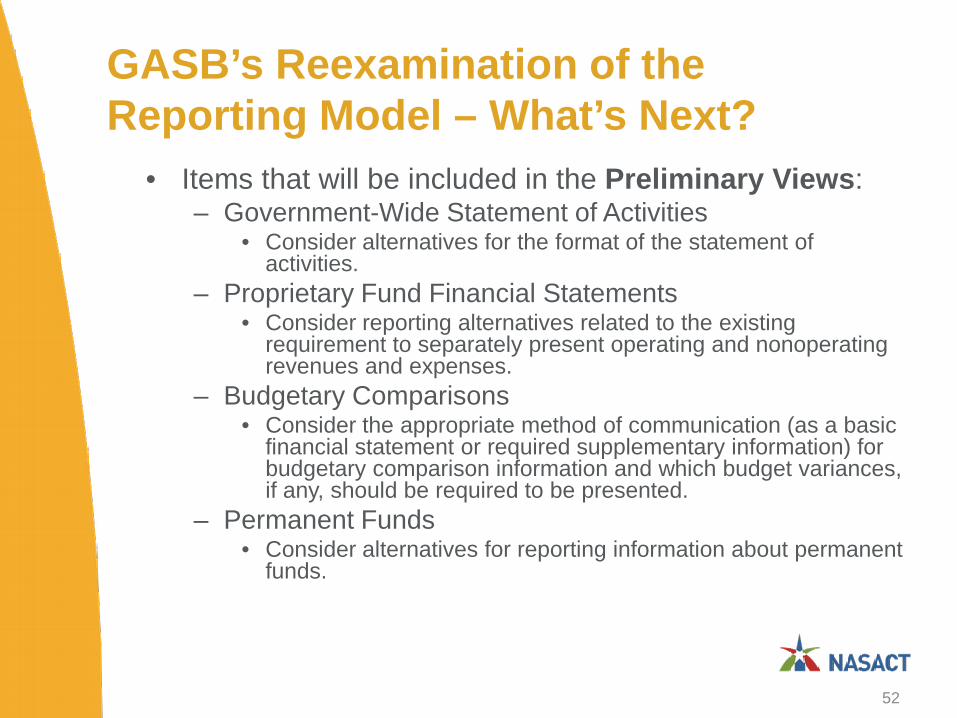

GASB’s Reexamination of the Reporting Model – What’s Next?

• Items that will be included in the Preliminary Views:– Government-Wide Statement of Activities

• Consider alternatives for the format of the statement of activities.

– Proprietary Fund Financial Statements• Consider reporting alternatives related to the existing

requirement to separately present operating and nonoperating revenues and expenses.

– Budgetary Comparisons• Consider the appropriate method of communication (as a basic

financial statement or required supplementary information) for budgetary comparison information and which budget variances, if any, should be required to be presented.

– Permanent Funds• Consider alternatives for reporting information about permanent

funds.

52

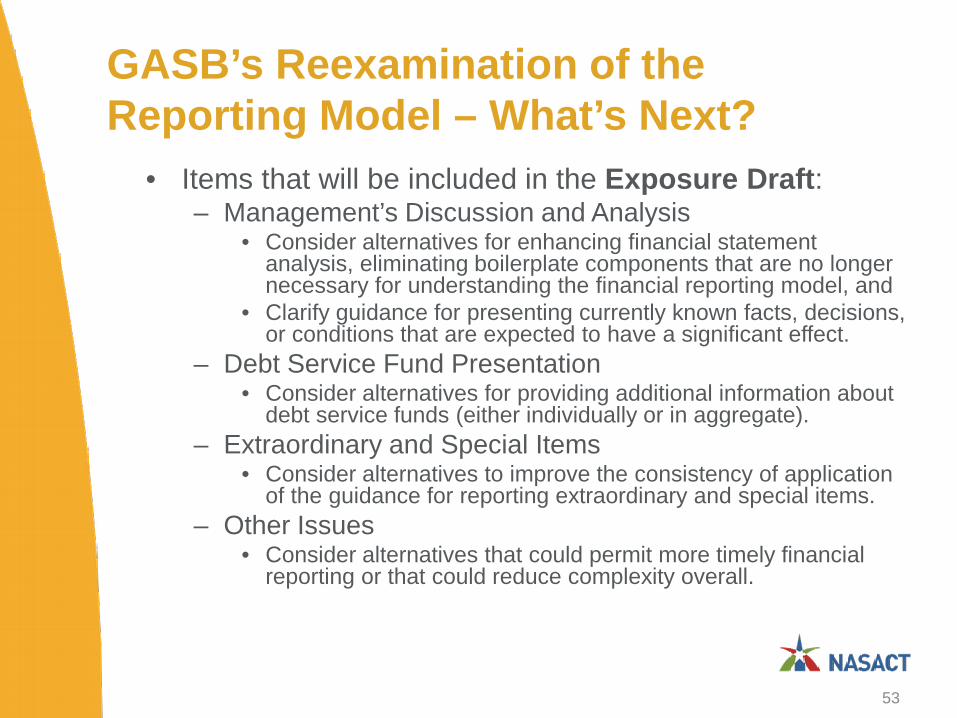

GASB’s Reexamination of the Reporting Model – What’s Next?

