Languages

Pages

Legal

1

EC7092: Investment Management

Suresh Mutuswami

October 30, 2011

Suresh Mutuswami EC7092: Investment Management

2

Outline

Bond markets

Bond Yields

Bond Pricing: Zero-coupon bonds, Coupon bonds

Price sensitivity: Duration and Convexity

The term structure of interest rates

Readings

BKM, Chapters 14 and 16 (up to 16.2 included).Other readings (optional)

BKM, Chapter 15.Nelson, C. and Siegel, A.F. (1987), Parsimonious Modeling ofYield Curves, Journal of Business, 60, 473-489.

Suresh Mutuswami EC7092: Investment Management

3

Bonds

Promised stream of future cash flows

fixed interest payments (“coupons”)fixed dates for coupon payments and repayment of principal

Failure to meet a coupon payment immediately puts the bondinto default

Issued by governments and companies

Example: UK government “gilts” can be

“short-dated” (less than 5 years)“medium-dated” (5 to 15 years)“long-dated” (more than 15 years)

Suresh Mutuswami EC7092: Investment Management

4

The Bond Family

Domestic bonds

issued on local market by domestic borrowerdenominated in local currencye.g. gilt issued in London by Bank of England

Foreign bonds

issued on local market by foreign borrowerdenominated in local currencye.g. sterling bond issued in London by US bank

Eurobonds

issued on international market denominated in a currency otherthan that of the country in which issuer is basede.g. sterling bond issued by US firm

Suresh Mutuswami EC7092: Investment Management

5

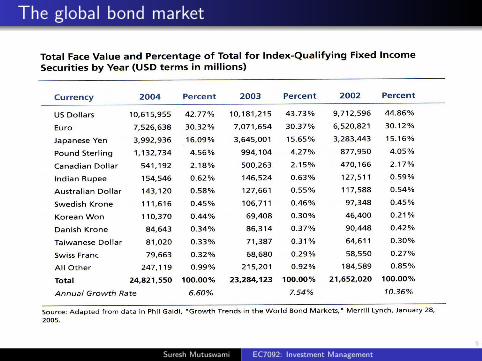

The global bond market

Suresh Mutuswami EC7092: Investment Management

6

The global bond market

Suresh Mutuswami EC7092: Investment Management

7

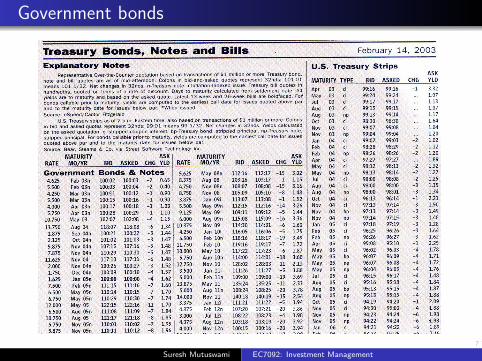

Government bonds

Suresh Mutuswami EC7092: Investment Management

8

Corporate bonds

Suresh Mutuswami EC7092: Investment Management

9

Participating investors and bond ratings

Bond ratings are provided by three major agencies (FitchInvestor Services, Moody’s and Standard and Poor’s).

Bond ratings is important in order to assess the probability ofdefault of a specific issuer (public or private).

Can the issuer service its debt in a timely manner over the lifeof a bond?

Ratings have impact on bonds marketability and effectiveinterest rates (risk premia).

Ratings are provided in letter format ranging from AAA to D(notations may change from agency to agency).

Suresh Mutuswami EC7092: Investment Management

10

Bond pricing

How do we price a bond? We rely on a present-value model.

We have to discount expected cash flows (coupon paymentsand principal) by an appropriate discount rate (r). Therefore:

Bond Value = Present value of coupons +

Present value of par value

Or,

BV =T∑t=1

Ct

(1 + r)t+

Par Value

(1 + r)T

Note that there is only one interest rate (r) appropriate todiscount cash flows. Different in practice.

Suresh Mutuswami EC7092: Investment Management

11

Bond pricing

Suppose we have a 30-year maturity bond with par value$1,000 paying 60 semi-annual coupon payments of $40 each.Annual interest rate (discount rate) is 8% (=4% every sixmonths).

We have

BV =60∑t=1

40

(1 + 0.04)t+

1000

(1 + 0.04)60= 904.94+95.06 = $1000

What about if the annual discount rate increases to 10%?

