Languages

Pages

Legal

NBER WORKING PAPER SERIES

DETERMINANTS OF ECONOMIC GROWTH:A CROSS-COUNTRY EMPIRICAL STUDY

Robert J. Barro

NBER Working Paper 5698

NATIONAL BUREAU OF ECONOMIC RESEARCH1050 Massachusetts Avenue

Cambridge, MA 02138August 1996

Prepared for the Lionel Robbins Lectures, delivered at the London School of Economics, February20-22, 1996. This paper is part of NBER’s research program in Economic Fluctuations and Growth.Any opinions expressed are those of the author and not those of the National Bureau of EconomicResearch.

O 1996 by Robert J. Barre. All rights reserved. Short sections of text, not to exceed two paragraphs,may be quoted without explicit permission provided that full credit, including @ notice, is given tothe source.

NBER Working Paper 5698August 1996

DETERMINANTS OF ECONOMIC GROWTH:A CROSS-COUNTRY EMPIRICAL STUDY

ABSTRACT

Empirical findings for a panel of around 100 countries from 1960 to 1990 strongly support

the general notion of conditional convergence. For a given starting level of real per capita GDP, the

growth rate is enhanced by higher initial schooling and life expectancy, lower fertility, lower

government consumption, better maintenance of the rule of law, lower inflation, and improvements

in the terms of trade. For given values of these and other variables, growth is negatively related to

the initial level of real per capita GDP. Political freedom has only a weak effect on growth but there

is some indication of a nonlinear relation. At low levels of political rights, an expansion of these

rights stimulates economic growth. However, once a moderate amount of democracy has been

attained, a further expansion reduces growth. In contrast to the small effect of democracy on growth,

there is a strong positive influence of the standard of living on a country’s propensity to experience

democracy.

Robert J. BarroDepartment of EconomicsLittauer Center 120Harvard UniversityCambridge, MA 02138and NBERbarro @husc3 .harvard.edu

The revival of interest in growth theory and empirics is now about ten years old.

The initial excitement centered on “endogenous growth” theories, in which the

long–term growth rate WM determined by government policies and other forces

mntained in the analysis. The first models were standard except that capital was

broadened to include human components and to allow for spillover effects (Romer

[1986], LUCM[1988], Rebelo [1991]). In these settings, the absence of diminishing

returns meant that the accumulation of capital cotid sustain growth indefinitely,

although the rates of growth and investment might not be Pareto optimal.

Subsequent analyses argued that technological progress generated by the discovery

of new ideas was the only way to avoid diminishing returns in the long run. In these

models, the purposive behavior that underlay innovations hinged on the prospect of

monopoly profits, which provided individud incentives to carry out costly research

(Romer [1990], Aghion and Hewitt [1992], Grossman and Helpman [1991, Chs. 3,4]).

Again, the equilibria need not be Pareto optimal, and there were some intriguing

implications for policy, notably for subsidies to basic research.

Despite these breakthroughs, the recent empirical work on growth across countries

and regions has not received its main inspiration horn the new theories. Rather, the

standard applied framework derives more from the older, neoclassical model, as

extended to incorporate government policies (including institutional choices that

maintain property rights and free markets), accumulation of human capital, fertility

decisions, and the diffusion of technology. In partictiar, the neoclassical model’s central

idea of conditional convergence receives strong support from the data: poorer countries

grow faster per capita once one holds constant measures of government policy, initial

levels of human capital, and so on.

Theories of basic technological change are most important for understanding why

the world as a whole-and, more specifically, the economies at the technological frontier–

can grow in the long run. But these theories have less to do with the determination of

relative rates of growth across economies; that is, with the relations studied in

cross-country or cross–region statistical analyses. It is surely an irony that one of the

lasting contributions of endogenous growth theory is that it stimulated empirical work

that demonstrated the explanatory power of the neoclassical growth model.

The first essay begins with a sketch of old and new growth theories. An empirical

framework that embodies the idea of condition convergence is then derived from an

extended version of the neoclassical growth model. In this setting, the growth rate

depends on the relation between the initial level of output, y, and its target position, y*.

The target, y*, depends on government policies and on household behavior with respect

to saving, work effort, and fertility. For given determinants of y*, the growth rate

vanes inversely with y (the condition convergence effect). For given y, the growth

rate increases with y*—for example, with improved property rights and lower tax rates.

In addition, the speed of convergence of y to y* is increased by a higher starting level of

human capital.

The empirical findings for a panel of around 100 countries strongly support the

general notion of conditional convergence. For a given starting level of real per capita

GDP, the growth rate is enhanced by higher initial schooling and life expectancy, lower

fertility, lower government consumption, better maintenance of the rde of law, lower

inflation, and improvements in the terms of trade. For given values of these and other

variables, growth is negatively related to the initial level of real per capita GDP.

The second essay details the interplay between economic development and a

measure of political freedom or democracy. The extent of democracy does not emerge as

a critical determinant of growth, but there is some evidence of a nonlinear relationship.

At low levels of political rights, an expansion of these rights stimulates economic

growth. However, once a moderate amount of democracy has been attained, a further

expansion reduces growth. A possible interpretation is that, in extreme dictatorships,

an increase in political rights tends to raise growth because the limitation on

governmental authority is critical. However, in places that have already achieved some

political rights, further democratization may retard growth because of the heightened

concern with social programs and income redistribution.

In contrast to the weak effect of democracy on growth, there is a strong positive

linkage from prosperity to the propensity to experience democracy (a relation called the

Lipset [1959] hypothesis). Various measures of the standard of living—real per capita

GDP, life expectancy, and a smaller gap between male and female educational

attainment —are found to predict democracy. Additional effects considered include

urbanization, natural resources, country size, inequality, colonial history, and religious

affiliation.

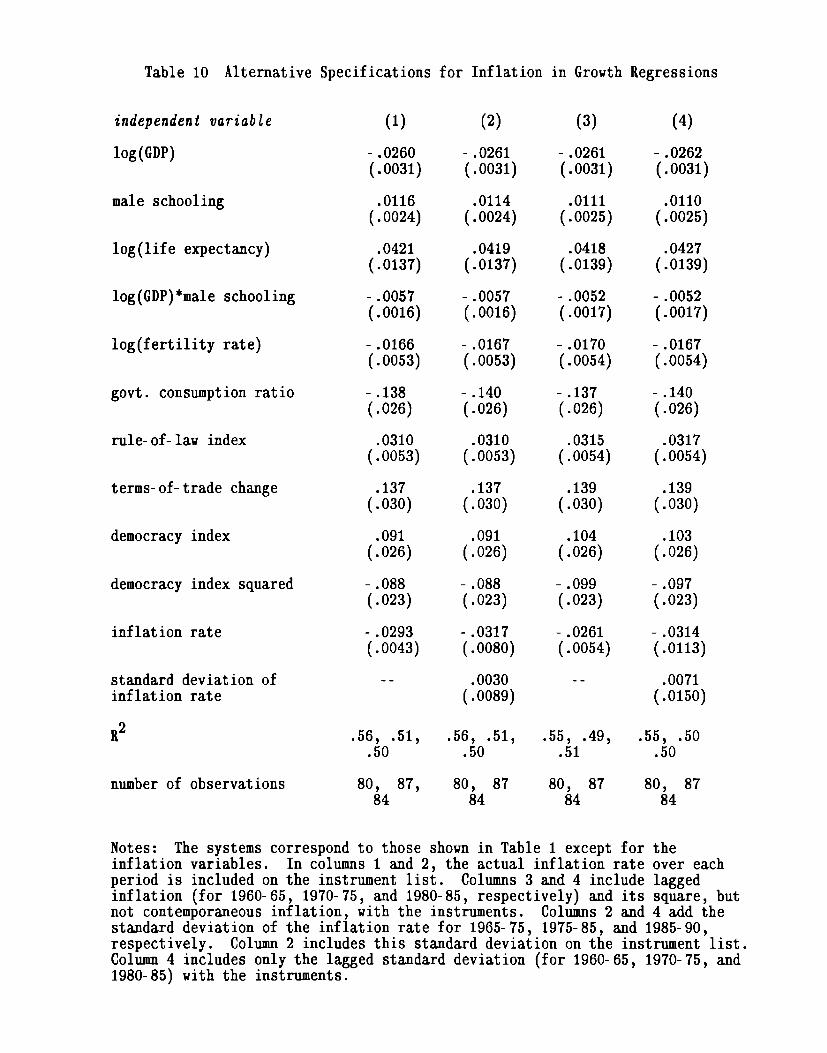

The final essay details the link between inflation/monetary policy and economic

growth. The basic finding is that higher inflation goes along with a lower rate of

economic growth. Moreover, the adverse effect of higher inflation on economic outcomes

is quantitatively important. This pattern shows up clearly for inflation rates in excess

of 15–20% annually, but cannot be isolated statistically for the more moderate

experiences. However, there is no evidence in any range of a positive relation between

itiation and growth. The analysis also suggests that the estimates isolate the direction

of causation from inflation to growth, rather than the reverse.

I. Economic Growth and Convergence

A. Ndastical and Endogenous Growth Theorim

In the 1960s, growth theory consisted mairdy of the neoclassical model, as

developed by Ramsey (1928), Solow (1956), Swan (1956), Cass (1965), and Koopmans

(1965). One feature of this model, which has been exploited seriously as an empirical

hypothesis only in recent years, is the convergence property. The lower the starting

level of real per capita gross domestic product (GDP) the higher is the predicted growth

rate.

