Languages

Pages

Legal

PROJECT REPORT

ON

“DYNAMICS OF INSURANCE AGENCY DEVELOPMENT”

At

(Submitted in Partial Fulfillment for the Award of Degree

Master of Business Administration)

(M.B.A)

Submitted by: -

Sandeep Sharma

Institute Of Management Studies

(Kurukshetra University, Kurukshetra)

Acknowledgements

I express my sincere gratitude to ICICI Prudential Life Insurance and its entire

staff for giving me this wonderful opportunity to work and get to know more about

the Insurance industry and Insurance Agency Development.

With deep sense of gratitude I express my indebtedness to my mentor and guide

Mr. Satnam Singh (UM), ICICI Prudential Life Insurance, Panipat. He has

been a great source of inspiration. I thank him for his keen interest and valuable

guidance. He was also kind to discuss the problems faced during the course of

this project.

I take this opportunity to thank Mr. Satnam Singh, (UM) who gave me this

opportunity to do my project at this Organization.

(Sandeep Sharma)

S.No Particulars

1. Acknowledgement

2. Executive Summary

3. Project Objective

4. Introduction

5. Introduction to Study Undertaken

6. Statement of objective

7. Research Methodology

8. Analysis And Interpretation

9. Conclusion & Finding

10. Recommendation

11. Limitation

12. Annexure

13. Bibliography

EXECUTIVE SUMMARY

ICICI Prudential Life Insurance co. ltd is the #1 private life insurers in the world.

The project was undertaken to study the dynamics of insurance agency

development and need of life insurance in human life. The study of ICICI

Prudential life group is undertaken to understand the services provided by ICICI

Prudential to their customers as well as the insurance advisors recruitment

process adopted by ICICI Prudential Life Insurance Company.

The project was studied to know how ICICI Prudential life is promoting

their insurance advisors in the field helping them to bring more and more

business by the means of handsome commission structure, renewal

commissions, rewards, trophies and certificate, honoring them in front of other

insurance advisors. ICICI Prudential also provides other future prospects to their

advisors. This all not only increases the efficiency of the winners but also of

those who have under performed. Through this process ICICI Prudential also win

customers by strong commitment to life insurance advisors.

INTRODUCTION TO INSURANCE INDUSTRY

Insurance is the outcome of man's search for security and for finding out ways

and means of ameliorating the evil consequence of sudden calamities.

Insurance is a co-operative venture whereby risks and many shares lose.

The modern setup of industrialization has rendered man and his property most

vunerable to different types of risks and uncertainties. Death, unemployment and

sickness are constantly staring the face of man and also his properties are

exposed to risks, which may arise, from fire, water, accident, wind-storm, earth

quakes and floods etc.

The total annual losses to humanity from untimely death and to businessman

from risks are too much to be calculated. Thus, arise the need of insurance in a

planned way whereby the above risks are minimized as explained above with the

growth of industrialization and rapid increase in the number of situations in which

the human life and property get exposed to risks. Thus, the effective solution of

reducing the burden of these risks has been devised by shifting these risks to

agencies or persons calling to share them are known as insurance.

Insurance is a 4 billion business in India and yet its spread in the country is

relatively thin. Insurance as a concept has not been able to make headway in

India. Presently LIC enjoys a monopoly in life insurance business while GIC

enjoys it in general insurance business. There have been very little option before

the consumer to decide the insurer. A successful or IRA BILL has cleared the

way of private operators in collaboration with their overseas partner. It is likely to

bring in a more professional and focused approach. Moreover the foreign players

would bring sophisticated techniques with then. It is very important that trained

professional who are able to communicate specific features of the policy should

sell the policy.

Definition General Definition

In the words of John Magee, "Insurance is a plan by which large number of

people associated themselves and transfer to the shareholders of all, risk that

attach to individuals."

Fundamental Definition:

In the words of D.S. Hansell, "Insurance may be defined as a social devices

providing financial compensation for the efforts of misfortune, the payment being

made from the accumulated contributions of all parties participating in the

scheme."

Characteristics of Insurance

Sharing of risks

Cooperative devices

Evaluation of risks

Payment on happening of a special event

The amount of payment depends on the nature of losses incurred

Opening Up Of Insurance Sector

Indian History: Time to turn the clock back-and open up insurance

For two years, around 30 foreign insurance have eagerly explored the

nationalized Indian Insurance market, preparing to leap in when private

participation is allowed. But it seems that they have an endless wait before the

sector is opened up. That's ironical: in 1947, many of these insurance were firmly

established here. BAT subsidiary eagle star, for example, opened offices in

Calcutta in 1894. By 1921, it was doing business with Brooke Bond and Birlas.

Prudential first Asia office was opened in India in 1923. Fifty years ago, India has

busting, if somewhat chaotic, entirely private insurance industry. The year after

independence, 209 life insurance companies were doing business worth Rs.

712.76 crores.

General insurance had its turn in 1972, when 107 insurers were amalgamated

into four companies headquartered in the four metros, with GIC as a holding

company. Nationalization has brought some benefits. Today 48% of LIC new

business is rural. Net premium in general insurance grew from Rs. 222 crores

in1973 to Rs. 5,956 crores in 1995-1996.

Marketplace in 21st Century

An in depth analysis of demographic factor that will effect the life health

insurance industry in the next century, has uncovered trends that show

increasing diversity that adds to challenges and opportunities. Coning &

Company, which did the study, said that success in the marketing of products

would come to those insurers that become creative in capturing a wider range of

customers by using multiple distribution channels. The diversity uncovered by the

coming study includes the aging population, increasing household income

inequality and social fragmentation.

Challenges/opportunities

The study, "21st century demographic for the life health industry, "delineates the

following and opportunities:

Population around the world is aging; number of people in his old age is growing

continuously. As the population ages products such as annuities, IRAS and

defined contribution retirement plans have enormous growth potential.

The changing composition of households from traditional family units to single

households also presents untapped market with real needs of life health and

retirement products. Growing income inequality means that insurance should find

ways to markets their services cost-effectively to all economic sector, particularly

middle class. Insurance must recognize that small business now make up a

growing portion of the world economy, presenting a huge opportunity for growth

in this market.

Governments Role

Governments are keen to reduce the dependency on the state via private

pension provision. They have a choice between using compulsion and

incentives. Most of the governments choose the latter method. Tax relief is

granted to the pensions plans and is extremely generous, reflecting the value

that the govt. and the society at a large place on the provision or retirement

benefit. Tax treatment of the benefit varies by countries. In India, the proceeds of

the gratuity and provident fund are tax free in the hands as tax free lump sum

and remainder as taxable income. Benefit due on withdrawal from schemes are

generally taxed unless they are transferred to another scheme.

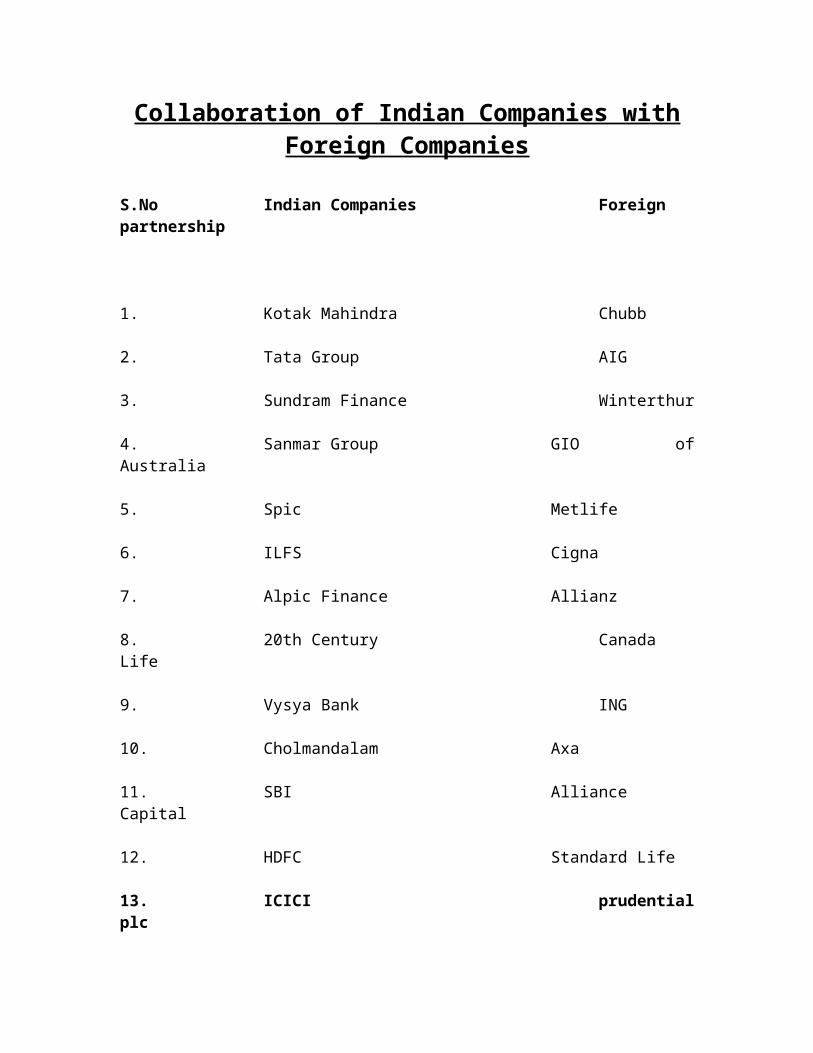

Collaboration of Indian Companies with Foreign Companies

S.No Indian Companies Foreign partnership

1. Kotak Mahindra Chubb

2. Tata Group AIG

3. Sundram Finance Winterthur

4. Sanmar Group GIO of Australia

5. Spic Metlife

6. ILFS Cigna

7. Alpic Finance Allianz

8. 20th Century Canada Life

9. Vysya Bank ING

10. Cholmandalam Axa

11. SBI Alliance Capital

12. HDFC Standard Life

13. ICICI prudential plc

14. Hindustan Times Commercial union

15. IDBI Principal

16. Max India New Yark Life

PRODUCT PORTFOLIO

PHILISOPHY

To provide protection to individuals at various life stages:

Young individuals, Married Couples with Children's, Matured Couples.

