Languages

Pages

Legal

POLITECNICO DI MILANO

Scuola di Ingegneria Industriale e dell’Informazione

Corso di Laurea Magistrale in

Ingegneria Gestionale

“Analysis and evolution of the Energy Service

Companies' Italian market”

Relatore: Prof. Davide CHIARONI

Autore: Michele Bassi

Matr. 837629

Anno Accademico 2015 – 2016

2

SUMMARY

1. Figures index ........................................................................................... 4

2. Tables index ............................................................................................. 6

3. Acronyms index ...................................................................................... 7

4. Abstract .................................................................................................... 8

5. Abstract (Italian version) ........................................................................ 9

6. General introduction ............................................................................. 10

7. Introduction and contextualization of the market .............................. 11

7.1 The energy efficiency target and the role of the ESCos .................... 11

7.2 What is an ESCo ............................................................................... 14

7.2.1 Definitions ........................................................................................... 14

7.2.2 Classifications and business models ................................................... 19

7.3 The contracts ..................................................................................... 24

7.3.1 Contracts typologies and financing modes .......................................... 24

7.3.2 The contracts related risks .................................................................. 29

7.3.3 SPINs and EPC+ contracts ................................................................. 32

8. Practical example of an energy efficiency project ............................. 36

9. The state-of-the-art of the Italian Energy Efficiency market .............. 42

10. Methodology of the analysis .............................................................. 58

11. The ESCo-market analysis by industry and by technology ............. 64

11.1 Results and comments by industry .................................................. 64

11.1.1 The “revenues-proportional” approach .............................................. 64

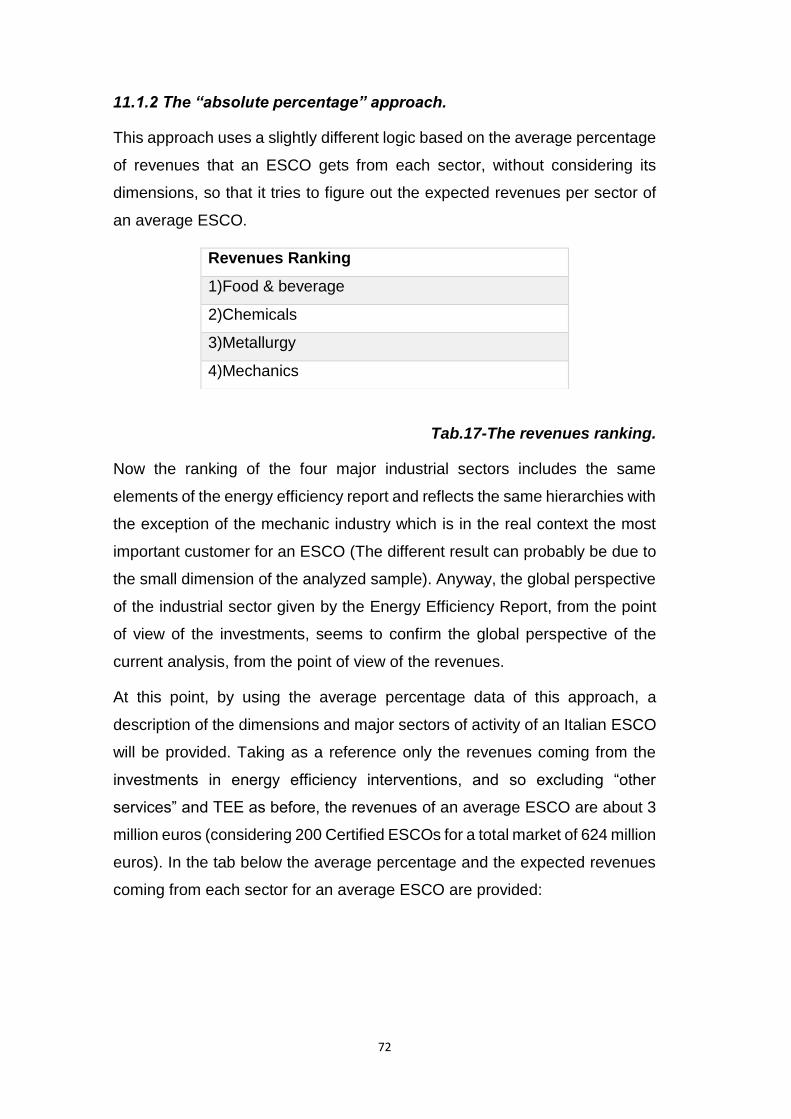

11.1.2 The “absolute percentage” approach ................................................. 70

11.2 Results and comments by technology ............................................. 73

11.2.1 The “revenues-proportional” approach .............................................. 73

11.2.2 The “absolute percentage” approach ................................................. 77

11.3 Results and comments per specific sectors and tecnologies .......... 81

12. ESCos’ market analysis by contract .................................................. 83

12.1 Results and comments .................................................................... 83

3

SUMMARY

13. Insights and trends ............................................................................. 88

13.1 Energy Service Companies and Small-Medium Enterprises ........... 88

13.2 Energy Service Companies and Logistics ....................................... 94

14. Conclusions and future perspectives ............................................... 99

15. Bibliography ...................................................................................... 104

4

1. FIGURES INDEX

Fig.1 The 20-20-20 targets.......................................................................... 11

Fig.2 The specialized operators’ market composition ................................. 21

Fig.3 The integrated operators’ market composition ................................... 21

Fig.4 The Energy Efficiency Service Providers’ market .............................. 22

Fig.5 The target markets ............................................................................. 23

Fig.6 Third parties financing with ESCo borrowing. ..................................... 28

Fig.7 Third parties financing with energy user/customer borrowing ............ 29

Fig.8 The phases of an energy efficiency project ........................................ 36

Fig.9 The phases of an energy efficiency project ........................................ 36

Fig.10 The growth of the Italian market for energy efficiency ...................... 44

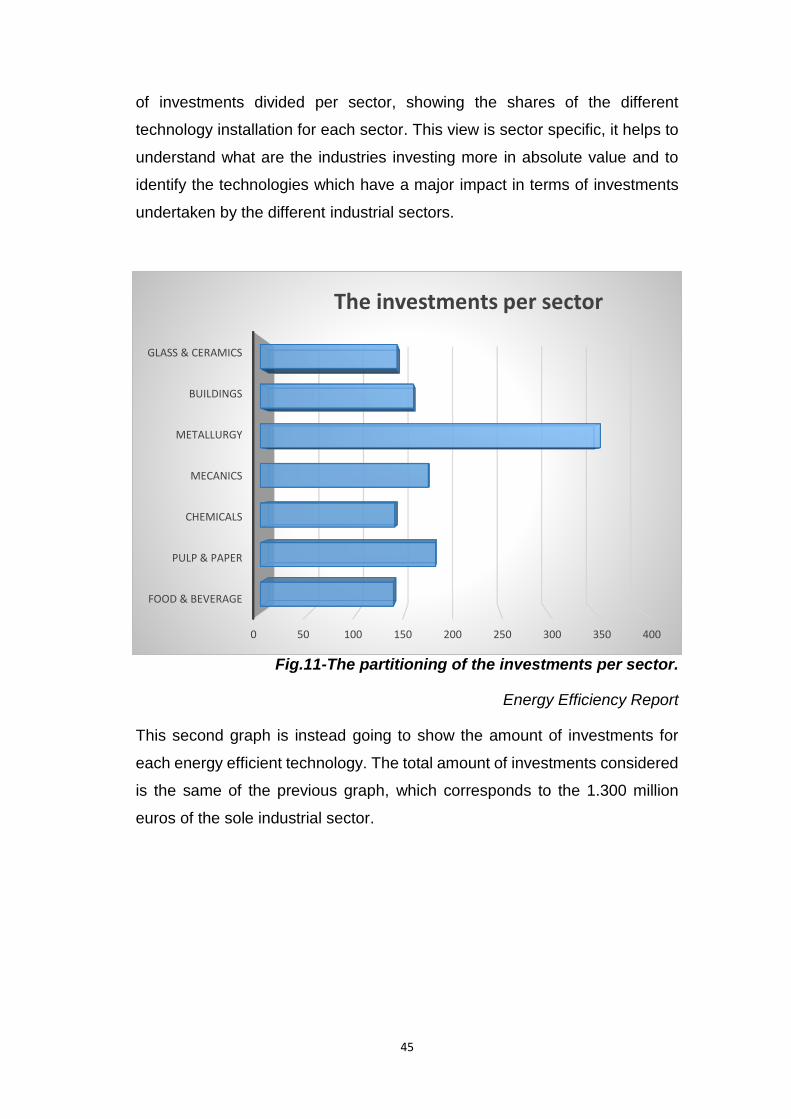

Fig.11 The partitioning of the investments per sector ................................. 45

Fig.12 The partitioning of the investments per technology .......................... 46

Fig.13 The investments in GDO and Hotels ................................................ 50

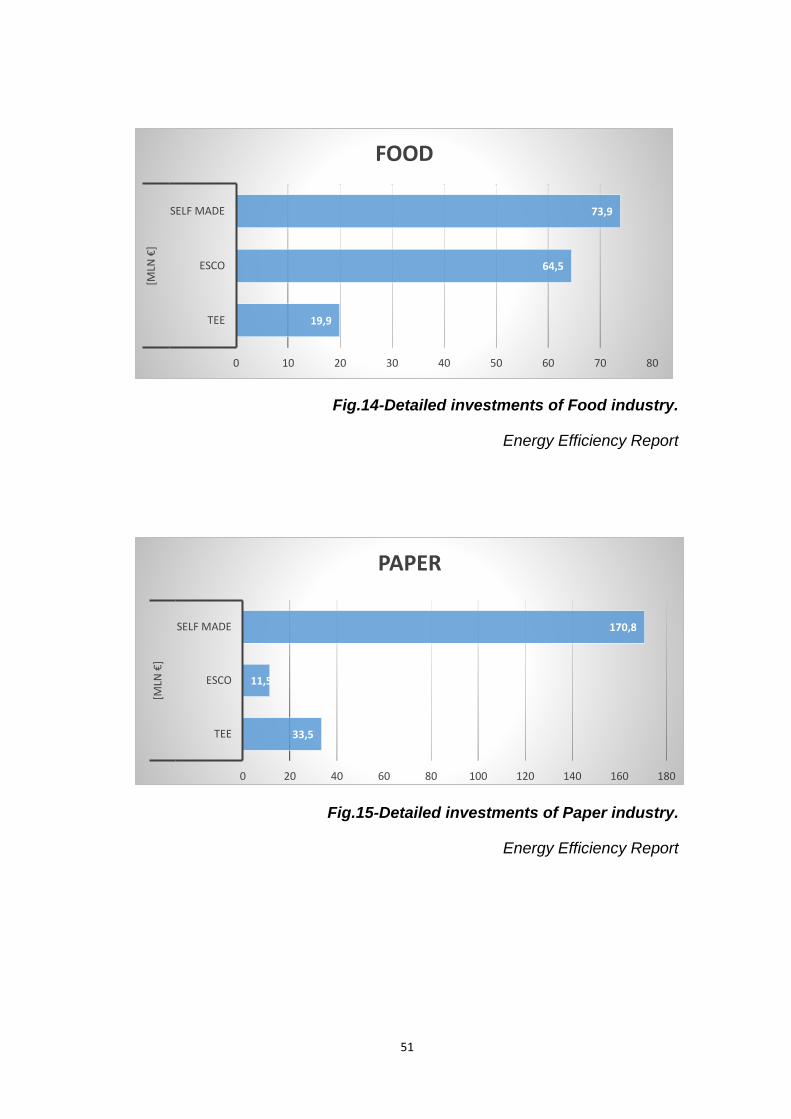

Fig.14 Detailed investments of Food Industry ............................................. 51

Fig.15 Detailed investments of Paper Industry............................................ 51

Fig.16 Detailed Investments of Chemical Industry ...................................... 51

Fig.17 Detailed investments of Mechanical Industry ................................... 52

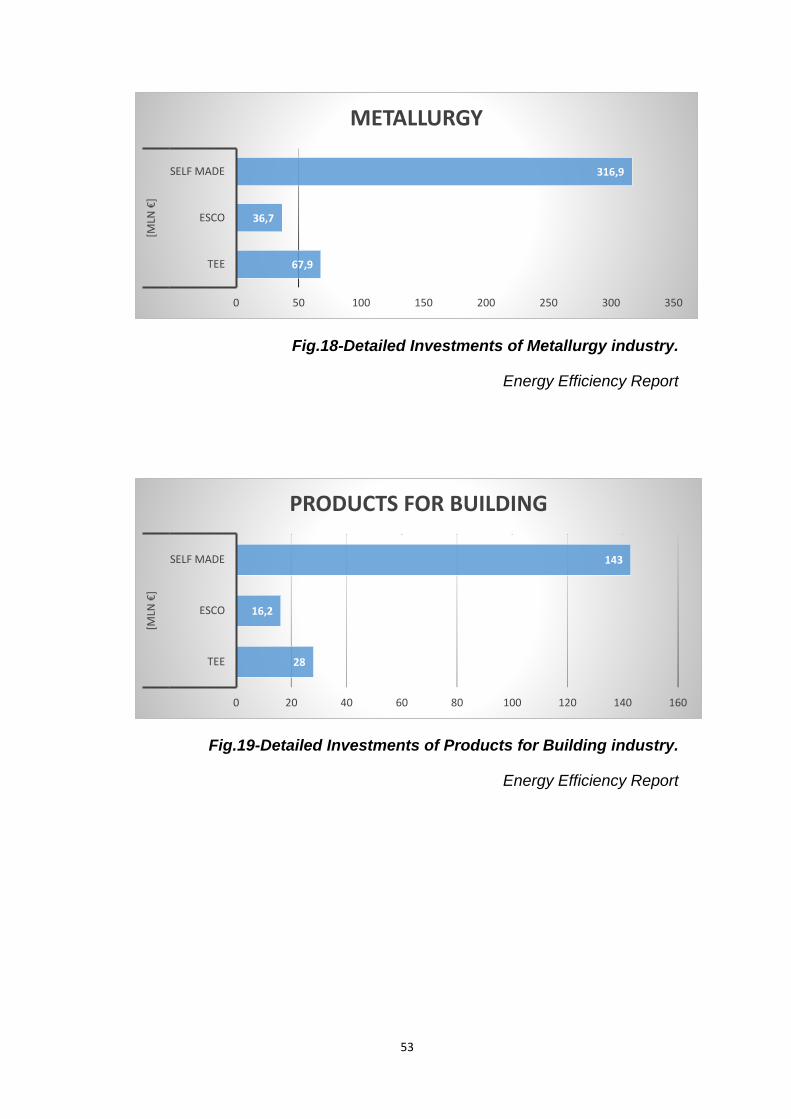

Fig.18 Detailed investments of Products for Metallurgy Industry ................ 52

Fig.19 Detailed investments of Products for Building Industry .................... 52

Fig.20 Detailed investments of Glass Industry ............................................ 53

Fig.21 Detailed investments of the GDO industry ....................................... 53

