Languages

Pages

Legal

CONCEPTUAL FRAMEWORK OF VALUATION

The term 'valuation' implies the task of estimating the worth/value of an asset, a security or a

business. The price an investor or a firm (buyer) is willing to pay to purchase a specific asset/

security would be related to this value. Obviously, two different buyers may not have the

same valuation for an asset/business as their perception regarding its worth/value may vary;

one may perceive the asset/business to be of higher worth (for whatever reason) and hence

may be willing to pay a higher price than the other. A seller would consider the negotiated

selling price of the asset/business to be greater than the value of the asset/business he is

selling.

Evidently, there are unavoidable subjective considerations involved in the task and process of

valuation. Inter-se, the task of business valuation is more awesome than that of an asset or an

individual security. In the case of business valuation, the valuation is required not only of

tangible assets (such as plant and machinery, land and buildings, office equipments, and so

on) but also of intangible assets (like, goodwill, brands, patents, trademark and so on) as well

as human resources that run/manage the business. Likewise, there is an imperative need to

take into consideration recorded liabilities as well as unrecorded/contingent liabilities so that

the buyer is aware of the total sums payable, subsequent to the purchase of business. Thus,

the valuation process is affected by, subjective considerations. In order to reduce the element

of subjectivity, to a marked extent, and help the finance manager to carry out a more credible

valuation exercise in an objective manner, the following concepts of value are explained in

this Section: (i) book value, (ii) market value, (iii) intrinsic value, (iv) liquidation value, (v)

replacement value, (vi) salvage value, (vii) value of goodwill and (viii) fair value.

Book Value

The book value of an asset refers to the amount at which an asset is shown in the balance

sheet of a firm. Generally, the sum is equal to the initial acquisition cost of an asset less

accumulated depreciation. Accordingly, this mode of valuation of assets is as per the going

concern principle of accounting. In other words, book value of an asset shown in balance

does not reflect its current sale value.

Book value of a business refers to total book value of all valuable assets (excluding fictitious

assets, such as accumulated losses and deferred revenue expenditures, like advertisement,

preliminary expenses, cost of issue of securities not written off) less all external liabilities

(including preference share capital). It is also referred to as net worth.

Market Value

In contrast to book value, market value refers to the price at which an asset can be sold in the

market. The market value can be applied with respect to tangible assets only; intangible assets

(in isolation), more often than not, do not have any sale value. Market value of a business

refers to the aggregate market value (as per stock market quotation) of all equity shares

"outstanding. The market value is relevant to listed companies only.

Intrinsic/Economic Value

The intrinsic value of an asset is equal to the present value of incremental future cash inflows

likely to accrue due to the acquisition of the asset, discounted at the appropriate required rate

of return (applicable to the specific asset intended to be purchased). It represents the

maximum price the buyer would be willing to pay for such an asset. The principle of

valuation based on the dis-counted cash flow approach (economic value) is used in capital

budgeting decisions.

In the case of business intended to be purchased, its valuation is equivalent to the present

value of incremental future cash inflows after taxes, likely to. accrue to the acquiring firm,

discounted at the relevant risk adjusted discount rate, as applicable to the acquired business.

The economic value indicates the maximum price at which the business can be acquired.

Liquidation Value

As the name suggests, liquidation value represents the price at which each individual asset

can be sold if business operations are discontinued in the wake of liquidation of the firm. In

operational terms, the liquidation value of a business is equal to the sum of (i) realisable

value of assets and (ii) cash and bank balances minus the payments required to discharge all

external liabilities. In general, among all measures of value, the liquidation value of an

asset/or business is likely to be the least.

Replacement Value

The replacement value is the cost of acquiring a new asset of equal utility and usefulness. It is

normally useful in valuing tangible assets such as office equipment and furniture and fixtures,

which do not contribute towards the revenue of the business firm.

Salvage Value

Salvage value represents realisable/scrap value on the disposal of assets after the expiry of

their economic useful life. It may be employed to value assets such as plant and machinery.

Salvage value should be considered net of removal costs.

Value of Goodwill

The valuation of goodwill is conceptually the most difficult. A business firm can be said to

have 'real' goodwill in case it earns a rate of return (ROR) on invested funds higher than the

ROR earned by similar firms (with the same level of risk). In operational terms, goodwill

results when the firm earns excess ('super') profits. Defined in this way, the value of goodwill

is equivalent to the present value of super profits (likely to accrue, say for 'n' number of years

in future), the discount rate being the required rate of return applicable to such business firms.

The value of goodwill in terms of the present value of super profits method can serve as a

useful benchmark in terms of the amount of .goodwill the firm would be willing to pay for

the acquired business. In the case of mergers and acquisition decisions, the value of goodwill

paid is equal to the net difference between the purchase price paid for the acquired business

and the value of assets acquired net of liabilities the acquiring firm has undertaken to pay for.

Fair Value

The concept of 'fair' value draws heavily on the value concepts discussed above, in particular,

book value, intrinsic value and market value. The fair value is hybrid in nature and often is

the average of these three values. In India, the concept of fair value has evolved from case

laws (and hence is more statutory in nature) and is applicable to certain specific transactions,

like payment to minority shareholders.

It may be noted that most of the concepts related to value are 'stock' based in that they are

guided by the worth of assets at a point of time and not the likely contribution they can make

towards earnings/cash flows of the business in the future. Ideally, business valuation should

be related to the cash flow generating ability of acquired business. The intrinsic value reflects

the firm's capacity to generate cash flows over the long-run and, hence, seems to be more

aptly suited for business valuation.

In fact, in general, business firms are not acquired with the intent to sell their assets in the

post-acquisition period. They are to be deployed primarily for generating more earnings.

However, from the conservative point of view, it will be useful to know the realisable value,

market value, liquidation value and other values, if the acquiring firm has to resort to

liquidation. In brief, the finance manager will find it useful to know business valuation from

different perspectives. For instance, the book value may be very relevant form accounting/tax

purposes; the market value may be useful in determining share exchange ratio and liquidation

value may provide an insight into the maximum loss, if the business is to be wound up.

APPROACHES/METHODS OF VALUATION

The various approaches to valuation of business with focus on equity share valuation are

examined in this Section. These approaches should not be considered as competing

alternatives to the dividend valuation model. Instead, they should be viewed as providing a

range of values, catering to varied needs, depending on the circumstances. The major

approaches, namely, the (i) asset based approach to valuation, (ii) earnings based approach to

valuation, (iii) market value based approach to valuation and (iv) the fair value method to

valuation are described below.

Asset-Based Approach to Valuation

Asset-based approach focuses on determining the value of net assets from the perspective of

equity share valuation. What should the basis of assets valuation be, is the central issue of this

approach. It should be determined whether the assets should be valued at book, market,

replacement or liquidation value. More often than not, they are (and should be) valued at

book value that is, original acquisition cost minus accumulated depreciation, as assets are

normally acquired with the intent to be used in business and not for resale. Thus, the

valuation of assets is based on the going concern concept. Some other value measure may be

used depending on circumstances of the case. For instance, if the plant and machinery has

outlived its economic useful life (earlier than its initial estimated period), and is not in use for

production, it will be in order to value the machinery at liquidation value.

Apart from tangible assets, intangible assets, such as goodwill, patents, trademark, brands,

know how, and so on, also need to be valued satisfactorily. It may be useful to adopt the super

profit method to value some of these assets.

To arrive at the net assets value, total external liabilities (including preference share capital)

payable are deducted from total assets (excluding fictitious assets). The company's net assets

are computed as per Equation

Net assets = Total assets - Total external liabilities

The value of net assets is also known as net worth or equity/ordinary shareholders’ funds.

Assuming the figure of net assets to be positive, it implies the value available to equity

shareholders after the payment of all external liabilities. Net assets per share can be obtained,

dividing net assets by the number of equity shares issued and outstanding. Thus,

Net assets per share = Net assets/Number of equity shares issued and outstanding

The value of net assets is contingent upon the measure of value adopted for the purpose of

valuation of assets and liabilities. In the case of book value, assets and liabilities are taken at

their balance sheet values. In the market value measure, assets shown in the balance sheet are

revalued at the current market prices. For the purpose of valuing assets, and liabilities, it will

be useful for a finance manager/valuer to accord special attention to the following points:

(i) While valuing tangible assets, such as plant and machinery, he should consider aspects

related to technological obsolescence and capital improvements made in the recent years.

Depreciation adjustment may also be needed in case the company is following unsound

depreciation policy in this regard.

(ii) Is the valuation of goodwill satisfactory, given the amount of profits, capital employed

and average rate of return available on such businesses?

(iii) With respect to current assets, are additional provisions required for "unrealisability"

of debtors? Likewise, are adjustments required for "unsaleable" stores and stock?

(iv) With respect to liabilities, there is a need for careful examination of 'contingent

liabilities', in particular when there is mention of them in the auditor's report, with a view to

assess what portion of such liabilities may fructify. Similarly, adjustments may be required on

account of guarantees invoked, income tax, sales tax and other tax liabilities that may arise.

The net assets valuation based on book value is in tune with the going concern

principle of. accounting. In contrast, liquidation value measure is guided by the realisable

value available on the winding up/liquidation of a corporate firm.

Liquidation value is the final net asset value (if any) per share available to the equity

shareholder. The value is given as per Equation.

Net assets per share = (Liquidation value of assets - Liquidation expenses - Total external

liabilities)/Number of equity shares issued and outstanding.

In the case of liquidation, assets are likely to be sold through an auction. In general, they are

likely to realise much less than their market values. This apart, sale proceeds from assets are

further dependent on whether the company has been forced to go into liquidation or has

voluntarily liquidated. In the case of the 'former' type of liquidation, the realisable value is

likely to be still lower.

The net asset value (NAV) per share will be the lowest under the liquidation value measure

(Example).

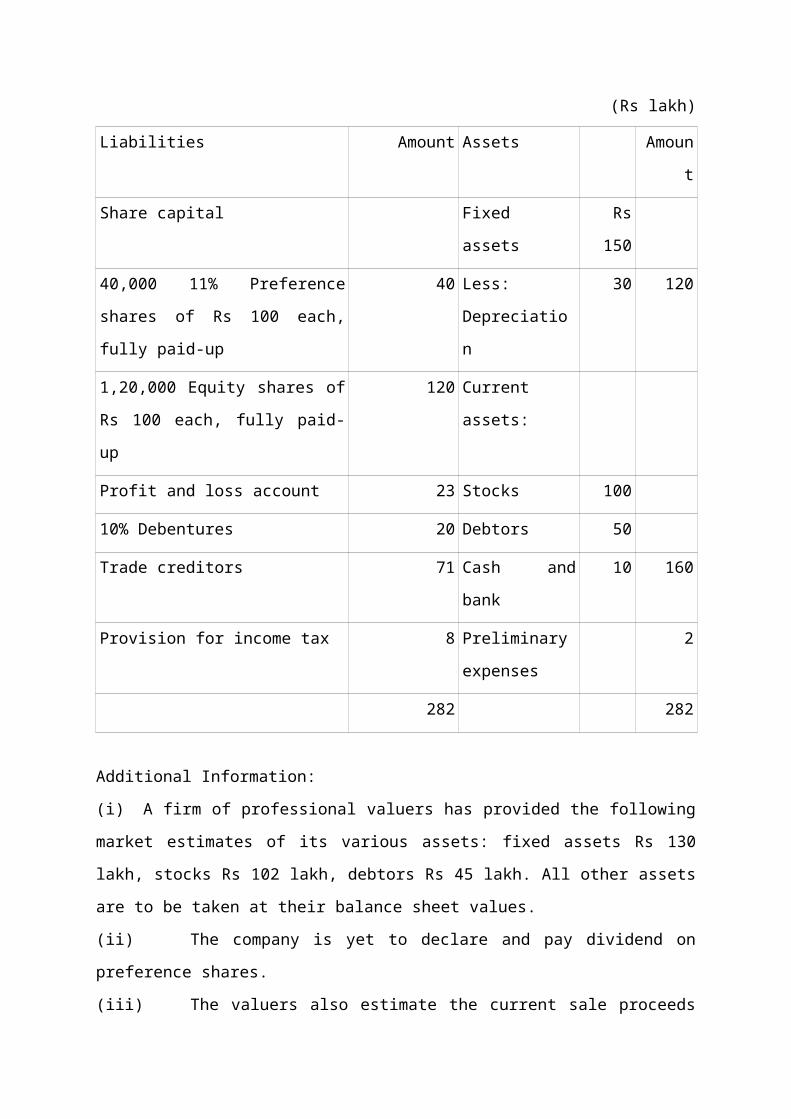

(Example Following is the balance sheet of Hypothetical Company Limited as on March

31, current year:

(Rs lakh)

Liabilities Amount Assets Amount

Share capital Fixed assets Rs 150

40,000 11% Preference shares of Rs

100 each, fully paid-up

40 Less:

Depreciation

30 120

1,20,000 Equity shares of Rs 100

each, fully paid-up

120 Current assets:

Profit and loss account 23 Stocks 100

10% Debentures 20 Debtors 50

Trade creditors 71 Cash and bank 10 160

Provision for income tax 8 Preliminary

expenses

2

282 282

Additional Information:

(i) A firm of professional valuers has provided the following market estimates of its

various assets: fixed assets Rs 130 lakh, stocks Rs 102 lakh, debtors Rs 45 lakh. All other

assets are to be taken at their balance sheet values.

(ii) The company is yet to declare and pay dividend on preference shares.