If all economies were intrinsically the same, except for their starting capital

intensities, then convergence would apply in an absolute sense; that is, poor places

would tend to grow faster per capita than rich ones. However, if economies differ in

various respects —including propensities to save and have children, willingness to work,

access to technology, and government policies— then the convergence force applies only

in a conditional sense. The growth rate tends to be high if the starting per capita GDP

is low in relation to its long–run or steady+tate position; that is, if an economy begins

far below its own target position. For example, a poor country that also has a low

long–term position—possibly because its public policies are harmful or its saving rate is

low—would not tend to grow rapidly.

The convergence property derives in the neoclassical model from the diminishing

returns to capital. Economies that have less capital per worker (relative to their long-

run capital per worker) tend to have higher rates of return and higher growth rates.

The convergence is condition because the steady+tate levels of capital and output per

worker depend in the neoclassical model on the propensity to save, the growth rate of

population, and the position of the production function+haractenstics that may vary

across economies. Recent extensions of the model suggest the inclusion of additional

sources of cross-country variation, especially government policies with respect to levels

of consumption spending, protection of property rights, and distortions of domestic and

international markets.

The concept of capital in the neoclassical model can be usefully broadened from

physical goods to include human capital in the forms of education, experience, and

health. (See Lucas [1988], Rebelo [1991], Caballe and Santos [1993], Mulligan and

Sala-i-Martin [1993], and Barro and Sala-i-Martin [1995a, Ch. 5].) The economy

tends toward a steady+tate ratio of human to physical capital, but the ratio may

depart from its long–run value in an initial state. The extent of this departure generally

affects the rate at which per capita output approaches its steady+tate value. For

example, a country that starts with a high ratio of human to physical capital (perhaps

because of a war that destroyed mainly physical capital) tends to grow rapidly because

physical capital is more amenable than human capital to rapid expansion. A supporting

force is that the adaptation of foreign technologies is facilitated by a large endowment of

human capital (see Nelson and Phelps [1966] and Benhabib and Spiegel [1994]). This

element implies m interaction effect whereby a country’s growth rate is more sensitive

to its starting level of per capita output the greater is its initial stock of human capital.

Another prediction of the neoclassical model+ven when extended to include

human capital—” 1s that, in the absence of continuing improvements in tethnology, per

capita growth must eventually cease. This prediction, which resembles those of Malthus

(1798) and Ricardo (1817), comes from the assumption of diminishing returns to a broad

concept of capital. The long–run data for many countries indicate, however, that

positive rates of per capita growth can persist over a century or more and that these

growth rates have no clear tendency to decline.

Growth theorists of the 1950s and 1960s recognized this modeling deficiency and

usually patched it up by usuming that technological progress occurred in an

unexplained (exogenous) manner. This device can reconcile the theory with a positive,

possibly constant per capita growth rate in the long run, while retaining the prediction

of conditional convergence. The obvious shortcoming, however, is that the long-run per

capita growth rate is determined entirely by an element-the rate of technological

progress—that comes from outside of the model. (The long-run growth rate of the levd

of output depends dso on the growth rate of population, another element that is

exogenous in the standard theory.) Thus, we end up with a model of growth that

explains everything but long-run growth, an obviously unsatisfactory situation.

Recent work on endogenous growth theory has sought to supply the missing

explanation of long–run growth. In the mtin, this approach provides a theory of

technical progress, one of the central missing elements of the neoclassical model. The

inclusion of a theory of technological change in the neoclassical framework is difficult,

however, because the standard competitive assumptions cannot be mtinttined. (These

=sumptions work fine in the framework of Ramsey, Cass, and Koopmans. )

Technological advance involves the creation of new ideas, which are partially

nonrival and therefore have aspects of public goods. For a given technology-that is,

for a given state of knowledge-it is reasonable to assume constant returns to scale in

the standard, rival factors of production, such as raw labor, broad capital, and lad.

But then, the returns to scale tend to be increasing if the nonrival ideas are included as

factors of production. These increasing returns conflict with perfect competition.

Moreover, the compensation of nonnvd old ideas in accordance with their current

marginal cost of production-zero-will not provide the appropriate reward for the

research effort that underlies the creation of new ideas.

Arrow (1962) and Sheshinski (1967) constructed models in which ideas were

unintended by-products of production or investment, a mechanism described as

learning-bydoing. In these models, each person’s discoveries immediately spilled over

to the entire economy, an instantaneous diffusion process that might be technictiy

feasible because knowledge is nonrival. Romer (1986) showed later that the competitive

7

framework can be retained in this case to determine an equilibrium rate of technological

advance, but the restiting growth rate would typically not be Pareto optimal. More

generally, the competitive framework breaks down if discoveries depend in part on

purposive R&D effort and if an individual’s innovations spread only gradually to other

producers. In this realistic setting, a decentralized theory of technological progress

requires basic changes in the framework to incorporate elements of imperfect

competition. These additions to the theory did not come until Romer’s (1987, 1990)

research in the late 1980s.

The initial wave of the new research-Romer (1986), Lucas (1988), Rebelo

(1991)—built on the work of Arrow (1962), Sheshinski (1967), and Uzawa (1965) and

did not really introduce a theory of technological change. In these models, growth may

go on indefinitely because the returns to investment in a broad class of capital goods,

which includes human capital, do not necessarily diminish as economies develop. (This

idea goes back to Knight [1944].) Spillovers of knowledge across producers and external

benefits horn human capital are parts of this process, but only because they help to

avoid the tendency for diminishing returns to capital.

The incorporation of R&D theories and imperfect competition into the growth

framework began with Romer (1987, 1990) and includes significant contributions by

Aghion and Hewitt (1992) and Grossman and Helpman (1991, Chapters 3 and 4). Barro

and Sala–i-Martin (1995a, Chs. 6, 7) provide expositions and extensions of these

models. In these settings, t ethnological advance results from purposive R&D activity,

and this activity is rewarded, along the lines of Schumpeter (1934), by some form of

e*post monopoly power. If there is no tendency to run out of ideas, then growth rates

can remain positive in the long run. The rate of growth and the underlying amount of

inventive activity tend, however, not to be Pareto optimal because of distortions related

to the creation of the new goods and methods of production. In these frameworks, the

8

long-term growth rate depends on governmental actions, such as taxation, maintenance

of law and order, provision of infrastructure services, protection of intellectual property

rights, and regulations of international trade, financial markets, and other aspects of the

economy. The government therefore has great potential for good or ill through its

influence on the long-term rate of growth.

One shortcoming of the early versions of endogenous growth theories is that they

no longer predicted conditional convergence. Since this behavior is a strong empirical

regularity in the data for countries and regions, it was important to extend the new

theories to restore the convergence property. One such extension involves the diffusion

of technology (see Barro and Sala-i-Martin [1995b]). Whereas the analysis of discovery

relates to the rate of technological progress in leading+dge economies, the study of

diffusion pertains to the manner in which follower economies share by imitation in these

advmces. Since imitation tends to be cheaper than innovation, the diffusion models

predict a form of condition convergence that resembles the predictions of the

neoclassical growth model. Therefore, this framework combines the long–run growth of

the endogenous growth theories (from the discovery of ideas in the leading+dge

economies) with the convergence behavior of the neoclassical growth model (from the

gradual imitation by followers).

Endogenous growth theories that include the discovery of new ideu and methods

of production are important for providing possible explanations for long–term growth.

Yet the recent cross-country empirical work on growth has received more inspiration

from the older, neoclassical model, as extended to include government policies, human

capital, and the diffusion of technology. Theories of basic technological change seem

most important for understanding why the world as a whole can continue to grow

indefinitely in per capita terms. But these theories have less to do with the

determination of relative rates of growth across countries, the key element studied in

9

cross-country st atisticd analyses. The remainder of this essay deals with the findings

from this kind of cross-country empirical work.

B. Framework for the Analytis of Growth Across Countries

The framework for the determination of growth follows the extended version of the

neoclassical model as already described. In equation form, the model can be represented

as

(1) DY = f(Y) Y*),

where Dy is the growth rate of per capita output, y is the current level of per capita

out put, and y* is the long-run or steady+t ate level of per capita output. 1 The growth

rate, Dy, is diminishing in y for given y* and rising in y* for given y. The target value

y* depends on an array of choice and environmental variables. The private sector’s

choices include saving rates, labor supply, and fertility rates, each of which depends on

preferences and costs. The government’s choices involve spending in various categories,

tax rates, the extent of distortions of markets and business decisions, maintenance of the

rule of law and property rights, and the degree of political freedom. Also relevmt for an

open economy is the terms of trade, typically given to a small country by external

conditions.

For a given initial level of per capita output, y, an increase in the st eady%t ate

level, y*, rtises the per capita growth rate over a transition interval. For example, if

the government improves the climate for business activity+ay by reducing the burdens

from regdation, corruption, and taxation, or by enhancing property rights-the growth

lWit h exogenous, labor-augmenting t echnologicd progress, the level of output per workergrows in the long run, but the level of output per e~~ectiveworker approaches a constant,y*. Hence, y* should be interpreted in this generalized sense.

10

rate increases for awhile. Similar effects arise if people decide to have fewer children or

(at least in a closed economy) to save a larger fraction of their incomes.

In these cases, the increase in the target, y*, translates into a transitional increase

in the economy’s growth rate. As output, y, rises, the workings of diminishing returns

eventually restore the growth rate, Dy, to a value determined by the rate of

technological progress. Since the transitions tend to be lengthy, the growth effects from

shifts in government policy or private behavior persist for a long time.

For given values of the choice and environmental variables-and) hence, y*—a

higher starting level of per capita output, y, implies a lower per capita growth rate.

This effect corresponds to conditional convergence. Note, however, that poor countries

would not grow rapidly on average if they tend also to have low steady+tate

positions, y*. In fact, a low level of y* expltins why a country would typically have a

low observed value of y in some arbitrarily chosen initial period.

