Languages

Pages

Legal

Emerging Financial Markets 5: Currency Trading & Risk Management

Prof. J.P. Mei

How Currency Crisis Happen? 1. The "first generation" currency crisis model represented

by Krugman (1979) and Flood and Garber (1984): Strong incentive to engage in inconsistent policies during elections by pursuing expansionary monetary and fiscal policies while holding exchange rates fixed to ensure price stability or other policy objectives.

2. The "second generation" model of Obstfeld (1994): Contradicting motives. Jobs and stability (Banking problems). In such a model, the cost of defending the currency increases when people suspect that the government is leaning towards abandoning the fixed rate.

5

How Currency Crisis Happen? 3. There is a possibility that fixed rates may be

abandoned but not inevitable. Massive exit will make this inevitable. Self-fulfilling exchange rate crises (see, Hong Kong).

4. Heading Behavior: You are just one buffalo and there are thousands of others!

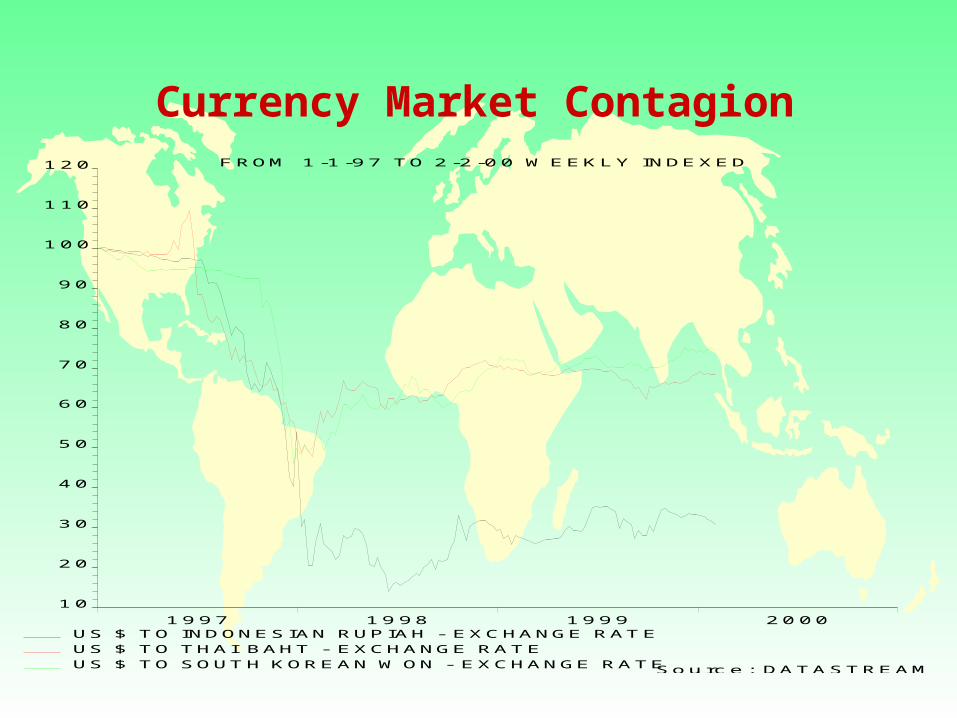

5. Contagion: Countries within geographic regions are often closely connected both in real and financial terms.

6. Contingent investment or "real options": foreign capital flow to Asia from a huge $93 billion inflow in 1996 to a $12 billion net outflow in 1997.

5

Currency Market Movement and Volatility(Notes for the following table )

Negative Means reflects devaluation against dollar. Some markets have low volatility due to currency peg.