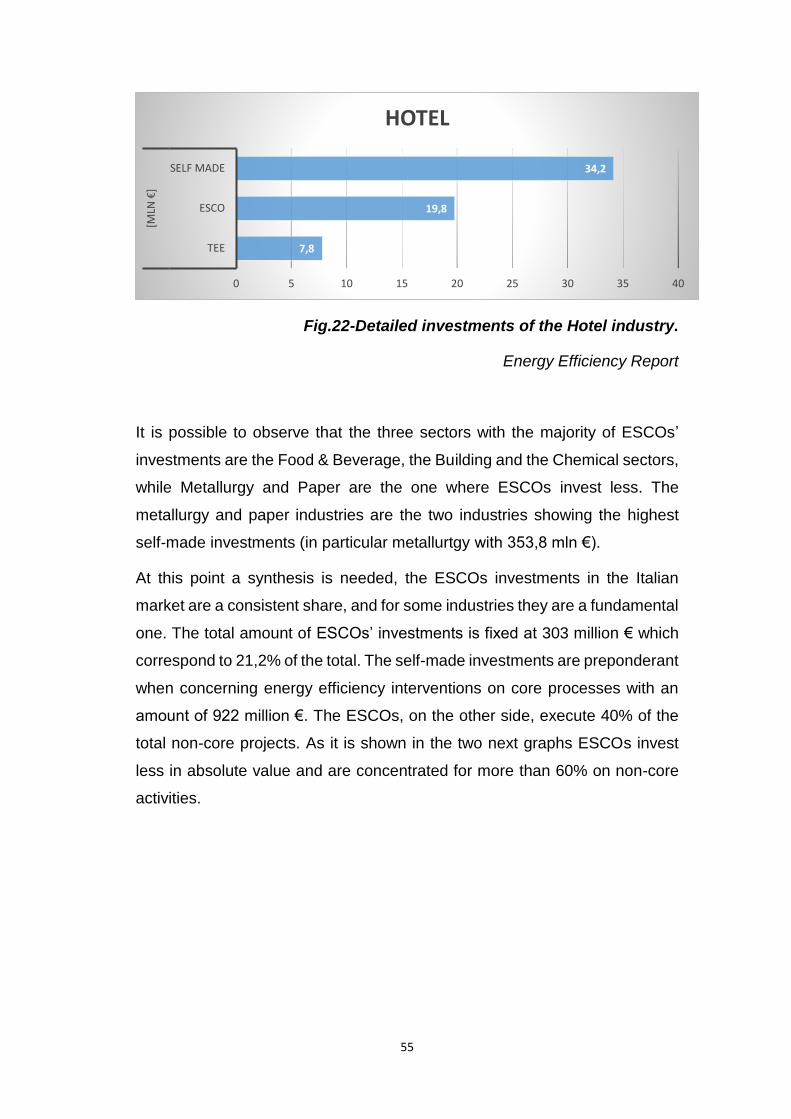

Fig.22 Detailed investments of the Hotel Industry ....................................... 53

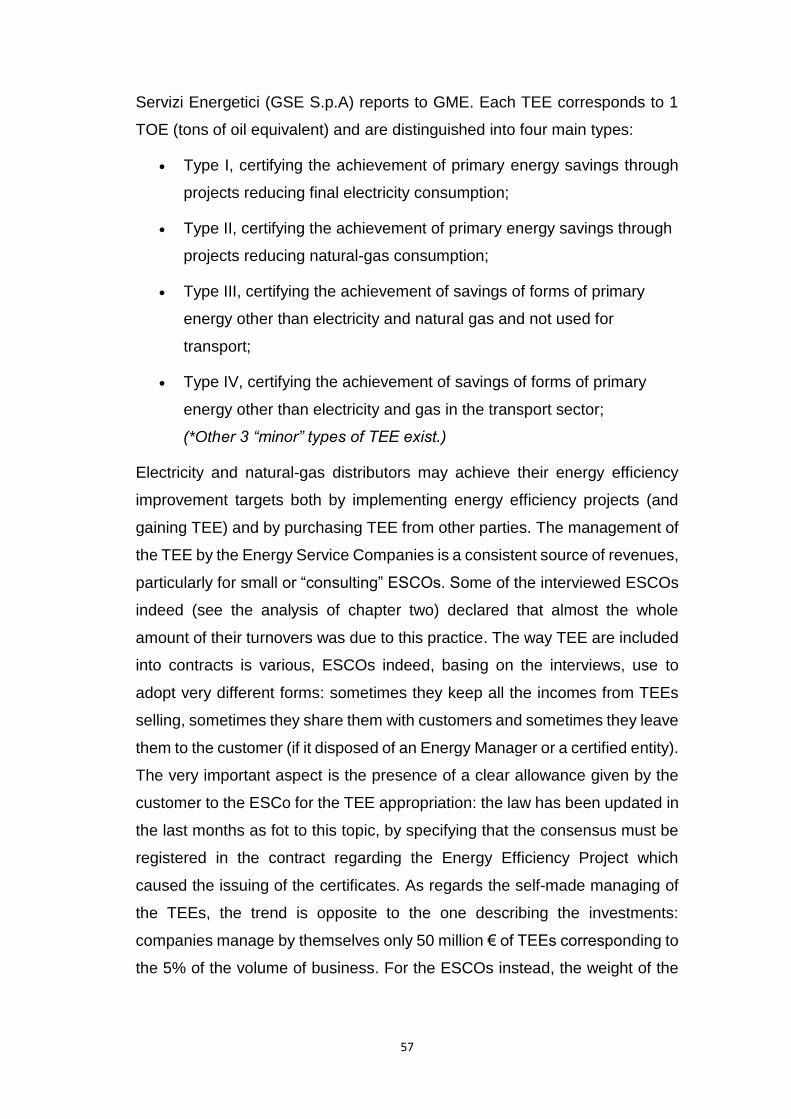

Fig.23 The ESCos incidence on core and non-core activities ..................... 54

Fig.24 The incidence of the TEE on the investments .................................. 56

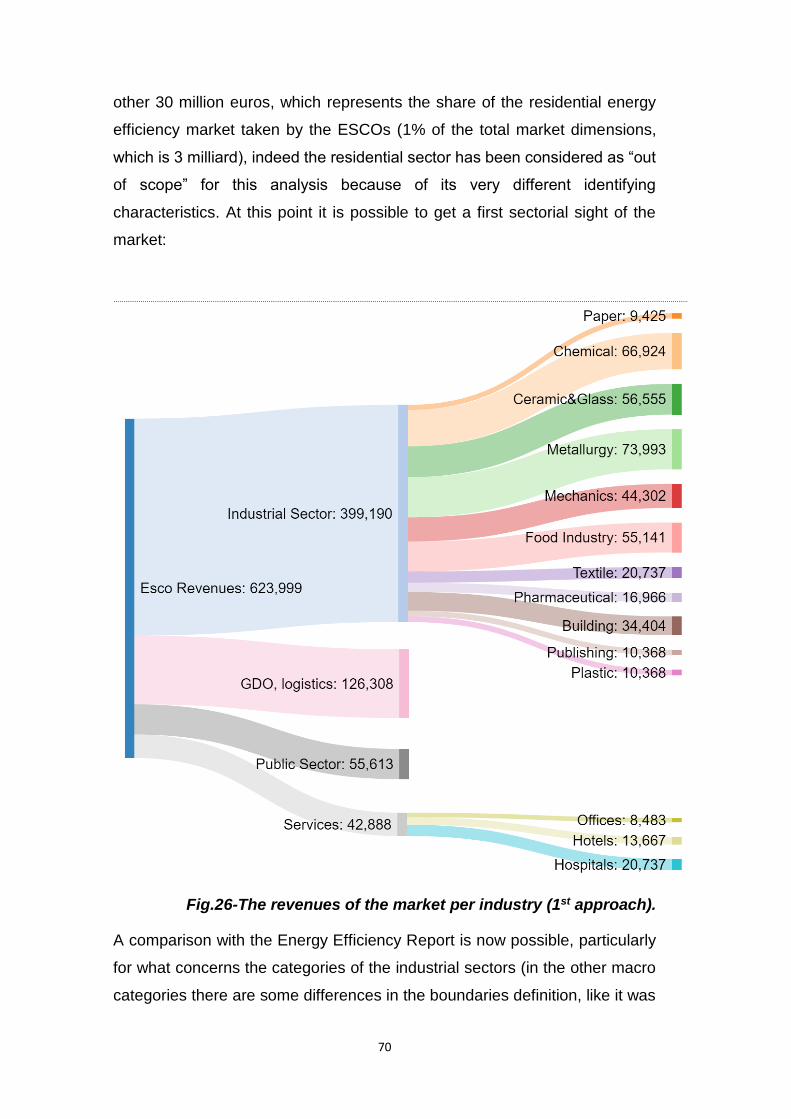

Fig.25 The revenues of the sample per industry ......................................... 64

Fig.26 The revenues of the market per industry (1st approach) .................. 68

Fig.27 The revenues of the market per industry (2nd approach) .................. 72

Fig.28 The revenues of the sample per technology .................................... 73

Fig.29 The revenues of the market per technology (1st approach) ............. 77

5

1. FIGURES INDEX

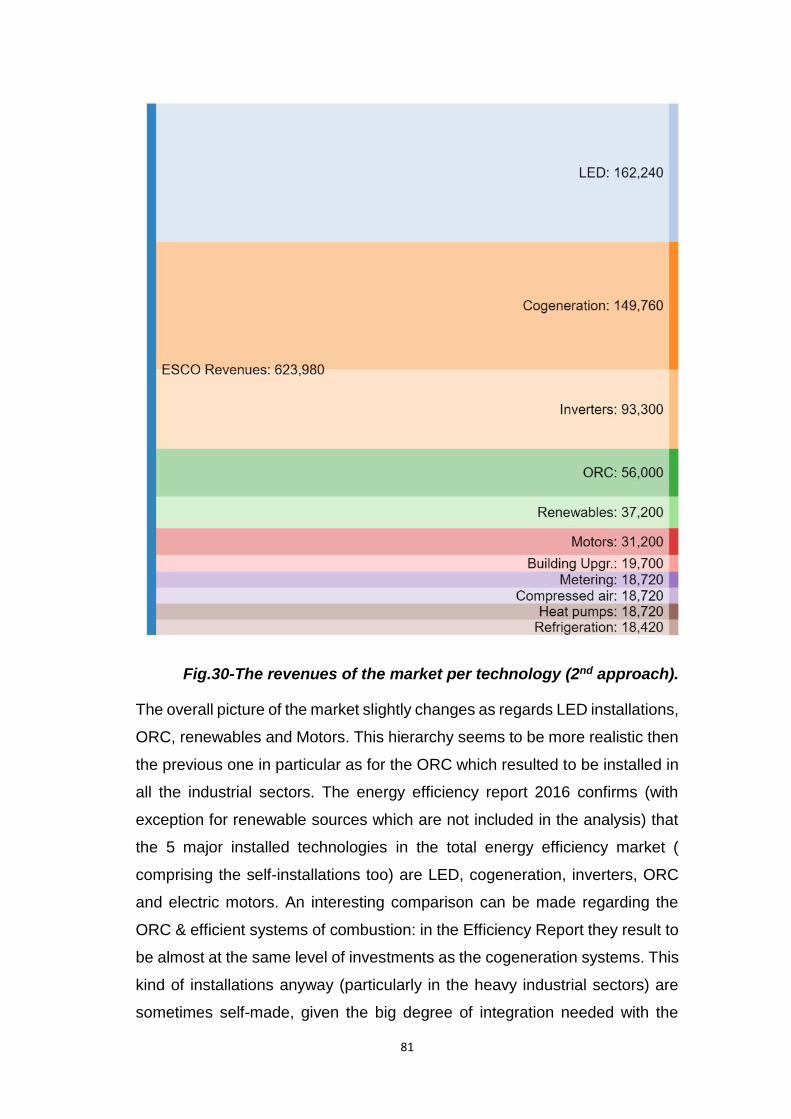

Fig.30 The revenues of the market per technology (2nd approach) ............. 79

Fig.31 The partitioning of the contracts typologies ...................................... 84

Fig.32 The revenues of the market per contract typology ........................... 85

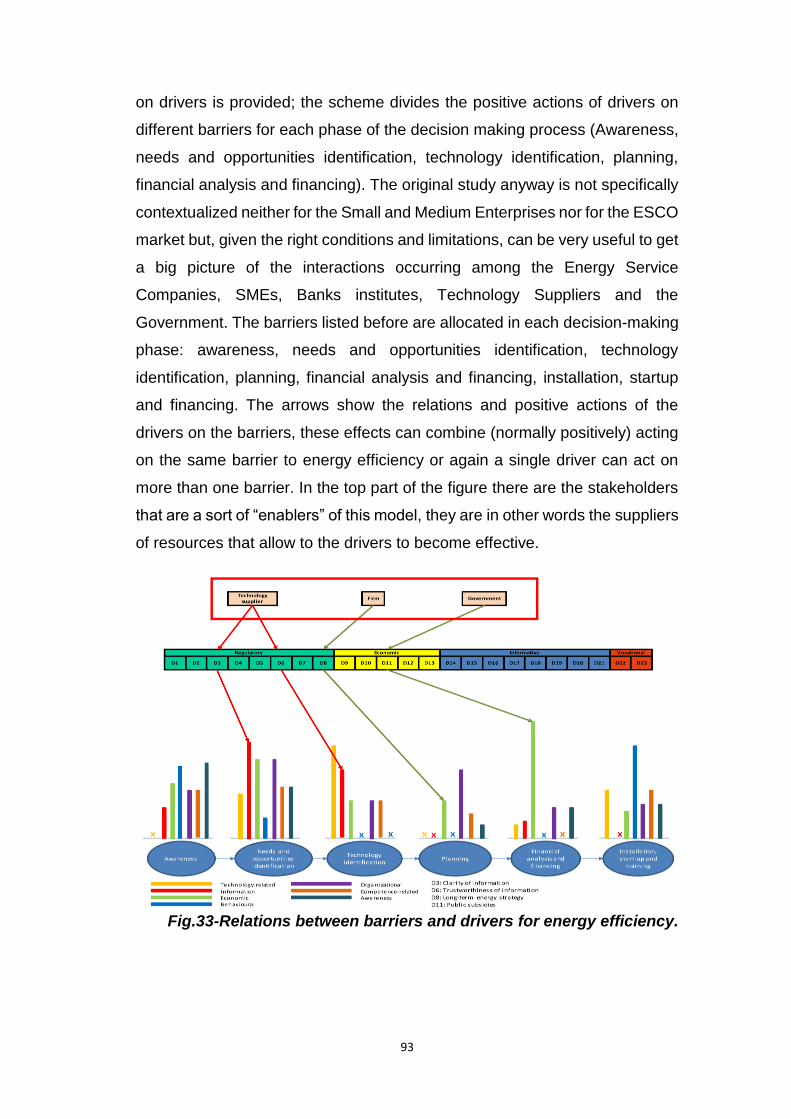

Fig.33 Relations between barriers and drivers for energy efficiency ........... 91