The last result shows that the framework can be reconciled with the now familiar

lack of wrrelation between the growth rate and initial level of real per capita GDP

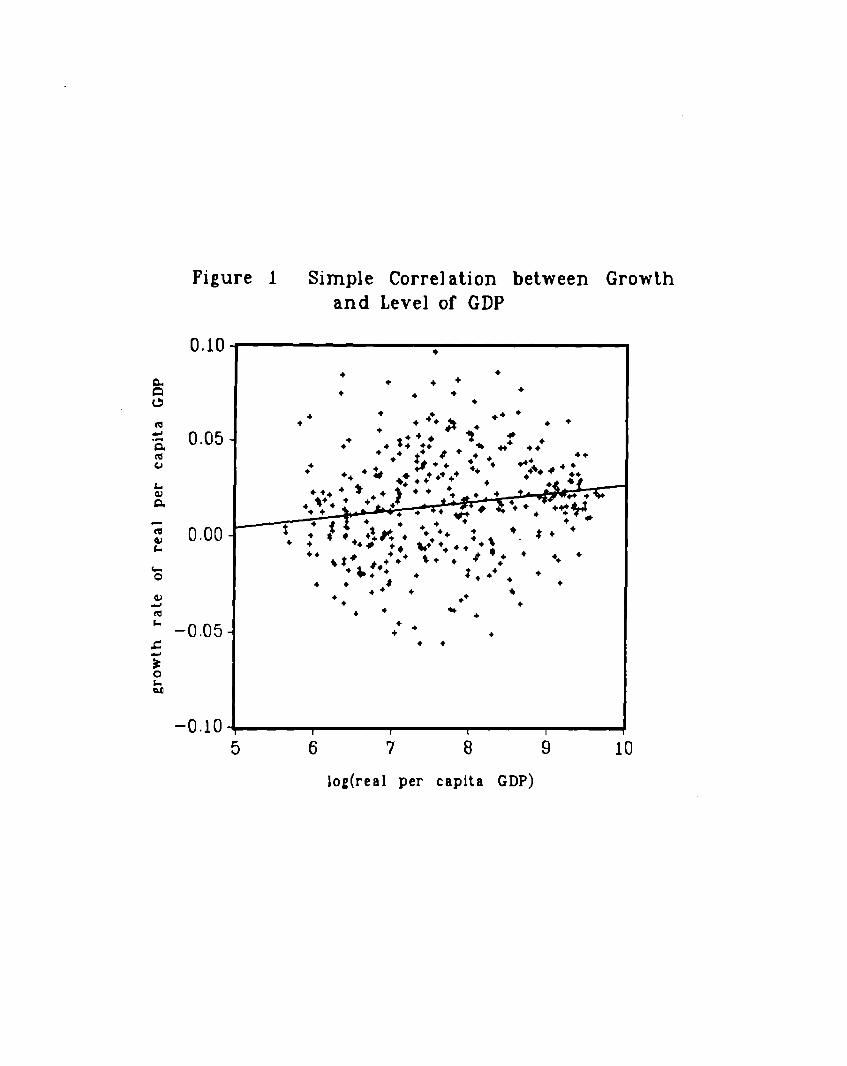

across a large number of countries over the period 1960 to 1990. Figure 1 shows that

this relationship is virtually nil. ~ (The slope actually hw the wrong sign+lightly

positiv~but is not statistically significant. ) The interpretation from the standpoint of

the neoclassical model is that the initially poor countries, which show up closer to the

origin along the horizontal tis, are not systematically far below their steady+tate

positions and therefore do not tend to grow relatively fast. The isolation of the

Whe data on real per capita GDP are the internationally comparable values generated bySummers and Heston (1993). The vertical axis in Figure 1 cent ains observations on percapita growth rates for 1965–75, 1975-85, and 1985–90, the three periods used in thedettiled empirical analysis described below. The horizontal tis shows the correspondingvalues of the logarithm of per capita GDP in 1965, 1975, and 1985.

11

convergence force requires a conditioning on the determinants of the steady state, as in

the crosscountry empincd analysis discussed in the next section.

Even if convergence held in an absolute sense-that is, if y* were identical across

economies and the poorer places tended accordingly to grow faster-the dispersion of

per capita product wodd not necessarily narrow over time. The evolution of dispersion,

or inequality, depends on a weighing of the convergence force against effects horn the

shocks that impinge on each economy. These shocks, if independent across economies,

tend to create dispersion and therefore work agtinst the equalizing pressure from

convergence.

The idea that the tendency for the poor to grow faster than the rich implies a

negative trend in inequality is a fallacy; in fact, it is Gdton’s fallacy, as discussed in the

growth contut by Quah (1994) and Hart (1995). Gdton’s (1886; 1889, Ch. VII)

research indicated that the deviation of children’s heights (and other physical and

mental characteristics) from the mean of the population were positively correlated with

the parent’s deviation, but the amount of deviation tended to regress+r converge

toward zero. Nevertheless, the poptiation’s distribution of heights did not tend

systematically to narrow over time.

The explanation of these facts is that a measure of the population’s dispersion—

say the standard deviation of the log of height (or GDP) —would tend to adjust toward

a long–run value that depends on the rapidity of the reversion to the mean (the rate of

convergence) and the variance of random shocks to height (or GDP). If the

determinants of the long–run distribution do not change, then dispersion would tend to

rise or fti depending on whether it happened to start below or above its long–run value.

Moreover, if the underlying determinants stay constant for a long time, then the

observed distribution for a large population would remain fixed (despite the presence of

the convergence tendency).

12

Empirically, for 114 countries with data, the standard deviation of the log of real

per capita GDP rose from 0.89 in 1960 to 1.14 in 1990. This observation of increased

inequality does not re~ct the convergence implications of the neoclassical growth

model—partly because the predicted convergence is only conditional and partly because

the poor tending to grow faster than the rich is not the same thing as a declining trend

in inequality.

C. Empirical Findings on Growth across Countries

Table 1 shows restits from regressions that use the general framework of

equation (1) from the previous section. The regressions apply to a panel of roughly 100

countries observed from 1960 to 1990.s The dependent variables a-re the growth rates of

real per capita GDP over three periods: 1965–75, 1975-85, and 1985–90. 1 (The first

period begins in 1965, rather than 1960, so that the 1960 value of real per capita GDP

can be used as an instrument; see below. ) Henceforth, the term GDP will be used as a

shorthand to refer to real per capita GDP.

Some previous analysis, such as Barro (1991), used a cross-sectional framework;

that is, the growth rate and the explanatory variables were observed ody once per

country. The main reason to extend to a panel setup is to expand the sample

information. Although the main evidence turns out to come horn the cross+ectional

(between+ountry) variation, the time-series (within-country) dimension provides some

additional information. This information is greatest for variables, such as the terms of

trade and inflation, that have varied a good deal over time within countries.

3The data ~d detailed definitions of the variables Me contained in the B~ro-Lee data set,which is available via anonymous FTP from the National Bureau of Economic Research.

lMost oft he GDP figures are from version 5.6 of the Surnmers-Heston data set (seeSummers and Heston [1991, 1993] for general descriptions). World Bank figures on redGDP growth rates (based on domestic accounts only) are used for 1985–90 when theSummers-Heston figures are unavailable.

13

The underlying theory relates to long–term growth, and the precise timing

between growth and its determinants is not well specified at the high frequencies

characteristic of “business cycles. “ For example, relationships at the annual frequency

wotid likely be dominated by mistiming and, hence, Wectively by measurement error.

In addition, many of the variables considered+uch as fertility rates, life expectancy,

and education attainment-are not actually measured for many countries at periods

finer than 5 or 10 years. These considerations suggest a focus on the determination of

growth rates over fairly long intervals. As a compromise with the quest for additiond

information, I settled on periods of five or ten years; specifically, growth rates were

considered for 1965–75 and 1975-85 and for a final five-year period, 1985–90. When

the data through 1995 become available, the third period will be lengthened to 1985–95.

The estimation uses an instrumental-variable technique, where some of the

instruments are earlier values of the regressors. (The method is t hree-st age least

squares, except that each equation contains a different set of instruments; see the notes

to Table 1 for details. ) This approach may be satisfactory because the residuals from

the growth-rate equations are essentially uncorrelated across the periods. In any event,

the regressions describe the relation between growth rates and prior values of the

explanatory variables.

The regression shown in column 1 includes explanatory variables that can be

interpreted as initial values of state variables or as choice and environmental variables.

The state variables include the initial level of GDP and measures of human capital in

the forms of schooling and health. The GDP level reflects endowments of physical

capital and natural resources (and dso depends on effort and the unobserved level of

technology). The choice and environmental variables me the fertility rate, government

consumption spending, an index of the maintenance of the rule of law, the change in the

14

terms of trade, an index of democracy (political rights), and the inflation rate. The

roles of democracy and itiation will be discussed in the subsequent essays.

1. Initial kel of GDP

For given values of the other explanatory variables, the neoclassical model predicts

a negative coefficient on initial GDP, which enters in the system in logarithmic form. s

The coefficient on the log of initial GDP has the interpretation of a conditional rate of

convergence. If the other explanatory variables are held constant, then the economy

tends to approach its long-run position at the rate indicated by the magnitude of the

coefficient. d The estimated cticient of -0.025 (se. = 0.003) is highly significant and

implies a condition rate of convergence of 2.570 per year. T The rate of convergence is

slow in the sense that it would take the economy 27 years to get half way toward the

steady+tate level of output and 89 years to get 9070 of the way. Similarly slow rates of

convergence have been found for regional data, such as the U.S. states, Canadian

protinces, Japanese prefectures, and regions of the mtin western European countries

(see Barro and Sala-i-Martin [1995a, Ch. 11]).