(Volatility could be under-estimated) The presence of short-run positive serial correlation for

most countries. Long-term mean reversion (negative serial correlation) Jumps as a result of government intervention and

speculative attacks (Thailand). Excess skewness and kurtosis may lead to under-pricing

of derivatives based on conventional approach. There is cross-correlation and currency market contagion

in the short-run. 4

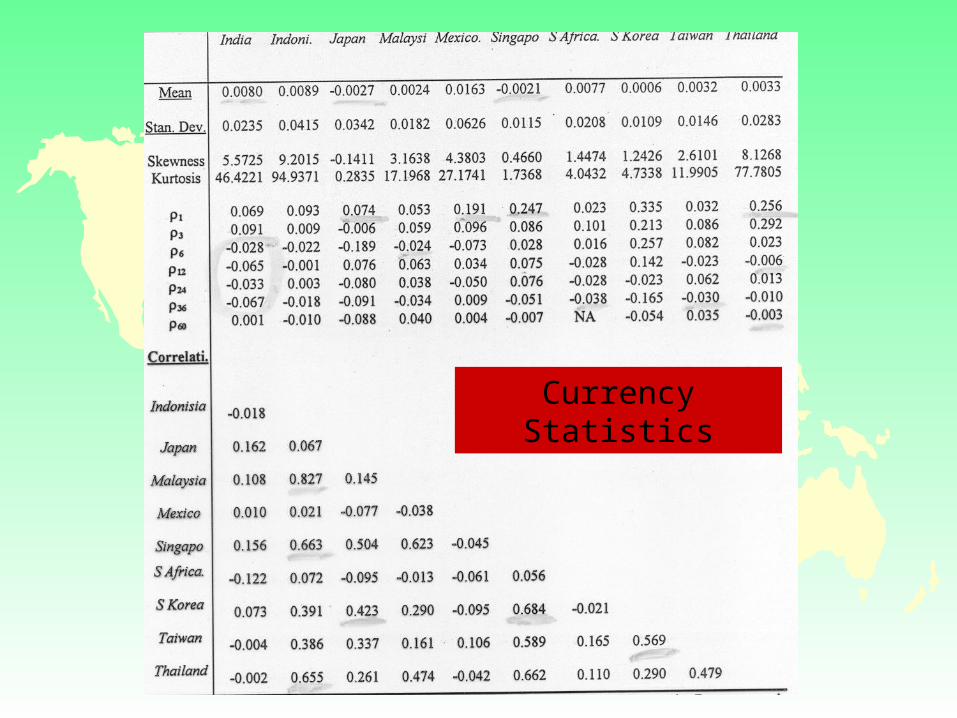

Currency Statistics

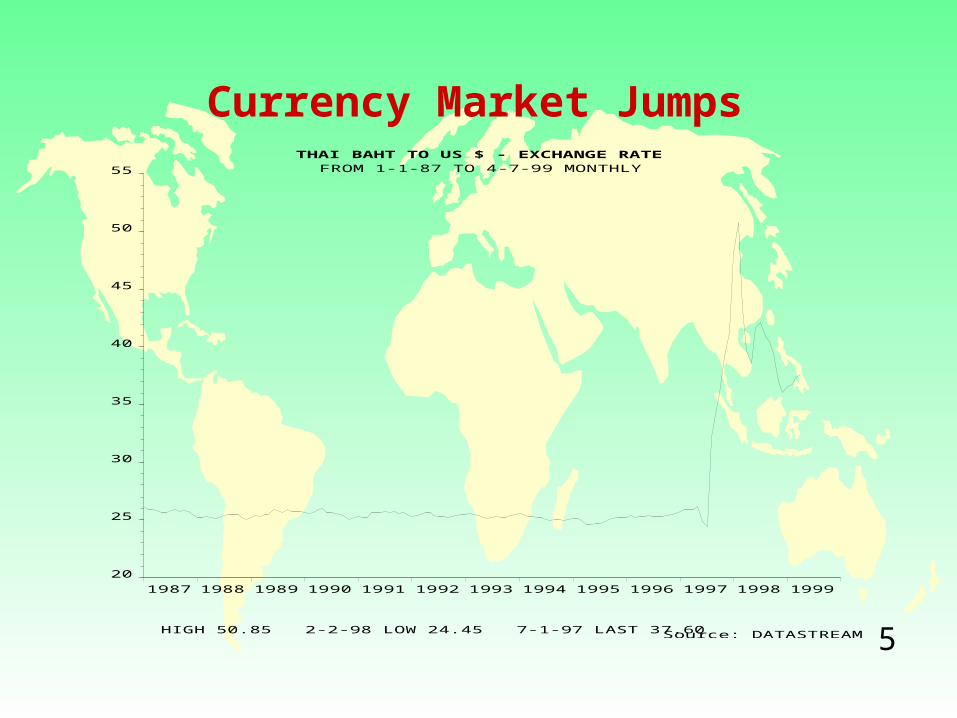

Currency Market Jumps

5

THAI BAHT TO US $ - EXCHANGE RATEFROM 1-1-87 TO 4-7-99 MONTHLY

1987 1988 1989 1990 1991 1992 1993 1994 1995 1996 1997 1998 199920

25

30

35

40

45

50

55

HIGH 50.85 2-2-98 LOW 24.45 7-1-97 LAST 37.60 Source: DATASTREAM

Currency Market ContagionFROM 1 -1 -97 TO 2 -2 -00 WEEKLY INDEXED

1997 1998 1999 200010

20

30

40

50

60

70

80

90

100

110

120