To provide solutions in various categories….

Life Insurance

Health Protection

Whole-Life Plans

Child Solutions

Retirement Planning

INTRODUCTION TO ICICI PRUDENTIAL LIFE CO. LTD.

ICICI Prudential Life Insurance Company is a joint venture between ICICI Bank,

a premier financial powerhouse and Prudential Plc, a leading international

financial services group headquartered in the United Kingdom. ICICI Prudential

was amongst the first private sector insurance companies to begin operations in

December 2000 after receiving approval from Insurance Regulatory

Development Authority (IRDA). ICICI Bank has 74% stake in the company, and

Prudential plc has 26%.

ICICI and Prudential came together in 1993 to form Prudential ICICI Asset

Management Company, which has today emerged as one of the leading mutual

funds in India. The two companies bring together two of the strongest financial

service brands in Asia, known for their professionalism, excellent quality of

service and long term commitment to YOU. Riding on the success of this

relationship, the two companies joined hands once more in 2000, to form ICICI

Prudential Life Insurance, with a commitment to provide leading-edge life

insurance solutions.

ICICI Prudential has recruited and trained over 60,000 insurance advisors to

interface with and advise customers. Further, it leverages its state-of-the-art IT

infrastructure to provide superior quality of service to customers.

The company has network with 12 bancassurance tie-ups, having agreements

with ICICI Bank, as well as some corporate agents. It has also tied up with

organisations like Dhan for distribution of Salaam Zindagi, a policy for the

socially and economically underprivileged sections of society.

Today the company is the No.1 private life insurer in the country.

COMPANY VISION

To be the dominant

Life and pension player

Built on trust by the world class people

And services

COMPANY VALUES

1. Integrity

Walk the talk: live the values

Stand up honestly and fearlessly for what I truly care about

Customer first

Own the customer: deliver the promise

Listen actively, stretch continually to add values to customers and

channel partners

2. Boundary less

Never say “it’s my job” go beyond the call of duty

Experiment –believe anything is possible

3. Ownership

Own mistake. Learn from failure

Confront hard facts, pursue goals relentlessly

4. Passion

Winning instincts-transmit boundless energy and enthusiasm to

drive results

Demonstrate speed for competitive advantage

Progress so far… No. 1 private life insurer in the country

Equity based stands at Rs. 925 crore

The company issued nearly 4,50,000 policies in a year, taking a

total policy to cover 7,80,000

Total sum assured since inception has risen to16,000 crore

The company’s total income received premium income in FY04

was Rs. 989 crore, up 135% from last year

ICICI Prudential has emerged as the leading private life insurer,

closing the year 31, 2004 with retail market share amongst

private life insurer of36%

Over 60,000 insurance advisors

Over 150 years of experience in life insurance business

Leading international financial services company in UK

Around US $276 Billions funds under management, and more

than 16,000,000 customers worldwide

Market share of 23% in the total pension market between all life

insurer and 725-market share among private insurer

Largest distribution network among private players

67 branches across 45 locations

PROFILE

COMPANY NAME: ICICI PRUDENTIAL LIFE INSURANCE CO. LTD.

INDIAN PARTNER: ICICI BANK

FORIGN PARTNER: PRUDENTIAL PLC

EQUITY RATIO: 74:26

COMMENCEMENT OF OPERATION: 19TH DECEMBER 2000

FIELD OF OPERATION: LIFE

HOME ADDRESS: ICICI PRUDENTIAL LIFE INSURANCE COMPANY

ICICI PRULIFE TOWERS, 1089, Appasaheb Marathe Marg, Prabhadevi,

MUMBAI- 400025

CEO OF THE COMPANY: Ms. SHIKHA SHARMA

MANAGEMENT: Board of Directors

Mr. K.V. Kamath, Chairman

Mr. Mark Norbom

Mrs. Lalita D. Gupte

Mrs. Kalpana Morparia

Mrs. Chanda Kochhar

Mr. Kevin Holmgren

Mr. M.P. Modi

Mr. R Narayanan

Ms. Shikha Sharma, Managing Director

Management Team

Ms. Shikha Sharma, Managing Director

Mr. Sandeep Batra, Chief Financial Officer & Company Secretary

Mr. Shubhro J. Mitra, Chief - Human Resources

Mr. Puneet Nanda, Head - Investments

Ms. Anita Pai, Chief - Operations & Underwriting

Mr. V. Rajagopalan, Appointed Actuary

Mr. Shridhar Sethuram, Chief - Sales & Marketing

Mr. Anil Tikoo, Head - Information Technology

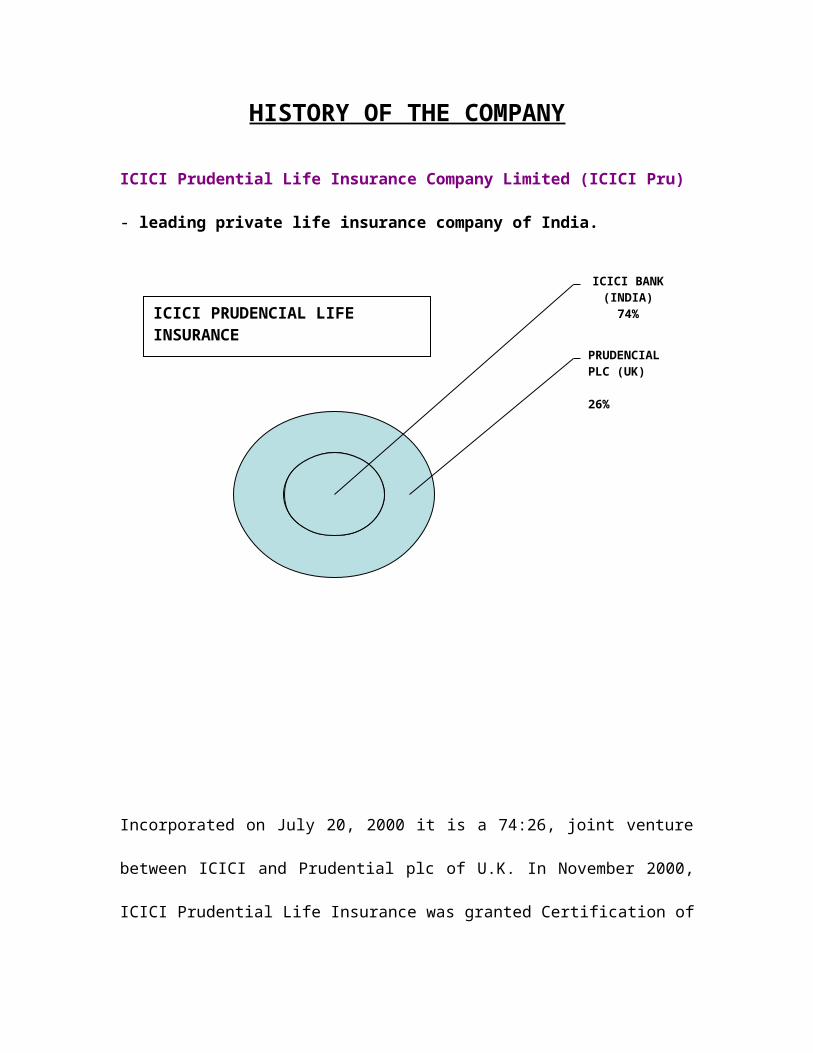

HISTORY OF THE COMPANY

ICICI Prudential Life Insurance Company Limited (ICICI Pru)

- leading private life insurance company of India.

Incorporated on July 20, 2000 it is a 74:26, joint venture between ICICI and

Prudential plc of U.K. In November 2000, ICICI Prudential Life Insurance was

granted Certification of Registration for carrying out life insurance business by

the Insurance Regulatory & Development Authority of India. The Company

issued its first policy on December 12, 2000.

PRUDENCIAL PLC (UK) 26%

ICICI BANK (INDIA)

74%ICICI PRUDENCIAL LIFE INSURANCE

Year of review 2003-2004:

ICICI Prudential has consolidated its position as the leading private life insurer in

India. ICICI Prudential's annualized premium grew more than three fold over the

previous year.