• Items that will be included in the Exposure Draft:– Management’s Discussion and Analysis

• Consider alternatives for enhancing financial statement analysis, eliminating boilerplate components that are no longer necessary for understanding the financial reporting model, and

• Clarify guidance for presenting currently known facts, decisions, or conditions that are expected to have a significant effect.

– Debt Service Fund Presentation• Consider alternatives for providing additional information about

debt service funds (either individually or in aggregate).– Extraordinary and Special Items

• Consider alternatives to improve the consistency of application of the guidance for reporting extraordinary and special items.

– Other Issues• Consider alternatives that could permit more timely financial

reporting or that could reduce complexity overall.

53

GASB’s Reexamination of the Reporting Model – What’s Next?

• Timing– Deliberations begin in October 2015– December 2016: Invitation to Comment– July 2018: Preliminary Views– April 2020: Exposure Draft– November 2021: Final Statement– Implementation dates: sometime in 2022,

2023

54

Auditing Issues

55

Government Auditing Standards

• “Yellow Book” or• Generally

Accepted Government Auditing Standards (“GAGAS”)

56

GAO’s Government Auditing Standards

• Exposure Draft issued April 6, 2017– First proposed changes since 2011– Comment period ended July 6, 2017– Why Issued?

• Represents a modernized version that takes into account developments in the accounting and auditing professions

• Intended to reinforce principles of transparency and provide a framework for high quality government audits

– Effective date: to be determined– http://gao.gov/yellowbook/overview

57

GAO’s Government Auditing Standards

• Some of the key proposed changes:1. New format and organization of GAGAS2. Independence threats related to

preparing records and financial statements

3. Independence guidance related to three-party arrangements

4. Independence guidance related to professional services in government

5. GAGAS qualification for CPE requirement

58

GAO’s Government Auditing Standards

• Key proposed changes (cont.):6. CPE guidance for 24-hour and 56-hour

requirements7. Peer review requirements8. Internal control: financial audits,

examination engagements, and performance audits

9. New requirements for waste10.Standards for reviews of financial

statements

59

GAO’s Government Auditing Standards

• Formatting Changes and Realignment– Requirements will be differentiated from

application guidance (“clarity format”)• “must” and “should” statements are

highlighted in the requirements– Supplemental Guidance (Appendix from

2011) is either removed or incorporated into individual chapters

60

GAO’s Government Auditing Standards

• Chapter reorganization and realignment– Chapter 1: Foundation and Principles– Chapter 2: General Requirements– Chapter 3: Ethics, Independence, Professional Judgment– Chapter 4: Competence and CPE– Chapter 5: QC and Peer Review – Chapter 6: Standards for Financial Audits– Chapter 7: Standards for Attestation Engagements and

Reviews of Financial Statements– Chapter 8: Fieldwork Standards for Performance Audits– Chapter 9: Reporting Standards for Performance Audits

61

GAO’s Government Auditing Standards

• Independence Threats: Preparing Accounting Records and Financial Statements (3.89)– Any services performed by auditors related to

preparing accounting records and FS, other than those defined as impairments, create significant threats to auditors’ independence

– Auditors should:• Document the threats and safeguards applied to

eliminate and reduce threats to an acceptable level OR

• Decline to perform the service

62

GAO’s Government Auditing Standards

• Independence Threats: Preparing Accounting Records and Financial Statements (cont.)– Certain services impair independence (3.88)

• Determining or changing JE, account codes, or accounting records without management’s approval

• Authorizing or approving the entity’s transactions• Preparing or making changes to source

documents without management approval

63

GAO’s Government Auditing Standards

• GAGAS Qualification CPE Requirement– Standards are revised to require that

auditors who conduct an engagement in accordance with GAGAS complete GAGAS qualification requirements by completing 4 hours of CPE in GAGAS topics: (4.15)

• Supervisors and partners or directors should obtain GAGAS Qualification before completing work on their first GAGAS engagement

• Entry-level staff should obtain GAGAS Qualification by the end of their first full 2-year CPE period

64

GAO’s Government Auditing Standards

• GAGAS Qualification CPE Requirement (cont.)– To update their GAGAS Qualification, auditors

should complete at least 4 hours of CPE in GAGAS topics each time the Comptroller General issues a revision of GAGAS (4.17)

• These CPE hours should be completed by the end of each auditor’s next full 2-year CPE period after the GAGAS revision is issued

• CPE Q&A document (2005) is superseded

65

GAO’s Government Auditing Standards

• New Requirements for Waste– For financial audits, examination engagements, and

performance audits, standards are expanded to require that auditors perform audit procedures to ascertain the potential effect on the audit objectives if they become aware of waste (6.16, 7.18, 8.69)

• Auditors are required to report when waste has occurred that is material or has a significant effect on the audit objectives for financial audits, examination engagements, and performance audits (6.35, 7.41, 9.32)

• Auditors are required to communicate in writing waste that does not have a material or significant effect on the audit objectives but warrants the attention of those charged with governance for financial audits, examination engagements, and performance audits (6.39, 7.42, 9.33)

66

GAO’s Government Auditing Standards

• What is Waste? (6.17, 7.19, 8.75)– The act of using or expending resources

carelessly, extravagantly, or to no purpose. – Waste involves the taxpayers not receiving

reasonable value for money in connection with any government-funded activities because of an inappropriate act or omission by parties with control over or access to government resources.