US $ TO INDONESIAN RUPIAH - EXCHANGE RATEUS $ TO THAI BAHT - EXCHANGE RATEUS $ TO SOUTH KOREAN WON - EXCHANGE RATESou rc e : DATASTREAM

Technical trading rules

Moving averages Buy and sell signals are usuallytriggered when a short-run moving average (SRMA) ofpast rates crosses a long-run moving average (LMRA).An LRMA will always lag an SRMA because it gives asmaller weight to recent movements of exchange ratesthan an SRMA does.

Filter methods generate buy signals when anexchange rate rises X percent (the filter) above its mostrecent trough, and sell signals when it falls X percentbelow the previous peak.

Momentum models determine the strength of acurrency by examining the change in velocity of currencymovements. If an exchange rate climbs at increasingspeed, a buy signal is issued.

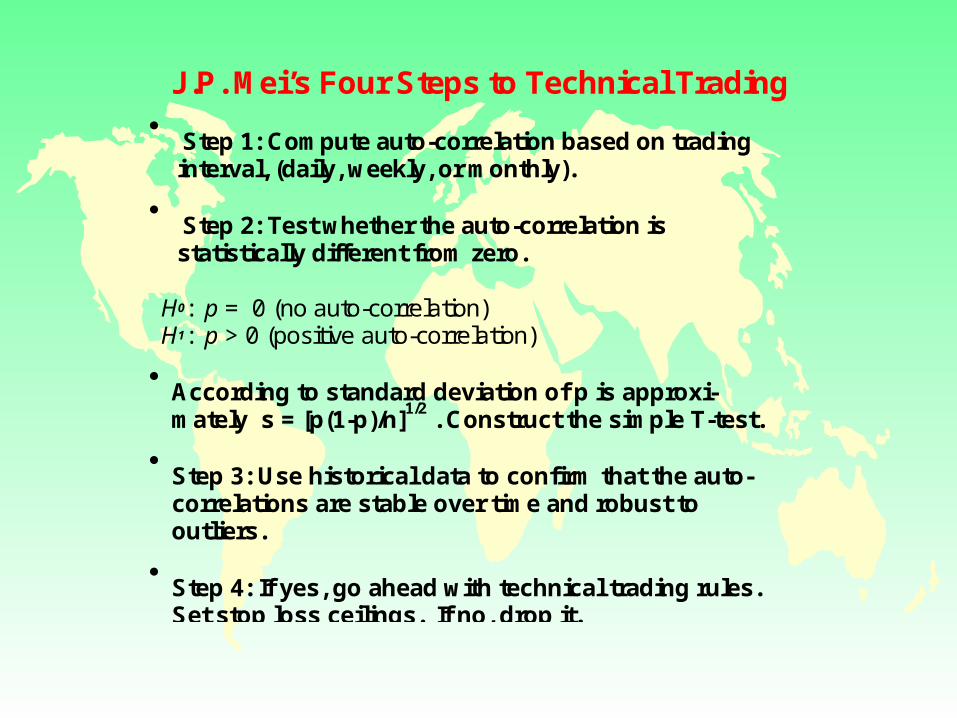

J.P. Mei’s Four Steps to Technical Trading

Step 1: Compute auto-correlation based on tradinginterval, (daily, weekly, or monthly).