Fig.34 Relations between ESCos and drivers for energy efficiency ............ 93

6

2. TABLES INDEX

Tab.1 Activities and phases of typical intervention ...................................... 16

Tab.2 Activities and phases of a typical intervention ................................... 16

Tab.3 The specialized operators’ activities ................................................. 19

Tab.4 The integrated operators’ activities ................................................... 20

Tab.5 The contracts’ typologies .................................................................. 32

Tab.6 SPIN’s strength and weaknesses ..................................................... 34

Tab.7 SPIN’s opportunities and threats ....................................................... 35

Tab.8 Economic evaluation of an energy efficiency project ........................ 39

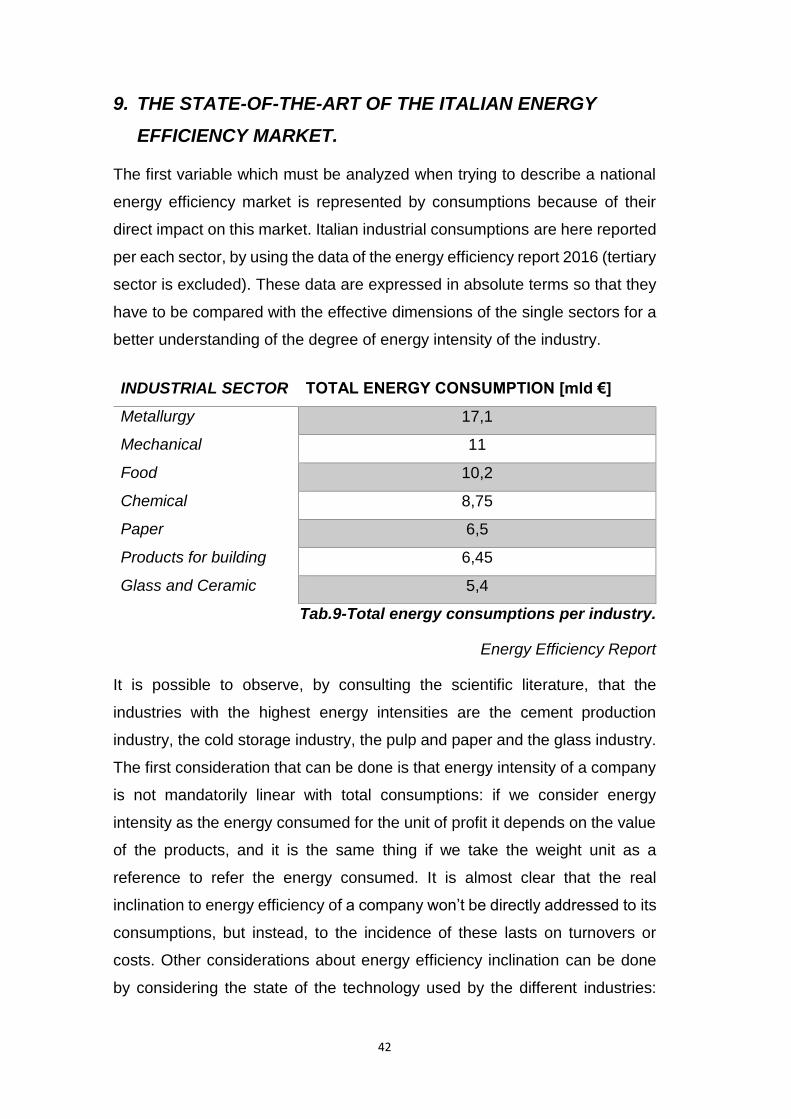

Tab.9 Total energy consumption per industry ............................................. 42

Tab.10 The partitioning of the Italian market for energy efficiency .............. 44

Tab.11 The inclination index towards energy efficiency .............................. 48

Tab.12 The inclination index for GDO and Hotels ....................................... 50

Tab.13 The revenues of the sample ............................................................ 63

Tab.14 The revenues of the sample ............................................................ 63

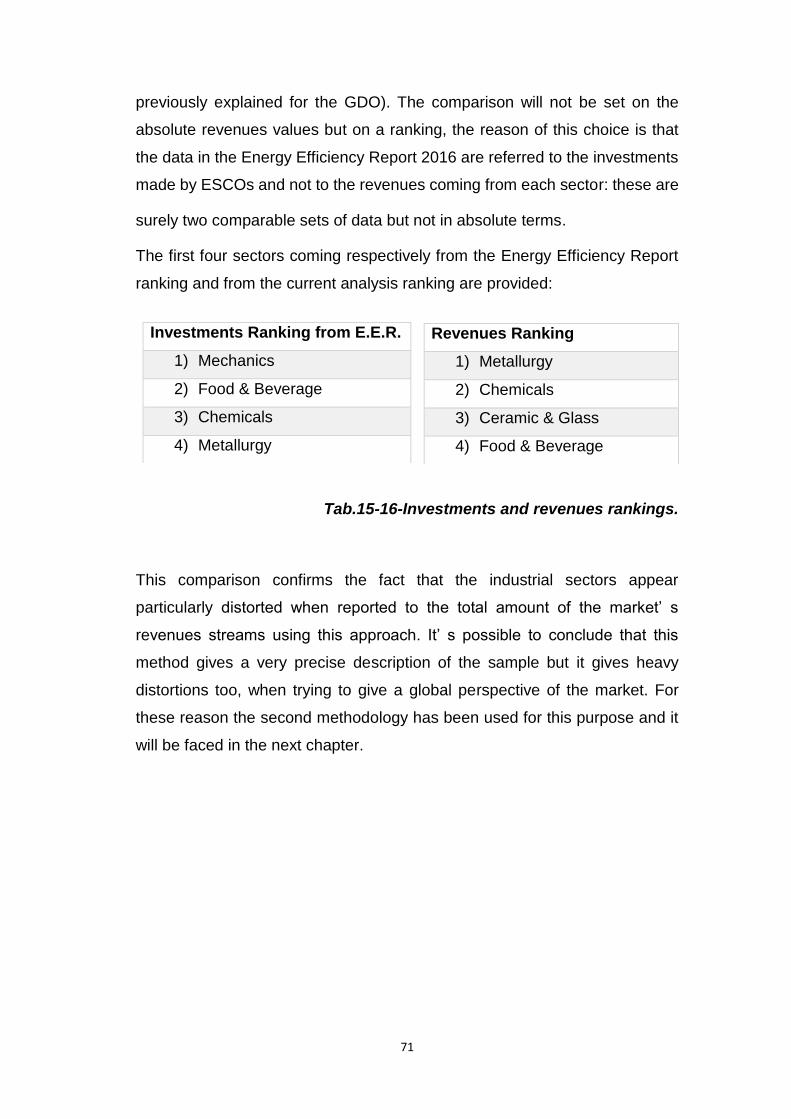

Tab 15-16 Investments and revenues rankings .......................................... 69

Tab 17 The revenues rankings .................................................................... 70

Tab 18 The shares of revenues per sector ................................................. 71

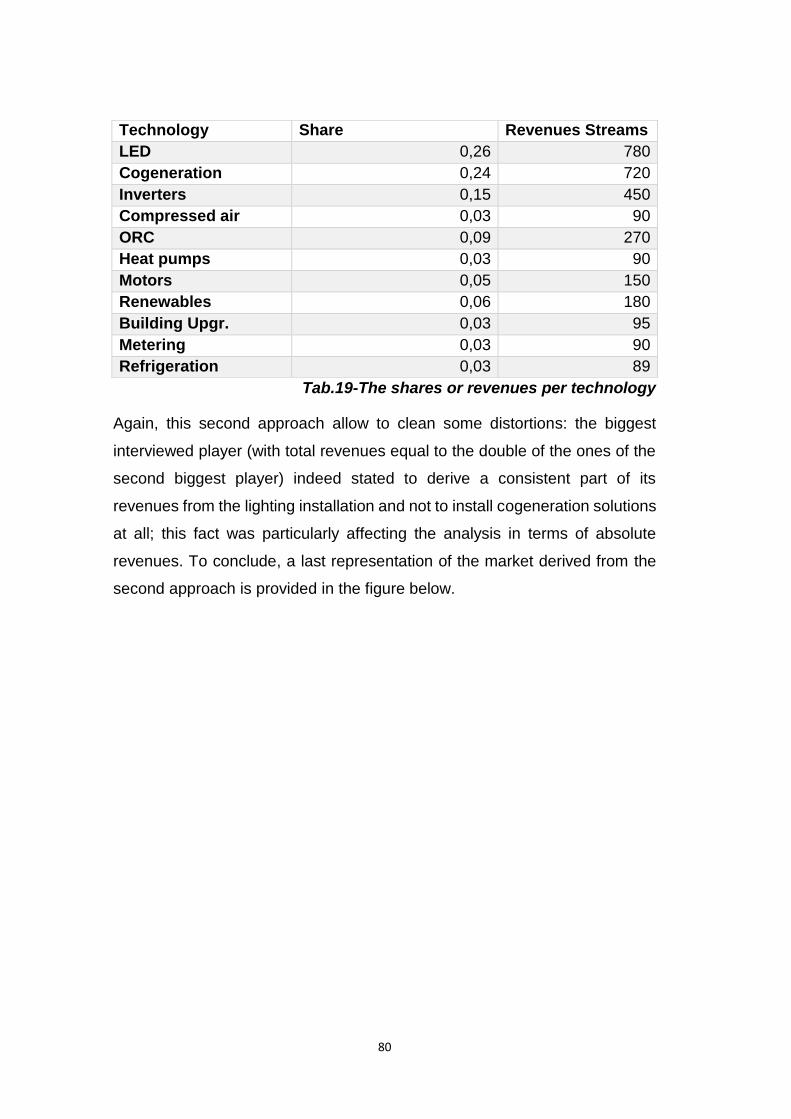

Tab 19 The shares of revenues per technology .......................................... 78

Tab 20 The revenues of the market ............................................................ 81

Tab 21 The revenues of the market ............................................................ 81

Tab 22 Categories of logistics operators ..................................................... 97

7

3. ACRONYMS INDEX

EESP Energy Efficiency Service Providers

ESCO Energy Service Company

P&P Pulp and Paper industry

F&B Food and Beverage industry

ROI Return on equity

NPV Net Present Value

UNI Ente Nazionale Italiano di Unificazione

OEM Original Equipment Manufacturer

TPF Third Party Financing

O&M Operation & Management

SPIN SME Partnerships for Innovative Energy Services

EPC Energy Performance Contract

EPC+ Energy Performance Contract Plus

GDO Grande Distribuzione Organizzata

PBT Payback Time

IRR Internal Rate of Return

TEE Titoli di Efficienza Energetica

EER Energy Efficiency Report

SME Small and Medium Enterprises

LE Large enterprises

PPM Parts per million

tCO2e Tones of CO2 equivalent

8

4. ABSTRACT

The concept of energy efficiency must not be confused with the “energy

conservation” one; with this one indeed, it is meant a decrease in consumption

which, not necessarily, coincide with the subsistence of the expected level of

performance. To switch-off lights at home it’s energy conservation; to

substitute an hold lamp with a LED one, and keep it switched-on for the same

time, it’ energy efficiency.

The actions of Energy Service Companies are based on this fundamental but

simple concept: to grant an equal (or even better) level of performance to the

customer, compared to a decrease in consumptions, and, consequently, in

the energy costs. The appropriation of a quote of the savings is the key to

success of this business model and it allows to offer to the customer “cash-

free” installations.

This thesis work, basing on previous industries classification studies, wants to

deepen the way ESCos interface with customers in the real world and how

they face the intrinsic complexity of the energy efficiency market. As shown in

the literature indeed, in this field there are many possible business models, as

well as many specific know-hows, portfolio of offered services and levels of

integration. About that, the ultimate goal of this thesis won’t be the one of

purposing further categorizations, but instead the one of analyzing the contact

mechanisms with the client, the barriers, the trends of the single industries

and the possible future developments for a market which was born more than

10 years ago.

The nature of this work will be twofold: quantitative and qualitative. It is

quantitative for what concerns the definition of the weights of the industries

and technologies, in terms of turnover. It is qualitative, once the dimensions

of the market have been understood, in terms of investigating the relationships

with customers before, during and AFTER an energy efficiency intervention.

The ESCos are a facilitator and an implementer, recognized by law, of the

achievement of the environmental goals: their mission is not just to “make the

business” but to create and to stimulate demand too.

9

5. ABSTRACT (ITALIAN VERSION)

Il concetto di efficienza energetica non va confuso con quello di

“conservazione dell’energia”; con quest’ultimo infatti, si intende una

diminuzione dei consumi, che non per forza coincide con il mantenimento del

livello atteso di performance. Spegnere la luce di casa è conservare energia;

sostituire la vecchia lampada con una a LED, utilizzandola per lo stesso

tempo, è fare efficienza energetica.

Su questo concetto basilare si fonda l’operato di una Energy Service

Company: garantire al cliente un livello di performance equivalente (o

migliorato), a fronte di una riduzione dei consumi e, conseguentemente, dei

costi energetici. L’appropriamento di una quota del risparmio è la chiave di

successo di questo modello di business e consente di offrire al cliente

un’installazione “cash-free”.

Questo lavoro di tesi, basandosi su precedenti studi di inquadramento del

settore, intende approfondire il modo in cui le ESCo si interfacciano con i

clienti nel mondo reale e come esse affrontino la complessità intrinseca del

mercato dell’efficienza energetica. Come si evince dalla letteratura infatti, i

modelli di business in questo campo sono molteplici, così come i know-how

specifici, i portafogli di servizi offerti ed i possibili livelli di integrazione. A tal

proposito, il fine ultimo della tesi non sarà quello di proporre ulteriori

categorizzazioni, ma bensì di analizzare i meccanismi di contatto col cliente,

le barriere, le tendenze dei singoli segmenti e i possibili sviluppi futuri di un

mercato che esiste ormai da più di un decennio.

La natura del lavoro sarà dunque duplice: quantitativa e qualitativa.

Quantitativa nella definizione dei pesi dei segmenti e delle tecnologie sul

piano dei fatturati. Qualitativa, una volta comprese le dimensioni del mercato,

nell’indagare i rapporti con i clienti prima, dopo e durante un intervento di

efficientamento energetico.

Le ESCo sono un facilitatore ed un attuatore, riconosciuto a norma di legge,

del raggiungimento degli obiettivi ambientali: la loro mission non è soltanto

“fare il business” ma è anche creare e stimolare la domanda.

10

6. GENERAL INTRODUCTION

The thesis work has been organized through eight main chapters, which will

guide the reader through a dissertation about the dynamics of the Energy

Service Companies’ market.

The chapters, from seven to fourteen, can be grouped into three phases:

1) The first phase will provide definitions and frameworks to give a precise

contextualization of the operators in terms of structures, level of

integration, portfolios of services and contracts. Chapter seven will focus

on the relationships between European Regulations and the role of the

ESCos and, in a second moment, on the theoretical classification of the

different actors and contracts. Chapter nine will provide the results of

previous market-analyses (mainly from the Energy Efficiency Report

2016 by the Energy & Strategy Group), which will be used as a basis and

a benchmark for the correct quantification of the results (chapters 10 and

11). Chapter eight describes instead the phases of a “typical” energy

efficiency project.