Suresh Mutuswami EC7092: Investment Management

12

Price-yield curve

Suresh Mutuswami EC7092: Investment Management

13

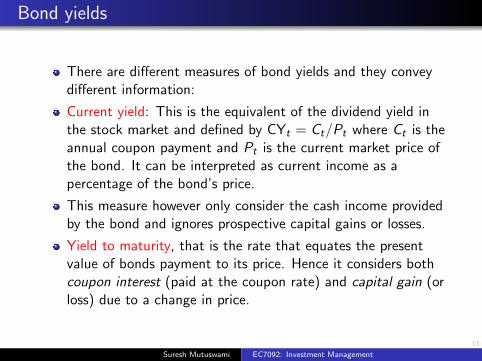

Bond yields

There are different measures of bond yields and they conveydifferent information:

Current yield: This is the equivalent of the dividend yield inthe stock market and defined by CYt = Ct/Pt where Ct is theannual coupon payment and Pt is the current market price ofthe bond. It can be interpreted as current income as apercentage of the bond’s price.

This measure however only consider the cash income providedby the bond and ignores prospective capital gains or losses.

Yield to maturity, that is the rate that equates the presentvalue of bonds payment to its price. Hence it considers bothcoupon interest (paid at the coupon rate) and capital gain (orloss) due to a change in price.

Suresh Mutuswami EC7092: Investment Management

14

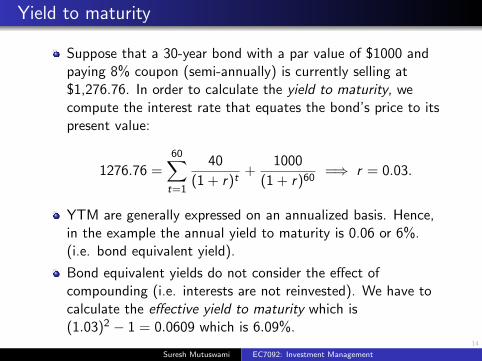

Yield to maturity

Suppose that a 30-year bond with a par value of $1000 andpaying 8% coupon (semi-annually) is currently selling at$1,276.76. In order to calculate the yield to maturity, wecompute the interest rate that equates the bond’s price to itspresent value:

1276.76 =60∑t=1

40

(1 + r)t+

1000

(1 + r)60=⇒ r = 0.03.

YTM are generally expressed on an annualized basis. Hence,in the example the annual yield to maturity is 0.06 or 6%.(i.e. bond equivalent yield).

Bond equivalent yields do not consider the effect ofcompounding (i.e. interests are not reinvested). We have tocalculate the effective yield to maturity which is(1.03)2 − 1 = 0.0609 which is 6.09%.

Suresh Mutuswami EC7092: Investment Management

15

Realized yields

Yields to maturity are rate of returns obtained over the fulllife of the bond if all coupons are reinvested at bond’s yield tomaturity.

What about if the bond is sold prior to its maturity?What about if the reinvestment rate is different from thebond’s yield to maturity?

The correct measure to employ in this case is the realizedyield:

yrealized =

[end-of-period wealth

initial wealth

] 1T

− 1

Consider a 2-year bond selling at par value ($1,000) paying anannual coupon of 10%. (The yield to maturity is in this casealso equal to 10%).

What if the reinvestment rate is equal to 8% at the end of thefirst year?

Suresh Mutuswami EC7092: Investment Management

16

Realized yields

In the first case,[1210

1000

]1/2− 1 = 0.10

In the second case,[1208

1000

]1/2− 1 = 0.099

Suresh Mutuswami EC7092: Investment Management

17

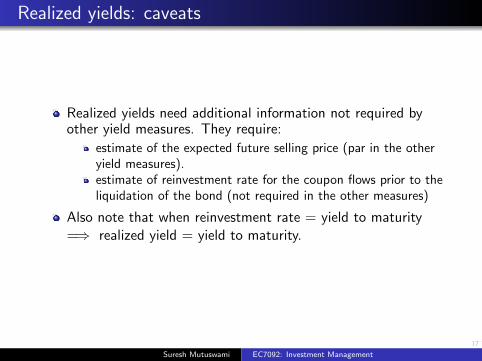

Realized yields: caveats

Realized yields need additional information not required byother yield measures. They require:

estimate of the expected future selling price (par in the otheryield measures).estimate of reinvestment rate for the coupon flows prior to theliquidation of the bond (not required in the other measures)

Also note that when reinvestment rate = yield to maturity=⇒ realized yield = yield to maturity.