Continuing with its 'Customer First' philosophy, ICICI Prudential has significantly

expanded its presence to 29 operational Branches (2001-2002: 16), with the

Advisor.

Force growing to over 18,000. Its has also strengthened its Alternate Distribution

channels, i.e. Banc assurance, Corporate Agents and Direct Marketing, making

purchase of insurance more accessible. Banc assurance and Direct Marketing

channels have contributed to over 18% of the Annualized Premium.

ICICI Prudential was amongst the first to identify the emerging opportunity in the

Pension segment and launched two linked pension products- Lifetime Pension

and Life Link Pension, which have been well received in the market

BANCASSURANCE PARTNERS: ICICI Bank, Federal Bank, Bank of India, South Indian Bank, Lord Krishna

Bank, Goa State Co-operative Bank, Indoor Paraspar Sahakari Bank,

Manipal State Co-operative Bank, Jalgaon People's Co-operative Bank,

Shamrao Vithal Co-operative Bank, Punjab & Maharashtra Co-operative

Bank.

ABOUT JOINT VENTURE PARTNERS:

ICICI BANK ICICI Bank (NYSE:IBN) is India's second-largest bank with total assets of about

Rs.125,229 crore and a network of over 450 branches and offices and about

1790 ATMs. ICICI Bank offers a wide range of banking products and financial

services to corporate and retail customers through a variety of delivery channels

and through its specialised subsidiaries and affiliates in the areas of investment

banking, life and non-life insurance, venture capital and asset management.

ICICI Bank is the only Indian company to be rated above the country rating by

the international rating agency Moody's and the only Indian company to be

awarded an investment grade international credit rating. The Bank enjoys the

highest AAA (or equivalent) rating from all leading Indian rating agencies.

ICICI Bank was originally promoted in 1994 by ICICI Limited, an Indian financial

institution and was its wholly owned subsidiary. ICICI's shareholding in ICICI

Bank was reduced to 46% through a public offering of shares in India in fiscal

1998, an equity offering in the form of ADRs listed on the NYSE in fiscal 2000,

ICICI was formed in 1955 at the initiative of the World Bank, the Government of

India and representatives of Indian industry. The principal objective was to

create a development financial institution for providing medium-term and long

-term project financing to Indian businesses. In the 1990s, ICICI transformed its

business from a development financial institution offering only project finance to

a diversified financial services group offering a wide variety of products and

services, both directly and through a number of subsidiaries and affiliates like

ICICI Bank. In 1999, ICICI become the first Indian company and the first bank or

financial institution from non-Japan Asia to be listed on the NYSE.

In October 2001, the Boards of Directors of ICICI and ICICI Bank approved the

merger of ICICI and two of its wholly owned retail finance subsidiaries, ICICI

Personal Financial Services Limited and ICICI Capital Services Limited, with

ICICI Bank. The merger was approved by shareholders of ICICI and ICICI Bank

in January 2002, by the High Court of Gujarat at Ahmedabad in March 2002,

and by the High Court of Judicature at Mumbai and the Reserve Bank of India in

April 2002. Consequent to the merger, the ICICI group's financing and banking

operations, both wholesale and retail, have been integrated in a single equity.

EQUITY SHAREHOLDINGS

ICICI Bank's equity shares are listed in India on stock exchanges at Kolkata and

Vadodara, the Stock Exchange, Mumbai and the National Stock Exchange of

India Limited and its American Depositary Receipts (ADRs) are listed on the

New York Stock Exchange (NYSE).

Prudential plc Established in 1848, Prudential plc is a leading international financial services

company in the UK, with around US$250 billion funds under management, and

more than 16 million customers worldwide. Prudential has championed

customer-centric products and services, supported by over 60,000 staff and

agents across the region

Prudential has brought to market an integrated range of financial services

products that now includes life assurance, pensions, mutual funds, banking,

investment management and general insurance.

M&G was acquired by Prudential in 1999 and is the Group's UK and European

fund manager, responsible for managing over £112 billion of funds (as at

31 March 2004).

Launched by Prudential in 1998, Egg is an innovative financial services

company, with over 2.5 million customers with a market share of nearly 5% of

UK credit card balances.

In Asia, Prudential is UK's largest life insurance company with a vast network of

23 life & fund management operations in 12 countries serving 4 million

customers- China, Hong Kong, India, Japan, Indonesia, Korea, Malaysia, the

Philippines, Singapore, Taiwan, Thailand & Vietnam.

In the US, Prudential owns Jackson National Life, a leading life ins. company &

has more than 1.5 million policies and contracts in force.

Commitment & Aim

According to them- our commitment to the shareholders who own Prudential is to

maximise the value over time of their investment. We do this by investing for the

long term to develop and bring out the best in our people and our businesses to

produce superior products and services, and hence superior financial returns.

Our aim is to deliver top quartile performance among our international peer

group in terms of total shareholder returns.

At Prudential our aim is lasting relationships with our customers and

policyholders, through products and services that offer value for money and

security. We also seek to enhance our Company's reputation, built over 150

years, for integrity and for acting responsibly within society.

DISTRIBUTION

ICICI Prudential has one of the largest distribution networks amongst private life

insurers in India, having commenced operations in 74 cities and towns in India.

These are: Agra, Ahmedabad, Ajmer, Allahabad, Amritsar, Anand, Aurangabad,

Bangalore, Bareilly, Bharuch, Bhatinda, Bhopal, Bhubhaneshwar, Calicut,

Chandigarh, Chennai, Coimbatore, Dehradun, Durgapur, Faridabad, Goa,

Guntur, Guwhati, Gurgaon, Gwalior, Hyderabad, Hubli, Indore, Jaipur, Jalandhar,

Jamnagar, Jamshedpur, Jodhpur, Kanpur, Karnal, Kochi, Kolkata, Kolhapur,

Kota, Kottayam, Kozhikode, Lucknow, Ludhiana, Madurai, Mangalore, Meerut,

Mehsana, Mumbai, Mysore, Nagpur, Nasik, Noida, New Delhi, Patiala, Pune,

Raipur, Rajkot, Ranchi, Rourkela, Saharanpur, Salem, Shimla, Siliguri, Surat,

Thane, Thrissur, Trichy, Trivandrum, Udaipur, Vadodara, Vapi, Vashi,

Vijayawada and Vizag.

The company has seven banc assurance tie-ups, having agreements with ICICI

Bank, Federal Bank, South Indian Bank, Bank of India, Lord Krishna Bank and

some co-operative banks, as well as over 150 corporate agents and brokers. It

has also tied up with NGOs, MFIs and corporates for the distribution of rural

policies and organizations like Dhan for distribution of Salaam Zindagi, a policy

for the socially and economically underprivileged sections of society.

Further, it leverages its state-of-the-art IT infrastructure to provide superior

quality of service to customers.

PROMOTERS

ICICI Bank is India’s second-largest bank with total assets of about Rs.112, 024

crore and a network of about 450 branches and offices and about 1750 ATMs. It

offers a wide range of banking products and financial services to corporate and

retail customers through a variety of delivery channels and through its

specialized subsidiaries and affiliates in the areas of investment banking, life and

non-life insurance, venture capital, asset management and information

technology. ICICI Bank posted a net profit of Rs.1,637 crore for the year ended

March 31, 2004.ICICI Bank’s equity shares are listed in India on stock exchanges

at Chennai, Delhi, Kolkata and Vadodara, the Stock Exchange, Mumbai and the

National Stock Exchange of India Limited and its American Depositary Receipts

(ADRs) are listed on the New York Stock Exchange (NYSE).

Established in London in 1848, Prudential plc, through its businesses in the UK

and Europe, the US and Asia, provides retail financial services products and

services to more than 16 million customers, policyholder and unit holders

worldwide. As of June 30, 2004, the company had over US$300 billion in funds

under management. Prudential has brought to market an integrated range of

financial services products that now includes life assurance, pensions, mutual

funds, banking, investment management and general insurance. In Asia,

Prudential is the leading European life insurance company with a vast network of

24 life and mutual fund operations in twelve countries - China, Hong Kong, India,

Indonesia, Japan, Korea, Malaysia, the Philippines, Singapore, Taiwan, Thailand

and Vietnam.

PRUDENTIAL PLC

Established in 1848, prudential plc is a leading international financial services

company in the UK, with around US$250 billion funds under management and

more than 16 million customers worldwide. Prudential has brought to market an

integrated range of financial services products that now includes life assurance,

pensions, mutual funds, banking, investment management and general

insurance. In Asia, Prudential is UK's largest life insurance company with a vast

network of 22 life and mutual fund operations in twelve countries - China, Hong

Kong, India, Indonesia, Japan, Korea, Malaysia, the Philippines, Singapore,

Taiwan, Thailand and Vietnam. Since 1923, Prudential has championed

customer-centric products and services, supported by over 60,000 staff and

agents across the region.