2) The second phase consists in the presentation of the results, coming

from the surveys and the interviews. The numerical data from the surveys

will be organized with a similar structure with respect to the Energy

Efficiency Report, so as to be able to make considerations about their

accuracy and affordability. The operative and “real-business” issues will

be discussed with reference to the interviews, to favor a better framing of

the dynamics and mechanisms which lay “behind the numbers”. Chapter

ten explains the methodologies used for the analysis of industries and

technologies (chapter eleven) and of the contracts (chapter twelve).

3) The third and last phase of the work consists in the evaluation of the

evolutionary dynamics in the short-medium and long term. Some topics

(which have been the objects of personal and direct experiences) will be

deeply analyzed and final conclusions will be presented together with

future perspectives (chapters thirteen and fourteen).

11

7. INTRODUCTION AND CONTEXTUALIZATION OF THE

MARKET.

7.1 The energy efficiency target and the role of the ESCOs.

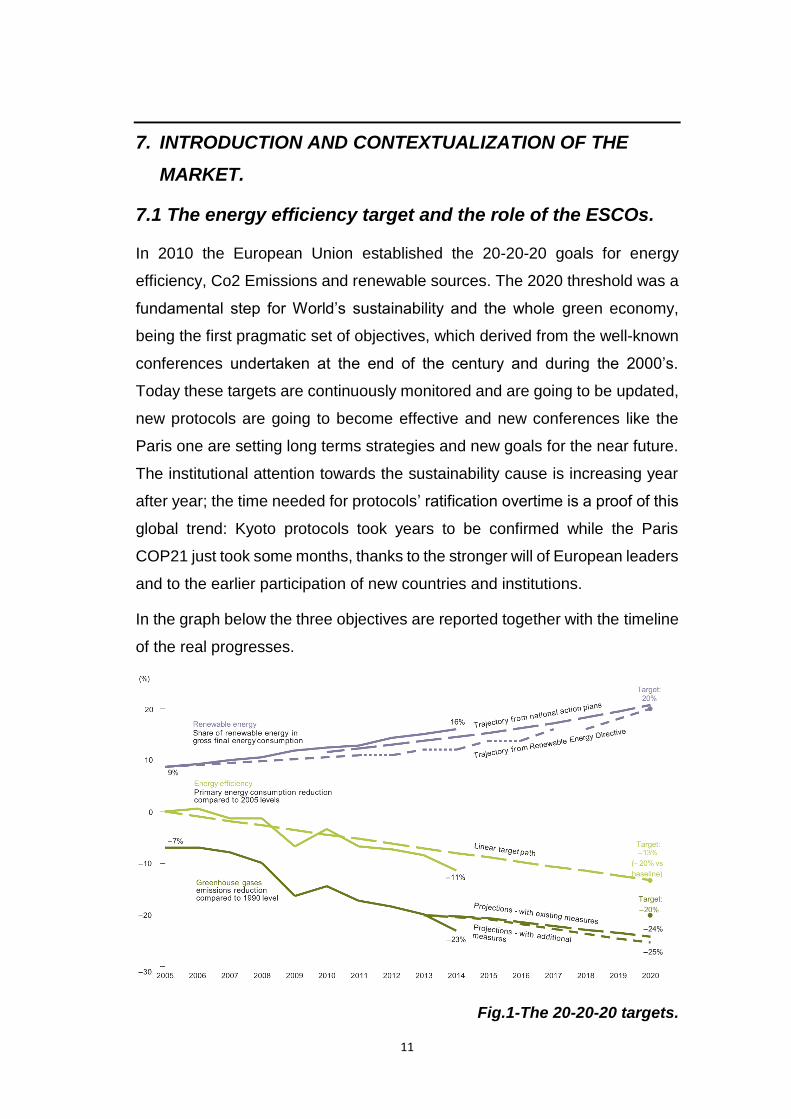

In 2010 the European Union established the 20-20-20 goals for energy

efficiency, Co2 Emissions and renewable sources. The 2020 threshold was a

fundamental step for World’s sustainability and the whole green economy,

being the first pragmatic set of objectives, which derived from the well-known

conferences undertaken at the end of the century and during the 2000’s.

Today these targets are continuously monitored and are going to be updated,

new protocols are going to become effective and new conferences like the

Paris one are setting long terms strategies and new goals for the near future.

The institutional attention towards the sustainability cause is increasing year

after year; the time needed for protocols’ ratification overtime is a proof of this

global trend: Kyoto protocols took years to be confirmed while the Paris

COP21 just took some months, thanks to the stronger will of European leaders

and to the earlier participation of new countries and institutions.

In the graph below the three objectives are reported together with the timeline

of the real progresses.

Fig.1-The 20-20-20 targets.

12

Some observations about this representation are then needed to clearly

understand what is the real distance from the benchmarks and to realize if the

current trends have the right intensity to meet them within the deadlines. The

Renewables and Greenhouse Gases objectives have been defined compared

with 1990, with the result that, when they were set in 2010, a part of them had

already been satisfied. Today these 2 goals have very good projection for the

future and they can be supposed to reach or even exceed final targets by

2020.

As for the Energy Efficiency Goal instead, the evaluation of the progresses

with respect to the final target must be particularly careful, given that it must

be compared to 2005 consumptions (which was the first year in which

consumptions started to decrease, and so the first useful year to set the

target), so that it is practically a more recent target. Looking at future

projections, it is understandable that it will not be easy to reach the decrease

of 20% of consumptions by 2020, even if some nations like Italy have already

reached it. During the next decade the Energy Efficiency target together with

the Renewable Sources one will be fundamental as a driver for the Emissions

Reduction target, which is actually set on the 450 ppm (Parts per million);

indeed, even if this target is going to be reached, it seems that it will not be

consistent enough to keep world temperature under the “2 degrees maximum

increase”. The Paris COP21 wants to move right on this direction, enforcing

measures and placing stricter standards, even if at the moment, the global

scientific community is skeptical about the containment of temperatures

increases within the 2 degrees. Given all these very generic considerations, it

is easy to understand that there are almost two main reasons why enforcing

the energy efficiency market is fundamental for the entire world: the energy

efficiency target is currently the most challenging one and it is a strong driver

to furtherly reduce CO2 emissions.

By relying on this strategic vision and on these macro trends, the European

Union issued the first Energy Efficiency Plan in 2011, which aims to put into

practice measures and guidelines to reach objectives, with a more

“operational” vocation. It is basically articulated over three main priorities:

1. Renewal of building stocks

13

2. Promoting the exemplary role of the public sector (3% restructuring per

year)

3. Promoting the development of the business model of the ESCOs

In 2012 with the directive 2012/27/EU each member state had to set its own

national energy efficiency targets in a non-binding way. For Italy, for example,

the quote was 126 Mtoe (Million tons of oil equivalent) and each state had to

bring into force these directives by 5th June 2014. During 2011 the three

aforementioned priorities were a little modified and redefined (the fact of

updating guidelines and priorities at a European level is crucial to keep contact

with the single countries in the medium term, putting “steps” for markets and

“references” for institutions and laws-adjournments) as following:

1. Promotion of long term strategies for renewal of building stocks

2. Promote the exemplary role of the public sector (3% restructuring per

year)

3. Reduction of the energy sales by 1.5% each year (importance of TEE

market)

4. Promotion of specific measures for energy audits and energy

management systems involving large enterprises.

These two lists of priorities constitute the “pillars” of the Energy Efficiency

market definition for what concerns operational procedures aimed to demand

stimulation and market development; furthermore it is possible to notice that

the individuation of the Energy Service Companies as enabling-actors of the

market is clear and well-defined. This is the evidence of the fact that the ESCo

,as an “entity”, is strongly incentivized by the European regulation, which also

certifies them uniformly (UNI-CEI11352): the ESCo is described as an actor

which works as a “trait d’ union” between EU guidelines and their application

into the real market, guaranteeing standardization, reliability and legality.

Anyway, as it will be explained afterwards in the next sections, the ESCos are

uniformly defined only for what concerns their final purpose (Energy

Efficiency) and European certifications: the structure, the size, the role in the

market, the contracting and the core activities instead, can slightly vary from

one company to another.

14

Now that the “macro” institutional role of the ESCOs is clarified, the aim of the

introduction will be the one to explain what they are, how they work, what are

the main contract forms and what is the state of the Italian energy efficiency

market.

7.2 What is an ESCO.

7.2.1 Definitions.

The energy efficiency objectives can bring very different types of advantages:

the decrease in the degree of energetic dependence from other countries and

from fossil fuels, the possibility to pursue costs reductions and the GHG

reduction are just some of them. It is evident that energy efficiency takes with

it a large series of benefits but it is also true that there are a lot of barriers to

it: some of them are the lack of information and knowledge, the presence of

not qualified entities carrying out projects, the high initial costs and sometimes

a sort of “general apathy” of the specific sectors. In this contest the Energy

Service Companies acts exactly as an “Access door to energy efficiency”,

offering consultancy, knowledge, experience, historical data, dedicated

solutions, assuming technological and financial risks.

It is very difficult to give a precise definition of an Energy Service Company,

because they sell very different services, have different internal structures,

work at different stages of the supply chain and have very different ranges of

integration and specialization, by the way a first definition was given in Italy in

the Decreto Legislativo 115/2008 :

“A person or a company selling energy services and efficiency actions

in the user’ s property assuming a well-defined financial risk. The

remuneration depends totally or partially on the value of the amount of

energy saved thanks to the efficiency intervention”.

The ESCos are different from the ESPCos (Energy Service Provider

Companies) which have not the same focus on energy efficiency that we find

in the previous definition, they are indeed a sort of more “generic actors” which

operate in the market for energy efficiency, but which have not the same

15

institutional value and do not mandatorily assumes technological or financial

risks. These are two central concepts for the definition of an Energy Service

Company which:

“assumes the technological risk of the intervention”

And moreover:

“assumes the financial risk of the intervention”

In the reality, none of these two last sentences is strictly necessary to define

an ESCO, but they are two key points for the framing of the entire business

model of an Energy Service Company which, as a consequence, will always

have to be technologically upgraded and able to make investments by itself or

through third parties. Some other general characteristics describing the

ESCOs, found out in the decrees and in literature, are the model of

remuneration (which is directly dependent on the customer savings), the

guarantee of the savings given by the ESCO itself and the general focus

towards energy efficiency topics.

At this point, it is almost clear that an ESCo, as it is defined, must use financial

and technological resources in the most effective way during the phases of a

project, so that this can be identified as an always-present characteristic for

every kind of company working in this sector. There is then another crucial

perspective which is useful to give definitions and generic figures of Energy

Service Companies: looking at its behavior and portfolio of offered services

over the different phases of a project. During the design & engineering,

construction, running and maintenance phases the ESCos are normally the

only responsible of the actions taken, so that the next step will be the one of

understanding the width and depth levels referred to the sets of actions

provided during an Energy Efficiency Project. These actions can be grouped

for every step of a “typical intervention” like it is proposed in the following tab:

16

Tab 1-Activities and phases of a typical intervention.

Tab 2-Activities and phases of a typical intervention.

The first step coincides with the energy audit phase; even if it can have very

different levels of analysis, (basically depending on the needed accuracy

degree, on the available financial resources, on the possibility to stop the lines,

on the endurance degree compared with invasive investigations, on the

availability of time and on other factors) it is usually composed of some of the

following typical actions: taking physical measurement, making surveys

(dedicated to personnel and to the different levels of management), drawing

up an initial “as is” situation of the site and of the employed machines,

gathering all the technical characteristics and coming up with final

consumptions over time. During these stages ERP data as SAP databases

are usually asked to the company’ s management and are used to select and

extract only pertaining categories.

An ESCO can decide to implement very different types of energy audits: the

ones which are currently (after 2015) mandatory for law belongs to the “very

low detail level” type. Depending on the detail degree required by the

customer and by the kind of process, different types of procedures are used;

with the increasing of the detail level, practices like simulations become

fundamental. The right setting of the level of detail is a very challenging issue

for an ESCO because it is a key-point to satisfy the customer need in the right

way: to give an example the typical Small-Medium Italian Enterprise does not

Energy Audit Contracting Design

Site inspection and data collection

Contract Definition Definition of technical specifications

Data Analysis Funding Definition Technical Design

Energy Consulting Terms Executive planning

Verification of safety standards

Execution Monitoring Operation & Maintentance

Facilities supply Results verification Management

Installation Measurement Maintenance

Starting Eventual corrective-actions

17

need high level of details and does not want to stop processes during

inspection phases, so the ESCOs are moving towards light solutions, quick

methodologies and software to make energy audits in the less invasive

possible way (it is important to remember that the basic concept to be

respected in this case, is that the final benefit brought by the energy audit

actions must exceed the total cost the energy audit itself). Another key-issue,

besides quickness and low invasiveness of procedures, is to provide

forecasted economic results (with the best approximation possible), in order

to give the customer an early idea of the savings, before going into deeper

investigations; this is a generic and fundamental principle for the “sales-area”,

and it is particularly effective when the customer is not completely aware of

the benefits given by the product/service: trying to sell the basic

product/service first, providing certain results, then going deeper into further

investigations and interventions opportunities. Another important issue at this

stage of an energy efficiency project is setting the right priorities both from an

economical-advantage point of view and from a “customer-preference” point

of view, so that the final solutions will be recommended in order of priority for

easier selection.

Once the type of intervention, together with very general parameters, has

been defined, the ESCO is in charge to offer a contract for each new plant or

retrofit-solution (i.e. the installation of new LED lamps into old fixtures

previously mounting neon lamps). The parameters of a contract are various

and this topic will be deepened in a dedicated chapter (depending on the kind

of contract the parameters can change in typology and value too), anyway the

most frequent elements inside this type of contracts are: the share of savings

dedicated to the ESCO, the share of saving dedicated to the customer, the

guaranteed saving performance, the duration of the contract, the condition

given by the ESCO for operating and managing the plant in the first years, the

presence or not of the possibility for the customer to redeem the plant and the

guaranteed payback-time. In this phase also the funding methodology is

defined, the investment indeed, can be carried out by the customer, by the

ESCO, by a bank institute or again by mixed quotes of different actors (this

final solution can get high degrees of complexity as returns must be divided

18

by taking into account different weights of the invested quotes and different

degrees of financial risk and cost of capital).

The third phase of an energy efficiency project is the design of the new

solution or of the retrofit solution; in the first case the design is simpler and

requires less collaboration between the ESCO and the customer. The

definition of the technical specification must coincide with the technical

translation of the economical parameters defined in the contracting phase: the

plant must be dimensioned to give the best possible economical result, under

the constraints of space, time required for installation, minimum performance,

health & safety, productivity and so on. At this point an executive planning can

be defined and, at the end of this procedure, all the safety standards must be

checked and valued as compliant both with law regulations and with company’

s safety policies.