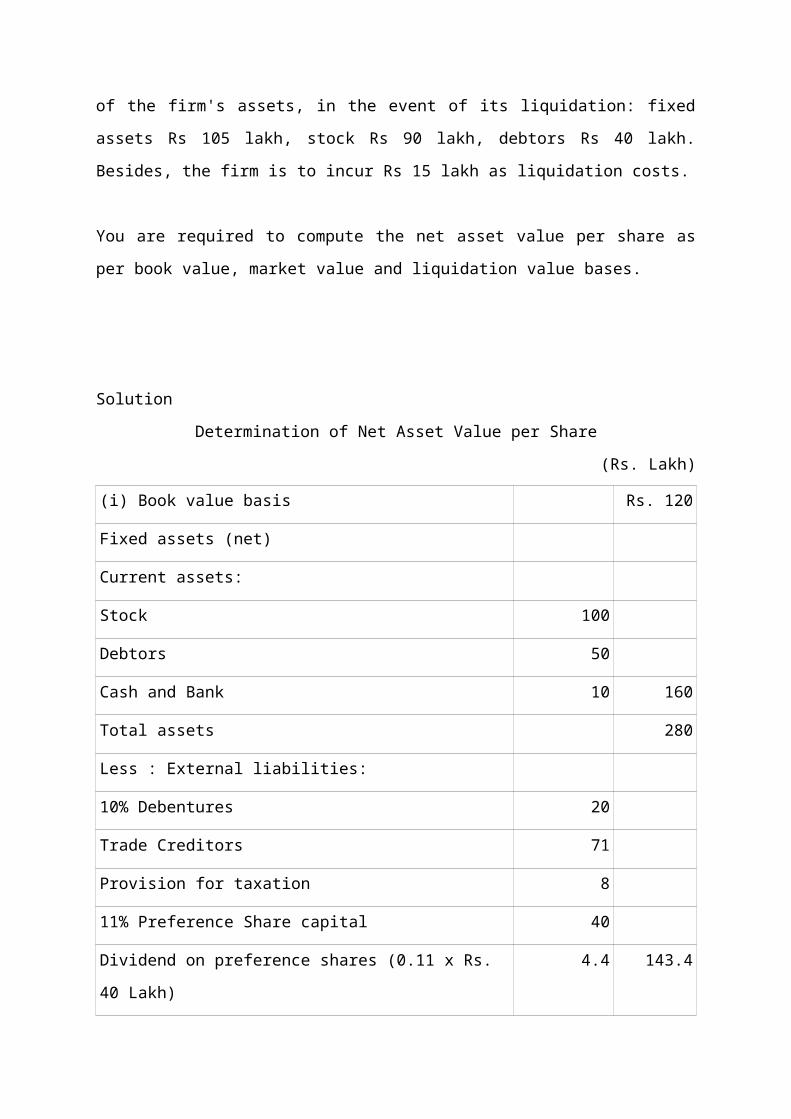

(iii) The valuers also estimate the current sale proceeds of the firm's assets, in the event of

its liquidation: fixed assets Rs 105 lakh, stock Rs 90 lakh, debtors Rs 40 lakh. Besides, the

firm is to incur Rs 15 lakh as liquidation costs.

You are required to compute the net asset value per share as per book value, market value and

liquidation value bases.

Solution

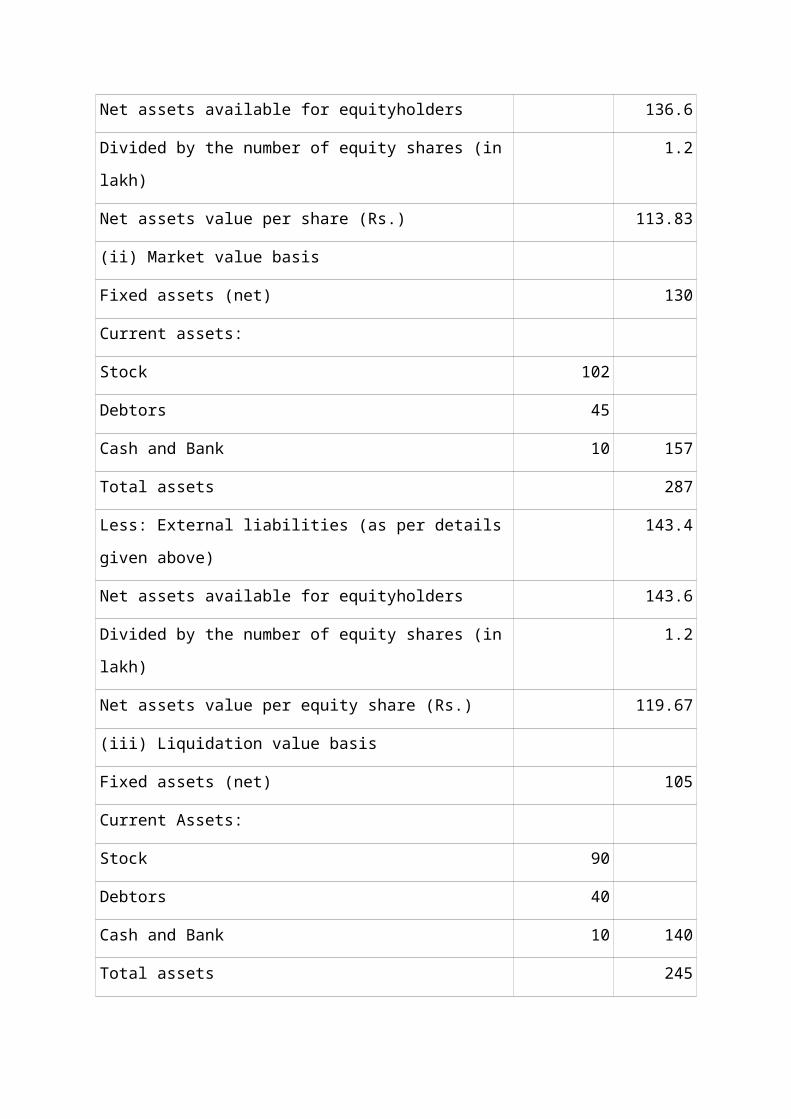

Determination of Net Asset Value per Share

(Rs. Lakh)

(i) Book value basis Rs. 120

Fixed assets (net)

Current assets:

Stock 100

Debtors 50

Cash and Bank 10 160

Total assets 280

Less : External liabilities:

10% Debentures 20

Trade Creditors 71

Provision for taxation 8

11% Preference Share capital 40

Dividend on preference shares (0.11 x Rs. 40 Lakh) 4.4 143.4

Net assets available for equityholders 136.6

Divided by the number of equity shares (in lakh) 1.2

Net assets value per share (Rs.) 113.83

(ii) Market value basis

Fixed assets (net) 130

Current assets:

Stock 102

Debtors 45

Cash and Bank 10 157

Total assets 287

Less: External liabilities (as per details given above) 143.4

Net assets available for equityholders 143.6

Divided by the number of equity shares (in lakh) 1.2

Net assets value per equity share (Rs.) 119.67

(iii) Liquidation value basis

Fixed assets (net) 105

Current Assets:

Stock 90

Debtors 40

Cash and Bank 10 140

Total assets 245

Less : external liabilities (listed above); 143.4

Less : Liquidation costs 15.0

Net assets available for equityholders 86.6

Divided by the number of equity shares (in lakh) 1.2

Net assets value per equity share (in Rs.) 72.17

The asset based approach is intuitively appealing in that it indicates the net assets backing per

equity share. However, the approach ignores the future earnings/cash flow generating ability

of the company's assets. In fact, the assets acquisition by business firms are not an end in

themselves; they are means to an end. The end is value maximization and firms acquire assets

for the purpose of creating value. The earning based approach reckons this perspective.

Earnings Based Approach to Valuation

The earnings approach is essentially guided by the economic proposition that business

valuation should be related to the firm's potential of future earnings or cash flow generating

capacity. This approach overcomes the limitation of assets-based approach, which ignores the

firm's prospects of future earnings and ability to generate cash in business valuation. Earnings

can be expressed in the sense of accounting as well as financial management. Accordingly,

there are two major variants of this approach: (i) earnings measure on accounting basis and

(ii) earnings measure on cash flow (financial management) basis.

Earnings Measure Based on Accounting—Capitalisation Method As per this method, the

earnings approach of business valuation is based on two major parameters, that is, the

earnings of the firm and the capatilisation rate applicable to such earnings (given the level of

risk) in the market. Earnings, in the context of this method, are the normal expected annual

profits. Normally to smoothen out the fluctuations in earnings, the average of past earnings

(say, of the last three to five years) is computed.

Apart from averaging, there is an explicit need for making adjustments, to the profits of the

past years, in extraordinary items (which are not likely to occur in the future), with a view to

arriving at credible future maintainable profits. The notable examples of extraordinary/non-

recurring items - include profits from the sale of land, losses due to sale of plant and

machinery, abnormal loss due to major fire, theft or natural calamities, substantial

expenditure incurred on the voluntury retirement scheme (not to be repeated) and abnormal

results due to strikes and lock-outs of major competing firm(s). Obviously, their non-

exclusion will cause distortion in determining sustainable future earnings.

Above all, it will be useful to understand the profile of the business, focussing on identifying

the major growth and income drivers. Are such drivers likely to continue in future years? If

not, projected profits need to be discounted. Finally, additional income expected in the

coming years— say, due to launch of a new product—should also be considered. In brief, the

valuer should try to familiarise himself or herself with all major factors/events that had

affected the profits of the business in the past year(s) and are likely to affect them in the

future years too.

Determination of appropriate capitalisation rate is another major requirement of this

approach. Capitalisation rate, normally expressed in percentages, refers to the investment

sum, that an investor is willing to make to earn a specified income. For instance, 12.5 per

cent capitalisation rate implies that an investor is prepared to invest Rs 100 to earn an income

of Rs 12.5 or an acquiring firm is prepared to invest Rs 100 to buy the expected profits of Rs

12.5 of another business.

Given the risk return framework of financial decision making, businesses that exhibit (or are

exposed to) higher business and financial risks obviously warrant a higher capitalisation

factor. Conversely, businesses carrying a low degree of risk are subject to lower capitalisation

factor. There are a host of factors that affect the risk complexion including fluctuation in

sales/earnings, degree of operating leverage, degree of financial leverage, nature of

competition, availability of substitute products and their prices, pace of change in technology

and the level of governmental regulations. Thus, there are a number of internal and external

factors associated with a business that can influence the risk and, hence, the capitalisation

factor.

The determination of the capitalisation factor is not an easy task in practice. A few guidelines/

principles may, however, be helpful to the valuer in its quantification. First, the capitalisation

factor for a business firm should be higher than that of a government security (normally

considered riskless). Secondly, the capitalisation factor should match/hover around the one

that is used for other firms operating in similar type of businesses. In case the valuer wants to

apply different capitalisation rate, there should be weighty and convincing reasons to do so.

For instance, firms having the potential and prospects of achieving abnormal growth rates

(for reasons that are firm specific), vis-a-vis other firms in the industry, managed by a well

known management team (having a good track record), may have low capitalisation factor

and vice versa.

Having determined the two major inputs, Equation, can be used to compute the value of

business ,VB, (from the perspective of share owners).

VB = Future maintainable profits / Relevant capitalisation factor

Example. In the current year, a firm has reported a profit of Rs 65 lakh, after paying taxes @

35 per cent. On close examination, the analyst ascertains that the current year's income

includes: (i) extraordinary income of Rs 10 lakh and (ii) extraordinary loss of Rs 3 lakh.

Apart from existing operations, which arc-normal in nature and are likely to continue in the

future, the company expects to launch a new product in the coming year.

Revenue and cost estimates in respect of the new product are as follows: (Rs lakh)

Sales 60

Material Cost 15

Labour Cost (additional) 10

Allocated fixed costs 5

Additional fixed costs 8

From the given information, compute the value of the business, given that capitalisation rate

applicable to such business in the market is 15 per cent.

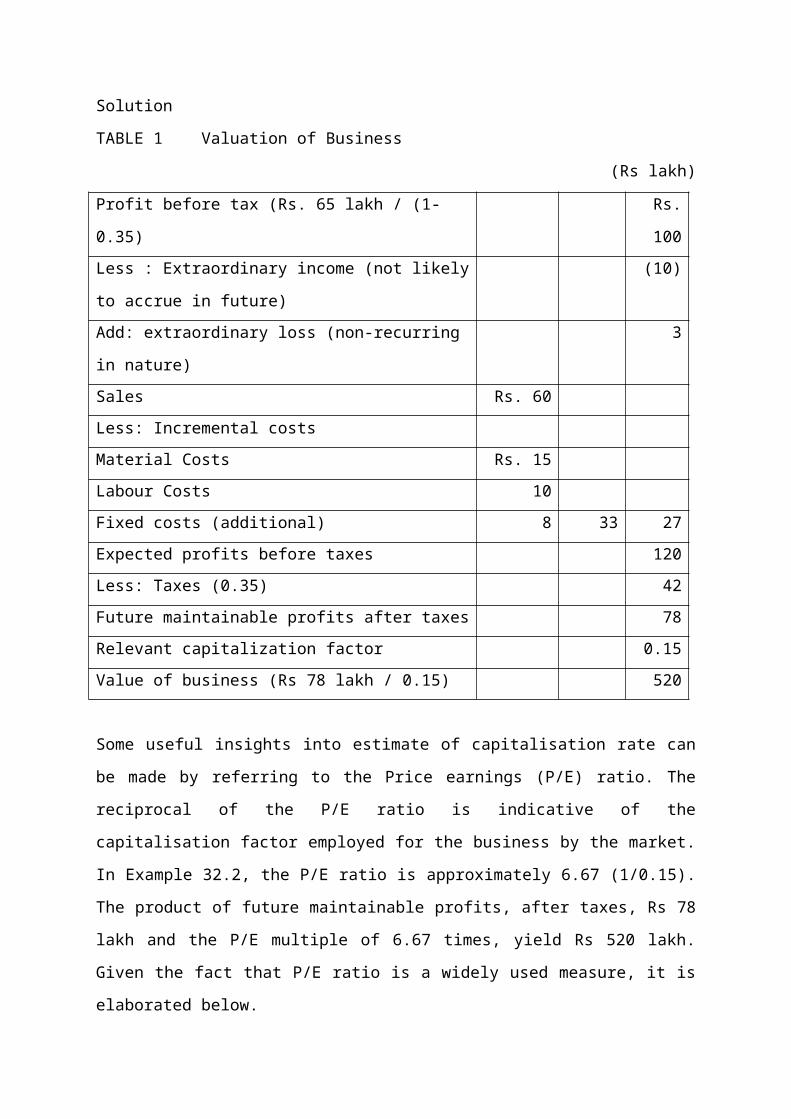

Solution

TABLE 1 Valuation of Business

(Rs lakh)

Profit before tax (Rs. 65 lakh / (1-0.35) Rs. 100

Less : Extraordinary income (not likely to accrue in

future)

(10)

Add: extraordinary loss (non-recurring in nature) 3

Sales Rs. 60

Less: Incremental costs

Material Costs Rs. 15

Labour Costs 10

Fixed costs (additional) 8 33 27

Expected profits before taxes 120

Less: Taxes (0.35) 42

Future maintainable profits after taxes 78

Relevant capitalization factor 0.15

Value of business (Rs 78 lakh / 0.15) 520

Some useful insights into estimate of capitalisation rate can be made by referring to the Price

earnings (P/E) ratio. The reciprocal of the P/E ratio is indicative of the capitalisation factor

employed for the business by the market. In Example 32.2, the P/E ratio is approximately

6.67 (1/0.15). The product of future maintainable profits, after taxes, Rs 78 lakh and the P/E

multiple of 6.67 times, yield Rs 520 lakh. Given the fact that P/E ratio is a widely used

measure, it is elaborated below.