PLANS OFFERED BY ICICI PRUDENTIAL

Protection Plans

Saving Plans

Investment Plans

Children Plans

Health Plans

Rural Plans

Group Plans

Retirement Solutions

Keyman Insurances

Riders

Some famous products offered by ICICI Prulife

Save’n’protect

ICICI Prudential life insurance co. ltd., India’s no. 1 private

life insurance company, offers you save’n’protect-an ideal

plan for those who want to accumulate funds on regular

basis while enjoying insurance protection.

Life Guard

Level term assurance – under this plan, in case of death of

the life assured during the term, the Sum Assured will be

paid to the beneficiary. There are no maturity benefits.

Hence on survival till maturity, the policy will terminate.

You will need to pay the regular annual premium, for

the term choosen. You will be provided with life cover equal

to the Sum Assured.

INVESTSHIELD LIFE

You have already set out your financial goals for the future.

However, life’s uncertainties make cause you to change

them over a period of time. While the need to protect your

family and your capital in your priority, you also want to earn

enough on your investment, so as to meet your wealth

creation requirement.

At ICICI Prudential, we constantly strive to understand

your needs and provide solutions that help you plan your

future better. In keeping with that endeavour, we present

INVESTSHIELD LIFE, a regular premium unit linked plan

with capital guarantee.

INVESTSHIELD PENSION

When it comes to retirement, you think you will manage just

fine. Are you making enough investments and savings

towards that end? Ordinary savings can get frittered away

due to unforeseen expenses. Besides, even when you

retired, you would still like to continue doing the things you

have always enjoyed such as eating out, taking a holyday,

buying gifts for loved ones, pursuing your hobby, taking your

grand children on outings, etc. after all, you would like to

“retire from work, not life.”

SMART KID

To bring your dreams to life, you need an investment that is

designed to provide adequate money for key educational

milestones in your child’s life, No matter what happens.

That’s why, we now present SMART KID REGULAR

premium plan. This is a regular premium; traditional plan

with two options to receive guaranteed educational benefits,

no matter what the uncertainties in your life.

HEALTH ASSURE PLAN

A long-term critical illness plan-health assure covers you for

a long term. It guarantees to pay the benefits amount on

diagnosis of the specified critical illness. This is a

comprehensive critical illness plan, which can take care of

direct medical expenses as well as other indirect expenses,

arising during the treatment. On diagnosis of a specified

critical illness, you can claim the benefits under this plan

through a simple claim procedure.

CANCER CARE

CANCER CARE plan keeps you financially prepared, so that

you can focus on getting better without worrying about the

money. Through its extensive coverage of both early and

advanced cancer, the plan provides the necessary financial

resources so that you get the best possible medical

treatment as early as possible, and maximize your chances

of survival.

INTRODUCTION TO

STUDY UNDERTAKEN

CHANNEL DEVELOPMENT

Recruitment of qualify & Persuasive insurance advisors

Further guidance

Team support

Smart Research work

Promotional opportunities

Recruitment of Life Insurance Advisors

ICICI Prudential is registered with the insurance regulatory & development

authority under the insurance act, 1938 (4 of 1938) (hereinafter referred to as

the“act”) as a life insurer, and accordingly is engaged in the business of life

insurance.

ICICI Prudential is desirous of appointing the insurance advisors as its

insurance advisor for soliciting and procuring life insurance business for and on

behalf of ICICI Prudential, and to provide various services to the customers and

policyholders.

The insurance advisors holds /shall obtain an insurance license (as defined in the

agreement hereinafter) to act as an insurance agent as provided by section 42 of

the insurance act, 1938 and is desirous of being appointed as an insurance

advisor of ICICI Prudential.

BE YOUR OWN BOSS EARN BEYOND YOUR

IMAGINATION

Who can be a Life Insurance Advisor

Businessman

House Wife

VRS Optee

General Insurance Agent

Teacher/Lecturer

Bond/Mutual fund/Postal Agent

Income Tax Officer/Advisor

Accountant/ Share Broker

JOIN ONE OF THE BIGGEST FORCES IN LIFE INSURANCE

WORK AS AN INSURANCE ADVISOR

Legal Advisor/Political Agent

Students etc.

Why to become an ICICI Prudential Life

Insurance Advisor?

Work from home or office

No prior selling skills required

Personals skills are enhanced by world class training

Foreign trips, Star Club Memberships, Consumer goods,

Gold coins, Reward items

What advisors get from ICICI Prudential Life?

No.1 private life insurance company

1st private life insurance company to have

more than 10 lac customers

Strong brand recognition

World class products and services

Career progression within the company

Unlimited earning potential

SOME GENERAL BENEFITS TO INSURANCE

ADVISORS

Handsome Commissions

Renewal Commissions

Identification

License to Sell insurance products

Zero Balance account in concerned bank

Growth Opportunities

Participations in contests

Company infrastructure facilities

Team support

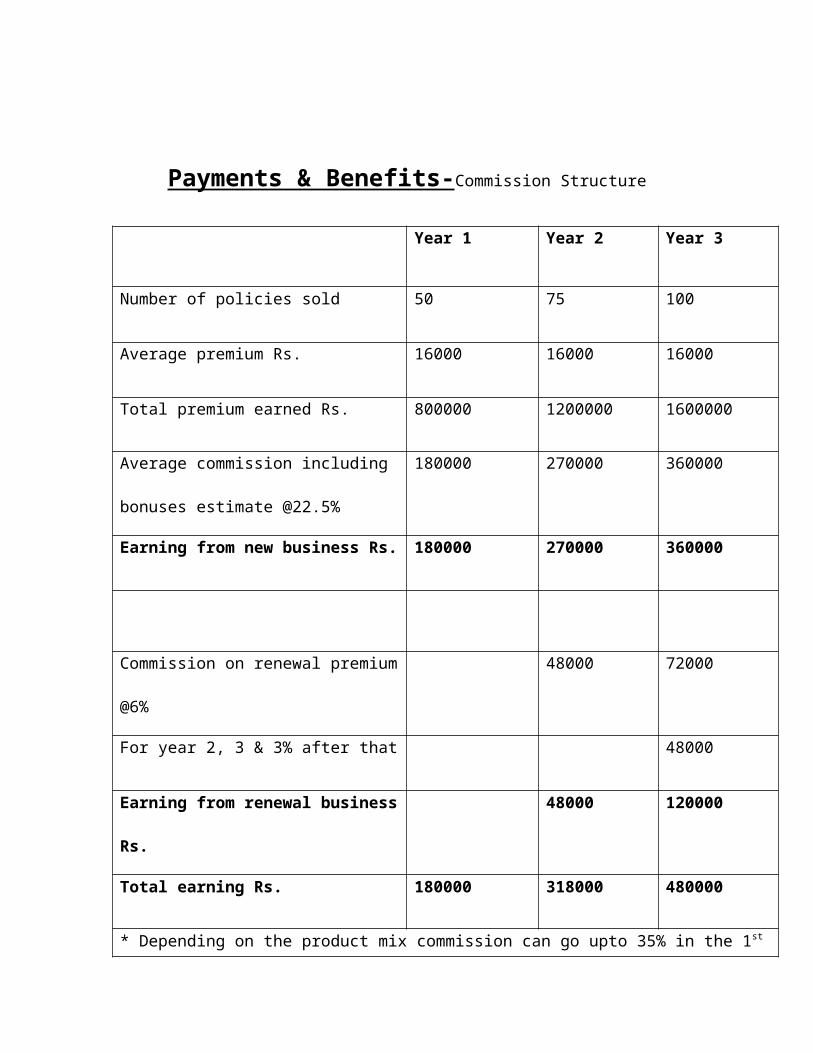

Payments & Benefits-Commission Structure

Year 1 Year 2 Year 3

Number of policies sold 50 75 100

Average premium Rs. 16000 16000 16000

Total premium earned Rs. 800000 1200000 1600000

Average commission including

bonuses estimate @22.5%

180000 270000 360000

Earning from new business Rs. 180000 270000 360000

Commission on renewal premium

@6%

48000 72000

For year 2, 3 & 3% after that 48000

Earning from renewal business Rs. 48000 120000

Total earning Rs. 180000 318000 480000

* Depending on the product mix commission can go upto 35% in the 1st year, 7.5% in the 2nd

& 3rd year & 5% 4th year onwards.