Step 2: Test whether the auto-correlation isstatistically different from zero.

H0: p = 0 (no auto-correlation)H1: p > 0 (positive auto-correlation)

According to standard deviation of p is approxi-mately s = [p(1-p)/n]1/2 . Construct the simple T-test.

Step 3: Use historical data to confirm that the auto-correlations are stable over time and robust tooutliers.

Step 4: If yes, go ahead with technical trading rules.Set stop loss ceilings. If no, drop it.

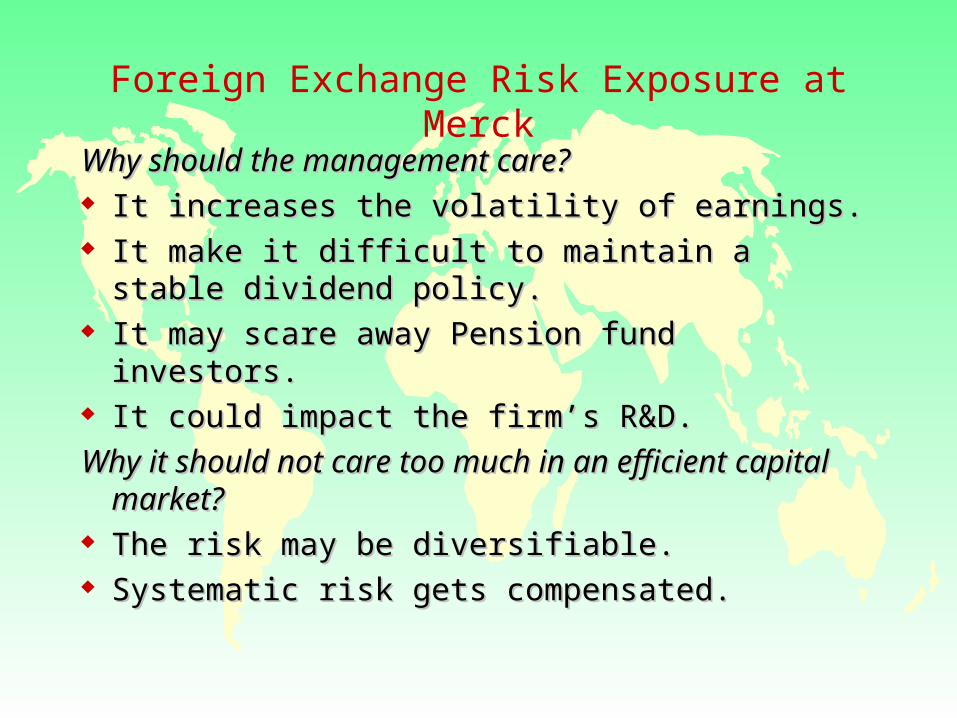

Foreign Exchange Risk Exposure at Merck

Why should the management care? Why should the management care? It increases the volatility of earnings.It increases the volatility of earnings. It make it difficult to maintain a stable It make it difficult to maintain a stable

dividend policy.dividend policy. It may scare away Pension fund investors. It may scare away Pension fund investors. It could impact the firm’s R&D.It could impact the firm’s R&D.

Why it should not care too much in an efficient Why it should not care too much in an efficient capital market?capital market?

The risk may be diversifiable.The risk may be diversifiable. Systematic risk gets compensated.Systematic risk gets compensated.