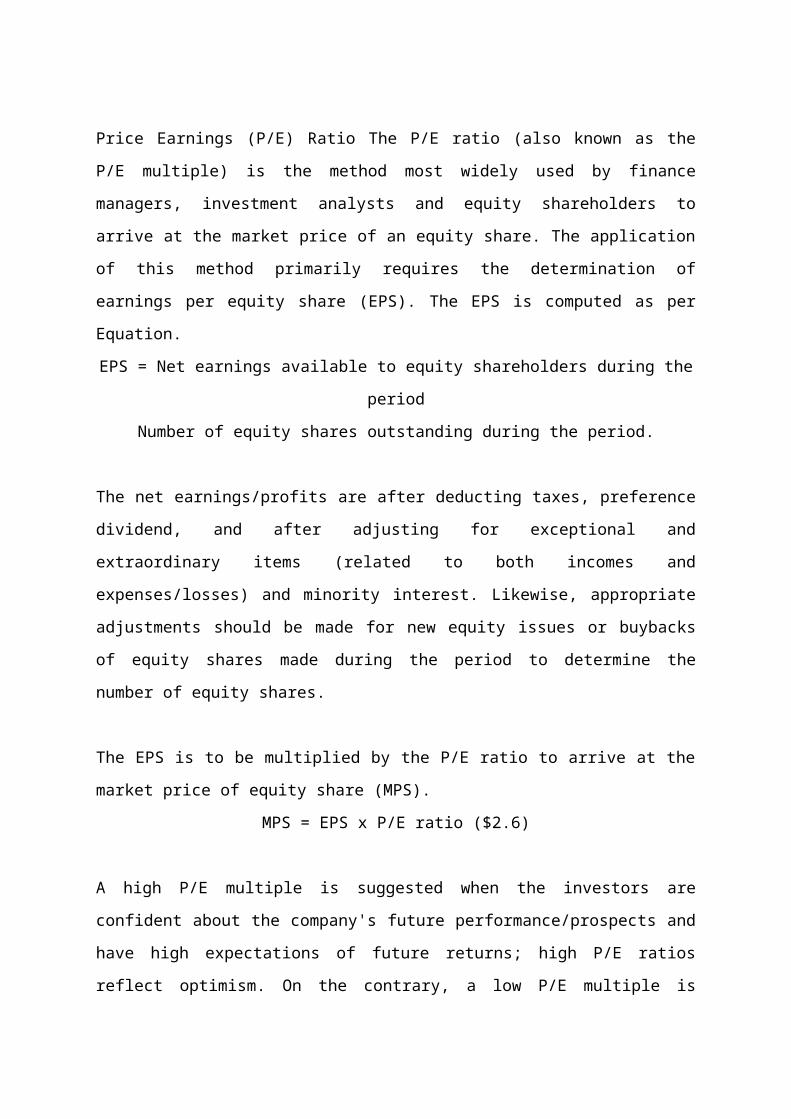

Price Earnings (P/E) Ratio The P/E ratio (also known as the P/E multiple) is the method most

widely used by finance managers, investment analysts and equity shareholders to arrive at the

market price of an equity share. The application of this method primarily requires the

determination of earnings per equity share (EPS). The EPS is computed as per Equation.

EPS = Net earnings available to equity shareholders during the period

Number of equity shares outstanding during the period.

The net earnings/profits are after deducting taxes, preference dividend, and after adjusting for

exceptional and extraordinary items (related to both incomes and expenses/losses) and

minority interest. Likewise, appropriate adjustments should be made for new equity issues or

buybacks of equity shares made during the period to determine the number of equity shares.

The EPS is to be multiplied by the P/E ratio to arrive at the market price of equity share

(MPS).

MPS = EPS x P/E ratio ($2.6)

A high P/E multiple is suggested when the investors are confident about the company's future

performance/prospects and have high expectations of future returns; high P/E ratios reflect

optimism. On the contrary, a low P/E multiple is suggested for shares of firms in which

investors have low confidence as well as expectations of low returns in future years; low P/E

ratios reflect pessimism.

The P/E ratio may be derived given the MPS and EPS.

P/E ratio = MPS/EPS

The future maintainable earnings/projected future earnings should also be used to determine

UPS. It makes economic sense in that investors have access to future earnings only. There is a

financial and economic justification to compute forward or projected P/E ratios with

reference to projected future earnings, apart from historic P/E ratios. This is all the more true

of present businesses-that operate in a highly turbulent business environment. Witness in this

context, the following: "In a dynamic business world, a firm's past earnings record may not

be an appropriate guide to its future earnings. For example, past earnings may have been

exceptional due to a period of rapid growth. This may not be sustainable in the future.

The P/E ratios should, however, be used with caution as the published P/E multiples are

normally based on the published financial statements of corporate enterprises. Obviously,

earnings are not adjusted for extraordinary items and, therefore, to that extent, may be

distorted. Besides, all financial fundamentals are often ignored in published data. Finally,

they reflect market sentiments, moods and perceptions. For instance, if investors are upbeat

about retail stocks, the P/E ratios of these stocks will be higher to reflect this optimism. This

can be viewed as a weakness as well, in particular when markets make systematic errors in

valuing entire sector. Assuming retail stocks have been overvalued, this error has to be built

into die valuation also.

In spite of these limitations attributed to the P/E ratio, it is the most widely used measure of

valuation.- The major plausible reasons are: (i) It is intuitively appealing in that it relates

price to earnings, (ii) It is simple to compute and is conveniently available in terms of

published data. (iii) It can be a proxy for a number of other characteristics of the. firm,

including risk and growth.

Example For facts in Example, determine the market price per equity share (based on

future earnings). Assuming:

(i) The company has 1,00,000 11% Preference shares of Rs 100 each, fully paid-up.

(ii) The company has 4,00,000 Equity shares of Rs 100 each, fully paid-up.

(iii) P/EE ratio is 8 times.

Solution

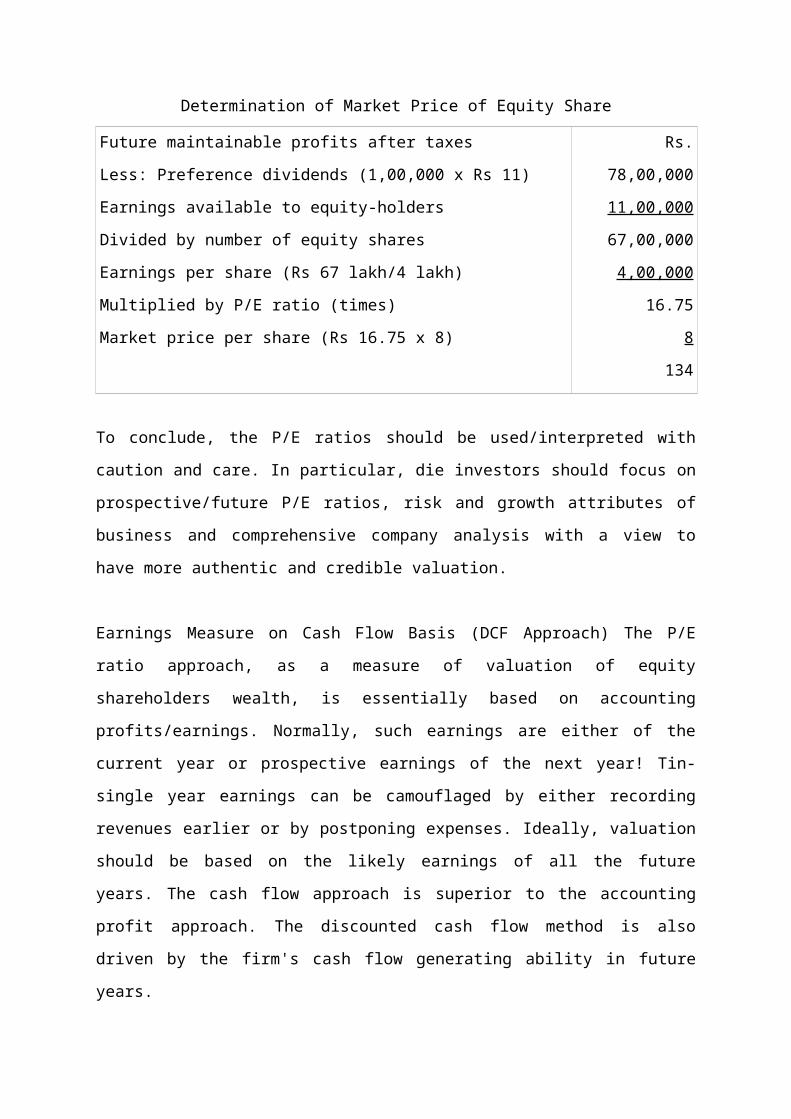

Determination of Market Price of Equity Share

Future maintainable profits after taxes

Less: Preference dividends (1,00,000 x Rs 11)

Earnings available to equity-holders

Divided by number of equity shares

Earnings per share (Rs 67 lakh/4 lakh)

Multiplied by P/E ratio (times)

Market price per share (Rs 16.75 x 8)

Rs. 78,00,000

11,00,000

67,00,000

4,00,000

16.75

8

134

To conclude, the P/E ratios should be used/interpreted with caution and care. In particular, die

investors should focus on prospective/future P/E ratios, risk and growth attributes of business

and comprehensive company analysis with a view to have more authentic and credible

valuation.

Earnings Measure on Cash Flow Basis (DCF Approach) The P/E ratio approach, as a measure

of valuation of equity shareholders wealth, is essentially based on accounting

profits/earnings. Normally, such earnings are either of the current year or prospective

earnings of the next year! Tin-single year earnings can be camouflaged by either recording

revenues earlier or by postponing expenses. Ideally, valuation should be based on the likely

earnings of all the future years. The cash flow approach is superior to the accounting profit

approach. The discounted cash flow method is also driven by the firm's cash flow generating

ability in future years.

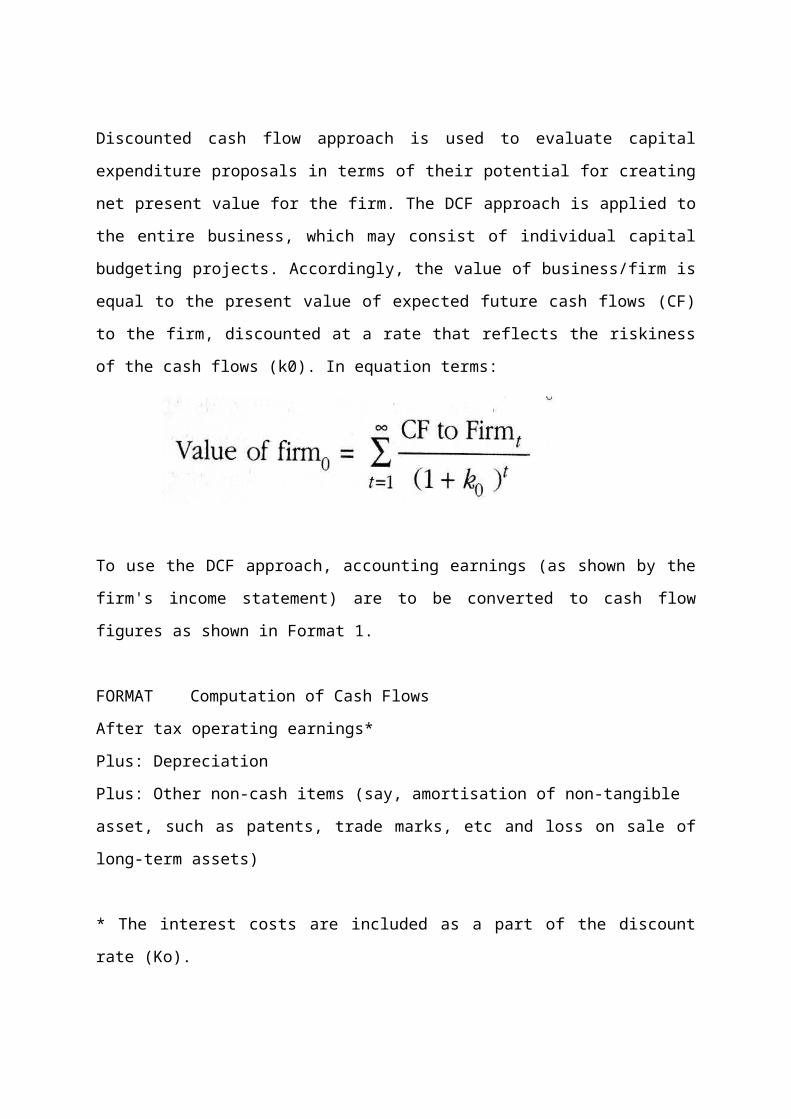

Discounted cash flow approach is used to evaluate capital expenditure proposals in terms of

their potential for creating net present value for the firm. The DCF approach is applied to the

entire business, which may consist of individual capital budgeting projects. Accordingly, the

value of business/firm is equal to the present value of expected future cash flows (CF) to the

firm, discounted at a rate that reflects the riskiness of the cash flows (k0). In equation terms:

To use the DCF approach, accounting earnings (as shown by the firm's income statement) are

to be converted to cash flow figures as shown in Format 1.