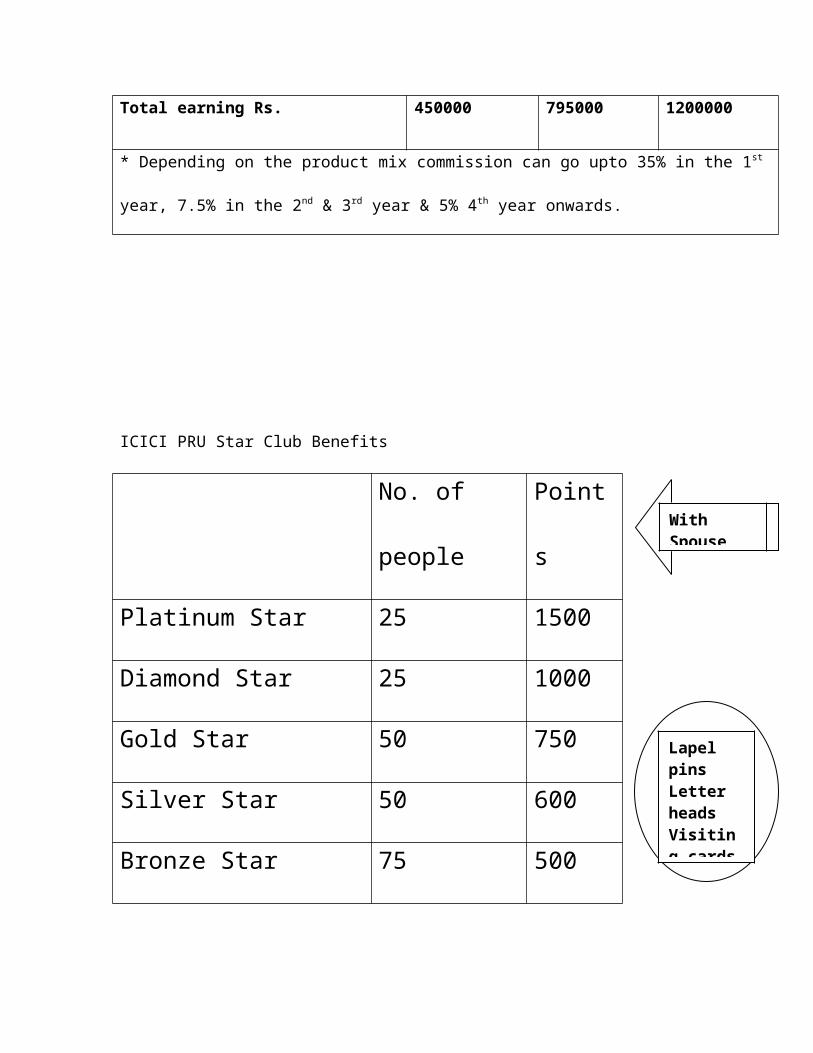

Some of Our High Performers Get….

Year 1 Year 2 Year 3

Number of policies sold 100 150 200

Average premium Rs. 20000 20000 20000

Total premium earned Rs. 2000000 3000000 4000000

Average commission including

bonuses estimate @22.5%

450000 675000 900000

Earning from new business Rs. 450000 675000 900000

Commission on renewal premium

@6%

120000 180000

120000

Earning from renewal business Rs. 120000 300000

Total earning Rs. 450000 795000 1200000

* Depending on the product mix commission can go upto 35% in the 1st year, 7.5% in the 2nd

& 3rd year & 5% 4th year onwards.

ICICI PRU Star Club Benefits

No. of

people

Points

Platinum Star 25 1500

Diamond Star 25 1000

Gold Star 50 750

Silver Star 50 600

Bronze Star 75 500

Total participants 225

Plus free accidental insurance for all of Rs. 10 lakhs

With Spouse

Lapel pinsLetter headsVisiting cards for all

Career opportunities for ICICI Prulife’s Advisors

Agency champion

Through this program we take your business to the next level by giving you

the opportunity to increase your reach and earnings potentials. Presenting the

opportunities to become our agency champion.

Pinnacle Program

Pinnacle program is a meticulously designed program for career progression of

Advisor as UNIT MANAGER. A full time career resulting in increased monetary

benefits and better growth prospects.

Subsequently you have the opportunity where you get promoted to a

agency manager with an earning potential of Rs. 10 lacs p.a. with an eligibility for

ICICI Prustar membership, overses conventions. Management development

programs and others such additional benefits.

FAST TRACK PINNACLE PROGRAM

A Full Time Career As A Unit Manager

Growth within ICICI Prudential

Greater earning potential

Personal Development

Perfomance Criteria

Age 25-45 years

At least 6 months in system

30 issuances within 6 months

Tiger team

A team handpicked with an aim to stave off competition with earnestness,

excellence and exuberance. The tiger team is a select cadre of performers

belonging to the different levels, leading upto the management level in the

organizations. Assimilating to the strength of its members, tiger team explores

the scope for enhanced learning and development from within and without, giving

you the dual advantage of career progression and self development. Currently

the organization has enrolled more than 65 aggressive Tiger Trainers (on rolls)

and 307 part time mobile tigers.

MDRT Program-

Another big program named as MILLION DOLLAR ROUND TABLE is also there

under which high performers get an opportunity to go abroad on the behalf of the

company. They represent their organization among the international players.

Support and training

At ICICI Prudential Life Insurance Co. Ltd., training is an intrinsic element of our

support system for our new advisors. Below are details of a few of our training

initiatives:

Foundation program:

Independent of your work experience, the foundation program will

perfect your knowledge about the insurance industry; equip you

with excellent selling skills along with a comprehensive knowledge

about our products.

Instant recognition:

Your achievements in the first three months of business will be well

acknowledged with our SPRINT and RACE awards. These are

trophies accompanied by a certificate and point rewards given to

you for getting off to a flying start.

Business development clinic:

After one month of the field experience, this programme will give

practical insights on objection handling and generate ideas to get

new customers and big premium policies.

Advance training programs:

Once you are accustomed to the life insurance industry, the

company will continuously upgrade your capabilities and knowledge

through sophisticated training programs on financial products and

markets. These advanced selling skills seminars will assist you in

planning for high net worth customers and building your business

through relationship management.

GENERAL TERMS AND CONDITIONS APPLICABLE TO FINANCIAL

CONSULTANTS OF THE COMPANY:

1. DEFINITIONS:

Unless the context otherwise requires

i. “Act” means the Insurance Act, 1938 and includes any amendment thereto or

enactment thereunder;

ii. “Agent” or “Insurance Agent” means an agent licensed under Section 42 of

the Insurance Act 1938 (as amended) and appointed by the Company and

shall have the meaning set out in Regulations framed by the Insurance

Regulatory and Development Authority from time to time;

iii. “Authority” or the “IRDA” means the Insurance Regulatory and Development

Authority constituted under section 3 of the IRDA Act 1999;

iv. “Company” means ICICI PRULIFE Insurance Company Limited;

v. “Insurance Advisor” means and includes an Agent.

2. CODE OF CONDUCT:

Every person who is appointed as Insurance Advisor by the Company and who

holds a licence under Section 42 of the Act, shall adhere to the model code of

conduct as specified below:-

I. EVERY INSURANCE ADVISOR SHALL;

(a) Identify himself and ICICI PRULIFE Insurance Company Limited, of

whom he is an insurance agent to all the prospects;

(b) Disclose his licence to the prospect if so demanded;

(c) Disseminate the requisite information in respect of insurance products

offered for sale by his insurer and take into account the needs of the

prospect while recommending a specific insurance plan;

(d) Disclose the scales of commission in respect of the insurance product

offered for sale, if asked by the prospect;

(e) Indicate the premium to be charged by the insurer for the insurance

product offered for sale;

(f) Explain to the prospect the nature of information required in the proposal

form by the insurer, and also the importance of disclosure of material

information in the purchase of an insurance contract and shall never

persuade or encourage any prospect not to divulge or disclose any

information which is relevant to the insurer for the purpose of underwriter;

(g) Bring to the notice of the insurer any adverse habits or income

inconsistency of the prospect, in the form of a report (called “Insurance

Agent’s Confidential Report”) along with every proposal submitted to the

insurer, and any material fact that may adversely affect the underwriting

decision of the insurer as regards acceptance of the proposal, by making

all reasonable enquiries about the prospect;

(h) Obtain the requisite documents at the time of filing the proposal form with

the insurer; and other documents subsequently asked for by the insurer

for completion of the proposal;

(i) Inform promptly the prospect about the acceptance or rejection of the

proposal by the insurer;

(j) Advise every individual policyholder to effect nomination or assignment or

change of address or exercise of options, as the case may be, and offer

necessary assistance in this behalf, wherever necessary;

(k) The Insurance Advisor may receive cheques or Demand Drafts from

the policyholders towards payment of premium. However, in such a

situation, he will ensure that the cheques received are not back dated and

the cheque/ demand draft are deposited with the Company within the

grace period.

(l) The Insurance Advisor is not authorized and shall not be entitled

anytime to collect premium from the policyholders in cash and shall be

under obligation to disclose the prospect / policyholder that the payment

towards premium charges shall be accepted by the Company by way of

crossed cheques or demand drafts only. The Insurance Advisor further

shall inform and encourage the policyholder to write his/her policy number

on the back side of the instrument paying the premium charges.

(m) Render necessary assistance to the policyholders or claimants or

beneficiaries in complying with the requirements for settlement of claims

by the insurer;

(n) Every Insurance Advisor shall maintain strict confidentiality of the

information received from any prospect and / or the Company in the

course of business. Confidential information is elucidated as follows:

(i) The Insurance Advisor agrees that the Confidential Information is to

be considered confidential and proprietary to the Company and the

Insurance Advisor shall hold the same in confidence, shall not use

the Confidential Information other than for the purposes of its business

with the Company, and shall disclose it only to its officers, directors, or

employees with a specific need to know. The Insurance Advisor

shall not disclose, publish or otherwise reveal any of the Confidential

Information received from the Company and/or the prospect to any

other party whatsoever except with the specific prior written

authorization of the Company.