As it will be better explained in the next chapter, an ESCO does not always

undertake all the previous and the next phases but its business model can be

focused just on some of them. An example of this fact is the frequent

outsourcing of the installation procedures (in particular for integrated

operators) or interventions (typical plants whose installation is outsourced by

the ESCOs are PV plant).

The installation follows the gathering of all the necessary components which

are rarely produced by the ESCO, (there are just some examples of big and

very specialized ESCO which produce some components for their own plants)

indeed in the current market the components are supplied by specialized

operators mainly for higher specialization and cost efficiency reasons.

After the plant has been installed and tested, and after that fixed parameters

have been confirmed by the real functioning of the plant, it can start working

under continuous monitoring. In this phase the role of the ESCO is

fundamental for the optimization of the plant, indeed even though the plant

have been properly designed and it is in line with the customer needs, some

changings in settings and parameters are always needed after the installation

(let’s think about the effects of the increase of external temperatures over the

setting of heating systems, or increasing the “lumen/m2” in a given area of a

19

site, due to changes in regulations), in order to get the best possible efficiency

from the plant. An ESCo is indeed much more qualified in monitoring plants

with respect to the customer; the data coming the monitoring activities

anyway, are usually available also for customer’s consultations. As for

operations & maintenance practices, the ESCos often support the customers

during the period in which it runs the plant so that the company will be able to

do it better when the period of competence for the ESCo will come to an end.

7.2.2 Classifications and Business models.

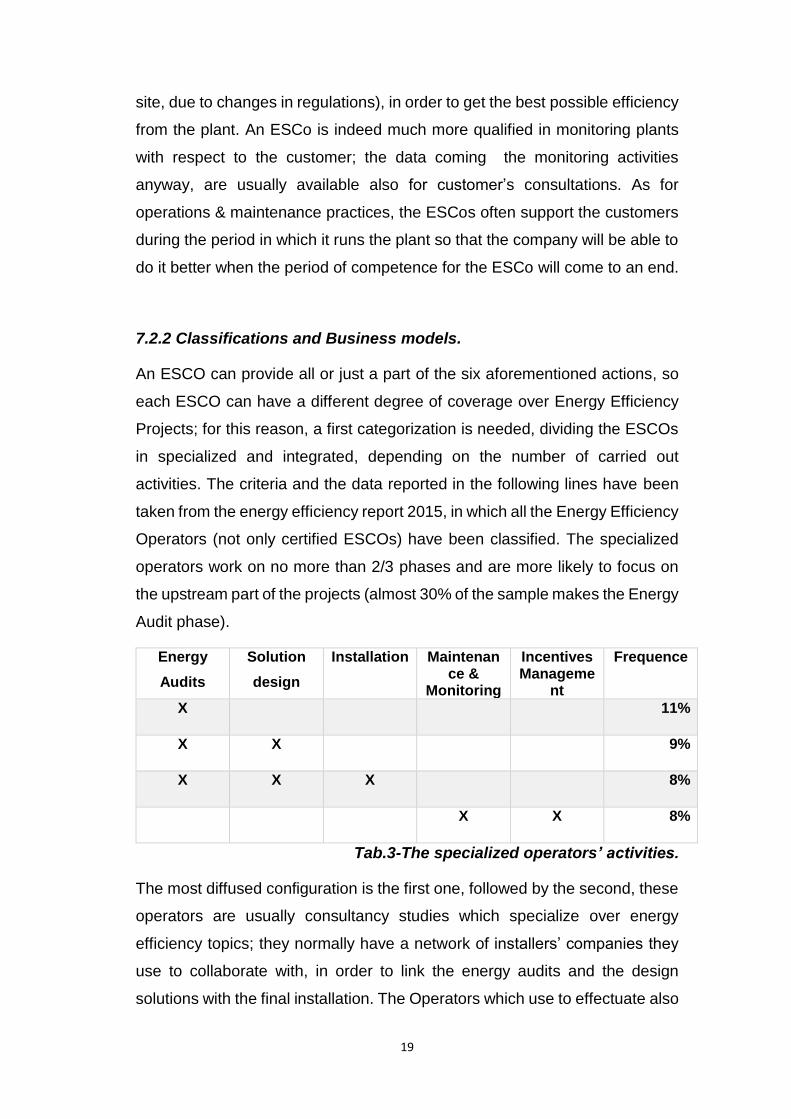

An ESCO can provide all or just a part of the six aforementioned actions, so

each ESCO can have a different degree of coverage over Energy Efficiency

Projects; for this reason, a first categorization is needed, dividing the ESCOs

in specialized and integrated, depending on the number of carried out

activities. The criteria and the data reported in the following lines have been

taken from the energy efficiency report 2015, in which all the Energy Efficiency

Operators (not only certified ESCOs) have been classified. The specialized

operators work on no more than 2/3 phases and are more likely to focus on

the upstream part of the projects (almost 30% of the sample makes the Energy

Audit phase).

Energy

Audits

Solution

design

Installation Maintenance &

Monitoring

Incentives Manageme

nt

Frequence

X

11%

X X

9%

X X X

8%

X X 8%

Tab.3-The specialized operators’ activities.

The most diffused configuration is the first one, followed by the second, these

operators are usually consultancy studies which specialize over energy

efficiency topics; they normally have a network of installers’ companies they

use to collaborate with, in order to link the energy audits and the design

solutions with the final installation. The Operators which use to effectuate also

20

the installation stages have more complex structures and need more

personnel and more heterogeneous competences. In the end a minority of the

operators focuses on monitoring and maintenance issues, these operators

rarely identify with ESCos because they don’ t carry out the first three phases

which are fundamental for being considered an ESCo (they do not assume

technological or financial risks and they do not stimulate demand in any way).

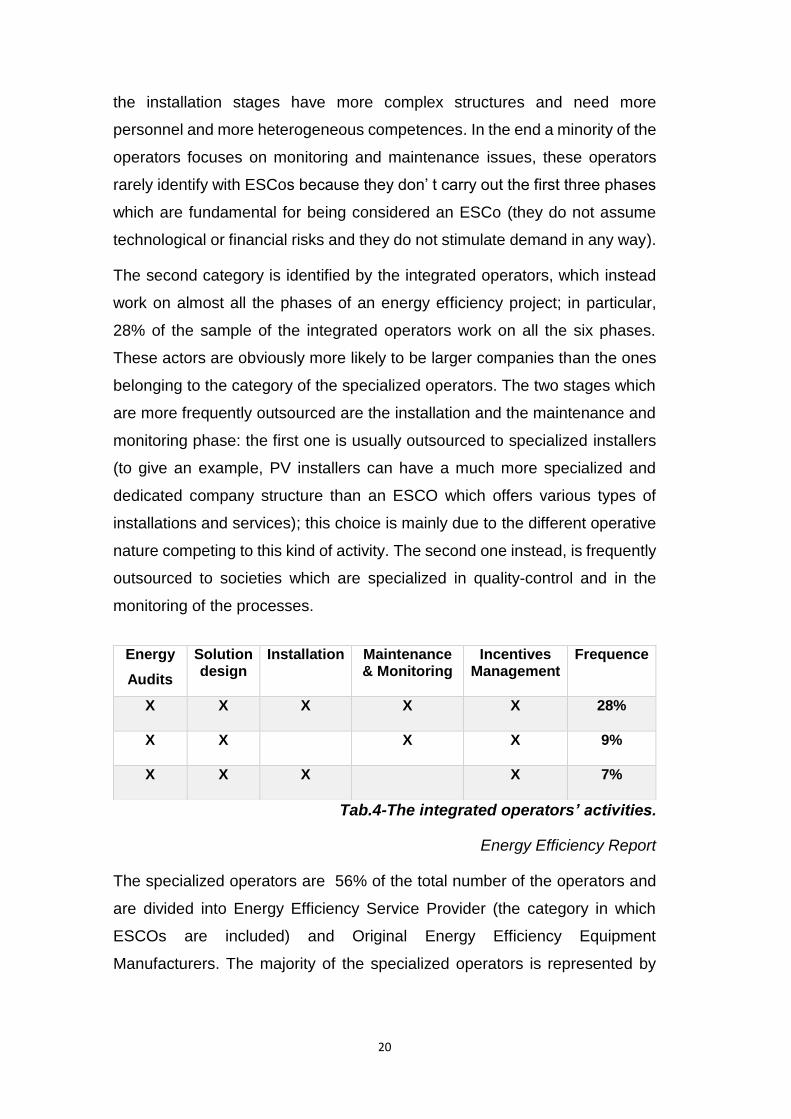

The second category is identified by the integrated operators, which instead

work on almost all the phases of an energy efficiency project; in particular,

28% of the sample of the integrated operators work on all the six phases.

These actors are obviously more likely to be larger companies than the ones

belonging to the category of the specialized operators. The two stages which

are more frequently outsourced are the installation and the maintenance and

monitoring phase: the first one is usually outsourced to specialized installers

(to give an example, PV installers can have a much more specialized and

dedicated company structure than an ESCO which offers various types of

installations and services); this choice is mainly due to the different operative

nature competing to this kind of activity. The second one instead, is frequently

outsourced to societies which are specialized in quality-control and in the

monitoring of the processes.

Tab.4-The integrated operators’ activities.

Energy Efficiency Report

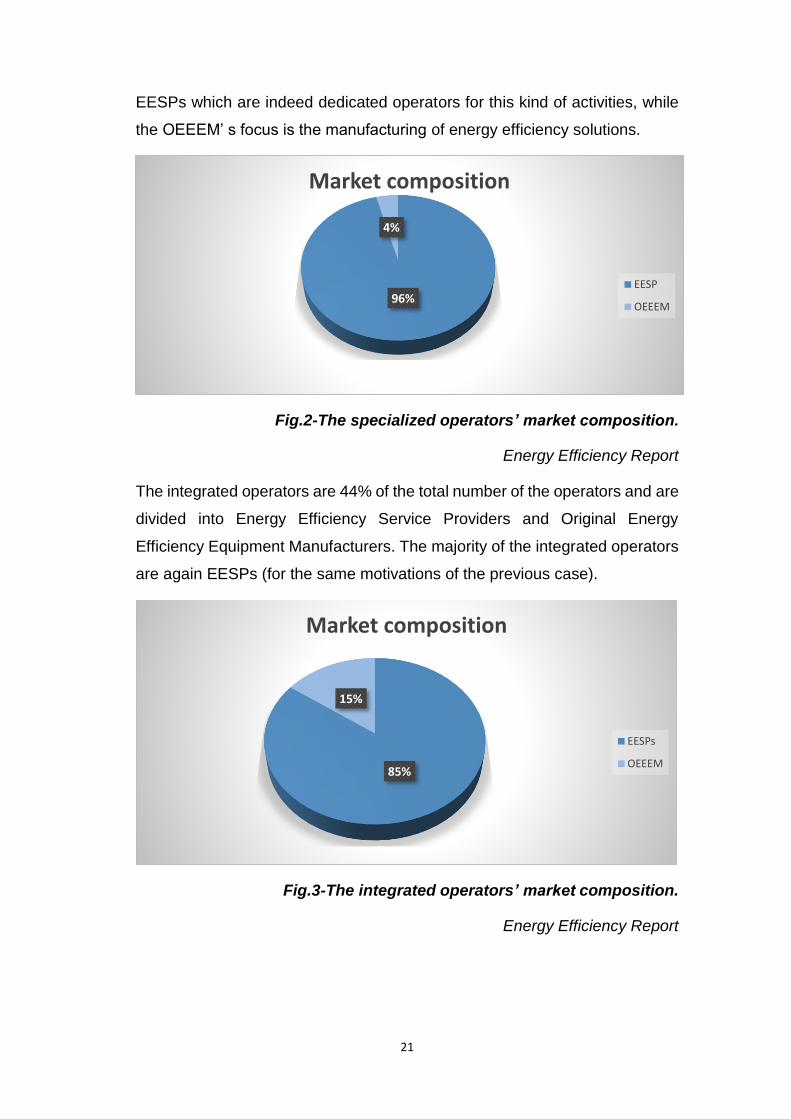

The specialized operators are 56% of the total number of the operators and

are divided into Energy Efficiency Service Provider (the category in which

ESCOs are included) and Original Energy Efficiency Equipment

Manufacturers. The majority of the specialized operators is represented by

Energy

Audits

Solution design

Installation Maintenance & Monitoring

Incentives Management

Frequence

X X X X X 28%

X X

X X 9%

X X X

X 7%

21

EESPs which are indeed dedicated operators for this kind of activities, while

the OEEEM’ s focus is the manufacturing of energy efficiency solutions.

Fig.2-The specialized operators’ market composition.

Energy Efficiency Report

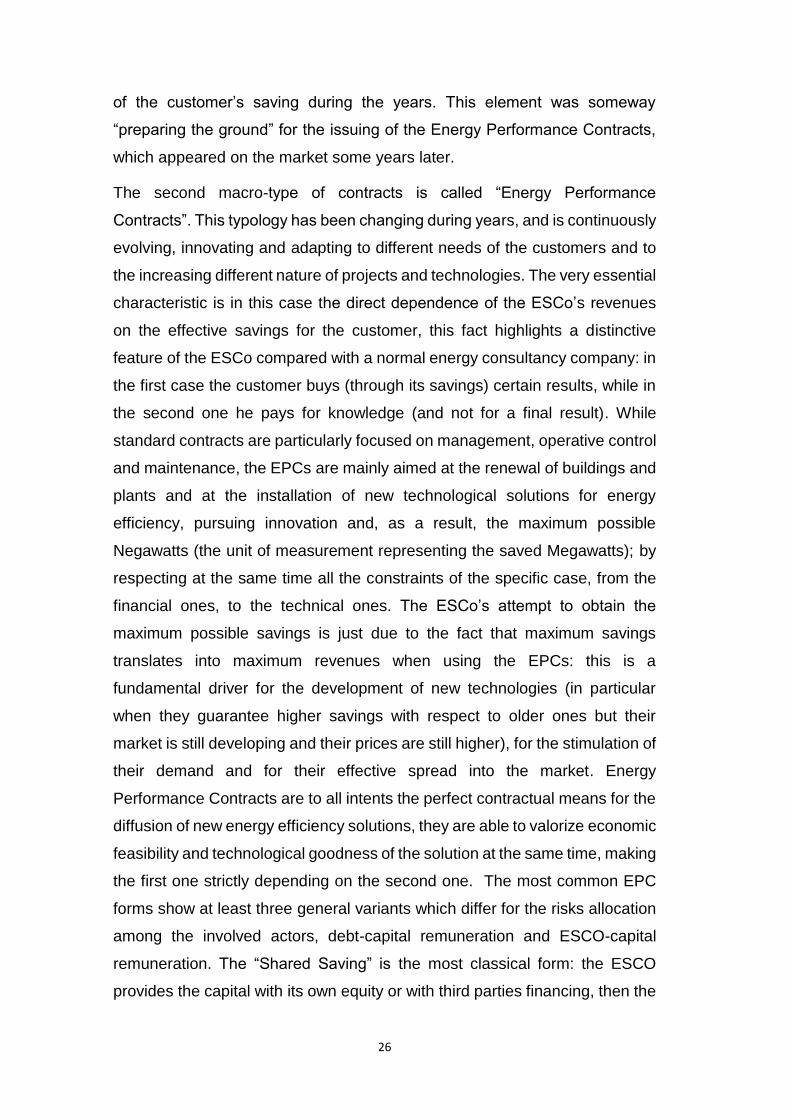

The integrated operators are 44% of the total number of the operators and are

divided into Energy Efficiency Service Providers and Original Energy

Efficiency Equipment Manufacturers. The majority of the integrated operators

are again EESPs (for the same motivations of the previous case).