FORMAT Computation of Cash Flows

After tax operating earnings*

Plus: Depreciation

Plus: Other non-cash items (say, amortisation of non-tangible

asset, such as patents, trade marks, etc and loss on sale of long-term assets)

* The interest costs are included as a part of the discount rate (Ko).

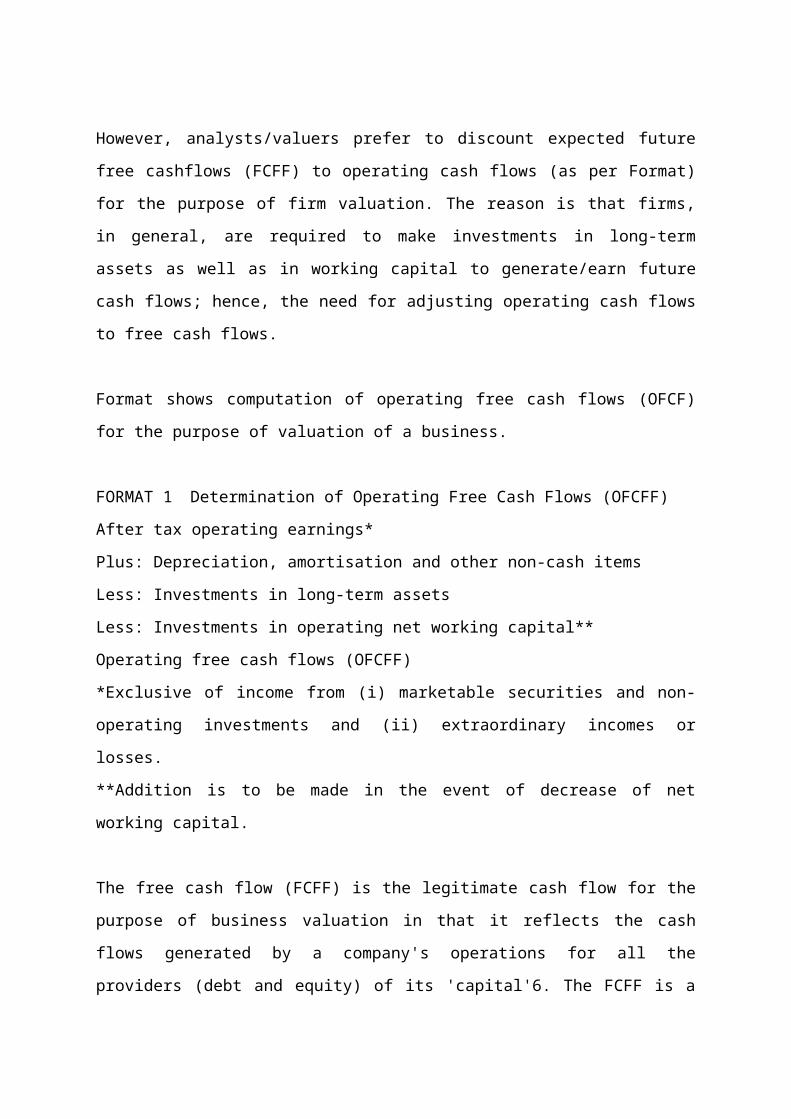

However, analysts/valuers prefer to discount expected future free cashflows (FCFF) to

operating cash flows (as per Format) for the purpose of firm valuation. The reason is that

firms, in general, are required to make investments in long-term assets as well as in working

capital to generate/earn future cash flows; hence, the need for adjusting operating cash flows

to free cash flows.

Format shows computation of operating free cash flows (OFCF) for the purpose of valuation

of a business.

FORMAT 1 Determination of Operating Free Cash Flows (OFCFF)

After tax operating earnings*

Plus: Depreciation, amortisation and other non-cash items

Less: Investments in long-term assets

Less: Investments in operating net working capital**

Operating free cash flows (OFCFF)

*Exclusive of income from (i) marketable securities and non-operating investments and (ii)

extraordinary incomes or losses.

**Addition is to be made in the event of decrease of net working capital.

The free cash flow (FCFF) is the legitimate cash flow for the purpose of business valuation in

that it reflects the cash flows generated by a company's operations for all the providers (debt

and equity) of its 'capital'6. The FCFF is a more comprehensive term as it includes cash flows

due to after tax non-operating income as well as adjustments for non-operating assets. Format

3 exhibits the procedure of determining FCFF.

FORMAT 2 Determination of Free Cash Flows (FCFF)

Operating free cash flows (as per Format 2)

Plus: After tax non-operating income/cash flows

Plus: Decrease (minus increase) in non-operating

Assets, say marketable securities

Free cash flows to Firm (FCFF)

*Non-operating income (1 - tax rate)

Since the FCFFs are available to all the capital providers of a corporate enterprise, the

discount rate to be applied to such cash flows should be indicative of the opportunity cost of

the funds made available by them, weighted by their relative contribution to the total capital

of a corporate enterprise. The opportunity cost is equivalent to the rate of return the investors

expect to earn on other investments of equivalent risk. The cost to the firm equals the

investors' cost less any tax benefits received by the company itself (say, tax advantage on the

payment of interest) plus any tax payments required to be made (say, dividend payment tax).

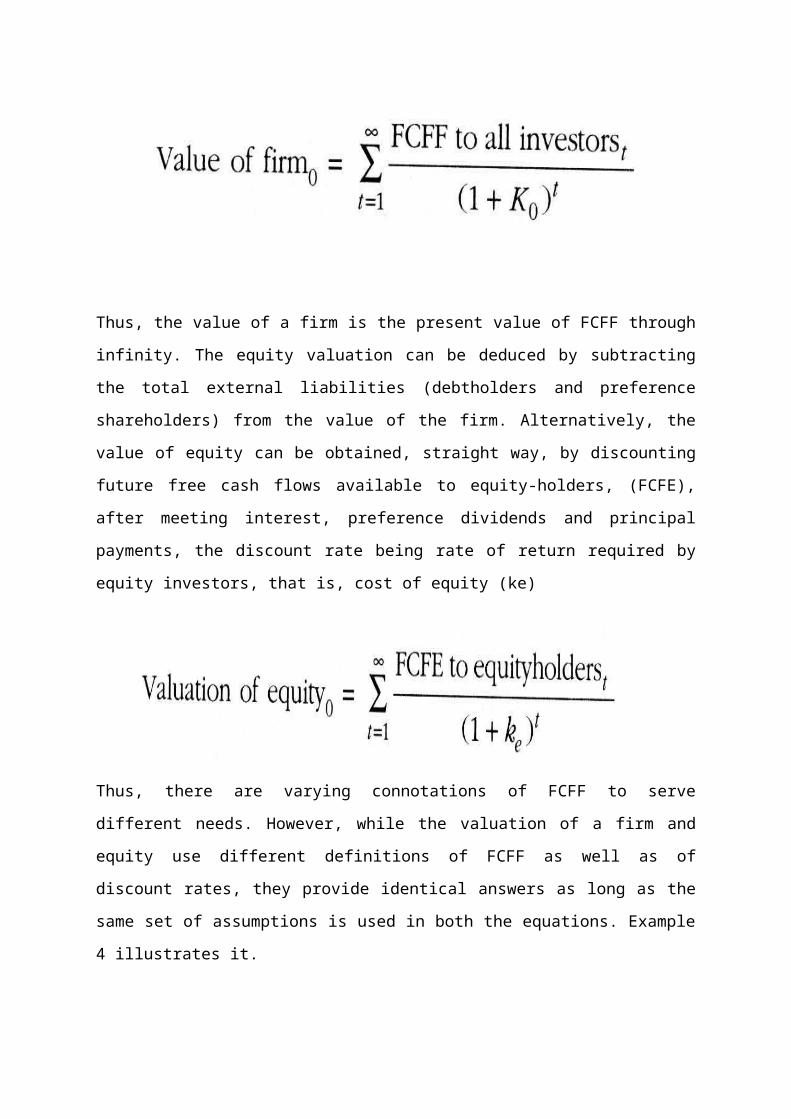

The value of the firm is given by Equation

Thus, the value of a firm is the present value of FCFF through infinity. The equity valuation

can be deduced by subtracting the total external liabilities (debtholders and preference

shareholders) from the value of the firm. Alternatively, the value of equity can be obtained,

straight way, by discounting future free cash flows available to equity-holders, (FCFE), after

meeting interest, preference dividends and principal payments, the discount rate being rate of

return required by equity investors, that is, cost of equity (ke)

Thus, there are varying connotations of FCFF to serve different needs. However, while the

valuation of a firm and equity use different definitions of FCFF as well as of discount rates,

they provide identical answers as long as the same set of assumptions is used in both the

equations. Example 4 illustrates it.

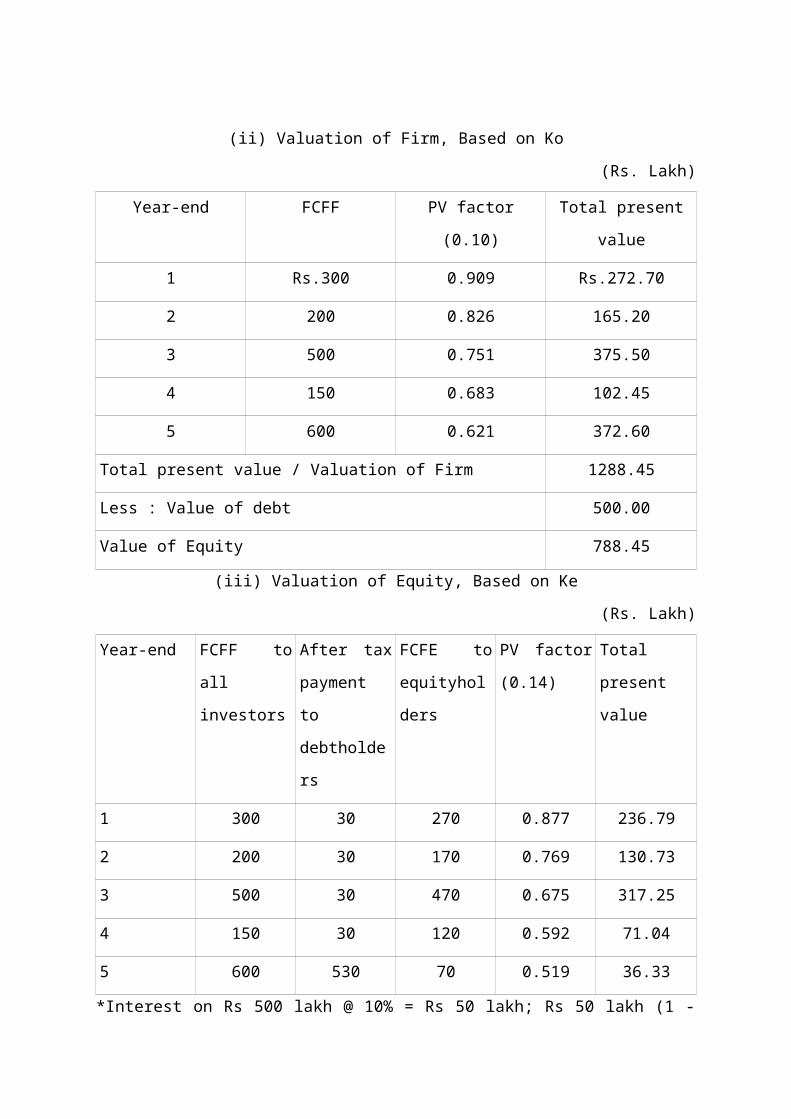

Example 4 Suppose a firm has employed a total capital of Rs 1,000 lakh (provided equally by

10 per cent debt and 5 lakh equity shares of Rs 100 each), its cost of equity is 14 per cent and

it is subject to corporate tax rate of 40 per cent. The projected free cash flows to all investors

of the firm for 5 years are given in the table:

(Rs. Lakh)

Year-end 1 Rs. 300

2 200

3 500

4 150

5 600

Compute (i) valuation of firm and (ii) valuation from the perspective of equityholders.

Assume 10 percent debt is rapayable at the year-end 5 and interest is paid at each year-end.

Solution

(i) Computation of Overall Cost of Capital

Source of capital After tax cost (%) Weights Total cost (%)

Equity 14 0.5 7

Debt 6* 0.5 3

Weighted average cost of capital (ko) 10

*10% (1-0.4 tax rate) = 6 percent

(ii) Valuation of Firm, Based on Ko

(Rs. Lakh)

Year-end FCFF PV factor (0.10) Total present value

1 Rs.300 0.909 Rs.272.70

2 200 0.826 165.20

3 500 0.751 375.50

4 150 0.683 102.45

5 600 0.621 372.60

Total present value / Valuation of Firm 1288.45

Less : Value of debt 500.00

Value of Equity 788.45

(iii) Valuation of Equity, Based on Ke

(Rs. Lakh)

Year-end FCFF to all

investors

After tax

payment to

debtholders

FCFE to

equityholders

PV factor

(0.14)

Total present

value

1 300 30 270 0.877 236.79

2 200 30 170 0.769 130.73

3 500 30 470 0.675 317.25

4 150 30 120 0.592 71.04

5 600 530 70 0.519 36.33

*Interest on Rs 500 lakh @ 10% = Rs 50 lakh; Rs 50 lakh (1 - 0.4) = Rs 30 lakh

**Inclusive of debt repayment of Rs 500 lakh at year-end 5.

Thus, the valuation of equity by both the methods is virtually the same (Rs 788.45 lakh and

Rs 792.14 lakh). The minor difference of Rs 3.69 lakh can be attributed primarily to

rounding-off the present value figures.