Figure 2 shows the partial relation between growth and the starting level of GDP,

as implied by the regression from column 1 of Table 1. The horizontal axis plots

log(GDP) for 1965, 1975, and 1985 for the observations included in the regression

sThe variable log(GDP) in Table 1 refers to 1965 in the first period, 1975 in the secondperiod, and 1985 in the third period. Five-year earlier values of log(GDP) are used asinstruments. The use of these instruments lessens the estimation problems associated withtemporary measurement error in GDP.

13Afull treatment of convergence would also require an analysis of how the variousexplanatory variables+uch as schooling, health, and fertility—respond to thedevelopment of the economy.

TThis result is ordy approximate because the growth rate is observed as an average over tenor five years, rather than at a point in time. The implied instantaneous rate ofmnvergence is slightly higher than the value indicated by the coefficient. See Barro andSala-i-Martin (1995a, Ch. 2) for a discussion.

15

sample. The vertical tis shows the corresponding growth rate of GDP after filtering

out the puts explained by all explanatory variables other than log(GDP). s Thus, the

negative slope shows the conditional convergence relation; that is, the effect of log(GDP)

on the growth rate for given values of the other independent variables. In contrast to

the lack of a simple correlation in Figure 1, the conditioned convergence relation in

Figure 2 is clearly defined in the graph, Also, the graph indicates that the relation is

not driven by a few outliers and does not appear to be nonlinear.

2. Initial kel of Human Capital

Initial human capital appears in three variables in the system: average years of

attainment for males aged 25 and over in secondary and higher schools at the start of

each period, the log of life expectancy at birth at the start of each period (an indicator

of health status), g and an interaction between the log of initial GDP and the years of

male secondary and higher schooling. The data on yeas of schooling are updated and

improved versions of the figures reported in Barro and Lee (1993).

The results show a significantly positive effect on growth from the years of

schooling at the secondary and higher level for males aged 25 and over (0.0118 [0.0025]). 10

On impact, an extra year of male upper–level schooling is therefore estimated to raise

the growth rate by a substantial 1.2 percentage points per year. (In 1990, the mean of

the schooling variable was 1.9 years with a st andard deviation of 1.3

BThe residual is calculated from the regression system that contains dl of the variables,including the log of initial GDP. But the contribution from initial GDP is left out tocompute the variable on the vertical axis in the scatter diagram. The residud has alsobeen normalized to have a zero mean. The fitted straight line shown in the figure comesfrom an ordinary–least-squares (OLS) regression of the residual on the log of initial GDP.

gThe results are similar if the infant mort alit y rat e is used instead of life expect anCy as ameasure of health status.

10Schooling of those aged 25 and over has somewhat more explanatory power than schoolingof those aged 15 and over.

16

years. ) The partial relation between the growth rate and the schooling variable

constructed analogously to the method described for log(GDP) in n. 8+s shown in

Figure 3.

Male primary schooling (or persons aged 25 and over) has an insignificant effect if

it is added to the system; the estimated coefficient is +.0005 (0.0011), whereas that on

upper–level schooling remains similar to that found before (0.0119 [0.0025]). Thus,

growth is predicted by male schooling at the upper levels but not by male schooling at

the primary level. Howe\’er, primary schooling is indirectly growth enhancing because it

is a prerequisitee for training at the secondary and higher levels.

More surprisingly, female education at various levels is not significantly related to

subsequent growth. For example, if years of schooling at the secondary and higher levels

for females aged 25 and over is added to the system shown in column 1 of Table 1, then

the estimated coefficient of this variable is +.0023 (0.0046), whereas that for males

remains significantly positive, 0.0132 (0.0036). For primary schooling of women aged 25

and over, the estimated coefficient is -0.0001 (0.0012), whereas that for men (25 and

over for secondary and higher schools) is 0.0118 (0.0025). Thus, these findings do not

support the hypothesis that education of women is a key to economic growth. Ii

Some additional results indicate that female schooling is important for other

indicators of economic development, such as fertility, infant mort tit y, and political

freedom (see the next essay). Specifically, female primary education has a strong

negative relation with the fertility rate (see Schultz [1989], Behrman [1990], and Barro

and Lee [1994]). A reasonable inference from this relation is that female education

wotid spur emnomic growth by lowering fertility, and this effect is not captured in the

llIn e~lier res~ts, Barro and Lee ( 1994) found that the estimated coefficient on femalesecondary and higher schoolin was significantly negative. With the revised data on

feducation, the estimated fema e coefficients are essentially zero.

17

regressions shown in Table 1 because the fertility rate is already held constant. If the

fertility rate is omitted from the system, then the ~timated coefficient on female

primary schooling (the level of female schooling that tiects fertility inversely) is 0.0012

(0.0012), which is positive but not significantly different horn zero. Thus, there is ordy

slight evidence that female education enhances economic growth through this indirect

channel.

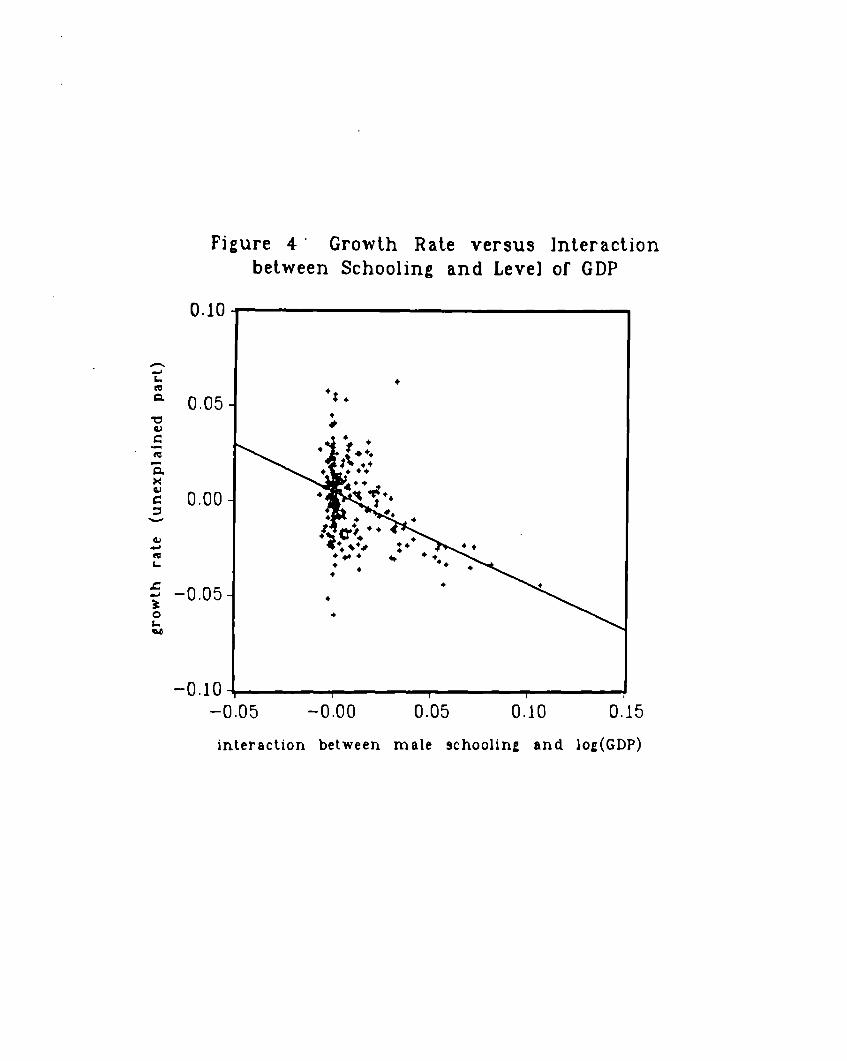

Returning to column 1 of Table 1, the significantly negative estimated coefficient

of the interaction term between mde schooling and log(GDP), -0.0062 (0.0017), implies

that more years of school raise the sensitivityy of growth to the starting level of GDP.

Starting from a position at the sample mean, an extra year of male upper-level

schooling is estimated to raise the magnitude of the convergence coefficient from 0.026

to 0.032. This result supports theories that stress the positive effect of education on an

economy’s ability to absorb new technologies. The partial relation between the growth

rate and the interaction variable appears in Figure 4. (The points at the far right of the

diagram are for the most developed countries+uch as the United States, Caada, and

Sweden—which have high values of GDP and schooling.)

The regression in column 1 also reveals a significantly positive effect on growth

from initial human capital in the form of health. The coefficient on the log of life

expectancy is 0.042 (0.014). As an interpretation, it may be that life expectancy proxies

not only for health status but more broadly for the quality of human capital. The

partial relation between growth and life expectancy is shown in Figure 5.

3. Fertfity Rate

If the population is growing, then a portion of the economy’s investment is used to

provide capital for new workers, rather than to rtise capital per worker. For this reason,

a higher rate of population growth has a negative effect on y*, the steady~t ate level of

18

output per effective worker in the neoclassical growth model. Another, reinforcing,

tiect is that a higher fertility rate means that increased resources must be devoted to

childrearing, rather than to production of goods (see Becker and Barro [1988]). The

regression in mlumn 1 shows a significantly negative coefficient, -0.016 (0.005), on the

log of the total fertility rate. The partial relation between growth and fertility is in

Figure 6.

Fertility decisions are surely endogenous; previous research has shown that fertility

typically declines with measures of prosperity, especially female primary education (see

Schultz [1989], Behrman [1990], and Barro and Lee [1994]). The estimated coefficient of

the fertility rate in the growth regression shows the response to higher fertility for given

values of male schooling, life expectancy, GDP, and so on. Since the average of the

fertility rate over the preceding five years is used as an instrument, the coefficient likely

rdects the impact of fertility on growth, rather than vice versa. (In any event, the

reverse effect would involve the level of GDP, rather than its growth rate, ) Thus,

although population growth cannot be characterized as the most important element in

economic progress, the restits do suggest that an exogenous drop in birth rates would

raise the growth rate of per capita output.