Foreign Exchange Risk Exposure at Merck

Translation and Transaction Translation and Transaction exposure:Changing the dollar value of net exposure:Changing the dollar value of net asset and expected transaction costasset and expected transaction cost

Future Revenue exposure: Changing the Future Revenue exposure: Changing the dollar value of future cash flowdollar value of future cash flow

Competitive Exposure: affect labor cost and Competitive Exposure: affect labor cost and pricing flexibilitypricing flexibility

How to measure the exposure from Merck’s How to measure the exposure from Merck’s point of view: Sales Indexpoint of view: Sales Index

Index = Index = q qj0j0*s*sjt jt qqj0j0 s sj0 j0

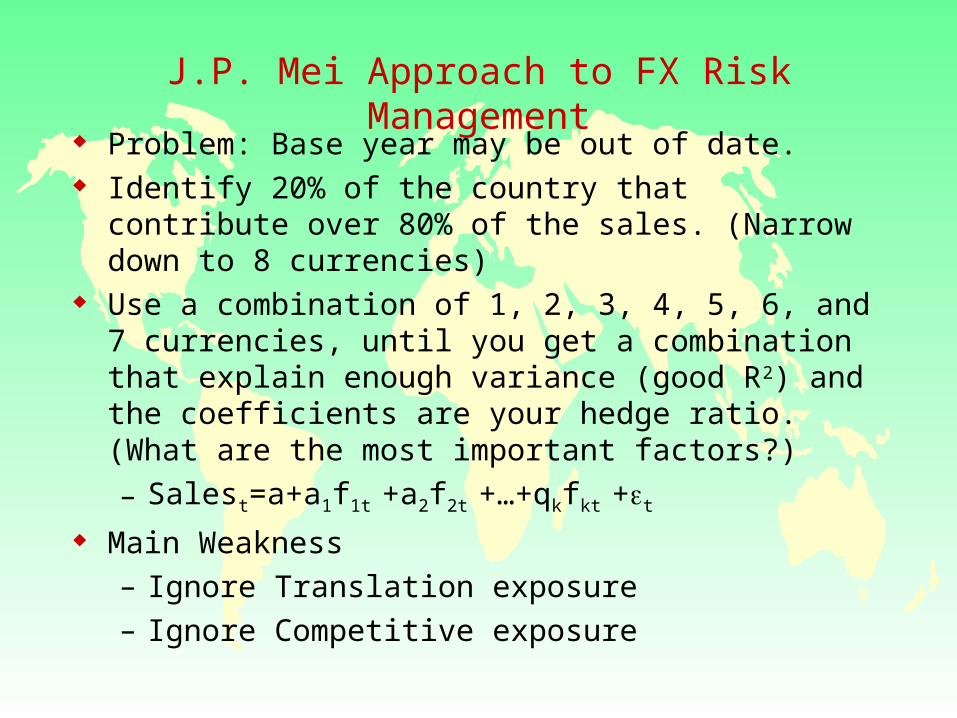

J.P. Mei Approach to FX Risk Management Problem: Base year may be out of date. Identify 20% of the country that contribute over 80% of

the sales. (Narrow down to 8 currencies) Use a combination of 1, 2, 3, 4, 5, 6, and 7 currencies,

until you get a combination that explain enough variance (good R2) and the coefficients are your hedge ratio. (What are the most important factors?)

– Salest=a+a1f1t +a2f2t +…+qkfkt +t

Main Weakness– Ignore Translation exposure– Ignore Competitive exposure

Highlights for Lecture 5

The presence of short-run positive serial correlation

form the basis for technical trading rules.

Currency market volatility could be under-estimated

due to sampling bias.

The presence of cross-correlation implies Market

Contagion, especially along regional blocks.

Diversification needs to be well balanced across

different regions.

Stability of auto-correlation is the key to the success

of technical trading rules.

Sales Index: Sales Index: Index = Index = q qj0j0*s*sjt jt qqj0j0 s sj0 j0

One need to update the sales index frequentlyOne need to update the sales index frequently. . One need to focus on the really important key One need to focus on the really important key

currencies.currencies.

The use of key currencies may take advantage of The use of key currencies may take advantage of

negative correlation as a result of long-short position in negative correlation as a result of long-short position in

different countries.different countries. Choice of hedging instruments: Forward or Spot Choice of hedging instruments: Forward or Spot

(Borrow and sell on the spot, invest the proceeds)(Borrow and sell on the spot, invest the proceeds)

Major determinant: credit risk.Major determinant: credit risk.

Top Related