Fig.3-The integrated operators’ market composition.

Energy Efficiency Report

96%

4%

Market composition

EESP

OEEEM

85%

15%

Market composition

EESPs

OEEEM

22

As mentioned before, ESCOs are included into EESPs, which is a much more

generic and less restrictive group of companies in terms of distinctive

characteristics: in the following graph we can notice that Energy Service

Companies are 58% of this wider categorization.

Fig.4-The Energy Efficiency Service Providers’ market.

Energy Efficiency Report

By analyzing these graphs, it is finally possible to conclude that ESCOs are

almost equally distributed between specialized and integrated operators (with

a prevalence of specialized operators).

Another, and probably more significant categorization, from a merely “market

perspective”, is related to the ESCos’ target market. This kind of perspective

indeed, gives the opportunity to group ESCos’ activities and competences with

a horizontal logic (basically concerning the width of the services and products

offered on the different target markets), while the previous categorization was

more likely to distinguish different portions of a sort of “extended supply-chain”

for energy efficiency. In the specific case of the Energy Efficiency market, it is

important to specify that the most fitting definition of supply chain (which is a

very wide, and sometimes undefined concept) is the one given by Mentzer in

2001 (“The Supply Chain is a series of three or more entities, organizations or

individuals, which are directly involved in upstream or downstream fluxes of

products, services, money or information from primary sources to the final

27%

4%

11%

58%

The Energy Efficiency Service Providers

Facility and plant management

Utility

Advisory

Energy Efficiency

23

customer”), considering the “efficiency project” as the “object” of the supply

chain and treating it as a unique product/service which is sold to the customer.

By going back to the subject, an ESCO has today three possibilities to set its

target market: focusing on the industrial sector, focusing on the tertiary,

residential and building sector or focus on both these two categories. In this

case the ESCO obviously needs a much more complex and developed

structure together with a spread knowledge, enabling to invest over different

realities which have completely different capability to invest, needs to be

satisfied, risks perceptions and type of competences. The diffusion of the

ESCOs in the residential sector is anyway very low in the current market,

which is constituted for the moment by just some pilot projects (mainly in the

field of energetic-class qualifications of residential complexes), while it is more

frequent to find collaborations between building companies and ESCOs for

what concerns the construction of big residential complexes respecting new

requirements in terms of energy consumptions, to obtain the higher possible

classification.

Fig.5-The target markets.

Energy Efficiency Report

Industrial ESCOs use to offer both custom and standard interventions, in

particular they use to carry out the design phases like the ones concerning

energy recovery and cogeneration systems. To do that, with the right level of

personalization and to accomplish all the different parameters of such a

system, they need to have very specific technical competences. Building

ESCos are focused on the tertiary and residential sector while full scope

Full Scope ESCOs

Industrial ESCOs Building ESCOs

24

ESCos act on both the target markets. Industrial ESCos are larger in terms of

revenues and generally offer specialized and technically advanced solutions

which need high personalization degrees and high durability. The other two

categories have a slightly different approach towards the final market: they

often try to enter partnerships with OEMs (Original Equipment Manufacturers),

they try to perceive standardization, ease of installation and sometimes cost

leadership.

As a conclusion of this chapter, it is important to give a unique view of all these

categories (both horizontal and vertical), by providing a general idea of the

nature of an ESCO. The first observation regards the huge variety in terms of

carried out activities and levels of integration (vertical perspective) in the

Energy Efficiency Supply Chain (see previous definition). The second one

instead, highlights the presence of different strategies in terms of approaching

the final customer and, as a consequence, the need of developing different

marketing skills and strategies (aimed at fixing quality or cost leaderships)

depending on the target market (horizontal perspective). The combination of

the two categorizations gives the big picture of the market, which results to be

very heterogeneous. This big variety perfectly reflects into the real market, in

which an ESCo division controlled by a big energy player, an Original

Equipment Manufacturer and a Consulting ESCO are acting together and,

maybe, offering similar services to the same target market. Furthermore

consider that also non-certified operators can compete in the market too, for

what concerns portfolios of services which do not mandatory need a UNI-

certified operator). At this point, the different degrees of operational structure,

technical knowledge and competences have been highlighted, but there are

other two very big elements of heterogeneity: the typology of the offered

contracts and the financing modes, which consequently affect the financial

structure of each company; these two aspects are going to be analyzed in the

following chapter.

25

7.3 The contracts.

7.3.1 Contracts typologies and financing modes.

Different contracts typologies are used in the nowadays market for energy

efficiency; their parameters usually differentiate depending on customer

needs and on the characteristics of the intervention so that, as consequence,

the ESCo must be able to find out the best-fitting contractual form for the

specific situation. In the following chapter the most spread contractual forms

will be analyzed, pointing out pros and cons of each typology.

The first type of contracts is called “Standard contracts”; they are usually

referred to the pure outsourcing of energy management and have been used

since the ‘80s, for turnkey services mainly related to plants dedicated to heat

production. The guaranteed performance in terms of volumetric units and day

degrees are both explicitly expressed parameters. The nature of the contract

is firstly related to the outsourcing of energy management issues and, as a

consequence, it is not mandatory that the specific project has to provide the

construction of a plant. In some cases indeed, some of these contracts directly

act on already existing plants, dealing with operational and maintenance

activities. During the whole duration of the contract the ESCo results in being

the effective owner of the plant and the customer lose every right to take

operational decisions over the plant. This type of contract does not usually

provide a direct dependence between the ESCo’s profits and the effective

savings for the customer, but some clauses can put upper and lower limits to

ESCO revenues on the basis of the procured savings. Another option of the

standard contracts is the possibility to protect the customer, by guaranteeing

a fixed price for fuels or electric energy supply, so that the variability of

performances decreases and the degree of guarantee over final results

increases (This fact can be an advantage not only for the customer but for the

ESCo too, which can better control and forecast the performance trends of the

plant). In Italy the evolution of these contracts over time went through two

subsequent stages: from the “contratto calore”, which provided the

management and maintenance of a boiler, trying to improve its overall

utilization-efficiency, to the “servizio energia”, which provided the insertion into

the contract of new parameters, the most important one is the explicit forecast

26

of the customer’s saving during the years. This element was someway

“preparing the ground” for the issuing of the Energy Performance Contracts,

which appeared on the market some years later.

The second macro-type of contracts is called “Energy Performance

Contracts”. This typology has been changing during years, and is continuously

evolving, innovating and adapting to different needs of the customers and to

the increasing different nature of projects and technologies. The very essential

characteristic is in this case the direct dependence of the ESCo’s revenues

on the effective savings for the customer, this fact highlights a distinctive

feature of the ESCo compared with a normal energy consultancy company: in

the first case the customer buys (through its savings) certain results, while in

the second one he pays for knowledge (and not for a final result). While

standard contracts are particularly focused on management, operative control

and maintenance, the EPCs are mainly aimed at the renewal of buildings and

plants and at the installation of new technological solutions for energy

efficiency, pursuing innovation and, as a result, the maximum possible

Negawatts (the unit of measurement representing the saved Megawatts); by

respecting at the same time all the constraints of the specific case, from the

financial ones, to the technical ones. The ESCo’s attempt to obtain the

maximum possible savings is just due to the fact that maximum savings

translates into maximum revenues when using the EPCs: this is a

fundamental driver for the development of new technologies (in particular

when they guarantee higher savings with respect to older ones but their

market is still developing and their prices are still higher), for the stimulation of

their demand and for their effective spread into the market. Energy

Performance Contracts are to all intents the perfect contractual means for the

diffusion of new energy efficiency solutions, they are able to valorize economic

feasibility and technological goodness of the solution at the same time, making

the first one strictly depending on the second one. The most common EPC

forms show at least three general variants which differ for the risks allocation

among the involved actors, debt-capital remuneration and ESCO-capital

remuneration. The “Shared Saving” is the most classical form: the ESCO

provides the capital with its own equity or with third parties financing, then the

27

parties agree on the subdivision of the final savings. These contracts usually

last longer than the case in which the savings are completely assumed by the

ESCO, because only one part of the savings is contributing to the recovery of

the investment. They can last from 5 to 10 years, even if the real payback time

of the investment (by considering the total returns/savings as the sum of the

returns for the customers and the returns for the Energy Service Company),

would be much lower. Also in this typology of contract the property of the plant

stays in the hand of the ESCOs and only at the end of the contract it comes

back to the customer. The operation & management is usually made by the

ESCO, with predefined comfort, operative and functioning parameters.

Another well-known typology is represented by the “first out” contracts, in

which the savings are used to repay the interests and the depreciation of the

contracted loans, for this reason they last less than the “shared savings” and

the return of the investment results to be faster (usually 3-5 years). At the

conclusion of the competence period of the contract, the savings completely

pass to the customer.

The “Guaranteed saving” instead, is the wording used to describe a sort of

leasing provided with a guaranteed energy saving for the customer. In the US

this form is typically accompanied with a third party financing: the customer

underwrites the loan with the third party, while the ESCo have to guarantee a

certain level of returns (the ESCo in this case is the guarantor of the technical

feasibility and provides the third party with technical parameters useful to set

the financial ones with the final customer). The financial risk is in the end in

charge of the client and of the third party, so the Energy Service Company is

only bearing one of the two typical risks which were mentioned in the

definition’s chapter: the financial risk. For this type of contracts the duration is

usually 4-8 years. Sometimes in the contracts there are some clauses which

can guarantee fixed energy savings, fixed energy prices or again the use of

the most convenient source of energy.

In short, the financing modes can be structured so that the entire invested

capital is provided by the customer or by the Energy Service Company. The

second alternative is represented by the intervention of the aforementioned

“third party” which was previously mentioned during the description of the

28

“guaranteed savings” contract: the third party is usually a bank institute

(sometimes it can also be represented by a big energy distributors) which can

participate to the investment by providing the whole amount of the investment

or just a part of it (in this case the other part can be provided by the ESCo or

by the customer itself). In the latter situation the definition of the contract

becomes more difficult, given that different actors have to remunerate different

portion of the capital invested. Besides the amount of capital with which the

bank institute is going to participate to the investment, there is another

important variable, which is the definition of the entity the third party is

interacting with. The bank instead, can find a financing agreement both with

the customer and with the ESCo, this passage basically defines who is the

final responsible for the financial risk. In Italy the very common situation is that

the bank interacts with the ESCo, which can assume the function of “technical

guarantor” which was previously described while defining the “guaranteed

savings” concept. Nowadays bank institutes are “adapting” to this financing

scheme, by providing dedicated offices and services with specific skills and

competences which can better interact with the ESCo. This could be a key-

issue for pushing investments in the Italian energy efficiency market: if bank

institutes succeed in defining standardized parameters and conditions which

can be met by ESCo competences and guarantees, it could be much easier

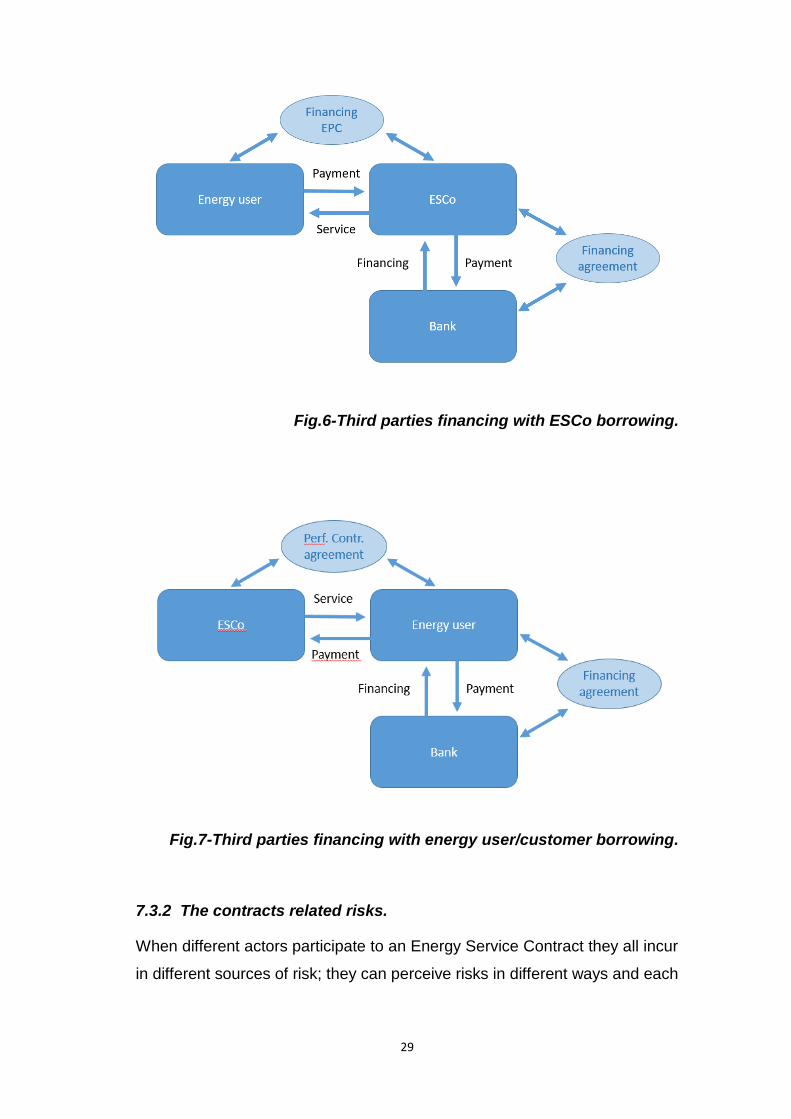

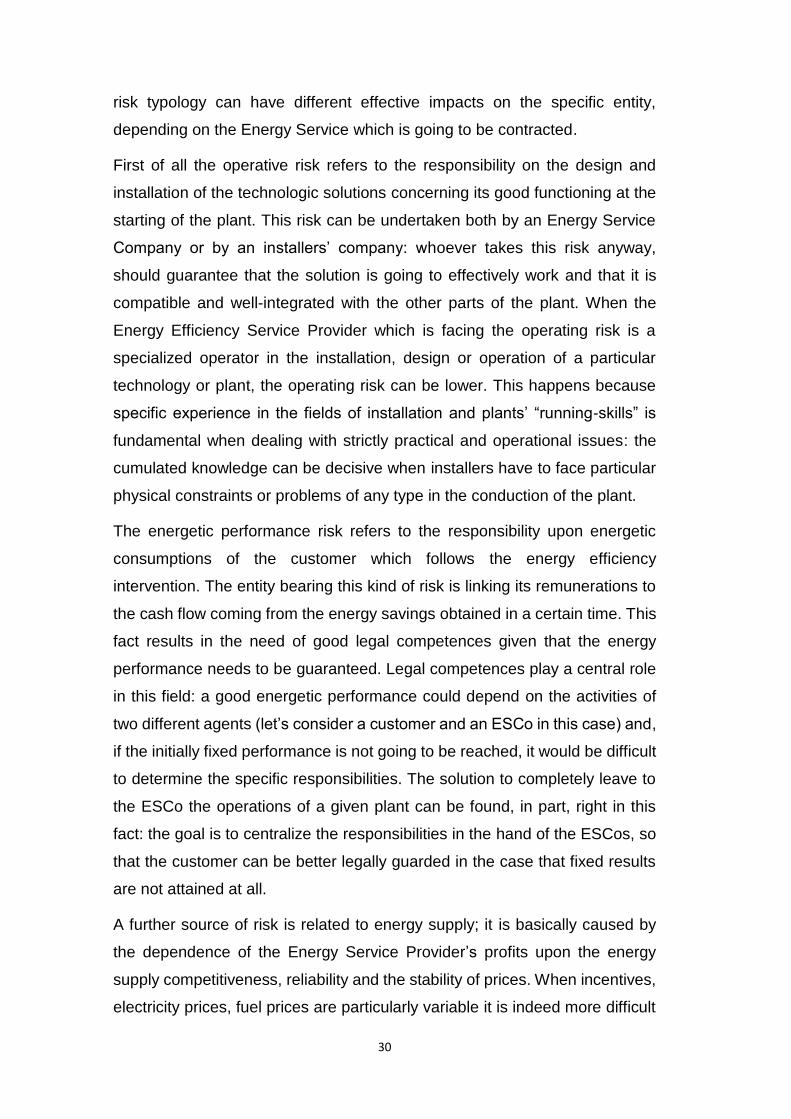

to finance energy efficiency investments.