4. Government Co~umption

The regression in column 1 of Table 1 dso shows a significantly negative effect on

growth from the ratio of government consumption (measured exclusive of spending on

education and defense) to GDP. The estimated coefficient is -0.136 (0.026). (The

period-average of the ratio enters into the regression, and the average of the ratio over

the previous five years is used as an instrument.) The particular measure of government

spending is intended to approximate the outlays that do not enhance productivity.

Hence, the conclusion is that a greater volume of nonproductive government

19

spending— and the associated taxation-reduce the growth rate for a given starting

value of GDP. In this sense, big government is bad for growth. The partial relation

between growth and the government consumption variable appears in Figure 7.

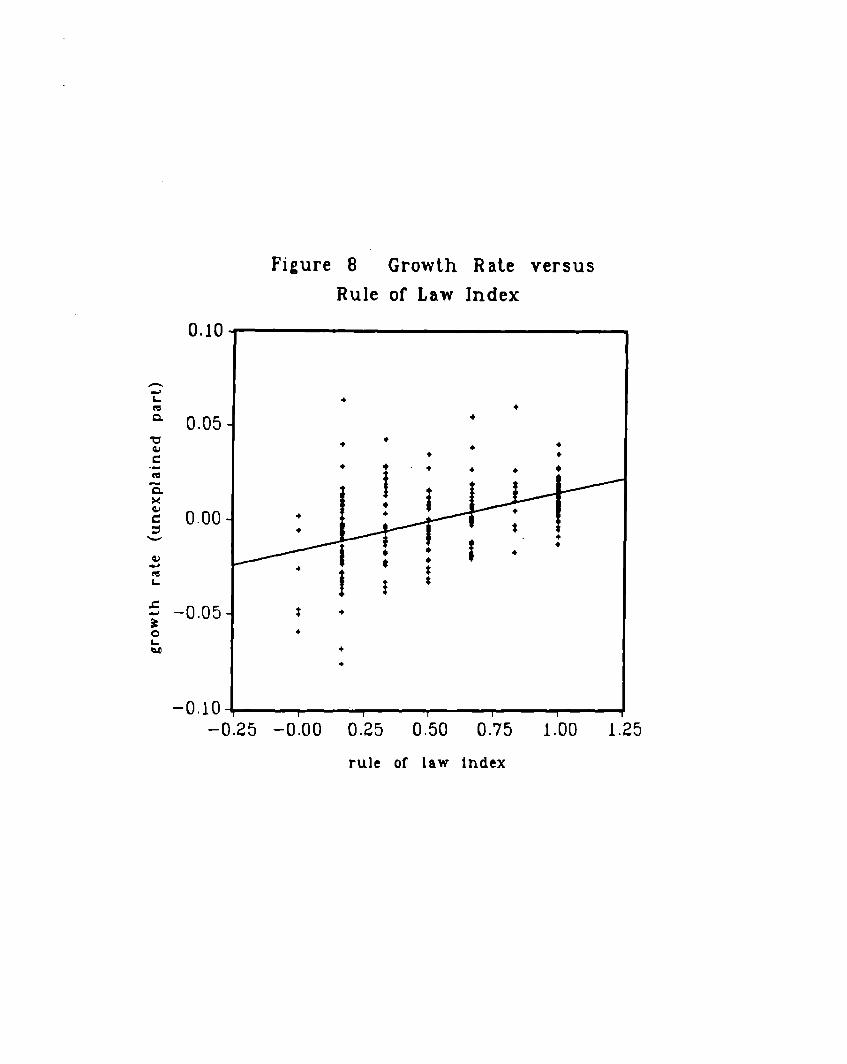

5. The Rd~f-Law Index

Knack and Keefer (1995) discuss a variety of subjective country indexes prepared

for f~paying international investors by International Country Risk Guide. The

mncepts covered include quality of the bureaucracy, political corruption, likelihood of

government repudiation of contracts, risk of government expropriation, and overall

maintenance of the rule of law. (The various time series cover 1982 to 1995 and are

available from Political Risk Services of Syracuse, New York. ) The general idea is to

gauge the attractiveness of a country’s investment climate by considering the

effectiveness of law enforcement, the sanctity of contracts, and the state of other

influences on the security of property rights. Although these data are subjective, they

have the virtue of being prepared contemporaneously by local experts. Moreover, the

willingness of customers to pay subst anti al fees for this information is perhaps some

testament to their validity.

Among the various series available, the indicator for overall maintenance of the

rule of law seemed a ptioti to be most relevant for investment and growth. This

indicator was initially measured in 7 categories on a Oto 6 scale, with 6 the most

favorable. The scale has been revised here to Oto 1, with Oindicating the worst

maintenance of the rule of law and 1 the best.

The rul~f-law variable (observed, because of lack of earlier data, only once for

each count ry in the early 1980s) was included in the regression system reported in

column 1 of Table 1 and has a significantly positive coefficient, 0.0293 (0.0054). (The

other measures of investment risk, including political corruption, and various indicators

20

of political instability are insignificant in these kinds of growth regressions if the

rule-of-law index is dso included.) The interpretation is that greater maintenance of

the rule of law is favorable to growth. Specifically, an improvement by one rank in the

underlying index (corresponding to a rise by 0.167 in the rule–of-law variable) is

estimated to rtise the growth rate on impact by 0.5 percentage points. The partial

relation bet ween growth and the rul~f-law index is in Figure 8. (Note that ordy seven

values for the index are observed. )

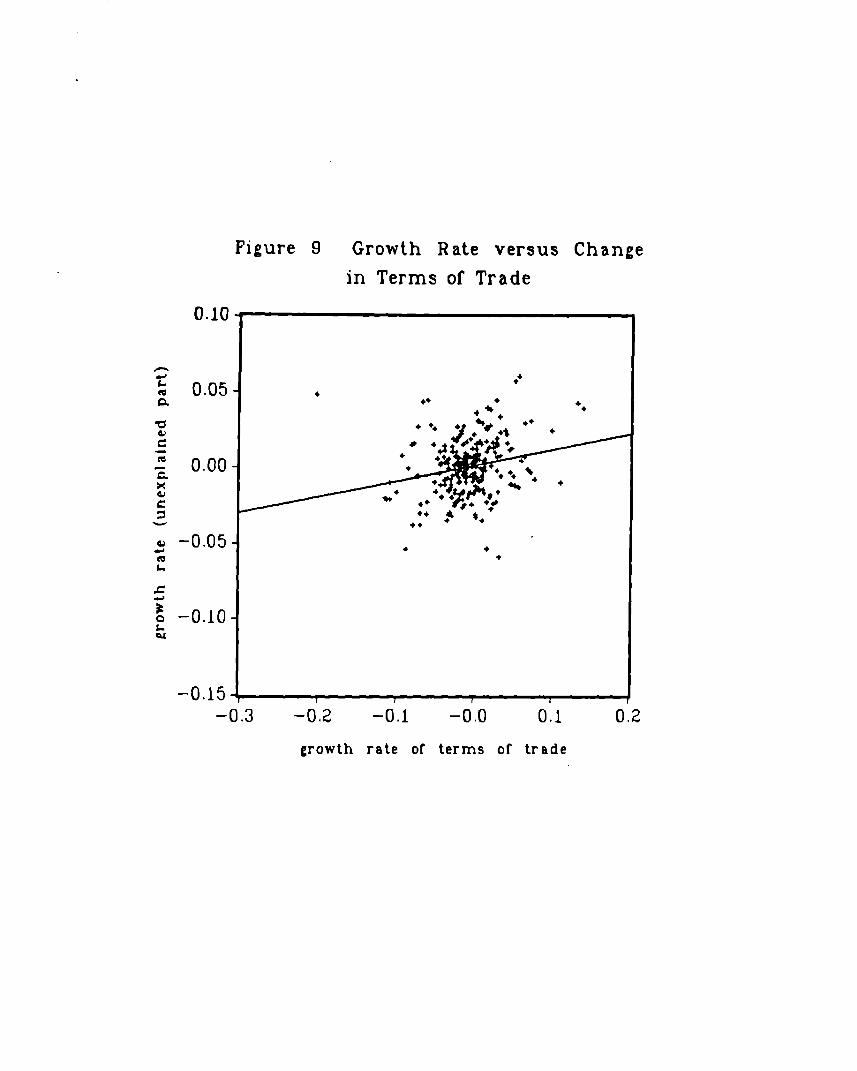

6. Terms of Trade

Changes in the terms of trade have often been stressed as important influences on

developing countries, which t ypic~y specialize their exports in a few primary products.

The effect of a change in the terms of trade—measured as the ratio of export to import

prices+n GDP is, however, not mechanical. If the physical quantities of goods

produced dom~ticdly do not change, then an improvement in the terms of trade raises

real domestic income and probably consumption, but would not affect real GDP.

Movements in real GDP occur ordy if the shift in the terms of trade stimulates a change

in domestic employment and output. For example, an oil-importing country might react

to an increue in the relative price of oil by cutting back on its employment and

production.

The result in column 1 of Table 1 shows a significantly positive coefficient on the

terms of trade: 0.14 (0,03). (The change in the terms of trade is regarded as exogenous

to an individual country’s growth rate and is therefore included as an instrument.)

Thus, an improvement in the terms of trade apparently does stimulate an expansion of

domestic output. The partial relation with growth appears in Figure 9. Although the

terms-of-trade variable is statistically significant, it turns out not to be the key

21

element in the weak growth performance of many poor countries, such as those in Sub

Saharan Africa.