Suresh Mutuswami EC7092: Investment Management

18

Price sensitivity

Return on a bond has two components:

coupon interest (paid at the coupon rate),capital gain (or loss) due to a change in price

Price of a bond changes with

time.unexpected changes in interest rates.

Suresh Mutuswami EC7092: Investment Management

19

Price sensitivity

Suresh Mutuswami EC7092: Investment Management

20

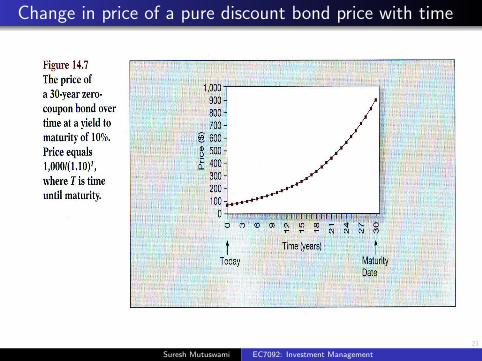

Change in bond price with time

Example: pure discount bond or zero-coupon bond (=a bondthat does not pay coupons) with 3 years to maturity (assumediscount rate r = 10% constant over the 3 years).

How does price vary with time to maturity (TTM)?

t = 0 t = 1 t = 2 t = 3TTM = 3 TTM = 2 TTM = 1 TTM = 0

P =100

(1 + 0.1)3P =

100

(1 + 0.1)2P =

100

(1 + 0.1)1P =

100

(1 + 0.1)0

= 75.13 = 82.64 = 90.91 = 100

Suresh Mutuswami EC7092: Investment Management

21

Change in price of a pure discount bond price with time

Suresh Mutuswami EC7092: Investment Management

22

Change in price of a pure discount bond price with time

Note that for premium bonds the coupon rate is greater thanthe market rate while the opposite is true for discount bonds.

Suresh Mutuswami EC7092: Investment Management

23

Change in price due to unexpected change in interest rates

Consider the same discount bond as before and imagine thatthe interest rate rises from 10% to 11%.

t = 0 t = 1 t = 2 t = 3

TTM = 3 TTM = 2 TTM = 1 TTM = 0

r = 0.1 75.13 82.64 90.91 100

r = 0.11 73.12 81.16 90.09 100

∆P −2.01 −1.48 −1.02 0

Suresh Mutuswami EC7092: Investment Management

24

Interest rate sensitivity

We have seen that

interest rates are inversely correlated with bond prices,interest rates fluctuate over time.

Interest rates rises and falls imply bond capital losses andgains. Even bonds are risky investments!

Bond prices sensitivity to interest rate changes is of greatconcern to investors.

Suresh Mutuswami EC7092: Investment Management

25

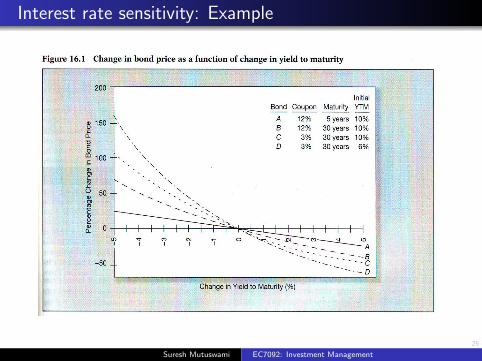

Interest rate sensitivity: Example

Suresh Mutuswami EC7092: Investment Management

26

Interest rate sensitivity: Example

What can we learn from this example?

Long-term bonds are more sensitive to interest rate changes (Avs. B).Interest rate risk is less than proportional to bonds maturity (Avs. B).Interest rate risk is inversely related to bonds coupon rate (Bvs. C).Bond price sensitivity is inversely related to the yield tomaturity at which the bond is currently selling (C vs. D).Yield to maturity rises and falls impact differently on bondprice changes (more “falls” than “rises”).Bond prices and yields are inversely correlated.

Suresh Mutuswami EC7092: Investment Management

27

Interest rate sensitivity (continued)

Bond maturity is crucial to define the impact of interest ratechanges on bond prices (i.e. B vs. C)

However it is not enough . . .

Suresh Mutuswami EC7092: Investment Management

28

Duration

What definition of maturity we should use?

Effective maturity = average maturity of coupon bondspromised cash flows.