Total present value of the projected free cash flows to equityholder can be used to compute

free cash flows per equity share FCFE as per Equation 11.

FCFE per equity share = PV of FCFE to equityholders

Number of equity shares outstanding

In Example 4, FCFE per equity share is =

Rs 792.14 lakh = Rs 158.428

5 lakh

In Example 4, for the sake of simplicity, we have assumed the life of the corporate firm as 5

years. In practice, firms have perpetual long-term existence/indefinite life. Evidently, the

indefinite life of business/corporate firms, in general, is an additional aspect to be reckoned in

a firm's valuation. Ideally, one approach is to forecast future FCFF for a very long period of

time, say 30-40 years and ignore all subsequent year's FCFF. The reason is the discounted

value of such FCFF in such distant years will be insignificant. However, there are genuine

difficulties in explicitly forecasting decades of performance. In fact, it is virtually impossible

to make reasonably accurate forecasts of profits/cash flows beyond a certain period (say 7—

10 years) in most of the businesses.

To overcome the problem Copeland et al suggest that the exercise related to valuation of

business can be segregated into two periods, during and after an explicit forecast period. The

value of a business/firm is:

Present value of cash flows during explicit forecast period + Present value of cash flows after

explicit forecast period. (12)

What constitutes an ideal explicit forecast period? This question is not easy to answer. The

following guidelines may be relevant and useful in selecting such a period. Whereas in

cyclical businesses, the period can correspond to one full business cycle, in other businesses,

the period can match with the number of years during which they are likely to perform well.

In operational terms, the period should not be very short, say 2—3 years, and given the

current turbulent dynamic business world, the period, in general, should not be very long

also, say 10-15 years.

The explicit forecast period is die period in which the firm grows at a rapid pace; it is said to

be at saturation point at the end of the explicit forecast period, so far as growth rate is

concerned (the economic premise is that firms, in general cannot sustain abnormal rates of

growth for an indefinite period). The firm is expected to have attained a steady rate (at the

end of explicit forecast period) and starts growing at a stable growth rate, which is likely to

continue in future years. The value determined after the explicit forecast period is referred to

as the continuing value. According to Copeland et al the continuing value can be estimated as

per Equation 13-

Continuing value = NOPLATT+1 (1-g/ROICI)

k0 - g

Where NOPLATT+1 = The normalised level of net operating profits less adjusted taxes in the

first year after the explicit forecast period.

g= The expected growth rate in NOPLAT in perpetuity.

ROICI = The expected rate of return on the net new investment.

The derivation of the formula as per Equation 13 to compute continuing value is as follows:

Continuing value = FCFFT+1

k0-g (13.1)

Where FCFFT+1 refers to the normalised level of free cash flow in the first year after the

explicit forecast period.

Free cash flows (FCFF) can be defined in terms of NOPLAT and investment rate, IR (that is,

the percentage of NOPLAT reinvested in the business each year).

FCFF= NOPLAT (1-IR) (13.2)

We know, growth rate, g is the product of return on invested capital, ROICI and IR, ie,

g=ROICIxIR (13.3)

or IR=g/ROICI (13.4)

Incorporating value of IR in FCFF definition

FCFF= NOPLAT (l-g/ ROICI) (13.5)

Continuing value = NOPLAT(1-g/ ROICI)

k0-g

Equation 13 is termed as a value driven formula. Since Equations 13 and 13.1 provide the

same answer of continuing value, it is logistically more convenient to compute continuing

value based on Equation 13.1.

The major simplifying assumptions made in determining continuing value are: (i) the firm

earns a constant return on the existing invested capital; (ii) the firm's NOPLAT grows at a

constant rate and it invests the same proportion of its gross cash flow in business each year

and (iii) the firm earns a constant return on all new investments.

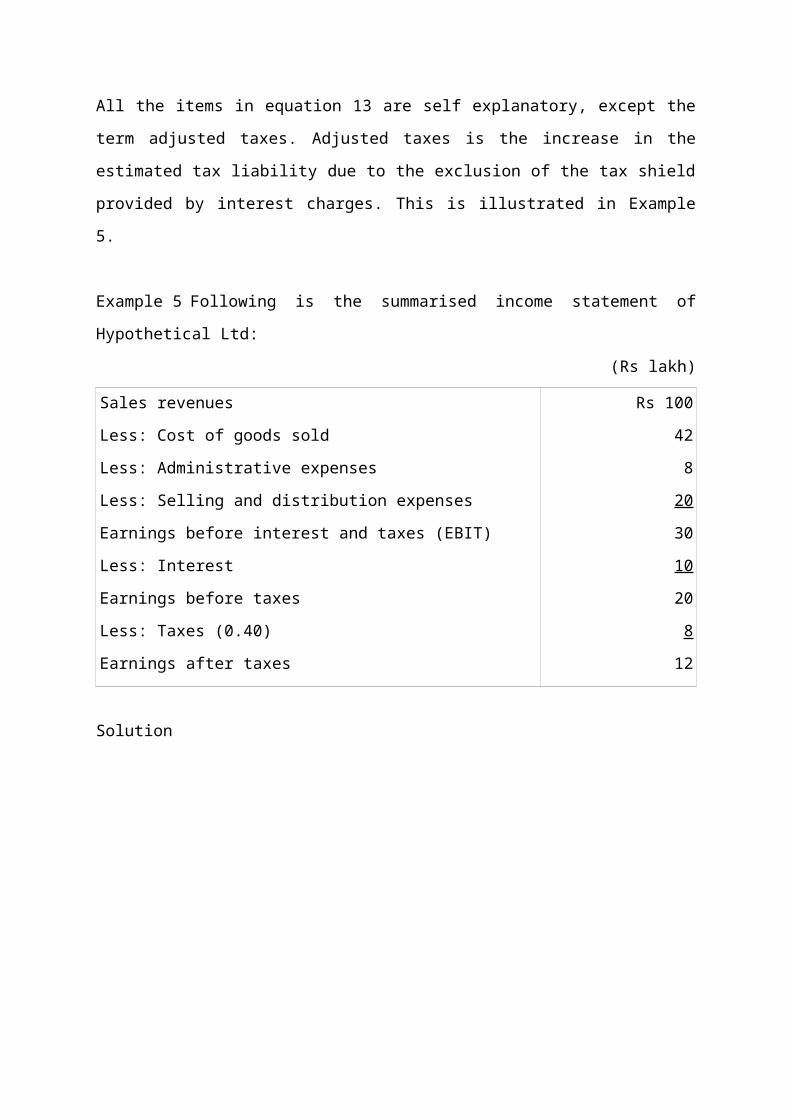

All the items in equation 13 are self explanatory, except the term adjusted taxes. Adjusted

taxes is the increase in the estimated tax liability due to the exclusion of the tax shield

provided by interest charges. This is illustrated in Example 5.

Example 5 Following is the summarised income statement of Hypothetical Ltd:

(Rs lakh)

Sales revenues

Less: Cost of goods sold

Less: Administrative expenses

Less: Selling and distribution expenses

Earnings before interest and taxes (EBIT)

Less: Interest

Earnings before taxes

Less: Taxes (0.40)

Earnings after taxes

Rs 100

42

8

20

30

10

20

8

12

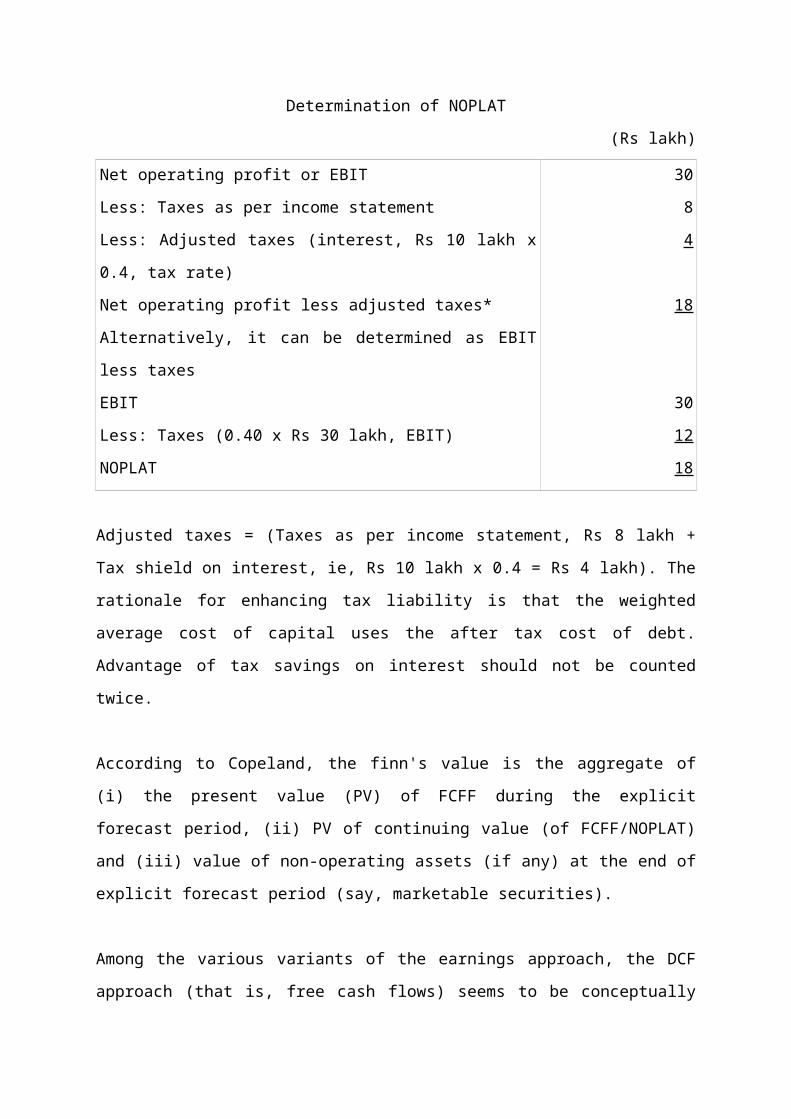

Solution

Determination of NOPLAT

(Rs lakh)

Net operating profit or EBIT

Less: Taxes as per income statement

Less: Adjusted taxes (interest, Rs 10 lakh x 0.4, tax rate)

Net operating profit less adjusted taxes*

Alternatively, it can be determined as EBIT less taxes

EBIT

Less: Taxes (0.40 x Rs 30 lakh, EBIT)

NOPLAT

30

8

4

18

30

12

18

Adjusted taxes = (Taxes as per income statement, Rs 8 lakh + Tax shield on interest, ie, Rs 10

lakh x 0.4 = Rs 4 lakh). The rationale for enhancing tax liability is that the weighted average

cost of capital uses the after tax cost of debt. Advantage of tax savings on interest should not

be counted twice.

According to Copeland, the finn's value is the aggregate of (i) the present value (PV) of FCFF

during the explicit forecast period, (ii) PV of continuing value (of FCFF/NOPLAT) and (iii)

value of non-operating assets (if any) at the end of explicit forecast period (say, marketable

securities).

Among the various variants of the earnings approach, the DCF approach (that is, free cash

flows) seems to be conceptually superior for business valuation as well as equity valuation..

The computation of FCFF and continuing value is illustrated in Example 6.

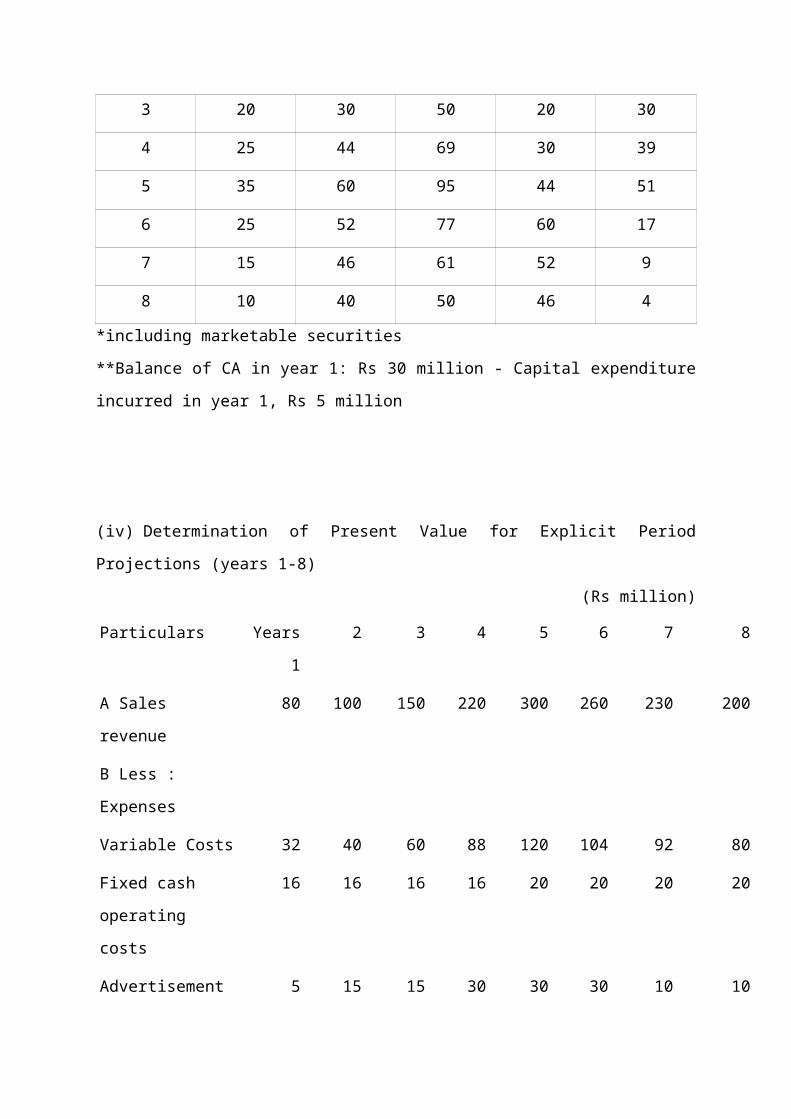

Example 6 Sagar Industries deals in production and sales of consumer durables. Its

expected sales revenues for the next 8 years (in Rs million) are given in the table:

Years Sales Revenue

1 Rs. 80

2 100

3 150

4 220

5 300

6 260

7 230

8 200

Its condensed balance sheet as on March 31, current year is as follows:

(Rs million)

Liabilities Amount Assets Amount

Equity Funds 120 Current Assets 30

12% Debt 80 Long-Term Assets (net) 170

200 200

Additional information:

(i) Its variable expenses will amount to 40 per cent of sales revenue. Fixed cash operating

costs are estimated to be Rs 16 million per year for the first 4 years and at Rs 20 million for

years 5 - 8. In addition, an extensive advertisement campaign will be launched, requiring

annual outlays as follows:

(ii) Long-term assets are subject to 15 per cent rate of depreciation on diminishing

balance method,

(iii) The company has' planned the following capital expenditure (assumed to have been

incurred in the beginning of each year) for the next 8 years,

(iv) Working capital in terms of investment in current assets are estimated at 20 per cent of

sales revenue,

(v) It is expected to have non-operating assets in terms of investments in marketable

securities in the initial year. The expected after tax non-operating cash flow in year 1 = Rs 0.5

million.