7. ~onal Vtiables

It has often been observed that recent rates of economic growth have been

surprisingly low in Sub Saharan Africa and Latin America and surprisingly high in East

Asia. For 1975-85, the mean per capita growth rate for all 124 countries with data was

1.0%, compared with -0.3% in 43 Sub Saharan African countries, 4.1% in 24 Latin

American countries, and 3.7% in 12 East Asian countries. For 1985–90, the average

growth rate was again 1.0% (for 129 places), compared with O.1% in 40 Sub Saharan

African countries, 0.4% in 29 Latin American countries, and 4.0% in 15 East Asian

countries. An important question is whether these regions continue to look like outliers

once the explanatory variables considered in Table 1 have been taken into account.

In some previous cross-country regression studies, such as Barro (1991), dummy

variables for Sub Saharan Africa and Latin America were found to enter negativdy and

significantly into growth regressions. However, column 2 of Table 1 shows in the

present specification that dummies for these two areas and also for East Asia are

individually insignificant. (The p-value for joint significance of the three dummy

variables is O.11.) Thus, the unusual growth experiences of these three regions is mostly

accounted for by the explanatory variables.

The inclusion of the inflation rate is critical for eliminating the significance of the

Latin America dummy —this interaction is discussed in the next essay. The Latin

America dummy also becomes significant if the fertility rate or the government

consumption ratio is omitted. In the case of Sub Saharan Africa, the government

consumption ratio is the only individual variable whose omission causes the dummy to

22

become significant. For East Asia, the dummy is significant if male schooling, the

rti~f-law indicator, or the democracy variables are deleted.

8. Investmat Ratio

In the neoclassical growth model for a closed economy, the saving rate is

exogenous and equal to the ratio of investment to output. A higher saving rate raises

the steady+tate level of output per effective worker and thereby raises the growth rate

for a given starting value of GDP. Some empirical studies of cross-country growth have

also reported an important positive role for the investment ratio; see, for example,

DeLong and Summers (1991) and Mankiw, Romer, and Weil (1992).

Reverse causation is, however, likely to be important here. A positive coefficient

on the contemporaneous investment ratio in a growth regression may reflect the positive

relation between growth opportunities and investment, rather than the positive effect of

an exogenously higher investment ratio on the growth rate. This reverse effect is

especially likely to apply for open economies. Even if cross-country differences in saving

ratios are exogenous with respect to growth, the decision to invest domesticdly, rather

than abroad, wotid reflect the domestic prospects for returns on investment, which

wotid relate to the domestic opportunities for growth.

The system from column 1 of Table 1 has been expanded to include the penod-

average investment ratio as an explanatory variable. If the instrument list includes the

investment ratio over the previous five years, but not the contemporaneous value, then

the estimated coefficient on the investment variable is positive, but not statistically

significant, 0.027 (0.021). In contrast, the estimated coefficient is almost twice as high

and statistically significant if the contemporaneous investment ratio is included as an

instrument, 0.043 (0.018). These findings suggest that much of the positive estimated

effect of the investment ratio on growth in typical cross-country regressions reflects the

23

reverse relation bet ween growth prospects and investment. Blomstrom, Lipsey, and

Zejan (1993) reach similar conclusions in their study of investment and growth.

To interpret these resdts further, Table 2 shows regression systems in which the

dependent variables are the average ratios of investment to GDP for 1965–74, 1975+4,

and 1985-89. The independent vtiables (aside from the investment ratio) are the same

as those used in Table 1. The key finding in column 1 of Table 2 is that a number of the

variables that are found to enhance the growth rate in Table 1 also appear as stimulants

to investment. In particular, the investment ratio is positively related to life expectancy

(a proxy for the quality of human capital) and the rul~f–law index and negatively

related to the government consumption ratio and the inflation rate. The investment

ratio also follows the same sort of quadratic relation with democracy that showed up for

the growth rate. The effects of democracy are explored in the next essay.

A reasonable interpretation of the results is that some policy variables+uch as

better maintenance of the rule of law, lower government consumption, and price

stability+ncourage economic growth partly by stimtiating investment. However, if

investment is higher for given values of the policy instruments—perhaps because of

variations in thriftiness across economies that lack perfect capital mobility—then the

positive effect on growth is weak, as indicated by the estimated coefficient of 0.027

(0.021) on the investment ratio.

D. Cr-ountry B.egressions and Country Fixed Effects

A comparison of Figures 1 and 2 shows that it is critical to hold fixed the

determinants of the long–run target value, y*, in equation (1) to isolate the conditional

convergence force; that is, the effect of initial GDP, y, on the growth rate, Dy, for a

given y*. Since y and y* tend to be positively correlated, the estimated coefficient on y

would be biased upwards if y* were not held constant. Since the true coefficient on y is

24

negative, the omission of y* tends to generate an underestimate of the rate of

convergence, possibly even to the extent of estimating divergence (a positive coficient

on y) rather than convergence. Hence, the omission of y* can account for the incorrect

(positive) sign in the simple relation between Dy and y shown in Figure 1.

One remaining problem in Figure 2 is that the estimated rate of convergence

would still tend to be underestimated if the measures used to hold fixed y* were

imperfect (w they must be). Specifically, underestimation of the convergence rate

wodd tend to apply if the omitted determinants of y* were still positively correlated

with y after holding fixed the variables included to measure y*. It is hard to get a direct

assessment of the magnitude of this problem, although the isolation of y*–like variables

that have a lot of explanatory power for growth—as highlighted in the previous

discussion+hould lessen the error.

Some researchers prefer to handle this type of estimation problem by allowing for

an unobserved fixed effect for each country (see Knight, Loayza, and Villanueva [1993];

Islam [1995]; and Caselli, Esquivel, and Lefort [1995]). Usually, this treatment is

applied by first differencing all variables in order to eliminate the fixed effect. This

procedure works if the underlying determinants of y*+uch as government policies and

preferences about saving and fertility+o not vary over time within a country. In

practice, problems wotid still exist because unobserved shifts in y* could still be

correlated with the movements in y.

The main drawback of the fixed-effects technique is that it relies on tim~enes

information within countries; that is, it eliminates the cross+ ectional information,

which is the principal strength of the broad crosscountry data. Aside from losing

information and, hence, precision, first differencing of the data tends to emphasize

measurement error over signal. In particular, the estimation becomes more sensitive to

incorrect timing in the relation between growth and its determinants.

25

If first differences of the determinants of y* are retained in the estimation, then

measurement error tends to bias toward zero the estimated coefficients of these

variables. For the estimated coefficient of Dy on y, one should consider a regression of y

(log[GDP]) on its own lag. Measurement error tends to bias this value toward zero and

leads accordingly to an overestimate of the rate of convergence.

Column 1 of Table 3 shows the restits from estimation of a first-differenced

version of the system from column 1 of Table 1. This setup includes two equations—in

the first, the dependent variable is the growth rate of GDP from 1975 to 1985 less that

from 1965 to 1975. In the second, the dependent variable is the growth rate from 1985

to 1990 less that from 1975 to 1985. Similarly, the independent variables are first

differences of the variables that appear in column 1 of Table l—for example, the first

equation contains log(GDP) for 1975 less log(GDP) for 1965. The system is estimated

in a seemingly-unrelated (SUR) framework, which allows for correlation of the errors

across the two equations. (Since the residuals from the growt h–rate equations in

Table 1 were essentially uncorrelated across the time periods, the residuals for the two

equations in column 1 of Table 3 have a strong negative correlation. )

Column 2 of Table 3 shows the results from ordinary-least+quares (OLS)

estimation of a pure cross section, which contains one observation for each country. In

this case, the dependent and independent variables are means over the three time

periods of the variables used in column 1 of Table 1.

Fintiy, column 3 of Table 3 is the same as column 1 of Table 1, except that the

estimation is by the SUR technique instead of instrumental variables. This setup is

basically a weighted combination of the tim~eries information from column 1 of

Table 3 with the cross-sectional information from column 2 of the table. In the main,

these estimates are close to those shown in column 1 of Table 1. The principal

26

differences from the use of instruments show up in the estimated coefficients of the

democracy and inflation variables.

If one compares the estimated coefficients from the first-difference specification

with those from the cross section, then the biggest discrepancy is in the estimated

convergence rate: -0.044 (0.007) in column 1 versus -0.022 (0.004) in mlumn 2. The

hypothesis of equality for these coefficients is rejected by a Wald test with a p-value of

0.000 (see column 4 of the table). For the other independent variables, the ordy cases in

which the estimated coefficients from the two specifications differ significantly at the 5%

level (when variables are considered one at a time) are those for life expectancy and

government mnsumption. However, a joint test of equality for all 10 pairs of

coefficients rejects decisively.

The standard errors of the coefficients in columns 1 and 2 indicate the information

available from the tim~eries and cross-sectional dimensions of the panel data, For

many of the variables—log( GDP), male schooling, log(life expectancy), the interaction

bet ween log(GDP) and male schooling, log(fertilit y rate), and the government

consumption ratiethe standard errors are much smaller in column 2 than in column 1,

This pattern indicates that the cross-country (between) variation in these independent

variables is much more informative than the time-series (Within+ountry) variation.

The extreme situation is for the rtie–of-law variable, which has no tim~enes

dimension (U presently measured) and therefore effectively has an infinite standard

error in the first-difference form. The only case in which the standard error is

noticeably smaller in column 1 is for the terms of trade; the variations here relate more

to changes over time than to differences across countries. For democracy and inflation,

the standard errors are similar in the two contexts.