(ii) The Confidential Information furnished in tangible form shall not be

duplicated by the Insurance Advisor except in the course of

business. Upon the request of the Company, the Insurance Advisor

shall return all Confidential Information received in written or tangible

form, including copies, or reproductions or other media containing

such Confidential Information, within ten (10) days of such request. At

the Recipient's option, any documents or other media developed by

the Insurance Advisor containing Confidential Information may be

destroyed by the Insurance Advisor. The Insurance Advisor shall

provide a written certificate to the Insurance Advisor regarding

destruction within ten (10) days thereafter.

(iii) The Insurance Advisor shall have no obligation under this with

respect to Confidential Information which is or becomes publicly

available.

II. NO INSURANCE ADVISOR SHALL:

(a) Solicit or procure insurance business without holding a valid licence;

(b) Induce or pursuade any prospect to omit any material information in the

proposal form;

(c) Induce the prospect to submit wrong information in the proposal form or

documents submitted to the insurer for acceptance of the proposal;

(d) Behave in a discourteous manner with the prospect;

(e) Interfere with any proposal introduced by any other insurance agent;

(f) Offer different rates, advantages, terms and conditions other than those

offered by his insurer;

(g) Demand or receive a share of claim proceeds from the beneficiary under

an insurance contract or offer any share payable out of the commission

which may be received by the Insurance Advisor from the Company. ;

(h) Force, pursuade or induce a policyholder to terminate any existing policy

and to effect a new proposal from him;

(i) Have, in case of a corporate agent, a portfolio of insurance business under

which the premium is in excess of fifty percent of total premium procured,

in any year, from one person (who is not an individual) or one organization

or one group of organizations;

(j) Become or remain a director of any insurance company;

III. EVERY INSURANCE ADVISOR SHALL:

With a view to conserve the insurance business already procured through him,

make every attempt to ensure remittance of the premiums by the

policyholders within the stipulated time, by giving notice to the policyholder

orally and in writing;

3. ADVERTISEMENT AND PUBLICITY:

Every Insurance Advisor shall, during the conduct of his agency business,

adhere to the provisions of the Insurance Regulatory and Development

Authority (Insurance Advertisements and Disclosure) Regulations, 2000.

In accordance with the advertisement regulations issued by the IRDA, the

Insurance Advisor are required to obtain prior approval in writing, of the

Company for issue of any advertisement. However in the following cases

such prior written approval is not required:

a. Advertisements developed by the Company and provided to the

Insurance Advisors;

b. Generic advertisements limited to information like the name, logo,

address, and phone numbers etc of Insurance Advisors; and

c. Advertisements that consist only of simple and correct statements

describing the availability of lines of insurance, references of

experience, service and qualifications; but making no reference to

specific policies, benefits, costs or the Company.

4. OTHER INSURANCE AGENCIES:

In accordance with the Insurance Regulatory and Development Authority

(Licensing of Insurance Agents) Regulations, 2000, an insurance agent can

act on behalf of only one life insurer and one general insurer at one time.

Hence the Insurance Advisors are needed to ensure that the do not take up

life insurance agency of any other life Insurer. He may however act as a

general insurance agent for one general insurer, subject to his meeting the

applicable regulatory requirements.

5. MINIMUM BUSINESS AND COMMISSIONS:

As our consultant, the Insurance Advisor shall be entitled to receive

Commission on the premium generated by the Insurance Advisor and the

rates of Commission will be informed to the Insurance Advisor separately

from time to time. While ensuring that the existing business continues, the

Insurance Advisors are also required to bring in minimum new business for

the Company, which will entitle the Insurance Advisor to a Net Effective

Premium at such rates as may be determined by the Company from time to

time. The minimum business to be procured by the Insurance Advisor

during a business year will be determined by the Company on an annual

basis. The business year would be a period of 12 months ending on 30th

June every year and the first business year will be a period from the date of

appointment upto the forthcoming 30th of June. The business targets for the

first business year shall be pro-rated on the number of complete months from

the date of appointment upto the end of the business year.

Net Effective Premium:

The Company would measure a consultant’s performance annually based on

commission on account of new business procured adjusted to commission on

reduced premiums and premiums not collected due to:

i- lapses,

ii- Cancellation of riders,

iii- Cancellation of policies,

iv- Surrenders,

v- Reduction of sum assured (including conversion to paid-up)

with respect to policies/ business procured in the previous 2 business years.

This measurement is termed as ‘Net Effective Premium’ and the weightages

for reduction in premiums or lapses of policies are in proportion to the

reduction of premiums and are subject to change from time to time.

6. PAYMENT OF COMMISSION ON POLICIES ON OWN LIFE:

In terms of Rule 16-B of the Insurance Rules, 1939, an agent shall not be

entitled to commission on any policy taken out by him on his own life unless

he has secured policies on six different lives excluding his own and he has

also been an insurance agent continuously from the time of his soliciting or

procuring the first policy on each of such six lives or proposing on the policy

of his own life, whichever is earlier, till the time when the policies on those six

lives and the policy on his own life have all been issued.

7. PAYMENT OF COMMISSION IN CASE OF DEATH:

In the event of death of an Agent, the commission payable to him under the

provisions of clause (b) and (c) of Section 44(1) of the Act, shall continue to

be payable to his nominees, if any, or to his heirs for so long as the

commission would have been paid to the Agent if he were alive.

8. PAYMENT OF COMMISSION IN CASE OF TERMINATION:

Where the agency contract has been terminated for reasons other than fraud,

the commission on renewal premium shall be paid in accordance with the

provisions of clauses (a), (b) & (c) of the proviso to Section 44(1) of the Act.

9. CHARGES:

Every agent shall at the time of applying for Agency, pay a sum of Rs. 600/-

to the Company towards licensing and examination fees and franking

charges. The said rates are subject to revision in accordance with the

applicable rules and regulations.

10.PROHIBITION OF REBATE:

Every agent shall observe and adhere to the provisions of Section 41 of the

Insurance Act, 1938 reproduced hereunder and also bring the same to the

notice of the prospect:

“Section 41

(1) No person shall allow or offer to allow either directly or indirectly, as an

inducement to any person to take out or renew or continue, an insurance

in respect of any kind of risk relating to lives or property in India, any

rebate of the whole or part commission payable or any rebate of the

premium shown on the policy nor shall any person taking out or renewing

or continuing a policy accept any rebate except such rebate as may be

allowed in accordance with the published prospectuses or tables of the

Insurer.

(2) Any person making default in complying with the provisions of this Section

shall be punishable with fine, which may extend to five hundred Rupees.”

11.RURAL SECTOR OBLIGATIONS:

The Insurance Advisor may be aware that under the Insurance Regulatory

and Development Authority (Obligations of Insurers to Rural or Social

Sectors) Regulations, 2000, the Company is required to procure a minimum

business from both the Rural and Social sectors. In view of this, we may

request the Insurance Advisors from time to time to procure certain

minimum business from these sectors.

For the purposes of procuring insurance business from the Rural sector, the

rural sector shall have the meaning as given in the Insurance Regulatory and

Development Authority (Obligations of Insurers to Rural or Social Sectors)

Regulations 2000 as amended from time to time.

12.SOCIAL SECTOR OBLIGATIONS:

For the purposes of procuring insurance business from the social sector, the

social sector shall have the meaning as given in the Insurance Regulatory

and Development Authority (Obligations of Insurers to Rural or Social

Sectors) Regulations 2000 as amended from time to time.

13.NO AUTHORITY TO COLLECT MONEYS:

The Insurance Advisors not authorized to collect any money/premium in

cash from the prospects and/ or policyholders under any circumstances.

14.NO AUTHORITY TO ACCEPT RISKS:

The Insurance Advisors are not authorised to accept any risk for or on

behalf of the Company.

15.NO AUTHORITY TO ISSUE RECEIPTS:

The Insurance Advisors are not authorised to issue any type of receipt

whether on personal letterhead or on the Company’s behalf to any person, in

respect of monies collected by them.

16.GROUP INSURANCE BUSINESS:

Unless specifically permitted, the Insurance Advisors are not authorised to

procure Group Insurance business for the Company.

16(a.) The Insurance Advisor authorises the Head-Retail Sales to act as a group

Organiser/Manager to arrange the group insurance on the life of Financial

Consultant as and when eligible for the same. It is understood that the

eligibility for the Group Insurance shall be on the basis of criteria to be

decided by the Head-Retail Sales at his sole discretion from time to time.