Effective maturity is generally called bond’s duration

that is, the weighted average of the times to each coupon orprincipal payment made by the bond, where the weight is thepresent value of the payment divided by the bond price.

Suresh Mutuswami EC7092: Investment Management

29

Duration

Duration

D =T∑t=1

t × wt , wt =1

P

CFt

(1 + y)t

Duration of coupon-paying bond

weighted sum of maturities of pure discount bonds,weights are equal to the proportion of the bond pricerepresented by the present value of the individual coupons,maturities of the pure discount bonds are equal to the couponmaturities.

Suresh Mutuswami EC7092: Investment Management

30

Factors affecting duration

Size of coupon, C

the larger the coupon, the more important are the intermediatecash-flows relative to the cash-flow at maturity.hence . . . duration decreases if coupon increases.

Maturity, T

the longer the maturity, the further in the future the face valueis re-paid.hence . . . duration increases with maturity

Interest rate, y

the higher the rate at which future cash-flows are discounted,the less important are distant cash-flowshence . . . duration decreases if the interest rate rises.

Duration of a zero-coupon bond = time to maturity

Suresh Mutuswami EC7092: Investment Management

31

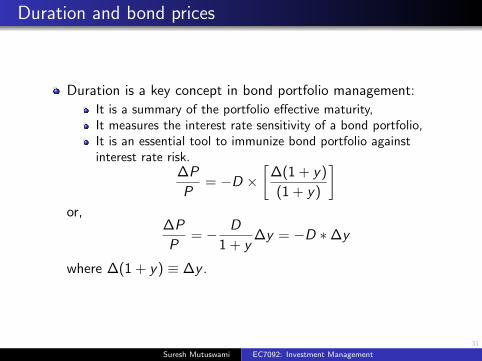

Duration and bond prices

Duration is a key concept in bond portfolio management:

It is a summary of the portfolio effective maturity,It measures the interest rate sensitivity of a bond portfolio,It is an essential tool to immunize bond portfolio againstinterest rate risk.

∆P

P= −D ×

[∆(1 + y)

(1 + y)

]or,

∆P

P= − D

1 + y∆y = −D ∗∆y

where ∆(1 + y) ≡ ∆y .

Suresh Mutuswami EC7092: Investment Management

32

Duration: Example

Consider a 2-year maturity, 8% coupon bond makingsemiannual payments (4% semiannually); selling atP = $964.54 for a yield to maturity (i.e. discount rate) of10% (5% semiannually).

Years CFtCFt

(1 + y)tw =

1

P

CFt

(1 + y)tw × t

0.5 40 38.09 0.039 0.0195

1.0 40 36.25 0.038 0.038

1.5 40 34.55 0.036 0.054

2.0 1040 855.61 0.887 1.774

Hence, the duration is 1.885 years.

Since∆P

P= − D

1 + y∆y = −D ∗∆y

we have ∆P = −1.714×∆y .

Suresh Mutuswami EC7092: Investment Management

33

Convexity

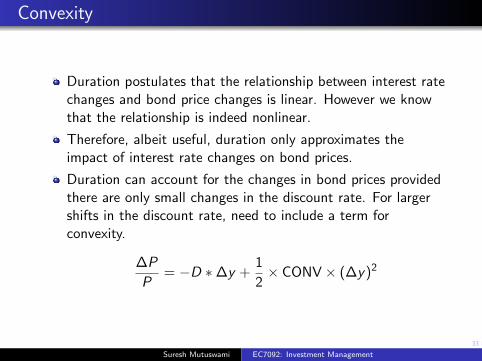

Duration postulates that the relationship between interest ratechanges and bond price changes is linear. However we knowthat the relationship is indeed nonlinear.

Therefore, albeit useful, duration only approximates theimpact of interest rate changes on bond prices.

Duration can account for the changes in bond prices providedthere are only small changes in the discount rate. For largershifts in the discount rate, need to include a term forconvexity.

∆P

P= −D ∗∆y +

1

2× CONV× (∆y)2

Suresh Mutuswami EC7092: Investment Management

34

Convexity (continued)

Suresh Mutuswami EC7092: Investment Management

35

Convexity (continued)

Suresh Mutuswami EC7092: Investment Management

36

Do investors like convexity?

Convexity is a desirablecharacteristic of a bond.

Large convexity implies:

larger gains when interestrates fall,smaller losses wheninterest rates rise.

Convexity comes at a cost.Investors have to acceptlower yields or pay more tohave bonds with greaterconvexity.