Many researchers seem to prefer the results from variants of first-difference

specifications, as in column 1 of Table 3, because of their concern with the possible bias

27

from correlated fixed effects. The high estimated convergent coefficient from this

mlumn4.4% per year-is similar to that reported from more sophisticated, but

related, techniques by Knight, Loayza, and Villanueva (1993, p. 529); Islam (1995,

Tables III and IV); and Caselli, Esquivel, and Lefort (1995, Tables 3 and 4). However,

the higher magnitude of these convergence coefficients, relative to those found from the

panel estimation in column 3 of Table 3 or column 1 of Table 1, may reflect an increase

in the relative amount of measurement error from the exclusion of the cross-sectional

information. That is, instead of eliminating the fixed-effects bias (which tends to

underestimate the convergence rate), the first-difference procedure may mainly

aaggerate the measurement-error bias (which tends to overestimate the convergence

rate).

The results in column 1 also show that it is hard to isolate effects from the

explanatory variables other than lagged GDP in a pure tim~eries context. The only

estimated coefficients that are significant at the 5% critical level are those for the

fertility rate, the terms of trade, and the inflation rate. Life expectancy is marginally

significant with the wrong sign! One reason for these findings is that the time series

offers little variation in many of the variables. In addition, the model likely misspecifies

the timing between growth and its determinants, and this error is much more important

for tim~enes estimation than in a cross section.

Undoubtedly, the confidence in the restits would be greater if the estimated

coefficients from first-difference and cross+ectional forms did not differ significantly.

Improvements in specification-for example, with regard to the lag structure between

growth and its determinants—may produce more uniform results. But, at this stage,

there seems to be no basis for preferring the first+ifference estimates to the

cross-sectional ones. I have focused on panel result s+olumn 3 of Table 3 or column 1

of Table l—as a weighing of these two imperfect sources of information, where the

weights are determined (by means of the SUR or thre~tage least+ quares procedures)

from the relative informativeness of the t wo sources.

E. Growth Projections

The results from column 1 of Table 1 can be used to construct long–term forecasts

of economic growth for individual countries. These predictions have been constructed

by using recent observations of the aplanatory variables+DP in 1994 (or sometimes

earlier), schooling in 1990, life expectancy and fertility in 1993, CPI inflation through

1993 or 1994, the rul~f-law indicator for 1995, the democracy index for 1994, and

government consumption in the late 1980s.12 Table 4 shows the 20 predicted best and

worst performers from 1996 to 2000 out of the 86 countries that have the necessary data

to make these projections. 13 There is, however, a substantial margin of error (of as

much as two percentage points) in the prediction for an individual country.

For aU 86 countries, the average forecast of per capita growth is 2.4% per year.

The breakdown by region is 3.7% for 18 Asian countries, 2.9% for 22 Latin American

countries, 2.4% for 21 OECD countries (not including Japan, Turkey, and Mexico), and

0.5% for 18 Sub Saharan African countries.

It is no surprise that many old and new tigers of East Asia are forecasted to grow

rapidly-South Korea, Malaysia, Singapore, Thailand, Hong Kong, and Taiwan are on

the high~rowth list. (Japan falls short with 3.2% growth. ) The unexpected finding is

the presence in the high-growth group of Asian laggards of the past: the Philippines,

i2The constantterm is the one applicable to the 1985–90 equation. More accurate growthforecasts might be obtainable frdfi a full vector–autogressive (VAR) system that r~ates allvariables to lagged observations.

lqJordan codd be included as the 87th country and actually has the highest growth forecast,6.9% per year. However, Jordan was omitted from Table 4 because the data for the westbank are intermingled with those for Jordan proper.

29

India, Sri Lanka, and Pakistan. (China and Vietnam would likely also appear but are

excluded because of missing data.)

South Korea places at the top with 6.2% growth because it has high educational

attainment, strong economic rights, low government spending, low fertility, high

investment, and low inflation. Although their underlying growth determinants are less

favorable, the Philippines, India, and Sri Lanka place nearly as high in projected growth

rates because their levels of per capita GDP are only one-eighth to one-quarter as large

as South Korea’s. These are cases in which the convergence force generates rapid

growth.

The high-growth list also has substantial representation in South America: Peru,

Argentina, Chile, Paraguay, Guyana, and Ecuador. A key assumption here is that the

recently achieved macroeconomic stability—as reflected in relatively low inflation

rates—will be maintained. As a contr=t, Brazil appears on the low-growth list with

roughly zero per capita growth. Aside from low school attainment, a major element is

projected inflation of around 50%.

In central Europe, post–transformation Poland appears as a prospective fast

grower, and Hungary (with 3.5% projected growth) just misses the list. Other count ries,

such as the Czech Republic, would likely have appeared but are excluded because of lack

of data.

On the low-growth list, 13 of the 20 countries are in Sub Saharan Africa. (Other

countries+uch as Nigeria, Rwanda, and Somalia —wotid likely have been included if

not for their missing data. ) Sierra Leone, as a prototype, has weak enforcement of

property rights, low school attainment, high fertility, low life expectancy, no political

freedom, high government consumption, moderately high inflation, and virtually no

30

investment. Being poor, which Sierra Leone and the other African countries surely are,

is not enough to generate high growth.

Among OECD countries, the ody place on the high-growth list is Greece. (Sptin

comes close with 3.8% growth.) Many of the advanced economies nearly made the

low-growth list: Denmark at 1.3%, Norway at 1.4%, the United States at 1.4%, Sweden

at 1.770, Finland at 1.9Y0,the United Kingdom at 2.070, Canada at 2.070, Germany at

2.1%, Italy at 2.2%, and Frace at 2.4%. (Note that the growth rate of the level of

GDP adds the growth rate of population; roughly 1% per year for the United States and

smaller amounts in western Europe.)

One can also use the results to ask, somewhat more speculatively, whether some

changes in institutions or policies could move the United States or the United Kingdom

or another advanced country to the high-growth list; that is, raise the long–t erm per

capita growth rate from 1–1 /2 to 270 to around 470. Unfortunate ely, the answer seems to

be no. The institutions and policies in the advanced countries are already reasonably

good (despite possible excesses of transfer programs and regulations), and long–term per

capita growth much above 2~0 seems to be incompatible with the prosperity that has

already been attained.

It would probably be feasible to raise the long–term growth rate by a few tenths of

a percentage point by cutting tax rates and nonproductive government spending or by

eliminating harmful regulations. (Some of these variables may be important but could

not be measured for the cross+ountr y empirical work discussed above. ) Moreover,

increases in growth rates by a few tenths of a percentage point matter a lot in the long

run and are surely worth the trouble. On the negative side, it would be possible to

lower the growth rate by a few tenths of a percentage point by moving away from price

stability or by interfering further with free markets. There is no evidence that increases

in infrastructure investment, research subsidies, or education spending would help a

31

lot. Basically, 2% per capita growth seems to be about as good as it gets in the long run

for a country that is already rich,

32

II. The IntemlaY between Economic and Political Develo~ment

A. Theoretical Notions

Economic freedoms, in the form of free markets and small governments that focus

on the maintenance of propert y rights, are often t bought to encourage economic growth.

This view receives support from the empirical findings discussed in the previous essay.

The connection between political and economic freedom is more controversial, as

stressed in the theoretical parts of the recent surveys by Sirowy and Inkeles (1990) and

Przeworski and Limongi (1993). Some observers, such as Friedman (1962), believe that

the two freedoms are mutually reinforcing. In this view, an expansion of political

rights-more “democracy” —fosters economic rights and tends thereby to stimulate

growth. But the growth retarding aspects of democracy have also been stressed. These

features involve the tendency to enact rich–to-poor redistributions of income (including

land reforms) in systems of majority voting and the enhanced role of interest groups in

systems with represent ative legislatures.

Authoritarian regimes may partially avoid these drawbacks of democracy.

Moreover, nothing in principle prevents nondemocratic governments from maintaining

economic freedoms and private property. A diet at or does not have to engage in central

planning. Examples of autocracies that have expanded economic freedoms include the

Pinochet government in Chile, the Fujimori administration in Peru, the Shah’s regime

in Iran, and several previous and current governments in East Asia. Furthermore, as

Schwarz (1992) observes, most OECD countries began thtir modern economic

development in systems with limited political rights and became full-fledged

represent ative democracies only much later.

33

The effects of autocracy on growth are adverse, however, if a dictator uses his

power to steal the nation’s wealth and to carry out nonproductive investments. Many

governments in Africa, some in Latin America, some in the formerly planned economies

of eastern Europe, and the Marcos administration in the Philippines seem to fit this

pattern. Thus, history suggests that dictators come in two types, one whose personal

ob@ctives often conflict with growth promotion and another whose interests dictate a

preoccupation with economic development. This perspective accords with Sah’s (1991,

pp. 70-71) view that dictatorship is a form of risky investment. In any event, the

theory that determines which kind of dictatorship will prevail seems to be missing.

Democratic institutions provide a check on governmental power and thereby limit

the potential of public officials to amass personal wealth and to carry out unpopular

policies. Since at least some policies that stimulate growth will also be politically

popular, more political rights tend to be growth enhancing on this count. Thus, the net

effect of democracy on growth is theoretically inconclusive.

The interplay between political institutions and economic outcomes also involves

the effect of the standard of living on a country’s propensity to experience democracy.

A common view since Lipset’s (1959) research is that prosperity stimtiates democracy;

this idea is often described as the Lipset hypothesis. Lipset (1959, p. 75) apparently

prefers to view it as the Aristotle hypothesis: “From Aristotle down to the present, men

have argued that only in a wealthy society in which relatively few citizens lived in real

poverty could a situation exist in which the mass of the population could intelligently

participate in politics and could develop the self–restraint necessary to avoid

succumbing to the appeals of irresponsible demagogues. ” (For a statement of Aristotle’s

views, see Aristotle [1932, book VI].)

Theoretical models of the effect of prosperit y on democracy are not well developed.