To better clarify the two “third party financing modes” described before, two

schemes showing fluxes of money and services between the entity are

provided:

29

Fig.6-Third parties financing with ESCo borrowing.

Fig.7-Third parties financing with energy user/customer borrowing.

7.3.2 The contracts related risks.

When different actors participate to an Energy Service Contract they all incur

in different sources of risk; they can perceive risks in different ways and each

30

risk typology can have different effective impacts on the specific entity,

depending on the Energy Service which is going to be contracted.

First of all the operative risk refers to the responsibility on the design and

installation of the technologic solutions concerning its good functioning at the

starting of the plant. This risk can be undertaken both by an Energy Service

Company or by an installers’ company: whoever takes this risk anyway,

should guarantee that the solution is going to effectively work and that it is

compatible and well-integrated with the other parts of the plant. When the

Energy Efficiency Service Provider which is facing the operating risk is a

specialized operator in the installation, design or operation of a particular

technology or plant, the operating risk can be lower. This happens because

specific experience in the fields of installation and plants’ “running-skills” is

fundamental when dealing with strictly practical and operational issues: the

cumulated knowledge can be decisive when installers have to face particular

physical constraints or problems of any type in the conduction of the plant.

The energetic performance risk refers to the responsibility upon energetic

consumptions of the customer which follows the energy efficiency

intervention. The entity bearing this kind of risk is linking its remunerations to

the cash flow coming from the energy savings obtained in a certain time. This

fact results in the need of good legal competences given that the energy

performance needs to be guaranteed. Legal competences play a central role

in this field: a good energetic performance could depend on the activities of

two different agents (let’s consider a customer and an ESCo in this case) and,

if the initially fixed performance is not going to be reached, it would be difficult

to determine the specific responsibilities. The solution to completely leave to

the ESCo the operations of a given plant can be found, in part, right in this

fact: the goal is to centralize the responsibilities in the hand of the ESCos, so

that the customer can be better legally guarded in the case that fixed results

are not attained at all.

A further source of risk is related to energy supply; it is basically caused by

the dependence of the Energy Service Provider’s profits upon the energy

supply competitiveness, reliability and the stability of prices. When incentives,

electricity prices, fuel prices are particularly variable it is indeed more difficult

31

to precisely determine contractual parameters and to guarantee the initially

fixed results. Two practices anyway can help to reduce this source of risk: the

energy trading and the risk management on energy prices (making forecasts

about the trend and the volatility of the future energy prices). Buying electricity

through futures can be a good instrument to get constant electricity prices and,

in general, all the so called “administrative energy efficiency” practices can

play an important role too.

The financial risk, by considering the most general definition possible, refers

to the uncertainty linked to the future value of any investment and its volatility.

The entity that bears this risk finances the investment through equity capital,

if the risk is considered too high, it will be necessary to try to resort to third

party financing. This risk is reduced thanks to the capability of evaluating

investments and to make affordable costs/benefit analysis. Furthermore, as a

definition, the financial risk is “linked” to the balance of incoming and

outcoming flows (given that it is the risk impacts on the company liquidity), and

when the volatility of these flows in linked to weather conditions, energy prices

and a lot of other variables, it becomes a fundamental source of risk to be

considered.

In the end the functioning risk is a sort of “all-in-one” risk which relieves the

customer from every kind of responsibility: in this case the entity bearing the

risk is not just carrying out an energy efficiency intervention but it is completely

guaranteeing and managing the entire service offered by the plant, ensuring

a continuous and efficient delivery of the service. A good perception and

capability of analysis of the company processes is a driver for the reduction of

this source of risk.

When an energy efficiency project has to be carried out, it is very important to

have a clear view of the risks set before the realization; that is a key point, the

complete evaluation of the risks must be clear before starting every kind of

activity because it represents an important threshold for outsourcing/in-house

decisions. An energy efficiency project is indeed composed of phases

completely different the one from the other, and one of these differences is

right the impact upon different risks categories: each phase of the project can

be more, or less adaptable to the ESCo’s structure and business plan in terms

32

of the set of risks (and related intensities) which it bears with itself. As a

conclusion (particularly for big players working on big energy efficiency

projects) the risks’ effects evaluation and combination is crucial in this sector.

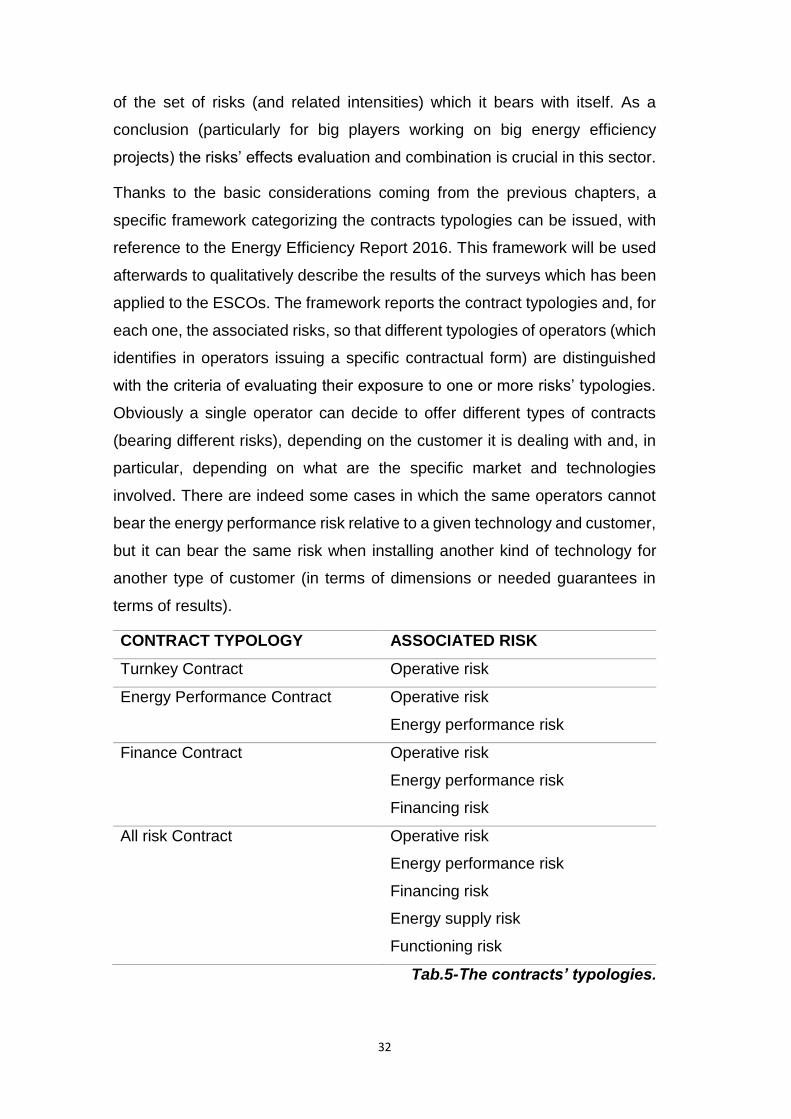

Thanks to the basic considerations coming from the previous chapters, a

specific framework categorizing the contracts typologies can be issued, with

reference to the Energy Efficiency Report 2016. This framework will be used

afterwards to qualitatively describe the results of the surveys which has been

applied to the ESCOs. The framework reports the contract typologies and, for

each one, the associated risks, so that different typologies of operators (which

identifies in operators issuing a specific contractual form) are distinguished

with the criteria of evaluating their exposure to one or more risks’ typologies.

Obviously a single operator can decide to offer different types of contracts

(bearing different risks), depending on the customer it is dealing with and, in

particular, depending on what are the specific market and technologies

involved. There are indeed some cases in which the same operators cannot

bear the energy performance risk relative to a given technology and customer,

but it can bear the same risk when installing another kind of technology for

another type of customer (in terms of dimensions or needed guarantees in

terms of results).

Tab.5-The contracts’ typologies.

CONTRACT TYPOLOGY ASSOCIATED RISK

Turnkey Contract Operative risk

Energy Performance Contract Operative risk

Energy performance risk

Finance Contract Operative risk

Energy performance risk

Financing risk

All risk Contract Operative risk

Energy performance risk

Financing risk

Energy supply risk

Functioning risk

33

At this point a clear general overview of the most used contractual forms has

been provided and it will be discussed again during the analysis phase.

7.3.3 SPINs and EPC+ contracts

There is anyway another innovative contract form which is further and further

being developed: the EPC+ contract. This particular contract allows different

Energy Efficiency Service Providers to issue a single EPC collaborative

contract regulating a unique intervention indeed, as it was previously shown,

EESPs are very different one from the other, especially for what concerns

competences and core activities. This practice has been experimented in

some contexts as a collaboration between partners acting at different levels

of the Energy Efficiency Projects (Specialized installers, auditors, designers

and so on) or partners focused on different technologies; the collaboration

among these small partners has taken the acronym of SPIN (Small-Medium-

Enterprise Partnership for Innovative Energy services). Let’s consider, for

instance, that an ESCo has very good performances for what concerns the

installation of HVACs systems, this ESCo has technical competences and the

right experts and contacts for this kind of intervention. An optimized HVAC

system anyway often requires a good combination with building envelope

measures (i.e. roof insulation, windows replacement, etc.) to obtain the best

performances. The aforementioned ESCo cannot be able to provide technical

skills for this kind of installations and, furthermore, the two specific financial

analysis could be completely different: while the HVACs investments are

typically judged from a pay-off point of view, the building envelope measures

are evaluated by a depreciation point of view. These very different

perspectives, together with the need for of the customer to be served in a

dedicated way (which allows an integrated installation of the two solution) is

the source of the need for the SPINs’ contract. A SPIN between the two actors

indeed, could be fundamental in a case like this one, and could afford to offer

a very highly specialized and integrated intervention, increasing the quality

and the satisfaction of the customer. It is easy to understand that a contract

which aims to regulate such a kind of collaborative intervention and to involve

in it the customer too, could be very complex. It must basically consider a very

34

wide range of variables from the technical point of view (parameters) and also

from the financial point one. If furthermore we conjecture that the contract

provides a remuneration through the sharing of the savings, the complexity

from the legal point of view will be consistent too, being the savings shared

between two entities (or three considering the customer). It will not be easy to

quantify the exact “competence-quotes” of the shares for each actor involved

(from an economical point of view) and defining different responsibilities upon

final results will be difficult too.

The EPC+ contracts have been progressively standardized in the last years

and some business model canvas have been redacted, a lot of pilot projects

have been started through Europe, creating clusters of SMEs offering

integrated energy efficiency services. The potential of this solution is

enormous, the knowledge can be shared between the ESCo, which can enter

new markets through partnerships. Another factor that must be considered is

the need of integration which would perfectly fit some interventions. Let’ s think

about the “home” environment: the PV, the heat pumps together with

automation and HVACs system: just a few big and very integrated players

can offer the entire package of interventions.

The “EPC platform” is today active for the European states, allowing to

exchange not only information and know-how relative to the standard EPC but

also to better develop the SPIN perspective; in Italy a list of ESCOs

participating to a SPIN is present and specified into the Federesco site. It is

for this moment anyway, a field in continuous evolution which has been

deepened more by pilot projects than by the natural market demand. To

conclude, a brief SWOT analysis of SPINs is reported below.

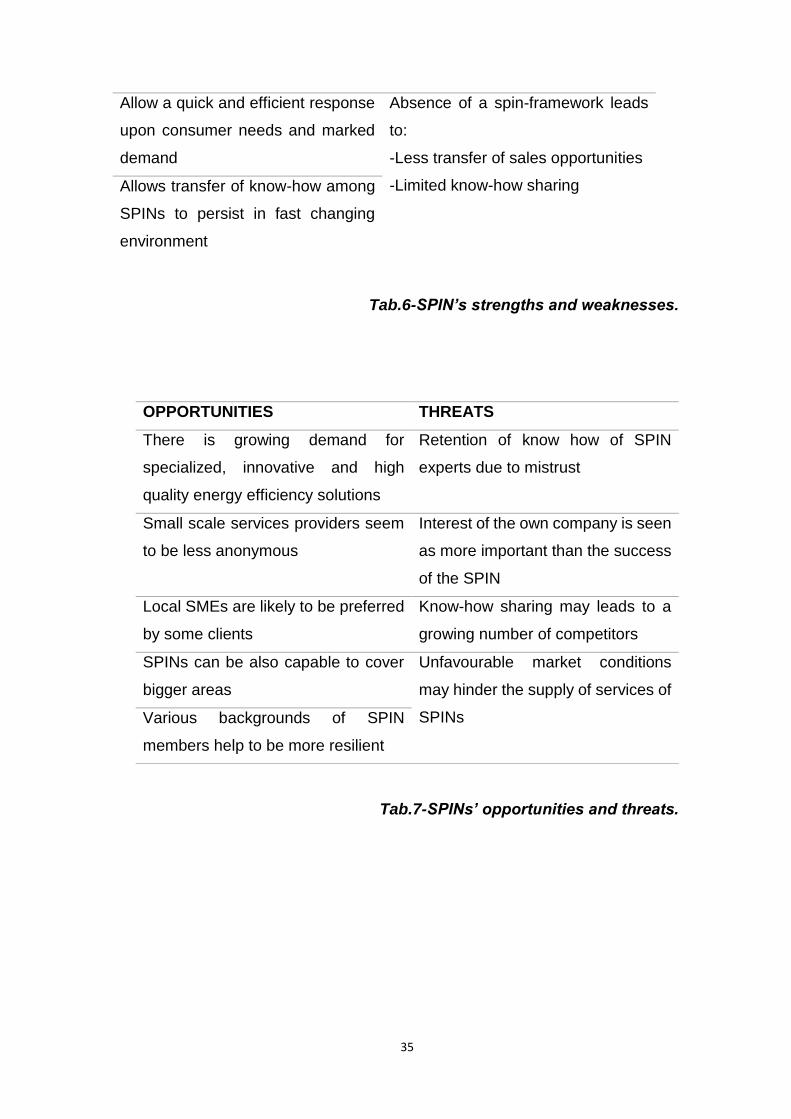

STRENGHTS WEAKNESSES

Services can be offered in higher

quality compared to services offered

by a single ESCO

Insufficient definition of an

appropriate SPIN-management

structure

Services can be provided at lower

cost to the customer

Different approaches from experts

lead to higher development costs

35

Tab.6-SPIN’s strengths and weaknesses.