(vi) Given the tax benefits available to Sagar, the effective tax rate estimated is 30 per

cent.

(vii) The corporate equity capital is estimated at 16 per cent.

(viii) The free cash flow of the firm are expected to grow at 5 per cent per annum, after 8

years. Determine the discounted cash flow (DCF) value of the (i) firm and (ii) equity.

(Rs million)

1 Rs. 5

2-3 15

4-6 30

7-8 10

(Rs million)

Year 1 Rs. 5

2 8

3 20

4 25

5 35

6 25

7 15

8 10

Solution

(i) Determination of Weighted Average Cost of Capital

Source of Funds Cost (%) Weights Total (%)

Equity 16 0.6* 9.60

12% Debt 8.4 0.4** 3.36

12.96 = 13

(Rs 120 million/Rs 200 million); *.* (Rs 80 million/Rs,200 million)

(ii) Determination of Depreciation (Years 1 - 8)

(Rs million)

Year Long-term assets at beginning of year

Additions during the year

Total at the year-end

Depreciation @15%

1 Rs. 170.00 Rs 5 Rs. 175.00 Rs. 26.25

2 148.74 8 156.75 23.51

3 133.24 20 153.24 22.99

4 130.25 25 155.25 23.29

5 131.96 35 166.96 25.04

6 141.92 25 166.92 25.04

7 141.88 15 156.88 23.53

8 133.35 10 143.35 21.50

(iii) Determination of Investment [Capital Expenditure + Current Assets, (CA)] Required,

Years 1-8

(Rs million)

Year Investment required Existing

investments in

CA

Additional

investments

requiredCapital

expenditure

CA (Sales x

0.2)

Total

1 Rs 5 Rs. 16 Rs. 21 30* Nil

2 8 20 28 25** 3

3 20 30 50 20 30

4 25 44 69 30 39

5 35 60 95 44 51

6 25 52 77 60 17

7 15 46 61 52 9

8 10 40 50 46 4

*including marketable securities

**Balance of CA in year 1: Rs 30 million - Capital expenditure incurred in year 1, Rs 5

million

(iv) Determination of Present Value for Explicit Period Projections (years 1-8)

(Rs million)

Particulars Years

1

2 3 4 5 6 7 8

A Sales revenue 80 100 150 220 300 260 230 200

B Less : Expenses

Variable Costs 32 40 60 88 120 104 92 80

Fixed cash operating

costs

16 16 16 16 20 20 20 20

Advertisement 5 15 15 30 30 30 10 10

Depreciation 26.25 23.51 22.99 23.29 25.04 25.04 23.53 21.50

C EBIT (A-B) 0.75 5.49 36.01 62.71 104.96 80.96 84.47 68.50

D Less: Taxes (0.30) 0.22 1.65 10.80 18.81 31.49 24.29 25.34 20.55

E NOPAT 0.53 3.84 25.21 43.90 73.47 56.67 59.13 47.95

F Non-operating

income

0.50 - - - - - - -

G Gross cash flow

(E+F+Depreciation) 27.28 27.35 48.20 67.19 98.51 81.71 82.66 69.45

H Less:Investment in

Capital expenditure

- 3 30 39 51 17 9 4

plus current assets)

I Free cash flow (G-

H)

27.28 24.35 18.20 28.19 47.51 64.71 73.66 65.45

J PV Factor (0.13) 0.885 0.783 0.693 0.613 0.543 0.480 0.425 0.376

K Total PV(IxJ) 24.14 19.07 12.61 17.28 25.80 31.06 31.31 24.61

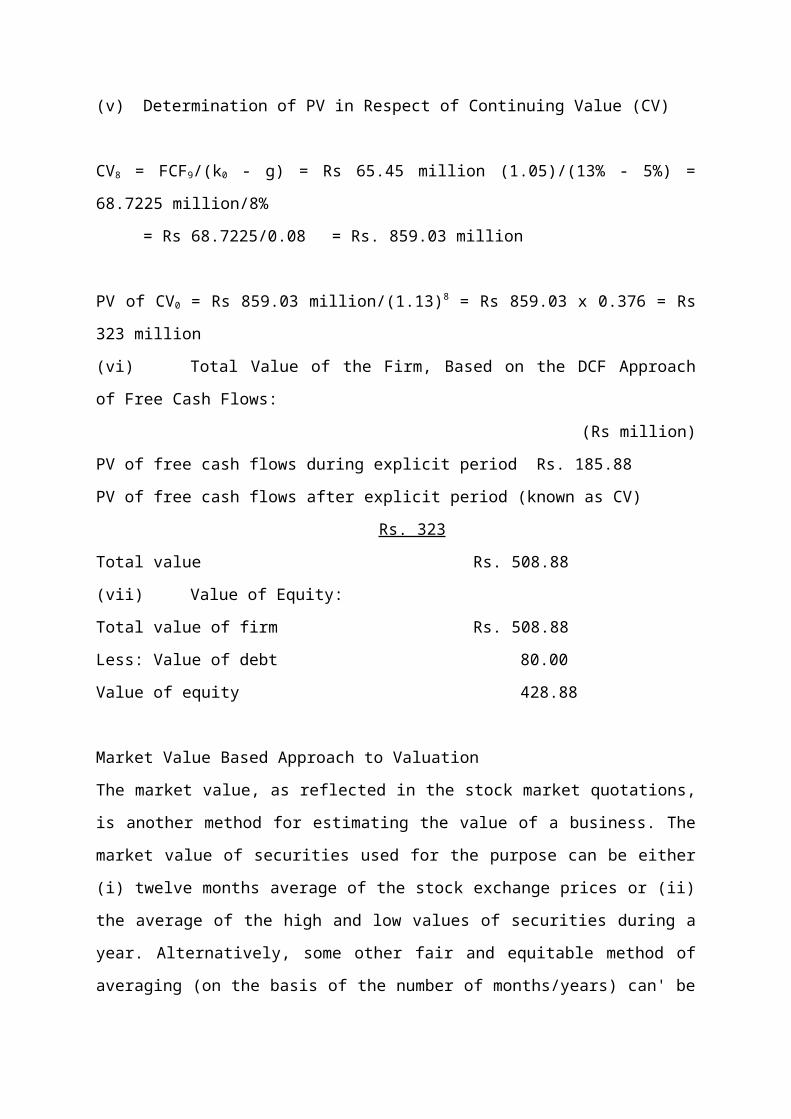

(v) Determination of PV in Respect of Continuing Value (CV)

CV8 = FCF9/(k0 - g) = Rs 65.45 million (1.05)/(13% - 5%) = 68.7225 million/8%

= Rs 68.7225/0.08 = Rs. 859.03 million

PV of CV0 = Rs 859.03 million/(1.13)8 = Rs 859.03 x 0.376 = Rs 323 million

(vi) Total Value of the Firm, Based on the DCF Approach of Free Cash Flows:

(Rs million)

PV of free cash flows during explicit period Rs. 185.88

PV of free cash flows after explicit period (known as CV)

Rs. 323

Total value Rs. 508.88

(vii) Value of Equity:

Total value of firm Rs. 508.88

Less: Value of debt 80.00

Value of equity 428.88

Market Value Based Approach to Valuation

The market value, as reflected in the stock market quotations, is another method for

estimating the value of a business. The market value of securities used for the purpose can be

either (i) twelve months average of the stock exchange prices or (ii) the average of the high

and low values of securities during a year. Alternatively, some other fair and equitable

method of averaging (on the basis of the number of months/years) can' be worked out, The

justification of market value as an approximation of the true worth of a firm is derived from

the fact that market quotations by and huge indicate the consensus of investors as to the firm's

earning potentials and the corresponding risk. The market value approach is one of the most

widely-used in determining value, in particular of large listed firms.

The major problem with this method is that the market value of a firm is influenced not only

by financial fundamentals but also by speculative factors. As a result, this value can change

abruptly due to speculative influences, market sentiments and personal expectations. Market

makers as well as other 'willing buyers or sellers' (interested in purchases or sales) can at

times significantly influence these prices. Another limitation of this approach is that this

approach cannot be applied if the shares are unlisted or are not actively traded.

Apart from the limited applicability of this method only to listed corporate enterprises, whose

shares/securities are actively traded, the valuation of a business is not in tune with the going

concern concept. Nevertheless, it may be/is of immense usefulness in deciding swap ratios of

shares in merger decisions. In fact, the market prices of the two companies can be the

objective of the decision. Alternatively, a certain percentage of premium, above the market

price may be offered as an inducement to the shareholders of the acquired company to

convince them to agree to sell their shares or to make them agree to the merger decisions.

Fair Value Method

The fair value method is not an independent method of share valuation like those discussed

above. This method uses the average/weightage average or one or more of the above

methods. Since this method uses the average concept, its virtue is that it helps in smoothening

out wide variations in estimated valuations as per different methods. In other words, this

approach provides, in a way, the 'balanced' figure of valuation.

In general, this method has limited application for business valuation. For instance, this

method of valuation of shares had been used till the early 1990's, by the erstwhile Controller

of Capital Issues (CCI) in India, for fixing the price of new equity issues. In case the equity

shares were to be issued at a premium, the amount of premium was based as the CCI

guidelines.

To sum up, no one method is appropriate for all circumstances/situations/requirements.

Therefore, it is important to recognise that the different methods are based on different

assumptions and depending on the circumstances, some methods may be more appropriate

than others. For instance, where there is paucity of information about profits, say (i) in the

case of new companies whose accounts do not serve as a guide to future profits, (ii) in the

case of companies operating at a loss with no prospects of earning profits in the near future

and (in) in the case of companies having unreliable statistics of profits owing to factors such

as disruption of business, the net asset method of valuation seems would be more appropriate.

In normal situations, the DCF (based on free cash flows) method would be suitable. In the

event of wide variations in the valuations as per these two methods, the fair value method

may be, used. In fact, it is useful for the finance manager/investor/valuer/analyst to know a

range of values from various perspectives.

OTHER APPROACHES TO VALUE MEASUREMENT

In recent years, a number of new approaches/techniques/methods to measure value (with

focus on shareholders) have been developed and practised. The two major approaches are

market value added (MVA) and economic value added (EVA). They are explanied in this

Section.

Market Value Added Approach (MVA)

The MVA approach measures the change in the market value of the firm's equity vis-a-vis

equity investment (consisting of equity share capital and retained profits). Accordingly,

MVA = Market value of firm's equity - Equity capital investment/funds

(14)

Though the concept of MVA is normally used in the context of equity investment (and, hence,

is of greater relevance for equity shareholders), it can also be adapted (like other previous

approaches) to measure value from the perspective of providers of all invested funds (i.e.,

including preference share capital and debt).

MVA = [Total market value of firm's securities - (Equity shareholders funds

+ Preference share capital + Debentures)] (15)

The MVA approach cannot be used for all types of firms. It is applicable to only firms whose

market prices are available. In that sense, the method has limited application. Besides, the

value provided by this approach may exhibit wide fluctuations, depending on the state of the

capital market/stock market in the country.

Example 7 Suppose, Supreme Industries has an equity market capitalisation of Rs 3,400

crore. in current year. Assume further that its equity share capital is Rs 2;000 crore and its

retained earnings are Rs 600 crore. Determine the MVA and interpret it.

Solution

MVA = (Rs 3,400 core - Rs 2,600 crore) = Rs 800 crore.

The value of Rs 800 crore implies that the management of Supreme Industries has created

wealth/value to the extent of Rs 800 crore for its equity shareholders. Well managed

companies (engaged in sunrise businesses),"having good growth prospects, and perceived so

by the investors, have positive MVA. Investors may be willing to pay more than the net

worth. In contrast, companies relatively less known or engaged in businesses that do not hold

future growth; potentials may have negative MVA.