Lipset (1959, pp. 83-84) emphasizes increased education and an erdarged middle class as

34

elements that -pand “receptivity to democratic political tolerance norms” (a phrase

that I wish I understood). He also stresses Tocqueville’s (1835) idea that private

organizations and institutions are important as checks on dictatorship. This point has

been extended by Putnam (1993), who argues that the propensit y for civic activit y is

the key underpinning of good government in the regions of Italy. 1AFor Huber,

Rueschemeyer, and Stephens (1993, pp. 74-75), the crucial concept is that capitalist

development lowers the power of the landlord class and raises the power and ability to

organize of the working and middle classes.

Despite the lack of a compelling underlying theory, the cross-country evidence

examined in the present study confirms that the Lipset hypothesis is a strong empirical

regularity. In particular, increases in various measures of the standard of living tend to

generate a gradual rise in democracy. In contrast, democracies that arise wit bout prior

economic development-sometimes because they are imposed by ex-colonial powers or

international organizations—tend not to last. Given the strength of this empirical

regularity, one would think that clear+ut theoretical analyses ought also to be

attainable. (This seems to be a case where the analysis works in practice but not in

theory.)

B. Effects of Dmocracy on Economic Growth

The principal measure of democracy used in the present study is the indicator of

political rights compiled by Gastil and his followers (1982+3 and subsequent issues)

from 1972 to 1994. A related variable from Bollen (1990) is used for 1960 and 1965.15

lAPutnam’s (1993) empirical work is, however, marred by his tendency to identify goodgoverment with big government.

i15see G~til 1991) for a &scussion of the methods that under~e ~s data sefiesm Inkeles

()1991 provi es an overview of measurement issues on democracy. He finds (p. x) aI ... high degree of agreement produced by the classification of nations as democratic or not,even when democracy is measured in somewhat different ways by different analyst s.”Bollen (1990) suggests that his measures are reasonably comparable to Gastil’s. It is

35

The Gastil concept of political rights is indicated by his basic definition: “Political

rights are rights to participate meaningftiy in the political process. In a democracy this

means the right of W adults to vote and compete for public office, and for elected

represent atives to have a decisive vote on public policies. ” (Gastil, 1986+7 edition,

p. 7.) In addition to the basic definition, the classification scheme rates countries

(somewhat impressionistically) as less democratic if minority parties have little irdluence

on policy.

Gastil applied the concept of political rights on a subjective basis to classify

countries annually into 7 categories, where group 1 is the highest level of political rights

and group 7 is the lowest. The classification is made by Gastil and his associates based

on an array of published and unpublished information about each country. Ufike the

rul~f-law index, which was discussed in the previous essay, the subjective ranking is

not made directly by local observers.

The original ranking from 1 to 7 has been converted here to a scale from Oto 1,

where Ocorresponds to the fewest political rights (Gastil’s rank 7) and 1 to the most

political rights (Gastil’s rank 1). The scale from Oto 1 corresponds to the system used

by Bollen.

Figure 10 shows the time path of the unweighed average across countries of the

democracy index for 1960, 1965, and 1972–94. The number of countries covered rises

horn 99 in 1960 to 109 in 1965 and 138 from 1972 to 1994. The figure shows that the

mean of the democracy index peaked at 0.66 in 1960, fell to a low point of 0.44 in 1975,

and rose subsequently to 0.58 in 1994.

difficult to check comparability directly because the two series do not overlap in time.Moreover, many countries+specially those in Africa+learly experienced ma@r declinesin the extent of democracy horn the 1960s to the 1970s. Thus, no direct inference aboutcomparability can be made from the higher average of Bollen’s figures for the 1960s thanfor Gastil’s numbers for the 1970s.

36

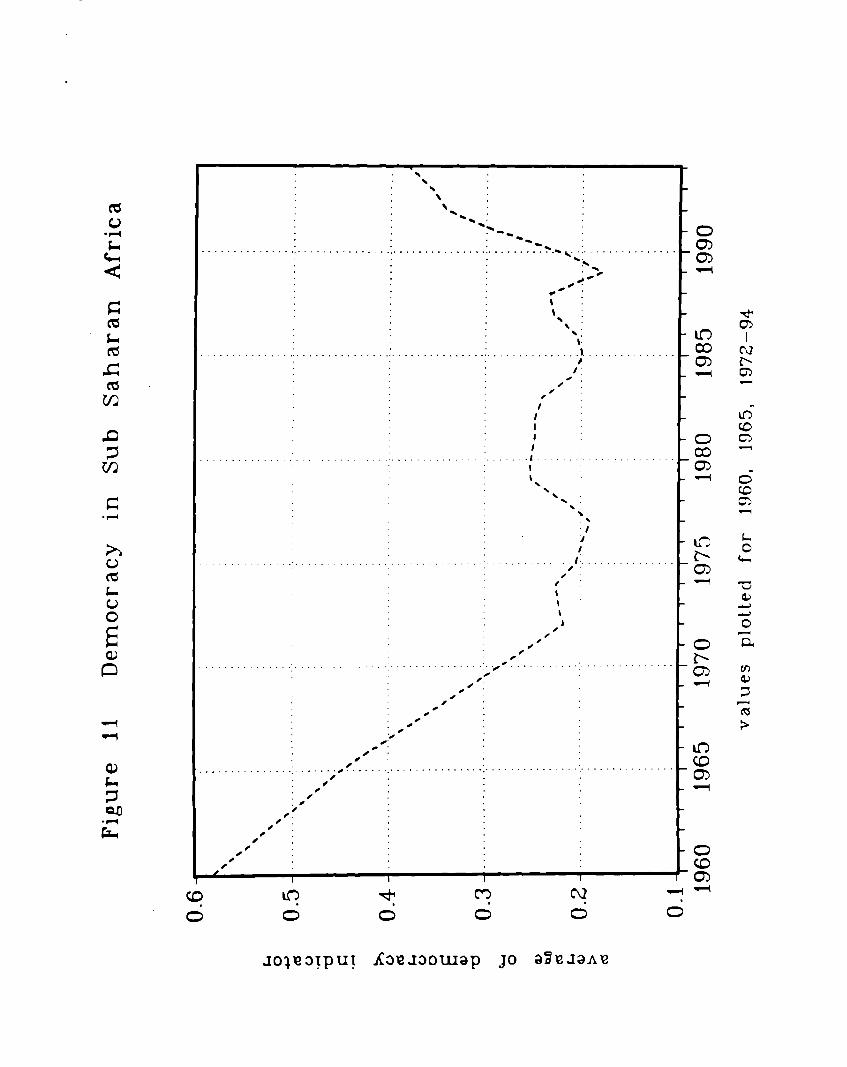

Figures 11 and 12 demonstrate that the main source of the decline in democracy

after 1960 is the experience in Sub Saharan Africa. Figure 11 shows that the average of

the democracy indicator in Sub Saharan Africa peaked at 0.58 in 1960 (26 countries),

then (for 43 countries) feU to low points of 0.19 in 1977 and 0.18 in 1989 before rising to

0.38 in 1994. This pattern emerges because many of the African countries began with

democratic institutions when they became independent in the early 1960s, but most

evolved into one-part y dictatorships by the early 1970s. (See Bollen [1990] for further

discussion.) The democratization in Atica since 1989 has been substantial; whether it

will be sustained is not yet known.

For countries outside of Sub Saharan Africa, Figure 12 shows that the average of

the democracy index fell from 0.68 in 1960 (73 countries) to 0.55 in 1975 (95 countries).

It then returned to 0.69 in 1990, but fell to 0.67 in 1994.

Some of the analysis also uses the Gastil indicator of civil liberties. The definition

here is “civil liberties are rights to free expression, to organize or demonstrate, as well as

rights to a degree of autonomy such as is provided by fxeedom of religion, education,

travel, and other personal rights” (Gastil [1986+7 edition, p.7]). Otherwise, the

sub@ctive approach is the same as the one used for the political rights indicator. The

original scale for the civil liberties index from 1 to 7 has again been converted to Oto 1,

where Orepresents the fewest civil liberties and 1 the most. In practice, as observed by

Inkeles (1991), the indicator for civil liberties turns out to be extremely highly

correlated with that for Political rights.

The previous discussion indicated that the net effect of more political freedom on

growth is theoretically ambiguous. If the indicator for democracy is entered linearly

37

into the regression system of Table 1, then the resulting coefficient estimate turns out to

be negative but statistically insignificant: -0.003 (0.006). 10

The system shown in column 1 of Table 1 allows for a quadratic in the indicator.

In this case, the estimated coefficients on democracy and its square are each statistically

significant. (The p–value for joint significance of the two terms is 0.001. ) The pattern

of restits-a positive coefficient on the line~ term and a negative coefficient on the

square-means that growth is increwing in democracy at low levels of democracy, but

the relation turns negative once a moderate amount of political freedom h~ been

attained. 17 The estimated turning point occurs at an indicator value of approximately

0.5, which corresponds to the levels of democracy in 1994 for Malaysia and Mexico.

Table 2 shows that an analogous nonlinear relation shows up in the effect of

democracy on the investment ratio. The level of democracy that maximizes this ratio is

again sound 0.5.

One way to interpret the results is that, in the worst dictatorships, an increase in

political rights tends to enhance growth and investment because the benefit from

limitations on governmental power is the key matter. But in places that have already

achieved a moderate amount of democracy, a further increase in political rights impairs

growth and investment because the dominant effect comes from the intensified concern

with income redistribution. Thus, growth would likely be reduced by further

democratization beyond the levels attained in 1994 in countries such as Malaysia and

Mexico. Moreover, growth will probably be retarded by the political liberalizations that

occurred by 1994 in places such as Chile, South Korea, and Taiwan. (These countries