17.DISQUALIFICATION OF AGENT:

A Insurance Advisor’s licence is liable to be cancelled if the Financial

Consultant suffers, at any time during the currency of the licence, from any of

the disqualification’s mentioned in sub-section (4) of Section 42 of the Act,

and the Company may recover from him the licence and the identity card

issued earlier along with all other documents, literatures, booklets, tables etc.

that belong to the Company. The disqualifications mentioned in Sub-section

(4) Of Section 42 of the Act are:

a. That the person is a minor.

b. That he is found to be of unsound mind by a Court of competent

jurisdiction;

c. That he is found guilty of criminal misappropriation or criminal breach of

trust or cheating or forgery or an abatement of or attempt to commit any

such offence by a court of competent jurisdiction;

Provided that where at least five years have elapsed since the completion

of the sentence imposed on any person in respect of any such offence,

the Authority shall ordinarily declare in respect of such person that his

conviction shall cease to operate as a disqualification under this clause.

d. That in the course of any judicial proceeding relating to any policy of

insurance or the winding up of an insurance company or in the course of

an investigation of the affairs of an insurer, it has been found that he has

been guilty of or has knowingly participated in or connived at any fraud,

dishonesty or misrepresentation against an insurer or an insured;

e. That he does not possess the requisite qualification and practical training

for a period not exceeding12 months, as may be specified by the

Regulations, made by the Authority in this behalf;

f. That he has not passed such examination as may be specified by the

Regulations made by the authority in this behalf;

Provided that a person who had been issued a licence under Section

41(1) or 64UM(1) of the Act shall not be required to possess the requisite

qualification, practical training and pass such examination as required by

clauses (e) and (f);

g. That he violates the code of conduct as may be specified by the

Regulations made by the Authority.

18.OBLIGATIONS UNDER THE IRDA (PROTECTION OF POLICYHOLDERS’

INTERESTS) REGULATIONS, 2002:

The following are the points to be noted and adhered to by the Financial

Consultants:

1. Regulation 3(2) - An insurer or its agent or other intermediary shall

provide all material information in respect of a proposed cover to the

prospect to enable the prospect to decide on the best cover that would be

in his or her interest.

2. Regulation 3(3) - Where the prospect depends upon the advice of the

insurer or his agent or an insurance intermediary, such a person must

advise the prospect dispassionately

3. Regulation 3(5) - In the process of sale, the insurer or its agent or any

intermediary shall act according to the code of conduct prescribed by:

i) The Authority

ii) The Councils that have been established under section 64C of the Act

and

iii) The recognized professional body or association of which the agent or

intermediary or insurance intermediary is a member.

4. Regulation 4(6) - Proposals shall be processed by the insurer with speed

and efficiency and all decisions thereof shall be communicated by it in

writing within a reasonable period not exceeding 15 days from receipt of

proposals by the insurer.

In order to assist the Company adheres to the time limit of 15 days

prescribed in this regulation, you are required to ensure that all

communications received by you in writing from the customer is delivered

to the Company within 24 hours of receipt.

5. Regulation 6(2) - While acting under regulation 6(1) in forwarding the

policy to the insured, the insurer shall inform by the letter forwarding the

policy that he has a period of 15 days from the date of receipt of the policy

document to review the terms and conditions of the policy and where the

insured disagrees to any of those terms or conditions, he has the option to

return the policy stating the reasons for his objection, when he shall be

entitled to a refund of the premium paid, subject only to a deduction of a

proportionate risk premium for the period on cover and the expenses

incurred by the insurer on medical examination of the proposer and stamp

duty charges.

This regulation provides an option to the Policyholder to return the policy

within 15 days of receiving it and getting a refund of the premium, less

certain specified deductions. Please note that in all such cases, the

Commission, NEP and all other benefits attached to such policy will be

recalled by us. This will be done either by way of adjustment from future

payments/benefits. Where such future payments are not available or are

inadequate, you may be required to pay over the same to us within such

time as we may specify then.

6. Regulation 11(4) - Any breaches of the obligations cast on an insurer or

insurance agent or insurance intermediary in terms of these regulations

may enable the Authority to initiate action against each or all of them,

jointly or severally, under the Act and/or the Insurance Regulatory and

Development Authority Act, 1999.

19.VALIDITY OF LICENCE & RENEWAL THEREOF:

The appointment as our Insurance Advisor is subject to your continuing to

hold a valid insurance licence at all times. If your insurance licence is

cancelled

or expires and is not renewed in time, the appointment as Insurance Advisor

shall ipso facto stand terminated on the cancellation or expiry of insurance

licence as the case may be. As required under the aforesaid Regulations,

before seeking renewal of the licence, the applicant would be required to

undergo practical training from an approved training institution.

It may be noted that once an appointment stand terminated as aforesaid, a

renewal or re-issue of licence shall not automatically revive agency with the

Company and the applicant shall have to submit a fresh application. In such

an event re-appointment shall be at the discretion of the Company.

20.DIRECTORSHIPS:

As required under the Insurance Regulatory and Development Authority

(Licensing of Insurance Agents) Regulations, 2000 please note that the

Insurance Advisors of the Company are not entitled to become or remain a

director of any Insurance Company.

21.MISSELLING AND PENALTY:

The Insurance Advisor shall fully understand the requirements of the

prospect and then suggest a suitable product. The Insurance Advisor shall

not induce any prospect into accepting any product, which the prospect didn’t

initially need, only for the generation of business. In the event of the prospect

rejecting the policy for the reason that the product was not what he had

required, such sale shall be treated as a miss-sale and the Company

Reserves the rights to penalise the Insurance Advisor by way of fine and/or

Penal action, which shall not be less than the cost incurred by the Company

on account of such sale.

22.TERMINATION OF THE AGENCY:

The Company shall also be entitled at any time to terminate your agency,

without thereby being liable for any compensation or damages, if in its sole

opinion,

(a) The performance of the Insurance Advisor has not been satisfactory; or

(b) The Insurance Advisor has acted in breach of the code of conduct or

any of the terms and conditions of appointment; or

(c) Any information furnished by the Insurance Advisor in relation with the

appointment is false; or

(d) The Insurance Advisor has acted in a fraudulent manner and continuing

the person as Insurance Advisor shall be prejudicial to the interest of

the Company.

23.TERMINATION

Notwithstanding anything herein before contained either party may terminate

the agency by giving a notice of one month to the other party without

assigning any reason thereto.

Any notice to be served hereunder shall be sufficiently served on the

Company, if served by Registered Post at its said Registered Office or any

other address as may be intimated by the Company to the Consultant in

writing, and shall be sufficiently served on the Consultant if sent to him by

Registered Post at his given address.

Upon termination of agency the terminated Insurance Advisor shall

forthwith surrender the identity Card as well as all other manuals, tables, rate

books, literatures, product guides etc. of the Company that are in there

possession, to the Company. Subject to the provisions of Section 44 of the

Insurance Act 1938 and the rules of the Company in this regard as laid down

from time to time, the terminated Insurance Advisor shall be entitled to

receive commission and renewal commission on the business brought in by

the Insurance Advisor prior to termination of the agency.

In the event of the agency being terminated within a period of 24 months from

the date of appointment, the Company shall be entitled to claim the entire

costs incurred on the Insurance Advisor for training. The Company

reserves the right to determine the extent of costs incurred as aforesaid.

This appointment shall be subject to jurisdiction of Courts at Mumbai. As a

matter of token of acceptance of the terms and conditions as detailed above,

the proposed Insurance Advisor / Insurance Advisor is required to sign

the original copy of the Terms and Conditions as having accepted and return

the original copy to the terms and conditions to the Company.

I SAY READ, UNDERSTOOD, AGREED AND CONFIRMED.

Name:

Address:

Date:

In the presence of Witness:

Signature:

Bancassurance

Why we are talking about Bancassurance?

Is it our idea or we have learnt from somebody?

Are we going to change the definition of ba?

What is our objective in starting ba?

Do we want to learn from the mistakes committed by established?

Definition of Bancassurance:

Bancassurance: Ba is the selling of insurance products through

a bank’s distribution channels to bank’s customers. It is a French term

bank Assurance, Bank Insurance, Assure Banking are used

interchangeably Universal Banking and One Stop Shop are further

extension of Ba.

Bank’s distribution channels:

Branch network

Tele banking

Statement inserts

ATMs I

Three Cutting Edge for banks:

Brand Loyalty

Data Bank

Face to face Contact

Bank’s advantage over Insurance:

Better hit ratio

Lower costs per sales

Access to middle income group

Better processing technology

More information knowledge of potential buyers of insurance

Objective of Banks:

Fee income which is risk free

To reduce operating expenses

Product diversification

Benefits to Insurers:

Sky is the limit

Lesser Procurement Cost

Known customer and therefore risk assessment is easier

Increase in turnover

Increase in Market Penetration

Access to middle market segment

Benefits to customers:

Lower cost

Refined, high

Quality product

Double Assurance

Delivery at doorsteps

Convenience in payment

Easy & Automatic renewals

Options for Banks:

Subsidiary

Mergers

Acquisitions

Joint Venture

Working Relationships with one or many insurers

Division with in bank

Options for insurers:

Subsidiary

Joint Venture

Working relationships with one or more banks

Post assurance

Strengths:

Huge pool of skilled professionals

Just needs to be relocated-no extra manpower required at any level

A big arsenal of personal line products already lined up INo or little R &

D effort required at the outset

Weaknesses:

No incentives for the people to go for insurance

Tax Exemption for all ba products required

Lack of goodwill by banks as well as insurance companies

Tariffs-inflexible

Ratings not based on sound actuarial principles

Opportunities:

Bank’s enormous database

Homogeneous groups can be churned out of the database to develop

and market products

Product Positioning

Experiment has already been done elsewhere and we know in advance

about the highs & lows of ba

Threats:

Required changes in approach, thinking & work culture on the part of

everybody concerned

Resistance to change due to any relocation

Non-response from target customers

Lessons:

Develop ba only gradually

Europe & USA-banks were first allowed to distribute insurance products

and later were allowed to carry risks

Distributional one can yield substantial fee income, which is net and is

free of any encumbrances that an insurer has to deal with.