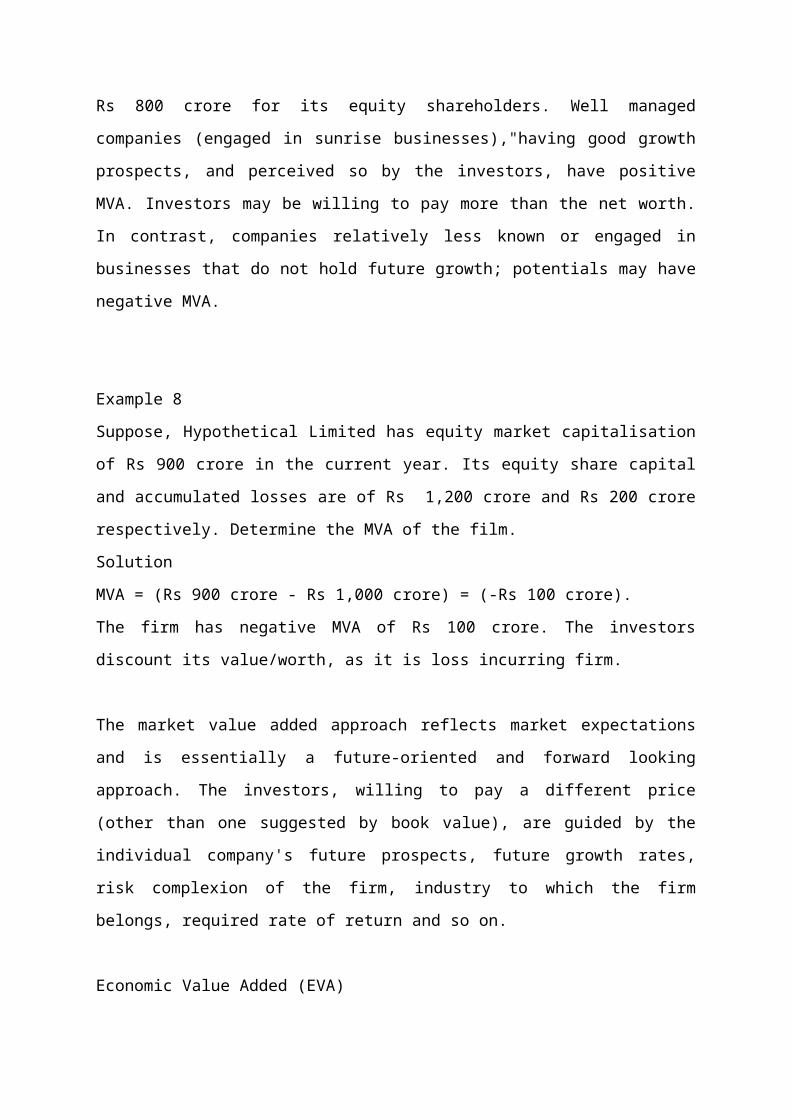

Example 8

Suppose, Hypothetical Limited has equity market capitalisation of Rs 900 crore in the current

year. Its equity share capital and accumulated losses are of Rs 1,200 crore and Rs 200 crore

respectively. Determine the MVA of the film.

Solution

MVA = (Rs 900 crore - Rs 1,000 crore) = (-Rs 100 crore).

The firm has negative MVA of Rs 100 crore. The investors discount its value/worth, as it is

loss incurring firm.

The market value added approach reflects market expectations and is essentially a future-

oriented and forward looking approach. The investors, willing to pay a different price (other

than one suggested by book value), are guided by the individual company's future prospects,

future growth rates, risk complexion of the firm, industry to which the firm belongs, required

rate of return and so on.

Economic Value Added (EVA)

The EVA method is based on the past performance of the corporate enterprise. The

underlying economic principle in this method is to determine whether the firm is earning a

higher rate of return on the entire invested funds than the cost of such funds (measured in

terms of the weighted average cost of capital, WACC). If the answer is positive, the firm's

management is adding to the shareholders value by earning extra for them. On the contrary, if

the WACG is higher than the corporate earning rate, the firm's operations have eroded the

existing wealth of its equity shareholders. In operational terms, the method attempts to

measure economic value added (or destroyed) for equity shareholders, by the firm's

operations, in a given year.

Since WACC takes care of the financial costs of all sources of providers of invested funds in

a corporate enterprise, it is imperative that operating profits after taxes (and not net profits

after taxes) should be considered to measure EVA. The accounting profits after taxes, as

reported by the income statement, need adjustments for interest costs. The profits should be

the net operating profits after taxes and the cost of funds will be product of the total capital

supplied (including retained earnings) and WACC.

EVA .= [Net Operating profits after taxes - (Total capital x WACC)]

(16)

The computation of EVA is illustrated in Example 9

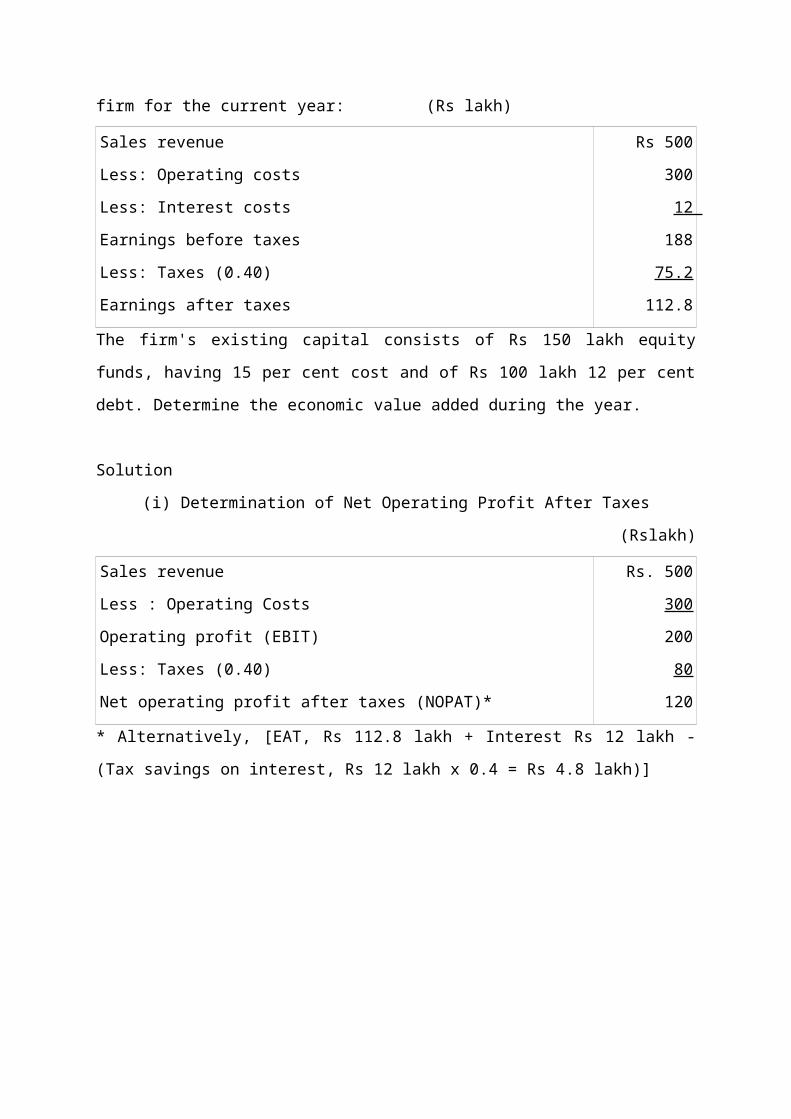

Example 9 Following is the condensed income statement of a firm for the current year:

(Rs lakh)

Sales revenue

Less: Operating costs

Less: Interest costs

Earnings before taxes

Less: Taxes (0.40)

Earnings after taxes

Rs 500

300

12

188

75.2

112.8

The firm's existing capital consists of Rs 150 lakh equity funds, having 15 per cent cost and

of Rs 100 lakh 12 per cent debt. Determine the economic value added during the year.

Solution

(i) Determination of Net Operating Profit After Taxes

(Rslakh)

Sales revenue Rs. 500

Less : Operating Costs

Operating profit (EBIT)

Less: Taxes (0.40)

Net operating profit after taxes (NOPAT)*

300

200

80

120

* Alternatively, [EAT, Rs 112.8 lakh + Interest Rs 12 lakh - (Tax savings on interest, Rs 12

lakh x 0.4 = Rs 4.8 lakh)]

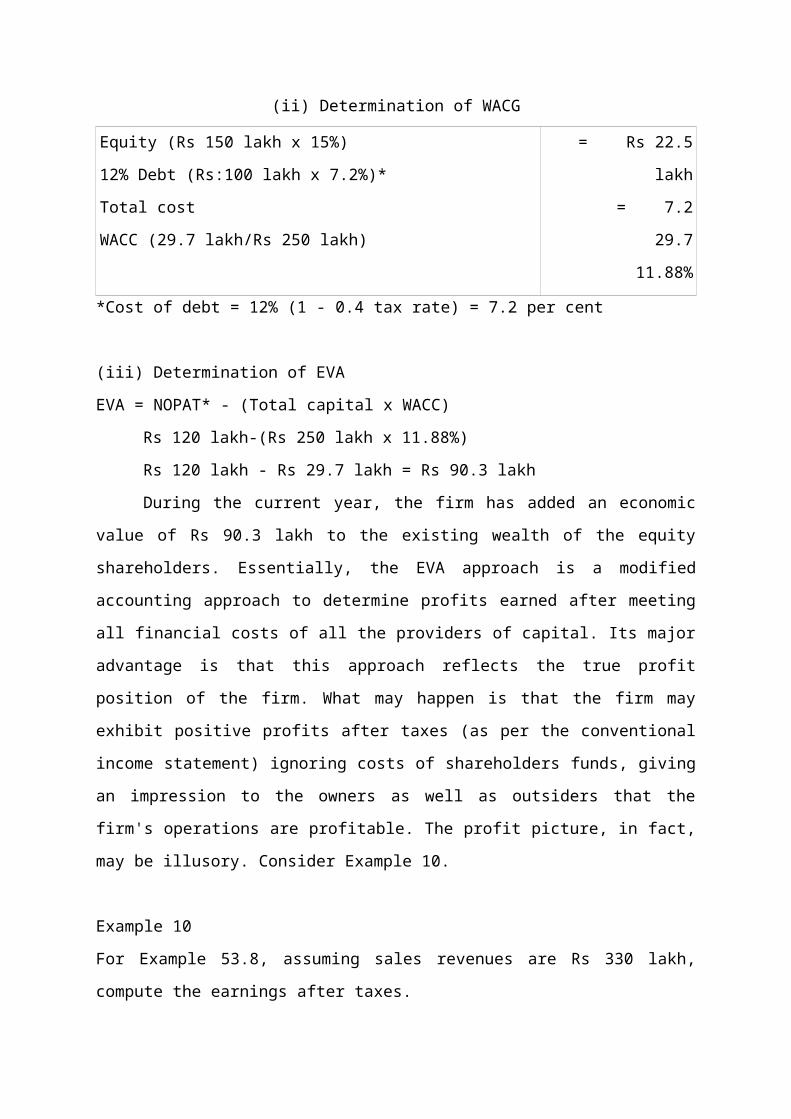

(ii) Determination of WACG

Equity (Rs 150 lakh x 15%)

12% Debt (Rs:100 lakh x 7.2%)*

Total cost

WACC (29.7 lakh/Rs 250 lakh)

= Rs 22.5 lakh

= 7.2

29.7

11.88%

*Cost of debt = 12% (1 - 0.4 tax rate) = 7.2 per cent

(iii) Determination of EVA

EVA = NOPAT* - (Total capital x WACC)

Rs 120 lakh-(Rs 250 lakh x 11.88%)

Rs 120 lakh - Rs 29.7 lakh = Rs 90.3 lakh

During the current year, the firm has added an economic value of Rs 90.3 lakh to the

existing wealth of the equity shareholders. Essentially, the EVA approach is a modified

accounting approach to determine profits earned after meeting all financial costs of all the

providers of capital. Its major advantage is that this approach reflects the true profit position

of the firm. What may happen is that the firm may exhibit positive profits after taxes (as per

the conventional income statement) ignoring costs of shareholders funds, giving an

impression to the owners as well as outsiders that the firm's operations are profitable. The

profit picture, in fact, may be illusory. Consider Example 10.

Example 10

For Example 53.8, assuming sales revenues are Rs 330 lakh, compute the earnings after

taxes.

Solution

Income Statement (Conventional)

(Rs lakh)

Sales revenue

Less: Operating costs

Less: Interest costs

Earnings before taxes

Less: Taxes (0.40)

Earnings after taxes

Rs 330

300

12

18

7.2

10.8

The firm has registered profits of Rs 10.8 lakh during the current year on the equity funds of

Rs 150 lakh, which has financial costs of Rs 22.5 lakh. Therefore, the firm has, suffered a

loss, (of Rsll.7 lakh) as the opportunity costs of equity funds invested by equity holders is

more than what has been earned by the firm for them. This point is brought to the fore by the

EVA approach. It is for this reason that the EVA approach is getting more attention. It is

superior to the conventional approach of determining profits.

Determination of EVA

(Rs. lakh)

(a) Sales revenue

Less : Operating Costs

Operating Profits

Less : taxes (0.4)

Net operating profits after taxes

(b) EVA = Rs. 18 Lakh – (Rs. 29.7 lakh, already computed above) =

-Rs. 11.7 lakh

Rs. 330

300

30

12

18

Example 10 demonstrates that there may be a substantial difference between profits

determined as per accounting approach and the EVA approach. Profits shown ass per the EVA

approach are conceptually realistic than shown by traditional accounting approach. In no way,

the firm can be said to have earned profits without meeting financial costs of all sources of

finance. The EVA approach is in tune with the basic financial tenet of cost-benefit analysis;

financial benefits have to be more than financial costs to have true profits.

Though the MVA and EVA are two different approaches, the MVA of the firm (in a technical

sense) can be conceived in terms of the present value of all the EVA profits that the firm is

expected to generate in the future.

Solved Problems

The following particulars are available in respect of a corporate:

(i) Capital employed, Rs 500 million.

(ii) Operating profits, after taxes, for last three years are: Rs 80 million, Rs 100 million,

Rs 90 million; current year's operating profit, after taxes, is Rs 105 million.

(iii) Riskless rate of return, 10 per cent.

(iv) Risk premium relevant to the-business of corporate firm, 5 per cent.

You are required to compute the value of goodwill, based on the present value of. the

super profits method. Super profits are to be computed on the basis of the average profits of 4

years. It is expected that the firm is likely to earn super profits for the next 5 years only.