Suresh Mutuswami EC7092: Investment Management

37

Passive bond management

Passive bond management takes bond prices as given andseek to control only the risk of the fixed-income portfolio.

Interest rates changes constitute the major source of risk tobond portfolios.

Two techniques for protecting the value of a fixed-incomeportfolio against changes in interest rates:

Indexing, a technique that attempts to replicate theperformance of a given bond index (similar to stock marketindexation).Immunization, which eliminates the sensitivity of a bondportfolio to changes in interest rates by offsetting price riskagainst re-investment risk (matching portfolios duration withliabilities duration).

Suresh Mutuswami EC7092: Investment Management

38

Yield curve

The assumption of a single discount rate is restrictive.

In general yields are different at different maturities and, forthe same maturities, over different periods of time.

Yields to maturity have been obtained under the assumptionsthat:

bonds are held until maturity.cash flows are reinvested at the computed yield to maturity.

The second assumption is in contrast with the evidence thatrates change over time and across maturities.

Investors at any point in time require a different rate of returnfor flows at different times (e.g. returns required are differentif zero-coupon bonds are offered at 2, 5 or 10 years maturity).

The rate of return used to discount flows at a certain maturityis called spot rate (or short rate).

Suresh Mutuswami EC7092: Investment Management

39

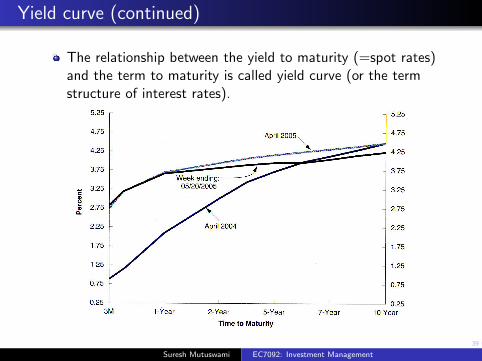

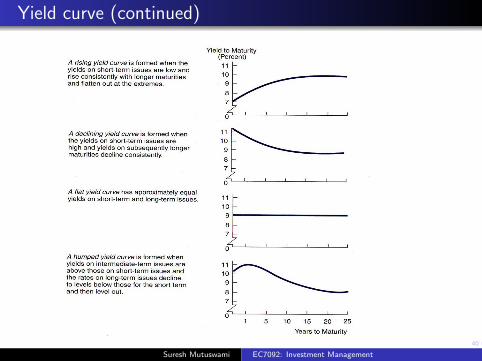

Yield curve (continued)

The relationship between the yield to maturity (=spot rates)and the term to maturity is called yield curve (or the termstructure of interest rates).

Suresh Mutuswami EC7092: Investment Management

40

Yield curve (continued)

Suresh Mutuswami EC7092: Investment Management

41

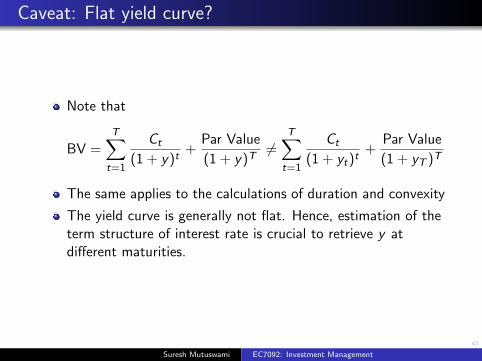

Caveat: Flat yield curve?

Note that

BV =T∑t=1

Ct

(1 + y)t+

Par Value

(1 + y)T6=

T∑t=1

Ct

(1 + yt)t+

Par Value

(1 + yT )T

The same applies to the calculations of duration and convexity

The yield curve is generally not flat. Hence, estimation of theterm structure of interest rate is crucial to retrieve y atdifferent maturities.

Suresh Mutuswami EC7092: Investment Management

42

Interpreting the yield curve

Suresh Mutuswami EC7092: Investment Management

43

What factors change the yield curve?

Underlying macroeconomic forces drive movements of theyield curve.

When macroeconomic variables are now generallyincorporated into yield curve models we find that:

Inflation is highly correlated with the level of the yield curve,real activity (GDP) is related to the slope of the yield curve.Inflation and real activity are likely to determine the shifts inthe yield curve.Monetary policy shocks affect the slope of the yield curve,GDP shocks affect the curvature of the yield curve whileinflation shocks affect the level of the yield curve.

Suresh Mutuswami EC7092: Investment Management

Top Related