BANKS SUPPORTING THE CONCERNED

INSURANCE FIRMS

LIFE INSURANCE CORPORATION

CENTRAL BANK OF INDIA

CENTURIAN BANK

VIJAYA BANK

CORPORATION BANK

JANTA URBAN CO-OPERATIVE BANK

YEOTMAL MAHILA SAHKARI BANK

ICICI PRUDENTIAL LIFE INSURANCE

ICICI BANK

BANK OF INDIA

HDFC STANDARD LIFE INSURANCE

UNION BANK OF INDIA

ING VYSYA LIFE INSURANCE

URBAN CORPORATIVE BANK {MUMBAI}

ING VYSYA BANK

PLANNING: BHARAT OVERSEAS BANK

FOCUS: MAHARASTRA, GUJRAT, WESTORN PART OF INDIA

AVIVA LIFE INSURANCE

ABN AMRO BANK

AMERICAN EXPRESS

CANARA BANK

LAXMI VILAS BANK

BAJAJ ALLIANZ LIFE INSURANCE

STANDARD CHARTED BANK

SYNDICATE BANK

BIRLA SUNLIFE INSURANCE

CITI BABK, DEUTSCHE BANK

IDBI BANK

DCB

BANK OF RAJASTHAN

BANK OF MUSKAT

TATA AIG LIFE INSURANCE

STATE BANK OF INDIA

ALLAHBAD BANK

LORD KRISHNA BANK

FEDRAL BANK

OBJECTIVE OF THE RESEARCH

Primary objectives:-

1. Depth study of Insurance Agency Development

Secondary objective:-

1. To gain familiarity with the phenomena.

2. To see what the people feel about the products and services of ICICI

Prudential.

Methods of Data Collection

• Primary Data - Those data, which are collected for the first time and thus

happen to be original in character. It can also be obtained through observations,

direct communications or personal interviews.

• Secondary Data -Those data, which have already been collected by someone

else and which have already been passed through the statistical process. When

the researcher utilizes secondary data, then he looks for the various sources

from where he can obtain them. Materials can be collected from:-

• Trade Journals.

• Newspapers

• Business Magazines.

• Statistical documents.

When I want to understand what is happening today or try to decide what will

happen tomorrow, I look back. Therefore, secondary data plays an important role

in a complete research. The various data collection tools used in this research

process is:-

• Observation: - In this, the various suggestions of peoples and various

consumers are being heard. It can be either the merits or demerits, said by the

consumers relating to the product.

• Interview schedule: - Here, I had personal contacts with all the people in the

field as well in the office to know for more of the ICICI Prudential, its products

and its services.

Methodological Assumptions

• The methodology used is based on Primary & Secondary data. It is assumed

that both methods is more suitable for my type of report.

• It is assumed that the staff has a good degree of knowledge about the

information collected so far.

ANALYSIS

&

INTERPRETATION

SWOT ANALYSIS

S – Strength

W – Weakness

O – Opportunity

T- Threat

ICICI Prudential is one of the most powerful, world class Life Insurance Co.

gaining appreciation for their strong ethics, excellent performance,

professionalism and team work which led them to progress in today’s

challenging environment. Though with its excellence performance and every

efforts has been made to present the most authentic and truly representative

findings, but some deviations and hurdles in progress. So, with its strength

and good quality, the company is having some weakness, and threats and

opportunities. SWOT analysis is explained below:

Strengths

ICICI Prudential is the largest private player in the insurance industry in

India.

Excellent services.

Customization of products as per customer’s needs.

Brand image.

Business Experience.

Strong Financial Base.

Innovative Products, Technology, Organization culture and climate.

The company has a large network of branches, which is helpful to

customer for the payment.

WEAKNESSES

Lot of competitors are in the market offer same product offered by

the difference in the premium and offering.

Target only higher income group whereas other companies are

trying to catch middle-class people.

Higher premium as compared to other companies.

Clients face problems to get insured due to large number of

formalities.

High targets for financial advisors and for the sales department.

OPPURTUNITIES

Huge market is literally untapped. Out of estimated 320 million

insurable markets only 20% of the population is insured.

In a conservative society of India where people are most inclined

towards risks free investment such as Bank FD’s and saving rather

than equity and high risk investment insurance offers the best of

both worlds – The security with high returns.

In the pension field where people want good life after their

retirement.

Indian people are more emotional towards their that’s why children

plans are selling like hot cakes.

Health insurance and pension schemes as estimated market

potential of approximately $15 dollars

THREATS

Weak perception of private players in the mind of Indian people

due to frequent financial scams.

Large number of insurance players.

Existing wrong business practices of companies like LIC first

premium is paid by their agents where –as IRDA suggests that

even forms to be filled by the clients themselves.

Players like Allianz Bajaj and Birla Sun Life with low premium for

the similar plans.

Entry of many other private companies with equally strong

experience and financial strength of foreign partners making the

competition difficult and saturating the urban markets.

LIC has woken up from sleep and is following competitive

strategies. Its huge surplus in life fund gives a capability to lodge

price war.

For the insurance sector Govt. set the authority that is IRDA which

is undertaken to track record of all the companies and change the

rules day by day more rigid, which is very difficult for the

companies.

CONCLUSION

CONCLUSION

It is clear from the above study that insurance business is mushrooming in the

country. Today there are number of insurance companies offering different

insurance plans with different added advantages. LIC is leading company in the

insurance business in India with a market share of 87% followed by ICICI

Prudential with a market share of 5.4%.

Today more and more private entrepreneurs are coming to

deal in life insurance products. It is not an easy task for a company to stay stable

and survive with rapidly growth in the tough competition. Hence a company

dealing in life insurance’s products needs qualify and persuasive insurance

advisors. Company must provide world-class training and promotional

opportunities to their advisors to better performance.

FINDINGS

FINDINGS

Universal insurance sector has now come to play an important role in the growth

of insurance sector of every country as well as economic development of the

country. ICICI Prudential provides wide range of financial services and products

to the clients. On the basis of whole study, conclude the following findings: -

Though the period of commitment is very long, the investors do not much

believe in private players.

ICICI Prudential is having the largest market share i.e. 40% among all the

private players.

There is no life cover provided during the extension period of vesting age.

The various challenges faced by the insurance industry are:

a) Broadening the Benefits.

b) Channels of Distribution.

c) Expectation of the customers.

d) Consumer Education.

e) Catering the rural areas.

f) Large no. of private companies.

Not much emphasis is given to create awareness in the rural sector.

RECOMMENDATIONS

RECOMMENDATIONS

ICICI Prudential should provide the home services to its customers.

ICICI Prudential should reduce its minimum policy payment in the first

installment.

To educate the client/customer, the interaction with the client should be

improved by conducting seminar, client meetings and workshops.

To increase the market share, ICICI Prudential should increase its branch

network, especially in the rural areas.

ANNEXURE

ANNEXURE

How Insurance Advisor’s Recruitment Is Done?

SELECTION OF PROFILES

MAKE A CALL

MAKE APPOINTMENTS

DISCLOSE ALL THE FACTS TO THEM

CLOSE THE CALL

COMPLETION OF FORMALITIES

PROVIDE INFORMATIONS ABOUT EXAMINATION TEST

Sr. No. Names Address Contact

Teachers

1. _ _ _

2. _ _ _

Entrepreneurs

3. _ _ _

Officials

4. _ _ _

5. _ _ _

Freshers

6. _ _ _

Formalities of Insurance Advisor’s Recruitment

Form Fillings

Insurance Advisor Application Form

Insurance Advisor Agreement Form

Examination Test Form/Yellow Form

Documentary

Age Proof (Certificate of matriculation)

Address Proof (Voter-Id, Ration Card, Telephone Bill etc.)

Education Proof (Highly Qualify Edu. Proof like 10+2 or Graduation’s

Certificate)

7-Photographs

Demand Draft

Frequently asked Questions in Examination

Test

Insurance Basics

Premium Calculations

Age Calculations

BIBLIOGRAPHY

BIBLIOGRAPHY

Study Material of ICICI PRUDENTIAL LIFE INSURANCE

Study Material of LIFE INSURANCE CORPORATION

Used Material from INTERNET

WEBSITES

www.icicibank.com

www.iciciprulife.com

www.birlasunlife.com

www.personalfn.com

www.irda.com

Limitations of the Study

Limitations of the Study

This summer training will always remain one of the best experience of my life.

But no study is complete in itself, however good it may be and every study has

some limitations, some of the limitations which I have confronted are as follows:-

Time period for covering the project was short.

It was not easy to convince the professionals.

Companies were not ready to give address of their respective customers

to conduct a survey.

Top Related