– Waste can include activities that do not include abuse and does not necessarily involve a violation of law. Rather, waste relates primarily to mismanagement, inappropriate actions, and inadequate oversight.

67

AICPA Proposed SSAE: Selected Procedures

• Exposure Draft issued Sept 1, 2017– Comments due December 1, 2017– A new engagement type; different than AUP

• Addresses a market gap that exists between a “verifier” and “adviser”

– Proposed standard would:• Provide flexibility by not requiring the specified parties to

either establish the procedures or agree to the sufficiency of the procedures

– Practitioner may determine the procedures• Not include a requirement to either request an assertion

or disclose in the report when the assertion is not obtained

• Not include a requirement for the practitioner to restrict the use of the report

68

AICPA Professional Ethics Division: State and Local Government Entities

• Exposure Draft issued July 7, 2017– Formerly Entities Included in State and

Local Government Financial Statements (ET sec. 1.224.020)

– Addresses a member’s (of the AICPA) independence with respect to entities that are required to be included in a state or local government’s financial reporting entity

69

AICPA Professional Ethics Division: State and Local Government Entities

• Makes use of terms downstream, upstream and brother-sister entities– Downstream: refers to those entities that are “below” the

f/s attest client in its organization structure• e.g., financial statement attest client is the primary government,

funds and component units to be evaluated are those required to be included in the primary government’s financial reporting entity

– Upstream: refers to those entities that are “above” the f/s attest client

• e.g., financial statement attest client is a fund or component unit– Bother-sister: refers to other funds and component units

that the member does not provide attest services to but are included in the same upstream financial reporting entity as the financial statement attest client

70

Other Emerging IssuesThings on the radar…

71

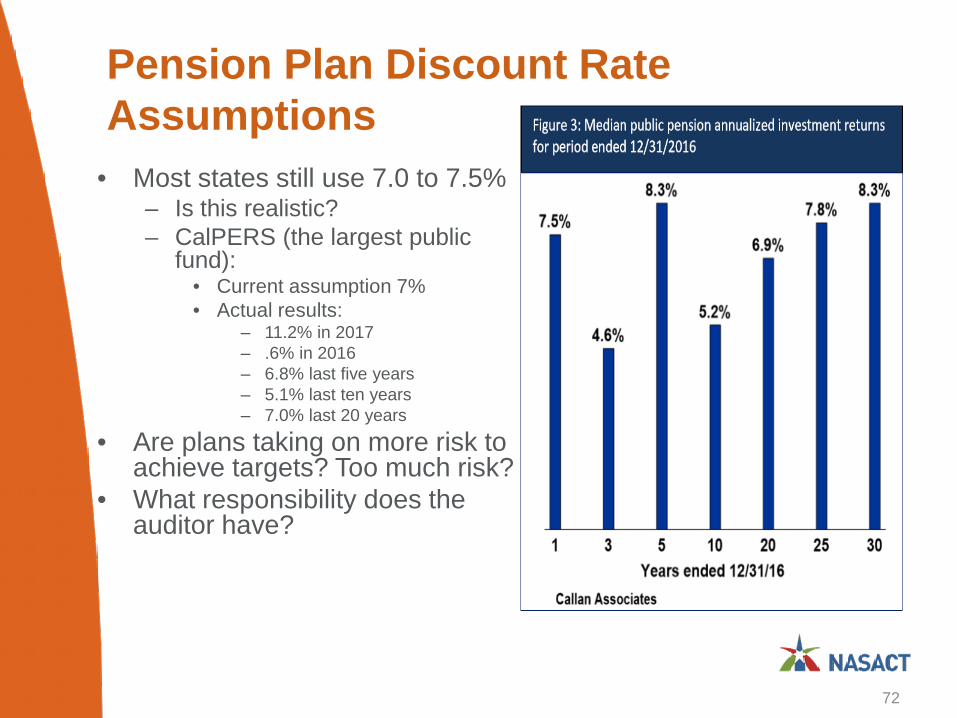

Pension Plan Discount Rate Assumptions

• Most states still use 7.0 to 7.5%– Is this realistic?– CalPERS (the largest public

fund):• Current assumption 7%• Actual results:

– 11.2% in 2017– .6% in 2016– 6.8% last five years– 5.1% last ten years– 7.0% last 20 years

• Are plans taking on more risk to achieve targets? Too much risk?

• What responsibility does the auditor have?

72

These continue to be interesting times…

73

Top Related