Tab.7-SPINs’ opportunities and threats.

Allow a quick and efficient response

upon consumer needs and marked

demand

Absence of a spin-framework leads

to:

-Less transfer of sales opportunities

-Limited know-how sharing Allows transfer of know-how among

SPINs to persist in fast changing

environment

OPPORTUNITIES THREATS

There is growing demand for

specialized, innovative and high

quality energy efficiency solutions

Retention of know how of SPIN

experts due to mistrust

Small scale services providers seem

to be less anonymous

Interest of the own company is seen

as more important than the success

of the SPIN

Local SMEs are likely to be preferred

by some clients

Know-how sharing may leads to a

growing number of competitors

SPINs can be also capable to cover

bigger areas

Unfavourable market conditions

may hinder the supply of services of

SPINs Various backgrounds of SPIN

members help to be more resilient

36

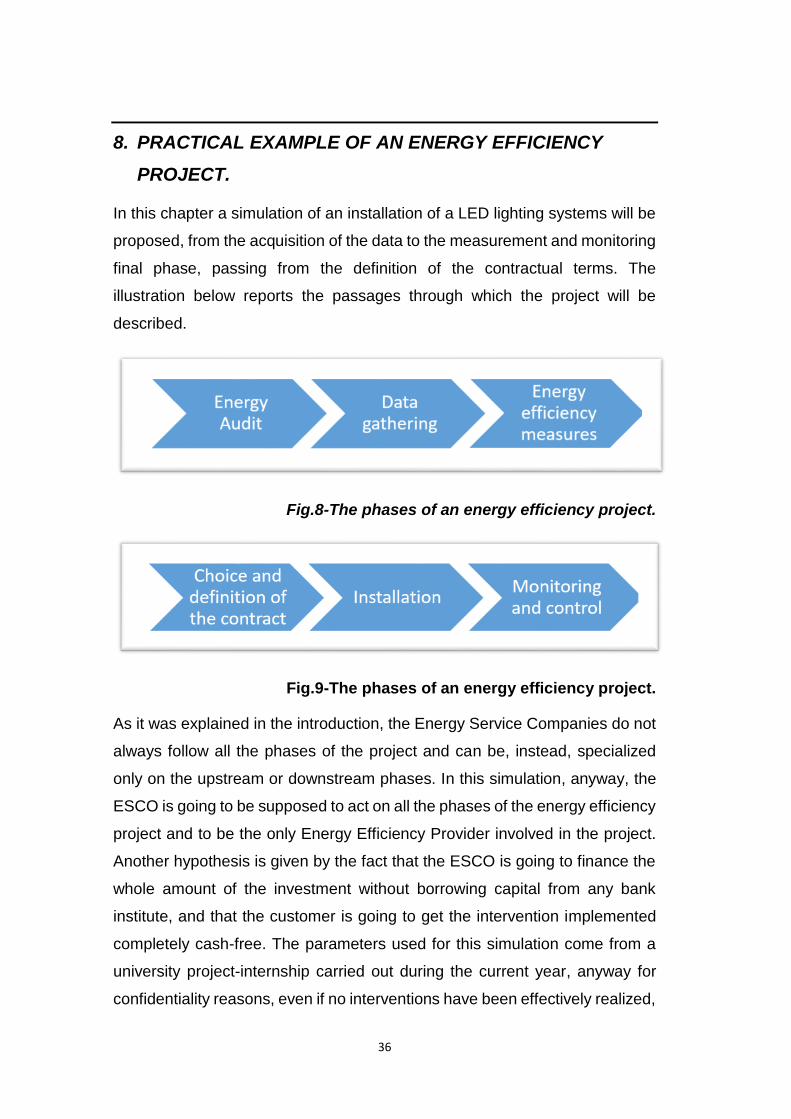

8. PRACTICAL EXAMPLE OF AN ENERGY EFFICIENCY

PROJECT.

In this chapter a simulation of an installation of a LED lighting systems will be

proposed, from the acquisition of the data to the measurement and monitoring

final phase, passing from the definition of the contractual terms. The

illustration below reports the passages through which the project will be

described.

Fig.8-The phases of an energy efficiency project.

Fig.9-The phases of an energy efficiency project.

As it was explained in the introduction, the Energy Service Companies do not

always follow all the phases of the project and can be, instead, specialized

only on the upstream or downstream phases. In this simulation, anyway, the

ESCO is going to be supposed to act on all the phases of the energy efficiency

project and to be the only Energy Efficiency Provider involved in the project.

Another hypothesis is given by the fact that the ESCO is going to finance the

whole amount of the investment without borrowing capital from any bank

institute, and that the customer is going to get the intervention implemented

completely cash-free. The parameters used for this simulation come from a

university project-internship carried out during the current year, anyway for

confidentiality reasons, even if no interventions have been effectively realized,

37

the name of the company will not be shown and indicators, numbers and

parameters have to be intended as “proportional” to real values, and not as

“equal in absolute terms”.

In the energy audit phase the ESCO analyzes general consumptions of the

site to understand what are the main sources of consumption, this operation

consisted in on-site measuring, by using technical instruments and by letting

the personnel compile some surveys about machines utilization. The results

of this analysis underline an incidence of 53% on total consumptions of the

lighting system which will be the subject of the energy efficiency project from

this point. At this point the ESCO has gathered all the possible data about the

lighting system to understand what is the AS-IS situation, what are the

currently used technologies and determine what are the energy efficiency

opportunities to get lower consumption values. The lighting system consumes

more than 1 GWh per year: this value is computed by multiplying the number

of lamps of each sector of the site by the nominal power of the lamps (taking

into account the transitory effect in the start-lighting phase) by the number of

hours in which the lighting system is working in the given sector. Other

considerations were necessary for a precise evaluation of the intervention, but

they have been considered out-of-scope for the intents of this analysis. The

next step is the individuation of all the possible energy efficiency measures for

the site, they are a lot and with very different natures the one from the others:

changing in the layout disposition, painting the walls white, using partitioning

of the systems, installing sensors and finally changing the old lamps with new

generation LED lamps (much more energy efficiency measures are possible,

just some were reported here). All the energy efficiency measures are then

grouped in different “offer-packages” which differentiate themselves in terms

of investments, savings opportunities and payback-time. The selection of the

packages and the right combination of the energy efficiency measures is the

most important part in order to be as effective as possible with the customer:

the packages must be the best combination of energy efficiency measures

and give at the same time a wide set of alternatives to the customer. In our

case anyway, the ESCO entirely finance the project, and so we can suppose

that the purpose of the ESCO can get an higher weight in the final decision

38

which is supposed to be the one of installing the best configuration possible:

the chosen configuration is an innovative smart-lighting system in which all

the selected energy efficiency measures are integrated to work all together in

an optimized way. It is basically a smart lighting system in which each lighting

fixture is equipped with different sensors such as motion, temperature and

daylight detectors. Each luminaire is then connected to a central server

through a Wi-Fi network, which serves as a controller for the performance of

the fixtures. The site’s personnel could control, wirelessly from the software,

the light utilization based on set parameters. Moreover, they could

automatically set up the system’s luminous output for the day, as well as

checking the status of each luminaire in all circumstances.

The definition of the financial parameters has been carried out by interviewing

some suppliers and so it refers to absolutely valid and real numbers. The

following step is the determination of the forecasted savings, which will be the

base for the definition of the contract parameters with the customer. The

smart-lighting solutions offers incredibly good results in terms of savings, so

that, despite of the very high initial investment needed, the offered paybacks

is inferior to 3 years, which is usually the limit imposed by the majority of the

Italian companies for what concerns investments in energy efficiency

measures. The estimated savings in terms of consumptions are indeed the

90%, this value must obviously be referred to the actual installed technology

of the site (in other cases the same intervention could lead to higher or lower

savings in terms of consumptions) and to the very high degree of

innovativeness of the new one. Considering the price of the energy at 0,158

€/kwh the savings per year have been estimated in 170.000 € as regards the

sole avoided energy consumption. In a second moment also TEE certificates

incomes and incentives have been evaluated and included in the returns.

Instead, as for the cost of the investment all the possible variables have been

taken into consideration: system layout modification costs, cost of the lamps,

costs of installation, insurance costs, disruption costs and VAT at 10% has

been considered too. At this point it is possible to define the investment with

the usual parameters NPV, IRR, ROI and payback-time, as it is reported in

the following tab.

39

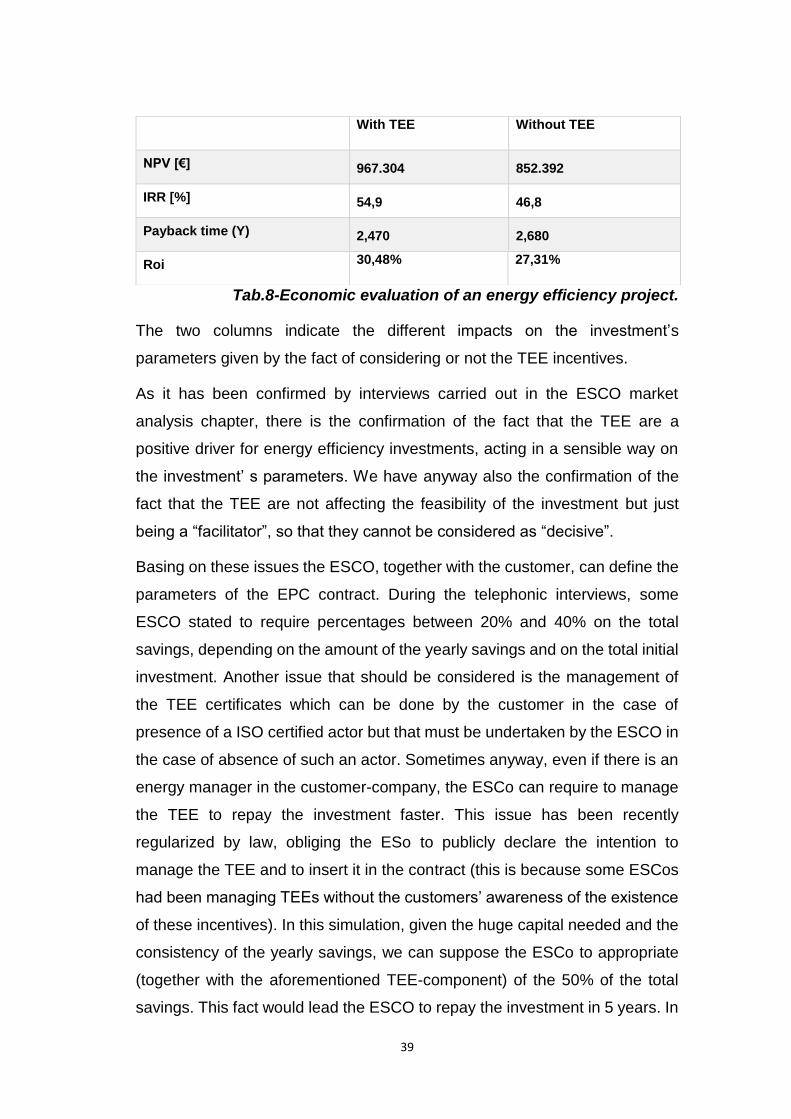

Tab.8-Economic evaluation of an energy efficiency project.

The two columns indicate the different impacts on the investment’s

parameters given by the fact of considering or not the TEE incentives.

As it has been confirmed by interviews carried out in the ESCO market

analysis chapter, there is the confirmation of the fact that the TEE are a

positive driver for energy efficiency investments, acting in a sensible way on

the investment’ s parameters. We have anyway also the confirmation of the

fact that the TEE are not affecting the feasibility of the investment but just

being a “facilitator”, so that they cannot be considered as “decisive”.

Basing on these issues the ESCO, together with the customer, can define the

parameters of the EPC contract. During the telephonic interviews, some

ESCO stated to require percentages between 20% and 40% on the total

savings, depending on the amount of the yearly savings and on the total initial

investment. Another issue that should be considered is the management of

the TEE certificates which can be done by the customer in the case of

presence of a ISO certified actor but that must be undertaken by the ESCO in

the case of absence of such an actor. Sometimes anyway, even if there is an

energy manager in the customer-company, the ESCo can require to manage

the TEE to repay the investment faster. This issue has been recently

regularized by law, obliging the ESo to publicly declare the intention to

manage the TEE and to insert it in the contract (this is because some ESCos

had been managing TEEs without the customers’ awareness of the existence

of these incentives). In this simulation, given the huge capital needed and the

consistency of the yearly savings, we can suppose the ESCo to appropriate

(together with the aforementioned TEE-component) of the 50% of the total

savings. This fact would lead the ESCO to repay the investment in 5 years. In

With TEE Without TEE

NPV [€] 967.304 852.392

IRR [%] 54,9 46,8

Payback time (Y) 2,470 2,680

Roi 30,48% 27,31%

40

the years following the fifth, the percentage of savings in favour of the ESCO

could progressively decrease, letting to the customer the possibility of highest

savings. In the case of this installation, it could be reasonable for the ESCO

to progressively decrease savings almost for another three or four years in

order to get the right profits by the project realization (the shared savings could

be scaled as following: 50%, 40%, 30%, 20%).

These parameters cannot be described in a standardized way, they indeed

strictly depend on the risk level of the intervention and on the yield of the

investment. The installation phase instead is surely the most complex from

the point of view of the operations; even if it is under the responsibility of the

ESCO, it can be carried out by a specialized installer, because of the use of

particular structures or machines and because of specific know-how reasons.

The height of the site is indeed considerable (14 meters) and normally also

the most integrated ESCo do not own the right equipment for such an

installation. Considering the current case of LED-installation a possible

criticality might be the mounting of the new lamps without interrupting the

activities of the site; issues like that must be carefully analysed with the site’s

management because they can decisively affect the profitability of the whole

investment, even if indirectly. Let’s suppose for example that lights must be

changed above a warehouse aisle, in this case the installation should be made