Solution

Determination of goodwill, using super profit method

(Rs million)

Average profits (Rs 80 million + Rs 100 million + Rs 90 million + Rs

105 million = Rs 375 million)/ 4 years

Rs. 93.75

Less: Normal profits (Rs 500 million x 0.15) 75.00

Super profits 18.75

Multiplied by the PV of .annuity for 5 years at 15 percent (x) 3.352

PV of super profits/Value of goodwill 62.85

2. The following is the balance sheet of a corporate firm as on March 31, current year.

(Rs lakh)

Liabilities Amount Assets Amount

Share capital (of Rs 100 each fully paid-up)

Reserves and surplus

Sundry creditors and other liabilities

Rs. 100

40

30

Land and buildings

Plant and machinery

Marketable securities

Stock

Debtors

Cash and bank balances

Rs. 40

80

10

20

15

5

170 170

Profit before tax for current year-end amount to Rs 64 lakh, including Rs 4 lakh as

extraordinary income. Besides, the firm has earned interest income of Rs 1 lakh in the current

year from investments in marketable securities. It is not usual for the firm to have excess cash

and invest in marketable securities. However, an additional amount of Rs 5 lakh per annum,

in terms of advertisement and other expenses, will be required to be spent for the smooth

running of the business in the years to come.

Market values of land and buildings, and plant and machinery are estimated at Rs 90 lakh and

Rs 100 lakh respectively. In order to match the revalued figures of these fixed assets,

additional depreciation of Rs 6 lakh is required to be taken into consideration. Effective

corporate tax rate may be taken at 30 per cent. The capitalisation rate applicable to businesses

of such risks is 15 per cent.

From the above information, compute the value of business, value of equity and price per

equity/share, based on the capitalisation method.

Solution

Valuation of business, value of equity and price per equity share (capitalisation method)

(Rs lakh)

Profit before tax

Less; Extraordinary income

Less: Interest on marketable securities (not likely to accrue in future)

64

4

1

Less: Additional expected recurring expenses

Less: Additional depreciation

Expected earnings before taxes

Less: Taxes (0.30)

Future maintainable profits after taxes

Divided by relevant capitalisation factor

Value of business (Rs 33.60 lakh/0.15)

Value of equity (Rs 224 lakh - Rs 30 lakh external liabilities)

Price per equity share (Rs 194 lakh/ 1 lakh)

5

6

48

14.40

33.60

0.15

224.00

194.00

194

3 Assume every thing to be the same as contained in P.32.2: Determine the expected

market price of the share, given the P/E multiple of (0 8 times and (ii) 5 times, and interpret

the result.

Solution

Determination of market price per share (P/E basis)

(Rs lakh)

Future maintainable profits after taxes (computed in P.2)

Divided by the number of equity shares issued and outstanding

Earnings per equity share, EPS, (Rs 33.60 lakh/1 lakh)

Multiplied by P/E ratio

(i) Market price per share (Rs 33.60 x 8 times)

Multiplied by P/E ratio

(ii) Market price per share (Rs 33.60 x 5 times)

Rs 33.60

1.00

33.60

8

268.8

5

168

Interpretation

(i) The P/E ratio of 8 times suggests that investors are confident about the company's

future prospects; they have high expectations of future returns. It is for this reasons that they

are prepared to pay a higher market price per equity share than warranted by the

capitalisation method (ie, Rs 194 per share), (ii) In contrast, the P/E multiple of 5 times

suggests that investors are less optimistic about die company's future performance. They have

low confidence as well as expectations of low returns in future years and therefore1 are

willing to pay a lower price vis-a-vis the capitalised price.

P.4 For facts contained in P.2, determine the value of business as per the net assets method.

Assets are to be valued at market value for this purpose. Value of goodwill is also to be

considered to value assets. Its value is to be reckoned as an equivalent to the present value of

super profits, which are likely to accrue for 4 years. For the purpose of determining super

profits, normal profits are to be computed with reference to the year-end value of net

assets/capital employed (excluding goodwill). Also compute the market value of equity share

as per this approach.

Solution

Determination of valuation of business and net asset value per share as per the net assets

method (assets are valued at market price)

(Rs lakh)

Land and buildingsPlant and machineryGoodwillMarketable securitiesStockDebtorsCash and bank, balancesTotal, assetsLess: External liabilities Net assets available for equity to shareholders Divided by the number of equity shares issued and outstanding Net assets value per share (Rs 216 lakh/1 lakh)

Rs 90100

61020155

24630

216

1

216

Valuation of goodwill

Future, maintable profits after taxes

Less: Normal profit (15% of capital employed, i.e., 0.15 x Rs 210 lakh*)

Super profits

Rs 33.60

31.50

Multiplied by PV factor at 15% for annuity of 4 years

Value of goodwill (Rs 2.10 lakh x 2.855)

2.10

2.855

6.0

*(Market value of assets, excluding goodwill, Rs 240 lakh - External liabilities, Rs 30 lakh).

Assume everything to be the same as given in P2. Determine the fair price of an equity share.

The fair price of an equity share is to be taken as an average of prices estimated according to

the capitalisation method and the net assets method.

Solution

Determination of a fair price of an equity share (fair value method)

Price per equity share (capitalisation method)

Net assets value per equity share (net assets method)

Fair value per equity share (Rs 194 + Rs 216)/2

Rs. 194

216

205

P.6 Determine the continuing value of the firm from the following information:

(Rs million)

Cash flow frorn business operations at the end of explicit forecast period (Year 6) Investment required in capital expenditure and current assets during year 6 Expected annual growth rate in free cash flows to the firm, after forecast period (%) Weighted average cost of capital (WACC) (%)Cost of equity capital (%)

Rs. 56

12

8

12

15

Solution

Determination of PV with respect to continuing value (CV)

CV6 = FCFF7 = Rs. 44 million * (1.08) = Rs. 47.52 million

WACC-g 12%-8% 4%

CV6 = Rs 1,188 million

CV0 = Rs 1,188 million x Present value factor at 12% for 6 years

CV0 = Rs 1,188 million x 0.507

= Rs 602.316 million

*(Gross cash flows Rs 56 million - Investment required in capital expenditures and current

assets Rs 12 million = Rs 44 million);

P.7 Hypothetical Limited is growing at an above average rate. It foresees a growth rate of 20

per cent per annum in free cash flows to equityholders in the next 4 years. It is likely to fall to

12 per cent in the next two years. After that, the growth rate is expected to stabilise at 5 per

cent per annum. The amount of free cash flow (FCFE) per equity share at the beginning of

current year is Rs 10. Find out the maximum price at which an investor, follower of the free

cash approach, will be prepared to buy the company's shares as on date, assuming an equity

capitalisation rate of 14 per cent.

Solution Maximum price of the equity share will be the sum of (i) PV of FCFE during 1 - 6

years and 00 PV of expected market price at the end of year 6, based on a constant growth

rate of 5 per cent.

(i) Present value of FCFE (years 1 - 6)

Year FCFE per share PV factor (0.14) Total PV

1 Rs. 10 (1+0.20)1 = Rs. 12 0.877 Rs. 10.52

2 10 (1+0.20)2 = 14.40 0.769 11.07

3 10 (1+0.20)3 = 17.28 0.675 11.66

4 10 (1+0.20)4 = 20.74 0.592 12.28

5 20.74 (1+0.12) = 23.23 0.519 12.06

6 23.23 (1+0.12) = 26.02 0.456 11.86

Total PV of FCFE 69.45

Market price of share at year-end 6

= FCFE7 = Rs. 26.02 (1.05)

ke-g 14% - 5%

P6 = Rs. 27.321 = Rs. 303.57

14% - 5%

(ii) PV of Rs. 303.57 = Rs. 303.57 x 0.456

= Rs. 138.43

Maximum price of share

= Rs 69.45 + Rs 138.43 = Rs 207.88

P.8 The Chemicals and Fertilizer Limited is a growing company. Its free cash flows for equity

holders (FCFE) have been growing at a rate of 25 per cent in recent years. This abnormal

growth rate is expected to continue for another 5 years; then these FCFE are likely to grow at

the normal rate of 8 per cent. The required rate of return on these shares, by the investing

community, is 15 per cent; the firm's weighted average cost of capital is 12 per cent. The

amount of FCFE per share at the beginning of the current year is Rs 30. Determine the

maximum price an investor should be willing to pay now it = 0), based on free cash flow

approach. The issue price of share is Rs 500.

Solution

(i) Present value of FCFE (years 1-5)

Year FCFE per share PV Factor (0.15) Total PV

1 Rs 30 (1+0.25)1 = Rs. 37.50 Rs. 0.870 Rs. 32.62

2 30 (1+0.25)2 = Rs. 46.86 0.756 35.43

3 30 (1+0.25)3 = 58.59 0.658 38.55

4 30 (1+0.25)4 = 73.23 0.572 41.89

5 30 (1+0.25)5= 91.56 0.497 45.51

Total PV of FCFE 194.00

Market price of share at year-end 5

= FCFE6 = Rs. 91.56 (1.08) = Rs. 1,412.64

ke-g 15% - 8%

PV at t = 0 = Rs 1,412.64 x 0.497 = Rs 702:08

Investor will be prepared to pay the maximum price at t = 0 = Rs 194 + Rs 702.08 = Rs

896.08

P.9 The most recent accounts of a corporate firm engaged in manufacturing business are

summarized below:.

(Rs million)

Income statement for the current year ended March 31 Amount

Sales revenue

EBIT

Less: Interest on loan

Earnings before taxes

Less: Corporate taxes (0.35)

Earnings after taxes

Rs 93.5

18.0

1.8

16.2

5.67

10.53

Balance sheet as at March 31, current year

(Rs million)

Liabilities Amount Assets Amount

Equity share capital (1 lakh

shares of Rs 100 each)

Reserves and surplus

10% Loan

Creditors and other liabilities

10.0

32.5

18.0

18.0

Freehold land and buildings

(net)

Plant and machinery (net)

Current assets:

Stock

Debtors

Bank and cash balance

20.0

29.5

10.0

15.0

4.0

78.5 78.5

Additional Information:

CO The finance manager of the firm has estimated the future free cash flows of the company

as follows:

Year

1

Rs.

22

2 23

3 24.5

4 26.0

5 30.0

6 32.0

Free cash flows in subsequent years, after year 6, are estimated to grow at 4 per cent. The

company's weighted average cost of capital is 12 per cent.

(ii) The current resale value of the following assets has been assessed by the professional

valuer as follows:

Freehold land and buildings Rs 60 million

Plant and machinery 20

Stock 11

The current resale values of the remaining assets are as per their book values.

(iii) A similar sized company (which is listed on Bombay Stock Exchange) and is engaged

in the same business has a P/E ratio of 7 times.

You are required to compute the value of the firm as well as value of an equity share on the

basis of the following methods: (i) Net assets method (book value and market value), (ii)

Price-earnings ratio method and (iii) Free cash flows to the firm.

Solution

Determination of value of firm and value of equity share (using various methods)

(Rs million)

(i) (a) Net asset method—book value basis:

Freehold land and buildings

Plant and machinery

Stock

Debtors

Rs. 20.0

29.5

10.0

15.0

Bank and cash balances

Total assets

Less: External liabilities

10°/o Loan

Creditors and other liabilities

Net assets available to equityholders

Divided by number of equity shares outstanding (lakh)

Net assets backing per share (Rs 42.5 million/ 1 lakh) (Rs)

(b) Market value basis:

Freehold land and buildings

Plant and machinery

Stock

Debtors

Bank and cash balances

Total assets

Less: External liabilities

Net assets at market value

Net assets backing per share (Rs 74 million/1 lakh shares)

(ii) Price-earnings ratio approach

Earnings after taxes (assumed to be normal and expected to be maintained

in future years; no adjustment is made as there are no extraordinary items)

Earnings per share (Rs 10.53 million/1 lakh shares)

Multiplied by P/E multiple

Market price of equity share (Rs 105.30 x 7 times)

4.0

78.5

36.0

42.5

1

425

60

20

11

15

4

110

36

74

740

10.53

105.30

7

737.10

(iii) Free cash flow basis:

(a) PV of FCFE during explicit forecast period:

(Rs in million)

Year FCFF PV Factor (0.12) Total PV

1 Rs. 22 0.893 Rs. 19.646

2 23 0.797 18.331

3 24.5 0.712 17.444

4 26.0 0.636 16.536

5 30.0 0.567 17.010

6 32.0 0.507 16.225

Total present value 105.191

(b) PV of FCFF subsequent to explicit forecast period

CV6 = Rs. 32 (1.04) = Rs. 33.28 = Rs. 416

0.12 – 0.04 0.08

PV0 = Rs 416, continuing value x PV factor at 12% for 6 years

= Rs 416 x 0.507 = Rs 210.912

(c) Total PV of FCFF (Rs 105.191 + Rs 210.912)

= 316.103 million 316.103

Less: External liabilities 36.000 36.00

FCFE available to equityholders 280.103 280.103

MPS (Rs 280.103 million/

1 lakh shares) = Rs 2801.03 280.10

P.10 Assume everything to be the same as given in P.32.9, determine the economic value

added during the current year. Assume the long-term funds shown in the balance sheet as the

total capital employed in the business.

Solution

Determination of economic value added (EVA)

(Rs. In million)

Net operating profits before taxes

Less: Corporate taxes (0.35).

Net operating profits after taxes

Less: Cost of capital employed (Rs 60.5 million" x 0.12 WACC)

Economic value added.

Rs 18

6.3*

11.7

7.26

4.44

Alternatively, corporate taxes can be conceived as sum of (i) taxes as per income statement

(Rs 5.67 million plus (ii) tax savings on interest (Rs 1.8 million x 0.35 = 0.63 million) = Rs

6.3 million "Equity share capital Rs 10 million + Reserves and surplus Rs 32.50 million +

10% loan Rs 18 million- Rs 60.5 million.

P.11 Assume every thing to be the same as given in P9. Assume further that the equity shares

of this company are currently quoted in the market at Rs 500 per share. Determine the

amount of market value added (MVA).

Solution

Determination of market value added

A. Market value per equity share

B. Multiplied by number of equity shares outstanding (lakh)

C. Total market value (A x B) (Rs million)

D. Equity funds (Rs 10 million equity share capital plus Rs 32.5 million

reserves and surplus)

E. Market value added (Rs 50 million - Rs 42.5 million)

Rs. 500

1

50

42.5

7.5

Top Related